Prepaid card industry survey -...

28

Prepaid card industry survey Edgar, Dunn & Company – EFMA Survey September 2008

-

Upload

trinhkhanh -

Category

Documents

-

view

216 -

download

0

Transcript of Prepaid card industry survey -...

Prepaid card industry surveyEdgar, Dunn & Company – EFMA Survey

September 2008

1

Why do prepaid cards matter?

“Visa Inc. plans to invest in the development of prepaid cards, funds transfers, Internet and mobile-payment applications,

Joseph W. Saunders, the card brand's CEO, told attendees at last week's UBS Global Financial Services conference.

"We believe [prepaid] is the next debit-sized opportunity for Visa," said Saunders.

"We're going to take products that are in the market today in the United States, like our general-purpose reloadable cards,

our payroll cards, our gift cards - and we are going to take them around the world…”

“Visa Inc. plans to invest in the development of prepaid cards, funds transfers, Internet and mobile-payment applications,

Joseph W. Saunders, the card brand's CEO, told attendees at last week's UBS Global Financial Services conference.

"We believe [prepaid] is the next debit-sized opportunity for Visa," said Saunders.

"We're going to take products that are in the market today in the United States, like our general-purpose reloadable cards,

our payroll cards, our gift cards - and we are going to take them around the world…”

Source: Cardline Global, May 21, 2008

2

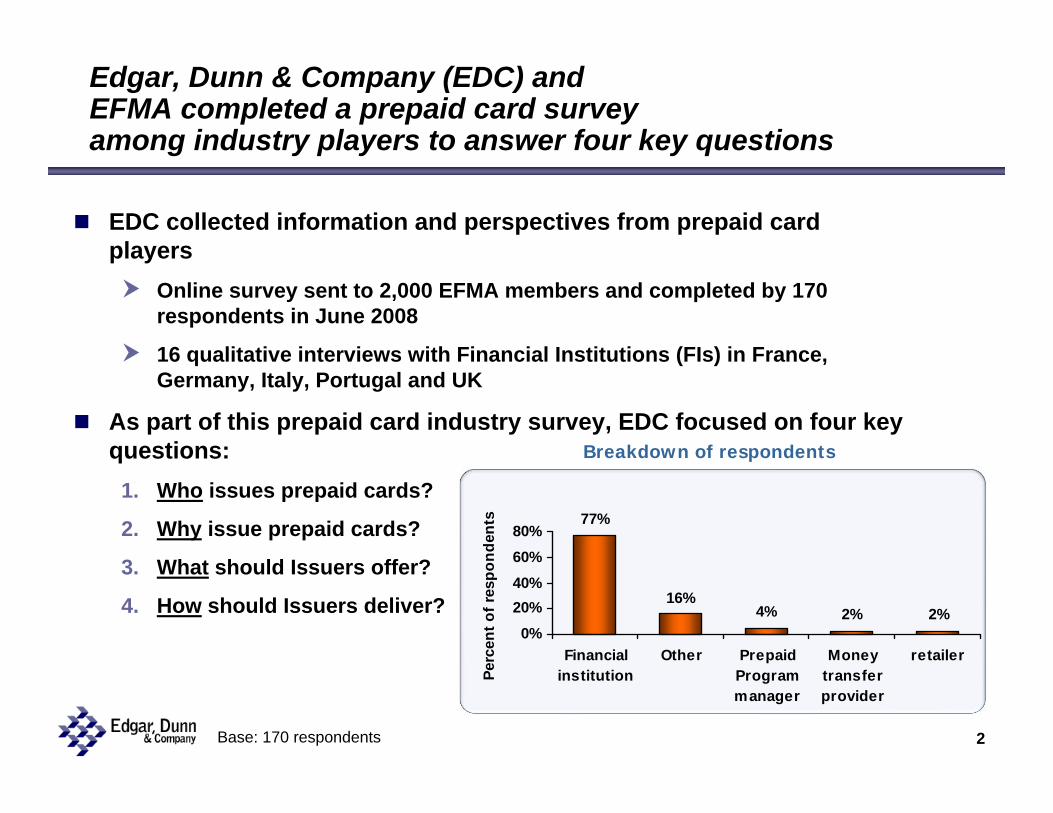

Edgar, Dunn & Company (EDC) and EFMA completed a prepaid card survey among industry players to answer four key questions

EDC collected information and perspectives from prepaid card players

Online survey sent to 2,000 EFMA members and completed by 170 respondents in June 2008

16 qualitative interviews with Financial Institutions (FIs) in France, Germany, Italy, Portugal and UK

As part of this prepaid card industry survey, EDC focused on four key questions:

1. Who issues prepaid cards?

2. Why issue prepaid cards?

3. What should Issuers offer?

4. How should Issuers deliver?

77%

16%4% 2% 2%

0%20%40%60%80%

Financialinstitution

Other PrepaidProgrammanager

Moneytransferprovider

retailer

Perc

ent o

f res

pond

ents

Base: 170 respondents

Breakdown of respondents

3

4

Key finding 1: Nearly half of respondents already issue prepaid cards, and another quarter will issue within the next 12 months

Survey question: Do you issue prepaid cards?

Already issue Do not issue nowWill issue Will not issue

49% 24%

Base: 170 respondents

Participants who plan to Issue in the next few months are finalising theirMarketing Plans and Customer Segmentation models

Distribution channels

Customer Due Diligence processes

Business Case

5

Key finding 1: … spanning over 34 countries

Breakdown of respondents byprimary country of Issuance

Poland 5%

Austria 6%

France 7%

Germany 8%

Italy 10%

United Kingdom 14%

TOP SIX TOP SIX COUNTRIESCOUNTRIES

Portugal

Norway

Morocco

Iceland

Greece

Belgium

Turkey

Spain

Netherlands

Croatia

NEXT 10 NEXT 10 COUNTRIESCOUNTRIES

UkraineTunisiaRussia

Israel

Bangladesh

United States

SyriaSwitzerland

SwedenSri Lanka

OmanLebanon

Latvia

DenmarkCyprus

China/Hong Kong

Andorra

REMAININGREMAININGCOUNTRIESCOUNTRIES

Group 1 50%Group 1 50% Group 2 28%Group 2 28% Group 3 22%Group 3 22%

Base: 80 respondents

66%

25%

8%

0%

20%

40%

60%

80%

100%

European Union EEMEA Rest of the World

Perc

ent o

f res

pond

ents

In what regions do respondents issue prepaid cards?

6

Key finding 2: Unlike debit / credit cards, there is a small (and fast growing) number of non-FIs that are issuing prepaid cards

Breakdown of type of prepaid card issuers

80%

5%11%

3%0%

20%

40%

60%

80%

100%

FinancialInstitution

Other PrepaidProgrammanager

Moneytransferprovider

Perc

ent o

f res

pond

ents

Base: 77 respondents

Non-FI Issuers have become more prevalent due to BIN sponsorship andthe introduction of the Electronic Money Directive in 2001

Traditional Money Transfer Providers seeking to remit money through additional product channels

Prepaid programme managers seeking to provide specific Financial Services to a niche customer segment

7

Key finding 2: … leveraging BIN sponsorship or Electronic Money Licenses to ensure appropriate regulatory and network coverage

Do you hold your own issuing license?

26%

5%

69%

Banking licenseUsing BIN sponsorElectronic Money License

Base: 80 respondents

Do you hold your own scheme license?

37%

26%37%

MasterCardVisaBIN sponsor

8

9

Key finding 3: Most issuers decided to issue prepaid cards due to long-term / strategic reasons (recruitment of new high-potential customers, differentiation strategy)

What are the most important business objectivesfor your prepaid card issuing business?

27%

42%

66%

69%

0% 20% 40% 60% 80%

Cost savings

Differentiate

Incrementalrevenues

Acquire newcustomers

Base: 120 respondents

10

Key finding 3: … with a specific focus on first- time users with a view to provide additional products and services in the future

Who are you primarily targeting with prepaid cards?

11%15%

45%

13%15%

0%

10%

20%

30%

40%

50%

First-time users Customers ofother banks

Own bankcustomers with

no card

Own bankcustomers with

debit / creditcards

OtherPerc

ent o

f res

pond

ents

Base: 120 respondents

11

Key finding 3: … and as part of the “war on cash”

What will be the main impact of prepaid cards?

10% 6%16%

36%

18% 22%

40%

18%

16%

44%

25%

11%

51%

25% 12%

33%

0%

20%

40%

60%

80%

100%

Replace Cash ReplaceCheques

Replace Cards Generate newtransactions

4 Less impact

3

2

1 Most impact

Porc

ent o

f res

pond

ents

Base: 120 respondents

12

Key finding 4: The current prepaid card market is small with relatively low levels of portfolio activity

Estimate of prepaid card penetration* in 2008

70%

16%5% 9% 9%

0%

20%

40%

60%

80%

100%

<10%` 10-20% 20-50% 50+% Did notknow

Customer Penetration

Perc

ent o

f Res

pond

ents

*Defined as % of consumers using at least one prepaid card^ Defined as used for one transaction in the last 3 months

Significant variance in estimates of market sizing, for instance:Large European market: estimates from 0.15m to 1m network-branded prepaid cards

19%13% 17% 16%

29%

0%

20%

40%

60%

80%

100%

<25% 25-50% 50-75% 75-100% Did notknow

Portfolio Activity Rate

Perc

ent o

f Res

pond

ents

Estimate of % of Portfolio with Active^ cards in 2008

Base: 80 respondents

13

Key finding 4: .. however >10% levels of annual growth are expected from current / future Issuers

Projected annual growth rate over next 2-3 years?

11% 11%

21%

38%

19%

0%

10%

20%

30%

40%

<10%` 10-20% 20-50% 50+% Did notknow

Annual growth

perc

ent o

f res

pond

ents

Base: 120 respondents

14

Key finding 4: … especially in large Western European countries

Projected annual growth rate over next 2-3 years?

Netherlands

Norway

SwedenIcelandAustria

PortugalGreeceGermany

FinlandDenmarkItaly

BelgiumFranceUnited Kingdom

GROWTH RATES OF GROWTH RATES OF LESS THAN 10%LESS THAN 10%

GROWTH RATES OFGROWTH RATES OF10% TO 20%10% TO 20%

GROWTH RATE OFGROWTH RATE OF20% TO 50%20% TO 50%

Base: 120 respondents

15

16

Key finding 5: Respondents expect gift cards to remain the most successful prepaid card application in terms of volume

What will be the most successful prepaid card applications in the next 2-3 years?

Gift Cards, 20%

Youth/teens, 18%

Government cards, benefits, insurance, 10%

Online, 10%

Consumer travel cards,

10%

Unbanked, 7% Payroll, 6%

Remittance, 6%

Transport infrastructure and low value

payments, 13%

Base: 155 respondents

17

Key finding 5: … with network branded cards focused on youth, remittance, transit and government/corporate segments to drive growth

What will be the most successful prepaid card applications in the next 2-3 years?

TransportInfrastructure

Online

Payroll

Government Cards

Government Cards

Youth

Payroll

VOLUME 3VOLUME 3RDRD

Corporate T&EYouthGift CardsSpain

MobileTransport InfrastructureYouthTurkey

RemittanceYouthGift CardsFrance

Online / LoyaltyConsumer Travel CardsGift CardsAustria

Remittance / Online

Consumer TravelCardsGift CardsGermany

YouthGovernment CardsGift CardsItaly

RemittanceGovernment CardsGift CardsUK

GROWTH 1GROWTH 1STSTVOLUME 2VOLUME 2NDNDVOLUME 1VOLUME 1STSTCOUNTRYCOUNTRY

Focus of Network Branded Propositions

Base: 155 respondents, EDC Analysis

18

Key finding 6: Successful products will not be “one size fits all”

19

Key finding 6: Successful products will not be “one size fits all” but products focused on specific segments with the relevant customer experience, services and pricing

All Purpose Youth Transit Online Travel Remittance Payroll Government

Segment-specificservices and

customer experience

Long Tail80%

ILLUSTRATIVE EXAMPLES

Prepaid card market: long (and “thick”) tail

Volu

me

Basic / generic needs Complex / specific needs

20%

20

21

Key finding 7: Most issuers are still currently using bank-centric sales and servicing channels

What are your main consumer focused sales channels?

21%Call centres34%Merchants

9%Post Office6%ATM

46%Online64%Bank branchesIMPORTANCE OF CHANNELIMPORTANCE OF CHANNELDISTRIBUTION/ SALES CHANNELDISTRIBUTION/ SALES CHANNEL

What are your main re-load channels?

ATM, 18%

Merchants, 11%

Bank Branches,

25%

Mobile, 11%

Online, 30%

Post Office, 5%

Base: 80 respondents

22

Key finding 7: … and are split equally between insourcing and outsourcing

Will you process internallyor outsource over next 2-3 years?

41%

42%

17%

In-houseOutsourcedDo not know

Base: 120 respondents

23

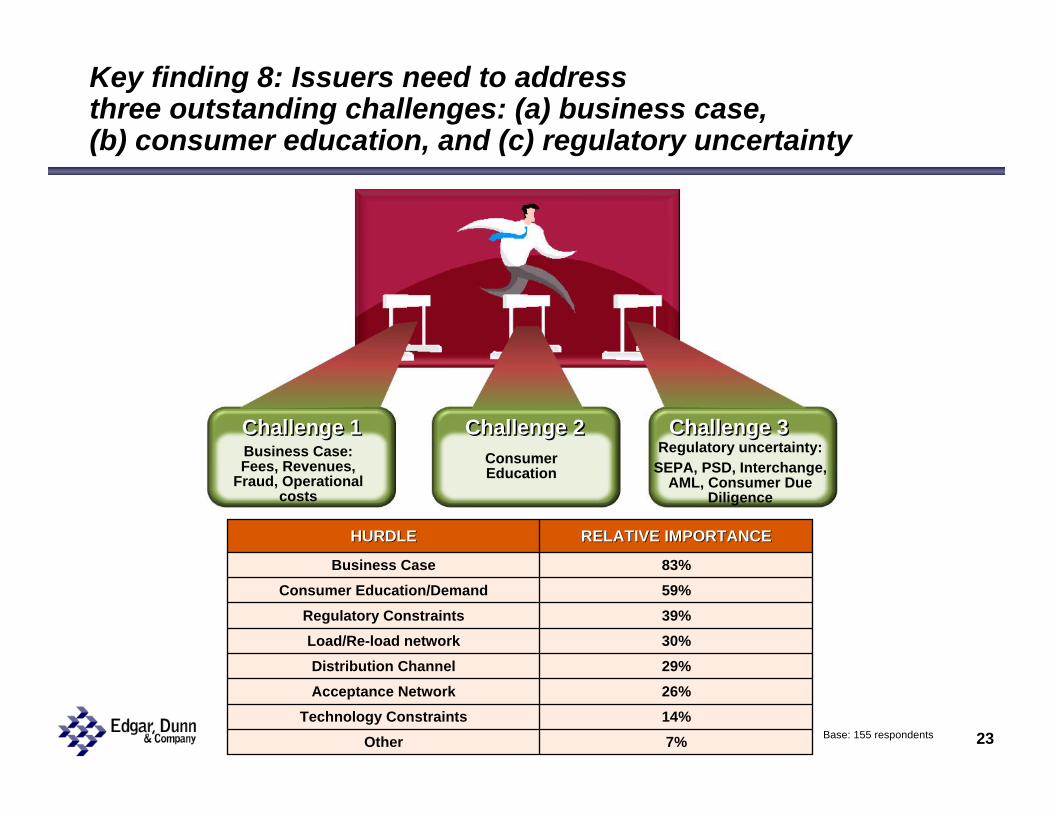

Key finding 8: Issuers need to address three outstanding challenges: (a) business case, (b) consumer education, and (c) regulatory uncertainty

Business Case:Fees, Revenues,

Fraud, Operational costs

Challenge 1Challenge 1Consumer Education

Challenge 2Challenge 2Regulatory uncertainty:

SEPA, PSD, Interchange, AML, Consumer Due

Diligence

Challenge 3Challenge 3

26%Acceptance Network

7%Other14%Technology Constraints

30%Load/Re-load network29%Distribution Channel

39%Regulatory Constraints59%Consumer Education/Demand83%Business Case

RELATIVE IMPORTANCERELATIVE IMPORTANCEHURDLEHURDLE

Base: 155 respondents

24

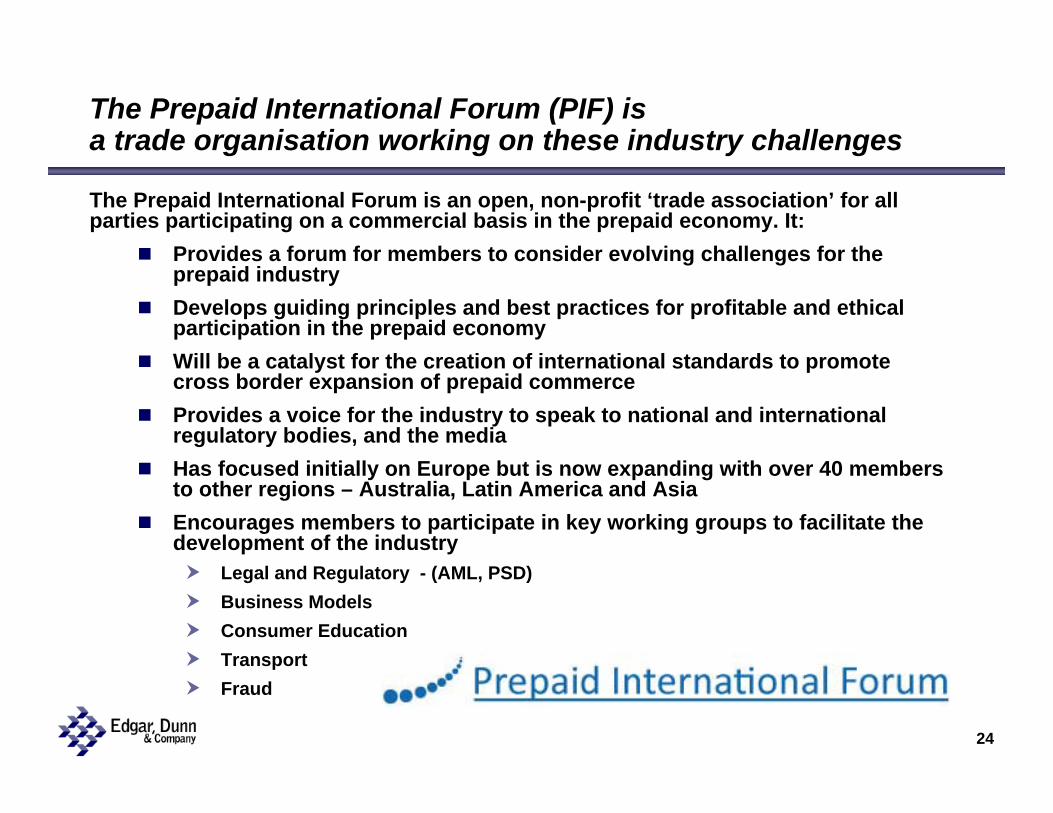

The Prepaid International Forum (PIF) is a trade organisation working on these industry challenges

The Prepaid International Forum is an open, non-profit ‘trade association’ for all parties participating on a commercial basis in the prepaid economy. It:

Provides a forum for members to consider evolving challenges for the prepaid industryDevelops guiding principles and best practices for profitable and ethical participation in the prepaid economyWill be a catalyst for the creation of international standards to promote cross border expansion of prepaid commerceProvides a voice for the industry to speak to national and international regulatory bodies, and the mediaHas focused initially on Europe but is now expanding with over 40 members to other regions – Australia, Latin America and AsiaEncourages members to participate in key working groups to facilitate the development of the industry

Legal and Regulatory - (AML, PSD)Business Models Consumer EducationTransportFraud

25

26

Based on the expert interviews and marketobservations, EDC highlighted four conclusions

1. Prepaid cards will be part of most FIs’ card offering for long-term / strategic reasons

To acquire new customers with long-term potential (e.g., youth segment, first-time users)As a defensive play

2. “Winning” in the prepaid card market will require deep marketing skills

Identifying specific segments / use casesUse cases of purchases or money movements that are not adequately serviced by existing forms of payment

Defining the appropriate customer experience, product features, services and pricing

How convenient compared to cash / cheques / other substitutes?Most likely different from the US experience

27

Based on the expert interviews and marketobservations, EDC highlighted four conclusions

3. “Winning” will also require partnership / channel management skillsCross-selling via internal divisions

Retail networkWholesale banking, etc.

Using external distribution channelsRetailers

4. There are significant untapped product development opportunitiesrelated to creating “new markets”. Examples include:

Developing “hybrid” products by linking prepaid cards with other banking or non-banking products

Savings accounts? Investment accounts? Insurance coverage?Mobile phones?

Developing partnerships with third parties such as large retailers