Online Retailing Conference 2009

42

eCommerce Europe 2009: Outlook for eCommerce and Online Retail Victoria Bracewell Lewis Senior Analyst Forrester Research 20 January 2009

-

Upload

carine-moitier -

Category

Business

-

view

852 -

download

0

Transcript of Online Retailing Conference 2009

eCommerce Europe 2009: Outlook for eCommerce and Online Retail

Victoria Bracewell LewisSenior AnalystForrester Research20 January 2009

3 Entire contents © 2008 Forrester Research, Inc. All rights reserved.

Christmas 2009 Offline Winners

4 Entire contents © 2008 Forrester Research, Inc. All rights reserved.

Christmas 2009 Online Winners and Losers

WinnerWinnerWinnerWinnerWinner

Winner WinnerWinner

WinnerWinner

Winner

WinnerWinner

Loser

Loser

Loser Loser

LoserLoser

LoserLoserLoser

LoserLoserLoser

LoserLoser

Loser

Loser Loser

The BIG online winner

Amazon

5 Entire contents © 2008 Forrester Research, Inc. All rights reserved.

eCommerce circa 2005

• Fewer than 44 million European adults had broadband

• Capacity to receive data was limited• Media categories dominated eCommerce

6 Entire contents © 2008 Forrester Research, Inc. All rights reserved.

Online shopping categories are evolving

1995-1999 1999-2001

Durable goods

2001-2008

Soft goods

Media

Discretionary hard goods

Travel

Luxury goods

7 Entire contents © 2008 Forrester Research, Inc. All rights reserved.

Slowly, other sectors such as auto, white goods, and luxury brands are coming on board

8 Entire contents © 2008 Forrester Research, Inc. All rights reserved.

With more firms that don’t sell online, now view the Net as a potential sales channel

May 2008 “Benchmark: Luxury Sector eBusiness Adoption”

9 Entire contents © 2008 Forrester Research, Inc. All rights reserved.

Online shopping has become a popular activity for online European consumers

Which of the following do you do regularly online? By regularly, we mean at least once a month

Source: Forrester’s European Technographics® Benchmark Survey, Q2 2008Base: 7,102 online European Adults

85%

55%

46%

43%

37%

45%

44%

22%

26%

27%

26%

34%

17%

18%

10%

15%

84%

59%

46%

40%

40%

36%

33%

32%

21%

21%

21%

20%

18%

14%

13%

8%

Send Email

Research products

Research holiday destinations

Use free Web-based email (e.g. Hotmail)

Make purchases

Read news onlinePrepare trips online (maps, directions, public

transport)Buy/sell things in auctions

Download free/shareware software

Look up sports information

Look up government informationUse an instant messenger (e.g.

MSN/Yahoo! Messenger)Look for/apply for jobs online

Listen to the radio

View stock-market prices

Watch TV programs (live or archived)

EU-7Germany

10 Entire contents © 2008 Forrester Research, Inc. All rights reserved.

The UK and Sweden lead online shopping adoption

U

PLVS RLT

25m28m

16m

5.6m4.8m

4.7m

8m

74%

73%

67%

65%

56%

29%

22%

56%

UK

Sweden

Netherlands

Germany

France

Spain

Italy

EU-7

Q2 2008

Germany and the UK account for almost 60% of Europe’s online shoppers

Base: 14,514 online European adults

“Have you bought any products or services online in the past three months?”

Source: European Technographics® Benchmark Survey, Q2 2008

11 Entire contents © 2008 Forrester Research, Inc. All rights reserved.

Retailers also growing their online presence in …

Tesco.com c1998

Tesco.com c2002 Tesco.com 2008

•2008 non-food sales rose 12% to £11.8B•12,000 non-food products available online, catalogue, phone, stores and kiosk•Tesco Personal Finance 1.7 million new customers this year, with 50% financial products sales made online

12 Entire contents © 2008 Forrester Research, Inc. All rights reserved.

Neckermann.de c1997

… and throughout Europe

Neckermann.de 2009

•Online since 1995• 140,000 products online•150M visitors a month•2007 - 55% turnover via Internet• 3M+ newsletter registrations• 20K + search terms

13 Entire contents © 2008 Forrester Research, Inc. All rights reserved.

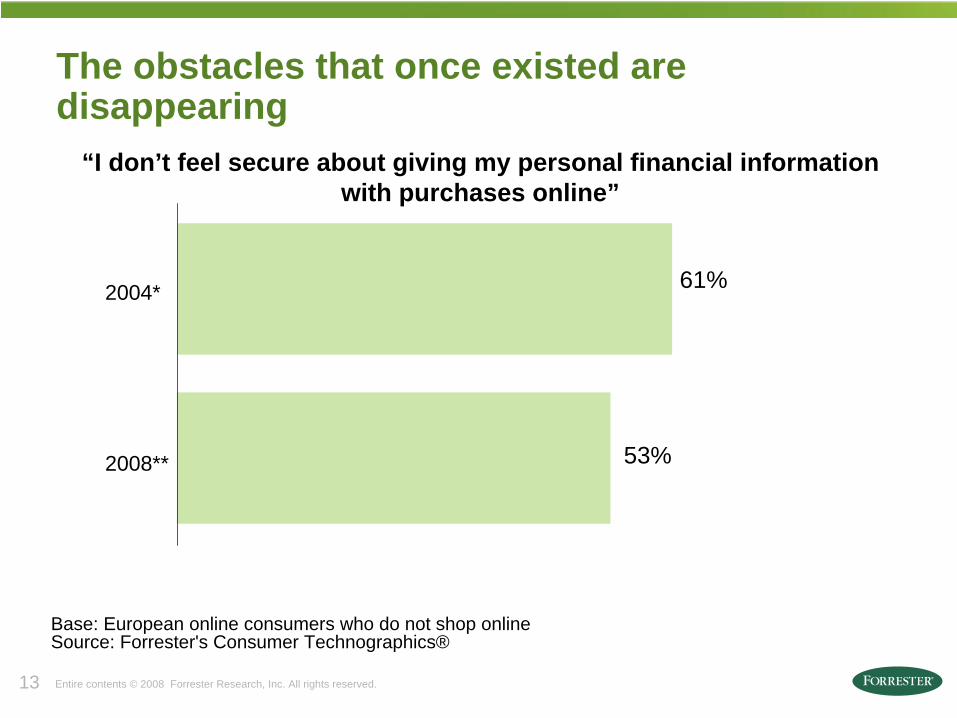

The obstacles that once existed are disappearing

53%

61%

Source: Forrester's Consumer Technographics®Base: European online consumers who do not shop online

“I don’t feel secure about giving my personal financial informationwith purchases online”

2008**

2004*

14 Entire contents © 2008 Forrester Research, Inc. All rights reserved.

However, Germans amongst least secure online

25%

10%

20%

25%

26%

33%

41%

47%

W. Europe

Italy

Spain

Germany

France

UK

Sweden

Netherlands

“I feel secure when giving personal financial information when making purchases online”

Base: 22,673 European consumers

Source: European Technographics® Benchmark Survey, 2008

15 Entire contents © 2008 Forrester Research, Inc. All rights reserved.

Today, the eCommerce experience is steeped in its heritage

Top search and nav bar

Special offers at top

Side navigation replicates top

Special offers at top

16 Entire contents © 2008 Forrester Research, Inc. All rights reserved.

…and are now considered THE de-factor basicsThumbnails, name,

price, ratings & recommendations

Additional side navigation

Click to buy button above fold

Delivery info and offers

Source: Amazon.com

Saved Check- out info and

updates

17 Entire contents © 2008 Forrester Research, Inc. All rights reserved.

This utilitarian approach continues to influence eCommerce and online retail

CONVENIENCE Tools Save Time

CONTENTMENT Selection Satisfies Needs

COST Price Saves Money

Source: European Technographics Retail, Customer Experience, and Travel Online Survey, Q3 2008

1¢39%

57%

51%

40%

65%

I preferred to purchase from onlineretailers that offered free shipping

I found better prices online than Idid offline

I found products online that I couldnot find offline

I shopped online to avoid crowds instores

I saved time by shopping online

Base: European population – All age brackets

18 Entire contents © 2008 Forrester Research, Inc. All rights reserved.

But the opportunity is much larger

Mastering What’s Important Now Evolving to the Future

Truly differentiated eCommerce experiences will do to Web shopping what the Apple Stores have done to bricks-and-mortar business.

Source: apple.com

Forrester predicts that by 2012 nearly half of retail sales will either be

transacted online or influenced by the Web.

19 Entire contents © 2008 Forrester Research, Inc. All rights reserved.

€ 4,316M

€ 948M

€ 4,325M

Since 2002, online spending grew 50%. The 55+ more than doubled amount they spend online

In the past 3 months, about how much in total (including shipping and handling) have you spent buying products online, regardless of how you paid?

Source: Forrester’s European Technographics® Benchmark Survey, Q2 2008, Q2 2002

Base: 2,155 online Germans who have made an online purchase in the past 3 months

€ 2,522M

€4,979M

€6,417M

16 to 34

35 to 54

55 and Over

2002**Total - €9,588M

2008Total - €13,921M

*In million on Euros (for a three month period)

20 Entire contents © 2008 Forrester Research, Inc. All rights reserved.

Germans are buying more products online

30%

14%

14%

12%

12%

11%

9%

10%

9%

7%

7%

Books

Clothing

Event tickets (e.g. cinema, theater, sport)

CDs/tapes/records

Leisure travel (flights, package tours, hotels, etc.)

Videos/DVDs

Printer supplies (e.g. cartridges, ink)

Toys

Computer software/video games

Footwear

Health products

2008

“And which if any of the following products have you bought online in the past 3 months? ”*

Source: Forrester’s European Technographics® Benchmark Survey, Q2 2002, 2008

Base: 3,769 online German adults

*Top 11 categories

21 Entire contents © 2008 Forrester Research, Inc. All rights reserved.

Driven significantly by why Germans buy increasingly more products online

• Because… it’s convenient – 71% say they save time by shopping online

• They love bargains… 62% say they find better deals online

• And, because the internet offers more choice – 52% say they find products online they can’t find anywhere else

22 Entire contents © 2008 Forrester Research, Inc. All rights reserved.

German online shoppers are younger, wealthier, more experienced and confident online

German online shoppers

German online shopping hold-outs

German online population

Millions of consumers 28 mil 32 mil 60 milMale 53% 45% 53%Age 40 years old 51 years old 41 years old

Income €30,008 €22,101 €28,445

Higher Education 42% 28% 39%

Online tenure 5.8 years 4.3 years 5.3 years

I like technology 55% 36% 52%

Personal financial information is secure

online38% 15% 31%

Spent online in the past 3 months €275 - -

Online shopping tenure 3.8 years - -

Base: 3,769 online German adultsSource: Forrester’s European Technographics® Benchmark Survey, Q2 2008

“And in the past 3 months, which of the following apply to you?”

23 Entire contents © 2008 Forrester Research, Inc. All rights reserved.

Increasingly the Internet is a preferred channel to buy products.

42%

26%

24%

20%

6%

19%

13%

1%

2%

6%

5%

30%

30%

32%

26%

23%

10%

15%

21%

20%

12%

8%

7%

3%

1%

1%

3%

1%

2%

1%

1%

1%

1%

1%

%

Clothing and footwear

Books

Music

Videos/DVDs

Event tickets

Beauty products

Video games

Hotel reservations

Airline tickets

Computer software

Computer hardware

Shop Internet Post/phone Other

“For each of those you have bought in the past three months, please select all the places you have bought from. ”

Base: 3,715 online German shoppersSource: European Technographics® Retail, Customer Experience and Travel online Survey, Q3 2008

24 Entire contents © 2008 Forrester Research, Inc. All rights reserved.

However, remember . . .

• More consumers online

• Spending more time online

• Spending more money online

• Expecting more online

25 Entire contents © 2008 Forrester Research, Inc. All rights reserved.

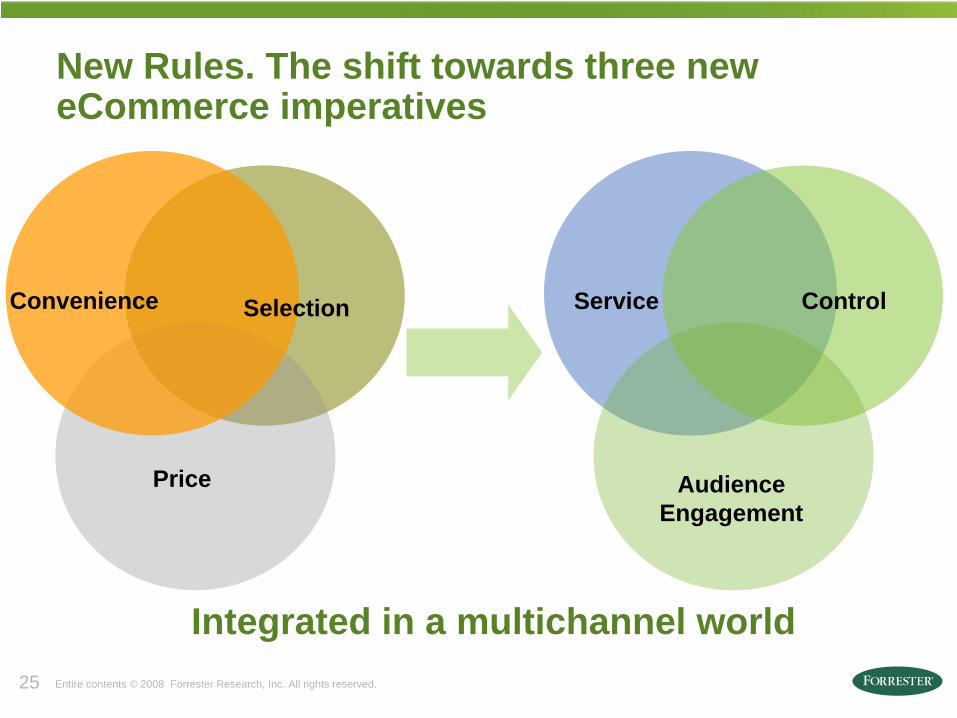

New Rules. The shift towards three new eCommerce imperatives

Service Control

Audience Engagement

Convenience Selection

Price

Integrated in a multichannel world

26 Entire contents © 2008 Forrester Research, Inc. All rights reserved.

Future retail: The new paradigm

Service Addressing explicit and implicit customer needs

Control Empowering customers to manage their experiences

AudienceEngagement Keeping customers involved and interested

27 Entire contents © 2008 Forrester Research, Inc. All rights reserved.

Service means answering questions

Live chat & personal assistants

Co-shopping

Live co-shopping

Source: smatch.de

Source: IKEA.co.uk

28 Entire contents © 2008 Forrester Research, Inc. All rights reserved.

...and transparency

Figleaves offers consumer ratings and reviews, and manages

blogs on social networking sitesSource: Figleaves.co.uk

29 Entire contents © 2008 Forrester Research, Inc. All rights reserved.

. . . And of content, tooRepeat visitors

New customers

Source: Neiman Marcus

30 Entire contents © 2008 Forrester Research, Inc. All rights reserved.

Personalization is more than recommendation engines and collaborative filtering

Source: Netflix

Victoria’s Collection

31 Entire contents © 2008 Forrester Research, Inc. All rights reserved.

79%

80%

81%

87%

90%

Checkoutprocess

Shopping cartpage

Home page

Search/browseresults

Product detailpage

Retailers are now responding to consumer’s higher expectations

Base: 60 to 80 online retailersSource: “The State of Retailing Online 2008,” a Shop.org studyconducted by Forrester Research

Browseexperience

Online retailers are finding that their best investment

efforts are those dedicated to improving the browse/shopping

experience.

32 Entire contents © 2008 Forrester Research, Inc. All rights reserved.

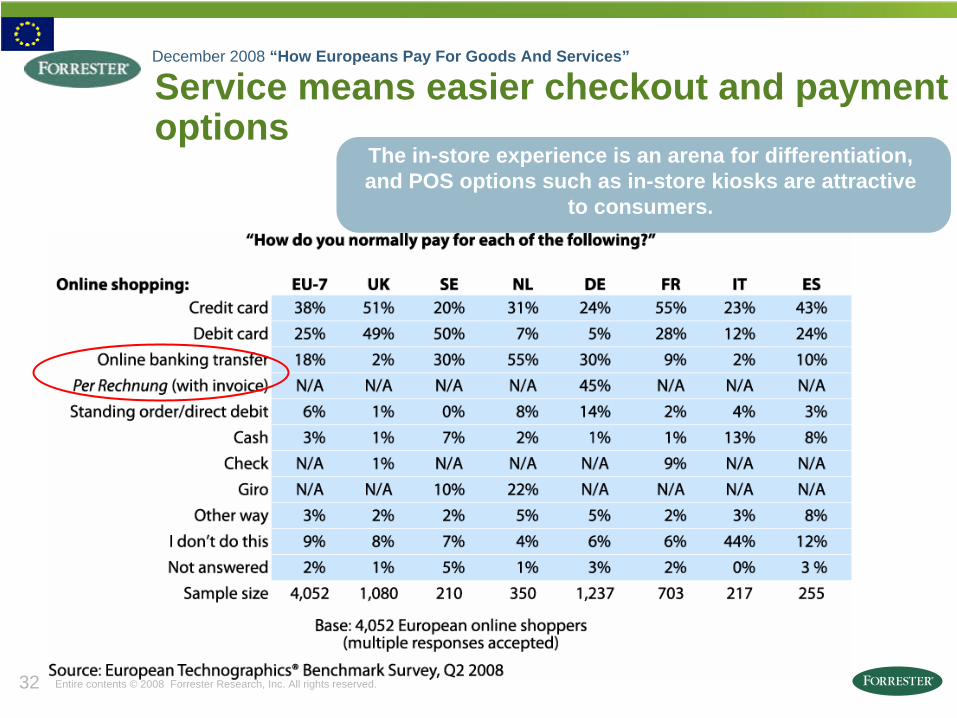

December 2008 “How Europeans Pay For Goods And Services”

Service means easier checkout and payment options

The in-store experience is an arena for differentiation, and POS options such as in-store kiosks are attractive

to consumers.

33 Entire contents © 2008 Forrester Research, Inc. All rights reserved. Source: Forrester's European Technographics® Online Media, Marketing, and Retail Survey, Q3 2007

“From which of the following types of companies do you have shopper/loyalty cards?”

...and here in Europe, loyalty . . .

60%

52%

32%

31%

18%

16%

12%

11%

8%

9%

64%

35%

32%

33%

12%

11%

6%

13%

4%

10%

Supermarkets

Multiretailer cards

Department stores

Petrol stations

Pharmacies/chemists

High-street shops

Airlines

Retailer charge cards or credit cards

Hotels

Other companies

Online shoppersNon-online shoppers

Base: 5,965 European online adults who participate in loyalty programs

Online shoppers own more loyalty cards than Europeans who don’t buy products online

34 Entire contents © 2008 Forrester Research, Inc. All rights reserved.

Future retail: The new paradigm

Service Addressing explicit and implicit customer needs

Control Empowering customers to manage their experiences

AudienceEngagement Keeping customers involved and interested

35 Entire contents © 2008 Forrester Research, Inc. All rights reserved.

Rich Internet Applications (RIAs) enables control

36 Entire contents © 2008 Forrester Research, Inc. All rights reserved.

As do new delivery models and options

37 Entire contents © 2008 Forrester Research, Inc. All rights reserved.

New channels also enable control

Source: Amazon.co.uk

38 Entire contents © 2008 Forrester Research, Inc. All rights reserved.

• m.ralphlauren.com covers a range of potential user needs from entertainment (exclusive content) to purchasing

• Mobile site offers additional customer touchpoint and deeper customer engagement

• RL premium customer base overlaps with mobile internet users demographics and their devices

• Customer captures QR code through cameraphone which is used to direct phone browser to website

With retailers and brands like Ralph Laruen embracing the mobile channel for closer engagement with consumers

Success of QR codes in Asia has led to it overtaking traditional PC based eCommerce

39 Entire contents © 2008 Forrester Research, Inc. All rights reserved.

Future retail: The new paradigm

Service Addressing explicit and implicit customer needs

Control Empowering customers to manage their experiences

AudienceEngagement Keeping customers involved and interested

40 Entire contents © 2008 Forrester Research, Inc. All rights reserved.

Audience engagement helps build community

Links to Web TV are easy to find on the home page

Audience engagement is entertainment

42 Entire contents © 2008 Forrester Research, Inc. All rights reserved.

...and educational...

Sources: Williams-Sonoma.com / Argos.co.uk/

...or bothDarty presents their products with the option of viewing them via WebTV

Source: http://www.darty.com/achat/web-tv/index.html?m=10001

43 Entire contents © 2008 Forrester Research, Inc. All rights reserved.

How to prioritize?

Service Control

Audience Engagement – Get buzz & interactivity

Live chatCo-shoppingCustomer reviewsTagged contentCustomized productPersonalized contentMobile

RIAsChannel diversityMobile

CommunitiesSocial merchandisingVirtual dressing roomsMobile