Perspectives on COVID-19 and P&C Coverages...Perspectives on COVID-19 and P&C Coverages. What you...

14

Perspectives on COVID-19 and P&C Coverages

Transcript of Perspectives on COVID-19 and P&C Coverages...Perspectives on COVID-19 and P&C Coverages. What you...

Perspectives on COVID-19 and P&C Coverages

What you need to know. As businesses around the world are reeling from the impact of COVID-19, the Alera Group team is working hard to keep you updated with the information you need to know to keep your employees and your business safe. Within this document, you’ll find the expected impact of COVID-19 on a variety of lines of coverage.

The thoughts provided in this document are general, and it is up to individuals and their brokers to determine what their unique policies cover. Please reach out to your Alera Group contact for assistance with identifying your current coverages.

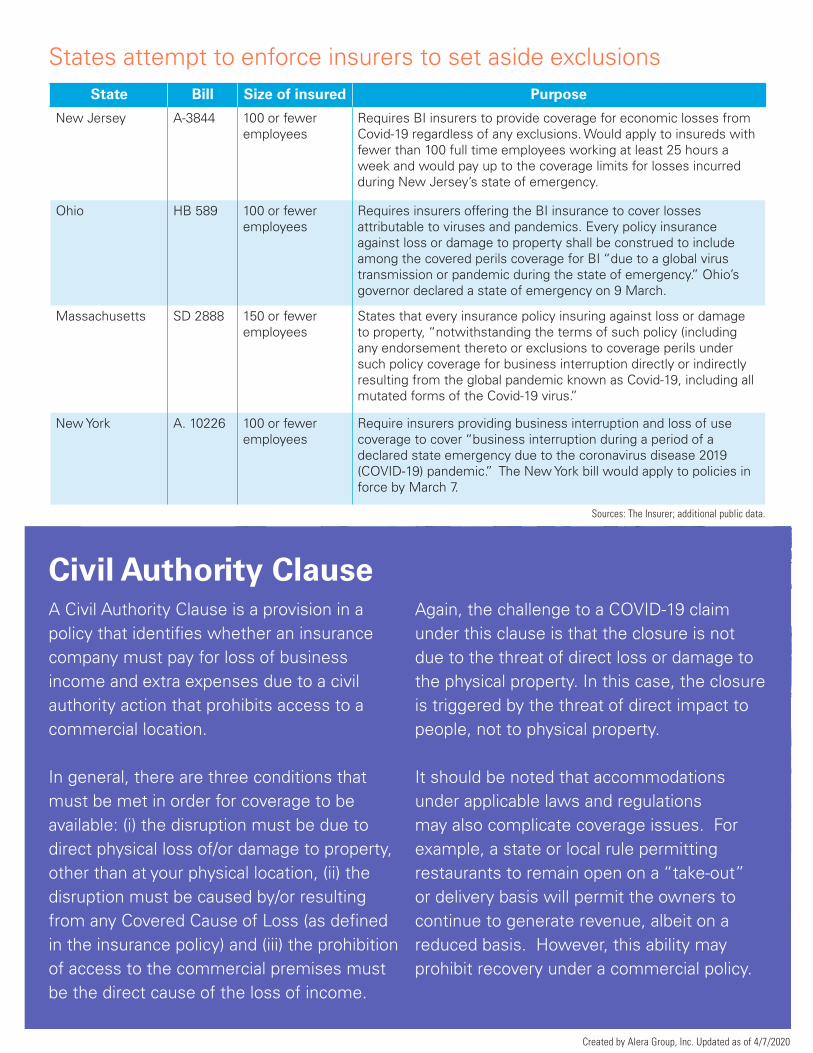

How this will play out remains to be seen. There are bills pending in several states that would require insurance carriers to pay these business interruption claims retroactively. While the insurance industry currently holds an estimated $800 billion in surplus, that surplus could quickly disappear if insurance carriers were required to retroactively pay multiple months of business interruption losses. The American Property Casualty Insurance Association estimates that the closure losses for small businesses can be as high as $431 billion per month.

Also tied to the Property policy, Contingent Business Income Insurance and Contingent Extra Expense coverage are intended to cover supply chain related claims resulting from damage or operational disruption at the location of a customer or supplier from a covered peril in the insurance policy. Although we have seen major business disruptions in the global supply chain, standard commercial insurance does not cover financial losses an insured company experiences when its suppliers experience loss and cannot supply key materials or goods.

Similarly, standard commercial insurance typically will not cover your company if your customers cannot accept goods due to a loss that they incurred. In most cases related to COVID-19, the direct physical damage and covered peril thresholds have not been met. As with any claim scenario, however, it is imperative to consult with your agent or broker and review the coverage, terms and conditions provided in your specific insurance policy.

With the widespread closure of businesses globally from COVID-19, Business Interruption and Contingent Business Income insurance coverages are in the spotlight. Both are tied to the Property policy and are intended to cover a loss of income due to direct physical damage or operational disruption to a property as the result of a covered peril.

With a Property policy, Business Interruption and Extra Expense are intended to cover loss of income or extra expenses should a business need to shut down or slowdown as a result of a loss, damage or destruction to an insured property. This coverage is typically triggered when the physical location incurs a direct physical loss or damage, such as fire or water damage.

The presence of a virus on the property does not normally trigger coverage under the terms of the policy. Courts have ruled that contamination which renders a property unusable for its primary purpose may establish direct property loss or damage. From what is known right now, COVID-19 does not meet the threshold under “contamination”.

Business Interruption

Mark EnglertNew York Metro Area

Created by Alera Group, Inc. Updated as of 4/7/2020

A Civil Authority Clause is a provision in a policy that identifies whether an insurance company must pay for loss of business income and extra expenses due to a civil authority action that prohibits access to a commercial location.

In general, there are three conditions that must be met in order for coverage to be available: (i) the disruption must be due to direct physical loss of/or damage to property, other than at your physical location, (ii) the disruption must be caused by/or resulting from any Covered Cause of Loss (as defined in the insurance policy) and (iii) the prohibition of access to the commercial premises must be the direct cause of the loss of income.

Again, the challenge to a COVID-19 claim under this clause is that the closure is not due to the threat of direct loss or damage to the physical property. In this case, the closure is triggered by the threat of direct impact to people, not to physical property.

It should be noted that accommodations under applicable laws and regulations may also complicate coverage issues. For example, a state or local rule permitting restaurants to remain open on a “take-out” or delivery basis will permit the owners to continue to generate revenue, albeit on a reduced basis. However, this ability may prohibit recovery under a commercial policy.

Civil Authority Clause

State Bill Size of insured PurposeNew Jersey A-3844 100 or fewer

employeesRequires BI insurers to provide coverage for economic losses from Covid-19 regardless of any exclusions. Would apply to insureds with fewer than 100 full time employees working at least 25 hours a week and would pay up to the coverage limits for losses incurred during New Jersey’s state of emergency.

Ohio HB 589 100 or fewer employees

Requires insurers offering the BI insurance to cover losses attributable to viruses and pandemics. Every policy insurance against loss or damage to property shall be construed to include among the covered perils coverage for BI “due to a global virus transmission or pandemic during the state of emergency.” Ohio’s governor declared a state of emergency on 9 March.

Massachusetts SD 2888 150 or fewer employees

States that every insurance policy insuring against loss or damage to property, “notwithstanding the terms of such policy (including any endorsement thereto or exclusions to coverage perils under such policy coverage for business interruption directly or indirectly resulting from the global pandemic known as Covid-19, including all mutated forms of the Covid-19 virus.”

New York A. 10226 100 or fewer employees

Require insurers providing business interruption and loss of use coverage to cover “business interruption during a period of a declared state emergency due to the coronavirus disease 2019 (COVID-19) pandemic.” The New York bill would apply to policies in force by March 7.

States attempt to enforce insurers to set aside exclusions

Created by Alera Group, Inc. Updated as of 4/7/2020

Sources: The Insurer; additional public data.

The COVID-19 pandemic is presenting the insurance industry with unprecedented challenges. General Liability, along with most lines of property and casualty coverage, will most likely be challenged in either the courts or state legislatures at a historic level. Most of the focus in the early stages of the pandemic has concentrated on the question of whether loss of income is covered under the Property policy. We expect liability claims to follow a similar path.

As an example, claims could arise from a business remaining open after an employee tests positive for the virus or from an outbreak occurring at the premises that exposes members of the public. The affected (or infected) persons could sue the business and attempt to collect under the Bodily Injury portion of the General Liability policy.

There are two main challenges to an insurer providing the company with coverage in this scenario. First, the claimant would have to prove that the alleged act or neglect caused the injury. Due to the long latency of this disease, it may be difficult to prove who or what caused the virus. Second, from a policy perspective, the insurance company will probably rely on the Pollution exclusion contained in almost every General Liability policy to deny coverage.

We are advising clients that these are the standard policy interpretations of policy language as of today. However, we are just one court decision or new state statute away from the landscape on this issue changing. Policyholders should stay informed and contact their agent or broker if they have any questions.

General Liability

John Beauregard, CIC, LIADartmouth, MA

Created by Alera Group, Inc. Updated as of 4/7/2020Created by Alera Group, Inc. Updated as of 4/7/2020

The surety industry has been very healthy over the last several years. However, as the coronavirus (COVID-19) continues to expand around the U.S. and the world, the virus could have a dramatic effect on construction companies that could, in turn, impact the surety industry’s results and underwriting.

Contractors with significant continued overhead expenses could have little or no revenue during this period, impacting their ability to recover or even sustain operations. In addition, as projects delay, the compression in schedules could impact the ability for contractors to complete their projects. Once contractors return to work, they will potentially be handicapped with weaker than usual cash flow, shortages of labor, shortages of materials and the risk of vendors and subcontractors being unable to honor their bids and commitments.

Surety bonds are provided by most large insurance carriers and are underwritten and priced with no anticipation of losses. Based on this, we anticipate credit tightening within the surety marketplace. Underwriters will closely underwrite their book of business and want to fully understand their client’s cash flow forecasts and business plan for profitability.

Contract Surety

Rob StriewigMechanicsburg, PA

Created by Alera Group, Inc. Updated as of 4/7/2020

For those providers who have rapidly deployed or expanded telemedicine services, liability carriers have extended coverage under existing policies as long as the patients are located in a state in which the provider is appropriately licensed to practice medicine. On the federal side, CMS and OCR have broadened access to telemedicine services by paying for them similar to in-person visits and waiving certain HIPAA penalties respectively.

Many healthcare providers are also small businesses that have felt the impact of the pandemic on the business side as well. Carriers have stepped up and offered to defer or reduce premium payments so that medical practices can continue to meet their overhead needs. While no one can predict how long this crisis will continue, we expect insurers to continue to provide critical support to healthcare providers.

Medical Malpractice

Jason Shah, M.D.Chicago, IL

Healthcare providers are on the front lines combating this pandemic, and med-mal insurance carriers are rising to the occasion by responding in three key areas: relaxing underwriting requirements, simplifying processing and offering premium deferment options.

With regard to underwriting requirements, carriers are offering presumptive coverage and streamlining the administrative process for adding providers to enable healthcare organizations directly treating COVID-19 patients to swiftly implement surge plans.

Created by Alera Group, Inc. Updated as of 4/7/2020

Data breaches are costly to any business, even in the best of times. With COVID-19 and increased telecommuting, the likelihood of a cyber attack increases—along with the possibility of a data breach.

COVID-19-related attacks via email have been reported to have increased by 667% since the end of February, according to research by cybersecurity firm Barracuda Networks.

This spike in cyberattacks comes at a time when businesses are often the most vulnerable, with IT teams working from home and often limited with the tools they have to troubleshoot issues*. Remote employees who are not used to working from home may not have adequate security, presenting new access points for hackers to gain network entry. Work-from-home employees are also vulnerable to scams such as phishing emails disguised as COVID-19 alerts. When opened, malware is implanted, giving hackers an opportunity to demand ransom or steal data.

As a result of this increase in attacks, the cyber liability market could see a dramatic increase in claims from data breaches. The industry is taking steps to help educate businesses on how to avoid and mitigate risks by securing their networks using protocols such as VPN and multi-factor identification, as well as other network security measures. *Fortune Data Sheet, March 27, 2020

Health

Financial

Energy

Industrial

Pharma

Technology

Education

Services

Entertainment

Transportation

Communication

Consumer

Media

Hospitality

Retail

Research

Public

$0 $1.75 $3.50 $5.25 $7

$6.45

$5.86

$5.60

$5.20

$5.20

$5.05

$4.77

$4.62

$4.32

$3.77

$3.45

$2.59

$2.24

$1.99

$1.84

$1.65

$1.29

Average total cost of a data breach by industry ($ Millions)

Cyber Liability

Stephen Paulin, CICNewport Beach, CA

Source: IBM Security, 2019. Cost of Data Breach Report

Created by Alera Group, Inc. Updated as of 4/7/2020

Environmental Liability

Gene NosovitchBethlehem, PA

Certain insurers limit the scope of coverage for virus-related claims to direct disinfection and/or remediation expenses incurred by the insured in responding to the presence of the virus.

Many environmental insurance forms also include coverage for business interruption losses. The triggering language for Business Interruption (BI) coverage under an environmental policy is significantly different than standard BI language and should be evaluated to determine if a pollution policy’s virus coverage extends to these types of losses.

Many environmental forms that include BI make the coverage contingent on the presence or release of a pollutant at a covered location. In the case of COVID-19 claims, the cause of a particular location’s shutdown, closure or suspension of operations must be tied to the presence or release of the coronavirus at such particular location. This may present a coverage hurdle when business closures are related to the outbreak as a whole. Existing policyholders should take note of their policies and consider submitting any COVID-19 related claims to their carriers.

Environmental insurance may be uniquely positioned to respond to situations like the coronavirus pandemic. The question of whether an environmental insurance policy will respond to claims or losses arising out of the coronavirus (COVID-19) outbreak depends on the language and structure of the specific policy form or endorsement(s). There are frequently important limitations or exclusions imposed by the environmental markets on the extent of virus coverage in general, but that should not preclude a careful review of your policy to identify potential coverage.

For those with environmental exposures, the first step in determining coverage is to review the policy’s definitions of “pollutants” to determine if viruses are included in the policy language. The policyholder will then need to determine how the “pollution condition” is defined, as this triggers the event for coverage and whether the loss can be traced to a specific dispersal or release of coronavirus. Once a policy’s classification of viruses has been identified, the next step is to identify potentially applicable Insuring Agreements within the policy.

Created by Alera Group, Inc. Updated as of 4/7/2020Created by Alera Group, Inc. Updated as of 4/7/2020

As the personal and financial impact of COVID-19 increases, Directors & Officers (D&O) face the potential for claims centered around corporate planning, oversight and contractual obligations.

With the economic impact of the virus, companies could experience a rise in shareholder lawsuits alleging the company’s poor financial results or drop in stock price is the result of management’s failure to establish proper protocols or contingency plans, along with possible disclosure issues. Depending on the specific terms and conditions of the D&O policy, coverage may apply. In addition, we could see a spike in employment-related lawsuits or complaints arising out of furloughs, layoffs and terminations. Depending on the nature of the allegations and the type of policy form, there could be coverage for EPLI claims or EEOC complaints.

As the virus continues to spread, there is also the potential for a rise in customer claims alleging that management failed to prevent the spread of the virus through improper emergency planning,

Directors & Officers Liability

Dan SandersonRaleigh, NC

communication and responsiveness. Typically, D&O policies include Bodily Injury and Pollution exclusions, some of which are absolute and would not provide coverage in this situation.

With the strain on businesses in most sectors, contract litigation will likely rise. D&O policies have breach of contract exclusion(s) and would not provide coverage. Some policies have carve-backs for liability that would exist in the absence of a contract, but it is highly unlikely that could apply in any situation. However, even if there is doubt or no chance of finding coverage for any D&O claim, it would be prudent to submit a claim and let the carrier make the determination.

Created by Alera Group, Inc. Updated as of 4/7/2020

Workers’ Compensation

Lisa LeBlancNewport Beach, CA

COVID-19 has essentially stalled-out the Workers’ Compensation (WC) claims process in most areas, and the question of what is covered under Workers’ Compensation is currently in flux on a state-by-state basis. Amid this uncertainty, we anticipate there will be an uptick in claims and litigation as employees remain at home.

The goal of a Workers’ Compensation claim is to get an employee back to work on either a transitional basis or full duty. The spike in company closings and layoffs is prolonging this process and increasing indemnity costs on the claim. Claims are also stalling as injured employees cannot get in for physical therapy treatments, to see specialists, or see their doctor for follow-up care. We are urging our adjustors to recommend Telemedicine and Teletherapy as an alternative to simply not receiving treatment during this time, however these are relatively new options.

Danyel BrentNewport Beach, CA

Carriers are also disagreeing on how to handle temporary total disability (TTD) payments for employees who were working modified duties. Most carriers are paying TTD to furloughed employees that have temporary restrictions and were working modified duties. But there are some carriers that are handling this case-by-case or have stated they are not paying TTD benefits to the above-mentioned employees.

Although we expect to see an influx of litigated claims, the courts are limiting cases and some courts are relying on remote services such as CourtCall. Coverage for COVID-19 also seems to be in debate and determined at a state level. Some of the first states to weigh-in on WC claims are Washington and Kentucky, which have guaranteed WC benefits for healthcare workers and first responders. South Carolina has stated COVID-19 claims are not covered if contracted by co-workers or employees are faced with equal exposure while away from work. In California, an employee is able to receive benefits if they are sickened by a communicable disease and are able to show they were particularly vulnerable. As the virus progresses, we anticipate more states making decisions in the coming weeks.

Created by Alera Group, Inc. Updated as of 4/7/2020

Captive insurance companies allow groups to lower their total cost of risk while also creating coverage where gaps exist in the commercial market or where current rate levels become unaffordable, unavailable or just inefficient. With the ongoing COVID-19 pandemic, captive insurance companies are likely to experience an uptick of claims in an array of coverage areas, including high cost medical claims and professional or management liability.

Organizations that have used captives to underwrite these coverages should to be able to meet these additional expenses with relative ease, assuming they have surplus and reinsurance protection to cover these possible

Captives

Peter JohnsonBoston, MA

adverse claim outcomes. These organizations would receive multiple benefits as a result. First, there should be limited cash flow impact on the organization since their captives hold reserves for future loss payments. Second, captive members should have insulation from hardening markets as future year premiums will be determined on the basis of their own experience, rather than the insurer’s overall experience. Finally, in certain cases, captives can be leveraged to provide premium holidays that would help organizations free up cash to invest in rebuilding the business and help meet budget shortfalls due to depressed revenue and profits.

Captives are generally set up to insure organizations with broader policy terms that may cover virus related events and may have funds available to supplement the loss of revenue, employee wages, etc. For example, a business interruption policy may drop down to cover a loss of revenue associated with COVID-19 and provide employee wage protections. We anticipate post-pandemic interest in companies seeking a captive to protect against future situations and in anticipation of a hardening market.

Created by Alera Group, Inc. Updated as of 3/31/2020

Have questions? In light of COVID-19, many companies will likely face scenarios that they’ve never encountered before. We’re committed to creating leading solutions to meet the needs of our clients, grappling with the complex problems arising from COVID-19 alongside those that come up in everyday business.

Please reach out to your Alera Group contact to discuss the topics in this white paper and ask any questions you may have. You can also reach us by visiting the Contact Us page of our website, aleragroup.com.

The information contained herein should be understood to be general insurance brokerage information only and does not constitute advice for any particular situation or fact pattern and cannot be relied upon as such. Statements concerning financial, regulatory or legal matters are based on general observations as an insurance broker and may not be relied upon as financial, regulatory or legal advice. This document is owned by Alera Group, Inc., and its contents may not be reproduced, in whole or in part, without the written permission of Alera Group, Inc. 4/7/2020.

Created by Alera Group, Inc. Updated as of 4/7/2020

Three Parkway North | Suite 500 | Deerfield, IL 60015D 847-582-4501 | aleragroup.com