O F OAFT: LL - ShopperTrak UK: Footfall Retail...

20

Bringing you the latest consumer behaviour trends across the globe Q1 2016 FOOTFALL: GLOBAL SHOPPER TRENDS REPORT www.footfall.com +44 (0) 121 711 4652

-

Upload

duongkhuong -

Category

Documents

-

view

216 -

download

3

Transcript of O F OAFT: LL - ShopperTrak UK: Footfall Retail...

Bringing you the latest consumer behaviour trends across the globeQ1 2016

FOOTFALL: GLOBAL SHOPPER TRENDS REPORT

www.footfall.com +44 (0) 121 711 4652

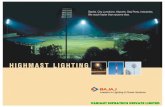

Spain

Switzerland

United

King

do

m

Portugal

Poland

Italy

Irela

nd

Aus

tral

ia

China

Hong Kong

India

Japan

Austria

France

Germ

anyEURO

PE

APAC

+9.8%

+1.2%

+2.8%

+0.5%

+0

.1%

+2.2%

+1.8

%

+0.7%

+0.7%

+0

.5%

-0.1%

-0.7%

-0.9%

-1.2%

-1.5%

Global Shopper Trends Report Q1 2016Global footfall increased by 1.1% during Q1, driven predominantly by the Asia-Pacific region, where consumer traffic rose +2.7%.

Confidence is rising as the Chinese economy rebounds and, while the knock on effects can still be seen, Asian economies are returning to business as usual.

In contrast, European footfall has stalled, with a negligible +0.1% rise in retail traffic during the first quarter. Much of this comes as a result of lack of consumer confidence and frozen wages affecting consumer spending in Europe’s best performing economies.

02

+1.1%*

Overall global footfall performance Year-on-Year was up +1.1%

intro

* Footfall Year-on-Year

03

APAC

Across the continent footfall increased by

+2.7% Year-on-Year

While 2016 began positively across all Asia-Pacific regions, footfall averages have been lifted by China’s exceptional rise in retail traffic.

Across the continent footfall increased by +2.7% Year-on-Year, with all regions experiencing an uplift in retail traffic. However, as with the previous quarter, these figures were not accompanied by a rise in retails sales in some regions such as Hong Kong and Japan, where consumers are showing continued spending caution.

The first quarter of 2016 saw a reversal of fortunes from last year, with China and Japan performing well, while India and Australia dropped straight from the top to the bottom of the footfall league table.

After a difficult 2015, China experienced a +9.8% rise in consumer traffic during Q1, with fiscal planning, rising wages, and the lunar New Year all contributing. However, unlike its neighbours, the increased footfall was matched by a 10% increase in sales and 27.8% growth in online sales Year-on-Year.

04

China

CHINA

+9.8%*

GDP in the world’s second-largest economy grew 6.7% in January-March from a year earlierThis is the weakest pace of growth since the global financial crisis, a positive sign that Chinese efforts to steer the economy away from reliance on manufacturing is beginning to take effect, even as the property and retail markets spike.

Footfall also grew by +9.8% Year-on-Year, in line with an average 10% increase in retail sales across the quarter. China’s National Bureau of Statistics reported that urban consumers contributed the majority of the increase, although rural consumer spending climbed faster. In the same period, online sales rose 27.8% Year-on-Year, accounting for about 13% of gross retail sales.

* Footfall Year-on-Year

The impressive performance has been attributed to a variety of factors, from rising salaries to low consumer prices. However, with fiscal methods, including government loans, driving the country’s transition from export-driven economy to a consumer society, some analysts warn about the sustainability of the growth rate for future months.

CHINA

ITALY

Fabe LinFootFall’s Senior Business Consultant, China

For further information connect with Fabe Lin on LinkedIn

“In the first quarter of 2016, the number of festivals and the warmer weather was good news for bricks and mortar stores. China celebrated three important festivals, The Solar Year, The Chinese New Year and Valentine’s Day. This was a great opportunity for retailers and shopping centres, as people purchased food, clothing and gifts. And as the new year brought sunny weather, people went out to enjoy shopping instead of staying home.

Although the stock market is still affecting consumer confidence, due to the first housing interest rate reduction, the real estate industry was quite hot in China.”

05

Asia-Pacific

Year-on-Year footfall increased by +2.8% during the first three months of 2016

Despite this rise, retail in Japan continues to suffer, as consumers spend cautiously. Across all sectors, including car and supermarket sales, there are no signs of improvement in real value. The continuing reluctance to spend may also cause the Japanese Government to delay their scheduled national sales tax increase.

As Japanese retailers continue to face poor sales at home, internationally they are also struggling. 2015 saw a 90% increase in Japanese bankruptcies linked to events in China. According to Tokyo Shoko Research’s survey, the biggest reason for the 120 bankruptcies was high costs caused by rising labour prices in China, and continued decline of the Yuan against the Yen.

+2.8%*JAPAN

* Footfall Year-on-Year

While this growth was smaller than the previous quarter, retail sales rose for the first time in four months, edging up 0.5% in February from a year earlier.

JAPAN

90%2015

¥

INCREASE INBANKRUPTCIES

Year-on-Year retail traffic across Q1 improved by +1.2%, however, this has not translated into sales.

06

Despite continued footfall growth, the first quarter of 2016 saw the largest Hong Kong retail sales decline in 17 years

February saw sales drop 21% to HK$37 billion ($4.8 billion) Year-on-Year, while over the first two months of the year, the decline was 14% according to Hong Kong’s statistics department.

The dramatic decline in sales was undoubtedly impacted by the 12% fall in Chinese tourists visiting the city during the Lunar New Year holiday. Hong Kong Tourism Board predicts that the number of tourists from the mainland will continue to drop 3.2% throughout the remainder of the year, while their average spending will shrink by 4%. For retailers this will be compounded by the fact that Hong Kong residents are also consuming less, due to stagnant property values and the weak stock market.

Despite signs of growth within the Chinese economy, analysts expect Hong Kong’s retail market will continue to decline for the rest of 2016, as the strong Hong Kong dollar and uncertain economic prospects continue to have an effect.

HONG KONG

Asia-Pacific

+1.2%*

12% fall in Chinese

tourists visitingthe city during the

Lunar New Year holiday

HONG KONG

* Footfall Year-on-Year

07

Asia-Pacific

AUSTRALIA

+0.5%*

GDP growth of

0.6%

Retail footfall saw a small increase of +0.5% in Q1

The Australian economy grew 3.0% in 2015; following this strong performance some analysts were worried that the country would be adversely affected by uncertainty in China in early 2016. However, results for the first quarter show promising GDP growth of 0.6%, while unemployment fell to its lowest point since 2013.

One of the main contributors to this growth was the 0.8% rise in household consumption expenditure. The latest findings of the Australian Bureau of Statistics revealed flat growth in retail sales (average 4%), although strong performance is still being recorded in the key divisions of household goods and clothing.

This is a welcome return to growth after the temporary dip in consumer activity at the end of 2015.

AUSTRALIA

* Footfall Year-on-Year

0.8% RISE INHOUSEHOLDEXPENDITURE

Asia-Pacific

08

While 2015 saw four quarters of continued growth in retail traffic, footfall in India has stalled at +0.1% in the first quarter of 2016Despite this, there is good news across India’s fast growing retail market, estimated to be worth close to $625 billion.

Retail inflation eased in March to a six-month low (4.83%), helped by smaller rises in food prices. This will be welcome news to policy makers at the central bank, which is aiming to bring retail inflation down to 4% by March 2018.

International retail brands continue to look to India for expansion. Talks are ongoing between The Walt Disney Co and India’s DLF Brands to open stores in the country, while mobile brands Virgin, Lebara and Tune Talk are all said to be considering the market. Ikea has confirmed that, despite long delays, it plans to open 25 stores across the country over the next decade, driven by the increased spending power of the urban middle class.

INDIA

+0.1%*

INDIA

* Footfall Year-on-Year

09

Automotive sales performed

worst, despite job gains

and lower gas prices

USAWith Q1 GDP set to meet the 0.8% growth forecast, it seems the U.S. economy may shake off the initial stall that affected the first quarter in the previous two years.

Retail growth over the quarter continued to fluctuate, with the Commerce Department reporting that overall retail sales fell by 0.3% in March, following a flat reading in February and a drop in January. Automotive sales performed worst, despite job gains and lower gas prices, and the 2.1% decline was the steepest fall in more than a year.

However, as the National Retail Federation reported, it is not all bad news. If automobiles, gasoline stations, and restaurants are excluded, consumer spending increased slightly in March, with a Year-over-Year increase of 5.8%. NRF Chief Economist, Jack Kleinhenz, stated “while colder temperatures in March lessened spending on apparel, recent job and income gains indicate positive prospects for future household spending.”

Retailers in the U.S. are contributing significant job growth, adding an average of 52,000 jobs per month over the last three months. The overall improvements in employment has meant that, despite uncertainty about the stock market in the first part of the quarter, consumer confidence remained steady. While consumers do not foresee the economy improving with any speed, they are not worrying about it worsening.

EUROPE

The Republic of Ireland topped the table in Q1 with

+2.2% footfall growth

After a turbulent 2015, European footfall has stalled at +0.1% growth.However, most regions are beginning to see increases in consumer spending.This matches forecasts of slow but important real value growth in 2016. It may come as no surprise that the Republic of Ireland topped the table in Q1 with +2.2% footfall growth; the country saw increased consumer traffic levels during every quarter of 2015.

Footfall was once again affected by poor performances in Switzerland, the UK, France and Austria. German footfall, meanwhile, returned to growth as consumer confidence rose, partly due to low fuel costs and a strengthening labour market.

Retailers in Spain and Portugal have reason to celebrate as footfall continued to grow; both countries expect to see continued decreases in unemployment this year, which should have a positive impact of consumer spending.

10

11

Europe

In line with its strong 2015 performance, The Republic of Ireland continued to lead the European footfall growth tables in Q1 2016

This comes as a result of the improved labour market and strong economic performance across the country. Not only have all retail categories, with the exception of fuel, seen annual increases in volume terms, 11 out of 13 retail categories also saw increases in sales values.

Despite this strong performance, Retail Ireland, the Ibec group that represents the retail sector, has warned of threats to continued growth. This comes in light of rising utility costs, the increase to the minimum wage and climbing rent across city centres. Retailers in Ireland are warned that sales are still 12.5% below February 2008 levels in value terms. As a result of strike action on Dublin’s two main forms of public transport, LAUS and DART, there are concerns that consumer confidence will suffer as instability may make the city less accessible and attractive to shoppers.

Reporting a steady +2.2% rise in consumer traffic, retail sales once again grew in the first quarter, rising by nearly 11% across January and February 2016 compared to the same period a year ago. Footfall, meanwhile, rose by +2.2%.

REPUBLIC OF IRELAND

Retails sales grew nearly11% across

January and February

2016

+2.2%*

REPUBLIC OF IRELAND

* Footfall Year-on-Year

With retail traffic rising +1.8% despite concerns, the Eurozone’s fourth largest economy continues to offer a wealth of opportunity for retailers.

12

During the first quarter of 2016, Spain saw Europe’s second highest growth in footfall

The end of 2015 saw widespread predictions that spending would stall in Spain. Contrary to this, retail trade increased by 3.9% Year-on-Year in February of 2016, following a 3.3% growth in January. While the challenges of an uncertain government, poor labour market, high unemployment, declining consumer confidence and low household income continue to cause worries, overall, the Spanish economy is recovering and maintaining positive growth of 1.8%.

Europe

+1.8%* SPAIN

ITALY

Ezequiel DuranFootFall’s Regional Director, Spain

For further information connect with Ezequiel Duran on LinkedIn

“Spain s economy continues emerging while facing political uncertainties that are slowing down the growth. The lack of an established government since December is impacting public and private investment, and consumer confidence has dropped during the last three months of Q1. Still, healthy GDP of +3.4% Year-on-Year and decreasing unemployment keeps retailing activity in positive sales and traffic, with the FootFall Index increasing by +1.8% in Q1 against last year. The marketplace as a whole is keen to end the political instability in order to achieve optimal performance levels.”

SPAIN

* Footfall Year-on-Year

Ezequiel DuranFootFall’s Regional Director, Spain

13

Europe

Germany posted moderate footfall growth during the first quarter of 2016

However, in terms of confidence, consumers’ income expectations and willingness to buy both also plateaued in Q1. In the context of the EU, these remained at high levels, driven by a strong labour market and low inflation, supporting income expectations and households’ propensity to buy.

The remainder of 2016 is likely to see an increase in consumer confidence levels, while record-high employment, rising wages, low inflation, and cheaper gasoline should boost private spending. As with every retail market in the world, store-based businesses continue to struggle in competition with online offerings.

Year-on-Year footfall grew by +0.7%, matched by retail sales increases of 0.7% in January, which continued to rise across the first quarter.

GERMANY

+0.7%*

This was built on the positive performance of 2015, a milestone year for the Italian economy, as it expanded for the first time in four years.

Italy saw a +0.7% increase in footfall during Q1

This marks a third quarter of continued improvement in retail traffic. Forecasters who hoped that this progress would continue into 2016 may have been disappointed to see retail sales in Italy decrease by 0.8% in January. However, in a market driven partly by summer tourism, retailers should see a return to growth later in the year.

Consumer confidence increased in the first three months of 2016, a positive sign for retailers, as the Italian retail sector demonstrated throughout 2015 that rising consumer confidence was matched by a consistent rise in spending levels.

There are also renewed signs of international interest in the Italian retail markets, as Primark launched its first retail space at the beginning of April. The store will employ 400 members of staff.

+0.7%*

ITALY

* Footfall Year-on-Year

GERMANY ITALY

14

Europe

Portuguese footfall volumes continued to recover in the first three months of 2015

Consumer confidence remained constant over the first three months of the year, while indicators point to modest improvements in consumer spending. After a slow January, retailers were boosted by a 3.5% growth Year-on-Year in retail sales during February.

Retailers and shopping centres benefitted from a more stable Portuguese national economy. Alongside this the unemployment rate is set to fall, with youth unemployment likely to see a decrease during 2016. While groceries continued to dominate household spending, there were promising signs that the retail market is witnessing greater consumption in fashion, electronics and comfort-related products.

PORTUGAL

3.5%growth

Year-on-Year in retail sales during

February

Q1 saw a steady +0.5% increase in retail traffic, driven by rising household spending and higher employment.

PORTUGAL

Polish retail traffic remained steady, but sales increased

While Polish retail sales increased throughout the first quarter, with a marked rise of 3.9% in February, shoppers were still cautious, as consumer confidence remained in the negative.

Retailers will be buoyed, however, by the six months of continued retail sales growth up to March 2016.

2015 saw bricks-and-mortar retailing experience moderate growth, whereas internet retailing registered a dynamic increase in revenue. This strength can be expected to continue, with retailers developing multi-channel and mobile presences.

After steady improvement in the latter half of 2015, Poland saw footfall stall in Q1 2016, with a small decline of -0.1%.

POLAND

POLAND

+0.5%*

-0.1%*

* Footfall Year-on-Year

15

Europe

Year-on-Year sales growth stalled, with the early Easter contributing only marginal improvements to the figures. Food in particular performed poorly, with sales over the last three-months falling 0.7%.

The UK’s footfall dropped by -0.7% during Q1

Continued falls in average store prices marks 21 consecutive months of Year-on-Year price decreases. For the first quarter of the year, this averaged at declines of just over 2% every month.

In her March statement Helen Dickinson OBE, Chief Executive, British Retail Consortium, said “looking at the long-term picture, the rolling 12-month average growth slowed to 1.4%, its lowest since August 2015. This slowdown can’t be viewed in isolation; retail is an industry undergoing significant structural change as the investment in the digital offer continues apace while, from a consumer perspective, more disposable income is being spent on leisure and entertainment.”

Nonetheless, the outlook for 2016 remains a positive one, with lower oil prices and moderate wage growth likely to drive consumer spending. However, the cost of implementing the National Living Wage and the EU referendum in June are likely to substantially affect the retail sector over the year.

UNITED KINGDOM

-0.7%*

Continued falls in average store

prices marks 21 consecutive months of Year-

on-Year price decreases

UNITED KINGDOM

* Footfall Year-on-Year

16

Europe

Predictions continue to suggest that while the French economy is gradually recovering, it is doing so at a slow rate.

GDP growth for 2016 is forecast at 1.4%, which would position France well within a broader EU context.

For retailers, the country’s urban centres remain an attractive opportunity, and tourism continues to deliver uplifts in sales during the summer months.

2016 will bring uncertainty, with labour law reforms causing some concern, as well as consumer and business confidence falling in the first quarter amid growing global economic concerns.

FRANCE

-0.9%*

French retail footfall declined for a third consecutive quarter, with traffic falling by -0.9%

FRANCE

* Footfall Year-on-Year

TOURISMCONTINUES TO DELIVER

UPLIFTS IN SALES

17

Europe

The first three months of this year saw slower but continued falls in confidence from -21% in January to -22% in February. Despite this trend, retail sales saw a return to growth in February (0.3%), despite January’s decline of 0.5% marking the first negative growth in 12 months.

2016 is likely to see internet retailing continuing to poach value share from store-based retailing, particularly from non-grocery specialists.

Retail traffic dropped by -1.2% during the first quarter of 2016 following low consumer confidence throughout 2015.

Austrian footfall dipped for a second quarter in a row -1.2%* AUSTRIA

ITALY

Thomas HillebrandFootFall’s Regional Director, CEE

For further information connect with Thomas Hillebrand on LinkedIn

“Retail in Austria showed light and shade during Q1 2016: The influx of refugees was noticeable on the retail store shelves. In particular, the food retail sector showed a strong performance but also the toys segment saw an upward trend. However, some retailers, especially those in shoes, textiles and electronic goods, were affected by consumers moving to transnational ecommerce sites. Nevertheless, the Austrian business associations expect economic stability to continue in 2016, combined with rising average transaction values.”

-21%JAN

-22%FEB

Consumer Confidence

+0.3%FEB

Retail Sales

AUSTRIA

* Footfall Year-on-Year

18

Europe

Year-on-Year retail traffic fell -1.5% during the first quarter, driven by widespread cross-border shopping and the high value of the Swiss Franc.

For the third consecutive quarter, Switzerland is bottom of the footfall league table

Looking to the remaining three quarters of 2016, Swiss retail will continue to face challenges and price will be a key differentiator. 2015 saw German discount grocery chains grow their market share, despite initial consumer distrust. In the non-grocery sector, the competition of online retail will have an ongoing effect on traditional bricks-and-mortar stores. Long term, retailers in Switzerland will place more importance in their use of internet and social media to increase brand awareness and build customer loyalty.

SWITZERLAND

-1.5%*

ITALY

Thomas HillebrandFootFall’s Regional Director, CEE

For further information connect with Thomas Hillebrand on LinkedIn

“Despite the ongoing strong purchasing power of Swiss consumers, significant changes in shopping behaviour pushed down retail traffic in the first quarter of 2016. Increasingly shoppers purchase high value items in online stores from Germany, France and Italy - and thus they are changing Swiss retail. As a result, one of worldwide most renowned Swiss specialty retail brands, Bata, is currently closing its doors.”

SWITZERLAND

* Footfall Year-on-Year

All retail traffic figures used in this report are original insights from FootFall, the leading global retail intelligence service.

About the Global Shopper Trends Report

We believe it is not enough to understand consumer trends, but acting on that insight to deliver rapid and measurable return on investment.

To find out more about how economic, social, cultural and political events are impacting your region, visit our online trends centre. This hub includes FootFall’s Global Retail Traffic Index, which provides a barometer of international shopper confidence.

We also offer the technology and consultancy to help retailers and shopping centres unlock the potential revealed in this data. We’ll support you with recommendations and action plans for tangible performance improvement, from pilot project through to full retail intelligence solution deployment.

@footfallinsight www.footfall.com

To find out how FootFall can improve your profits visit www.footfall.com

© 2014 Tyco Retail Solutions All rights reserved. TYCO and the product names listed in this document are marks and/or registered marks. Unauthorized use is strictly prohibited.

19

FootFall Head OfficeYorke House, Arleston Way, Solihull B90 4LH

+44 (0) 121 711 4652

www.footfall.com @footfallinsight

© 2014 Tyco Retail Solutions All rights reserved. TYCO and the product names listed in this document are marks and/or registered marks. Unauthorized use is strictly prohibited.

FootFall: know your customers inside and out to increase profitability

FootFall, the retail intelligence company, works with retailers and shopping centres around the world to provide actionable insight into customer behaviour, which delivers increased revenue and improved profitability.

Part of Tyco Retail Solutions, we provide 3D data for clear cut decisions. By analysing the most relevant mix of metrics from both store and online behaviour - including customer numbers, queues, sales, marketing and other key performance data - we can identify the widest range of profit drivers.

More than 1200 retail businesses across 64 countries partner with FootFall for long-term retail intelligence.

www.footfall.com