January 2018 - semenindonesia.com · 8 Strategic Projects (2017) Strategic Projects Capacity...

20

January 2018

Transcript of January 2018 - semenindonesia.com · 8 Strategic Projects (2017) Strategic Projects Capacity...

January 2018

2

think about theENVIRONMENT

3

• Design Capacity : 106.3 mt• Production Capacity : 74.0 mit• Domestic Growth : 7.5%• Domestic Utilization: 63%•Supply Domestic : 66.5 mt Export :

Clinker : 1,8 mtCement : 1,1 mt

Domestic Capacity (2017)

2017

Cement companies in Indonesia

1. Semen Indonesia 35.5 mt2. Indocement TP 24.9 mt3. Lafarge Holcim Indonesia 14.5 mt4. Semen Merah Putih 7.5 mt5. Semen Bosowa 7.0 mt6. Semen Anhui Conch 4.5 mt7. Semen Baturaja 3.8 mt8. Semen Pan Asia 1.9 mt9. Siam Cement Group 1.8 mt 10. Semen Jui Shin 1.5 mt11. Semen Serang (Haohan) 1.2 mt12. Semen Jakarta 1.0 mt13. Semen Hippo (Sun Fook) 0.6 mt14. Semen Kupang 0.3 mt15. Semen Puger 0.3 mt

TOTAL 106,3 mio ton

*) Source: SMGR intemal calculation*) Source: SMGR intemal calculation

4source: Company data

SMGR’s Sales Volume

Nov-17 Dec-17 Dec-16 Chg (%) 2017FY 2016FY Chg(%)

Domestic 2,566,901 2,359,967 2,182,947 8.1 27,091,728 25,682,143 5.5

Export 169,638 170,607 48,676 250 1,870,862 599,510 212

TOTAL 2,736,539 2,530,574 2,231,623 13.4 28,962,590 26,281,653 10.2

TLCCDomesticExport

166,75746,400

174,30045,000

173,29972,800

0.5(38.1)

1,832,563342,080

1,760,000776,000

4.1(55.9)

TOTALSemen Indonesia Group

2,949,696 2,749,874 2,477,722 (10.9) 31,137,233 28,817,653 8

731

600

650

700

750

800

NET ASP - DOMESTIC CEMENT (Rp Ribu/Ton)

ACTUAL

2,670

1600.0 1800.0 2000.0 2200.0 2400.0 2600.0 2800.0 3000.0 3200.0 3400.0

Dec-

16

Jan-

17

Feb-

17

Mar

-17

Apr-

17

May

-17

Jun-

17

Jul-1

7

Aug-

17

Sep-

17

Oct

-17

Nov-

17

Dec-

17

SALES VOLUME

ACTUAL

5Source: Company data, Indonesia Cement Association

Indonesia Cement Sales VolumeNov-17 Dec-17 Dec-16 Chg (%) 2017FY 2016FY Chg(%)

Domestic 2,566,901 2,359,967 2,182,947 8.1 27,091,728 25,682,143 5.5

Export 169,638 170,607 48,676 250 1,870,862 599,510 212

TOTAL 2,736,539 2,530,574 2,231,623 13.4 28,962,590 26,281,653 10.2

TLCCDomesticExport

166,75746,400

174,30045,000

173,29972,800

0.5(38.1)

1,832,563342,080

1,760,000776,000

4.1(55.9)

TOTALSemen Indonesia Group

2,949,696 2,749,874 2,477,722 (10.9) 31,137,233 28,817,653 8

6

Retail (residential) sector is still the largest consumer of cement in Indonesia

BAG74.5%

BULK25.5%

Bag Bulk

• Ready-mix (infrastructure): ± 60%

• Fabricator (pre-cast, fiber cement, cement based industry): ± 35%

• Projects (mortar, render): ± 5%

• Ready-mix (infrastructure): ± 60%

• Fabricator (pre-cast, fiber cement, cement based industry): ± 35%

• Projects (mortar, render): ± 5%

• Housing: ± 90%

• Cement based industry: ± 10%

• Housing: ± 90%

• Cement based industry: ± 10%

source: Indonesia Cement Association

domestic market consumption (2017) – type of cement

7

Infrastructure Spending Planned for 2015 – 2019 (USD Bn)

INFRASTRUCTURE DEVELOPMENT

COMMERCIAL & INDUSTRIAL High growth in retail, commercial and

institutional sector in urban and semi-urban area High growth industry segment (precast, light brick,

cement fiber, pave, ready mixed concrete)

HOUSING Population Growth Rising per Capita Income Mass urbanization

CEMENT CONSUMPTION 2016 (KG/CAPITA)

Rapidly Growing Productive Population

Key Factors Supporting Domestic Cement Consumption

172 42106

113 433

CentralGovt

RegionalGovt

SOEs Private Total

POTENTIAL MARKETThe fourth largest population in the world: 258millions people (2015)

DEMOGRAPHIC BONUS

1648

1000763 617

458 399 262 248 244 163

0

500

1000

1500

2000

Cement Consumption per Capita (kg)

average (ex china) = 459kg

8

Strategic Projects (2017)

Strategic Projects Capacity InvestmentConstruction Start up commercial

Start Completion

Packing Plant Maluku Utara 500,000 ton/year

300,000 (bags)200,000 (bulk)

IDR 66 Bio January 2017 Q1-2018 Q2-2018

Packing Plant Bengkulu IDR 75 Bio February 2017 Q1–2018 Q2-2018

Waste Heat Recovery Power Generation 30.6 MW IDR 574 Bio Q2-2016 Q1-2018 Q2-2018

Proyek Packing Plant BengkuluProyek Packing Plant Maluku Utara

Proyek Waste Heat Recovery Power Generation (WHRPG) - Pabrik Tuban

9

Integrated Cement Plant 4 location

Kiln 15 Unit

Cement Mill 26 Unit

Grinding Plant 3 location

Cement Mill 4 Unit

Warehouse 30 location

Packing Plant 22 location

Sea Port 12 location

Kiln 1 unit

Cement Mill 1 unit

Kiln 5 unit

Cement Mill 8 unit

Kiln 5 unit

Cement Mill 11 unit

Grinding Plant

1 unit Cement Mill

Kiln 4 unit

Cement Mill 6 unitGrinding Plant

3 unit Cement Mill

Our facilities

10

Opportunity Regional Cement Market

11

Supply-Demand Cement in Asia Pacific

2017E (mtpa) Design Cap. Production Cap. Consumption Export

(Import) China 3794,4 2390,6 2380,5 10,1India 396 313,7 311,7 2

Indonesia 106,3 74 69 5Vietnam 91,5 74,6 57,5 17,1

South Korea 71,6 53,1 50,2 2,9Thailand 60,5 36,4 31,3 5,1Pakistan 48 39,7 30,8 8,9Malaysia 41,3 23,6 22,9 0,7

Philippines 34,2 26 26,5 -0,5Australia 13,2 8,7 9,5 -0,8Myanmar 10,5 8 9,8 -1,8

Laos 10 6 3,3 2,7

Source : Global Cement, Bloomberg, Digital Cement

12

think about theENVIRONMENT

13

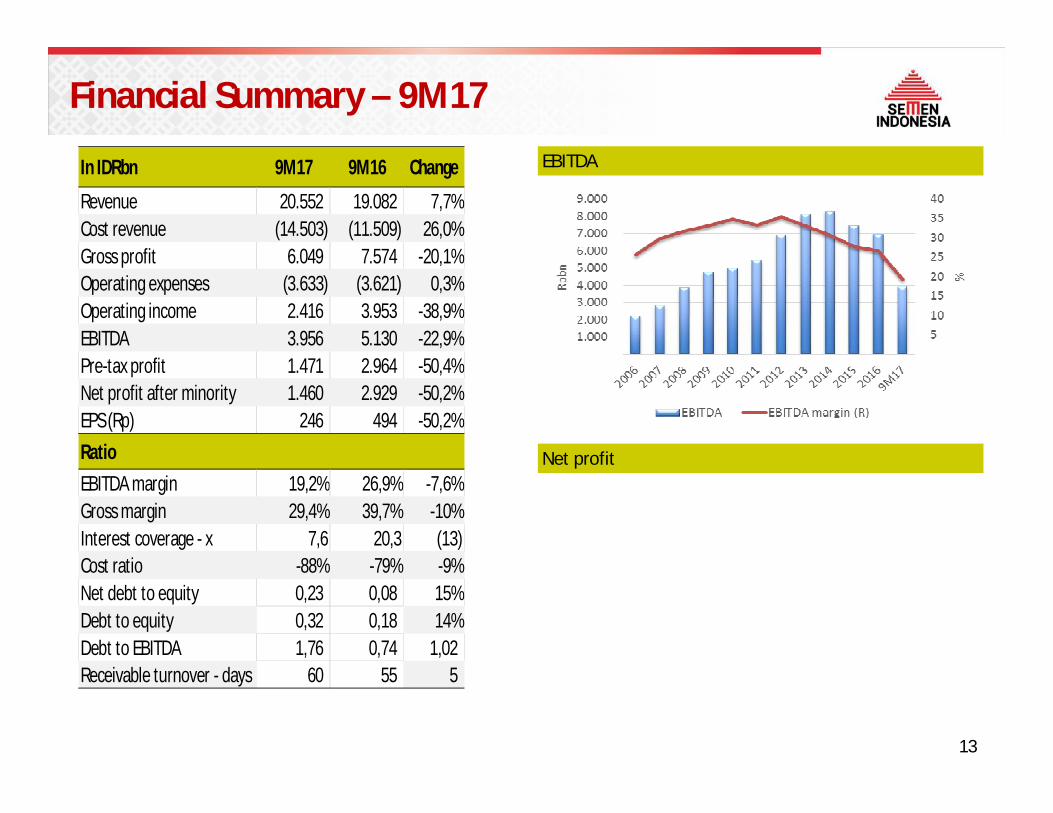

Financial Summary – 9M17

EBITDA

Net profit

In IDRbn 9M17 9M16 Change

Revenue 20.552 19.082 7,7%Cost revenue (14.503) (11.509) 26,0%Gross profit 6.049 7.574 -20,1%Operating expenses (3.633) (3.621) 0,3%Operating income 2.416 3.953 -38,9%EBITDA 3.956 5.130 -22,9%Pre-tax profit 1.471 2.964 -50,4%Net profit after minority 1.460 2.929 -50,2%EPS (Rp) 246 494 -50,2%RatioEBITDA margin 19,2% 26,9% -7,6%Gross margin 29,4% 39,7% -10%Interest coverage - x 7,6 20,3 (13) Cost ratio -88% -79% -9%Net debt to equity 0,23 0,08 15%Debt to equity 0,32 0,18 14%Debt to EBITDA 1,76 0,74 1,02 Receivable turnover - days 60 55 5

14

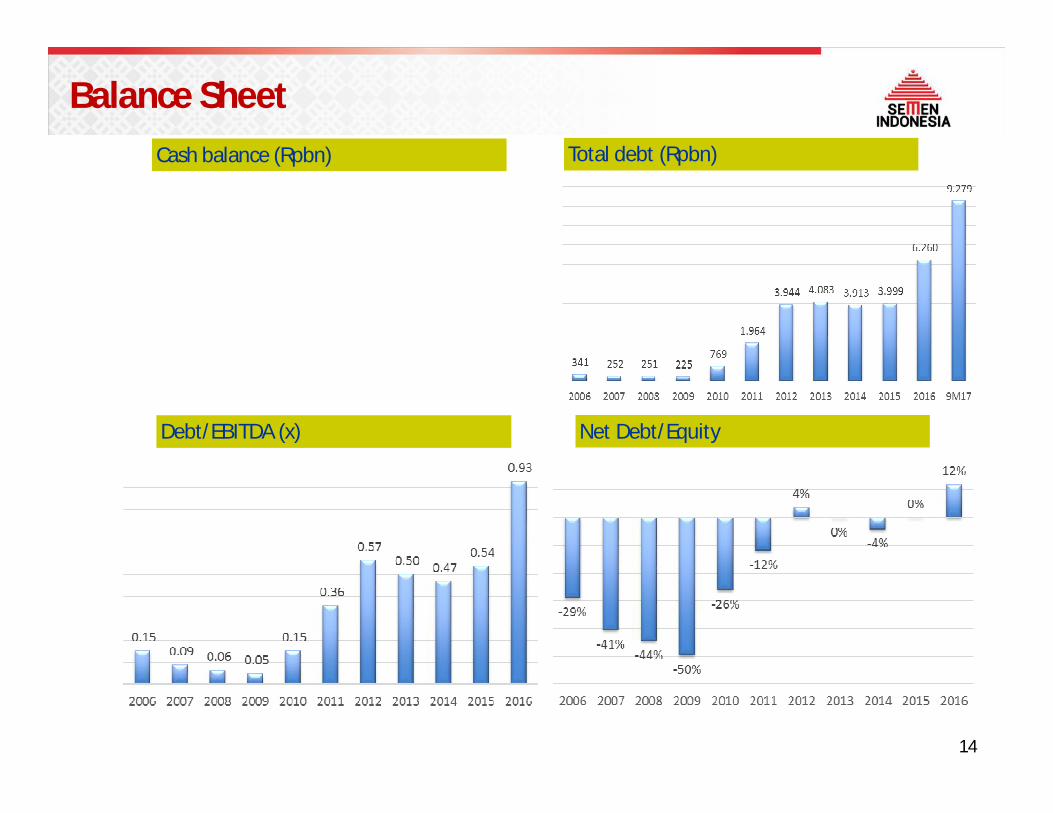

Balance SheetCash balance (Rpbn) Total debt (Rpbn)

Debt/EBITDA (x) Net Debt/Equity

15

Likuiditas dan Solvabilitas

15

(Dal

amRp

Mili

ar) 4,070

4,926

3,964

2,834 2,674

2013Audited

2014Audited

2015Audited

2016Audited

9M 2017

CASH

1.88 2.21

1.60 1.27

2013Audited

2014Audited

2015Audited

2016Audited

CURRENT RATIO

4,083 3,913 4,001

6,260

9,279

2013Audited

2014Audited

2015Audited

2016Audited

9M 2017

INTEREST BEARING DEBT

(Dal

amRp

Mili

ar)

0.50 0.47 0.54

0.90

2013Audited

2014Audited

2015Audited

2016Audited

DEBT TO EBITDA

16

Dividend Pay Out

Dividen Pay Out (DPO)

Earning Per Share (EPS)

17

think about theENVIRONMENT

18

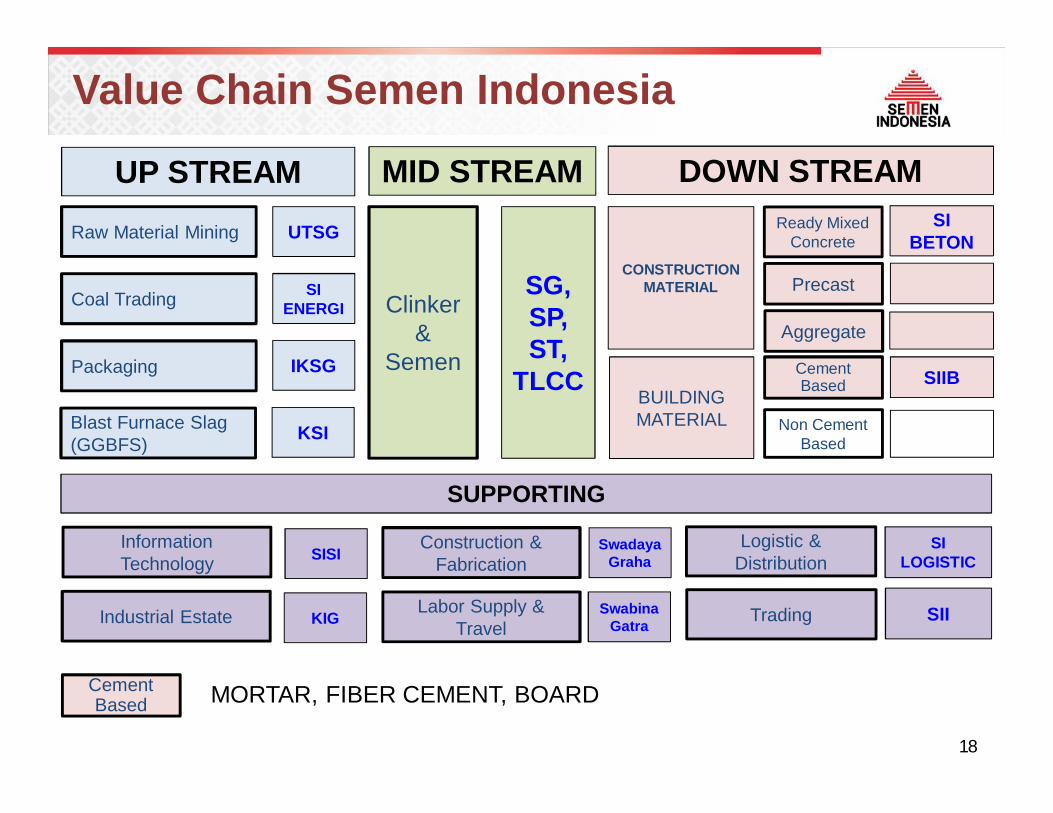

Value Chain Semen Indonesia

UP STREAM MID STREAM DOWN STREAMRaw Material Mining UTSG

Coal Trading SI ENERGI

Packaging IKSG

Clinker&

Semen

SG, SP, ST,

TLCC

CONSTRUCTION MATERIAL

SI BETON

Blast Furnace Slag (GGBFS) KSI

BUILDING MATERIAL

SIIB

SUPPORTING

Logistic & Distribution

SI LOGISTIC

Construction & Fabrication

SwadayaGraha

Information Technology SISI

Labor Supply & Travel

SwabinaGatraIndustrial Estate KIG

Ready Mixed Concrete

Precast

Cement Based

Non Cement Based

Aggregate

Trading SII

Cement Based MORTAR, FIBER CEMENT, BOARD

19

2018 - KEY STRATEGY

Supply Chain Optimization

Cost Transformation & Enable Corporate Growth

(Growth) Strategy Refresh

Centralize Marketing

Centralize Procurement

20

IMPORTANT NOTICETHIS PRESENTATION IS NOT AND DOES NOT CONSTITUTE OR FORM PART OF, AND IS NOT MADE IN CONNECTION WITH, ANY OFFER FOR SALE OR SUBSCRIPTION OF ORSOLICITATION, RECOMMENDATION OR INVITATION OF ANY OFFER TO BUY OR SUBSCRIBE FOR ANY SECURITIES NOR SHALL IT OR ANY PART OF IT FORM THE BASIS OFOR BE RELIED ON IN CONNECTION WITH ANY CONTRACT, COMMITMENT OR INVESTMENT DECISION WHATSOEVER.THE SLIDES USED IN THIS PRESENTATION ARE STRICTLY CONFIDENTIAL AND HAVE BEEN PREPARED AS A SUPPORT FOR ORAL DISCUSSIONS ONLY. THE INFORMATIONCONTAINED IN THIS PRESENTATION IS BEING PRESENTED TO YOU SOLELY FOR YOUR INFORMATION AND MAY NOT BE REPRODUCED OR REDISTRIBUTED TO ANY OTHERPERSON, IN WHOLE OR IN PART.This presentation includes forward-looking statements, which are based on current expectations and forecast about future events. Such statements involve known / unknown risksuncertainties and other factors, which could cause actual results to differ materially from historical results or those anticipated. Such factors include, among others:● economic, social and political conditions in Indonesia, and the impact such conditions have on construction and infrastructure spending in Indonesia;● the effects of competition;● the effects of changes in laws, regulations, taxation or accounting standards or practices;● acquisitions, divestitures and various business opportunities that we may pursue;● changes or volatility in inflation, interest rates and foreign exchange rates;● accidents, natural disasters or outbreaks of infectious diseases, such as avian influenza, in our markets;● labor unrest or other similar situations; and● the outcome of pending or threatened litigation.We can give no assurance that our expectations will be attained.

DISCLAIMERThe information contained in this report has been taken from sources which we deem reliable. However, none of PT Semen Indonesia (Persero) Tbk and/or its affiliated companies and/or their respective employees and/or agents make any representation or warranty (express or implied) or accepts any responsibility or liability as to, or in relation to, the accuracy or completeness of the information and opinions contained in this report or as to any information contained in this report or any other such information or opinions remaining unchanged after the issue thereof.We expressly disclaim any responsibility or liability (express or implied) of PT Semen Indonesia (Persero) Tbk, its affiliated companies and their respective employees and agents whatsoever and howsoever arising (including, without limitation for any claim, proceedings, action, suits, losses, expenses, damages or costs) which may be brought against or suffered by any person as a result of acting in reliance upon the whole or any part of the contents of this report and neither PT Semen Indonesia (Persero) Tbk, its affiliated companies or their respective employees or agents accepts liability for any errors, omission or mis-statements, negligent or otherwise, in the report and any liability in respect of the report or any inaccuracy therein or omission therefrom which might otherwise arise is hereby expresses disclaimed.

Thank You

Head Office:Gedung Utama Semen Indonesia

Jalan Veteran, Gresik 61122, East Java – IndonesiaPhone: (62-31) 3981731 -2, 3981745

Fax: (62-31) 3983209, 3972264

Representative Office:The East Tower, 18th floorJalan Dr. Ide Anak Agung Kav. E3.2 No. 1,Jakarta 12950, IndonesiaTelp.: (62-21) – 5261174, 5261175; Fax : (62-21) – 5261176

www.semenindonesia.com