LIVING - UCT Retirement Funductrf.co.za/useruploads/files/living+annuity+info+leaflet_new.pdf ·...

24

UCT RETIREMENT FUND LIVING ANNUITANTS BOOKLET Secure your future – it’s never too late to start www.uctrf.co.za JULY 2013

Transcript of LIVING - UCT Retirement Funductrf.co.za/useruploads/files/living+annuity+info+leaflet_new.pdf ·...

1

UCT RETIREMENT FUND

LIVINGANNUITANTSBOOKLET

Secure your future – it’s never too late to start

www.uctrf.co.za

JULY 2013

2

WELCOME MESSAGE

Dear Living Annuitant/ prospective Living Annuitant,

A living annuity (as opposed to a life annuity) can be (but is not always) an appropriate form of pension. As with any financial instrument it carries both risks and opportunities. If you are considering using a living annuity to provide you with a pension at retirement

• takeadvice,andmakesurethisisrightforyoubeforeyoudecide.

If you have decided to use a living annuity to provide you with a pension at retirement

• considertheadvantagesofaUCTRFlivingannuitybeforeyoudecide.

This leafletgives you somepointers about livingannuities (LA’s, oroften referred to asInvestmentLinkedLivingAnnuitiesorILLA’s).

Content:

1. What is a Living Annuity

2. Should you choose a Living Annuity?

3. Managing a Living Annuity

4. Exits from a Living Annuity

5.CostsassociatedwithLivingAnnuities

6. Summary

7. Life annuities vs. living annuities?

8.ArticlesfromPersonalFinance

3

WHAT IS A LIVING ANNUITY?

A Living Annuity (LA) is an annuity (or pension payment) that should “live” for the rest of your life time. Your retirement capital is used to set up an account from which annuity or pension payments (usually called drawdowns) are made, fees are deducted and investment returns added (these can be negative).

As a Living Annuitant, your responsibility increases in that you assume mortality risk over and above the investment risk that you have carried up to now. As your capital must last for your lifetime, you need to be very aware when you start “eating” into capital, (you eat into your capital when your annuity (drawdown) amount is more than the investment returnsonyourcapital.)Thiscouldresultinyournothavingenoughmoneytolastyoutherest of your life. You should also be very aware of which Portfolio you choose to invest in - if you are, for example, fully invested in a market -linked portfolio and the markets crash, it will have a detrimental effect on your annuity as well as on the term it will be payable. Thisformspartoftheinvestmentriskyoucarry.

Legislated minimum and maximum annual drawdown amounts are set by law. Thecurrent legislated minimum and maximum drawdown amounts are set at 2.5% and 17.5%, respectively, of the capital balance of the living annuity account at the anniversary date. It isimportanttonotethattheUCTRFdoesofferaLivingannuityinthefund,andthetrusteesalso have the right to limit your annual drawdown amount to a prudent maximum amount as determined by the actuary based on certain assumptions for each living annuitant (unless you provide the fund with certain information and undertakings to confirm that you are aware of the risks associated with drawing a higher percentage).

4

SHOULD YOU CHOOSE A LIVING ANNUITY?

Advantages of living annuities:

Flexible drawings

Youcanselecttheannualrateofdrawings.Thisfacilitycangreatlyassistinminimisingtaxpaidon pension. If you are in poor health and/or suffer from a terminal disease, you can draw higher amountsformedicalcare.Thisisonetimethatyoucouldconsiderdrawingmorethan5%ofyour capital every year.

An ILLA might be suitable for a retiree who expects to continue earning for, say, 5 years after retirement and thus “park” his retirement capital for 5 years and buy a life annuity 5 years later (taking advantage of the fact that rates for a 70 year old are very different from rates for a 65 year old, other things – especially interest rates – being equal).

Investment flexibility

YouwillhavearangeofinvestmentportfoliostochoosefromifyouareintheUCTRF(andwith most ILLA products). You can also switch investments in order to obtain improved investment returns. Investing a portion of your funds in asset classes such as equities, could improve the probability of beating inflation over the medium to long term.

Capital protection/ legacy

Your remaining capital is not lost in the event of death after retirement, and is paid out to yourdependantsornominees(if inaretirementFund)ortoyournominees(withotherILLA’s).Thisisaparticularlyattractivefeatureforretireessufferingfrompoorhealth.

Conventional annuities seem less attractive as they offer a predeterminedpension, noinvestment choice and the possibility of loss of capital upon death (although the latter can be mitigated by choosing an annuity with a long guarantee term).

So why would any retiree not choose a living annuity given all these advantages?

Living annuities hold a host of dangers for very many retirees, and are probably not suitable investments for the average man (or woman) in the street

5

Risks associated with Living Annuities (disadvantages)

As a living annuitant, there are four important risks, namely: • Investment risk • Inflation risk • Theriskoflivingtoolong!• Drawing risk

Investment risk

Investment risk refers to the chance that the investment returns you earn on the money you invest at your retirement are insufficient to provide a reasonable income throughout your retirement. Theinvestmentriskdependsontheassetclassinwhichyouinvestyourmoney,investmentperformance and on how long you can invest the money before you need to use it (i.e. your investment horizon). Inflation risk

One of the big risks you face in retirement is that inflation reduces the buying power of your pension.

It is very difficult to predict the future course of inflation (i.e. it may go much lower or maybe it could increase sharply). It is therefore important that you invest your retirement money, or at least that part which covers your basic needs, in such a way that your income goes up each year more or less in line with inflation. Risk of living too long (mortality risk)

Thisseemslikeanunusualrisk-butthelongeryouandyourdependantslive,themoremoney you will need after retirement. Many people have a pessimistic view of how much longertheywillliveoncetheyretire.Thefollowingtableshows,howlong,onaverageamale and female are expected to live if they retire at different ages.

Retirement ageLife expectancyMale Female

55 22 years 27 years60 18 years 22 years65 14 years 18 years

Theabovefiguresmaywellunderstatetheposition,becauselifeexpectancyofpeopleisincreasingandlivingintoone’s90’sisnowcommon.

6

No mortality insurance is provided by living annuities, unlike conventional/ life annuities. Retireeswhopurchaselifeannuitiesareeffectivelyinsuringagainsttheriskoflivingtoolong.

ILLA’s may seem attractive in the early years following retirement, but there is a highprobability that these annuities will not be delivering an adequate pension as early as 10 years after retirement (unless the starting capital is very large in relation to your income needs and you are able to draw a relatively small percentage each year). If you live 20 to 30 years after retirement you might find yourself facing a continually dropping standard of living because living annuities are designed so as to pay out all that remaining capital to the dependants of pensioners who die in the early years following retirement rather than retaining the remaining capital for those pensioners who live longer than anticipated by the actuaries.

Drawing risk

Theannuitantassumestheresponsibilityforchoosingtheamountofdrawingseachyear.Thetemptationmayexisttodrawatoohighpercentage.Ahighdrawingwillveryquicklyerode the capital base, and will result in an inadequate pension within the space of a few years. As a rough rule of thumb an annual drawing rate above 6% will probably result in great hardship in later years.

BY EXAMPLE:IF WE LOOK AT THE LIVING ANNUITY IN PRACTICE YOU WILL SEE THAT IF YOUR RETURN ON INVESTMENT IS LESS THAN THE CHOSEN DRAW DOWN, YOUR CAPITAL WILL BEGIN TO BE DEPLETED.

Let’s look at a pensionerwith R1 000 000 retirement savings. The table below showswhathappenstothepensioner’sincomeifhewantstoincreasehisincomebyinflationeachyear.Therealityisthatstartingoffwitha7%drawdownistoohighandwillresultinincome decreasing if the pensioner survives 10 years as the pensioner is not allowed to drawmorethan17.5%oftheirlumpsum.Consideringthattheaveragelifeexpectancyfor a 65 year old is 20 years, this points to an unacceptable situation.

Age FundCredit Draw % Draw p.a. Draw p.m.65 1 000 000 7,0% 70 000 5 833,33 66 1 002 625 7,4% 74 200 6 183,33 67 1 001 105 7,9% 78 652 6 554,33 68 994867 8,4% 83 371 6947,5969 983283 9,0% 88 373 7 364,45 70 965657 9,7% 93676 7 806,32 71 941228 10,5% 99296 8274,6972 909155 11,6% 105 254 8 771,18 73 868 516 12,8% 111569 9297,4574 818 301 14,5% 118 264 9855,29

7

Age FundCredit Draw % Draw p.a. Draw p.m.75 757397 16,6% 125359 10 446,61 76 684590 17,5% 119803 9983,6077 612 066 17,5% 107 112 8925,9778 547 226 17,5% 95765 7980,3879 489254 17,5% 85 620 7134,9680 437 424 17,5% 76549 6379,1081 391085 17,5% 68 440 5 703,32 82 349654 17,5% 61190 5099,1383 312 613 17,5% 54 707 4558,9484 279496 17,5% 48912 4075,9885 249887 17,5% 43 730 3 644,18

Realisticallythemaximumdrawdownthatshouldbetakenonalivingannuityis4%whichtranslatestoamonthlyincomeofR3333perR1millionrand.The living annuity is therefore typically suitable for the domain of the wealthy individual who has overfunded for his/her retirement.

CAPITAL PROTECTION SHOULD BE A SECONDARY CONSIDERATION – FIRST MAXIMISE YOUR INCOME FOR LIFE!!!!

Living annuities are very flexible products and offer many attractions to the sophisticated investor.Theydo,however,havesomesignificantdisadvantages,andassuchareprobablynot suitable for the vast majority of South African retired persons, therefore, if you choose a Living Annuity you are confident that you:

• Have the relevant financial knowledge to make the correct decisions in choosing your Portfolio’sorhavetakenadvicefromafinancialadvisor

• Canaccepttheriskoflivinglongerthantheaveragemale/female,ratherthaninsuringthat risk with an Insurer, i.e. purchasing a Life Annuity

• Have sufficient assets to support you in the event of continued bearish markets which may deplete your assets in your Living Annuity Account

8

MANAGING A LIVING ANNUITY FROM THE UCTRF

AsamemberordeferredpensionerorotherbeneficiaryoftheUCTRF,youmaypurchasealivingannuityfromtheFund,becomingentitledtoapension.

Drawdown percentage

A drawdown is the percentage of annual income which a Living Annuitant chooses to receivefortheyear.Youmustelectyourannuity/pensionlevelannually.Thepensioncanbepaidtoyoumonthly,quarterly,biannuallyorannually.Thismustbeapercentageofyourlivingannuitybalanceatthetimeofelection.Thispercentagemaynotbe:

i. lessthantheminimumpercentageasprescribedbytheCommissioner(seeabove);ii. morethanthelesserofthemaximumpercentageprescribedbytheCommissioner

andthemaximumpercentageprescribedannuallybytheTrusteesontheadviceofthe Actuary (unless you provide the necessary information and undertakings to the Trustees,inwhichcaseyoumaydrawuptotheprescribedmaximumpercentage– although generally it would not be wise to do so).

The Administrator of the Fundwill send your Annual Income Change form to you forcompletion within two to three months of your annuity anniversary date. Please complete and return this form to the Administrator by the due date to ensure the continuous payment of your pension.

Please note that the Fund has the discretion to limit the income percentage you draw to the prescribed maximum as calculated by the Actuary and prescribed in the Fund Rules, unless you provide the information and undertakings specified below in Rule 4.4(4)(a)(ii)(bb).

RULE4.4(4):

“(a) ThePENSIONERorBENEFICIARYmustelecthisorherpensionlevelannually.Thismust be a percentage of the LIVING ANNUITY BALANCE at the time of election. Thepercentage may not be (i) less than the minimum or more than the maximum percentage prescribed bytheCOMMISSIONERinthisregard; (ii) more than the lesser of the maximum percentage prescribed by the COMMISSIONERandthemaximumpercentageprescribedannuallyby the TRUSTEESontheadviceoftheACTUARYinthisregard,providedthat (aa) where the LIVING ANNUITY BALANCE falls below the amount prescribed

!

9

bytheCOMMISSIONER,thePENSIONERorBENEFICIARY,asthecasemaybe,may commutetheamountandbepaidthisincash;and (bb) aPENSIONERorBENEFICIARYwho (i) declaresinfavouroftheFUNDthatinmakinghisorherMEMBER investment choice for the investment of his or her LIVINGANNUITYBALANCEheorsheassumesthe investment risk associated with this choice and makes both this, and his or her election of percentage, on the basis of financial advice given to him or her, (ii) shows to the satisfactionof theTRUSTEES thatheor shehas taken advice from a financial adviser, (iii) acknowledges that by doing so he or she may erode the value of hisorherLIVINGANNUITYBALANCEtosuchanextentthatthe value of the annuity reduces to a level which is unable to support him or her, (iv) absolvesandundertakesnottoholdtheTRUSTEESortheFUND liable or responsible for the resulting erosion of the value of the LIVINGANNUITYBALANCE,then (v) may elect a percentage higher than the maximum prescribed by the TRUSTEES, but which may not exceed the maximum percentageprescribedbytheCOMMISSIONER.”

Choosing the appropriate drawdown:

WhenaLivingAnnuity ispurchasedandat leastonceayear thereafter, theFundmustprovide you with written guidance as to whether your withdrawal rate places your future pension at risk.

Apart from explaining both the advantages and the risks of a Living Annuity, a financial adviser must explain and compare these advantages and risks against conventional annuities, where a longterm insurer carries the full investment risk and the risk of the annuitant living longer than expected.

TheFundmustinformlivingannuitantsthat:

• A living annuity allows you to set your income level within the official drawdown limits (currently between 2.5% and 17.5%) and allows you to select a range of investments in respect of the capital that will generate the annuity.

• NeitherthepercentagenortheRandincomelevelselectedisguaranteedforlife.Thelevel of income may be too high and may not be sustainable if:

1)Youlivelongerthanoriginallyexpected;or2)Thereturnonthecapital is lowerthanthatrequiredtoprovideasustainableincomefor life.

10

***ThefollowingtableissuedbytheAssociationofSavingsandInvestmentsSouthAfrica(ASISA) can be used as a guideline in determining your maximum withdrawal rates:

AGE 55 60 65 70 75 80 85Male 5.4% 6.2% 7.2% 8.5% 10.3% 12.8% 16.3%Female 4.7% 5.3% 6.1% 7.2% 8.7% 10.9% 14.1%

• It is your responsibility (in consultation with the financial adviser) to ensure that the income level selected isata level thatwillbesustainable fora lifetime.The incomedrawdown relative to the investment return on the capital to achieve this, needs to be carefully managed.

• Drawdown percentages depend on each individual ‘s circumstances.

Years before your income will start to reduce:

NETINVESTMENTRETURN

(before inflation & after all fees)

ANNUALDRA

WDOWN

PERC

ENTAGE

2.5% 5% 7.5% 10%2.5% 21 30 >50 >505% 11 14 19 33

7.5% 6 8 10 1310% 4 5 6 7

12.5% 2 3 3 415% 1 1 2 2

17.5% 1 1 1 1

Thetableassumesthatthedrawdownpercentageincomeselectedwillbeadjustedovertime to maintain roughly the same amount of real income after inflation (in this case using a rate of 6.0% per annum.)

Once the number of years in the table has been reached, the income will start to diminish rapidly in subsequent years.

Thus,forexample,ifinflationremainsatabout6%p.a.overthelongterm:

1. ifyouelectadrawdownrateof5.0%perannumandtheFundearnsanaverage7.5%per annum on the underlying investment, you can expect to be able to maintain a real levelofincome(afterinflation)forsome19yearsbutthereafteryouwillhavetoaccepta reduced real income level.

2. if you buy into the living annuity at age 65, you may face a problem if you live beyond age 84, so perhaps, to err on the side of caution, the drawdown level should be reduced to 4.5% initially.

11

3. if you buy into the annuity at age 60, a drawdown level of 3.5% to 4.0% would be realistic, since (on these assumptions) 2.5% would result in the income level being maintained for over 50 years but a drawdown of 5.0% would only support the income foranexpected19years.

• It is always better to start on the lowest possible drawdown level that the you can afford, since this will allow for less chance of the capital being eroded quickly, more growth and the likelihood of being able to afford higher drawdown levels later, when you may need more (e.g. for medical costs).

• When using the table, the full financial situation should be taken into account, with all sources of income. It is an indicative guideline to assist in making informed decisions about a living annuity only.

• Living Annuitants may transfer a living annuity investment from one product providertoanother,subjecttothetermsoftheLongTermInsuranceAct(orthePensionFundsActifprovideddirectlybytheretirementfund).

• A living annuity may be converted to a conventional guaranteed life annuity administeredbyaninsurer.Thisisa“once-off ’optionthatcannotbereversed,butis useful in specific cases.

!! IT IS ADVISABLE THAT YOU SPEAK TO A FINANCIAL ADVISOR TO HELP YOU DECIDE ON THIS PERCENTAGE!!

Furtherreading:Seetheattachedarticlesfrompersonalfinance.

Investment choice

i. Living Annuity investment portfolio optionsAs a Living Annuitant you have exactly the same Portfolio options to choose from as youhadasanactivemember/deferredpensioneroftheFund,i.e.PortfolioA,B,CandD.

ii. How do I choose an investment portfolio?Living Annuitants have different needs and requirements when it comes to investments andtherisksthey,aspensioners,canaccommodate.EachPortfoliointheUCTRFhasits own unique risk profile and you choose the portfolio that is most suitable for you and with a risk profile that closely matches your needs and expectations.

iii. How important are historic returns when choosing an investment portfolio?Portfolios invested in shares will usually have good returns in some years and poor returnsinotheryears.Butoveratwenty-yearperiod,theirchanceofachievinggoodreturns is high. It is therefore not a good idea to look at short-term historic returns whendecidingonwhichportfolio tochoose.Typically,membersswitchoutofpoorperforming portfolios when markets fall and are not there to reap the good returns when these portfolios eventually recover.

12

iv. When may I switch?Living Annuitants may switch between portfolios on 31 March and 30 September of every year.

EXITS FROM A LIVING ANNUITY

Can I transfer my Living Annuity with the UCTRF to another insurer?

You may use the balance in your Living Annuity Account to purchase either a Living Annuity oraLifeAnnuityfromanotherInsurer.ThisrepresentsatransferintermsofSection14ofthePensionFundsActwhichrequirestheapprovaloftheRegistrarofPensionFunds–thisis a routine process but unfortunately tends to delay the transfer.

Can I withdraw the capital from my Living Annuity?

IfthelivingannuitybalancefallsbelowtheamountprescribedbytheCommissioner,atthat time, the pensioner or beneficiary as the case may be, may commute the amount and be paid this in cash. Otherwise, you cannot withdraw the capital.

What happens to my living annuity in the event of my death?

When selecting a living annuity, and at any time thereafter, you can nominate a beneficiary or beneficiaries to inherit your capital balance in your living annuity account.

The remainingcapital cancontinue tobepaid toyourbeneficiaryorbeneficiariesas itwas paid to you, or it can be taken as any other pension that may be purchased, or your beneficiariescanelecttotakealumpsumpayment.TheallocationisdeterminedbytheTrusteesintermsofSection37CofthePensionFundsAct24of1956.

Section37CofthePensionFundActandtherulesoftheUCTRetirementFundstatethatintheeventofyourdeath,yourbenefitintheFundshouldbedistributedasfollows:

• Tofinancialdependants;or• Financialdependantsandnominees;or• If there are no financial dependants, to nominees (but any deficit in your estate first

hastobesettled);or• If there are no dependants or nominees, to your estate.

Although the Trustees will follow members’ wishes in terms of their nomination ofbeneficiaryformasfaraspossible,thefinaldecisionofwhowillreceivetheFunddeathbenefitsrestswiththeTrustees,whomustabidebytheRulesoftheFundaswellasSection37CofthePensionFundsAct.

13

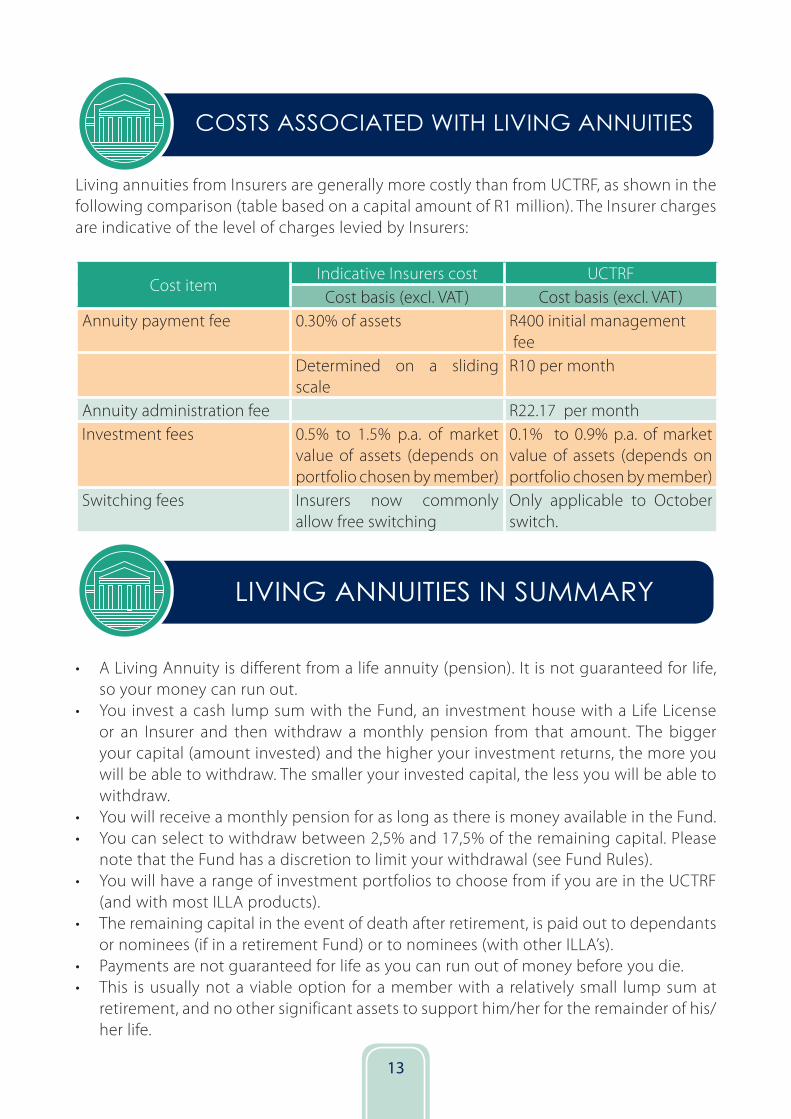

COSTS ASSOCIATED WITH LIVING ANNUITIES

LivingannuitiesfromInsurersaregenerallymorecostlythanfromUCTRF,asshowninthefollowingcomparison(tablebasedonacapitalamountofR1million).TheInsurerchargesare indicative of the level of charges levied by Insurers:

CostitemIndicative Insurers cost UCTRFCostbasis(excl.VAT) Costbasis(excl.VAT)

Annuity payment fee 0.30% of assets R400initialmanagement fee

Determined on a sliding scale

R10permonth

Annuity administration fee R22.17permonthInvestment fees 0.5% to 1.5% p.a. of market

value of assets (depends on portfolio chosen by member)

0.1% to0.9%p.a.ofmarketvalue of assets (depends on portfolio chosen by member)

Switching fees Insurers now commonly allow free switching

Only applicable to October switch.

LIVING ANNUITIES IN SUMMARY

• A Living Annuity is different from a life annuity (pension). It is not guaranteed for life, so your money can run out.

• You investacash lumpsumwiththeFund,an investmenthousewithaLifeLicenseor an Insurer and thenwithdraw amonthly pension from that amount.The biggeryour capital (amount invested) and the higher your investment returns, the more you willbeabletowithdraw.Thesmalleryourinvestedcapital,thelessyouwillbeabletowithdraw.

• YouwillreceiveamonthlypensionforaslongasthereismoneyavailableintheFund.• You can select to withdraw between 2,5% and 17,5% of the remaining capital. Please

notethattheFundhasadiscretiontolimityourwithdrawal(seeFundRules).• YouwillhavearangeofinvestmentportfoliostochoosefromifyouareintheUCTRF

(and with most ILLA products).• Theremainingcapitalintheeventofdeathafterretirement,ispaidouttodependants

ornominees(ifinaretirementFund)ortonominees(withotherILLA’s).• Payments are not guaranteed for life as you can run out of money before you die. • This isusuallynotaviableoption foramemberwitha relatively small lumpsumat

retirement, and no other significant assets to support him/her for the remainder of his/her life.

14

LIFE ANNUITIES VS. LIVING ANNUITIES?

An ILLA, for example, might be suitable for a retiree who expects to continue earning for, say, 5 years after retirement and thus “park” his retirement capital for 5 years and buy a life annuity 5 years later (taking advantage of the fact that rates for a 70 year old are very different from rates for a 65 year old, other things – especially interest rates – being equal).

Therightquestionsyoushouldask:

• How much income do you want in retirement?• How much income do you need in retirement?• How much can you afford with your retirement savings?• Do you have other sources of income? • Do you have the relevant financial knowledge to make the correct decisions in choosing

yourPortfolio’s• What will happen to the pension income over time taking into account the future

inflation? Or put simply, how much would you be able to afford to buy with your pension 20 years from now?

• Canyousacrificeaportionoftheincomenow,toenjoyrelativelyhigherincomelaterin retirement?

• What impact will different investment strategies have on you pension in the future?• What is the risk of outliving your retirement savings?

Receive a guaranteed income for the rest of your life (life annuity)

If you choose the life annuity, you will be provided with a guaranteed income throughout your retirement years as long as you are alive. You will receive the annuity income after the deduction of any required tax throughout your lifetime. On death, the annuity income will end (unless you choose a life annuity with a guaranteed payment term and you die before the end of the guarantee term).

The life annuity provides the following options at the start of your policy (note, thesecannot be changed after the start of your policy):

• Annuity income increase rate: You can choose at what level to have your income increase at each policy anniversary.

• Guarantee term: You can choose to have your income payable for a guaranteed period.Thisensuresthatondeathbeforetheendoftheguaranteeterm,yourannuityincomewillcontinueuntiltheendoftheguaranteeterm.Theincomewillbepayableto your chosen beneficiaries.

• Joint annuity: You can choose to have your income payable for as long as you or your spouse is alive. You may also choose to have your income decrease to a certain level after the first death for the remainder of the life of the surviving spouse.

15

OR

Manage your own investment and leave a legacy (living annuity/ ILLA)

A living annuity allows you to manage your investment. Your investment will be invested in your choice of funds and the income you receive will be determined by the amount you choose to withdraw out of your living annuity account. According to current legislation, you may choose to withdraw between 2.5% and 17.5% of your investment fund each year. You may change the amount of income which is paid each year in accordance with legislated limits. You also have the option to transfer the remaining funds in your living annuityalifeannuity;however,alifeannuitycannotbetransferred.Thisoptionwillsuityour needs if you want to manage your investment and have the flexibility to change your incomefromtimetotime.Underthisstructureitwillbeyourresponsibilitytoensurethatyour investment is enough to sustain your income throughout your retirement years. On death, any remaining funds will be paid to your beneficiaries. You need your savings to continuetosustaintheincomeyouneedforacomfortableretirementonceyou’reretired.That’swhyit’simportanttochooseaninvestmentstrategythatminimisesthelikelihoodof a shortage in incomeduring retirement.Thebest solutionmaynotbe theone thatgives you what you want right away.

Here’s an example of aman retiringwith R1 000 000 in fund savings.The table belowshows the initial monthly income you could expect to get from different types of annuities (pensions):

TypeofpensionInitial monthly pension

Value of pension in 10years’time,afterinflation*

Value of pension in 20years’time,afterinflation*

Level annuity 7 160 3998 2233Fixedincreaseannuity(atafixedrateof5%peryear)

4 333 3942 3585

With-profitannuity 4960 4700 4404Inflation-linked annuity 4110 4110 4110Living annuity (at 7% income draw down rate)

5733 5733 1136

*Figuresarebasedoncertainactuarialassumptions*Key observations:

• Level annuity is unlikely to meet your income needs and wants.• Fixedincreasesannuityhasagoodchanceofmeetingyourincomeneeds.• With-pofit annuity has a fair chance of meeting your income needs and a poor chance

of meeting your income wants.• Inflation-linked annuity is certain to meet your income needs throughout retirement.• Living annuity has a fair chance of meeting both your income needs and wants in

retirement.

16

ARTICLES FROM PERSONAL FINANCE

LIVING ANNUITIES MUST BE USED CORRECTLY

June 10 2012 at 12:05pm ByBruceCameron

To start with a bald statement: there is nothing fundamentally wrong with using aninvestment-linked living annuity (illa) to provide a pension. The costs do need to bereduced, but illas are an essential pension-paying option.

Theproblemwithillaslieswithhowtheyhavebeenusedincorrectlybyannuitants,oftenon the basis of poor advice from financial advisers who, without any qualifications in assetmanagement,haveneverthelessprovidedadviceoninvestments.Thefeeschargedbytheseadvisersalsocontributetothecoststhat,NationalTreasurysays,reduceanillapension by about 20 percent.

Despite these drawbacks, illas are an essential option in times of low interest rates.Traditional guaranteed annuities,which are bought from life assurance companies, arebased on prevailing long-term interest rates, your age and your gender.

Theolder you are, thehigher thepension youwill bepaid, because the life assurancecompany does not expect that you will live as long as someone who is younger.

Women are expected to live longer than men, so they receive a lower monthly pension, but on average over time the same as earlier-dying men.

Thekeyproblemisinterestrates.Ifinterestratesarelowwhenyouretire,thelowratewillbe reflected in your pension, because the life assurance company will use mainly long-term bonds as the underlying asset to pay your pension, locking you into that low rate. If interest rates are high when you retire, you will receive a much higher pension, then and into the future.

So currently, if you are under the age of 70, a traditional guaranteed annuity may be an unwise decision.

Lastweek,PersonalFinancepublisheddetailsoftwopiecesofresearchthatshowedthat

17

many, if not most, pensioners with illas face the probability of running out of money before they die, particularly if they live for longer than average.

It is absolutely essential that the investments underlying an illa are made by people who know what they are about. And it is just as important that the pension you draw down as a percentage of your annual capital is kept at five percent or less.

Thefive-percentruleisbasedonvariouspiecesofresearchundertakeninrecentyears.If you draw more than five percent a year, there is a very good chance that you will run outofmoney.Theonlyexceptionsareifyouretirelaterinlifeorifyouexpectashorterlifespan, such as suffering from a life-shortening medical condition.

Theresearchwepublishedlastweek,showinghowprecariousthesituationisformanyilla pensioners, resulted in some rather silly financial advisers claiming on various websites thatPersonalFinancehadgotitwrongandthatwewerescaringretireesoffillas.

What nonsense. We reported on research that shows that, on average, illa pensioners are drawing down too much as a pension, and the situation is getting worse every year.

Wecouldnotget itwrong, simplybecause itwasnotour research.The researchcamefrom financial services industry organisation the Association for Savings & Investment SA (Asisa)andthecountry’sbiggestretirementfundservicesprovider,AlexanderForbes.Andthere is no reason to assume that either of them got it wrong – both have a sound track record on research.

Perhaps some of those silly financial advisers provided inappropriate advice and now they have unhappy clients.

Overall, the Asisa figures do not look that bad, with the average drawdown rate at seven percent – two percentage points more than the target of five percent.

Asisa was pleased that, on average, the drawdown figure was not greater than seven percent – it had been concerned that the situation could be worse.

Theproblemwithpercentagesisthenumberofpeoplewhoareabovetheaverage.Forevery person below the average, there is another one who is above the average.

What is of concern is that the average pensioner over the age of 75 is receiving a monthly illapensionofR1640,and21.3percentinthisagegrouparedrawingdownapensionat17.5 percent or greater, meaning they could outlive their capital.

Thismeansthatsomethingwentverywrongintheearlyyearsoftheirretirement.Theirinvestment choices were a mess and/or they drew down too large a percentage of their retirement savings.

18

The research is an apt and timely reminder that great caremust be taken with livingannuities. If you get it wrong at the start of your retirement, you will pay a significant penalty later on.Peter Dempsey, Asisa deputy chief executive, correctly warned last week that no pension can make up for a shortfall in retirement savings – and particularly not an illa.

Incidentally, all illa pensioners should consider switching to a guaranteed annuity in their seventies, because, even if interest rates are low, a guaranteed pension becomes a lot more favourable and can better an illa, particularly because of the guarantees.

LIVING ANNUITY PENSIONERS IN DANGER OF RUNNING OUT OF MONEY

June 3 2012 at 12:35pm ByBruceCameron

Thevastmajorityofpensionerswhodependoninvestment-linkedlivingannuities(illas)are drawing down incomes that could leave them unable to maintain their lifestyles if they live for a long time.

A financial services industry survey released this week shows that almost 70 percent of illa pensioners are, in the initial years of their retirement, drawing down more than five percent of their retirement savings – a drawdown rate of five percent will enable an illa to be sustainable, numerous researchers have found.

The figures were revealed in the first annual Association for Savings & Investment SA(Asisa) illa survey.

TheAsisaresearchshowsthat21percentofillapensionersmayrunoutofmoneywithin7.5 years, because they are drawing down pensions equivalent to 15 percent or more of their retirement savings.

Most pensioners who are drawing down higher-than-acceptable pensions have smaller rand amounts saved for retirement. And, by number of pension contracts sold, 12 percent of illa pensioners are drawing the maximum allowed pensions of 17.5 percent (on illas sold from 2007) and 20 percent (on illas sold before 2007).

Theresearchalsoshowsthatthe6693illapensionerswhoaredrawingamonthlyincomeatratesof17.5percentto20percentarereceivinganaverageofonlyR1640,whichisamereR440morethanthestateold-agegranttotheindigentwhoare60yearsandolder.

Thisindicatesthatthesepensionersaresufferingtheconsequencesofhaving:*Madebadinvestments;*Drawndownanincomeatratesthatweretoohighintheearlyyearsoftheirretirement;and/or

19

* Saved too little for retirement.Although Asisa says the situation is, on average, better than it expected, other research released this week by retirement fund ser-vices provider Alexander Forbes shows aworsening trend, with illa pensioners drawing down more and more each year (see graph, link at the end of the article).

AlexanderForbeshasfoundthatillapensionersarereasonablyactiveintheirdrawdownchoices every year and have generally increased their percentage drawdown rates over the past few years.

JohnAnderson,AlexanderForbes’smanagingdirector:researchandproductdevelopment,says there is also a trend of more illa pensioners choosing the highest drawdown category.In 2007, 22 percent of annuitants were on the maximum drawdown rate of 17.5 percent, but last year 35 percent of pensioners were on the maximum drawdown rate. Anderson says it is of concern that the percentage of annuitants who are drawing down more than 15 percent has risen from 27 percent in 2007 to 43 percent in 2011.

“With muted returns expected in future, this leaves very little option for these pensioners other than adjusting their lifestyles downwards or running out of money,” he says.

Last year, R23.9 billion flowed into living annuities provided by 21 Asisa companies,bringingthetotalamountinvestedtoR155.2billionbyDecember31,2011.Intotal,therewere278415 illacontracts.Basedonthenumberofpoliciesheld, theaveragepensiondrawdownratelastyearwas9.31percent,butwhencalculatedbytherandvalueofeachilla,theaveragedrawdownratewasonly6.99percent.

Consulting actuaries Geoff London & Associates, which collated the figures for theAsisa research, say this “significant discrepancy” implies that illa pensioners with smaller amounts of money are drawing down, as a percentage, larger amounts than are wealthier illa pensioners.

Peter Dempsey, Asisa deputy chief executive, says overall the figures show that, at an averagedrawdownrateofaboutsevenpercent,Asisaconsiderstheriskofanillapensioner’scapital “being completely eroded is much lower than previously thought”.However, the industry would prefer to see an average drawdown rate that is closer to five percent. An unknown percentage of drawdowns at higher rates are made by people who had a shorter life expectancy due to ill-health or advancing age, as well as withdrawals by beneficiaries who receive an illa after the death of the pensioner. Shorter life expectancy explains the high drawdown rates of people under the age of 55 and over the age of 70, Dempsey says.

“Asset managers and economists agree that investors can expect returns of between five and 10 percent in the foreseeable future, which will help to protect capital, provided drawdown rates remain in the same range and policyholders maintain an appropriate asset composition in their portfolios,” he says.

20

Unfortunately,therearepeoplewhohavenotsavedenoughforretirementwhoturntoillas for the wrong reason, Dempsey says.

Pensioners who have chosen illas because they can draw down higher initial pensions than those offered by guaranteed annuities will face hardship if they have sufficient retirement capital to maintain a certain lifestyle only in the early years of their retirement, he says.

ILLAS PUT THE BALL IN YOUR COURT

Theinvestment-linkedlivingannuity(illa)structure,whichwascreated22yearsago,hasleft a large but unknown number of pensioners facing destitution, because they were not provided with proper advice by either the product providers or financial planners.

The illa (pension)productsareboughtat retirementusingsavings ina tax-incentivisedretirement fund, including pension funds and retirement annuity funds.

An illa pensioner is required to:* Withdraw an annual income of between 2.5 percent and 17.5 percent of his or her residual capital.Thedecisionontheratemustbemadeannuallyontheanniversaryoftheproduct.*Takeresponsibilityfortheunderlyinginvestments.Thepensionertakestheriskthattheinvestments will provide, after costs, an after-inflation return that will sustain the income flowuntildeath.Byindustryagreement(notlaw),theunderlyingassetallocationshouldmeettheprudentialinvestmentrequirementsofregulation28ofthePensionFundsAct,which limits how much may be invested in a particular asset class and sub-asset class.

On death, the annuitant may bequeath the illa to his or her heirs, who can decide to withdraw the capital in cash or receive an income taxed in their hands. As a consequence, a bequeathed illa is not subject to estate duty.

STANDARDS AIM TO ENSURE YOUR PENSION LASTS

In an attempt to ensure the proper use of investment-linked living annuities (illas), the Association for Savings & Investment SA (Asisa) has provided a set of standards to govern the sale and maintenance of the products.

The action was taken following tales of financial hardship from illa pensioners, withcomplaints to various adjudicators and ombuds, and subsequent government intervention, as well as research that established it is very unwise, in most cases, to withdraw more than five percent of the annual value of the residual capital if an illa is to be sustainable.

Members of Asisa must ensure that all the illas they market, administer or underwrite comply with the “Standards on living annuities”, and they must ensure that independent intermediaries who sell their products also comply with the standards.Thefourillaproductstandardsare:

21

Standard 1. Appropriate drawdown

An illa allows you to set your income level subject to the official drawdown limits (between 2.5 and 17.5 percent).

Neither the percentage nor the rand income level you select is guaranteed for the rest of yourlife.Theincomelevelyouselectmaybetoohighandmaynotbesustainableif:

• Youlivelongerthanyouexpected;or• Thereturnonthecapitalislowerthanthatrequiredtoprovideasustainableincome

for life.

As part of the standard, Asisa has published an indicative table (see “Years before your income will start to reduce”, link at the end of the article) to assist you to decide on an appropriate drawdown rate. The table assumes that, over time, you will adjust thepercentage drawdown to maintain the same amount of real income (that is, allowing for inflation of six percent a year). Once the number of years in the table has been reached, your income will diminish rapidly in the subsequent years. When using the table to set a drawdown rate, you should take into account your financial situation and all your sources of income.

Thetableisaguidelineonly,toassistyouinmakinginformeddecisionsaboutyourannuity.Thetablemayalsobestructuredsothatitshowstheeffectsofinflation,withthecolumnheadingsasreal(after-inflation)returns,suchas“CPI–3.5%;CPI–1%;CPI+6.5%”.

In terms of the standard, you may:

• Transfer your illa fromoneproductprovider to another, in termsof either theLongTermInsuranceActorthePensionFundsAct;and

• Convertanilla(inpartorinfull),whenitisgovernedbytheLongTermInsuranceAct,to a conventional guaranteed life annuity administered by the current life assurer or by anotherassurer.Thisisaonce-offoptionthatcannotbereversed.

Standard 2. Appropriate investments

An illa allows you to select a wide range of investments in respect of the capital that will generate theannuity.The risk to the investments thatunderlieyourannuity shouldbeassessed annually.

You shoulduseprudential investment regulation28under thePension FundsAct as ageneral guide to assess the overall asset composition of the investments that underlie your annuity. Among other things, regulation 28 sets a maximum exposure of 75 percent to equities and 25 percent to property.

22

Standard 3. Asset composition information

You must be told the actual asset composition of your illa at retirement and at least once a year thereafter, to allow you and your financial adviser to assess the risk in line with standard 2.

Standard 4. Industry-based analysis and monitoring

Asisa members that provide illas are required at the end of each year to provide illa status reports to Asisa.

PRESERVATION FUNDS MAY NOT SURVIVE

National Treasury is considering changing the drawdown rates for investment-linkedliving annuities (illas) from between 2.5 percent and 17.5 percent to between zero and 17.5 percent.If the rate can be as low as zero, preservation funds are likely to be under threat, because you may be able to transfer directly to an illa the savings you have accumulated in an occupationalretirementfundthatyouwanttopreserveforretirement.Thiswouldsaveyou the future cost of transferring from a preservation fund to an illa, bypass the costs of a preservation fund and potentially provide you with a better pension.

And in a financial emergency, you may have greater access to your money on an ongoing basis (as a pension withdrawal) than you would with a preservation fund, which allows you to make one withdrawal.

TREASURY WARNS IT MAY REGULATE ALL RETIREMENT PRODUCTS

National Treasury has warned that it may have to consider regulating the costs of allretirement products if the financial services industry and government cannot resolve the problem of the excessively high cost of retirement and pension products.

ThiswarningwasissuedbyOlanoMakhubela,NationalTreasury’schiefdirectoroffinancialinvestments and savings, at a series of roadshows on retirement fund regulation organised bytheFinancialServicesBoard.

NationalTreasurywouldprefernottohavetoregulatecosts,anditiscurrentlyindiscussionwith the industry on how it can reduce the costs of its products to acceptable levels, Makhubela says.

Researchbygovernmentandothershasshownthatretirementproductsofferedbythefinancial services industry in South Africa are high by international standards.

Makhubela also repeated concerns about the potential for investment-linked living annuities (illas) to provide a sustainable income in retirement.

23

Makhubela says that illas have three risks, namely, that pensioners will draw down too much, live for a long time and make poor investment decisions – and any of these risks could “quite easily result in a depletion of retirement savings”.

Pension products are costly and often confusing, and this is why government is pressing for the introduction of default pension products that retirement fund trustees can offer to their members and that will be low cost and simple, requiring no financial advice, he says.Inarecentdiscussiondocumentonsaving,NationalTreasurysaidthatcostsarereducingpotential illa pensions by 20 percent.

Tomake illasmore competitive on costs, NationalTreasury plans to introduce its ownlow-costillalinkedtoRSARetailBonds,whichoffer,amongotherthings,inflation-linkedreturns.

THE COST OF RETIREMENT SURVEYBY BRUCE CAMERON

Thecostofretirementisfargreaterthanmostpensionersbelievedatretirementitwouldbe. Only 40 percent of pensioners now believe they saved enough for retirement.

But themessage isgettingthroughto retirement fundmembers -75percentofactivemembersnowbelievetheyneedtostartsavingforretirementatage20,although19.4percent are of the opinion that it can be left until age 30.

However, only half of active members say they are on track for a financially secure retirement.These are two findings of the SanlamEmployee Benefits Benchmark annualretirement survey. For the 2010 survey Sanlam |included extensive research on theattitudes andexperienceofboth active retirement fundmembers |andpensioners.Thepensioners surveyed have a message for those people still saving for retirement: you must start checking whether you are saving enough money for retirement more than 20 years before you retire.

Even those pensioners who believe they saved enough are worried that their money may run out if they are in retirement for an extended period because of increased longevity.About 30 percent of the surveyed pensioners, whose average age was 67, indicated that theyarealready |experiencingfinancial |difficultiesandarebeingforcedtocutbackonnon-essentialitems.Almost75percentofthepensionersgetapensionoflessthanR10000 a month. Against this, the average amount active members who were surveyed earn nowisR15449amonth.

ThesurveyconfirmsearlierresearchbyAlexanderForbes,whichshowedthatretirementfund members are going into retirement without having saved for long enough and are compounding the effects of their lack of savings by retiring too early. And most pensioners find they have not taken sufficient account of the costs of retirement, particularly medical expenses.

24

Of the 250 pensioners surveyed, the average period of contributing to a retirement fund (an occupational fund or a retirement annuity) was 26.6 years.

Theaverageageof retirementwas59,withalmost60percenthavingnochoiceaboutretiring early because of retrenchment or disability. Consequently, their pensions arelower than expected.

Most active members expect to have retired by the age of 61.

Other facts revealed by the pensioner survey include:

• The vastmajority say if they could havedone anythingdifferently before retiring itwouldhavebeentoplanbetterandsavemore;

• More than half the pensioners believe you have to save a capital amount for retirement in excess of 10 times your final annual income.

• In worst-case scenarios, 12.1 percent of the pensioners forced into early retirement say that early retirement had “huge financial implications” for them, with 16 percent depending on others for additional income, 3.4 percent having to sell their homes and 5.2percenthavingtogiveuptheirmedicalschememembership;

• Almostsixpercentofthepensionerslivewithrelatives;• •Manypensioners go into retirement having to use lump sumpayments from their

retirement|savingsorothersavingstopayoffdebt,andalmostsixpercentcontinuetopayoffahomeloan;

• About 35 percent of the pensioners had to cut back on spending because of the economicrecession;

• About54percentofthepensionershaveotherinvestmentsapartfromtheirpensions;• Of the surveyed pensioners, 16.4 percent changed jobs at some stage, and of these 44

percentcashedintheirretirementsavings,leavingthemworseoffinretirement;• Morethan40percentofthepensionersreceivedpre-retirementadvicefromemployers;• Of those who received financial advice before retiring, 71 percent received advice

based on a financial analysis, with the vast majority then understanding their needs in retirement;

• Mostpensionersspentlump-sumpaymentsreceivedatretirementwithin30months;and

• Thereare27percentofpensionerswhostillmanagetosavemoneyeverymonth.