Does Your Truth Match Reality? Dr. Heinz Lycklama [email protected] .

Page 0

March 2006

Heinz-Joachim Neubürger, CFO

Page 1

Safe harbor statement

This presentation contains forward-looking statements and information – that is, statements related to future, not past, events. These statements may be identified either orally or in writing by words as “expects”, “anticipates”, “intends”, “plans”, “believes”, “seeks”, “estimates”, “will” or words of similar meaning. Such statements are based on our current expectations and certain assumptions, and are, therefore, subject to certain risks and uncertainties. A variety of factors, many of which are beyond Siemens’ control, affect its operations, performance, business strategy and results and could cause the actual results, performance or achievements of Siemens worldwide to be materially different from any future results, performance or achievements that may be expressed or implied by such forward-looking statements. For us, particular uncertainties arise, among others, from changes in general economic and business conditions, changes in currency exchange rates and interest rates, introduction of competing products or technologies by other companies, lack of acceptance of new products or services by customers targeted by Siemens worldwide, changes in business strategy and various other factors. More detailed information about certain of these factors is contained in Siemens’ filings with the SEC, which are available on the Siemens website, www.siemens.com and on the SEC’s website, www.sec.gov. Should one or more of these risks or uncertainties materialize, or should underlying assumptions prove incorrect, actual results may vary materially from those described in the relevant forward-looking statement as anticipated, believed, estimated, expected, intended, planned or projected. Siemens does not intend or assume any obligation to update or revise these forward-looking statements in light of developments which differ from those anticipated.

Page 2

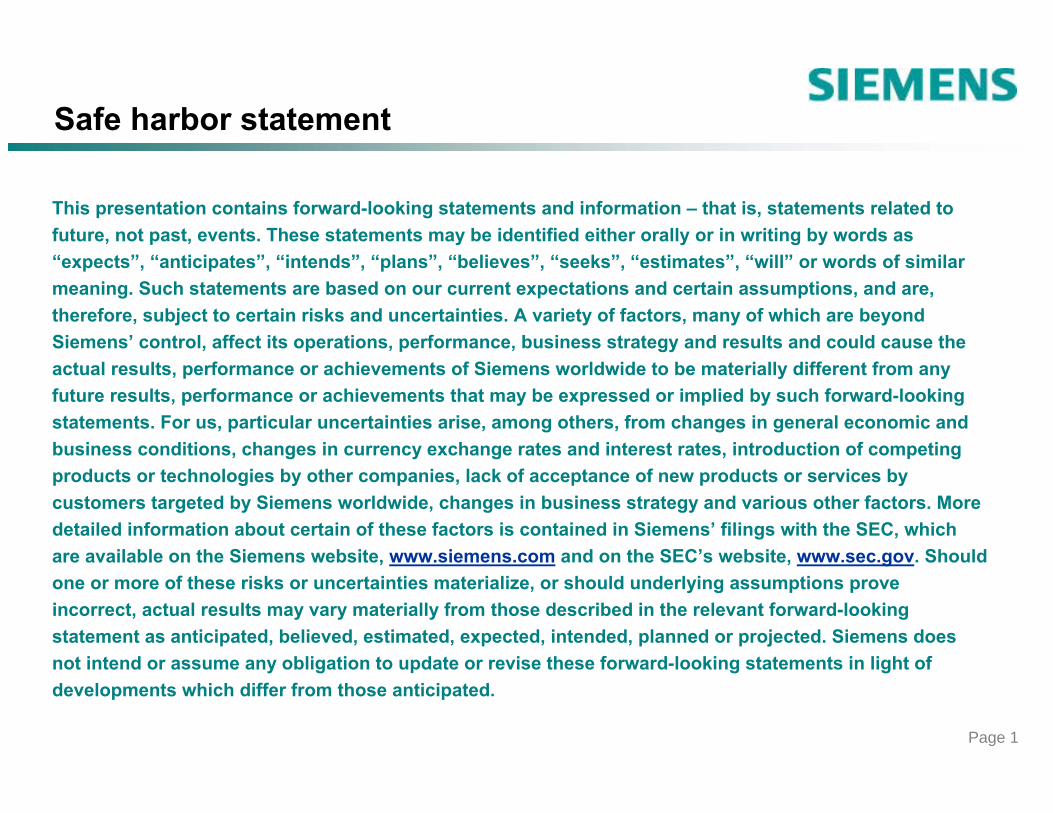

Active in six business areas

LightingAutomation and Control

Information andCommunications Power Transportation Medical

OSRAMAutomation andDrives

Industrial Solutions and Services

Communications

Siemens BusinessServices

Power Generation

PowerTransmission andDistribution

TransportationSystems

Siemens VDOAutomotive

Medical Solutions

Siemens Building Technologies

€21.1 bn€18.5 bn €12.3 bn €7.6 bn€13.8 bn €4.3 bn

27%24%

16%10%

18%

5%

Fiscal Year 2005 total sales of Operations Groups excluding Other Operations

Page 3

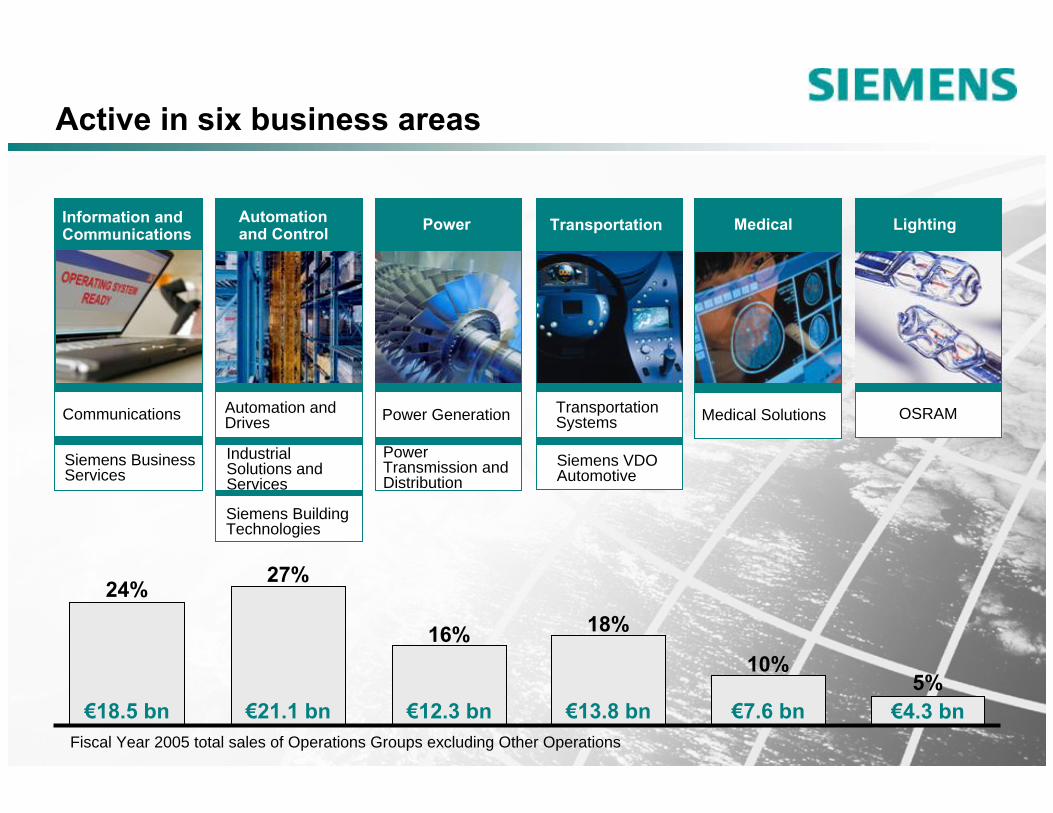

Key figures

8%

(4.504)

(0.44)

0%

(9)%

7%

11%

∆

1.186

(0.30)

(25)%

(10)%

22%

31%

∆

1.25

3.015

3.87

3.0471

5.136

70.237

75,789

FY 04

(1.489)(0.820)Net Cash from operating and investing activities

3.0580.815Income from continuing operations

1.35–Dividend (in euros)

4.6871.402Group Profit from Operations

3.43

75.445

83.791

FY 05

0.92

20.719

26.788

Q1 FY06

Sales

EPS from continuing operations(in euros)

New Orders

in billions of euros

1 Income from continuing operations, excluding a positive effect related to Infineon share sale and a goodwill impairment. Including these effects, income from continuing operations for FY 04 amounts to EUR 3.450 bn.

Page 4

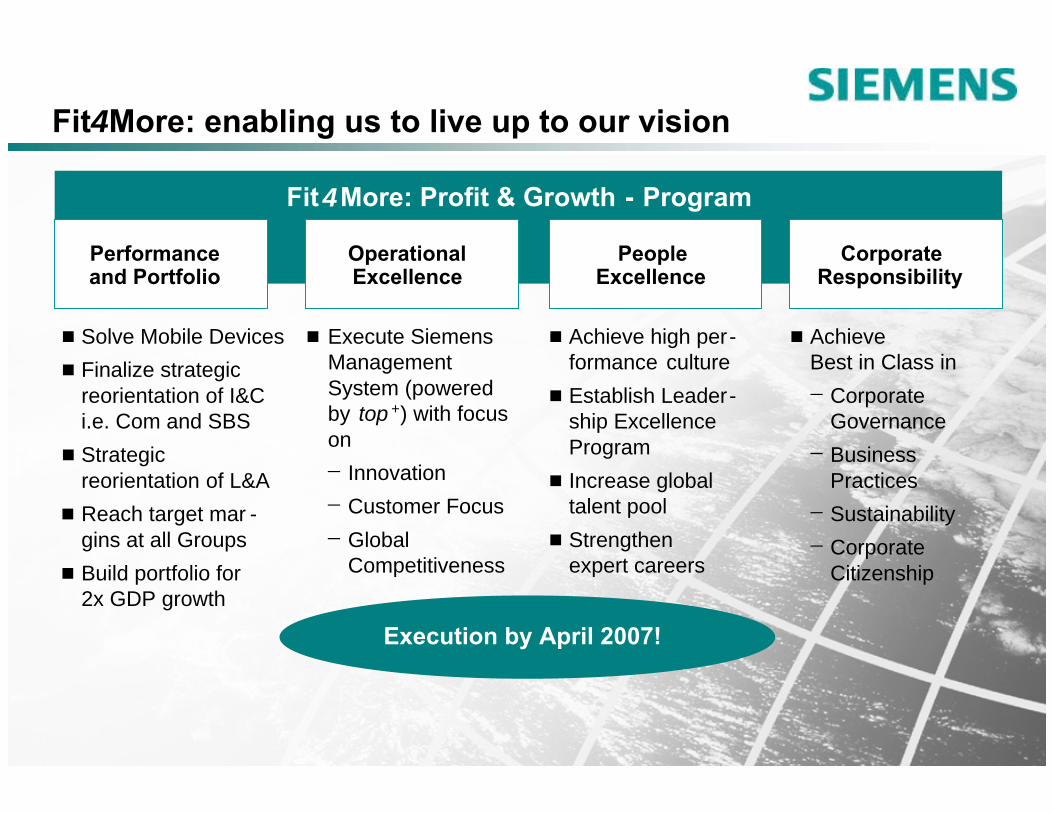

Performanceand Portfolio

OperationalExcellence

CorporateResponsibility

PeopleExcellence

Execute SiemensManagement System (powered by top +) with focus on− Innovation− Customer Focus− Global

Competitiveness

Achieve high per-formance cultureEstablish Leader-ship ExcellenceProgramIncrease global talent poolStrengthen expert careers

Solve Mobile DevicesFinalize strategicreorientation of I&Ci.e. Com and SBSStrategicreorientation of L&AReach target mar -gins at all GroupsBuild portfolio for2x GDP growth

Achieve Best in Class in− Corporate

Governance− Business

Practices− Sustainability− Corporate

Citizenship

Fit4 More: Profit & Growth - Program

Fit 4

Execution by April 2007!

Fit4More: enabling us to live up to our vision

Page 5

Performanceand Portfolio

OperationalExcellence

CorporateResponsibility

PeopleExcellence

Build portfolio for2x GDP growth

Fit4 More: Profit & Growth - Program

Building the future portfolio

Exogenous growthOrganic growth Growth Platforms

A&D

Med

SiemensONE

US Filter

BonusEnergy

VA Tech

CTI Molecular Imaging

Flender

Solve Mobile DevicesFinalize strategicreorientation of I&Ci.e. Com and SBSStrategicreorientation of L&AReach target marginsat all Groups

Page 6

… support our profitable growth strategy

Strategic goals of M&A activities …

Enhance regional presence fitting to worldwide strategy

Speed up consolidation / market penetration

Gain selected specific R&D competence

Create growth platforms by broadening the existing portfolio

Complement existing business portfolio adjacencies

Page 7

Transactions have been proven to be successful !

YearSignificant

strategic goalPurchase price (EV) Assessment

write-off1.6Strengthening position in DSL broadband access market 2001Efficient

on-track0.8Strengthening position in ultrasound2000Acuson

success6.8 Strengthening position in automotive, logistics and industrial turbines

2000Atecs

success1.0Strengthening position in fossil-fired power plants, equipment and services worldwide

1998Westinghouse

on-track2.1Expansion into healthcare IT2000Shared Medical

on-track1.6Strengthening position in the Building Systems Division1998Electrowatt

success0.75Strengthening position in the US market1993Sylvania

success0.9Strengthening position in industrial turbines

2003Alstom

in billions of euros

Track record of major M&A activities

Page 8

Strengthening our portfolio through activeportfolio management

Page 9

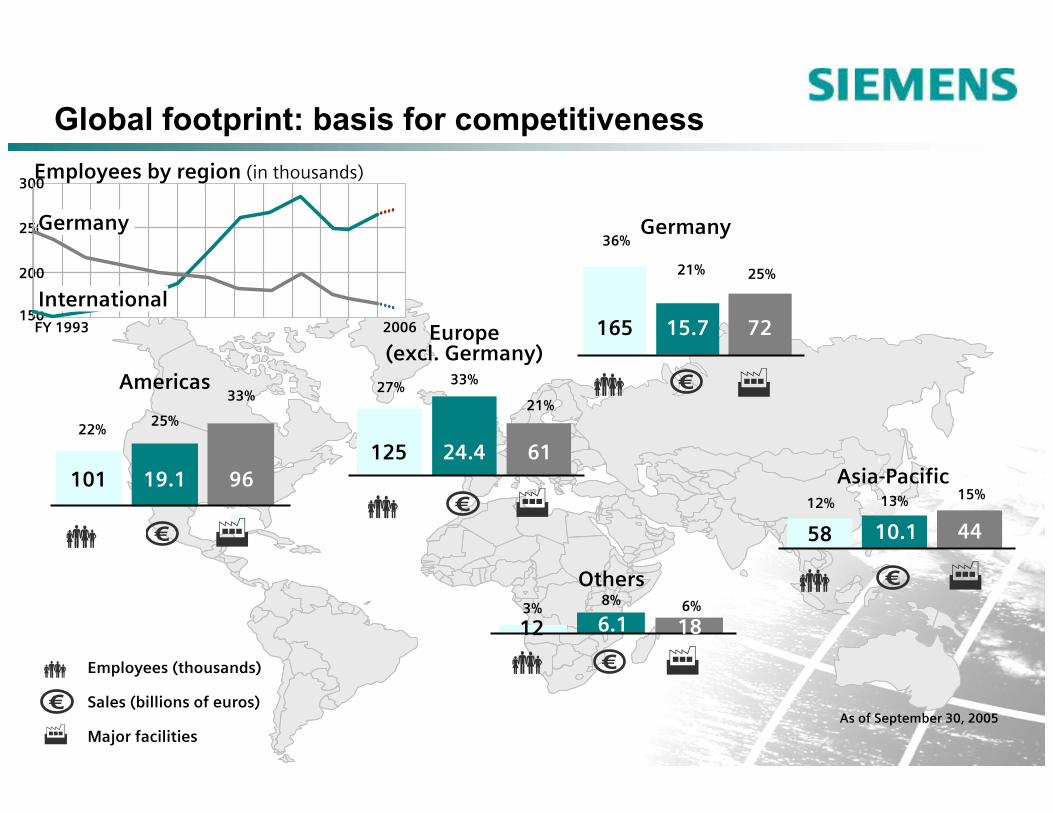

Americas

22%25%

33%

101 19.1 96

€

Europe(excl. Germany)

27% 33%

21%

125 24.4 61

€

Germany36%

21% 25%

165 15.7 72

€

Others3% 8% 6%

12 6.1 18

€

Asia-Pacific12% 13% 15%

58 10.1 44

€

Employees (thousands)

Sales (billions of euros)

Major facilities

€As of September 30, 2005

Global footprint: basis for competitivenessEmployees by region (in thousands)

250

300

150

200

FY 1993 2006

Germany

International

Page 10

Well prepared to master global trends

Siemens todayDrinking water treatment Water distributionWastewater treatment

1.2 billion people without drinking water2.4 billion people not connected to waste water systems40% increase in water consumption by 2025

More than 60% increase in worldwide energy demand by 2030Increase of CO2 emission risk to global climate

Siemens todayStrong No. 2 in power technologies worldwideComplete range of offerings for wind power, hydropower, biomass, fuel cells and fossil fuelsTrendsetter in intelligent power generation and distributionLow-loss electricity transport

Water

Power

Page 11

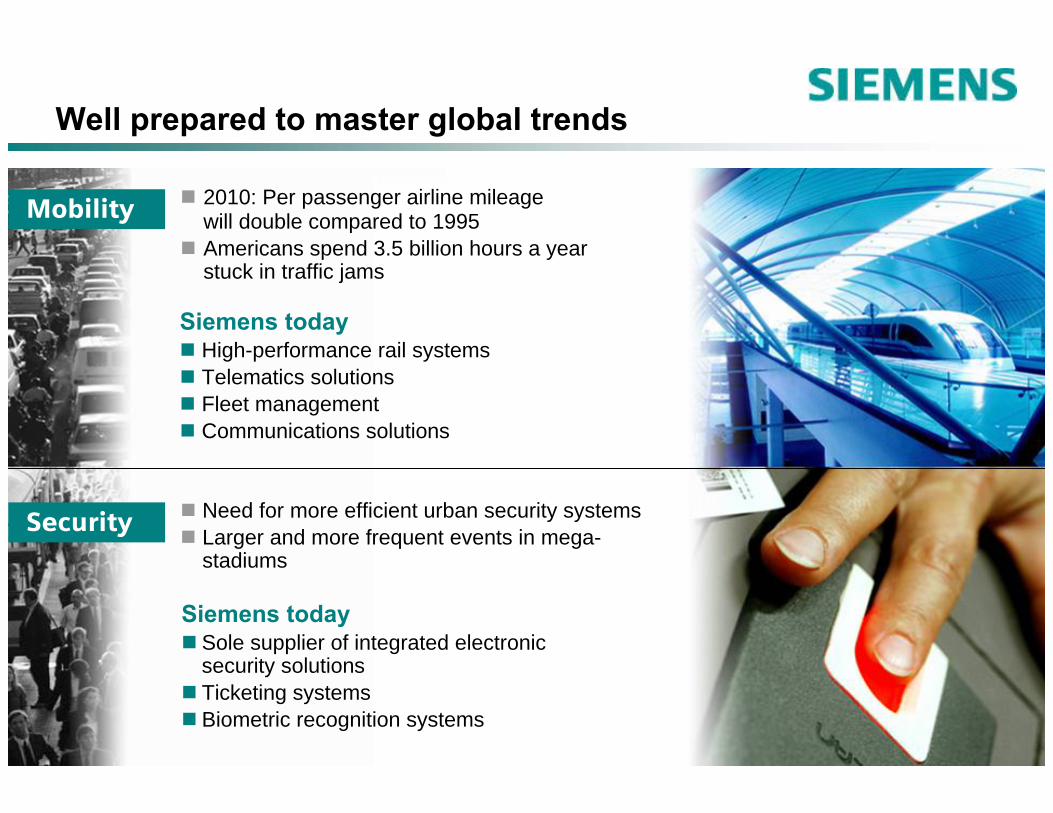

Well prepared to master global trends

Siemens todayHigh-performance rail systemsTelematics solutionsFleet managementCommunications solutions

2010: Per passenger airline mileagewill double compared to 1995Americans spend 3.5 billion hours a year stuck in traffic jams

Need for more efficient urban security systemsLarger and more frequent events in mega-stadiums

Siemens todaySole supplier of integrated electronic security solutionsTicketing systemsBiometric recognition systems

Mobility

Security

Page 12

Well prepared to master global trends

Siemens todayNo. 1 in healthcare ITTechnology leader in imaging systemsInnovation leader in healthcare processes

Percentage of 80+ generation to grow globallyHealthcare costs in industrialized nations rise to €3.8 trillion in 2010 (2002: €2.9 trillion) In Germany, healthcare costs account for 10.7% of GDP

Increasing consumption of oil (until 2030 CAGR 1.8%), natural gas (2.5%) and coal (1.6%) to fuel global energy demand requires efficient systems and solutions for mining industriesIncreasing world population requires efficient production and supply of food and goods

Siemens todayLeading solution provider for mining, oil & gas industries No. 1 in industry automation

Healthcare

Industry

Page 13

Ningbo

Shenyang

Changchun

Fuzhou

Guangzhou

Shenzhen

South

Qingdao

Northeast

NanningDongguan

LiuzhouFoshan

Xiamen

Haikou

Wuhan

Nanchang

GuiyangPanzhihua Guilin

Chongqing

Yichang

Yibin

Mianyang

Tanggu

Urumqi

Yinchuan

Lanzhou

Tangshan

BeijingHuhhot

XuzhouLuoyangZhengzhou

Taiyuan

Xi ‘an

Baotou

North

Yantai

JiningJinan

Chengdu

Zibo

Hefei

Hangzhou

Kunming

Harbin

Changsha

Changde

East

Wenzhou

NanjingSuzhou

Nantong

Dalian

Jinzhou

Shanghai

TianjinShijiazhuang

Jinhua

Wuxi

Zhuhai

Jiangmen

Shantou

YangzhouSouthwest

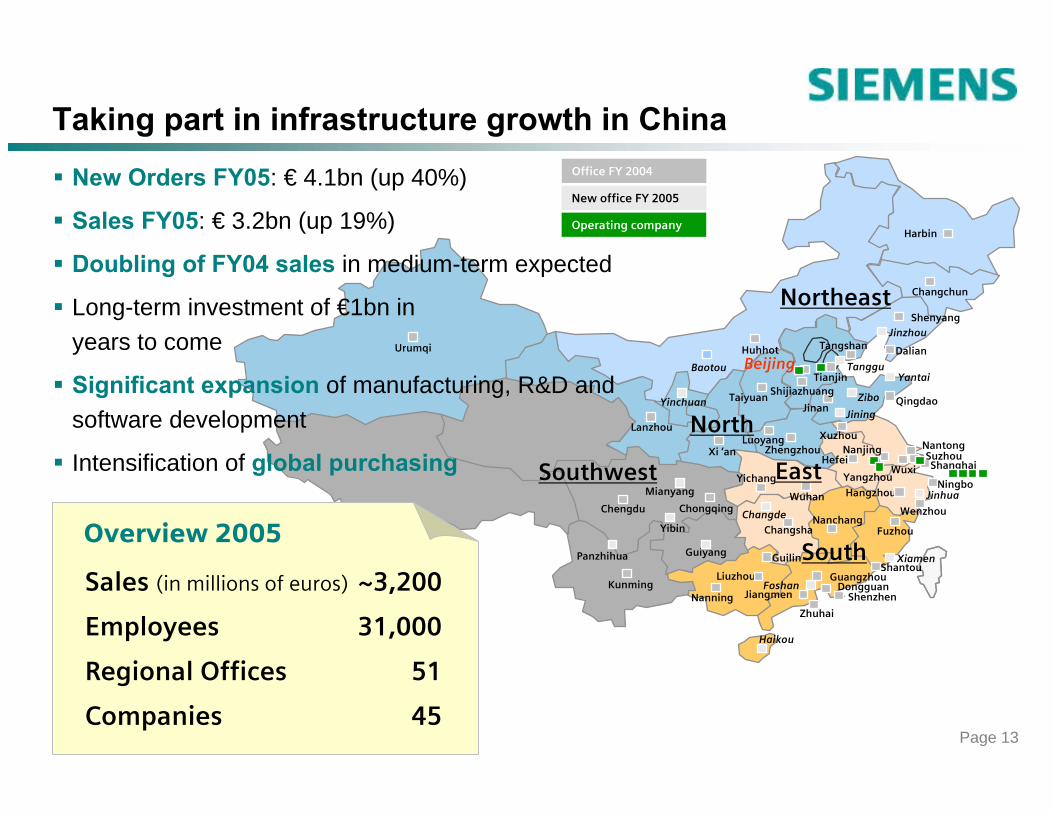

Taking part in infrastructure growth in China

New office FY 2005

Operating company

Office FY 2004New Orders FY05: € 4.1bn (up 40%)

Sales FY05: € 3.2bn (up 19%)

Doubling of FY04 sales in medium-term expected

Long-term investment of €1bn inyears to come

Significant expansion of manufacturing, R&D and software development

Intensification of global purchasing

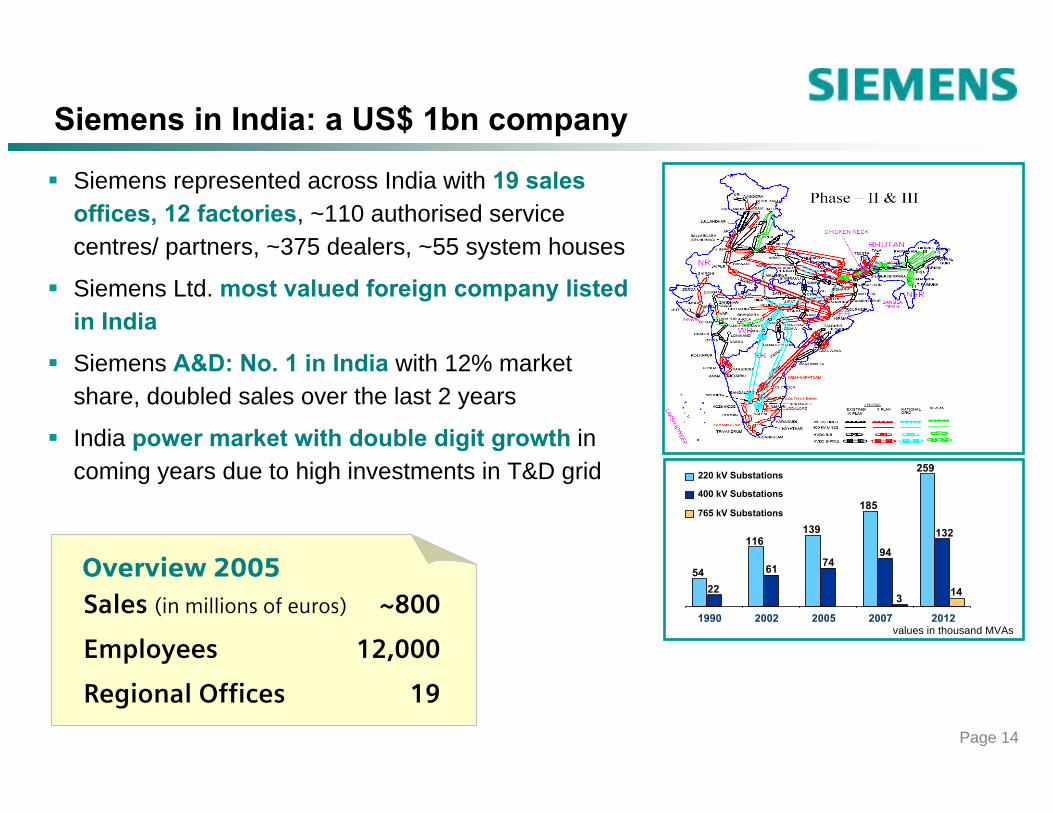

Sales (in millions of euros) ~3,200

Employees 31,000

Regional Offices 51

Companies 45

Overview 2005

Page 14

Siemens in India: a US$ 1bn company

Siemens represented across India with 19 sales offices, 12 factories, ~110 authorised service centres/ partners, ~375 dealers, ~55 system houses

Siemens Ltd. most valued foreign company listed in India

Siemens A&D: No. 1 in India with 12% market share, doubled sales over the last 2 years

India power market with double digit growth in coming years due to high investments in T&D grid

values in thousand MVAs

54

116139

185

259

22

61 7494

3 14

132

1990 2002 2005 2007 2012

220 kV Substations

400 kV Substations

765 kV Substations

Sales (in millions of euros) ~800

Employees 12,000

Regional Offices 19

Overview 2005

Page 15

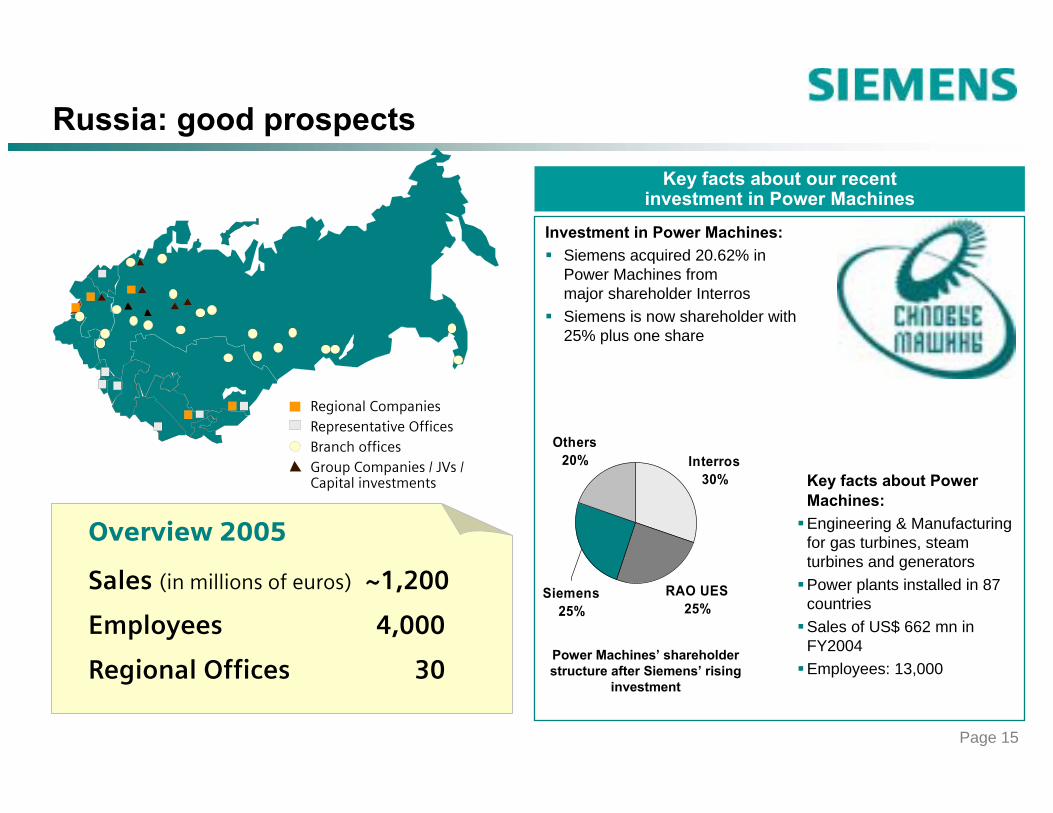

Russia: good prospects

Regional Companies Representative OfficesBranch officesGroup Companies / JVs / Capital investments

Sales (in millions of euros) ~1,200

Employees 4,000

Regional Offices 30

Overview 2005

Investment in Power Machines:Siemens acquired 20.62% inPower Machines frommajor shareholder InterrosSiemens is now shareholder with25% plus one share

Key facts about our recentinvestment in Power Machines

Interros30%

RAO UES25%

Others20%

Siemens25%

Power Machines’ shareholder structure after Siemens’ rising

investment

Key facts about Power Machines:Engineering & Manufacturing for gas turbines, steam turbines and generatorsPower plants installed in 87countriesSales of US$ 662 mn in FY2004Employees: 13,000

Page 16

Continuous rigorous execution of Fit4More program

Outlook: sights set on targets for 2007

Strategic reorientation with focus on megatrends and the growth markets of tomorrow

Boosting our power of innovation to drive organic growth

Well on track to continue growing profitably

Page 17

Our vision – setting the pace

A growth company that provides every customerwith the highest sustainable value.

Technology leader in the global electrical industry.

Attractive to the best and brightest in the world. Our employees are proud of their company.

Committed to an ambitious value code:Humaneness, equal opportunity, strict ethical standards in all business dealings.

One of the most valuable companies in the world.

One of the world's most successful companies inthe electrical industry.Number one or two in all of its businesses.

Page 18

Appendix

Page 19

Sales (in millions of euros)

Sales 13,141

Orders 13,802

Group profit 454

Employees 55,000

Group profit margin

Sales by region

Germany

Others

Americas

Asia-Pacific

Target: 8-11%

5.6%

Communications (Com)

12,238 12,708

(in millions of euros) FY 2005

Europe (excl. Germany)

35%16%

13%

15% 21%

2003*) 2004

No. 1 IP PBX systems

No. 1 UMTS networks (with partner NEC)

No. 1 Wireless modules

No. 1 IP convergence for carriers

3.5%

13,141

2005*) Figures not consolidated

-2.0%

Page 20

Sales 5,373

Orders 6,531

Group profit -690

Employees 39,000

Group profit margin

Sales by business field

Operation Related Services

ProductRelatedServices

Solution Business

52%

23%

25%

Target: 5-6%

Siemens Business Services (SBS)

6,034 5,773 5,205 4,716

1.7% 0.2% 0.8%

(in millions of euros) FY 2005

No. 1 Outsourcing partner in the European media business

No. 1 IT service provider in the German financial sector

No. 1 Solutions provider in discrete manufacturing in West. Europe

Sales (in millions of euros)

5,373

2001 2002 2003 2004

-4.3%

2005-12.8%

Page 21

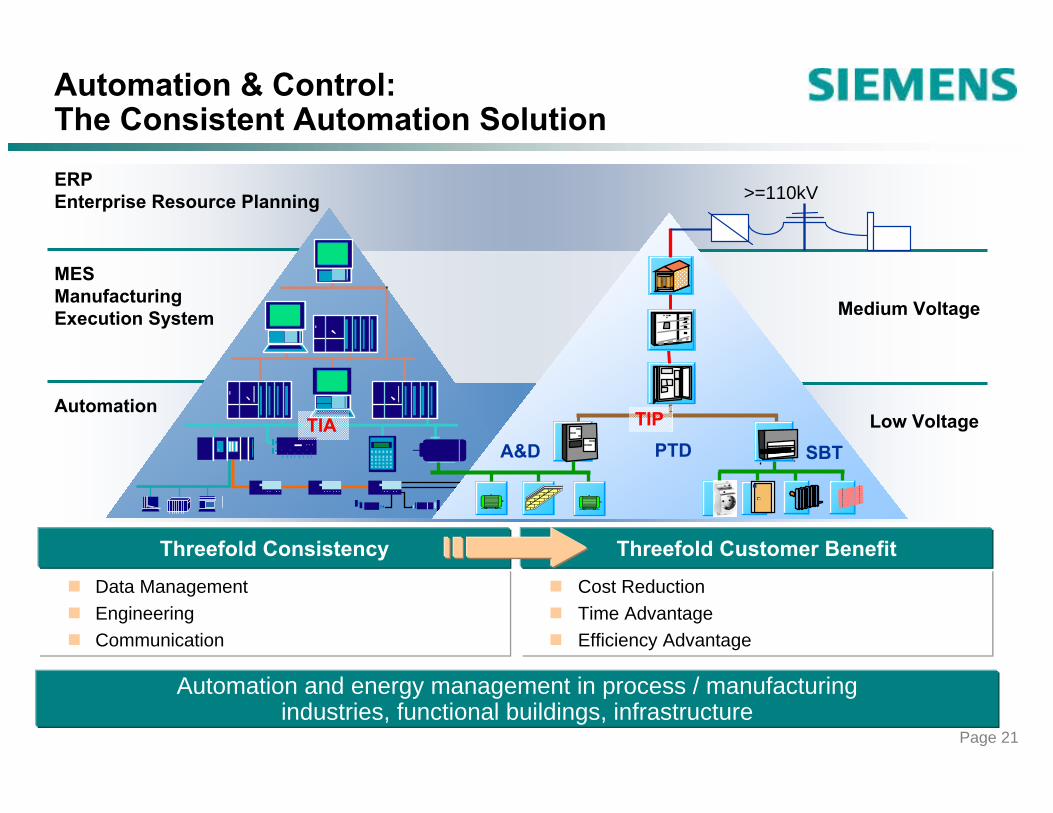

Automation & Control: The Consistent Automation Solution

Data ManagementEngineeringCommunication

Cost ReductionTime AdvantageEfficiency Advantage

A&D PTD SBT

>=110kV

MESManufacturing Execution System

ERPEnterprise Resource Planning

Automation

Medium Voltage

Low Voltage

Threefold Consistency Threefold Customer Benefit

Automation and energy management in process / manufacturing industries, functional buildings, infrastructure

TIA TIP

Page 22

Power: The future energy landscape will be environmental-friendly and integrated

Deep Sea Exploration

Gas Liquefaction LNG Gas To Liquids GTL

Integrated Gasification IGCC

Off-shore Windpark

Unconventional Oils(tar sands, oil shales)

Synfuels from Gasification

System Load Management

Fuel Cells

CO2 Separation/Deposition

Power PlantDispatch Optimization

Hydrogen Economy

Flue Gas Cleaning(Scrubbers, Mercury)

Nuclear Power Plant

Page 23

Medical: New business opportunitiesare large and fast growing

2004 2007

~ 96

~ 130

~ 61

~ 35 ~ 41Major market segmentscurrently served

New potentialfocus areas, e.g.:

Contrast mediaIn vitro diagnostics(incl. Biochips and mass spectroscopy)Tissue engineering

(in € billions; currency adjusted)

+13% p.a.

+6% p.a.

Page 24

Med: Soarian and Syngo cover the continuum of care ...

Resourceplanning ADT

POE

BillADT

Document

OR, Onco, Cardio

Intensive

Station

Ward

LaboratoryECG

Administrative Cycle

Therapeutic Cycles

Diagnostic Cycles

Care Cycles

ClinicalCycles

Radiology

Rehabilitation

syngoTM

syngoTM

syngoTM

SoarianTM

... combining the diagnostic, therapeutic and care cycles, with the clinical and administrative cycles

syngoTM

SoarianTM

23,000 Soarian userson a daily basis,72+ live customers,over 1 billion patientresults converted

Page 25

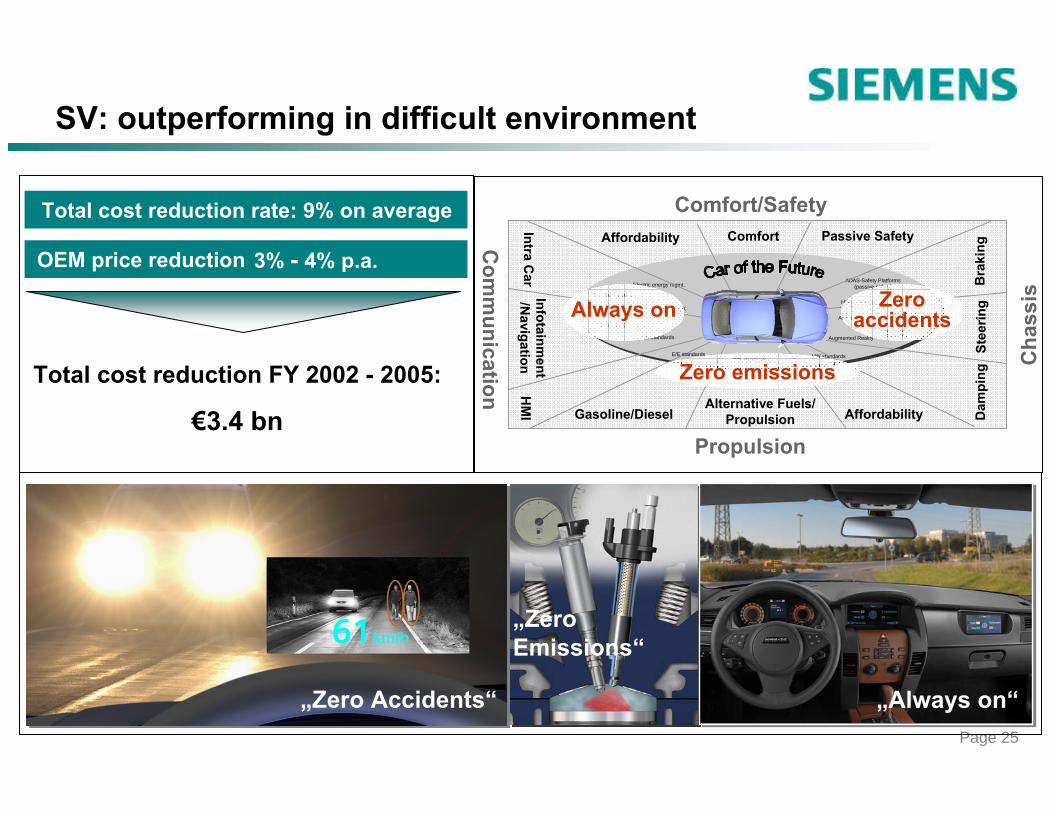

SV: outperforming in difficult environment

OEM price reduction

Total cost reduction FY 2002 - 2005:

€3.4 bn

3% - 4% p.a.

Total cost reduction rate: 9% on average

„Zero Accidents“

„ZeroEmissions“

„Always on“

Comfort/Safety

Com

munication

Affordability Comfort Passive Safety

Dam

ping

Stee

ring

Bra

king

HM

IInfotainm

ent/N

avigationIntra C

ar

Gasoline/DieselAlternative Fuels/

Propulsion Affordability

Cha

ssis

E/E standards

Active Safety

Key less cockpit

HW standards

New production concepts

Improved Diagnostics

E/E standards Augmented Reality

ADAS-Safety Platforms (passive safety)Electric energy mgmt.

Workload manager

1st gen ADAS

Propulsion

E/E standards

HW standards Zeroaccidents

Zero emissions

Always on

Page 26

Osram: applications for future lighting business

Illumination Visualization Sensing Special

Making something visible Other applications from material and water treatment to medical

Use light to displayany type of information

Light is detected or detects something

3%* 10%* 6%* 6%*

e.g. backlighting for electronic devices, high-tech lamps for projection, ...

e.g. sensors for automotiveapplications (rain sensors, distance control), ...

e.g. water purification systems (UV light), purification of wafer, ...

* Market CAGR (2006-2015) / estimation by OSRAM

Megatrends: Demographic Change and Urbanization

e.g. energy saving lamps,high-brightness LEDs, head-lights for automotive, ...

Page 27

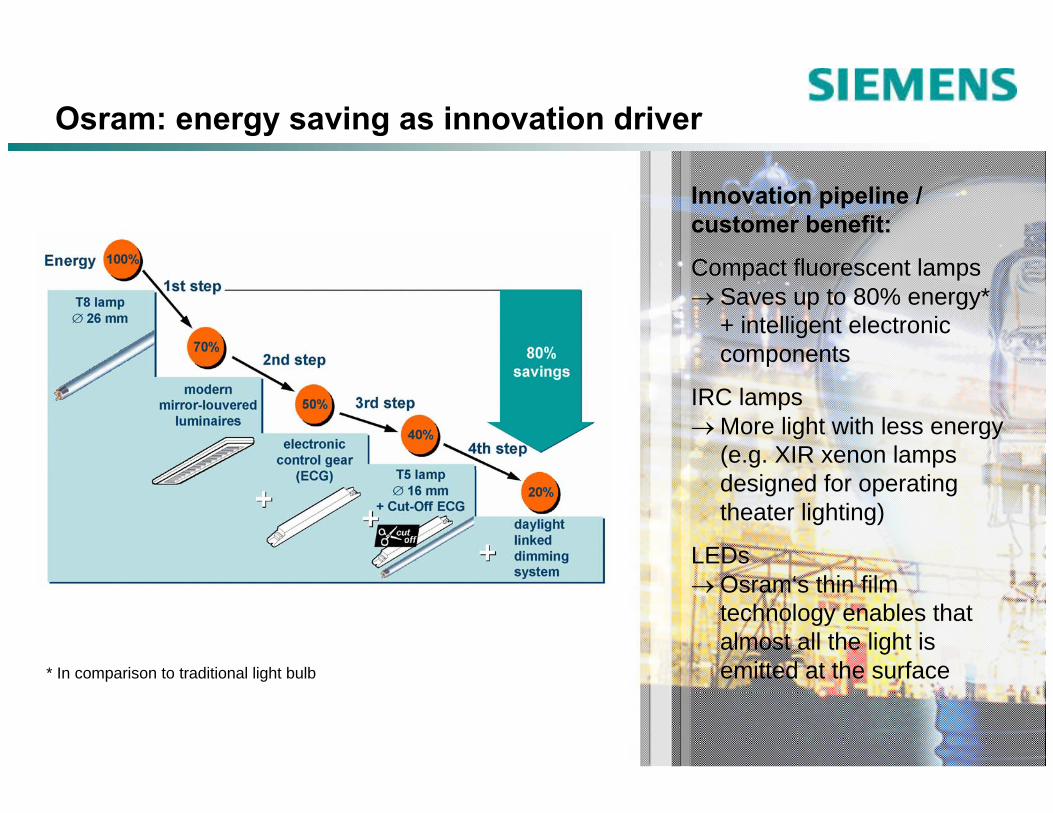

Osram: energy saving as innovation driver

Innovation pipeline / customer benefit:

Compact fluorescent lamps→ Saves up to 80% energy*

+ intelligent electronic components

IRC lamps→ More light with less energy

(e.g. XIR xenon lamps designed for operating theater lighting)

LEDs→ Osram‘s thin film

technology enables that almost all the light is emitted at the surface* In comparison to traditional light bulb

Page 28

”Group profit from Operations” is reconciled to ”Income before income taxes” of Operations under ”Reconciliation to financial statements”on the table ”Segment information.” See ”Financial Reports / Fiscal 2005, Annual Report Fiscal 2005 or Fiscal 2006 / Quarter 1 / Financial Statements” at our Investor Relations website under www.siemens.com

The allocated equity for SFS is determined and influenced by the respective credit ratings of the rating agencies and by the expected size and quality of its portfolio of leasing and factoring assets and equity investments and is determined annually. This allocation is designed to cover the risks of the underlying business and is in line with common credit risk management standards in banking. The actual risk profile of the SFS portfolio is monitored and controlled monthly and is evaluated against the allocated equity.

”ROE” (Return on equity) margin for SFS was calculated as SFS’ income before income taxes divided by the allocated equity for SFS. Allocated equity for SFS as of September 30, 2005 was €983 million. See also Siemens’ Form 20-F at our Investor Relations website under www.siemens.com

Siemens ties a portion of its executive incentive compensation to achieving economic value added (EVA) targets. EVA measures theprofitability of a business (using Group profit for the Operating Groups and income before income taxes for the Financing and Real estate businesses as a base) against the additional cost of capital used to run a business, (using Net capital employed for the Operating Groups and risk-adjusted equity for the Financing and Real estate businesses as a base). A positive EVA means that a business has earned more than its cost of capital, and is therefore defined as value-creating. A negative EVA means that a business is earning less than its cost of capital and is therefore defined as value-destroying. Other organizations that use EVA may define and calculate EVA differently.

A reconciliation of EVA may be found on our Investor Relations website under www.siemens.com

Reconciliations and definitions

Page 29

Siemens Investor Relations Team

Webpage: http://www.siemens.com Investor Relations

e-mail: [email protected]

Fax: +49-89-636-32830

Marcus Desimoni +49-89-636-32445

Frank Heffter +49-89-636-34095

Irina Pchelova +49-89-636-33693

Christina Schmöe +49-89-636-32677

Susanne Wölfinger +49-89-636-30639