Order to Cash Cycle: Best Practices and Industry...

4

Getting the OTC process right is the current focus of CFOs worldwide, says Soumen Mukerji Order to Cash Cycle: Best Practices and Industry Trends A diagnostic of process controls and adoption of relevant global practices to improve DSOs and the cost of collections is needed T he uncertainty and volatility in the global economy have had an irreversible impact on the process of preserving cash in corporate entities. While earlier it was common to hear people say ‘cash is king’; today, ‘cash is the entire royal family’! The process of cash generation has come under in- tense scrutiny in the credit-strapped economy. Now, there is a realisation that improving upstream and down- stream processes can indeed help in quicker collections, and improve working capital turns. The process of Order to Cash (OTC) which is the business process for receiving and processing customer sales is the cur- rent focus of CFOs. In a regime of tight credit controls and an uncertain economic recovery, the finance func- tion can ill-afford to be lax in its OTC processes. The need of the hour is a diagnostic of process controls and adoption of relevant global practices to improve the process output metric of lower day sales outstanding (DSO) and optimised cost of collections. Companies are taking several steps globally, to make this process more efficient and effective. A mismatch between perception and practice? In a recent survey conducted by PwC in India, CFOs rated the effi- ciency of their OTC cycle at 3.42, on an overall score of 5. But this is not borne out by the results of the BSE Top 100 companies. On investigation of the balance sheets of these companies we see ballooning working capital to sales ratios. Clearly, there is a mismatch be- tween how CFOs perceive their OTC operations (which CFOs in the PwC 4. Billing – generating invoices for orders captured based on actual shipment of goods or rendering services. 5. Collections – collecting payments against orders executed and billed to customers. Collections can happen through physical means (cheque or cash) or wire transfers via banking channels. 6. Refunds – refunding to customer any money wrongly received, either because of product-related issues (defects, returns, and claims among others), or due to cancella- tion of orders or excess payments received. 7. Deductions’ management – nego- tiating with the customers for short payments received and recovering or agreeing on the deficit. 8. Cash applications – applying col- lections received against specific survey said are performing at above- average efficiencies), and financial results of the BSE Top 100 companies which do not show lower day sales outstanding (DSO) and a consequent improvement in working capital. Key components of the OTC cycle The OTC in a typical organisation broadly comprises the following work streams: 1. Customer master set up – creating the master data base for all custom- ers that will permit any commercial transactions. Typically, the masters contain data such as, addresses, tax and statutory registrations, and credit limits, among others. 2. Order entry – capturing the order received from a customer for a specific product or service at a negotiated price, and terms. 3. Credit check – validating the credit- worthiness of the customer based on past transactions and open orders before permitting further order execution. ON THE JOB 14 CFOCONNECT August 2012

Transcript of Order to Cash Cycle: Best Practices and Industry...

Getting the OTC process right is the current focus of CFOs worldwide, says Soumen Mukerji

Order to Cash Cycle: Best Practices and

Industry trendsA diagnostic of process controls and adoption of relevant global practices to improve DSOs and the cost of collections is needed

the uncertainty and volatility in the global economy have had an irreversible impact on the process of preserving cash in corporate entities. While

earlier it was common to hear people say ‘cash is king’; today, ‘cash is the entire royal family’! The process of cash generation has come under in-tense scrutiny in the credit-strapped economy. Now, there is a realisation that improving upstream and down-stream processes can indeed help in quicker collections, and improve working capital turns. The process of Order to Cash (OTC) which is the business process for receiving and processing customer sales is the cur-rent focus of CFOs. In a regime of tight credit controls and an uncertain economic recovery, the finance func-tion can ill-afford to be lax in its OTC processes. The need of the hour is a diagnostic of process controls and adoption of relevant global practices to improve the process output metric of lower day sales outstanding (DSO) and optimised cost of collections. Companies are taking several steps globally, to make this process more efficient and effective.

a mismatch between perception and practice?

In a recent survey conducted by PwC in India, CFOs rated the effi-ciency of their OTC cycle at 3.42, on an overall score of 5. But this is not borne out by the results of the BSE Top 100 companies. On investigation of the balance sheets of these companies we see ballooning working capital to sales ratios. Clearly, there is a mismatch be-tween how CFOs perceive their OTC operations (which CFOs in the PwC

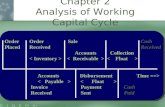

4. Billing – generating invoices for orders captured based on actual shipment of goods or rendering services.

5. Collections – collecting payments against orders executed and billed to customers. Collections can happen through physical means (cheque or cash) or wire transfers via banking channels.

6. Refunds – refunding to customer any money wrongly received, either because of product-related issues (defects, returns, and claims among others), or due to cancella-tion of orders or excess payments received.

7. Deductions’ management – nego-tiating with the customers for short payments received and recovering or agreeing on the deficit.

8. Cash applications – applying col-lections received against specific

survey said are performing at above-average efficiencies), and financial results of the BSE Top 100 companies which do not show lower day sales outstanding (DSO) and a consequent improvement in working capital.

key components of the OTC cycle

The OTC in a typical organisation broadly comprises the following work streams:1. Customer master set up – creating

the master data base for all custom-ers that will permit any commercial transactions. Typically, the masters contain data such as, addresses, tax and statutory registrations, and credit limits, among others.

2. Order entry – capturing the order received from a customer for a specific product or service at a negotiated price, and terms.

3. Credit check – validating the credit-worthiness of the customer based on past transactions and open orders before permitting further order execution.

on ThE Job

14 cFoConnECT august 2012

Use ‘Denied Party Lists’ based on publicly available and specially subscribed databases such as Dun & Bradstreet or CRISIL for credit ratings of new customers

by using a duplicate audit tool at the time of data capture.

l Ensure the parent-child relation-ship mapping for every new cus-tomer so that credit checks can be correctly applied.

l Have in-built logic defined to auto-capture inconsistencies in data en-try, for example, the PAN number is always a 10-digit alpha numeric entry and anything otherwise is immediately flagged.

l Set up central mailing addresses (email or physical mail) to handle all requests for master changes with clear definitions of what constitutes a priority request and needs accel-erated handling.

l Use ‘Denied Party Lists’ (DPL) based on publicly available and specially subscribed databases such as Dun & Bradstreet (D&B) or CRISIL for credit ratings of new customers before a decision is made to accept the requests. Very often this may require an organisation-level decision to define the param-eters for rejection. The DPL needs regular monitoring and updates to keep it contemporary.

l Establish robust quality check pro-cesses for data-entry accuracy and timeliness of response. Order entry - The transactional

cycle of OTC kicks off with the capture of a customer order. Entering the right order in the system will ensure that the downstream processes of billing and collections are handled efficiently. Typically, the process of

order entry starts with the receipt of a Purchase Order (PO) from a customer specifying the quantity of goods and services required and the agreed price and terms. If there are existing contracts with the customer, the T&Cs and prices are often defined within them and additional checks may not be necessary. However, for first-time customers or for those with no con-tracts, the sales team should certify the orders before the finance function captures them in its systems. Some best practices around these processes include the following:l Have a pre-defined escalation and

rejection policy to handle incom-plete or inconsistent orders. In some cases, this may require having access to customer organisations for quick resolutions.

l Availability of customer contracts in an easily accessible database for reference to key terms and prices for validation.

l Have standard processes defined for prioritisation of orders using logic of (a) customer priority, (b) product availability, (c) economic situations, if any, (d) credit history, and (e) shipment schedules.

l Availability of data on shipments to close the loop on the order-entry process, and formally close an open order.

l Robust quality control processes to track accuracy and timely action on orders. Measurement parameters around ageing of open orders and resolution of disputes.

l Well-defined process for cancella-tion of orders with levels of approv-als and notifications to sales’ teams.Credit check – Having a robust

credit check mechanism is a primary controls requirement to ensure that organisations do not run up bad debts. Most global organisations implement meticulous procedures to check the credit worthiness of customers before any order is booked. A key enterprise-level control that needs to be in place for an effective OTC process is to en-sure that no orders get executed with-out a credit check and order release. There have been countless examples of debt write-off cases where this basic control has been compromised.

invoices, to knock off the outstand-ing in the ledger. This is the final accounting of collections to reduce debts in the books.For most large global organisa-

tions, the best-in-class transformation of processes has already begun with consolidation in a shared services en-vironment. This article explores a mul-titude of other best practices that are helping to transform OTC processes worldwide, and which therefore, need to be in focus for finance organisations to have better controls and improved fiscal performance.

a CFO’s definition of the best-in-class OTCl DSOs well within the planned tar-

get and optimally balanced with Days Payables Outstanding (DPO), to have the least working capital needs.

l Cost of collections at less than 0.03 per cent of the value of collections, tracked, and measured regularly.

l Deductions as a per cent of collec-tions are less than 2 per cent, and 95 per cent of deductions and disputes are resolved within five days from receipt of collections.

l 95 per cent of collections in elec-tronic form with auto applications to invoices based on remittance advice and in-built system logic.

l All manual collections applied to invoices within two days with over 99 per cent accuracy.

l Invoices are generated on time and accurately in 99 per cent cases with least manual interventions.

l Customer satisfaction survey (C-SAT) scores of over 90 per cent on efficiency of dealing with the OTC processes.

Strategies for achieving best-in-class in key OTC processes

Customer master set up - A robust customer master is a first precondition for an effective OTC process. Master data management goes a long way in determining the accuracy of billing and reduction of disputes. Leading organisations try to adopt some world class controls in their master setup such as the following:l Avoid setting up duplicate records

on ThE Job

august 2012 cFoConnECT 15

Some best practices in credit control that merit attention are the following: l Define organisation-level credit

policies with focus on elements such as (a) maximum exposure limits for customers using segmen-tation analytics and credit history records, (b) credit limit override exceptions and approvals’ poli-cies, and (c) credit limit revisions’ process.

l Establish a process for real-time check and update of unpaid in-voices and unapplied collections before performing credit checks. Very often the process excludes unapplied collections and hence, incorrectly rejects valid orders.

l There may be a case for setting up a value tolerance limit for credit checks. Depending upon an organ-isation’s risk appetite, some orders from trusted customers, upto a value threshold may be allowed to be processed without the credit check; subject to an overall value limit exposure at an Account or Group level. This will help optimise the cost of controls vs benefits.

l Establish a process for regular re-view of credit history of customers based on a cycle of priority. Use of external databases such as Dun & Bradstreet and internal financial records of payments will be a key influencer for the credit history review.Billing – the financial impact of

the OTC cycle commences with the generation of an invoice, which signi-fies the creation of debt in the books of accounts, on account of execution of orders. Billing tends to be a trans-action-intensive process with multiple checks and controls. Finance teams tend to invest a lot of time and effort to ensure that the bills are generated on time and accurately and there have been scores of best practices to make this process world class, such as the following: l Automation of billing process based

on order entry and credit check in a fully integrated ERP system – many telecom companies have deployed customised billing platforms to make this process fully automated. Electronic billing using customised

or ready-to-use billing software is a step change in the process expedit-ing the time and lowering costs.

l For milestone-based billings, hav-ing ready access to all back-up documents justifying the milestone is an important process improve-ment. This requires project and bill-ing teams to be well synchronised and many companies have invested in workflow solutions to automate this interface.

l Wherever invoices need to be sent to customers, many companies have come out of the manual pro-cess of physical mailing to (a) email, (b) e-fax, or (c) electronic invoicing presentation and payment (EIPP). Under EIPP, the invoices are up-loaded directly into the customer’s portal and using an algorithm-based logic, are flipped back to the PO to expedite payment. In a variant of this process, XML files can be exported from the billing software for direct interface, to the Customers’ Payables software us-ing a gateway validation. Globally many organisations are realising the potential for invoice exchange which cuts down processing costs and payment cycles many times.

l Billing process often interfaces with multiple sub-processes such as or-der entry, delivery, and customer master. This needs the process to be well monitored and with rigid quality control checks focussing on accuracy, first pass yield, timeli-ness, and rejects analysis.Collections – As a standalone

process, collection is perhaps most exploited for best practices. In many

industries such as credit cards, compa-nies specifically handle collections and have built an ecosystem of practices and processes. The use of statistical tools and analytics is a significant best practice that has revolutionised the efficacy of the collections’ process. Others worth noting are the following:l Educating the sales team on the

importance of timely collections and impact on financials often goes a long way in reducing the cash collection cycle. A suitable incen-tive plan that has adequate weights for the accounts receivable (AR) balance is also an acclaimed best practice.

l Business to Business (B2B) and Business to Customer (B2C) col-lections have very different char-acteristics and need different sets of rules and focus. While B2C collections is rules-driven and often a repetitive process, B2B col-lections require a different skill set of collection agents and is often a personalised task.

l Using Dunning letters as a tool for reminder for payments is time tested. However, indiscriminate use of the Dunning letters runs the risk of antagonising customers.

l Companies use advanced statistical modelling to identify customer be-haviour patterns and propensity to default. Use of analytics solutions can optimise the cost of collections and channel focus on those clients who require follow-up action. There are several tools in the mar-ket that specialise in AR analytics and segmentation using a variety of tools and statistical methods.

l Organising teams in a collections’ process requires training in voice skills and soft skills such as in-fluencing and persistence. Setting targets for collection agents, regular monitoring of achievements and an incentive scheme often help in per-formance management and gradual improvement.

l For voice-based calling processes for collections, an automated dialler system is used by organisations to increase calling effectiveness and team utilisations.

l Setting tolerance limits for low-

Organising teams in a collections’ process requires training in voice skills and soft skills such as influencing and persistence

on ThE Job

16 cFoConnECT august 2012

value collections and empowering agents for negotiated settlements, subject to limits, is another best practice that organisations adopt to optimise the cost of collections.

l For processes with credit card col-lections, awareness of Processing Card Industry (PCI) security stan-dards and checks and balances to prevent credit card-related fraud is a must-have control.Refunds – This is often an under-

emphasised process in the OTC cycle that leads to customer noise and col-lection challenges. The origin of a refunds’ claim often leads to future deductions from subsequent pay-ments and a disputed client account. Some best practices around refunds include the following: l Centralised function for handling

all refunds’ claims. Very often refunds do not get attention from collection agents and hence having a central function often helps in expediting claims’ processing.

l Having a workflow solution inte-grated with collections and bill-ing is an automation investment that goes a long way in easing the process-related approvals for re-funds. Typically, a refunds’ claim goes through a defined multi-level approval based on the value. The workflow automates this process and helps speed up the disposal of claims.

l Handling a refunds’ process re-quires a specialised skill set to front-end customer claims with professionalism. Thus many or-ganisations provide training to staff to help them cope with customer interactions with financial respon-sibility.Deductions’ management – The

reverse of refunds is managing de-ductions made by customers where the short payments need to be under-stood and recovered, and accounted. The process of handling deductions requires a skill and finesse to negoti-ate with the customers and influence a recovery process. Some best practices are the following:l Having a workflow solution linked

to the collections’ process that routes all cases of deductions to

The final milestone in the OTC cycle is to apply collections to specific invoices in the AR sub-ledger. This completes the accounting cycle of knocking off debtors

a separate work flow and tracks it separately through a dedicated team. This allows visibility to such cases and can be measured for time-liness of disposal and ageing. The workflow can also be leveraged for subsequent follow-ups with cus-tomers. The need for an integrated end-to-end workflow solution for the OTC process linking billing, collection, refund, deduction, and cash applications is evident and the market offers solutions to meet this need.

l Sometimes a deduction is in the na-ture of an early payment discount that has been negotiated by the sales’ team without keeping the fi-nance team informed. In ideal situ-ations, such discount arrangements should be a part of the contract with the customer and updated in the master, so that handling deductions on the account becomes easy and control checked. Cash applications - The final

milestone in the OTC cycle is to ap-ply collections to specific invoices in the AR sub-ledger. This completes the accounting cycle of knocking off debtors. The cash applications’ process has undergone a metamorphosis in recent times with the introduction of IT solutions that ‘read’ the remittance advices in bank systems and apply logic to update the AR sub-ledger in the company’s systems. With the pro-liferation of electronic billing and net banking, many organisations in utility industries are adopting automation solutions for cash applications from

their B2C clients.While automation has made this

process less effort-intensive, some best practices that organisations adopt are the following:l Regular reconciliation of bank

statements with the customer led-ger to ensure that book-keeping controls are not compromised. As a best practice cash applications’ agents are not supposed to perform bank reconciliations in the interest of segregation of duties.

l Focussing on unapplied cash as a key metric and having finite tar-gets (for example, unapplied cash as a per cent of collections) often helps to improve process efficien-cies. Analysis of any cash lying in ‘suspense’ with specific follow up through a workflow solution is an acknowledged best practice.

l Institutionalising a robust quality control process for cash applica-tions is an essential control mecha-nism. This is particularly important as this process has a direct interface with financial statements and impacts the upstream function of collections’ efficiencies.

Conclusion The post-recession world will

demand a new economic order based on fiscal prudence and world class processes. In the struggle for the sur-vival of the fittest, organisations will need to step up and build and modify their internal processes to support competitiveness in an increasingly combative market. The OTC process is at the heart of corporate economic resurgence. Getting it right the first time, will be a demand on the CFO’s organisation and will need strategic planning and investment in automa-tion solutions. Lean and efficient OTC models have become not just a neces-sity, but an indispensible requirement. Realising this reality and living up to this challenge will differentiate the leaders from the laggards in effective

finance functions.

The author is Soumen Mukerji, Associate Director, Consulting, PricewaterhouseCoopers Private Limited

on ThE Job

august 2012 cFoConnECT 17

![Order to Cash Flow Cycle in Order Management [ID 985504.1]](https://static.fdocuments.us/doc/165x107/55cf9d7b550346d033adce1d/order-to-cash-flow-cycle-in-order-management-id-9855041.jpg)