London Residential Breakfast Briefing 2015 | Estates Gazette

139

NIGEL EVANS HEAD OF LONDON RESIDENTIAL RESEARCH Copyright: LRR/EGi THIS PRESENTATION IS BASED ON DATA DERIVED FROM 3 OF LRR’S 2015 REPORTS. DOWNLOAD ALL 3 REPORTS HERE: http ://www.estatesgazette.com/egi-about/london-residential-market-analysis-2015 /

-

Upload

estatesgazettecom-rbi -

Category

Real Estate

-

view

126 -

download

1

Transcript of London Residential Breakfast Briefing 2015 | Estates Gazette

NIGEL EVANS HEAD OF LONDON RESIDENTIAL RESEARCH

Copyright: LRR/EGi

THIS PRESENTATION IS BASED ON DATA DERIVED FROM 3 OF LRR’S 2015 REPORTS.

DOWNLOAD ALL 3 REPORTS HERE:http://www.estatesgazette.com/egi-about/london-residential-market-analysis-2015/

Headlines from our latest reports:

• Construction Starts skyrocket

• More Towers in London than NY

• Where did all the social housing go?

• Were the commuted payments enough?

Where our data comes from

Copyright: LRR/EGi

DOWNLOAD ALL 3 REPORTS HERE:http://www.estatesgazette.com/egi-about/london-residential-market-analysis-2015/

DATA

Copyright: LRR/EGi

Where does it come from?The engine

Copyright: LRR/EGi

Methodology

Copyright: LRR/EGi

Trigger source:

Planning applications

Copyright: LRR/EGi

Was planning permission granted/refused/deferred?

• Deferred - we’ll get it next time• Refused - we’ll check for appeals• Granted - we’ll site visit it

*not just for Islington…

Copyright: LRR/EGi

City

Camden

Westminster

K&C

Islingt’n Hackney

Lambeth

City

Camden

Westminster

K&C

Islingt’n Hackney

Lambeth

All of LondonAll 33 Boroughs

No exceptionsNo arbitrary boundariesNo selected boroughs

All of itWe look at…

200,000 applications

1,000 committeesPer annum

Then we visit every single site with permission…

…as well as all those under construction

Site Visits

6 month cycle33 boroughs

4 questions…

Has it Started?

Has it Finished?

Is it being Marketed?

Has it Stalled?

Or perhaps more common these days

Have you sold it all off plan?

160 site visits per week

640 site visits per month

3,840 site visits per 6 month cycle

130 site visits per weekx

7,680 site visits per annum

1996All this to maintain a database of nearly

25,000 individual developments

updated daily since 19961996

Headlines

24,806Construction starts…the highest number of starts for over

PART 1

Copyright: LRR/EGi

Copyright: LRR/EGi

24,806Construction starts…the highest number of starts for over

Copyright: LRR/EGi

2DECADES

Copyright: LRR/Copyright:

To

we

r H

am

lets

So

uth

wa

rk

Wa

nd

sw

ort

h

Ha

mm

ers

mith

& F

ulh

am

We

stm

ins

ter

Ha

ck

ne

y

La

mb

eth

Ca

md

en

Islin

gto

n

Ke

ns

ing

ton

& C

he

lse

a

City

Ne

wh

am

Le

wis

ha

m

Gre

en

wic

h

Cro

yd

on

Bre

nt

Ba

rne

t

Hill

ing

do

n

Wa

ltha

m F

ore

st

Ea

ling

Ho

un

slo

w

Ha

rro

w

En

field

Ha

ve

rin

g

Su

tto

n

Ha

rin

ge

y

Ba

rkin

g &

Da

ge

nh

am

Bro

mle

y

Me

rto

n

Be

xle

y

Re

db

rid

ge

Ric

hm

on

d

Kin

gs

ton

0

500

1000

1500

2000

2500

3000

STARTS by Borough 2014

Copyright: LRR/EGi

innerTOP5

STARTSTOP 5 INNER BOROUGHS PRIVATE UNITS 2014 TOWER HAMLETS – 2,307

UNITS STARTED

SOUTHWARK – 2,188 UNITS STARTED

WANDSWORTH – 1,703 UNITS STARTED

HAMMERSMITH & FULHAM – 964 UNITS STARTED

WESTMINSTER – 942UNITS STARTED

Copyright: LRR/EGi

outer

5TOP more polarised

STARTSNEWHAM – 2,591 UNITS STARTED

LEWISHAM – 1,247 UNITS STARTED

GREENWICH– 1,187 UNITS STARTED

CROYDON – 1,179 UNITS STARTED

BRENT – 1,074 UNITS STARTED

TOP 5 OUTER BOROUGHS PRIVATE UNITS 2014

Copyright: LRR/EGi

STARTS

DEVELOPMENT FOCUSD TO THE

EASTODD THING

ODD THING

Starts/under construction

up completions

down

…another look at our main table again

UP

DOWN**on what we expected

Copyright: LRR/EGi:

Copyright: LRR/EGi:

connection with UNITS under construction one year

Copyright: LRR/EGi:

and completions the next

Copyright: LRR/EGi:

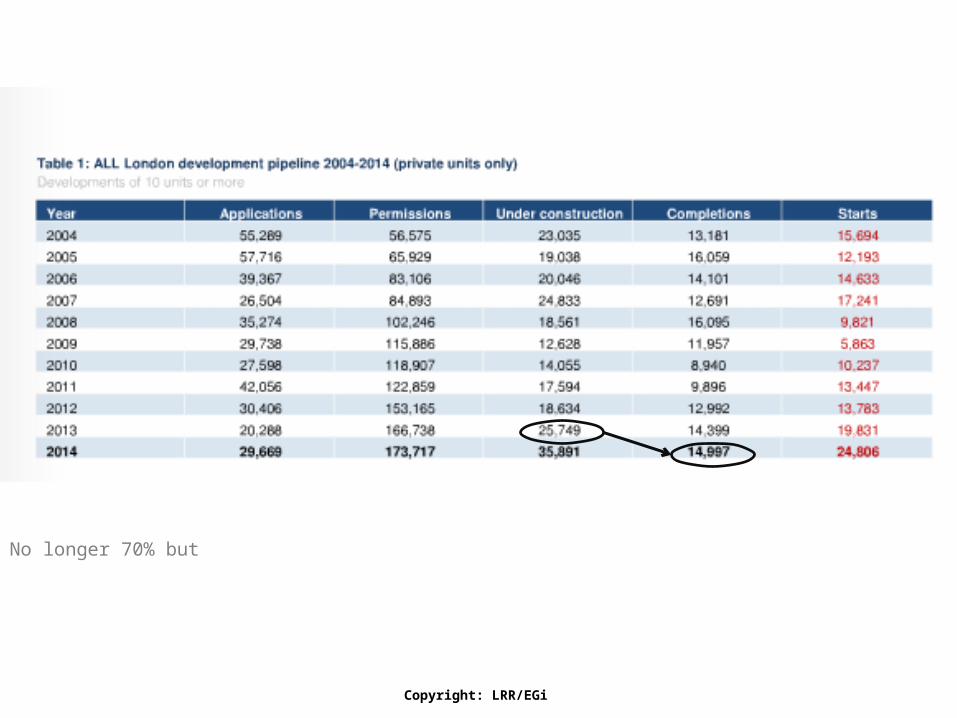

on average 70% of units U/C one year complete the following one…until you get to

No longer 70% but

Copyright: LRR/EGi:

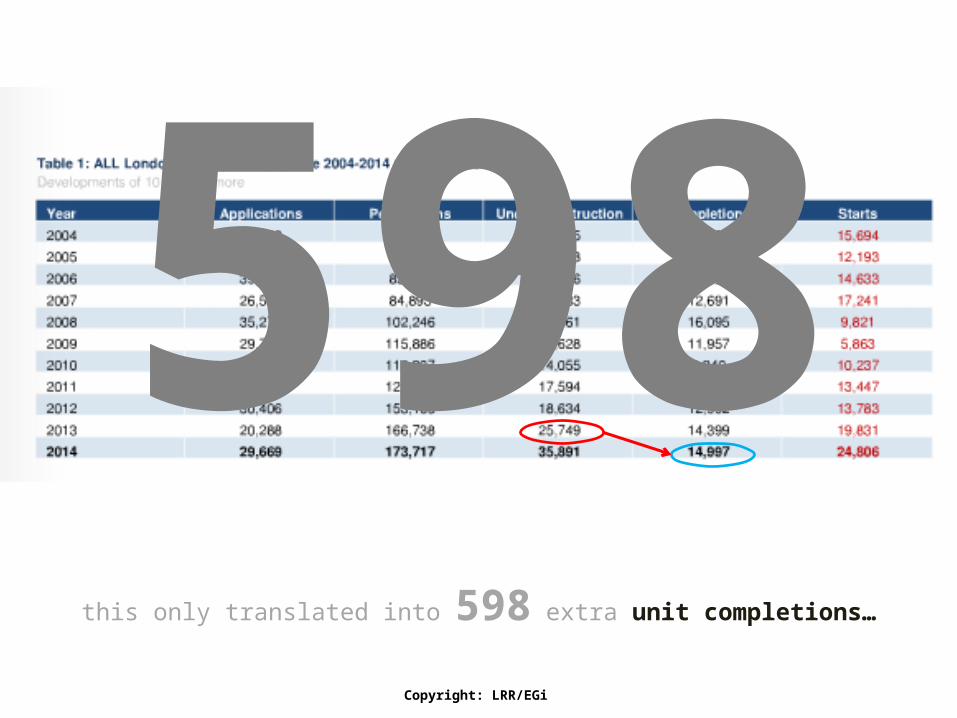

Only 58% of UNITS under construction in 2013 completed in 2014. 58%

Copyright: LRR/EGi:

despite 7,000 MORE UNITS U/C in 2013 compared to 2012

Copyright: LRR/EGi:

despite 7,000 MORE UNITS U/C in 2013 compared to 2012

18,634 units

25,749units

this only translated into 598 extra unit completions…

598Copyright: LRR/EGi:

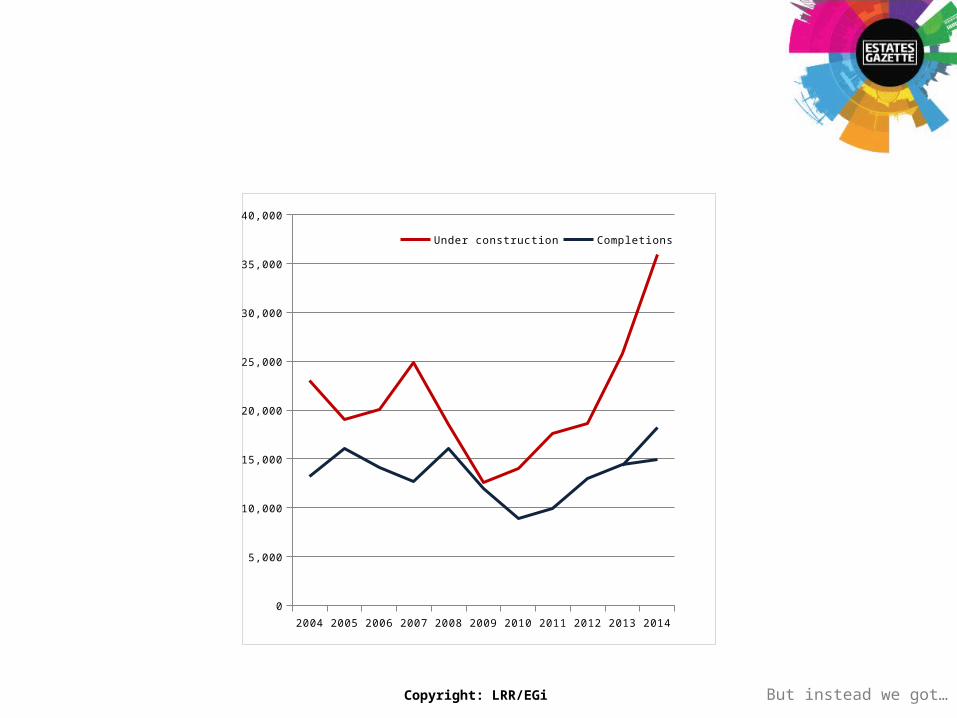

Had we’d seen the normal 70% relationship

then we would have got a graph like this:

70%Copyright: LRR/EGi:

But instead we got…

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

Under construction Completions

Copyright: LRR/EGi:

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

Under construction Completions

Copyright: LRR/EGi:

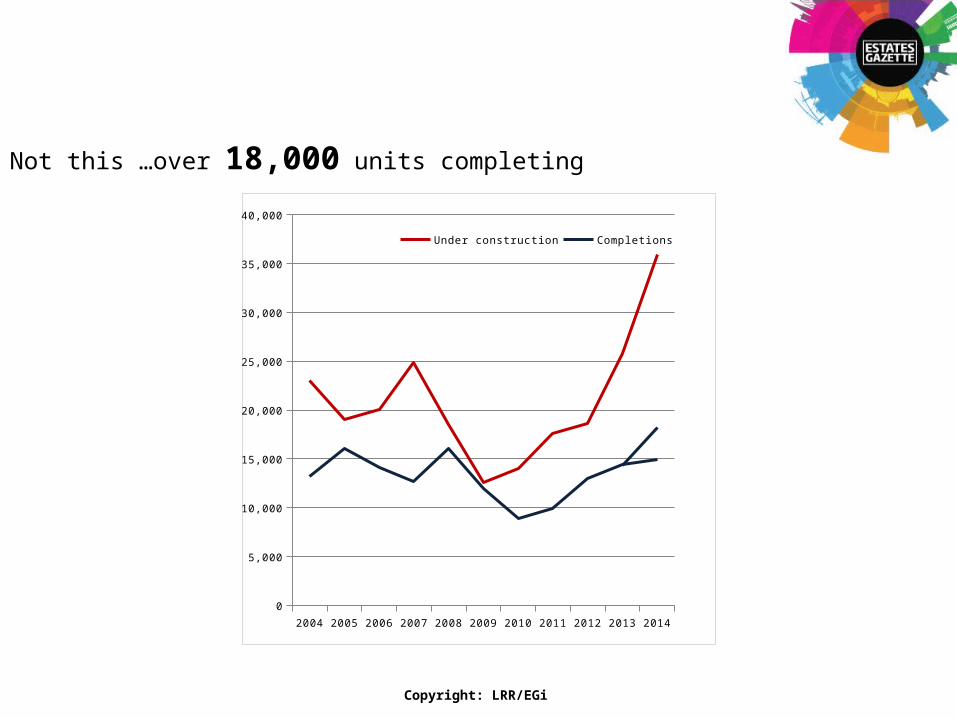

Not this …over 18,000 units completing

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

Under construction Completions

Copyright: LRR/EGi:

But this… just under 15,000 units

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

Under construction Completions

Copyright: LRR/EGi:

Not this

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

Under construction Completions

But this

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

Under construction Completions

Copyright: LRR/EGi:

What’s going on?

24,806Construction starts…the highest number of starts for over

PART 2

What’s going on is …

TOWERS

Tower starts since 2006…

2006 2007 2008 2009 2010 2011 2012 2013 20140

5

10

15

20

25

30

35

Tower Starts

20+ 30+ 40+ 50+

5 815

30

Copyright: LRR/EGi:

Where are they?

VNEBOA – Vauxhall6

The Elephant3

Stratford5

Copyright: LRR/EGi

NINE ELMS POINT28 & 37

VAUXHALL SKY GARDENS36

MERANO28

THE CORNICHE27 & 24

360 London44

South Village23

Eileen House44

CATALYST Copyright: LRR/EGi

NINE ELMS

VAUXHALL

WATERLOO

and may be a catalyst Copyright: LRR/EGi

171 BATTERSEA PK. RD:325 UNITS

BATTERSEA GARDENS:850 UNITS

THAMES WATER SITE:515 UNITS

46 PONTON ROAD:362 UNITS

TINTAGEL HOUSE:454 UNITS

TEXACO STATION:164UNITS

FLORIAN PLACE :275 UNITS

54 KENNINGTON RD:145 UNITS

374 WANDSWORTH RD:124 UNITS

BLORE CLOSE:20 UNITS

2 CORNELL SQUARE:9 UNITS

GAS WORKS SITE:500 UNITS

1 WORGAN STREET:13 UNITS

73 BLACK PRINCE RD:8 UNITS

123 W’MNST BRIDGE RD:5 UNITS

98 LOWER MARSH:34 UNITS

TEACHER CENTRE:17 UNITS

131 WATERLOO ROAD:6 UNITS

26 LOWER MARSH:6 UNITS

3 CARLISLE LANE:6 UNITS

THACKERY HOUSE:6 UNITS

POWER HOUSE:5 UNITS

BONNINGTON SQUARE:6UNITS

22 WYVIL ROAD:9 UNITS

1-30 DAVIDSON GDNS:12 UNITS

3-13 WILCOX ROAD:9 UNITS

438 WANDSWORTH RD:7 UNITS

3,100 units

Some withdrawn, refused, lapsed or master plans being formulated

Copyright: LRR/EGi

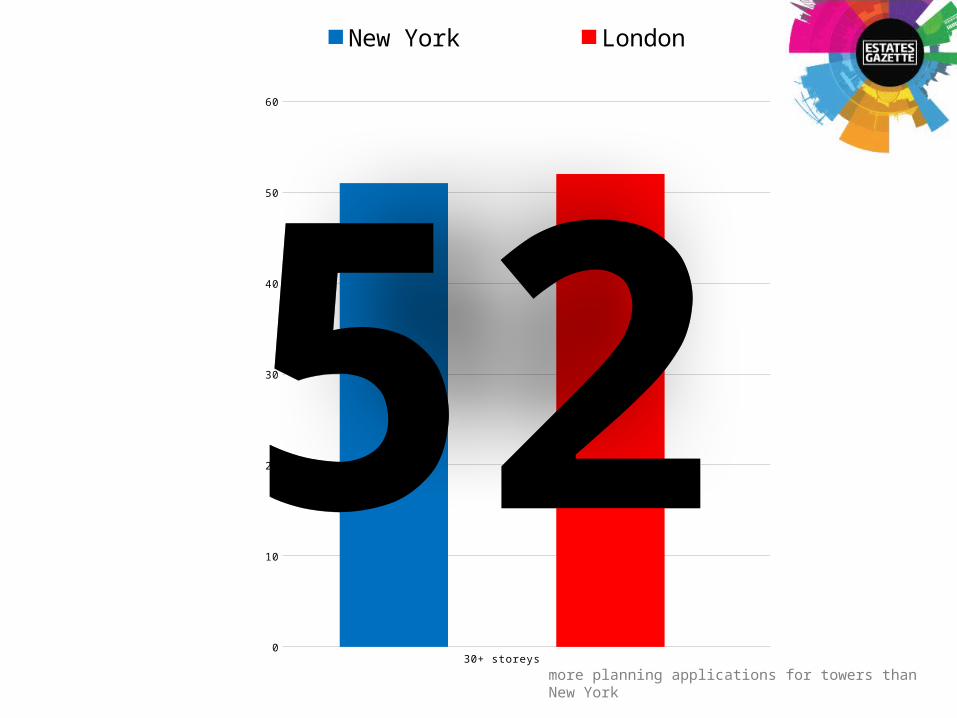

London was going to build

more towers than New York…?

JV New York YIMBY.

Last year they published a set of figures regarding the number of applications submitted during the course 2014 for residential towers, by their definition above 30 storeys.

LRR’s US counterparts

New York YIMBY.

Last year they published a set of figures regarding the number of applications submitted during the course 2014 for residential towers, by their definition above 30 storeys.

LRR’s US counterparts

51 applications for towers* in NY in 2014

*YIMBY definition of towers over 30 storeys

LRR definition over 20 storeys

In the same period London received 52applications for towers over 30 storeys

5230+ storeys 50+ storeys

0

10

20

30

40

50

60

New York London

more planning applications for towers than New York

52

Where are they?

Copyright: LRR/EGi

only a fraction of what’s in the pipeline

As well as those applications we can add…

157 permissions

Copyright: LRR/EGi

Copyright: LRR/EGi

and on top of those 17 possible sites

17 sites

Copyright: LRR/EGi

Copyright: LRR/EGi

possible future starts in the pipeline right now…and this is where they are

220Copyright: LRR/EGi

VNEBOA Elephant

Waterloo/Blackfriars

Stratford

But to really look to the future we must

we have to go back… back to where these towers started in the first place…

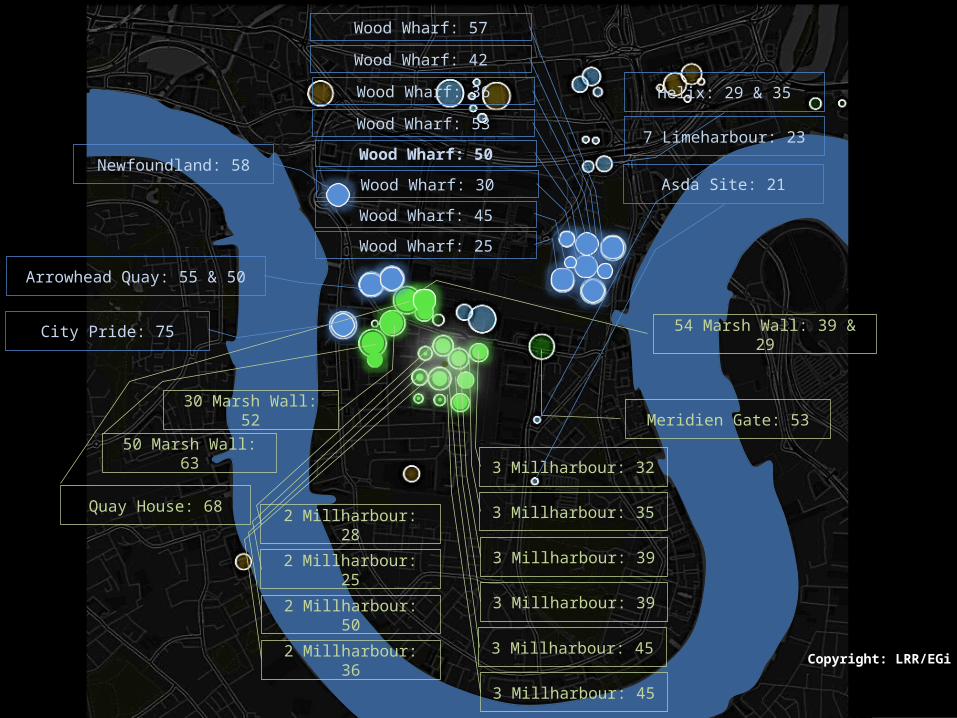

DOCKLANDS

Copyright: LRR/EGi

3 Millharbour: 32

54 Marsh Wall: 39 & 29

50 Marsh Wall: 63

30 Marsh Wall: 52

Quay House: 68

City Pride: 75

Arrowhead Quay: 55 & 50

Wood Wharf: 57

Wood Wharf: 42

Wood Wharf: 36

Wood Wharf: 53

Wood Wharf: 50

Wood Wharf: 30

Wood Wharf: 45

Wood Wharf: 25

3 Millharbour: 35

3 Millharbour: 39

3 Millharbour: 39

3 Millharbour: 45

3 Millharbour: 45

2 Millharbour: 28

2 Millharbour: 25

2 Millharbour: 50

2 Millharbour: 36

Meridien Gate: 53

Newfoundland: 58

Helix: 29 & 35

7 Limeharbour: 23

Asda Site: 21

Copyright: LRR/EGi

Why high?

0 5 10 15 20 25£900.00

£1,100.00

£1,300.00

£1,500.00

£1,700.00

£1,900.00

£2,100.00

Goodmans Fields

0 5 10 15 20 25 30 35 40 45 50£500.00

£600.00

£700.00

£800.00

£900.00

£1,000.00

£1,100.00

New Providence Tower

0 5 10 15 20 25 30 35£500.00

£600.00

£700.00

£800.00

£900.00

£1,000.00

£1,100.00

One The Elephant

4 9 14 19 24£900.00

£1,000.00

£1,100.00

£1,200.00

£1,300.00

£1,400.00

£1,500.00

£1,600.00The Eagle

Storeys Storeys

Storeys Storeys

£psq

ft

£psq

ft

£psq

ft

£psq

ft

UNITS UNITS

UNITSUNITS

Copyright: LRR/EGi

A note of caution

Copyright: LRR/EGi

In 2014 we saw

phenomenal increases in the number of construction

starts

Copyright: LRR/EGi

Was there a corresponding boost in the number of units sold?

No

The number of sales in

2013 totalled

12,700 units

Copyright: LRR/EGi

The number of sales in

2014 totalled

12,900 units

Copyright: LRR/EGi

a mere

1.6% increase.

Copyright: LRR/EGi

Some 800 more units remained un-sold and 7,000 more units remained un-launched at the end of 2014 compared to the end of 2013.

800

7,000Copyright: LRR/EGi

Causefor

Concern

Rapid and unprecedented rises

in the number of units being built…

Rapid unprecedented rises

without a corresponding spike in sales …

could be the precursor to oversupply and an

eventual drop in prices.

Not that we’re calling the top of the market…

Not that we’re calling the top of the market… not just yet.

24,806Construction starts…the highest number of starts for over

PART 3

Social Housing

Copyright: LRR/EGi

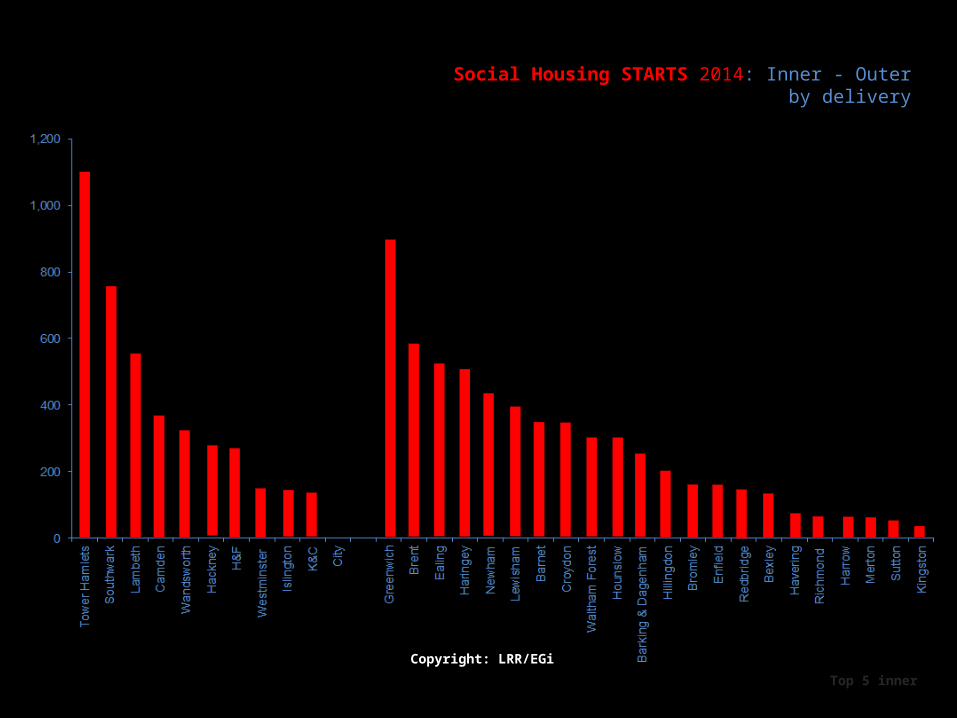

9,798Social Starts in 2014

Copyright: LRR/EGi

Social Housing STARTS by borough 2014

Alphabetically

Copyright: LRR/EGi

Top 5 inner

Social Housing STARTS 2014: Inner - Outer by delivery

Copyright: LRR/EGi

24,806Construction starts…the highest number of starts for over

LAMBETH – 544UNITS STARTED

SOUTHWARK – 743 UNITS STARTED

TOWER HAMLETS– 1,086 UNITS STARTED

CAMDEN – 359 UNITS STARTED

WANDSWORTH – 313 UNITS STARTED

Top 5 outer

TOP 5 BOROUGHS SOCIAL STARTS - INNER

24,806Construction starts…the highest number of starts for over

EALING – 510 UNITS STARTED

BRENT – 577 UNITS STARTED

GREENWICH – 809 UNITS STARTED

HARINGEY – 495 UNITS STARTED

NEWHAM – 425 UNITS STARTED

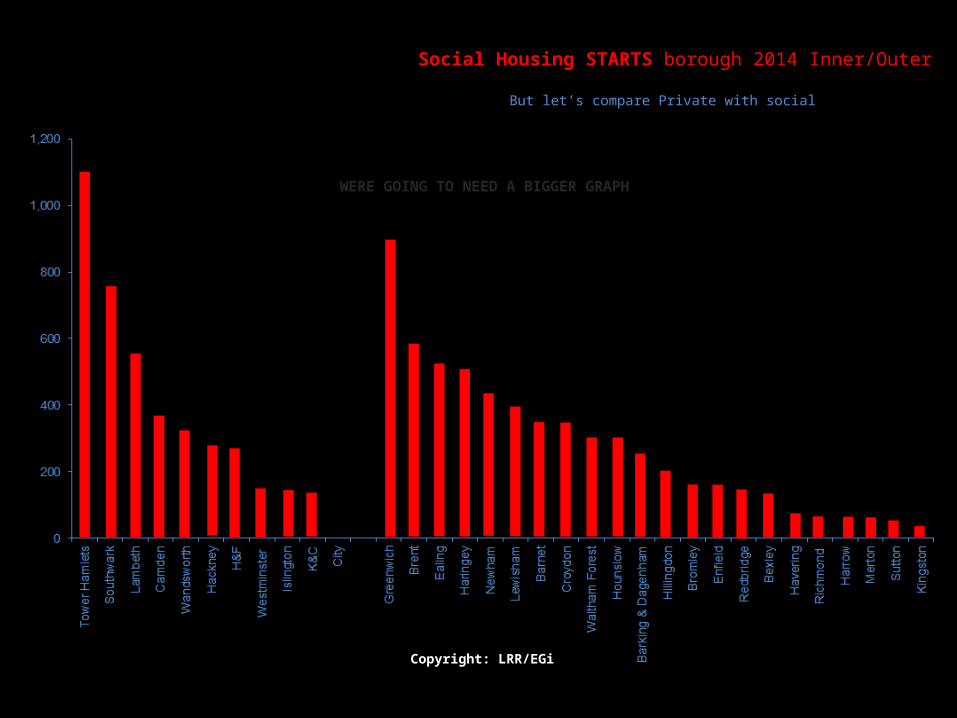

Compare private and social

TOP 5 BOROUGHS SOCIAL STARTS - OUTER

Copyright: LRR/EGi

Social Housing STARTS borough 2014 Inner/Outer

But let’s compare Private with social

WERE GOING TO NEED A BIGGER GRAPH

Copyright: LRR/EGi

Construction starts…the highest number of starts for over

1,400

1,600

1,800

2,000

Social Housing AND PRIVATE STARTS borough 2014 Inner/Outer

Copyright: LRR/EGi

Copyright: LRR/EGi

24,806Construction starts…the highest number of starts for over

Copyright: LRR/EGi

2DECADES

Copyright: LRR/EGi

9,798Not such a magic number

Copyright: LRR/EGi

3YEARS

Private starts have shot up but social starts have remained roughly static

Stick this on a graph…

Copyright: LRR/EGi

24,806Construction starts…the highest number of starts for over

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

0

5,000

10,000

15,000

20,000

25,000

30,000

a distinct symmetry.

PRIVATE STARTS

SOCIAL STARTS

PRIVATE V SOCIAL STARTS 2004-2014

Copyright: LRR/EGi

24,806Construction starts…the highest number of starts for over

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

0

5,000

10,000

15,000

20,000

25,000

30,000

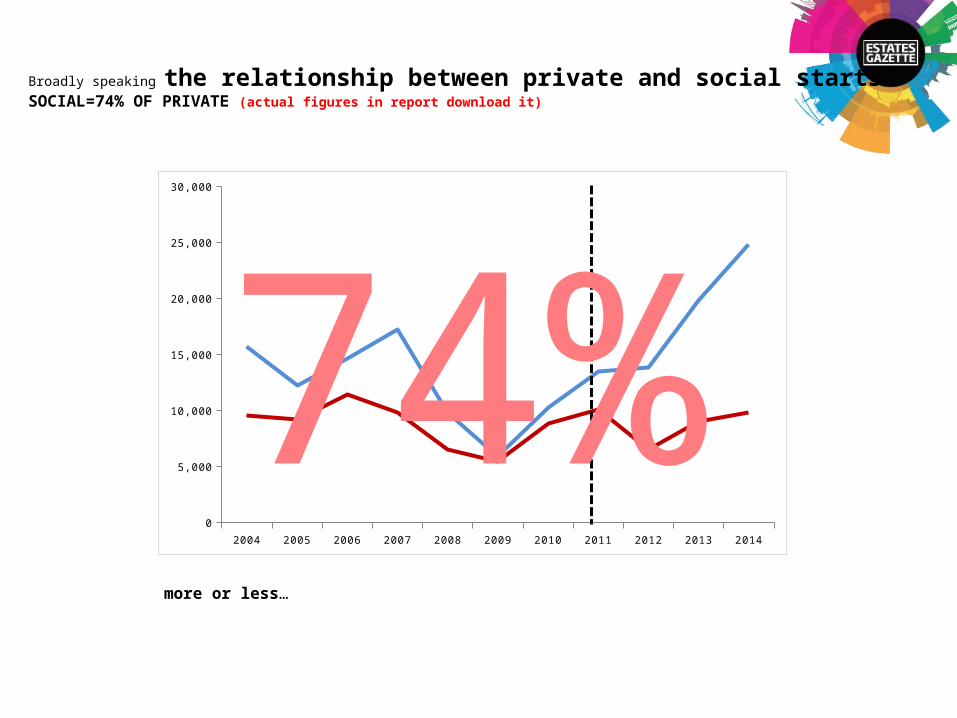

Broadly speaking the relationship between private and social starts SOCIAL=74% OF PRIVATE (actual figures in report download it)

74%more or less…

24,806Construction starts…the highest number of starts for over

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

0

5,000

10,000

15,000

20,000

25,000

30,000

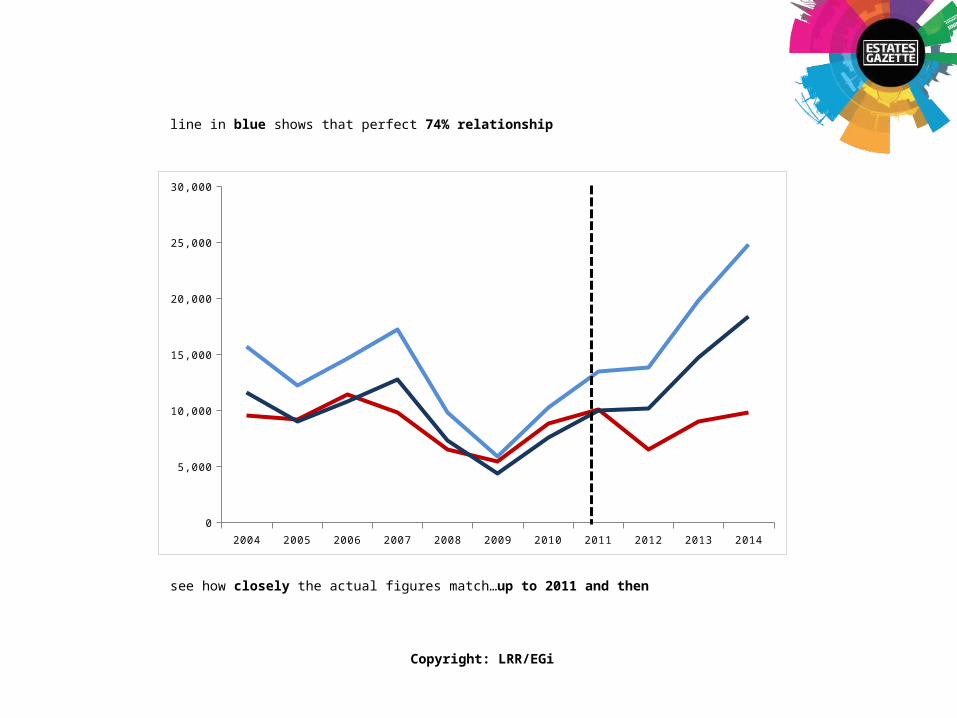

see how closely the actual figures match…up to 2011 and then

line in blue shows that perfect 74% relationship

Copyright: LRR/EGi

24,806Construction starts…the highest number of starts for over

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

0

5,000

10,000

15,000

20,000

25,000

30,000

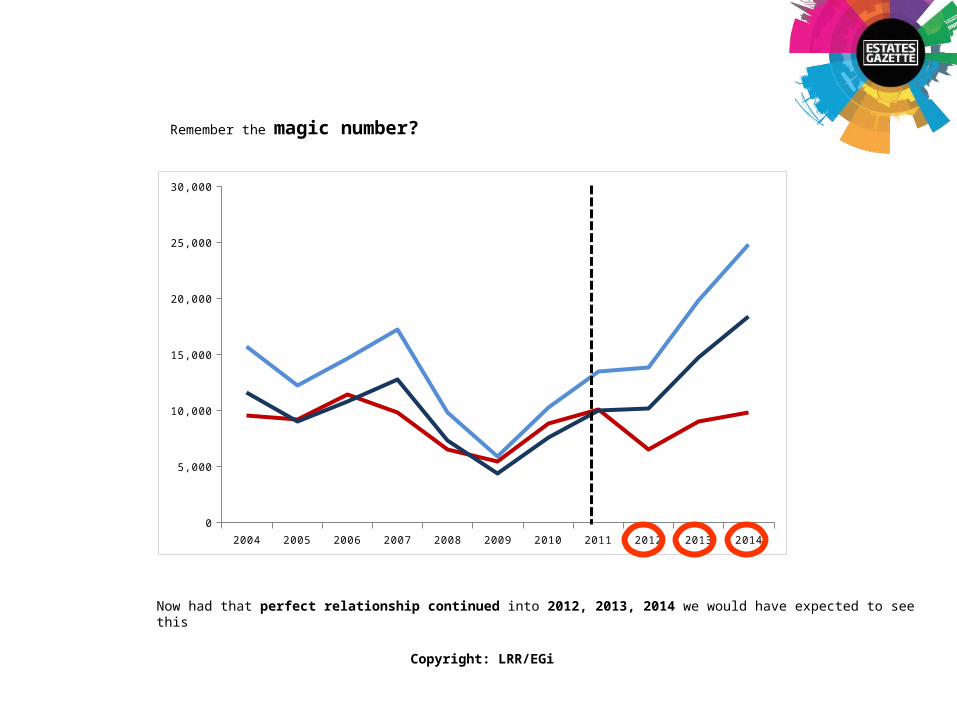

Now had that perfect relationship continued into 2012, 2013, 2014 we would have expected to see this

Remember the magic number?

Copyright: LRR/EGi

24,806Construction starts…the highest number of starts for over

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

0

5,000

10,000

15,000

20,000

25,000

30,000

Just as social mirrored private starts in the past so it would in the future

24,806Construction starts…the highest number of starts for over

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

0

5,000

10,000

15,000

20,000

25,000

30,000

But we didn’t get that…

Copyright: LRR/EGi

24,806Construction starts…the highest number of starts for over

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

0

5,000

10,000

15,000

20,000

25,000

30,000

Copyright: LRR/EGi

24,806Construction starts…the highest number of starts for over

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

0

5,000

10,000

15,000

20,000

25,000

30,000

Copyright: LRR/EGi

24,806Construction starts…the highest number of starts for over

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

0

5,000

10,000

15,000

20,000

25,000

30,000

Copyright: LRR/EGi

24,806Construction starts…the highest number of starts for over

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

0

5,000

10,000

15,000

20,000

25,000

30,000

Copyright: LRR/EGi

24,806Construction starts…the highest number of starts for over

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

0

5,000

10,000

15,000

20,000

25,000

30,000

Copyright: LRR/EGi

24,806Construction starts…the highest number of starts for over

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

0

5,000

10,000

15,000

20,000

25,000

30,000

on the graph represents a loss of nearly 18,000 units since 2011

18,000 shortfall in social units

Copyright: LRR/EGi

However, the provision of social housing can

take two forms.

the bricks on the ground failed? seriously stalled?

commuted payments in lieu of on/off-site provision?

S106

These are schemes that got permissions which included a payment in-lieu of social housing provision

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

0

10

20

30

40

50

60

70

80

90

100

-

50,000,000

100,000,000

150,000,000

200,000,000

250,000,000

300,000,000

S106 payments v PPG with S106 conditions 2004-2010 Developments of 10 units or more

Number of schemes S106 payments (£)

S106 PAYMENTS

SCHEMES with S106

Copyright: LRR/EGi

Only 70 developments contained an S106 payment in lieu for this entire period

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

0

10

20

30

40

50

60

70

80

90

100

-

50,000,000

100,000,000

150,000,000

200,000,000

250,000,000

300,000,000

S106 payments v PPG with S106 conditions 2004-2010 Developments of 10 units or more

Number of schemes S106 payments (£)

S106 PAYMENTS

SCHEMES with S106

Then after 2010…a seismic shift in the number of S106 payments coupled with an increase in schemes.

Copyright: LRR/EGi

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

0

10

20

30

40

50

60

70

80

90

100

-

50,000,000

100,000,000

150,000,000

200,000,000

250,000,000

300,000,000

S106 payments v PPG with S106 conditions 2004-2010 Developments of 10 units or more

Number of schemes S106 payments (£)

S106 PAYMENTS

SCHEMES with S106

70 payments in lieu

239 payments in lieu

How does that translate to cash?Copyright: LRR/EGi

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 20140

5,000

10,000

15,000

20,000

25,000

30,000

£184m

£86m

£192m

2011:

2012:

2013:

£467mCopyright: LRR/EGi

A huge increase in payments nearly £467m since 2011. So although the level of physical provision has gone down the level of cash in lieu payments has gone up….

£467m since 2011PHYSICAL PROVISION££PAYMENT IN LIEU££

Copyright: LRR/EGi

So the question we have to ask now is…

Were the payments enough?

24,806Construction starts…the highest number of starts for over

Can we build 18,000 social units with £467 m?

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 20140

5,000

10,000

15,000

20,000

25,000

30,000

18,000 shortfall in social units

£467mCopyright: LRR/EGi

Lets go back to the graph…

NO

=

Lets go back to the graph…

6,500*£467m

£467 m equates to 6,500 social units*Methodology in the report download there or from GS in QA

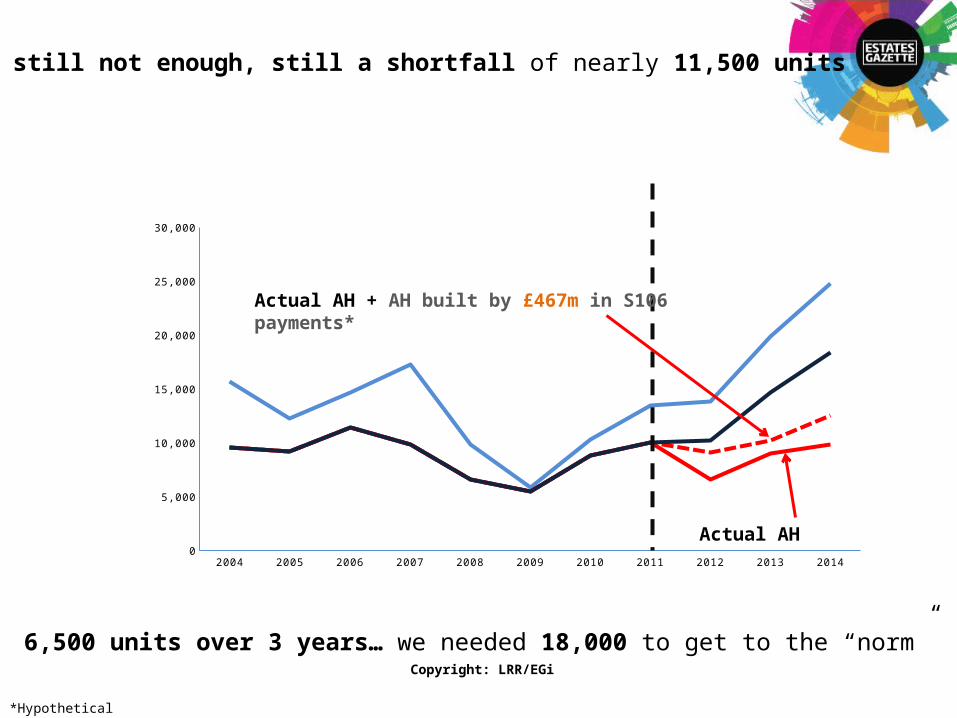

still not enough, still a shortfall of nearly 11,500 units

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 20140

5,000

10,000

15,000

20,000

25,000

30,000

Actual AH

Actual AH + AH built by £467m in S106 payments*

*Hypothetical

6,500 units over 3 years… we needed 18,000 to get to the “norm”Copyright: LRR/EGi

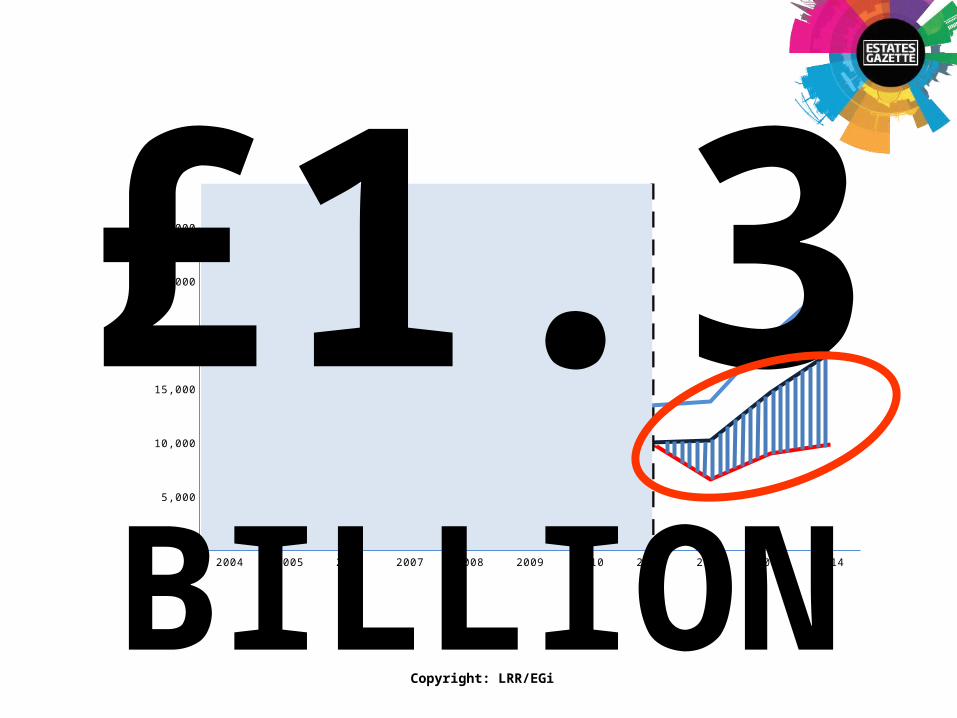

So if nearly £467m didn’t make up the shortfall – what amount would have?By our calculations…..

£467m

24,806Construction starts…the highest number of starts for over

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 20140

5,000

10,000

15,000

20,000

25,000

30,000£1.3BILLION

Copyright: LRR/EGi

Would be…

LONDON

Sites, withdrawn, refused, lapsed all were thought to have potential once…and they could have again

Used to take a lot of work to extract the dataand map it

But a new service by Egi makes finding these sites simple

It’s called Site Finder and it does just that

Follow this link: http://estatesgazette.com/site-finder

Or call Ken Norton on 0207 911 1785

NIGEL EVANS HEAD OF LONDON RESIDENTIAL RESEARCH

THIS PRESENTATION IS BASED ON DATA DERIVED FROM 3 OF LRR’S 2015 REPORTS.

DOWNLOAD ALL 3 REPORTS HERE:http://www.estatesgazette.com/egi-about/london-residential-market-analysis-2015/