Growing Annual Report 2008 Partnerships Worldwide

88

Annual Report 2008 Growing Partnerships Worldwide

Transcript of Growing Annual Report 2008 Partnerships Worldwide

A n n u a l R e p o r t 2 0 0 8G r o w i n gP a r t n e r s h i p sW o r l d w i d e

Fenner is a world leader in reinforced polymer technology.

Our strategy is to increase market share and target newvalue added product areas.

We will continue to concentrate on growing thosebusinesses where we already demonstrate leadershipthrough our skills in applications, design, materialstechnology and dedication to customer service as well asby carefully planned acquisitions.

G r o w i n gP a r t n e r s h i p sW o r l d w i d e

Contents

1 Financial Highlights

2 Chairman’s Statement

5 Business Review - ChiefExecutive Officer’s Review

1 3 Business Review - GroupFinance Director’s Review

1 6 Business Review - Definition ofKey Performance Indicators Used

1 7 The Board

1 8 Corporate Governance

2 3 Corporate Responsibility Report

2 7 Board Remuneration Report

3 4 Directors’ Report

3 8 Independent Auditors’ Report

3 9 Group Financial Statements

7 6 Independent Auditors’ Report- Company

7 7 Company Financial Statements

8 2 Five Year Summary of the Group

8 3 Annual General MeetingAdvisorsFinancial Calendar

F i n a n c i a l H i g h l i g h t s

F e n n e r P L C 1

2008 % increase£m on 2007

Revenue 437.8 +15%

Operating profit before amortisation of intangible assets acquired and exceptional items 49.3 +26%

Operating profit 43.8 +15%

Profit before taxation 36.3 +8%

Adjusted earnings per share before amortisation of intangible assets acquired and exceptional items 17.5p +16%

Basic earnings per share 15.5p +3%

Dividend per share 6.6p +6%

A y e a r o f s t r o n go r g a n i c a n da c q u i s i t i v e g r o w t h

C h a i r m a n ’ s S t a t e m e n t

FINANCIAL HIGHLIGHTSRevenue increased to £437.8m (2007£380.8m), driven by robust activity levels inboth divisions and acquisitive growth of£18.5m. The Conveyor Belting ("CB")Division experienced high levels of demandin its major markets against a backdrop ofbuoyant global coal markets. In theAdvanced Engineered Products ("AEP")Division, overall high activity levels andstrong performances from the acquiredbusinesses were marginally tempered bysome softer markets in our PrecisionPolymers businesses.

Operating profit before amortisation ofintangible assets acquired and exceptionalitems increased to £49.3m (2007 £39.0m),with the contribution from acquisitionsamounting to £4.1m.

Exceptional items of £3.4m (2007 £0.2m)principally related to the costs associatedwith the expansion of the heavyweightconveyor belting business in North Americaand the profit on disposal of its non-corelightweight PVC conveyor belting operation.

Operating profit was £43.8m (2007 £38.2m).Net finance costs increased to £7.5m (2007£4.6m) as a result of higher borrowingsrelating to the Group’s strategic expansion.

The headline and underlying tax rates were29% and 30% respectively. Adjustedearnings per share before amortisation ofintangible assets acquired and exceptionalitems was 17.5p per share (2007 15.1p).Basic earnings per share amounted to 15.5pper share (2007 15.0p).

Net cash from operations generated £45.7m(2007 £53.3m) and included an investmentin working capital of £8.2m associated withgrowth, with working capital ratiosmaintained at prior year levels. Investingactivities amounted to £104.2m (2007£35.4m), in accordance with our strategicexpansion plans. In part, this expansion wasfunded by £35.4m of equity raised in March2008 through the placing of 15.7m ordinaryshares. Net debt was £97.6m (2007£36.3m), in line with expectations despite anincrease of £10.9m relating to the translationof foreign currency borrowings. Interestcover was 6.8 times (2007 8.9 times).

The Board is recommending a final dividendof 4.4p per share which gives a totaldistribution for the year of 6.6p per share(2007 6.225p), a 6% increase on 2007.

ACQUISITIONS AND INVESTMENTIt is most encouraging to report on the majorgrowth initiatives around the Group. Theimplementation of our strategic plan hasbeen successful with seven businessesacquired during the year and one disposal.After the year end, two further acquisitionswere completed. This reflects our plansindicated in our share placing which wasannounced in March 2008.

In November 2007, B-LOC in the US wasacquired by AEP for an initial considerationof £4.4m with future contingent deferredconsideration estimated at £0.6m at the yearend. Its products extend and complementour existing range of high value added,proprietary drive solutions.

I am delighted to report on a year of strong organic and acquisitive growth. The

number of new businesses acquired has been unprecedented. These have performed

well in the period from acquisition and their contribution, when combined with

excellent results from our existing operations, has led to a 26% increase in operating

profit before amortisation of intangible assets acquired and exceptional items.

2 F e n n e r P L C

In December 2007, Spliceline in Australiawas acquired by CB, expanding our servicecoverage in the Northern Territory. The initialconsideration was £0.7m with £0.2mdeferred to a later period.

In February 2008, Prodesco, Inc in the USwas acquired by AEP for an initialconsideration of £24.2m and estimatedcontingent deferred consideration at the yearend of £8.1m, over a five year period.Prodesco, Inc comprises two businesses;Prodesco and Secant Medical. Prodescoproduces a range of highly specialisedwoven, knitted and braided fabrics which areused in the industrial, aerospace andchemical sectors. Secant Medicalspecialises in the design, development andmanufacture of complex implantable fabricsfor the medical device industry. Theacquisition enhances our core expertise intextile engineering and provides an excitingopportunity to expand our product portfoliointo a growth segment of the medical market.

In March 2008, Winfield Industries in the USwas acquired by AEP for £6.9m. Winfield is aleading supplier of performance criticalrollers for digital imaging applications and isa natural fit with our Precision business.

Also in March, our geographical coverage inSouth Australia was enhanced whenNorthern Belting Specialists Pty Ltd wasacquired by CB for £2.3m. The businessspecialises in belt splicing, rubber lining,mechanical and technical servicing andbelting sales.

In April 2008, the business of King EnergyServices in New Mexico, US was acquiredby CB for £2.9m followed in August 2008 bythe acquisition of the business of KingEnergy Services in Colorado, US for £3.5m.These businesses, which are now integratedinto Fenner Dunlop Conveyor Services,enable us to offer a full service capability inthe south west mining region of the US.

Our non-core lightweight PVC conveyorbelting business in the US was divested inJuly 2008 for £5.0m excluding costs.

Post year end, in October 2008, the Groupacquired the businesses of the Conveyor

Services Corporation group of companies,including Loadout Services, principallylocated across the US, with a majorityinterest in Conveyor Services, SA in Chile,and Solid Systems Engineering, LLC inWyoming. The total initial consideration was£31.0m with estimated contingent anddeferred consideration payable of £22.0m(based on the exchange rates at the dates ofcompletion). These acquisitions extend therange and scope of services offered to ourcustomers and represents an importantfurther step towards our goal of building aworld class mining service operation whichmakes Fenner Dunlop Conveyor Services theleader in its field in the Americas.

Our organic capital investment programmesadvanced during the year. The integration ofour seals business in Houston onto a singlesite was completed ahead of schedule whilstour major projects in the CB Divisioncontinued to progress and will contribute tooperational performance in 2009.

OPERATIONSThe CB Division’s result was strong asdemand levels benefited from buoyantmining conditions in its major markets. InAsia Pacific, the continuing expansion andwider geographical coverage enabled us tofurther develop our product and serviceofferings. In Europe, the focus on developingnew markets and leveraging our strongDunlop brands was rewarded with highervolumes. In North America, demandremained high while some anticipatedmargin decline was evident in the lattermonths of the year as raw material costsincreased significantly. The growth of ourservice businesses through the acquisitionscompleted to date has enhanced ourcapability to offer a complete engineeredsolution to our customers.

The AEP Division traded well, overcominguncertainty and some softer markets in thePrecision Polymers businesses. Our newlyacquired businesses performed strongly andassisted in the penetration of growthmarkets. The Advanced SealingTechnologies businesses made solidprogress with continuing strength in the oiland gas and mining sectors.

F e n n e r P L C 3

PEOPLEThe success of the Group is due to the talentand dedication of colleagues around theworld. On behalf of the Board, I would like toextend my gratitude and appreciation fortheir continuing support.

OUTLOOKWe enter the new year with healthy orderbooks for our CB businesses. Despite thetemporary disruption from Hurricane Ike, ourAEP businesses started with similar saleslevels to the end of last year.

There has been a limited initial impact on usfrom the global financial crisis but we are ofcourse alert to the wider economic effectsthat are generally expected. These are morelikely to be seen in industrial marketsalthough the niche nature of our businessesand the diversity of our markets provideadditional strength and resilience. Theenergy markets remain buoyant with apositive outlook, particularly for coal,notwithstanding the recent reduction in theprices of commodities. The majority of ourproducts and services are consumablesupplies and are therefore driven by usagerather than the price of commodities.Accordingly the output for these remainsrobust.

Despite the inevitable challenges, we believewe are very strongly placed to out-perform.For the longer term, our business driversremain highly positive.

Colin CookeChairman

4 F e n n e r P L C

C h a i r m a n ’ s S t a t e m e n t c o n t i n u e d

INTRODUCTIONThis Business Review sets out the strategicobjectives of the Group and its businesses,as well as a review of progress in 2008, theoutlook for 2009 and beyond and anassessment of the key risks anduncertainties.

During the past year Fenner hasstrengthened its position as a world leaderin reinforced polymer technology throughboth acquisition and organic investment.The aim of the Fenner businesses is todeliver high quality, value added productsand services to our customers. Whereverpossible we operate in niche markets whichenable the operations to avoid the highlycompetitive, low margin commodity end ofthe markets in which we operate. Thiscommon aim enables Fenner to deliver asolid basis for long term growth, stabilityand shareholder value. Fenner is proud tobe a world class global manufactureroperating in key territories in establishedand emerging markets.

The Fenner Group consists of two Divisions,the Conveyor Belting (“CB”) Division and theAdvanced Engineered Products (“AEP”)Division.

The CB Division is a recognised worldleader in the global conveyor belting market,concentrating on heavyweight ply, solidwoven and steel cord conveyor belting formining, power generation and industrialapplications. During the year, it has beenexpanding its service offering throughorganic growth and acquisitions to satisfy itscustomers' requirements from belt order toinstallation and maintenance. Thelightweight non-rubber conveyor beltingoperation, based in Charlotte, NorthCarolina, was sold to Forbo Seigling, Inc (amajor force in that market) and, although wedivested manufacturing capability, strongstrategic links remain.

The AEP Division is divided into five productgroup based businesses which aremanaged on a global basis. Thesebusinesses are as follows:• Fenner Precision, which is a leading

supplier of performance critical polymercomponents to the office automationindustry;

• Fenner Drives, which designs,manufactures and sells an extensiverange of bespoke solutions for mechanicalpower transmission and motion transferapplications;

• The supply of silicone and EPDMspeciality hoses for the diesel engine,truck, bus and off-road equipment OEMmarket, trading as James Dawson;

• Fenner Advanced Sealing Technologies("FAST") comprising hydraulic andpneumatic seals for the global fluid powerindustry, trading as Hallite and bespokesealing products for process applicationsincluding oil and gas, electronics, pumps,valves, compressors and aerospaceapplications, trading as CDI/EGC; and

• Technical textiles, trading as Prodescoand Secant Medical.

Prodesco, Inc together with its subsidiarySecant Medical, LLC, acquired in February2008, not only brought a complementaryindustrial textile business but also satisfied along term goal of entering into niche medicalapplications which provide further excitingopportunities for AEP.

Both CB and AEP provide high quality,comprehensive, whole life value products fortheir customers, and both have a strongbrand and reputation in their chosenmarkets. These characteristics areconsidered to be key to the success of theGroup over its long history. Customersatisfaction is of importance to all businessunits, who ensure they are meeting theircustomer expectations which are specific toeach market. Performance measurements

“After a year of strategic investment the Group is strongly positioned to face the

challenges of economic circumstances.”

Mark Abrahams - Chief Executive Officer

R o b u s t a n dr e s i l i e n t

B u s i n e s s R e v i e wC h i e f E x e c u t i v e O f f i c e r ’ s R e v i e w

F e n n e r P L C 5

B u s i n e s s R e v i e wC h i e f E x e c u t i v e O f f i c e r ’ s R e v i e w c o n t i n u e d

include customer surveys and “on time infull” performance.

STRATEGIC OBJECTIVESIt has been a very exciting year for theGroup with organic investment andacquisition activity in both Divisions whichexpand the product ranges, geographiccoverage, routes to market, service offeringand market shares. The investments andacquisitions ensure Fenner continues togrow its reputation as a specialist polymerengineering company and help it maintainprofitability throughout the economic cycle.

The acquired Secant Medical business isthe ideal custom manufacturing partner forthe most demanding medical deviceengineering challenges. Working withpartners, both large and small, itsexperience with specialised biocompatiblemedical textile structures is aimed to helpbring new biomedical device ideas tomarket. Prodesco produces highlyspecialised technical fabrics forperformance critical applications inindustrial, aerospace and chemicalequipment markets. The Prodesco andSecant Medical businesses will remainautonomous operations within the Group.

The other acquisitions for AEP were B-LOCand Winfield Industries. B-LOC, which hasbeen fully integrated into the Fenner Drivesbusiness of AEP in Manheim, is a leadingsupplier of multi-screw keyless bushings andcomplements the existing Fenner Drivesrange. It has opened up channels to marketfor both the historical Fenner Drives andB-LOC products. Winfield Industries isrecognised as a leading supplier ofperformance critical rollers for digital imagingapplications and allows Fenner Precision togain access to the rapidly growing market fordigital printing presses. With a significantmarket share in the mature inkjet market, thisacquisition enables Fenner Precision to offeran unrivalled range of technical capability,products and experience to the global officeautomation market.

The seals manufacturing operation inHouston completed the major factoryexpansion ahead of schedule. Not only did itsuccessfully integrate the EGC business intothe new facility on budget but also out-performed the plan throughout the process.The improved layout and investment inequipment has seen efficiencies and marginsimprove at the combined facility, which is nowstate of the art, and provides the springboardfor further growth and market diversification

from this dynamic business with strongadvanced materials capabilities.

The FAST operations in China continue to dowell and additional manufacturing lines havebeen relocated from the Hampton site toChina ahead of plan. The Hampton sealsoperation was highly successful in securingnew and additional business which enabledit to grow, notwithstanding the transfer ofbusiness to China. Other strategic initiativesprogressed well during the year. Theseincluded the geographical expansion ofmarkets serviced with sales, technical andcustomer service teams recruited in Chinaand Brazil and strengthened service teamsacross the globe.

The CB operations in Australia havereceived both major organic and acquisitioninvestment. A planned investment in a newsteel cord facility is now underway in Perth,Western Australia. This facility is located toservice the fast growing iron ore sector ofthe Australian economy which, together withcoal, are the main trading and exportsectors for Australia. There have also beenstrategic acquisitions of service businessesin Darwin and Whyalla which service theNorthern Territories and the multi-mineral orebodies in South Australia respectively. Thesehave added to the successful FennerDunlop Conveyor Services business alreadyoperating in Australia. Leading with a focuson safety, the expertise and strength of theservice team and management continuesthe strategy to maintain the broadestnational coverage in Australia and to ensurethat the operation is well placed to takeadvantage of opportunities in the regionswith significant mining growth.

The success of the service model inAustralia is being leveraged in the Americaswith the acquisitions of King EnergyServices in Colorado, King Energy Servicesin New Mexico, the Conveyor ServicesCorporation group of companies and SolidSystems Engineering. These businesses willform the backbone of the Fenner DunlopConveyor Services business for NorthAmerica. Work is underway to integratethese businesses into the Group. Not only isFenner Dunlop Conveyor Services thelargest belt servicing business focused onthe mining industry but the locations of ourbranches also align with those of ourcustomers. The strength of the servicebusiness will support the wider productoffering from the expanded Fenner DunlopAmericas manufacturing operation. Further,experience suggests the service business is

6 F e n n e r P L C

counter cyclical to belt sales, helping toensure that the CB operation has someprotection from market cycles.

CB has also invested in a significant numberof manufacturing plants with the continuationof the investment in the North Americanplants in Port Clinton and Toledo togetherwith the construction of a purpose built,bespoke weaving operation in Hart County,Georgia. These new facilities will improveflexibility and efficiencies in both productionand energy consumption and reduce waste.As well as extending the product range,capacity constraints of prior years,particularly for steel cord belting, will also beeased. Coupled with our new plant, theservice business acquisitions mean thatFenner Dunlop Americas not onlymanufactures the full range of productsrequired by our customers but also haslocations close by, offering comprehensiveservice and support.

Investment in the South African operationwas also completed in the year with theinstallation of a steel cord line to enable it tosupply both the domestic and exportmarkets. Following investment in theprevious year, China saw the introduction ofa range of Dunlop branded belts,successfully targeted at broadening thecustomer base.

As a diversified Group, Fenner uses a widerange of materials, from traditional cottonyarns to the latest perfluoroelastomers. Notonly do we use significant volumes of somematerials, we also work closely with selectedsuppliers to ensure that our customersbenefit from the latest technicaldevelopments in materials and processes.Most of these relationships are in the normalcourse of business, ensuring quality,continuity of supply and reasonablecommercial terms. Where appropriate, andusually relating to technical developments,relationships are formally documented.

CONVEYOR BELTINGMost of the CB operations experiencedpositive trading conditions through the yearunder review although all faced a variety ofchallenges including the effects of volatile rawmaterial prices and availability, competitivethreats and availability of skilled labour.Capacity constraints of prior years have beenaddressed and, where new constraints havearisen, are being addressed with the resultthat the operations are well placed to defendtheir position in the markets.

The global demand for bulk commoditiesincluding iron ore, copper, potash and thedemand for power, in the form of coal,helped to ensure that the global CBoperations had a strong year with increaseddemand and improved return on sales,particularly in Europe, Australia and China.North American operations had strong orderbooks through the year but were impactedsomewhat by pricing constraints and rawmaterial price volatility. Price increases arebeing implemented where possible and theoperations work closely with suppliers andcustomers to help facilitate and build on thestrong relationships in the supply chain.

Volume constraints have driveninternationally traded coal prices to an alltime high, as shown in the McCloskey graphbelow. Over the last three years coal priceshave remained comfortably over the“trigger” value at which coal companies buybelt. The volume of coal being minedcontinues to increase as demand for energyin China, India and South East Asia remainsstrong, together with a desire in the US to beindependent from energy suppliers,particularly for oil. Globally, coal resourcesare located in less politically fragile markets.Whilst prices have probably peaked, thevolume demand for coal remains bullish andthe long term outlook remains good.

With the additional steel cord capacity, otherminerals, particularly iron ore, become moreimportant to Fenner and, almost withoutexception, volumes and prices have beenstrong throughout the year.

ADVANCED ENGINEERED PRODUCTSAll operations within AEP aim to providehigh value added solutions to theircustomers’ needs using advancedpolymeric materials, expertise in applicationdesign, effective manufacturing design skillsand timely delivery.

F e n n e r P L C 7

NW Europe - Steam Coal Marker

Monthly Average

B u s i n e s s R e v i e wC h i e f E x e c u t i v e O f f i c e r ’ s R e v i e w c o n t i n u e d

Raw material price increases and the risingcost of energy were a feature of tradingthroughout the year, driven by the increasein commodity prices. Flexible pricingstrategies with customers enabled many ofthese costs to be recovered. The focusremains on performance critical productswhich are not selected on price alone butthe value they add to the customer.

FAST continued with its recent strongperformance and achieved yet anotherrecord year of growth. Continuing demandfor seals used in oil, gas and miningapplications remains robust but there hasalso been an increase in demand forproducts used in general hydraulic andaerospace applications. The roll out of theSix Sigma continuous improvementprogramme continued across all locationswith the result that lead times and availabilityimproved significantly during the year. FASTremains committed to its geographicalexpansion of markets served to include Asiaand South America. Some product areas areexpected to be impacted by the slowdownin the economy, principally seals used in thesemiconductor industry, processingequipment and seals for hydraulicequipment used in the construction industry.Any weakening of demand is expected tobe compensated for by the initiatives thathave been put in place to grow the businessoverall.

The James Dawson hose business finishedthe year well despite some unforeseenadverse impacts of VAT changes in China.Demand levels were good for the first threequarters of the year but slowed in the finalquarter as the effects of the downturn in theconstruction industry impacted on theoff-road equipment market. The outlook forthe construction industry is not expected toimprove in 2008/09. The operation in Chinacontinues to grow in strength and capabilityas domestic Chinese manufacturers seek toredesign engines and vehicles to complywith emissions legislation which wasenacted in China in the summer of 2008.

Fenner Precision completed the acquisitionof Winfield Industries in March 2008 andquickly integrated the global sales andmarketing activities of both businesses sothat the consolidated sales force is focusedon cross selling products. This has resultedin new opportunities for growth beingidentified. Fenner Precision enjoyed strongdemand from the ATM sector as well as thecommercial digital printing market but therewas some shortfall from the consumer

related office automation sector. Growth isexpected to resume in 2008/09, led by thedigital printer market demand.

Fenner Drives integrated the acquiredB-LOC business and produced excellentresults with synergies from the acquisitionbeing achieved during the year. Salesincreased rapidly in targeted markets as aresult of the investments made during theprior two years. The business continues todevelop and market a growing range ofinnovative, proprietary products which solveproblems in the motion control, powertransmission and unit handling markets. Thegeneral industrial markets are feeling theeffects of the economic slowdown,particularly in the latter stages of the yearunder review, and this trend is expected tocontinue into the first half of the newfinancial year.

The Prodesco and Secant Medicalbusinesses have yet to complete a full yearwithin the Fenner Group but early indicationsare very positive and the cultural fit with AEPis excellent. They produced encouragingresults in the half year they have beenowned by Fenner. A strategic review of thebusiness was carried out during the year tohelp identify future growth and development.Secant Medical is believed to be cushionedfrom the effects of the slowing economybecause its growth is largely driven by thedemographics of an ageing population. TheProdesco business is exposed to theindustrial and aerospace markets.

The AEP division will continue to look forgrowth opportunities and to build upon itsconsiderable strengths and overall ismaking good progress against the currentstrategic plan.

OUTLOOKGiven the global financial crisis, we continueto monitor very closely all relevant aspectsof our business including credit, customerand supplier stability and raw material pricevolatility. Although commodity prices areweakening, the volume demand remainsstrong and it is volume rather than pricewhich leads to consumption of our products.The niche nature of our businesses providessignificant additional strength in times ofuncertainty.

EMPLOYEESFenner continues to benefit from a stable,skilled and committed workforce in both ouracquired and existing businesses and weacknowledge the importance of our

8 F e n n e r P L C

employees’ contribution to the performanceof the Group. All businesses have processesthat require high levels of skill and technicalexpertise. Many of the end products areused in safety critical applications, perhapsepitomised by the Secant Medicalsubstrates, and therefore a skilled andmotivated workforce is essential to maintainproduct safety, reliability and quality.

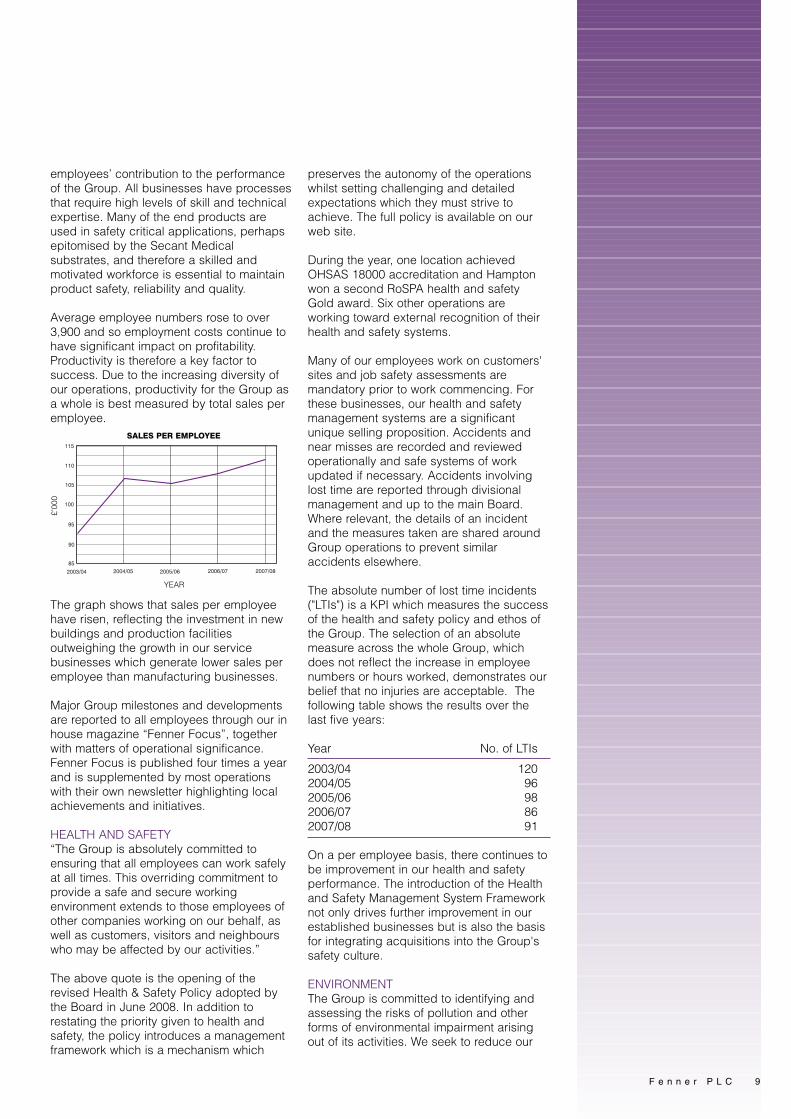

Average employee numbers rose to over3,900 and so employment costs continue tohave significant impact on profitability.Productivity is therefore a key factor tosuccess. Due to the increasing diversity ofour operations, productivity for the Group asa whole is best measured by total sales peremployee.

The graph shows that sales per employeehave risen, reflecting the investment in newbuildings and production facilitiesoutweighing the growth in our servicebusinesses which generate lower sales peremployee than manufacturing businesses.

Major Group milestones and developmentsare reported to all employees through our inhouse magazine “Fenner Focus”, togetherwith matters of operational significance.Fenner Focus is published four times a yearand is supplemented by most operationswith their own newsletter highlighting localachievements and initiatives.

HEALTH AND SAFETY“The Group is absolutely committed toensuring that all employees can work safelyat all times. This overriding commitment toprovide a safe and secure workingenvironment extends to those employees ofother companies working on our behalf, aswell as customers, visitors and neighbourswho may be affected by our activities.”

The above quote is the opening of therevised Health & Safety Policy adopted bythe Board in June 2008. In addition torestating the priority given to health andsafety, the policy introduces a managementframework which is a mechanism which

preserves the autonomy of the operationswhilst setting challenging and detailedexpectations which they must strive toachieve. The full policy is available on ourweb site.

During the year, one location achievedOHSAS 18000 accreditation and Hamptonwon a second RoSPA health and safetyGold award. Six other operations areworking toward external recognition of theirhealth and safety systems.

Many of our employees work on customers'sites and job safety assessments aremandatory prior to work commencing. Forthese businesses, our health and safetymanagement systems are a significantunique selling proposition. Accidents andnear misses are recorded and reviewedoperationally and safe systems of workupdated if necessary. Accidents involvinglost time are reported through divisionalmanagement and up to the main Board.Where relevant, the details of an incidentand the measures taken are shared aroundGroup operations to prevent similaraccidents elsewhere.

The absolute number of lost time incidents("LTIs") is a KPI which measures the successof the health and safety policy and ethos ofthe Group. The selection of an absolutemeasure across the whole Group, whichdoes not reflect the increase in employeenumbers or hours worked, demonstrates ourbelief that no injuries are acceptable. Thefollowing table shows the results over thelast five years:

Year No. of LTIs

2003/04 1202004/05 962005/06 982006/07 862007/08 91

On a per employee basis, there continues tobe improvement in our health and safetyperformance. The introduction of the Healthand Safety Management System Frameworknot only drives further improvement in ourestablished businesses but is also the basisfor integrating acquisitions into the Group'ssafety culture.

ENVIRONMENTThe Group is committed to identifying andassessing the risks of pollution and otherforms of environmental impairment arisingout of its activities. We seek to reduce our

SALES PER EMPLOYEE

YEAR

£’00

0

F e n n e r P L C 9

B u s i n e s s R e v i e wC h i e f E x e c u t i v e O f f i c e r ’ s R e v i e w c o n t i n u e d

impact on the environment to the lowestpractical levels and with each newinvestment ensure that we exemplify thebest contemporary practice in respect of theenvironment. At Board level, the ChiefExecutive Officer has specific responsibilityfor the development of policy andmanagement systems. Responsibility forenvironmental matters in each operatingdivision is designated to the DivisionalManaging Director and, at a local level, to asenior manager on each site. EachDivisional Managing Director is required toreport to the Board on a regular basis and toadvise the Board immediately of anyenvironmental risks or other incidents likelyto be significant to the business. No newrisks or incidents were reported to the Boardin the last year.

All acquisitions are subject to appropriateenvironmental due diligence which isspecifically extended to includeenvironmental management systems andoperational compliance. Compliance withapplicable regulatory standards is aminimum which is subject to official audit;other larger facilities validate theirmanagement systems by independent audit.Significant progress is being made onenvironmental management systems withone site achieving ISO 14000 and six otherlocations actively progressing towardsaccreditation in 2008 or 2009.

We are exploring suitable environmentalKPIs for the Group as a whole which canthen be reported in future years. Areasbeing looked at include energy consumptionand waste management, both of whichpotentially have a direct environmental andbusiness impact. A small number ofoperations have assessed their carbonfootprint with a view to seeing if somemeaningful actions can result from suchmeasures and to prepare for a localcompliance requirement. To date the view isthat, whilst progress is being made, carbonfootprint estimates are not yet a validconsistent measure comparable across thewide range of sizes, technologies andlocations of the Group’s units.

In addition to our environmentalresponsibilities, there are sound commercialreasons to minimise and recycle waste. As amanufacturing Group, the obvious focus ison raw materials as the reductionopportunities are well known and, for theresidual waste, recycling well understood.However, in a number of locations there issubstantial water usage. This can be a

significant local issue, for example inAustralia, where our conveyor belting plantin Melbourne voluntarily reducedconsumption by over 60%.

Air quality can be adversely affected bysome of our processes and significantinvestment and maintenance costs areincurred to ensure this does not happen.A number of locations use processes whichinvolve a range of chemicals which aregenerically referred to as volatile organiccompounds (“VOCs”). These chemicals aresubject to strict regulation with their storageand use carefully controlled. In addition tominimising any emissions to air of VOCs,potential substitutes are assessed as soonas they become commercially available.

The majority of the Group’s businesses haveoccupied their sites for many years, somefor over 100 years. The Group thereforerecognises and manages risk of exposure toenvironmental legacy issues.

Fenner continues to be committed toundertaking regular reviews of its activitiesand the workings of the environmental policyto ensure that it is comprehensive andeffective, identifying objectives and standardsthat will enable a demonstrable continuousimprovement in environmental matters.

PRINCIPAL RISKS AND UNCERTAINTIES Fenner considers the following to be themost significant risk factors for Fenner toconsider, but the risk factors listed do notnecessarily comprise all those associatedwith Fenner and are not set out in anyparticular order of priority.

Additional risks and uncertainties notpresently known to Fenner or that Fennercurrently deems immaterial may also havean adverse effect on its business.

Strength of key marketsThe impact of the recent unprecedentedfinancial market movements andsubsequent government interventions onFenner’s key markets are uncertain.However, Fenner is well positioned to benefitfrom the underlying volume growth in energymarkets, particularly oil and coal, andrecovery in industrial markets. AlthoughFenner has successfully traded throughprevious cycles, a substantial downturn inone or more of these key markets couldhave a material adverse impact on thebusiness. Fenner continues to look foropportunities that are counter cyclical tohelp balance out any market downturn.

1 0 F e n n e r P L C

Fluctuations in raw material costsVolatility in raw material costs continues tobe a key risk for the Group as there is adirect impact on the costs of production andmanaging customer expectation. The Groupcontinues to try to manage raw materialcosts. For example, where materials are asignificant cost of sale, we have long termsupply agreements and arrangements whichare driven by the constraints of the marketsinto which we sell. However, increases insuch costs could have a material adverseimpact upon the Group’s profitability andcash flow if such increases cannot berecovered through increased sales prices.

Climate changeIncreasing media attention is being given toclimate change and the political will to actappears to be responding to that coverage.Fenner takes full account of the substantivepublicised research in evaluating itsstrategic projects. The adoption of non-fossilfuel generation substantially in excess of theIEA Advanced Technology Scenario wouldhave a material adverse effect on thebusiness.

Fluctuations in foreign currencyDue to the global nature of the Group,Fenner derives a large proportion of itsrevenues from overseas and hence has anexposure to foreign currency fluctuations.Whilst the Group seeks to reduce this riskthrough formal contracts and borrowings,adverse movements in foreign currencies,particularly the US dollar relative to sterling,could lead to material adverse movementsin reported earnings.

CompetitionProducts are available which competedirectly or indirectly with the Group’sproducts. New technology, changingcommercial circumstances and new entrantsto the markets in which the Group operatesmay adversely affect the Group’s business.One source of competition comes from thelow cost economies but whilst these cancompete on price, they cannot alwayscompete on quality or service. Aggressive orpredatory pricing from competitors couldlead to a reduction in margin or volume.

Dependence on key personnelThe future success of Fenner is dependenton the continued services of key personnel.Although the Group has succession plansand seeks to develop and promote fromwithin, the loss of the services of theexecutive officers of the Group and other

key employees could have a materialadverse effect on the business.

Fluctuations of revenues, expenses andoperating resultsFenner’s revenues, expenses and operatingresults could vary from period to period as aresult of a variety of factors, some of whichare outside Fenner’s control. These factors,which are actively monitored andconsidered in all relevant managementdecisions, include general economicconditions, adverse movements in interestrates, conditions specific to the energymarkets, seasonal trends in revenues,capital expenditure, other costs and theintroduction of new products by Fenner or itscompetitors.

In response to a changing competitiveenvironment, Fenner may elect from time totime to make certain pricing, service ormarketing decisions or acquisitions thatcould have a material adverse effect on theGroup’s revenues, results of operations andfinancial condition. Despite the currentstrength of Fenner’s order book and orderpipeline, there is no guarantee that theseorders and expected orders will beconverted into sales, which could have amaterial adverse effect upon continuingprofitability and cash flow.

Employee benefit schemesThe Group has a number of employeebenefit schemes, including defined benefitpension schemes and US healthcareprogrammes. These schemes expose theGroup to changes in interest rates, otherinvestment returns and inflation as well asthe longevity of scheme members.Developments in medical science andchanges in healthcare management cansignificantly increase the cost of maintainingbenefits in the future. Appropriate financialand legal advice is taken on the rules andfunding of all such schemes.

Major projectsThe successful completion of major projects,such as significant capital expenditureprojects or acquisitions, is important to bothsustain and grow the business. All majorprojects have clearly identified resourcesand management responsibilitiesestablished during the approval process.However, failure to deliver on major projectscould have a material adverse impact onFenner’s ability to maximise both profitabilityand cash flow.

F e n n e r P L C 1 1

LitigationSubsidiaries of the Group are currentlyinvolved in certain disputes, actual andthreatened, and regulatory investigations.These disputes are actively managed inconjunction with our lawyers, other advisorsand insurers, with appropriate Boardreporting and oversight. If such disputesand investigations are not resolved inaccordance with the directors’ expectationsor in favour of the relevant subsidiary of theGroup or if a subsidiary incurs significantand unexpected costs or is required todevote significant additional resources,including management time, in the pursuit,defence or investigation of these matters,such disputes and investigations may havea material adverse impact on the business,financial resources, results and/or futureoperations of the Group.

FORWARD-LOOKING STATEMENTSCertain statements contained in thisdocument including those under thecaptions “Outlook” and “Principal Risks andUncertainties”, constitute forward-lookingstatements. Such forward-lookingstatements involve risks, uncertainties andother factors which may cause the actualresults, performance or achievements ofFenner, or industry results, to be materiallydifferent from any future results,performance or achievements expressed orimplied by such statements. Such risks,uncertainties and other factors include,among others: growth in the energy markets,general economic conditions and thebusiness environment, especially followingthe recent unprecedented financial marketmovements and subsequent governmentinterventions.

Mark AbrahamsChief Executive Officer

1 2 F e n n e r P L C

B u s i n e s s R e v i e wC h i e f E x e c u t i v e O f f i c e r ’ s R e v i e w c o n t i n u e d

B u s i n e s s R e v i e wG r o u p F i n a n c e D i r e c t o r ’ s R e v i e w

REVENUE AND OPERATING PROFITReported Group revenue increased by 15%to £437.8m (2007 £380.8m). Of thisincrease, 10% was generated by existingbusinesses and 5% by businesses acquiredduring the year.

In the CB Division, revenue increased to£292.2m (2007 £255.8m), with growth in allterritories as demand for its products andservices remained strong in the principalterritories in which it operates.

In the AEP Division, revenue increased to£145.6m (2007 £125.0m) from acquisitionactivity and strong growth from the sealsbusinesses.

Group operating profit before amortisation ofintangible assets acquired and exceptionalitems increased by 26% to £49.3m (2007£39.0m). Divisional profits contributed were£29.1m (2007 £24.2m) from the CB Divisionand £26.1m (2007 £20.0m) from the AEPDivision.

Exceptional items incurred of £3.4m (2007£0.2m) related to costs associated with theexpansion of the conveyor belting businessin North America of £3.7m (2007 £1.9m),acquisition integration costs of £0.4m (2007£0.8m) and a £0.7m profit on disposal of thelightweight PVC conveyor belting businessin the US.

Amortisation of intangible assets acquiredincreased to £2.1m (2007 £0.6m), reflectingacquisitions completed in the year.

Group operating profit increased by 15% to£43.8m (2007 £38.2m).

INTERESTThe net finance cost was £7.5m (2007£4.6m) and included £0.3m (2007 £0.2m) offinance costs on both discounted provisionsand contingent deferred consideration onacquisitions. The increase largely reflectedthe growth of net debt in the year as a resultof the planned acquisitions and capitalexpenditure. Interest cover was 6.8 times(2007 8.9 times).

TAXATIONThe taxation rate for the year was 29%(2007 29%). The underlying taxation ratebefore amortisation of intangible assetsacquired and exceptional items was 30%(2007 30%). Although the overall rate didnot change, the mix of the taxation chargereflected relatively high taxation ratesincurred on North American profits and an

additional deferred tax charge in the UKcaused by the phasing out of industrialbuildings allowances. These were offset bylower rates elsewhere, which included theutilisation of tax losses and tax assets notpreviously recognised for deferred taxation,particularly in the UK and continentalEurope, and the benefit of a tax holiday inChina.

EARNINGS PER SHARE AND DIVIDENDSBasic earnings per share was 15.5p (200715.0p) and, adjusted for amortisation ofintangible assets acquired and exceptionalitems, was 17.5p (2007 15.1p).

The interim dividend of 2.2p (2007 2.075p)was paid on 8 September 2008. The Boardis recommending a final dividend of 4.4p(2007 4.15p) to make a total dividend for theyear of 6.6p (2007 6.225p).

ACQUISITIONS AND DISPOSALSThe Group has completed sevenacquisitions during the year and two afterthe year end. One business was divestedduring the year.

The acquisitions completed during the yearare disclosed in note 33 to the Groupfinancial statements. The total cashpayments made in respect of theseamounted to £45.9m. The present value ofcontingent and deferred considerationpayable in future periods is estimated at£8.9m at the year end, with a maximumpresent value amount payable of £10.1m.The provisional fair value of net assetsacquired, including intangible amounts, was£41.0m and goodwill of £13.7m wascapitalised.

In October 2008, after the year end, £31.0mwas paid for the businesses of the ConveyorServices Corporation group of companies,including Loadout Services, and SolidSystems Engineering, LLC. The presentvalue of contingent and deferredconsideration payable is estimated at£22.0m (based on exchange rates at thedates of completion), with a maximumpresent value of £25.0m and excluding anyadjustment relating to the final value ofworking capital acquired.

In July 2008, substantially all of the assetsand liabilities of our non-core lightweightPVC conveyor belting operation held withinFenner Dunlop (Charlotte), Inc wasdisposed of for £5.0m, excluding costs, andresulted in an exceptional profit on disposalof £0.7m.

F e n n e r P L C 1 3

B u s i n e s s R e v i e wG r o u p F i n a n c e D i r e c t o r ’ s R e v i e w c o n t i n u e d

1 4 F e n n e r P L C

CASH FLOW, NET DEBT AND FINANCINGStronger profits generated a £53.9m (2007£42.5m) operating cash flow beforemovements in working capital. Toaccommodate growth in the business andmaintain an effective pipeline of inventoryholding while our order book increased inthe final quarter, an investment in workingcapital of £8.2m (2007 decrease of £10.8m)was made. The resultant net cash fromoperations was £45.7m (2007 £53.3m). Afterpayment of interest of £6.3m (2007 £4.3m)and taxation of £11.2m (2007 £10.2m), thenet cash from operating activities was£28.2m (2007 £38.8m). Capital expenditureincreased to £63.7m (2007 £32.0m) inaccordance with our strategic expansionplans. This compares to a depreciationcharge of £10.1m (2007 £8.0m). Afterfunding these expansion programmes anddisposing of assets of £0.5m (2007 £0.2m)the free cash outflow was £35.0m (2007inflow of £7.0m).

The net outflow on acquisition and disposalactivity was £41.0m (2007 £3.6m).Dividends paid of £9.9m (2007 £9.5m) andan inflow from other financing activities of£35.5m (2007 £0.4m), principally relating tothe share placing outlined below, gave anincrease in net debt before the effects ofexchange rate movements of £50.4m (2007£5.7m). The translation effect of strongerexchange rates increased this amount by£10.9m (2007 decrease of £2.5m) whichresulted in an increase in net debt of £61.3mto £97.6m (2007 £36.3m).

Gross debt at the year end amounted to£141.2m (2007 £102.4m). Cash and cashequivalents at the year end were £43.6m(2007 £66.1m).

The Group is financed principally by a mixof equity, retained earnings, US dollarprivate placement loan notes and committedbank facilities. The principal loan facilitiesare raised centrally whilst operatingcompanies supplement this funding withlocal overdraft and working capital facilities.

To support the Group’s growth, a mix ofadditional sources of funding was securedduring the year.

In November 2007, the committed revolvingcredit bank facility with three leading UKbanks was increased from £75m to £100mon the same terms as previously agreed inJune 2007. In May 2008, an Australian $35m(£16.5m) committed five year bank facility

maturing in May 2013 was secured to assistin the funding of our Australian operations’expansion. This was achieved on covenantterms which were aligned with the UKcommitted facility. At 31 August 2008,£65.2m (2007 £33.5m) of these facilitieswere drawn down leaving £51.3m (2007£41.5m) available.

In March 2008, a placing of 15.7m newordinary shares with institutional investors at233p per share raised £35.4m after costs.

The Group’s other principal source of fundsremained two US dollar private placements;$90m of Senior Notes repayable in June2017 carry a fixed interest coupon of 5.78%;and $27.2m (2007 $34.1m) of Senior Notes,repayable between 2009 and 2012 carry afixed interest coupon of 7.29%.

The committed bank facilities and the 2017private placement have net debt to EBITDAratio and interest cover covenants. At 31August 2008, the Group’s net debt toEBITDA ratio was 1.7 times (2007 0.8 times).The increase reflects the plannedexpenditure in the year and remainscomfortably within the Board’s parameters.For compliance with loan covenants, theEBITDA reported in the financial statementsis adjusted for, inter alia, acquisitions anddisposals, which makes the net debt toEBITDA ratio significantly lower.

The Group is well placed, notwithstandingthe current disruption of financial markets, tofund and support its operations, withcontinuing access to medium and long termdebt finance, cash resources and, wherenecessary, shorter term facilities.

ACCOUNTING POLICIESThe Group financial statements have beenprepared in accordance with the accountingpolicies described in note 1 to the Groupfinancial statements, in accordance withIFRS as adopted by the European Union.

The Company financial statements havebeen prepared in accordance with theaccounting policies described in note 1 tothe Company financial statements, inaccordance with UK GAAP.

FINANCIAL RISK MANAGEMENTIn the normal course of business, the Groupis exposed to certain financial risks,principally foreign exchange risk, interestrate risk, liquidity risk and credit risk. Theserisks are managed by the central treasury

. F e n n e r P L C 1 5

function in conjunction with the operatingunits, in accordance with risk managementpolicies that are designed to minimise thepotential adverse effects of these risks onfinancial performance. The policies arereviewed and approved by the Board.

The exposures are managed through theuse of foreign currency and sterlingborrowings, derivatives and creditmanagement procedures. The use ofderivatives is undertaken only where theunderlying interest or currency risk arisesfrom the Group’s operations or sources offinance. No speculative trading inderivatives is permitted.

In the normal course of business, derivativeshave been used to hedge future non-functional currency cash flows arising fromtrading transactions relating to the sale andpurchase of goods and services. The Grouphas chosen not to hedge account for suchtransactions under the requirements of IAS39 ‘Financial Instruments: Recognition andMeasurement’, recognising that cash flowsthrough to the maturity of the derivative areunaffected. In compliance with IAS 39, allfinancial instruments have been measuredat their fair value as at the balance sheetdate. A charge or credit to the incomestatement has been recognised for the lossor gain on these instruments. In addition, inaccordance with IAS 21 ‘The Effects ofChanges in Foreign Exchange Rates’, allforeign currency monetary items have beenre-translated at the closing rate, withchanges in value charged or credited to theincome statement.

The interest rate swap entered into in 2006to hedge interest rate cash flows continuedduring the year. This instrument fixes theinterest rate on $40m of floating rate bankborrowings until 2011. At 31 August 2008,the fair value of this instrument was a liabilityof £1.5m (2007 £0.7m). In 2007, the Groupalso swapped $27.2m of the 2017 privateplacement into €20.0m, with cash flowsmirroring the private placement at a fixedrate of 5.05%. This swap matures in June2017 when the private placement isrepayable. At 31 August 2008, the fair valueof this instrument was a liability of £0.3m(2007 £nil).

These swaps have been accounted for ashedges in accordance with IAS 39, with thecharge or credit recognised directly inequity.

POST-RETIREMENT BENEFITSThe Group operates a number of definedbenefit post-retirement schemes for qualifyingemployees in operations around the world.

The principal scheme is the Fenner PensionScheme which is based in the UK. The mostrecent funding valuation of the FennerPension Scheme was carried out with aneffective date of 31 March 2008. Whilst thishas yet to be formally completed, theTrustees and the Group have agreed tocontinue funding the Scheme in broadly thesame way going forward. This arrangementreflects the strong covenant provided by theGroup and a commitment to fund theScheme over the long term.

The total defined benefit post-retirementliability as calculated by the schemes'actuaries in accordance with IAS 19'Employee Benefits' and recorded on thebalance sheet increased to £19.1m (2007£14.1m). Of this amount, the Fenner PensionScheme represents £15.5m (2007 £13.1m)and the overseas schemes totalled £3.6m(2007 £1.0m). During the year, the fair valueof assets in the schemes has reduced due tofalling equity markets whilst the present valueof obligations has also reduced as corporatebond yields increased.

KEY FINANCIAL PERFORMANCEINDICATORS

Richard PerryGroup Finance Director

2008 2007

Adjusted earnings per share 17.5p 15.1p

Interest cover (times) 6.8 8.9

Net debt to EBITDA (ratio) 1.7 0.8

Return on gross capital employed 18% 20%

1 6 F e n n e r P L C

B u s i n e s s R e v i e wD e f i n i t i o n o f K e y P e r f o r m a n c e I n d i c a t o r s U s e d

INTERNATIONALLY TRADED COAL PRICESAs published by, and used with thepermission of, the McCloskey GroupLimited, the coal industry recognised marketanalysis and trade reporting company.These bi-weekly prices reflect the deliveredto port price of coal for the two major coalimporting markets.

SALES PER EMPLOYEETotal annual third party revenue at constantexchange rates divided by the averagenumber of employees derived from a simpletotal head count with no distinction betweenfull time, part time, temporary or casualemployees. Where employees are employedfor part of a year, the average number iscalculated on a pro-rata basis.

LOST TIME INCIDENTSThe number of incidents connected withwork which result in an injured person beingaway from work or unable to do the fullrange of their normal duties, not includingthe day of the incident.

ADJUSTED EARNINGS PER SHAREThis is a measure of performance andgrowth. It is calculated by dividing the profitfor the year before amortisation of intangibleassets acquired and exceptional items bythe weighted average number of shares inissue and ranking for dividend.

INTEREST COVERThis measure provides an indication ofwhether the Group’s profit is sufficient tocover its interest obligations. It is calculatedby dividing the operating profit beforeamortisation of intangible assets acquiredand exceptional items by net interestpayable on bank overdrafts and loans, otherloans and bank interest receivable.

NET DEBT TO EBITDAThis is a measure of the Group’s ability toservice its debt obligations. It is calculatedby dividing net debt, defined as short andlong term borrowings less cash and cashequivalents, by the profit for the year afteradding back net finance costs, taxation,depreciation, amortisation and exceptionalitems.

RETURN ON GROSS CAPITAL EMPLOYEDThis is a measure of performance relative toamounts invested. It is calculated bydividing operating profit before amortisationof intangible assets acquired andexceptional items by gross capitalemployed. Gross capital employed isdefined as the average of the opening andclosing non-current assets (excludingdeferred tax), inventories, trade and otherreceivables and trade and other payables.

T h e B o a r d

Appointed in May 1993 as executive Chairmanand became non-executive Chairman in May1994. He is also non-executive Chairman ofAltitude plc and non-executive Chairman ofEnergybuild Group Plc.

Appointed to the Board as Group FinanceDirector in 1990 and became Chief ExecutiveOfficer in May 1994. He is also non-executiveChairman of Inditherm plc.

Appointed to the Board in September 1994.He is also a non-executive director of ScapaGroup plc.

Appointed to the Board in January 2003, hewas formerly an executive director ofD S Smith Plc.

Appointed to the Board in November 2005,he was formerly Chief Executive of BritishVita plc and is a non-executive director ofZotefoams Plc.

Joined the Company in 2001 and wasappointed Company Secretary in July 2002.

COLIN COOKE (68)* r n

Chairman

MARK ABRAHAMS (53) n

Chief Executive Officer

RICHARD PERRY (58)Group Finance Director

DAVID BUTTFIELD (62)* a r n

Senior Independent Director

DAVID CAMPBELL (58)* a r n

DEBRA BRADBURY (43)Company Secretary

* Non-executive a Audit Committeer Remuneration Committeen Nomination Committee

F e n n e r P L C 1 7

1 8 F e n n e r P L C

The Group remains committed to maintaining high standards of corporate governance as set out in the Combined Code onCorporate Governance (“Combined Code”), revised in June 2006.

Compliance with the Combined CodeThe Group has complied with the main provisions of the Combined Code during the year ended 31 August 2008 and this statementexplains how the Principles of Corporate Governance are applied within the Group. It should be read in conjunction with theBusiness Review and the Board Remuneration Report on pages 5 to 16 and pages 27 to 33 respectively.

The BoardAs at 31 August 2008, the Board comprised a non-executive Chairman, two executive directors and two non-executive directorsand is collectively responsible to shareholders for the proper management of the Group. Biographical details of the directors areset out on page 17.

The roles of the Chairman and Chief Executive Officer are separate and distinct from one another.

The Board is satisfied that it has met the Combined Code’s requirements for its effective operation. Specific matters are reserved forthe Board’s consideration under a formal schedule. These include developing Group strategy, reviewing trading performance,considering senior management appointments, formulating policy on key issues (including the approval of significant capitalexpenditure, acquisitions and disposals) and reporting to shareholders. The schedule is reviewed at least annually. Various othermatters are delegated to duly authorised sub-committees of the Board consisting of directors and senior executives. Details of theircomposition and purpose are outlined below. In addition, the Chairman and non-executive directors meet every year without theexecutive directors being present.

All directors are subject to election by shareholders at the first Annual General Meeting ("AGM") following their appointment and tore-election thereafter at intervals of no more than three years. Due to his length of tenure, the Chairman seeks annual re-election inaccordance with best practice.

The Group holds appropriate Director’s and Officer’s liability insurance.

Board balance and independenceThe Board is satisfied that the current balance of skills and experience is appropriate for the requirements of the business. Overhalf of the Board comprises non-executive directors, inclusive of the Chairman, and they are deemed by the Board to beindependent of management and do not have any business relationships which could interfere with the exercise of their judgement.

The Senior Independent Director is David Buttfield.

Information and professional developmentPrior to each Board, Committee or General Meeting, the Board is provided with timely, appropriate and sufficient information toenable it to discharge its duties proficiently.

Non-executive directors receive an induction to the Group and its operations when they are appointed to the Board. They are alsoencouraged to visit the Group’s offices and factories whenever the opportunity presents itself where they meet management andare briefed on local business operations. At least one Board meeting during the year is held at an operational site outside of theUK. In 2008, this took place at the conveyor belting factory in South Africa.

All directors have access to the Company Secretary, who is responsible for ensuring that Board procedures are followed and thatthe Group complies with all applicable rules, regulations and obligations governing its operations. A procedure exists for directorsto take independent professional advice, at the Group’s expense, if necessary, in the furtherance of their duties.

Performance evaluationA Board performance evaluation was carried out in the year which comprised of a questionnaire and individual meetings with theChairman. The review looked at the effectiveness of the Board overall, its structure, composition, Board processes and Committees.The Chairman also evaluated the performance of the individual directors as part of the review. It was concluded that thecomposition, experience and effectiveness of the Board was appropriate and robust.

Audit CommitteeThe Audit Committee comprises the two non-executive directors and is chaired by David Buttfield, who has recent and relevantfinancial experience. The Company Secretary acts as a secretary to the Committee. In undertaking its duties, the Committee hasaccess to the services of the Group Finance Director and the Company Secretary as well as access to external professionaladvice. The Committee has the power to request the attendance at meetings of any director, external auditor or Group employee asconsidered appropriate. The Committee also meets external auditors without the executive directors being present.

Corporate Governance

The principal duties of the Committee are to monitor the integrity of the financial statements, to review the internal controls and riskmanagement systems, to review the work of internal audit and to consider all aspects of the relationship with the external auditors.The Committee has the authority to obtain external legal or other professional advice on any matter within its terms of reference.

The work of the Audit CommitteeDuring the year, the Committee carried out the following work:

- review, prior to Board approval, of the Preliminary and Interim Results, the Annual Report and the Interim Report; - consideration of the Group’s key business risks, including the arrangements for the identification and management of risk;- overseeing the implementation of a Group-wide risk management system;- receive the reports on internal control and review the effectiveness of the internal control function, monitor progress and

evaluate the internal control reports at least twice a year.- meet with the external auditors, both with and without the executive management being present, to discuss audit issues;- approve the external auditors' terms of engagement and associated fees;- monitor the level of non-audit work of the external auditors;- review the terms of reference of the Audit Committee and the Whistleblowing Policy.

No non-routine matters of concern were drawn to the Committee’s attention by either the external or internal auditors through theyear. Matters of material concern would be immediately drawn to the Committee’s attention if and when they arise.

There is a policy on the provision of non-audit services by the external auditors. Certain services such as due diligence in relationto acquisitions and disposals, taxation services and actuarial advice are permitted but others, for example, internal audit,information technology and HR consultancy are generally considered inappropriate. Non-audit fees are reported to the Committee.

The Committee has received and reviewed written confirmation from the external auditors on all relationships that, in theirjudgement, may bear on their independence. The external auditors have also confirmed that they consider themselves independentwithin the meaning of UK regulatory and professional requirements.

Audit Committee and internal controlThe Audit Committee reviews the effectiveness of the Group’s system of internal control and receives a report on internal control atleast twice a year. This review covers all controls, including operational, financial, compliance and risk management.

In accordance with the requirements of the Combined Code and the recommendations of the Turnbull Guidance on internal control,the directors have reviewed the effectiveness of the internal control system. During the period under review, no significant changesto the material risks were identified and no control failings or weaknesses were identified that resulted in unforeseen material losses.

The directors are responsible for the Group’s system of internal control which, like any system of internal control, can only providereasonable and not absolute assurance against material misstatement or loss.

The key procedures within the control structure are: - the identification of major business and insurance risks faced by the Group’s operations, by both the Board and senior

management, and the determination of the most appropriate course of action to deal with these risks; - central review and approval procedures in respect of major areas of risk such as acquisitions and disposals, litigation,

treasury management, taxation and environmental issues; - a clear management structure with well defined lines of responsibility and the appropriate levels of delegation; - regular review of the Group’s business units by operational and executive management; - a structured process for appraising and authorising capital projects. This process includes clearly defined authorisation

levels. Projects are subject to post-investment appraisals; - well established consolidation and reporting systems for both the statutory and monthly management accounts, with all

Board members receiving a monthly statement of the financial results; - comprehensive budgeting systems with an annual budget approved by the Board. Monthly results are reported against

budget and revised forecasts for the year are prepared regularly; - an internal programme of monitoring visits by the internal audit team, as agreed with the Audit Committee, reviews the

compliance of each business unit with the Group's standard internal financial control procedures; - competition compliance programmes are in place in several jurisdictions and the Group-wide Whistleblowing Policy

continues to be applied; and - a programme of business risk reviews with operational management focusing on non-financial controls and risk

management.

F e n n e r P L C 1 9

Corporate Governance continued

2 0 F e n n e r P L C

Remuneration CommitteeThe Remuneration Committee comprises the Chairman and the non-executive directors and is chaired by David Campbell. TheChief Executive Officer also attends the meetings by invitation but does not participate in any decision in relation to his ownremuneration. The Committee has the power to request the attendance at meetings of any director or Group employee asconsidered appropriate.

The Committee is responsible to the Board for determining the remuneration packages of the executive directors and other seniorexecutives and advises on executive remuneration policy issues. The Committee administers the long term Performance Share Plan(“PSP”) and the outgoing Long Term Share Incentive Plan (“LTIP”). It also approves the granting to employees of a long termShadow Performance Share Plan which is a cash incentive scheme with performance criteria which are the same as the PSP.The Remuneration Committee received advice during the year from Hewitt New Bridge Street Consultants LLP (“HNBSC”), whoadvised the Committee in relation to director and senior executive remuneration and the PSP. MM&K Ltd assisted the Committee inconsideration of matters in relation to the outgoing LTIP.

Nomination CommitteeThe Nomination Committee comprises the Chairman, the non-executive directors and the Chief Executive Officer. The Committee ischaired by the Chairman and meets at least annually. The Committee has the power to request the attendance at meetings of anydirector or Group employee as considered appropriate.

Terms of reference set out the Committee’s role and duties which include reviewing the composition of the Board, havingresponsibility for the identification and nomination of candidates to fill Board vacancies and considering succession planning for allBoard positions and senior executives.

Candidates for appointment to the Board are considered by the Committee, taking advice from external consultants whereappropriate.

Meetings of the BoardThe attendance of each director at Board, Audit, Remuneration and Nomination Committee meetings is set out below.

Terms of referenceThe terms of reference of the Audit, Remuneration and Nomination Committees are reviewed at least annually and are available toview on the Group’s website at www.fenner.com or upon request to the Company Secretary.

Executive CommitteeThe Executive Committee is chaired by the Chief Executive Officer and consists of the two executive directors, the CompanySecretary and five members of the Group’s senior management. The Executive Committee meets at least six times a year and dealswith the daily management of the Group through powers delegated to it by the Board.

Directors' remunerationPolicy and procedure are set out in the Board Remuneration Report on pages 27 to 33.

Number of meetings during the year

Chairman C I Cooke

Executive directorsM S Abrahams

R J Perry

Non-executive directorsD F Buttfield

D A Campbell

* By invitation

6

6

6

6

6

6

Board

3

3*

3*

3*

3

3

Audit Committee

RemunerationCommittee

3

3

2*

0

3

3

1

1

1

1*

1

1

NominationCommittee

Relations with shareholdersThe Company encourages regular dialogue with its institutional shareholders and also with private investors at the AGM. The ChiefExecutive Officer and Group Finance Director hold update meetings with institutional shareholders following the announcement ofPreliminary and Interim Results and as requested throughout the year. Similar meetings are held with private client brokers so thatthe same information can be disseminated to private investors. The Chairman and non-executive directors are offered theopportunity to attend meetings with major shareholders and attend if requested.

The Board is provided with broker reports and feedback from shareholder meetings on a regular basis.

The Group’s website provides comprehensive investor relations information for shareholders to view. The website includes analystpresentations, the current share price, regulatory announcements, financial performance information, shareholder information andan investor relations contact address.

Annual General MeetingIn relation to the Company’s AGM:

- proxy forms allow for voting either for a resolution, against a resolution or for a vote to be withheld;- a separate resolution is proposed for each substantially separate issue, including the receipt of the Annual Report;- the proxy count in respect of each resolution is announced after it has been dealt with on a show of hands;- all executive and non-executive Board members normally attend the meeting;- the Notice of Meeting, the Annual Report and any other related papers are normally sent to shareholders more than one

month before the meeting; and- shareholders are invited to ask questions during the AGM and have an opportunity to meet the Board directors before and

after the formal meeting.

Statement of directors’ responsibilities in respect of the Annual Report, the Board Remuneration Report and thefinancial statements The directors are responsible for preparing the Annual Report, the Board Remuneration Report and the Group and Companyfinancial statements in accordance with applicable law and regulations.

Company law requires the directors to prepare financial statements for each financial year. Under that law, the directors haveprepared the Group financial statements in accordance with International Financial Reporting Standards (“IFRS”) as adopted by theEuropean Union and the Company financial statements and the Board Remuneration Report in accordance with applicable law andUnited Kingdom Accounting Standards (United Kingdom Generally Accepted Accounting Practice). The Company and Groupfinancial statements are required by law to give a true and fair view of the state of affairs of the Company and the Group and of theprofit or loss of the Group for that period.

In preparing those financial statements, the directors are required to:- select suitable accounting policies and then apply them consistently;- make judgements and estimates that are reasonable and prudent ;- state that the Group financial statements comply with IFRS as adopted by the European Union and with regard to the

Company financial statements that applicable UK Accounting Standards have been followed, subject to any materialdepartures disclosed and explained in the financial statements; and

- prepare the Group and Company financial statements on the going concern basis unless it is inappropriate to presume thatthe Group will continue in business, in which case there should be supporting assumptions or qualifications as necessary.

The directors confirm that they have complied with the above requirements in preparing the financial statements.

The directors are also required by the Disclosure and Transparency Rules of the Financial Services Authority to include amanagement report containing a fair review of the business and a description of the principal risks and uncertainties facing theGroup and Company.

The directors are responsible for keeping proper accounting records that disclose with reasonable accuracy at any time thefinancial position of the Company and the Group and to enable them to ensure that the Group financial statements comply with theCompanies Act 1985 and Article 4 of the IAS Regulation and the Company financial statements and the Board RemunerationReport comply with the Companies Act 1985. They are also responsible for safeguarding the assets of the Company and the Groupand hence for taking reasonable steps for the prevention and detection of fraud and other irregularities.

The directors are responsible for the maintenance and integrity of the Company’s website. Legislation in the United Kingdomgoverning the preparation and dissemination of financial statements may differ from legislation in other jurisdictions.

F e n n e r P L C 2 1

Directors’ statement pursuant to the Disclosure and Transparency RulesEach of the directors, whose names and functions are listed in The Board on page 17 confirm that, to the best of each person’sknowledge and belief:

- the Group financial statements, prepared in accordance with IFRS as adopted by the European Union, and the Companyfinancial statements, prepared in accordance with applicable law and United Kingdom Generally Accepted AccountingPractice, give a true and fair view of the assets, liabilities and financial position of the Group and Company and of the profitof the Group; and

- the Business Review on pages 5 to 16 includes a fair review of the development and performance of the business and theposition of the Company and Group, together with a description of the principal risks and uncertainties that they face.

Going concernAfter making enquiries, the directors have formed a judgment at the time of approving the financial statements that there is areasonable expectation that the Company and Group have adequate resources to continue in operational existence for theforeseeable future. For this reason, the directors continue to adopt the going concern basis in preparing the financial statements.

C I Cooke Chairman12 November 2008

2 2 F e n n e r P L C

Corporate Governance continued

F e n n e r P L C 2 3

Fenner is aware of and takes seriously its responsibilities towards customers, employees, suppliers and the local communities inwhich it works. The Group has identified that health and safety, its people, how it does business, reducing environmental impactand involvement within the community are all important to contributing to its overall business performance. As such, these issuesare embedded into the business decision making process and the Group believes that this proactive attitude and approachenhances its reputation, profitability and shareholder return.

The risks associated with the non-financial aspects of the Group’s business are managed within the Group’s risk managementframework and are continuously monitored and assessed, with necessary controls put in place in order to reduce the potentialimpact.

The Chief Executive Officer has overall responsibility for the development and monitoring of the Group’s policies relating toCorporate Responsibility. The task of ensuring these policies are communicated and applied at a divisional and operational unitlevel is delegated through the divisional managing directors to each unit’s senior management. The policies and associatedmanagement systems are reviewed at least annually and at any time when significant changes in the business, legislation orindustry standard demand.

The Group’s Health & Safety Policy and Environmental Policy are available to view on the Company’s website at www.fenner.com orby contacting the Company Secretary.

The Company is proud to continue to be a member of the FTSE4Good UK Index which measures the performance of companiesthat meet globally recognised Corporate Responsibility standards and facilitates investment into those companies.