Pecking order versus trade off theory and the issue of ...

32

Document de travail IDP (EA 1384) n°2013-13 Pecking order versus trade off theory and the issue of debt constraint problem? Mohamed Ramdani et Ludovic Vigneron RIO – Risque, Information, Obligation

Transcript of Pecking order versus trade off theory and the issue of ...

Document de travail IDP (EA 1384) n°2013-13

Pecking order versus trade off theory and the issue of debt

constraint problem?

Mohamed Ramdani et Ludovic Vigneron

RIO – Risque, Information, Obligation

Pecking order versus trade off theory and the issue

of debt constraint problem?

Mohamed Ramdani et Ludovic Vigneron

Mohamed Ramdani

PRES Université Lille Nord de France, Université de Valenciennes et du Hainaut-

Cambrésis, IDP, EA1384, Valenciennes, France

Ludovic Vigneron

PRES Université Lille Nord de France, Université de Valenciennes et du Hainaut-

Cambrésis, IDP, EA1384, Valenciennes, France

1

“Pecking order versus trade off theory and

the issue of debt constraint problem?”

Mohamed Ramdani

Maître de Conférences

Université de Lille Nord de France - IDP

Institut du Développement et de la Prospective

Ludovic Vigneron1

Maître de Conférences

Université de Lille Nord de France - IDP

Institut du Développement et de la Prospective

Abstract:

This paper presents a new test investigating competing capital structure theories. Our test was

performed more particularly on a sample of French quoted firms. The question is which one

of pecking order or trade off theory can be considered as a better first order explanation for

firms’ behaviors. This test seeks to shed some new light on the issue of debt constraint

problem and its effects. We use both linear and un-linear specifications of the relationship

between the firm’s debt variation and financial deficit to deal with this difficulty. In the

classical linear context, our findings show that trade off theory dominates pecking order for

constrained firms whereas pecking order dominates trade off theory for unconstrained ones.

However, we will show the introduction of that un-linear specifications improves pecking

order adjustment and makes it difficult to distinguish which theory better fits.

Key words: Capital structure, Trade off theory, Pecking order theory, debt constraint

JEL classification: G32

1 Contact : [email protected]

2

INTRODUCTION

Financial structure puzzle is one of the oldest and more prolific research topics in corporate

finance. Since Modigliani and Miller (1958, 1963) seminal papers, many other articles have

dealt with the issue of firms’debt rational choice. Current debates focus on whether trade-off

or pecking order theory better explains companies’ behaviors. Shyam-Sunder and Myers

(1999) proposed a test to arbitrate between these two analyses and concluded in favor of

pecking order. But their results were contested by Chirinko and Singha (2000) and Frank and

Goyal (2003). One of the most important addressed criticisms is that their empirical evidence

did not perfectly reflect pecking order financing. Lemmon and Zender (2010) stated that this

relatively poor performance of Shyam-Sunder and Myers’ test could be explained through of

firms’ limited debt capacity and proposed a modified test to deal with this issue. They

considered an un-linear relationship between debt variation and need for external finance.

The new test we develop in this paper seeks to contribute to the pecking order versus trade off

debate. It considers the impact of difficulties that firms can face if they want to finance

important needs (or if they want to use the important excess in their internal resources) on

discriminatory power of previous test. We examine the question of which one these two

theories is a better first order explanation of firms’ financial behaviors considering debt

constraint problem. Our investigation was conducted in a different institutional context than

previous studies used to consider. More specifically a new dataset of French firms provided

different results from the previous studies which were mostly conducted in an Anglo-Saxon

context. Through the example of France and its economy based on a bank-centered financial

system, our data have allowed us to present original results. In our sample, pecking order

behavior must be more relevant because of difficulties in issuing equities in the French capital

market.

To start our analysis, we first replicate classical versions of pecking order theory tests by

financial deficit and trade off theory test by target adjustment through mean reversion. These

two dependent variables have a significant impact on the variations of the debt of firms. Then,

we consider differences in debt financial behaviors for constrained and unconstrained firms.

We clearly observe that access to debt is an important dimension to be considered especially

when the question of capital structure puzzle is at stake and when you consider pecking order

theory tests. For classical linear specifications of financial deficit, we document that, in the

case of debt constrained firms, target adjustment is a better first order explanation of debt

3

variation than financial deficit and, for unconstrained ones, we document that financial deficit

appears to be a better first order explanation for debt variation. For un-linear specifications,

more exploration is needed. Indeed, the relationship between financial deficit and debt

variations become more important and we can’t distinguish whether pecking order or trade off

theory is a better first order explanation for capital structure.

This article is organized as follows. Section one quickly discusses the literature about

financial structure and focuses on prior tests and develops our hypotheses. Section two

describes the dataset and specifications of our tests. Section three presents our main results we

obtained after we performed some robustness checks tests.

I. LITERATURE AND HYPOTHESES

A. LITERATURE

On perfect market contexts, the capital structure issue is irrelevant (Modigliani and Miller,

1958). The firms’ financing choice is only a question of cash flow allocation and it does not

influence the project choice or firm value. Modern financial theory goes beyond this

simplified analytical context. Two dominant classes of models are currently employed to

explain capital structure: trade-off and pecking order. Empirical researches continuously fuel

approaches without conclusive answers in favor of one or the other because they are not

mutually exclusive and do not fully explain firms’ behavior2.

For trade-off theory, firm capital structure choice results from an arbitrage between costs and

debt benefits. The most important explaining factors used in literature are tax reduction and

increases in bankruptcy costs. Bradley et al. (1984) present a static version of this class of

model in which firms choose optimal financial leverage balancing debt and equity finance to

maximize their value. They consider different tax rates for investors who buy bonds or

equities. They show that optimal debt level increases with both tax rate on equities and costs

of distress but decreases with tax rate on bonds. The main problem of these static models is

that they predict only one optimal solution that the firm must always met. This is not realistic.

For example, there are no retained earnings. This imperfect model requires the necessity to

use a new class of models, such as dynamic trade-off models in which the financing decision

2 For a more exhaustive review see Franck and Goyal (2007)

4

depends on the financing margin anticipated by the firm. These models include retained

earnings as internal equities and focus on the fact that the money which stay in the firm is not

taxed but the money paid out is taxed (Stiglitz, 1973). Following this approach, Kane et al.

(1984), Brennan and Schwartz (1984) show that firms rebalance their leverage to adapt

themselves after shocks and to converge to optimal structures. Fischer et al. (1989) introduce

transaction costs in the dynamic trade-off to obtain a more realistic rebalancing behavior. In

this context, convergence to optimal capital structure can be slower.

As regards, pecking order theory, there is not necessarily an optimal capital structure but a

hierarchy between different sources of funds which try to minimize asymmetric information

problems. Firms prefer internal to external financing and debt to equity. They first employ all

their retained earnings and then they use debt. Equities are issued after the firms’ debt

capacity is reached. Myers and Majluf (1984) are at the origin of this class of models. They

consider an adverse selection problem which leads good firms to prefer internal financing to

fund their positive net present value projects, because external investors will charge them at

the same level as bad firms. In this context, the cost of external equity can lead good firms to

give up profitable opportunities. External debts are not explicitly included in the analysis but,

as Myers (1984) notes, lenders priority over firm’s cash flow make debt less risky than equity

and so cheaper. Myers (2003) proposes a version of pecking order based on agency costs.

Managers always prefer internal financing because outside financing exposes them to

monitoring which reduces their perk consumption. If it is not enough, external equity issue is

not an inefficient solution because it leads to underinvestment. Managers limit profitable

projects they can undertake to preserve their perk consumption. External debt is a better

solution because of fix cash flow associate with which can discipline managers.

The main tests of current theories currently focus on two empirical strategies: target

adjustment of companies’ leverage for trade-off theories and debt funding of financial deficit

for pecking order theories.

The first strategy is the oldest approach (Taggart, 1977). It postulates that, because of random

exogenous shocks in their access to the different sources of funds, the capital structure of

firms may be different from the optimal structure, but they sequentially correct this fact by

issuing or buying back debts or equities to converge to the optimal structure. The tests consist

in two sequences. The first sequence consists in checking if the leverage ratio is effectively

adjusted to reach a target and the second one in measuring the speed of this adjustment. The

5

main difficulty here is to estimate optimal leverage. The most classic way to proceed is to use

the historical means of leverage as a proxy (Marsh, 1982; Jalilvand and Harris, 1984; Fama

and French, 2001). This method implicitly supposes that the firms’ characteristics which

influence optimal capital structure are relatively stable over time. More recently, more

sophisticated estimations for target leverage have been developed. Hovakimian et al. (2001)

use a two-stage method. In a first step, they use regression leverage over the firms’

characteristics and in a second step, they use obtained estimations minus the firm’s actual

leverage with control factors in a logit regression of financing choice of firm. Kotrajczyk and

levy (2003), Kayhan and Titman (2007) use the same kind of method. The main results of

these studies are that firms adjust their leverage to a target. The leverage in question is mean

reverting, but this move toward optimal ratio is relatively slow (Fama and French, 2002). In a

study about the United Kingdom and continual Europe, Wanzenried (2006) documents that

the speed of adjustment depends on the institutional context.

The second strategy was originally elaborated by Shyam-Sunder and Myers (1999). The

starting point is that in pecking order context, every need for external funds must be fulfilled

with debts because debts are cheaper than equities. So we must document a strictly

proportional link between the need for external funds, the firms’ financial deficit, and the

debts variation. When firms have a positive financial deficit, they must issue debts, and when

they have a negative one, they must pay back their debts. Unfortunately, studies based on this

method fail to find perfect correlation between changes in debt and financial deficit but they

document all the same evidences of a strong one. In France, we can refer to Aktas et al.

(2011) for very small business, or to Molay (2005) for big firms. Shyam-Sunder and Myers

(1999) compare these findings with the classical target adjustment method and conclude that

pecking order theory is more efficient to predict a firm’s behavior than trade-off theory. Frank

and Goyal (2003) contest this interpretation. They show over a larger and longer dataset that

the relations between debt variations and financial deficit depend on the period and the

category of the firms. They point at two paradoxical results which contradict pecking order

predictions. First, young and rapidly growing firms, for which adverse selection problems are

important, finance most of their needs by equities. Second, big and mature firms, for which

adverse selection problems are low, mostly rely on debts to finance their needs. Globally, in

line with Fama and French (2005), the authors document that too many issues of equities are

not launched at an appropriate time to support pecking order theory.

6

Chirinko and Singha (2000) propose a critical analysis of these two strategies. They point that

both test pecking order test by financial deficit and tradeoff test by target adjustment - are

misleading because their results can be explained by other factors. One of them is credit

constraint (Leary and Roberts, 2010). Lemmon and Zender (2010) address the problem and

offer a new test for pecking order theory. They modify Shyam-Sunder and Myers test by

using a quadratic specification for financial deficit. Their point is that if firms are constrained

in issuing debts, they cannot borrow more after a certain amount. So the link between

financial deficit and debt variation must be important before this limit and marginally small

after. In this context, they estimate that it is easier for companies to finance a small financial

deficit than a big one because of limited debt capacity. They offer evidence in line with this

hypothesis documenting that quadratic specifications significantly improve inference for

credit constrained firms and have no effect for unconstrained ones.

B. HYPOTHESES

Following Shyam-Sunder and Myers (1999), we have been conducting an analysis with the

two previously described empirical strategies. Our purpose is to test which theory, pecking

order or trade-off, is a better first order explanation for firm’s capital structure choice

considering the firm’s debt constraints.

Our starting point is the classic pecking order test based on financial deficit. Previous studies

document mixed results about the link between debt variation and financial deficit. The initial

hypothesis of a perfect correlation fails to fit the facts. Coefficients of regression documented

in literature are always smaller than 1. These results show that firms partially finance their

financial deficit with new equities. Taking into account these facts, following Aktas et al.

(2011), we consider a less restrictive hypothesis than the initial test. We only expect a positive

correlation between the firms’ debt variations and their financial deficit (hypothesis 1).

According to Leary and Robert (2010) and Lemmon and Zender (2010), the poor performance

of classic pecking order test is attributed to the firms’ debt constraints. Two causes can

explain the constraints. First, as Myers (1977) points out, firms can have so many debts that

every increase in debt reduces the total market value of their debt. Because of more probable

distress and implied costs, potential lenders will charge a higher rate which makes debts as

expensive as equities. Firms have issued too many debts in the past and they have reached the

limit. Second, as point Stiglitz and Weiss (1981), lenders can ration debt because of

7

asymmetric information problems. Because of adverse selection problems or anticipated

moral hazard problems, debt suppliers limit their lending to firms for which it is hard to assess

real risk. In this context, even good firms, those with low real risks, can be constrained for

their debt issuance because lenders cannot distinguish them from bad firms, those with high

real risks. The Equities issues subscribed by the CEO (Leland and Pile, 1977) and collateral

(Bester, 1987) can be used to mitigate these difficulties. Considering that it could be hard for

firms to issue debts, we expect that the link between the firms’ debt variations and their

financial deficit will be more important for unconstrained firms than for constrained ones

(hypothesis 2).

Previous empirical research documents disturbing results in pecking order theory point of

view for both young rapidly growing firms and large mature ones. Young rapidly growing

firms rely mostly on equities to finance their financial deficit and large mature firms on debts

(Frank and Goyal, 2003). Two opposite explanations are given. Halov and Heider (2011)

argue that the classic interpretation of debt in pecking order theory is misleading. Because of

asymmetric information problems, debts can be mispriced and finally more costly than

equities. In this context, more opaque firms, such as young and rapidly growing ones, prefer

equities to debts and mature ones prefer debts to equities. Lemmon and Zender (2010)

attribute these counter intuitive results to the firms’ debt constraints. Young firms face an

important mortality rate and have few tangible assets to offer as a warranty to debt suppliers.

These firms have no way to distinguish themselves if they are less risky. In this context,

young firms can quickly reach their limit debt ratio. Mature firms do not have to deal with this

kind of problems. To cope with the firm’s debt constraints in the pecking order test, Lemmon

and Zender (2010) use the quadratic specification for the relationship between debt variation

and financial deficit. The idea is that for debt constrained firms, a big deficit must be harder to

finance than a small one. Following this approach, we expect that the use of an un-linear

specification for financial deficit improves the inference quality of classic pecking order

behavior for firms suffering from debt constraints (hypothesis 3).

Our second point is the test for trade off theory through target adjustment. We use a mean

reverting process to model firms’ behavior. As in Shyam-Sunder and Myer (1999) or in Frank

and Goyal (2003), we estimate the target with the historical mean of debt ratio. Trade off

theory predicts that firms issue or pay back debts to meet their optimal debt ratio. This latter

maximizes the firm’s value by taking into account distress costs, taxes reduction associated

8

with debts and reduction of agency costs. This behavior is not affected by debt constraint

because if firms cannot adjust their ratio through debt variation, they can do it by variation of

equities. Previous studies find evidence of positive correlations between debt variations and

mean reverting factor even if, as for financial deficit in the pecking order theory, this

correlation appears relatively small. Fischer et al. (1989) attribute this fact to the cost of

transactions associated with adjustments. According to these elements, we expect a positive

correlation between debt variation and the mean reverting factor of debt ratio (hypothesis 4).

This correlation will not be different for debts of constrained and unconstrained firms

(hypothesis 5).

As previously discussed, the question of which theory, pecking order or trade off theory, can

be a better explain the firm’s capital structure, have not been answered yet. One difficulty is

that they are not mutually exclusive (Graham and Leary, 2011). Results of joint tests, tests on

the firm’s debt variations, including both financial deficit and target adjustment, depend on

the sample selection and the period during which they are performed (Frank and Goyal,

2003). Even if robustness of conclusion can be discussed, some regularity has been

documented. For example Psillaki and Daskalis (2009) show that determinants of capital

structure do not differ across countries in which a civil law system is prominent. Their study

focuses on four European countries including France. This particular context seems to be

favorable for the pecking order behavior. Even if we focus on big quoted firms, less

developed equity markets than US ones and bank centered financial system, limit possibilities

to issue external equities. So financial deficit is expected to be a better first order determinant

of debt variations than target adjustment (hypothesis 6).

II. DATA AND METHODOLOGY

A. SAMPLE DESCRIPTION:

In order to conduct our investigation, we used a sample of 335 firms which were part of SBF

2503 at least once during the period 2001-2010. This choice has allowed us to work with a

sufficiently large number of firms which present differences in size and age and for which

information is easily available. Our data were extracted from both DIANE4 database, for

3 This index is composed by the 250 biggest market capitalizations trade in Paris stock exchange its base is

one thousand the 28th December 1990. 4 DIANE is edited by Bureau Van Dijk (92, rue de Richelieu 75002 PARIS)

9

accounting data, and Europe Daily5 database, for market ones. We did not consider

observations before Initial Public Offering (IPO) and after delisting. Mistakes and gaps in

data were either directly corrected with the information provided by alternative sources like

companies’ reports when it was possible or there were dropped when no data could be found.

Finally, we only kept the firms for which the financial statement for at least a two-year

consecutive twelve-month accounting period has available. From this preliminary database,

we computed the firms’ financial deficit, the net debt variation debt and the mean reversion of

financial leverage. Then we deleted the observations part of the 1st and the 99

th percentile of

these variables to solve the potential outlier problems. Table 1 offers details about our

sampling procedure and the main characteristics of the resulting sample. We have an

unbalanced panel with gaps. It includes 332 firms providing a total of 2,848 observations.

About 55% percent of these firms operate in the service sector, 16% in the finance sector and

15.5% in the industry sector.

In table 2, we present some descriptive statistics computed for our sample. Some points have

to be discussed before going further. First, we note an important heterogeneity between the

companies’ sizes and ages of the companies. We both have very old big firms and young

quoted small and medium-sized companies. The differences in total asset6 and market

capitalization are huge across the sample. Second, the proportion of tangible assets in total

assets is relatively low for the firms of our sample, a mean ratio of 5%. Two reasons explain

this low level: most of them belong to big groups with important long-term investments

and/or operate in the service sector. Third, the firms’ operating performance is also relatively

low with a mean return on assets (ROA) of -2.7% over the total period. About a third of the

observed, ROAs is negative. This proportion was more important after the beginning of the

financial crisis in 2007. Thirty-four percent of firms reported a negative operating income

after the crisis against 30% before. Fourth, statistics on total leverage and financial leverage

ratios indicate that total liabilities are composed on average for 47.9% of debts and 36.7% of

financial debts. These values are in line with 42% (without reprocessing) of the total leverage

documented by Molay (2005) over the first Paris market between 1995 and 2002. Aktas et al.

(2011), who worked on French very small businesses between 1998 and 2006, documented a

more important total leverage of 52% and a lower financial leverage of 20%. They attributed

5 Europe Daily is edited by EUROFIDAI and distributed by IODS (48, rue de Provence 75009 PARIS). 6 Every accounting data used in the study is reprocessed to provide a more informative content. We have

cancelled subscribed but not called stock, preliminary expenses, subscribed-called but not paid stock,

premium bonds. We have re-entered leasing and discounted bills.

10

the relatively high value of the total leverage to limited access to the primary equity market

and to the absence of the secondary market. Equities are mainly held by the owner’s family.

They explain the low financial leverage through credit rationing. The main external source of

debt for small firms is the trade credit offered by their suppliers. Fifth, in our sample, the

firm’s main source of debt is what we call other borrowing. It includes the partners’ current

accounts, the employee profit-sharing and so on. We qualify this form of debt as internal

debts. The second most important source of debt and the first external one are bank loans

which account for 25.2% of total debts. The second and third external source of debt is trade

credit, 18.2%. Bond issues are relatively small and only represent an average of 9.6% in total

debts. Most of the companies do not use the market debt. The median ratio of bond in debts is

0. Financial leasing is seldomly used. On average, this form of financing is inferior to 1%.

During the total period, less than half of our sample had had an ongoing contract.

B. METHODOLOGY:

In this subsection, we present our econometric models and briefly discus variables included in

the specifications. We provide summary statistics and synthetic definitions for those different

variables in table 2 and appendices 1 and 2. We test the hypothesis presented in section 2 on

our sample of 332 French quoted firms. Our methodology is inspired from the two step

procedure used by Lemmon and Zender (2010). In the first step, we build a proxy of debt

constraint and we use it to split our dataset in three groups using terciles. Then we have highly

constrained, moderately constrained and less constrained firms. In the second step, we run our

regressions inspired from Shyam-Sunder and Myer (1999) over the two extreme groups to

compare inference about our different specifications between the subsamples of the most and

least constrained firms.

In order to measure the debt constraint, we estimate the probability for a firm to issue public

debts as a function of its characteristics. Using this proxy, we follow the theoretical analysis

provided by Bolton and Freixas (2000). They show that the safest firms, those which can

borrow more easily because of their low probability of distress, prefer to issue public debt to

avoid cost of intermediation incurred with bank debt. Riskier firms borrow only from banks to

benefit from flexibility provided by these financial intermediaries. Holstrom and Tirole

(1997) reach the same conclusion. Lemmon and Zender (2010), following Almeida, Campello

and Weisbach (2004) and others, use the existence of a bond rating as proxy of public debt

use. We opt for a more direct measure. This choice is in line with Faulkender and Petersen

11

(2006) who asked whether the use of finance sources affected the capital structure choice. Our

method allows us to examine if access to bond market affects pecking order or target

adjustment behaviors. We use accounting data to infer if a firm has issued a new public debt

or not. We code a dummy variable whose value is 1 if the firm’s total outstanding public debt

increased between a period of two years and we use it as a dependent variable in a probit

regression over the firms’ characteristics. The explanatory variables are the firm’s size (ln

total assets), profitability (ROA), assets tangibility, leverage, age (ln age), risk (standard

deviation of stocks returns) and industry dummy variables (NAF2 Rev. 2 digit or big

sectors7). All variables are lagged for period 1. These variables are the same as those used by

Faulkender and Petersen (2006). Table 3 provides estimation results for three different

specifications in which we control or not for industrial sectors. We use predictions associate

with the first model to split our sample.

We performed the main tests over the entire sample, over the most constrained firms and the

least constrained firms. These tests are built on the same basis. We used regression to estimate

the variations of the net financial debt between two consecutive years over pecking order

and/or trade off factors. Contrary to other comparable studies, we opted for the net financial

debt which is computed by taking the total of the financial debts minus the firm’s treasury

assets. This choice allowed us to control the effect of the use of the treasury variations

required to the firm’s financial needs. All our estimations considered both the year and the

firm’s fixed-effects so that constant over time and over firm omitted variables were taken into

account.

To test hypothesis 1, we adopted the following econometric specification:

(1)

Where is the variation of net debts for the firm i over the t t-1 period, represents

the year fixed-effect, represents the firm’s fixed-effect and is the financial

deficit for the firm i over the t t-1. This last variable measures the needs for external funds.

We computed it as the sum of dividends paid plus the net investment expense plus the change

in working capital minus the operational cash flow after interests and taxes. Both variations of

net debts and financial deficit are standardized by total economic assets8 in t-1. We

extensively described the mechanism of this test in appendix 2. To test hypothesis 2, we run

7 Commerce, Construction, Finance, Real estate, Manufacturing, Service. 8 Net fixed assets plus working capital.

12

regression over subsamples of the most constrained or the least constrained firms and

compared . To test hypothesis 3, we introduced the square of in the regression

equation. A positive coefficient associated with the classic variable and a negative one

associated with the squared variable indicated that the debt variation increased with the

financial deficit up to a certain deficit level and after it increased more slowly.

To test hypothesis 4, in which we focus on the target adjustment process, we adopted the

following specifications:

(2)

Where is the target financial leverage ratio that we estimate by the average financial ratio

over the entire period of study and where is the financial leverage ratio in t-1,

represents the target adjustment factor. To test hypothesis 5, we run the regression

over the most constrainted and the least constrained firms and compared the results.

To test hypothesis 6, we adopted the following specifications:

(3)

We included both financial deficit and target adjustment factors in the regression equation.

This allowed us to compare pecking order and trade off theory as a first order explanation for

a firm’s variation when taking into account financial debts having an impact on debt

constraints.

In addition, in order to consider the potential effects of the debt constraint, we modified the

specifications.

(4)

We also added the squared of the financial deficit in the current equation.

III. RESULTS:

A. MAIN RESULTS:

Table 4 reports the results for the tests of our different hypotheses. In the first column, we

present the classic Shyam-Sunder and Myer (1999) test performed on variation of net debt for

13

the total sample. The coefficient associated with the financial deficit is 0.224. It is relatively

low but positive and significant, which is in line with our hypothesis 1. Previous studies

reported higher values but they did not correct for treasury variation. In the US context,

Shyam-Sunder and Myer (1999) documented a value of 0.79. Frank and Goyal (2003), who

performed the same test over a longer period in the US, globally documented 0.748, but only

0.33 after 1990. They concluded that pecking order had a decreasing explanatory power for

more recent years. Our results are close to them. For very small businesses in the French

context, Aktas et al. (2011) documented a coefficient of 0.79. This value was even more

important for the firms which had a positive deficit. We attribute the difference with our

findings mainly to difficulties that very small businesses encounter to issue equities compared

with quoted firms. A previous study, performed by Molay (2005) between 1995 and 2002,

documented a coefficient of 0.41 for quoted firms.

Relatively low values of pecking order adjustment, in our first regression, can be associated

with the firm’s debt constraints. Our estimates of the same model on sub-samples of the most

constrained and the least constrained firms are in line with this statement. We report a

coefficient of 0.112 with a relatively low adjusted R2 (0.191) for the first group and 0.383

with a higher adjusted R2 (0.420) for the second one. This difference is significant at the level

of 0.05. The value of the t of the Student, for the mean comparison test that we performed, is

2.296. This result is in agreement with the prediction formulated in hypothesis 2.

In the second column of the table, we use the Lemmon and Zender (2010) test for the entire

sample. The introduction of the squared financial deficit strongly improves the pecking order

adjustment. The coefficient associated with the linear specification is 0.224. In the un-linear

one, it is almost twice as high (0.411) and the coefficient associated with the squared term is

negative (-0.016) and significant. The adjusted R2 of the model also increased significantly. It

increased from 0.332 to 0.407. Even if difficulties to finance big deficits affect constrained

and unconstrained firms, the coefficient associated with the squared term is negative and

significant in both cases, for the most constrained firms, the un-linear transformation has an

more important impact on inference quality. The coefficient associated with the financial

deficit has almost tripled and the adjusted R2 has increased by a 7-point basis. For the least

constrained firms, the coefficient has only doubled and adjusted R2 has also increased also

about 7 basis points. This difference appears to be consistent with our hypothesis 3.

14

The test for our hypothesis 4 is presented in the third column of the table. The coefficient

associated with the target adjustment by mean reverting, 0.67, is positive and significant as

we expected. Its relatively low value, less than one, is generally attributed to the adjustment

cost. When we include this new factor in the previous regression equation, we document both

a lower coefficient for the target adjustment and for the financial deficit. The link between the

net debt variation and the new factor, which can be interpreted as the speed of adjustment to

optimal capital structure, is almost the same if we compare constrained and unconstrained

firms in both linear and un linear specifications of pecking order adjustment. The difference

between the coefficients for the two groups is not significantly different from 0. This report is

consistent with our hypothesis 5.

For our hypothesis 6, the most important one, we examine values of coefficients associated

with the financial deficit and target adjustment to determine which of pecking order theory or

trade off theory is the better first order explanation for a firm’s net debt variation. In the linear

specification regression, the target adjustment clearly appears to be the main factor with a

coefficient of 0.45 against 0.153 for the financial deficit in the total sample analysis. This

difference is even more important for the sub-sample of most constrained firms for which the

introduction of target adjustment makes the coefficient associated with the financial deficit is

not significantly different from 0. The results for least constrained firms are close to those

discussed on the total sample (0.421 against 0.232). In the un-linear specification regressions,

differences between pecking order and trade-off theory are not significant, and those on the

total sample as well as on each sub-sample. The introduction of a squared financial deficit,

aiming at controlling growing difficulties to deal with the biggest deficit, improve the

explanatory power of pecking order theory. This makes the question of which the theory

prevails. In each of our estimation, on sub-groups and on the total sample, we cannot tell

which theory prevails with any certainty. is not significantly different from in

quadratic context. So, we do not validate our last hypothesis.

B. ADDITIONAL RESULTS AND ROBUSTNESS CHECK TESTS:

In this section, we examine whether the results are robust for alternative measures of debt

constraints. We consider two categories of alternative ways to split the sample to distinguish

potentially most and less constraint firms. First, we consider the fact that firms issue or not

bonds instead of estimation then probability of doing it. Secondly, following Hadlock and

Pierce (2010) who recommended using the firms’ ages and sizes as proxies for financial

15

constraints, we split the sample on tercile for these two variables. Then, we oppose the

smallest firms in terms of total assets to the biggest ones in a first step, and the youngest ones

to oldest ones in a second step.

By computing the yearly firms’ probability to issue bonds with the view to assessing their

access to external financial debts, we consider both the firms that effectively follow this

framework and those whose characteristics allow them to do so bur do not. The procedure

gives us the possibility to work with more important groups of firms considered as debt

constrained or not. In table 5, we present alternative results associated with a more restrictive

approach to bond issues. We did not reproduce each test performed in table 4 but only the

most important ones. We provide new estimations for equations 1, 2 and 4. The first part of

the table presents the sample decomposition between the firms which issued bonds between

2001 and 2010 and those which did not. The second part presents the decomposition between

the firms that issued bonds at least once during the period of the study and those which did

not. Each time, we opposed the least debt-constrained firms to the most debt-constrained

ones. Results are globally consistent with conclusions provided by the analysis of the main

tests. The financial deficit and target adjustment factors are positive and significant. The

inclusion of a squared financial deficit in the regression improves the pecking order

adjustment for the most constrained firms but have no significant effect for the least

constrained ones. The financial deficit and target adjustment appear to have no significantly

different explanatory powers on variation of net financial debt for the least constrained firms

and for the most constrainted ones in un-linear specifications.

In the second robustness check tests, instead of focusing on the type of the debts firms issue in

order to assess their potential debt constraints, we used the firms’ sizes and ages to split our

sample. The smallest and the youngest firms are reputed to have a more limited access to

external finance than the biggest and oldest ones. As in the main tests, we compared extreme

terciles to document behavioral differences in terms of financial net debt variations. We

performed the same regressions as those in table 5. Estimation results are presented in table 6.

The sub-sample change slightly affects coefficients for pecking order and trade - off theory.

The conclusions about our different hypotheses are globally the same. If we want to explain a

firm’s capital structure evolution, we notice that the financial deficit and the target adjustment

are both positive and have significant factors. However, we cannot distinguish which one is a

better first order explanatory factor for the smallest and youngest firms, in the un-linear

specification. The only exception is for the biggest and oldest firms when we include a

16

squared financial deficit. We report a significant difference between the pecking order

adjustment and trade off theory. The first one appears to be more important than the second

one. In this particular context, the results we have found are consistent with our hypothesis 6.

Pecking order is a better first order determinant for big and old firms when you consider that

it is more difficult to finance a big financial deficit than a small one.

IV. CONCLUSION:

In this article, we have examined the question of whether pecking order or trade-off theory is

a better first order explanation for a firm’s capital structure choice. Previous tests, following

Shyam-Sunder and Myers (1999) methodology, produce mixt results (Frank and Goyal,

2003). These difficulties are attributed to the failure of tests based on financial deficit to

consider the impact of firms’ limited debt capacity (Leary and Roberts, 2010). Lemmon and

Zender (2010) provide a modified version of these tests of pecking order theory based on an

un-linear specification of the relationship between financial deficit and debt variation. In

doing so, they consider difficulties for debt-constrained firms to finance the biggest financial

deficits. We have adapted this framework to consider both pecking order and trade off theory

adjustment to firms’ behaviors. We have confronted the explanatory power of debt financial

deficit and target adjustment by taking into account the firms’ debt constraint problem using

an un-linear specification.

We have found evidence that both pecking order and trade off theory are relevant to explain

the firms’ debt variation. Considering the debt constraint problem through many proxies, we

have shown that the access to credit has a significant impact on the way that firms finance

their external needs of funds but has virtually no effect on speed in which they adjust their

capital structure. The tests performed on un-linear specifications of financial deficit clearly

show that it is more difficult for a firm to finance bigger deficits than smaller ones. This

phenomenon appears more important for firms identified as more likely to be debt-

constrained. In a linear context, a first set of tests showed that trade off theory better fits the

data than pecking order theory for debt-constrained firms whereas a second set of tests

demonstrated that pecking order theory better fits the data than trade off theory for

unconstrained ones. However, the introduction of un-linear specifications makes it hard to

distinguish which theory is a better first order explanation for the choice of the firms’ capital

structure.

17

This last result leaves the question unanswered. Other investigations have to be conducted to

reach a better understanding of the firms’ financial structure and debts. Alternative theories

have to be considered and evaluated relatively to pecking order and trade-off theories. Market

timing theory is one of those. It postulates that firms do not seek to reach an optimal capital

structure or do not seek to issue debts or equities to minimize their adverse selection

problems. Firms finance themselves according to the opportunities offered in the market

(Baker and Wurgler, 2002). Firms issue debts or equities when these financing means are

widely available at a good price. A much more recent study advocates a model of life patterns

in firmrs’financing choice (La Rocca et al. 2011). Firms start to rely on debts at the first stage

of their life-cycle and gradually, when they reach a more mature stage, substitute internal

capitals to debts. Kayhana and Titman (2007) provide evidences that the firms’ capital

structure depends on their history even if, over the long term, they tend to adjust their debts to

their target structure. Behavioral finance also investigates the field. Heaton (2002), Ayres de

Barros and Di Miceli da Silviera (2008) document that overconfident and optimistic managers

tend to use more often debts. The main difficulty to deal with these different theories of

capital structure is that they are not mutually exclusive. The problem is to find a hierarchy

between them and not to reject or accept one or another.

18

Bibliography:

· Aktas N., Bellettre I. and Cousin J.G., 2011, “Capital structure decision of French very

small businesses”, Finance, 32, 43-73.

· Ayeres D. de C. Barros and Di Miceli da Silvieira, 2008, “Overconfidence, managerial

optimism and the determinants of capital structure”, European Financial Management

Conference, Athen.

· Baker M. and Wurgler J., 2002, “Market timing and capital structure”, Journal of

Finance, 57, 1-30.

· Bester H., 1987, “The role of collateral in credit markets with imperfect information”,

European Economic Review, 31, 887-899.

· Bolton P. and Freixas X., 2000, “Equity, bonds and bank debt: capital structure and

financial market equilibrium under asymmetric information”, Journal of Political

Economy, 108, 324-351.

· Bradley M., Jarrell G. and E.H. Kim, 1984, “On the existence of an optimal capital

structure: theory and evidence”, Journal of Finance 39, 857-877.

· Brennan M.J. and Schwartz E., 1984, “Optimal financial policy and firm valuation”,

Journal of Finance 39, 593-607.

· Chirinko R.S. and Singha A.P., 2000, “Testing static tradeoff against pecking order

models of capital structure: a critical comment”, Journal of Financial Economics 58,

417-425.

· Fama E. and French K., 2005, “Financing decisions: Who issues stock?”, Journal of

Financial Economics, 76, 549-582.

· Fama E.F. and French K.R., 2001, “Disappearing dividends: changing firm

characteristics or lower propensity to par?”, Journal of Financial Economics, 60, 3-43.

· Fama E.F. and French K.R., 2002, “Testing the tradeoff and pecking order predictions

about dividends and debt”, Review of Financial Studies, 15, 1-33.

· Faulkender M. and Petersen M. A., 2006, “Does the source of capital affect capital

structure?”, Review of Financial Studies, 19, 45–79.

· Fischer E., Heinkel R. and Zechner J., 1989, “Dynamic capital structure choice: theory

and tests”, Journal of Finance 44, 19-40.

· Franck M. and Goyal V., 2007, “Trade off and pecking order theory of debt”, ed.

Eckbo E., Handbook of Corporate Finance: Empirical Corporate Finance, 1-82.

· Frank M. and Goyal V., 2003, “Testing the pecking order theory of capital structure”,

Journal of Financial Economics, 67, 217-248.

· Graham J. and Leary M., 2011, “A review of empirical capital structure research and

directions for the future”, Annual review of Finance, 3, 309-345.

· Hadlock C.J. and Pierce J.R., 2010, “New evidence on measuring financial

constraints: moving beyond the KZ index”, Review of Financial Studies, 213, 1909-

1940.

· Heaton J., 2002, “Managerial optimism and corporate finance”, Financial

Management, 31, 33-45.

19

· Halov N. and Heider F., 2005, “Capital structure, risk and asymmetric information”,

Quarterly Journal of Finance, 1, 767-809.

· Holstrom B. and Tirole J., 1997, “Financial intermadiation, loanable funds, and real

sector”, Quarterly Journal of Economics, 112, 663-691.

· Hovakimian A., Opler T. and Titman, 2001, “The debt-equity choice”, Journal of

Financial and Quantitative Analysis, 36, 1-24.

· Jalilvand A. and Harris R.S., 1984, “Corporate behavior in adjusting to capital

structure and dividend targets: an econometric study”, Journal of Finance, 39, 127-

145.

· Kane A., Marcus A.J. and McDonald R.L., 1984, “How big is the tax advantage to

debt?”, Journal of Finance 39, 841-853.

· Kayhan A. and Titman S., 2007, “Firms’ histories and their capital structures”, Journal

of Financial Economics, 83, 1-32.

· Kotrajczyk R.A. and Levy A., 2003, “Capital structure choice: macroeconomic

conditions and financial constraints”, Journal of Financial Economics, 68, 75-109.

· La Rocca M., La Rocca T. and Cariola A., 2011, “Capital structure decisions during a

firm’s life cycle”, Small Business Economics, 37, 107-130.

· Leland H. and Pile D., 1977, “Informational asymmetries, financial structure, and

financial intermediation”, Journal of Finance, 32, 371-387.

· Lemmon M.L. and Zender J. F., 2010, “Debt capacity and tests of capital structure

theories”, Journal of Financial and Quantitative Analysis 45, 1161-1187.

· Marsh P., 1982; “The choice between equity and debt: an empirical study”, Journal of

Finance, 37, 121-144.

· Modigliani F. and Miller M. H., 1958, “The cost of capital, corporate finance and the

theory of investment”, American Economic Review 48, 261-297.

· Modigliani F. and Miller M.H., 1963, “Corporate income taxes and the cost of capital:

A correction”, American Economic Review 53, 433-443.

· Molay E., 2005, “La structure financière du capital: tests empirique sur le marché

français”, Finance, Contrôle, Stratégie, 8, 153-175.

· Myers S.C. and Majluf N.S., 1984, “Corporate financing and investment decision

when firms have information that investors do not have”, Journal of Financial

Economics 13, 187-221.

· Myers S.C., 1977, “Determinants of corporate borrowing”, Journal of Financial

Economics, 5, 145-175.

· Myers S.C., 1984, “The capital structure puzzle”, Journal of Finance 39, 575-592.

· Myers S.C., 2003, “Financing of corporations”, in G. Constantinides, M. Harris and

Stulz R. (eds.) Handbook of Economics of Finance: Corporate Finance (Elsevier

North Holland).

· Psillaki M. and Daskalis N., 2009, “Are the determinants of capital structure country

or firm specific?”, Small Business Economics, 33, 319-333.

· Shyam-Sunder L. and Myers S.C., 1999, “Testing static tradeoff against pecking order

models of capital structure”, Journal of Financial Economics 51, 219-244.

20

· Stiglitz J.E. and Weiss A., 1981, “Credit rationing in markets with imperfect

information”, American Economic Review, 71, 393-410.

· Stiglitz J.E., 1973, “Taxation, corporate financial policy and the cost of capital”,

Journal of Public Economics 2, 784-793.

· Taggart R.A., 1977, “A model of corporate financing decisions”, Journal of Finance,

32, 1467-1484.

· Wanzenried G., 2006, “Capital structure dynamics in the UK and continental Europe”,

European Journal of Finance, 12, 693-716.

21

Table 1: Sample description

Panel A: selection criteria

Panel B: panel composition

Years 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 Total

Observations 279 270 267 252 277 286 297 314 302 304 2,848

Panel C: The firms’ sectors and observations

Number of

Firms

Frequency Number of

Observations

Frequency

Trade 30 9.04 263 9.23

Building 6 1.81 48 1.69

Finance 53 15.96 471 16.54

Real-estate 9 2.71 66 2.32

Industry 52 15.66 473 16.61

Service 182 54.82 1 527 53.62

332 100.00 2 848 100.00

Selection criteria Number

of firms

Number of

observations

1 We started with firms which were in SBF250 at least once

during the period 2001-2010. 335 3,350

2 We dropped observations which existed before the first year

of the quotation. 335 3,124

3 We also dropped observations which were made after

delisting. 335 3,115

4 We only kept observations corresponding to a twelve-month

accounting period. 335 3, 086

5 Taking into account the first four criteria, we only kept firms

for which at least two fiscal years were available. 335 3,077

6 Then, we dropped observations for which two consecutive

year-accounting data were not available. 332 3,045

7 We dropped the observations in the 1st and 99

th percentile of

the financial deficit, the net debt variation and the target

adjustment factors to solve potential outliers.

332 2,848

22

Table 2: Descriptive statistics

Mean Standard

deviation

Median Minimum Maximum

Accounting data

Total assets (in thousand Euros)

10 200 000 23 300 000 1 800 000 7 521 139 000 000

Asset tangibility 0.054 0.133 0.008 0.000 0.810

ROA -0.027 0.751 0.0006 -0.539 0.241

Total leverage 0.479 0.208 0.481 0.000 0.856

Financial leverage 0.367 0.186 0.385 0.000 0.777

Market data

Market capitalization (in thousand Euros)

3 200 000 11 200 000 148 000 2 390 60 500 000

Market to book ratio 5.143 78.976 1.740 -0.803 22.835

Stand. Dev. of returns 0.032 0.040 0.024 0.009 0.168

Other data

Age 44.30 33.66 35 2 177

Debt structure data (ratio of total debts)

Bond 0.096 0.216 0.000 0.000 0.895

Bank debt 0.252 0.284 0.134 0.000 0.958

Trade credit 0.182 0.221 0.087 0.000 0.875

Other debt 0.456 0.294 0.399 0.006 0.999

Leasing 0.009 0.056 0.000 0.000 0.265

Evolution variables

Net debt variation 0.053 0.451 0.002 -2.303 4.856

Financial deficit 0.135 0.773 0.001 -3.159 7.311

Target adjustment 0.060 0.267 0.024 -0.850 2.524

23

Table 3: Estimations of debt constraints

This table presents estimations for the probit model of debt constraint for different models.

The dependent variable is an indicator equal to 1 if the firm issues bonds during the year. The

independent variable includes the natural log of total assets, return on assets (ROA). We use

the following elements : the fraction of total assets invested in property, plants and equipment

(tangible assets), the market to book ratio, the firm’s leverage (financial debt over total

assets), the natural log of the firm’s age, the standard deviation of its stock return over the

year. Model 1 does not include industry indicators. Model 2 and 3 include industry indicators

which take into account two different classifications, the NAF2 rev 2 digits and a reduce one

including only six big sectors.

Dependent variable is 1 if the firm has issued

quoted debt during the year

Variables Model 1 Model 2 Model 3

Constant -5.890***

(0.333)

-5.569***

(0.489)

-5.653***

(0.351)

Ln(Total Assets) 0.240***

(0.017)

0.253***

(0.021)

0.232***

(0.018)

ROA -0.113***

(0.029)

-0.109***

(0.034)

-0.107***

(0.030)

Tangible asset

-0.517*

(0.2767)

-0.517

(0.456)

-0.523*

(0.320)

Market to Book ratio

-0.002

(0.001)

-0.003

(0.002)

-0.002

(0.001)

Leverage 0.962***

(0.159)

1.023***

(0.181)

0.939***

(0.162)

Ln(Firm Age)

-0.119***

(0.044)

-0.167***

(0.049)

-0.110***

(0.044)

Standard deviation of stock returns

2.456***

(0.588)

2.785***

(0.639)

2.615***

(0.614)

Industrial Indicators

no

yes

NAF2digit2

yes

6 big sectors

Number 2 947 2 337 2 647

Pseudo R2 17.09 17.67 17.73 * indicates significance at the 0.1 level, ** indicates significance at the 0.05 level, *** indicates significance at the 0.01 level.

24

Table 4: Pecking order test vs. target adjustment test

This table presents regression estimations by the MCO for different models. The dependent variable is the variation of net debts (financial debt

minus treasury assets). Model 1 follows the classic Shyam-Sunder and Myers (1999) test specification including only the annual firm’s financial

deficit as independent variables. Model 2 adds the squared financial deficit to model 1. Model 3 only includes the target adjustment factor. Model

4 includes both the financial deficit and the target adjustment factors. Finally, in model 5, we add the squared financial deficit to the

specifications of model 3. All the variables are scaled by the economic assets of the firm in t-1. Estimations are conducted for the total sample

and for sub-samples of the most and the least constrained firms. We estimate the probability of issuing bonds, respectively through the first and

the last tercile, in the first regression presented in table 3. We report both coefficient estimates and White’s robust standard deviation which are

put in brackets.

All firms Most constrained firms Least constrained firms

(1) (2) (3) (4) (5) (1) (2) (3) (4) (1) (2) (3) (4)

Constant 0.411*

(0.211)

0.325*

(0.168)

0.521*

(0.268)

0.443*

(0.229)

0.365

(0.189)

-0.060

(0.096)

-0.126

(0.111)

-0.021

(0.098)

-0.090

(0.142)

0.054**

(0.026)

0.064

(0.025)

0.022

(0.025)

0.031

(0.025)

Financial Deficit 0.224***

(0.060)

0.411***

(0.036)

0.153***

(0.058)

0.323***

(0.040)

0.112***

(0.054)

0.318***

(0.056)

0.068

(0.055)

0.267***

(0.032)

0.383***

(0.064)

0.604***

(0.077)

0.232***

(0.075)

0.454***

(0.079)

Squared

Financial Deficit

-0.016***

(0.002)

-0.013***

(0.002)

-0.013***

(0.002)

-0.012***

(0.001)

-0.084**

(0.037)

-0.086***

(0.031)

Target

adjustment

0.670***

(0.057)

0.450***

(0.067)

0.355***

(0.057)

0.428***

(0.170)

0.342***

(0.080)

0.421***

(0.084)

0.431***

(0.083)

Dummy years yes yes yes yes yes yes yes yes yes yes yes yes yes

Dummy firms yes yes yes yes yes yes yes yes yes yes yes yes yes

Adjusted R2 0.332 0.407 0.329 0.396 0.444 0.191 0.261 0.222 0.280 0.420 0.495 0.494 0.573

Number of

observations 2587 2587 2587 2587 2587 808 808 808 808 930 930 930 930

* indicates significance at the 0.1 level, ** indicates significance at the 0.05 level, *** indicates significance at the 0.01 level.

25

Table 5: Pecking order test for the sub-sample of bond issuers and not bond issuers

This table presents estimation of model 1, 2, 4 and focus on firms that issued bonds between 2001 and 2010, those which did not; those which

issued bonds at least once during the period of the study and those which did not. Variables and estimation methods are the same as in table 4.

We report both estimated coefficients estimated and White’s robust standard deviation which are reported in brackets.

Bond issuers Not bond issuers At least one-time bond issuer Never bond issuer

(1) (2) (4) (1) (2) (4) (1) (2) (4) (1) (2) (4)

Constant

Variables

0.113*

(0.068)

0.081

(0.078)

0.085

(0.086)

0.408***

(0.115)

0.443***

(0.110)

0.365***

(0.106)

0.064

(0.078)

0.042

(0.075)

0.045

(0.075)

0.416*

(0.216)

0.450***

(0.122)

0.365***

(0.117)

Financial

Deficit

0.380***

(0.146)

0.308**

(0.135)

0.387***

(0.150)

0.222***

(0.009)

0.151***

(0.010)

0.324***

(0.016)

0.457***

(0.021)

0.342***

(0.024)

0.369***

(0.031)

0.203***

(0.060)

0.137***

(0.011)

0.313***

(0.019)

Squared

Financial

Deficit

-0.102

(0.208)

-0.013***

(0.001)

-0.021

(0.016)

-0.012***

(0.001)

Target

Adjustment

0.287***

(0.093)

0.285***

(0.090)

0.458***

(0.032)

0.358***

(0.031)

0.309***

(0.034)

0.315***

(0.035)

0.476***

(0.042)

0.374***

(0.041)

Dummy Years yes yes yes yes Yes yes yes yes yes yes yes yes

Dummy Firms yes yes yes yes Yes yes yes yes yes yes yes yes

Adjusted R2 0.788 0.822 0.529 0.327 0.388 0.437 0.366 0.419 0.420 0.344 0.398 0.447

Number. of

observations 197 197 197 2390 2390 2390 967 967 967 1620 1620 1620

* indicates significance at the 0.1 level; ** indicates significance at the 0.05 level, *** indicates significance at the 0.01 level

26

Table 6: Pecking order test for subsamples (small-big / young- old firms)

This table presents estimations of model 1, 2 and 4 for four subsamples of observations: the smallest firms, those which are part of the first tercile

of the firms’ total assets, the biggest ones, those which are part of the last tercile of the firms’ total assets, the youngest ones, those which are part

of the first tercile of age, and the oldest ones, those which are part of the last tercile of age. Variables and estimation methods are the same as in

table 4. As previously, we report both coefficient estimates and White’s robust standard deviations which are put in brackets.

The smallest Firms The biggest Firms The youngest Firms The oldest Firms

(1) (3) (4) (1) (3) (4) (1) (3) (4) (1) (3) (4)

Constant Variables -0.039

(0.093)

0.001

(0.095)

-0.044

(0.102)

0.151*

(0.091)

0.171

(0.106)

0.119

(0.086)

0.525**

(0.232)

0.535**

(0.246)

0.438**

(0.201)

0.017

(0.024)

0.002

(0.026)

0.016

(0.026)

Financial Deficit 0.133***

(0.055)

0.091*

(0.056)

0.233***

(0.058)

0.401***

(0.061)

0.282***

(0.073)

0.504***

(0.064)

0.165**

(0.066)

0.114*

(0.066)

0.314***

(0.068)

0.381***

(0.087)

0.287***

(0.113)

0.469***

(0.092)

Squared Financial

Deficit

-0.008***

(0.003)

-0.087***

(0.033)

-0.012***

(0.003)

-0.081*

(0.043)

Target Adjustment

0.415***

(0.127)

0.360***

(0.128)

0.327***

(0.078)

0.358***

(0.071)

0.424***

(0.123)

0.307***

(0.112)

0.325**

(0.160)

0.359**

(0.154)

Dummy Years yes yes yes yes Yes yes yes yes yes yes yes yes

Dummy Firms yes yes yes yes Yes yes yes yes yes yes yes yes

Adjusted R2 0.257 0.296 0.325 0.442 0.484 0.577 0.368 0.406 0.458 0.257 0.294 0.341

Number of

observations 787 787 787 928 928 928 747 747 747 911 911 911

* indicates significance at the 0.1 level, ** indicates significance at the 0.05 level, *** indicates significance at the 0.01 level.

27

Appendix 1: Variables definition

Variable Description

Debt variation

Debt used to finance financial deficit

Debt [n] – Debt [n-1]

Debt is equal to bond issue + loan from credit

Institution + other financial debt – current bank

overdraft + lease purchase commitments

Financial Deficit

The amount that the firm has to finance computed as

follows:

Dividend + net investment that includes new leasing +

change in working capital – cash flow after interest

and taxes

Squared Financial Deficit

Squared Financial Deficit

Mean reverting The difference between the mean of leverage over the

total period minus leverage in t-1

Quoted Debt

Dummy variable equal to 1 when the firm has quoted

outstanding debt during the measurement

Ln(Total Assets)

Logarithm of net total assets

ROA

Ratio net earnings over total net assets

Asset tangibility

Ratio net value of tangible assets over total net assets

Market to Book

Ratio market value of equities over their accounting

value

Leverage

Ratio total debts over total assets

Ln(Firm Age)

Logarithm of the firm’s age

Standard deviation of stock returns

Standard deviation of daily stock returns (bought and

held)

28

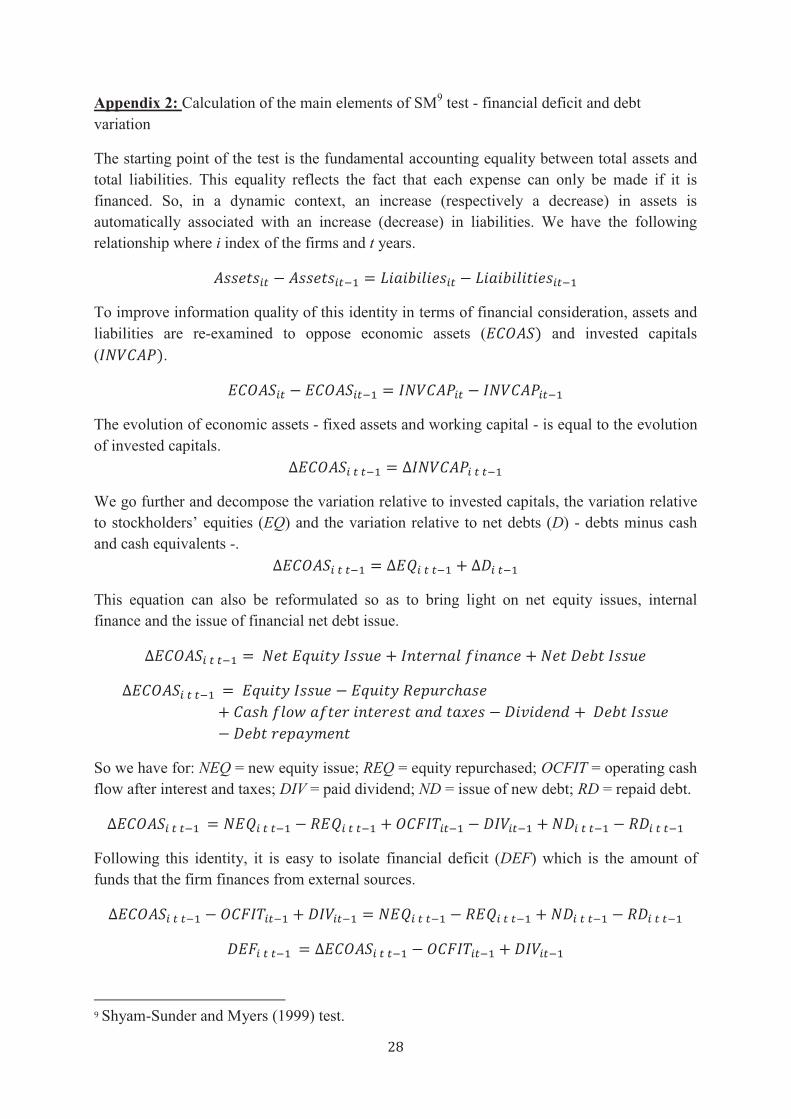

Appendix 2: Calculation of the main elements of SM9 test - financial deficit and debt

variation

The starting point of the test is the fundamental accounting equality between total assets and

total liabilities. This equality reflects the fact that each expense can only be made if it is

financed. So, in a dynamic context, an increase (respectively a decrease) in assets is

automatically associated with an increase (decrease) in liabilities. We have the following

relationship where i index of the firms and t years.

To improve information quality of this identity in terms of financial consideration, assets and

liabilities are re-examined to oppose economic assets ( and invested capitals

( .

The evolution of economic assets - fixed assets and working capital - is equal to the evolution

of invested capitals.

We go further and decompose the variation relative to invested capitals, the variation relative

to stockholders’ equities (EQ) and the variation relative to net debts (D) - debts minus cash

and cash equivalents -.

This equation can also be reformulated so as to bring light on net equity issues, internal

finance and the issue of financial net debt issue.

So we have for: NEQ = new equity issue; REQ = equity repurchased; OCFIT = operating cash

flow after interest and taxes; DIV = paid dividend; ND = issue of new debt; RD = repaid debt.

Following this identity, it is easy to isolate financial deficit (DEF) which is the amount of

funds that the firm finances from external sources.

9 Shyam-Sunder and Myers (1999) test.

29

By dividing the above expression by economic assets in t-1 (ECOASi t-1), we can isolate

change in net debts and its relationship to the financial deficit.

We go back to our previous notation to consider global accounting information. Financial

deficit is fulfilling with change in net debt ratio and the difference between changes in equity

ratio and profit. This last point is specific the French context because accounting reports are

made before profit appropriation. Profit has to be neutralized to avoid double calculation of

internal finance.

When applying this equation, it is easy to see that the variation in leverage ratio from one year

to the next is necessarily explained by financial deficit and equity issuance.

In the pecking order context, as long as safe debts can be issued, firms never issue equities

because of the cost of asymmetric information. In order to verify this assertion, Shyam-

Sunder and Myers (1999) suggests regressing changes in leverage over financial deficit.

is the pecking order coefficient. It is expected that and . Debt variation

must be equal to the financial deficit if firms follow pecking order. Every positive financial

deficit is funded by issue of debts and every negative one allows firms to reduce their debts.

ITIS – Innovation, territoires et inclusion sociale

MDD – Mobilités et développement durable

RIO – Risque, information, organisation

DOBIM – Droit des obligations et activités bancaires et immobilières

THEMOS – Théorie, Modèles, Systèmes

Documents de travail récents

ü Joseph Hanna, «R&D rivalry and cooperation with spillovers cleanup costs: Industry organization

and welfare policy performances », [2013-03].

ü Naïké Lepoutre, « L’européanisation du contentieux des étrangers en situation irrégulière »,

[2013-04].

Romain Gosse, « L’exemple du principe d’intégration en droit de l’environnement », [2013-05].ü

Gabriela Condurache, « Européanisation par influence horizontale : l’exemple du statut des ü

agents publics », [2013-06].

Nadia Beddiar, « L’Européanisation par influence de règles incitatives, l’exemple du droit ü

pénitentiaire », [2013-07].

Aurélien Fortunato, « Les finalités de l’européanisation du droit – créer un modèle commun : ü

l’exemple des clauses restrictives de concurrence dans les contrats d’affaires », [2013-08].

Yves Mard et Ludovic Vigneron, « Does public/private status affect SMEs earnings management ü

practices ? A study on Franch case », [2013-09].

Joseph Hanna, « De la transposition des modèles alternatifs de l’économie dans la théorie pure ü

du commerce international », [2013-10].

Kirill Borissov, Joseph Hanna et Stéphane Lambrecht, « Heterogenous agents, public investment ü

and growth in an intertemporal voting equilibrium model », [2013-11].

Sylvain Petit, « Allers et retours entre théorie et empirique dans la literature du commerce ü

international: l’exemple du commerce intrabranche », [2013-12].

Responsable de l’édition des documents de travail de l’IDP : Sylvain Petit ([email protected])