How Managerial Motives Can Erode Value Creation

29

-

Upload

xuxia-concepcion -

Category

Documents

-

view

286 -

download

19

description

Strategic Management Lumpkin, Dess, Eisner 5th Edition Chapter 6 Corporate-Level Strategy

Transcript of How Managerial Motives Can Erode Value Creation

managers acting in their own interest rather than in maximizing long-term shareholder value

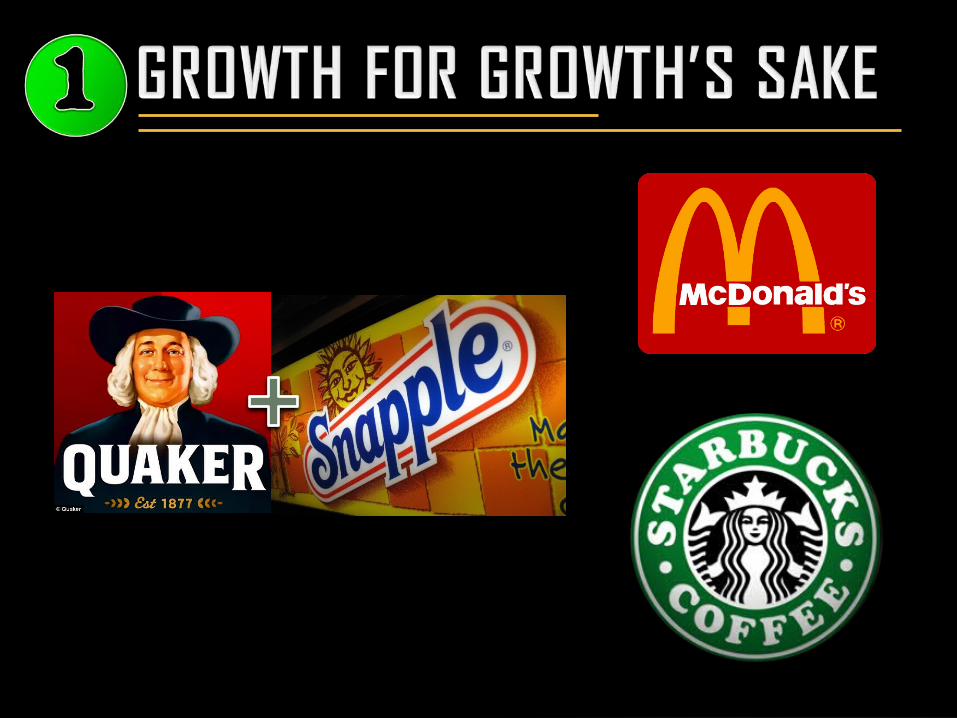

Increasing the size of the firm to achieve greater revenues leaving out the greater need to increase profits

The executive ego, especially when combined with the influences from the bankers, lawyers and other assorted advisers who can earn big fees from clients engaged in mergers, is a major force in expanding the business. Most CEOs get to where they are because they want to be the biggest and the best, and many top executives get a big bonus for merger deals, no matter what happens to the share price later.

management team feels they have no choice and must acquire a rival before being acquired. The idea is that only big players will survive a more competitive world.

the practice of purchasing enough shares in a firm to threaten a takeover, thereby forcing the target firm to buy those shares back at a premium in order to suspend the takeover.

ADVANTAGEperpetuates the company's existing management and employeesDISADVANTAGEwhile benefiting the predator,the company and its shareholderslose money

Changes in the details of corporate ownership structure, in the investment markets generally, and the legal Requirement in some jurisdictions for companies to impose limits for launching formal bids, or obligations to seek shareholder approval for the buyback of its own shares, and in Federal tax treatment of greenmail gains (a 50% excise tax) have all made greenmail far less common since the early 1990s.

RUPERTMURDOCH

GREENMAILER

GREENMAILER

GREENMAILEE

A pre-arranged contract with managersspecifying that, in the event of hostiletakeover, the target firm’s executives will be paid a significant severance package (severance pay, stock options, and cash bonuses).

The terms can be weighed so heavily in the employee’s favor that it almost seems like termination could come as good news.

1. Cost the company money.2. Deter motivation.3. Create resentment with other employees. 4. Expose the fact that executives may not be

objective in the event of a takeover.5. May not necessarily discourage hostile

takeovers.

ADVANTAGES

Help companies attract the

best executive talent

Discourages mergers, which are usually beneficial to investors

DISADVANTAGESExecutives may not be as

motivated to do their job because they stand to make as much or more through their various severance packages than by working

The existence of golden parachutes is evidence that there is a strong management bias

TONY HAYWARD

CARLY FIORINA

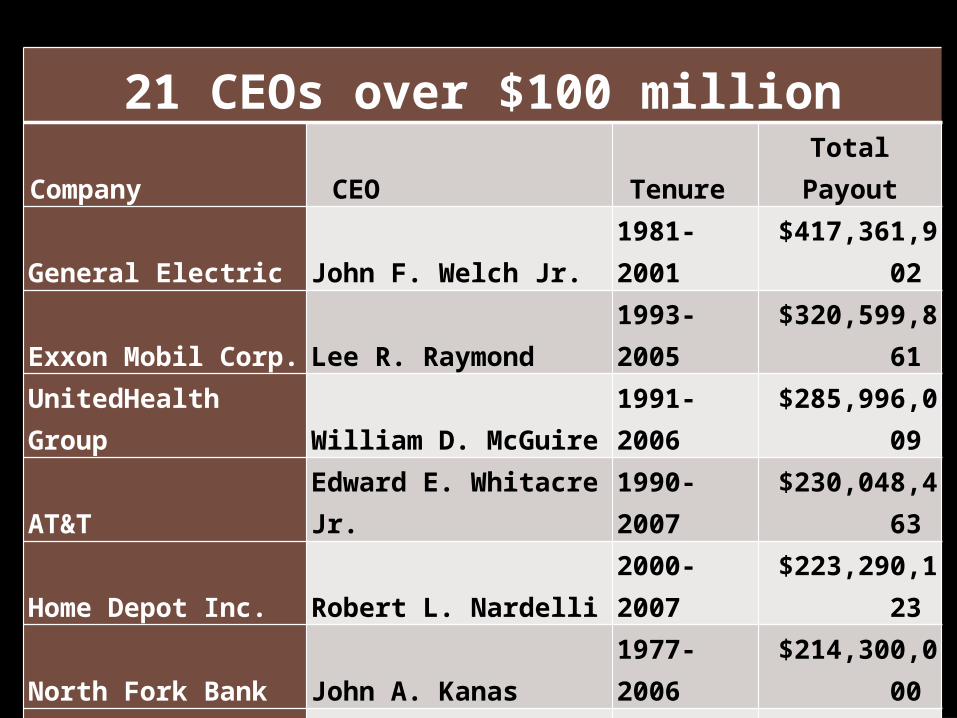

21 CEOs over $100 million

Company CEO Tenure Total

Payout

General Electric John F. Welch Jr. 1981-2001

$417,361,902

Exxon Mobil Corp. Lee R. Raymond 1993-2005

$320,599,861

UnitedHealth Group William D. McGuire

1991-2006

$285,996,009

AT&T Edward E. Whitacre Jr.

1990-2007

$230,048,463

Home Depot Inc. Robert L. Nardelli 2000-2007

$223,290,123

North Fork Bank John A. Kanas 1977-2006

$214,300,000

Merck & Co., Inc./Schering-Plough Fred Hassan

2003-2009

$189,352,324

IBM Louis V. Gerstner Jr. 1993-2002

$189,005,929

Pfizer Inc. Hank A. McKinnell Jr.

2001-2006

$188,329,553

CVS Caremark Corp. Thomas M. Ryan

1998-2011

$185,415,435

Gillette Co. James M. Kilts 2001-2005

$164,532,192

Company CEO Tenure Total

Payout

Target Corp. Robert J. Ulrich 1994-2008

$164,162,612

Merrill Lynch & Co. E. Stanley O'Neal 2002-2007

$161,500,000

U.S. Bancorp Jerry A. Grundhofer

2001-2006

$159,064,090

Omnicare, Inc. Joel F. Gemunder2001-2010

$146,001,476

Wachovia/South Trust

Wallace D. Malone Jr.

1981-2004

$125,292,818

United Technologies Corp.

George A. L. David

1994-2008

$122,631,309

eBay Inc. Margaret C. Whitman

1998-2008

$120,427,360

WellPoint Health Leonard Schaeffer

1992-2004

$119,041,000

XTO Energy Inc. Bob R. Simpson 1986-2008

$103,485,972

Viacom Thomas E. Freston 2006

$100,839,772

- used by public companies togive shareholders certain rights in the event of takeover by another firm

- to protect themselves from investors they fear may oust themfollowing a takeover

If a hostile takeover occurs, investors have the option to purchase the bidder’s shares at a discount, thereby devaluing the acquirer’s stock and diluting its stake in the company.

Management offers shares to investors at a discount if an acquirer merely purchases a certain percentage of the company. The discount is not available to the acquirer, and so it becomes extremely expensive for that acquirer to complete the takeover. Experts estimate that it would cost an unwanted bidder, on average, four to five times more to “swallow” a poison pill in order to acquire a target.