HPMC12: Aviva - Existing Customer Management: Poor data,no analytics,no chance?

23

Copyright © 2010 Accenture All Rights Reserved. Accenture, its logo, and High Performance Delivered are trademarks of Accenture. High Performance Marketing Conference 2012 Aviva UK Life & Pensions ?

-

Upload

accenture-the-netherlands -

Category

Business

-

view

1.181 -

download

0

Transcript of HPMC12: Aviva - Existing Customer Management: Poor data,no analytics,no chance?

Copyright © 2010 Accenture All Rights Reserved. Accenture, its logo, and High Performance Delivered are trademarks of Accenture.

High Performance Marketing Conference 2012

Aviva UK Life & Pensions

?

Copyright © 2010 Accenture All Rights Reserved. Accenture, its logo, and High Performance Delivered are trademarks of Accenture.

Aviva UK Life & Pensions

Existing Customer Management: Poor data, no analytics, no chance?

3

Contents

• Background & Context

• Existing Customer Management

• From Tactical to Strategic

• Benefits & Reflections

4

Background & context

5

About Aviva

© 2011 Accenture. All rights reserved.

A significant global business:

- 6th largest insurer globally

- 44m customers

- 12 focus markets

- 36,000 employees

- 300bn+ funds under mgt

A clear strategy:

- Geographic focus

- Exploit composite advantage

- Build on core capabilities

6© 2011 Accenture. All rights reserved.

• Life, pensions, savings and retirement• 12% market share• 6.5m customers mostly through IFA and

Bancassurance

• House, car, pet, business insurance • Direct and broker distribution• 6m customers

• Private medical insurance and group risk

• Direct and intermediated business• #3 in market

Aviva UK – a 300 year pedigree

UK Life

UK GI

UK Health

7

Aviva UK Life – the problem and the opportunity

© 2011 Accenture. All rights reserved.

ProblemMore customers leaving than arriving

£XXXm commission bill

Creaking legacy infrastructure

Overwhelmingly intermediated

Opportunity

6.5m customers

Regulatory dynamics

Compelling customer brand

Existing Customer Management:

“We’ll invest in analytics-led customer marketing

to drive more value from our existing base”

8

Existing Customer Management

Starting from a low base

Old approach constrained by: Existing Customer Management team created

• Increase up/ cross sell, retention, rollover campaigns with analytics

• Identify additional opportunities

• Build Aviva internal sustainability

• Define the roadmap and investment case

• Pilot value from customer analytics

• Poor view of customer data

• No analytics tools

• No analytical skills

• Campaign selections by intuition / experience

• Little visibility of new opportunities

• DM campaigns with long lead times

• Belief DQ = bad

New brand position focused on understanding the

individual customer and being relevant

ItalyIndia

UK

10

Feb’10 March 2012Aug.’10

Analytics managed serviceValue exploitationProof of value / pilot

Feb’ 11

Key project phases and evolution of capability

•Data Check •Exploratory Analytics•Test Campaigns •Process Changes•Build Awareness

Jul’ 11

© 2011 Accenture. All rights reserved.

•Increase Campaign Volumes

•Test Multiple Channels / Mechanics

•Broaden Use•Inform Customer Retention Strategy

•Inform IFA Analytics Proposition

•Campaign Prioritisation•Pure Off-shore Model •Transition To In-House (plan)

Did we have poor data?

Life Insurance Data Model Structure

Accenture’s Life Insurance Customer Analytic Record (CAR): • Facilitates rapid descriptive and

propensity model development• Identified overall data quality and

identify key data gaps.

DWH

Policy

Campaigns

Complaints

PaymentsClaims

Value Segment

Demographics

© 2011 Accenture. All rights reserved. 11

We developed a new “single-view-of-the- customer”

DWH

If you really want to know what it looked like…

Descriptive Modelling: shining a light to identify value

© 2011 Accenture. All rights reserved. 13

X.Xm active Life1 Customers

31% are joint policies

XXm no longer active Life1 Customers

X.Xm customers with at least one Protection policy

X.Xmil customers with at least one IPP policy, 0.5m for GPP, 0.6m for

Annuities, 0.1m for Equity Release

X.Xm customers with at least one

Investment policy

X.Xm Active Life1 Policies

X.Xm Active Joint Life1 Policies

• X.X million Life policy holder records in our CIC database

• X.X million are currently active

• Average Life product holding is 1.06 products.

• Average Life policy holding is 1.2 policies.

Product Holdings

PH with Single Policy (#)

PH with Single Policy (%)

PH with multiple policies within same product holding

PH with multiple policies within same product holding (%)

Total Policy Holders (PH) (#)

Protection

Investments

IPP

GPP

Annuities

Equity Release

X.X.m Policyholders are between 35 and 49 and represent future

growth opportunity

1ST POLICY AnnuitiesGroup

Pension InvestmentsIndividual Pension

Equity Release Protection

Unknow Life Grand Total

Annuities 59% 0% 31% 2% 3% 4% 0% 88,528 GPP 8% 49% 3% 21% 0% 19% 0% 48,815 Investments 5% 1% 66% 9% 0% 18% 0% 442,480 IPP 18% 7% 11% 40% 0% 24% 0% 331,664 Equity Release 3% 0% 19% 0% 64% 13% 0% 9,382 Protection 2% 3% 8% 9% 1% 77% 0% 407,887 Uknown Life 8% 2% 50% 9% 1% 21% 10% 4,953 Grand Total 11% 5% 29% 17% 1% 36% 0% 1,333,709

2ND POLICY

90 Campaign Ideas Generated

Multiple Layers Of Analysis ….

Propensity Model Top 2 Deciles of Customers –

203K

Active policy holders

– 144K

Age Profiling Cut

(30 -60 yrs)– 108K

Has Phone– 74 K

After Supp. 28K

Campaign targeting through analytics

We enhanced

Customer T

argetin

g by

overlaying Resp

onder

Profiling on th

e

Propensity M

odel

Results

Increased targeting by applying filters based on insights from profiling of responders

14

15

Campaign results - significant uplift over BAU selection

CAMPAIGNS LIFT OVER RANDOMANNUITY CROSS_SELL 2.59PROTECT CROSS_SELL 1.57EQUITY RELEASE CROSS_SELL 1.36MOTOR TO LIFE 1.5HOME TO LIFE 3.8IPP RESTART 0.9 (negative performance)Annuity Pensions base 7.1Annuity Non Pensions base 3.6

16

From tactical to strategic

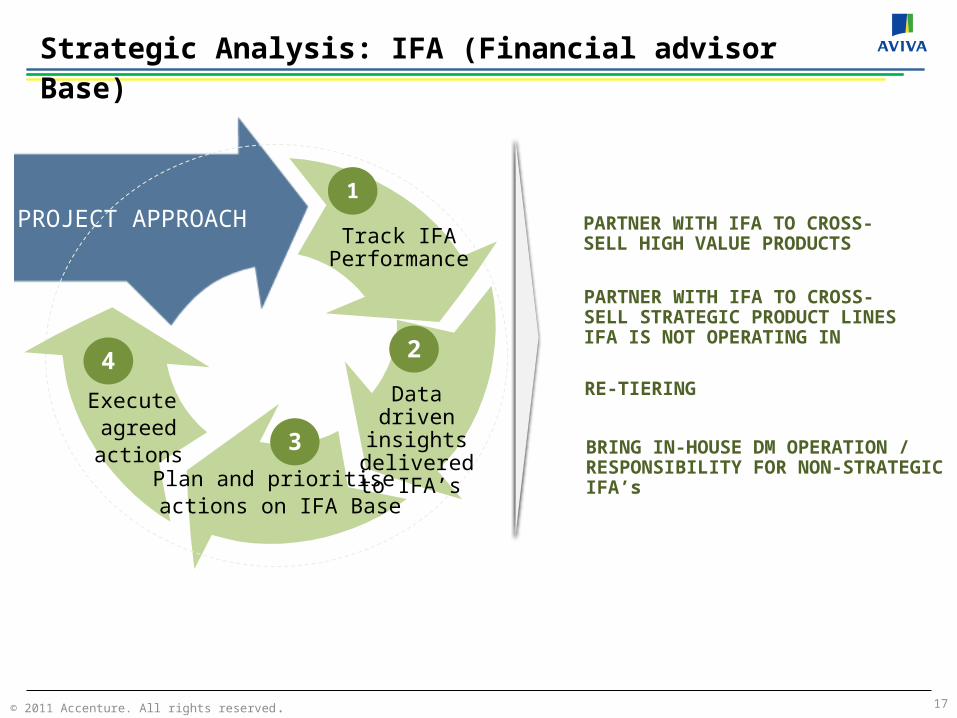

Strategic Analysis: IFA (Financial advisor Base)

Data driven insights

delivered to IFA’s

Execute agreed actions

PROJECT APPROACHTrack IFA

Performance

1

24

3Plan and prioritise

actions on IFA Base

PARTNER WITH IFA TO CROSS- SELL HIGH VALUE PRODUCTS

PARTNER WITH IFA TO CROSS- SELL STRATEGIC PRODUCT LINES IFA IS NOT OPERATING IN

RE-TIERING

BRING IN-HOUSE DM OPERATION / RESPONSIBILITY FOR NON-STRATEGIC IFA’s

© 2011 Accenture. All rights reserved. 17

Strategic Analysis - churn segmentation

Joint holders : 10%Active products and joint policy holder group

Golden geese: 19%Older customer, high value and high ticket policy holder with bond surrender

Protection seekers : 19% Young customers, protection focused group

Loyal customers : 17%Middle age group, matured policies, high tenure group, pension and annuity base, mostly IFA customers

Movers & Changers: 35%Older customer, voluntary inactive group, low value, joint policyholders, pension customers

• Cluster analysis of inactive accounts to identify the types of customer attitudes and behaviour toward churn.

• Overlaid sample of bond surrender customer feedback to validate

© 2011 Accenture. All rights reserved. 18

19

Benefits & Reflections

Benefits delivered

• Uplift of 2.84 in sales conversion achieved against BAU customer selections.

• £XXmillion incremental value delivered through ECM campaigns 2011

•200k customers added to multiple Life policy holders in 18 months: 23% vs 20.5% (adding in GI policies 34% vs 26%)

• Proved tactical and strategic value of analytics• Insight generation and dissemination has led to snowball of new insight requests

•

1. Incremental sales conversion & revenues

3. Analytics & Strategy

• 25+ insight driven campaign waves executed• First cross BU campaign by customer management team• Campaign timelines reduced by 50%• 100% increase in marketable base by challenging existing suppressions and data management routines

2. Campaign Management & Process

© 2011 Accenture. All rights reserved. 20

21

Reflections from Aviva

• We developed analytics too early – the marketing infrastructure wasn’t ready

• The business wasn’t bought in enough – limiting the effectiveness of some campaigns

• We can use analytics as a tradeable currency – why aren’t we doing more?

• Is there more we can use CIC for... Predictive underwriting...?

• We still haven’t developed processes to deploy the analytics in anger – but we are near

• The value added from Accenture was outstanding – far more that their remit……..

22

Aviva’s Accenture Legacy

• We have proven the case for analytics in UK Life

• We have reduced campaign speed to market substantially

• We have a usable single customer view… after 6 years of trying

• We have sold the benefits of analytics to the wider UK region

But essentially……

• We have a platform for significant value growth over three years

23

Questions?