Characterization of selective polysilicon deposition for ...

PV Polysilicon and Wafering Industry – Supply Chain and Market Updates

Marcus Lentz Sr. Industry Analyst PVMC

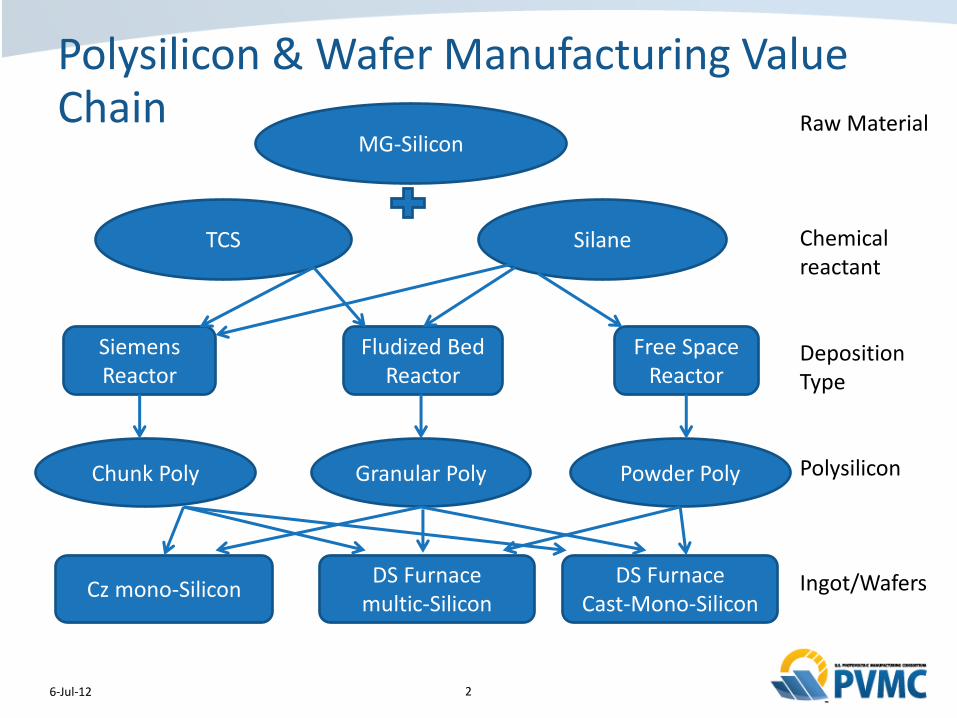

Polysilicon & Wafer Manufacturing Value Chain

2 6-Jul-12

MG-Silicon

TCS Silane

Siemens Reactor

Fludized Bed Reactor

Free Space Reactor

Chunk Poly Granular Poly Powder Poly

Cz mono-Silicon DS Furnace

multic-Silicon

Raw Material Chemical reactant Deposition Type Polysilicon Ingot/Wafers DS Furnace

Cast-Mono-Silicon

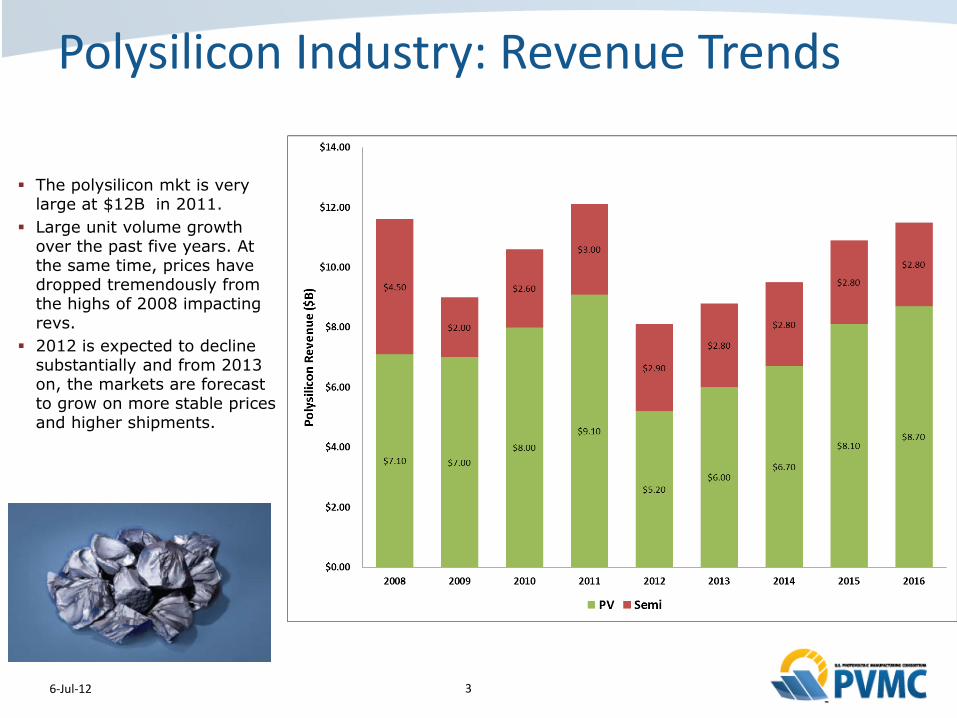

Polysilicon Industry: Revenue Trends

3 6-Jul-12

The polysilicon mkt is very large at $12B in 2011.

Large unit volume growth over the past five years. At the same time, prices have dropped tremendously from the highs of 2008 impacting revs.

2012 is expected to decline substantially and from 2013 on, the markets are forecast to grow on more stable prices and higher shipments.

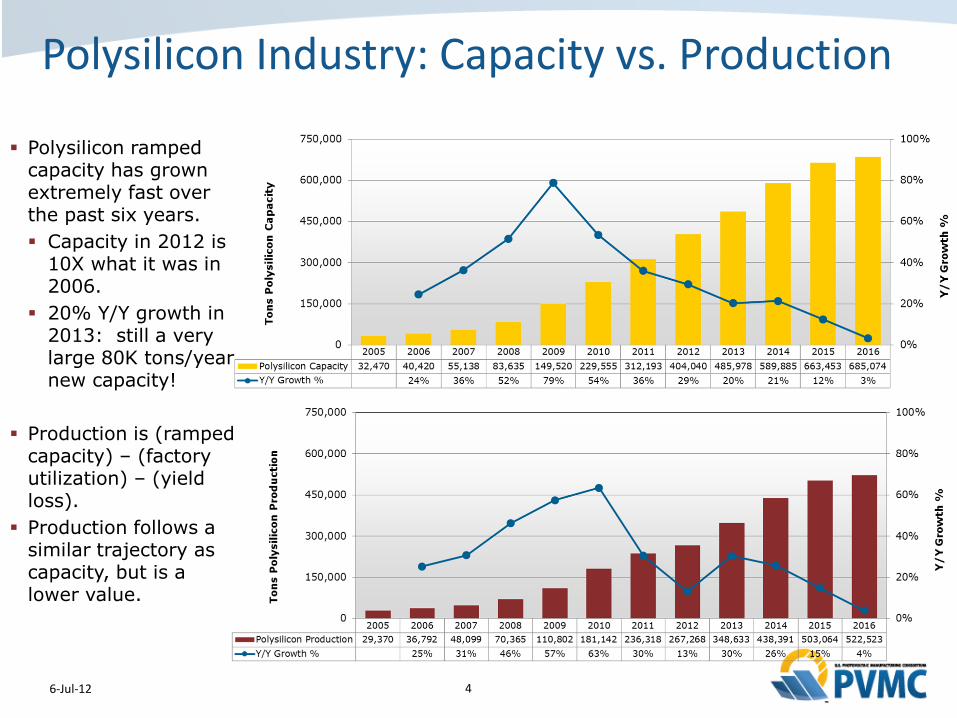

Polysilicon Industry: Capacity vs. Production

4 6-Jul-12

Polysilicon ramped capacity has grown extremely fast over the past six years.

Capacity in 2012 is 10X what it was in 2006.

20% Y/Y growth in 2013: still a very large 80K tons/year new capacity!

Production is (ramped capacity) – (factory utilization) – (yield loss).

Production follows a similar trajectory as capacity, but is a lower value.

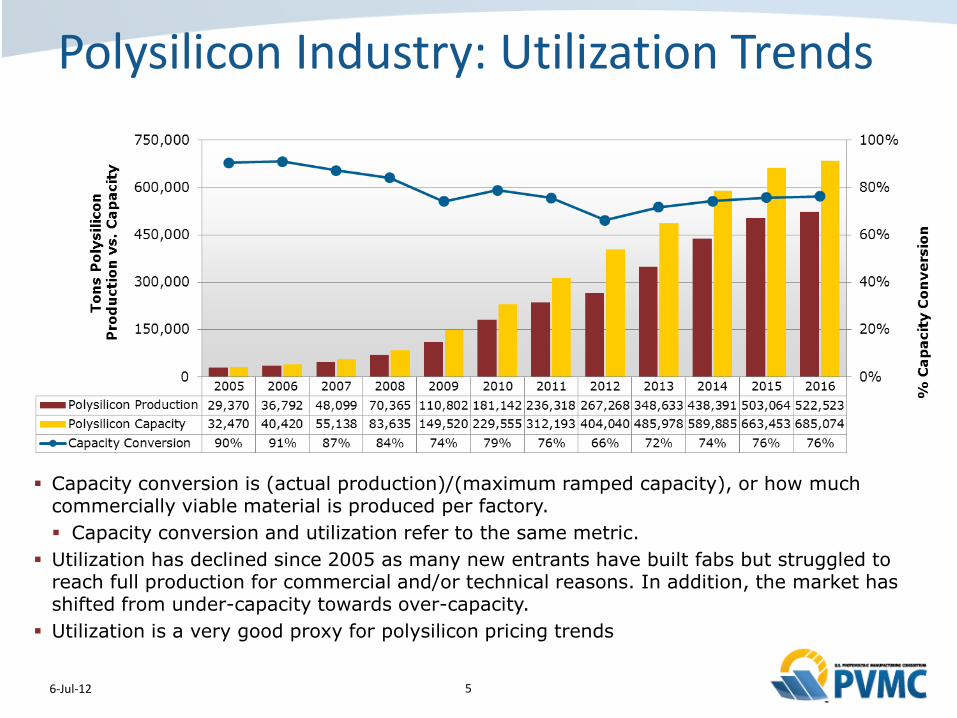

Polysilicon Industry: Utilization Trends

5 6-Jul-12

Capacity conversion is (actual production)/(maximum ramped capacity), or how much commercially viable material is produced per factory.

Capacity conversion and utilization refer to the same metric.

Utilization has declined since 2005 as many new entrants have built fabs but struggled to reach full production for commercial and/or technical reasons. In addition, the market has shifted from under-capacity towards over-capacity.

Utilization is a very good proxy for polysilicon pricing trends

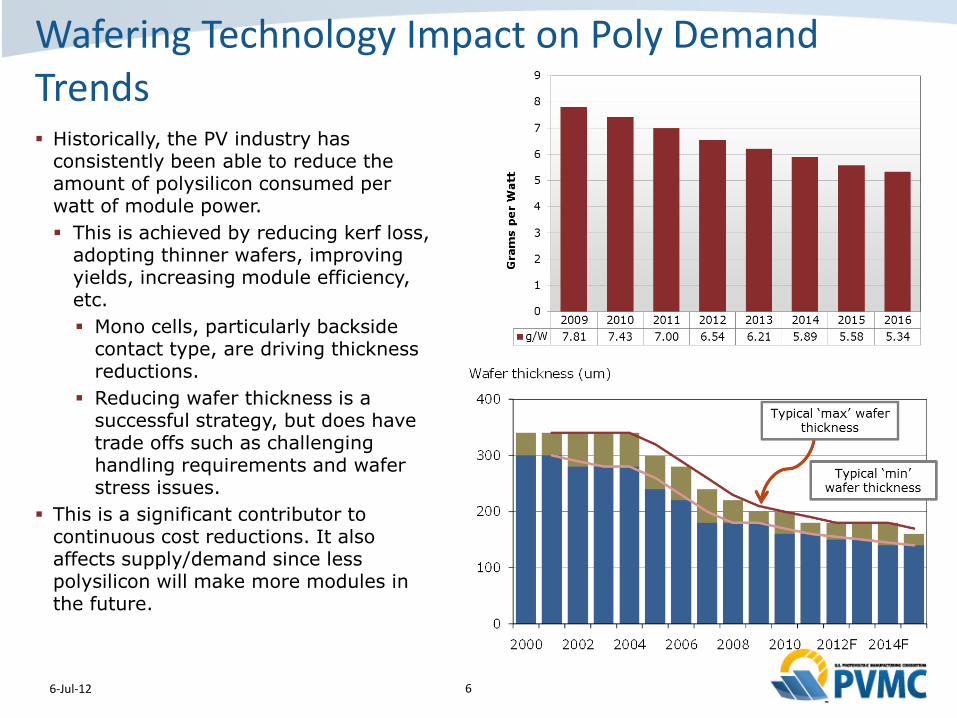

Wafering Technology Impact on Poly Demand Trends

6 6-Jul-12

Historically, the PV industry has consistently been able to reduce the amount of polysilicon consumed per watt of module power.

This is achieved by reducing kerf loss, adopting thinner wafers, improving yields, increasing module efficiency, etc.

Mono cells, particularly backside contact type, are driving thickness reductions.

Reducing wafer thickness is a successful strategy, but does have trade offs such as challenging handling requirements and wafer stress issues.

This is a significant contributor to continuous cost reductions. It also affects supply/demand since less polysilicon will make more modules in the future.

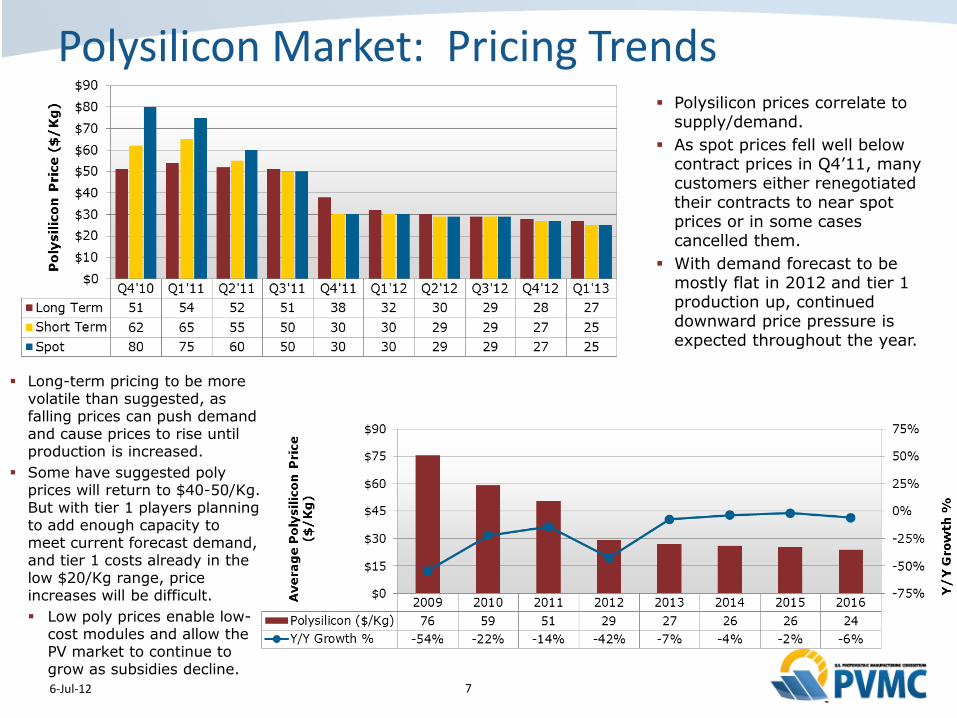

Polysilicon Market: Pricing Trends

7 6-Jul-12

Polysilicon prices correlate to supply/demand.

As spot prices fell well below contract prices in Q4’11, many customers either renegotiated their contracts to near spot prices or in some cases cancelled them.

With demand forecast to be mostly flat in 2012 and tier 1 production up, continued downward price pressure is expected throughout the year.

Long-term pricing to be more volatile than suggested, as falling prices can push demand and cause prices to rise until production is increased.

Some have suggested poly prices will return to $40-50/Kg. But with tier 1 players planning to add enough capacity to meet current forecast demand, and tier 1 costs already in the low $20/Kg range, price increases will be difficult.

Low poly prices enable low-cost modules and allow the PV market to continue to grow as subsidies decline.

PV Wafer Industry: Market Updates

8 6-Jul-12

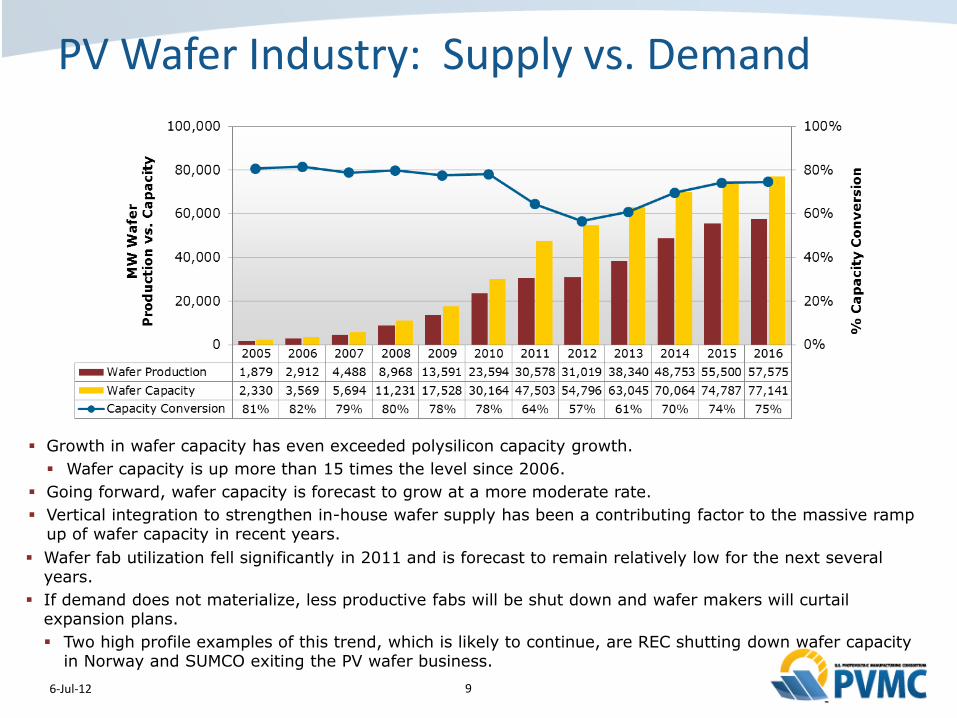

PV Wafer Industry: Supply vs. Demand

9 6-Jul-12

Wafer fab utilization fell significantly in 2011 and is forecast to remain relatively low for the next several years.

If demand does not materialize, less productive fabs will be shut down and wafer makers will curtail expansion plans.

Two high profile examples of this trend, which is likely to continue, are REC shutting down wafer capacity in Norway and SUMCO exiting the PV wafer business.

Growth in wafer capacity has even exceeded polysilicon capacity growth.

Wafer capacity is up more than 15 times the level since 2006.

Going forward, wafer capacity is forecast to grow at a more moderate rate.

Vertical integration to strengthen in-house wafer supply has been a contributing factor to the massive ramp up of wafer capacity in recent years.

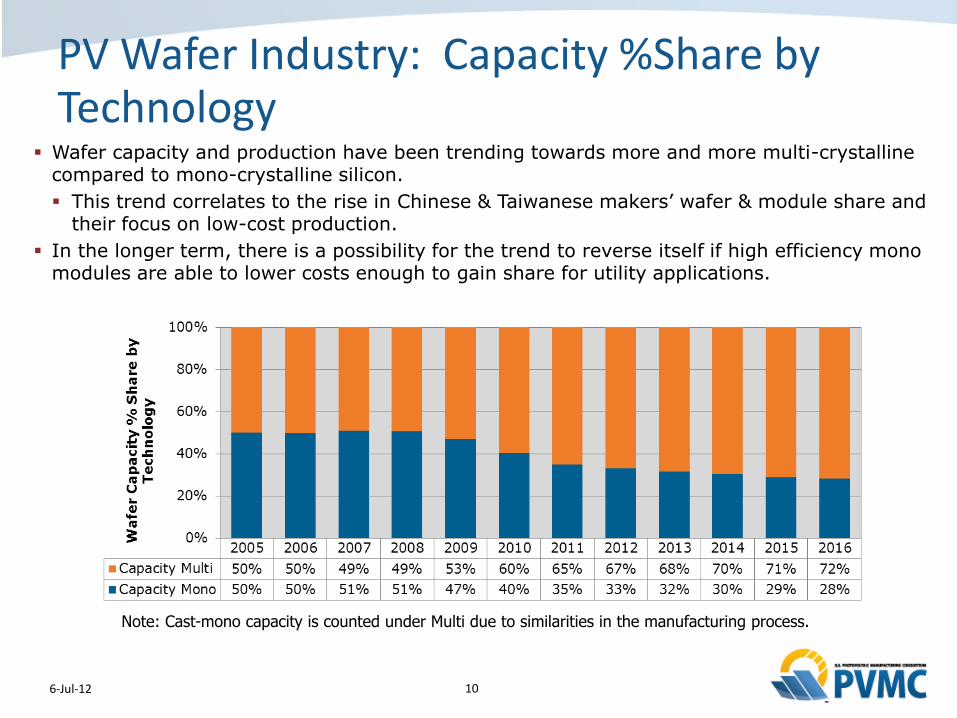

PV Wafer Industry: Capacity %Share by Technology

10 6-Jul-12

Wafer capacity and production have been trending towards more and more multi-crystalline compared to mono-crystalline silicon.

This trend correlates to the rise in Chinese & Taiwanese makers’ wafer & module share and their focus on low-cost production.

In the longer term, there is a possibility for the trend to reverse itself if high efficiency mono modules are able to lower costs enough to gain share for utility applications.

Note: Cast-mono capacity is counted under Multi due to similarities in the manufacturing process.

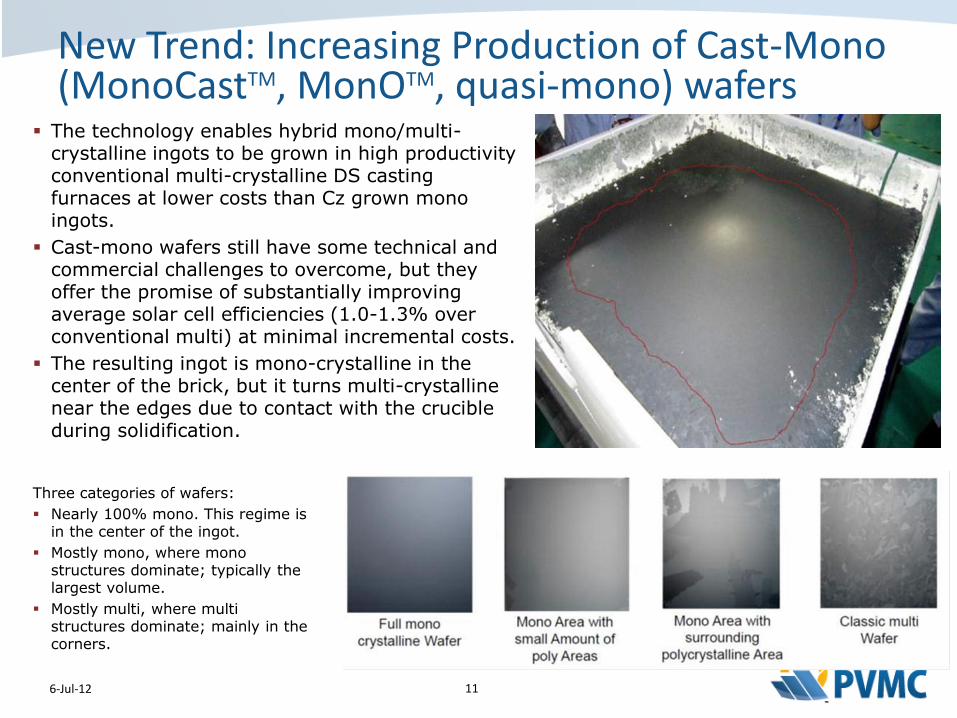

New Trend: Increasing Production of Cast-Mono (MonoCastTM, MonOTM, quasi-mono) wafers

11 6-Jul-12

The technology enables hybrid mono/multi-crystalline ingots to be grown in high productivity conventional multi-crystalline DS casting furnaces at lower costs than Cz grown mono ingots.

Cast-mono wafers still have some technical and commercial challenges to overcome, but they offer the promise of substantially improving average solar cell efficiencies (1.0-1.3% over conventional multi) at minimal incremental costs.

The resulting ingot is mono-crystalline in the center of the brick, but it turns multi-crystalline near the edges due to contact with the crucible during solidification.

Three categories of wafers:

Nearly 100% mono. This regime is in the center of the ingot.

Mostly mono, where mono structures dominate; typically the largest volume.

Mostly multi, where multi structures dominate; mainly in the corners.

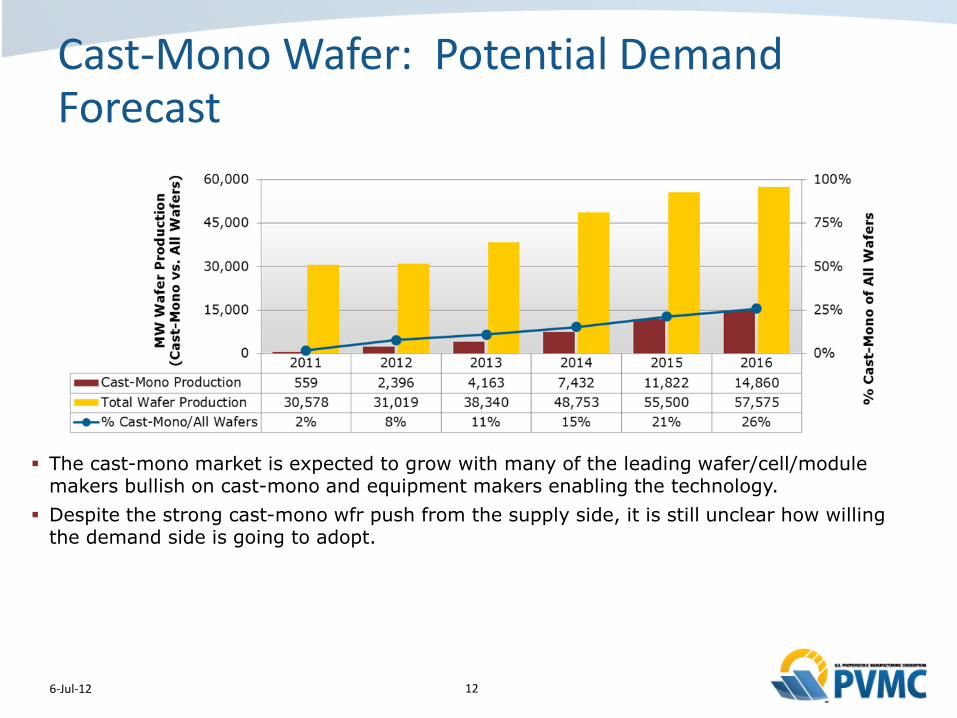

Cast-Mono Wafer: Potential Demand Forecast

12 6-Jul-12

The cast-mono market is expected to grow with many of the leading wafer/cell/module makers bullish on cast-mono and equipment makers enabling the technology.

Despite the strong cast-mono wfr push from the supply side, it is still unclear how willing the demand side is going to adopt.

PV Wafer Industry: Wafer Pricing Trends

13 6-Jul-12

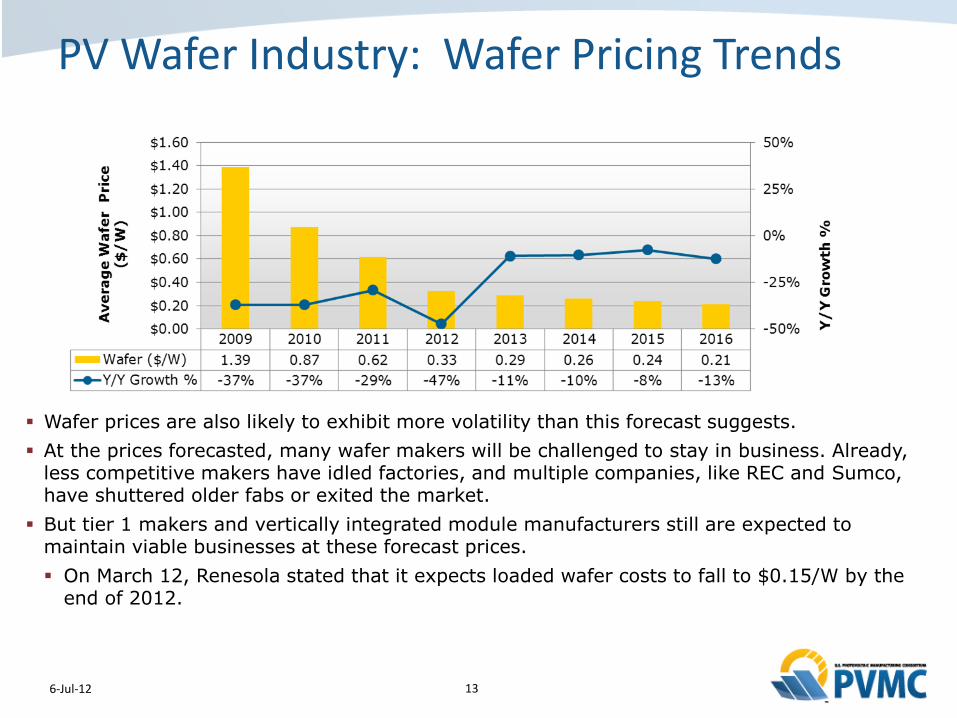

Wafer prices are also likely to exhibit more volatility than this forecast suggests.

At the prices forecasted, many wafer makers will be challenged to stay in business. Already, less competitive makers have idled factories, and multiple companies, like REC and Sumco, have shuttered older fabs or exited the market.

But tier 1 makers and vertically integrated module manufacturers still are expected to maintain viable businesses at these forecast prices.

On March 12, Renesola stated that it expects loaded wafer costs to fall to $0.15/W by the end of 2012.

Short Term Industry Challenges

• Continue innovation investments (R&D) in polysilicon and wafering in current “unhealthy” market environment

14 6-Jul-12

• Maintain the positive effects of ~$20/kg polysilicon prices on overall PV solar market demand

Long Term Industry Challenges

• More balanced supply/demand polysilicon and wafer market which leads to pricing stability and long term profitability.

• Maintain PV module cost reductions as polysilicon and wafer prices (costs) begin leveling off at minimums which are sustainable

Summary & Conclusions

• Very large increase in polysilicon and wafer capacity since 2010 has led to industry level under utilization

• Extreme under-utilization (over capacity) has caused polysilicon pricing to drop to the ~$20/Kg level and expected to stay at this level

• Polysilicon contract and spot pricing nearly equivalent causing major shift away from contracts to spot market buying/selling.

• Cast-mono ingot/wafering technology will possibly push wafer pricing even lower (due to lower cast-mono production cost)

• All indications suggest lower polysilicon and wafer pricing in the future which will continue to lower overall PV module costs (but not the same % declines seen in recent years)

15 6-Jul-12

Acknowledgement

• All market data and graphs in this presentation are provided by

NPD Solarbuzz

16 6-Jul-12

BACKUP

17 6-Jul-12

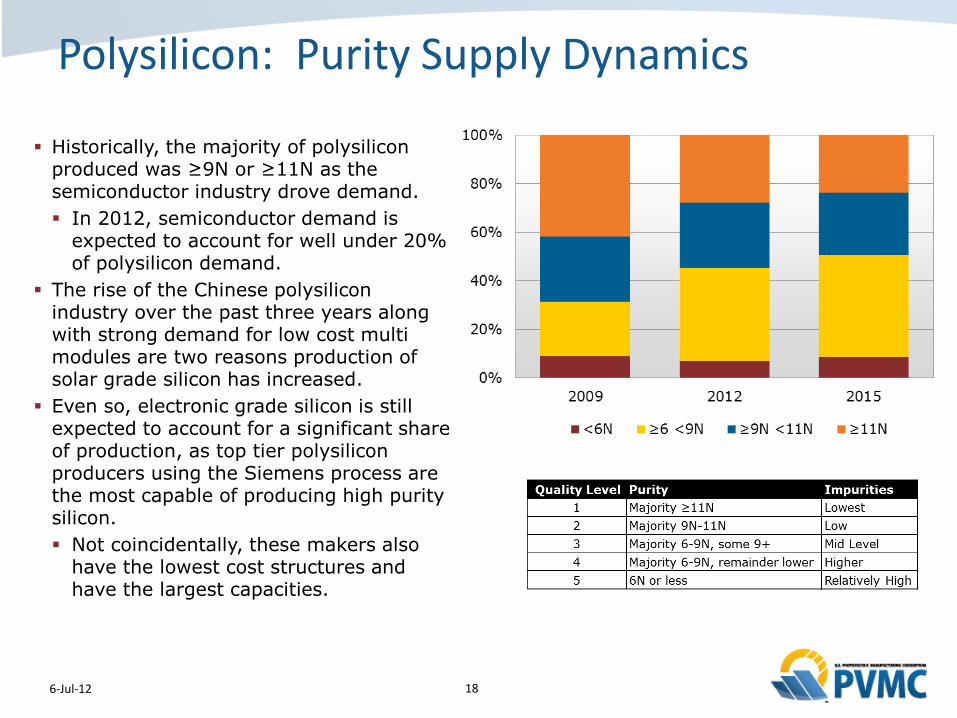

Polysilicon: Purity Supply Dynamics

18 6-Jul-12

Historically, the majority of polysilicon produced was ≥9N or ≥11N as the semiconductor industry drove demand.

In 2012, semiconductor demand is expected to account for well under 20% of polysilicon demand.

The rise of the Chinese polysilicon industry over the past three years along with strong demand for low cost multi modules are two reasons production of solar grade silicon has increased.

Even so, electronic grade silicon is still expected to account for a significant share of production, as top tier polysilicon producers using the Siemens process are the most capable of producing high purity silicon.

Not coincidentally, these makers also have the lowest cost structures and have the largest capacities.

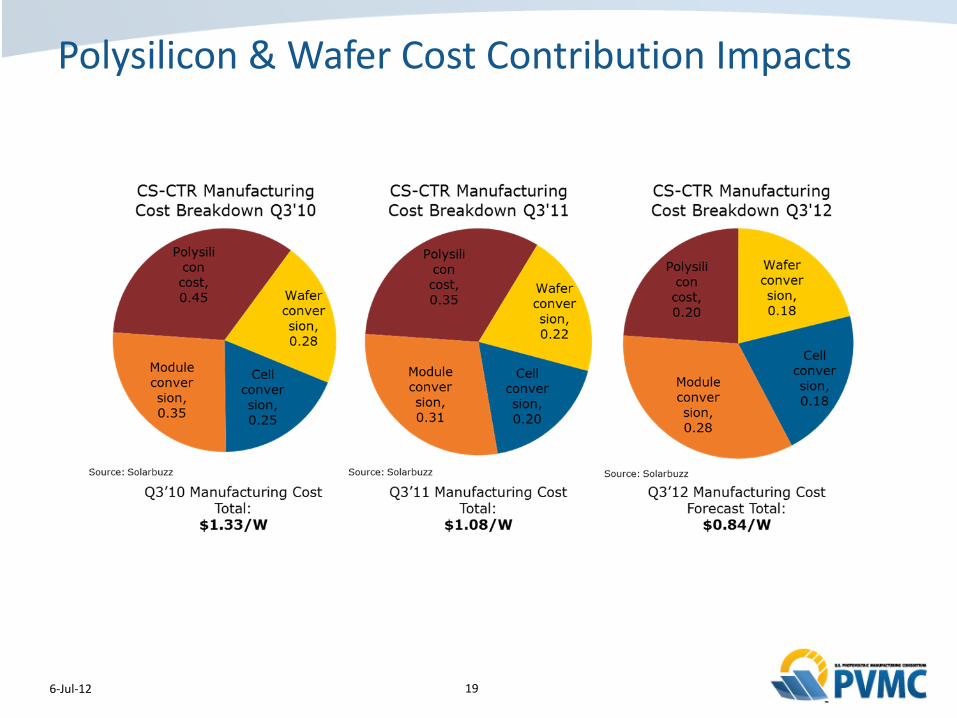

Polysilicon & Wafer Cost Contribution Impacts

19 6-Jul-12