INFLATION REPORT - Bangko Sentral Ng Pilipinas · he primary objective of monetary policy is to...

75

i INFLATION REPORT First Quarter 2008 Bangko Sentral ng Pilipinas

-

Upload

nguyenkhue -

Category

Documents

-

view

214 -

download

2

Transcript of INFLATION REPORT - Bangko Sentral Ng Pilipinas · he primary objective of monetary policy is to...

i

INFLATION REPORT

First Quarter 2008

Bangko Sentral ng Pilipinas

i

FOREWORD

he primary objective of monetary policy is to promote a low and stable rate of inflation conducive to a balanced and sustainable economic growth. The adoption

in January 2002 of the inflation targeting framework for monetary policy was aimed at helping fulfill this objective.

One of the key features of inflation targeting is greater transparency, which means greater disclosure and communication by the BSP of its policy actions and decisions. This Inflation Report is published by the BSP as part of its transparency mechanisms under inflation targeting. The objectives of this Inflation Report are: (i) to identify the risks to price stability and discuss their implications for monetary policy; and (ii) to document the rigorous economic analysis behind the conduct of monetary policy and convey to the public the overall thinking behind the BSP’s decisions on monetary policy. The broad aim is to make monetary policy easier for the public to follow and understand and enable them to better monitor the BSP’s commitment to the inflation target, thereby helping both in anchoring inflation expectations and encouraging informed debate on monetary policy issues.

The government’s targets for annual headline inflation under the inflation targeting

framework have been set at 4.0 percent and 3.5 percent for 2008 and 2009, respectively, both with a tolerance interval of ± 1.0 percentage point.

The report is published on a quarterly basis, presenting a survey of the various

factors affecting inflation. These include recent price and cost developments, prospects for aggregate demand and output, monetary and financial market conditions, labor market conditions, fiscal developments, and the international environment. A section is devoted to the BSP’s view of the inflation outlook during the policy horizon. This is followed by a discussion of the implications of the assessment of inflation and economic conditions on the monetary policy settings of the BSP. This issue also features a box article on the developments in global food prices and their impact on domestic food prices.

The Monetary Board approved this Inflation Report at its meeting on 30 April 2008.

AMANDO M. TETANGCO, JR.

Governor

May 2008

T

ii

List of Acronyms, Abbreviations and Symbols AMCs Asset Management Companies ARMM Autonomous Region of Muslim Mindanao BAS Bureau of Agricultural Statistics BES Business Expectations Survey BI Bureau of Immigration BIR Bureau of Internal Revenue BNM Bank Negara Malaysia BNBs Bank Negara Bills BOC Bureau of Customs BOE Bank of England BOJ Bank of Japan BOK Bank of Korea BOT Bank of Thailand BTr Bureau of the Treasury CalPERS California Public Employees’ Retirement System CAMPI Chamber of Automotive Manufacturers of the Philippines, Inc. CAR Capital Adequacy Ratio CBD Central Business District CCRs Credit Card Receivables CES Consumer Expectations Survey CDS Credit Default Swaps CPI Consumer Price Index DBCC Development Budget Coordinating Committee DCS Depository Corporations Survey ECB European Central Bank ERC Energy Regulatory Commission FBT Food, beverage and tobacco FIREBS Financial institutions, real estate and business services FLW Fuel, light and water FOMC Federal Open Market Committee GDP Gross Domestic Product GNP Gross National Product GRAM Generation Rate Adjustment Mechanism GS Government Securities HICP Harmonized Indices of Consumer Prices ICERA Incremental Currency Exchange Rate Adjustment IMF International Monetary Fund KBs Commercial banks KWH Kilowatt hour LFS Labor Force Survey LPG Liquefied Petroleum Gas LTO Land Transportation Office MAS Monetary Authority of Singapore MEM Multi-Equation Model Meralco Manila Electric Company MISSI Monthly Integrated Survey of Selected Industries MS Monetary Survey MSBs Monetary Stability Bonds MT Metric Tons

iii

MTP Major Trading Partner NCR National Capital Region NEER Nominal Effective Exchange Rate NFIA Net Factor Income From Abroad NG National Government NIA National Income Accounts NPC National Power Corporation NPLs Non-performing loans NSO National Statistics Office OFs Overseas Filipinos OMOs Open market operations OPEC Organization of Petroleum Exporting Countries PBC People’s Bank of China PMI Purchasing Managers’ Index PSEi Philippine Stock Exchange Composite Index PSS Postal Savings System PSIC Philippine Standard Industrial Classification PTIC Philippine Telecommunications Investment Corporation RDA Reserve Deposit Account REER Real Effective Exchange Rate RM Reserve Money ROP Republic of the Philippines RP Repurchase RRP Reverse Repurchase RVAT Reformed Value Added Tax SEM Single-Equation Model SDA Special Deposit Account TLP Total Loan Portfolio TMA Truck Manufacturers Association TransCo National Transmission Corporation U/KBs Universal/commercial banks VAPI Value of Production Index VOPI Volume of Production Index WESM Wholesale Electricity Spot Market

iv

THE MONETARY POLICY OF THE BANGKO SENTRAL NG PILIPINAS

The BSP Mandate The BSP’s main responsibility is to formulate and implement policy in the areas of money, banking and credit, with the primary objective of maintaining stable prices conducive to a balanced and sustainable economic growth in the Philippines. The BSP also aims to promote and preserve monetary stability and the convertibility of the national currency. Monetary Policy Instruments The BSP uses various instruments to effect the desired monetary policy stance to achieve the inflation target. These include (a) raising/reducing the BSP's policy interest rates; (b) increasing/decreasing the reserve requirement; (c) encouraging/discouraging deposits in the special deposit account (SDA) facility by banks and trust entities of BSP-supervised financial institutions; (d) increasing/decreasing its rediscount rate on loans extended to banking institutions on a short-term basis against eligible collaterals of banks’ borrowers; and (e) outright sales/purchases of the BSP’s holdings of government securities. The BSP’s primary monetary policy instruments are its overnight reverse repurchase (borrowing) rate and overnight repurchase (lending) rate. Policy Target The BSP uses the Consumer Price Index (CPI) or headline inflation rate which is compiled and released to the public by the National Statistics Office (NSO) as its target for monetary policy. The policy target is set by the Development Budget Coordinating Committee (DBCC)1 in consultation with the BSP. For 2008, the Government’s target for annual headline inflation has been set at 4.0 percent with a tolerance interval of ± 1.0 percentage point. For 2009, the headline inflation target has been set at 3.5 percent ± 1.0 percentage point. BSP’s Explanation Clauses These refer to the predefined set of acceptable circumstances under which an inflation-targeting central bank may fail to achieve its inflation target. These clauses recognize the fact that there are limits to the effectiveness of monetary policy and that deviations from the inflation target may sometimes occur because of factors beyond the control of the central bank. Under the inflation targeting framework of the BSP, these exemptions include inflation pressures arising from: (a) volatility in the prices of agricultural products; (b) natural calamities or events that affect a major part of the economy; (c) volatility in the prices of oil products; and (d) significant government policy changes that directly affect prices such as changes in the tax structure, incentives and subsidies.

1 The DBCC, created under Executive Order (E.O.) No. 232 dated 14 May 1970, is an inter-agency committee tasked

primarily to formulate the National Government's fiscal program. It is composed of the Department of Budget and Management (DBM), National Economic and Development Authority (NEDA), and the Department of Finance (DOF). The BSP sits as a resource agency.

v

The Monetary Board The powers and functions of the BSP, such as the conduct of monetary policy and the supervision over the banking system, are exercised by its Monetary Board, which has seven members appointed by the President of the Philippines. Beginning in July 2006, the Monetary Board meets every six weeks to review and decide on the stance of monetary policy. Prior to July 2006, monetary policy meetings by the Monetary Board were held every four weeks.

Chairman Amando M. Tetangco, Jr. Members Romulo L. Neri

Vicente B. Valdepeñas, Jr.

Raul A. Boncan

Juanita D. Amatong

Nelly F. Villafuerte

Alfredo C. Antonio

The Advisory Committee The Advisory Committee was established as an integral part of the institutional setting for inflation targeting. It is tasked to deliberate, discuss and make recommendations on monetary policy to the Monetary Board. The Committee meets every six weeks (beginning July 2006) but may also meet in between the regular meetings, whenever it is deemed necessary. Prior to July 2006, the Committee met every four weeks.

Chairman Amando M. Tetangco, Jr.

Governor Members2 Diwa C. Guinigundo

Deputy Governor Monetary Stability Sector

Nestor A. Espenilla, Jr. Deputy Governor Supervision and Examination Sector

Ma. Cyd N. Tuaño-Amador

Managing Director Monetary Policy Sub-Sector

Ma. Ramona GDT Santiago Managing Director Treasury Department

2 The Advisory Committee is supported by a Technical Secretariat composed of officers and staff from the Department of

Economic Research, Center for Monetary and Financial Policy, and the Treasury Department.

vi

Mtg. No. Advisory Committee 1/ Monetary Board 2/ Publication of Monetary Board Highlights 3/

1 28 January, Monday 31 January, Thursday 28 February, Thursday

2 10 March, Monday 13 March, Thursday 10 April, Thursday

3 21 April, Monday 24 April, Thursday 22 May, Thursday

3 2 June, Monday 5 June, Thursday 03 July, Thursday

5 14 July, Monday 17 July, Thursday 14 August, Thursday

6 26 August, Tuesday /a 28 August, Thursday 25 September, Thursday

7 6 October, Monday 9 October, Thursday 06 November, Thursday

8 17 November, Monday 20 November, Thursday 17 December, Thursday

9 15 December, Monday 18 December, Thursday 22 January 2009, Thursday

Notes:

SCHEDULE OF THE MEETINGS ON MONETARY POLICYAND PUBLICATION OF HIGHLIGHTS FOR 2008

2008

starting July 2006. Prior to this, the Advisory Committee and Monetary Board meetings were held every four weeks. 2/ Monetary Board meetings on monetary policy are held on the Thursday after the latest Advisory Committee meeting. 3/ Under MB Resolution No. 630, the lag in the publication of the highlights of the Monetary Board meetings on monetary policy issues

1/ Under MB Resolution No. 630, the frequency of meetings of the Advisory Committee and the Monetary Board was set at every six weeks

was reduced to four weeks. Prior to this, the highlights were published six weeks after the reference meeting date.a/ The AC meeting will be held a day later since the scheduled AC meeting date on 25 August 2008 (Monday) coincides with the celebration of the Ninoy Aquino Day and the National Heroes' Day.

vii

CONTENTS

Overview 1

I. Inflation and Real Sector Developments 3

Prices 3

Box Article: Developments in Global Food Prices and their Impact on Domestic Prices

8

Aggregate Demand and Supply 19

Labor Market Conditions 30

II. Monetary and Financial Conditions

31

Interest Rates 31

Financial Market Conditions 33

Banking System 35

Exchange Rate 39

Monetary Aggregates 42

Fiscal Developments 43

III. External Developments 44

IV. Monetary Policy Developments 50

V. Inflation Outlook 52

Private Sector Economists’ Inflation Forecasts BSP Inflation Forecasts

52

53

Risks to the Inflation Outlook 57

IVI. Implications for the Monetary Policy Stance 62

Summary of Monetary Policy Decisions 67

1

OVERVIEW3

Price pressures increased in Q1 2008. Average headline inflation rose to 5.6 percent from 3.3 percent in the previous quarter. Similarly, core inflation, an indicator of the long-term trend of inflation, increased during the review quarter to 4.1 percent from 2.4 percent in the previous quarter. Rising inflation pressures stemmed mainly from the higher international prices of oil and non-oil commodity products. Higher food prices, particularly of rice, continued to drive the trend of headline inflation.

Gross Domestic Product (GDP) increased by 7.4 percent in Q4 2007, maintaining the

growth rate (revised) in the previous quarter. This growth was faster compared to the 5.5 percent growth in the comparable period last year. The Q4 year-on-year performance was supported by household spending and capital investments. By major production sectors, services remained the key contributor to growth, accounting for more than half of total GDP growth. Other demand indicators similarly showed modest strengthening: employment increased, business confidence remained positive and consumer confidence improved, property prices rose and the vacancy rates of both residential and office spaces decreased, and volume sales of passenger cars, commercial vehicles, appliances, and electricity continued to grow. Similarly, external demand was stronger in Q4 relative to the same period in the previous year as reflected in the growth of exports.

Domestic interest rates displayed mixed trends in Q1 2008. Primary interest rates fell

while secondary market yields rose during the quarter. Rates were lower in the primary market for government securities as the National Government rejected some bids because of its stable cash position. Secondary market yields, however, rose on concerns of a prolonged slowdown in the US economy, and possibly the global economy, as well as the continued uptrend in international oil and food prices. The high inflation outturn during the first quarter of 2008 and worries about the possible knock-on effects on the Philippine economy of a US economic slowdown contributed to higher risk aversion.

Investor sentiment was cautious. The equity market was bearish, with weaker trading

reflecting investors’ cautious stance due to global economic concerns, rising inflation pressures and local political noise. In the market for government securities, oversubscription for T-Bills declined during the quarter. Meanwhile, the average monthly peso-dollar exchange rate depreciated in March relative to the levels in the previous two months as market uncertainty rose in February amid the turbulence in global financial markets.

Global financial markets continued to experience volatility during the review period.

The financial market strains have started to be felt in the real sector, with indicators pointing to a slowing down of the US, Euro area, and Japanese economies. In contrast, emerging Asian economies continued to expand, although they too are vulnerable to the effects of weak global growth particularly if the duration of the slowdown becomes longstanding. Meanwhile, the sustained elevated levels of oil and non-oil commodity prices have pushed up inflation in most parts of the world.

Domestic liquidity growth slowed down in February. Domestic liquidity or M3 grew by 6.6

percent year-on-year in February, lower than the 22.0 percent expansion recorded during the same month a year ago and the 9.0 percent growth as of end-December 2007. The slowdown in the growth of domestic liquidity can be traced to the decline in the net domestic assets (NDA) and the slowdown in the growth of net foreign assets (NFA). The tapering off of M3 growth is also seen to reflect in part the impact of the measures implemented by the BSP in May 2007.

3 The analyses in this report are based on information as of 31 March 2008.

2

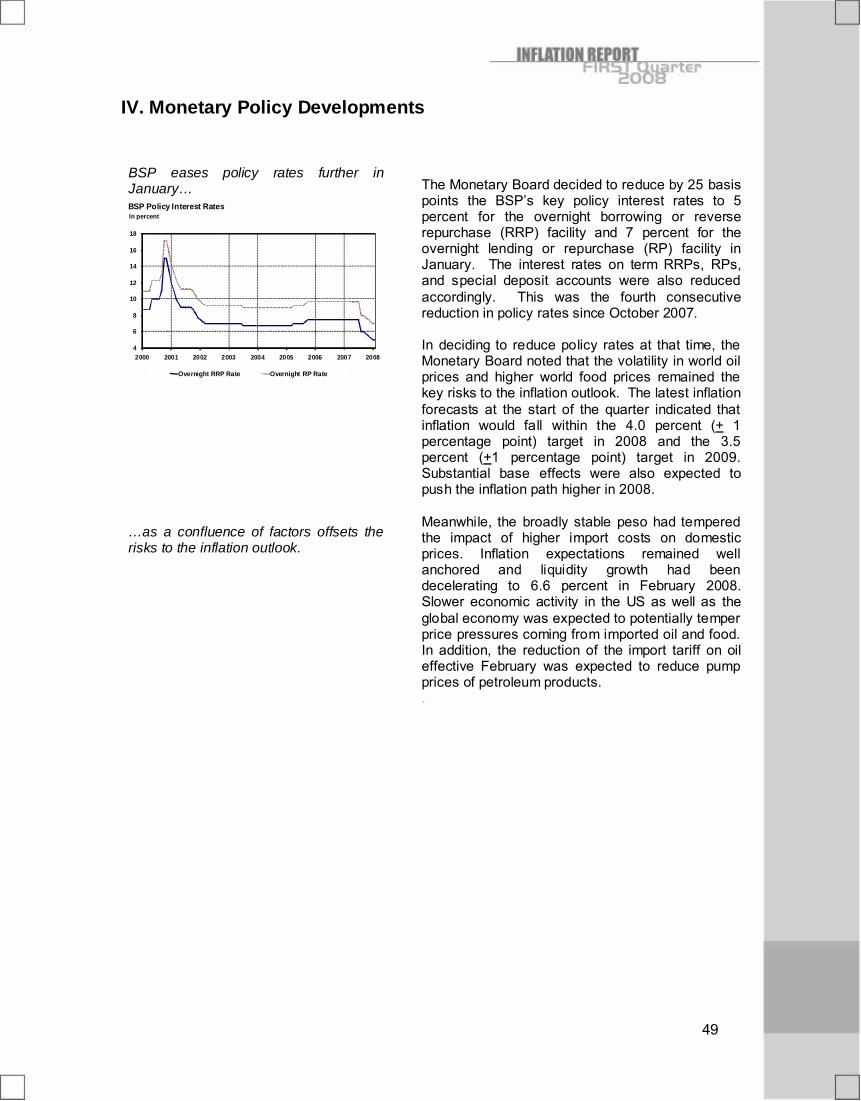

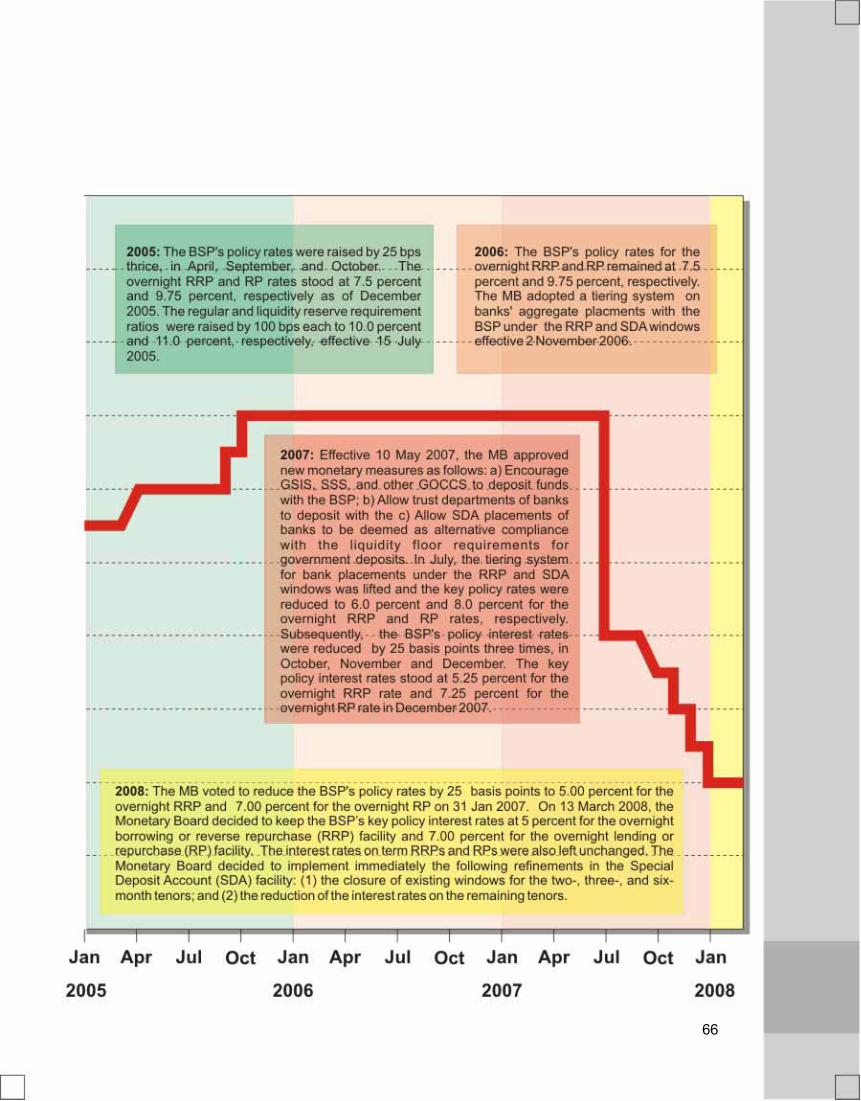

The BSP eased policy rates further during the quarter. The Monetary Board decided in January to reduce by 25 basis points the BSP’s key policy interest rates to 5 percent for the overnight borrowing or reverse repurchase (RRP) rate and 7 percent for the overnight lending or repurchase (RP) rate. This was the fourth consecutive reduction in policy rates since October 2007. In March, the Monetary Board fine tuned the Special Deposit Account (SDA) facility by: 1) closing the windows for the two-three- and six-month tenors; and 2) reducing the interest rates on the remaining tenors.

In its latest assessment, the Monetary Board noted that, depending on the movements

in oil and non-oil commodity prices, inflation could settle above the 2008 inflation target range but will be within the 3.5 percent ± 1.0 percentage point target range for 2009. The factors driving inflation have come mostly from the supply side and such pressures are also evident in other countries. While the balance of risks to the inflation outlook is tilted to the upside, price movements could return to manageable levels over the policy horizon as supply responses come on stream and prospects of a prolonged global economic slowdown moderate demand pressures.

[Subsequently, in April, the Monetary Board decided to keep the BSP’s key policy interest rates at 5 percent for the overnight borrowing or reverse repurchase (RRP) facility and 7 percent for the overnight lending or repurchase (RP) facility.]

3

I. INFLATION AND REAL SECTOR DEVELOPMENTS Prices

0

2

4

6

8

10

12

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Average headline inflation rose to 5.6 percent from 3.3 percent in the previous quarter. Similarly, core inflation, an indicator of the long-term trend of inflation, increased during the review quarter to 4.1 percent from 2.4 percent in the previous quarter. Rising inflation pressures stemmed mainly from the higher international prices of oil and non-oil commodity products. Higher food prices, particularly of rice, continued to drive the trend of headline inflation.

Headline and Core Inflation

Average headline inflation rose to 5.6 percent in Q1 2008 from 3.3 percent in the previous quarter and 2.9 percent in the same quarter a year ago. Of the 5.6 percent average headline inflation rate for Q1 2008, 3.4 percentage points were attributed to food alone. Services contributed 0.9 percentage point while housing and repairs contributed 0.5 percentage point. In terms of contribution to headline inflation, core inflation accounted for 3.5 percentage points of the headline inflation rate in Q1 2008, higher than 2.1 percentage points in Q4 2007 and 2.5 percentage points in the same quarter a year ago. Similarly, the contribution of non-core CPI items increased to 2.0 percentage points from 1.2 percentage points in the previous quarter; it was also higher than 0.4 percentage point in the same quarter a year ago.

Inflation strengthens in Q1 2008.

Q1 2008

Contribution to Quarterly InflationContribution to Quarterly Inflationin percent in percent

ItemItem Weight in Weight in Headline CPIHeadline CPI

Percentage Contribution to Percentage Contribution to YearYear--onon--Year Headline Year Headline

InflationInflationQ1 Q1

20082008Q4 Q4

20072007Q1 Q1

20072007Core Inflation 81.6 3.56 2.06 2.55Non-core Items 18.4 2.01 1.20 0.35

Rice 9.4 0.81 0.65 0.15Corn 0.9 0.05 0.02 0.06Fruits and Vegetables 5.3 0.56 0.18 0.20Gas, LPG 1.3 0.28 0.18 -0.06Kerosene 0.3 0.04 0.02 0.01Oil, Gasoline and Diesel 1.3 0.26 0.15 -0.01

Headline Inflation100.00 5.57 3.27 2.90

Source of Basic Data: NSO, BSP

Contribution to Quarterly InflationContribution to Quarterly Inflationin percent in percent

ItemItem Weight in Weight in Headline CPIHeadline CPI

Percentage Contribution to Percentage Contribution to YearYear--onon--Year Headline Year Headline

InflationInflationQ1 Q1

20082008Q4 Q4

20072007Q1 Q1

20072007Core Inflation 81.6 3.56 2.06 2.55Non-core Items 18.4 2.01 1.20 0.35

Rice 9.4 0.81 0.65 0.15Corn 0.9 0.05 0.02 0.06Fruits and Vegetables 5.3 0.56 0.18 0.20Gas, LPG 1.3 0.28 0.18 -0.06Kerosene 0.3 0.04 0.02 0.01Oil, Gasoline and Diesel 1.3 0.26 0.15 -0.01

Headline Inflation100.00 5.57 3.27 2.90

Source of Basic Data: NSO, BSP

4

-2

0

2

4

6

8

10

12

14

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Headline Inflation Food Inflation Non-food Inflation

Headline, Food and Non-food Inflation Quarterly average in percent (2000=100)

Both food and non-food inflation were higher compared to the previous quarter and the same quarter a year ago. Inflation for food, beverages and tobacco (FBT) increased to 7.0 percent in Q1 2008 from 4.1 percent in the previous quarter and 3.3 percent in the same quarter a year ago. Likewise, non-food inflation was higher at 4.2 percent relative to 2.6 percent in the last quarter and 2.5 percent in the same quarter a year ago.

0

2

4

6

8

10

12

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Headline Inflation Core Inflation

Headline and Core InflationQuarterly average in percent (2000=100)

Core inflation, an indicator of the long-term trend of inflation, increased during the review quarter. The official NSO core inflation measure rose to 4.1 percent in Q1 2008 from 2.4 percent in the previous quarter and 3.2 percent in the same quarter a year ago. Similarly, alternative measures of core inflation estimated by the BSP all went up in Q1 2008. The trimmed mean went up to 5.1 percent from 2.9 percent in the previous quarter and in the same quarter a year ago; the weighted median went up to 4.5 percent from 2.5 percent in the previous quarter and in the same quarter a year ago; and the net of volatile items measure went up to 4.6 percent from 3.0 percent in the previous quarter and in the same quarter a year ago.

Alternative Core Inflation MeasuresQuarterly averages of year-on-year change

Quarter TrimmedMean 1/

WeightedMedian 2/

Net of Volatile Items 3/ *

2006 5.4 5.0 6.9Q1 5.9 5.4 8.1Q2 5.8 5.0 7.6Q3 5.2 5.2 6.7Q4 4.5 4.2 5.0

2007Q1 2.9 2.5 3.0Q2 2.2 2.2 2.5Q3 2.3 2.1 2.5Q4 2.9 2.5 3.0

2008Q1 5.1 4.5 4.6

1/ The trimmed mean represents the average inflation rate of the (weighted) middle 70 percent in a lowest-to-highes t ranking of year-on-year inf lation rates for all CPI components .

2/ The weighted median represents the middle inflation rate (corresponding to a cumulative CPI weight of 50 percent) in a lowes t-to-highest rank ing of year-on-year inflat ion rates .

3/ The net of volat ile items method excludes the following items : educational serv ices, f ruits and vegetables, personal services, rentals, recreat ional services, rice, and corn.

* The series has been recomputed using a new methodology that is aligned with NSO’s method of comput ing the off ic ial core inf lation, which re-weights remaining items to comprise 100 percent of the core basket af ter excluding non-core items . The previous methodology retained the weights of volat ile items in the CPI basket while keeping their indices constant at 100.0 f rom month to month.

Source: NSO, BSP estimates

Looking at the distribution of price changes in the CPI basket, it would also be useful to determine the proportion of CPI basket components (at the 4-digit Philippine Standard Industry Classification (PSIC) level) showing inflation rates above a given threshold and find out whether that proportion has been increasing or decreasing. This would provide an indication as to whether pressures on consumer prices are becoming generalized over time.

Core inflation increases in Q1 2008.

Both food and non-food items register stronger price pressures.

5

The number of items with above-target inflation rates increases.

0

10

20

30

40

50

60

70

80

90

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1

2004 2005 2006 2007 2008

Cumulative Weight (in percent) Number of Items Exceeding Threshold Inflation

CPI Items with Inflation Above Threshold

As may be expected with higher inflation, the number of items with inflation rates greater than 5.0 percent, the upper end of the inflation target for 2008, increased to 55 in Q1 2008 from 28 in the previous quarter. Likewise, these items accounted for a bigger proportion of the CPI basket at 40.1 percent compared to 27.1 percent in the last quarter. Dividing the CPI basket into food and non-food components generates the same trend. There were 41 food items with inflation rates above threshold compared to 20 in the previous quarter. Meanwhile, 14 non-food commodities posted inflation rates higher than the threshold in the current quarter compared to 8 a quarter earlier.

6

Inflation Rates for Selected Food ItemsQuarterly averages in percent (2000=100)

Commodity2008 2007 Q1 Q4 Q3 Q2 Q1

Food, Beverage and Tobacco 7.0 4.1 2.9 2.7 3.3Food 7.2 4.1 2.9 2.6 3.3Cereal & Cereal Products 8.6 6.0 3.5 2.2 2.7o/w Rice 8.7 7.0 3.4 1.6 1.6

Corn 5.9 2.7 4.3 4.1 6.7Dairy Products 11.4 7.6 5.5 4.1 4.4Eggs 8.1 7.6 7.6 6.3 5.5Fish 7.8 3.8 2.6 3.3 3.4Fruits & Vegetables 10.6 3.4 1.7 2.8 3.8Meat 4.9 2.6 3.1 2.4 2.3Misc. Food 4.2 2.5 1.9 2.3 3.8Beverages 3.7 2.7 2.9 3.5 5.4Tobacco 3.1 2.5 2.4 2.1 2.2

Source of Basic Data: NSO, BSP

Food Prices Higher food prices have continued to dominate overall headline inflation for the past five quarters starting Q1 2007. In the past two quarters, this was mainly triggered by the elevated global prices of virtually all agricultural commodities, particularly dairy and cereals, including rice and wheat, on account of global supply and demand factors.4 Both processed and unprocessed foods registered increases in Q1 2008, but the developments in global commodity prices appeared to have had the most impact on processed foods particularly in cereal preparations and dairy products. All prices of food items rose, with cereals (particularly rice), fruits and vegetables, and fish recording the top contributions to quarterly inflation during Q1 2008. Rice, which constitutes 9.4 percent of the CPI basket, increased by 8.7 percent in Q1 2008 from 7.0 percent in the previous quarter. Domestic retail prices of rice increased sharply during this quarter, following the sudden spike in international rice prices during the same period. Domestic retail prices of ordinary and special rice increased in March 2008 year-on-year by 14.5 percent and 16.8 percent, from 8.4 percent and 9.0 percent in December 2007, respectively. Similarly, the All Rice Price Index (ARPI) from FAO had increased by 17 percent year-on-year in March 2008. Coupled with tight demand-supply conditions in global rice markets, the spillover effect from rising prices of other agricultural commodities has made the price increases for rice even more pronounced. Higher prices for wheat, for example, raise the demand for substitutes such as rice, pushing up the price of rice even further. The hoarding of rice, whether by consumers or speculators may also be exacerbating the hike in domestic rice prices.

4 See box article for a thorough discussion of the developments in international food prices.

Food prices continue to drive headline inflation.

7

In order to moderate the rise in rice prices, the government, through the DA, has implemented various programs to help alleviate the impact of the rice price increases on the poorest of the poor. For one, the National Food Authority (NFA) will carry out “supervised selling” of medium-priced commercial varieties in addition to NFA- subsidized rice as well as undertake measures to prevent the diversion of NFA rice to private warehouses and profiteering by rice traders. In addition, President Arroyo ordered the revocation of licenses of some 5,000 NFA retailers in the country to flush out hoarders and other erring grains traders. Meanwhile, a shortage of top-quality spring wheat in the US (the world’s largest wheat exporter) helped push up the domestic prices of flour, which is the primary ingredient for making bread and instant noodles (together accounting for 1.7 percent of the CPI basket). The price spikes in fruits and vegetables were traced mainly to base effects due to low price levels in 2007. The price of meat products also increased, due mainly to the rising costs of feeds and the tight domestic supply of beef and pork.

8

Box Article: Developments in Global Food Prices and their Impact on Domestic Prices Overview International food prices rose significantly in 2007 as income growth in emerging as well as developing economies, and the high demand for biofuel are redefining the pattern of food consumption and production globally. Since these structural changes are expected to affect food prices for years, developments in world food prices could become a major issue as monetary authorities worldwide are concerned that this may trigger higher food-based domestic inflation and inflation expectations. In addition to the spike in world oil prices, the rise in global food prices has already led to significant increases in domestic prices of several countries. Accelerating food and energy prices lifted inflation sharply throughout Asia, with headline inflation at its highest in 25 years in Singapore, almost 12 years in China, and nearly 10 years in Hong Kong and Taiwan. This prompted governments across the Asian region to use fiscal policy in response to these supply shocks. The fiscal measures include price subsidies, cuts in import duties, export restrictions and temporary price controls that cover basic goods, fertilizer, school and transportation fees, oil products, natural gas, and electricity. In Latin America, sharp increases in food prices also pushed Chile’s inflation to levels well above the tolerance range of its inflation target. Similarly, Brazilian inflation surged to 4.6 percent in February 2008 from 3.0 percent in the previous year, the first time since 2002 that inflation accelerated in Latin America's largest nation. In the euro area, higher food prices pushed year-on-year inflation to 3.3 percent in March 2008 from 3.2 percent in the previous month, the highest level in more than six years. Meanwhile, Russia’s inflation rate rose to 11.9 percent in 2007 from 9.0 percent in 2006, the highest in four years, even as the government cut dairy and vegetable oil import duties, sold grain from state reserves, and added a grain export duty. What is causing the surge in food prices? The dramatic increase in the prices of grains and edible oils over the past year was attributed mainly to the strong demand for biofuel, the rising prosperity in China and other emerging nations, and supply concerns following abnormal weather conditions in major agriculture-exporting countries. In 2007, the World Bank’s food price index was at its highest level since 1960 at 146.0 as prices of grains and edible oils—the commodity groups that are used heavily in biofuel production—increased significantly (Figure 1). Figure 1

9

Supply disruptions caused by bad weather, local cases of animal disease outbreaks and crop infestation also contributed to the spike in food prices over the past year. Global harvests were severely affected by the drought in major wheat-producing countries like Australia and Canada, while abnormal monsoon patterns affected rice production in Latin America and the Caribbean (LAC), Asia (Bangladesh, China, India, Indonesia, Philippines, and Nepal), Western Africa, and Southern Africa. In China, the outbreak of the “blue ear pig disease” drove up pork prices, igniting fears of a global pandemic as a similar virus has been detected in neighboring countries like Vietnam and Myanmar. The more recent trends in food prices and the supply and demand fundamentals in food products, however, are now affected by the income growth in emerging countries and the strong demand for biofuel following the renewed surge in crude oil prices. The following diagram illustrates the interplay of interrelated factors which affected global prices in 2007 and up to early 2008. Figure 2: Factors Affecting Global Food Prices

New Factors: Affluence in Asia, High Demand for Biofuel and Financial Trends With the rising incomes in China, India and other emerging economies, demand has shifted from grains and other staple crops to high-value food products such as meat and dairy products, resulting in higher demand for animal feeds. That, in turn, is stoking the demand for grains many times over since it takes more grains to produce a kilo of meat than to produce bread. On top of this, the growing demand for feed ingredients will push up the prices of grains further as it competes with the demand for biofuel raw materials. Ultimately, this leads to rapidly escalating prices of cereals, meat, poultry and dairy products.

10

The demand for biofuel has affected the prices of other food items as it competes with agricultural land needed for food production. Strong demand for biofuel has led more farmers to switch to more profitable crops used for biofuel production, such as barley for example. The reduction in land areas used for planting barley in favor of other crops used as biofuel feedstocks has brought down its supply, driving up the price of barley in 2007. Robust economic growth in the emerging markets is also indirectly linked with the demand for biofuel. The tight supply-demand condition in the oil market was in part triggered by the surge in demand for fuel from China and India, thus the call for alternative sources of fuel. The International Monetary Fund (IMF) attributes recent trends in the global financial market as one of the main drivers of the recent run-up in global commodity prices.5 Specifically, the dollar depreciation in 2007 has stimulated demand as it increased the purchasing power of consumers in the non-dollar region. The falling US dollar also made commodities a more attractive class of alternative assets. Speculative inflows toward the commodity market were also observed to have increased, leading to more volatility and escalating prices. Lastly, freight costs have risen because of high and volatile oil prices coupled with increasing global trade activity. All these factors combined have made food importation more costly, and have therefore contributed to higher food prices. The magnitude of the impact of these factors on food prices and the influence of the food price increases on headline inflation, however, vary across economies. In more developed countries, food accounts for only about 10 to 15 percent of the consumer price index (CPI) basket on average. By contrast, food has a bigger share (30 percent or more) in the CPI basket in many emerging market economies. In many developing Asian countries including the Philippines, it is 50 percent or more. Is Philippine inflation vulnerable to swings in international food prices? Recent developments in global food prices have spawned interest on the direct pass-through effects of the international price of food products on domestic inflation in the Philippines. This is in consideration of the fact that food accounts for 50 percent of the Philippine CPI basket. Evidence from past empirical studies for other countries are mixed. A considerable amount of literature point to small pass-through effects. Herrero and Thornton (1997), using cointegration and an error-correction model (ECM), concluded that world commodity prices seemed to have little predictive power in forecasting movements in domestic retail prices in the United Kingdom (U.K.), both in the long run and in the short run. They also found that there was little evidence of causality from world commodity prices to U.K. retail prices. The study noted that commodity price indices, particularly food, are inherently volatile in that they exhibit inflation variances that are many times larger than that of the consumer price index. Moreover, supply conditions in world food prices may deviate significantly from aggregate demand in an individual economy. Similarly, Boughton and Branson (1988), using ordinary least squares (OLS) and ECM found no stable long-run relationship between commodity prices and retail prices but suggested that in the short run, world commodity prices exhibited a signaling power on domestic inflation. Meanwhile, a number of studies which used unstructured vector autoregression (VAR) models yielded the following results:6

• Higher food prices, particularly in developing countries, seemed to be a significant determinant of non-food inflation through its indirect impact on the demand for higher wages (Cheng and Samiei, 2007); and

• World food commodity prices may be directly linked to broad inflation because these commodities are used as valuable inputs to production and should eventually be passed on to final goods’ prices. Large direct input price effects have historically been concentrated in food and energy commodities. Not surprisingly, food and oil, which are particularly sensitive

11

to major supply disruptions, appear to have more explanatory power in the link between commodity prices and consumer price inflation (Bloomberg and Harris, 1995).

Empirical Findings Staff estimates using both ordinary least squares and vector-autoregression indicate minimal direct pass-through. An error-correction model, however, yielded results that show a more significant impact of international food prices on domestic inflation. For some broad measure of long-run and short-run pass-through effects of imported food prices on domestic food prices, simple linear regression was used to derive the long-run effect while an error-correction representation was used to estimate the short-run impact. These relationships were represented as follows: Long Run:

LOG(CPIFBT) = c + α*LOG(GFINDEX) + β*LOG(FOREX) + γ*LOG(CPIFBT(-1)) Short Run:

D(LOG(CPIFBT)) = c + η*resid(-1) + α*D(LOG(GFINDEX)) + β*D(LOG(PCEFOOD(-1))) + γ*D(LOG(CPIFBT(-1))) where: CPIFBT = domestic food price index GFINDEX = Global Food Price Index FOREX = nominal peso-dollar exchange rate PCEFOOD = personal consumption expenditure on food Table 1. Summary of Results7

Coefficients (t-statistics)

Long-run Dependent variable: Domestic food price GFINDEX 0.06

(5.34) FOREX 0.05

(4.32) Lagged CPIFBT 0.91

(47.52) Adjusted R2 0.98 Short-run Dependent variable: Change in domestic food price ECM term -0.94

(-5.97) Change in GFINDEX 0.04

(1.83) Change in PCEFOOD 0.02

(2.81) Lagged change in CPIFBT 0.98

(13.00) Adjusted R2 0.56

The proposed specification passed all residual tests. All variables are expressed in logs, hence, coefficients are interpreted as elasticities. All regressors are significant at one percent level of significance.

The ECM results showed that a 1 percent increase in global food prices will lead to a 0.04 percent to 0.06 percent increase in domestic food prices. This implies that movements in global food prices have limited direct impact on domestic food prices and on domestic inflation. This could be because the share of imported food commodities to total demand based on the 2000 input-output (I-O) table is just 13.2 percent. This is consistent with the observation that the pass-through of import prices of commodities (particularly food and oil) to domestic inflation appears to have a stronger effect on

12

countries with a larger import share (Mc Carthy, 1999). However, with the recent surge in the global food index, the impact on domestic food inflation is expected to be more pronounced. In Q1 2008, for example, global food price index rose by 55.6 percent from the same period a year ago. This implies that the impact of the increase in global food index on domestic food inflation is estimated to be around 2.2 percentage points for Q1 2008 if the resulting coefficient from the ECM is applied.

Figure 3

To account for the disaggregated impact of international prices on the prices of the country’s three major food imports —cereals, feeds and dairy products — an unstructured VAR analysis was conducted. The objective of the VAR analysis is to capture the impact of increases in the import prices of various food products on domestic food inflation. Import prices of certain food products serve as a channel through which international food prices impact domestic food prices, and hence broad inflation. The VAR system has five endogenous variables: import price indices of cereals (CERIMP), feeds (FFEDS), and dairy (DAIRY), domestic food CPI (FOOD), and the nominal exchange rate (XRATE).8 A time trend is included to account for the trend decline in inflation. Two sets of statistics were used to assess the effect of import prices of these three major food imports on domestic food inflation. First, impulse responses to shocks on the import prices of each of these food imports were estimated over a two-year period (eight quarters). Second, variance decompositions were obtained to assess how much of the variance in the domestic prices of food and indices over the period can be attributed to variances in the imported food prices. Figure 4 displays the impulse responses9—from the VAR system of equations—of domestic food CPI to a shock in the import prices of cereals, feeds and dairy, which would reflect the movements in world food prices. The impact of a shock10 on the imported price of cereals is small, owing largely to low percentage share of imported cereals (11.2 percent) to domestic requirements. Similarly, the impact on domestic food inflation from a shock in the imported price of feeding stuffs is minimal.11 This may be attributed to the high corn sufficiency level of the Philippines at 88 percent as of 2007.12 On the other hand, a shock on the international price of dairy products has a relatively higher impact on domestic inflation, albeit the magnitude is also small. This is expected since almost 99 percent of the country’s dairy requirement is imported, but its weight in the CPI basket is only around 2.9 percent.13

Figure 4

13

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

1 2 3 4 5 6 7 8 9 10

Accumulated Response of D(FOOD(-1)) to D(CERIMP(-1))

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

1 2 3 4 5 6 7 8 9 10

Accum ulated Response of D(FOOD(-1)) to D(FEEDS(-1))

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

1 2 3 4 5 6 7 8 9 10

Accumulated Response of D(FOOD(-1)) to D(DAIRY(-1))

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

1 2 3 4 5 6 7 8 9 10

Accumulated Response of D(FOOD(-1)) to D(FOOD(-1))

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

1 2 3 4 5 6 7 8 9 10

Accum ulated Response of D(FOOD(-1)) to D(XRATE(-1))

Accumulated Response to Cholesky One S.D. Innovations ± 2 S.E.

In determining the extent to which these shocks account for the variances in domestic food price inflation over the horizon, the variance decomposition of the price variables was obtained. The variance explained by the import price of dairy 1 period after a shock is 6.1 percent. Over time, the explanatory power of dairy import prices increases and becomes more pronounced, averaging at about 12.0 percent 3 to 10 periods after the shock. This is higher than the variance explained by cereals and feeds, averaging at about 1.0 percent and 8.0 percent, respectively, throughout the horizon. Exchange rate variations also appear to be explaining only a small share of the fluctuations in domestic food prices, contributing only a range of about 2.4 to 3.6 percent. Table 2. Variance Decomposition of Domestic Food Inflation

Period Cereals Feeds Dairy Products Exchange Rate

1 0.581980 8.517446 6.069621 0.000000 2 0.818875 7.538437 11.44329 2.433805 3 0.846071 7.728077 12.06762 3.374878 4 0.934462 7.787152 12.25076 3.541627 5 0.967411 7.865361 12.22868 3.569854 6 1.016549 7.920535 12.22648 3.565776 7 1.044662 7.962701 12.22454 3.563065 8 1.069044 7.995840 12.22151 3.560886 9 1.087110 8.020940 12.22038 3.559067

10 1.101060 8.040426 12.21901 3.557764

14

In summary, the variance decompositions indicate that the influence of external factors appears to be modest in the initial periods after a shock, but persists and increases over a longer time period particularly with respect to dairy products that have a larger import share to domestic requirements. Conclusion The results of the OLS and VAR estimations show that the estimated direct pass-through effects of imported food prices on domestic food inflation are proportionally limited. In the unstructured VAR estimation, it was seen that the response of domestic food CPI to shocks in the import prices of cereals, feeds, and dairy is low. Meanwhile, the measure of short-run pass-through effects using the ECM showed that the sensitivity of food inflation is only at 0.04 percentage point for every one percent increase in the global food price index, while the long-run impact is estimated at 0.06 percentage point. However, it is important to emphasize that the global food index has increased rapidly over the past year and well into 2008, so that the total pass-through effect of global food prices on domestic food price movements has become more pronounced. Trends in commodity prices—particularly food and oil—bear close and diligent monitoring as these price indices contain forward-looking characteristics and have the ability to nudge up inflation expectations (Herrerro 1997) and even encourage speculative behavior as agents may view commodities as a useful hedge against inflation. Against this backdrop, there would be upward pressure on the price and wage-setting behavior of economic agents in response to the movement in domestic food prices. Another area for further study is the role of inflation expectations in the short-run relationship between international commodity prices and domestic food inflation as this may well be a relevant channel by which the surge in global food prices affects the domestic economy. Moreover, another area to consider is how to isolate the impact of exchange rate movements on prices of imported commodities and, ultimately, on domestic food CPI. The peso has helped moderate the pass-through effects of higher global food prices on domestic food inflation. However, given that food accounts for half of the Philippine CPI basket, the tight condition in the global food market will continue to exert pressure on domestic headline inflation. Thus, the risks posed by the rising global food prices will remain a long-term challenge for monetary authorities.

Bibliography: Bloomberg, S. and E. Harris, 1995, “The Commodity-Consumer Price Connection: Fact or Fable?” FRBNY Economic Policy Review, October 1995 Branson, W., and J. Boughton, 1988, “Commodity Prices as Leading Indicator of Inflation,” IMF Working Paper, WP/88/87 Cheng, K. and H. Samiei, 2007, “Who Is Harmed by the Surge in Food Prices?” IMF World Economic Outlook, October 2007. Green, H. Herrero, A. and J. Thornton, 1997, “World Commodity Prices as a Forecasting Tool for Retail Prices: Evidence From the United Kingdom,” IMF Working Paper, WP/97/70 Johansen, M., 1988, “Estimation and Hypothesis Testing of Cointegration Vectors in Gaussian

15

Vector Autoregressions,” Econometrica 59, no. 6:1551-80 McCarthy, J., 1999, “Pass-through of Exchange Rates and Import prices to Domestic Inflation in Some Industrialized Economies,” BIS Working Paper, November 1999

International Monetary Fund, World Economic Outlook, January 2008

16

Inflation Rates for Selected Non-Food ItemsQuarterly averages in percent (2000=100)

Commodity2008 2007 Q1 Q4 Q3 Q2 Q1

Non-Food Items 4.2 2.6 2.2 2.0 2.4Clothing 3.1 1.8 2.1 2.5 2.8Housing & Repairs 2.7 1.2 1.3 1.5 2.2Fuel, Light & Water 5.4 2.8 4.2 3.3 2.4

Fuel 16.8 10.1 0.8 3.5 -1.1Ligh t -1.8 -2.6 6.7 2.8 3.8Water 2.5 4.4 4.5 5.0 6.9

Services 5.9 4.3 2.1 2.1 2.8Transpo & Comm. 5.6 3.2 -1.1 -0.5 0.5Miscellaneous 2.0 1.3 1.4 1.6 2.1

Source of Basic Data: NSO, BSP

5

15

25

35

45

55

65

75

85

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Dubai Crude OilQuarterly average spot price in US dollars per barrel

Q1 2008 US$91.38

Non-Food Prices Non-food inflation reached its highest level since Q1 2007, driven mainly by fuel and the transportation and communication sectors. High global oil prices were directly reflected in the five rounds of increases in the domestic pump prices of gasoline products, kerosene and diesel oil in March. This, in turn, translated into higher price levels of fuel, and of transportation and communication services. The inflation rate of services, which accounts for 15.9 percent of CPI, was higher at 5.9 percent in Q1 2008 as against 4.3 percent in the previous quarter, and was considerably higher than the 2.8 percent registered in the same period last year. Meanwhile, all other non-food sub-components registered increases in their inflation rates during the quarter compared to a year ago and the previous quarter Energy Prices International oil prices averaged higher in Q1 2008 partly due to geopolitical tensions in oil-producing nations like Nigeria and Iraq. Supply disruptions due to the suspension of crude oil deliveries of Venezuela’s state petroleum company (Petroleos de Venezuela SA) to the biggest energy company in the US (Exxon Mobil) along with the unrest in Pakistan also pushed prices up. OPEC’s decision in its 5 March 2008 meeting to keep its output unchanged as well as speculative investment in the oil commodity market, driven by the weak US dollar, also supported high oil prices. Dubai crude oil reached an average of US$91.38 per barrel in Q1 2008, higher by 9.8 percent compared to the previous quarter’s average of US$83.19 per barrel.

Likewise, fuel and transportation costs push up non-food inflation.

International oil prices strongly rise.

17

Local pump prices of oil products are raised during the quarter.

6

11

16

21

26

31

36

41

46

51

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Premium Gasoline Diesel Oil

Local Retail Prices of Selected Oil ProductsPrice in pesos per liter

Mar P47.07

Mar P39.44

10

20

30

40

50

60

70

80

90

100

110

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Spot and Estimated Future Prices of Dubai Crude Oil* Price in US dollars per barrel

*Futures price derived using Brent crude futures data.

31 Mar 08

28 Dec 07

In the domestic market, pump prices of gasoline products increased by an average of P2.00 per liter while that of diesel oil increased by about P1.00 in Q1 2008 relative to the end of Q4 2007. The increase, however, was lower compared to that of the previous quarter. During the review quarter, prices of gasoline products and diesel oil were reduced once in February but increased five times in March. Meanwhile, the price of LPG decreased four times (three times in February and once in March) in Q1 2008. In response to escalating world oil prices which translated to higher domestic pump prices of petroleum products, the tariff on imported oil products was reduced from three percent in January to one percent in February, and then raised to two percent in March. Under the implementing guidelines, the tariff on imported oil products will be reduced to between 0-2 percent when oil prices reach the (revenue neutral) trigger price levels indicated by the Department of Finance (DOF). The actual oil prices with which the trigger price levels will be compared shall be based on the average price of oil during the first 15 days of the month. If the actual prices reach any of the trigger price levels, the Department of Energy shall issue a certification to DOF for the latter to implement the corresponding reduction in the oil import tariff. The estimated future price of Dubai crude oil, based on movements in Brent crude oil futures, suggested higher prices in 2008. Market fundamentals are projected to remain tight despite forecasts of slower global economic growth which could weaken demand for oil.

Outlook for world prices remains tight.

18

Power rates are higher in Q1. PSALM bids out 12 power plants, accounting for 42.8 percent of the capacity target set to be bidded out by 2009. The MWSS approves the rate increase of MWCI as a result of rate rebasing. Meanwhile, water rates of Maynilad are lower due to the higher discount in the FCDA charge.

Power Electricity rates were generally higher in the first quarter of 2008 as the National Power Corporation (NPC) reverted to its higher dry-season (semestral) rates for Luzon and Mindanao for the first half of the year in January. There was no increase in the rates for Visayas, as semestral rates only apply to regions with major hydroelectric power plants. The higher discount from the incremental currency exchange rate adjustment (ICERA) for Luzon has tempered the increase in the semestral rates by P0.11/kwh. Nonetheless, more pressures on electricity rates in the coming months are expected with the start of the summer season. This, however, may be tempered by the broadly steady peso and higher utilization of hydroelectric power plants with expectations of more rainfall due to La Niña even as weather conditions are forecast to normalize by June 2008. On the status of the privatization program, the Power Sector Assets and Liabilities Management Corporation (PSALM) had successfully bid out 12 plants (Tolomo, Agusan, Barit, Cawayan, Loboc, Pantabangan-Masiway, Magat, Masinloc, Calaca, and Ambuklao-Binga) as of Q1 2008. This translates to 1,855.5 MW operating capacity, or 42.8 percent of the 4,336 MW aggregate capacity target set for bidding by 2009. Water Water rates were higher in the first quarter of 2008 as the Manila Water Company, Inc. (MWCI) implemented a higher rate increase compared to the rate reduction of Maynilad. The Metropolitan Waterworks and Sewerage System (MWSS) approved the increase in the rate of Manila Water Company, Inc. (MWCI), following the rate rebasing. The rate hike was implemented on a staggered basis over the first three months of the year. The rebasing allowed for an average tariff increase of P4.00 per cubic meter, equivalent to a 20 percent increase from the average tariff as of December 2007.

19

Rate rebasing is done every five years to review the water concessionaire’s service improvement plan and evaluate the required capital investment to implement the plan. Meanwhile, Maynilad rates declined despite the increase in its basic charge as this was offset by the higher discount from the foreign currency differential adjustment (FCDA) charge. Residential water rate charged by Maynilad was lower by P1.30 per cubic meter in the first quarter.

Aggregate Demand and Supply Domestic economy grows by 7.4 percent in Q4

2007.

-3

-1

1

3

5

7

9

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

GDP GNP

GDP and GNP Growth Rates Annual Growth in Real Terms

* Data for 1995-2003 is based on the old series of the National Income Accounts (NIA) of the NSCB. The quarterly GDP data from Q1 2004-Q1 2007 has been revised by the NSCB as of May 2007. The revision involves the addition or re-estimation of source subsectors under business process outsourcing (BPOs), manufacturing, and construction.

Gross Domestic Product (GDP) grew by 7.4 percent in Q4 2007, maintaining the growth rate (revised) in the previous quarter but faster compared to the 5.5 percent growth in the comparable period in the previous year. On the expenditure side, GDP growth was boosted by household spending and capital investments. By major production sectors, services remained the key contributor to growth, accounting for more than half of total GDP growth. On the expenditure side, GDP growth was boosted by steady consumer spending and expanding capital investments. By major production sectors, services remained the key contributor to growth, as it grew at its fastest pace in 25 years at 9.0 percent. Industry and agriculture likewise expanded at a brisk pace, both rising by 5.8 percent from their year-ago growth of 3.6 percent and 1.7 percent, respectively. Seasonally-adjusted GDP accelerated to 1.8 percent in Q4 from 1.0 percent in the previous quarter. Full-year GDP growth was 7.3 percent, surpassing the Government’s full-year growth target of 6.1-6.7 percent.

The economy grows by 7.4 percent in Q4 2007.

20

Aggregate Demand Expenditures (by major economic sectors) PCE growth was robust, expanding by 6.3 percent in Q4 2007 from 5.8 percent in the same quarter last year. Higher household spending was supported by the low inflation environment, modest improvement in employment, and the surge in remittances from OFs. Nonetheless, household spending remained concentrated on necessities such as food, clothing, and utilities. Expenditures on food, which comprised over half of total PCE, rose faster at 6.6 percent. Household spending on beverages and miscellaneous items also registered higher growth rates relative to the previous year.

Government consumption accelerated further to 10.8 percent in Q4 2007 from 9.9 percent a year ago. This may be partly traced to the disbursement of government funds for infrastructure projects during the quarter. Supported by positive investor sentiments and the low and stable interest rate environment, investments rose further in Q4 2007, with investments in fixed capital posting a 10.3 percent growth, a significant improvement from the year-ago growth of 2.2 percent. The expansion was driven by the 17.6 percent surge in construction,14 particularly private construction, during the period.

Household and public sector spending boost aggregate demand.

-25-20-15-10-505

1015202530

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Govt. Spending Private Consumption Fixed Investment

Domestic Demand Annual Growth in Real Terms

2006

5.86.06.3Personal consumption9.96.710.8Government Consumption1.88.414.7Capital Formation2.29.210.3Fixed Capital Formation2.30.7-2.0Exports1.4-5.5-2.3Imports

Q4By expenditure item

Q3Q4

Source: NSCB

2007Sector

Economic PerformanceGrowth rate (in percent)

2006

5.86.06.3Personal consumption9.96.710.8Government Consumption1.88.414.7Capital Formation2.29.210.3Fixed Capital Formation2.30.7-2.0Exports1.4-5.5-2.3Imports

Q4By expenditure item

Q3Q4

Source: NSCB

2007Sector

Economic PerformanceGrowth rate (in percent)

21

Imports Based on the Balance of Payments (BOP) data, imports of goods rose by 14.6 percent year-on-year to US$15.5 billion in Q4 2007, an acceleration from both the previous quarter and the previous year. 15 All major commodity groups posted year-on-year increments during the review quarter. In particular, imports of mineral fuels and lubricants rose significantly by 58.6 percent to US$2.9 billion due to higher prices of petroleum crude and other mineral fuels and lubricants. Imports of consumer goods at US$1.3 billion also posted a hefty increase of 47.6 percent led by the increase in the procurement of rice, the rising cost of dairy products, and the robust demand for passenger cars and motorized vehicles. For 2007, merchandise imports increased at a slower pace of 8.1 percent from the 10.9 percent growth rate posted in 2006.

Imports of Goods (BOP data)Growth rate (in percent)

Commodity Group2007 2006

Q4 Q3 Q4Capital Goods 11.3 -3.7 -0.3Raw Materials & Intermediate Goods 3.1 4.7 6.1

Mineral Fuels & Lubricant 58.6 26.6 30.0Consumer Goods 47.6 28.6 17.1Total Imports1/ 14.4 7.9 7.5Conceptual and coverage

adjustments -15.2 -154.2 -44.4Total Imports, BPM5 14.6 8.9 8.3

1/ Include valuation adjustments to NSO dataSource: BSP

Imports of Goods (BOP data)Growth rate (in percent)

Commodity Group2007 2006

Q4 Q3 Q4Capital Goods 11.3 -3.7 -0.3Raw Materials & Intermediate Goods 3.1 4.7 6.1

Mineral Fuels & Lubricant 58.6 26.6 30.0Consumer Goods 47.6 28.6 17.1Total Imports1/ 14.4 7.9 7.5Conceptual and coverage

adjustments -15.2 -154.2 -44.4Total Imports, BPM5 14.6 8.9 8.3

1/ Include valuation adjustments to NSO dataSource: BSP

22

*Base year chosen was the earliest year for which data was available

Other Demand Indicators Other demand indicators similarly showed modest strengthening: 1) property prices increased and vacancy rates decreased; 2) sales of vehicles, power and appliances continued to grow; and 3) business confidence remained positive and consumer confidence improved. Property Prices • Based on estimates from Colliers International

Research, land values in Q4 2007 rose by 30.3 percent year-on-year for the Makati Central Business District (CBD) and 20.9 percent year-on-year for Ortigas Center. Quarter-on-quarter, the estimated land values in the Makati CBD and the Ortigas area were 5.5 percent and 4.0 percent higher, respectively. Colliers expects land values to rise further by 10.0 percent year-on-year in Q4 2008. Colliers further noted that the land value appreciation is expected to be tempered in 2008 and 2009 because of the massive potential supply of business process outsourcing (BPO) office space in 2009 across Metro Manila and the over-supply of residential condominium units in locations such as Fort Bonifacio where rents may be lower.16 Land values were about 60-70 percent of their 1997 levels in nominal terms, but only about one-third of their 1997 levels in real terms.

Vacancy Rates, Makati CBD (%)

2007 2006Forecast

2008Q4 Q3 Q4 Q4 Q1

Office 2.3 3.7 3.9 2.6 2.9Residential (3-bedroom

condominiums) 6.6 7.1 10.0 6.5 6.7

Source: Colliers International Research

Vacancy Rates • Office and residential vacancy rates in the

Makati CBD at 2.3 percent and 6.6 percent were lower in Q4 2007, respectively, compared to the previous quarter and year-ago levels. For Q1 2008, Colliers projects the office vacancy rate at 2.9 percent as office spaces being completed have already been pre-leased. For residential space, Colliers projects the Q1 2008 vacancy rate at 6.7 percent. For Q4 2008, Colliers expects the average office vacancy rate to settle at 2.6 percent, which is lower than the Q3 2008 forecast, while the residential vacancy rate is projected to remain at 6.5 percent with expectations that new office spaces would be quickly occupied during the year.

*Average Land Values, Makati CBD and Ortigas Real prices, based on CPI (1991=100) (in pesos per square meter)

0 50,000

100,000

150,000

200,000

250,000

300,000

1998 2001 2002 2003 2004 2005 2006 2007

Makati Ortigas

23

Rental Values

• Office rents in the Makati CBD increased by 25.6 percent year-on-year in Q4 2007 to an average of P795/sq.m. and are forecasted to rise further by 10.0 percent in Q4 2008. Rents for 3-bedroom condominium units rose by 14.0 percent year-on-year to P539/sq.m. in Q4 2007 and are expected to increase by 10.0 percent in Q4 2008.

• Office rental values continued to rise in Q4

2007 and have breached the 1997 levels for premium grade offices. In real terms, however, office rents are only 60 percent of the levels in 1997.

• Consistent with the data from Colliers

International Research, Makati CBD data from Jones Lang La Salle in Q3 2007 showed year-on-year increases in office and residential rents of around 30.0 percent and 33.0 percent (in peso terms), respectively. Jones Lang La Salle noted that the sustained growth of rentals in Makati CBD was driven mainly by the growing BPO industry.

• Colliers also reported that residential rents in

Rockwell and Fort Bonifacio as of Q4 2007 rose year-on-year by 4.6 percent to P636/sq.m. and 4.5 percent to P578/sq.m. Colliers expects residential rents in Rockwell and Fort Bonifacio to escalate by 10 percent and 5 percent, respectively, in 2008.

Office and Residential Rental Values Real prices, based on CPI (1995=100)(in pesos per square meter per month)

0 100 200 300 400 500 600 700 800 900

1,000

1998 2001 2002 2003 2004 2005 2006 2007

Office rental value Residential rental value

24

-100

-50

0

50

100

150

200

2003 2004 2005 2006 2007 2008Passenger Cars Commercial Vehicles

Sales of Passenger Cars and Commercial VehiclesYear-on-year change in percent

-80

-60

-40

-20

0

20

40

60

80

100

120

140

2003 2004 2005 2006 2007 2008

Sales of Trucks and BusesYear-on-year change in percent

Sales of Vehicles • Passenger car sales in January-February 2008

increased by 19.0 percent year-on-year, a turnaround from the 4.0 percent decline recorded in the comparable period last year. This was also higher than the 15.1 percent year-on-year growth registered in the first two months of the previous quarter. According to the Chamber of Automotive Manufacturers of the Philippines, Inc. (CAMPI), the increase in sales can be attributed to the promotional activities of car dealerships coupled with the introduction of new models. Meanwhile, total sales of passenger cars increased by 11.3 percent year-on-year in Q4 2007.

• Likewise, sales of commercial vehicles grew

although at a slower pace of 12.6 percent year-on-year in the first two months of the year from 28.7 percent a year ago and 33.7 percent in the comparable period in Q4 2007. Total commercial vehicle sales for the last quarter of 2007 registered a growth of 32.8 percent year-on-year.

• Meanwhile, sales of trucks and buses for the

first two months of Q1 2008 went down by 5.3 percent year-on-year compared to the 52.5 percent expansion in the same period last year and the 2.8 percent decline in October-November 2007. On a full-quarter basis, sales of trucks and buses posted a 6.2 percent decline year-on-year in Q4 2007.

25

-10

-5

0

5

10

15

2000 2001 2002 2003 2004 2005 2006 2007 2008

Meralco Power SalesYear-on-year change in percent

Power Sales • Energy sales by Meralco rose by 5.2 percent

year-on-year for the first two months of the year, up from 2.9 percent in the comparable period last year. However, this was slightly lower compared to the growth of 5.8 percent in the first two months of the previous quarter. The rise in energy sales can be attributed mainly to the favorable sales to all sectors particularly the commercial sector which accounts for more than 50 percent of the increase in sales. Meanwhile, energy sales growth for Q4 2007 reached 3.8 percent year-on-year.

-60

-50

-40

-30

-20

-10

0

10

20

30

40

J F M A M J J A S O N D J F M A M J J A S O N D J F

Appliance SalesYear-on-year change in percent

2006 2007 2008

Appliance Sales • Appliance sales surged by 19.9 percent year-

on-year in January-February 2008, more than double the 7.9 percent growth recorded in the same period a year ago. This was also slightly higher than the 19.6 percent year-on-year expansion in the first two months of the previous quarter. Total appliance sales in Q4 2007 registered a growth of 17.2 percent year-on-year.

75.0

76.0

77.0

78.0

79.0

80.0

81.0

82.0

83.0

84.0

85.0

2007 2008

Average Capacity Utilization for Manufacturing In percent

• Based on the NSO’s Monthly Integrated Survey of Selected Industries (MISSI), average capacity utilization in manufacturing was relatively steady for the sixth consecutive month at 80.2 percent in January 2008 from 80.1 percent in Q4 2007.

26

-15

-10

-5

0

5

2007 2008

Volume of Production Value of Production

Volume and Value Indices of Manufacturing Production year-on-year change in percent

• On a quarterly basis, the average growth rate of the value of production index (VAPI) in Q4 2007 remained negative at -4.2 percent from the -1.7 percent average growth rate in the previous quarter. Likewise, the VAPI continued its decline at a rate of 1.4 percent year-on-year in January 2008 from its declines of 1.3 percent in December 2007 and 0.5 percent a year ago.

• After posting a -4.0 percent average growth

rate in Q4 2007, the positive outturn in the January 2008 volume of production index (VOPI) may indicate a possible recovery in Q1 2008. The VOPI grew modestly by 0.5 percent year-on-year in January 2008 from 0.1 percent in December 2007 and a decline of 3.6 percent a year ago.

Business sentiment remains positive in Q1.

Business Expectations SurveyIndex 2008 2007

Q1 Q4 Q3 Q2 Q1

Business Outlook Index

Current Quarter 29.9 48.0 40.9 46.4 44.9

Next Quarter 41.0 40.9 53.0 44.7 49.4

Source: BSP

Business Expectations Survey • Business confidence remained positive but the

lower index point for the current quarter indicated that more firms expect a slowdown in business activity. The overall confidence index (CI) remained positive at 29.9 percent as respondent firms with a positive outlook continued to outnumber those with a negative outlook. This index, however, was lower compared to the levels in the previous quarter and a year ago by 18.1 index points and 15.0 index points, respectively.

• The lower index was attributed to the weakening in the outlook particularly of exporter firms.17 Expectations of weaker demand after the holiday season also contributed to the weaker business optimism. Firms cited the following factors for their cautious outlook: 1) production slack in the first quarter due to seasonality; 2) concerns over a possible recession in the US economy; 3) reduced competitiveness of exports due to the peso appreciation; 4) unabated increase in crude oil prices; and 5) local political noise.

• Nonetheless, respondents believed that

business activity would be upbeat in Q2 2008 as the survey registered a higher confidence index of 41.0 percent, since consumer expenditures usually pick up during the summer season and the school year opening.

27

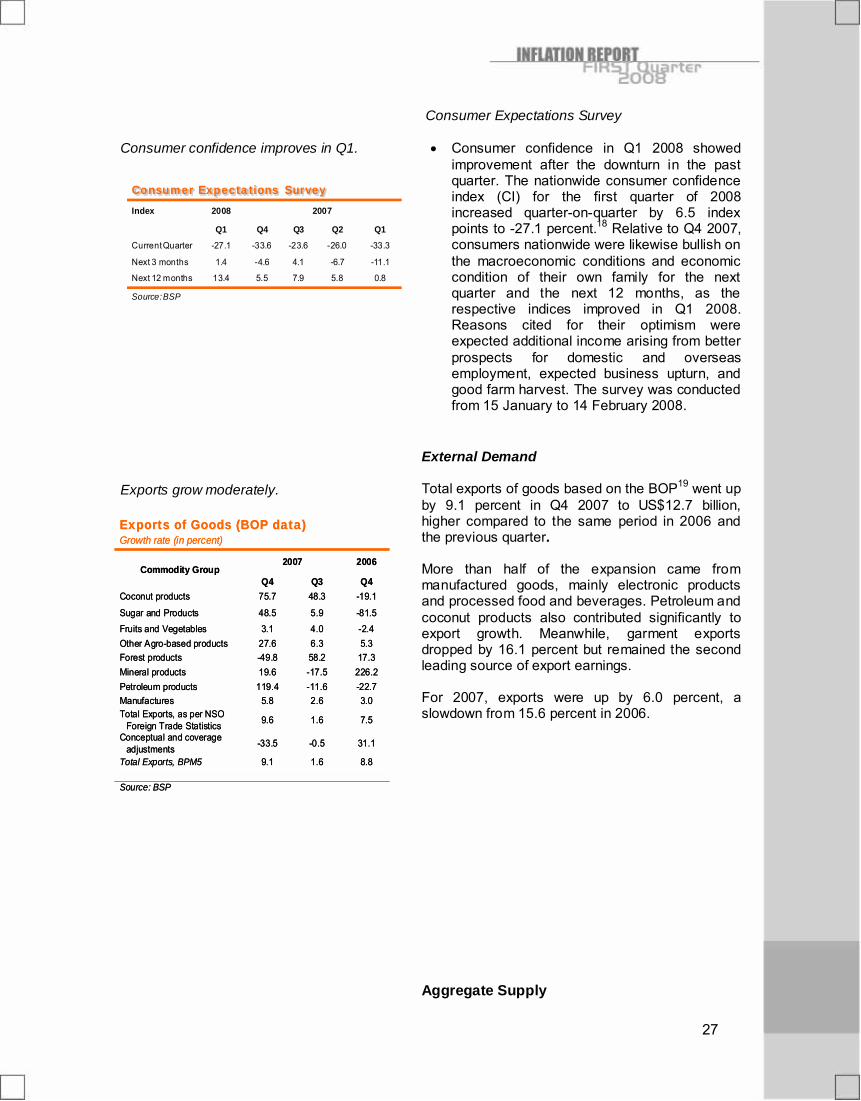

Consumer confidence improves in Q1.

Consumer Expectations SurveyIndex 2008 2007

Q1 Q4 Q3 Q2 Q1

Current Quarter -27.1 -33.6 -23.6 -26.0 -33.3

Next 3 months 1.4 -4.6 4.1 -6.7 -11.1

Next 12 months 13.4 5.5 7.9 5.8 0.8

Source: BSP

Consumer Expectations Survey • Consumer confidence in Q1 2008 showed

improvement after the downturn in the past quarter. The nationwide consumer confidence index (CI) for the first quarter of 2008 increased quarter-on-quarter by 6.5 index points to -27.1 percent.18 Relative to Q4 2007, consumers nationwide were likewise bullish on the macroeconomic conditions and economic condition of their own family for the next quarter and the next 12 months, as the respective indices improved in Q1 2008. Reasons cited for their optimism were expected additional income arising from better prospects for domestic and overseas employment, expected business upturn, and good farm harvest. The survey was conducted from 15 January to 14 February 2008.

Exports grow moderately.

External Demand Total exports of goods based on the BOP19 went up by 9.1 percent in Q4 2007 to US$12.7 billion, higher compared to the same period in 2006 and the previous quarter. More than half of the expansion came from manufactured goods, mainly electronic products and processed food and beverages. Petroleum and coconut products also contributed significantly to export growth. Meanwhile, garment exports dropped by 16.1 percent but remained the second leading source of export earnings. For 2007, exports were up by 6.0 percent, a slowdown from 15.6 percent in 2006. Aggregate Supply

Exports of Goods (BOP data)Growth rate (in percent)

Commodity Group2007 2006

Q4 Q3 Q4Coconut products 75.7 48.3 -19.1

Sugar and Products 48.5 5.9 -81.5Fruits and Vegetables 3.1 4.0 -2.4Other Agro-based products 27.6 6.3 5.3Forest products -49.8 58.2 17.3Mineral products 19.6 -17.5 226.2Petroleum products 119.4 -11.6 -22.7Manufactures 5.8 2.6 3.0Total Exports, as per NSO

Foreign Trade Statistics 9.6 1.6 7.5

Conceptual and coverage adjustments -33.5 -0.5 31.1

Total Exports, BPM5 9.1 1.6 8.8

Source: BSP

Exports of Goods (BOP data)Growth rate (in percent)

Commodity Group2007 2006

Q4 Q3 Q4Coconut products 75.7 48.3 -19.1

Sugar and Products 48.5 5.9 -81.5Fruits and Vegetables 3.1 4.0 -2.4Other Agro-based products 27.6 6.3 5.3Forest products -49.8 58.2 17.3Mineral products 19.6 -17.5 226.2Petroleum products 119.4 -11.6 -22.7Manufactures 5.8 2.6 3.0Total Exports, as per NSO

Foreign Trade Statistics 9.6 1.6 7.5

Conceptual and coverage adjustments -33.5 -0.5 31.1

Total Exports, BPM5 9.1 1.6 8.8

Source: BSP

28

Major production sectors, led by services, boost output growth in Q4.

On the production side, GDP growth was boosted by services which registered a 9.0 percent expansion in Q4 2007 following the acceleration in the growth registered by trade, transportation, communication and storage (TCS), and private services relative to the same period in the previous year. Retail trade also remained strong, supported by brisk sales from the newly-opened malls and hypermakets all over the country. Meanwhile, private services accelerated in the fourth quarter due to the robust expansion in the tourism industry. The growth of other services sectors including hotels and restaurants, recreational services, medical and health services, and educational services also accelerated in the fourth quarter compared to the same period in the previous year. Meanwhile, industry growth at 5.8 percent was supported by the stronger growth in mining and quarrying, construction, and electricity, gas and water sectors. The turnaround in mining and quarrying from the 25.1-percent decline a year ago to the 27.7 percent expansion in Q4 2007 was due to the upsurge in gold mining and other non-metallic minerals, particularly coal. The higher production of coal can be attributed to the rising demand for coal both in the local and international market as an alternative fuel source following the rise in the cost of crude oil. Likewise, boosted by the growing demand for both residential and commercial space, construction posted a robust growth of 18.4 percent during the quarter. Favorable weather conditions during Q4 2007 boosted growth in agriculture, fishery and forestry (AFF), which accelerated to 5.8 percent from 1.7 percent in the same quarter in the previous year. Growth in AFF during the period, which accounted for 18.3 percent of total GDP, was driven by the palay, other crops, fishery, corn, and banana subsectors.

Agriculture sustained its growth in Q4 2007 notwithstanding the destruction brought by typhoons that visited certain areas of the country during the quarter as a result of the ongoing La Niña phenomenon which started in August 2007. According to the DA, agricultural production will be supported by the anticipated rise in public spending on irrigation and other infrastructure, postharvest facilities, research and development (R&D), and agricultural extension work. The palay subsector surged by 10.1 percent in Q4

8.48.78.8Private services

8.48.49.0Services7.05.87.1Transport., Comm., & Storage8.110.910.7Trade

15.69.013.3Finance6.66.95.4O. Dwellings & real estate

-25.122.227.7Mining and quarrying4.83.72.5Manufacturing 7.618.518.4Construction4.58.410.6Electricity, gas and water

6.14.33.9Government services

8.6-1.68.4Forestry 1.75.85.8Agriculture and Fishery

2006

1.75.85.8Agriculture, Fishery & Forestry

3.66.65.8Industry

Q4

By industrial origin

Q3Q4

Source: NSCB

2007Sector

Economic PerformanceGrowth rate (in percent)

8.48.78.8Private services

8.48.49.0Services7.05.87.1Transport., Comm., & Storage8.110.910.7Trade

15.69.013.3Finance6.66.95.4O. Dwellings & real estate

-25.122.227.7Mining and quarrying4.83.72.5Manufacturing 7.618.518.4Construction4.58.410.6Electricity, gas and water

6.14.33.9Government services

8.6-1.68.4Forestry 1.75.85.8Agriculture and Fishery

2006

1.75.85.8Agriculture, Fishery & Forestry

3.66.65.8Industry

Q4

By industrial origin

Q3Q4

Source: NSCB

2007Sector

Economic PerformanceGrowth rate (in percent)

29

2007 from a decline of 2.0 percent in the same period of 2006, due to the sustained usage of hybrid and high quality inbred seed and favorable weather conditions. Corn continued to grow at 15.7 percent from 16.0 percent in the same quarter in the previous year as it benefited from the sustained rainfall and usage of open-pollinated varieties (OPV) and hybrid seeds through the DA-GMA Corn Program. Higher demand for yellow corn by seed millers was also noted in SOCCKSARGEN, Northern Mindanao, Davao, and Zamboanga Peninsula. Despite the favorable palay production, however, domestic rice prices increased sharply in Q1 2008, influenced partly by the surge in imported rice prices which are now at historic highs. Contributing further to the increase in domestic rice prices is the rise in farm gate prices of palay coming from the provinces, attributed to higher fertilizer, fuel, and irrigation costs. Amid rising international prices of rice and other agricultural products, the DA is pushing for a concerted effort by all sectors to sustain the growth momentum of the farm sector in 2008 and onwards in the face of looming downward supply trends following the recent tightening in global supply and surging prices of commodities. In particular, the DA is pushing for the introduction of productivity-enhancing technologies and the construction of irrigation and postharvest facilities to improve farm productivity in the medium term.

30