Step-by-Step Guides to Strategic Media Relations by Hoem Seiha

Upload

hoem-seihaCategory

view

884download

0

MACRO-PERSPECTIVES:

REAL ESTATE INDUSTRY &

OUTLOOK 2016

1

By Hoem Seiha

Director of Research

H/p: (012/010)-699-553 | [email protected]

Website: www.vtrustappraisal.com

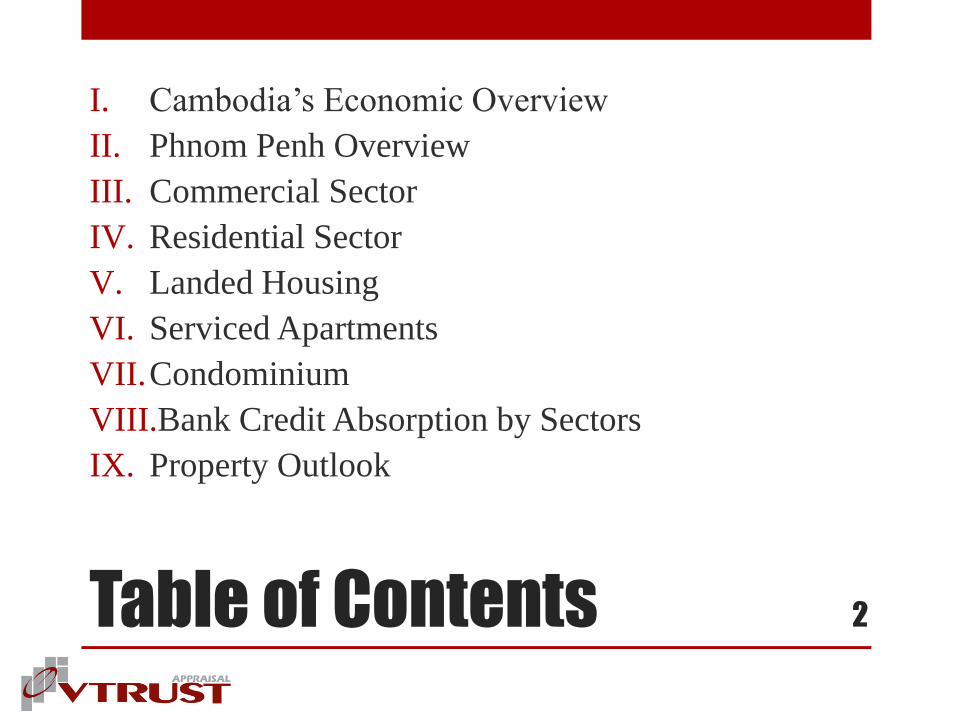

Table of Contents

I. Cambodia‟s Economic Overview

II. Phnom Penh Overview

III. Commercial Sector

IV. Residential Sector

V. Landed Housing

VI. Serviced Apartments

VII.Condominium

VIII.Bank Credit Absorption by Sectors

IX. Property Outlook

2

Cambodia’s Economic

Snapshot

“Cambodian economy remains strong, despite a slight growth for 2015 and 2016 due to economic disturbances, with a forecast at 7 percent of GDP growth in 2015 and 7.2 percent in 2016.”

Source: Asian Development Outlook 2015, ADB

3

Fast Stats

Fast Stats 2014 2015

GDP, nominal, US$ million

(World Bank) 16,600 18,381

GDP, real growth, %

(ADB)

7.0 7.0

GDP, per capita, US$

(MEF)

1,130 1,225

Inflation, %

(ADB)

1.3 2.7

Population, in million

(NIS)

15.3 15.6

Phnom Penh (current, million) 2.2

Annual Growth (%) 4

4

Phnom Penh Map 5

Source: World Trust Estate

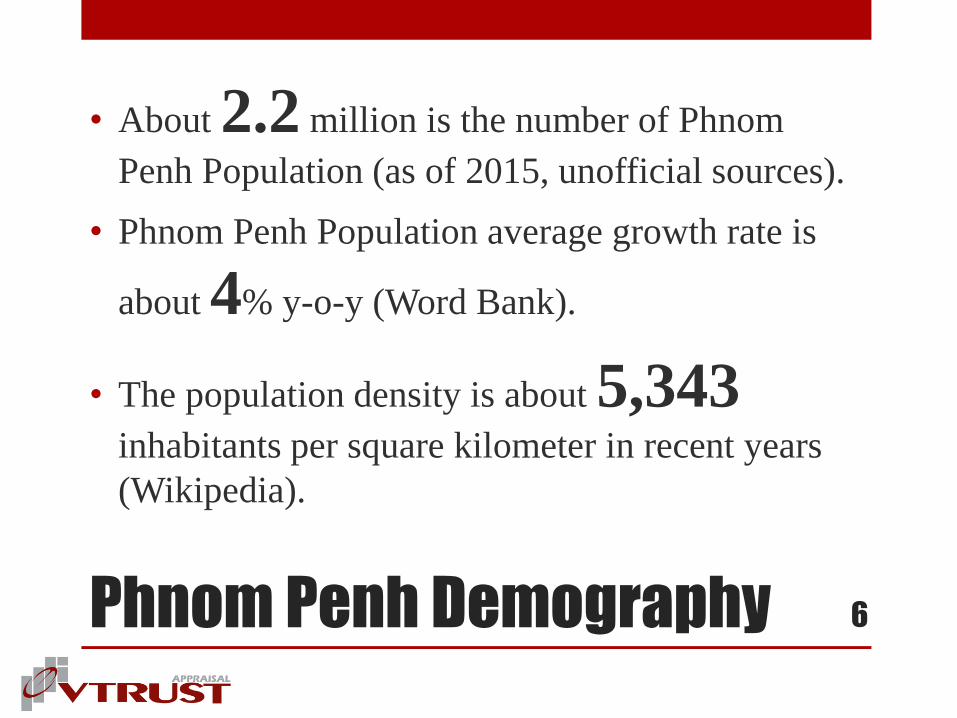

Phnom Penh Demography

• About 2.2 million is the number of Phnom

Penh Population (as of 2015, unofficial sources).

• Phnom Penh Population average growth rate is

about 4% y-o-y (Word Bank).

• The population density is about 5,343 inhabitants per square kilometer in recent years

(Wikipedia).

6

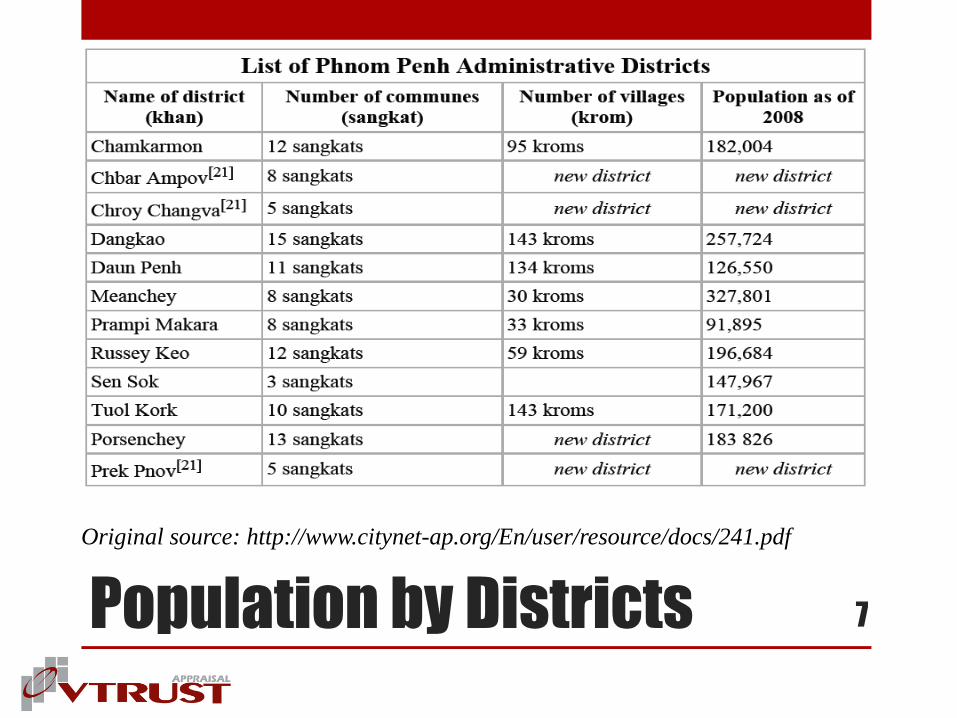

Population by Districts

7

Original source: http://www.citynet-ap.org/En/user/resource/docs/241.pdf

Incomes of Population 8

$102 $106 $100 $107 $136

$498 $480 $443 $462

$587

3%

-5%

6%

28%

-4%

-8%

4%

27%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

$-

$100

$200

$300

$400

$500

$600

$700

$800

2009 2010 2011* 2012* 2013*

(*) Preliminary results

Source: National Institute of Statistics; Graphed by Park Cafe

Disposable Income in Phnom Penh (Average Value per Month)

Per Capita Per Household

Change (%), per capita Change (%), per household

9 Rising of Middle Class

Surveyed conducted in 2014 among 990 white collar population in Phnom Penh

Construction Sector 10

2.7

2013

2.1

2012 3.3

2014

1.2

2011 3.2

2015

Source: Cambodian authorities, World Bank, Phnom Penh Post, US

Commercial Service, Department of Commerce

Values of Approved Construction Projects in

Cambodia (in US$ Billion)

Construction Sector

• In 2015, 55 high rise construction projects were

approved by the Ministry of Land Management,

Urban Planning and construction, bringing a total

of 13,000 units into the whole country, with

the majority clustering in the Capital.

• Most construction investments were injected into

condominium complexes, with an estimate of

10,000 units in 2015 alone.

11

Commercial Real Estate 12

• Commercial property market has been growing strong

since the last few years, with the supply of major

commercial development centers such as Sovanna Mall,

Canadia Tower, Phnom Penh Tower, and lately the

Ratannac Tower and AEON shopping mall as well as the

soon-coming Parkson Mall.

• About 275,000 sqm is the total supply of

retail space in 2015, contributed hugely by the

coming of AEON Mall (Retail Market Phnom Penh, Sept

2014, CBRE).

Retail Sector 13

• It is estimated that about 300,000 sqm of net leasable

retail space is slated for the market supply by the end of 2016 (Retail Market Phnom Penh, Sept 2014, CBRE).

• Parkson Mall will be ready by early 2016, bringing about

70,200 sqm of leasable area.

• AEON 2 will be ready by the end of 2018, bringing about

151,000 sqm of leasable area.

• About 450,000 sqm of total retail space is forecast to

be in the market by 2018, largely contributed by AEON 2 located in Phnom Penh Thmey (Estimate, VTrust Appraisal Research Department).

Office Space Market

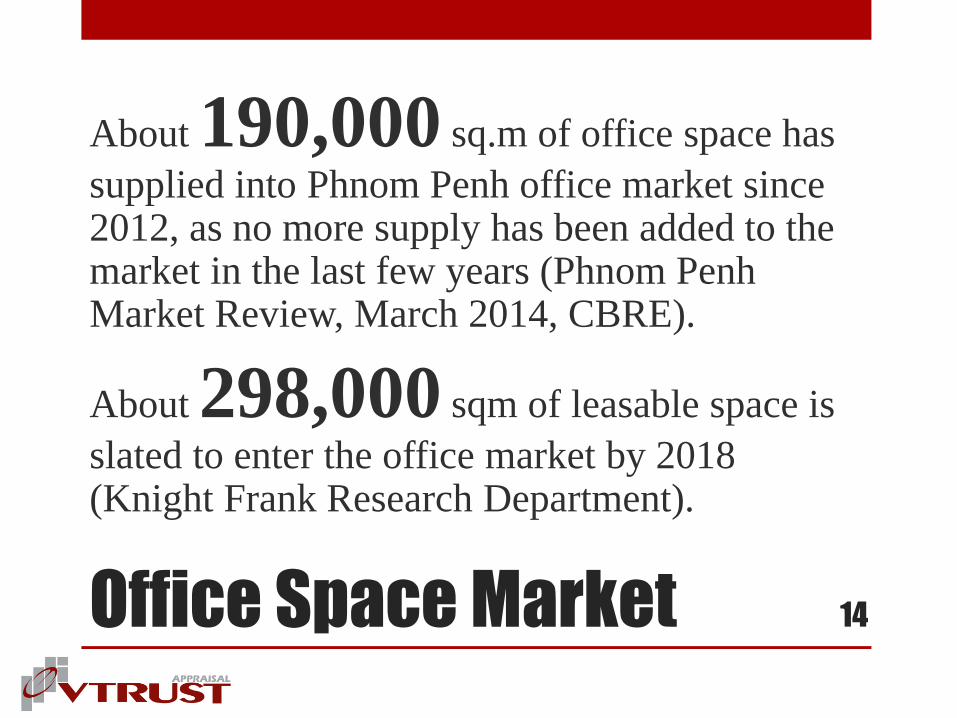

About 190,000 sq.m of office space has

supplied into Phnom Penh office market since 2012, as no more supply has been added to the market in the last few years (Phnom Penh Market Review, March 2014, CBRE).

About 298,000 sqm of leasable space is

slated to enter the office market by 2018 (Knight Frank Research Department).

14

Residential Market Overview

• Demand for villas and shop houses within „borey‟ landed developments remains strong, driven principally by Cambodian nationals able to take advantage of staggered payment options and in-house finance schemes.

• Shop houses, comprising upper floor residential accommodation and ground floor retail space continue to be a popular option for Cambodian nationals, due to their relative affordability and the option of using the unit for business purposes in addition to residential accommodation.

Source: CBRE Residential Market Review (Dec, 2014)

15

Housing Demand

“10,000 is the number of families from other provinces moving to Phnom

Penh every year.”

Lao Tip Seiha, director of the department of construction at the Ministry of Land Management, Urban

Planning and Construction, as quoted by the Phnom Penh Post, 2011

Therefore, housing demand is therefore estimated at a modest figure of

10,000 units every year (Phnom Penh Post, 2015).

122 is the number of registered “borey” landed development projects, both

complete and under construction (Ministry of Land Management, Urban

Planning and Construction, as of March 2016).

Housing demand is also driven by a shifting trend from extended to

nuclear family and increase of newly-married couples every year as a result of baby boom.

16

Phnom Penh’s Apartment Market 2014

There are almost 400 apartment buildings,

the majority of which are small and family-

run apartments.

Source: VTrust Report on Apartment Market (2014)

17

Supply & Demand

About 3,500 is the number of high grade

serviced apartment units offered for rent in

Phnom Penh in 2014.

This market is driven by some of the 50,000

expats living and working in Phnom Penh.

Source: VTrust Report on Apartment Market (2014)

18

Occupancy 19

Source: VTrust Report on Apartment Market (2014)

Real Estate Prices

• Real estate prices grew about 20 percent a year.

• Land prices in prime commercial district (i.e.

Chamkar Mon) grew by 10 percent in 2015.

• Land prices in new developing areas (i.e. Chroy

Changvar) grew by 20 percent in 2015.

Source:

Maintaining High Growth: Cambodia Economic Update, World Bank

VTrust Appraisal Research Department

20

Bank Deposits from Private Sector

US$

8.81 Billion

2014

US$

6.88 Billion

2013

14.2% yoy

30.6% yoy

Sourc

e: W

orl

d B

ank;

Cam

bodia

n A

uth

ori

ties

Sourc

e: W

orl

d B

ank;

Cam

bodia

n A

uth

ori

ties

Loan-to-deposit ratio

Bank Credit Absorbed by Sector

19 %

Construction

& Real Estate

10.4 %

Agriculture

35.9%

Wholesale

& Retail

So

urc

e: W

orl

d B

an

k; C

am

bo

dia

n A

uth

ori

ties

9.6 %

Manufacturing

Shares of Credit by Sector in 2014

Credit to Real Estate & Construction

1.76

2014

1.23

2013 2.02

2015

Sou

rce:

Nati

onal

Bank

of

Cam

bodia

0.96

2012

Values of Credit Absorbed by Construction and Real

Estate Sector (Values in US$ billion)

Credit to Real Estate & Construction

433

Real Estate

Services

699

Housing

Mortgage

889

Construction

So

urc

e: N

ati

on

al

Ban

k of

Cam

bo

dia

Credit Shares in Real Estate and Construction Sector

as of June-2015 (Value in US$ million)

Sourc

e: W

orl

d B

ank;

Cam

bodia

n A

uth

ori

ties

Residential Outlook

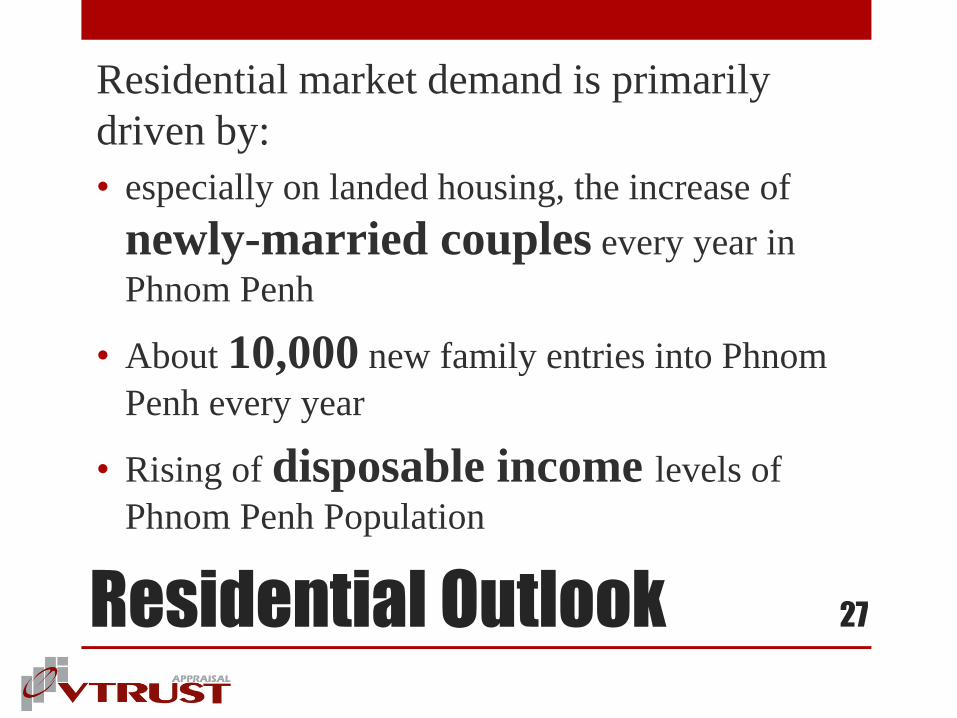

Residential market demand is primarily

driven by:

• especially on landed housing, the increase of

newly-married couples every year in

Phnom Penh

• About 10,000 new family entries into Phnom

Penh every year

• Rising of disposable income levels of

Phnom Penh Population

27

Commercial Outlook

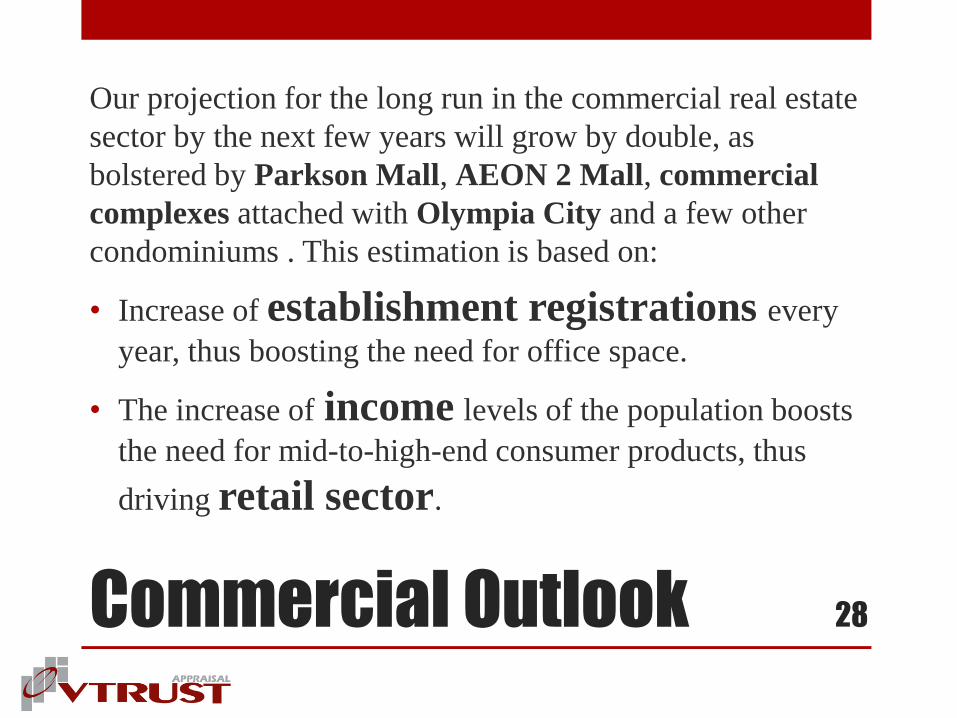

Our projection for the long run in the commercial real estate

sector by the next few years will grow by double, as

bolstered by Parkson Mall, AEON 2 Mall, commercial

complexes attached with Olympia City and a few other

condominiums . This estimation is based on:

• Increase of establishment registrations every

year, thus boosting the need for office space.

• The increase of income levels of the population boosts

the need for mid-to-high-end consumer products, thus

driving retail sector.

28

External Impacts

Recent economic slowdown in China, with real growth of

6.8 percent (Source: IMF) in 2015, down from 7.7

percent in 2013, has a very minimal spillover effects on Cambodia economy in term of:

• Slight slowdown in tourism sector because China

is the second top tourist arrivals to Cambodia, after Vietnam.

• For real estate sector, there will be a slight slowdown

in condominium market because Chinese are

currently one of the leading buyers.

29

Key Factor Analysis

It‟s too early to estimate the spillover effects of China‟s

slowdown on Cambodian economy, because early symptoms

still show of sign of strong growth compared to last year.

Look at the number of tourist arrivals in Cambodia.

30

460

Jan-2015

466

Jan-2016

Total (Thousand)

53 66 China

(Thousand) So

urc

e: M

inis

try

of

Tou

rism

Key Factor Analysis

Condominium Market Performance

31

25

2015, Whole

7

Jan-2016

Sales-to-Stock

Ratio, %

48.1 168.8 Absorption Rate,

Months

It is an early sign for the slowdown in real estate market in

2016, yet it could be TOO EARLY to predict the whole

performance for this year…

56

Avg., 2007-2015

32.4

So

urc

e: C

entu

ry 2

1 C

am

bo

dia

Conclusion

Real Estate Sector Outlook for 2016

32

Construction and Real estate sector growth remain strong this year, and it will

continue to do so over the next coming year, mainly bolstered by:

• Maintained real growth of Cambodia‟s GDP at 7.2 percent in 2016 (ADB‟s

prediction, last updated).

• Therefore, this lead to a continuous growth of population incomes, thus

continuing to still drive local demand on landed housing units.

• However, apartment, condominium market is starting

to see a slowdown due to its too much reliance on foreign

buyers and excessive supply coming at the same time where

the market absorption isn‟t fast enough to offset the accumulative stock.

Thanks for your Time

Contact #113 (Parkway Square) Mao Tse Tong Blvd., Phnom Penh, Cambodia |

H/p: (855)12-699-553 / 10-699-553

(855) Office: (855)23-220-098

E-mail: [email protected]

Website: www.vtrustappraisal.com

33