MBT BUY JAPHET LOUIS O. TANTIANGCO · MBT BUY Last Traded Price 67.50 Entry Point 64.00 - 68.00...

10

Philstocks Research 2019 |Page CLAIRE T. ALVIAR Research Associate (632)588-1925 Ground Floor, East Tower PSE Center, Tektite Towers Ortigas Center, Pasig City PHILIPPINES JAPHET LOUIS O. TANTIANGCO Sr. Research Analyst (632)588-1927 PIPER CHAUCER E. TAN Engagement Officer/Research Associate (632)588-1928 JUSTINO B. CALAYCAY, JR AVP-Head, Research & Engagement (632)588-1962 Philstocks Research DISCLAIMER The opinion, views and recommendations contained in this material were prepared by the Philstocks Research Team, individually and separately, based on their specific sector assignments, contextual framework, personal judgments, biases and prejudices, time horizons, methods and other factors. The reader is enjoined to take this into account when perusing and considering the contents of the report as a basis for their stock investment or trading decisions. Furthermore, projection made and presented in this report may change or be updated in between the periods of release. Ergo, the validity of the projections and/or estimates mentioned are good as of the date indicated and may be changed without immediate notification. This report is primarily intended for information purposes only and should not be considered as an exclusive basis for making investment decision. The recommendations contained in this report is not tailored-fit any particular investor type, situation, or objective and must not be taken as such. Determining the suitability of an investment remains within the province of the investor. Our estimates are based on information we believe to be reliable. Nevertheless, nothing in this report shall be construed as an offer of a guarantee of a return of any kind and at any time. Rating Definitions: BUY - More than 15% upside base on the target price in the next 9-12 months SELL - More than 15% downside base on the target price in the next 9-12 months HOLD - TRADE - A potential 10% and above short-term upside base on entry price and selling price. 15% or less upside or downside in the next 9-12 months MBT BUY Last Traded Price 67.50 Entry Point 64.00 - 68.00 Target Price 96.65 Potential Upside / Downside 43.19% Net Foreign Position* (Php 5.892B) 52 wk High and Low 64.00 - 84.80 20 MA Volume 2.898M P/E Ratio 11.33 P/B Ratio 0.906 YTD performance -16.62% Attractive Valuations (Relative, Absolute) RRR cuts have positive effects on the Banks Good Loan portfolio mix Net Interest Margin may get lower due to the BSP rate cuts Ratios are still attractive vs peers * YTD as of September 20, 2019 PHEN TRADE Last Traded Price 2.69 Entry Point 2.69 Target Price 3.00 Potential Upside / Downside 11.52% Net Foreign Position* (Php431.81M) 52 wk High and Low 3.06—0.85 20 MA Volume 29.238 million P/E Ratio - P/B Ratio 1.61 YTD performance 133.91% PIP TRADE Last Traded Price 2.08 Entry Point 2.10 Target Price 2.45 - 2.60 Potential Upside / Downside 17% - 23.81% Net Foreign Position* (Php 167M) 52 wk High and Low 1.33 - 2.22 20 MA Volume 14.823M P/E Ratio 26.10 P/B Ratio 0.81 YTD performance 55.22% Trading Guide Date : September 23 – October 4, 2019 1 Phen is regarded as a tradable stock as bright prospects amid its acquisition by AC Energy , Inc. overshadows its challenged financial performance for the 1st half of 2019. It’s current trend together with the OBV conveys bullishness. * YTD as of September 20, 2019 Penant Pattern Improving Financials Attractive Valuations in terms of its P/B ratio * YTD as of September 20, 2019

Transcript of MBT BUY JAPHET LOUIS O. TANTIANGCO · MBT BUY Last Traded Price 67.50 Entry Point 64.00 - 68.00...

Philstocks Research 2019 |Page

CLAIRE T. ALVIAR

Research Associate

(632)588-1925

Ground Floor, East Tower

PSE Center, Tektite Towers

Ortigas Center, Pasig City

PHILIPPINES

JAPHET LOUIS O. TANTIANGCO

Sr. Research Analyst

(632)588-1927

PIPER CHAUCER E. TAN

Engagement Officer/Research Associate

(632)588-1928

JUSTINO B. CALAYCAY, JR

AVP-Head, Research & Engagement

(632)588-1962

Philstocks Research

DISCLAIMER

The opinion, views and recommendations

contained in this material were prepared by

the Philstocks Research Team, individually

and separately, based on their specific

sector assignments, contextual framework,

personal judgments, biases and prejudices,

time horizons, methods and other factors.

The reader is enjoined to take this into

account when perusing and considering the

contents of the report as a basis for their

stock investment or trading decisions.

Furthermore, projection made and presented

in this report may change or be updated in

between the periods of release. Ergo, the

validity of the projections and/or estimates

mentioned are good as of the date indicated

and may be changed without immediate

notification.

This report is primarily intended for

information purposes only and should not be

considered as an exclusive basis for making

investment decision. The recommendations

contained in this report is not tailored-fit any

particular investor type, situation, or

objective and must not be taken as such.

Determining the suitability of an investment

remains within the province of the investor.

Our estimates are based on information we

believe to be reliable. Nevertheless, nothing

in this report shall be construed as an offer

of a guarantee of a return of any kind and at

any time.

Rating Definitions:

BUY - More than 15% upside base on the target price

in the next 9-12 months

SELL - More than 15% downside base on the target

price in the next 9-12 months

HOLD -

TRADE - A potential 10% and above short-term upside

base on entry price and selling price.

15% or less upside or downside in the next

9-12 months

MBT BUY Last Traded Price 67.50

Entry Point 64.00 - 68.00

Target Price 96.65

Potential Upside / Downside 43.19%

Net Foreign Position* (Php 5.892B)

52 wk High and Low 64.00 - 84.80

20 MA Volume 2.898M

P/E Ratio 11.33

P/B Ratio 0.906

YTD performance -16.62%

Attractive Valuations (Relative,

Absolute)

RRR cuts have positive effects on

the Banks

Good Loan portfolio mix

Net Interest Margin may get lower

due to the BSP rate cuts

Ratios are still attractive vs peers

* YTD as of September 20, 2019

PHEN TRADE

Last Traded Price 2.69

Entry Point 2.69

Target Price 3.00

Potential Upside / Downside 11.52%

Net Foreign Position* (Php431.81M)

52 wk High and Low 3.06—0.85

20 MA Volume 29.238 million

P/E Ratio -

P/B Ratio 1.61

YTD performance 133.91%

PIP TRADE

Last Traded Price 2.08

Entry Point 2.10

Target Price 2.45 - 2.60

Potential Upside / Downside 17% - 23.81%

Net Foreign Position* (Php 167M)

52 wk High and Low 1.33 - 2.22

20 MA Volume 14.823M

P/E Ratio 26.10

P/B Ratio 0.81

YTD performance 55.22%

Trading Guide Date : September 23 – October 4, 2019

1

Phen is regarded as a tradable

stock as bright prospects amid its

acquisition by AC Energy , Inc.

overshadows its challenged

financial performance for the 1st

half of 2019.

It’s current trend together with the

OBV conveys bullishness.

* YTD as of September 20, 2019

Penant Pattern

Improving Financials

Attractive Valuations in terms of its

P/B ratio

* YTD as of September 20, 2019

Philstocks Research 2019 |Page

OUR TAKE

FINANCIAL HIGHLIGHTS

2

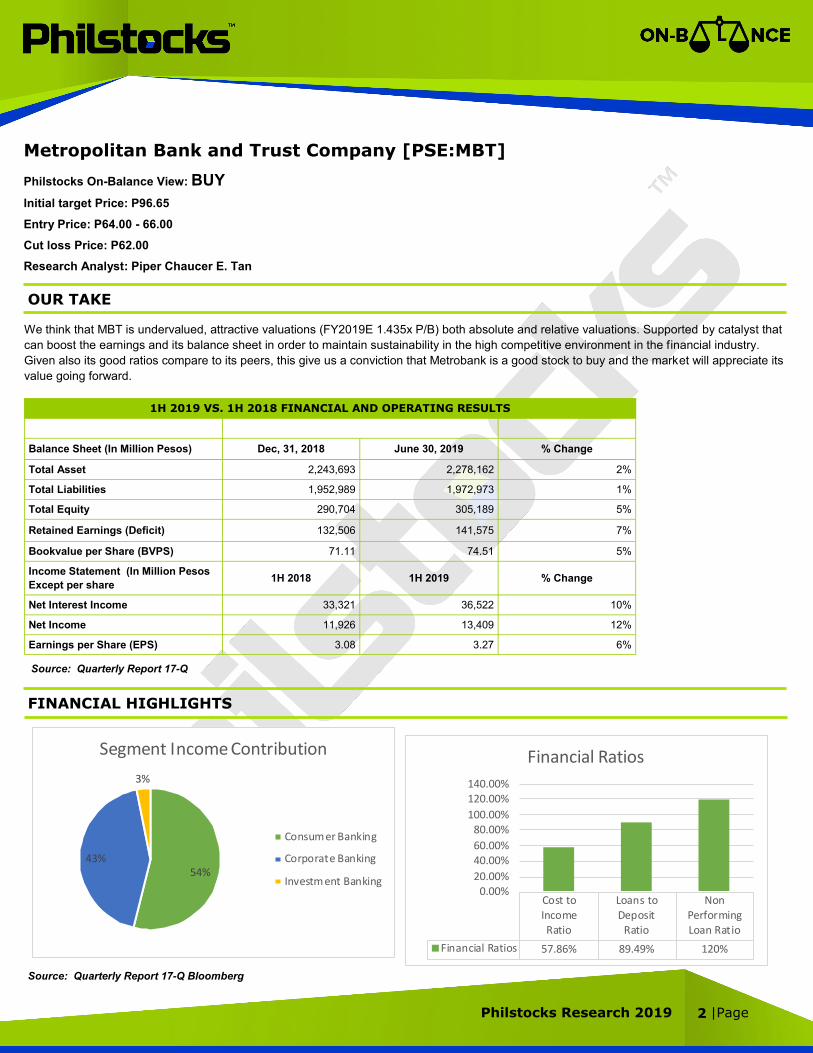

Metropolitan Bank and Trust Company [PSE:MBT]

Philstocks On-Balance View: BUY

Initial target Price: P96.65

Entry Price: P64.00 - 66.00

Cut loss Price: P62.00

Research Analyst: Piper Chaucer E. Tan

We think that MBT is undervalued, attractive valuations (FY2019E 1.435x P/B) both absolute and relative valuations. Supported by catalyst that

can boost the earnings and its balance sheet in order to maintain sustainability in the high competitive environment in the financial industry.

Given also its good ratios compare to its peers, this give us a conviction that Metrobank is a good stock to buy and the market will appreciate its

value going forward.

1H 2019 VS. 1H 2018 FINANCIAL AND OPERATING RESULTS

Balance Sheet (In Million Pesos) Dec, 31, 2018 June 30, 2019 % Change

Total Asset 2,243,693 2,278,162 2%

Total Liabilities 1,952,989 1,972,973 1%

Total Equity 290,704 305,189 5%

Retained Earnings (Deficit) 132,506 141,575 7%

Bookvalue per Share (BVPS) 71.11 74.51 5%

Income Statement (In Million Pesos

Except per share 1H 2018 1H 2019 % Change

Net Interest Income 33,321 36,522 10%

Net Income 11,926 13,409 12%

Earnings per Share (EPS) 3.08 3.27 6%

Source: Quarterly Report 17-Q

Source: Quarterly Report 17-Q Bloomberg

54%43%

3%

Segment Income Contribution

Consumer Banking

Corporate Banking

Investment Banking

Cost toIncomeRatio

Loans toDeposit

Ratio

NonPerformingLoan Ratio

Financial Ratios 57.86% 89.49% 120%

0.00%20.00%

40.00%60.00%

80.00%100.00%

120.00%140.00%

Financial Ratios

Philstocks Research 2019 |Page 3

TECHNICAL ANALYSIS

Based on the charts of Metrobank, we think that the entry price should be on the highlighted rectangular box on the price for MBT, this is

also confirmed by the RSI reaching oversold levels as highlited also on the rectangular box below.

On-Balance Volume may show distribution bias for the share price movement but we think that on the abovementioned price range,

investors may come in again to Metrobank.

The crucial resistance for Metrobank is at Php 84.00/share and if the down trend persist and breaks below the 52-wk low of Php64.00/sh

we set a cutloss point at Php 62.00/share due to the change of sentiment towards the stock if the Php 64/share strong support line is

breaks

Highly competitive environment for banks can also increase the cost for companies thus squeezing the margins for banks and its costs.

Unlike other industries that competition is not much high compared to banks such as Telco industry.

Fintech industry may somehow be a threat to the banks if they do not integrate the fintech into their current business model and this may

also help for banks to reduce its operational costs in putting branches and tapping and serving the unbanked. Research shows that Number

of Filipinos that has a smartphone is much higher than Filipinos with a bank account.

Easing of Interest rate could hurt Net Interest Margin (NIM) of the company . Since the cuts in interest rate could minimize the margins of

banks since the interest on loans will be lower but this may be offset by the increase in loan demand and RRR cuts can offset the cuts for

NIM’s for banks

RISKS

INVESTMENT NARRATIVES

Attractive valuations both Absolute and Relative, based on our estimated Metrobank should be valued at (FY2019E 1.435x P/B) using

historical, comparing to the industry and to its peers (BDO, BPI, SECB, PNB)

Earnings Drivers are still present, consumer banking is still the earning driver for Metrobank, with the RRR cuts we see that the consumer

banking still be the major driver for Metrobank for 2H 2019.

Attractive financial ratios comparing to its peers, we think this ratios such as Cost to income ratio and loans to deposit ratio

Financials is way undervalued in terms of its historical P/B of 1.2x compared to its five year (5) average historical P/B of 1.467x

Philstocks Research 2019 |Page

OUR TAKE

FINANCIAL HIGHLIGHTS

2

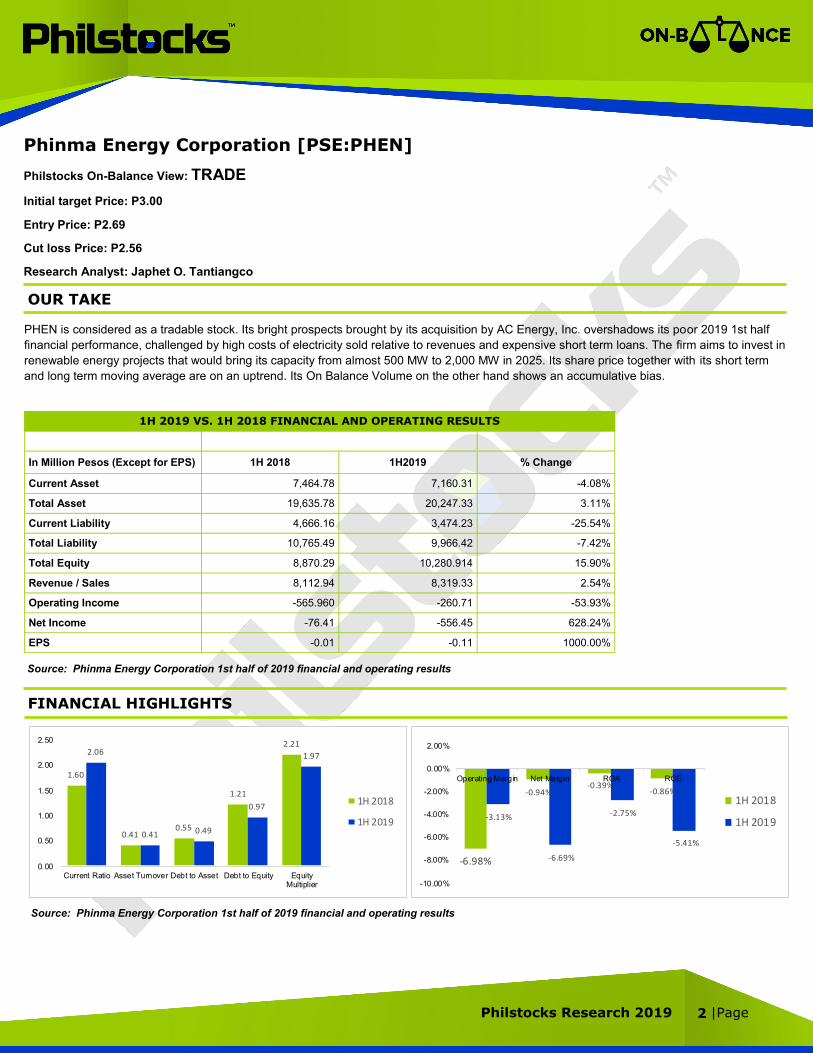

Phinma Energy Corporation [PSE:PHEN]

Philstocks On-Balance View: TRADE

Initial target Price: P3.00

Entry Price: P2.69

Cut loss Price: P2.56

Research Analyst: Japhet O. Tantiangco

PHEN is considered as a tradable stock. Its bright prospects brought by its acquisition by AC Energy, Inc. overshadows its poor 2019 1st half

financial performance, challenged by high costs of electricity sold relative to revenues and expensive short term loans. The firm aims to invest in

renewable energy projects that would bring its capacity from almost 500 MW to 2,000 MW in 2025. Its share price together with its short term

and long term moving average are on an uptrend. Its On Balance Volume on the other hand shows an accumulative bias.

1H 2019 VS. 1H 2018 FINANCIAL AND OPERATING RESULTS

In Million Pesos (Except for EPS) 1H 2018 1H2019 % Change

Current Asset 7,464.78 7,160.31 -4.08%

Total Asset 19,635.78 20,247.33 3.11%

Current Liability 4,666.16 3,474.23 -25.54%

Total Liability 10,765.49 9,966.42 -7.42%

Total Equity 8,870.29 10,280.914 15.90%

Revenue / Sales 8,112.94 8,319.33 2.54%

Operating Income -565.960 -260.71 -53.93%

Net Income -76.41 -556.45 628.24%

EPS -0.01 -0.11 1000.00%

Source: Phinma Energy Corporation 1st half of 2019 financial and operating results

Source: Phinma Energy Corporation 1st half of 2019 financial and operating results

1.60

0.410.55

1.21

2.212.06

0.41 0.49

0.97

1.97

0.00

0.50

1.00

1.50

2.00

2.50

Current Ratio Asset Turnover Debt to Asset Debt to Equity EquityMultiplier

1H 2018

1H 2019

-6.98%

-0.94%-0.39%

-0.86%

-3.13%

-6.69%

-2.75%

-5.41%

-10.00%

-8.00%

-6.00%

-4.00%

-2.00%

0.00%

2.00%

Operating Margin Net Margin ROA ROE

1H 2018

1H 2019

Philstocks Research 2019 |Page 3

TECHNICAL ANALYSIS

PHEN is on an uptrend, currently standing on its 2.69 support. If it fails to hold, next support level would be 2.20. Initial resistance is at 2.80,

next is at 3.00.

Both 50-day and 200-day Exponential moving averages are moving upward, with the former serving as a dynamic support.

Its On balance volume is still showing an accumulative bias, forming higher highs and higher lows.

Its 14-day RSI however is biased towards the oversold territory. Currently, the 40-day support line holds.

Volatility in energy prices especially in the Wholesale Electricity Spot Market which may pressure PHEN’s margins.

Capital intensive nature of its business which could squeeze net cash flows.

Negatively biased general market sentiment amid economic slowdown fears and global geopolitical tensions which could drag PHEN’s share

price. PHEN has a direct relationship with the local market’s movement with a 30-day beta of 1.42.

RISKS

INVESTMENT NARRATIVES

PHEN is currently being combined with AC Energy’s assets, as the former is soon to carry the name of the latter. This would enlarge is

operational capacity.

It has already bagged a power supply agreement with Meralco for 200 MW of energy at P4.7450 per kilowatt-hour from December 26, 2019

to December 25, 2029. It also has a bid for 110 MW of Meralco’s mid-merit power requirement from December 26, 2019 to December 25,

2024 under post qualification evaluation.

The firm is planning to spend $2 billion for renewable energy projects that would bring its renewable energy capacity to 2,000 MW by 2025.

Philstocks Research 2019 |Page

OUR TAKE

FINANCIAL HIGHLIGHTS

2

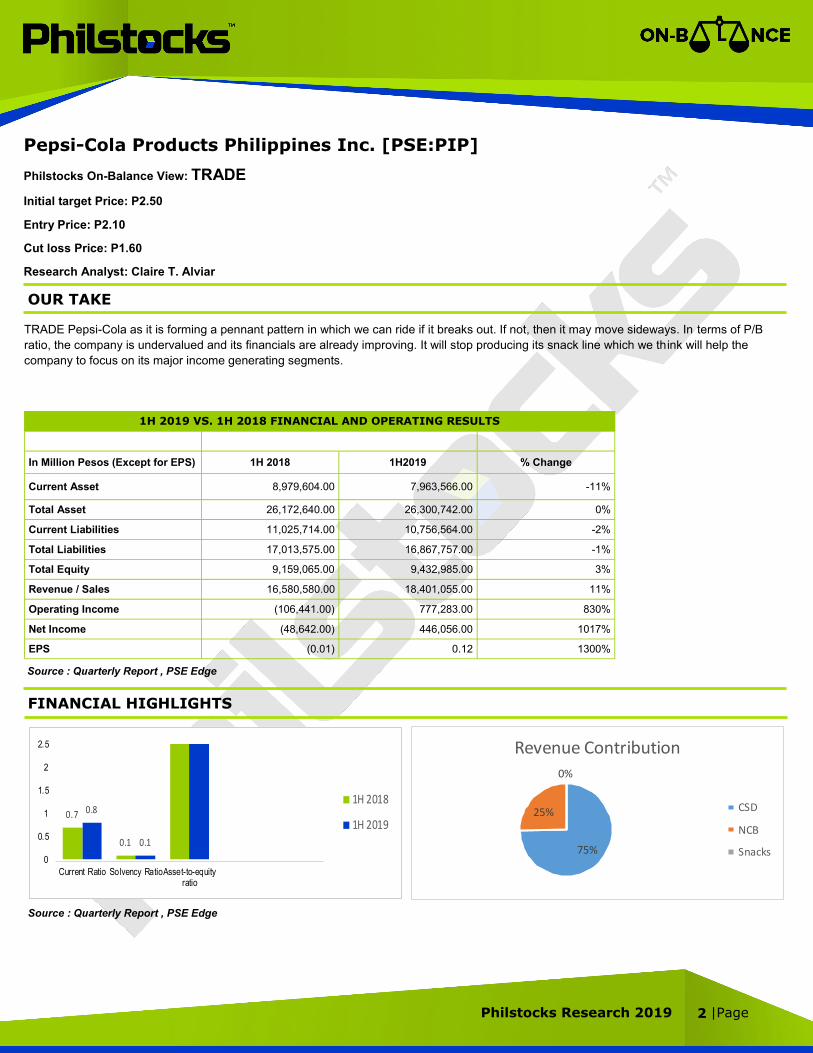

Pepsi-Cola Products Philippines Inc. [PSE:PIP]

Philstocks On-Balance View: TRADE

Initial target Price: P2.50

Entry Price: P2.10

Cut loss Price: P1.60

Research Analyst: Claire T. Alviar

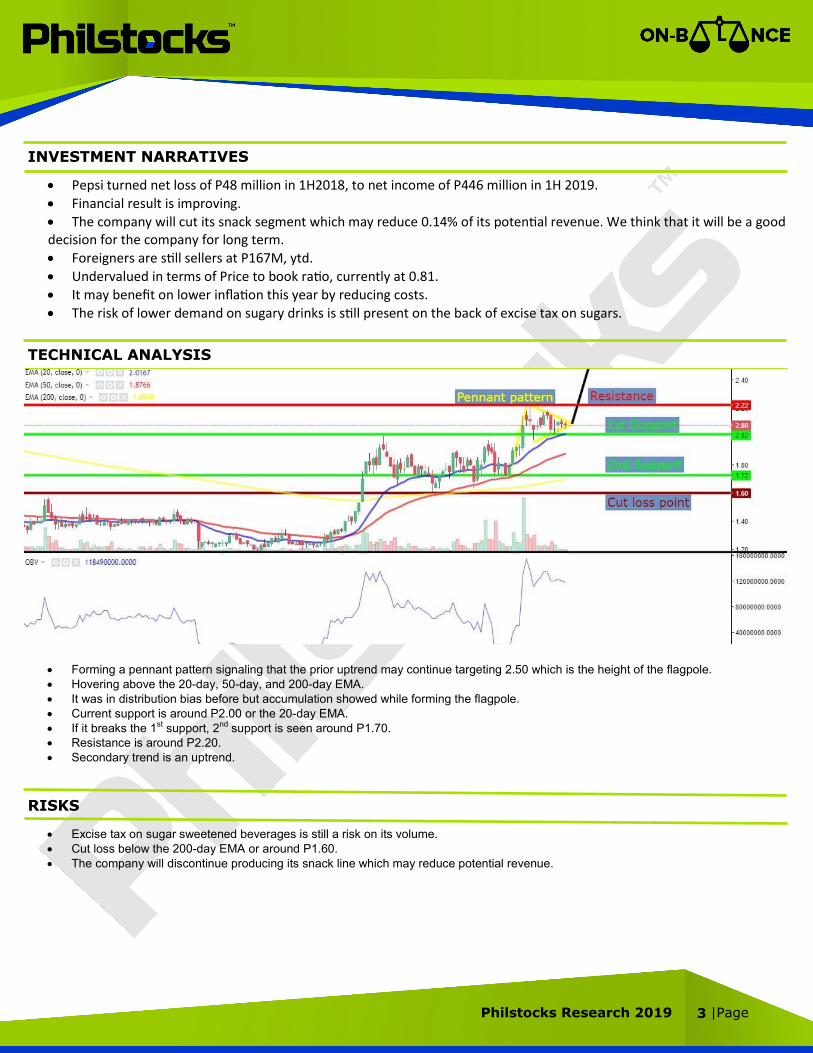

TRADE Pepsi-Cola as it is forming a pennant pattern in which we can ride if it breaks out. If not, then it may move sideways. In terms of P/B

ratio, the company is undervalued and its financials are already improving. It will stop producing its snack line which we think will help the

company to focus on its major income generating segments.

1H 2019 VS. 1H 2018 FINANCIAL AND OPERATING RESULTS

In Million Pesos (Except for EPS) 1H 2018 1H2019 % Change

Current Asset 8,979,604.00 7,963,566.00 -11%

Total Asset 26,172,640.00 26,300,742.00 0%

Current Liabilities 11,025,714.00 10,756,564.00 -2%

Total Liabilities 17,013,575.00 16,867,757.00 -1%

Total Equity 9,159,065.00 9,432,985.00 3%

Revenue / Sales 16,580,580.00 18,401,055.00 11%

Operating Income (106,441.00) 777,283.00 830%

Net Income (48,642.00) 446,056.00 1017%

EPS (0.01) 0.12 1300%

Source: Quarterly Report , PSE Edge

Source : Quarterly Report , PSE Edge

0.7

0.1

0.8

0.1

0

0.5

1

1.5

2

2.5

Current Ratio Solvency RatioAsset-to-equityratio

1H 2018

1H 2019

75%

25%

0%

Revenue Contribution

CSD

NCB

Snacks

Source : Quarterly Report , PSE Edge

Philstocks Research 2019 |Page 3

TECHNICAL ANALYSIS

Forming a pennant pattern signaling that the prior uptrend may continue targeting 2.50 which is the height of the flagpole.

Hovering above the 20-day, 50-day, and 200-day EMA.

It was in distribution bias before but accumulation showed while forming the flagpole.

Current support is around P2.00 or the 20-day EMA.

If it breaks the 1st support, 2nd support is seen around P1.70.

Resistance is around P2.20.

Secondary trend is an uptrend.

Excise tax on sugar sweetened beverages is still a risk on its volume.

Cut loss below the 200-day EMA or around P1.60.

The company will discontinue producing its snack line which may reduce potential revenue.

RISKS

INVESTMENT NARRATIVES

Pepsi turned net loss of P48 million in 1H2018, to net income of P446 million in 1H 2019. Financial result is improving. The company will cut its snack segment which may reduce 0.14% of its potential revenue. We think that it will be a good decision for the company for long term. Foreigners are still sellers at P167M, ytd.

Undervalued in terms of Price to book ratio, currently at 0.81. It may benefit on lower inflation this year by reducing costs.

The risk of lower demand on sugary drinks is still present on the back of excise tax on sugars.

Philstocks Research 2019 |Page 5

Philstocks Research 2019 |Page 6

Philstocks Research 2019 |Page 7