Jim Splinter HRL Investor Day 2015

25

Grocery Products Jim Splinter Group Vice President 1

-

Upload

hormel-foods-corporation -

Category

Business

-

view

91 -

download

1

Transcript of Jim Splinter HRL Investor Day 2015

1

Grocery Products

Jim Splinter

Group Vice President

CY 2009 CY 2010 CY 2011 CY 2012 CY 2013 CY 2014

$155,427 $156,819 $163,000 $167,901 $170,542 $172,342

76,598 77,652 77,834 77,060 77,313 77,436

Dollar Sales (MM) Unit Sales (MM)

Total Center of Store Food is a $172B Category Five Year CAGR: + 2.1% in Dollars and + 0.2% in Units

Source: IRI TSV, Total U.S. MULO, Calendar Year (CY) Ending Periods 2

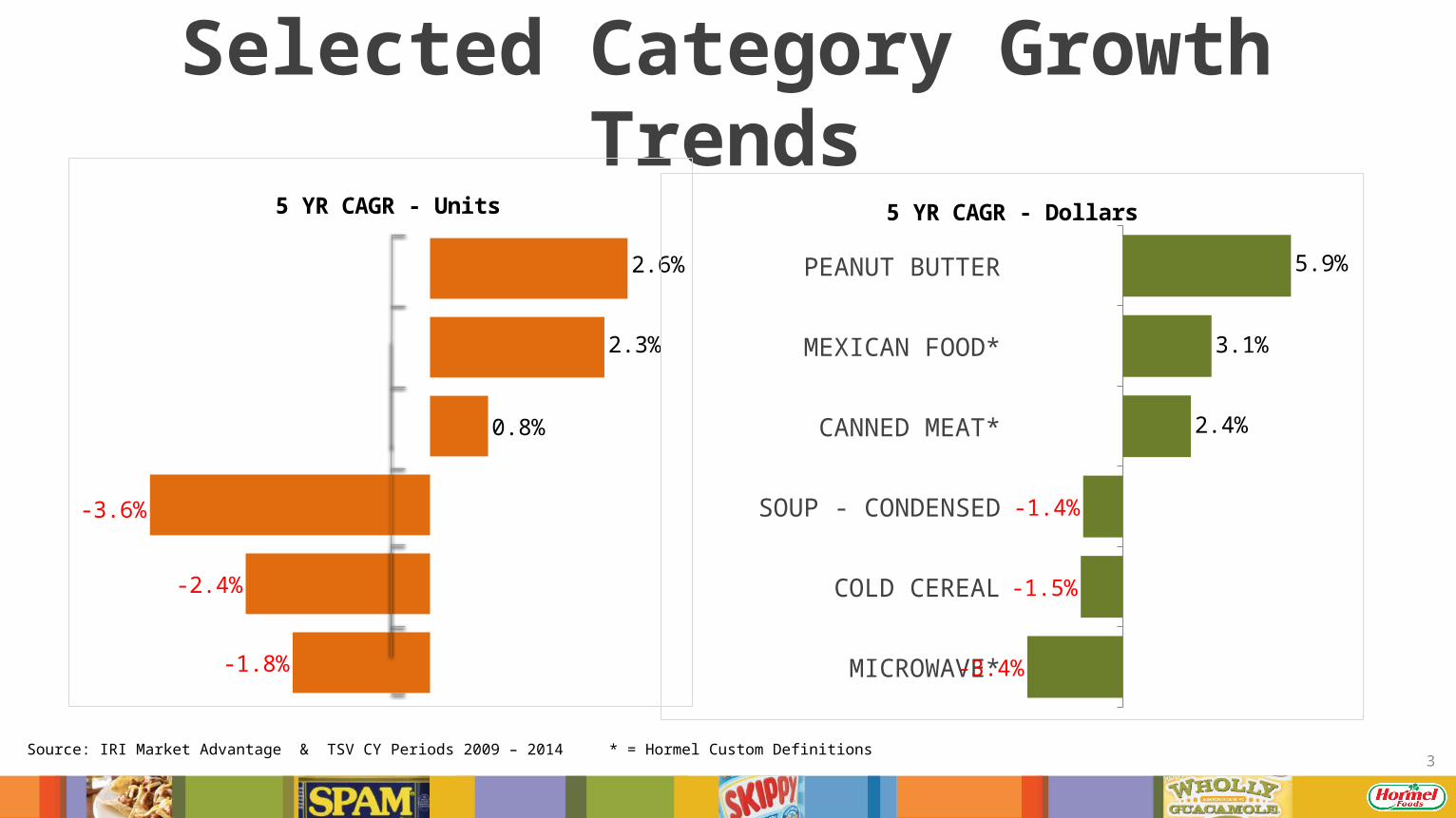

Selected Category Growth Trends

-1.8%

-2.4%

-3.6%

0.8%

2.3%

2.6%

5 YR CAGR - Units

MICROWAVE*

COLD CEREAL

SOUP - CONDENSED

CANNED MEAT*

MEXICAN FOOD*

PEANUT BUTTER

-3.4%

-1.5%

-1.4%

2.4%

3.1%

5.9%

5 YR CAGR - Dollars

Source: IRI Market Advantage & TSV CY Periods 2009 – 2014 * = Hormel Custom Definitions3

3Yr CAGR Net Sales 14% & Segment Profit 6%

Grocery Products

(Dollars in Millions)

% Net Sales Change to YrAgo

% Segment Profit Change to YrAgo

* MMX’s Don Miguel Foods revenues reported in Grocery Products ** Hormel Foods acquisition of SKIPPY® peanut butter 4

Financial Evolution

+ 2%

+ 10%

+ 30%

+ 3%

2011

2012*

2013**

2014

+ 4%

+ 12%

+ 18%

- 9%

5

Key Performance Targets

Revenue Growth of 3%

Brand Building & Innovation

Segment Profit Growth of 6%

6

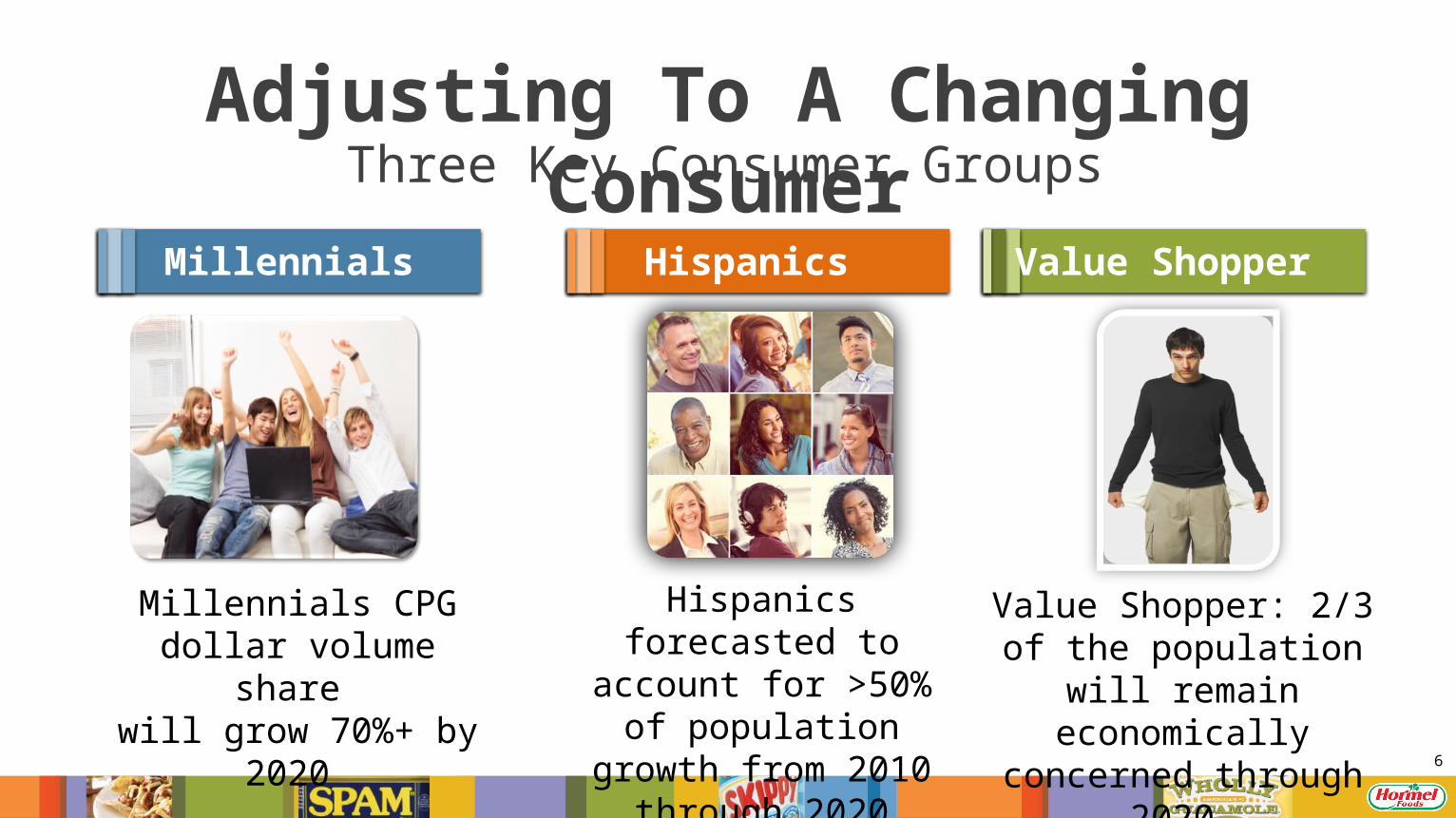

Value Shopper: 2/3 of the population will

remain economically concerned through 2020

Hispanics forecasted to account for >50% of

population growth from 2010 through 2020

Millennials CPG dollar volume share

will grow 70%+ by 2020

Adjusting To A Changing ConsumerThree Key Consumer Groups

Millennials Hispanics Value Shopper

Transparency, Relevancy and Authenticity

7Multicultural On-the-go Healthy / Holistic

Innovation Hitting $3B X ‘16 Expectations

Multicultural On-the-go Healthy / Holistic8

•15% of sales are from products new to the division since 2000

CAGR + 6% vs. 2010

Increased Baseline Marketing Support

20152010

Advertising Investment Levels*

* = Includes MegaMex

Data Source: Internal Reporting & Revenue Accounting

9

10

• Effortless meal creativity• Defines the category• Iconic equity

11

12

• Effortless meal creativity• Defines the category• Iconic equity

On-the-go

13

• America’s #1 chili since 1936• Universal appeal• In & out of the bowl usage• Iconic brand equity

14

15

• #1 in single-serve, shelf-stable meals

• Delivering moments of satisfaction

• Established blue-collar adults

16

50%

MegaMex Foods

17

• Headquartered in Orange, CA

• 5 locations worldwide• 3,500 employees

Vision

To bring the spirit of Mexico to every table

Structure

50%

18

• Authentic• Innovative• Social engaged• Solutions-focused

Multicultural

19

• Relevant / fun• “Power food”• Organic offerings• Socially engaged• Innovative• Category leader

WHOLLY GUA-

CAMOLE42.7%

YUCATAN15.2%

SABRA13.5%

PRIVATE LABEL9.9%CALAVO

3.8%

All Other14.8%

Healthy / Holistic Multicultural

20

SKIPPY® is the PEANUT BUTTER that SPREADS SIMPLE FUN!

On-the-go

Healthy / Holistic

21

22

SKIPPY is the PEANUT BUTTER that SPREADS SIMPLE FUN!

On-the-go

Healthy / Holistic

23

Summary • Performance target guidance of 3% topline

and 6% bottom-line

• Division is adjusting to a changing consumer

• Managing the legacy core portfolio for modest growth

• Restructuring Microwave Meals with a renewed focus on core users

• Expect MegaMex to continue being our “growth engine”

• Executing our SKIPPY® strategic growth plan

24

The End

25

![[MS-HRL]: Hyper-V Replica Log (HRL) File Format...FileType: This field identifies the type of the log file. For an HRL file, this field’s value is set to 0. For an HRL file, this](https://static.fdocuments.us/doc/165x107/5f3c75afbcdce535f956eeb6/ms-hrl-hyper-v-replica-log-hrl-file-format-filetype-this-field-identifies.jpg)