The Australian economy in 2009 -...

23

The Australian economy in 2009 Presentation to ANZ Management Board Melbourne 19 th January 2009 Saul Eslake Chief Economist, ANZ

Transcript of The Australian economy in 2009 -...

The Australian economy in 2009

Presentation to ANZ Management Board

Melbourne19th January 2009

Saul EslakeChief Economist, ANZ

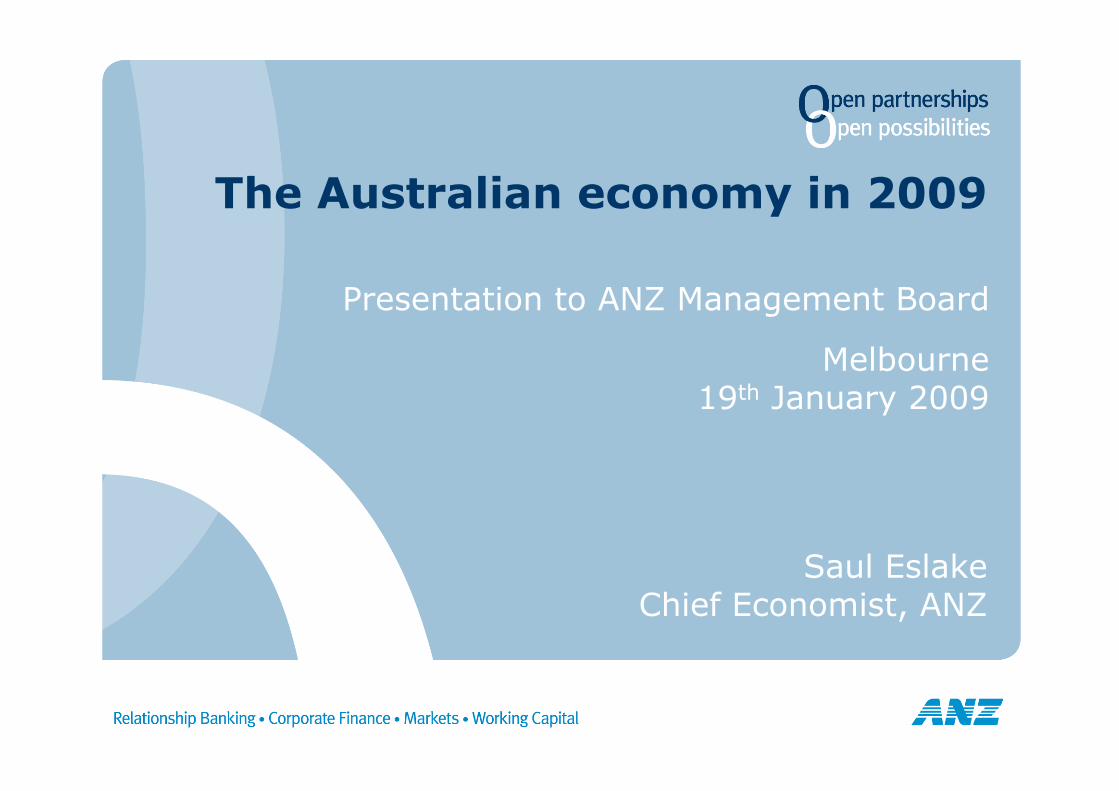

2The global economy turned down sharply in the final quarter of 2008

Industrial production

North America

Europe

Sources: National statistical agencies; ANZ.

Other Asia

Japan

-8-6-4-20246

01 02 03 04 05 06 07 08

% change from year earlier

US

Canada

-8-6-4-20246

01 02 03 04 05 06 07 08

% change from year earlier Euro area

UK

-15

-10

-5

0

5

10

01 02 03 04 05 06 07 08

% change from year earlier

-10-505

10152025

01 02 03 04 05 06 07 08

% change from year earlierChina

Other East Asia

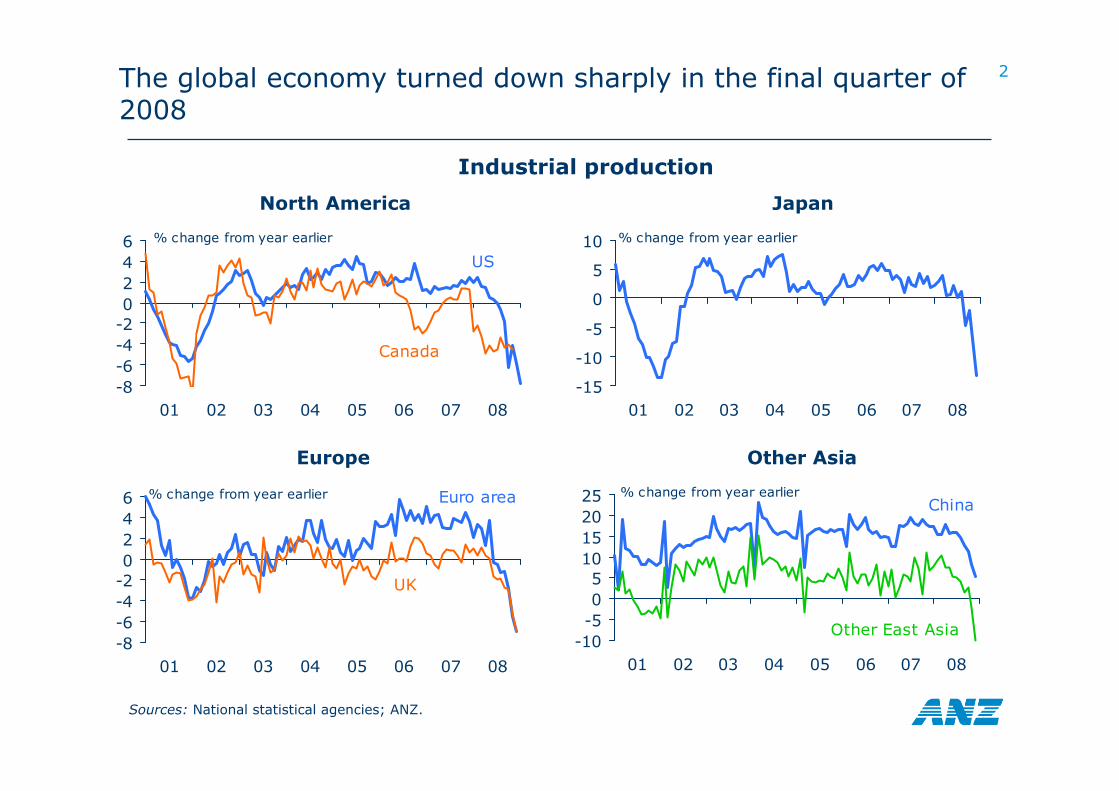

3International trade declined precipitously at the end of 2008, especially in the Pacific region

Merchandise exports

United States

Euro area

Note: Data for Japan in yen; for Euro area in euros; for US and Asia in US$.Sources: National statistical agencies; ANZ.

Other Asia

Japan

-20

-10

0

10

20

30

01 02 03 04 05 06 07 08

% change from year earlier

-30-20

-100

10

2030

01 02 03 04 05 06 07 08

% change from year earlier

-20-10

01020304050

01 02 03 04 05 06 07 08

% change from year earlier(3-mth mvg avge)

China

Other East Asia-10-505

10152025

01 02 03 04 05 06 07 08

% change from year earlier(3-mth mvg avge)

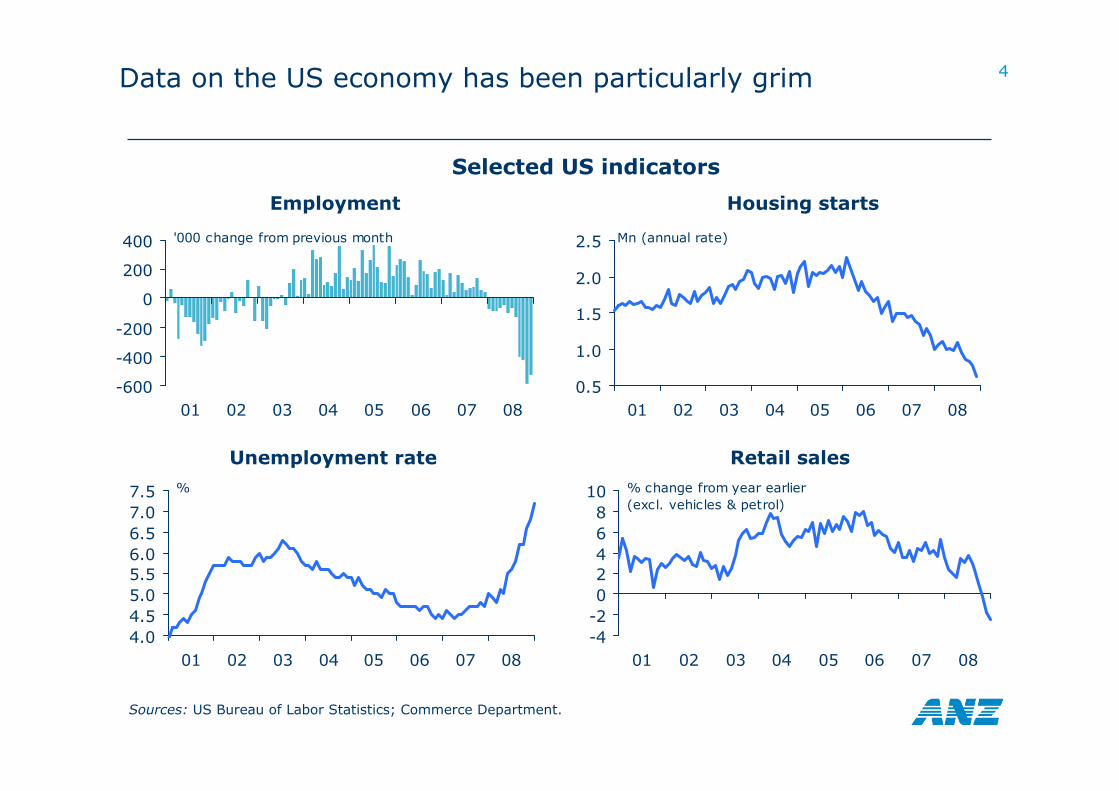

4Data on the US economy has been particularly grim

Selected US indicators

Employment

Unemployment rate

Sources: US Bureau of Labor Statistics; Commerce Department.

Housing starts

-600

-400

-200

0

200

400

01 02 03 04 05 06 07 08

'000 change from previous month

0.5

1.0

1.5

2.0

2.5

01 02 03 04 05 06 07 08

Mn (annual rate)

4.04.55.05.56.06.57.07.5

01 02 03 04 05 06 07 08

%

Retail sales

-4-202468

10

01 02 03 04 05 06 07 08

% change from year earlier(excl. vehicles & petrol)

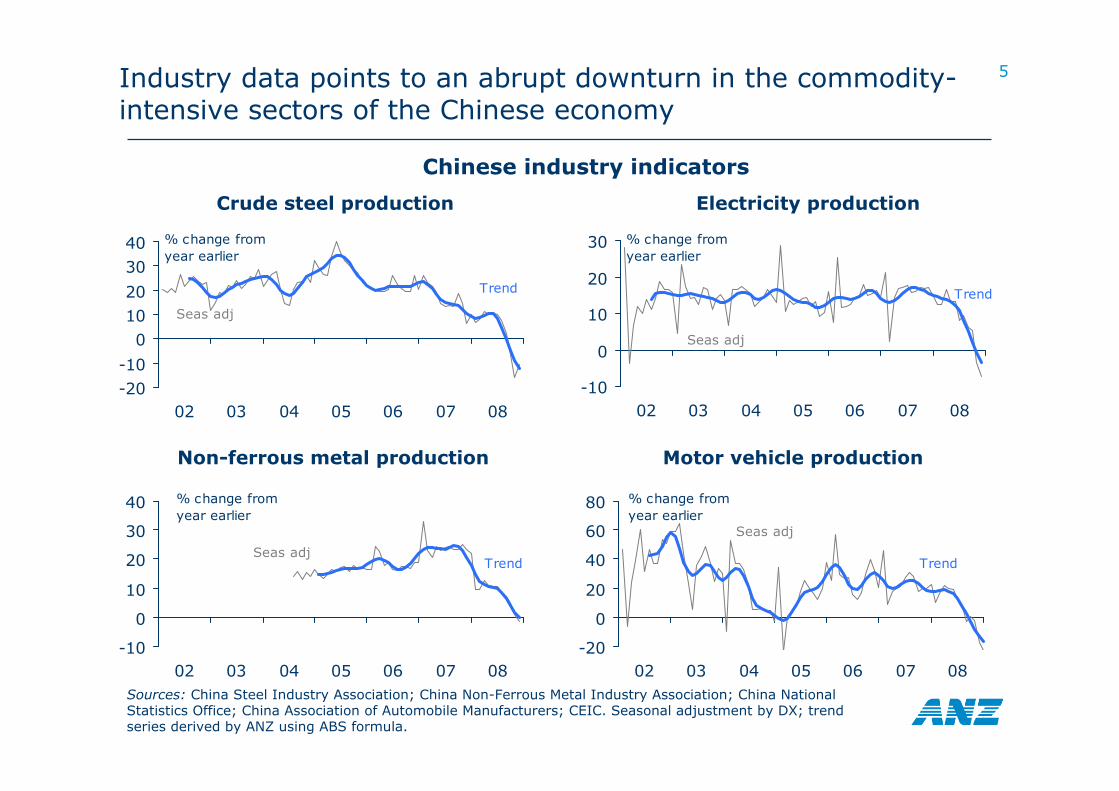

5Industry data points to an abrupt downturn in the commodity-intensive sectors of the Chinese economy

Chinese industry indicators

Crude steel production

Non-ferrous metal production

Sources: China Steel Industry Association; China Non-Ferrous Metal Industry Association; China National Statistics Office; China Association of Automobile Manufacturers; CEIC. Seasonal adjustment by DX; trend series derived by ANZ using ABS formula.

-20-10

01020

3040

02 03 04 05 06 07 08

% change from year earlier

Seas adj

Trend

-10

0

10

20

30

40

02 03 04 05 06 07 08

% change fromyear earlier

Seas adjTrend

Electricity production

-10

0

10

20

30

02 03 04 05 06 07 08

% change from year earlier

Seas adj

Trend

Motor vehicle production

-20

0

20

40

60

80

02 03 04 05 06 07 08

% change fromyear earlier

Seas adj

Trend

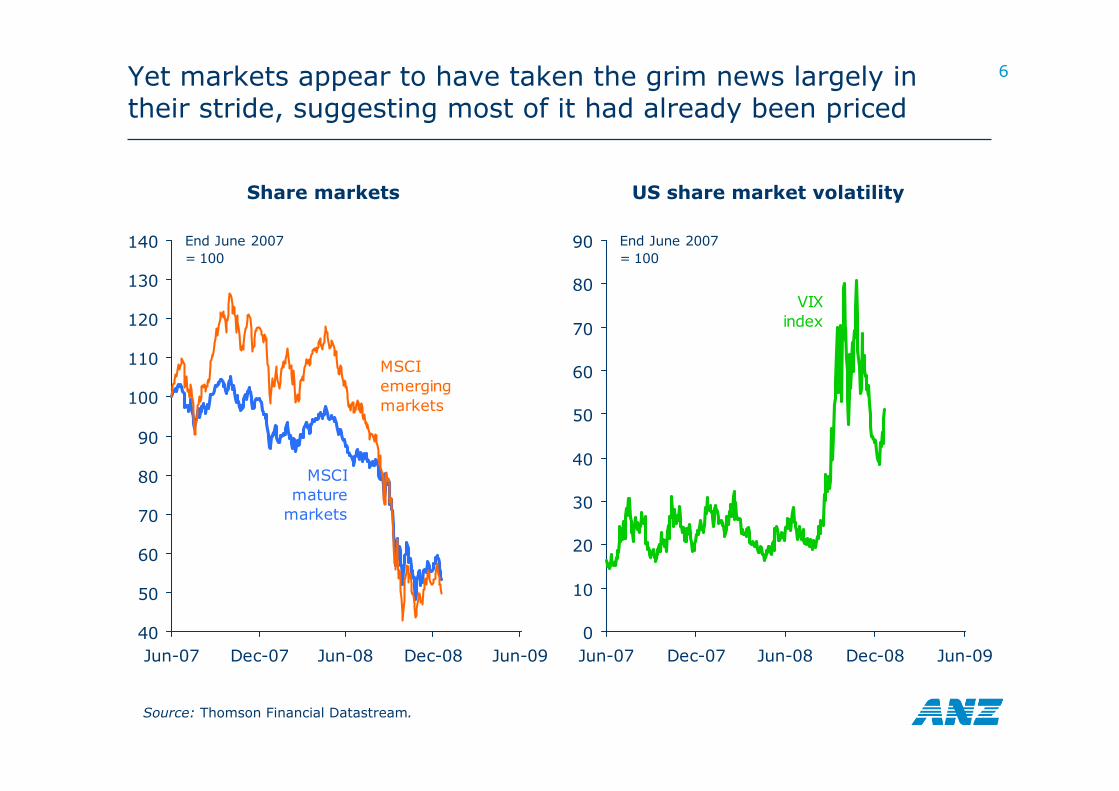

6Yet markets appear to have taken the grim news largely in their stride, suggesting most of it had already been priced

Source: Thomson Financial Datastream.

40

50

60

70

80

90

100

110

120

130

140

Jun-07 Dec-07 Jun-08 Dec-08 Jun-09

End June 2007= 100

MSCIemergingmarkets

MSCImature

markets

Share markets

0

10

20

30

40

50

60

70

80

90

Jun-07 Dec-07 Jun-08 Dec-08 Jun-09

End June 2007= 100

VIXindex

US share market volatility

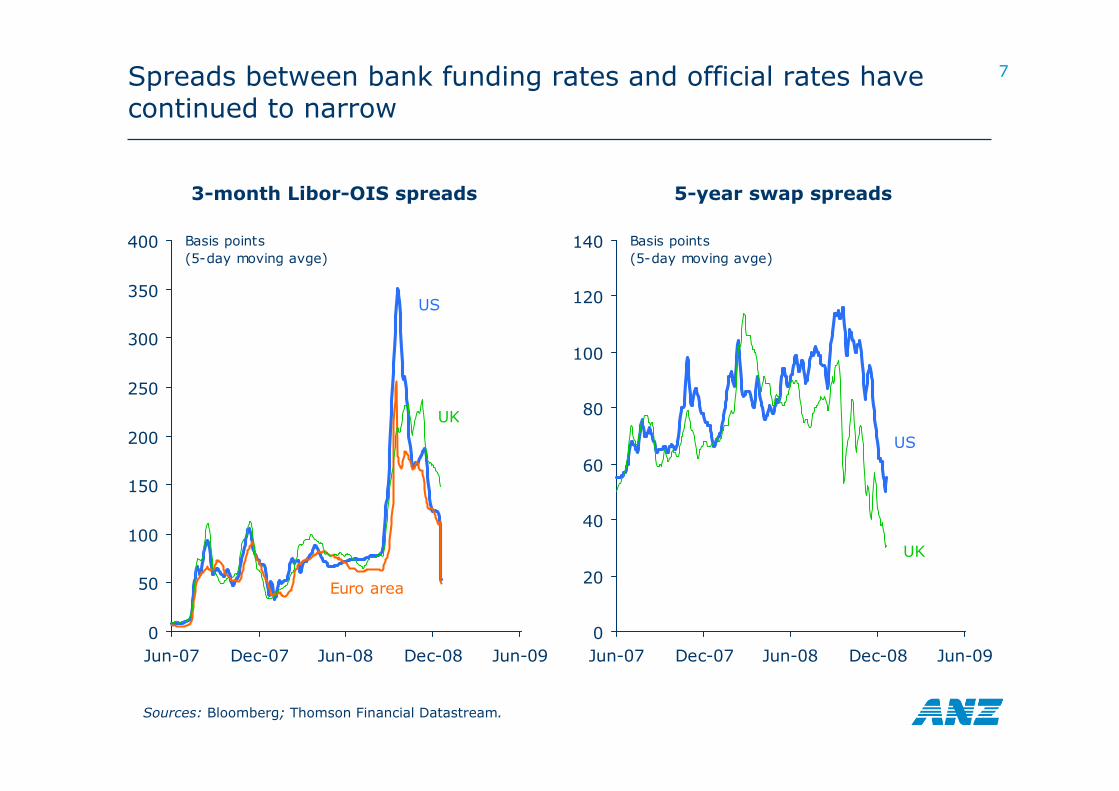

7Spreads between bank funding rates and official rates have continued to narrow

Sources: Bloomberg; Thomson Financial Datastream.

0

50

100

150

200

250

300

350

400

Jun-07 Dec-07 Jun-08 Dec-08 Jun-09

Basis points(5-day moving avge)

Euro area

US

UK

3-month Libor-OIS spreads 5-year swap spreads

0

20

40

60

80

100

120

140

Jun-07 Dec-07 Jun-08 Dec-08 Jun-09

Basis points(5-day moving avge)

US

UK

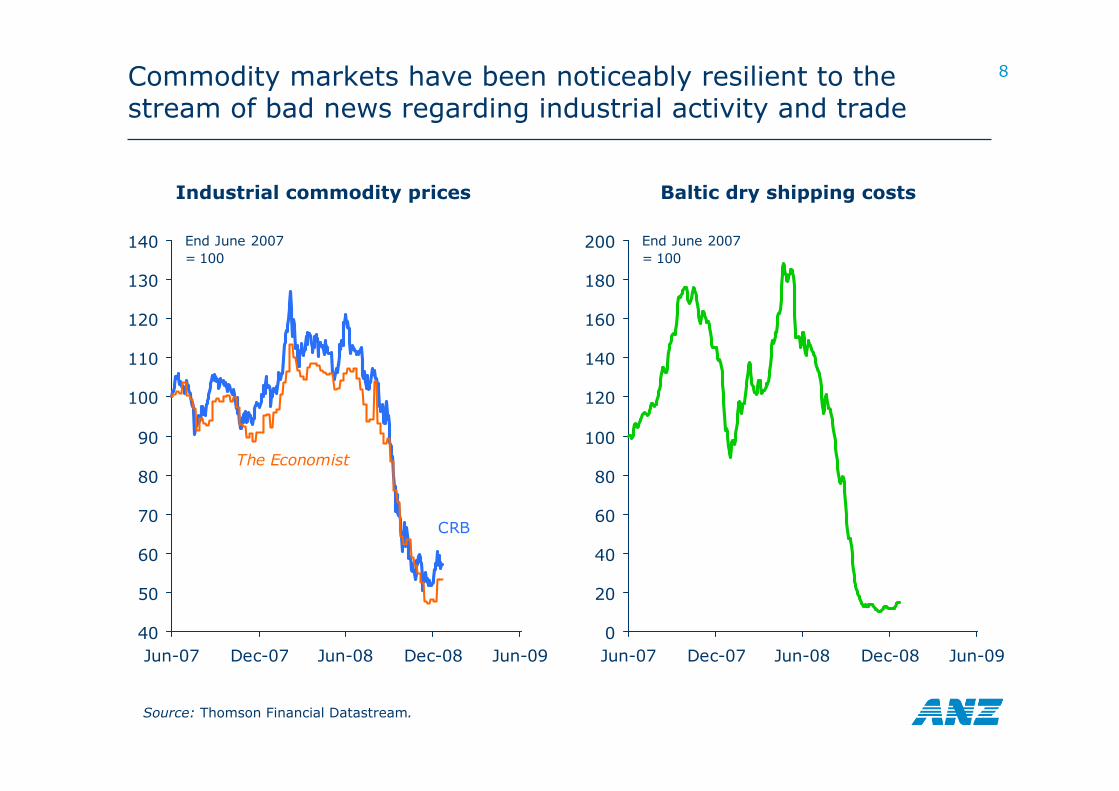

8Commodity markets have been noticeably resilient to the stream of bad news regarding industrial activity and trade

Source: Thomson Financial Datastream.

40

50

60

70

80

90

100

110

120

130

140

Jun-07 Dec-07 Jun-08 Dec-08 Jun-09

End June 2007= 100

The Economist

CRB

Industrial commodity prices Baltic dry shipping costs

0

20

40

60

80

100

120

140

160

180

200

Jun-07 Dec-07 Jun-08 Dec-08 Jun-09

End June 2007= 100

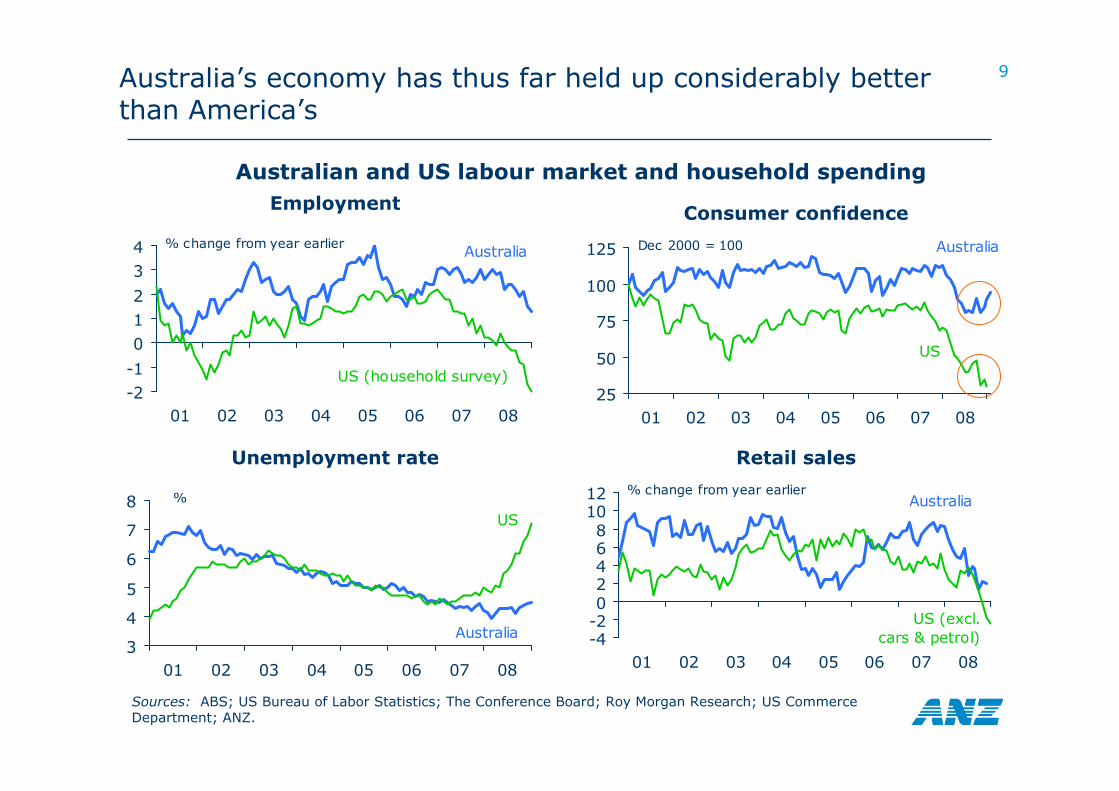

9Australia’s economy has thus far held up considerably better than America’s

Australian and US labour market and household spendingEmployment

Sources: ABS; US Bureau of Labor Statistics; The Conference Board; Roy Morgan Research; US Commerce Department; ANZ.

-2-1

012

34

01 02 03 04 05 06 07 08

% change from year earlier

US (household survey)

Australia

Retail sales

-4-202468

1012

01 02 03 04 05 06 07 08

% change from year earlier

US (excl.cars & petrol)

Australia

Unemployment rate

3

4

5

6

7

8

01 02 03 04 05 06 07 08

%

US

Australia

Consumer confidence

25

50

75

100

125

01 02 03 04 05 06 07 08

Dec 2000 = 100

US

Australia

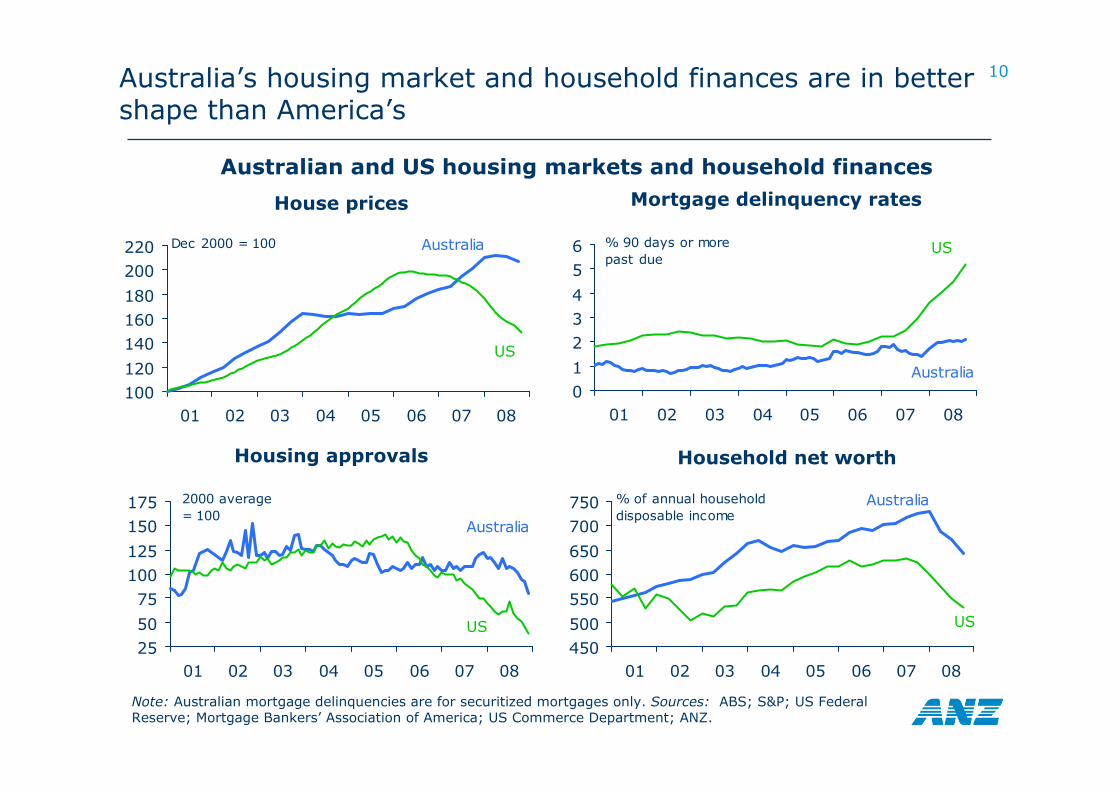

10Australia’s housing market and household finances are in better shape than America’s

Australian and US housing markets and household finances

Note: Australian mortgage delinquencies are for securitized mortgages only. Sources: ABS; S&P; US Federal Reserve; Mortgage Bankers’ Association of America; US Commerce Department; ANZ.

Household net worth

450500

550600650

700750

01 02 03 04 05 06 07 08

% of annual householddisposable income

US

Australia

Housing approvals

2550

75100125

150175

01 02 03 04 05 06 07 08

2000 average= 100

US

Australia

House prices

100120

140160180

200220

01 02 03 04 05 06 07 08

Dec 2000 = 100

US

Australia

Mortgage delinquency rates

01

234

56

01 02 03 04 05 06 07 08

% 90 days or more past due

US

Australia

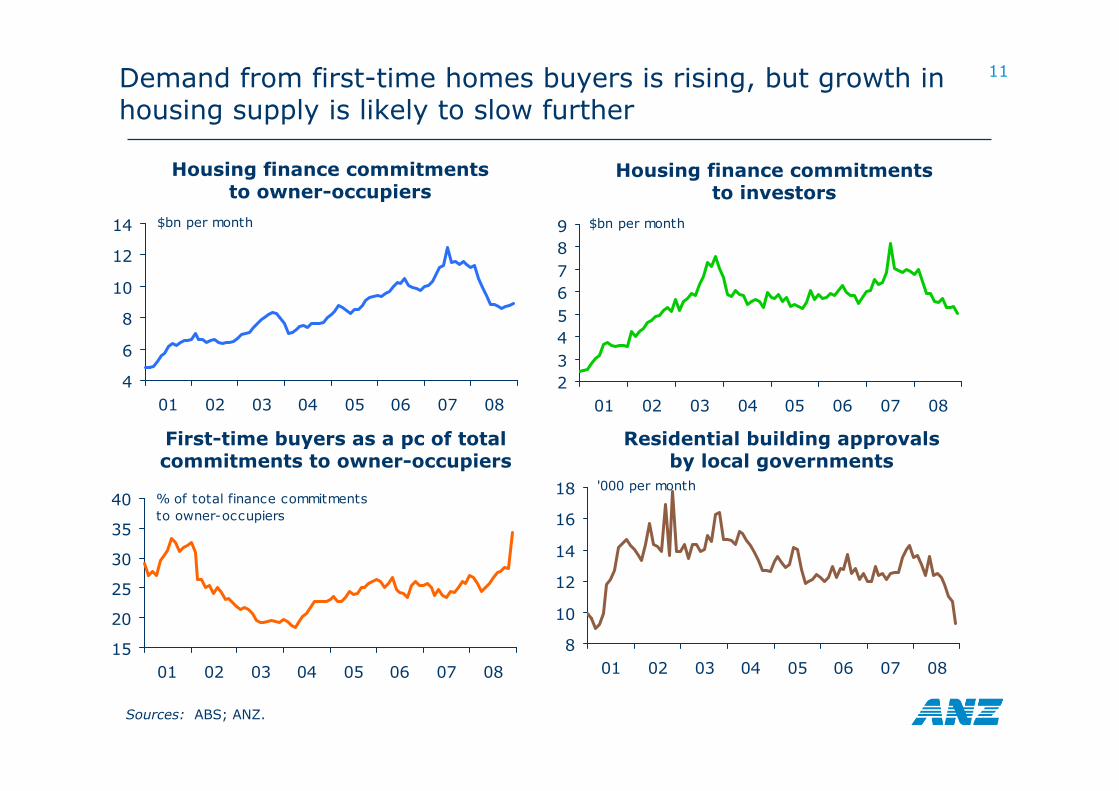

11Demand from first-time homes buyers is rising, but growth in housing supply is likely to slow further

Sources: ABS; ANZ.

Housing finance commitmentsto owner-occupiers

4

6

8

10

12

14

01 02 03 04 05 06 07 08

$bn per month

15

20

25

30

35

40

01 02 03 04 05 06 07 08

% of total finance commitmentsto owner-occupiers

Housing finance commitmentsto investors

First-time buyers as a pc of totalcommitments to owner-occupiers

23456789

01 02 03 04 05 06 07 08

$bn per month

8

10

12

14

16

18

01 02 03 04 05 06 07 08

'000 per month

Residential building approvalsby local governments

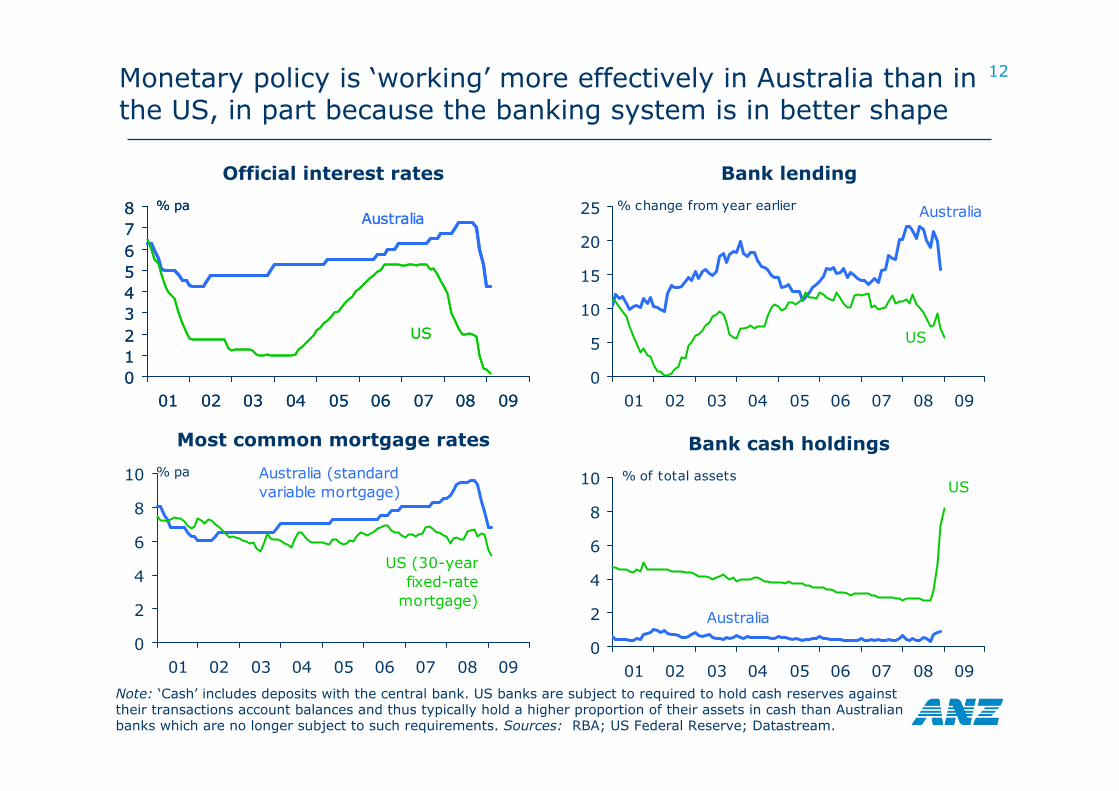

12Monetary policy is ‘working’ more effectively in Australia than in the US, in part because the banking system is in better shape

Official interest rates

Note: ‘Cash’ includes deposits with the central bank. US banks are subject to required to hold cash reserves against their transactions account balances and thus typically hold a higher proportion of their assets in cash than Australian banks which are no longer subject to such requirements. Sources: RBA; US Federal Reserve; Datastream.

012345678

01 02 03 04 05 06 07 08 09

% pa

US

Australia

012345678

01 02 03 04 05 06 07 08 09

% pa

US

Australia

Most common mortgage rates

0

2

4

6

8

10

01 02 03 04 05 06 07 08 09

% pa

US (30-yearfixed-rate

mortgage)

Australia (standardvariable mortgage)

Bank lending

0

5

10

15

20

25

01 02 03 04 05 06 07 08 09

% change from year earlier

US

Australia

Bank cash holdings

0

2

4

6

8

10

01 02 03 04 05 06 07 08 09

% of total assetsUS

Australia

13Is Australia just lagging the United States, or are there some more fundamental differences?

Australia’s economy is yet to feel the full effects of the downturn in the US, European and north Asian economies

– in particular, the impact of the 11% decline in (US$-denominated) export commodity prices has yet to be felt, let alone the further ~32% expected over the first three quarters of 2009 (as contract prices are renegotiated downwards)

– most businesses have been taking a ‘wait and see’ approach to their headcount

There are nonetheless some fundamental differences between Australia and other overseas economies -

– Australia has not had a banking crisis in the same sense as the US and Europe– Australia’s housing market has thus far proved to be more resilient than those of the

US & Europe – for good reasons (shortage of stock relative to underlying demand, relatively low number of ‘forced sellers’) – and should remain so provided unemployment does not rise sharply

Policy responses have been more effective than in other countries─ the RBA has cut rates more quickly than most other central banks (partly but not only

because it had more room to)─ more importantly, cuts in official interest rates have for the most part been reflected in

lower rates paid by end-borrowers (unlike the US and UK in particular)─ fiscal policy has responded more quickly and in a more targeted fashion

The sharp fall in the A$ (with more to come in 2009) has provided an additional ‘buffer’ against contractionary external forces ─ for example commodity prices have actually risen in A$ terms since last July

Australia’s population growth rate is 0.6pc pa above that of the US, 1pc pa above Europe’s and 1½pc pa above Japan’s

14So will Australia experience a recession in 2009?

Possibly not, if a recession is defined as ‘two or more consecutive quarters of negative GDP growth’

– Australia’s faster rate of population growth than most other countries makes negative real GDP growth less likely, everything else being equal

– everything else isn’t equal as between Australia and other Western economies– the Government is likely to time its fiscal policy initiatives with a view to reducing the

likelihood of consecutive quarters of negative GDP growth– we currently expect only one quarter of negative real GDP growth (in the June

quarter), although some others will come very close

Almost certainly, if real gross domestic income (GDI) rather than GDP is used as the ‘measuring stick’

– real GDI is real GDP adjusted for changes in the ‘terms of trade’ (export relative to import prices) and thus captures the effects of major swings in commodity prices (particularly on business income)

– while we expect only one quarter of negative real GDP growth, we expect four consecutive quarters of negative real GDI growth (in 2009)

Probably, if a recession is defined as ‘a rise in the unemployment rate of 1½percentage points or more in 12 months or less’─ note this definition (a) is transferable between countries with different rates of

population and productivity growth; (b) captures all of the periods conventionally regarded as ‘recessions’ in Australia; and (c) makes more intuitive sense to the vast majority of people who have no idea what ‘GDP’ is or when it is contracting

─ we expect Australia’s unemployment rate to rise from 4.5% in December 2008 to 6% by December 2009, peaking at 6¾% in the second half of 2010

15

3.54.04.55.05.56.06.57.0

07 08 09 10

% of labour force

-0.5

0.0

0.5

1.0

1.5

07 08 09 10

% change from previous quarter

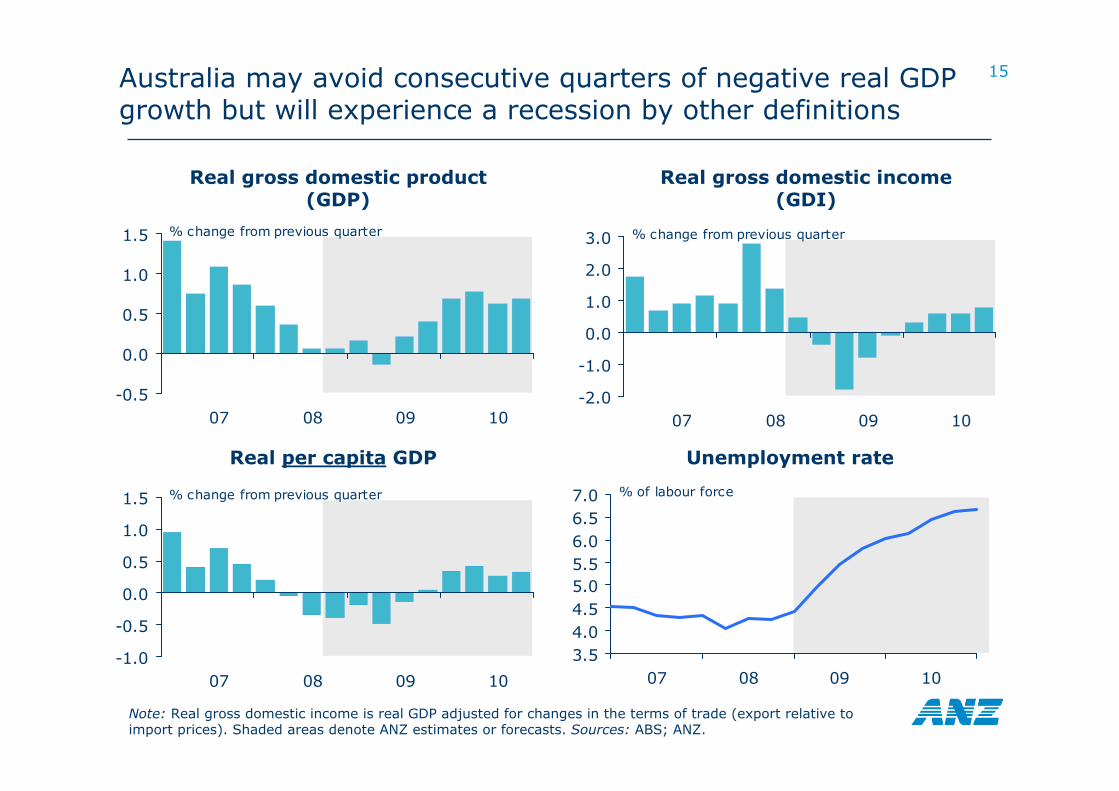

Australia may avoid consecutive quarters of negative real GDP growth but will experience a recession by other definitions

Real per capita GDP

Note: Real gross domestic income is real GDP adjusted for changes in the terms of trade (export relative to import prices). Shaded areas denote ANZ estimates or forecasts. Sources: ABS; ANZ.

Real gross domestic income (GDI)

Unemployment rate

Real gross domestic product (GDP)

-1.0

-0.5

0.0

0.5

1.0

1.5

07 08 09 10

% change from previous quarter

-2.0

-1.0

0.0

1.0

2.0

3.0

07 08 09 10

% change from previous quarter

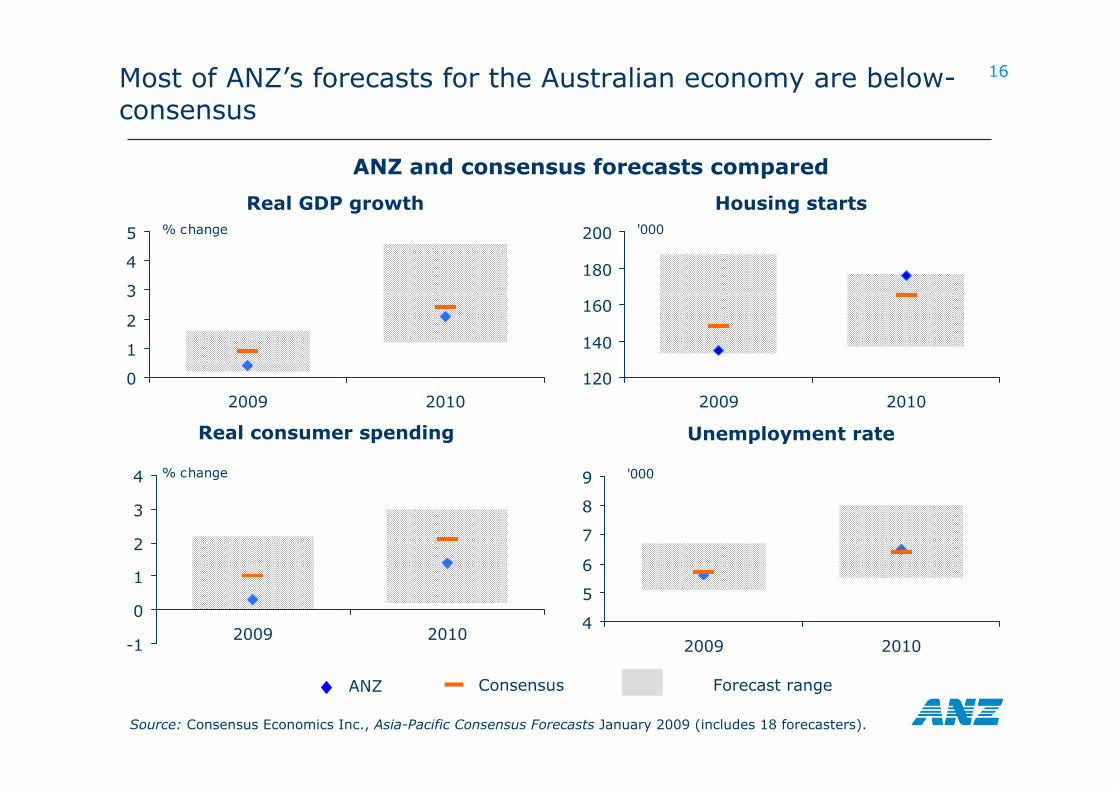

16Most of ANZ’s forecasts for the Australian economy are below-consensus

ANZ and consensus forecasts compared

Real GDP growth

Source: Consensus Economics Inc., Asia-Pacific Consensus Forecasts January 2009 (includes 18 forecasters).

0

1

2

3

4

5

2009 2010

% change

Real consumer spending

-1

0

1

2

3

4

2009 2010

% change

Housing starts

120

140

160

180

200

2009 2010

'000

Unemployment rate

4

5

6

7

8

9

2009 2010

'000

ANZ Consensus Forecast range

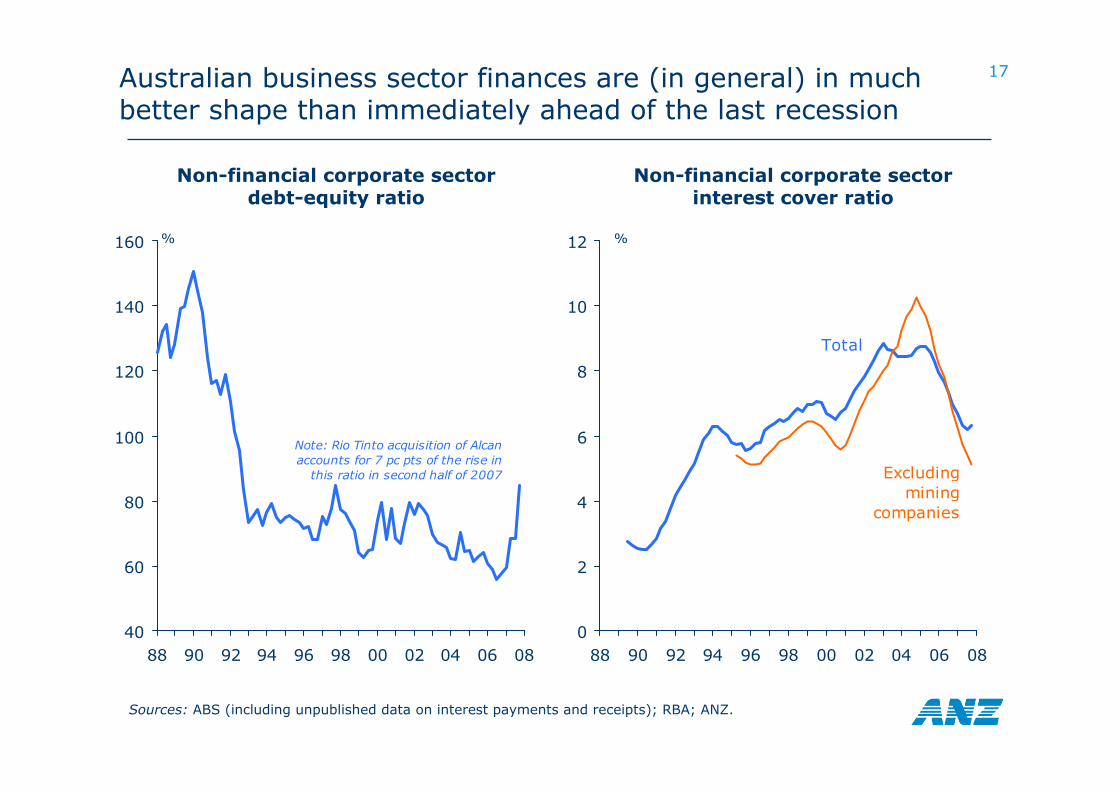

17Australian business sector finances are (in general) in much better shape than immediately ahead of the last recession

Non-financial corporate sectordebt-equity ratio

Sources: ABS (including unpublished data on interest payments and receipts); RBA; ANZ.

40

60

80

100

120

140

160

88 90 92 94 96 98 00 02 04 06 08

%

Note: Rio Tinto acquisition of Alcanaccounts for 7 pc pts of the rise in

this ratio in second half of 2007

0

2

4

6

8

10

12

88 90 92 94 96 98 00 02 04 06 08

%

Total

Excludingmining

companies

Non-financial corporate sectorinterest cover ratio

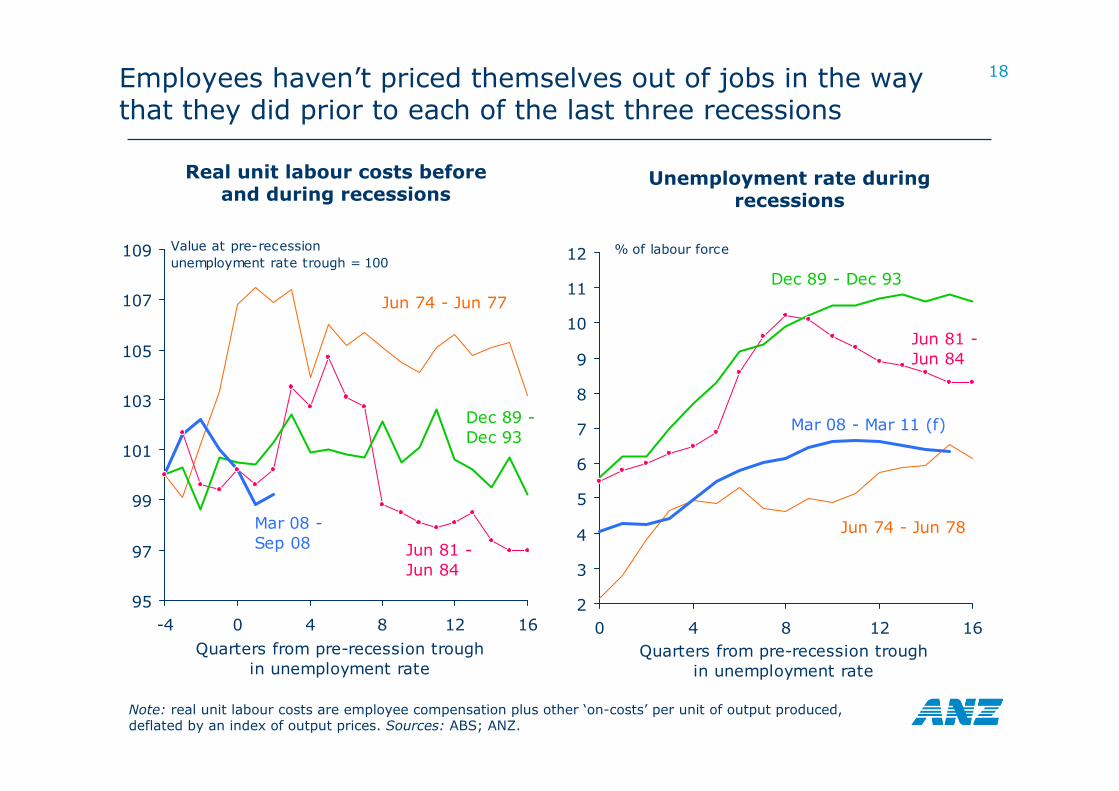

18Employees haven’t priced themselves out of jobs in the way that they did prior to each of the last three recessions

Unemployment rate during recessions

Note: real unit labour costs are employee compensation plus other ‘on-costs’ per unit of output produced, deflated by an index of output prices. Sources: ABS; ANZ.

Real unit labour costs before and during recessions

2

3

4

5

6

7

8

9

10

11

12

0 4 8 12 16

% of labour force

Quarters from pre-recession troughin unemployment rate

Jun 74 - Jun 78

Dec 89 - Dec 93

Jun 81 - Jun 84

Mar 08 - Mar 11 (f)

95

97

99

101

103

105

107

109

-4 0 4 8 12 16

Value at pre-recessionunemployment rate trough = 100

Quarters from pre-recession troughin unemployment rate

Jun 74 - Jun 77

Dec 89 - Dec 93

Jun 81 - Jun 84

Mar 08 - Sep 08

19Inflation will fall quite quickly – but although deflation is possible in some other countries it’s less likely in Australia

Unlike many other countries, Australia had both a ‘headline’ and an ‘underlying’inflation problem up until mid-2008

– as in other countries, higher energy and food prices had pushed ‘headline’ inflation well above the central bank’s ‘comfort zone’ during first half of 2008

– however unlike most other countries, Australia’s ‘underlying’ inflation rate was also significantly outside the RBA’s target range throughout 2008 (reflecting the persistence of demand growth in excess of potential output growth, in circumstances where almost all ‘spare capacity’ had been absorbed)

The Reserve Bank remains pessimistic about the outlook for inflation, despite giving priority since last September to ameliorating the financial crisis

– the RBA has actually raised its forecasts for ‘underlying’ inflation in 2009 and 2010 by ¼ pc pt since last May, and pushed back the time horizon over which it expects inflation to return to the 2-3% target band from H2 2010 to H1 2011

– this more pessimistic view stems largely from the sharp fall in the A$ since July

We think inflation will actually fall more quickly─ ‘headline’ and ‘underlying’ inflation has already begun to decline sharply overseas─ deflation is a distinct possibility in countries whose exchange rates have appreciated

since mid-2008 (including the US, Japan, China, and HK) – although it is much less likely in countries whose currencies have fallen significantly (eg Australia, NZ & UK)

─ Australia (and NZ) are about the only countries in the world without monthly readings on inflation – but unofficial monthly data suggests that ‘headline inflation’ has declined, and ‘underlying’ inflation’ has stopped rising, since the end of September

─ Business and household inflation expectations have fallen significantly since mid-2008

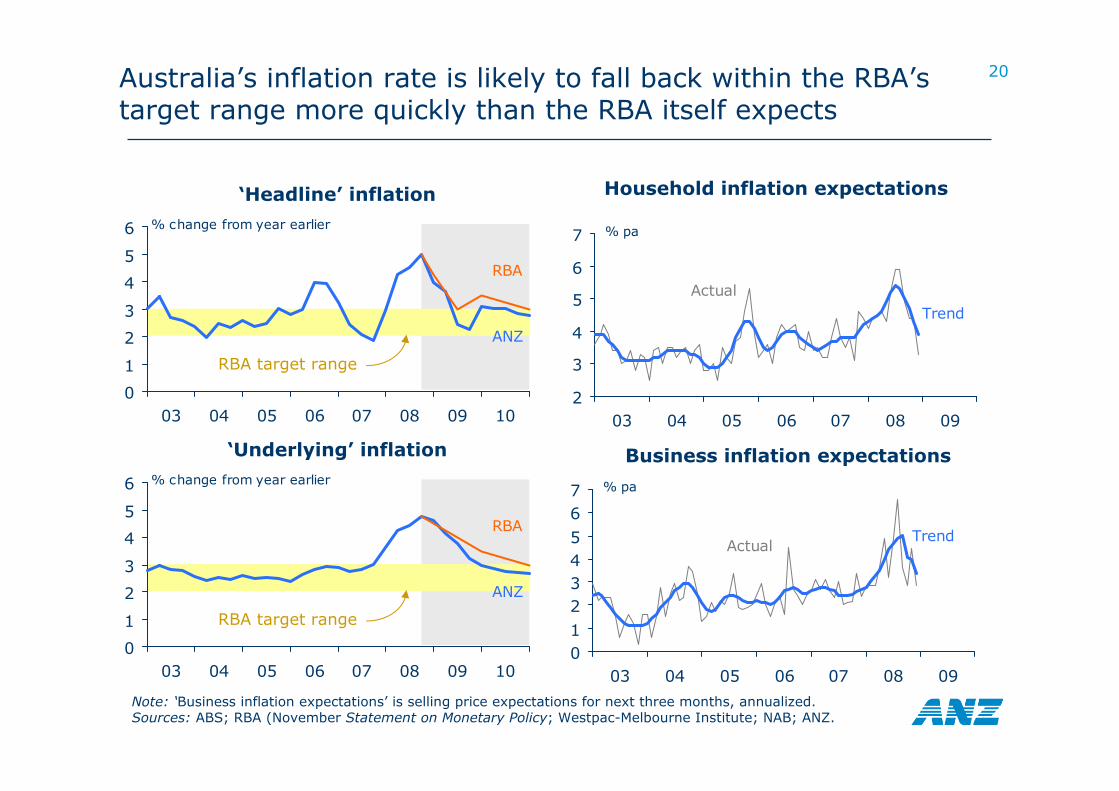

20Australia’s inflation rate is likely to fall back within the RBA’s target range more quickly than the RBA itself expects

Note: ‘Business inflation expectations’ is selling price expectations for next three months, annualized.Sources: ABS; RBA (November Statement on Monetary Policy; Westpac-Melbourne Institute; NAB; ANZ.

‘Headline’ inflation Household inflation expectations

2

3

4

5

6

7

03 04 05 06 07 08 09

% pa

Actual

Trend

‘Underlying’ inflation

0

1

2

3

4

5

6

03 04 05 06 07 08 09 10

% change from year earlier

RBA

ANZ

0

1

2

3

4

5

6

03 04 05 06 07 08 09 10

% change from year earlier

RBA

ANZ

RBA target range

RBA target range

Business inflation expectations

01234567

03 04 05 06 07 08 09

% pa

ActualTrend

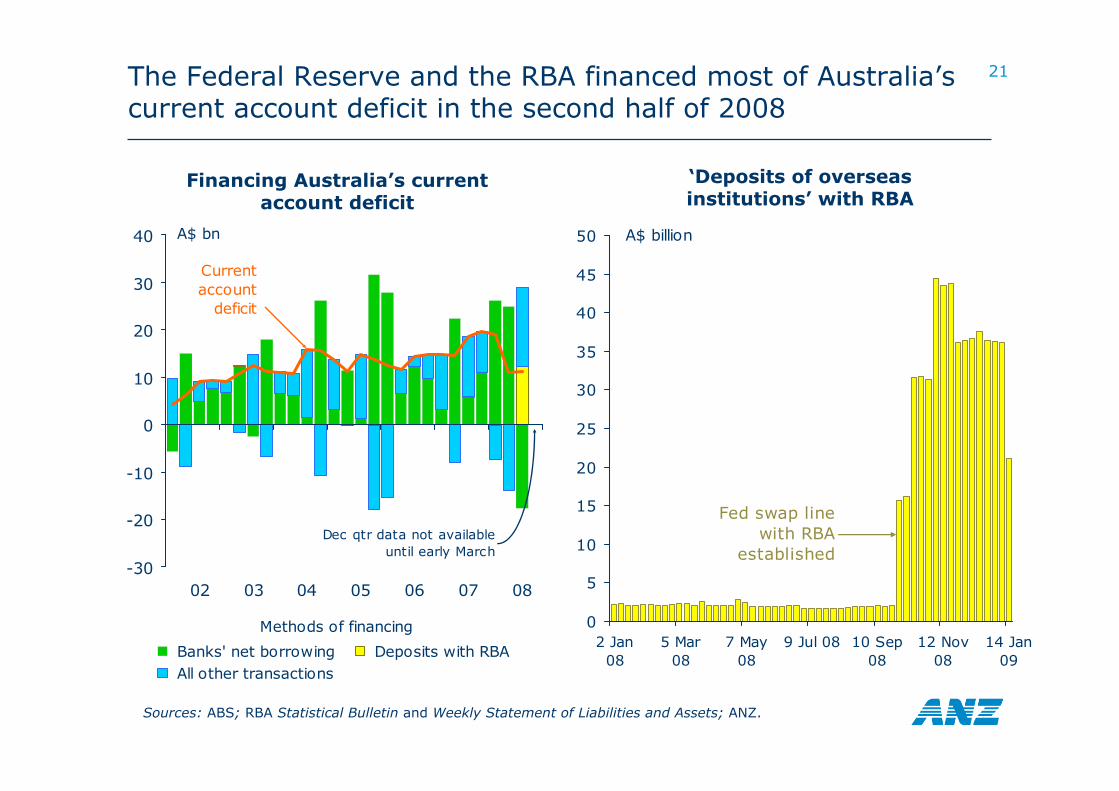

21The Federal Reserve and the RBA financed most of Australia’s current account deficit in the second half of 2008

Sources: ABS; RBA Statistical Bulletin and Weekly Statement of Liabilities and Assets; ANZ.

0

5

10

15

20

25

30

35

40

45

50

2 Jan08

5 Mar08

7 May08

9 Jul 08 10 Sep08

12 Nov08

14 Jan09

A$ billion

Fed swap linewith RBA

established

‘Deposits of overseas institutions’ with RBA

Financing Australia’s current account deficit

-30

-20

-10

0

10

20

30

40

02 03 04 05 06 07 08

Banks' net borrowing Deposits with RBA All other transactions

A$ bn

Current account

deficit

Methods of financing

Dec qtr data not available until early March

22

Summary

The global financial crisis is by no means over – there will be more write-offs, more capital raisings, more government bail-outs, and a lot more regulatory interventions – but there is a good chance that we have passed the ‘end of the beginning’A severe downturn in global economic activity is now under way, and is unlikely to hit bottom before the third quarter of 2009

– the current global downturn is unusually synchronized– conventional monetary policy will be ineffective in reversing it– global economic growth for 2009 as a whole may be as weak as 1982’s 1% (the

slowest since World War II), and possibly lower– some countries will experience deflation

Australia will experience a recession (on some definitions) in 2009─ there might not be consecutive quarters of negative real GDP growth, but real income

will decline, and the unemployment will rise by at least 1½ pc pts However Australia’s recession need not be as severe as those experienced in other countries, or as severe as previous Australian recessions─ Australia’s banking system and residential property markets have thus far been and

should continue to be more robust than those of the US and Europe─ business finances are (in general) in better shape, and labour costs have been better

contained, than ahead of previous Australian recessions – so there is less ‘need’ for mass retrenchments than occurred during previous downturns

─ economic policy responses have been more pro-active than during previous downturns, and appear to be having more impact in Australia than in other countries during the current downturn

23

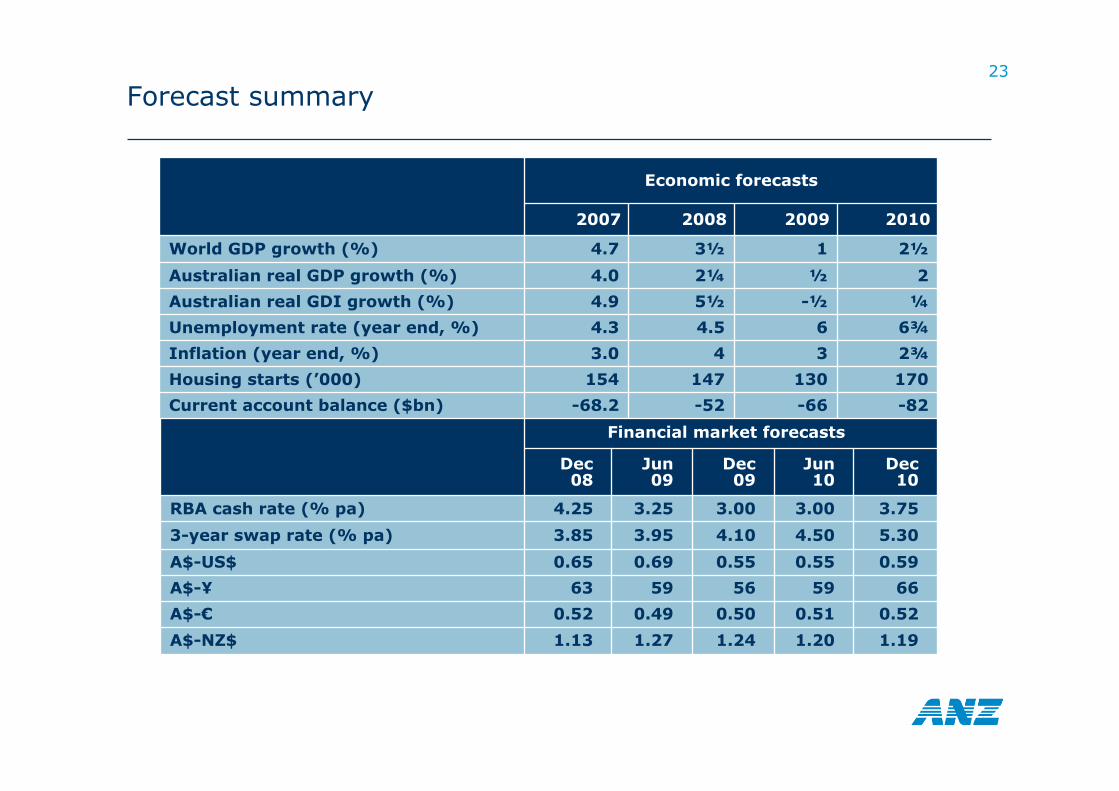

Forecast summary

1.191.201.241.271.13A$-NZ$

5.304.504.103.953.853-year swap rate (% pa)

6659565963A$-¥

0.590.550.550.690.65A$-US$

Financial market forecasts

0.50

3.00

Dec 09

0.51

3.00

Jun 10

0.49

3.25

Jun 09

0.52

4.25

Dec 08

0.52

3.75

Dec 10

A$-€

RBA cash rate (% pa)

¼-½5½4.9Australian real GDI growth (%)

Economic forecasts

6¾64.54.3Unemployment rate (year end, %)

2½2¼4.0Australian real GDP growth (%)

170130147154Housing starts (’000)

2¾343.0Inflation (year end, %)

-52

3½

2008

-66

1

2009

-68.2

4.7

2007

-82

2½

2010

Current account balance ($bn)

World GDP growth (%)