Research & Forecast Report - Amazon S3 fileResearch & Forecast Report Jakarta | Apartment 3Q 2014...

12

Research & Forecast Report Jakarta | Apartment 3Q 2014 Accelerating success. “Despite political tension in Indonesia, the apartment market maintained a stable performance. Apartment price increase slowed to 17% increase YoY, compared to 20% in the same period last year. e average price in the CBD is recorded at IDR41.8 million/sq m, in South Jakarta is IDR 31.2 million/sq m and is IDR20.3 million in the non-prime areas. e overall take- up rate climbed by 1.4% QoQ to 86.6% this quarter.” - Ferry Salanto, Associate Director | Research Apartment Sector Apartment for Strata-title Supply Several projects currently under construction rescheduled their hand-over targets to the end of this year or early 2015. Technical issues, such as mechanical and electrical installation, and other finishing work were the most widely reported problems causing a delay in the hand-over process in this period. e long Idul Fitri holiday also hampered the finishing progress of new development. Overall, in 3Q 2014, the cumulative supply of strata-title apartments only increased by less than 2% QoQ and was registered at 139,239 units. e increase accounted for an additional 2,183 units that came from the completion of eight towers at six apartment projects, including Ambassade Residence, MyHome Apartment, e Pakubuwono Signature, Sherwood Residence (Tower Regent), Sky Terrace Lagoon, and e Green Pramuka (Tower Bougenville). Tower Regent is the final tower being handed over at the Sherwood Residence project, while Tower Bougenville is the fourth of a total of seven towers planned to be built at e Green Pramuka project. Ambassade Residence, MyHome Apartment, e Pakubuwono Signature and Sky Terrace Lagoon are brand-new projects comprising 1,083 units scattered in the CBD, South Jakarta and West Jakarta areas. Until the third quarter of 2014, 33% of the total 20,899 projected units this year have been handed over, leaving about 14,000 units which will be available in the next quarter or next year. Currently, there are 21 projects left which are expected to be completed by 2014; 48% of them will likely meet their target of beginning operations this year, while the rest are predicted to commence in the first or second quarter of 2015. As a result, the total annual supply of 2015 will post a new record of approximately 28,950 units should all of these projects be completed. Based on our database combined with a field survey, from a total of 51 projects that are expected to be completed in 2015 plus the additional projects from 2014, 66.7% of projects consisting of 19,213 apartment units will likely meet the target.

Transcript of Research & Forecast Report - Amazon S3 fileResearch & Forecast Report Jakarta | Apartment 3Q 2014...

Research & Forecast Report

Jakarta | Apartment3Q 2014

Accelerating success.

“Despite political tension in Indonesia, the apartment market maintained a stable performance. Apartment price increase slowed to 17% increase YoY, compared to 20% in the same period last year. The average price in the CBD is recorded at IDR41.8 million/sq m, in South Jakarta is IDR 31.2 million/sq m and is IDR20.3 million in the non-prime areas. The overall take-up rate climbed by 1.4% QoQ to 86.6% this quarter.”

- Ferry Salanto, Associate Director | Research

Apartment SectorApartment for Strata-title

SupplySeveral projects currently under construction rescheduled their hand-over targets to the end of this year or early 2015. Technical issues, such as mechanical and electrical installation, and other finishing work were the most widely reported problems causing a delay in the hand-over process in this period. The long Idul Fitri holiday also hampered the finishing progress of new development. Overall, in 3Q 2014, the cumulative supply of strata-title apartments only increased by less than 2% QoQ and was registered at 139,239 units. The increase accounted for an additional 2,183 units that came from the completion of eight towers at six apartment projects, including Ambassade Residence, MyHome Apartment, The Pakubuwono Signature, Sherwood Residence (Tower Regent), Sky Terrace Lagoon, and The Green Pramuka (Tower Bougenville). Tower Regent is the final tower being handed over at the Sherwood Residence project, while Tower Bougenville is the fourth of a total of seven towers planned to be built at The Green Pramuka project. Ambassade Residence, MyHome Apartment, The Pakubuwono Signature and Sky Terrace Lagoon are brand-new projects comprising 1,083 units scattered in the CBD, South Jakarta and West Jakarta areas.

Until the third quarter of 2014, 33% of the total 20,899 projected units this year have been handed over, leaving about 14,000 units which will be available in the next quarter or next year. Currently, there are 21 projects left which are expected to be completed by 2014; 48% of them will likely meet their target of beginning operations this year, while the rest are predicted to commence in the first or second quarter of 2015. As a result, the total annual supply of 2015 will post a new record of approximately 28,950 units should all of these projects be completed.

Based on our database combined with a field survey, from a total of 51 projects that are expected to be completed in 2015 plus the additional projects from 2014, 66.7% of projects consisting of 19,213 apartment units will likely meet the target.

2 Research & Forecast Report | 3Q 2014 | Apartment | Colliers International

Source: Colliers International Indonesia - Research

List of Completed Projecs During 3Q 2014development location region developer no. of Units

Ambassade Residence Tower A Jl. Denpasar Raya CBD PT. Duta Regency 234

MyHome Apartment Jl. Prof Dr Satrio CBD Ciputra 136

The Pakubuwono Signature Jl. Teuku Nyak Syarief South Jakarta PT. Mandiri Eka Abadi 188

Sherwood Residence (Tower Regent) Kelapa Gading North Jakarta Summarecon 100

Sky Terrace Lagoon (3 Towers) Jl. Tampak Siring blok KJE No. 30-32, Kalideres

West Jakarta PT. Fajar Surya Perkasa 525

The Grreen Pramuka (Tower Bougenville) Jl. Jenderal Ahmad Yani Central Jakarta PT. Duta Paramindo 1,000

The Hive @ Tamansari Jl. DI Panjaitan East Jakarta Wika Realty 422

The Green Pramuka (Tower Chrysant) Jl. Jenderal Ahmad Yani Central Jakarta PT Duta Paramindo 1,000

total 2,183

List of Newly Introduced Apartments Projects During 3Q 2014

newly introdUced apartment location region expected completion time

estimated price/sq m*

asking price/sq m (exclUding vat)

Lavie Kuningan CBD 2018 40 - 42 Mio 320

Grand Madison Park Tanjung Duren West Jakarta 2018 34 - 35 Mio 300

Sedayu City @ Kelapa Gading (14 Tower) Kelapa Gading North Jakarta 2018** 27 – 28 Mio 12,000

Source: Colliers International Indonesia - Research

*Price exclude VAT 10%**First Phase

During this quarter, some developers have introduced their new projects to their loyal customers by using the NUP system. Recently, the NUP system has been commonly used for new apartment projects in Jakarta, especially for middle- and upper-class projects. This system involves a mutualism symbiotic relationship between the developer and the buyer. For developers, through the NUP system, the marketing team will get the “big picture” from the buyers, regarding the attractiveness

and the affordability of their new project, so they will have a formula to boost apartment sales. On the other hand, since there is a claim that the booking fee is 100% refundable, the buyer will not lose their money if the desired apartment unit does not meet their expectations. During this period, three new projects in West Jakarta, North Jakarta and CBD area had soft launches. These new projects will officially launch either in 4Q 2014 or early 2015.

Newly Introduced Apartments Projects During 3Q 2014

Lavie Grand Madison Park Sedayu City

3

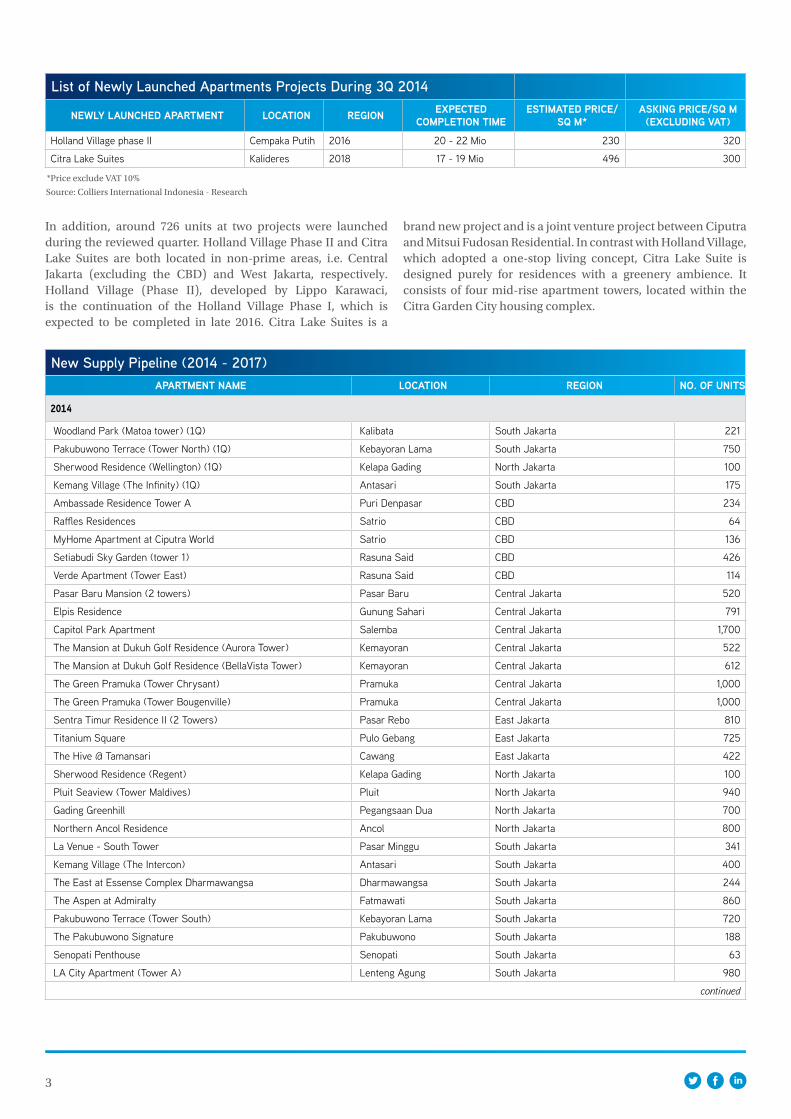

List of Newly Launched Apartments Projects During 3Q 2014

newly laUnched apartment location region expected completion time

estimated price/sq m*

asking price/sq m (exclUding vat)

Holland Village phase II Cempaka Putih 2016 20 - 22 Mio 230 320

Citra Lake Suites Kalideres 2018 17 - 19 Mio 496 300

Source: Colliers International Indonesia - Research

*Price exclude VAT 10%

In addition, around 726 units at two projects were launched during the reviewed quarter. Holland Village Phase II and Citra Lake Suites are both located in non-prime areas, i.e. Central Jakarta (excluding the CBD) and West Jakarta, respectively. Holland Village (Phase II), developed by Lippo Karawaci, is the continuation of the Holland Village Phase I, which is expected to be completed in late 2016. Citra Lake Suites is a

brand new project and is a joint venture project between Ciputra and Mitsui Fudosan Residential. In contrast with Holland Village, which adopted a one-stop living concept, Citra Lake Suite is designed purely for residences with a greenery ambience. It consists of four mid-rise apartment towers, located within the Citra Garden City housing complex.

New Supply Pipeline (2014 - 2017)apartment name location region no. of Units

2014

Woodland Park (Matoa tower) (1Q) Kalibata South Jakarta 221

Pakubuwono Terrace (Tower North) (1Q) Kebayoran Lama South Jakarta 750

Sherwood Residence (Wellington) (1Q) Kelapa Gading North Jakarta 100

Kemang Village (The Infinity) (1Q) Antasari South Jakarta 175

Ambassade Residence Tower A Puri Denpasar CBD 234

Raffles Residences Satrio CBD 64

MyHome Apartment at Ciputra World Satrio CBD 136

Setiabudi Sky Garden (tower 1) Rasuna Said CBD 426

Verde Apartment (Tower East) Rasuna Said CBD 114

Pasar Baru Mansion (2 towers) Pasar Baru Central Jakarta 520

Elpis Residence Gunung Sahari Central Jakarta 791

Capitol Park Apartment Salemba Central Jakarta 1,700

The Mansion at Dukuh Golf Residence (Aurora Tower) Kemayoran Central Jakarta 522

The Mansion at Dukuh Golf Residence (BellaVista Tower) Kemayoran Central Jakarta 612

The Green Pramuka (Tower Chrysant) Pramuka Central Jakarta 1,000

The Green Pramuka (Tower Bougenville) Pramuka Central Jakarta 1,000

Sentra Timur Residence II (2 Towers) Pasar Rebo East Jakarta 810

Titanium Square Pulo Gebang East Jakarta 725

The Hive @ Tamansari Cawang East Jakarta 422

Sherwood Residence (Regent) Kelapa Gading North Jakarta 100

Pluit Seaview (Tower Maldives) Pluit North Jakarta 940

Gading Greenhill Pegangsaan Dua North Jakarta 700

Northern Ancol Residence Ancol North Jakarta 800

La Venue - South Tower Pasar Minggu South Jakarta 341

Kemang Village (The Intercon) Antasari South Jakarta 400

The East at Essense Complex Dharmawangsa Dharmawangsa South Jakarta 244

The Aspen at Admiralty Fatmawati South Jakarta 860

Pakubuwono Terrace (Tower South) Kebayoran Lama South Jakarta 720

The Pakubuwono Signature Pakubuwono South Jakarta 188

Senopati Penthouse Senopati South Jakarta 63

LA City Apartment (Tower A) Lenteng Agung South Jakarta 980

continued

4 Research & Forecast Report | 3Q 2014 | Apartment | Colliers International

apartment name location region no. of Units

continuation

La Maison Barito Barito South Jakarta 80

Botanica Apartment (3 Towers) Simprug South Jakarta 626

The Bellevue at Pondok Indah Pondok Indah South Jakarta 40

Green Central Tower Cerberra Gajah Mada West Jakarta 420

The Windsor (Tower I) Puri Indah West Jakarta 176

The Windsor (Tower II) Puri Indah West Jakarta 164

Sky Terrace Lagoon Kalideres West Jakarta 525

Metro Park Residence Kebon Jeruk West Jakarta 1,200

Green Palm Residence @ Puri Kosambi West Jakarta 1,000

2015

East Park Apartment (Tower C) KRT Radjiman East Jakarta 550

The Residence (CWJ 2) Satrio CBD 119

The Orchad Satrio (CWJ 2) Satrio CBD 349

Setiabudi Sky Garden (tower 2) Setiabudi CBD 160

T - Plaza Residence (Tower B) Pejompongan Central Jakarta 500

Menteng Park Cikini Central Jakarta 756

The Grreen Pramuka (Tower Orchid) Pramuka Central Jakarta 1,000

The Grreen Pramuka (Tower Penelope) Pramuka Central Jakarta 1,000

The Green Pramuka (Tower Scarlet) Pramuka Central Jakarta 1,000

The H Residence Kemayoran (Amethyst) Kemayoran Central Jakarta 800

Green Signature Apartment MT. Haryono East Jakarta 800

Bassura City (Tower Flamboyan) Basuki Rahmat East Jakarta 1,000

Bassura City (Tower Edelweiss) Basuki Rahmat East Jakarta 1,000

Bassura City (Tower Dahlia) Basuki Rahmat East Jakarta 1,000

Bassura City (Tower Cattleya) Basuki Rahmat East Jakarta 600

Bassura City (Tower Alamanda) Basuki Rahmat East Jakarta 600

Teluk Intan (Tower Saphire) Teluk Gong North Jakarta 1,100

Tifolia Apartment Perintis Kemerdekaan East Jakarta 500

Pluit Seaview (Tower Belize) Pluit North Jakarta 300

Callia Apartment Perintis Kemerdekaan East Jakarta 560

The Oakwood Sky Garden (2 Towers) Pluit North Jakarta 700

Pluit Seaview (Tower Ibiza) Pluit North Jakarta 500

Pluit Seaview (Tower Bahama) Pluit North Jakarta 650

Green Bay Pluit (Sea View) Pluit North Jakarta 2,072

Kemang Village - The Bloomington Antasari South Jakarta 150

The Royal Olive Residence Tower I Buncit Raya South Jakarta 225

Woodland Park (Cendana Tower) Kalibata South Jakarta 218

Senopati Suites 2 Senopati South Jakarta 81

1 Park Avenue Gandaria South Jakarta 279

Nine Residence Warung Buncit South Jakarta 246

Providence Park Permata Hijau South Jakarta 114

Kencana Residence Pondok Indah South Jakarta 173

District 8 (Tower Eternity) Senopati South Jakarta 400

District 8 (Tower Infinity) Senopati South Jakarta 280

Izzara Apartment (2 Tower @ 225 unit) TB. Simatupang South Jakarta 450

Lexington Rersidence (Tower 1) Pondok Pinang South Jakarta 270

Lexington Rersidence (Tower 2) Pondok Pinang South Jakarta 270

continued

5 Research & Forecast Report | 3Q 2014 | Apartment | Colliers International

apartment name location region no. of Units

continuation

The Aspen Peak at Admiralty Fatmawati South Jakarta 644

Belmont Residence (Tower Montblanc) Meruya Ilir West Jakarta 350

Gianetti Apartment Kemanggisan West Jakarta 500

St. Moritz (New Presidential Tower) Puri Indah West Jakarta 150

Satu8 Residence Kedoya West Jakarta 174

The Nest Apartment Meruya Utara West Jakarta 1,100

Point 8 (Air Crew Tower) Daan Mogot West Jakarta 546

Gallery West Kebon Jeruk West Jakarta 280

19 Avenue Apartment Daan Mogot West Jakarta 338

2016

St Moritz (The New Ambassador Suite Tower) Puri Indah West Jakarta 200

The H Residence MT Haryono East Jakarta 383

Sudirman Suites Sudirman CBD 380

Senopati Suites 3 Senopati South Jakarta 54

Signature Park Grande MT Haryono East Jakarta 1,100

Grand Pakubuwono Terrace Kebayoran Lama South Jakarta 435

Sentosa Residence Cempaka Putih Central Jakarta 687

Gold Coast Apartment (Atlantic Tower) Pantai Indah Kapuk North Jakarta 568

Grand Pancoran Pancoran South Jakarta 120

Sudirman Hill Residence Karet Central Jakarta 255

Apartment Pejaten Park Residence Warung Buncit South Jakarta 380

Belmont Residence (TowerAthena) Meruya West Jakarta 165

Four Winds Permata Hijau South Jakarta 122

Capitol Suites Prapatan Raya Central Jakarta 327

Puri Mansion Apartment (Tower A) Puri Kembangan West Jakarta 900

Madison Park Tanjung Duren West Jakarta 1,200

Gayanti City (2 Towers) Gatot Subroto CBD 318

Verde Two (Tower 1) Rasuna Said CBD 152

Verde Two (Tower 2) Rasuna Said CBD 152

Bellevue Place Tebet South Jakarta 128

Kebayoran Icon Kebayoran Lama South Jakarta 256

Veranda Pesanggrahan West Jakarta 174

2017

Regatta London Tower Pantai Mutiara North Jakarta 276

Central 88 (2 Towers) Kemayoran Central Jakarta 612

Holland Village Cempaka Putih Central Jakarta 400

Domaine Sudirman CBD 186

Skyline Residence (2 Towers) DI Panjaitan East Jakarta 481

Kemang Penthouse Kemang South Jakarta 262

The Foresque Pasar Minggu South Jakarta 600

Springhill Golf Suites Kemayoran Central Jakarta 450

Sentra Timur Residence (Tosca Tower) Pulogebang East Jakarta 133

Taman Anggrek Residence Tanjung Duren West Jakarta 3,000

Puri Orchad (3 Tower) Kembangan West Jakarta 3,000

The Langham Residences Senopati South Jakarta 57

continued

6

apartment name location region no. of Units

continuation

Anandamaya Residences (3 towers) Sudirman CBD 500

Maqna Residence Meruya West Jakarta 380

Vittoria Residence (3 tower) Daan Mogot West Jakarta 1,100

One Otium Residence Antasari South Jakarta 160

Wang Residence Kedoya West Jakarta 250

The Batik @ Pejaten Pejaten South Jakarta 200

Source: Colliers International Indonesia - Research

DemandSales activity in the Jakarta apartment market during 3Q 2014 increased modestly. The overall take-up rate of the Jakarta apartment market was 86.6%, an increase of only 1.4% QoQ. Based on the findings in the field, after the Idul Fitri holiday and the presidential election, sales activities have gradually trended upward. Less newly launched / introduced projects, compared to the previous quarter, has affected the increase of the overall take-up rate. Based on a field survey and findings from the marketing of several apartment projects, the sales activity has been slightly hampered, on the back of uncertainty prior to the presidential election. However, sales activity has bounced back in a positive trend since the new president elect was announced.

In addition to the high demand for inner city living and a gradual shift in the trend of living from landed houses to high-rise apartment buildings, people buy apartments for investment reasons. Both end-users and investors treat apartment units as an asset. From the end-user’s perspective, the apartment can be an asset that hedges against inflation. For investors, owning an apartment can provide recurring income from rent and keep cash flow stable if the owners buy the apartment with a mortgage.

Take-up Rate Trend Between Existing and Future Projects

Source: Colliers International Indonesia - Research

50%

60%

70%

80%

90%

100%

2007

2008

2009

2010

2011

2012

2013

2014

YTD

Existing Future

Until September 2014, the take-up rate of existing apartments in Jakarta reached 95%, relatively stable from the previous quarter and an increase of only 2% YoY. On the other hand, the take-up rate of under-construction projects was 73.2%, rising by 2.7% from the previous quarter.

Based on the market segment, the pre-sales rate of middle upper class projects achieved the highest take-up rate of 84%, followed by upper class at 78%. The high pre-sales absorption rate of middle upper and upper class was related to the high demand in those areas, such as Pondok Indah, Simprug, Senopati, Permata Hijau, Kemayoran, Kedoya and in the CBD area. The large number of apartment units from low and middle lower class apartment projects will likely increase market competition and impact the overall sales rate, evidenced by lower take-up rates of 71 and 72%, respectively. However, there are only two luxury apartment projects under construction, Raffles Residences and The Langham Residences, which posted an average sales rate of 71%.

Average Take-up Rate Performance by Class on Future Projects

Source: Colliers International Indonesia - Research

50%

60%

70%

80%

90%

100%

Low Middle-Low Middle-Upper Upper Lux

7 Research & Forecast Report | 3Q 2014 | Apartment | Colliers International

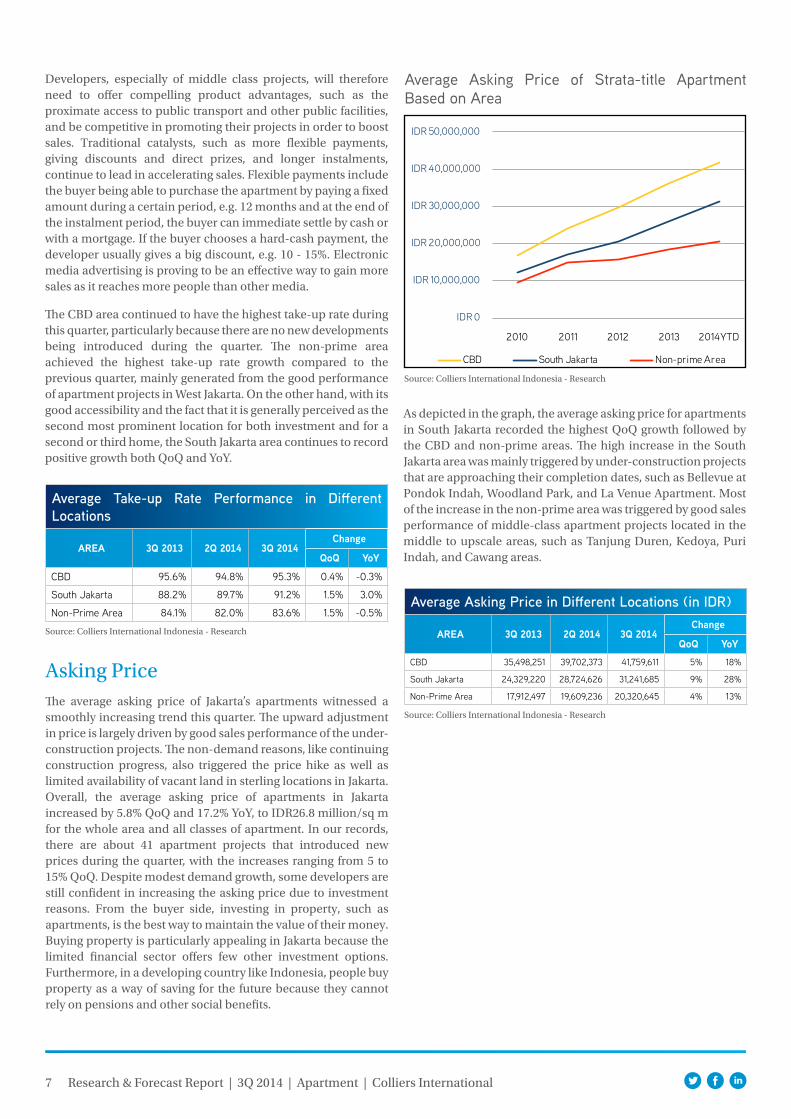

Developers, especially of middle class projects, will therefore need to offer compelling product advantages, such as the proximate access to public transport and other public facilities, and be competitive in promoting their projects in order to boost sales. Traditional catalysts, such as more flexible payments, giving discounts and direct prizes, and longer instalments, continue to lead in accelerating sales. Flexible payments include the buyer being able to purchase the apartment by paying a fixed amount during a certain period, e.g. 12 months and at the end of the instalment period, the buyer can immediate settle by cash or with a mortgage. If the buyer chooses a hard-cash payment, the developer usually gives a big discount, e.g. 10 - 15%. Electronic media advertising is proving to be an effective way to gain more sales as it reaches more people than other media.

The CBD area continued to have the highest take-up rate during this quarter, particularly because there are no new developments being introduced during the quarter. The non-prime area achieved the highest take-up rate growth compared to the previous quarter, mainly generated from the good performance of apartment projects in West Jakarta. On the other hand, with its good accessibility and the fact that it is generally perceived as the second most prominent location for both investment and for a second or third home, the South Jakarta area continues to record positive growth both QoQ and YoY.

Source: Colliers International Indonesia - Research

Average Take-up Rate Performance in Different Locations

area 3q 2013 2q 2014 3q 2014change

qoq yoy

CBD 95.6% 94.8% 95.3% 0.4% -0.3%

South Jakarta 88.2% 89.7% 91.2% 1.5% 3.0%

Non-Prime Area 84.1% 82.0% 83.6% 1.5% -0.5%

Asking PriceThe average asking price of Jakarta’s apartments witnessed a smoothly increasing trend this quarter. The upward adjustment in price is largely driven by good sales performance of the under-construction projects. The non-demand reasons, like continuing construction progress, also triggered the price hike as well as limited availability of vacant land in sterling locations in Jakarta. Overall, the average asking price of apartments in Jakarta increased by 5.8% QoQ and 17.2% YoY, to IDR26.8 million/sq m for the whole area and all classes of apartment. In our records, there are about 41 apartment projects that introduced new prices during the quarter, with the increases ranging from 5 to 15% QoQ. Despite modest demand growth, some developers are still confident in increasing the asking price due to investment reasons. From the buyer side, investing in property, such as apartments, is the best way to maintain the value of their money. Buying property is particularly appealing in Jakarta because the limited financial sector offers few other investment options. Furthermore, in a developing country like Indonesia, people buy property as a way of saving for the future because they cannot rely on pensions and other social benefits.

Average Asking Price of Strata-title Apartment Based on Area

Source: Colliers International Indonesia - Research

As depicted in the graph, the average asking price for apartments in South Jakarta recorded the highest QoQ growth followed by the CBD and non-prime areas. The high increase in the South Jakarta area was mainly triggered by under-construction projects that are approaching their completion dates, such as Bellevue at Pondok Indah, Woodland Park, and La Venue Apartment. Most of the increase in the non-prime area was triggered by good sales performance of middle-class apartment projects located in the middle to upscale areas, such as Tanjung Duren, Kedoya, Puri Indah, and Cawang areas.

IDR 0

IDR 10,000,000

IDR 20,000,000

IDR 30,000,000

IDR 40,000,000

IDR 50,000,000

2010 2011 2012 2013 2014YTD

CBD South Jakarta Non-prime Area

Source: Colliers International Indonesia - Research

Average Asking Price in Different Locations (in IDR)

area 3q 2013 2q 2014 3q 2014change

qoq yoyCBD 35,498,251 39,702,373 41,759,611 5% 18%

South Jakarta 24,329,220 28,724,626 31,241,685 9% 28%

Non-Prime Area 17,912,497 19,609,236 20,320,645 4% 13%

8 Research & Forecast Report | 3Q 2014 | Apartment | Colliers International

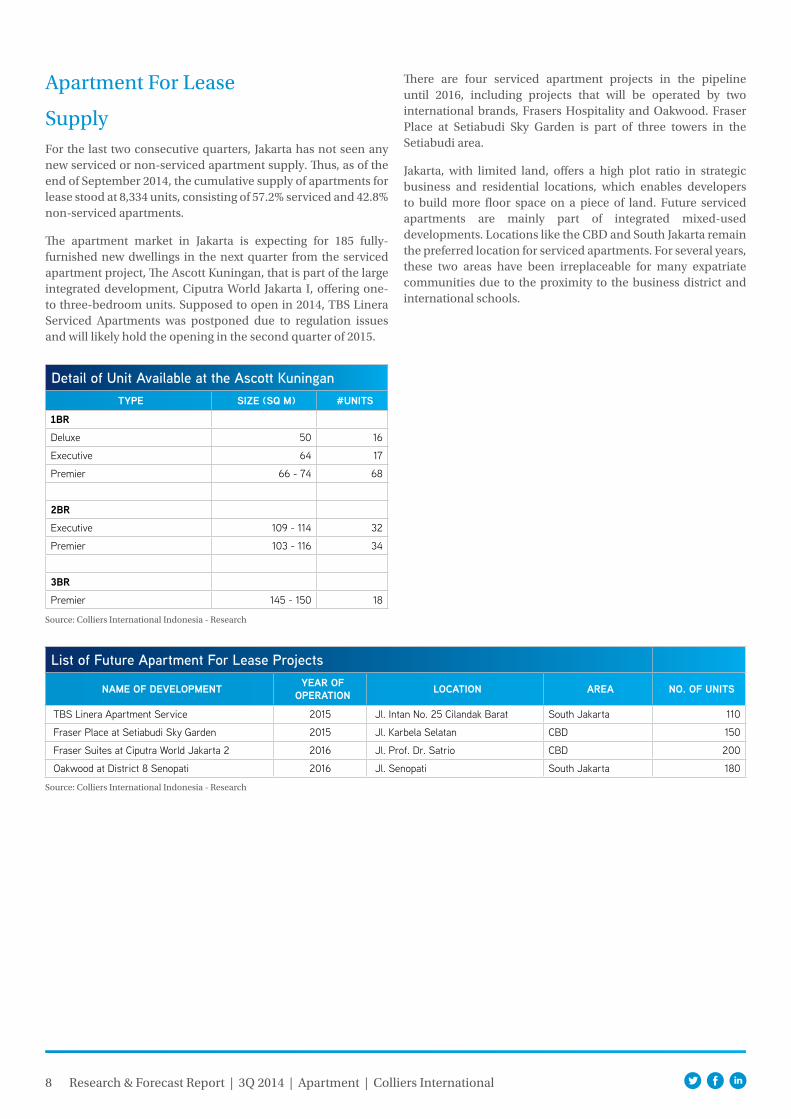

Apartment For Lease

SupplyFor the last two consecutive quarters, Jakarta has not seen any new serviced or non-serviced apartment supply. Thus, as of the end of September 2014, the cumulative supply of apartments for lease stood at 8,334 units, consisting of 57.2% serviced and 42.8% non-serviced apartments.

The apartment market in Jakarta is expecting for 185 fully-furnished new dwellings in the next quarter from the serviced apartment project, The Ascott Kuningan, that is part of the large integrated development, Ciputra World Jakarta I, offering one- to three-bedroom units. Supposed to open in 2014, TBS Linera Serviced Apartments was postponed due to regulation issues and will likely hold the opening in the second quarter of 2015.

Source: Colliers International Indonesia - Research

List of Future Apartment For Lease Projects

name of development year of operation location area no. of Units

TBS Linera Apartment Service 2015 Jl. Intan No. 25 Cilandak Barat South Jakarta 110

Fraser Place at Setiabudi Sky Garden 2015 Jl. Karbela Selatan CBD 150

Fraser Suites at Ciputra World Jakarta 2 2016 Jl. Prof. Dr. Satrio CBD 200

Oakwood at District 8 Senopati 2016 Jl. Senopati South Jakarta 180

Source: Colliers International Indonesia - Research

Detail of Unit Available at the Ascott Kuningantype size (sq m) #Units

1BrDeluxe 50 16

Executive 64 17

Premier 66 - 74 68

2BrExecutive 109 - 114 32

Premier 103 - 116 34

3BrPremier 145 - 150 18

There are four serviced apartment projects in the pipeline until 2016, including projects that will be operated by two international brands, Frasers Hospitality and Oakwood. Fraser Place at Setiabudi Sky Garden is part of three towers in the Setiabudi area.

Jakarta, with limited land, offers a high plot ratio in strategic business and residential locations, which enables developers to build more floor space on a piece of land. Future serviced apartments are mainly part of integrated mixed-used developments. Locations like the CBD and South Jakarta remain the preferred location for serviced apartments. For several years, these two areas have been irreplaceable for many expatriate communities due to the proximity to the business district and international schools.

9 Research & Forecast Report | 3Q 2014 | Apartment | Colliers International

Average Rental RatesOverall, no rental increases occurred during the quarter. As we previously predicted in the 2Q 2014 report, despite the hike in electricity tariffs in July 2014, most apartments did not immediately increase the rental rates, and will only apply a yearly cyclical rent increase instead. During 3Q 2014, the average rental rate of apartments for lease stood at USD21.80/sq m/month. This figure represents the average for all of Jakarta with the CBD posting the highest average rental rates at USD27.60/sq m/month, followed by South Jakarta at USD15.34 and Non-prime areas at USD19.45/sq m/month.

The direct competition from individually owned apartments does not immediately impact the drop in occupancy rates. One of the reasons for this is the long-term partnership between companies with the serviced apartment operators to provide houses for their client’s representatives in Jakarta. Despite a massive amount of future strata-titled apartment supply, the occupancy rate of apartments for lease is projected to hold steady at between 70 and 80%. Such a steady condition is likely to hold back rental rate growth. Rent growth is anticipated to be less aggressive going ahead as compared to the previous years.

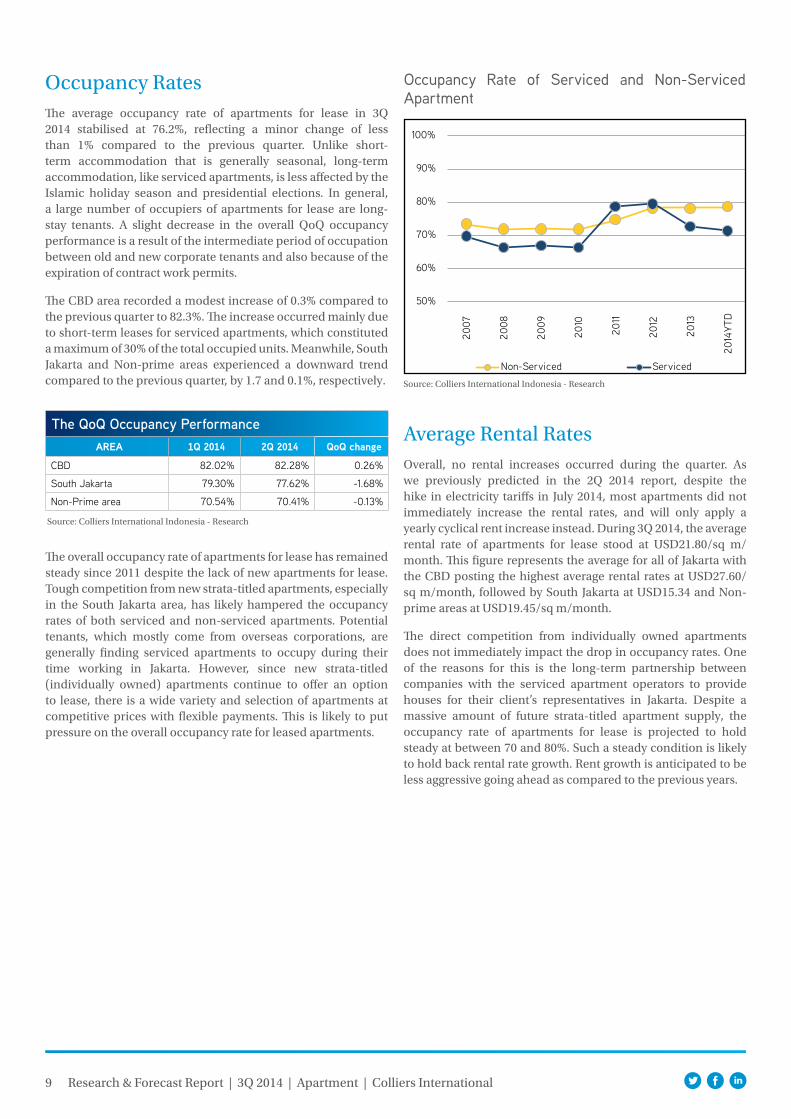

Occupancy RatesThe average occupancy rate of apartments for lease in 3Q 2014 stabilised at 76.2%, reflecting a minor change of less than 1% compared to the previous quarter. Unlike short-term accommodation that is generally seasonal, long-term accommodation, like serviced apartments, is less affected by the Islamic holiday season and presidential elections. In general, a large number of occupiers of apartments for lease are long-stay tenants. A slight decrease in the overall QoQ occupancy performance is a result of the intermediate period of occupation between old and new corporate tenants and also because of the expiration of contract work permits.

The CBD area recorded a modest increase of 0.3% compared to the previous quarter to 82.3%. The increase occurred mainly due to short-term leases for serviced apartments, which constituted a maximum of 30% of the total occupied units. Meanwhile, South Jakarta and Non-prime areas experienced a downward trend compared to the previous quarter, by 1.7 and 0.1%, respectively.

Source: Colliers International Indonesia - Research

The QoQ Occupancy Performancearea 1q 2014 2q 2014 qoq change

CBD 82.02% 82.28% 0.26%

South Jakarta 79.30% 77.62% -1.68%

Non-Prime area 70.54% 70.41% -0.13%

The overall occupancy rate of apartments for lease has remained steady since 2011 despite the lack of new apartments for lease. Tough competition from new strata-titled apartments, especially in the South Jakarta area, has likely hampered the occupancy rates of both serviced and non-serviced apartments. Potential tenants, which mostly come from overseas corporations, are generally finding serviced apartments to occupy during their time working in Jakarta. However, since new strata-titled (individually owned) apartments continue to offer an option to lease, there is a wide variety and selection of apartments at competitive prices with flexible payments. This is likely to put pressure on the overall occupancy rate for leased apartments.

Occupancy Rate of Serviced and Non-Serviced Apartment

Source: Colliers International Indonesia - Research

50%

60%

70%

80%

90%

100%

2007

2008

2009

2010

2011

2012

2013

2014

YTD

Non-Serviced Serviced

10 Research & Forecast Report | 3Q 2014 | Apartment | Colliers International

OutlookPositive outlook in the Jakarta apartment market, particularly strata-titled apartments, is expected to continue. Despite current market conditions softening due to a slowdown in the economy and the presidential election which hampered buying activities from both investors and end-users, the take-up rate of Jakarta apartments during this quarter increased modestly. After gradually softening for three consecutive quarters, the market has started to show positive momentum, evidenced by a slight increase in the average take-up rate, particularly in under-construction projects.

The growing middle class, which more than doubled in size from 2006 to 2011 (source: Euromonitor International), as well as traffic jams in Jakarta, will further push demand for apartments, especially from young families or executives who work in Jakarta. As mentioned above, there are currently about 46,688 apartment units to be completed in the market between now and 2016.

However, the plan to slowly reduce fuel subsidies in Indonesia is currently an issue in the news because there is a strong link between the increase in fuel prices and economic growth, including inflation rate. Overall, the increasing fuel price likely means that the cost of anything relying on transport will be affected, including raw materials for building.

From 2010 to 2014 YTD, the average asking rental rate for apartments in the CBD grew by 8% per annum, while for apartments in South Jakarta (including Non-prime areas), it only grew by 4% per annum. In fact, the upward trend of rental rates was mostly affected by periodic increases in serviced apartment rents, typically by 10 - 12% per year. Meanwhile, non-serviced apartments generally reviewed the new rental rate in every two or three years with a lower percentage of increase than serviced apartments.

With tight competition from the new, individually owned apartments, as well as limitations on expatriate arrivals since the government implemented the new decree from the Ministry of Manpower and Transmigration, the rental rate growth is expected to be less aggressive compared to the previous years.

Average Rental Rates of Apartment For Lease (Serviced and Non-Serviced)

Source: Colliers International Indonesia - Research

USD 0

USD 5

USD 10

USD 15

USD 20

USD 25

USD 3020

09

2010

2011

2012

2013

2014

YTD

CBD South Jakarta (including Non-prime Area)

11 Research & Forecast Report | 3Q 2014 | Colliers International

Copyright © 2013 Colliers International.

The information contained herein has been obtained from sources deemed reliable. While every reasonable effort has been made to ensure its accuracy, we cannot guarantee it. No responsibility is assumed for any inaccuracies. Readers are encouraged to consult their professional advisors prior to acting on any of the material contained in this report.

About Colliers International

Colliers International is a global leader in commercial real estate services, with over 15,800 professionals operating out of more than 485 offices in 63 countries. A subsidiary of FirstService Corporation, Colliers International delivers a full range of services to real estate users, owners and investors worldwide, including global corporate solutions, brokerage, property and asset management, hotel investment sales and consulting, valuation, consulting and appraisal services, mortgage banking and insightful research. The latest annual survey by the Lipsey Company ranked Colliers International as the second-most recognized commercial real estate firm in the world.

colliers.com

Primary Authors:Ferry SalantoAssociate Director | Jakarta62 21 521 1400 ext [email protected]

Colliers International IndonesiaWorld Trade Centre 10th & 14th floorJalan Jenderal Sudirman Kav. 29 - 31Jakarta 12920Indonesia

TEL 62 21 521 1400

Accelerating success.

485 offices in 63 countries on 6 continentsUnited States: 146 Canada: 44 Latin America: 25 Asia: 38 ANZ: 148 EMEA: 84

$2.1billion in annual revenue

1.46billion square feet under management

15,800professionals and staff