I Conferencia Nacional de Desenvolvimiento Regional. Financial System and Regional Development /...

32

I CONFERÊNCIA NACIONAL DE DESENVOLVIMENTO REGIONAL MARCO CROCCO LABORATORY OF STUDIES IN MONEY AND SPACE CENTER FOR REGIONAL DEVELOPMENT AND PLANNING - UFMG

-

Upload

eurosocial-ii -

Category

Economy & Finance

-

view

125 -

download

0

Transcript of I Conferencia Nacional de Desenvolvimiento Regional. Financial System and Regional Development /...

I CONFERÊNCIA NACIONAL

DE DESENVOLVIMENTO

REGIONAL MARCO CROCCO

LABORATORY OF STUDIES IN MONEY AND SPACE

CENTER FOR REGIONAL DEVELOPMENT AND PLANNING - UFMG

Main Message

Financial System and Regional Development

It is not a discussion about regional development funds;

Neither a discussion about public banks;

Is a discussion about private financial system and its role on regional

development;

Theories of Regional Development

First Generation Regional Policy

Neoclassical Approach: money are considered as neutral

The Keynesian Approach

Explicitly incorporated the concept of autonomous

investment and effective demand;

The role of money and financial system and understood

based on the theory of loanable funds and/or based on the

horizontalista approach money supply;

Theories of Regional Development

The second and third generations: the focus on competitiveness

A lower role for the state, allowed only to correct market failures;

Emphasis on human capital as a determinant of growth;

Emphasis on competitiveness - measured by international position - as the key to development, implying a focus on innovation, economies of knowledge and mechanisms to facilitate this process: networking, cooperation, contacts face to face, learning regions; Regional Innovation Systems, among others;

Local endogenous development: industrial districts, clusters, delegation of powers to regions

No systematic analysis of the role of monetary and financial system;

Only general indications as part of the national (regional or local) innovation

Monetary Theory for Regional

Development

From the economics side a Seminal contribution of Dow (1996, 1999)

and Chick and Dow (1988):

Capitalists (including banks) don’t only choose between applying in

different assets (financial or industrial circuits) due to uncertainties of the

environment (liquidity preference), but also they choose, by

comparison, in which region they will apply its resources

Liquidity Preference Differentiated across the Space

Determines the willingness to lend (financial system) and / or go into

debt (individuals)

Monetary Theory for Regional

Development

The concept of liquidity preference can be used to increase the understanding of many aspects of the geography of finance, like:

Financial exclusion

The theory of liquidity preference (TLP) of banks can be used to understand both why banks choose to open a branch in a specific region instead of other, and what kind of service should be offered in a specific region;

Financialization

The TLP can help to understand de degree of financialization of a specific region;

Centrality

Resilience

Role of the resilience of regional financial system to the understanding of the resilience of regions;

Empirical Analysis of Brazil

Total Assets / GDP

(Indicator of Financial Deppening)

Regions

0,00

2,00

4,00

6,00

8,00

10,00

12,00

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

North South Central-West Northeast Southeast

Financial System

Resileience

Liquidity Preference of Banks Branches

Regions

0,000

0,020

0,040

0,060

0,080

0,100

0,120

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

North South Central-West Northeast Southeast

LPB = Cash Deposits / Supply

of Credit (willingness to

supply credit)

Decrease and

Convergence of

Regional LPB

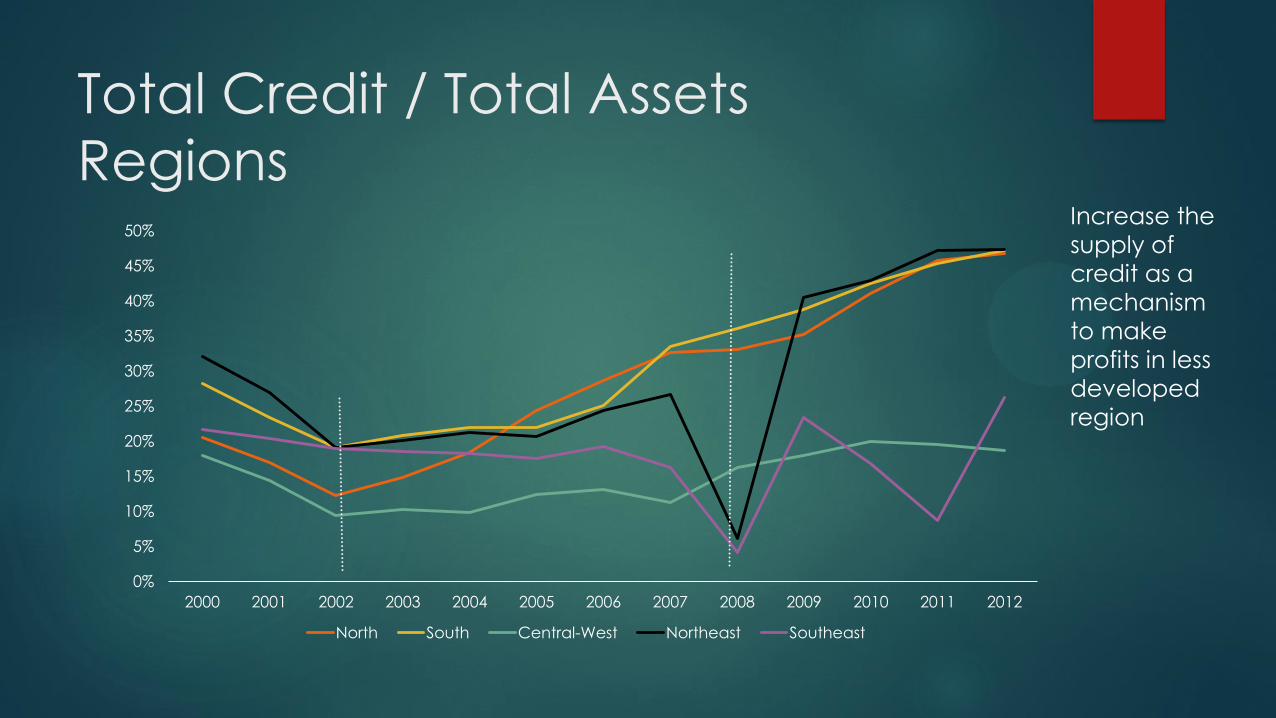

Total Credit / Total Assets

Regions

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

North South Central-West Northeast Southeast

Increase the

supply of

credit as a

mechanism

to make

profits in less

developed

region

Total Credit by Regions

0,00

200.000,00

400.000,00

600.000,00

800.000,00

1.000.000,00

1.200.000,00

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

North South Central-West Northeast Southeast

Regional Quotient of Credit

Regions

0,00

0,20

0,40

0,60

0,80

1,00

1,20

1,40

1,60

1,80

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

North South Central-West Northeast Southeast

Most

developed

regions have a

share in

distribution of

the supply of

credit greater

than their

contribution to

GPD

Futher

regional

disparities

Profits / Assets (Return on Assets

Regions

-5,000

-4,000

-3,000

-2,000

-1,000

0,000

1,000

2,000

3,000

4,000

5,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

North South Central-West Northeast Southeast

After 2005 the less developed regions

become more profitable

ROA and QRC

North Region

-0,500

0,000

0,500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Profits/ Assts QRC

Little

Functionality

of Financial

System

ROA and QRC

Northeast Region

-1,500

-1,000

-0,500

0,000

0,500

1,000

1,500

2,000

2,500

3,000

3,500

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Profits / Assets QRC

Little

Functionality

of Financial

System

ROA and QRC

Southeast Region

-0,600

-0,400

-0,200

0,000

0,200

0,400

0,600

0,800

1,000

1,200

1,400

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Profits / Assets QRC

QRC BNDES

Norte e Nordeste

QRC BNDES

Sudeste, Sul e Centro-Oeste

Urban Financial Structure

Supply of Financial Services

Preliminary Conclusions

Financial System (public and private) must be a component in the

analysis of regional development;

Financial crisis shed lights on the regulation of internacional financial

system

The same applies for regulations inside countries;

Take a look on history:

What are the configuration of financial system in cases of succesful

poicies of regional development, as example , third Italy.

Thank You

Anexos

Total Assets / GDP

Degree of Financialization

-

0,500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Inexistent Soft Medium Hard

Distribution of Bank Branches

by Degree of Financialization

0,00

10,00

20,00

30,00

40,00

50,00

60,00

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Inexistent Soft Medium Hard

Liquidity Preference of Banks Branches

Degree of Financialization

0,000

0,050

0,100

0,150

0,200

0,250

0,300

0,350

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Brazil Soft Medium Hard

Total Credit / Total Assets

Degree of Financialization

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Brazil Soft Medium Hard

Total Credit by Regions

0,00

200.000,00

400.000,00

600.000,00

800.000,00

1.000.000,00

1.200.000,00

1.400.000,00

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Soft Medium Hard

Regional Quotient of Credit

Degree of Financialization

0,0

0,1

0,2

0,3

0,4

0,5

0,6

0,7

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Soft Medium Hard

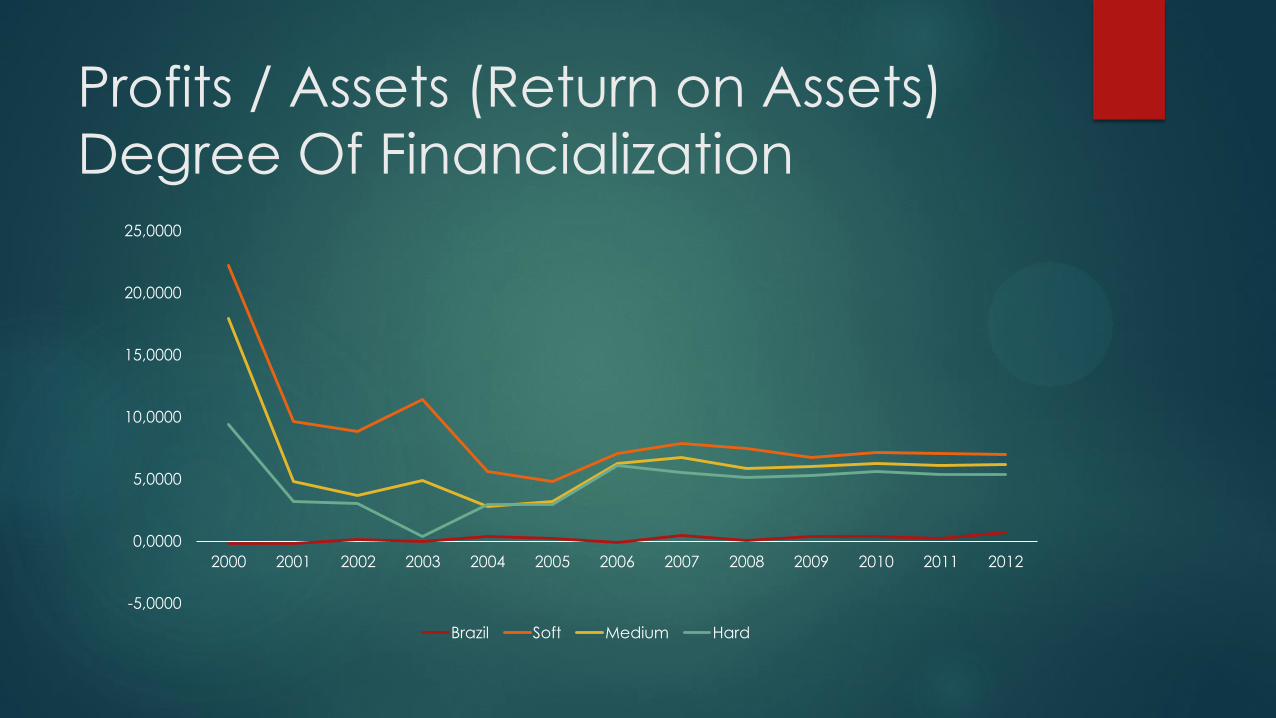

Profits / Assets (Return on Assets)

Degree Of Financialization

-5,0000

0,0000

5,0000

10,0000

15,0000

20,0000

25,0000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Brazil Soft Medium Hard

Regional Distribution of Bank’s

Branches

0,00

10,00

20,00

30,00

40,00

50,00

60,00

2000-2003 2004-2007 2008-2012

Central-West Northeast North Southeast South

Stability of

the

distribution

despite the

financial

crises

Monetary Theory for Regional

Development

Empirical studies

Scarcity of financial data in regional scale;

Due to the short relevance of money to understand the economic

performance of a specific region according to the mainstream theory

(neoclassical);

Brazil is a special case (just a little)

Data of aggregated balance sheet of bank branches by city, monthly since

1988;

Data on employment and type of financial institution by city since 1990;

Make possible to analyse the behaviour of banks and financial system and

their contribution to the understanding of regional disparities ;