NRB Bearings CMP - Spark Capitalmailers.sparkcapital.in/uploads/Mukesh/NRB_Bearings... · NRB...

19

NRB Bearings CMP Rs. 122 Target Rs. 155 Rating Buy Date Sep 23, 2014 Market Data SENSEX 27207 Nifty 8146 Bloomberg NRBBR IN Shares o/s 97mn Market Cap Rs. 12bn 52-wk High-Low Rs. 133-31 3m Avg. Daily Vol Rs. 42mn Index member BSESMCAP Latest shareholding (%) Initiating Coverage Moving the needle NRB Bearings (NRB) is the leading needle roller bearing supplier in India with a 70% market share. The company has created a niche by catering to customized requirements. With exposure to all domestic auto segments we expect the OEM demand revival to result in strong domestic revenue growth (FY14-FY17: ~16% CAGR ). Exports are expected to record 25% CAGR driven by new orders from key customers, Getrag and ZF. PAT CAGR of 43% from FY14-FY17 is driven by EBITDA margin improving to 22% in FY17. NRB is currently trading at (11.8x Sep’16 EPS) a steep discount to its peers. We initiate with a Buy rating and TP of Rs. 155 based on 15x Sep’16 EPS Strong domestic growth visible: NRB is among the few needle bearings manufacturers globally and has technology at par with MNCs. The company maintains strong relationship with OEMs by way of partnering from conceptualisation stage and manufacturing customized bearings. Key USP of NRB is to maintain large number of SKUs (2.5x that of nearest competitor), ability to supply smaller batch sizes and faster turn around time. With exposure to 2W (25% of domestic), CV (20%) and PV(20%) we expect domestic revenue to see strong growth with revival in CV and PV volumes and continued growth in 2W volumes. After market business has seen slower growth as NRB focused on OEM and exports in the recent years. However, with renewed focus and plans to supply kits in the aftermarket (including other complementary products) we expect aftermarket growth to improve and record a CAGR of 13% from FY14 – FY17 Steep exports growth: NRB’s technology to manufacture needle roller bearings has been inherited through its acquisitions of JVs with Nadella (France) and INA (Germany) who are currently among the leaders of needle roller 1 Stock performance (%) 1m 3m 12m NRB 15% 53% 276% Sensex 3% 8% 34% BSE Auto 7% 23% 63% Financial summary (Standalone) Year Revenues (Rs. mn) EBITDA (Rs. mn) EBITDA Margin % PAT (Rs. mn) EPS (Rs.) P/E (x) EV/EBITDA (x) FY14 5,945 1,006 16.9% 382 3.9 31.0 14.6 FY15E 6,792 1,324 19.5% 568 5.9 20.8 10.9 FY16E 8,186 1,760 21.5% 864 8.9 13.7 8.0 Find Spark research on Bloomberg (SPAK <go>), Thomson First Call, Reuters Knowledge and Factset Promoters 60.1 Institutions 23.8 Public 16.1 Mukesh Saraf [email protected] +91 44 4344 0041 Rohit Krishna [email protected] +91 44 4344 0020 bearings globally. With global OEMs and Tier-1 suppliers looking to expand vendor base with every new platform, NRB has a large scope given its ability to customize and supply at competitive prices. Currently, Getrag and ZF are key customers and are expected to drive growth in the near future. We expect 25% exports CAGR from FY14-FY17. Margin improvement: We expect NRB’s EBITDA margin to go back to its peak levels of 22% in FY17 driven primarily by steep volume growth and better product mix through higher exports and improvement in CVs. Historically, margin movements have mirrored 2W and CV OEM volumes and the expected pick-up in volumes augurs well for NRB Our analysis comparing NRB to SKF India, FAG India and Timken India suggests that NRB is the only company with in- house R&D and no royalty payments. NRB’s EBITDA margins are the best due to absence of traded products, which is also the reason for lower asset turns. Working capital is the highest due to lower after market exposure, higher SKUs and exports resulting in inventory at overseas warehouses. Net/net NRB stacks well amongst the MNC peers and we believe margin, revenue growth (current cap utilization of 65-70%) along with debt reduction would result in ~20% ROCE by FY17

Transcript of NRB Bearings CMP - Spark Capitalmailers.sparkcapital.in/uploads/Mukesh/NRB_Bearings... · NRB...

NRB Bearings CMP

Rs. 122

Target

Rs. 155

Rating

Buy

Date Sep 23, 2014

Market Data

SENSEX 27207

Nifty 8146

Bloomberg NRBBR IN

Shares o/s 97mn

Market Cap Rs. 12bn

52-wk High-Low Rs. 133-31

3m Avg. Daily Vol Rs. 42mn

Index member BSESMCAP

Latest shareholding (%)

Initiating Coverage

Moving the needle

NRB Bearings (NRB) is the leading needle roller bearing supplier in India with a 70% market share. The companyhas created a niche by catering to customized requirements. With exposure to all domestic auto segments weexpect the OEM demand revival to result in strong domestic revenue growth (FY14-FY17: ~16% CAGR ). Exportsare expected to record 25% CAGR driven by new orders from key customers, Getrag and ZF. PAT CAGR of 43%from FY14-FY17 is driven by EBITDA margin improving to 22% in FY17. NRB is currently trading at (11.8x Sep’16EPS) a steep discount to its peers. We initiate with a Buy rating and TP of Rs. 155 based on 15x Sep’16 EPS

Strong domestic growth visible: NRB is among the few needle bearings manufacturers globally and has technology at

par with MNCs. The company maintains strong relationship with OEMs by way of partnering from conceptualisation stage

and manufacturing customized bearings. Key USP of NRB is to maintain large number of SKUs (2.5x that of nearest

competitor), ability to supply smaller batch sizes and faster turn around time. With exposure to 2W (25% of domestic), CV

(20%) and PV(20%) we expect domestic revenue to see strong growth with revival in CV and PV volumes and continued

growth in 2W volumes. After market business has seen slower growth as NRB focused on OEM and exports in the recent

years. However, with renewed focus and plans to supply kits in the aftermarket (including other complementary products)

we expect aftermarket growth to improve and record a CAGR of 13% from FY14 – FY17

Steep exports growth: NRB’s technology to manufacture needle roller bearings has been inherited through its

acquisitions of JVs with Nadella (France) and INA (Germany) who are currently among the leaders of needle roller

1

Stock performance (%)

1m 3m 12m

NRB 15% 53% 276%

Sensex 3% 8% 34%

BSE Auto 7% 23% 63%

Financial summary (Standalone)

YearRevenues (Rs. mn)

EBITDA (Rs. mn)

EBITDA Margin %

PAT (Rs. mn)

EPS (Rs.)

P/E (x)

EV/EBITDA (x)

FY14 5,945 1,006 16.9% 382 3.9 31.0 14.6

FY15E 6,792 1,324 19.5% 568 5.9 20.8 10.9

FY16E 8,186 1,760 21.5% 864 8.9 13.7 8.0

Find Spark research on Bloomberg (SPAK <go>), Thomson First Call, Reuters Knowledge and Factset

Promoters 60.1

Institutions 23.8

Public 16.1

Mukesh [email protected]+91 44 4344 0041

Rohit [email protected]+91 44 4344 0020

bearings globally. With global OEMs and Tier-1 suppliers looking to expand vendor base with every new platform, NRB

has a large scope given its ability to customize and supply at competitive prices. Currently, Getrag and ZF are key

customers and are expected to drive growth in the near future. We expect 25% exports CAGR from FY14-FY17.

Margin improvement: We expect NRB’s EBITDA margin to go back to its peak levels of 22% in FY17 driven primarily by

steep volume growth and better product mix through higher exports and improvement in CVs. Historically, margin

movements have mirrored 2W and CV OEM volumes and the expected pick-up in volumes augurs well for NRB

Our analysis comparing NRB to SKF India, FAG India and Timken India suggests that NRB is the only company with in-

house R&D and no royalty payments. NRB’s EBITDA margins are the best due to absence of traded products, which is

also the reason for lower asset turns. Working capital is the highest due to lower after market exposure, higher SKUs and

exports resulting in inventory at overseas warehouses. Net/net NRB stacks well amongst the MNC peers and we believe

margin, revenue growth (current cap utilization of 65-70%) along with debt reduction would result in ~20% ROCE by FY17

NRB Bearings CMP

Rs. 122

Target

Rs. 155

Rating

Buy

Corporate Factsheet

Promoter Background

NRB Bearings (NRB) was incorporated in 1965 as a JV between French needle bearing manufacturer Nadella SA (Timken

France SAS) and Sahney family to become the first needle bearing manufacturing company in India. In 2005, Sahney family

bought out Nadella’s 26% stake. In 2012, the company’s industrial bearing business was demerged as NRB Industrial

Bearing ltd in which the promoters own 72.6%.

Business

Needle roller bearings form ~10% of the Indian auto bearings industry and NRB has a ~70% market share in needle roller

bearings. The company has inherited the technology by way of its JV with Nadella and then by way of the acquisition of SNL

Bearings (which was a JV between INA Germany of Schaffeler group and Shriram Group). The company supplies to all the

auto segments and hence OEM segment growth is driven by volume growth for OEMs. After market growth is driven by

distribution reach and range (variety) of products. NRB is looking to expand exports significantly by way of working with the

customer from R&D stage for new technologies and products.

ManagementMr. Trilochan S. Sahney – Executive Chairman; Ms. Harshbeena S. Zaveri – MD & President

Mr. Satish C. Rangani – Executive Director ; Ms. Tanushree Bagrodia – CFO

Mr. Gagan Mathur – VP, Sales & Marketing (India & ASEAN) ; Mr. Sumit Mitra – VP, International Business & Supply Chain

Company Background

2

PresenceThe company has manufacturing facilities at Jalna, Waluj, Hyderabad, Aurangabad, Thane, Pantnagar, Ranchi and Thailand.

NRB’s after market business is catered to through its ~250 dealers and distributors

Corporate StructureThe promoters stake in NRB is 60.1% as of June 2014. The company has two subsidiaries – NRB Bearings (Thailand) ltd, a

100% subsidiary and SNL Bearings, 73.45% owned

Revenue ModelNeedle roller bearings comprise of 50% of the company’s revenue. Domestic (77% in FY14) could broadly be broken up into

2W: 24%, CV: 20%, PV: 20%, Farm & Off Highway: 16% and Aftermarket: 20%. Exports account for 23% of revenues.

Key Success Factors

Domestically NRB is the market leader in needle roller bearings. Needle roller bearings typically find application when space

is a constraint and load bearing capability is needed. Hence in most areas where automation is required and there is a

requirement for lighter parts needle roller bearing is applied. Simple example is when cars move from manual windows to

power windows. NRB’s USP comes from its ability to maintain large number of SKUs as its bearings are customised to a

large extent. Also the batch sizes could be significantly lower given the niche segment.

Credit Rating CRISIL: Long term AA-, Short Term A1+

Corporate Bankers BNP Paribas, Citibank N.A and DBS Bank

Auditors Deloitte Haskins & Sells

NRB Bearings CMP

Rs. 122

Target

Rs. 155

Rating

BuyManufacturing facilities strategically located near auto OEM hubs

NRB also has a facility in Thailand.

Currently 31% of revenues in Thailand is

from manufactured products and the

remainder are from trading revenues

(manufactured in India)

Location: Waluj, Maharashtra

Commenced: 1991

Location: Aurangabad, Maharashtra

Commenced: 1978

Products: Needle Rollers

Location: Pantnagar, Uttarakhand

Commenced: 2008

Products: Ball bearings, NF Cages, SL

Bushes, DB Bushes, CRB, NRB

Location: Ranchi, Jharkhand

Commenced: 1983

Products: Needle rollers, Needle

cages, Needle bearings,

3

Location: Hyderabad, Telangana

Commenced: 1992

Products: drawn cup cages, non

ferrous cages, turned cages, welded

cages, FS cages, thrust bearings, con

rod kits

Location: Jalna, Maharashtra

Commenced: 1982

Products: CRB, SRB, BB, NRB, TRB,

Textile bearings, wide inner ring bearing,

rings & sleeves, rocker arm bearings, ball

thrust cages

Commenced: 1991

Products: Bushes, crank pin, Big end

bearing, small end bearing, polymide

cage bearings, hub pin kits

Location: Thane, Maharashtra

Commenced: 1966

Products: Needle Bushes, Needle Cages

and Needle Bearings

NRB Bearings CMP

Rs. 122

Target

Rs. 155

Rating

Buy

NRB Bearings Revenue break-up

Source: Company, Spark Capital Research

2W30%

CV25%

PV25%

Farm/Off highway/Others

20%

Needle roller bearings form 50% of revenues

Source: Company, Spark Capital Research; CRB: Cylindrical roller bearing, SRB: Spherical,

TRP: Taper, BB: Ball bearing

CRB16%

BB8% SRB

1%

TRB3%

Needle Roller Bearings

50%

Others22%

OEM62%

After Market15%

Exports23%

NRB supplies to all segments within autos

4

Source: Company, Spark Capital Research TRP: Taper, BB: Ball bearing

Domestic revenues historically have mirrored 2W volumes

Source: Company, Spark Capital Research, SIAM

-20%

-10%

0%

10%

20%

30%

40%

FY

03

FY

04

FY

05

FY

06

FY

07

FY

08

FY

09

FY

10

FY

11

FY

12

FY

13

FY

14

Domestic Revenue YoY % 2 & 3 Wheeler industry YoY growth %

Export revenues have recorded steep revenue growth in recent past

Source: Company, Spark Capital Research

0

200

400

600

800

1000

1200

1400

1600

FY

02

FY

03

FY

04

FY

05

FY

06

FY

07

FY

08

FY

09

FY

10

FY

11

FY

12

FY

13

FY

14

NRB Bearings CMP

Rs. 122

Target

Rs. 155

Rating

BuyBearings Industry in India

Indian Bearings Industry (Rs. 95bn in FY12, down to Rs. 75bn in FY14)

Source: Industry, Spark Capital Research * industry break-up as per FY12

Tapered42%

Cylindrical29%

Spherical17%

Needle9%

Thrust4%

Roller Bearing52%

Ball Bearing48%

After Market35%

OEM65%

Imports38%

Organised46%

Unorganised16%

Electrical equipment

5%

Heavy Industries

20%

General Engineering

27%

Automotive48%

5

ProductsProductsSource: Industry, Spark Capital Research * industry break-up as per FY12

Indigenous and Imported composition

Source: Industry, Spark Capital Research

Indegenous62%

Imported38%

•Unorganised bearings primarily represent small scale manufacturers and suppliers of spurious bearings.

These generally have strong regional presence and cater to the replacement markets for both industrial

and automotive segments

• Imported bearings account for ~40% of total Indian bearings industry. Imported bearings are primarily

used in the industrial markets, whereas automobile markets are catered to by manufactured bearings

• Industrial segment typically requires customisation, large sized bearings and maintaining large number

of SKUs. Volumes for a particular type of bearings wouldn’t be large (as in the case of automobiles),

while portfolio of products would be large. Hence the major players in this segment prefer to cater to the

demand via imports

•Most bearing manufacturers in India are MNCs having technology backing from the parent company or

have technology that has been acquired from MNCs.

•Each of the manufacturers have specialised in certain bearing types and maintain market shares in the

respective segments

NRB Bearings CMP

Rs. 122

Target

Rs. 155

Rating

Buy

Types of roller bearings, applications and major players

Type of

bearingApplication Major players

Major Market

Share

Tapered

roller bearings

Vehicle front wheels, differential & pinion configurations, conveyor rolls,

machine tool spindles, trailer wheels

SKF India, FAG Bearings Limited,

NEI, Timken India, ABC Bearings

TIMKEN: 45%

Cylindrical

roller bearings

Cement and coal pulverizers, pumps, compressors, gear boxes, centrifuges,

mining equipment, transmissions

NEI, SKF India, FAG Bearings, NRB

BearingsFAG: 45%

Spherical Gearboxes, casters, aggregates, heavy

Each of the top companies have a niche and technology is from MNC parent/collaboration

Market share of top 5 players

Source: Spark Capital Research

SKF30%

FAG18%

NEI (NBC)13%

NRB8%

Timken8%

Most manufacturers have a technical collaboration with MNCs

6

Spherical

roller bearings

Gearboxes, casters, aggregates, heavy stationary, industrial conveyor systems,

industrial fans

SKF India, FAG Bearings, NEI

FAG: 45%

Needle roller

bearings

Transmissions, transfer cases, engines and valve trains, steering and braking

systems, axle supports, outboard engines, power tools, copiers

INA Bearings, SKF India, NRB Bearings

NRB: 70%

Thrust roller

bearings

Classifiers, extruders, oil well swivels, pumps, pulp refiners, machine tools

SKF India, FAG Bearings, Timken

India

-

Ball Bearings

Wide applications in 2W, 3W and four wheelers. Used primarily in wheels and

axles

SKF India, FAG Bearings, Timken

India, ABC Bearings, NEI

SKF 65%

Source: Industry, Spark Capital Research

Company Technology Relationship Specialisation

SKF India SKF, Sweden Subsidiary Ball bearings

FAG India FAG, Germany SubsidiaryCylindrical & Spherical roller bearings

Timken India Timken, USA Subsidiary Taper roller bearings

NRB BearingsNadella (France) and INA (Germany)

Acquisition Needle roller bearings

ABC Bearing NSK JapanJV / Technical Collaboration

Ball bearings

NEI Bearings NTN JapanTechnical Collaboration

Ball and Taper roller bearings

Koyo India JTEKT Corp, Japan SubsidiarySingle ball bearing,Taper roller bearings

Bimetal Bearings

Clevite Inc, USATechnical Collaboration

Engine bearings

Source: Industry, Spark Capital Research

NRB Bearings CMP

Rs. 122

Target

Rs. 155

Rating

Buy

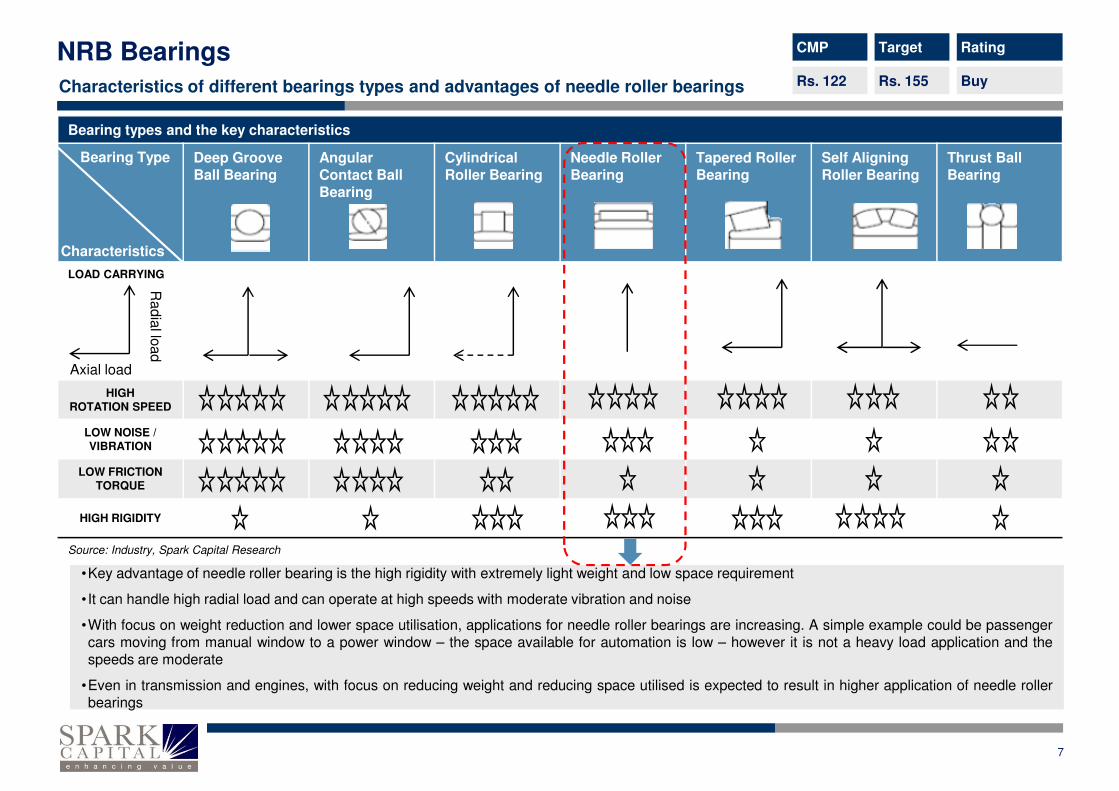

Bearing types and the key characteristics

Deep Groove Ball Bearing

Angular Contact Ball Bearing

Cylindrical Roller Bearing

Needle Roller Bearing

Tapered Roller Bearing

Self AligningRoller Bearing

Thrust Ball Bearing

LOAD CARRYING

HIGH

Bearing Type

Characteristics

Axial load

Radia

l load

Characteristics of different bearings types and advantages of needle roller bearings

HIGH ROTATION SPEED

LOW NOISE / VIBRATION

LOW FRICTIONTORQUE

HIGH RIGIDITY

Source: Industry, Spark Capital Research

7

•Key advantage of needle roller bearing is the high rigidity with extremely light weight and low space requirement

• It can handle high radial load and can operate at high speeds with moderate vibration and noise

•With focus on weight reduction and lower space utilisation, applications for needle roller bearings are increasing. A simple example could be passenger

cars moving from manual window to a power window – the space available for automation is low – however it is not a heavy load application and the

speeds are moderate

•Even in transmission and engines, with focus on reducing weight and reducing space utilised is expected to result in higher application of needle roller

bearings

NRB Bearings CMP

Rs. 122

Target

Rs. 155

Rating

BuyNRB leads in operating margins; has meaningful R&D spend and zero royalty payments

NRB has among the best gross margin for manufactured bearings

FY11/CY10 FY12/CY11 FY13/CY12 FY14/CY13

NRB 52.2% 55.1% 52.4% 51.1%

SKF 52.9% 51.9% 48.6% 51.6%

FAG 50.4% 49.9% 49.2% 47.6%

TIMKEN NA 42.8% 41.5% 44.7%

EBITDA margin differential reflects the impact of traded bearings

FY11/CY10 FY12/CY11 FY13/CY12 FY14/CY13

NRB 22.1% 19.6% 16.2% 16.9%

SKF 13.5% 12.3% 11.6% 11.5%

FAG 18.0% 19.6% 15.2% 12.8%

TIMKEN 15.2% 12.8% 10.7% 9.9%

• NRB Bearings gross margins are comparable to the margins

made by the other large (MNC) bearing makers for the

manufactured bearings. This we believe is from the fact that the

company enjoys 70% market share in the segment that it

specialises

• EBITDA margins are significantly higher than the other bearing

manufacturers given that the others trade in bearing catering to

the industrial segment

• While the improvement in end markets (auto and industrial) are

expected to drive margins up for all bearing manufacturers, we

expect NRB’s EBITDA margins to record a steep improvement

and go back towards its historical peak margin of 22%+

8

Only NRB has a meaningful R&D spend

FY11/CY10 FY12/CY11 FY13/CY12 FY14/CY13

NRB 0.8% 1.0% 1.2% 1.3%

SKF - - - -

FAG 0.4% 0.5% 0.7% 0.9%

TIMKEN - - - -

Other companies have royalty payments to the parent

FY11/CY10 FY12/CY11 FY13/CY12 FY14/CY13

NRB - - - -

SKF 3.4% 5.0% 4.0% 5.0%

FAG 2.5% 2.4% 2.5% 2.3%

TIMKEN NA 2.9% 3.0% 3.5%

Source: Company, Spark Capital; Royalty payments are as a % of revenues ex-trading

• NRB has absorbed the technology to manufacture needle roller

bearings by way of it buying out its JV partner (Nadella) and

acquisition (INA’s JV with)

• Apart from NRB, only FAG has spent on R&D. We believe this

could be a factor of FAG planning to increase manufacture of

Industrial bearings in India and make it an export hub

• Absence of R&D and dependence on the parent company also

reflects in the royalty that has been paid by SKF, FAG and

Timken. However, NRB has no royalty payments as all the

technology is internalised

NRB Bearings CMP

Rs. 122

Target

Rs. 155

Rating

Buy

Lower ROCE as working capital is high and asset turns is lower

FY11/CY10 FY12/CY11 FY13/CY12 FY14/CY13

NRB 17.9% 13.7% 11.4% 9.3%

SKF 20.9% 22.4% 17.5% 11.4%

FAG 21.6% 24.2% 16.0% 9.7%

TIMKEN 12.1% 18.8% 12.3% 10.4%

ROE is higher as NRB is the only company having leverage

FY11/CY10 FY12/CY11 FY13/CY12 FY14/CY13

NRB 25.9% 20.8% 20.6% 17.1%

SKF 22.6% 22.4% 17.5% 14.9%

FAG 23.5% 27.0% 19.8% 13.0%

TIMKEN 14.4% 23.3% 13.5% 12.4%

• NRB’s ROCE is on the lower end vs. peers despite better

operating margin as the company has lower asset turnover and

higher working capital requirement

• ROE is however higher than peers as NRB had a leveraged

balance sheet, while others are debt free

Return ratios are at the lower end as working capital is high and asset turns are low

9

Gross fixed asset turns lower due to absence of traded revenues

FY11/CY10 FY12/CY11 FY13/CY12 FY14/CY13

NRB 1.3 1.3 1.3 1.2

SKF 2.7 2.9 2.4 2.3

FAG 2.5 2.9 2.7 2.1

TIMKEN 2.3 3.7 2.8 2.7

Working capital days is highest among peers

FY11/CY10 FY12/CY11 FY13/CY12 FY14/CY13

NRB 118 131 144 154

SKF 30 47 49 54

FAG 28 42 55 56

TIMKEN 86 68 110 109

Source: Company, Spark Capital; Royalty payments are as a % of revenues ex-trading

• NRB’s gross fixed asset turnover is lower than peers due to the

absence of traded revenues for NRB

• Assuming only manufactured revenue for peers NRB’s fixed asset

turnover ratio is in-line with peers

• Working capital days for NRB is higher primarily driven by higher

inventory and debtors

NRB Bearings CMP

Rs. 122

Target

Rs. 155

Rating

Buy

Inventory days

FY11/CY10 FY12/CY11 FY13/CY12 FY14/CY13

NRB 83 85 86 82

SKF 65 63 63 65

FAG 44 45 36 44

TIMKEN 83 66 76 70

Debtor days

FY11/CY10 FY12/CY11 FY13/CY12 FY14/CY13

NRB 83 89 101 120

SKF 48 56 54 54

FAG 46 60 64 74

TIMKEN 65 48 70 76

• Inventory and debtor days for NRB is higher than peers driven by

• Lower sales from aftermarket business

• Company maintains a large number of SKUs – as high as

2.5x the nearest competitor. NRB has more customised

bearings and lower off the shelf bearings

• Exports business requires maintaining inventory at

warehouses situated in different geography’s

Working capital higher due to revenue mix, absence of trading revenue and higher SKUs

10

• Peers have trading revenues where the billing to the

customers is directly done by the parent companyCreditor days

FY11/CY10 FY12/CY11 FY13/CY12 FY14/CY13

NRB 48 43 43 48

SKF 84 72 68 64

FAG 62 63 45 61

TIMKEN 62 46 35 38

Imported content in raw material costs

FY11/CY10 FY12/CY11 FY13/CY12 FY14/CY13

NRB 28% 30% 28% 28%

SKF 45% 43% 21% 27%

FAG 28% 30% 34% 36%

TIMKEN 38% 36% 36% 27%

Source: Company, Spark Capital; Royalty payments are as a % of revenues ex-trading

• Imported content in the bearings is comparable across the board

NRB Bearings CMP

Rs. 122

Target

Rs. 155

Rating

BuyNRB’s operating margins are more predictable given exposure only to the auto segment

NRB has lower exposure to the aftermarket and no supplies in the industrial segment

NRB SKF FAG Timken

Auto -

Domestic77% 45% 35% 17%

OEM 62% 30% 23% NA

After

Market 15%15%

12%NA

Industrial -

Domestic -47% 51% 30%

OEM-

15%33%

NA

After

Market -32%

18%NA

Exports 23% 8% 14% 33%

Source: Company, Spark Capital Research; * Approx

NRB EBITDA margins are more predictable as they move in tandem with 2W & CV

Source: Company, Spark Capital Research

12.0%

14.0%

16.0%

18.0%

20.0%

22.0%

24.0%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

FY

03

FY

04

FY

05

FY

06

FY

07

FY

08

FY

09

FY

10

FY

11

FY

12

FY

13

FY

14

2 & 3W YoY growth % NRB EBITDA margin % (RHS)

12.0%

14.0%

16.0%

18.0%

20.0%

22.0%

24.0%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

FY

03

FY

04

FY

05

FY

06

FY

07

FY

08

FY

09

FY

10

FY

11

FY

12

FY

13

FY

14

Commercial Vehicles NRB EBITDA margin % (RHS)

11

Source: Company, Spark Capital Research; * Approx numbers

Source: Company, Spark Capital Research

SKF, FAG and TIMKEN margins are not so predictable and do not move in tandem with key end-market volumes due to traded bearings segment

Source: Spark Capital Research

10%

12%

14%

16%

18%

20%

22%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

FY

03

FY

04

FY

05

FY

06

FY

07

FY

08

FY

09

FY

10

FY

11

FY

12

FY

13

FY

14

PV Industry growth YoY % SKF EBITDA margin %

10%

12%

14%

16%

18%

20%

22%

24%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

FY

03

FY

04

FY

05

FY

06

FY

07

FY

08

FY

09

FY

10

FY

11

FY

12

FY

13

FY

14

PV Industry growth YoY % FAG EBITDA margin %

8%

10%

12%

14%

16%

18%

20%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

FY

03

FY

04

FY

05

FY

06

FY

07

FY

08

FY

09

FY

10

FY

11

FY

12

FY

13

FY

14

CV Industry growth YoY % TIMKEN EBITDA margin %

NRB Bearings CMP

Rs. 122

Target

Rs. 155

Rating

BuyStrong visibility in OEM; exports & aftermarket driven by new orders and renewed focus

OEM revenue growth to be aided by 2W, PV & CV

Export growth expected on the back of new orders

-

1,000

2,000

3,000

4,000

5,000

6,000

FY10 FY11 FY12 FY13 FY14 FY15E FY16E FY17E

(Rs.

mn)

FY10-FY14: 13%

FY14-FY17: 15.5%

2,500

3,000 FY10-FY14: 71%

FY14-FY17: 25%

FY10-FY14: 71%

FY14-FY17: 25%

•FY14 – FY17 CAGR expectations - 2W: 14%, CV: 23%, PV: 15%, Others: 9%

•1) Technology is at par with MNCs 2) Maintains large SKUs (2.5x of the nearest

competitor) 3) Customisation of products as NRB works from design stage with

OEMs 4) Willingness to supply lower batch sizes 5) low turn around time

•Currently among the bearings used in a 2W, 65% are needle roller and in a 4W, 35%

are needle roller. With more electronics and automation in 4W and the requirement to

make the engines, transmission and steering lighter and more compact, we expect

the application of needle roller bearings to increase over time

•Key customers- 2W: HMCL, BJAUT, HMSI; 4W & CV: TAMO, MM, AL, MSIL. Key

competitors include INA (Schaeffler group), Koyo, SKF and NSK

•NRB is among the few manufacturers of needle roller bearings globally. Focus on

exports by way of working with the customer from the design stage is resulting in

bagging orders

•1) Most OEMs and Tier 1 suppliers looking to add vendor as currently very few

12

After market growth to be aided by renewed focus

-

500

1,000

1,500

2,000

FY10 FY11 FY12 FY13 FY14 FY15E FY16E FY17E

(Rs.

mn)

-

200

400

600

800

1,000

1,200

1,400

FY10 FY11 FY12 FY13 FY14 FY15E FY16E FY17E

(Rs.

mn)

FY10-FY14: 71%

FY14-FY17: 25%

FY10-FY14: 8.5%

FY14-FY17: 13%

•1) Most OEMs and Tier 1 suppliers looking to add vendor as currently very few

vendors for needle roller bearings 2) Cost advantage 3) Technology at par with

MNCs 4) High customisation and willingness to supply low batch sizes 5) low turn

around time

•Key customers include Getrag, ZF, John Deere, GKN. Key competitors: INA, Koyo,

Nadella, NSK among others

•Low growth in the last four years as focus was on OEM segment

•Distribution network (~250) in place and the company plans to focus on the segment

by building the brand in the mechanic circles by showcasing the product range and

product quality

•NRB offers higher range of products than competitors. Replacement market for

needle roller bearing used in gear box etc is lower, however other applications such

as clutch, wheel and steering have a replacement market

•NRB is planning to supply aftermarket ‘kits’ which would include grease and other

related (complementary) products along with needle bearings

NRB Bearings CMP

Rs. 122

Target

Rs. 155

Rating

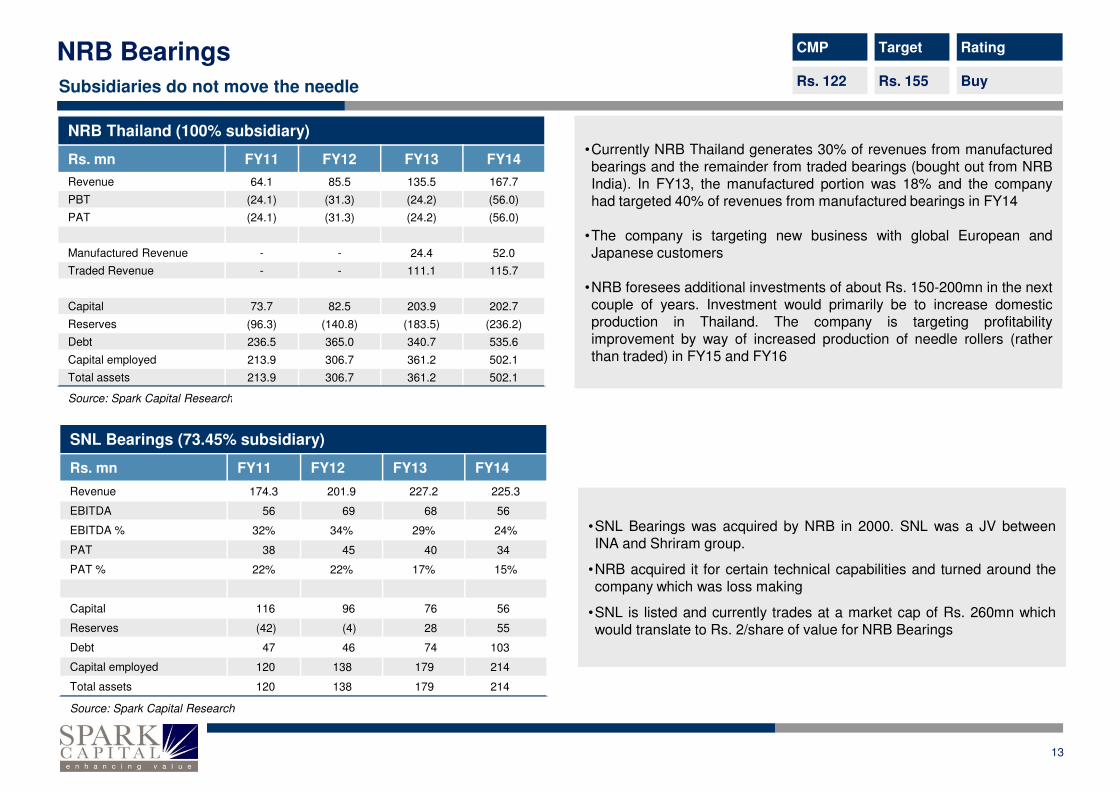

BuySubsidiaries do not move the needle

NRB Thailand (100% subsidiary)

Rs. mn FY11 FY12 FY13 FY14

Revenue 64.1 85.5 135.5 167.7

PBT (24.1) (31.3) (24.2) (56.0)

PAT (24.1) (31.3) (24.2) (56.0)

Manufactured Revenue - - 24.4 52.0

Traded Revenue - - 111.1 115.7

Capital 73.7 82.5 203.9 202.7

Reserves (96.3) (140.8) (183.5) (236.2)

Debt 236.5 365.0 340.7 535.6

Capital employed 213.9 306.7 361.2 502.1

Total assets 213.9 306.7 361.2 502.1

Source: Spark Capital Research

•Currently NRB Thailand generates 30% of revenues from manufactured

bearings and the remainder from traded bearings (bought out from NRB

India). In FY13, the manufactured portion was 18% and the company

had targeted 40% of revenues from manufactured bearings in FY14

•The company is targeting new business with global European and

Japanese customers

•NRB foresees additional investments of about Rs. 150-200mn in the next

couple of years. Investment would primarily be to increase domestic

production in Thailand. The company is targeting profitability

improvement by way of increased production of needle rollers (rather

than traded) in FY15 and FY16

13

Source: Spark Capital Research

SNL Bearings (73.45% subsidiary)

Rs. mn FY11 FY12 FY13 FY14

Revenue 174.3 201.9 227.2 225.3

EBITDA 56 69 68 56

EBITDA % 32% 34% 29% 24%

PAT 38 45 40 34

PAT % 22% 22% 17% 15%

Capital 116 96 76 56

Reserves (42) (4) 28 55

Debt 47 46 74 103

Capital employed 120 138 179 214

Total assets 120 138 179 214

Source: Spark Capital Research

•SNL Bearings was acquired by NRB in 2000. SNL was a JV between

INA and Shriram group.

•NRB acquired it for certain technical capabilities and turned around the

company which was loss making

•SNL is listed and currently trades at a market cap of Rs. 260mn which

would translate to Rs. 2/share of value for NRB Bearings

NRB Bearings CMP

Rs. 122

Target

Rs. 155

Rating

BuyCorporate guarantees to group companies is a risk

Related party transactions

Rs. mn SNL Bearings NRB Thailand NRB Industrial Bearings Ltd

TransactionPayables as at

March'14Transaction

Receivables as on

March'14Transaction

Receivables as on

March'14

Sale of raw materials / fixed assets 12.4 - 85.2 - 36.6 172.7

Purchase of raw materials / fixed assets 125.3 33.1 46.4 - 52.2 -

Proceeds from redemption of cumulative pref. shares 20.0 - - - - -

Inter corporate deposit given - - 24.9 - 61.7 -

Interest received on Inter Corporate deposit - - 1.9 - 1.0 -

Stand by letter of credit given by NRB Bearings Ltd - - - 60.7 - -

Guarantee given by NRB Bearings Ltd - - - 112.6 - 635.6

Source: Spark Capital Research

14

Source: Spark Capital Research

•NRB Industrial bearings ltd (NIBLB) was demerged from NRB Bearings in October 2012.

NRBIB is ~73% promoter owned entity and is in the business of manufacturing needle roller

bearings for process industries.

•NRB bearings and NIBL have a non-compete agreement wherein NRB bearings can only

cater to motion industries. We are given to understand that the non-compete agreement is

valid until 2016.

•Related part transactions suggest that NRB Bearings has provided guarantees to NRBL for

Rs. 635.6mn and also an inter corporate deposit of Rs. 61.7mn. Recently, NRB also sought

shareholders approval to increase the amount of corporate guarantee to Rs. 900mn till 30th

September 2018. It also proposed to increase the limit of inter corporate deposits to Rs.

200mn to meet the loan obligations under the corporate guarantee already given by NRB.

•While this means that the total outstanding for NIBL would not exceed Rs. 900mn, we believe

this is a risk for NRB.

NRB Industrial Bearings Ltd.

Rs. mn Dec’2013 (15 months)

Revenue 300.2

EBITDA (129.4)

EBITDA % -43%

PAT (242.3)

PAT % -81%

Capital 48

Reserves 338

Debt 1,101

Capital employed 1,488

Total assets 1,488

Source: Spark Capital Research

NRB Bearings CMP

Rs. 122

Target

Rs. 155

Rating

Buy

NRB 12 months forward PE band

Source: Bloomberg, Spark Capital Research

SKF 12 months forward PE band

Source: Bloomberg, Spark Capital Research

16.0x

11.0x

6.0x

26.0x

21.0x

0

200

400

600

800

1000

1200

1400

Mar-

06

Jul-

06

No

v-0

6

Mar-

07

Jul-

07

No

v-0

7

Mar-

08

Jul-

08

No

v-0

8

Mar-

09

Jul-

09

No

v-0

9

Mar-

10

Jul-

10

No

v-1

0

Mar-

11

Jul-

11

No

v-1

1

Mar-

12

Jul-

12

No

v-1

2

Mar-

13

Jul-

13

No

v-1

3

Mar-

14

Jul-

14

11.0x

8.0x

5.0x

17.0x

14.0x

0

20

40

60

80

100

120

140

Mar-

06

Jul-

06

No

v-0

6

Mar-

07

Jul-

07

No

v-0

7

Mar-

08

Jul-

08

No

v-0

8

Mar-

09

Jul-

09

No

v-0

9

Mar-

10

Jul-

10

No

v-1

0

Mar-

11

Jul-

11

No

v-1

1

Mar-

12

Jul-

12

No

v-1

2

Mar-

13

Jul-

13

No

v-1

3

Mar-

14

Jul-

14

NRB trades at a steep discount to its peers

15

Source: Bloomberg, Spark Capital Research Source: Bloomberg, Spark Capital Research

FAG 12 months forward PE band

Source: Bloomberg, Spark Capital Research

TIMKEN 12 months forward PE band

Source: Bloomberg, Spark Capital Research

22.0x

17.0x

12.0x

32.0x

27.0x

0

100

200

300

400

500

600

Feb-0

7

Jun

-07

Oct-

07

Feb-0

8

Jun

-08

Oct-

08

Feb-0

9

Jun

-09

Oct-

09

Feb-1

0

Jun

-10

Oct-

10

Feb-1

1

Jun

-11

Oct-

11

Feb-1

2

Jun

-12

Oct-

12

Feb-1

3

Jun

-13

Oct-

13

Feb-1

4

Jun

-14

17.0x

12.0x

7.0x

27.0x

22.0x

0

500

1000

1500

2000

2500

3000

3500

Mar-

06

Jul-

06

No

v-0

6

Mar-

07

Jul-

07

No

v-0

7

Mar-

08

Jul-

08

No

v-0

8

Mar-

09

Jul-

09

No

v-0

9

Mar-

10

Jul-

10

No

v-1

0

Mar-

11

Jul-

11

No

v-1

1

Mar-

12

Jul-

12

No

v-1

2

Mar-

13

Jul-

13

No

v-1

3

Mar-

14

Jul-

14

NRB Bearings CMP

Rs. 122

Target

Rs. 155

Rating

BuyPeer comparison

CMP MCAP Revenue (Rs. mn) EBITDA (Rs. mn) EBITDA Margin %

Rs. Rs. mn FY14 FY15E FY16E FY17E FY14 FY15E FY16E FY17E FY14 FY15E FY16E FY17E

NRB 122 11,728 5,945 6,792 8,186 9,716 1,006 1,324 1,760 2,138 16.9% 19.5% 21.5% 22.0%

SKF India 1,109 58,480 22,750 24,961 30,593 36,553 2,614 3,219 4,130 5,008 11.5% 12.9% 13.5% 13.7%

Timken India 418 28,389 7,201 9,277 11,386 13,094 716 1,438 1,879 2,226 9.9% 15.5% 16.5% 17.0%

FAG India 2,920 48,530 14,300 16,800 20,604 - 1,836 2,482 3,223 - 12.8% 14.8% 15.6% -

SKF and FAG : CY13, CY14, CY15, CY16; FAG and Timken based on Consensus

16

PAT EPS P/E EV/EBITDA

FY14 FY15E FY16E FY17E FY14 FY15E FY16E FY17E FY14 FY15E FY16E FY17E FY14 FY15E FY16E FY17E

NRB 382 568 864 1,1323.9 5.9 8.9 11.7

30.7 x 20.7 x 13.6 x 10.4 x 14.2 x 10.8 x 8.1 x 6.7 x

SKF India 1,809 2,252 2,918 3,63034.3 42.7 55.3 68.8

32.3 x 26.0 x 20.0 x 16.1 x 20.3 x 16.5 x 12.9 x 10.6 x

Timken India 447 888 1,175 2,0556.6 13.1 17.3 30.2

63.4 x 32.0 x 24.2 x 13.8 x 39.6 x 19.7 x 15.1 x 12.7 x

FAG India 1,218 1,730 2,245 -73.3 106.6 143.0

- 39.8 x 27.4 x 20.4 x - 23.8 x 17.6 x 13.6 x -

SKF and FAG : CY13, CY14, CY15, CY16; FAG and Timken based on Consensus

SKF and FAG : CY13, CY14, CY15, CY16; FAG and Timken based on Consensus

NRB Bearings CMP

Rs. 122

Target

Rs. 155

Rating

BuyAbridged standalone financials

Abridged Financial Statements Key metrics

Rs. mn FY14 FY15E FY16E FY17E FY14 FY15E FY16E FY17E

Profit & Loss Growth ratios

Revenues 5,945 6,792 8,186 9,716 Revenues 2.6% 14.3% 20.5% 18.7%

Manufacturing & Other Expenses 4,939 5,468 6,426 7,579 EBITDA 7.4% 31.6% 32.9% 21.5%

EBITDA 1,006 1,324 1,760 2,138 PAT -18.8% 48.7% 52.2% 31.0%

Depreciation 333 355 388 415 Margins

EBIT 673 970 1,372 1,722 EBITDA 16.9% 19.5% 21.5% 22.0%

Net Interest Exp / (inc) 172 190 172 142 EBIT 11.3% 14.3% 16.8% 17.7%

Profit Before Tax 547 811 1,235 1,618 PAT 6.4% 8.4% 10.6% 11.7%

Tax 165 243 370 485 Leverage & WC ratios

Adj. Net Profit 382 568 864 1,132 Debt to equity (x) 1.2 1.1 0.7 0.5

Balance Sheet (Rs. mn) Current ratio (x) 0.6 0.6 0.5 0.4

Shareholders Equity 2,367 2,737 3,310 4,094 Debtor days (Sales) 120 110 100 90

17

Loan funds 2,930 2,930 2,367 2,017 Inventory days (COGS) 82 82 83 85

Sources of funds 5,412 5,782 5,792 6,226 Creditor Days (COGS) 48 47 45 43

Net block 2,026 2,301 2,263 2,298 Performance & turnover ratios

Investments 209 209 209 209 RoACE 9.3% 12.1% 16.6% 20.1%

Capital WIP 330 0 0 0 RoAE 17.1% 22.3% 28.6% 30.6%

Current assets, loans & advances 773 773 773 773 Total asset turnover (x) 0.8 0.8 0.9 1.0

Current liabilities & provisions 1,203 1,406 1,680 1,924 Fixed asset turnover (x) 1.2 1.3 1.4 1.6

Net Current Assets 2,847 3,272 3,320 3,719 Valuation metrics

Application of funds 5,412 5,782 5,792 6,226 Current price (Rs.)

Cash Flows (Rs. mn) Shares outstanding (mn) 97 97 97 97

Cash flows from operations 607 735 916 1,185 Market capitalisation (Rs. mn) 11,825 11,825 11,825 11,825

Capex 546 300 350 450 Enterprise value (Rs. mn) 14,704 14,392 14,024 13,580

Free Cash Flow 61 435 566 735 EV/EBIDTA (x) 14.6 10.9 8.0 6.4

Cash flows from investments (588) (300) (350) (450) Adj. Per-share earnings (Rs.) 3.9 5.9 8.9 11.7

Cash flows from financing (3) (124) (761) (641) Price-earnings multiple (x) 31.0 20.8 13.7 10.4

Cash & Cash equivalents 51 363 167 262 Dividend yield (%) 0.9% 1.4% 2.0% 2.5%

122

NRB Bearings CMP

Rs. 122

Target

Rs. 155

Rating

Buy

Absolute Rating Interpretation

Buy Stock expected to provide positive returns of >15% over a 1-year horizon

Add Stock expected to provide positive returns of >5% – <15% over a 1-year horizon

Reduce Stock expected to provide returns of <5% – -10% over a 1-year horizon

Sell Stock expected to fall >10% over a 1-year horizon

Spark Disclaimer

Spark Capital Advisors (India) Private Limited (Spark Capital) and its affiliates are engaged in investment banking, investment advisory and institutional equities. Spark Capital is registered with

SEBI as a Stock Broker and Category 1 Merchant Banker.

This document does not constitute or form part of any offer or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction. This document is

provided for assistance only and is not intended to be and must not alone be taken as the basis for an investment decision. Nothing in this document should be construed as investment or financialadvice, and nothing in this document should be construed as an advice to buy or sell or solicitation to buy or sell the securities of companies referred to in this document.

Each recipient of this document should make such investigations as it deems necessary to arrive at an independent evaluation of an investment in the securities of companies referred to in this

document (including the merits and risks involved), and should consult its own advisors to determine the merits and risks of such an investment. This document is being supplied to you solely fordocument (including the merits and risks involved), and should consult its own advisors to determine the merits and risks of such an investment. This document is being supplied to you solely foryour information and may not be reproduced, redistributed or passed on, directly or indirectly, to any other person or published, copied, in whole or in part, for any purpose. This report is not

directed or intended for distribution to or use by any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution, publication,availability or use would be contrary to law, regulation or which would subject Spark Capital and/or its affiliates to any registration or licensing requirement within such jurisdiction. The securitiesdescribed herein may or may not be eligible for sale in all jurisdictions or to a certain category of investors. Persons in whose possession this document may come are required to inform

themselves of and to observe such applicable restrictions. This material should not be construed as an offer to sell or the solicitation of an offer to buy any security in any jurisdiction where such anoffer or solicitation would be illegal.

Spark Capital makes no representation or warranty, express or implied, as to the accuracy, completeness or fairness of the information and opinions contained in this document. Spark Capital , itsaffiliates, and the employees of Spark Capital and its affiliates may, from time to time, effect or have effected an own account transaction in, or deal as principal or agent in or for the securitiesmentioned in this document. They may perform or seek to perform investment banking or other services for, or solicit investment banking or other business from, any company referred to in this

report.

This report has been prepared on the basis of information, which is already available in publicly accessible media or developed through an independent analysis by Spark Capital. While we would

endeavour to update the information herein on a reasonable basis, Spark Capital and its affiliates are under no obligation to update the information. Also, there may be regulatory, compliance orother reasons that prevent Spark Capital and its affiliates from doing so. Neither Spark Capital nor its affiliates or their respective directors, employees, agents or representatives shall beresponsible or liable in any manner, directly or indirectly, for views or opinions expressed in this report or the contents or any errors or discrepancies herein or for any decisions or actions taken in

reliance on the report or the inability to use or access our service in this report or for any loss or damages whether direct or indirect, incidental, special or consequential including without limitationloss of revenue or profits that may arise from or in connection with the use of or reliance on this report.

Spark Capital and/or its affiliates and/or employees may have interests/positions, financial or otherwise in the securities mentioned in this report. To enhance transparency, Spark Capital has incorporated a disclosure of interest statement in this document. This should however not be treated as endorsement of views expressed in this report:

NRB Bearings CMP

Rs. 122

Target

Rs. 155

Rating

Buy

Analyst Certification of Independence

The views expressed in this research report accurately reflect the analyst’s personal views about any and all of the subject securities or issuers; and no part of the researchanalyst’s compensations was, is or will be, directly or indirectly, related to the specific recommendation or views expressed in the report.

Additional Disclaimer for US Institutional Investors

This research report prepared by Spark Capital Advisors (India) Private Limited is distributed in the United States to US Institutional Investors (as defined in Rule 15a-6 under the SecuritiesExchange Act of 1934, as amended) only by Decker & Co, LLC, a broker-dealer registered in the US (registered under Section 15 of Securities Exchange Act of 1934, as amended). Decker &

Co accepts responsibility on the research reports and US Institutional Investors wishing to effect transaction in the securities discussed in the research material may do so through Decker & Co.All responsibility for the distribution of this report by Decker & Co, LLC in the US shall be borne by Decker & Co, LLC. All resulting transactions by a US person or entity should be effectedthrough a registered broker-dealer in the US. This report is not directed at you if Spark Capital Advisors (India) Private Limited or Decker & Co, LLC is prohibited or restricted by any legislation

or regulation in any jurisdiction from making it available to you. You should satisfy yourself before reading it that Decker & Co, LLC and Spark Capital Advisors (India) Private Limited arepermitted to provide research material concerning investment to you under relevant legislation and regulations;

Disclosure of interest statement Yes/No

Analyst ownership of the stock No

Group/directors ownership of the stock No

19

Group/directors ownership of the stock No

Broking relationship with the company covered No

Investment banking relationship with the company covered No