IMPLEMENTATION OF INTUIT QUICKBOOKS IN PT. TRISAN …

119

IMPLEMENTATION OF INTUIT QUICKBOOKS IN PT. TRISAN PAKAR BAJA SKRIPSI Presented in partial fulfillment of the requirements for The Bachelor’s Degree in Accounting By Roy Bratakusuma Uni 008201500027 FACULTY OF BUSINESS ACCOUNTING STUDY PROGRAM PRESIDENT UNIVERSITY Cikarang Baru – Bekasi 2018

Transcript of IMPLEMENTATION OF INTUIT QUICKBOOKS IN PT. TRISAN …

IMPLEMENTATION OF INTUIT QUICKBOOKS IN

PT. TRISAN PAKAR BAJA

SKRIPSI

Presented in partial fulfillment of the requirements for The Bachelor’s

Degree in Accounting

By

Roy Bratakusuma Uni

008201500027

FACULTY OF BUSINESS

ACCOUNTING STUDY PROGRAM

PRESIDENT UNIVERSITY

Cikarang Baru – Bekasi

2018

ii

PLAGIRSM DOCUMENT

iii

iv

v

ACKNOWLEDGEMENT

All gratitude and praises to The Almighty God, with all God’s blessings so the researcher

finally able to complete the thesis with entitled” Implementation of Intuit Quickbooks in

PT. Trisan Pakar Baja” as one part of the fulfilments to graduate as Bachelor Degree of

Science in Accounting.

I would like to give special gratitude toward the several people that always provide support

for me from the beginning until the end of this thesis.

1. Mrs. Andi Ina Yustina, M.Sc.,CMA as Head of Accounting Study Program

President University. I would like to express my gratitude for Mrs. Ina for the

motivation, support, and encouragement and provide me the best advisor that can

guide from beginning until completing my thesis.

2. I would like to express my sincere gratitude to my advisor, Mrs. Setyarini Santosa,

SE.,MAFIS.,Ak for the support, her advice, motivation, patience, knowledge, and

encouragement. Her guidance helped me in writing and completing this thesis.

3. Deepest gratitude goes to my parents, Fransiskus Ateng Uni and Linda Susanti, my

sister, Christine Angelia. Thank you for all the support and prayer that has been

given to me. Without them, I would not be able to go through many hard times.

4. Thank you to my friends, Fernando Van Wis Lee, Robin, Billy Sutanto, Kevin

Marcelius, Richard Wijaya, Jonathan Hardi, and Ignatius Maria for always remind

me to finishing my thesis, and give me motivation also spirit to do this research.

5. Finally for all the other parties that I could not mention one by one who help and

support me during the thesis writing process. May God gives the blessings.

vi

RECOMMENDATION LETTER FROM THESIS ADVISOR

This thesis is prepared and submitted by

Name : Roy Bratakusuma Uni

Student ID : 008201500027

Faculty : Business

Study program : Accounting

Field of study : Management Accounting

Thesis title :

IMPLEMENTATION OF INTUIT QUICKBOOKS IN PT. TRISAN PAKAR

BAJA

has been reviewed and found to have satisfied the necessities for oral defense as

partial fulfillment of the requirements for the Bachelor’s Degree in Accounting.

Cikarang, 13th December 2018

Bekasi, Indonesia

Acknowledged

Head of the Accounting Study Program Thesis Advisor

(Andi Ina Yustina, M. Sc.,CMA) (Setyarini Santosa, SE.,MAFIS.,Ak)

vii

TABLE OF CONTENTS

SKRIPSI TITLE….................................................................................................i

PLAGIARISM DOCUMENT……………………………………….......………ii

DECLARATION OF ORIGINALITY……………….....………………….......iii

PANEL OF EXAMINERS APPROVAL SHEET……………………………..iv

ACKNOWLEDGEMENT...…………………………………………….….........v

RECOMMENDATION LETTER FROM THE THESIS ADVISOR………..vi

TABLE OF CONTENTS………………………………………….……….…...vii

LIST OF FIGURES……………………………………………………….….…..x

LIST OF TABLES..……………………………………………………………xiii

ABSTRACT…………………………………………………………….......…...xv

INTISARI……………………………….………………………………...…….xvi

CHAPTER I INTRODUCTION………………………………………………...1

1.1 Research Background…………………………………...…………1

1.2 Problem Identification and Statement…...........................................6

1.3 Research Scope and Limitation……………………………………9

1.4 Research Objectives……………………………………………...10

1.5 Research Benefits………………………………………………...10

1.5.1 For The Researcher…………………………………………10

1.5.2 For The Future Researcher………………………………….11

1.5.1 For PT Trisan Pakar Baja…………………………………...11

1.6 Research Method…………………………………………………11

1.6.1 Interview……………………………………………………11

1.6.2 Observation………………………………………………...11

1.6.3 Documentation……………………………………………..12

1.6.4 Tracing……………………………………………………..12

1.6.5 Vouching…………………………………………………...12

1.6.6 Conversion…………………………………………………12

CHAPTER II LITERATURE REVIEW………………………………………13

2.1 Faithful Representation as Fundamental Quality of Financial

viii

Statement………………………………………………………..13

2.2 Timeliness in Financial Reporting……………………………....14

2.3 Manual Accounting Process and Computerized Accounting

Process…………………………………………………………15

2.4 Intuit Quickbooks…………………………………………..…..16

CHAPTER III DATA PROCESSING METHOD AND COMPANY'S

EXISTING CONDITION……………………………………..18

3.1 Data Collecting and Processing………………………………….18

3.1.1 Interview…………………………………………………..18

3.1.2 Observation……………………………………………….20

3.1.3 Documentation……………………………………………24

3.2 Company's Existing Condition…………………………………..26

3.2.1 History of PT. Trisan Pakar Baja………………………….26

3.2.2 PT. Trisan Pakar Baja's Operation………………………...27

3.2.3 PT. Trisan Pakar Baja's Organization Structure…………..28

3.2.4 PT. Trisan Pakar Baja’s Accounting Activities……………29

3.3 Consideration of PT. Trisan Pakar Baja Accepting Adoption of

Intuit Quickbooks……………………………………………….30

CHAPTER IV ANALYSIS AND EVALUATION…………………………….32

4.1 Faithful Representation Checking in PT. Trisan Pakar Baja……..33

4.2 Faithful Representation (Free From Error) Issue in PT. Trisan Pakar

Baja……………………………………………………………...44

4.2.1 Proposed and Implemented Solution……………………...46

4.3 Timeliness Issue in Generating Monthly Financial Report………51

4.3.1 Proposed and Implemented Solution……………………...52

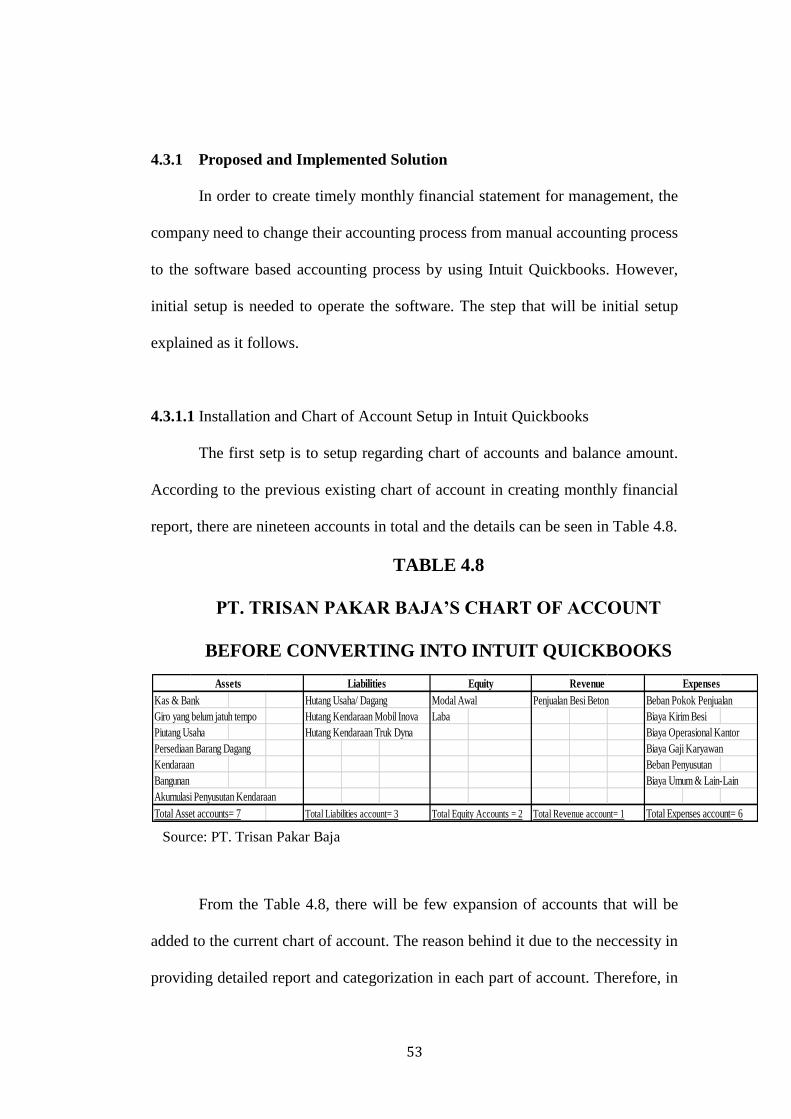

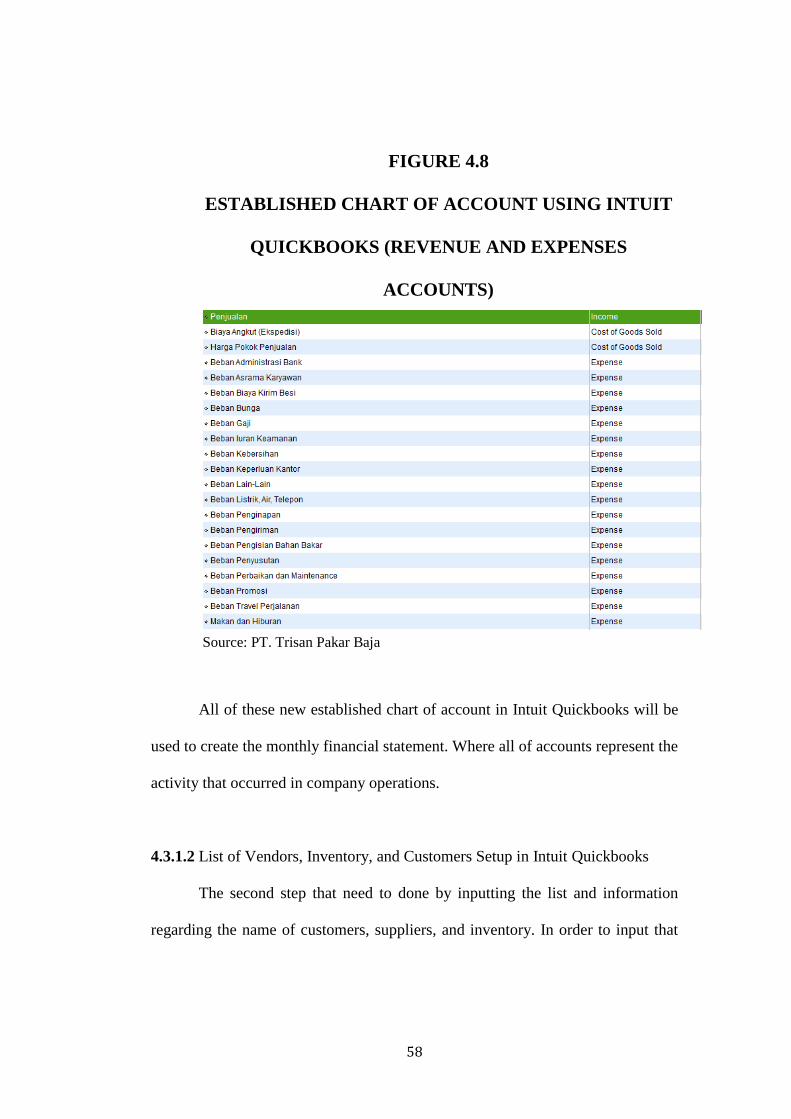

4.3.1.1 Installation and Chart of Account Setup in Intuit

Quickbooks ………………………………………53

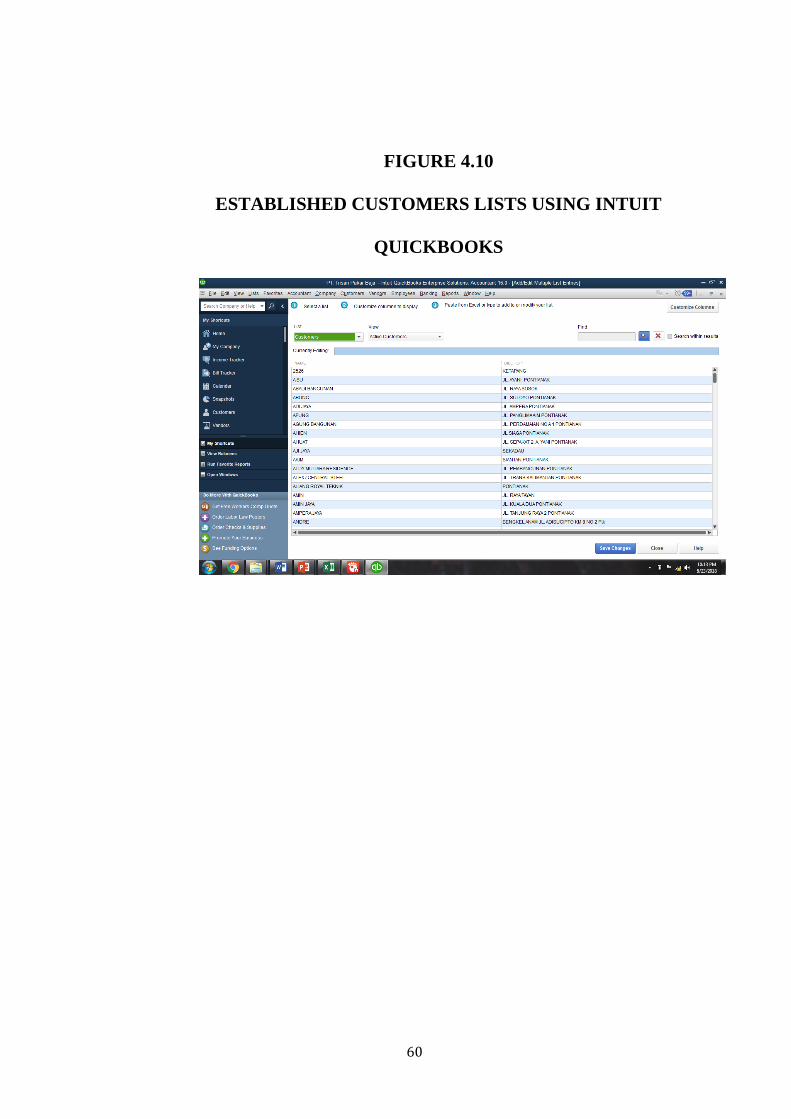

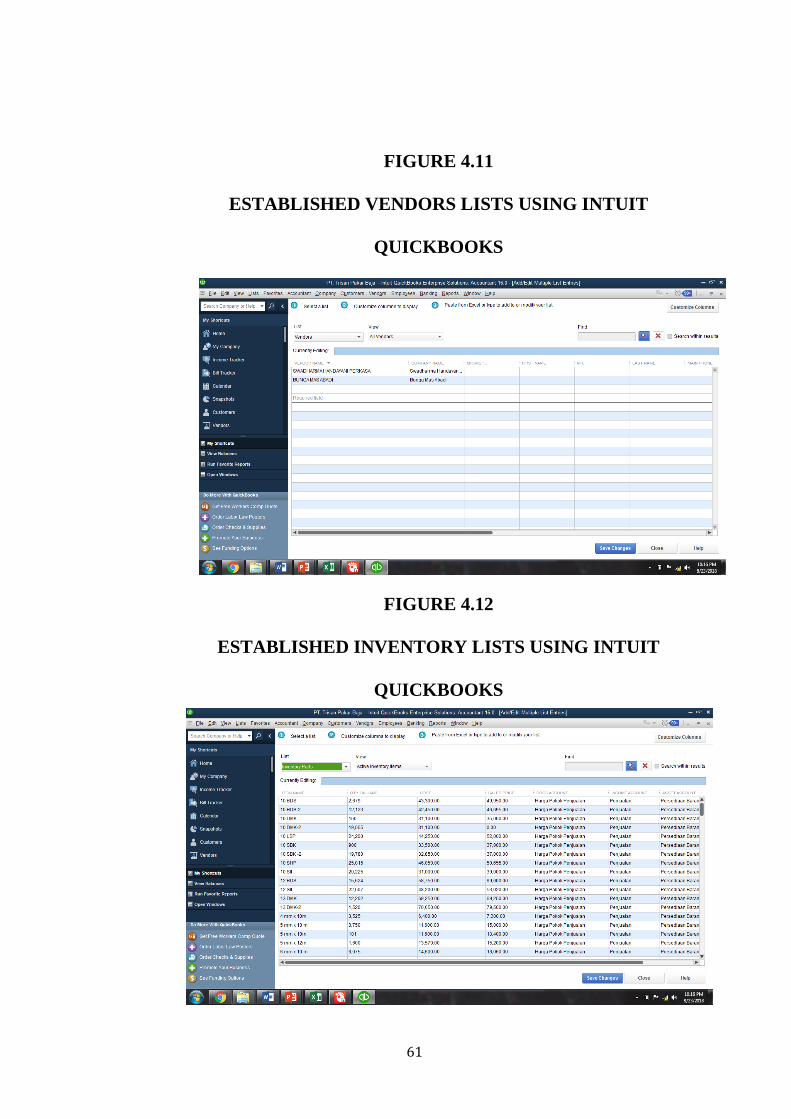

4.3.1.2 List of Vendors, Inventory, and Customers Setup in

Intuit Quickbooks ………………………………..57

4.3.1.3 Balance Amount and Accounting Period Setup in

ix

Intuit Quickbooks………………………………...61

4.3.1.4 Generalization of Inputting The Transactions in Intuit

Quickbooks ………………………………………63

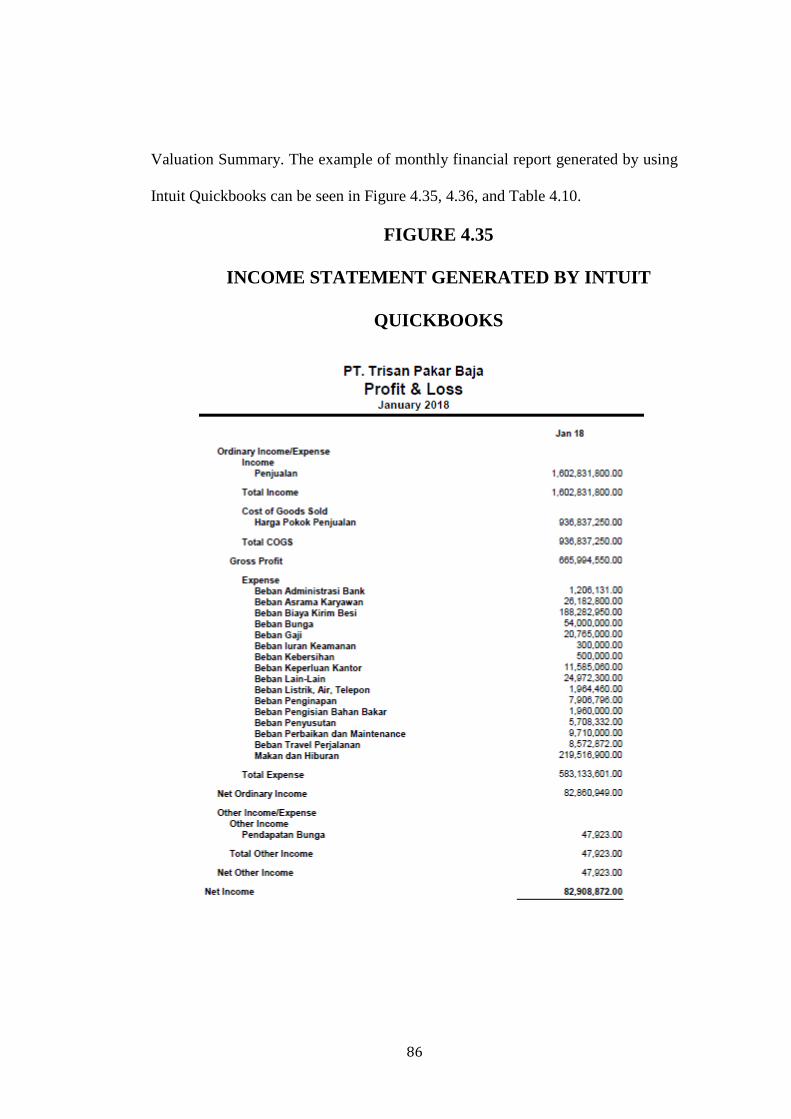

4.3.1.5 Creating Financial Statement in Intuit Quickbooks .84

CHAPTER V CONCLUSION AND RECOMMENDATION………………..93

5.1 Conclusion……………………………………………………….93

5.2 Recommendation………………………………………………...94

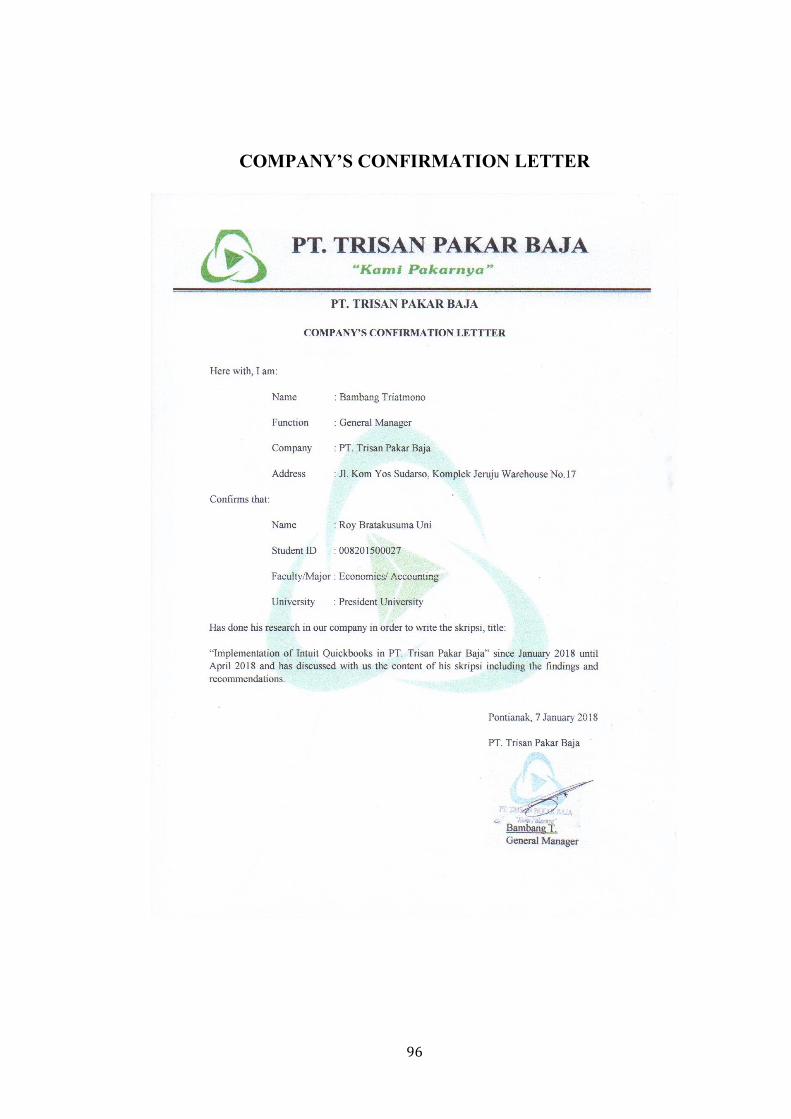

COMPANY'S CONFIRMATION LETTER………………………………….95

REFERENCES………………………………………………………………….96

APPENDICES…………………………………………………………………..98

x

LIST OF FIGURES

Figure 1.1 The Recorded Journal of Vehicle Acquisition by Credit (In Rupiah) ...... 3

Figure 1.2 The Value of Vehicle Fixed Assets Acquired (In Rupiah) ....................... 4

Figure 3.1 Monthly Income Statement PT. Trisan Pakar Baja December 2017 ...... 22

Figure 3.2 Monthly Statement of Financial Position PT. Trisan Pakar Baja December

2017 ........................................................................................................ 23

Figure 3.3 Illustration of The Invoice of Vehicle Acquisitions ............................... 25

Figure 3.4 Illustration of Inventory Bill of Ladding ................................................ 26

Figure 3.5 PT. Trisan Pakar Baja Organization Chart ............................................. 29

Figure 4.1 Company’s Problem Framework ............................................................. 33

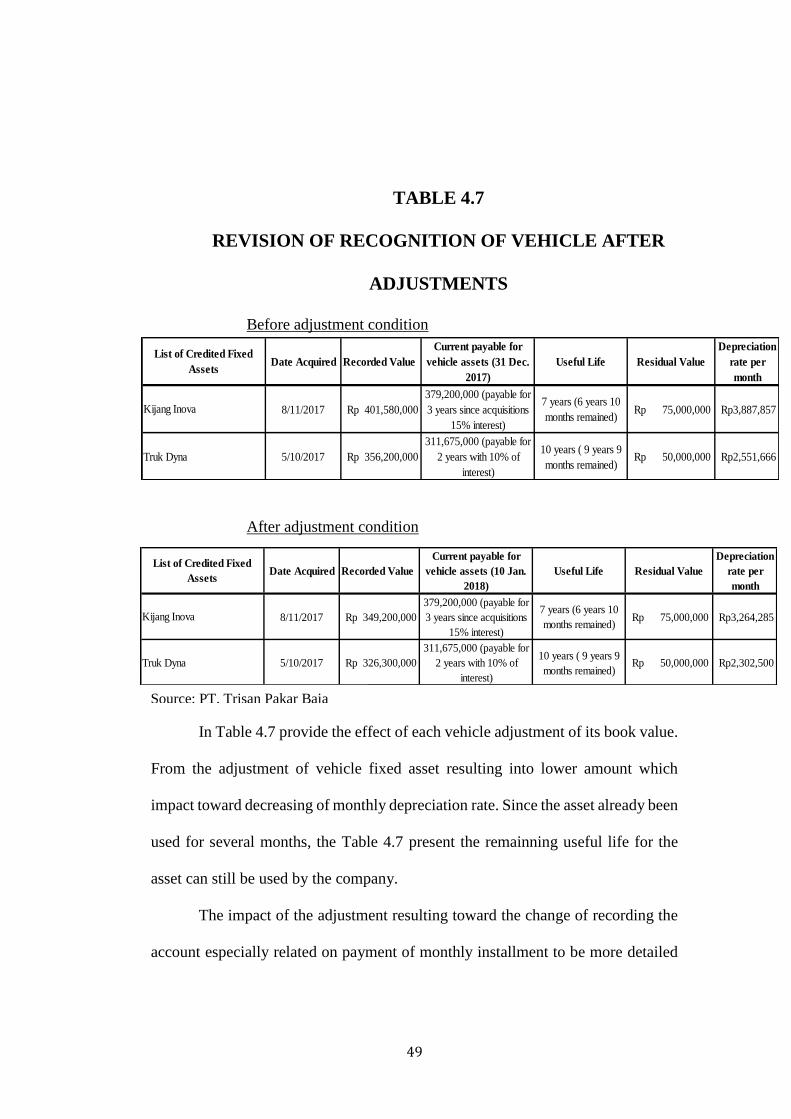

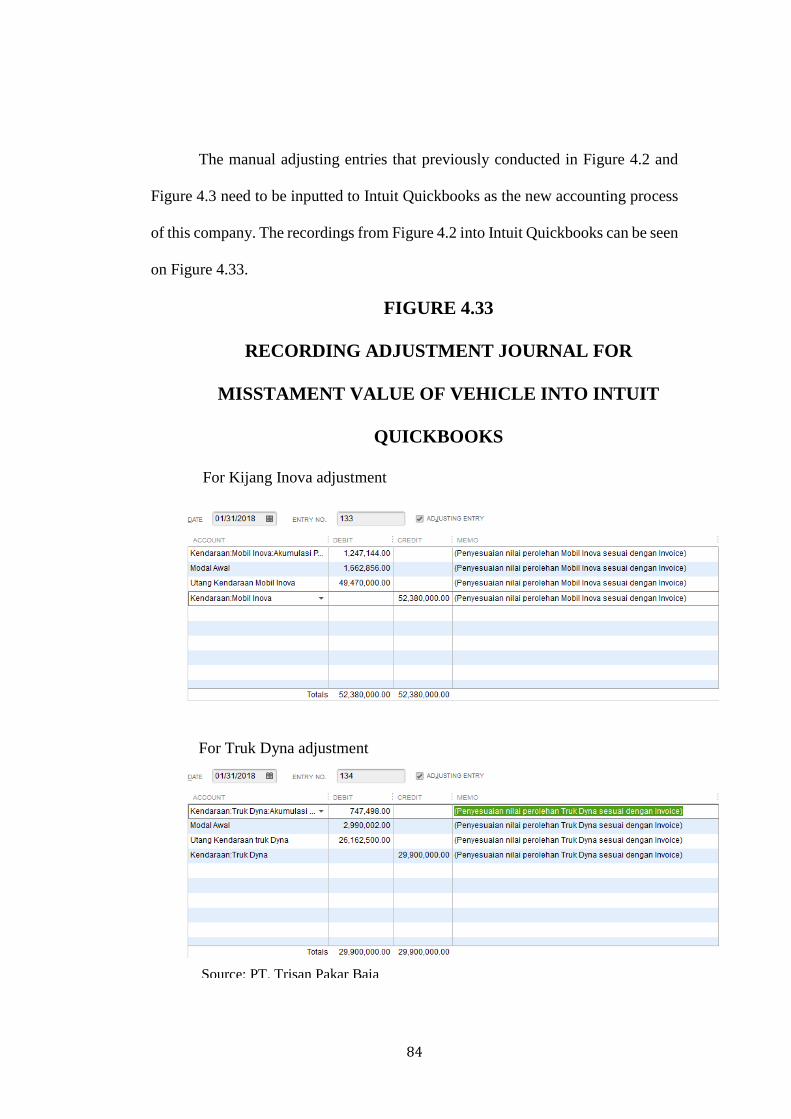

Figure 4.2 Adjustment Journal for Mistatement Value of Vehicle .......................... 47

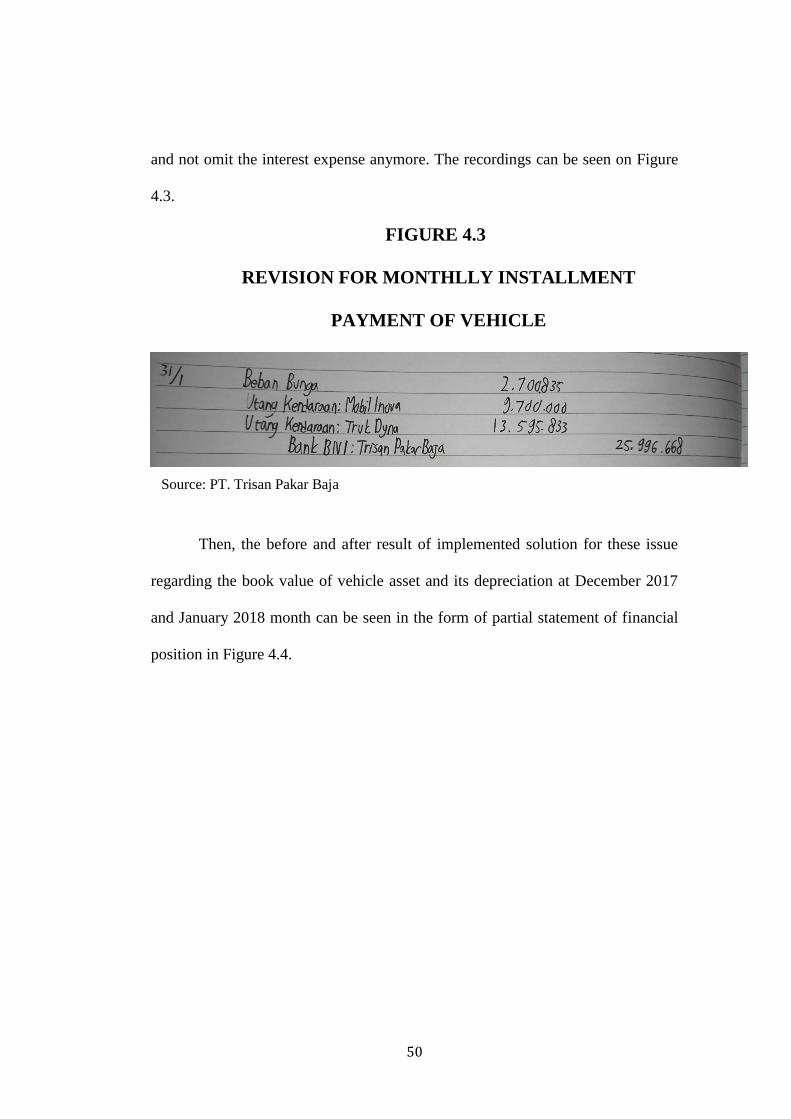

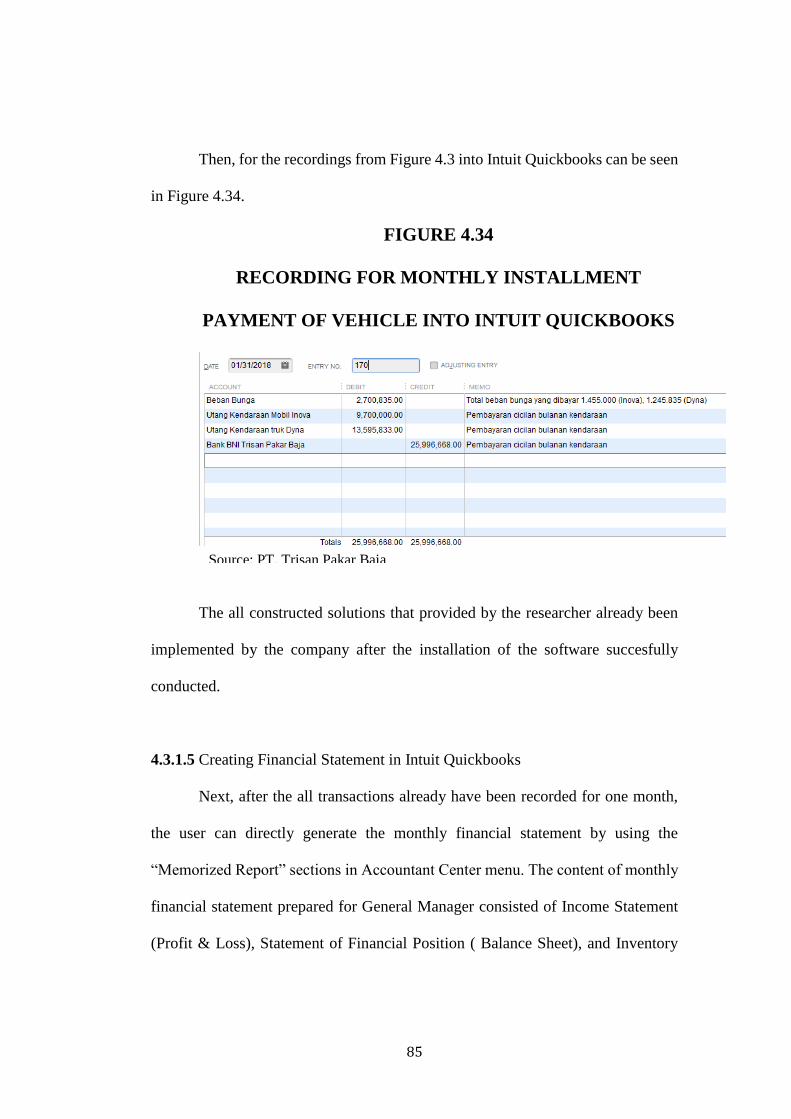

Figure 4.3 Recording for Monthly Installment Payment of Vehicle ......................... 50

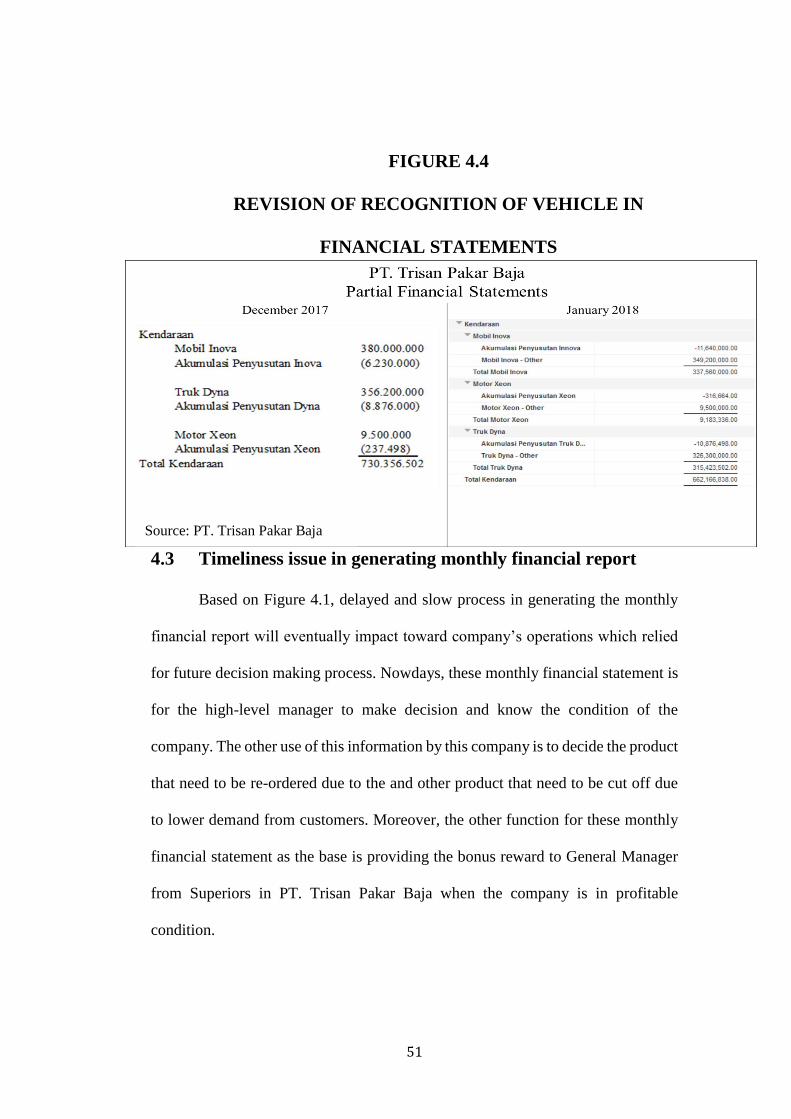

Figure 4.4 Revision of Recognition of Vehicle in Financial Statements ................... 50

Figure 4.5 Accounting & Finance Department Job Description ................................ 52

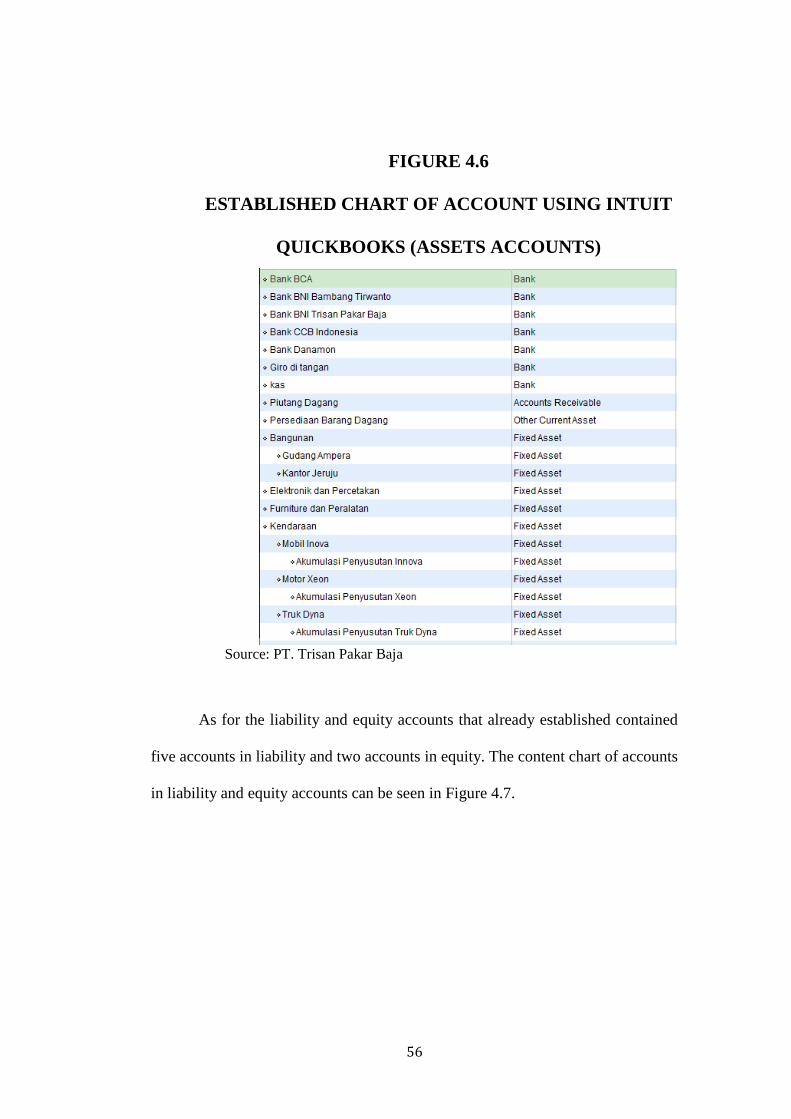

Figure 4.6 Established Chart of Account Using Intuit Quickbooks (Asset

Accounts) ................................................................................................ 55

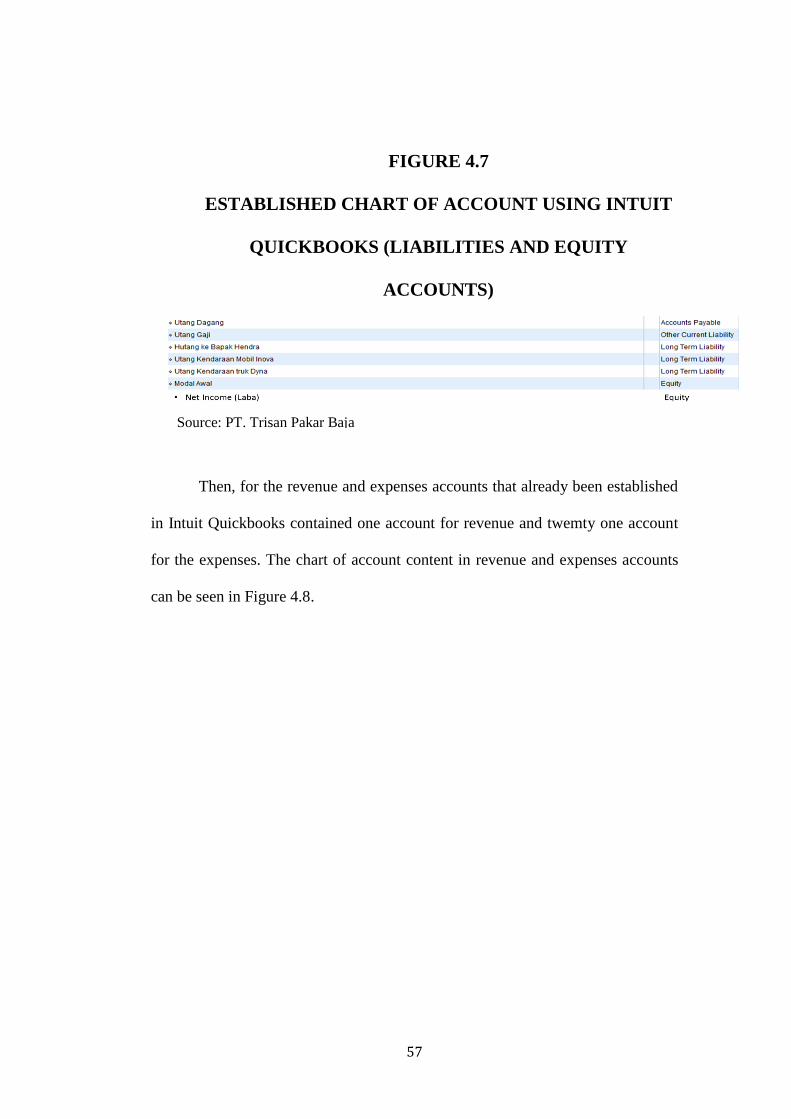

Figure 4.7 Established Chart of Account Using Intuit Quickbooks (Liabilities and

Equity Accounts) .................................................................................... 56

Figure 4.8 Established Chart of Accounts Using Intuit Quickbooks (Revenue and

Expenses Accounts) ............................................................................... 57

Figure 4.9 List of Customers and Vendors of PT. Trisan Pakar Baja ........................ 58

Figure 4.10 Established Customers Lists Using Intuit Quickbooks........................... 59

Figure 4.11 Established Vendors Lists Using Intuit Quickbooks .............................. 60

Figure 4.12 Established Inventory Lists Using Intuit Quickbooks ............................ 60

xi

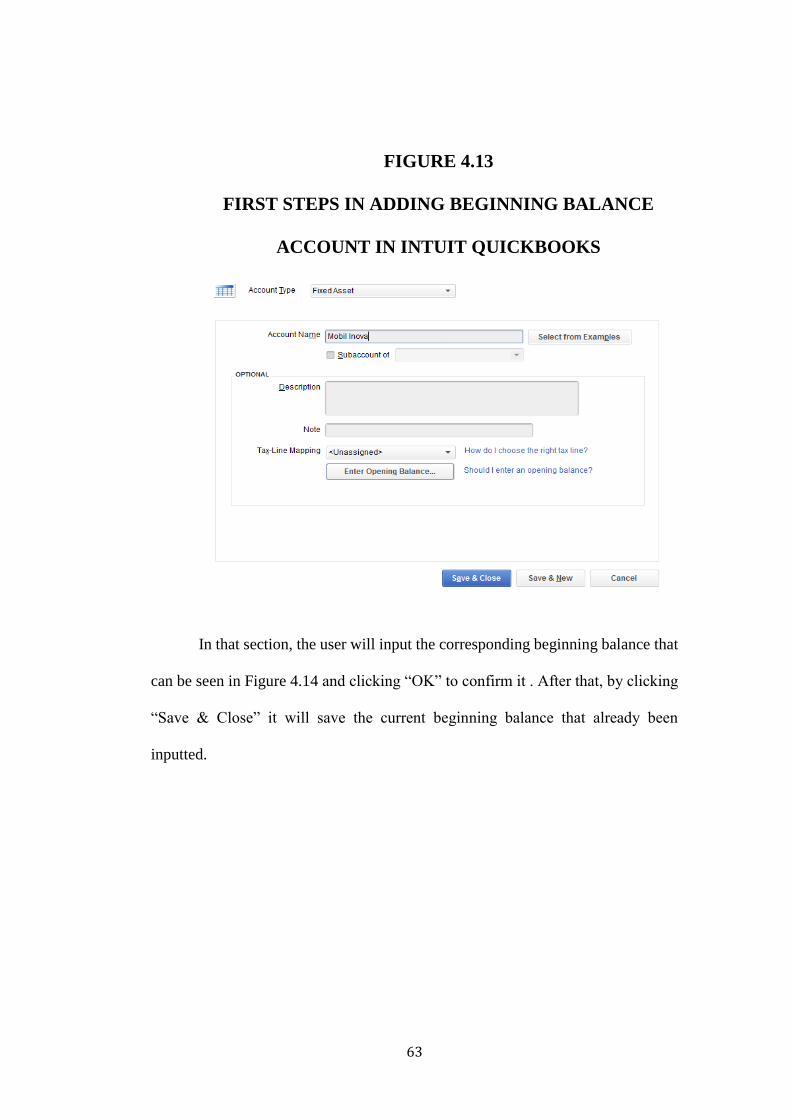

Figure 4.13 First Steps in Adding Beginning Balance of Account in Intuit Quickbooks

............................................................................................................... .62

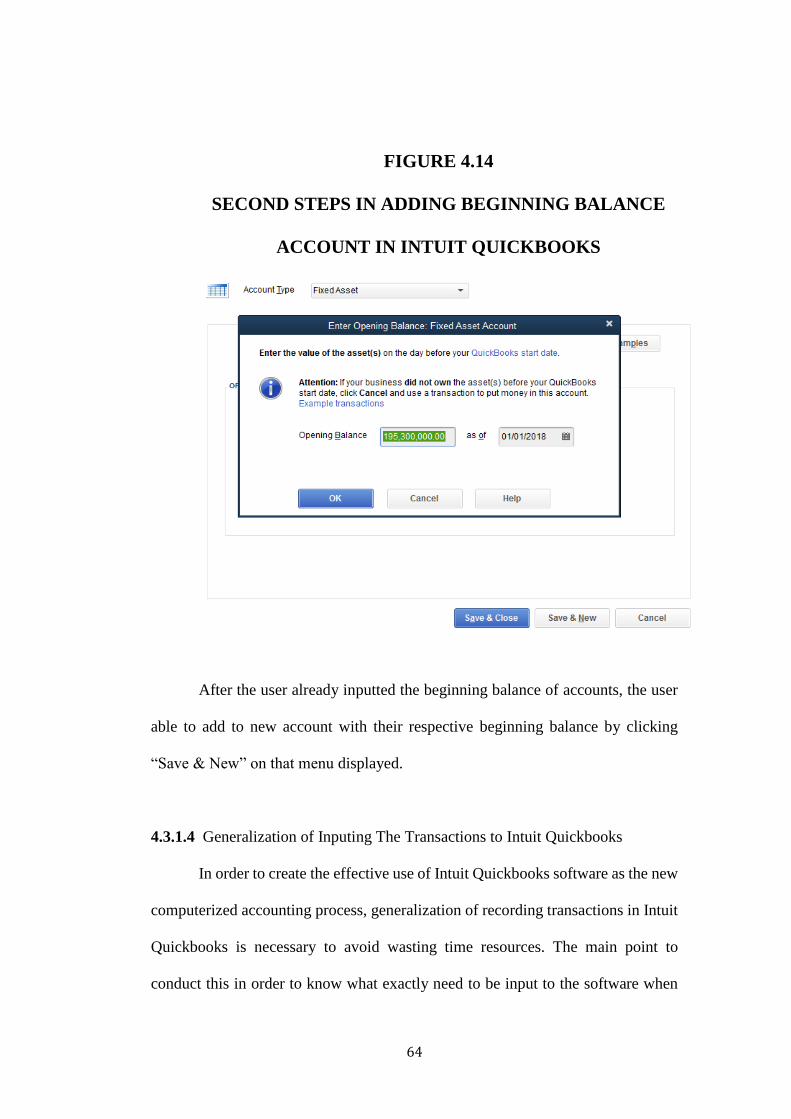

Figure 4.14 Second Steps in Adding Beginning Balance of Account in Intuit

Quickbooks ............................................................................................ .63

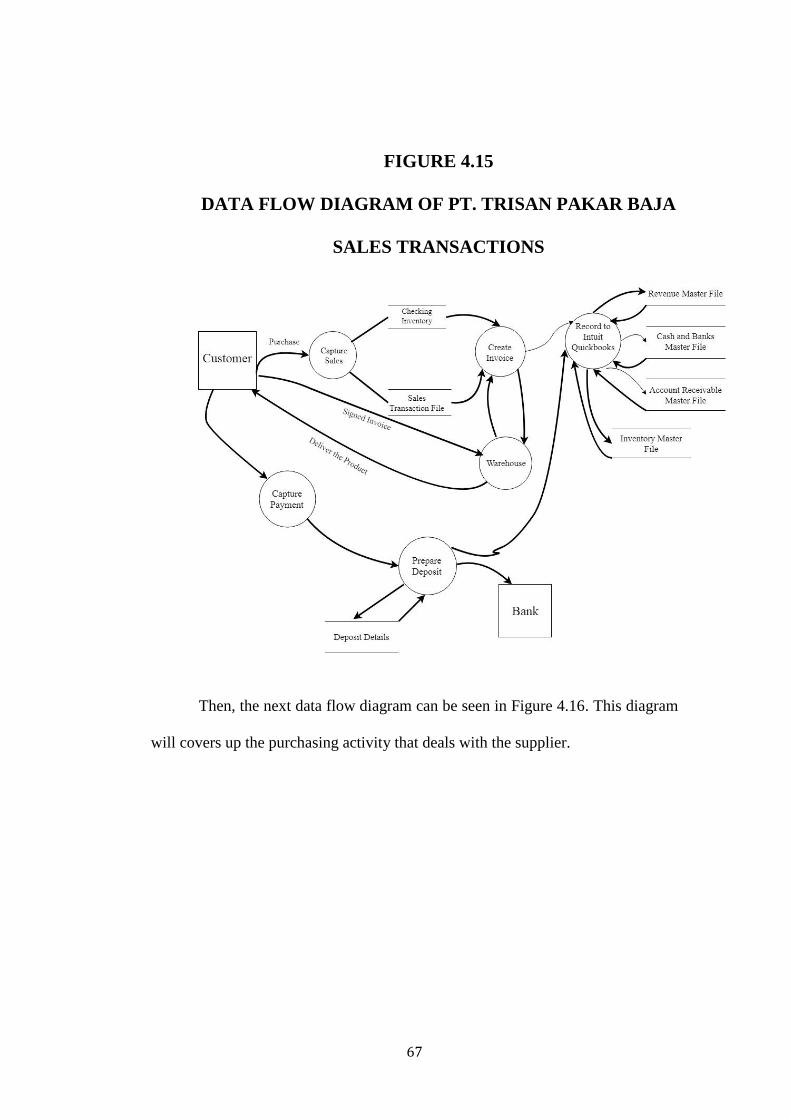

Figure 4.15 Data Flow Diagram of PT. Trisan Pakar Baja Sales Transactions ......... 66

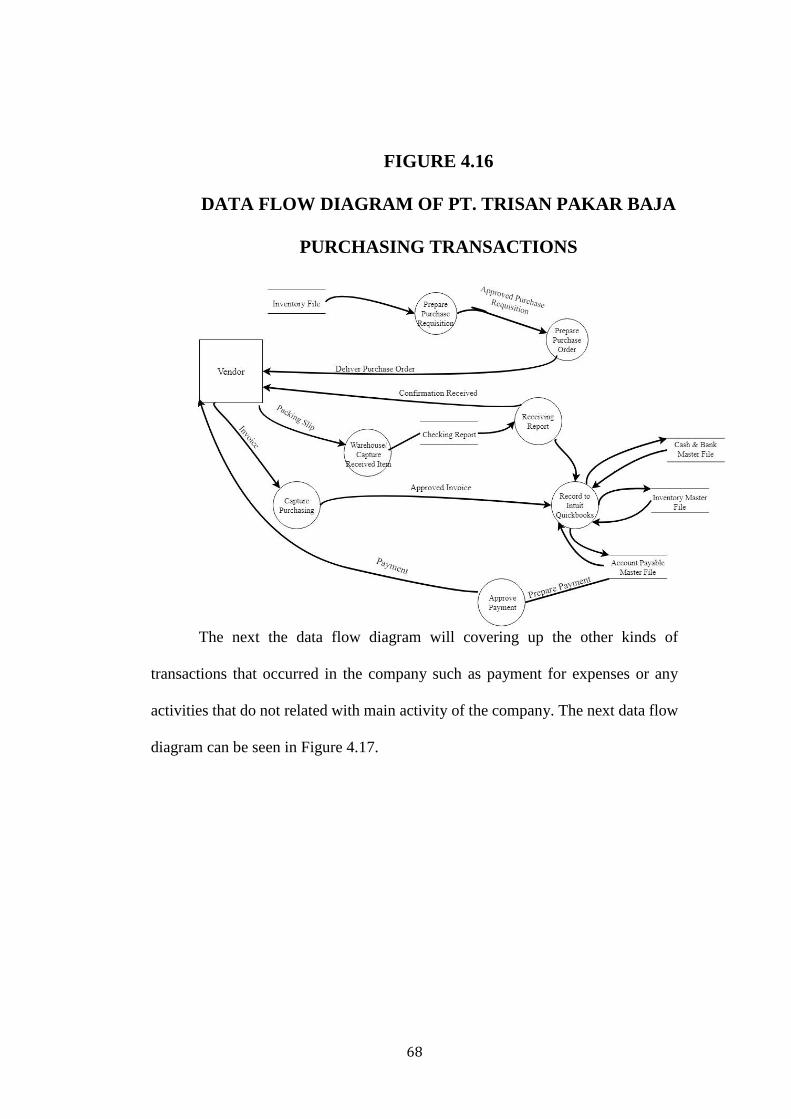

Figure 4.16 Data Flow Diagram of PT. Trisan Pakar Baja Purchasing Transactions 67

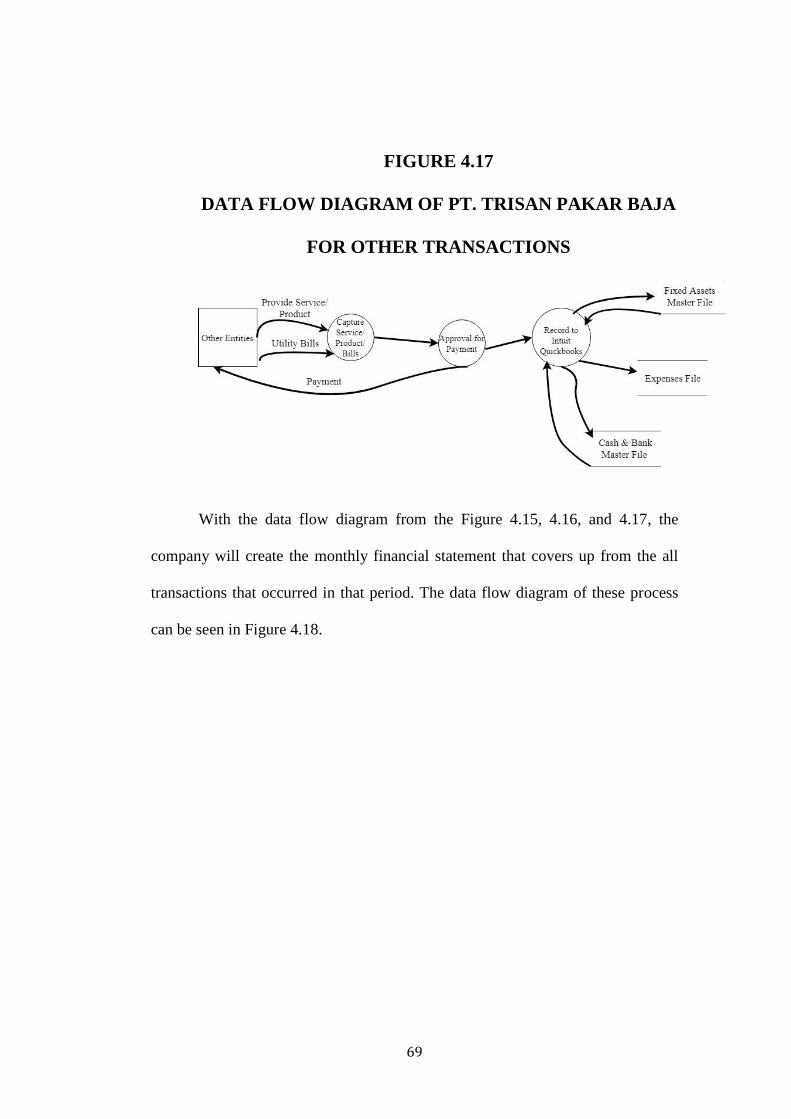

Figure 4.17 Data Flow Diagram of PT. Trisan Pakar Baja Other Transactions......... 68

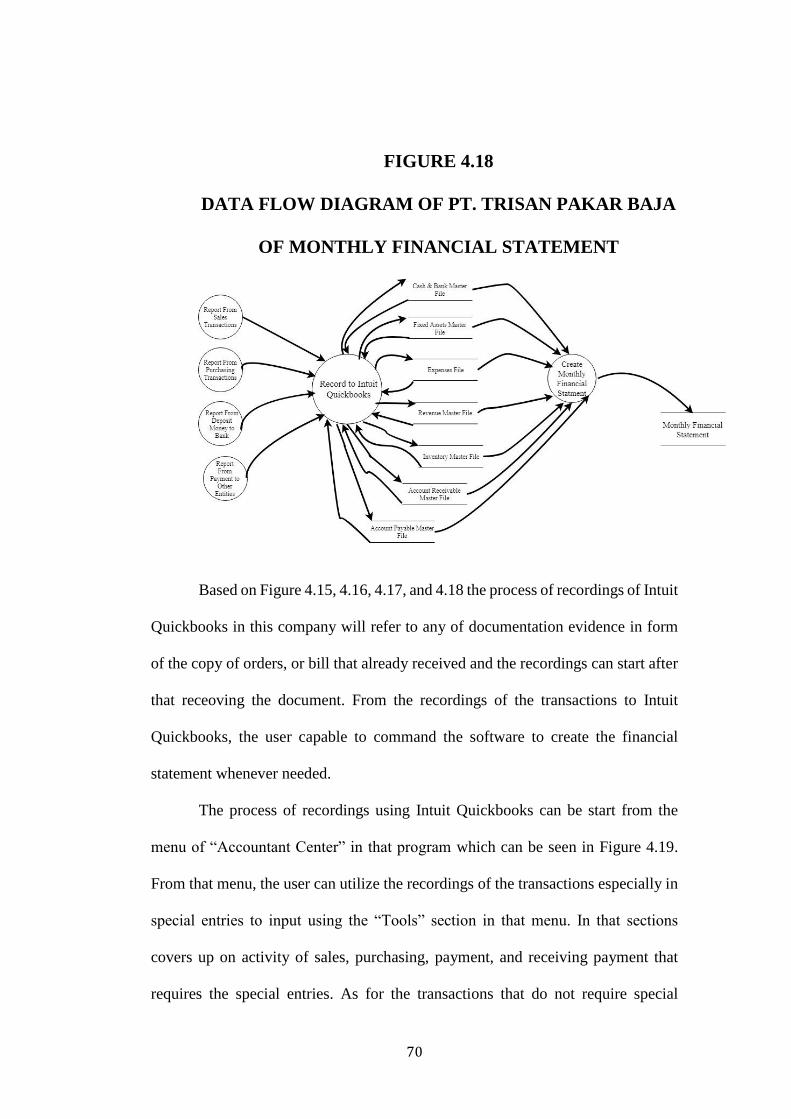

Figure 4.18 Data Flow Diagram of PT. Trisan Pakar Baja of Monthly Financial

Statement ................................................................................................ 69

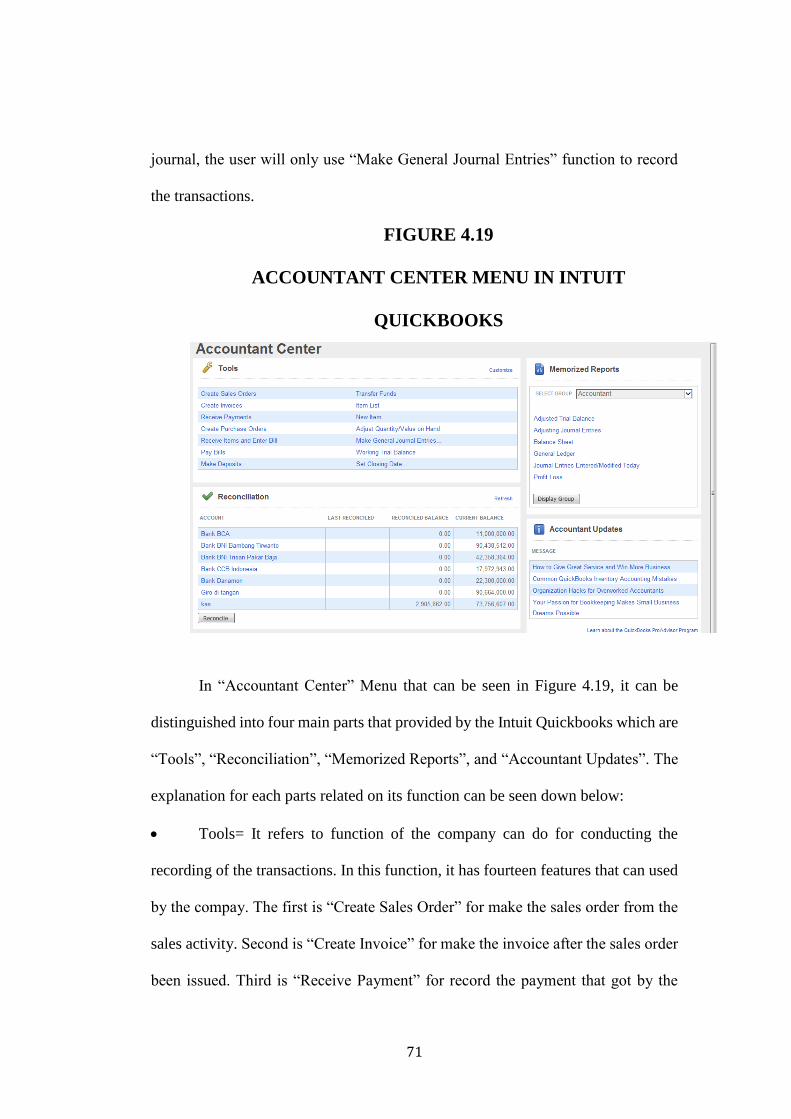

Figure 4.19 Accountant Center Menu in Intuit Quickbooks ...................................... 70

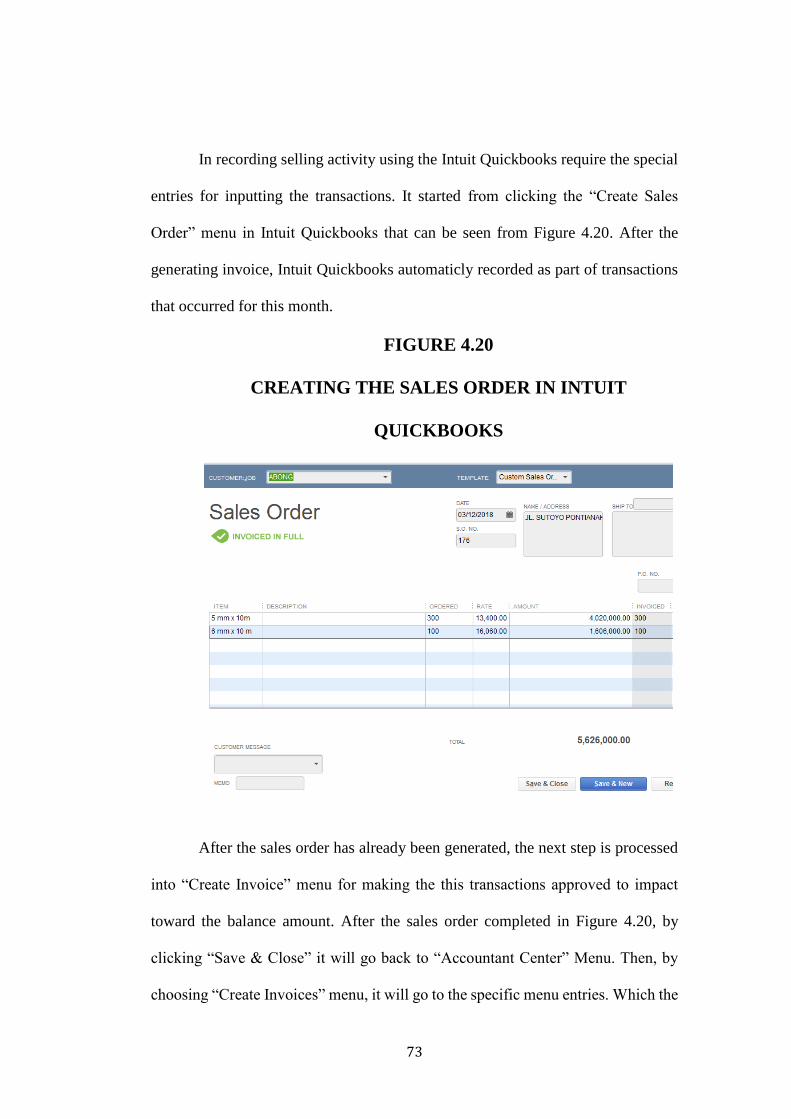

Figure 4.20 Creating The Sales Order in Intuit Quickbooks ..................................... 72

Figure 4.21 Processing The Sales Order Into Invoice in Intuit Quickbooks .............. 73

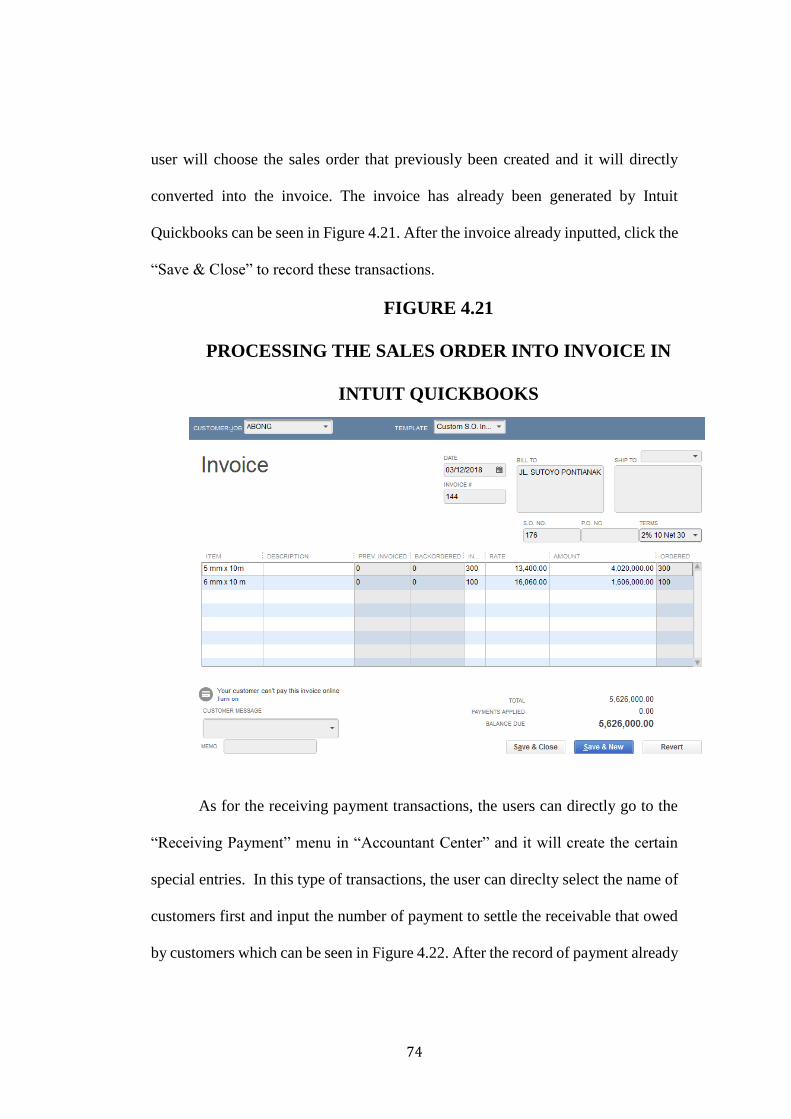

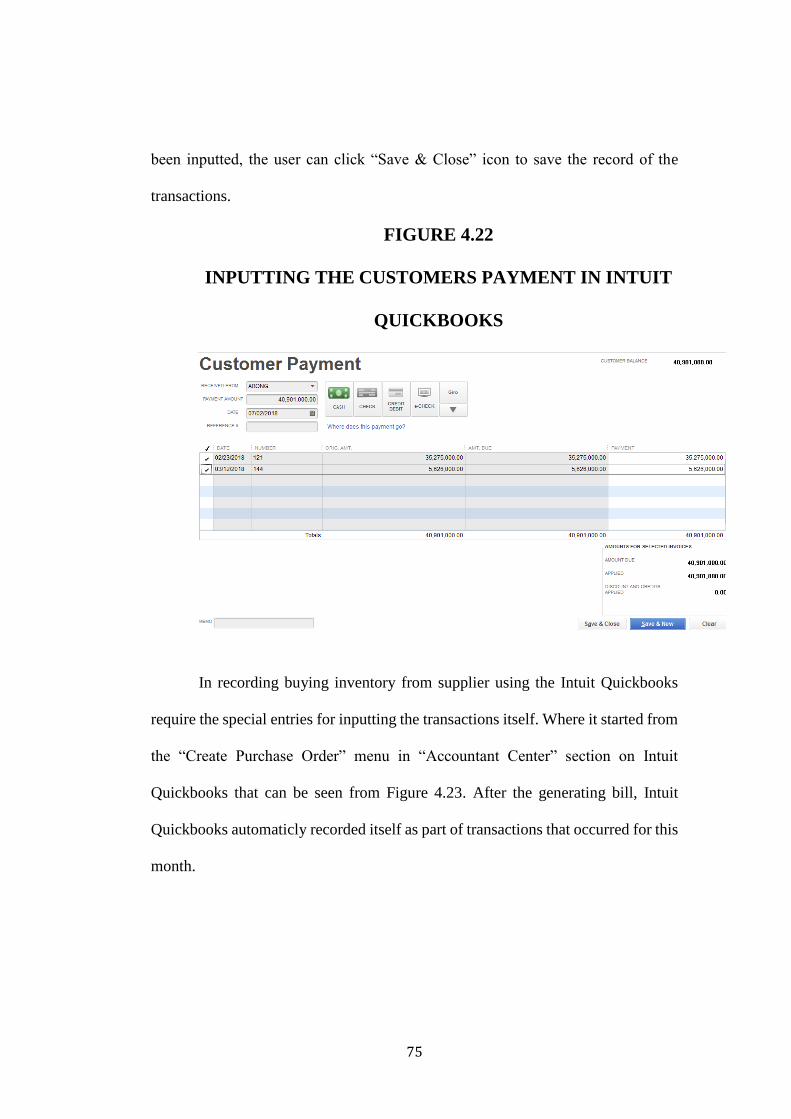

Figure 4.22 Inputting The Customers Payment in Intuit Quickbooks ....................... 74

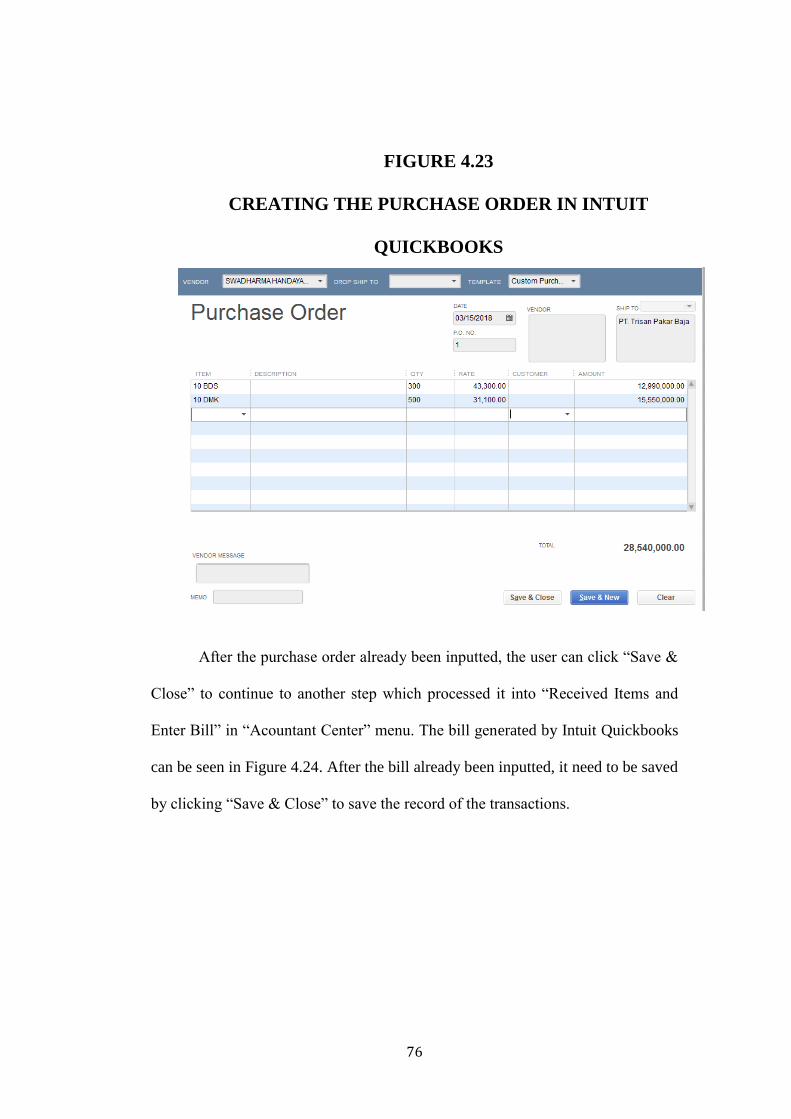

Figure 4.23 Creating The Purchase Order in Intuit Quickbooks ............................... 75

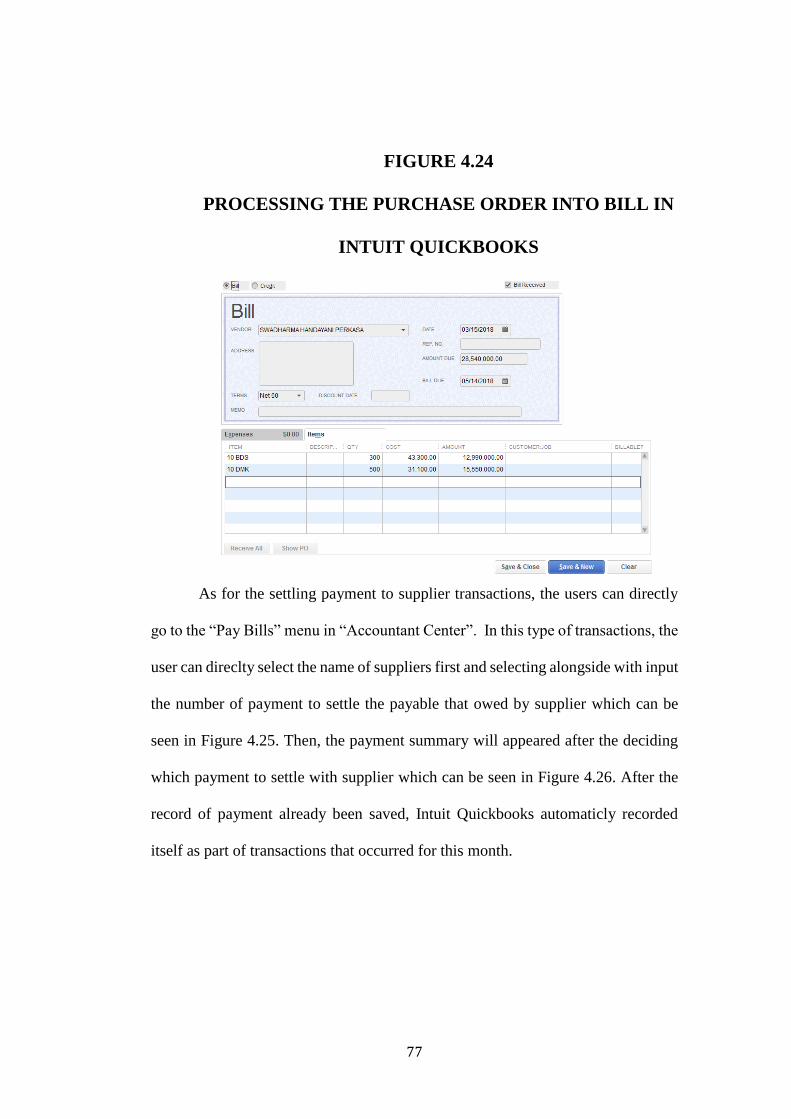

Figure 4.24 Processing The Purchase Order Into Bill in Intuit Quickbooks .............. 76

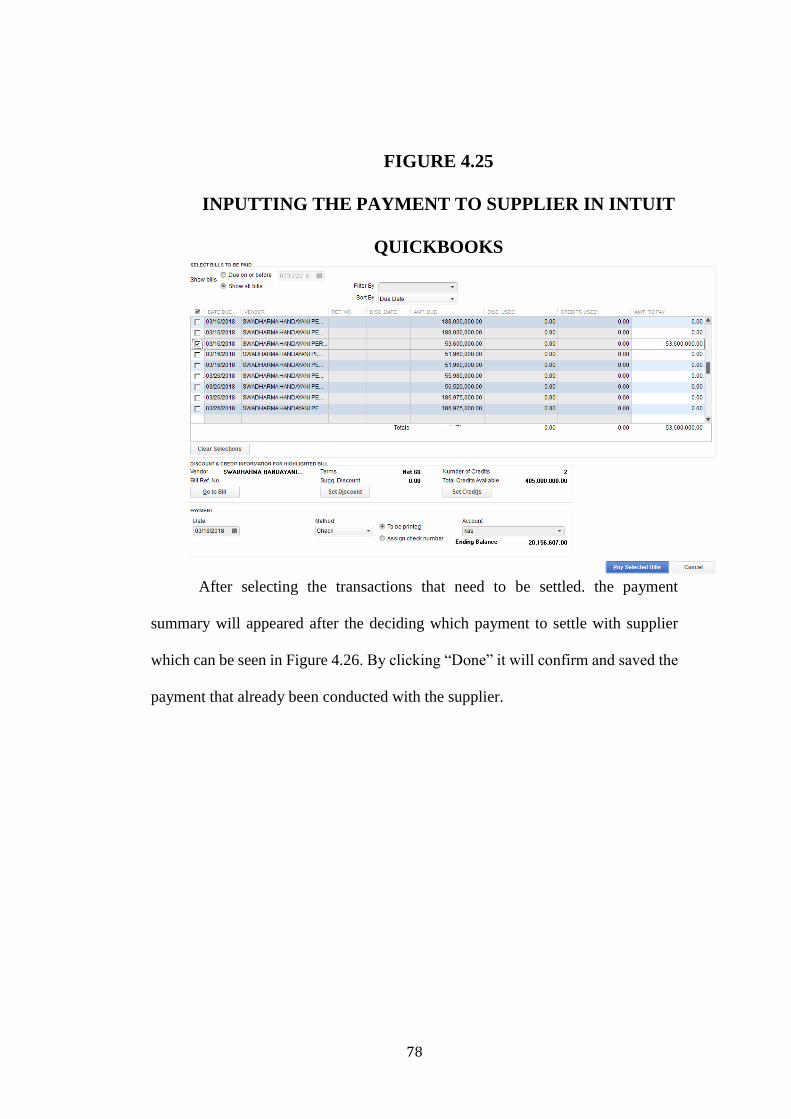

Figure 4.25 Inputting The Payment to Supplier in Intuit Quickbooks ....................... 77

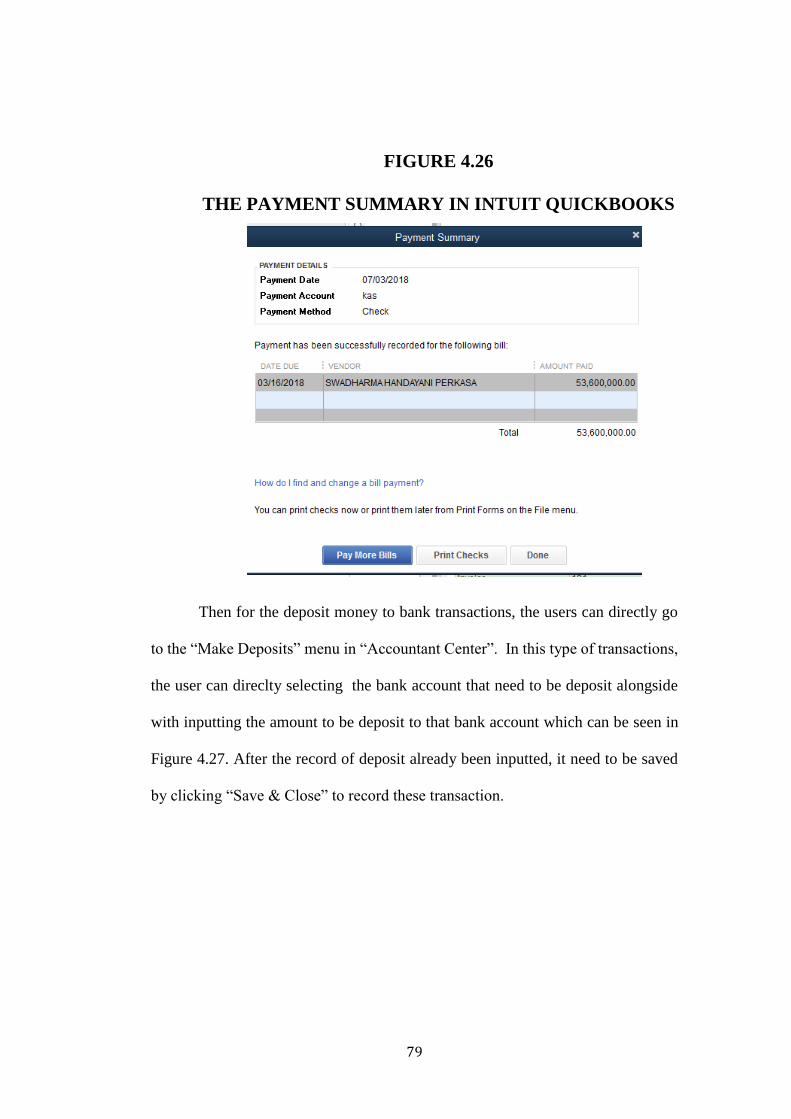

Figure 4.26 The Payment Summary in Intuit Quickbooks ........................................ 78

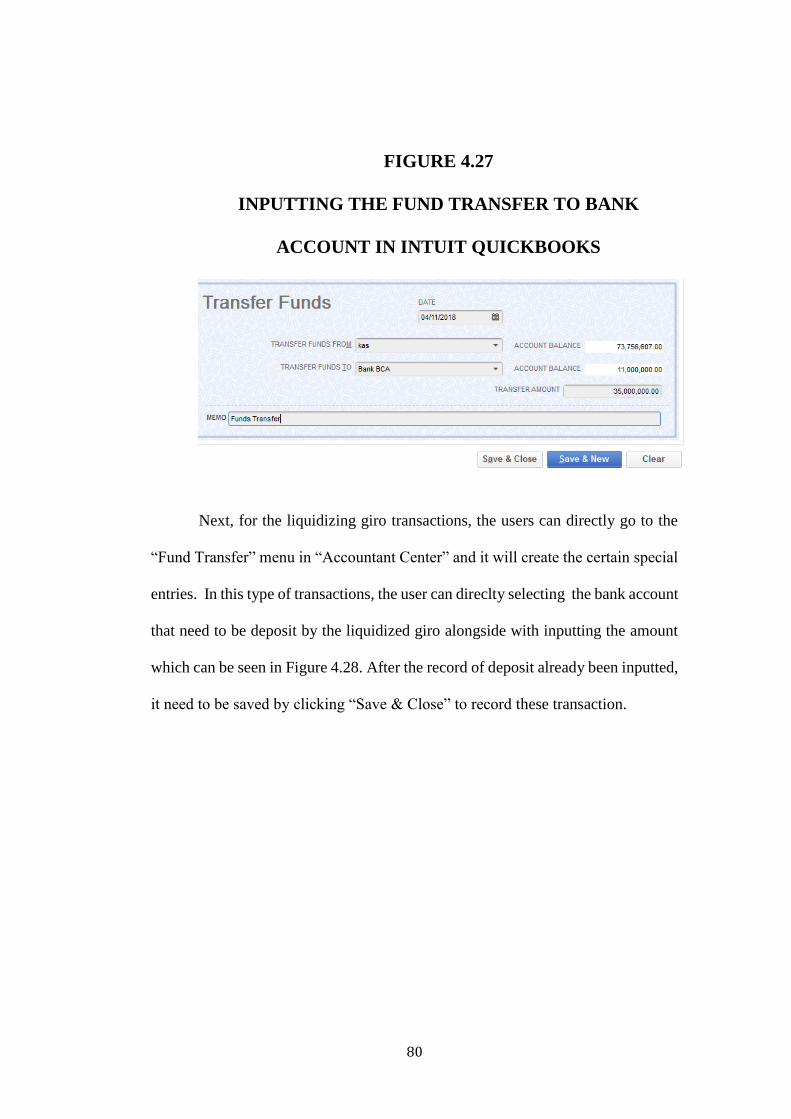

Figure 4.27 Inputting The Fund Transfer to Bank Account in Intuit Quickbooks ..... 79

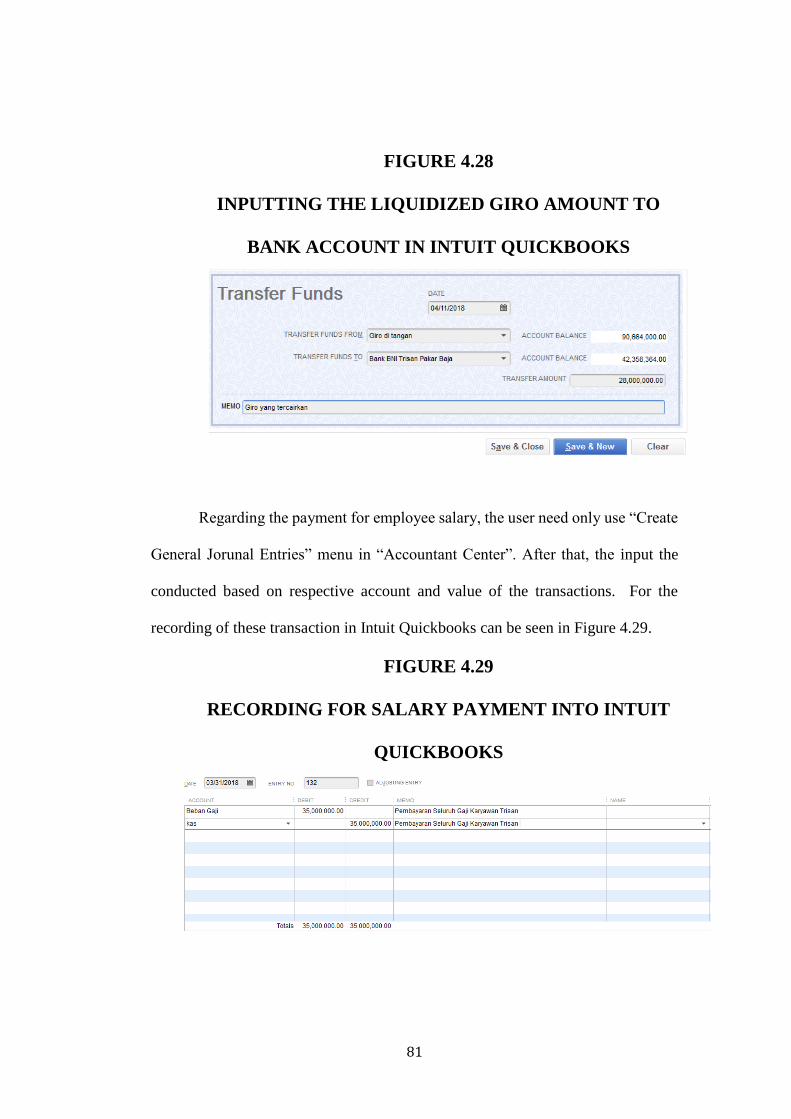

Figure 4.28 Inputting The Liquidized Giro Amount to Bank Account in Intuit

Quickbooks ............................................................................................. 80

Figure 4.29 Recording for Salary Payment Into Intuit Quickbooks .......................... 80

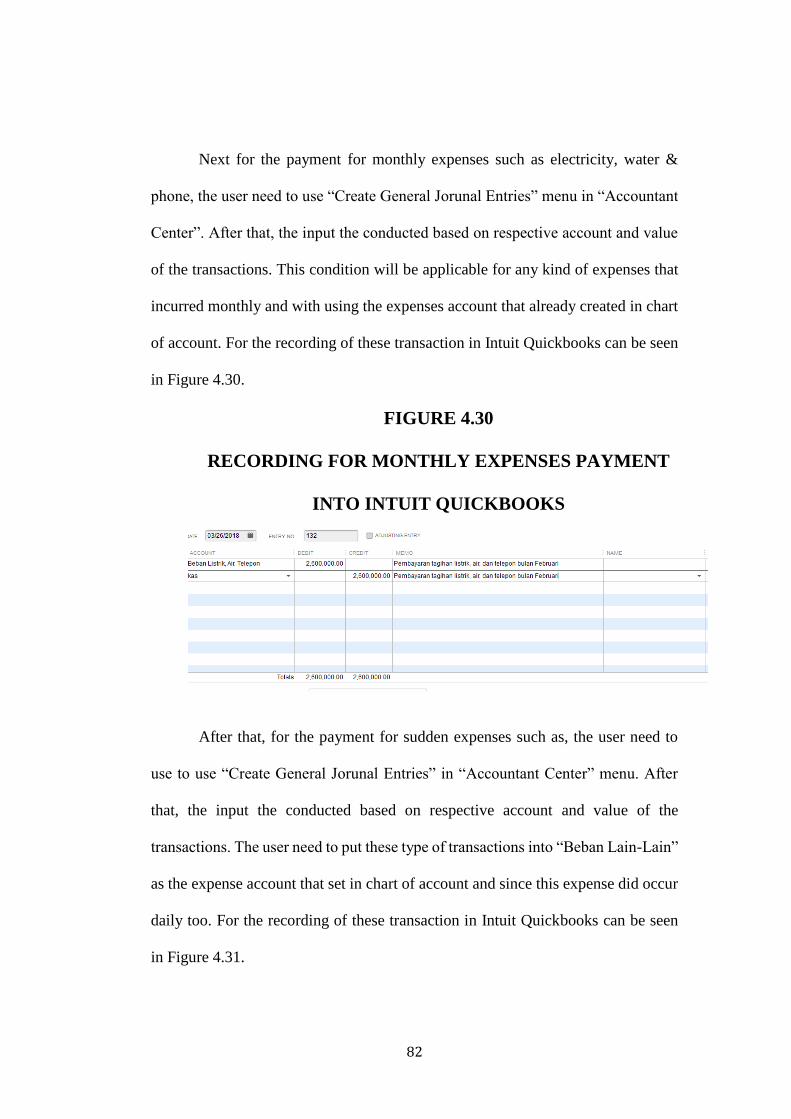

Figure 4.30 Recording for Monthly Expenses Payment Into Intuit Quickbooks ....... 81

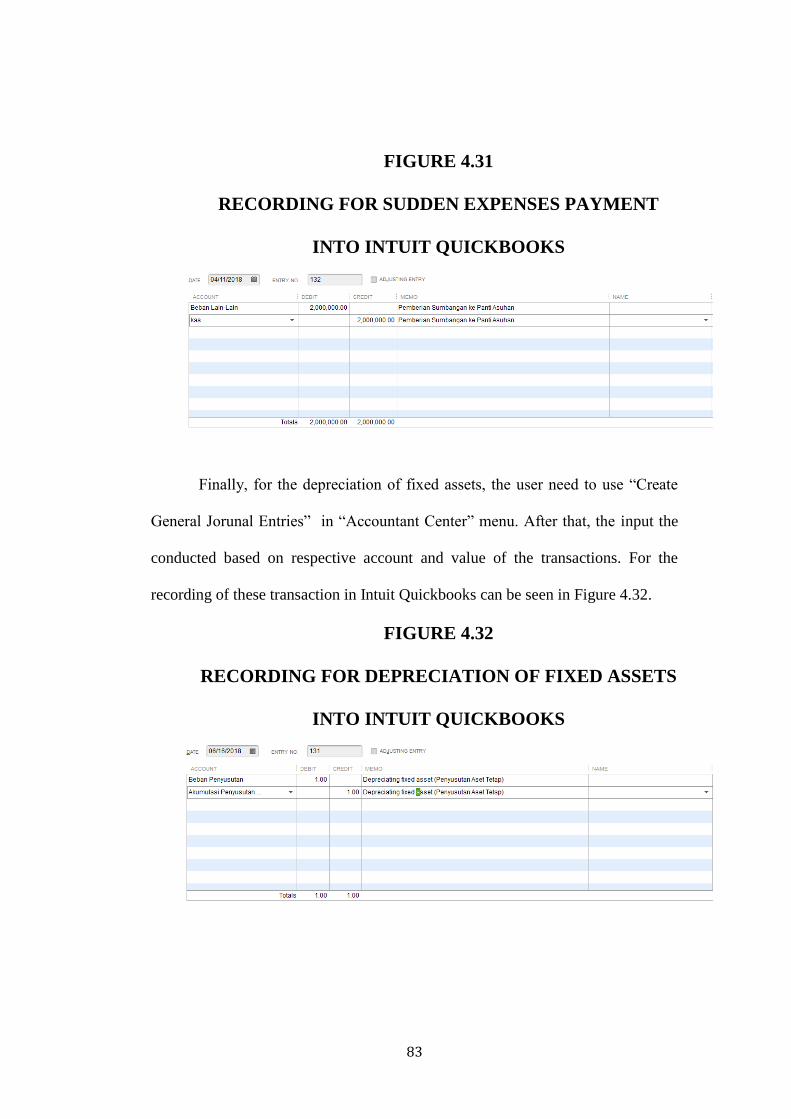

Figure 4.31 Recording for Sudden Expenses Payment Into Intuit Quickbooks ......... 82

Figure 4.32 Recording for Depreciation of Fixed Assets Into Intuit Quickbooks ..... 82

Figure 4.33 Income Statement Generated by Intuit Quickbooks ............................... 83

xii

Figure 4.34 Recording Adjustment Journal for Misstatement Value of Vehicle into

Intuit Quickbooks ................................................................................... 84

Figure 4.35 Recording of Monthly Installment Payment of Vehicle into Intuit

Quickbooks ............................................................................................. 85

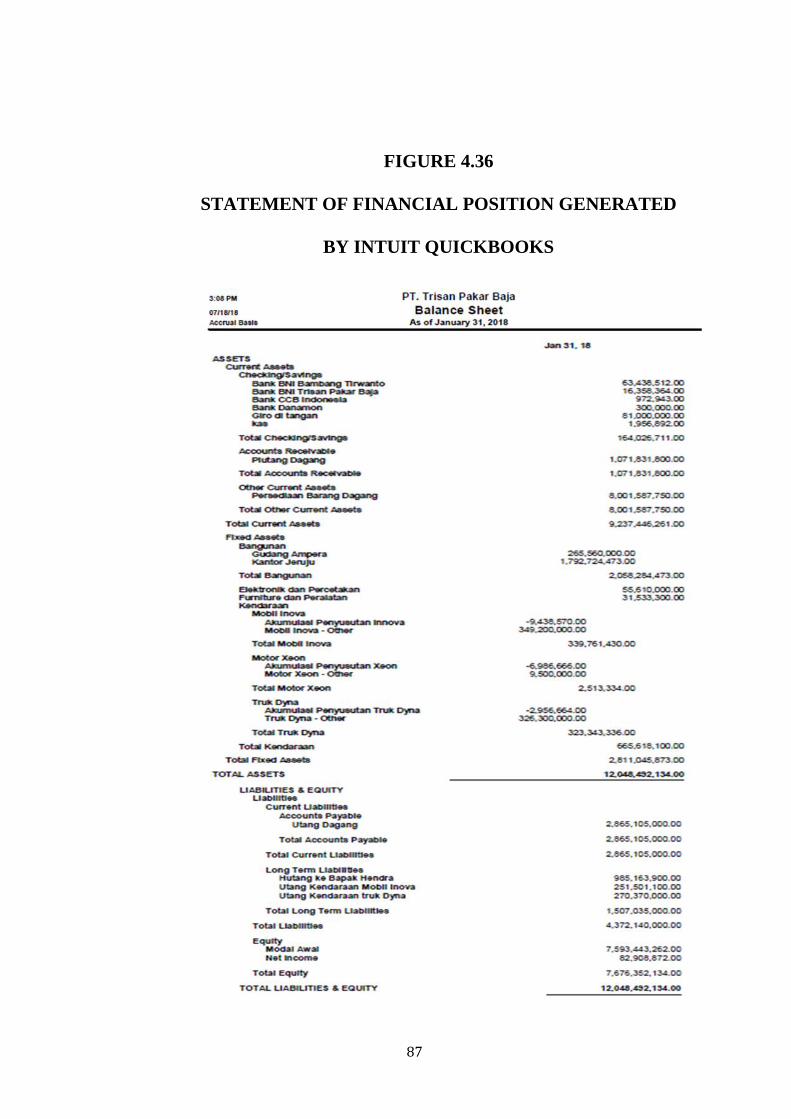

Figure 4.36 Statement of Financial Position Generated by Intuit Quickbooks .......... 86

Figure 4.37 Income Statement Manually Generated by PT. Trisan Pakar Baja for

January 2018 ......................................................................................... 89

Figure 4.38 Statement of Financial Position Generated by PT. Trisan Pakar Baja for

January 2018 ......................................................................................... 90

xiii

LIST OF TABLES

Table 1.1 The Monthly Comparisson Effect of Depreciation Charg between The

mistatement and Real Value of Vehicle Fixed Assets from October until

December 2017 ........................................................................................ 5

Table 3.1 Illustration of The Journalizing Transactions in PT. Trisan Pakar Baja .. 21

Table 3.2 Monthly Inventory Evaluation Summary PT. Trisan Pakar Baja December

2017 ........................................................................................................ 24

Table 4.1 Conducted Checklist of All Accounts in PT. Trisan Pakar Baja .............. 36

Table 4.2 Example of Recapitulated Transactions List of Cash Account in PT. Trisan

Pakar Baja ............................................................................................... 38

Table 4.3 Example of Recapitulated Transactions List of Account Payable Account

in PT. Trisan Pakar Baja ......................................................................... 40

Table 4.4 Example of Recapitulated Transactions List of Sales Revenue Account in

PT. Trisan Pakar Baja ............................................................................. 41

Table 4.5 Example of Recapitulated Transactions List of Expense Account in PT.

Trisan Pakar Baja .................................................................................... 43

Table 4.6 Comparisson of Monthly Depreciation Charge for Credited Vehicle Fixed

Assets ...................................................................................................... 45

Table 4.7 Revision of Recognition of Vehicle after Adjustment ............................ 49

Table 4.8 PT. Trisan Pakar Baja’s Chart of Account Before Conversion into Intuit

Quickbooks ............................................................................................. 53

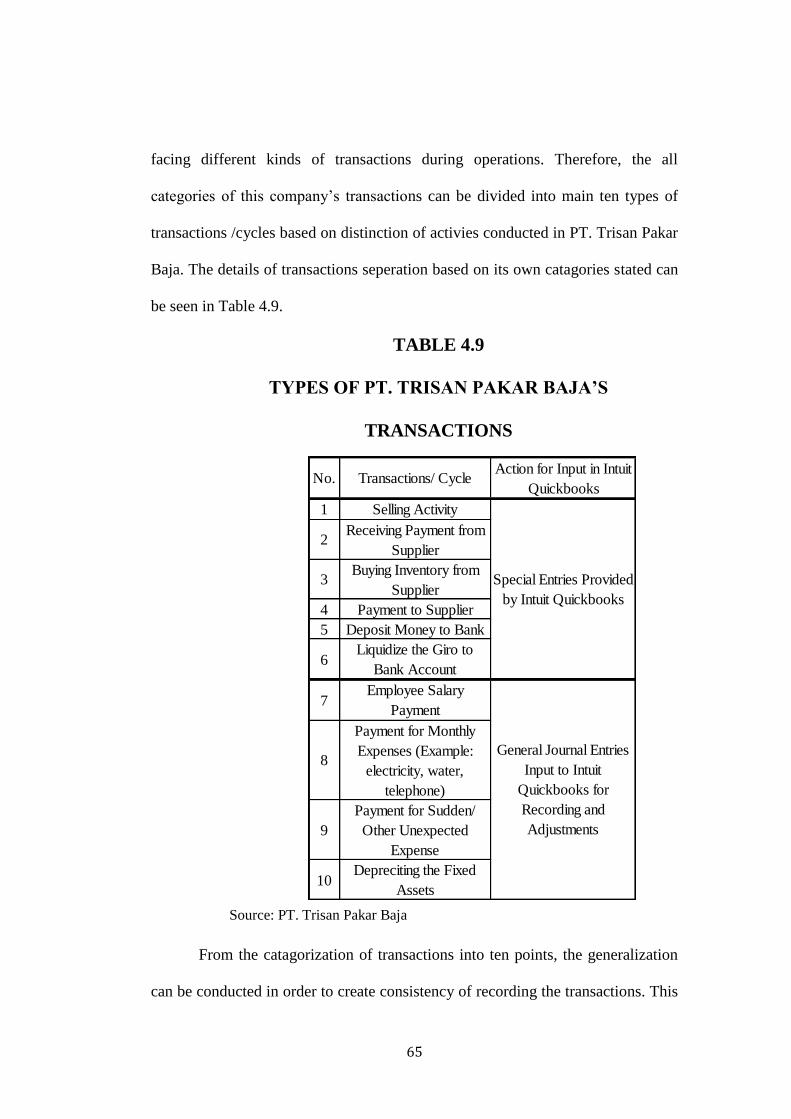

Table 4.9 Types of PT. Trisan Pakar Baja’s Transactions ...................................... 64

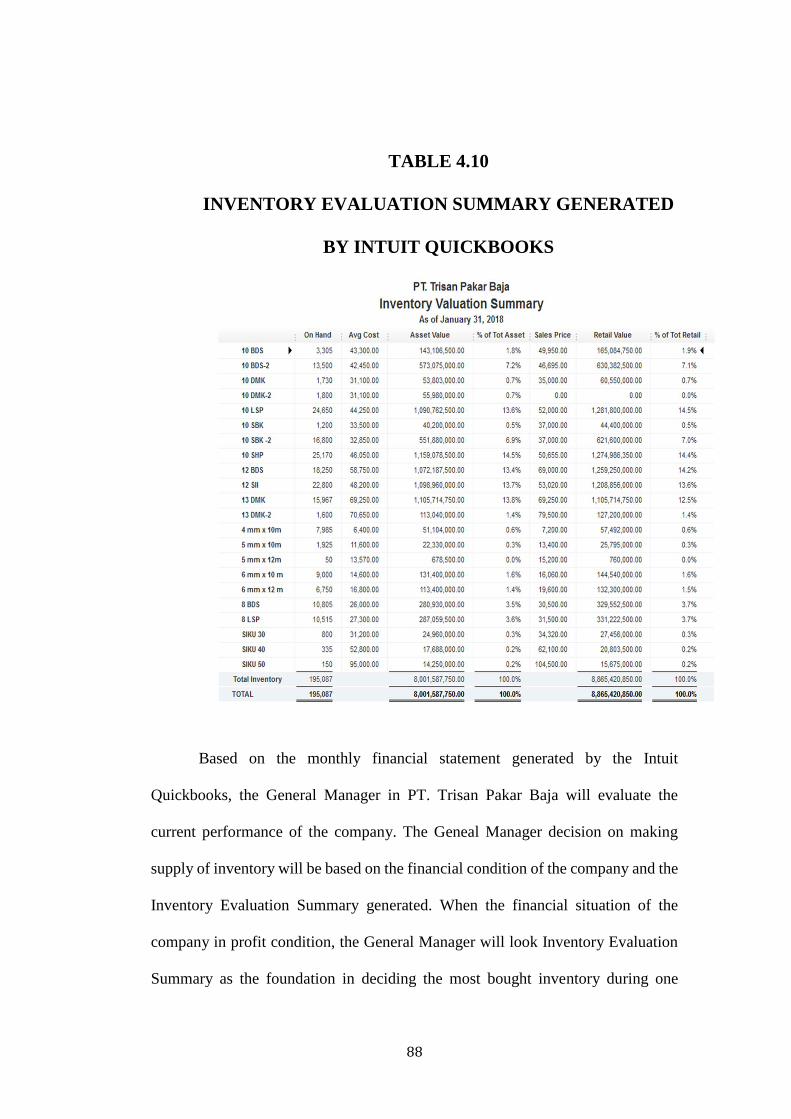

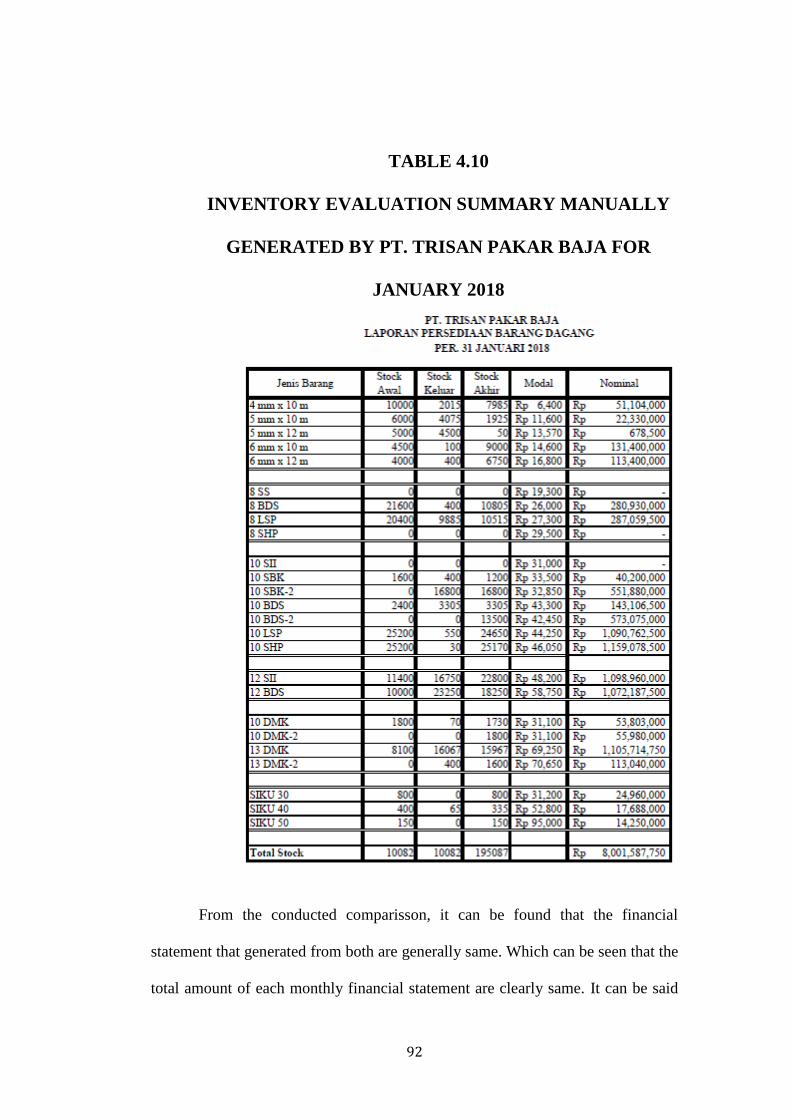

Table 4.10 Inventory Evaluation Summary Generated by Intuit Quickbooks ......... 87

xiv

Table 4.11 Inventory Evaluation Summary Generated by PT. Trisan Pakar Baja for

January 2018 ......................................................................................... 91

xv

IMPLEMENTATION OF INTUIT QUICKBOOKS IN

PT. TRISAN PAKAR BAJA

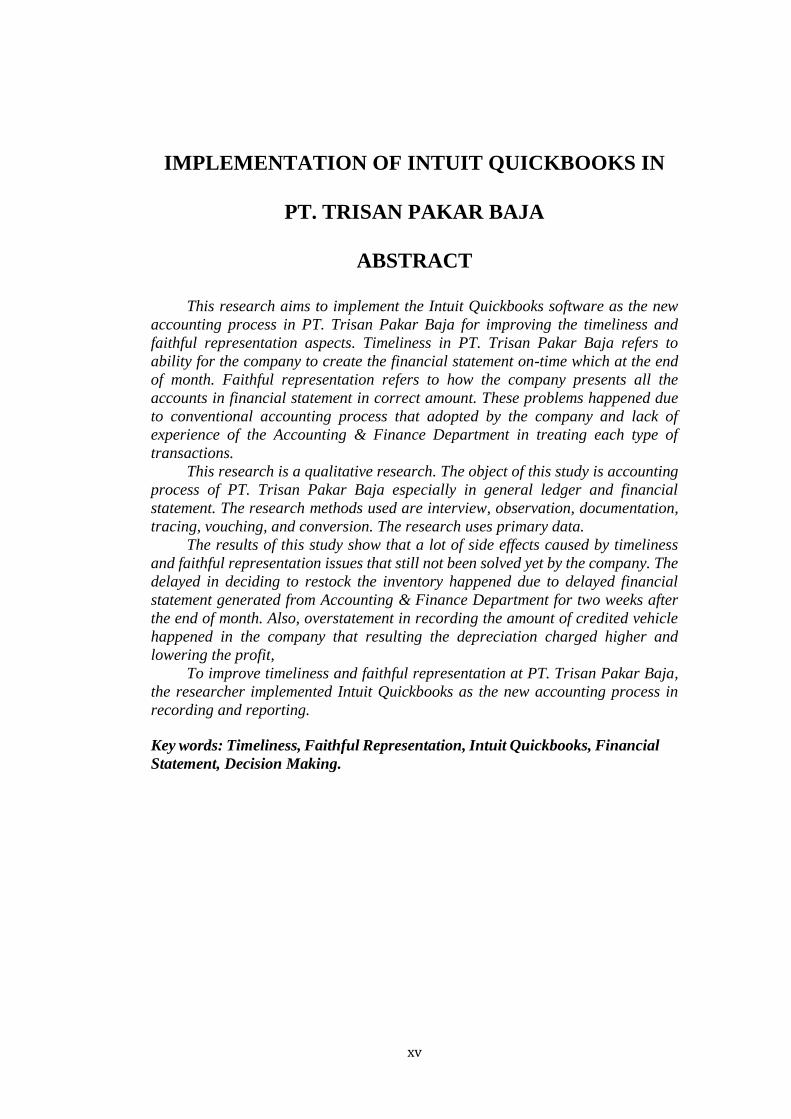

ABSTRACT

This research aims to implement the Intuit Quickbooks software as the new

accounting process in PT. Trisan Pakar Baja for improving the timeliness and

faithful representation aspects. Timeliness in PT. Trisan Pakar Baja refers to

ability for the company to create the financial statement on-time which at the end

of month. Faithful representation refers to how the company presents all the

accounts in financial statement in correct amount. These problems happened due

to conventional accounting process that adopted by the company and lack of

experience of the Accounting & Finance Department in treating each type of

transactions.

This research is a qualitative research. The object of this study is accounting

process of PT. Trisan Pakar Baja especially in general ledger and financial

statement. The research methods used are interview, observation, documentation,

tracing, vouching, and conversion. The research uses primary data.

The results of this study show that a lot of side effects caused by timeliness

and faithful representation issues that still not been solved yet by the company. The

delayed in deciding to restock the inventory happened due to delayed financial

statement generated from Accounting & Finance Department for two weeks after

the end of month. Also, overstatement in recording the amount of credited vehicle

happened in the company that resulting the depreciation charged higher and

lowering the profit,

To improve timeliness and faithful representation at PT. Trisan Pakar Baja,

the researcher implemented Intuit Quickbooks as the new accounting process in

recording and reporting.

Key words: Timeliness, Faithful Representation, Intuit Quickbooks, Financial

Statement, Decision Making.

xvi

IMPLEMENTATION OF INTUIT QUICKBOOKS IN

PT. TRISAN PAKAR BAJA

INTISARI

Penelitian ini bertujuan untuk mengimplementasikan perangkat lunak Intuit

Quickbooks sebagai proses akuntansi baru di PT. Trisan Pakar Baja untuk

meningkatkan ketepatan waktu dan representatsi yang terpercaya. Ketepatan

waktu di PT. Trisan Pakar Baja mengacu pada kemampuan perusahaan untuk

membuat laporan keuangan tepat waktu yang pada akhir bulan. Representasi yang

terpercaya mengacu pada bagaimana perusahaan menyajikan semua akun dalam

laporan keuangan dalam jumlah yang benar. Masalah-masalah ini terjadi karena

proses akuntansi konvensional yang masih diadopsi oleh perusahaan dan

kurangnya pengalaman dari Departemen Akuntansi & Keuangan dalam

memperlakukan setiap jenis transaksi.

Penelitian ini merupakan penelitian kualitatif. Objek penelitian ini adalah

proses akuntansi PT. Trisan Pakar Baja terutama dalam buku besar dan laporan

keuangan. Metode penelitian yang digunakan adalah wawancara, observasi,

dokumentasi, penelusuran, vouching, dan konversi. Penelitian ini menggunakan

data primer.

Hasil penelitian ini menunjukkan bahwa banyak efek samping yang

disebabkan oleh ketepatan waktu dan masalah representasi terpercaya yang masih

belum dapat diatasi oleh perusahaan. Penundaan dalam memutuskan untuk

mengisi kembali persediaan terjadi karena laporan keuangan tertunda yang

dihasilkan dari Departemen Akuntansi & Keuangan selama dua minggu setelah

akhir bulan. Kemudian, kesalahan pencatatan dalam harga yang berlebih pada

kendaraan yang dikreditkan terjadi di perusahaan yang mengakibatkan depresiasi

dibebankan lebih tinggi dan menurunkan laba.

Untuk meningkatkan ketepatan waktu dan representasi yang terpercaya di

PT. Trisan Pakar Baja, peneliti melakukan implementasikan Intuit Quickbooks

sebagai bagian dari proses akuntansi dan pelaporan.

Kata kunci: Kinerja Perusahaan, Keuntungan, Peraturan, Standar Operasional

Prosedur, Target Perusahaan.

1

CHAPTER I

INTRODUCTION

1.1. Research Background

As the market constantly change from time to time, timely and precise

information will be needed in order to face the global economic situation. This

condition will affect to the decision making process conducted by the manager to

decide the direction of the company. Nowadays, it really hard to make decision

making process when the information are not presented in accurate and timely

manner.

In Indonesia, small or big companies currently facing the impact of slow

action to face the current market. For example, Matahari is a well-known company

that suffers from the impact of slow reaction of decision making in concerning

market needs and trends from information that already obtained (Julianto, 2017).

As a results, a lot of branches in Indonesia right now are closing due to lack of

action conducted to face the market that rapidly changes.

This study will discuss a company that suffers from the economic changes.

PT. Trisan Pakar Baja is a steel distributor located in Pontianak, West Borneo. The

company established in 2015. During the year of operations until right now, this

company already build many relations with different kinds of customers from inside

and outside of Pontianak as the company keep to expanding their business.

2

It is necessary for company to concern about the market demand on the

product being sold to get more profit. According the interview results from the

General Manager from PT. Trisan Pakar Baja, they experienced the decision

making lateness since business expansion in 2017. The lateness to decide on

ordering the product appeared due to timeliness issue related with delay in

presenting the company’s monthly financial statement. In that monthly financial

statement contains additional information regarding summary of inventory

evaluation for one month, which will be used as main information for deciding the

types of inventory that need to be purchased.

The financial statement is one of the core information that necessary for the

manager to know financial condition of the company and as the benchmark for

various types of decisions such as resupplying inventory or providing incentives/

bonus to the manager. One of the factor, that caused the lateness of information

presentation come from the accounting cycle that adopted by the company. The

company still adopt conventional/ manual accounting process in journalizing the

transaction and later on process it. As the result, these process tend to generate the

financial report for two or three weeks after the end of month. However, the General

Manager of PT. Trisan Pakar Baja feel concerned regarding these situation. Since,

the company’s monthly financial statement usually generated in two or three days

after the end of month due to lack of manpower in handling the accounting tasks

and during 2017 the situation changed drastic into lateness in presenting the report.

These problem will certainly related the timeliness factor that concerned with the

speed of presenting the current financial condition in the company.

3

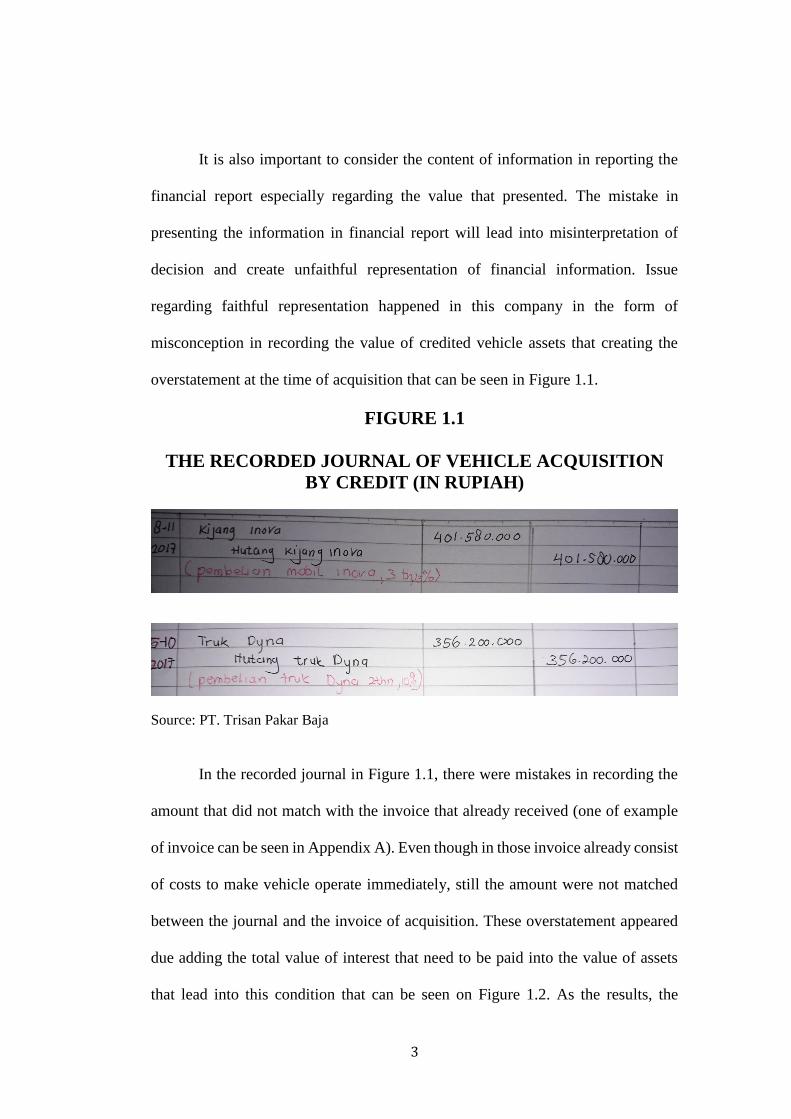

It is also important to consider the content of information in reporting the

financial report especially regarding the value that presented. The mistake in

presenting the information in financial report will lead into misinterpretation of

decision and create unfaithful representation of financial information. Issue

regarding faithful representation happened in this company in the form of

misconception in recording the value of credited vehicle assets that creating the

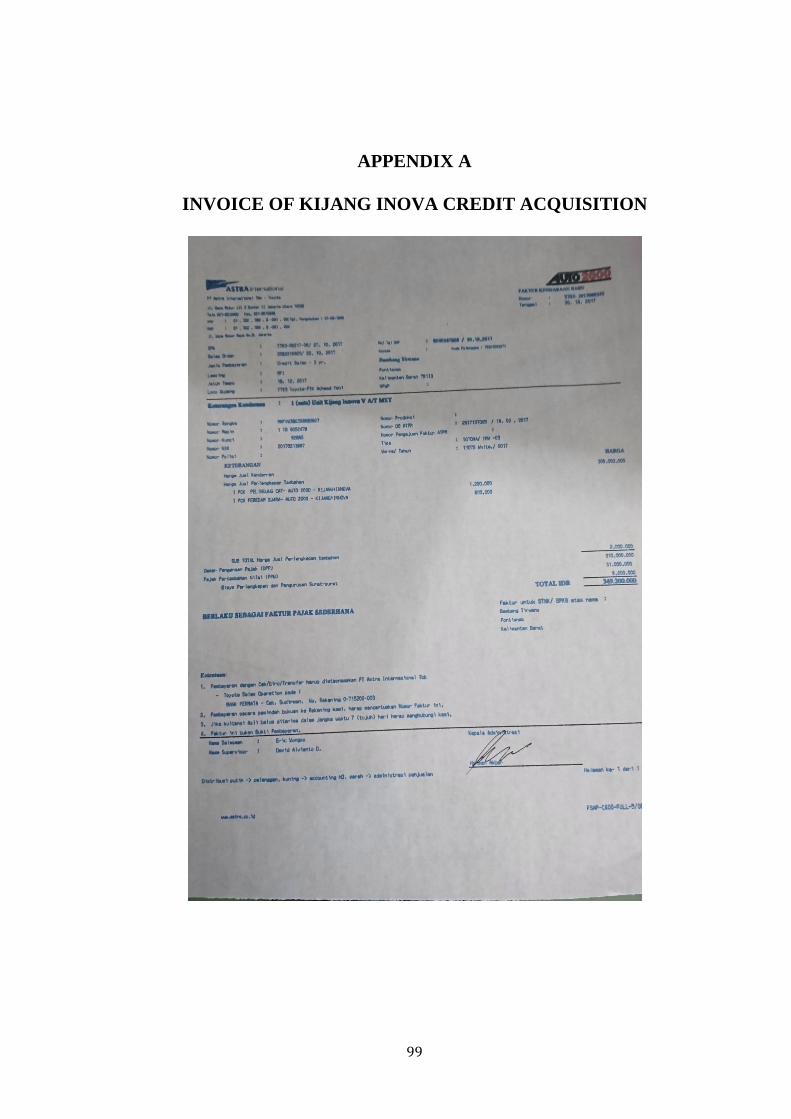

overstatement at the time of acquisition that can be seen in Figure 1.1.

FIGURE 1.1

THE RECORDED JOURNAL OF VEHICLE ACQUISITION

BY CREDIT (IN RUPIAH)

Source: PT. Trisan Pakar Baja

In the recorded journal in Figure 1.1, there were mistakes in recording the

amount that did not match with the invoice that already received (one of example

of invoice can be seen in Appendix A). Even though in those invoice already consist

of costs to make vehicle operate immediately, still the amount were not matched

between the journal and the invoice of acquisition. These overstatement appeared

due adding the total value of interest that need to be paid into the value of assets

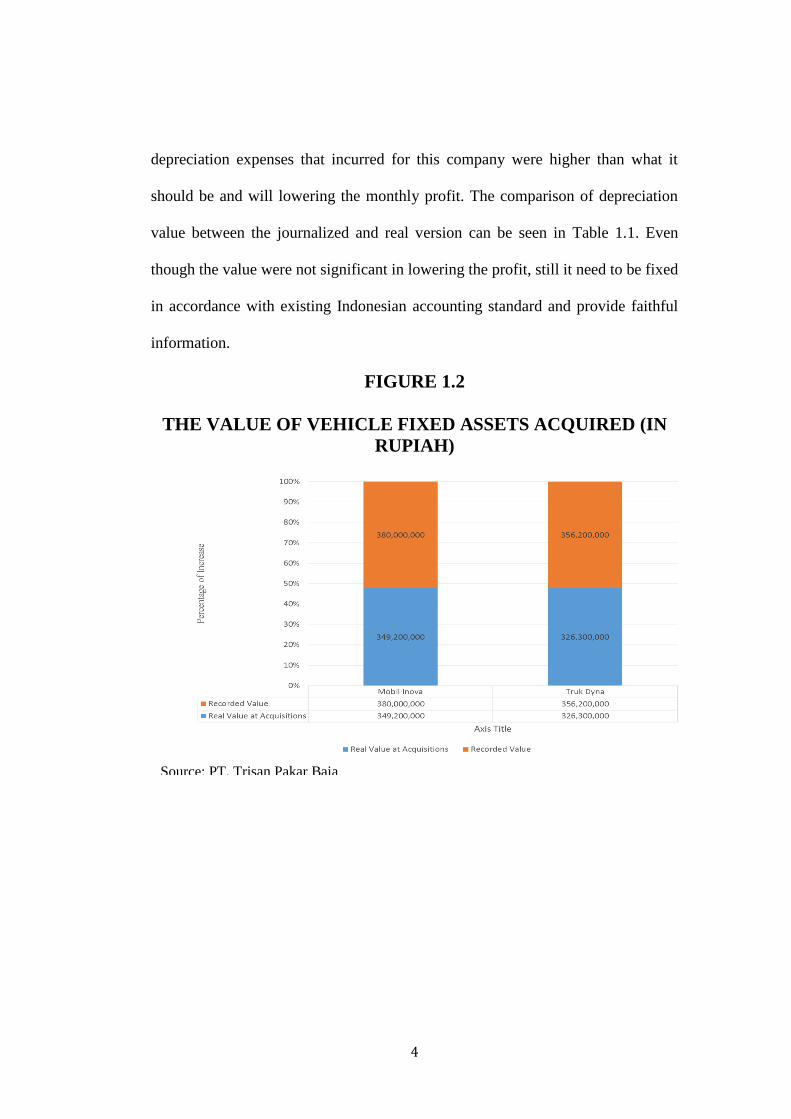

that lead into this condition that can be seen on Figure 1.2. As the results, the

4

depreciation expenses that incurred for this company were higher than what it

should be and will lowering the monthly profit. The comparison of depreciation

value between the journalized and real version can be seen in Table 1.1. Even

though the value were not significant in lowering the profit, still it need to be fixed

in accordance with existing Indonesian accounting standard and provide faithful

information.

FIGURE 1.2

THE VALUE OF VEHICLE FIXED ASSETS ACQUIRED (IN

RUPIAH)

Source: PT. Trisan Pakar Baja

5

TABLE 1.1

THE MONTHLY COMPARISSON EFFECT OF

DEPRECIATION CHARGE BETWEEN THE MISTATEMENT

AND REAL VALUE OF VEHICLE ASSETS FROM OCTOBER

UNTIL DECEMBER 2017 (IN RUPIAH)

Corresponding with the current company situation, lighten up the researcher

initiative to solve the problem occurred and implementing accounting software in

the current accounting process by using Intuit Quickbooks. If this issues related

with accounting process keep on existing, it will certainly affect the future condition

of company in decision making process. By that means, PT. Trisan Pakar Baja

accepting for improving their accounting process using Intuit Quickbooks as part

of accepting and moving forward from the existing problem to avoid any kinds of

new potential side effects occurred.

Therefore, the researcher expects that by translating PT. Trisan Pakar Baja

into computerized version with Intuit Quickbooks will help on improving the time

Source: PT. Trisan Pakar Baja

6

consumption in creating the monthly financial report and the accuracy of providing

the reliable information. Also, with solving the faithful representation issue

regarding the overstatement in vehicle fixed assets will provide more reliable

financial information presented.

1.2. Problem Identification and Statement

The current accounting process adopted by the company was still in

conventional ways. All of the process begin with the manually recording the

transactions into a book by handwriting. At the end of month, they will compile all

of the journals and process it to create the company’s own monthly financial

statement that consist of income statement, balance sheet, and inventory valuation

summary. This process had already been done ever since it was built until the end

of 2017.

However, in the beginning of 2017 when the company’s business keep

expanding, these accounting process could not keep up with the tasks and

transactions being given to Accounting & Finance Department. That result to the

delayed time in creating and presenting the monthly financial report from 2 or 3

days after the end of month to 2 or 3 weeks. With these circumstances, the decision

making process that relied on monthly financial report also affected. The company

usually order for resupply inventory at the beginning of month dragged into middle

of next month due to these lateness. Due to ordering the inventory around middle

of next month resulting on the goods delivered to the company at the end of month

during the ordering month. That situation was very risky for the stock of inventory

in that company especially when they had zero stock of inventory and there were

7

some customers ordered that products. Which make the company lost some of its

customers for not having inventory prepared for them. According interview result

from the General Manager, those situation already happened for several times in

2017, but the customers were still able to tolerate that situation and wait until the

inventory were ready. Therefore, the problem lead into the timeliness factor of the

accounting process that need to be improved and updated with current new

technologies by using computerized accounting process.

Also, the other function that decision making relied upon the monthly

financial report for providing the bonus reward for the General Manager from the

Board of Directors of PT. Trisan Pakar Baja. The monthly financial statement

mostly will be reviewed by the Board of Director for gaining the financial insight

of this company. When, the company is in profitable situation, the Board of Director

will provide the bonus personally for the General Manager as the present for his

effort. However, since there was lateness in presenting monthly financial report

affect to the time of incentive provided. Where this result might impact the General

Manager behavior to be less motivated in making the company more profitable.

These condition is important for the company’s initiative especially the General

Manager in this company being responsible for decision making on profitable daily

activities.

In order to implement the new computerized accounting process in the

company to solve timeliness, there will be need strong foundation for all of accounts

that presented in financial statement to avoid misleading information. To ensuring

the quality of information, it need to be determine by comparing all of accounts

8

whether in accordance with the existing conceptual framework especially in faithful

representation concept. The faithful representation aspects focus in presenting the

reliable financial information by checking all the accounts with completeness,

neutrality, and free from error as part of quality that focused by faithful

representation.

During the checking of all the accounts towards the faithful representation

aspects, there were several errors detected in the accounts recorded. The error

related with misstatement in the recordings of book value of vehicle fixed assets.

In that value of credited vehicle fixed assets, there are overstatements of the value

of the assets that mismatch with the documentation (invoice). These overstatement

appeared due to capitalizing of all interest expense that need to be paid as the initial

recording during the acquisitions. Also, The method of capitalizing interest

conducted by the Accounting & Finance Department due to not knowing the

existing rule for treating these kind of transactions. With that conditions, provide

the researcher need to solve these problems first to assure that the accounts are in

accordance with faithful representations before converted into the computerized

accounting process to ensure the quality of information provided and help to solve

the timeliness issue.

In conclusion, the existing problems could be identified into several

research questions which are:

1. How to solve the accounting information system problem occurred in the

company which resulting the delay in generating financial statement?

2. How to assure all of accounts in comprehend with faithful representation?

9

Questions that will need to be investigated in this research whether the

solution provided by researcher capable in solving the company’s current

accounting process using Intuit Quickbooks as the new method of recording and

reporting. This research will solving, translating and implementing the new

computerized accounting process that is in accordance with existing standard of

accounting.

1.3. Research Scope and Limitation

PT. Trisan Pakar Baja concerns in upgrading their accounting process by

adopting the new accounting software to improve general ledger and financial

statement. The company already approved and accepted to implement Intuit

Quickbooks as their new accounting process. Therefore, this research will focus on

general ledger and financial statement conversion to Intuit Quickbooks by using the

existing daily operations activities in the company as the data sources.

This study will focus on the journalizing process of this company as the first

step and process it for creating the monthly financial statement with the use of Intuit

Quickbooks software. Besides from that, this research will translating the current

accounting process of the company in computerized method in Intuit Quickbooks

which will create the synchronization of existing procedures by using the source of

data from existing operations of the company. These procedure conducted in order

to improve the effectiveness in recording the transactions and ensuring to generate

the monthly financial statement on time (at the end of month).

10

1.4. Research Objectives

Due to lateness of decision making from conventional method of accounting

control adopted by PT. Trisan Pakar Baja researcher will conduct research, with the

objectives:

1. Success in journalizing all of the transactions in accordance with faithful

representations concepts embed in each accounts for providing non-

misleading information.

2. Success to convert the current general ledger and reporting cycle of PT.

Trisan Pakar Baja into Intuit Quickbooks as the new computerized

accounting process for this company in order to improve the timeliness in

reporting financial statement.

1.5. Research Benefits

This research will provide benefit about improving current conditions of

accounting process in the company that impacted to the decision making that based

on timeliness and precise information financial report. Moreover, this research will

be expected to be beneficial for the following parties and uses:

1.5.1 For the Researcher

Researcher will obtain more knowledge regarding the accounting process

of the company especially in general ledger and reporting. Also, it will provide the

additional knowledge in converting the existing accounting process into accounting

software.

11

1.5.2 For Future Researchers

This research will provide the readers better understanding toward the

company’s accounting process. Specifically the research will focus on the aspects

of general ledger and reporting for the faithful representations and timeliness in

presenting monthly financial report. Furthermore, it will give insight for readers to

test other possibilities of software or program to be implemented for improving

other aspect of internal company’s activities.

1.5.3 For PT. Trisan Pakar Baja

The benefits for the company is to be able to identify and present the reliable

information related with the accounting information that happened during the

accounting process adopted and provide improvement in faithful representation and

timeliness of the company in generating the monthly financial statement for

decision making process.

1.6. Research Method

1.6.1 Interview

Based on Arens et al. (2017) interview means giving oral questions or

discussion from the members of the company being researched. From the

invalidated information obtained will be validated with other procedures.

1.6.2 Observation

Based on Arens et al. (2017) observation mean obtaining information

related with company situation, activities, and procedures of certain task, and work

environment by observation itself (smelling, hearing, feeling, and seeing).

12

1.6.3 Documentation

Based on Arens et al. (2017) documentation refers to tracking down the

internal or external evidences from the researched transactions or activities.

Furthermore, the result form investigation will be explained later on by the

researcher.

1.6.4 Tracing

According to Arens et al. (2017), tracing refers to activity in tracking the

recordings of transactions back into the document source all the way until the

financial statements reporting. This method will be used by the researcher to ensure

the faithful representation concepts existed in each accounts of PT. Trisan Pakar

Baja.

1.6.5 Vouching

According to Arens et al. (2017), vouching refer to activity that ensuring

the amount that existed in financial statement can be found in the original

recordings or documents that proved that transactions exist. This also another

method used by the researcher to provide the assurance that faithful representations

concepts already appeared in each accounts of the company.

1.6.6 Conversion

This method refers to changing the existing condition into the new activities

that lead into same end results (Kawulich, 2004). Before these method conducted,

the existing condition need to be prepared thoroughly and free from error to avoid

failure in conversion.

13

CHAPTER II

LITERATURE REVIEW

2.1. Faithful Representation as Fundamental Quality of Financial

Statement

In presenting the financial statement for the use of stakeholders, it need to

concern about the quality of information presented (Krismiaji et al., 2016).

According to Krismiaji et al. (2016), the quality in reporting is essential as the basis

for economic decision making for internal and external party. In high quality of

financial statement, the faithful representation will be the core concept that need to

be embed in the statement (Cheung et al., 2010). Faithful representation refers to

the representation of financial condition that related with amount and details are

same with the real condition that existed. The concept of faithful representation

exist as part on conceptual framework of qualitative reporting that focus in

representing the information regarding financial conditions of the company to be

not misleading (Kieso et al., 2011).

In order to obtain faithful representation in financial statement quality,

several ingredients of fundamental quality need to be existed and conducted

altogether. There are three essential areas which are completeness, neutrality and

free from error (Kieso et al., 2011). The completeness refers to the all content of

information presented in financial report have provided thoroughly (Kieso et al.,

2011). Then, neutrality concern in limiting the company in selecting the

14

information for one of party interest only over another (Kieso et al., 2011). Finally,

all information that presented need to be free from error to provide accuracy

representation of financial information of the company.

Financial statement is important since the several decisions require financial

statement as their base in making decision for internal or external perspective.

Without the quality, misleading and information asymmetry could be possible to be

happen and will impact to wrong decision that taken for.

2.2. Timeliness in Financial Reporting

As the quality aspects are important for the financial report presented,

timeliness also become additional aspect to add the relevancy of information

(Agyei-Mensah, 2018). Timeliness refers to the availability of information at the

point of decision-makers need it. The other capability of timeliness related in

reducing the environmental uncertainty especially in making decision using the

timely information (Gullberg, 2016). When the information could not be available

at needed time or available for longer period after the reported transaction, it will

give no value toward future action since the relevancy of information decreasing

and becoming less useful. Therefore, lack of timeliness will be able to lower

relevancy of information especially for the decision of future action.

15

2.3. Manual Accounting Process and Computerized Accounting

Process

The accounting process always exist in each company for presenting

financial information of the company (Ji et al., 2016). This process itself refers to

the step by step procedures from the recording of transactions to journal, post to

ledger, prepare the trial balance, prepare adjustment of end of period trial balance,

and finally preparing the financial statement.

The accounting process has already been growing to provide more

convenience and saving cost while presenting the high quality of information.

Based on Victoria (2017), there are transition from manual accounting process until

the recent development of computerized accounting process that mostly used by the

companies. Manual accounting process implies the employee will conduct the

accounting process manually on periodic basis from journalizing until the creation

of financial statements which requires a lot of time spent and effort to conduct the

process. However, using computerized accounting means the employee only

conduct recording of the transaction to the computer that already been installed with

certain accounting software and the rest of the process will be automatically

processed until the financial report.

The main advantages of computerized accounting will definitely provide the

timeliness of reporting as the effectiveness of work increasing which can reduce the

amount of error happened in manual accounting (Victoria, 2017). Grant et al. (2008)

also supported the use of computerized accounting to be accounting process of the

16

company, where the use of the accounting software will reduce the significant error

that usually appeared in financial report.

2.4. Intuit Quickbooks

Quickbooks is software developed by Intuit. This software coverages in

accounting section in business area. One capability of this software is its ability to

confront on a whole accounting process in one business (McCraigh et al. 2000).

Also, there are nine significant features that differentiate Intuit Quickbooks with

other accounting software according to Schiff & Szendi (2014) which are: 1)

organized main interface on daily business operations; 2) command using English-

language; 3) Error can be adjusted; 4) a single journal combined all transactions; 5)

help certain transaction to be efficiently inputted; 6) closing entries at the end of

fiscal year are unnecessary to conducted; 7) payroll tax returns can be easily printed

and income tax return can be connected with various individual accounts; 8)

Extensions software, which are internet banking and verification of credit card, can

be synchronized with this software to increase convenience and efficiency of

transaction; 9) Personalized version of Intuit Quickbooks based on the industries or

variant users are available. These features made the popularity of using this

software as main operation in handling all financial transactions in the firm rather

than manual accounting process and other software.

According to Schiff & Szendi (2014), the Intuit Quickbooks software

already almost used by the small business in United States. The reasons behind it

due to use uniqueness and simplicity of this software towards the accounting

17

process in the business. The capability and features in handling the accounting

aspect in business provide convenience for the users that lack with accounting

background (Perry, 2006). However, Schiff and Szendi (2014) suggested that

person with the accounting background should be the one handle this software in

order to avoid any kind of error during the inputting the data and due to the

accountant is the person who understand the process of creating reliable financial

statement. Therefore, the user need to be someone that at least have knowledge of

accounting in principle for the implementation of accounting process from using

this software.

18

CHAPTER III

DATA PROCESSING METHOD AND COMPANY’S

EXISTING CONDITION

3.1. Data Collecting and Processing

This research will improve and convert the current accounting process of

PT. Trisan Pakar Baja. Data collection was conducted to gather the evidence and

insight regarding the condition of the company by conducting interview with

related stakeholders, observation, and documentation.

3.1.1 Interview

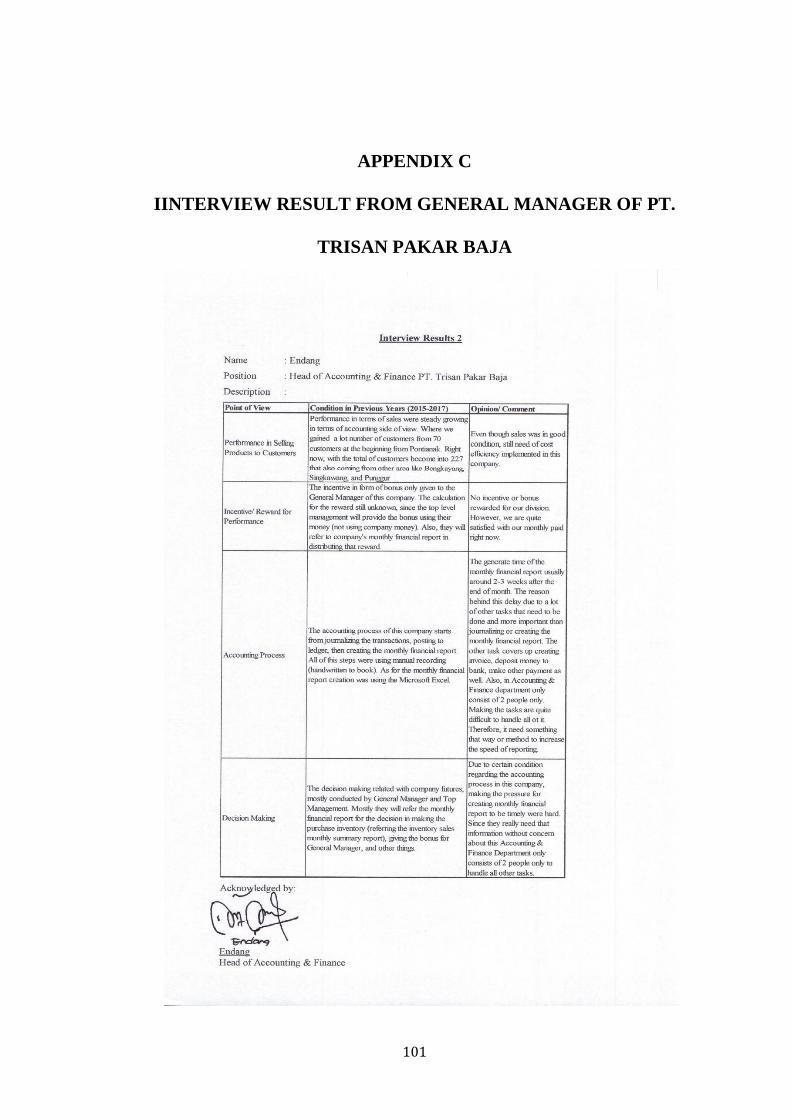

Researcher conducted unstructured interview with General Manager and

Head of Accounting & Finance for the concern about the current accounting process

did by the company that lead toward decision making process. The real interview

results from General Manager and Head of Accounting & Finance can be seen in

Appendix B and C. The summary of information obtained by the researcher during

interview are:

1. PT. Trisan Pakar Baja consistently having growth from year over year

since it was founded on 2015, which came from getting more diverse

type of customers from time to time. In 2016, the numbers of customers

of PT. Trisan Pakar Baja were only 70 customers and all of them reside

in Pontianak, West Borneo. Then in 2017, sudden increase in the

19

numbers of customers and the different area that customers reside in the

total of 157 new customers varied from other area such as Singkawang,

Punggur, Bengkayang.

2. PT. Trisan Pakar Baja accounting process mainly constructed from the

moment of the invoice or any supporting documents came to the

Accounting & Finance Department, all of transactions will be

collectively journalize at near end of working time in the empty blank

sheet. At the end of month all of the journal will be directly grouped

based on each accounts and totaled the amount alongside with the other

necessary adjustment entries that need to be made too. After that, the

grouped account will be used to make the financial statement.

3. PT. Trisan Pakar Baja’s Accounting & Finance Department only

consist of two persons which one act as Head of Accounting & Finance

and the other as the Vice. They explained responsibilities of the

Accounting & Finance Department not only to prepare the financial

statement, but to make the invoice, deposit money to bank, make

transfer payment, settle any expenditures for operation and conducting

stock opname. Due to overwhelming transactions need to be processed

by the company, the financial statement tend to get delayed until middle

of next month rather than in the end of month.

4. General Manager of PT. Trisan Pakar Baja confessed that during year

of 2017 as the business expanding, he sensed the lateness on making

decision for resupplying inventories from supplier since he usually

20

refers to the monthly financial report especially on inventory evaluation

summary as the part of consideration. The decision will be based on

percentage of retail contained in that inventory evaluation summary for

the each item to be exceed 10% of the retail amount and the resupply

can be conducted on each item that meet that criteria.

The General Manager felt that delay is the main problem since monthly

financial statement provided by the Accounting & Finance department

from usually at four or five days after the end of month into two or three

weeks after the end of month. Also, the General Manager was afraid if

this condition continued further it will make certain demanded product

will be out of stock when customers wanted to purchase the product

which will make the company lost their customer.

5. Both of General Manager and Head of Accounting & Finance confess

that they need some kind of accounting software that can help them to

create faster financial report without trouble by only input the journal

of the transactions

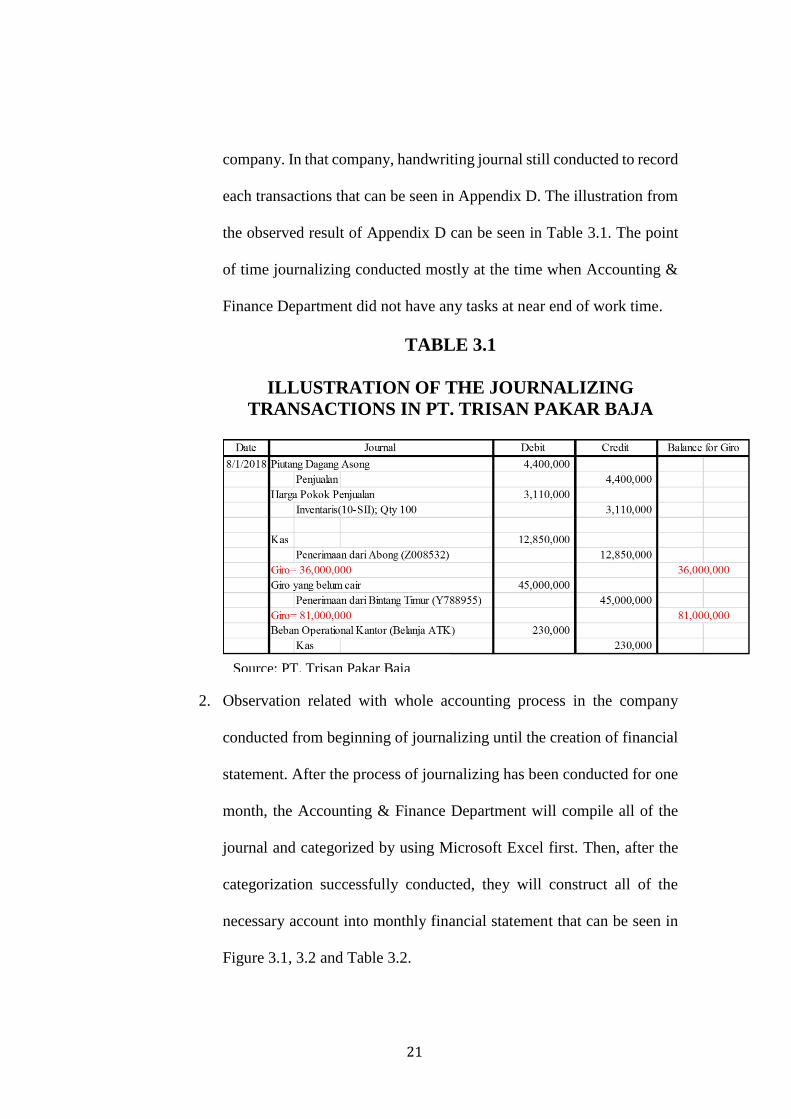

3.1.2 Observation

During the four months of observation in PT. Trisan Pakar Baja, researcher

could obtain data and information. The researcher observes PT. Trisan Pakar Baja

employee’s activities especially in Accounting & Finance Department. Result of

observation obtained by researcher:

1. Observation in accounting process in the company especially in

journalizing the transactions that occurred in daily operations of the

21

company. In that company, handwriting journal still conducted to record

each transactions that can be seen in Appendix D. The illustration from

the observed result of Appendix D can be seen in Table 3.1. The point

of time journalizing conducted mostly at the time when Accounting &

Finance Department did not have any tasks at near end of work time.

TABLE 3.1

ILLUSTRATION OF THE JOURNALIZING

TRANSACTIONS IN PT. TRISAN PAKAR BAJA

2. Observation related with whole accounting process in the company

conducted from beginning of journalizing until the creation of financial

statement. After the process of journalizing has been conducted for one

month, the Accounting & Finance Department will compile all of the

journal and categorized by using Microsoft Excel first. Then, after the

categorization successfully conducted, they will construct all of the

necessary account into monthly financial statement that can be seen in

Figure 3.1, 3.2 and Table 3.2.

Source: PT. Trisan Pakar Baja

22

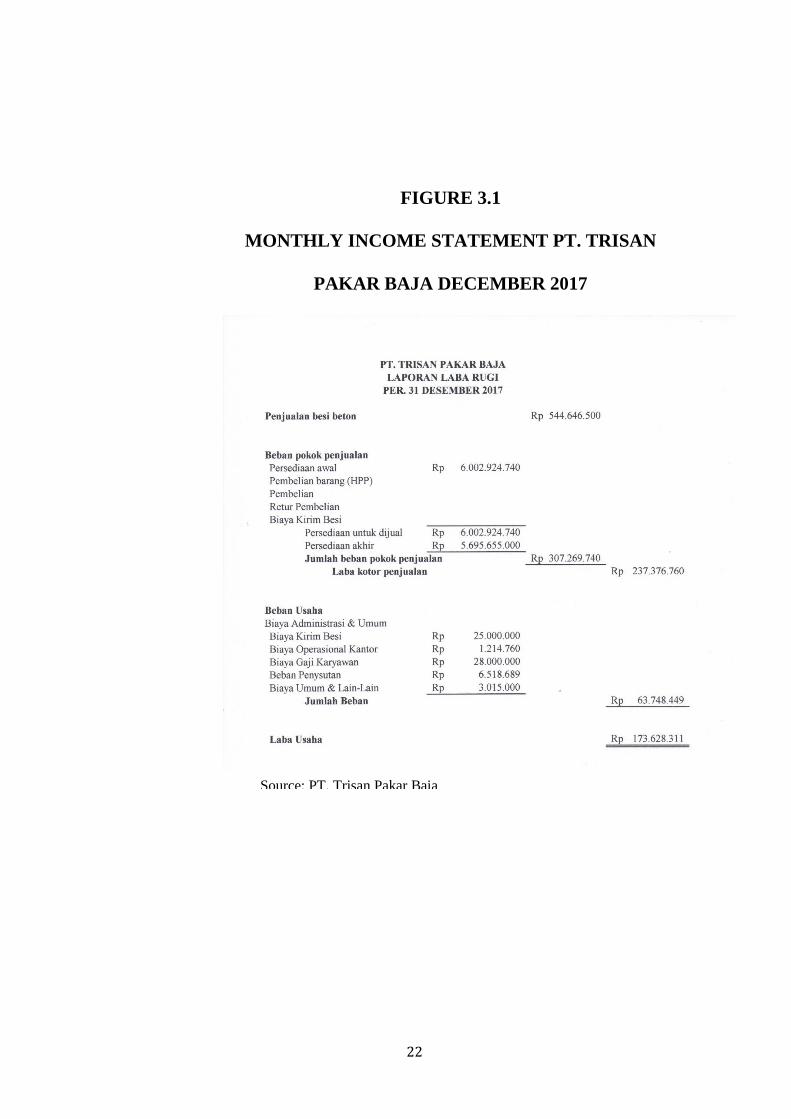

FIGURE 3.1

MONTHLY INCOME STATEMENT PT. TRISAN

PAKAR BAJA DECEMBER 2017

Source: PT. Trisan Pakar Baja

23

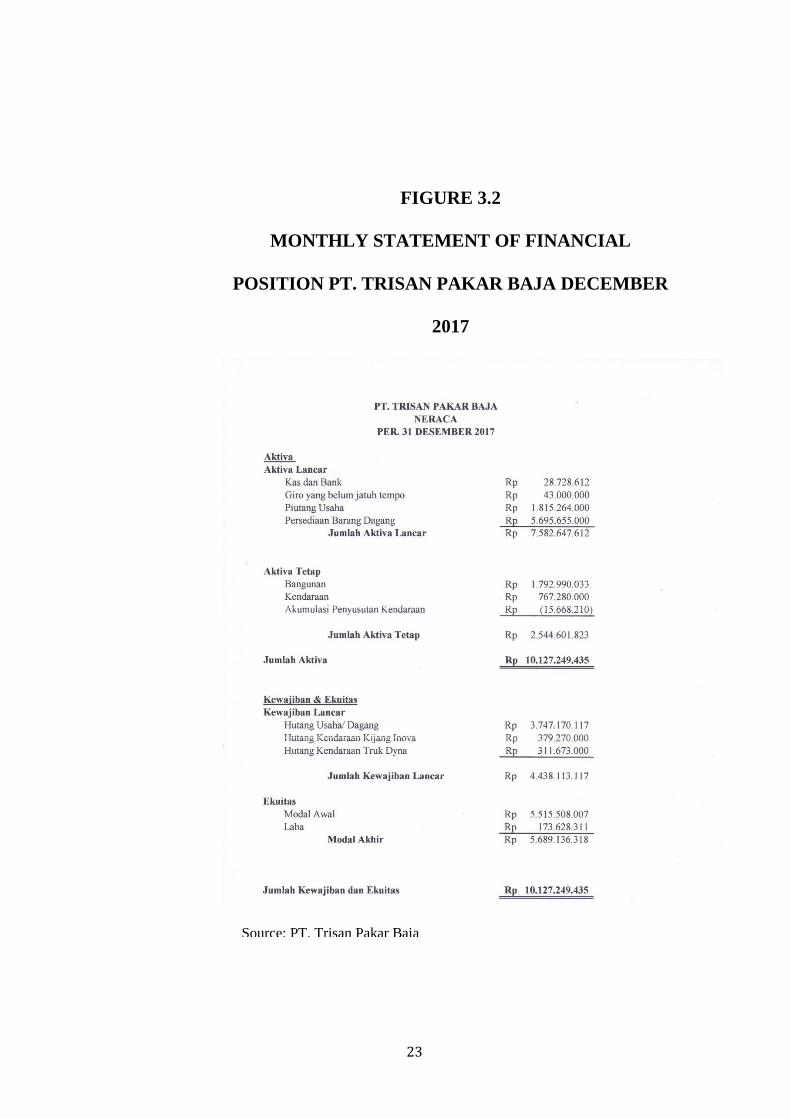

FIGURE 3.2

MONTHLY STATEMENT OF FINANCIAL

POSITION PT. TRISAN PAKAR BAJA DECEMBER

2017

Source: PT. Trisan Pakar Baja

24

TABLE 3.2

MONTHLY STATEMENT OF FINANCIAL

POSITION PT. TRISAN PAKAR BAJA DECEMBER

2017

3.1.3 Documentation

Source: PT. Trisan Pakar Baja

25

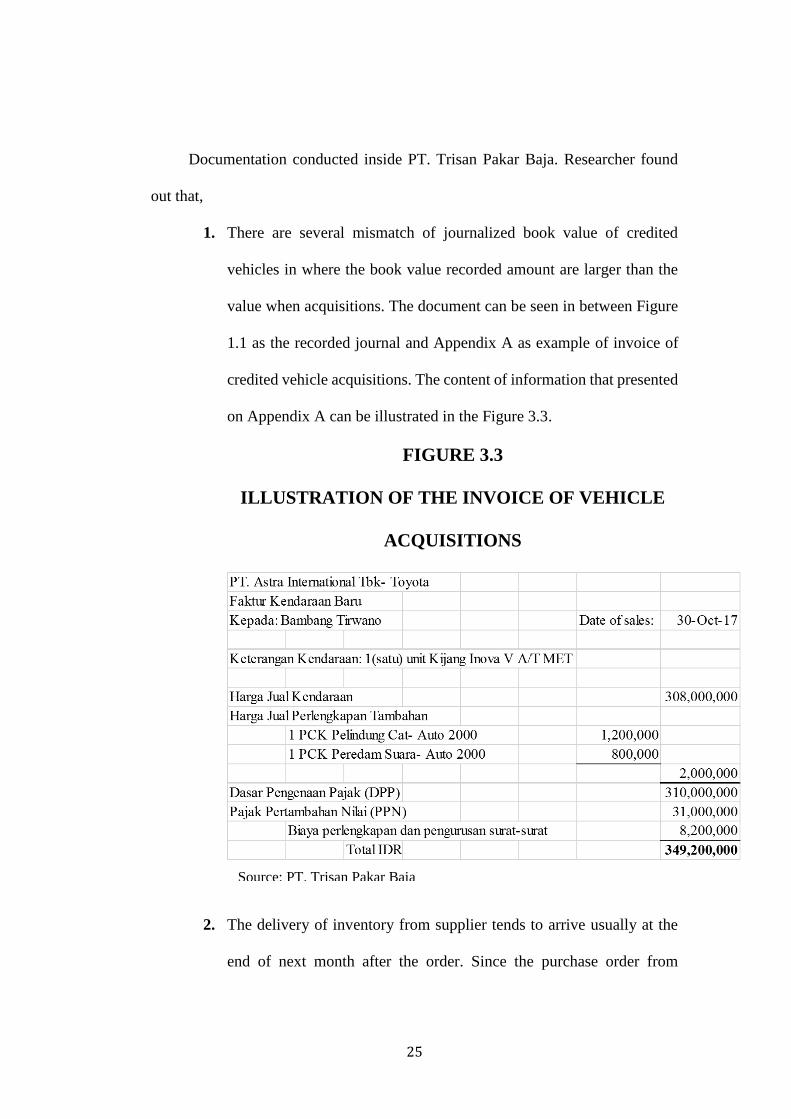

Documentation conducted inside PT. Trisan Pakar Baja. Researcher found

out that,

1. There are several mismatch of journalized book value of credited

vehicles in where the book value recorded amount are larger than the

value when acquisitions. The document can be seen in between Figure

1.1 as the recorded journal and Appendix A as example of invoice of

credited vehicle acquisitions. The content of information that presented

on Appendix A can be illustrated in the Figure 3.3.

FIGURE 3.3

ILLUSTRATION OF THE INVOICE OF VEHICLE

ACQUISITIONS

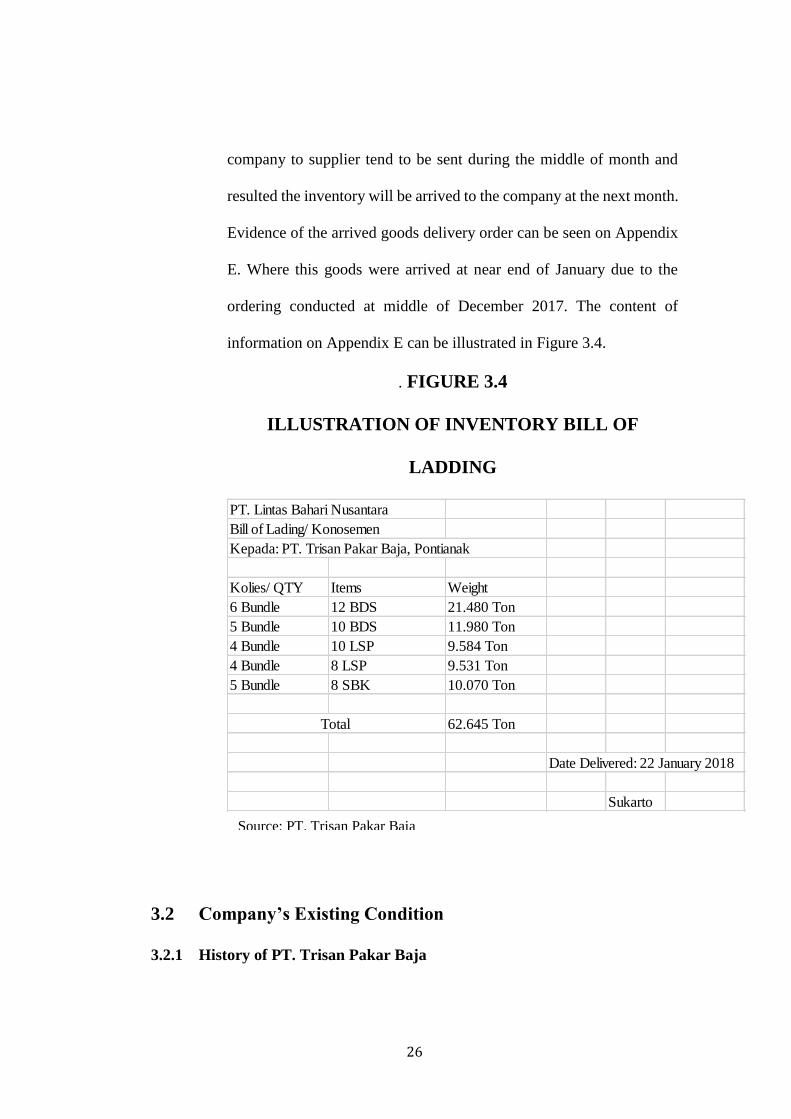

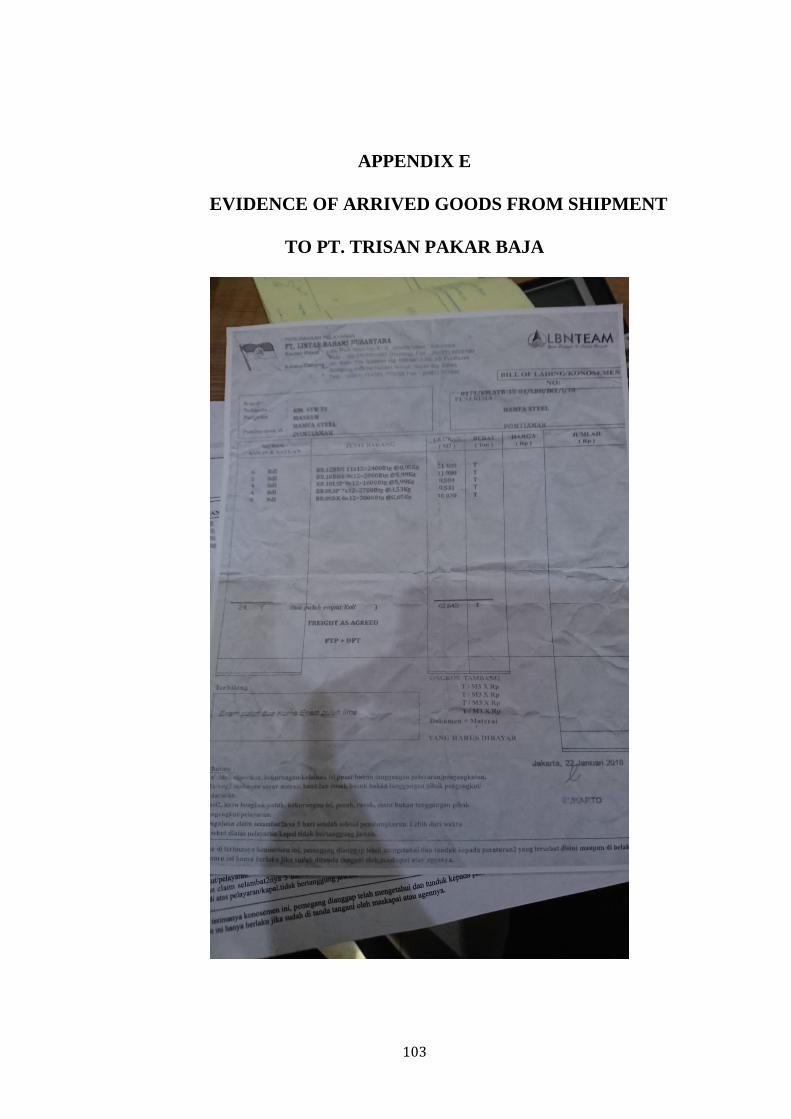

2. The delivery of inventory from supplier tends to arrive usually at the

end of next month after the order. Since the purchase order from

Source: PT. Trisan Pakar Baja

26

company to supplier tend to be sent during the middle of month and

resulted the inventory will be arrived to the company at the next month.

Evidence of the arrived goods delivery order can be seen on Appendix

E. Where this goods were arrived at near end of January due to the

ordering conducted at middle of December 2017. The content of

information on Appendix E can be illustrated in Figure 3.4.

. FIGURE 3.4

ILLUSTRATION OF INVENTORY BILL OF

LADDING

3.2 Company’s Existing Condition

3.2.1 History of PT. Trisan Pakar Baja

PT. Lintas Bahari Nusantara

Bill of Lading/ Konosemen

Kepada: PT. Trisan Pakar Baja, Pontianak

Kolies/ QTY Items Weight

6 Bundle 12 BDS 21.480 Ton

5 Bundle 10 BDS 11.980 Ton

4 Bundle 10 LSP 9.584 Ton

4 Bundle 8 LSP 9.531 Ton

5 Bundle 8 SBK 10.070 Ton

62.645 Ton

Date Delivered: 22 January 2018

Sukarto

Total

Source: PT. Trisan Pakar Baja

27

Mr. Fajar Tjandra is the founder of PT. Trisan Pakar Baja. The company

was established in Pontianak, West Borneo on 2015. PT. Trisan Pakar Baja build

as a distributor of steel company, which helps other companies or projects to fulfill

their need of resources in building construction or for selling. PT. Trisan Pakar Baja

continuing as a resources provider due to less number of distributor in steel operated

in Pontianak and great demand of steel in Pontianak, made them able to operate

well.

3.2.2 PT. Trisan Pakar Baja’s Operation

As in 2015 until right now, PT. Trisan Pakar Baja act as the distributor of

steel in Pontianak. The main operation that conducted by this company is trading

steel products. The product that are traded consist of:

Plain Steel, this type of steel is one of the most purchased items due to its

function for main material for building construction in order to create strong

foundation. This product varies into several size which are 4 mm x 10 m; 5

mm x 10 m; 5 mm x 12 m; 6 mm x 10 m; 6 mm x 12 m.

Threaded Steel Bars, this product is the second best seller item that used

alongside with plain steel bars. As the use of this threaded steel bars mainly

complement with the use of plain steel bars. This product also varies in

terms of size which can be defined into 10 DMK, 13 DMK, and 13 DMK-

2.

Elbow steel, this product is one of the newest product that offer by this

company to the customers around October 2017. This product mainly help

in construction of building especially in connecting between steels in order

28

to create more than one floor building and etc. This product varies with the

size which are Siku 30, Siku 40, Siku 50.

All of the current stock and details of each quantity of stock can be seen in

Inventory Evaluation Summary of PT. Trisan Pakar Baja in Desember 2017 at the

Figure 3.4. That report contains the details of beginning stock of each inventory and

how much inventory being sold and resupplied to get the ending quantity of each

inventory.

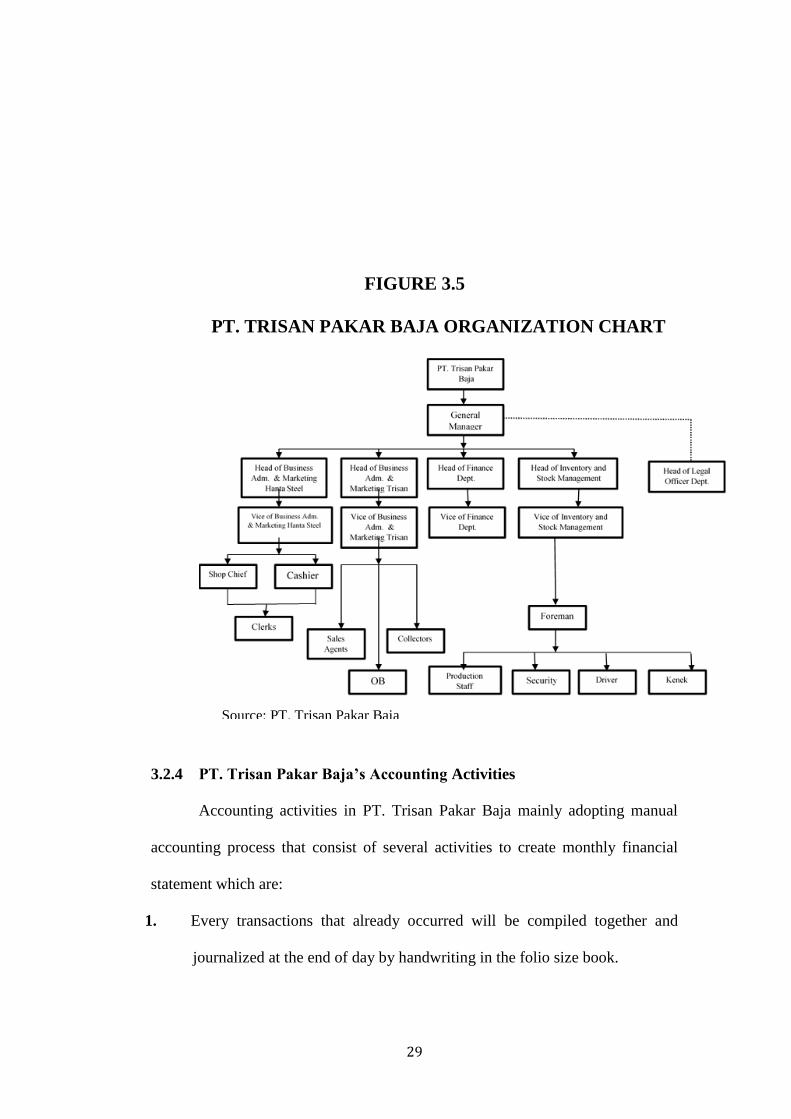

3.2.3 PT. Trisan Pakar Baja’s organization structure

This research will only focus in observing on Accounting & Finance Department

activities on accounting process especially in journalizing and reporting activities.

PT. Trisan Pakar Baja Organization Structure Chart can be seen on Figure 3.5.

Where the total of employees that worked in this company only twenty five

employees with the Accounting & Finance Department only two people handling

that department, one as the head of Accounting & Finance Department and the other

as the Vice of this department.

29

FIGURE 3.5

PT. TRISAN PAKAR BAJA ORGANIZATION CHART

3.2.4 PT. Trisan Pakar Baja’s Accounting Activities

Accounting activities in PT. Trisan Pakar Baja mainly adopting manual

accounting process that consist of several activities to create monthly financial

statement which are:

1. Every transactions that already occurred will be compiled together and

journalized at the end of day by handwriting in the folio size book.

Source: PT. Trisan Pakar Baja

30

2. After the transactions recorded already one month, all of the journalized

journal will be sorted based on each account and summation also conducted

to get the amount. These step conducted by using Microsoft Excel.

3. Financial statement can be constructed by using account that already prepared

from previous step. In preparing and presenting the financial statement the

company used Microsoft Excel.

3.3 Consideration of PT. Trisan Pakar Baja Accepting Adoption

of Intuit Quickbooks

In order to improve the company accounting control especially in the flow

of reporting, Intuit Quickbooks software was introduced to the General Manager

and Head of Accounting & Finance in the company. In order get approval to install

these software, the author explain the advantages of using this software compared

with the other accounting software such as Xero, Freshbooks, Wave, and Zoho in

the following explanations:

1. User-friendly interface that provided by Intuit Quickbooks make it easy to

use and understandable even for someone without any of accounting

background.

2. Integration with whole operations in the business compared with other

competitors software, make Intuit Quikbooks become convenient tools to

control and monitor the existing operations in the business.

3. The customization based on the need and business type of each company

can be conducted by using Intuit Quickbooks. That allows the company to

31

set the projected report in the form of table, diagram, or in the financial

statement for showing financial condition of company right now.

These features of Intuit Quickbooks become good input to explained to

General Manager and Head of Accounting & Finance in PT. Trsian Pakar Baja,

made them accepted and approved the implementation of Intuit Quikbooks to their

accounting process. That will lead this research focus toward beginning

implementation of Intuit Quikbooks. It need to be started from the setting up of the

chart of accounts until the setting up recording the daily transactions occurred in to

setting up a complete monthly financial statement.

32

CHAPTER IV

ANALYSIS AND EVALUATION

There are one of the major aspects that become focus in this study, which is

decision making process conducted by general manager of PT. Trisan Pakar Baja

that concerned with faithful representation and timeliness issues in presenting

monthly financial statement. In each issues there are several problems existed in

the current condition of this company. First, regarding the faithful representation

leading the free from error concern related with misstatement by capitalizing

interest expense on vehicle fixed assets account. Next, regarding the timeliness

issue that lead toward the timing issue/ punctuality of generating monthly financial

statement that could halt the decision in resupplying inventory and bonus reward

for General Manager from Superior since these report will be the basis on those

decisions.

33

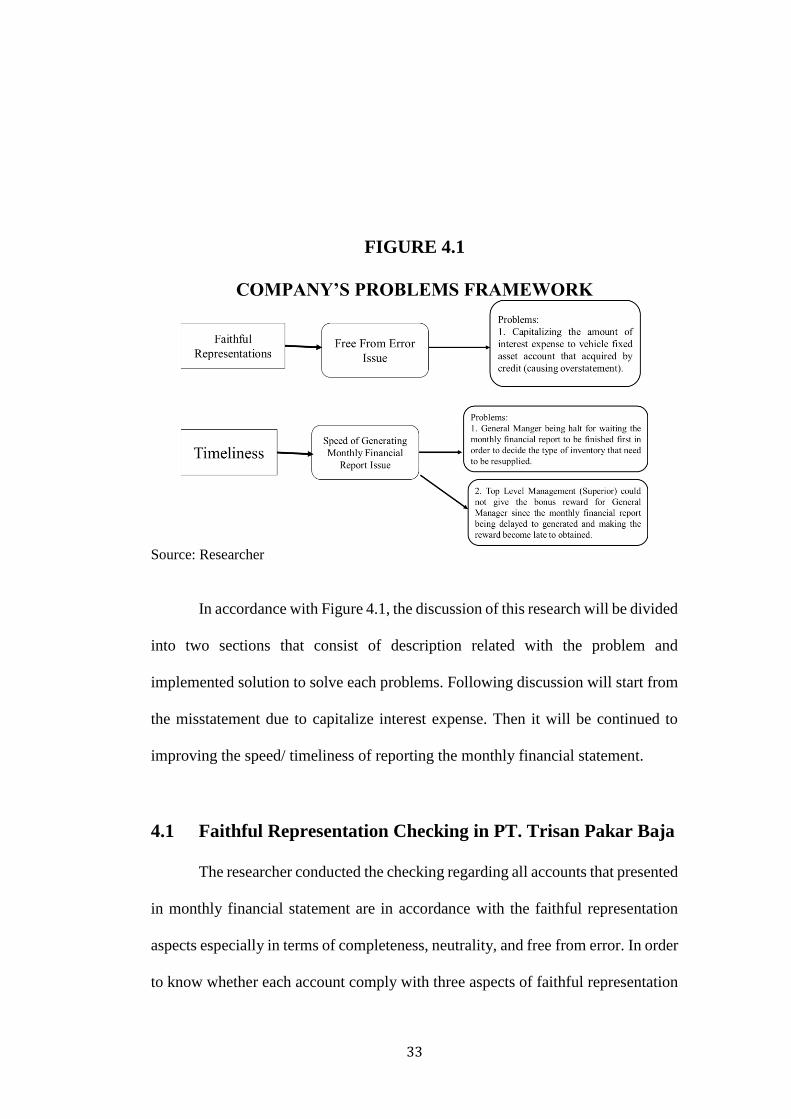

FIGURE 4.1

COMPANY’S PROBLEMS FRAMEWORK

Source: Researcher

In accordance with Figure 4.1, the discussion of this research will be divided

into two sections that consist of description related with the problem and

implemented solution to solve each problems. Following discussion will start from

the misstatement due to capitalize interest expense. Then it will be continued to

improving the speed/ timeliness of reporting the monthly financial statement.

4.1 Faithful Representation Checking in PT. Trisan Pakar Baja

The researcher conducted the checking regarding all accounts that presented

in monthly financial statement are in accordance with the faithful representation

aspects especially in terms of completeness, neutrality, and free from error. In order

to know whether each account comply with three aspects of faithful representation

34

or not, several requirements have been set in completeness, neutrality and free from

error aspects alongside with the method that will be conducted to check:

In completeness, all of the existing accounts need to be presented from the

beginning of recording until in financial statement without omitting any part

of information. That means, the checking on all of the accounts started on

transactions that happened in the beginning of December 2017 until the end

of month. In condition where the certain accounts that listed on company’s

chart of account such as vehicle and building did not appear during the

journalizing in December 2017, the researcher will look into the existing

journal related with that account to assess the completeness aspect.

As for neutrality refers to capability of each account to present based on the

reality without favoring one concerned parties over another. Where this

aspect refer to the how the recognition of the basis in each account. In order

to check whether all of the account using the consistent same basis from

time to time, the checking will be based on comparing the date of recording

of the transactions with the existing documents such as invoice, bills, or

other supporting documents. Since different recording time will result on

different value to be presented in financial statement. Therefore, the

checking will conducted to all of journalized transactions that occurred

during December 2017 until the end of that month by comparing it with the

supporting documents. The range of time checking conducted in

transactions occurred during December 2017 due to reassure that all of the

transactions been recorded properly since the balance amount of December

35

2017 will become the beginning balance for the new recordings that start in

January 2018.

Finally for free from error aspect, it requires for all of the accounts to be

accurate for presenting the value in financial statement. Specifically, the

value that represent each account need to free from misstatement especially

in the form of estimation of several accounts that require it. That means,

vouching will be conducted in order to ensure estimation in defining the

value such as vehicle, building, depreciation accounts. Moreover, in order

to confirm other accounts for free from error, the tracing will be conducted

to the journalized transactions in December 2017 till the end of month by

comparing the existing supporting documents whether the amount recorded

are same.

At that time, the researcher found out that all of the accounts were complete

and neutral. However, there are issues identified in several accounts due to

overstatement value of vehicle fixed accounts. The list and result of accounts that

have already been checked by researcher can be seen in Table 4.1.

36

TABLE 4.1

CONDUCTED CHECKLIST OF ALL OF ACCOUNTS IN

PT. TRISAN PAKAR BAJA

Completeness Neutrality Free from Error

Kas & Bank V V (Accrual Basis) V

Giro yang belum jatuh tempo V V (Accrual Basis) V

Piutang Usaha V V (Accrual Basis) V

Persediaan Barang Dagang V V (Accrual Basis) V

Kendaraan V V (Accrual Basis)

X (Error regarding the

misstament of recorded

value of asset at point of

purchase)

Bangunan V V (Accrual Basis) V

Akumulasi Penyusutan Kendaraan V V (Accrual Basis)

X (Error due to

overstament of creditted

vehicle fixed asset resulting

the depreciation rate per

monthly higher than it

should be)Hutang Usaha/ Dagang V V (Accrual Basis) V

Hutang Kendaraan Mobil Inova V V (Accrual Basis)

X (Error regarding the

misstament of recorded

value of asset at point of

purchase)

Hutang Kendaraan Truk Dyna V V (Accrual Basis)

X (Error regarding the

misstament of recorded

value of asset at point of

purchase)

Modal Awal V V (Accrual Basis) V

Laba V V (Accrual Basis) V

Revenue Penjualan Besi Beton V V (Accrual Basis) V

Beban Pokok Penjualan V V (Accrual Basis) V

Biaya Kirim Besi V V (Accrual Basis) V

Biaya Operasional Kantor V V (Accrual Basis) V

Biaya Gaji Karyawan V V (Accrual Basis) V

Beban Penyusutan V V (Accrual Basis)

X (Error due to

overstament of creditted

vehicle fixed asset resulting

the depreciation rate per

monthly higher than it

should be)

Biaya Umum & Lain-Lain V V (Accrual Basis) V

Equity

Expense

Faithful RepresentationsAccounts

Type of

Accounts

Assets

Liability

Source: Researcher Note: V= Checked with no errors

X= Checked but with errors found

37

Based on Table 4.1, that list provide the result of checking in each accounts

existing in company’s financial statement. The overall explanation regarding the

checking of faithful representation aspects towards the main five categories of

account that consist of asset, liability, equity, revenue and expenses can be

explained in below:

Assets= The accounts that used by the company in this type consist of Kas

& Bank, Giro yang belum jatuh tempo, Piutang Usaha, Persediaan Barang

Dagang, Bangunan, Kendaraan, Akumulasi Penyusutan Kendaraan. The

purpose of these accounts to be existed for making the main operating

activities of this company based on the business that company have. The

assessment of the asset accounts especially in faithful representation area

that consist of completeness, reliability, and free from error define several

findings. In completeness aspects, all of the accounts are cleared this

aspects. This can be proved based on the accounting process of this

company, where at the end of month the company will recapitulate

transactions based on the related accounts for making the financial

statement. The example of recapitulate conducted by the company can be

seen on Table 4.2. All of the transactions that journalized related with

respective accounts in assets have been recorded based on respective date

(accrual basis) and amount that located in supporting documents such as

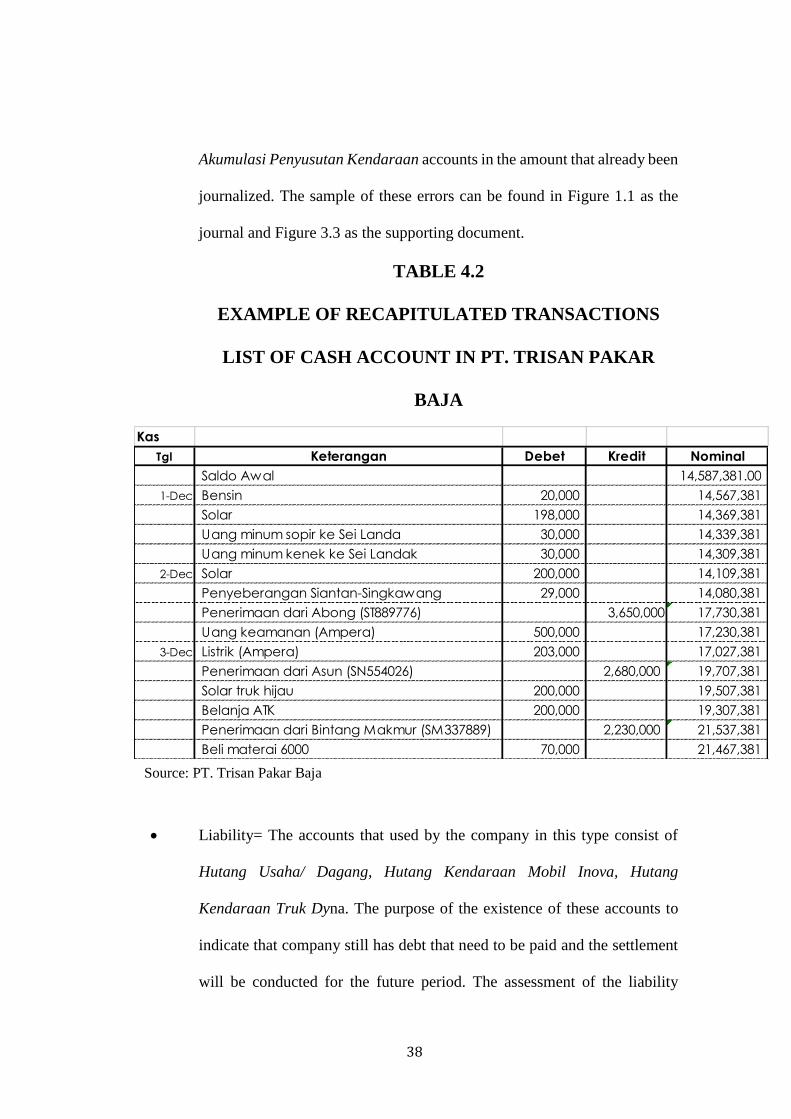

invoice, bills, or others. However, the errors are found in Kendaraan and

38

Akumulasi Penyusutan Kendaraan accounts in the amount that already been

journalized. The sample of these errors can be found in Figure 1.1 as the

journal and Figure 3.3 as the supporting document.

TABLE 4.2

EXAMPLE OF RECAPITULATED TRANSACTIONS

LIST OF CASH ACCOUNT IN PT. TRISAN PAKAR

BAJA

Liability= The accounts that used by the company in this type consist of

Hutang Usaha/ Dagang, Hutang Kendaraan Mobil Inova, Hutang

Kendaraan Truk Dyna. The purpose of the existence of these accounts to

indicate that company still has debt that need to be paid and the settlement

will be conducted for the future period. The assessment of the liability

Kas

Tgl Keterangan Debet Kredit Nominal

Saldo Awal 14,587,381.00

1-Dec Bensin 20,000 14,567,381

Solar 198,000 14,369,381

Uang minum sopir ke Sei Landa 30,000 14,339,381

Uang minum kenek ke Sei Landak 30,000 14,309,381

2-Dec Solar 200,000 14,109,381

Penyeberangan Siantan-Singkawang 29,000 14,080,381

Penerimaan dari Abong (ST889776) 3,650,000 17,730,381

Uang keamanan (Ampera) 500,000 17,230,381

3-Dec Listrik (Ampera) 203,000 17,027,381

Penerimaan dari Asun (SN554026) 2,680,000 19,707,381

Solar truk hijau 200,000 19,507,381

Belanja ATK 200,000 19,307,381

Penerimaan dari Bintang Makmur (SM337889) 2,230,000 21,537,381

Beli materai 6000 70,000 21,467,381

Source: PT. Trisan Pakar Baja

39

accounts especially in faithful representation area that consist of

completeness, reliability, and free from error define several findings. In

completeness aspects, all of the accounts are completely present the amount

in financial statements. This can be proved based on the accounting process

of this company, where at the end of month the company will recapitulate

transactions especially the purchase to supplier based on the related

accounts for making the financial statement. The example of recapitulation

conducted by the company can be seen on Table 4.3. As for reliability and

free from error aspects, most the accounts already in complied, however

several errors found in that account. Regardless of all the account are in

terms of accrual basis and the journalized value are in accordance with

supporting documents such as bills, the errors are found in Hutang

Kendaraan Mobil Inova and Hutang Kendaraan Truk Dyna accounts in the

recorded value even though the date of recording are correct. The sample of

these errors can be found too in Figure 1.1 as the journal and Figure 3.3 as

the supporting document since the accounts that involved are connected

together.

40

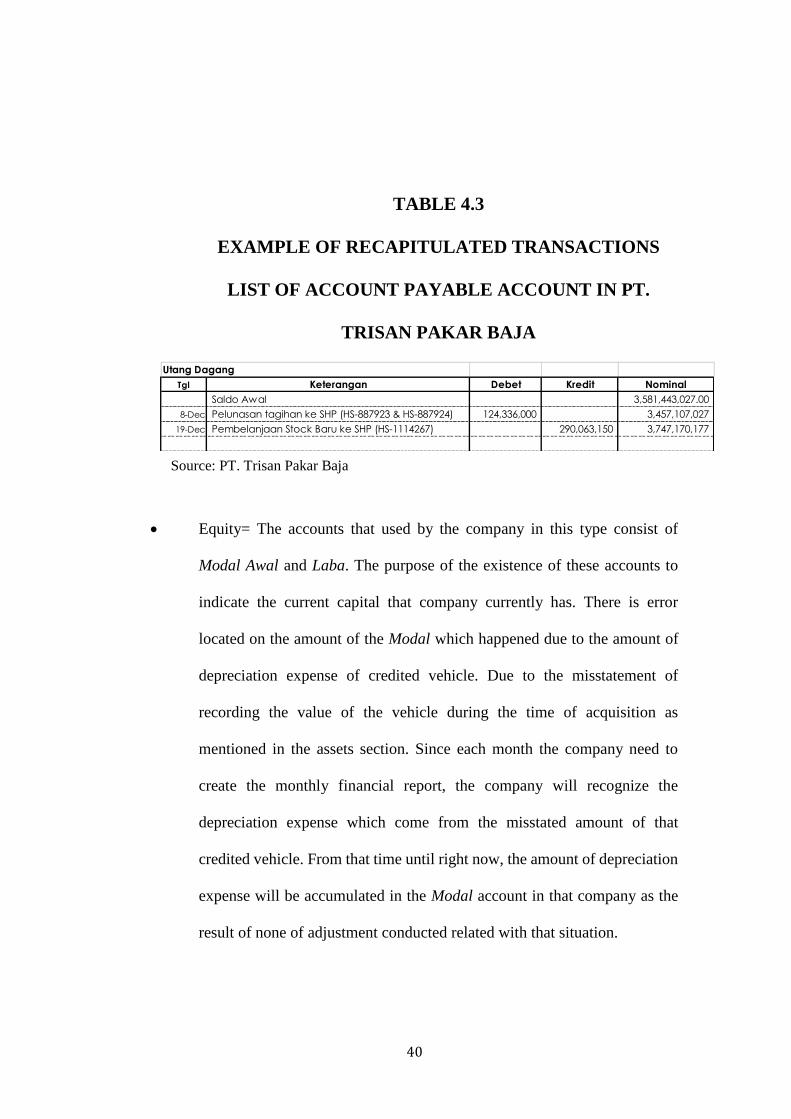

TABLE 4.3

EXAMPLE OF RECAPITULATED TRANSACTIONS

LIST OF ACCOUNT PAYABLE ACCOUNT IN PT.

TRISAN PAKAR BAJA

Equity= The accounts that used by the company in this type consist of

Modal Awal and Laba. The purpose of the existence of these accounts to

indicate the current capital that company currently has. There is error

located on the amount of the Modal which happened due to the amount of

depreciation expense of credited vehicle. Due to the misstatement of

recording the value of the vehicle during the time of acquisition as

mentioned in the assets section. Since each month the company need to

create the monthly financial report, the company will recognize the

depreciation expense which come from the misstated amount of that

credited vehicle. From that time until right now, the amount of depreciation

expense will be accumulated in the Modal account in that company as the

result of none of adjustment conducted related with that situation.

Utang Dagang

Tgl Keterangan Debet Kredit Nominal

Saldo Awal 3,581,443,027.00

8-Dec Pelunasan tagihan ke SHP (HS-887923 & HS-887924) 124,336,000 3,457,107,027

19-Dec Pembelanjaan Stock Baru ke SHP (HS-1114267) 290,063,150 3,747,170,177

Source: PT. Trisan Pakar Baja

41

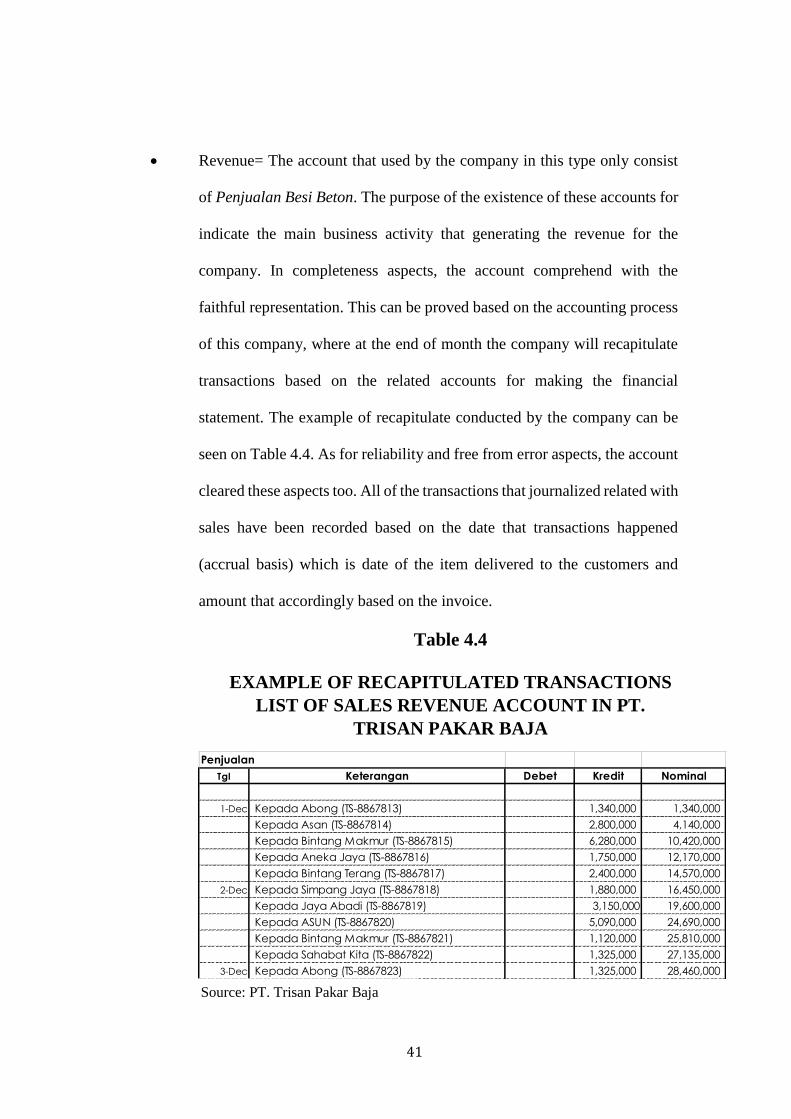

Revenue= The account that used by the company in this type only consist

of Penjualan Besi Beton. The purpose of the existence of these accounts for

indicate the main business activity that generating the revenue for the

company. In completeness aspects, the account comprehend with the

faithful representation. This can be proved based on the accounting process

of this company, where at the end of month the company will recapitulate

transactions based on the related accounts for making the financial

statement. The example of recapitulate conducted by the company can be

seen on Table 4.4. As for reliability and free from error aspects, the account

cleared these aspects too. All of the transactions that journalized related with

sales have been recorded based on the date that transactions happened

(accrual basis) which is date of the item delivered to the customers and

amount that accordingly based on the invoice.

Table 4.4

EXAMPLE OF RECAPITULATED TRANSACTIONS

LIST OF SALES REVENUE ACCOUNT IN PT.

TRISAN PAKAR BAJA

Penjualan

Tgl Keterangan Debet Kredit Nominal

1-Dec Kepada Abong (TS-8867813) 1,340,000 1,340,000

Kepada Asan (TS-8867814) 2,800,000 4,140,000

Kepada Bintang Makmur (TS-8867815) 6,280,000 10,420,000

Kepada Aneka Jaya (TS-8867816) 1,750,000 12,170,000

Kepada Bintang Terang (TS-8867817) 2,400,000 14,570,000

2-Dec Kepada Simpang Jaya (TS-8867818) 1,880,000 16,450,000

Kepada Jaya Abadi (TS-8867819) 3,150,000 19,600,000

Kepada ASUN (TS-8867820) 5,090,000 24,690,000

Kepada Bintang Makmur (TS-8867821) 1,120,000 25,810,000

Kepada Sahabat Kita (TS-8867822) 1,325,000 27,135,000

3-Dec Kepada Abong (TS-8867823) 1,325,000 28,460,000

Source: PT. Trisan Pakar Baja

42

Expense= The accounts that used by the company in this type consist of

Beban Pokok Penjualan, Biaya Kirim Besi, Biaya Operasional Kantor,

Biaya Gaji Karyawan, Beban Penyusutan, Biaya Umum & Lain-Lain. The

purpose of the existence of these accounts for supporting and ensure for

main operations of the company worked. In completeness aspects, all of the

accounts are in comprehend with the aspect. This can be proved based on

the accounting process of this company, where at the end of month the

company will recapitulate transactions based on the related accounts for

making the financial statement. The example of recapitulation conducted by

the company can be seen on Table 4.5. As for reliability and free from error

aspects, most the accounts cleared these aspects but, several errors found in

that account. All of the transactions that journalized related with respective

accounts in assets have been recorded based on the date of the transactions

happened (accrual basis) and amount that located in supporting documents

such as invoice, bills, or others. However, the errors are found in Beban

Penyusutan account in the amount that journalized even though the date of

recording are correct. This happened due to after effect from the error that

occurred in recording the acquisition value of credited vehicle that were not

same with the invoice.

43

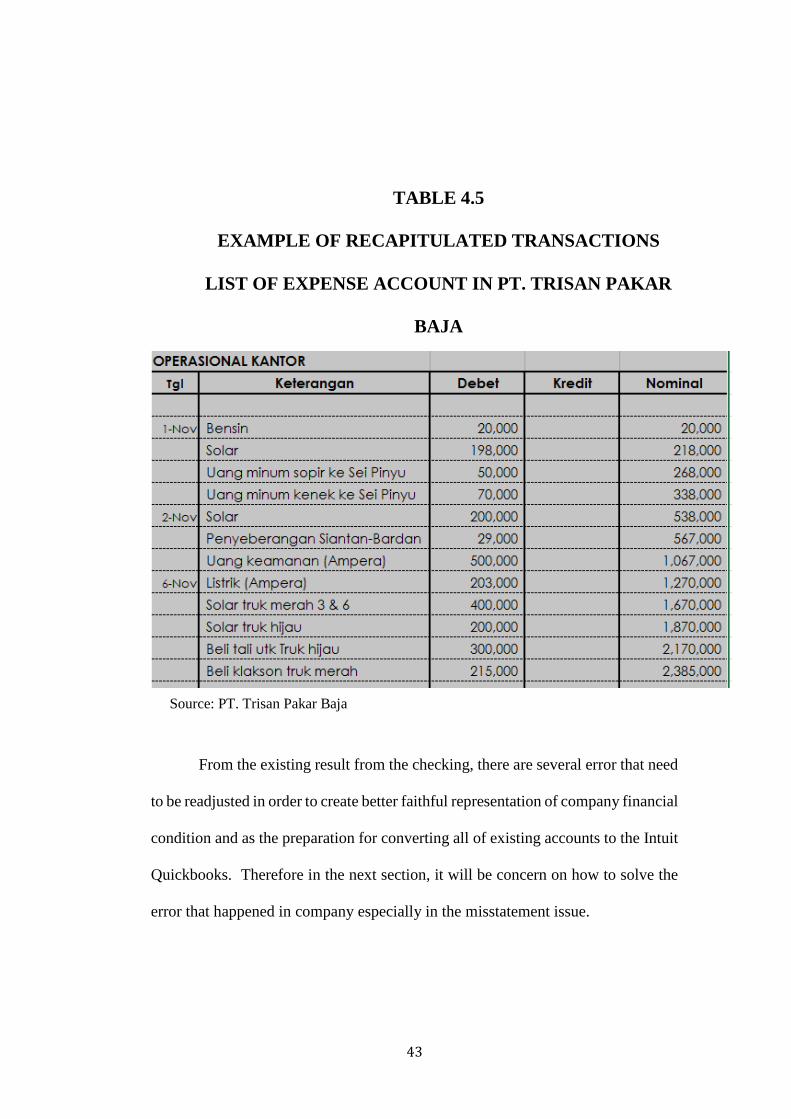

TABLE 4.5

EXAMPLE OF RECAPITULATED TRANSACTIONS

LIST OF EXPENSE ACCOUNT IN PT. TRISAN PAKAR

BAJA

From the existing result from the checking, there are several error that need

to be readjusted in order to create better faithful representation of company financial

condition and as the preparation for converting all of existing accounts to the Intuit

Quickbooks. Therefore in the next section, it will be concern on how to solve the

error that happened in company especially in the misstatement issue.

Source: PT. Trisan Pakar Baja

44

4.2 Faithful representation (free from error) issue in PT. Trisan

Pakar Baja

Based on the Figure 4.1, the adding amount of total interest expense to the

book value of credited fixed asset (vehicle) will impact toward incompliance use of

existing accounting standard that is Pernyataan Standar Akuntansi Keuangan

(PSAK). These incompliance will create unreliable information related valuation in

financial statement. These issue itself can be considered as violation in faithful

representation aspect especially in free from error concept due to the transactions

are recorded in the wrong amount. The free from error aspects define that the

transactions need to be accurate in terms of amount and its estimation. With that

being said, the condition of the company had regarding with the credited fixed asset

(vehicle) is having issue with the free from error aspects in faithful representation.

Based on the conducted research methods, these action happened due to not

knowing the existing accounting standard treatment even though the all members

in Accounting & Finance Department having previous experience in accounting.

However, they confess that experience that they have only regarding about how to

record and process it into the financial statement with unawareness of the existing

regulations in PSAK. That resulting the all transactions that recorded by

Accounting & Finance Department mostly recorded in the total amount of each

transactions that will be charged only and recorded at the only time that transactions

happened since they think that the accounting treatment will be the same for all of

the account with only just record the same way as the other transactions. From that

45

point, it create the mind set for all members in Accounting & Finance Department

to record the transactions with the total amount that will be charged with that

transactions at the time transactions occurred without pay exact attention related

the treatment for each account.

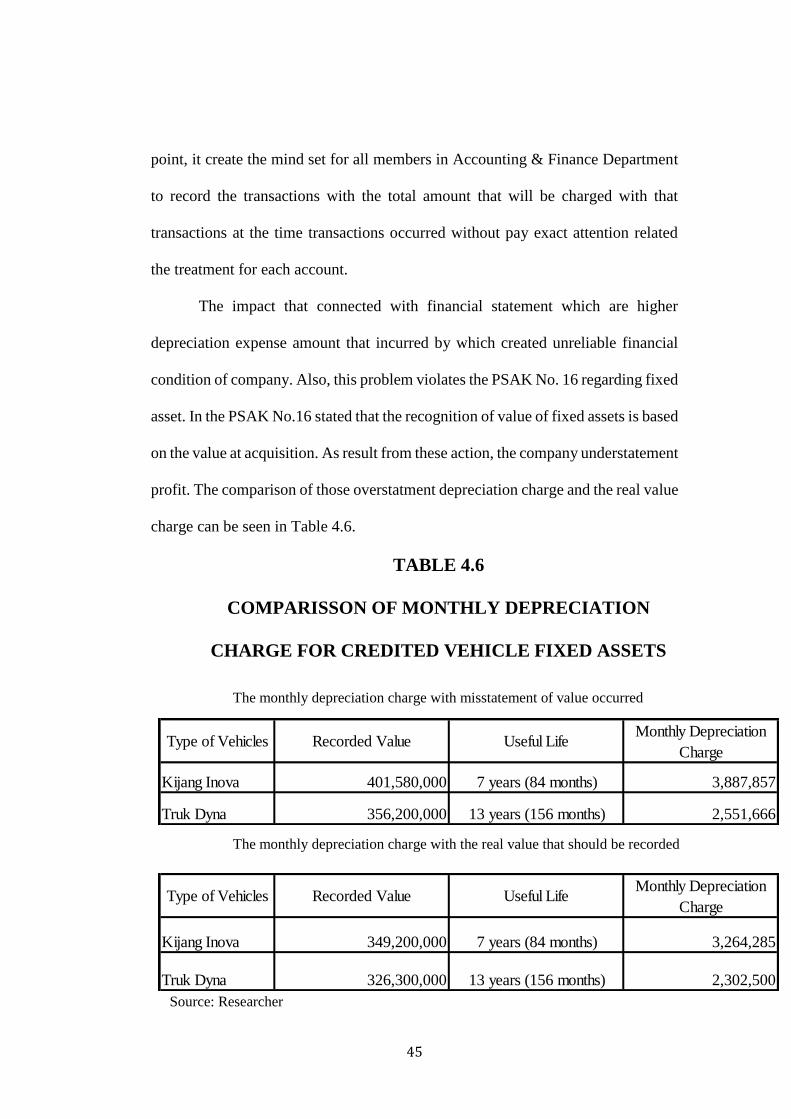

The impact that connected with financial statement which are higher

depreciation expense amount that incurred by which created unreliable financial

condition of company. Also, this problem violates the PSAK No. 16 regarding fixed

asset. In the PSAK No.16 stated that the recognition of value of fixed assets is based

on the value at acquisition. As result from these action, the company understatement

profit. The comparison of those overstatment depreciation charge and the real value

charge can be seen in Table 4.6.

TABLE 4.6

COMPARISSON OF MONTHLY DEPRECIATION

CHARGE FOR CREDITED VEHICLE FIXED ASSETS

The monthly depreciation charge with misstatement of value occurred

The monthly depreciation charge with the real value that should be recorded

Source: Researcher

Type of Vehicles Recorded Value Useful LifeMonthly Depreciation

Charge

Kijang Inova 401,580,000 7 years (84 months) 3,887,857

Truk Dyna 356,200,000 13 years (156 months) 2,551,666

Type of Vehicles Recorded Value Useful LifeMonthly Depreciation

Charge

Kijang Inova 349,200,000 7 years (84 months) 3,264,285

Truk Dyna 326,300,000 13 years (156 months) 2,302,500

46

4.2.1 Proposed and Implemented Solution

a. Accounting treatment for the misstatement vehicle fixed assets

Since there is issue regarding overstatement of credited vehicle fixed assets

that need to be fixed in order to avoid the understatement of reporting the profit, the

discussion will lead in the way of researcher fixed the overstatement through

adjustment in the value of credited fixed assets. In order to create the faithful

representation information for financial statement, company need to change the

amount into real book value at the time of acquisitions. The book value according

to PSAK No.16 is the value at acquisition only without adding other component

which is value that existed in the invoice. Also, the amount of interest expense that

need to be paid during each month will be seperated and recorded when only paid.

All of these steps are necessary in order to comply with PSAK concept in recording

and reporting the fixed asset. Also, the accumulated depreciation account will be in

the seperated from the fixed asset account and act as the contra account of that

account.

Therefore, adjustment entries will be necessary to solve the valuation

problem of fixed asset there will be need of necessary adjustment entries for the

fixed asset vehicle account and the account payable amount that affected due to this

transactions. The adjustment journal for this kind of condition can be shown in

Figure 4.2.

47

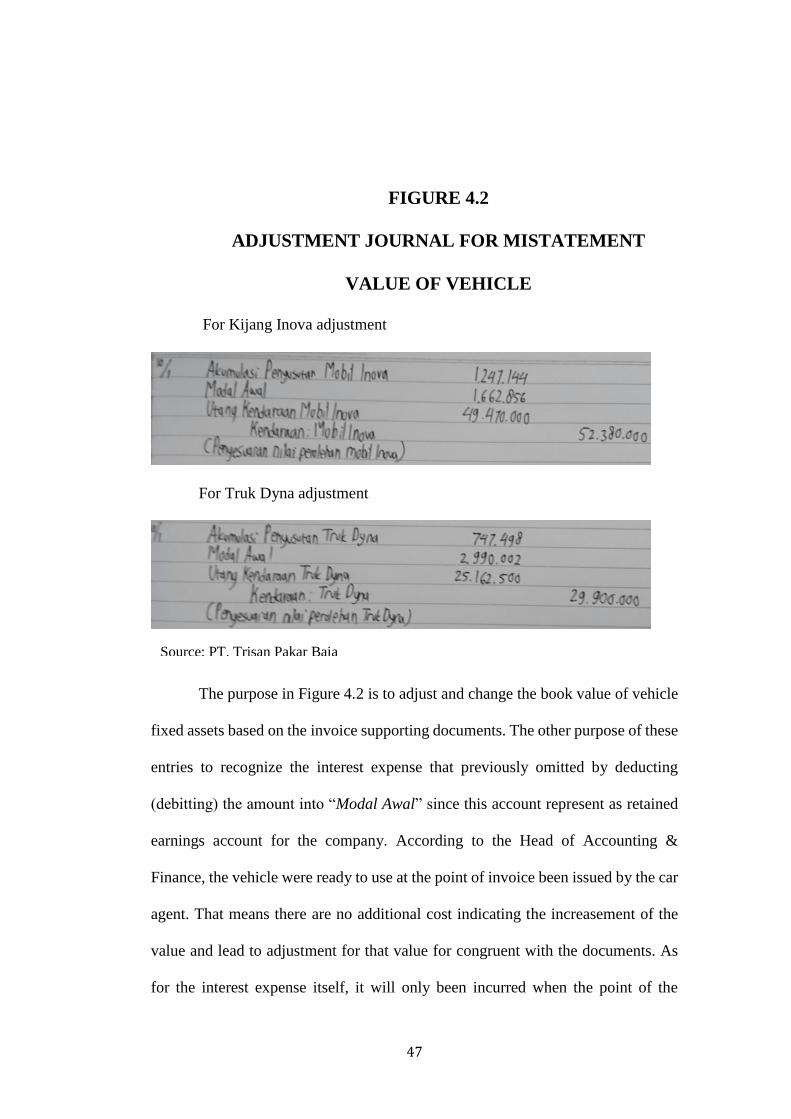

FIGURE 4.2

ADJUSTMENT JOURNAL FOR MISTATEMENT

VALUE OF VEHICLE

For Kijang Inova adjustment

For Truk Dyna adjustment

The purpose in Figure 4.2 is to adjust and change the book value of vehicle

fixed assets based on the invoice supporting documents. The other purpose of these

entries to recognize the interest expense that previously omitted by deducting