Research & Forecast Report Q1 2015 Jakarta Apartment

of 6

-

Upload

indra-nymk -

Category

Documents

-

view

217 -

download

0

Transcript of Research & Forecast Report Q1 2015 Jakarta Apartment

-

8/19/2019 Research & Forecast Report Q1 2015 Jakarta Apartment

1/11

Apartment Sector Apartment for Strata-title

Supply

Commencing in 2015, the cumulative supply of apartment units in

Jakarta grew at a moderate pace. Te apartment market received

3,255 new units, up by 2.3% QoQ, from seven projects comprising

four brand new projects and three extension towers. Tese 3,255

units, or 11% of the total projected 29,451 new units that will be

completed this year, are scattered in all areas of Jakarta, except the

CBD. Of the total supply in this quarter, 38% is located in South

Jakarta, while the remaining portions are located in North Jakarta

(25%), East Jakarta (22%), West Jakarta (11%) and Central Jakarta

(6%). Overall, with the addition from newly-completed projects,

the total existing stock of strata-title apartments in Jakarta rose

to 146,300 units. By location, the non-prime areas (North Jakarta

and West Jakarta) dominate the market with 22.2% and 21.6% of

the total stock, respectively. Te remaining stock is distributed in

South Jakarta, CBD area and Central Jakarta at 21.1%, 15.7% and

13.2%, respectively, while East Jakarta had a mere 6.2% of the total

inventory.

Te first quarter of the year began with optimism amongdevelopers as they launched several new apartment projects.

Compared to the same quarter last year, there were 7,276 newly-

introduced and launched units, 115% higher than in the same

period last year. Demand for apartments in Jakarta has been

notably strong during the last three years, evidenced by almost

all new completed apartment projects achieving more than a 90%

sales rate. Apartment units are still perceived as an investment

tool as they provide capital gains of around 10 - 25% (if bought at

the initial offering) and rental yield expectations of around 6 to 8%

per year.

Te reform of Indonesia’s fuel subsidy policy will have a positive

impact on the property sector as the government aims to allocatethe budget to more productive uses, such as improvements in

infrastructure. Te acceleration of infrastructure projects will

expand the economy, in line with the government’s target of a

5.5% GDP growth this year, an increase 0.5% from the growth in

2014.

Research &Forecast Report

Jakarta | Apartment1Q 2015

Accelerating success.

“The “wait and see” attitude caused by national elections in 2014

and a slowing economy as a result of the strengthening US dol-

lar against local currencies in the Asia Pacific region reduced thegrowth rate of apartment supply last year. With only half of the

total projected supply in 2014 being materialized (around 10,000

units), 2015 will become a tougher market as 29,451 units are

projected to be completed. As a result of the softening apartment

market, prices of apartments only climbed modestly by 2.7% QoQ

slightly lower than in the previous quarter of 3.1%. Meanwhile, the

absorption rate of future apartment projects was down by 3.7% to

68.4% QoQ.”

Ferry Salanto | Associate Director - Research

https://twitter.com/colliersintl

-

8/19/2019 Research & Forecast Report Q1 2015 Jakarta Apartment

2/11

2

Source: Colliers International Indonesia - Research

Notes:

*Price excludes 10% VA

**NUP (Indonesian term for Nomor Urut Pemesanan) or also known as priority pass is a new marketing strategy commonly applied by reputable developers to gauge the interestof potential buyer in the initial offering

Source: Colliers International Indonesia - Research

Research & Forecast Report | 1Q 2015 | Apartment | Colliers International

List of Completed Projects During 1Q 2015

NAME OF DEVELOPMENT LOCATION REGION DEVELOPER NO. OF UNITS

Belmont Residence (Tower Montblanc) Jl. Meruya Ilir West Jakarta Gapura Prima 350

The Royal Springhil l (Lotus Tower) Jl. Spring Hill Residence Kemayoran Central Jakarta Springhil l Golf Group 192

Titanium Square Jl. Raya Bogor, Pasar Rebo East Jakarta PT Titanium Property 725

Northern Ancol Residence Ancol North Jakarta Jaya Ancol 800

La Venue - South Tower Jl. Pasar Minggu South Jakarta PT Bintang Rajawali (Sinar Mas Group) 341

Botanica Apartment Simprug, Kebayoran Baru South Jakarta Pikko Group 626

Woodland Park (Trambesi tower) Jl. Kalibata Raya South Jakarta PT. Pardika Wisthi Sarana 221

Newly-Introduced Apartment During 1Q 2015

NAME OF DEVELOPMENT LOCATION REGIONEXPECTED

COMPLETIONTIME

ESTIMATED PRICE/SQ M*

NO. OFUNITS

REMARKS

South Hill Jl. Denpasar Raya CBD 2018 IDR37 - 39 million 611 Pre-sales

Green Pramuka (Nerine Tower) Jl. Pramuka Central Jakarta 2017 IDR16.7 million 1,000 Launched

Podomoro Park Jl. I Gusti Ngurah Rai East Jakarta 2018 IDR18.5 million 3,000 Introduced (NUP system **)

The Hamilton Jl. Teuku Nyak Arief South Jakarta 2017 IDR49.5 million 112 Introduced (NUP system**)

Pakubuwono Spring Jl. Teuku Nyak Arief South Jakarta 2018 IDR51 million 545 Launched

La Terrasse Jl. Deplu Raya No.12 South Jakarta 2018 IDR37 million 111 Launched

Branz Simatupang (2 tower) Jl. TB Simatupang South Jakarta 2018 IDR28 million 381 Introduced

Synthesis Residence Kemang Jl. Ampera Raya South Jakarta 2018 IDR29.5 million 1,100 Introduced (NUP system**)

19 Avenue (Tower B) Jl. Daan Mogot West Jakarta 2017 IDR10.5 million 416 Launched

https://twitter.com/colliersintlhttp://www.linkedin.com/company/colliers-international%3Ftrk%3Dhb_tab_compy_id_5227https://www.facebook.com/colliersglobal%3Frf%3D105632526137251

-

8/19/2019 Research & Forecast Report Q1 2015 Jakarta Apartment

3/11

3

As of 1Q 2015, there are 7,276 units at either newly-introduced

or newly-launched projects, which are mainly located in South

Jakarta, representing 53% of the total units. Among the districts

in South Jakarta, B Simatupang remains in the spotlight as can

be seen by the growing number of office developments that drive

the growth of apartment development in the surrounding area.

Te supply of new apartment units during 2015 is projected to be

substantial, i.e. 29,451, should all projects be completed. All in

all, the total projected units that will come into the market from

2015 to 2018 will be 80,881 new units, mainly supplied in West

Jakarta with 23% of the total supply, followed by East Jakarta

and South Jakarta with 22 and 20%, respectively. ypically,

apartment development in West Jakarta is characterised by

massive unit projects targeting the middle-low income segment,

offering small units in order to make prices affordable. Te units

of these apartment projects typically come with areas from 22

sq m for studio units to 70 - 80 sq m for 3-bedroom units. On

the other hand, East Jakarta will see abundant new projects in

the next two to three years, mainly coming from two projects, i.e.

Green Signature and Bassura City, which are located in Cawangand Cipinang, respectively.

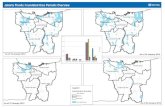

The Distribution of Future Apartment Developmentsin Several Regions of Jakarta

Source: Colliers International Indonesia - Research

Research & Forecast Report | 1Q 2015 | Apartment | Colliers International

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

2015F 2016F 2017F 2018F

U n i t s

CBD Central Jakarta South Jakarta

North Jakarta East Jakarta West Jakarta

New Supply Pipeline (2015 - 2019)

APARTMENT NAME LOCATION REGION NO. OF UNITS

The Grove (Empyreal + Masterpiece) Jl. HR Rasuna Said CBD 438

Ciputra World - Luxurious Raffles Residences Jl. Prof Dr Satrio CBD 64

Setiabudi Sky Garden (tower 1) Jl. Karbela Selatan CBD 426

Setiabudi Sky Garden (tower 2) Jl. Karbela Selatan CBD 160

Elpis Residence Gunung Sahari Central Jakarta 790

Capitol Park Apartment (Tower T) Jl. Salemba Raya, Menteng Central Jakarta 727

Capitol Park Apartment (Tower U) Jl. Salemba Raya, Menteng Central Jakarta 976

The Mansion at Dukuh Golf Residence (Aurora Tower) Jl. Benyamin Sueb Kemayoran Central Jakarta 522

The Mansion at Dukuh Golf Residence (BellaVista Tower) Jl. Benyamin Sueb Kemayoran Central Jakarta 612

The H Residence Kemayoran (Amethyst) Jl. Rajawali Selatan Central Jakarta 800

The Royal Springhill (Lotus Tower) Jl. Spring Hill Residence Kemayoran Central Jakarta 192

The Royal Springhill (Bouvardia Tower) Jl. Spring Hill Residence Kemayoran Central Jakarta 120

Casablanca East Residence (2 Twr) + Tower Dallas Jl. Pahlawan Revolusi East Jakarta 1,904

Titanium Square Jalan Raya Bogor Kav. 27 Pasar Rebo East Jakarta 725

The H Residence MT Haryono East Jakarta 383

Bassura City (Tower Flamboyan) Jl. Basuki Rahmat East Jakarta 1,000

Bassura City (Tower Edelweiss) Jl. Basuki Rahmat East Jakarta 1,000

Bassura City (Tower Dahlia) Jl. Basuki Rahmat East Jakarta 1,000

Bassura City (Tower Alamanda) Jl. Basuki Rahmat East Jakarta 600

Bassura City (Tower Geranium) Jl. Basuki Rahmat East Jakarta 900

Teluk Intan (Tower Saphire) Jl. Teluk Gong North Jakarta 1,100

Pluit Seaview (Tower Maldives) Pluit North Jakarta 940

Pluit Seaview (Tower Belize) Pluit North Jakarta 300

Cal lia Apartment Jl. Perintis Kemerdekaan North Jakarta 560

The Oak Tower (2 Towers) Jl. Perintis Kemerdekaan North Jakarta 821

continued

https://twitter.com/colliersintlhttp://www.linkedin.com/company/colliers-international%3Ftrk%3Dhb_tab_compy_id_5227https://www.facebook.com/colliersglobal%3Frf%3D105632526137251

-

8/19/2019 Research & Forecast Report Q1 2015 Jakarta Apartment

4/11

4 Research & Forecast Report | 1Q 2015 | Apartment | Colliers International

APARTMENT NAME LOCATION REGION NO. OF UNITS

continued

Northern Ancol Residence (1Q) Ancol North Jakarta 800

Green Bay Pluit (Sea View) Jl. Pluit Karang Ayu North Jakarta 2,072

La Venue - South Tower (1Q) Jl. Pasar Minggu South Jakarta 341

The Royal Olive Residence Tower I Jl. Buncit Raya South Jakarta 225

Senopati Penthouse Jl. Senopati Kav 45 South Jakarta 63Senopati Suites 2 Jl. Senopati South Jakarta 81

LA City Apartment (Tower A) Jl. Raya Lenteng Agung, Jagakarsa South Jakarta 980

La Maison Barito Barito South Jakarta 80

Botanica Apartment (3 Towers) Simprug, Kebayoran Baru South Jakarta 626

Woodland Park (Trambesi tower) Jl. Kemukus No. 6, Fatahil lah South Jakarta 221

1 Park Avenue (3 Towers) Jl. KHM Syafi' I Hadzami South Jakarta 279

Nine Residence Warung Buncit South Jakarta 246

Providence Park Jl. Kalimaya - Iskandar Muda South Jakarta 114

Kencana Residence Jl. Sultan Iskandar Muda South Jakarta 173

Izzara Apartment (South and North Tower) TB. Simatupang South Jakarta 542

The Aspen Peak at Admiralty Jl. Fatmawati South Jakarta 644Niffaro Apartment (Ebony Tower) Jl. Kalibata Raya South Jakarta 288

Grand Dhika Mansion Pejaten (Sector 1) Jl. Siaga Raya South Jakarta 44

Metro Park Residence Kebon Jeruk West Jakarta 1,451

St. Moritz (New Presidential Tower) Jl. Puri Indah West Jakarta 159

Satu8 Residence Jl. Pilar Komp. Delta, Kedoya West Jakarta 174

Belmont Residence (Tower Montblanc) Jl. Meruya Ilir West Jakarta 350

The Nest Apartment Jl. Raden Saleh Raya, Meruya Utara West Jakarta 1,100

Green Palm Residence @ Puri Jl. Kosambi West Jakarta 1,000

19 Avenue Apartment 9 (Tower A) Daan Mogot West Jakarta 338

The Residence (CWJ 2) Jl. Prov Dr Satrio Kav 6, Kuningan CBD 119

The Orchad Satrio (CWJ 2) Jl. Prov Dr Satrio Kav 6, Kuningan CBD 349

Sudirman Suites Jl. Sudirman CBD 380

Gayanti City (2 Towers) Jl. Gatot Subroto CBD 318

T - Plaza Residence (Tower A) Jl. Penjernihan I Kav.1 Pejompongan Central Jakarta 307

Sentosa Residence Cempaka Putih Central Jakarta 687

Sudirman Hi ll Residence Jl. Karet Pasar Baru Central Jakarta 255

The Green Pramuka (Tower Orchid) Jl. Jenderal Ahmad Yani Central Jakarta 1,000

The Green Pramuka (Tower Penelope) Jl. Jenderal Ahmad Yani Central Jakarta 1,000

The Green Pramuka (Tower Scarlet) Jl. Jenderal Ahmad Yani Central Jakarta 1,000

Capitol Suites Jl. Prapatan Raya Central Jakarta 327

The Royal Springhill (Bulgari Tower) Jl. Spring Hill Residence Kemayoran Central Jakarta 192

Hol land Village (Phase II) Cempaka Putih Central Jakarta 230

Signature Park Grande Jl. MT. Haryono East Jakarta 1,100

Bassura City (Tower Cattleya) Jl. Basuki Rahmat East Jakarta 600

East Park Apartment (Tower C) Jl. KRT Radjiman East Jakarta 550

Sentra Timur Residence (Tower Tosca) Pulo Gebang East Jakarta 133

Pluit Seaview (Tower Ibiza) Pluit North Jakarta 500

Pluit Seaview (Tower Bahama) Pluit North Jakarta 650

La Venue - North Tower Jl. Pasar Minggu South Jakarta 253

Kemang Vil lage (The Bloomington) Jl. P Antasari South Jakarta 150

continued

https://twitter.com/colliersintlhttp://www.linkedin.com/company/colliers-international%3Ftrk%3Dhb_tab_compy_id_5227https://www.facebook.com/colliersglobal%3Frf%3D105632526137251

-

8/19/2019 Research & Forecast Report Q1 2015 Jakarta Apartment

5/11

5 Research & Forecast Report | 1Q 2015 | Apartment | Colliers International

APARTMENT NAME LOCATION REGION NO. OF UNITS

continuation

Senopati Suites 3 Jl. Senopati South Jakarta 54

Pakubuwono Terrace Grand Tower Kebayoran Lama South Jakarta 435

District 8 (Tower Eternity) Jl. Senopati South Jakarta 400

District 8 (Tower Infinity) Jl. Senopati South Jakarta 280

Lexington Rersidence Pondok Pinang South Jakarta 275Apartment Pejaten Park Residence Jl. Warung Buncit Raya No.21 South Jakarta 560

Four Winds Jl. Permata Hijau Raya No.1 South Jakarta 122

Bellevue Place MT Haryono, Tebet South Jakarta 240

Kebayoran Icon Jl. Ciledug Raya South Jakarta 256

Sapphire Residence Lebak Bulus South Jakarta 37

St Moritz (The New Ambassador Suite Tower) Jl. Puri Indah Kembangan West Jakarta 200

The Windsor (Tower II) Jl. Puri Indah West Jakarta 164

Gianetti Apartment Jl. Kebon Jeruk Raya, Kemanggisan West Jakarta 500

Gallery West Jl. Panjang No 5 West Jakarta 280

Belmont Residence (TowerAthena) Jl. Meruya Ilir West Jakarta 193

Puri Mansion Apartment (Tower A) Puri Mansion West Jakarta 900Madison Park Tanjung Duren West Jakarta 1,200

Veranda Jl. Pesanggrahan Raya, Kembangan West Jakarta 174

Domaine Jl. Jend. Sudirman Kav 1 CBD 186

Verde Two (Tower East) Jl. Rasuna Said CBD 182

Anandamaya Residences (3 towers) Jl. Jend Sudirman CBD 500

Central 88 (2 Towers) Jl. Trembesi, Kemayoran Central Jakarta 612

Menteng Park Jl. Cikini Raya No.79 Central Jakarta 756

Holland Village Cempaka Putih Central Jakarta 400

Royal Suites Kemayoran Central Jakarta 450

The Green Pramuka (Tower Nerine) Jl. Jenderal Ahmad Yani Central Jakarta 1,000

Green Signature Apartment Jl. MT. Haryono East Jakarta 800

Podomoro Park Jl. I Gusti Ngurah Rai, Klender East Jakarta 3,000

Bassura City (Tower Jasmine) 2 tower Jl. Basuki Rahmat East Jakarta 2,000

Bassura City (Tower Heliconia) Jl. Basuki Rahmat East Jakarta 700

La Terrasse Jl. Deplu Raya No.12 South Jakarta 111

The Foresque Pasar Minggu, Ragunan South Jakarta 660

The Langham Residences Senopati South Jakarta 57

The Batik @ Pejaten Jl. Siaga Raya South Jakarta 200

La Foret Vivante Jl. Limo, Permata Hijau South Jakarta 253Selatan 8 (Tower Sultan) Kebayoran Lama South Jakarta 336

The Hamilton Jl. KHM Syafi'I Hadzami South Jakarta 112

Puri Orchad (3 Tower) Jl Raya Adicipta West Jakarta 3,000

Maqna Residence Jl. Meruya Ilir No. 88 West Jakarta 312

Vittoria Residence (3 tower) Jl. Daan Mogot West Jakarta 1,100

Wang Residence Jl. Panjang No 18 West Jakarta 250

Taman Anggrek Residence (6 towers) Tanjung Duren West Jakarta 3,000

19 Avenue Apartment (Tower B) Daan Mogot West Jakarta 416

Regatta London Tower Jl. Pantai Mutiara North Jakarta 186

continued

https://twitter.com/colliersintlhttp://www.linkedin.com/company/colliers-international%3Ftrk%3Dhb_tab_compy_id_5227https://www.facebook.com/colliersglobal%3Frf%3D105632526137251

-

8/19/2019 Research & Forecast Report Q1 2015 Jakarta Apartment

6/11

6

Source: Colliers International Indonesia - Research

Research & Forecast Report | 1Q 2015 | Apartment | Colliers International

APARTMENT NAME LOCATION REGION NO. OF UNITS

continuation

Verde Two (Tower West) Jl. Rasuna Said CBD 152

Lavie Jl. Denpasar Raya CBD 320

South Hill Jl. Denpasar Raya CBD 611

Le' Parc Jl. Thamrin CBD 100

Regent Residences (tower 1) Semanggi CBD 100

Core Sky Residence Pulo Gebang East Jakarta 282

Sahid Garden Residence Ciracas East Jakarta 476

Gold Coast Apartment (Atlantic Tower) Pantai Indah Kapuk North Jakarta 568

Regatta Apartment (Tower New York) Pantai Mutiara North Jakarta 186

Sedayu City (Tower Berlin) Jl. Pegangsaan Dua Raya North Jakarta 912

The Kensington Royal Suites (4 Tower) Kelapa Gading North Jakarta 790

Jaya Ancol Seafront - Oceana Tower Pademangan, Ancol North Jakarta 524

Casa Grande Residence 2 (Tower Angelo) Jl. Casablanca South Jakarta 350

Casa Grande Residence 2 (Tower Bella) Jl. Casablanca South Jakarta 350

Casa Grande Residence 2 (Tower Milano) Jl. Casablanca South Jakarta 350

Pondok Indah Residences (3 Towers) Pondok Indah South Jakarta 880

Selatan 8 (Tower Prabu) Jl. Raya Ulujami South Jakarta 344

One Otium Residence Jl. Pangeran Antasari No.8 South Jakarta 160

45 Antasari (2 Tower) Antasari South Jakarta 1,924

Arzuria Apartment Jl. Tendean South Jakarta 210

Pakubuwono Spring (2 towers) Jl. Teuku Nyak Arief No.9 South Jakarta 545

Branz Simatupang (2 tower) TB. Simatupang South Jakarta 381

Synthesis Residence Kemang Jl. Ampera Raya South Jakarta 1,100

Ciputra International Puri Indah (Tower Amsterdam) Puri Indah West Jakarta 412

Grand Madison Tanjung Duren West Jakarta 300

Citra Lake Suites (Tower Rosewood) Jl. Raya Kresek West Jakarta 104

Citra Lake Suites (Tower Greenwood) Jl. Raya Kresek West Jakarta 126

Citra Lake Suites (Tower Oakwood) Jl. Raya Kresek West Jakarta 117

Citra Lake Suites (Tower Sherwood) Jl. Raya Kresek West Jakarta 122

Apartemen Taman Permata Buana Taman Permata Buana West Jakarta 550

https://twitter.com/colliersintlhttp://www.linkedin.com/company/colliers-international%3Ftrk%3Dhb_tab_compy_id_5227https://www.facebook.com/colliersglobal%3Frf%3D105632526137251

-

8/19/2019 Research & Forecast Report Q1 2015 Jakarta Apartment

7/11

7

Demand

Following a downturn trend in the previous quarter, the sales

of strata-title apartments, particularly in the primary market,

continued to record slow absorption. Tis slow market situation

was highlighted by low GDP growth and a rupiah depreciation

against the US dollar, which affected the overall economy of

Indonesia, particularly by lowering the purchasing power of themiddle class. Te weakening local currency against the US dollar

has made construction costs more expensive, particularly for

upper- to luxury-class apartments, as 30 to 40% of the material

components are imported goods. Furthermore, the abundance

of supply puts the overall market in a tough situation since there

are about 80,000 units (during 2015 - 2018) being marketed. In

view of this, we expect to see a further softening in the strata-title

apartment market throughout 2015.

Source: Colliers International Indonesia - Research

Source: Colliers International Indonesia - Research

As of 1Q 2015, the overall average take-up rate for strata-title

apartments (both existing and under-construction projects) in

Jakarta was 85.5%, down slightly from the previous quarter’s

87%. Te table above shows that existing apartment projects

in South Jakarta experienced a decrease in the take-up rates

from the previous quarter, while the non-prime area posted an

increase of 0.3% from the previous quarter but experienced a

drop for the under-construction projects. On the other hand, thetake-up rates for existing projects in the CBD apartment market

remain the same as the previous quarter, at 99.3%.

Source: Colliers International Indonesia - Research

Te pre-sales activity of under-construction projects underwent

a declining trend in all regions of Jakarta. Te take-up rate in

South Jakarta experienced the lowest drop, mostly due to the

abundant supply of newly-introduced or launched projects in

the last three years. Similar to South Jakarta, the pre-sales rate

in the CBD area also experienced a declining sales rate because

most of the projects saw slower absorption than in 2014. Te

sales performance of under-construction projects is very muchaffected by the influx of new projects. For example, one new

middle-upper class project entering the pre-sales stage put

downward pressure on the overall take-up rate during January

- March 2015. Similarly, the continued influx of new projects in

the non-prime area (including Central, North, West and East

Jakarta) has resulted in a downswing of the take-up rate by 2.3%

compared to the previous quarter.

Asking Price

Despite the lowering sales performance during the quarter,average asking prices for strata-title apartments continued to

demonstrate an upward trend. As of 1Q 2015, the average asking

price of apartments in Jakarta rose by 2.7% QoQ to IDR28.4

million/sq m. Based on location, the new apartments in non-

prime locations posted the highest price increase, followed by

South Jakarta and the CBD area. Benefiting from a relatively

lower price compared to South Jakarta and the CBD area, some

projects in non-prime areas are enjoying a good take-up rate and

that has helped the average price to improve. On the other hand,

the market perceives that the current prices of apartments in the

CBD have reached a peak.

Source: Colliers International Indonesia - Research

Te pace of apartment prices in 2014 slowed compared to the

aggressive price growth in 2011 - 2013. Te slowdown is in line

with the government’s expectations, as they are very concerned

with the persistently soaring prices. Tis trend is expected to

continue throughout 2015 as the government is planning tofurther tighten the real estate market by imposing taxes on a

broader range of the property segment.

Bank Indonesia’s target to curb the growth of property prices by

tightening the LV (Loan to Value) regulation has shown results.

As on the chart below, the average QoQ changes of apartment

prices in 2014 has been relatively slower than the strong growth

since 2012 - 2013. During 2011 - 2013, the average QoQ changes

in apartment prices increased by 3.34%.

Research & Forecast Report | 1Q 2015 | Apartment | Colliers International

Take-up Rates Performance of Existing and Under

Construction Projects

AVERAGE TAKE-UP RATES Q Q QoQ

Existing Projects 95.6% 95.7% 0.10%

Pre-Sales rate of Under ConstructionProjects

72.1% 68.4% -3.70%

Average 87.00% 85.50% -1.50%

Take-up Rates Performance of Existing Projects in

Three Major Areas

TAKE-UP EXISTING PROJECTS Q Q QoQ

CBD 99.3% 99.3% 0.0%

South Jakarta 97.9% 97.6% -0.3%

Non-Prime area 93.7% 94.0% 0.3%

Average Asking Price of Apartment per Sq m

ASKING PRICE/SQ M Q Q QoQ

CBD 43,472,842 44,135,684 1.5%

South Jakarta 32,033,471 32,713,013 2.1%

Non-Prime area 20,764,022 21,285,155 2.2%

Take-up Rates Performance of Future Projects in

Three Major Areas

TAKE-UP EXISTING PROJECTS Q Q QoQ

CBD 88.3% 83.9% -4.4%

South Jakarta 78.0% 68.6% -9.4%

Non-Prime area 69.4% 67.1% -2.3%

https://twitter.com/colliersintlhttp://www.linkedin.com/company/colliers-international%3Ftrk%3Dhb_tab_compy_id_5227https://www.facebook.com/colliersglobal%3Frf%3D105632526137251

-

8/19/2019 Research & Forecast Report Q1 2015 Jakarta Apartment

8/11

8

Te trend of slowing demand is likely to persist in the upcoming

quarters. o anticipate this, developers continue to offer

financing incentives like cash instalment payments and in some

cases, buyers are not required to make a down payment. Tis

payment scheme has become a preferable method of paying

since it does not require bank approval and offers flexibility to

manage the cash flow. Furthermore, developers, especially those

having strong working capital, are confident in offering longer

cash instalments for up to 60 months.

Payment Method Composition in PurchasingApartment

Source: Colliers International Indonesia - Research

QoQ Changes of Average Asking Prices of Apartmentin Jakarta

Source: Colliers International Indonesia - Research

Apartment For Lease

Supply

After Ascott Kuningan became available in the last quarter, there

was no new supply of apartments for lease during 1Q 2015.

As such, the total supply of both serviced and non-serviced

apartments in Jakarta remained at 8,519 units. Te majority ofapartments for lease in Jakarta are designed to meet expatriate

standards with spacious sizes, and therefore these projects are

mainly found in the CBD and South Jakarta for two main reasons,

i.e. the locations are in close proximity to the commercial area

and are still in the catchment area of reputable international

schools.

The Distribution of Apartment for Lease by Area

Source: Colliers International Indonesia - Research

Te apartment for lease market in Jakarta was mainly dominated

by two global brands of serviced apartment operator, i.e. Te

Ascott Limited and Frasers Hospitality. Te Ascott Limited has

three brands in operation, Ascott Residence, Somerset and

Citadines. Frasers Hospitality has only Fraser Residence but in

the upcoming years, Fraser Hospitality will have Fraser Suites

(Ciputra World II), Fraser Place (Setiabudi Sky Garden) and

Capri by Fraser.

A strong operator brand for serviced apartments is a crucial

factor for differentiation from other products and to guarantee a

global service level. Several major serviced apartment operators

have multiple brands to serve different market segments.

Research & Forecast Report | 1Q 2015 | Apartment | Colliers International

Mortgage

26%

Cash

Installment

58%

Hard Cash

16%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

2011 2012 2013 2014 2015YTD

CBD

44%

South Jakarta

35%

Non-prime

21%

https://twitter.com/colliersintlhttp://www.linkedin.com/company/colliers-international%3Ftrk%3Dhb_tab_compy_id_5227https://www.facebook.com/colliersglobal%3Frf%3D105632526137251

-

8/19/2019 Research & Forecast Report Q1 2015 Jakarta Apartment

9/11

9

Source: Colliers International Indonesia - Research and Fraser Cachet (Issue 18)

Occupancy

Te apartment for lease market experienced a minor occupancy

decrease of 0.4% QoQ to 75.3%. Leasing activity during the

initial period of 2015 was relatively stagnant highlighted with

“come and go” tenants and the absence of new enquiries from

expatriates. Tis figure also marked a 0.9% decrease compared

to the same quarter in 2014. Moreover, it should be noted that

a large number of new middle-upper to upper class strata-title

apartments is likely to put downward pressure on occupancy

levels of apartments for lease. Generally, individually owned

apartment units are offered furnished, which meets expatriate

standards and taste.

Source: Colliers International Indonesia - Research

Source: Colliers International Indonesia - Research

New enquiries were reportedly limited, with only a few

apartments in South Jakarta enjoying an increase in occupancy

during the reviewed quarter. Softening demand during this

quarter was mostly limited to inquiries from western expatriates.

Te recent plunge in oil prices has impacted the overall

sluggish performance of apartments for lease in Jakarta as some

companies related to the oil business reduced the number of

their expatriates working in Jakarta. For some years, the oil and

gas industry has consistently driven the leasing market, mainly

for western expatriates.

o cope with this situation, some apartments for lease (bothserviced and non-serviced) offered more flexible leasing terms

and payment to entice tenants, allowing for short-term leasing.

Previously, the apartments for lease require a minimum lease

term of six months paid in advance. Recently, landlords are

offering monthly accommodation that can be paid monthly.

Rental Rates

Te average monthly rent of apartments for lease in Jakarta

persisted in its decline, falling 2% QoQ to USD21.8/sq m/

month. Te overall downward trend in the rental rate was

triggered by sluggish demand in the previous year, which caused

management adjust rents to maintain the occupancy level.

Several apartments for lease are offered in local currency,

however with the weakening rupiah against the US dollar and

that the overall rental rates presented here are in US dollars, the

overall figure dropped somewhat. During the “tenants’ market”

in the coming period, rents are expected to soften during 2015

and this will characterise the whole leasing market.

Research & Forecast Report | 1Q 2015 | Apartment | Colliers International

List of Serviced Apartments Managed by Ascott and Frasers

NAME OF DEVELOPMENTYEAR OF

OPERATIONOPERATOR LOCATION TYPE

The Ascott Residence 1995 Ascott Limited Kebon Kacang Serviced Apartment

Somerset Grand Citra 1996 Ascott Limited Satrio Serviced Apartment

Countrywoods Residence 1996 Ascott Limited WR Supratman, Ciputat Serviced Apartment

Somerset Berlian 2006 Ascott Limited Permata Hijau Serviced ApartmentFraser Residence Sudirman 2011 Frasers Hospitality Setiabudi Serviced Apartment

Citadines Rasuna Jakarta 2013 Ascott Limited Rasuna Said Condotel

Fraser Residence Menteng 2014 Frasers Hospitality Menteng Serviced Apartment

Ascott Kuningan Jakarta 2014 Ascott Limited Satrio Serviced Apartment

Fraser Place at Setiabudi Sky Garden 2015 Frasers Hospitality Karbela Selatan Serviced Apartment

Somerset Kencana Jakarta 2015 Ascott Limited KHM Syafi'I Hadzami Condotel

Fraser Suites at Ciputra World Jakarta 2 2016 Frasers Hospitality Satrio Serviced Apartment

Fraser Suites Kebon Melati 2018 Frasers Hospitality Kebon Melati Serviced Apartment

Capri by Fraser 2018 Frasers Hospitality TB Simatupang Condotel

The QoQ Occupancy Performance for Non-Serviced

Apartment

AREA Q Q QoQ change

CBD 84.5% 84.6% 0.1%

South Jakarta 77.1% 76.7% -0.4%

Non-Prime area 74.9% 74.8% -0.1%

The QoQ Occupancy Performance for Serviced

Apartment

AREA Q Q QoQ change

CBD 78.7% 76.1% -2.6%

South Jakarta 74.6% 75.5% 0.9%

Non-Prime area 51.8% 53.4% 1.6%

https://twitter.com/colliersintlhttp://www.linkedin.com/company/colliers-international%3Ftrk%3Dhb_tab_compy_id_5227https://www.facebook.com/colliersglobal%3Frf%3D105632526137251

-

8/19/2019 Research & Forecast Report Q1 2015 Jakarta Apartment

10/11

10

Average Rental Rates of Apartment for Lease

Source: Colliers International Indonesia - Research

As mentioned above, some serviced apartments in the CBD

raised their rental rates by 3 to 5%. One serviced apartment

building adjusted the rental rate quite significantly and thus

impacted the drop of overall rental rates in the CBD. On the other

hand, apartments for lease in South Jakarta (including non-

prime area), which mostly consist of non-serviced apartments,

kept the rental rate the same as in the previous quarter. In

addition, since many non-serviced apartments quote the rental

rate in rupiah, the strengthening US dollar impacted the overall

rental rates in US dollars.

Source: Colliers International Indonesia - Research

Concluding Tought

Te government plans to introduce a new scheme of luxury

goods tax on residential property would adversely impact

property sales, particularly in the middle segment. Previously, a

5% luxury tax was expected to be imposed on property valued

at IDR10 billion but a revision is pending to reduce this to IDR2

billion. Te planned revisions would encompass a much widerrange of property sales, as a IDR2 billion apartment in Jakarta is

currently considered as middle to middle-upper segment, which

comprises about 23% of the total existing apartments. On the

other hand, it is unlikely to have a dramatic impact on the upper

to luxury class apartments, since this kind of buyer will pay for a

high-quality product and is not relatively price sensitive.

Te apartments for lease market is expected to remain quiet

in the upcoming quarters due to the current issues regarding

an additional regulation that will require foreigners to master

the Indonesian language before they are able to obtain a work

permit. Tis regulation may hamper the inflow of a number of

expatriates coming to Indonesia. In contrast, the establishmentof the ASEAN Economic Community should create a business

momentum that will gradually improve the Jakarta apartments

for lease market.

Research & Forecast Report | 1Q 2015 | Apartment | Colliers International

USD 0.00

USD 3.00

USD 6.00

USD 9.00

USD 12.00

USD 15.00USD 18.00

USD 21.00

USD 24.00

USD 27.00

USD 30.00

2 0 0 9

2 0 1 0

2 0 1 1

2 0 1 2

2 0 1 3

2 0 1 4

2 0 1 5 Y T D

R e n t a l R a t e s / s q m

/ m o n t h

CBD South Jakarta (inc . Non-Prime Area)

Average Rental Rates of Apartment for Lease

AREA Q Q QoQ change

CBD USD28.58 USD27.81 -2.7%

South Jakarta (includingnon-prime area)

USD15.94 USD15.83 -0.7%

https://twitter.com/colliersintlhttp://www.linkedin.com/company/colliers-international%3Ftrk%3Dhb_tab_compy_id_5227https://www.facebook.com/colliersglobal%3Frf%3D105632526137251

-

8/19/2019 Research & Forecast Report Q1 2015 Jakarta Apartment

11/11

Copyright © 2013 Colliers International.

The information contained herein has been obtained from sources deemed reliable. While every reasonable effort has been made to

ensure its accuracy, we cannot guarantee it. No responsibility is assumed for any inaccuracies. Readers are encouraged to consult

their professional advisors prior to acting on any of the material contained in this report.

About Colliers International

Colliers International is a global leader in commercial real estate services, with over 16,300 professionalsoperating out of more than 502 offices in 67 countries. A subsidiary of FirstService Corporation, ColliersInternational delivers a full range of services to real estate users, owners and investors worldwide,including global corporate solutions, brokerage, property and asset management, hotel investmentsales and consulting, valuation, consulting and appraisal services, mortgage banking and insightfulresearch. Te latest annual survey by the Lipsey Company ranked Colliers International as the second-most recognized commercial real estate firm in the world.

colliers.com

Primary Authors:

Ferry SalantoAssociate Director | Jakarta62 21 3043 [email protected]

Colliers International Indonesia

World Trade Centre 10th & 14th FloorsJalan Jenderal Sudirman Kav. 29 - 31Jakarta 12920Indonesia

TEL 62 21 3043 6888

Accelerating success.

502 offices in

67 countries on

6 continentsUnited States: 140

Canada: 31

Latin America: 24

Asia: 39

ANZ: 160

EMEA: 108

$2.3billion inannual revenue

158million square metersmanaged

16,300professionalsand staff

https://twitter.com/colliersintlhttp://www.linkedin.com/company/colliers-international%3Ftrk%3Dhb_tab_compy_id_5227https://www.facebook.com/colliersglobal%3Frf%3D105632526137251