Lamaque Mine Due Diligence Report - StockIgloo a long-term, modern and efficient mining operation....

51

Lamaque Due Diligence www.centurymining.com Lamaque Mine Due Diligence Report January 14, 2009 Prepared by: Century Mining Corporation

Transcript of Lamaque Mine Due Diligence Report - StockIgloo a long-term, modern and efficient mining operation....

Lamaque Due Diligence

www.centurymining.com

Lamaque Mine Due Diligence Report

January 14, 2009

Prepared by: Century Mining Corporation

Lamaque Due Diligence January 2009

Section i

EXECUTIVE SUMMARY Overview

This Due Diligence Report was prepared by Century Mining Corporation’s (“Century” or the “Company”) technical, corporate and mine site staff. The Company is listed on the Toronto Venture Stock Exchange (TSXV) under the symbol “CMM”. Century controls, among other mineral assets, mineral properties in the province of Quebec, Canada, which contain gold deposits and are the subject of this report. This report describes the Lamaque Underground Gold Mine (“Lamaque Mine” or “Project”) camp which is host to massive gold bearing quartz veins, dykes and shears along the historically productive Abitibi Gold Belt. This report also defines the mineral reserves and resources which served as the basis for the April, 2008 NI 43-101 compliant technical report submitted by Mr. Callum Mark, M.Sc., P.Geo, of Clearwater Resources Limited, included as Appendix A. The compliant reserves and resources were later reviewed and updated in December, 2008 by Dr. Ed van Hees. Dr. Ed van Hees results can be found in a January 13, 2009 independent due diligence report prepared by Puma Resources Ltd. Dr. Ed van Hees and Mr. Callum Mark are designated as Qualified Persons with the ability and authority to verify the authenticity and validity of the data. Century’s property contains many underexplored or grass roots ore targets that in aggregate contain a large tonnage of material which is currently classified as inferred resources. The due diligence report was developed by Century, and shows the economic feasibility of mining the Lamaque Mine complex. A summary of salient results of the Project is shown in Table i-1. Numerous documents in digital, scanned, or hard-copy format, the majority of which pertain to the Lamaque Mine complex, were used in the preparation of this Technical Report, with the primary reference being an independent due diligence report prepared by Puma Resources Limited and Independent Associates comprising of Dr. Ed van Hees and EBA Engineering Consultants Ltd. The combined due diligence efforts are located near the end of this document summary.

2

The Lamaque Mine property was personally inspected by independent Qualified Persons (QP) and Century Technical staff numerous times throughout 2008. The listed QP’s did not independently verify this report in its entirety, but, contributed through their own independent reports referenced in the appendices. All personal direct and indirect references utilized in reviewing and compiling this Due Diligence Report are as follows:

Lamaque Due Diligence January 2009

• Mr. Callum Mark, M.Sc., P.Geo, Clearwater Resources Limited

• Mr. Patrick Gorman, C.Eng, M.S, M.s, B.Sc., MIMM, Managing Director, Puma Resources Limited.

• Mr. Edmond H.P. van Hees, Ph.D., P.Geo., Assistant Professor, Wayne State University, Detroit, Michigan, USA.

• Mr. John A. Foster, PhD., RPBio., Principal Consultant, EBA Engineering Consultants.

• Mr. Richard A. W. Hoos, M.Sc, RPBio., Principal Consultant & Senior Environmental Scientist, EBA Engineering Consultants.

• Ms. Margret M. Kent, B.Sc., M.Sc., President & CEO, Century.

• Mr. David Swisher B.Sc., Vice President, Senior Project Manager Century.

• Mr. Ross Burns, B.Sc., P.Geo., Vice President Exploration, Century.

• Mr. Adrian McNutt, B.Sc., Vice President Operations, Century.

• Mrs. Eileen Olivier, Human Resources Manager, Century.

• Mr. Pascal Hamelin, B.Sc., P.Eng., Lamaque General Manager, Century.

• Mr. Wolfgang Schleiss, P.Geo., M.Sc., Senior Geologist, Century.

• Mr. Albert Siega, B.Sc., MBA, Mining & Resource Engineer, Century.

• Mr. Justin Smoak, B.A., B.Sc., M.Eng., Mining & Financial Engineer, Century.

Century Mining Corporation is re-developing its wholly owned Lamaque Underground Gold Mine at Val D’Or in Quebec, Canada. The underground mine has an 80 year history and has produced 9.2 million ounces of gold at a head grade of 5.2 g/t gold. Currently the mine has a NI 43-101 reserve of 1.13 million ounces of gold. The surface infrastructure is in place and fully serviceable including a nearly new, state-of-the-art, 1.25 million tonne per annum CIP plant, which was upgraded in 2001. The mine is currently permitted at a rate of 1,200 tonnes per day but has been on care and maintenance since July 2008, due to the lack of available capital needed to properly expand operations and achieve reasonable commercial returns. The Company is seeking a senior debt facility of USD$55 million to restart the Mine and establish a long-term, modern and efficient mining operation. Century’s Due Diligence Report shows that the mine will produce over 1 million ounces of gold at a cash cost of USD$421 per ounce and has a NPV @ 10% discount rate of USD$88.2 million. The mine, over a 10-year mine life, will generate USD$168 million in free cash.

3

Lamaque Due Diligence January 2009

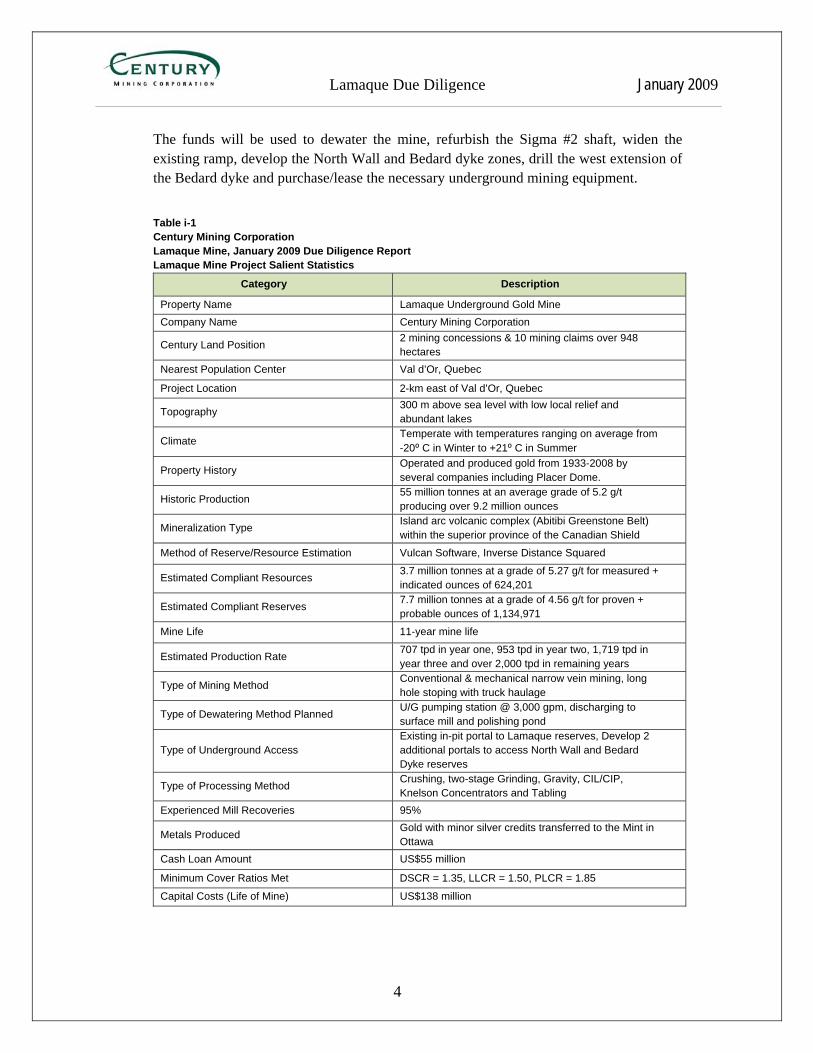

The funds will be used to dewater the mine, refurbish the Sigma #2 shaft, widen the existing ramp, develop the North Wall and Bedard dyke zones, drill the west extension of the Bedard dyke and purchase/lease the necessary underground mining equipment. Table i-1 Century Mining Corporation Lamaque Mine, January 2009 Due Diligence Report Lamaque Mine Project Salient Statistics

4

Category Description

Property Name Lamaque Underground Gold Mine Company Name Century Mining Corporation

Century Land Position 2 mining concessions & 10 mining claims over 948 hectares

Nearest Population Center Val d’Or, Quebec

Project Location 2-km east of Val d’Or, Quebec

Topography 300 m above sea level with low local relief and abundant lakes

Climate Temperate with temperatures ranging on average from -20⁰ C in Winter to +21⁰ C in Summer

Property History Operated and produced gold from 1933-2008 by several companies including Placer Dome.

Historic Production 55 million tonnes at an average grade of 5.2 g/t producing over 9.2 million ounces

Mineralization Type Island arc volcanic complex (Abitibi Greenstone Belt) within the superior province of the Canadian Shield

Method of Reserve/Resource Estimation Vulcan Software, Inverse Distance Squared

Estimated Compliant Resources 3.7 million tonnes at a grade of 5.27 g/t for measured + indicated ounces of 624,201

Estimated Compliant Reserves 7.7 million tonnes at a grade of 4.56 g/t for proven + probable ounces of 1,134,971

Mine Life 11-year mine life

Estimated Production Rate 707 tpd in year one, 953 tpd in year two, 1,719 tpd in year three and over 2,000 tpd in remaining years

Type of Mining Method Conventional & mechanical narrow vein mining, long hole stoping with truck haulage

Type of Dewatering Method Planned U/G pumping station @ 3,000 gpm, discharging to surface mill and polishing pond

Type of Underground Access Existing in-pit portal to Lamaque reserves, Develop 2 additional portals to access North Wall and Bedard Dyke reserves

Type of Processing Method Crushing, two-stage Grinding, Gravity, CIL/CIP, Knelson Concentrators and Tabling

Experienced Mill Recoveries 95%

Metals Produced Gold with minor silver credits transferred to the Mint in Ottawa

Cash Loan Amount US$55 million

Minimum Cover Ratios Met DSCR = 1.35, LLCR = 1.50, PLCR = 1.85

Capital Costs (Life of Mine) US$138 million

Lamaque Due Diligence January 2009

Operating Costs per ounce US$421 per ounce NPV @ 10% Discount US$88.2 million

Net Cash Flow US$168.3 million

Gold Spot Price Assumption $780/oz in 2009, $825/oz in 2010, $800 for 2011, $650/oz for 2012-2013 and $600 for the remainder.

Location

Century’s Lamaque properties, are located approximately 500 km (300 mi.) northwest of Montreal, Quebec, Canada, within the City limits of Val-d’Or, Quebec, in Bourlamaque Township, Abitibi County, Province of Quebec, at latitude 48°06’ N and longitude 77°45’ E. The Project area is within the Abitibi belt adjacent to the Cadillac break and is one of the few mines in North America that has produced in excess of 300 tonnes of gold. The region is typical Canadian Shield type terrain with low local relief and abundant lakes. Topographic elevation is approximately 300 m above sea level and generally varies less than 100 m. Large areas are dominated by swamp and ponds. Predominant local flora in the area includes spruce, pine, fir and larch with a much smaller percentage of deciduous trees, such as birch and poplar. The mine site is bordered to the north by a large unpopulated wooded area that is currently used for tailings and waste rock disposal. Winter conditions are temperate to sub-arctic, with mean average January temperatures at -17° C. Summers are hot and relatively dry with long daylight periods and a mean July temperature of +17.2° C. The mean annual precipitation is 90.9 cm, with the heaviest precipitation occurring between May and October. Comprehensive environmental surveys by past and present operators have been completed as input into the Due Diligence Report, and monitoring is discussed in more details in Section 9.0. Access to the Project area is by 530 kilometres of paved Provincial Highway 117 north from Montreal, Quebec to Val d’Or, Quebec. The Lamaque Mine is located two kilometres east of the City of Val d’Or and straddles Provincial Highway 117. Val d’Or has all major services including hydro-electric power, an airport with scheduled jet service from Montreal, a rail terminal and a daily bus service from Montreal to Val d’Or and to other cities in the Abitibi region.

5

Lamaque Due Diligence January 2009

Project Ownership

The Lamaque Mine is located on 6 mining concessions totalling 805.61 hectares, one mining lease of 41.58 hectares and 11 claims containing 148 hectares. A 100% owned Century subsidiary owns 58 contiguous claims on the eastern border of the mine property containing 775.9 hectares plus a non contiguous mining lease. Another 100% owned subsidiary controls the Sigma II open pit mine, located 20 km. east of Sigma, that produced during the late 1980’s. The Lamaque claims are primarily contiguous and cover a portion of the geological feature known as the Abitibi Greenstone Belt. The property is not subject to any NSR royalties. Surface rights in this area are of Crown ownership, and may be used in conjunction with valid mineral tenure.

Geology

The Lamaque mine is located in the eastern end of the Abitibi Greenstone Belt (AGB). The AGB is an Island Arc volcanic complex, 750 km long by 250 km wide, within the Superior Province of the Canadian Shield. All of the rocks within the region are of Archean age, except for Proterozoic Diabase dykes that crosscut lithologies on both a regional and local scale. Volcanic and sedimentary rock thicknesses in the Abitibi Greenstone Belt range up to 18,000 meters thick with as much as 80% of the assemblage comprised of volcanic rocks. The eastern segment of the Southern Volcanic Zone (SVZ) of the Abitibi Greenstone Belt is a complex sequence of volcano-sedimentary rocks (2,705 + 2 Ma) cut by post-volcanic plutonic suites. This segment can be subdivided into two stratigraphic groups based on regional tectonics and volcano-sedimentary stratigraphy: the basal Malartic Group composed of the La Motte-Vassan, Dubuisson, and Jacola formations, and the overlying Louvicourt Group, containing the Val d'Or and Héva formations. The Malartic Group represents an Archean oceanic floor controlled by extensional mantle plume tectonics and characterized by effusive komatiites and basalts and intrusive dykes and sills. The Louvicourt Group marked a change to subduction-related processes with incipient arc construction that is represented by the lower Val d'Or Formation. This contemporaneous volcanic activity indicates a conformable relationship. Subsequent rifting, represented by the Héva Formation, formed voluminous lavas that flooded the arc-related lavas.

6

The area has undergone a complex structural evolution that consists of a dominant steep east-west foliation that overprints both volcanic and sedimentary rocks and an overall

Lamaque Due Diligence January 2009

east-west arrangement of most lithological units resulting from a north-south shortening across the belt. Abundant shear zones, parallel to the structural trend, are present in the district and have been grouped into three orders of shearing. First order shear zones are represented by the Larder Lake-Cadillac fault zone, a complex high strain zone reaching 1 km in thickness and at least 200 km long. This fault zone has an overall east-west strike and dips steeply north. Second order shear zones are typically 1 – 10 km long and 10-100 m wide. They have steep to sub-vertical dips and vary in strike from south-east in the western part of the district to east-west in the eastern part. Third order shear zones, which are the most abundant, are a few meters thick and reach 1 km in length. They strike between northwest and northeast and dip between 35 and 75 degrees to the north or to the south. These third order shears formed a large-scale interconnected plumbing system that at some stage in the structural evolution of the district resulted in extensive gold deposition. The Lamaque mine is located 1.5 km south of the Bourlamaque Batholith within the Central Pyroclastic Belt of the Val d’Or Formation and just north of the Larder Lake-Cadillac Break. A belt of Timiskaming sediments lies 4.5 km to the south. The volcanics have been cut by dykes, sills and several large composite stocks which range in composition from diorite to granodiorite (tonalite). A series of shears zones also intersect the rocks.

Mineralization Gold mineralization at the Lamaque Mine is hosted entirely within quartz-tourmaline-carbonate +/- sulphide veins. Some veins are confined for their entirety within intrusive rocks whereas others have considerable strike and dip length outside of the intrusives. There are also several major veins that have no direct relationship to any intrusive bodies. All veins form boudin structures and can pinch down to a simple shear structure, however, it has been found that dilation can develop at any point along these shear structures resulting in vein formation of economic length and width (Burns and Mark, 2008).

7

As was stated, vein material consists predominantly of Quartz-Tourmaline-Carbonate +/- Pyrite +/- Scheelite. Gold is typically associated with pyrite but can also occur as visible specks or patches in the quartz. Silver is also present in a ratio of 1 to 20 (Burns and Mark, 2008). Tourmaline can form up to 95% of the vein material. Sub-horizontal veins show tourmaline fibbers cut by quartz ribbons indicating repeated opening episodes. As many as 8 pulses of mineralization within a single vein have been recorded (Burns and

Lamaque Due Diligence January 2009

Mark, 2008) although gold mineralization has only been recorded associated with three of them. Accessory minerals identified at Lamaque include ankerite, pyrrhotite, chalcopyrite, fuchsite, mariposite, lepidolite, tellurides (petzite, calaverite, krennerite, and tellurbismuth), sphalerite, magnetite and galena. Pyrite, chalcopyrite, pyrrhotite, magnetite, sphalerite, and the gold tellurides formed late in sequence of mineralizing events.

Mineral Resource and Reserves

The mineral resources/reserves at Lamaque were estimated by Century using two methodologies based on the CIM Ad Hoc Committee definitions (Appendix C-5a). The majority of the proven and probable reserves (~71%) utilized within this report were derived via hand calculation by previous operators of the mine. These previous operators include Placer Dome, Lamaque and McWatters who used the industry standard polygon method to calculate reserves. Their numbers have been checked and validated by Burns and Mark (2008). The remainder of the proven and probable reserves (29%) reported were derived using Vulcan mine modeling software based on open pit parameters that were developed using various statistical methods conducted on DDH assays obtained from different parts of the mine. On April 24, 2008, Mr. Callum Mark, M.Sc., P.Geo, with Clearwater Resources Limited, completed a compliant NI 43-101 Technical Report for proven and probable reserves of 1,134,971 million ounces along with 624,201 ounces as measured and indicated. The NI 43-101 reserve and resource results are shown in Table i-2. Table i-2 Century Mining Corporation Lamaque Mine, January 2009 Due Diligence Report Summary of NI 43-101 Reserves & Resources, April 2008

8

CIM Class Tonnes Grams /Tonne

Ounces Gold

Proven 2,416,993 5.26 409,045

Probable 4,517,162 4.67 677,706 Proven + Probable 7,736,181 4.56 1,134,971

Measured 760,964 5.08 124,334

Indicated 2,926,614 5.31 499,867 Total M&I

Resources 3,687,308 5.27 624,201

Total Inferred Resources 17,839,915 4.83 2,832,389

Lamaque Due Diligence January 2009

Mining

The Lamaque mine will produce all of its ore from underground operations as it had done prior to being placed on care and maintenance in July 2008. Access to the underground will include three declines driven from the current Sigma open pit to access the Lamaque II, North Wall, and Sigma West mining regions and a vertical shaft to access deeper ore (Figure i-1). Initial ramp-up production will be sourced from the existing Lamaque II decline at the south east end of the Sigma Pit, which will provide haulage access to the Lamaque II and cross-over section (Figure i-2). Planned declines in the west and north of the pit will access the Bedard Dyke and the sub parallel structures in the north wall of the open pit. Once the mine is recommissioned, production will be steadily increased to a targeted 2,000 tonnes per day for an annualized throughput of 720,000 tonnes. It is forecast that the mine will reach full production of 2,000 tonnes per day at the end of year 3 (Figure i-3). Beginning in 2012, mid to long-term production will be supported by refurbishing the Sigma 2 shaft and recommissioning the sub level Sigma 3 shaft. The Sigma 2 shaft is situated in the east end of the Sigma pit close to the existing processing plant and other infrastructure. Recommissioning the two shafts will complete the access to all of the remaining reserves from the surface to the 40 level located over 6,000 ft (2,000m) below the surface. Beginning in 2014, ore will also be mined from the West Plug and trucked to the mill, at an average rate of 308 tonnes per day.

Figure i-1 Century Mining Corporation Lamaque Mine, January 2009 Due Diligence Report Sigma Pit Portal Locations

9

Lamaque Due Diligence January 2009

Figure i-2 Century Mining Corporation Lamaque Mine, January 2009 Due Diligence Report Photo of Lamaque II & Staging Area

The Lamaque Mine will utilize mechanized mining whenever possible. The mining methods will include longhole mining of narrow veins, dykes and plugs which are relatively vertical in nature; however shrinkage stopes might be used to some advantage in certain situations. Cut and fill mining will be used in zones of poor ground or where the geometry is best addressed by transverse cut and fill. Flat veins, which were traditionally room and pillar mining with jackleg and slushers, will initially require conventional techniques while mechanization is implemented and development access is completed. During mechanized mining operations in the flat veins, a split-firing technique will be utilized to minimize internal and external dilution and waste haulage to surface. The reserve grades in the flats include an overall 6 foot mining height so reduction of the waste dilution will result in much higher grades. The long-term mine plan calls for a flat to stope productivity ratio of 1 to 4.

Waste Disposal Employee Transportation

ROM Ore Stockpile Lamaque II Portal Access

Haul Road

Staging Area

10

Lamaque Due Diligence January 2009

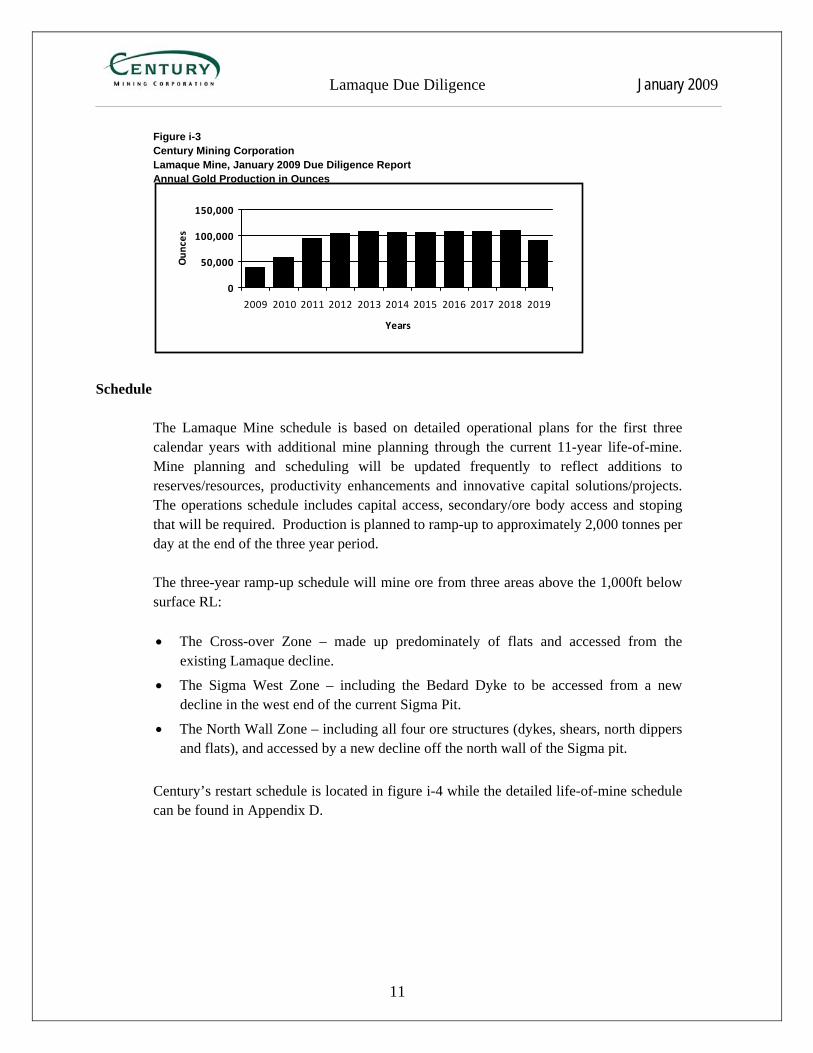

Figure i-3 Century Mining Corporation Lamaque Mine, January 2009 Due Diligence Report Annual Gold Production in Ounces

Schedule

The Lamaque Mine schedule is based on detailed operational plans for the first three calendar years with additional mine planning through the current 11-year life-of-mine. Mine planning and scheduling will be updated frequently to reflect additions to reserves/resources, productivity enhancements and innovative capital solutions/projects. The operations schedule includes capital access, secondary/ore body access and stoping that will be required. Production is planned to ramp-up to approximately 2,000 tonnes per day at the end of the three year period.

The three-year ramp-up schedule will mine ore from three areas above the 1,000ft below surface RL:

• The Cross-over Zone – made up predominately of flats and accessed from the

existing Lamaque decline.

• The Sigma West Zone – including the Bedard Dyke to be accessed from a new decline in the west end of the current Sigma Pit.

• The North Wall Zone – including all four ore structures (dykes, shears, north dippers and flats), and accessed by a new decline off the north wall of the Sigma pit.

Century’s restart schedule is located in figure i-4 while the detailed life-of-mine schedule can be found in Appendix D.

11

0

50,000

100,000

150,000

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Years

Oun

ces

Lamaque Due Diligence January 2009

Figure i-4 Century Mining Corporation Lamaque Mine, January 2009 Due Diligence Report Project Restart Schedule

Mo. ‐2 Mo. ‐1Start‐up Month Mo. 2 Mo. 3 Mo.4 Mo.5 Mo.6 Mo.7 Mo.8 Mo.9 Mo.10 Mo.11 Mo.12

Project restart go‐aheadRecruiting Mobilize Bedrad Dyke drilling Permitting processRehabilitation Place Orders

Flats Flats re‐setablishStoping

Sigma West Sigma West PortalDevelopmentOre Dev. & Stoping

North Wall ZonePortalDevelopment

ProcessingRecommission, ramp upFull production

6,7876,622

6,4614522

3,8073,210 3,209

Century Mining Corporation

Processed Gold Ounces

Lamaque Gold Project Restart Schedule

Processing

The underground mining operations will deliver higher grade and lower tonnages than experienced during the open pit operations. Processing will not begin immediately upon Project start-up but will include a four month stockpile build up period. Processing will begin at the end of four months at a rate of 1,200 tonnes per day. Near the latter half of year two operations, mill capacity will be ramped up to meet the ultimate design capacity of 2,200 tpd. As all infrastructure is currently in place, the productivity change from 1,200 tpd to 2,200 tpd is minor and includes modification of the rod mill feed chute, sheave changes to increase the speed of rod mill feed conveyors, and first fills of mill supplies and spare parts. The existing Sigma/Lamaque process plant was originally designed to process 5,000 tpd and utilized by Century during both open pit and underground operations. For the purposes of this section, the mill designed throughput is assumed at 1,200 tpd ramping up to 2,200 tpd and the ability to ramp up to over 3,400 tpd as mining efficiencies improve and additional virgin ore becomes available.

12

Lamaque Due Diligence January 2009

The Sigma mill has been in operation since 1937 and increased steadily from 750 tpd in 1939 to 2,200 tpd in 1995 and later modernized with updated electrical, instrumentation control, a carbon-in-pulp (CIP) gold recovery circuit, and a 2nd ball mill for a conventional circuit capacity of 3,400 tpd. Century Mining Corporation purchased the operation in September 2004. In November 2007 the Company ceased mining operations from the open pit and focused entirely on increasing production from the Lamaque underground mine at which operating capacity was converted back to the conventional circuit (rod mill / ball mill) suitable for a 2,000 tpd underground operation. The mill will be fed by a closed circuit crushing facility sized for a maximum capacity of 3,800 tpd at 67% availability exceeding the ultimate capacity of the mill with two ball mills operating. Final product reporting to stockpile is a nominal 13 mm. The existing stockpile will have a permanent enclosure at the discharge of the stacker conveyor. Milling is performed with cyanide present and includes gravity recovery of 25 to 40% of the gold. Final mill product is sized and thickened prior to leaching 24 hours in the agitated aerated leach. The slurry flows by gravity to the CIP circuit and gold is recovered from activated carbon. Washed carbon is transferred to stripping in 3 tonne lots, gold is eluted at high temperature and pressure and recovered from the pregnant strip solution using electro-winning cells fitted with stainless steel mesh cathodes. Gold is refined from cathodes smelted in an induction furnace producing gold doré containing 78% gold, 14% silver and 8% impurities. With the exception of the crushing circuit, the Lamaque Mill is complete with all infrastructure including tailings disposal. Currently, 2 years of tailings storage is available and expandable to 5 – 7 years by raising the east half of the tailings structure. Future capacity is available by expanding the current facility to the North.

Environment & Permit

There are a number of statutory reporting requirements to government authorities, both provincial and federal. These authorities include the Ministry of Natural Resources, Ministry of Environment, Environment Québec and Environment Canada.

Reports are prepared using in-house and specialist technical consultants. The Mine has an Environmental Superintendent who oversees a team of technicians that undertakes all environmental monitoring, management and ongoing work, including the environmental presentations for permitting.

13

Lamaque Due Diligence January 2009

The Mine’s Environmental Superintendent has been retained as a key member of the care and maintenance team. His current role is to assist the Company with its current due diligence, undertake ongoing monitoring and assist with current permit applications. In August, 2008, EBA engineering was contracted by Puma Resources Ltd, and paid by Century as part of a due diligence process for financing. During this time, EBA conducted a site visit, inspection and discussions with mine personnel and determined that none of the environmental and permitting issues are considered to pose a significant risk to the environment or the current or planned near-future operations of the mine. See Appendix B for the EBA report titled “EBA Environmental Review Lamaque Aug.29.2008”. Waste rock from production is non-acid generating and has often been used by external crushing contractors for aggregate supply. Waste rock dumps from past open pit operations are relatively stable with monitoring programs in place. Management of the waste water from the process plant is a major priority of the environmental management program on site, with focus on tailings ponds and quality of water before release downstream. Issues of dust and water management in the tailings ponds have resulted in notices of infraction from the government. These issues will be dealt with in the upcoming dewatering permit and will be a key performance indicator for the environmental superintendent. The aesthetics of the current open pit and rock dumps have been a concern but management plans to address these concerns once operations resume. Prior dust generated from the crusher/conveyor/stockpile areas in the past will be addressed through capital projects upon mine start-up which will enclose and mist these areas. Road dust will be controlled by water spray. There is little risk associated with hazardous or non-hazardous waste management programs at the mine site. Hazardous waste is well stored in secure locations and records are maintained of storage and shipping. There are no landfills or incinerators on site and all waste is stored prior to recycling or removal. Fuel and lubes are well managed with environmentally modern, above ground double walled tanks. Chemical and waste management in the maintenance shop is well maintained with no outstanding issues present. There does not appear to be any known or potential soil contamination issues and planned future independent studies will confirm soil conditions.

14

There are over seven years of storage capacity remaining in the existing tailings facilities based on current mining schedules. For future operations, there is an area available and within the concession area that Century can utilize to construct additional tailings cells. A

Lamaque Due Diligence January 2009

series of studies are planned for the area immediately to the north of the existing tailings facility to provide tailings and supernatant water storage in the future. All permits required for start-up of the Lamaque mine and mill operation are in place. Follow-up environmental compliance items were identified early in 2008 and include the following: • Relocation of the self contained air compressors to an area inside the gate; • Seeding of the B2 tailings lift; • Initiation of reclamation of the west end of the main waste dump; • Removal of waste oil from the property; and • Soil characterization around the mobile maintenance building. Century Mining has stayed in contact with the Ministry of Environment (MOE) throughout 2008 and has given notice of completion of the seeding of B2 tailings lift and air compressor relocation. Century has located vendors and equipment to complete all remaining compliance items upon spring melt of 2009. The Lamaque Mine is currently permitted for 1,200 tonnes per day production which also includes the Northeast portion of the North Wall zone. Based on current production schedules, the Company has identified the following permit priorities:

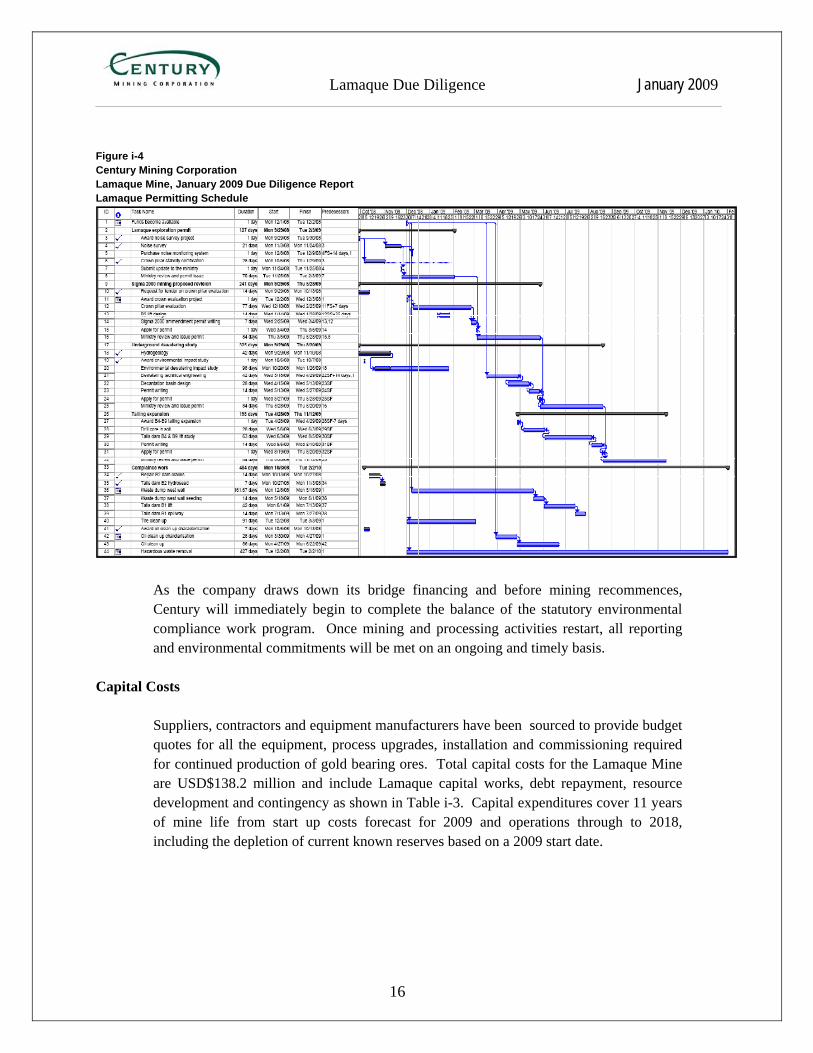

• Lamaque 2000 Permit (Allows the bulk sample mining of Bedard Dyke) • Sigma 2000 Permit (Allows mining of the North Wall & Bedard Dyke) • Dewatering Permit (Allows pumping up to 3,000 gallons per day from underground) Century developed a working Gantt chart which coincides with its production schedule and is currently meeting the scheduled requirements as indicated in Figure i-4.

15

Lamaque Due Diligence January 2009

Figure i-4 Century Mining Corporation Lamaque Mine, January 2009 Due Diligence Report Lamaque Permitting Schedule

As the company draws down its bridge financing and before mining recommences, Century will immediately begin to complete the balance of the statutory environmental compliance work program. Once mining and processing activities restart, all reporting and environmental commitments will be met on an ongoing and timely basis.

Capital Costs

Suppliers, contractors and equipment manufacturers have been sourced to provide budget quotes for all the equipment, process upgrades, installation and commissioning required for continued production of gold bearing ores. Total capital costs for the Lamaque Mine are USD$138.2 million and include Lamaque capital works, debt repayment, resource development and contingency as shown in Table i-3. Capital expenditures cover 11 years of mine life from start up costs forecast for 2009 and operations through to 2018, including the depletion of current known reserves based on a 2009 start date.

16

Lamaque Due Diligence January 2009

Table i-3 Century Mining Corporation Lamaque Mine, January 2009 Due Diligence Report Lamaque Capital Expenditures

Lamaque projectSigma Shaft Refurbishment $0 $548 $14,979 $8,820 $3,584 $1,795 $0 $0 $0 $0 $29,726Underground Development $11,584 $7,824 $4,024 $4,024 $4,024 $2,315 $1,460 $605 $605 $605 $37,070Underground Utilities $299 $774 $321 $321 $0 $0 $0 $0 $0 $0 $1,714Underground Equipment $5,118 $2,096 $1,959 $1,276 $1,276 $404 $2,541 $0 $0 $0 $14,670Mill and Processing $1,291 $1,111 $0 $0 $0 $214 $427 $214 $214 $214 $3,684Surface Equipment $786 $256 $855 $77 $68 $385 $77 $256 $0 $77 $2,838Surface Infrastructure $1,030 $1,026 $684 $171 $85 $85 $85 $85 $85 $85 $3,423Other $0 $150 $107 $0 $0 $0 $0 $0 $0 $0 $256Sustaining Capital $128 $684 $684 $427 $427 $214 $427 $641 $641 $427 $4,701

Sub Total $20,236 $14,468 $23,612 $15,115 $9,464 $5,411 $5,018 $1,802 $1,545 $1,409 $98,081Contingency $3,035 $2,170 $3,542 $2,267 $1,420 $812 $753 $270 $232 $211 $14,712

Total Project Costs $23,272 $16,638 $27,154 $17,382 $10,884 $6,223 $5,770 $2,072 $1,777 $1,620 $112,793

Interest on Escrow @4% -$200 -$208 -$216 -$225 -$234 -$243Escrow Overrun Account $5,000 -$5,000Bridge Repayment $2,500Warehouse Inventory $2,000 $2,000Investissement Quebec Debt Repayment $9,000 $9,000Outstanding Quebec payables $10,000 $10,000G & A $3,000 $3,000Environmental Bond $1,200 $1,200Lamaque Resource Upgrade $1,000 $1,000 $500 $500 $500 $3,500Total Other Costs (In CAD) $33,700 $800 $292 $284 $275 -$234 -$5,243 $0 $0 $0 $29,873Total Other Costs (in USD) $28,803 $684 $250 $242 $235 -$200 -$4,481 $0 $0 $0 $25,533

Total Capital Expenditure (In USD) $52,075 $17,322 $27,404 $17,625 $11,119 $6,023 $1,289 $2,072 $1,777 $1,620 $138,326

Other (All 2009 Payments Fixed in Canadian Dollars)

All amounts in US$ (000) 2009 2010 2011 2012 Total2013 2014 2015 2016 2017 2018

Operating Costs

The operating costs for the Lamaque Mine Project have been calculated from first principles based on actual quotations, where possible, and from actual mining activities prior to the Project going on care and maintenance. The model has a budgeted life of mine total operating cash cost of USD$432.7 million equating to a unit cash cost of USD$421/oz of gold. Operating costs include mining and processing, as well as administrative and service costs. Life of mine average operating costs per tonne are located in Table i-4. These costs are in US dollars and reflect the use of two exchange rates of CAD$1.17:USD$1.00 (hedged) and CAD$1.10:USD$1.00 (spot). Over the life of the currency hedge, 69% of the total operating costs are hedged at CAD$1.17:USD$1.00

17

Lamaque Due Diligence January 2009

Table i-4 Century Mining Corporation Lamaque Mine, January 2009 Due Diligence Report Average Operating Cost per Tonne Summary

Activity Cost per tonne

($USD)

Labour $30.62

Mining (Excluding Fuel and Labour) $8.31

Fuel $2.20 Milling --Processing (Excluding Fuel and Labour) $7.12

Services (Excluding Fuel and Labour) $4.58

G & A (Excluding Fuel and Labour) $5.84

Reclamation $0.50

Refining & Transportation $0.12

Resource Upgrading $1.54

Total $60.83

Financial Analysis

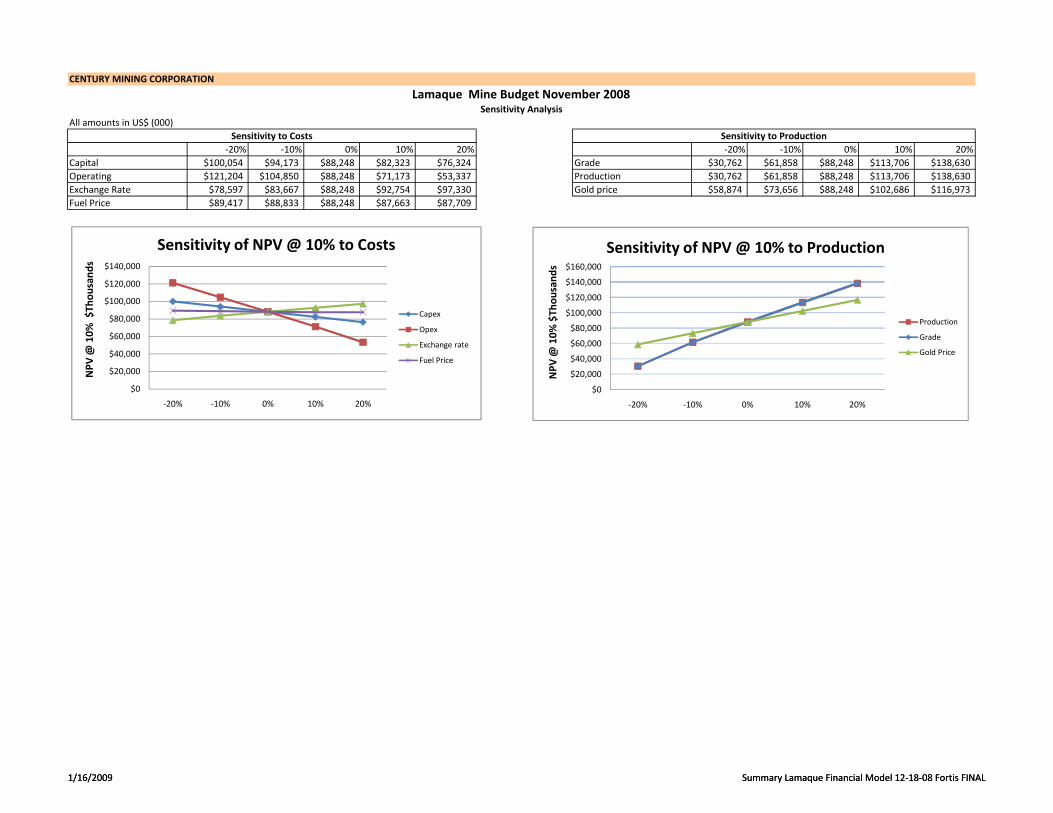

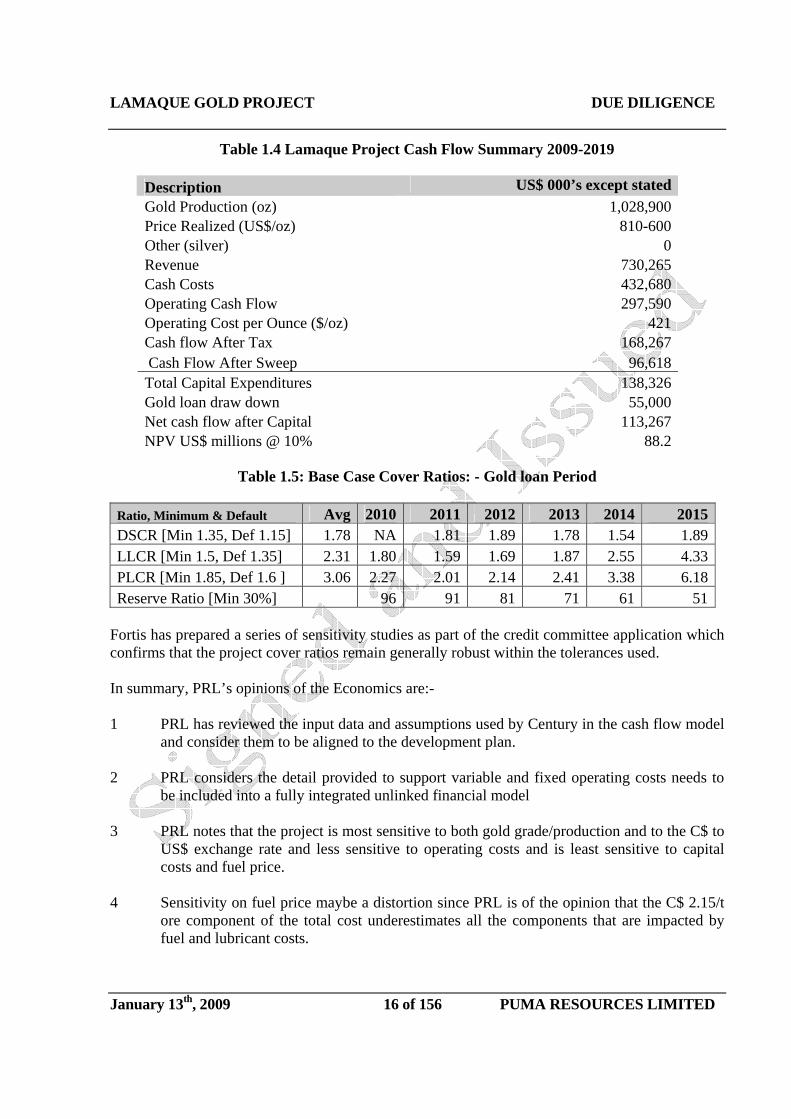

The financial model resulted in positive project economics. The net cash flow for the operations is USD$168.3 million, and the NPV at 10% is USD$88.2 million. There is sufficient production and revenues to meet or exceed all required banking cover ratios once full production is achieved. Sensitivity analysis were performed on the financial model with respect to operating costs, capital costs, CAD/USD exchange rate and fuel costs, as well as another on price, recovery, and production. These can be found in Figures i-5 and i-6, respectively. It can be seen that the project is most sensitive to changes in the operating costs and grade/production. The project is less sensitive to the gold price and exchange rate due to forward sales and hedging strategies.

18

Lamaque Due Diligence January 2009

Table i-5 Century Mining Corporation Lamaque Mine, January 2009 Due Diligence Report Sensitivity Analysis: NPV at 10% to Costs

$0

$20,000

$40,000

$60,000

$80,000

$100,000

$120,000

$140,000

‐20% ‐10% 0% 10% 20%

NPV

@ 10%

$Th

ousand

s

Sensitivity of NPV @ 10% to Costs

Capex

Opex

Exchange rate

Fuel Price

Table i-6 Century Mining Corporation Lamaque Mine, January 2009 Due Diligence Report Sensitivity Analysis: NPV at 10% to Production

19

$0

$20,000

$40,000

$60,000

$80,000

$100,000

$120,000

$140,000

$160,000

‐20% ‐10% 0% 10% 20%

NPV

@ 10%

$Th

ousand

s

Sensitivity of NPV @ 10% to Production

Production

Grade

Gold Price

Lamaque Due Diligence January 2009

20

Conclusions

Considering the economic viability of the Lamaque Mine Project as demonstrated by the cash flow analysis, the project is feasible and will provide satisfactory returns with acceptable risk.

CENTURY MINING CORPORATION

Model assumptionsModel based on USD unless otherwise notedExchange Rate Hedged $1.17 CAD/$1.00 USDg gSpot Exchange Rate $1.10 CAD/$1.00 USDGold prices Varies by year as follows

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019Spot 780 825 800 650 650 600 600 600 600 600 600Hedged 788 801 821 845 871 900 931 965 994 1,020 1,020 Amount of Gold Hedged 45,000 ounces/yearGold loan ounces sold at $780/oz USDInterest rate on gold loan 6.00%Unused cash from initial loan to be held in account earning 3% interestCash flow model run unescalated but model is capable of indicating effects of inflationCash flow model run unescalated, but model is capable of indicating effects of inflationNo value to be recognized from silver credit, though past indicates some revenue to be generated by silverCash sweep to provide early repaymentVariables can be changed in Sensitivity section of Summary Cash Flow

Production assumptionsOnly proven and probable class reserves included in mine planMining Recovery 95%External Waste Dilution 10%Dilution to occur from barren (0 g/t) material( g/ )1% of each years production to be held over until following year as stockpile material.Stockpile material could be included in annual production if needed (due to excess milling capacity)Metallurgical recovery assumed at 95% based on actual operating resultsRamp up period of 257,921 tonnes in 2009 and 347,683 tonnes in 2010Full production achieved in Year 3Production from Lamaque II to begin in March 2009, production from Sigma West to begin in May 2009, and North Wall to begin in February 2010Mill capable of running at tonnages above 1,300 tonnes per day and below 2,500 tonnes per dayCentury was conservative by holding Mechanical flat mining OPEX the same as Conventional flat mining OPEX

CostsCostsActual operating cost data valid for forecasting purposesLabor assumed to be a fixed cost in cash flowLabor will be hired according to schedule$5 million overrun to be held in escrow, and will earn 4% interest annuallyCapital depreciated over five years on units of production basis$80 million in tax losses from previous operation will be carried forward and used as needed to minimize taxA 15% contingency has been applied to capital estimatesMining duty of 12% applied to profits

1/16/2009 Summary Lamaque Financial Model 12‐18‐08 Fortis FINAL1/16/2009 Summary Lamaque Financial Model 12‐18‐08 Fortis FINAL

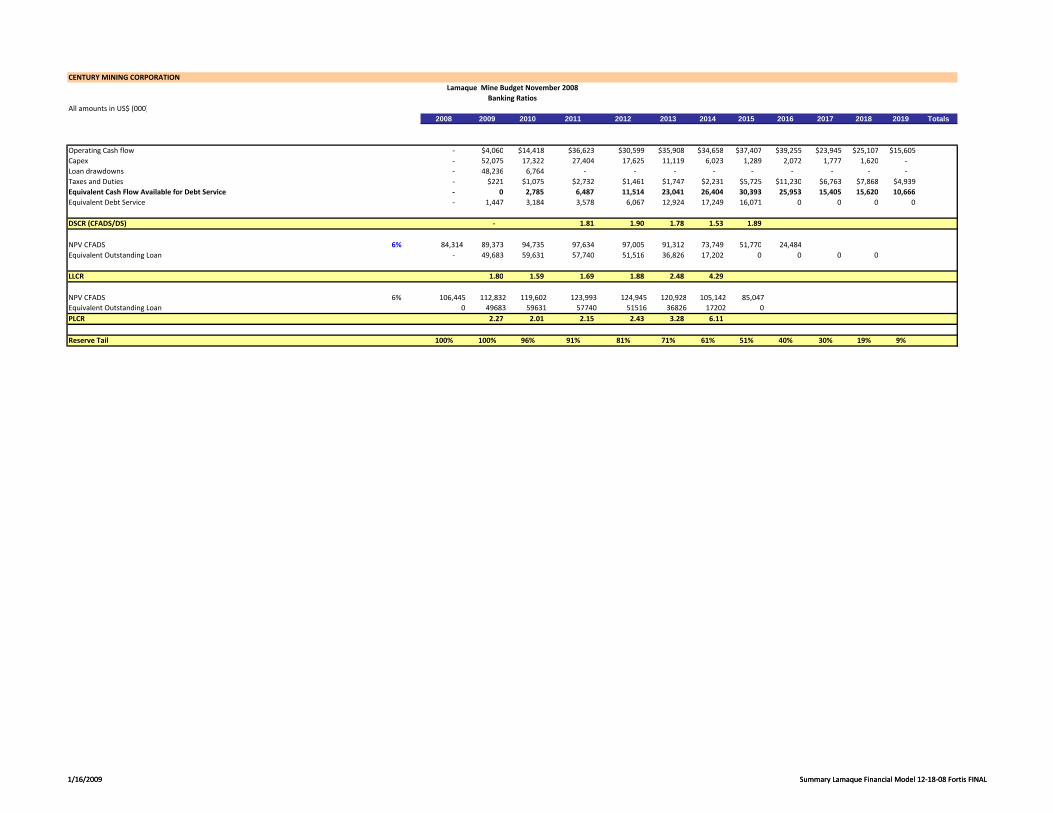

CENTURY MINING CORPORATIONLamaque Mine Budget November 2008

Summary Cash FlowAll amounts in US$ (000)

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 TotalsRevenues Gold Production (oz) - 38,363 58,439 94,900 102,993 107,115 105,005 106,345 106,897 108,588 109,880 90,342 1,028,868 Price Realized ($/oz) - 780 807 810 735 743 729 740 754 600 600 600 Revenue ($) - 29,923 47,132 76,865 75,720 79,570 76,503 78,702 80,563 65,153 65,928 54,205 730,265

Cash Costs ($) ‐ 25,863 32,715 40,243 45,121 43,662 41,845 41,295 41,308 41,208 40,820 38,600 432,680 Cash Costs Covered ($) 19,141 9,602 20,515 28,207 34,359 40,418 41,308 Cash Costs Uncovered ($) 13,573 30,640 24,606 15,455 7,485 877 ‐ Cash Cost ($/oz) 674 560 424 438 408 399 388 386 379 372 427 421

Operating Cash flow ($) - 4,060 14,418 36,623 30,599 35,908 34,658 37,407 39,255 23,945 25,107 15,605 297,585

Depreciation 2,222 5,460 13,858 18,428 21,349 16,064 13,667 8,531 5,443 3,582 2,092 Mining Duties - 221 1,075 2,732 1,461 1,747 2,231 2,849 3,687 2,220 2,583 1,622 22,427Federal and Provincial Taxes - - - - - - - 2,876 7,543 4,543 5,285 3,318 23,565Back in Depreciation 2,222 5,460 13,858 18,428 21,349 16,064 13,667 8,531 5,443 3,582 2,092 After Tax Cash Flow - 3,840 13,343 33,891 29,138 34,161 32,427 31,681 28,025 17,182 17,240 10,666 251,593

Project Capex - 23,272 16,638 27,154 17,382 10,884 6,223 5,770 2,072 1,777 1,620 - Other Costs - 28,803 684 250 242 235 (200) (4,481) - - - -

Cash Flow after CAPEX - (48,236) (3,979) 6,487 11,514 23,041 26,404 30,393 25,953 15,405 15,620 10,666 113,267

Loan Draw Down 48,236 6,764

CAFDS - - 2,785 6,487 11,514 23,041 26,404 30,393 25,953 15,405 15,620 10,666 168,267 Interest Payment 1,447 3,184 3,578 3,384 2,787 1,744 567 0 0 0 0 16,691 Scheduled Repayment 2,683 10,137 15,504 15,504 - - - - 43,829 capitalisation of interest (1,447) (3,184) - - - - - Free Cash Flow - 2,785 2,909 5,446 10,117 9,155 14,321 25,953 15,405 15,620 10,666 Cash Sweep % 65% 65% 45% 45% 45% 0% 0% 0% 0%Cash Sweep (USD) 1,891 3,540 4,553 4,120 1,698 - - - - 15,802

Free Cash Flow after sweep - 2,785 1,018 1,906 5,564 5,035 12,623 25,953 15,405 15,620 10,666 Cumulative Free Cash Flow after sweep - - 2,785 3,803 5,710 11,274 16,310 28,933 54,886 70,291 85,910 96,576

Loan Amount 55,000Loan Interest 6%Scheduled Repayments 2,683 10,137 15,504 15,504 15,802 Loan outstanding 49,683 59,631 57,740 51,516 36,826 17,202 0 0 0 0 0 capitalisation of interests? 1 1 0 0 0 0 0 0 0 0 0

Repayment Schedule 4.50% 17.00% 26.00% 26.00% 26.50%

Gold Assumption Base Case 780 825 800 650 650 600 600 600 600 600 600 600 Gold Fwd Base Case 788 801 821 845 871 900 931 965 994 1,020 1,020 Gold Assumptions ($/oz) 780 825 800 650 650 600 600 600 600 600 600 600 Gold Forward Curve (Fortis update 01-12-08) ($/oz) 865 788 801 821 845 871 900 931 965 994 1,020 1,020

2009 2010 2011 2012 2013 2014 2015 2016Sensitivity Ratios

Gold Price Avg DSCR DSCRSpot Gold Price Variation 0% 1.78 ‐ ‐ 1.81 1.90 1.78 1.53 1.89 ‐ Hedged Gold Price Variation 0% Avg LLCR LLCRExchange Rate Hedged Rev (USD/CAD) 1.17 2.29 1.80 1.59 1.69 1.88 2.48 4.29 ‐ ‐ Volume Hedged oz 45,000 Avg PLCR PLCRExchange Rate (USD/CAD) 1.10 3.04 2.27 2.01 2.15 2.43 3.28 6.11 ‐ ‐

Production Reserve TailGrade U/G 0% 100% 96% 91% 81% 71% 61% 51% 40%Fuel Price 0%Ounces 0% Min DSCR allowed for distribution 1.35 Default DSCR 1.15Recovery 0% Min LLCR allowed for distribution 1.50 Default LLCR 1.35

Min PLCR allowed for distribution 1.85 Default PLCR 1.60Costs Min Reserve Tail 30%

Opex 0%Capex 0%Inflation 0%

Project Outcomes

NPV @ 10% ($) 88,248

Free Cash ($) 168,267 Production oz 1,028,868 Cash Cost US$/oz 421

CENTURY MINING CORPORATIONLamaque Mine Budget November 2008

RevenueAll amounts in US$ (000)

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 TotalSensitivity

Ounces Produced (oz) 100% 38,363 58,439 94,90 0 102, 993 10 7,115 105,005 106,345 106,897 108,588 109,880 90,342 1,028,868 Gold Loan Repayment (oz) 0 0 0 0 0 0 0 0 0 0 0 0 Gold Sold (oz) 38,363 58,439 94,90 0 102, 993 10 7,115 105,005 106,345 106,897 108,588 109,880 90,342 1,028,868 Hedged (oz) 45,000 45,00 0 45, 000 4 5,000 45,000 45,000 45,000 315,000 Hedge Price $/oz 788 801 82 1 845 871 900 931 965 994 1,020 1,020 Revenue on Hedged Production $ - $ 36,045 36,94$ 5 38,$ 025 3$ 9,195 $ 40,500 $ 41,895 $ 43,425 -$ -$ -$ Spot (oz) 38,363 13,439 49,90 0 57, 993 6 2,115 60,005 61,345 61,897 108,588 109,880 90,342 713,868 Spot Price $/oz 780 825 80 0 650 650 600 600 600 600 600 600 Revenue on Production Sold Spot $ 29,923 $ 11,087 39,92$ 0 37,$ 695 4$ 0,375 $ 36,003 $ 36,807 $ 37,138 65,153$ 65,928$ 54,205$ Sub Total $ 29,923 $ 47,132 76,86$ 5 75,$ 720 7$ 9,570 $ 76,503 $ 78,702 $ 80,563 65,153$ 65,928$ 54,205$ 730,265$

Average Realized Price $/oz 780 807 81 0 735 743 729 740 754 600 600 600 710

Total $ ‐ $ 29,923 $ 47,132 76,86$ 5 75,7$ 20 7$ 9,570 $ 76,503 $ 78,702 $ 80,563 65,153$ 65,928$ 54,205$ 730,265$

42,173 43,226 44,489 45,858 47,385 49,017 50,807 012,972 46,707 44,103 47,239 42,123 43,064 43,452 76,229

1/16/2009 Summary Lamaque Financial Model 12‐18‐08 Fortis FINAL1/16/2009 Summary Lamaque Financial Model 12‐18‐08 Fortis FINAL

CENTURY MINING CORPORATION

All amounts in US$ (000)2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 Totals

Operating Cash flow ‐ $4,060 $14,418 $36,623 $30,599 $35,908 $34,658 $37,407 $39,255 $23,945 $25,107 $15,605Capex ‐ 52,075 17,322 27,404 17,625 11,119 6,023 1,289 2,072 1,777 1,620 ‐ Loan drawdowns ‐ 48,236 6,764 ‐ ‐ ‐ ‐ ‐ ‐ ‐ ‐ ‐ Taxes and Duties ‐ $221 $1,075 $2,732 $1,461 $1,747 $2,231 $5,725 $11,230 $6,763 $7,868 $4,939Equivalent Cash Flow Available for Debt Service ‐ 0 2,785 6,487 11,514 23,041 26,404 30,393 25,953 15,405 15,620 10,666Equivalent Debt Service ‐ 1,447 3,184 3,578 6,067 12,924 17,249 16,071 0 0 0 0

DSCR (CFADS/DS) ‐ 1.81 1.90 1.78 1.53 1.89

NPV CFADS 6% 84,314 89,373 94,735 97,634 97,005 91,312 73,749 51,770 24,484 Equivalent Outstanding Loan ‐ 49,683 59,631 57,740 51,516 36,826 17,202 0 0 0 0

LLCR 1.80 1.59 1.69 1.88 2.48 4.29

NPV CFADS 6% 106,445 112,832 119,602 123,993 124,945 120,928 105,142 85,047Equivalent Outstanding Loan 0 49683 59631 57740 51516 36826 17202 0PLCR 2.27 2.01 2.15 2.43 3.28 6.11

Reserve Tail 100% 100% 96% 91% 81% 71% 61% 51% 40% 30% 19% 9%

Lamaque Mine Budget November 2008Banking Ratios

1/16/2009 Summary Lamaque Financial Model 12‐18‐08 Fortis FINAL1/16/2009 Summary Lamaque Financial Model 12‐18‐08 Fortis FINAL

Debt

CENTURY MINING CORPORATIONLamaque Mine Budget November 2008

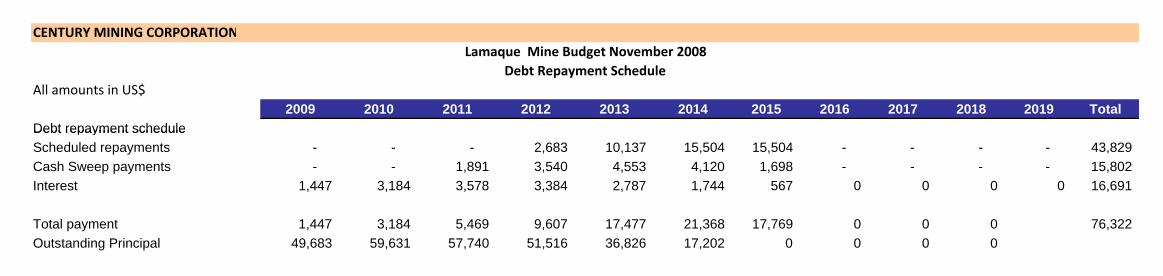

Debt Repayment ScheduleAll amounts in US$

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 TotalDebt repayment schedule repayment scheduleScheduled repayments - - - 2,683 10,137 15,504 15,504 - - - - 43,829 Cash Sweep payments - - 1,891 3,540 4,553 4,120 1,698 - - - - 15,802 Interest 1,447 3,184 3,578 3,384 2,787 1,744 567 0 0 0 0 16,691

Total payment 1,447 3,184 5,469 9,607 17,477 21,368 17,769 0 0 0 76,322 Outstanding Principal 49,683 59,631 57,740 51,516 36,826 17,202 0 0 0 0

CENTURY MINING CORPORATION

All amounts in US$ (000)

‐20% ‐10% 0% 10% 20% ‐20% ‐10% 0% 10% 20%$100,054 $94,173 $88,248 $82,323 $76,324 $30,762 $61,858 $88,248 $113,706 $138,630$121,204 $104,850 $88,248 $71,173 $53,337 $30,762 $61,858 $88,248 $113,706 $138,630$78,597 $83,667 $88,248 $92,754 $97,330 $58,874 $73,656 $88,248 $102,686 $116,973$89,417 $88,833 $88,248 $87,663 $87,709

Lamaque Mine Budget November 2008Sensitivity Analysis

Sensitivity to Costs Sensitivity to Production

Gold price

Capital

Exchange RateFuel Price

Operating ProductionGrade

$20,000

$40,000

$60,000

$80,000

$100,000

$120,000

$140,000

NPV

@ 10%

$Th

ousand

s

Sensitivity of NPV @ 10% to Costs

Capex

Opex

Exchange rate

Fuel Price

$20,000

$40,000

$60,000

$80,000

$100,000

$120,000

$140,000

$160,000

NPV

@ 10%

$Th

ousand

s

Sensitivity of NPV @ 10% to Production

Production

Grade

Gold Price

1/16/2009 Summary Lamaque Financial Model 12‐18‐08 Fortis FINAL

$0

‐20% ‐10% 0% 10% 20%

$0

‐20% ‐10% 0% 10% 20%

1/16/2009 Summary Lamaque Financial Model 12‐18‐08 Fortis FINAL

LAMAQUE GOLD PROJECT DUE DILIGENCE

January 13th 2009 1 of 156 PUMA RESOURCES LIMITED

Final Independent Technical Due Diligence Report

on Century Mining Corporation’s

Lamaque Gold Project Quebec, Canada

Prepared for Fortis Bank, as Mandated Lead Arranger

by Puma Resources Limited

and Independent Associates

comprising of Dr Ed van Hees and EBA Engineering Consultants Ltd

Effective Date:- January 13th, 2009

LAMAQUE GOLD PROJECT DUE DILIGENCE

January 13th, 2009 2 of 156 PUMA RESOURCES LIMITED

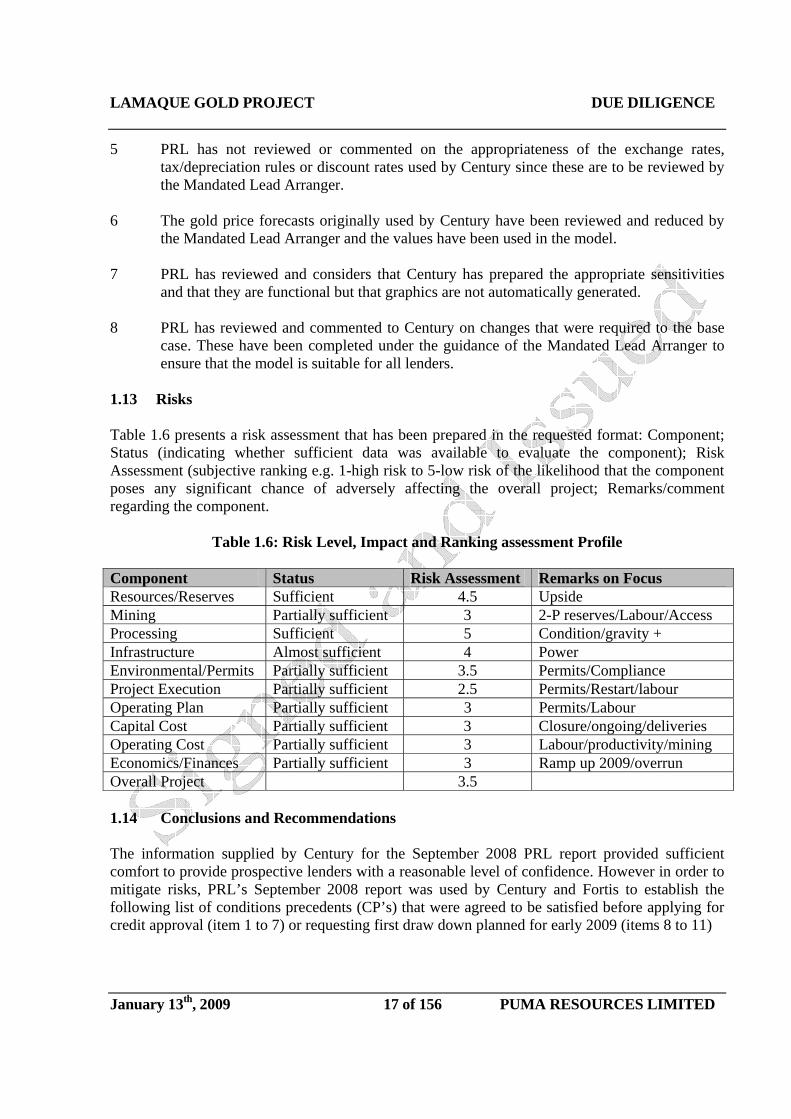

1.0 EXECUTIVE SUMMARY 1.1 Introduction This independent technical due diligence report has been prepared by Puma Resources Limited (PRL) based upon work completed by three independent entities, namely Dr van Hees, EBA Engineering Consultants Ltd (EBA) and PRL. Dr van Hees provided the Resources & Reserves section and contributed to the dilution section in mining. Personnel from EBA addressed the Environmental & Permitting subjects. PRL prepared all other sections and consolidated and edited the report. Collectively the entities are referred to in this report as “PRL and Independent Associates”. Between July and August 2008 personnel from each of the entities completed separate due diligence visits to both the corporate office of Century Mining (Century) in Blaine, Washington, USA and to the Lamaque project site, near Val D’Or, Quebec, Canada. Following delivery of data from Century, a full draft report was issued by PRL on September 30th, 2008. Subsequent review and discussions between Century and Fortis Bank (Fortis) resulted in an agreed work plan to be completed on eleven specific items. This final report is based on a systematic review of the work prepared and delivered by Century between November 2008 and January 2009. 1.2 Disclaimer PRL and Independent Associates have each used their best efforts to endeavor to ensure that there are no factual errors in their respective sections of this report. The only representations or warranties in relation to the preparation of this report and the information in it (such as its accuracy, reliability or completeness) or referred to, are those which are implied by law and which cannot be excluded by law. All projections and opinions in this report have been prepared on the basis of information made available to PRL and Independent Associates prior to the effective date on the cover page. Said information is subject to uncertainties and contingencies, which are difficult to predict and many of which are beyond the control of PRL and Independent Associates. As a result the recipient of the report is advised that PRL and Independent Associates are neither responsible nor liable for any outcomes that result from any recipient’s decision to rely on all or any part of this report. 1.3 Resources/Reserves The Lamaque Project combines the Sigma Mine previously operated by Placer Dome and the Lamaque Underground Mine previously operated by Teck. The properties are contiguous and consist of five mining concessions and 11 mining claims covering approximately 933 hectares. To date the Lamaque Project has produced a total of 9.4 million ounces of gold, at an average head grade of 5.8 g Au/t. Of the total only 0.2 million ounces of gold were produced from the open pit. Mineralisation at the Lamaque Project is hosted in dykes, shears and flat veins. The flat veins typically exhibit very good continuity and extension along both strike and dip. Drill intercepts indicate that variable thicknesses and assay values occur within the mineral resource blocks.

LAMAQUE GOLD PROJECT DUE DILIGENCE

January 13th, 2009 3 of 156 PUMA RESOURCES LIMITED

The geology of the mineralized zones is well understood and identifiable in most locations. The number of drill core and moil samples are a sufficient basis upon which the mineral resources have been prepared.

The summary of the Lamaque mineral resources for all areas are presented in Table 1.1. These resources are in addition to the ore reserve inventory provided in Table 1.2. For resource and reserves computations a cut off grade of 2.1 g Au/t was used for Lamaque #2 /Cross Over areas and 2.5 g Au/t used for all other areas. The minimum sample was 0.3 m and a mining thickness of 1.8 m. The validity of the cut off grade is discussed in section 1.4.

Table 1.1 Lamaque Mineral Resources (effective August 14, 2008)

Class Tonnes Grade g Au/t Contained g Au Contained oz Au

Measured

760,694 5.08 3,867,143 124,333

Indicated

2,926,614 5.31 15,547,370 499,867

M & I Total 3,687,308 5.27 19,414,513 624,200

Inferred

17,350,243 5.06 87,854,802 2,824,641

Table 1.2 : Lamaque Insitu Ore Reserves (effective January 11, 2009)

Class/Type Tonnes Grade g/t Contained Au gms Constained Au ozsProven

2,336,285 5.62 13,134,710 422,163 Probable

4,480,219 4.88 21,871,079 703,171 Underground 2P

6,816,504 5.14 35,005,789 1,125,334 Other (west plug)

635,733 4.68 2,975,203 95,593 Total 2 P

7,452,237 5.10 37,975,103 1,220,927 The total non NI-43-101 compliant total geological inventory of both resources and reserves is 28.49 Mt containing 145.2 t Au (4.67 M oz). The resource ounces that are reported in Table 1.1 were prepared on August 14th, 2008 and are different from those published in the April 24th, 2008 NI 43-101 report. The revised figures resulted from the initial and subsequent reviews by Dr van Hees. The adjustments included correcting a series of computational errors involving arithmetic conversions and other changes but fortunately for Century, these largely cancelled each other out in terms of contained ounces.

LAMAQUE GOLD PROJECT DUE DILIGENCE

January 13th, 2009 4 of 156 PUMA RESOURCES LIMITED

The Proven and Probable (2P) category reserve that was published in the NI-43-101 report was 7.74 Mt at 4.56 g Au/t and contained 1.13 M oz of gold. By referring to 2P reserves presented in Table 1.2 it can be seen that the contained gold in the 2P reserve effective January 11th 2009 is at 1.22 M oz is 8% higher than the NI-43-101 statement for the Lamaque project. The adjustments to the overall Lamaque project numbers have resulted due in an increase in grade but a minor reduction in tonnage. As a result of the detailed systematic review the revised resource and reserve statements presented above are acceptable and have been endorsed by Dr van Hees. In addition, Dr van Hees considers the result to be a conservative estimate of the potential mineralization present in the Lamaque project. Some 71% of the NI 43-101 resources and reserves were generated by the industry standard polygonal method and are reported without dilution. The remaining 29% of the NI 43-101 numbers were based on a model generate using Vulcan. Allowances for dilution were included in the mining schedules and are discussed in section 1.4.

For due diligence purposes, Dr van Hees requested Century to complete a check computation of the mineral resource contained within a cubic block measuring approximately 250 ft (76 m) per side and which contained representative forms of all four main types of mineralization encountered in the Project. The reserves within the large test cube were estimated using the Vulcan programme and smaller cubes 15ft (4.6 m) on a side used for open pit planning, as well as 6’ x 6’ x 3’ (1.8 m by 1.8m by 0.9m) blocks. These results were compared to reserves hand-calculated using the traditional polygon method that more closely simulate underground parameters. Overall Vulcan slightly under estimated the tonnage compared to the polygonal method. The Vulcan program also underestimates the grade and therefore the amount of gold by an average of 50% compared to the polygonal method. These results suggest that the ~0.35 million ounces of gold that were computer generated for inclusion in the April 2008 NI 43-101 resource statement might have been seriously underestimated. Dr van Hees also noted that no correction for the dip of the steep-dipping mineralized zones had been applied. The correction would increase the total ounces by ~ 1.0 ± 0.5%. This advantage is likely to be offset when eliminating 86 out of 565 mineralized blocks (15 %) that are in the Lamaque Main and #2 areas, which contain less than 100 tons of resource since these are unlikely to be recovered. This material accounts for only 0.62% of the proven and probable tons that were identified.

Throughout the due diligence period, Century has continued to incorporate moil data and update the resources and, as a consequence, Century expects to add to the 2P category of reserves so as to provide additional sources of mine production. The mot recent changes that have been included in Table 1.2 have resulted from work on the Lamaque 2 and cross over area and in the West Plug. In Dr van Hees opinion there are indications that litho geochemical analysis might assist Century to use portable XRF units to aid grade control by identifying rock units that are amenable to the deposition of gold in the wall rocks near the vein. Detailed structural modelling has the potential to further define the location and behaviour of the mineralised portions of the shear or dyke hosted veins. Dr van Hees considers that Century has a good opportunity in the future to drill to establish the bulk potential of the deep Lamaque Plug located at a depth of 3600 ft (1100m). This is not

LAMAQUE GOLD PROJECT DUE DILIGENCE

January 13th, 2009 5 of 156 PUMA RESOURCES LIMITED

currently in the reserve and cannot be accessed for 3 years until the mine is pumped out and the Sigma shafts are refurbished and are operational. 1.4 Mining Century acquired the Lamaque project properties in 2004, and began operations by reactivating the Sigma open pit mine. During early 2007, the Company began redevelopment of the Lamaque underground mine. In November 2007 the Company completed the transition from surface to underground mining and the Sigma open pit operation was discontinued due to high costs resulting from significant increases in the prices of fuel, tires and other spares, and higher than planned dilution of the ore. Underground mining was put into care and maintenance in July 2008 due to the lack of available capital needed to properly expand and sustain operations to a level where reasonable commercial returns could be achieved. Although it is unfortunate that active mining recently ceased, it is useful that the decline and haulage drifts are still open and that Dr van Hees and PRL were able to visit a variety of flat vein production stopes and underground infrastructure. The three main areas that are scheduled to be mined in the initial 3 years of operation and produce 1.6 Mt of ore at a grade of 4.78 g Au/t are the bulk ores contained in the Bedard Dyke (Sigma West) and the North Wall and the thin but higher grade flat veins in Lamaque 2 and Lamaque 2 Cross Over area which are either continuous or occur between shear zones or are influenced by dykes. All future mining will use underground methods due to the need for selectivity that was proved during open pit mining. Each of the three zones will be accessed independently by three separate ramps each with a cross section that permits 35 t trucks to be used. The ramps all originate from the lower levels of the existing Sigma open pit. The visit underground confirmed that flat vein stopes were typically 5’ to 8’ in height (1.5 to 2.4m) and provided evidence that the ore and host rocks are strong and competent, ventilation is adequate, workings are dry and the geometry of the veins is typically, but not always, predictable. From the existing ramp, production will commence in the flat vein. Since the Bedard dyke is close to the pit wall, production is also scheduled to occur in month 4 of 2009 but an accelerated ramp up is planned. The North Wall zone that is located below the pit limit is scheduled to produce in early 2010. A review of historic records by Dr van Hees indicated that dilution factors in flat veins ranged from 0 to 33%. In the past mining schedules typically added an average of 20% dilution. If a 10% dilution factor is applied to the expected Lamaque reserve grades the mined grade of 4.2 g Au/t would be comparable to the 0.14 to 0.15 oz/t historically achieved by Placer-Dome in the late 1980s and early 1990s. The changes in the mining method proposed by Century are anticipated to reduce dilution in many of the flat veins. The flat veins will be mined using a customised, partially mechanised, room and pillar method. To reduce dilution, split firing will be used to separate ore and waste in room headings plus excavating only mineralised slots on either side of the rooms thereby increasing extraction and reducing dilution. In PRL’s opinion the proposed flat vein method is workable since it is based on previous direct experience and has good potential to be improved upon by using other configurations and techniques used in South African gold mines. In the production plan used for the economic model, Century has conservatively assumed that full dilution will occur over the full 6ft (1.8 m) stope height. Century has also used conservative stope productivities of 60 tpd and an additional dilution of 5% and

LAMAQUE GOLD PROJECT DUE DILIGENCE

January 13th, 2009 6 of 156 PUMA RESOURCES LIMITED

losses of 5% of insitu tonnage. The planned dilution in the flats is expected to be reduced considerably (perhaps by 30-50%) when using the mechanised, selective method proposed but this will only be determined after experience is gained and only if strict controls are employed. As a result, PRL advocates no reduction in dilution is applied to the grades mined from flat vein areas.

To date, Century’s own experience of mining 15 flat vein stopes on 4 levels have demonstrated that almost all stopes have been more continuous and produced many more tonnes than were reported to be contained in the NI-43-101 compliant reserve or the geologists estimates prior to mining. In many cases economic ores have been stoped without any NI-43-101 compliant reserves even being recorded. Mining flat veins in the Sigma mine has resulted in producing nearly double the ounces than were predicted by the polygonal method. If this experience is repeated in the future, it suggests that insitu reserves in flat veins might have been underestimated. As a result the resources identified but not mined by Placer-Dome (e.g. the 76-77 vein) could contain resources comparable to that mined in the Lamaque main ore zone. This is regarded as an upside benefit to the project and if this trend continues to be confirmed by the budgeted drilling in advance of mining, it will allow Century to optimise the mining layouts and schedule additional tonnage. Mining access could potentially be a problem to some of the reserve zones since 45% of the mineralized blocks occur in close proximity to old mine workings and 20% were identified as potentially having access problems. As a result Century agreed to reconfigure the production schedule to recommence operating where there is existing access before mining from the upper levels down to the lower levels in a systematic manner. The Bedard Dyke and North Wall zones are to be mined using conventional long hole open stoping methods (LHOS). Previously, various types of shrinkage and cut and fill methods were used to mine vertical ore bodies. In PRL’s opinion LHOS is an appropriate method for the vertical orebodies. A memo provided by Century outlines the dilution that is expected to be achieve and why. Combining the 6% estimated dilution in the dykes (75% of the ore) with 20% dilution in the shear zones (10% of the ore) results in an expected average dilution of 7.6%. Given that figure, diluting the reserve / resources in the dykes and shear zones by 10% was considered by PRL to be appropriate. Since PRL’s visit, Century has reviewed and adjusted planned dilution to 10% and this remains acceptable. Century’s estimated losses due to the efficiency of mining extraction initially ranged from 5% to 25%. These were reduced in September 2008 to 20% and have since been adjusted to 5%. Overall a mining extraction of 95% (5% losses) is considered to be reasonable until operating experience is gained. PRL advocates computing for each area the best estimate of planned (primary) and unplanned (secondary) dilution based on geometry and method that is to be implemented. PRL considers that dilution and extraction targets will only be achieved if the Century mine geologist(s) work very closely with the mining department (shift bosses etc.). The section of the Bedard Dyke that is to be mined has been delineated by only 3 drill holes but has been previously successfully mined by Century in the open pit. The programme of a further 12 to 15 holes are scheduled to be drilled before commencing development in order to prove up the geometry ahead of mining commencing in month 4 of 2009. After completing an examination

LAMAQUE GOLD PROJECT DUE DILIGENCE

January 13th, 2009 7 of 156 PUMA RESOURCES LIMITED

of the drill plans, sections and spreadsheets provided in November 2008 by Century, Dr van Hees has concluded that the first phase of drilling on the Bedard Dyke is acceptable since it is aimed at establishing the extent of the mineralization exposed in the pit wall. The planned 30 ft (9m) wide stopes are to be located beneath the limit of the City of Val D’Or. Although the design includes a 120 ft (35m) crown pillar, the Bedard Dyke open stope has the potential to be up to a 1000 ft (300m) in height. PRL considers that although specific geotechnical studies need to done to support the design, a number of geotechnical studies have been completed in the past to investigate the impact that mining has had on the stability of the process plant and other surface facilities. These have confirmed that no surface subsidence has occurred and that modest sized pillars to date have been sufficient to ensure stability. As a result PRL considers that the initial mining of the Bedard Dyke would be considered as low geotechnical risk but that strict monitoring will be required. Century’s re-evaluation of the LHOS method will permit mined stopes to be filled with development waste thereby reducing geotechnical risks and reducing waste transport requirements. The geometry of the North Wall requires that a single decline ramp is threaded through the ore zones rather than establishing two ring mains at the extremities of the zones plus interconnections to allow multiple accesses. This is functional and reduces capital cost but warrants future review during production to ensure access is maintained and mucking distances are optimised. Production after year 3 will include mining the lower levels down to 6,000 ft (1,830 m) in depth. This requires that the Sigma 2 main and Sigma 3 internal shafts will have been dewatered, refurbished, re-equipped and upgraded. The Sigma 2 shaft was partially backfilled during open pit mining but is understood to be open at lower elevations. Water was not a significant problem in the past but over time the water levels have continued to rise and pumps need to be installed and commence operation in order to provide urgent relief as soon as funds and permits to dewater can be secured. The potential of equipping and operating some or the entire Sigma 2 shaft to permit hoisting while working on refurbishing the lower levels will be assessed during 2009. In the November 2008 plans Century has delayed reliance on the operating shafts and allowed more time to complete the upgrade. In the September 2008 report PRL considered that it was appropriate to downgrade 2009 production estimate from Century’s 0.36 Mtpa to 0.2 Mtpa pending further analysis and to maintain 0.72 Mtpa from 2010 onwards. After further analysis by Century a revised plan was presented in November 2008. This plan anticipates production of 0.28 Mt in 2009, 0.48 Mt is 2010 and a production rate that varies from 0.77 Mtpa to 0.70 Mtpa for the next 5 years (2011 to 2015). Following review PRL considers the November 2008 plan to be acceptable. From 2011 onwards PRL considers that a nominal 2,000 tpd (0.72 Mtpa) mining rate is achievable and accepts that a 3 year schedule (compared to 20 months previously) of flat vein and other mining have been fully scheduled. In particular the flat vein portion of the mine development sequence and schedule has been prepared in considerable detail. The schedule of the Bedard Dyke is conceptual since infill drilling has not been completed. The North wall schedule is also conceptual. The schedule for the Sigma West and Below open pit areas is indicative since grades are fixed. Although a logical conceptual plan for years 4 to 10 has been generated by Century, PRL is of the opinion that the sequence will be subject to adjustment depending on the results of the mining and exploration.

LAMAQUE GOLD PROJECT DUE DILIGENCE

January 13th, 2009 8 of 156 PUMA RESOURCES LIMITED

Table 1.3 presents a comparison of the 2P reserve and insitu ore scheduled for production. Table 1.3 Comparison between 2P reserves and insitu ore scheduled for production

Category 2P Reserve (Refer Table 1.2) Scheduled Insitu Ore

Area Tonnes grams/ tonne

Ounces Gold Tonnes grams/

tonne Ounces

Gold

Lamaque #2 396,884 6.11 77,969 446,420 5.72 78,049

Lamaque Main Plug 574,707 5.46 100,947 615,025 5.37 100,924

Sigma (Below Pit) 3,889,884 5.34 667,540 3,877,760 5.33 631,644

North Wall 1,804,327 4.43 256,770 1,661,895 4.99 253,535

Sigma West (Bedard Dyke) 150,702 4.56 22,108 150,404 4.80 22,050

West Plug 635,733 4.68 95,593 449,680 4.27 58,646

Total 7,452,237 5.10 1,220,927 7,201,184 4.94 1,144,848

Over the 11 year mine life Century has scheduled insitu reserves of 7.2 Mt at 4.94 g/t which converts to mine production of 7.5 Mt at 4.75 g Au/t. By comparison the underground 2P designated reserve is 7.45 Mt at 5.10 g/t (refer Table 1.2). Overall Century has scheduled mining 1.14 M oz compared to Century’s updated 2P estimate (reviewed by Dr van Hees) of 1.22 Moz. As stated in section 1.3 Century used a cut off grade of 2.5 g Au/t for the bulk of the reserves. PRL has confirmed that by using the average realised gold price of US$ 710/oz together with total cash operating cost (US$ 60/t), mining dilution (10%) and process recovery (95%) that the cash breakeven run-of-mine grade is 3.1 g Au/t and is equivalent to a cut off grade (COG) of 1.4 g/t. However for mine planning purposes, PRL accepts and endorses Century’s use of the 2.5 g Au/t COG which generates an economic breakeven grade of 4.5 g Au/t and is in excess of the average mined grade of 4.75 g/t. The mine planning COG is derived by adding provisions for capital cost amortization (US$ 19.44/t) and a 10% allowance for profit margin. Although PRL accepts that a single COG has been applied to all zones, Century understands that ongoing COG analysis will be required in response to changes in mining methods and economic drivers.

LAMAQUE GOLD PROJECT DUE DILIGENCE

January 13th, 2009 9 of 156 PUMA RESOURCES LIMITED

Although the contained 2P ounces at Lamaque #2 and Lamaque Main Plug are not exceeded, Century has reasonably assumed that an additional minor proportion of tonnes at a lower grade will mined during access and exploitation of 2P reserves. In addition there are a further 0.6 Million ounces of Measured and Indicated resources which are available to be considered for reclassification as reserves. In the September 2008 report PRL considered that it was appropriate to downgrade 2009 production estimate from Century’s 0.36 Mtpa to 0.2 Mtpa pending further analysis and to maintain 0.72 Mtpa from 2010 onwards. After further analysis by Century a revised plan was presented by Century in November 2008. This plan anticipates production of 0.26 Mt in 2009, 0.35 Mt in 2010 and 0.63 Mt in 2011. Thereafter the production rate varies from 0.74 Mtpa to 0.76 Mtpa for the next 7 years (2012 to 2018). Following review PRL considers the plan included in the current finance model to be acceptable. From 2012 onwards PRL considers that a nominal 2,000 tpd (0.72 Mtpa) mining rate is achievable and accepts that just over 3 years (compared to 20 months previously) of flat vein has been schedule in detail and conceptual life of mine planning has been provided. The schedule of the Bedard Dyke is conceptual since infill drilling has not been completed. The North wall schedule is also conceptual. The schedule for the Sigma West, West Plug and below open pit areas is indicative since grades are fixed. Although a logical conceptual plan for years 4 to 10 has been generated by Century, PRL is of the opinion that the sequence will be subject to adjustment depending on the results of the mining and exploration. PRL notes that Century has also scheduled mining of both the West Plug (0.45 Mt at 4.27 g/t) and Lamaque Plug (0.62 Mt at 5.37 g/t) during production years 7 to 11. The mining of the West Plug was originally planned to be carried out using Open Pit methods but will now be done using underground access which has not been defined to sufficient detail. The inclusion of production from the modest reserve in the Lamaque plug is acceptable since it has reached the standard necessary to be classified as a reserve. The overall magnitude of the Lamaque plug needs to be subjected to confirmatory drilling as discussed in section 1.3. Since this production occurs towards the end of loan service period more work will need be done during the first 3 years of operation to validate the plan. Overall PRL is of the opinion that the mining plan is realistic and that after start up, Century will have the time needed to prepare detailed annual plans for the duration of the loan service period (to 2015) plus a further 2 years (to 2017) as contingency planning. As mining and exploration data becomes available, work needs to be done on stope sequences; access verification; productivities and efficiencies; clarifying waste rock dumping strategies; applying dilution and losses appropriate to each method and stope configuration; costs and cut-off grades. There is a tourist mine owned by the City of Val D’Or which has access to a decline that Century does not use. The only operating interface is at depth and will be eliminated after Century completes the by-pass that will separate the tour mine from the producing mine. This plan has been discussed and agreed by the parties involved.

LAMAQUE GOLD PROJECT DUE DILIGENCE

January 13th, 2009 10 of 156 PUMA RESOURCES LIMITED

1.5 Processing PRL notes that the existing Sigma process plant that was originally designed to process 5,000 tpd will be utilised by Century to treat all ores. The plant flowsheet has been downsized to process up to 3,400 tpd and reconfigured to the circuit successfully used previously by Placer Dome to process underground ores. The SAG mill has been sold and two stage crushing followed by rod & ball milling in combination with Knelson concentrators and tabling will be used to recover gravity concentrate and prepare ore for CIL. The absorption/elution facility and gold room complete the conventional circuit. The extensive prior experience of Century, Teck and Placer Dome has demonstrated consistency of metallurgical response for all ore types. Based on a review of historical data by Dr van Hees, free gold recovery in a gravity circuit will likely be between 30 and 50%. In PRL’s opinion this factor and the short duration of the cyanide leaching is expected to combine to achieve the projected overall 95% recoveries. Given the probability that higher-grade feed and better native gold recovery from the underground ores will provide more free gold to the gravity system, it is recommended that security be improved in this part of the mill. Better lighting, more infrared cameras and a digital recording system should be installed in the gravity circuit area. Century has the plant on care and maintenance and is mechanically rotating mills regularly to facilitate restart. PRL did not identify any significant issues in Century’s plan to use the existing process plant. 1.6 Infrastructure The existing infrastructure is suitable and adequate to support the production plan. Water will be obtained from the tailings dams and make up from underground dewatering. Quebec Hydro is one of the world’s largest generators of electricity and provides power to Century’s facilities. Century is negotiating with Hydro Quebec to work out a payment schedule plan on the C$ 0.2 million owing. On-going payments are currently being made to Hydro Quebec. Century reports that the signing of the contract with Quebec Hydro will occur by the end of Q1 2009 when capacity payments become due. Nevertheless, Century will provide before closing the final draft of the contract a statement from Quebec hydro that they will agree to enter into such contract and that they will have available capacity to deliver the power to Century. Century will enter into a new M-contract with Hydro Quebec. Century’s existing M-contract expires on February 28th, 2009. The Company has no negotiating ability with Hydro Quebec as rates are established under legislation. It is Century’s intention to enter into a “pay for usage” contract as the power demand and consumption will be significantly less than the power and consumption was during the open pit operations. The Lamaque mine is now scheduled to produce and mill 2,000 tpd which is within the regular power demand for the area and availability of power is assured. At this time, it is not in Century’s best interest to sign any long term contract until the operation has reached full capacity and accurate power draw can be assessed.

LAMAQUE GOLD PROJECT DUE DILIGENCE

January 13th, 2009 11 of 156 PUMA RESOURCES LIMITED

1.7 Environmental/Permitting The EBA review consisted of a site visit, inspection and discussions with the available mine personnel. Since Lamaque is in a state of care and maintenance no observations could be made of the operating mine or processing plant. EBA determined that none of the environmental and permitting issues are considered to pose a significant risk to the environment or the current or planned near-future operations of the mine. None of the 13 risk areas in this topic scored higher in subjective terms than moderately low. Regulatory requirements in Quebec are well understood by Mine Management and applications for certificates of approval have been made or are in process for future development plans. Issues of environmental concern to the Quebec regulatory agency have been resolved or are in the process of being resolved. Monitoring programs for surface water and groundwater quality and slope stability are carried out to satisfy government requirements. Reports are provided to appropriate government agencies as required.