Gorenje Groupstatic14.gorenje.com/files/default/corporate/investor...disposal of furniture...

37

Gorenje Group Investor Conference Zagreb, 26 May 2015

Transcript of Gorenje Groupstatic14.gorenje.com/files/default/corporate/investor...disposal of furniture...

Gorenje Group Investor Conference

Zagreb, 26 May 2015

OWN

PRODUCTION

Slovenia

Serbia

Czech Republic

CONSOLIDATED

REVENUE

EUR 1.25 bn

NUMBER OF

EMPLOYEES

10,468

EXPORT

95%

of sales

GLOBAL

PRESENCE

90 Countries

Worldwide,

mostly in Europe (92%),

also in USA, Australia,

Near and Far East

CORE BUSINESS

Products and

services for home

(MDA, SDA, HVAC,

kitchen furniture)

One of Leading European

Manufacturers of Products for Home

2

Gorenje

Group

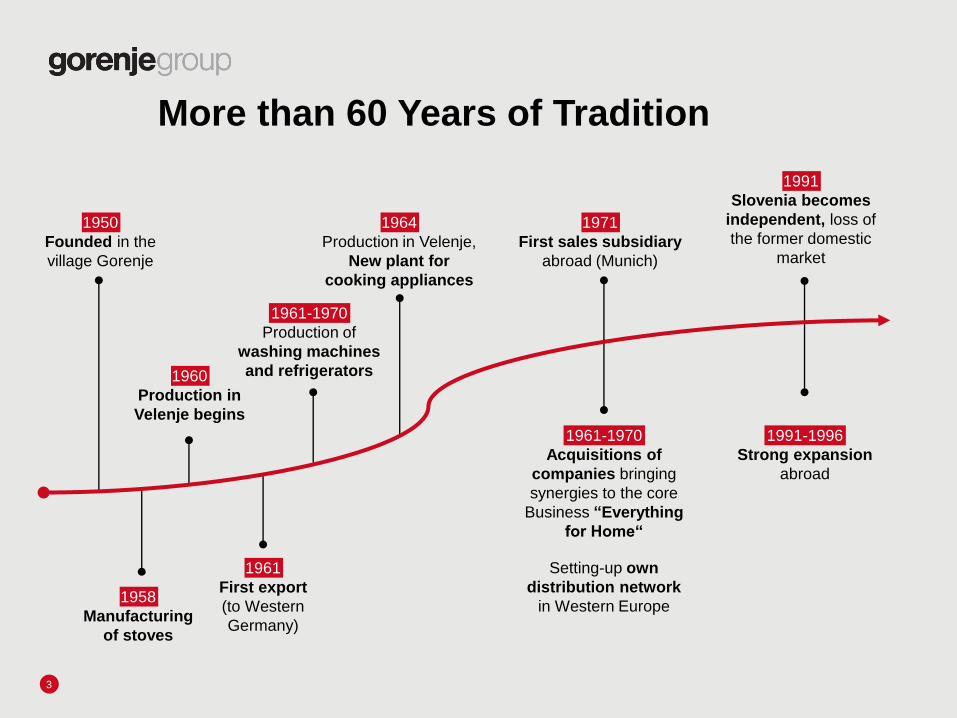

1950

Founded in the

village Gorenje

More than 60 Years of Tradition

3

1960

Production in

Velenje begins

1961-1970

Production of

washing machines

and refrigerators

1964

Production in Velenje,

New plant for

cooking appliances

1971

First sales subsidiary

abroad (Munich)

1991

Slovenia becomes

independent, loss of

the former domestic

market

1958

Manufacturing

of stoves

1961

First export

(to Western

Germany)

1961-1970

Acquisitions of

companies bringing

synergies to the core

Business “Everything

for Home“

Setting-up own

distribution network

in Western Europe

1991-1996

Strong expansion

abroad

1998

Gorenje, d.d.,

becomes a

public company, listing

on the

Ljubljana Stock

Exchange

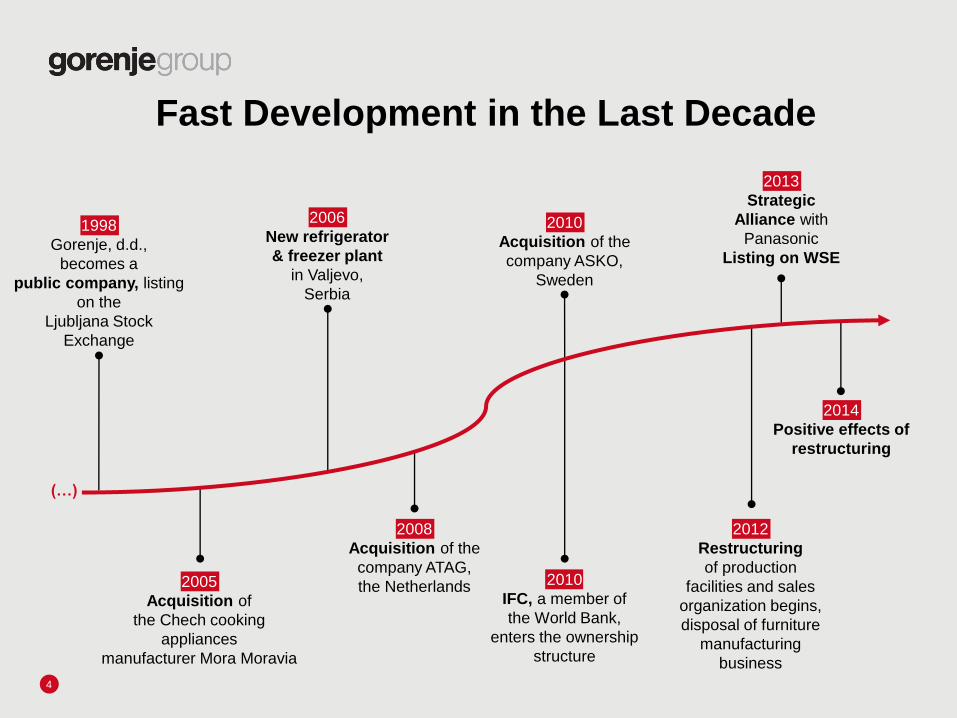

Fast Development in the Last Decade

4

2006

New refrigerator

& freezer plant

in Valjevo,

Serbia

2010

Acquisition of the

company ASKO,

Sweden

2013

Strategic

Alliance with

Panasonic

Listing on WSE

2005

Acquisition of

the Chech cooking

appliances

manufacturer Mora Moravia

2010

IFC, a member of

the World Bank,

enters the ownership

structure

(…)

2008

Acquisition of the

company ATAG,

the Netherlands

2014

Positive effects of

restructuring

2012

Restructuring

of production

facilities and sales

organization begins,

disposal of furniture

manufacturing

business

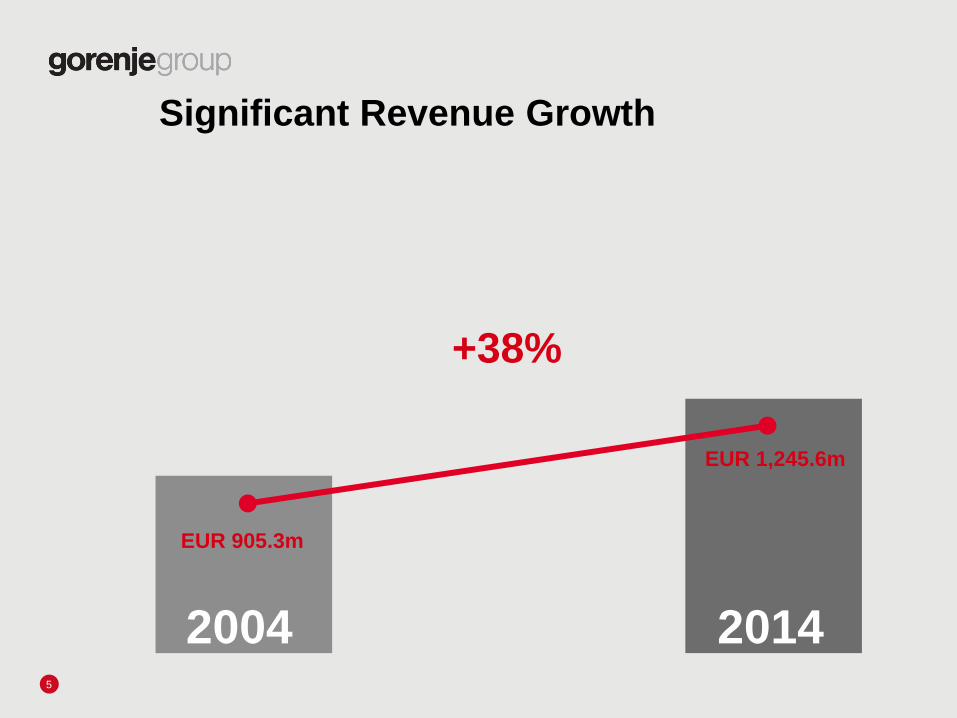

Significant Revenue Growth

5

+38%

EUR 905.3m

EUR 1,245.6m

2004 2014

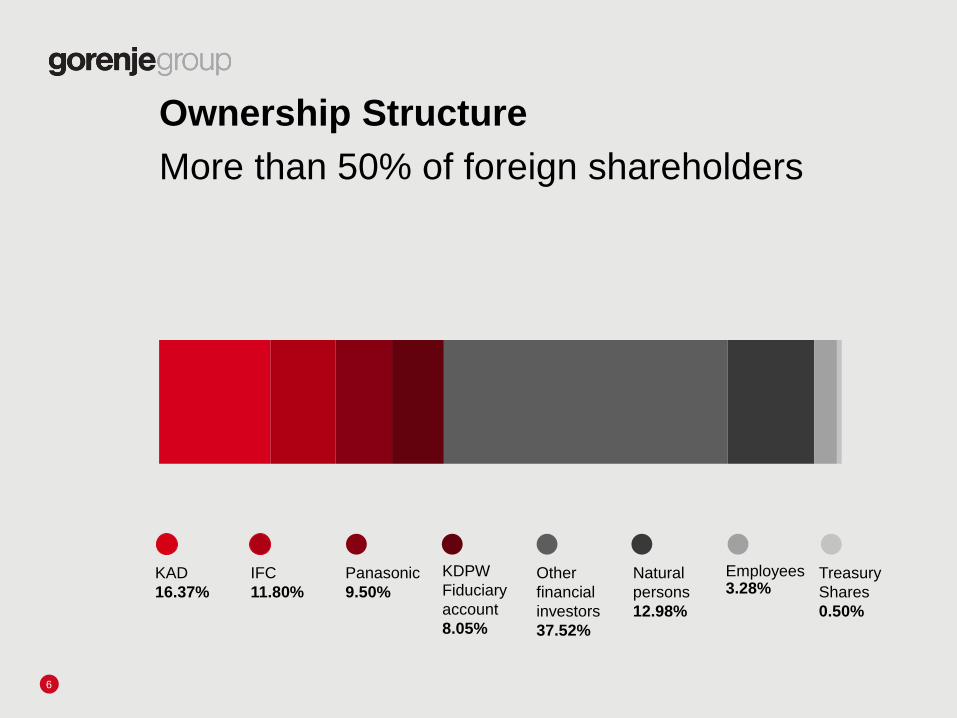

Ownership Structure

More than 50% of foreign shareholders

6

KAD

16.37%

IFC

11.80%

Panasonic

9.50%

KDPW

Fiduciary

account

8.05%

Other

financial

investors

37.52%

Natural

persons

12.98%

Employees 3.28%

Treasury

Shares

0.50%

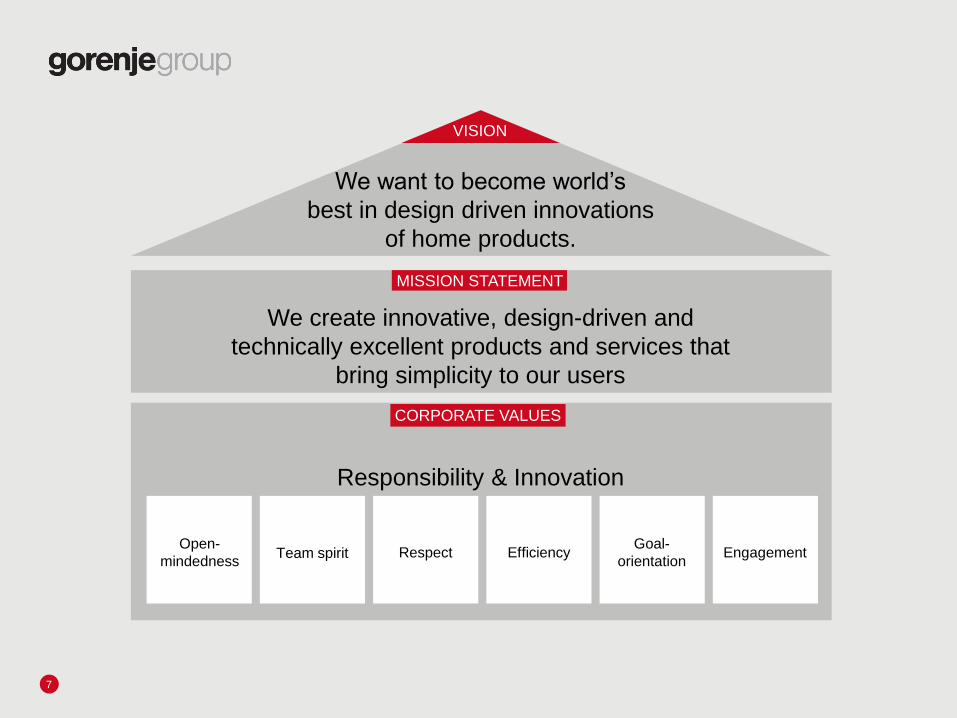

CORPORATE VALUES

MISSION STATEMENT

7

VISION

We want to become world’s

best in design driven innovations

of home products.

We create innovative, design-driven and

technically excellent products and services that

bring simplicity to our users

Responsibility & Innovation

Open-

mindedness Team spirit Respect Efficiency

Goal-

orientation Engagement

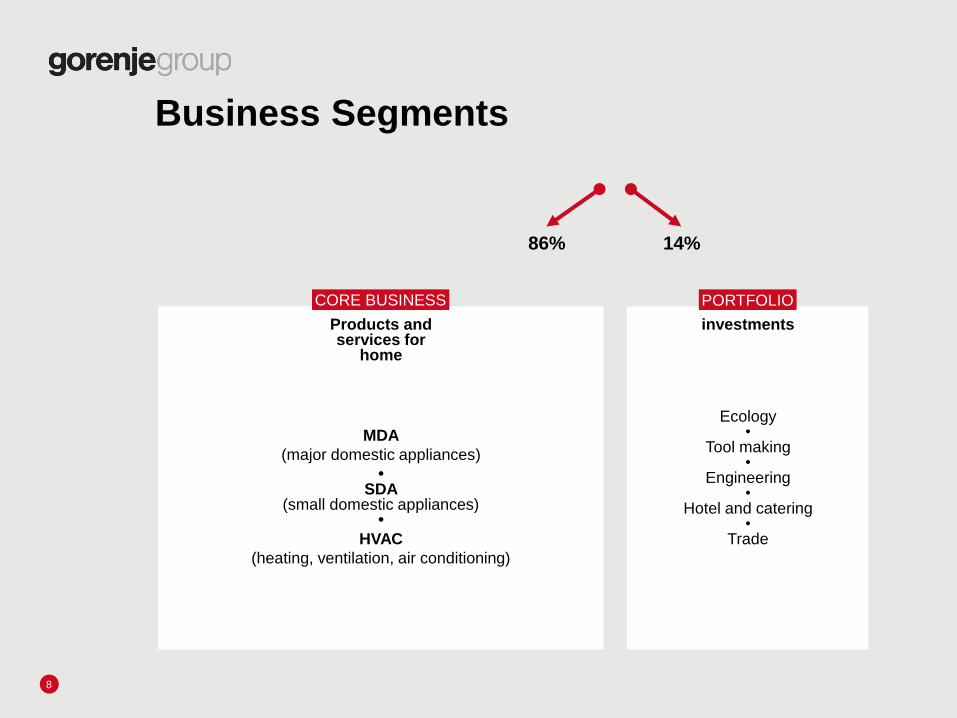

CORE BUSINESS

Business Segments

8

Products and services for

home

MDA

(major domestic appliances)

• SDA

(small domestic appliances) •

HVAC

(heating, ventilation, air conditioning)

investments

Ecology •

Tool making •

Engineering •

Hotel and catering •

Trade

86% 14%

PORTFOLIO

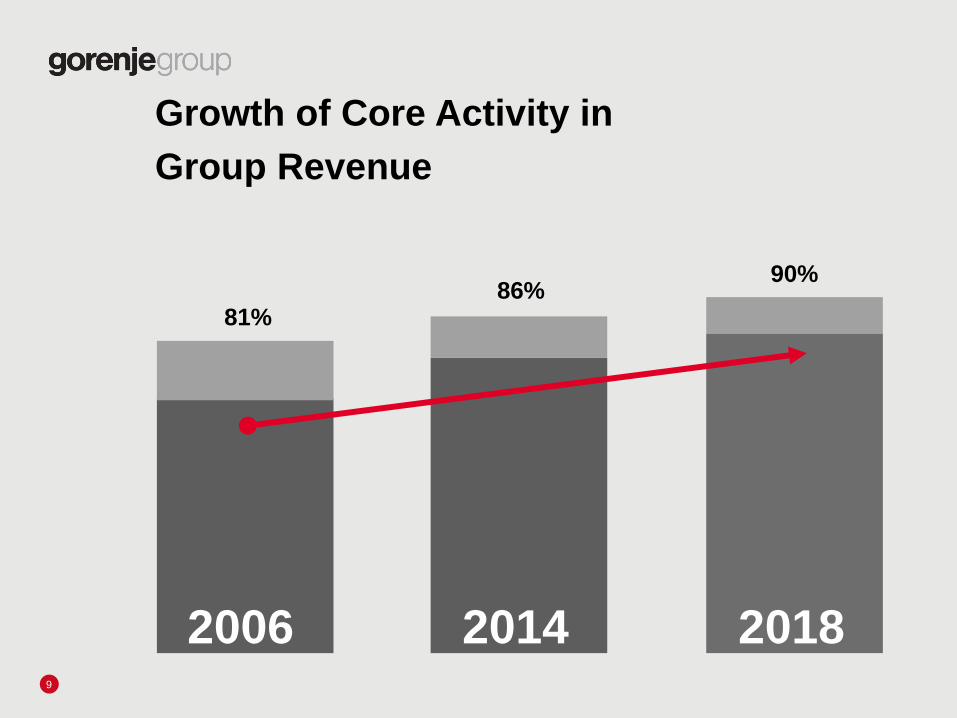

Growth of Core Activity in

Group Revenue

9

2006 2018 2014

81% 86%

90%

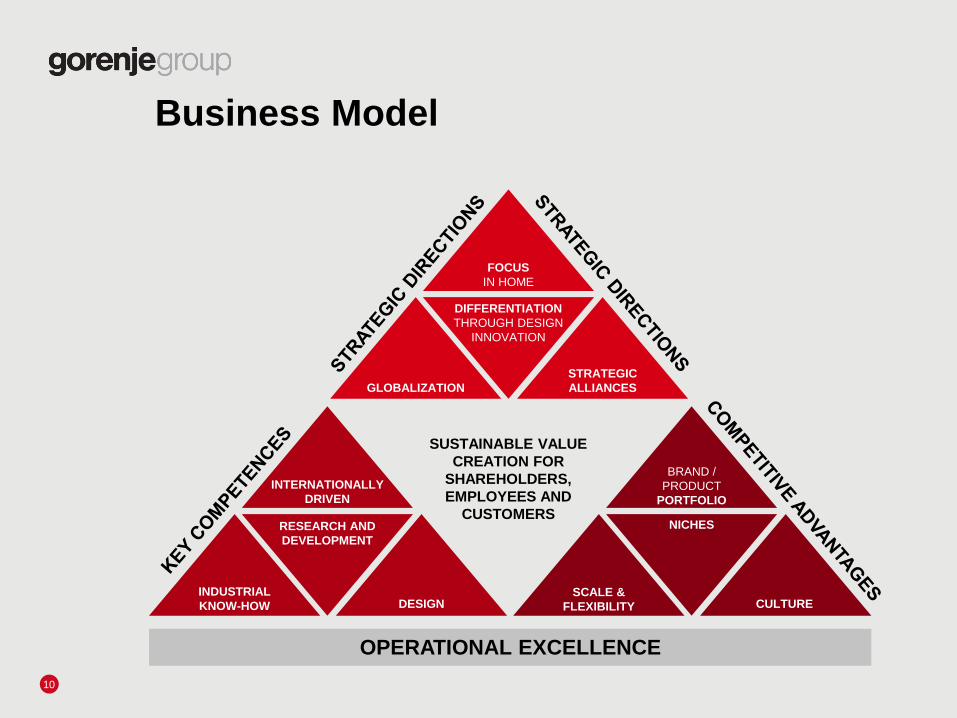

Business Model

10

FOCUS

IN HOME

DIFFERENTIATION

THROUGH DESIGN

INNOVATION

GLOBALIZATION

STRATEGIC

ALLIANCES

SUSTAINABLE VALUE

CREATION FOR

SHAREHOLDERS,

EMPLOYEES AND

CUSTOMERS

BRAND /

PRODUCT

PORTFOLIO

SCALE &

FLEXIBILITY CULTURE DESIGN INDUSTRIAL

KNOW-HOW

INTERNATIONALLY

DRIVEN

RESEARCH AND

DEVELOPMENT

NICHES

OPERATIONAL EXCELLENCE

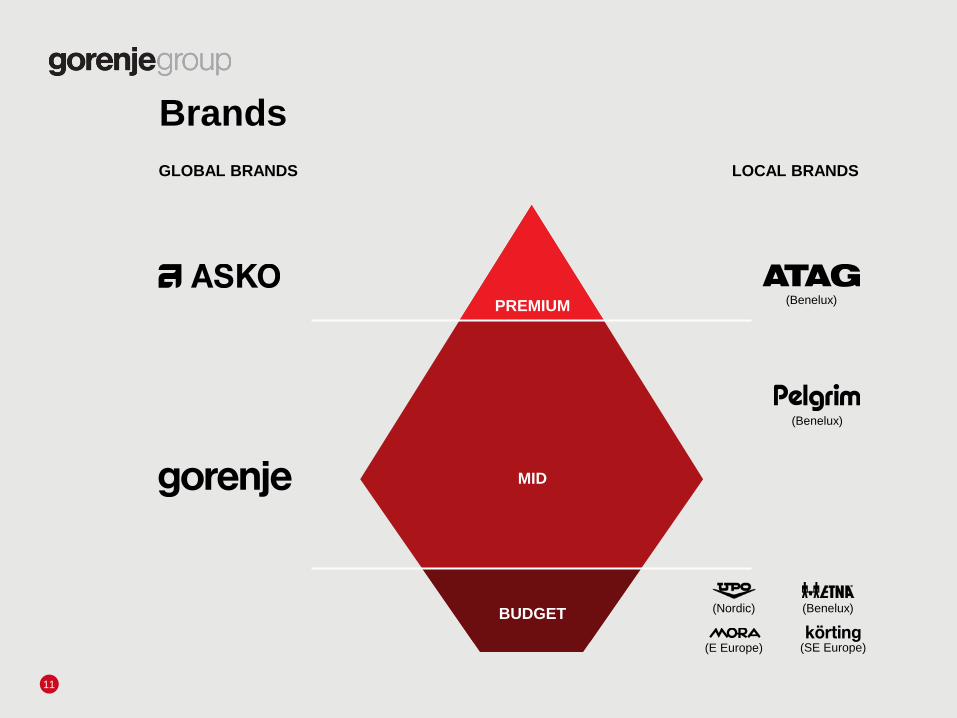

Brands

11

GLOBAL BRANDS LOCAL BRANDS

(Benelux) PREMIUM

MID

BUDGET

(Benelux)

(Nordic) (Benelux)

(E Europe) (SE Europe)

Global brand

(mid and high-mid price segment, design

lines) MDA and SDA brand

70 % of MDA revenue

Majority of revenue: Germany, Russia, SEE, Scandinavia

Global premium brand

Sales: EUR 100 m

Main markets: USA, Australia, Scandinavia,

Russia, Asia (selected markets)

Short-term: extend product portfolio and

strengthen position on key markets

Mid-term: expand to new markets

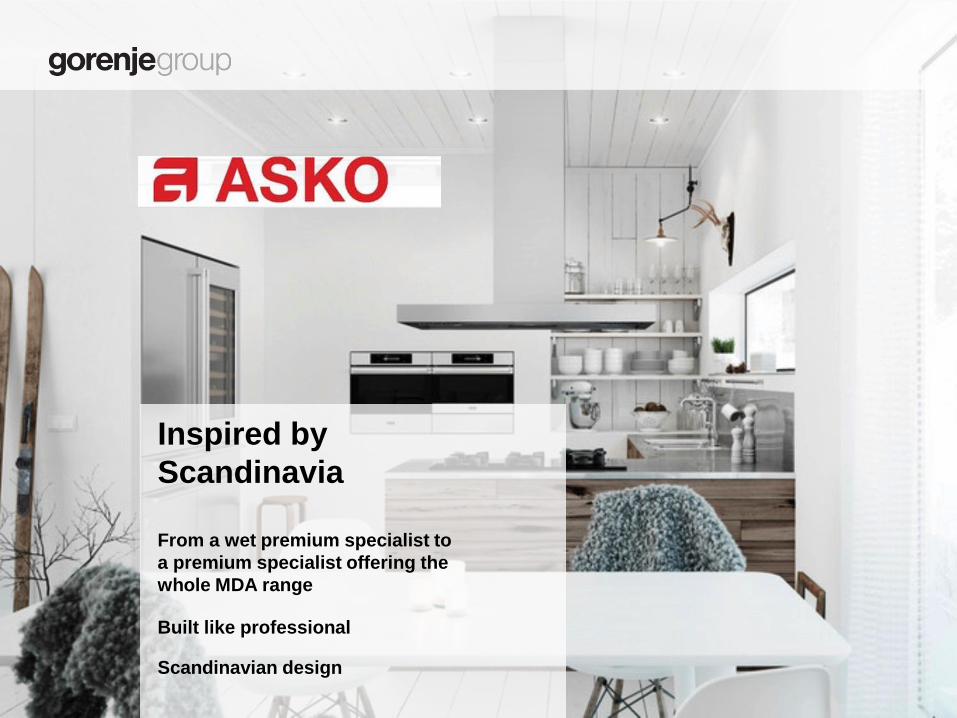

Inspired by

Scandinavia

From a wet premium specialist to

a premium specialist offering the

whole MDA range

Built like professional Scandinavian design

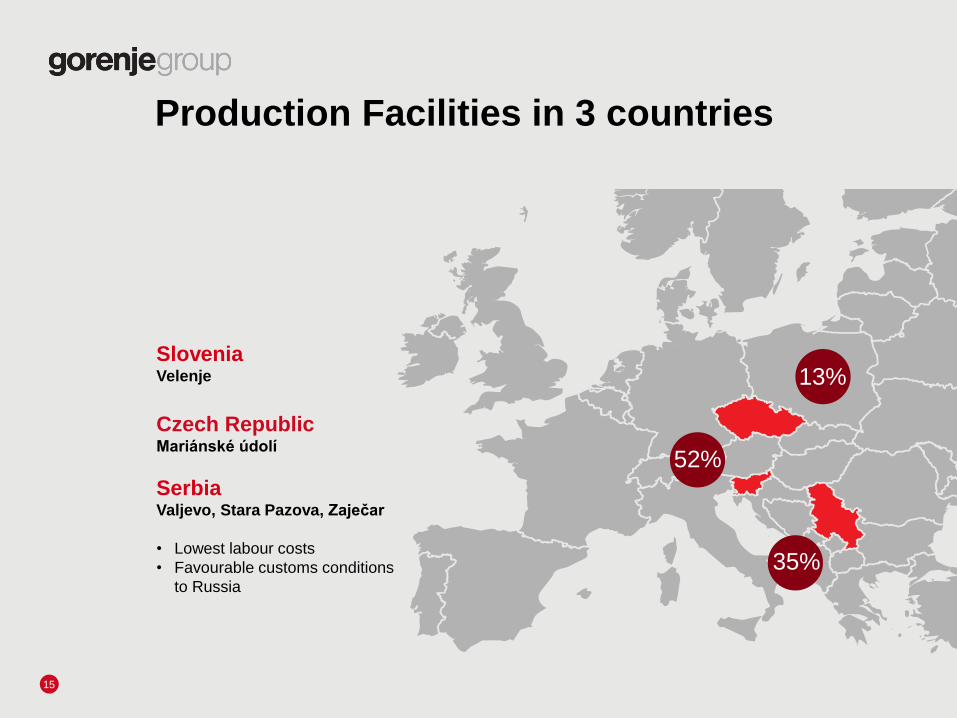

Production Facilities in 3 countries

15

Slovenia Velenje

Czech Republic Mariánské údolí

Serbia Valjevo, Stara Pazova, Zaječar

• Lowest labour costs

• Favourable customs conditions

to Russia

13%

35%

52%

Most Important Markets:

Germany, Russia and the Netherlands

16

RUSSIA GERMANY THE NETHERLANDS SERBIA SLOVENIA CZECH REPUBLIC CROATIA DENMARK AUSTRALIJA USA

UKRAINE

BIH

AUSTRIA

POLAND

BELGIUM

HUNGARY

FINLAND

NORWAY

RUMANIA

SLOVAKIA

SWEDEN

BULGARIA

GREAT BRITAIN

FRANCE

MONTENEGRO

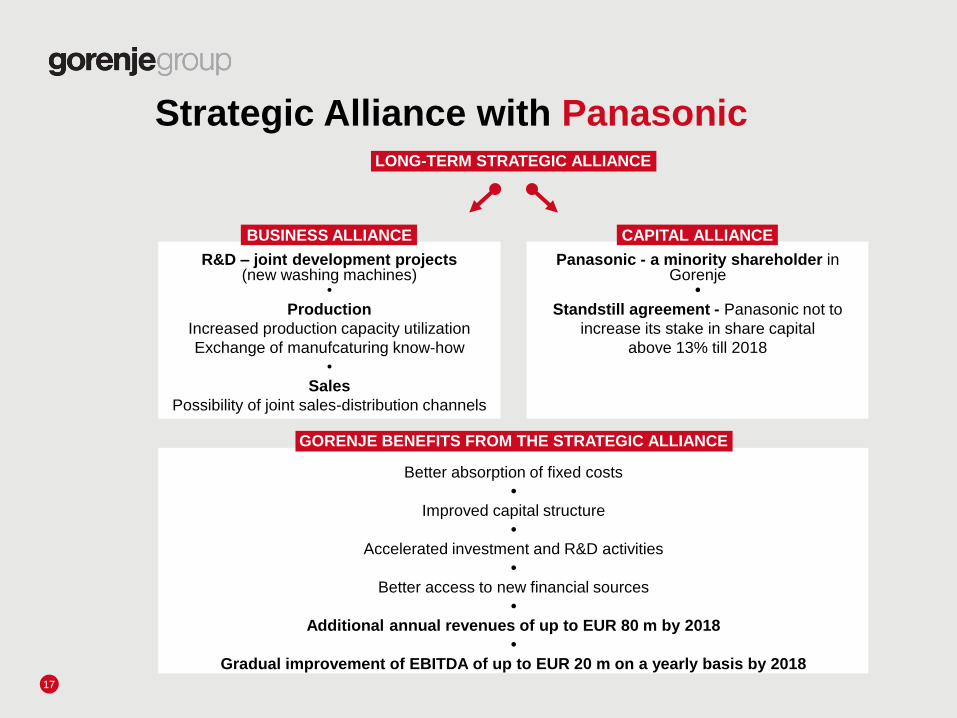

Strategic Alliance with Panasonic

17

R&D – joint development projects (new washing machines)

•

Production

Increased production capacity utilization

Exchange of manufcaturing know-how

•

Sales

Possibility of joint sales-distribution channels

CAPITAL ALLIANCE

LONG-TERM STRATEGIC ALLIANCE

BUSINESS ALLIANCE

Panasonic - a minority shareholder in Gorenje

•

Standstill agreement - Panasonic not to

increase its stake in share capital

above 13% till 2018

Better absorption of fixed costs

•

Improved capital structure

•

Accelerated investment and R&D activities

•

Better access to new financial sources

•

Additional annual revenues of up to EUR 80 m by 2018

•

Gradual improvement of EBITDA of up to EUR 20 m on a yearly basis by 2018

GORENJE BENEFITS FROM THE STRATEGIC ALLIANCE

GRADUALLY

IMPROVE

EBIT

MARGIN

Strategic Goals 2014 - 2018

18

NET DEBT/

EBITDA

not more than 3.0

from 2015 onwards

To be the

WORLD’S

LEADING

design-driven

innovator and

manufacturer of

home

appliances FOCUS

ON CORE

ACTIVITY

– Segment Home –

revenues more than

90%of all Group

revenue by

2018

INCREASE

THE SHARE

OF PREMIUM

BRANDS

SALES

to more

than 25%

GRADUAL

DIVESTMENT

of Portfolio

Companies

INCREASE

SALES

OUTSIDE

EUROPE

to close to

EUR 180 m

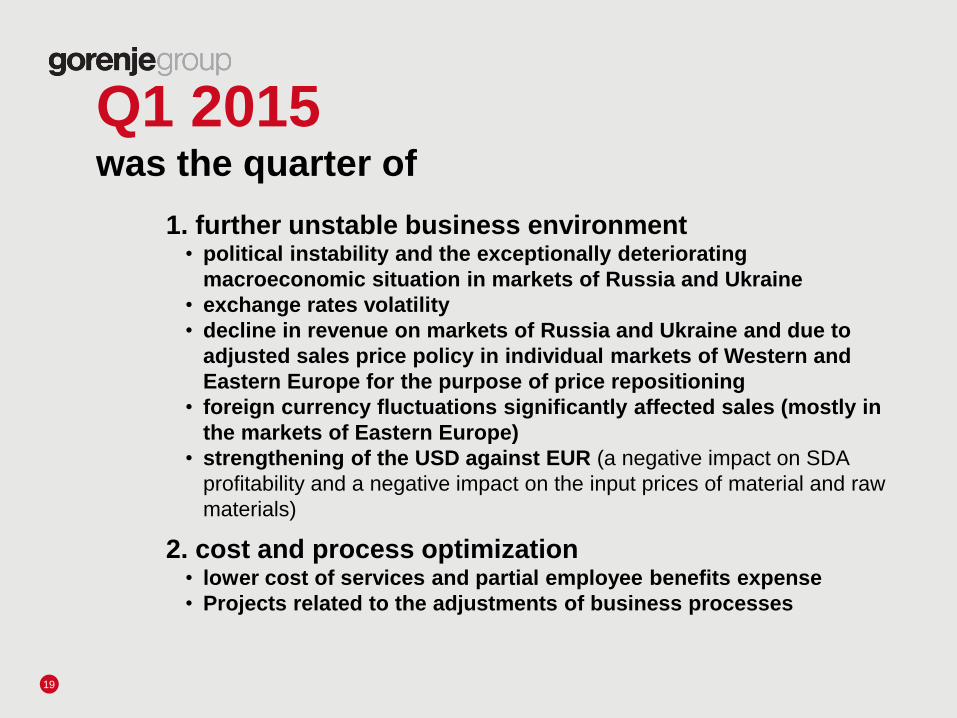

Q1 2015 was the quarter of

19

1. further unstable business environment • political instability and the exceptionally deteriorating

macroeconomic situation in markets of Russia and Ukraine

• exchange rates volatility

• decline in revenue on markets of Russia and Ukraine and due to

adjusted sales price policy in individual markets of Western and

Eastern Europe for the purpose of price repositioning

• foreign currency fluctuations significantly affected sales (mostly in

the markets of Eastern Europe)

• strengthening of the USD against EUR (a negative impact on SDA

profitability and a negative impact on the input prices of material and raw

materials)

2. cost and process optimization • lower cost of services and partial employee benefits expense

• Projects related to the adjustments of business processes

Q1 2015 was the quarter of

20

3. higher but seasonally dependent indebtedness • working capital management (higher inventories of finished

products and merchandise due to the sudden recall of orders by

customers in Russia, Ukraine and the markets of Caucasus)

• planned growth of indebtedness

• improved maturity profile

4. development of strategic partnership with

Panasonic Corporation

5. development of new markets and business

partnerships • cooperation with the company SubZero in the US

• development of the Asko brand

• development of innovative appliances for own brands

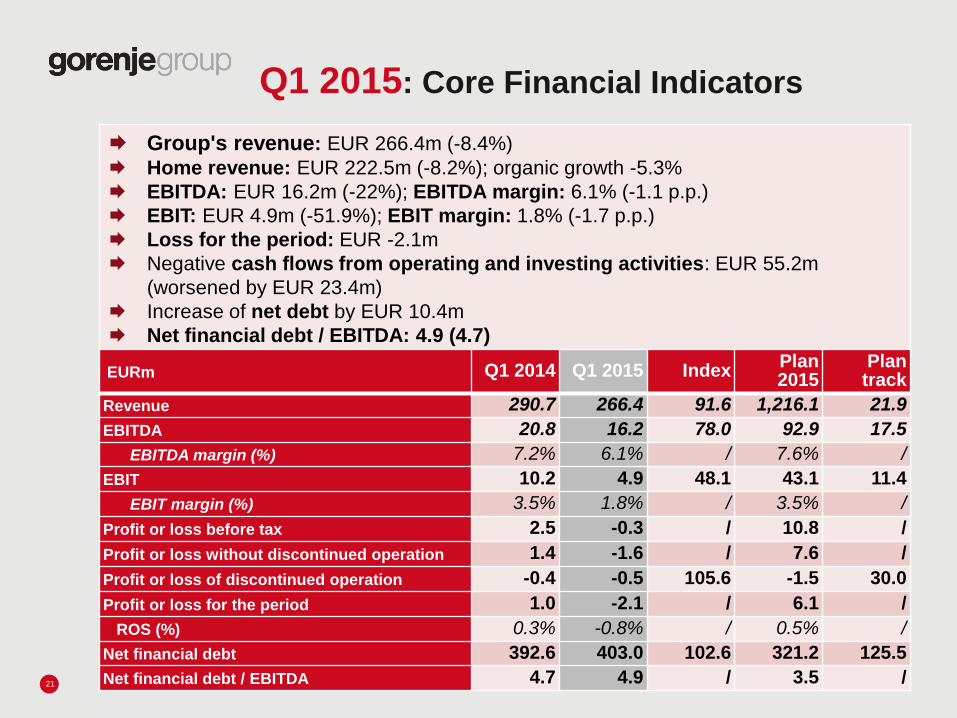

Q1 2015: Core Financial Indicators

21

Group's revenue: EUR 266.4m (-8.4%)

Home revenue: EUR 222.5m (-8.2%); organic growth -5.3%

EBITDA: EUR 16.2m (-22%); EBITDA margin: 6.1% (-1.1 p.p.)

EBIT: EUR 4.9m (-51.9%); EBIT margin: 1.8% (-1.7 p.p.)

Loss for the period: EUR -2.1m

Negative cash flows from operating and investing activities: EUR 55.2m

(worsened by EUR 23.4m)

Increase of net debt by EUR 10.4m

Net financial debt / EBITDA: 4.9 (4.7)

EURm Q1 2014 Q1 2015 Index Plan 2015

Plan track

Revenue 290.7 266.4 91.6 1,216.1 21.9

EBITDA 20.8 16.2 78.0 92.9 17.5

EBITDA margin (%) 7.2% 6.1% / 7.6% /

EBIT 10.2 4.9 48.1 43.1 11.4

EBIT margin (%) 3.5% 1.8% / 3.5% /

Profit or loss before tax 2.5 -0.3 / 10.8 /

Profit or loss without discontinued operation 1.4 -1.6 / 7.6 /

Profit or loss of discontinued operation -0.4 -0.5 105.6 -1.5 30.0

Profit or loss for the period 1.0 -2.1 / 6.1 /

ROS (%) 0.3% -0.8% / 0.5% /

Net financial debt 392.6 403.0 102.6 321.2 125.5

Net financial debt / EBITDA 4.7 4.9 / 3.5 /

290.7 266.4

310.0 308.5 336.4

0.0

100.0

200.0

300.0

400.0

Q1 2014 Q1 2015 Q2 2014 Q3 2014 Q4 2014

mio

EU

R

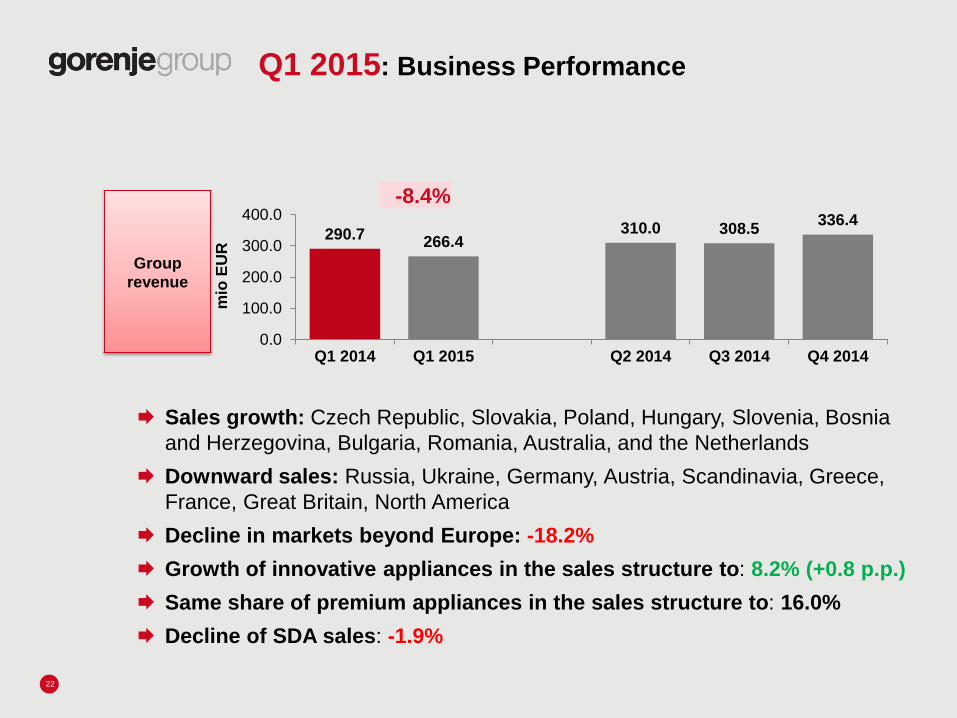

Q1 2015: Business Performance

Group

revenue

22

-8.4%

Sales growth: Czech Republic, Slovakia, Poland, Hungary, Slovenia, Bosnia

and Herzegovina, Bulgaria, Romania, Australia, and the Netherlands

Downward sales: Russia, Ukraine, Germany, Austria, Scandinavia, Greece,

France, Great Britain, North America

Decline in markets beyond Europe: -18.2%

Growth of innovative appliances in the sales structure to: 8.2% (+0.8 p.p.)

Same share of premium appliances in the sales structure to: 16.0%

Decline of SDA sales: -1.9%

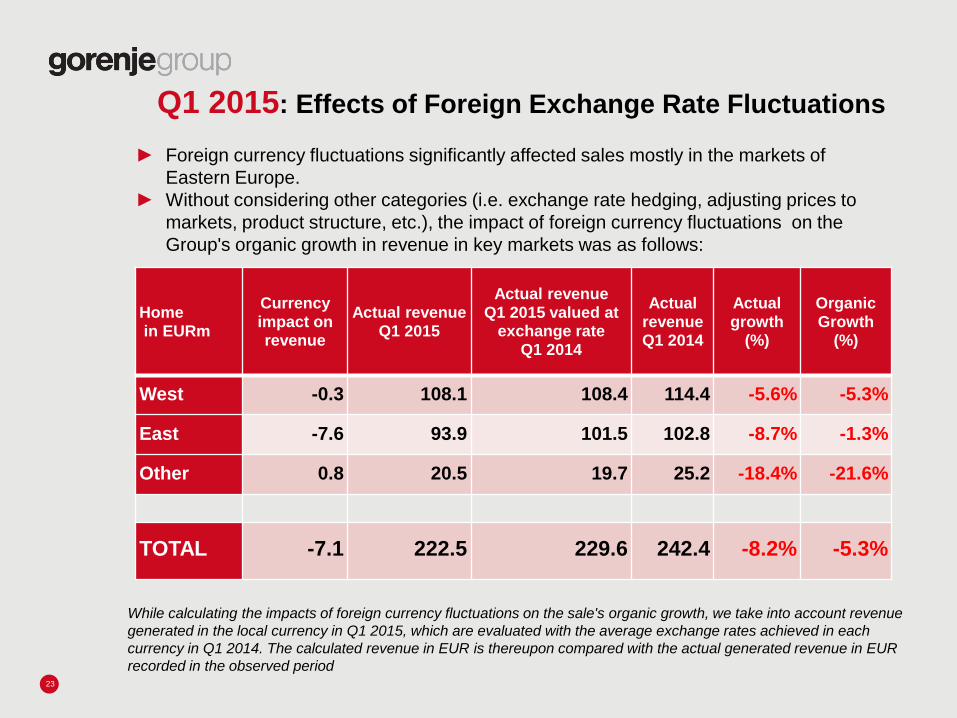

Q1 2015: Effects of Foreign Exchange Rate Fluctuations

23

Home in EURm

Currency

impact on revenue

Actual revenue Q1 2015

Actual revenue Q1 2015 valued at

exchange rate Q1 2014

Actual

revenue Q1 2014

Actual

growth (%)

Organic

Growth (%)

West -0.3 108.1 108.4 114.4 -5.6% -5.3%

East -7.6 93.9 101.5 102.8 -8.7% -1.3%

Other 0.8 20.5 19.7 25.2 -18.4% -21.6%

TOTAL -7.1 222.5 229.6 242.4 -8.2% -5.3%

► Foreign currency fluctuations significantly affected sales mostly in the markets of

Eastern Europe.

► Without considering other categories (i.e. exchange rate hedging, adjusting prices to

markets, product structure, etc.), the impact of foreign currency fluctuations on the

Group's organic growth in revenue in key markets was as follows:

While calculating the impacts of foreign currency fluctuations on the sale's organic growth, we take into account revenue

generated in the local currency in Q1 2015, which are evaluated with the average exchange rates achieved in each

currency in Q1 2014. The calculated revenue in EUR is thereupon compared with the actual generated revenue in EUR

recorded in the observed period

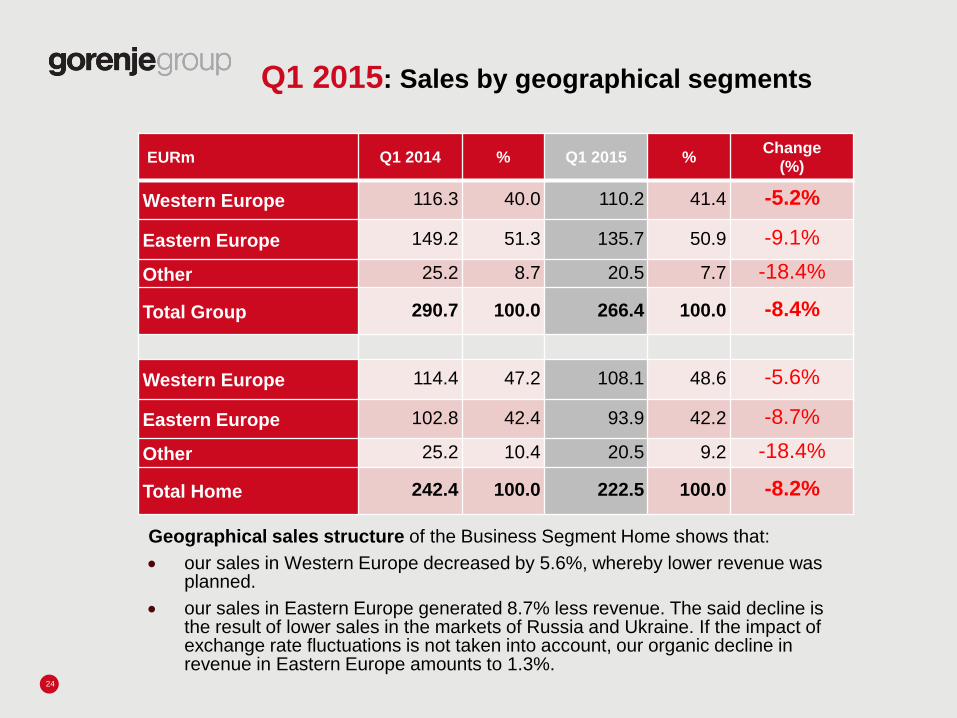

Q1 2015: Sales by geographical segments

24

EURm Q1 2014 % Q1 2015 % Change

(%)

Western Europe 116.3 40.0 110.2 41.4 -5.2%

Eastern Europe 149.2 51.3 135.7 50.9 -9.1%

Other 25.2 8.7 20.5 7.7 -18.4%

Total Group 290.7 100.0 266.4 100.0 -8.4%

Western Europe 114.4 47.2 108.1 48.6 -5.6%

Eastern Europe 102.8 42.4 93.9 42.2 -8.7%

Other 25.2 10.4 20.5 9.2 -18.4%

Total Home 242.4 100.0 222.5 100.0 -8.2%

Geographical sales structure of the Business Segment Home shows that:

our sales in Western Europe decreased by 5.6%, whereby lower revenue was planned.

our sales in Eastern Europe generated 8.7% less revenue. The said decline is the result of lower sales in the markets of Russia and Ukraine. If the impact of exchange rate fluctuations is not taken into account, our organic decline in revenue in Eastern Europe amounts to 1.3%.

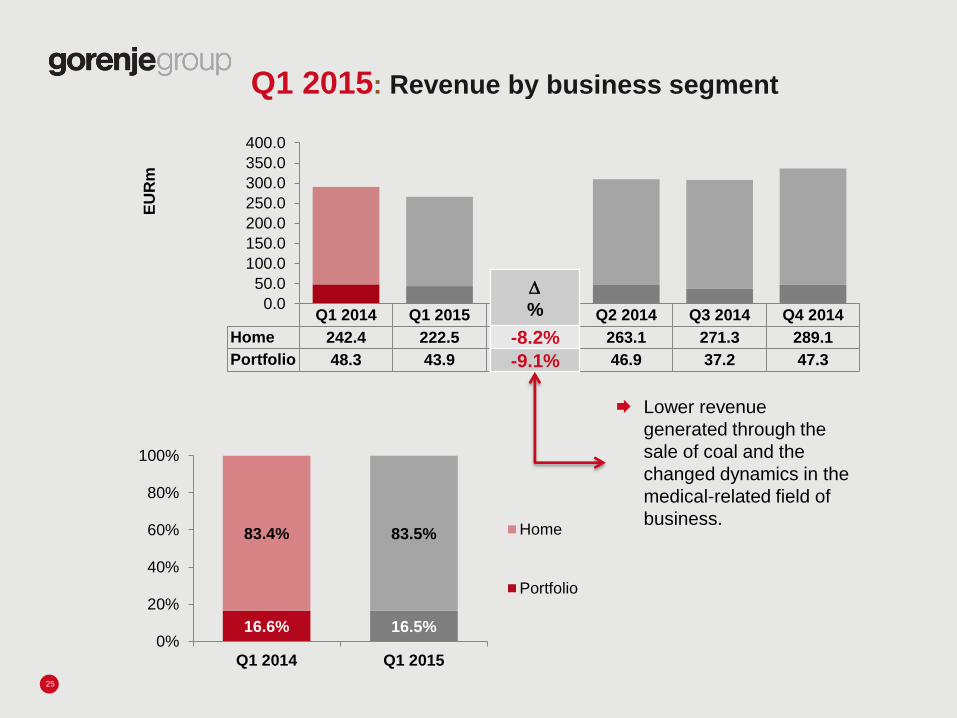

Q1 2014 Q1 2015 Q2 2014 Q3 2014 Q4 2014

Home 242.4 222.5 263.1 271.3 289.1

Portfolio 48.3 43.9 46.9 37.2 47.3

0.0

50.0

100.0

150.0

200.0

250.0

300.0

350.0

400.0E

UR

m

Q1 2015: Revenue by business segment

25

%

-8.2%

-9.1%

16.6% 16.5%

83.4% 83.5%

0%

20%

40%

60%

80%

100%

Q1 2014 Q1 2015

Home

Portfolio

Lower revenue

generated through the

sale of coal and the

changed dynamics in the

medical-related field of

business.

Key innovations:

a new generation of

built-in ovens under

the Gorenje

trademark that were

launched on most of

the markets,

the new Essential

washing machine,

preparation for

launching the new

Magna premium

collection of cooking

appliances.

Increased investments

in R&D, which account

for 3.0% in the Group’s

revenue structure (+0.6

p.p.).

26

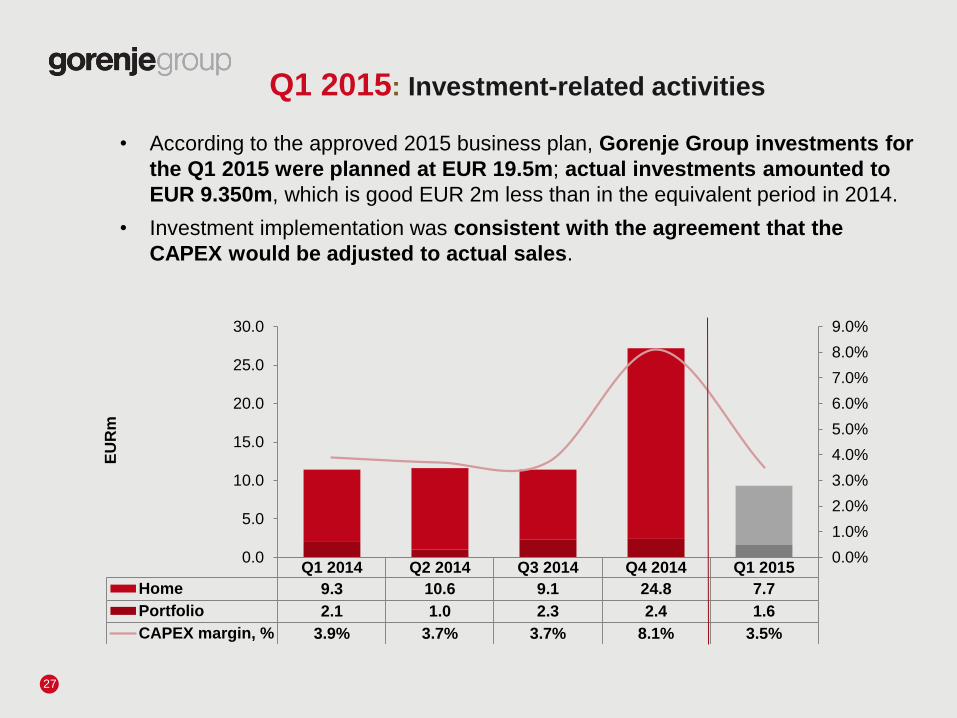

Q1 2015: Development & New products

• According to the approved 2015 business plan, Gorenje Group investments for

the Q1 2015 were planned at EUR 19.5m; actual investments amounted to

EUR 9.350m, which is good EUR 2m less than in the equivalent period in 2014.

• Investment implementation was consistent with the agreement that the

CAPEX would be adjusted to actual sales.

27

Q1 2015: Investment-related activities

Q1 2014 Q2 2014 Q3 2014 Q4 2014 Q1 2015

Home 9.3 10.6 9.1 24.8 7.7

Portfolio 2.1 1.0 2.3 2.4 1.6

CAPEX margin, % 3.9% 3.7% 3.7% 8.1% 3.5%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

0.0

5.0

10.0

15.0

20.0

25.0

30.0

EU

Rm

Q1 2014 Q1 2015 Q2 2014 Q3 2014 Q4 2014

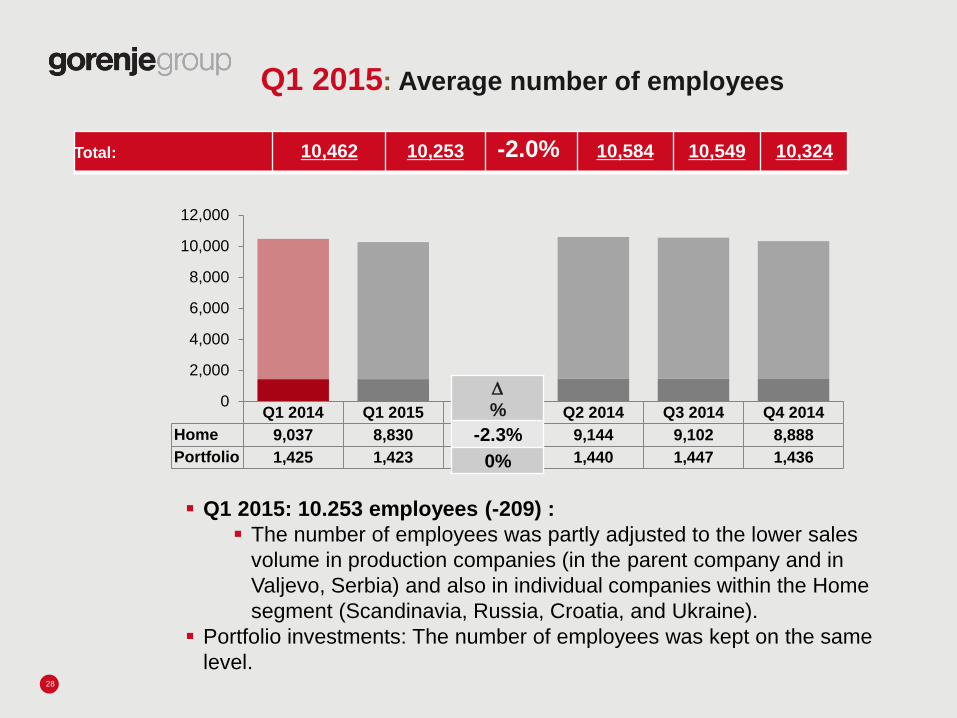

Home 9,037 8,830 9,144 9,102 8,888

Portfolio 1,425 1,423 1,440 1,447 1,436

0

2,000

4,000

6,000

8,000

10,000

12,000

Q1 2015: Average number of employees

Q1 2015: 10.253 employees (-209) :

The number of employees was partly adjusted to the lower sales

volume in production companies (in the parent company and in

Valjevo, Serbia) and also in individual companies within the Home

segment (Scandinavia, Russia, Croatia, and Ukraine).

Portfolio investments: The number of employees was kept on the same

level. 28

%

-2.3%

0%

Total: 10,462 10,253 -2.0% 10,584 10,549 10,324

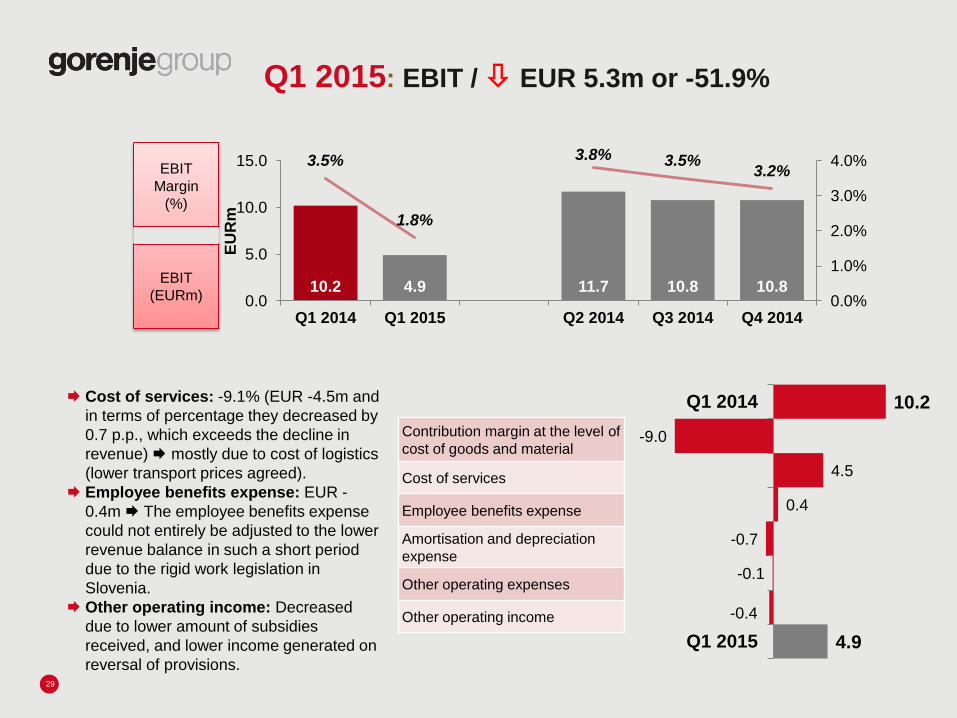

Q1 2015: EBIT / EUR 5.3m or -51.9%

EBIT

Margin

(%)

EBIT

(EURm)

Contribution margin at the level of

cost of goods and material

Cost of services

Employee benefits expense

Amortisation and depreciation

expense

Other operating expenses

Other operating income

10.2

-9.0

4.5

0.4

-0.7

-0.1

-0.4

4.9

Q1 2014

Q1 2015

29

10.2 4.9 11.7 10.8 10.8

3.5%

1.8%

3.8% 3.5% 3.2%

0.0%

1.0%

2.0%

3.0%

4.0%

0.0

5.0

10.0

15.0

Q1 2014 Q1 2015 Q2 2014 Q3 2014 Q4 2014

EU

Rm

Cost of services: -9.1% (EUR -4.5m and

in terms of percentage they decreased by

0.7 p.p., which exceeds the decline in

revenue) mostly due to cost of logistics

(lower transport prices agreed).

Employee benefits expense: EUR -

0.4m The employee benefits expense

could not entirely be adjusted to the lower

revenue balance in such a short period

due to the rigid work legislation in

Slovenia.

Other operating income: Decreased

due to lower amount of subsidies

received, and lower income generated on

reversal of provisions.

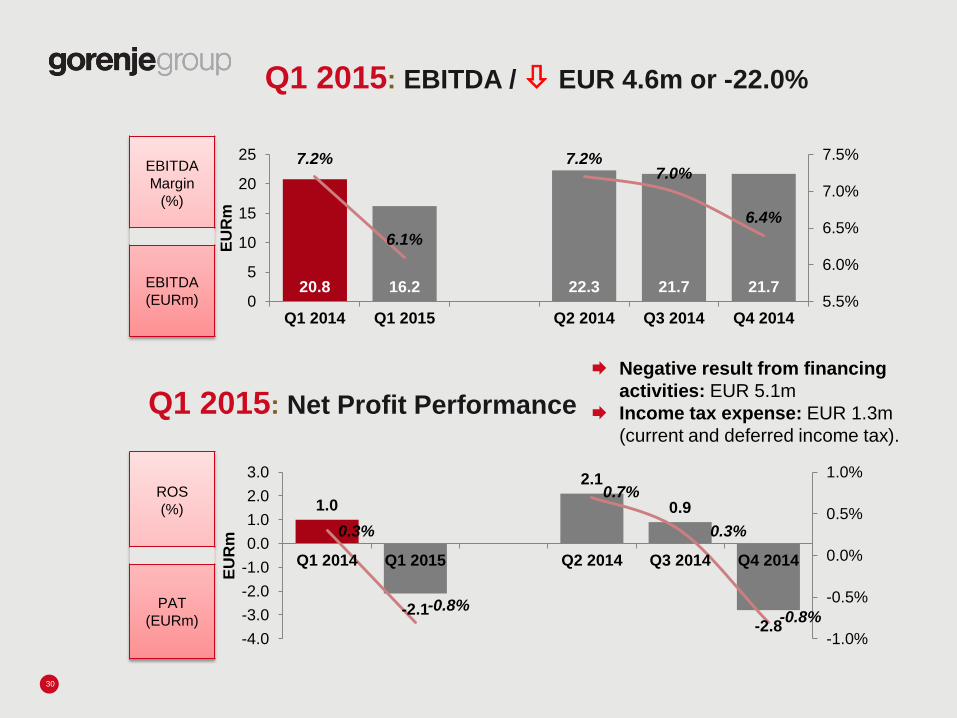

Q1 2015: EBITDA / EUR 4.6m or -22.0%

EBITDA

Margin

(%)

EBITDA

(EURm)

Q1 2015: Net Profit Performance

ROS

(%)

PAT

(EURm)

30

20.8 16.2 22.3 21.7 21.7

7.2%

6.1%

7.2% 7.0%

6.4%

5.5%

6.0%

6.5%

7.0%

7.5%

0

5

10

15

20

25

Q1 2014 Q1 2015 Q2 2014 Q3 2014 Q4 2014

EU

Rm

1.0

-2.1

2.1

0.9

-2.8

0.3%

-0.8%

0.7%

0.3%

-0.8%

-1.0%

-0.5%

0.0%

0.5%

1.0%

-4.0

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

Q1 2014 Q1 2015 Q2 2014 Q3 2014 Q4 2014

EU

Rm

Negative result from financing

activities: EUR 5.1m

Income tax expense: EUR 1.3m

(current and deferred income tax).

Q1 2015: Financial Performance / Indebtedness

Movement of total and net financial liabilities in Q1 for the period 2012-2015 * (EURm)

and maturity structure of financial liabilities

31

* Accounting aspect

467.3 473.2 418.2 422.5 425.5

451.9

392.6 403.0

0.0

50.0

100.0

150.0

200.0

250.0

300.0

350.0

400.0

450.0

500.0

31.3.2012 31.3.2013 31.3.2014 31.3.2015

Total financial liabilities Net financial liabilities

62.4% 57.2% 46.4%

60.2%

37.6% 42.8% 53.6%

39.8%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

31.3.2012 31.3.2013 31.3.2014 31.3.2015

LT financial liabilities ST financial liabilities

Gross debt: EUR 422.5m (+EUR 4.3m) result complies with interim seasonal

dynamics as the Group generates most of negative cash flows from operating and

investing activities; result comprises also liabilities under the fair value of forward

contracts used for hedging against interest rate and currency fluctuations.

Net financial debt: EUR 403.0m (+EUR 10.3m)

Net financial debt / EBITDA: 4.9 (decline by 0.2)

Cash flows from operating and investing activities: -EUR 55.2m; -EUR 31.9m

in Q1 2014

In 2015 we focus on

32

Sales • growth

• improved sales structure

Cost cutting • services

• labour

• material

Deleveraging • divestments

• improved working capital

management

R&D • new products development &

innovation

Processes • SCM

• Complexity

Projects • Lean, TQM, forecasting

Asko premium brand development

Strategic partnership with

Panasonic

Risk Management

Organizational structure and

corporate governance

Strategy 2020

Responsibility • towards all shareholders

• personal responsibility

• for the future of Gorenje Group

*

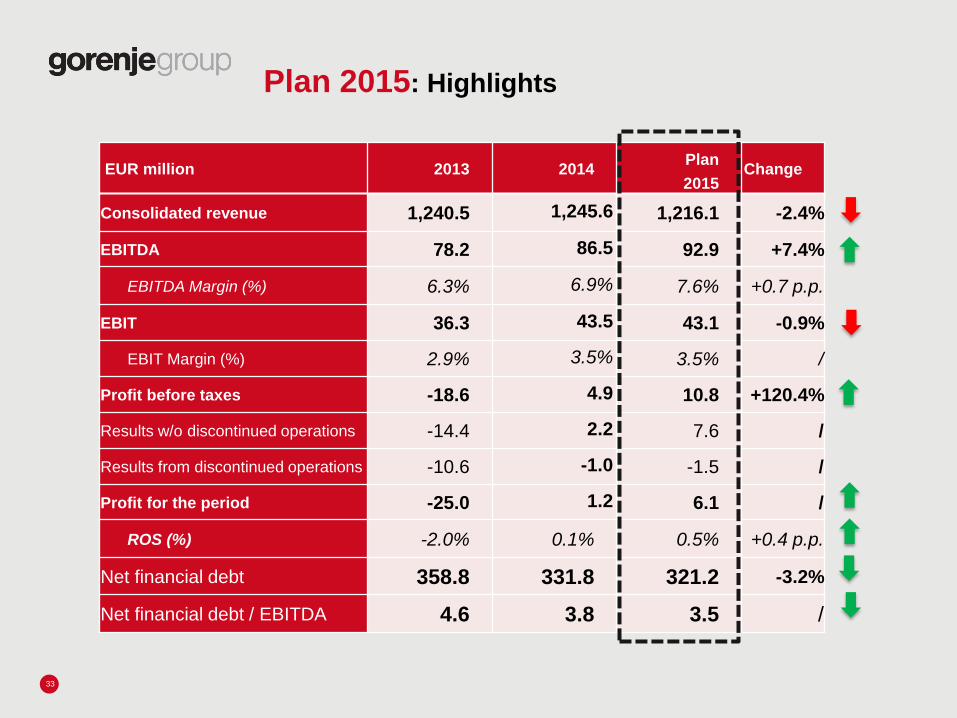

33

EUR million 2013 2014 Plan 2015

Change

Consolidated revenue 1,240.5 1,245.6 1,216.1 -2.4%

EBITDA 78.2 86.5 92.9 +7.4%

EBITDA Margin (%) 6.3% 6.9% 7.6% +0.7 p.p.

EBIT 36.3 43.5 43.1 -0.9%

EBIT Margin (%) 2.9% 3.5% 3.5% /

Profit before taxes -18.6 4.9 10.8 +120.4%

Results w/o discontinued operations -14.4 2.2 7.6 /

Results from discontinued operations -10.6 -1.0 -1.5 /

Profit for the period -25.0 1.2 6.1 /

ROS (%) -2.0% 0.1% 0.5% +0.4 p.p.

Net financial debt 358.8 331.8 321.2 -3.2%

Net financial debt / EBITDA 4.6 3.8 3.5 /

Plan 2015: Highlights

34

New launches: • New generation of Gorenje cooking appliances

• New Asko dishwashers

• New line of Asko cooking appliances

• New line of Magna cooking appliances by Atag

• New Matrix cooking hobs by Atag

Development of new premium and innovative products to

support the growth of sales in upmarket segments

Thank you

for your attention.

Gorenje Representatives

36

Mr. Štefan Kuhar

Executive director, Finance, Tax and Asset

Management

T +386 3 899 7394

M +386 41 343 500

Gorenje, d.d.

Partizanska cesta 12, SI-3320 Velenje, Slovenia

Slovenia

www.gorenjegoup.com

Mrs. Bojana Rojc

Head of IR

T +386 3 899 1345

M +386 51 351 706

Gorenje, d.d.

Partizanska cesta 12, SI-3320 Velenje, Slovenia

Slovenia

www.gorenjegoup.com

Forward-looking statements

This presentation includes forward-looking information and forecasts – i.e. statements regarding the future, rather

than the past, and statements regarding events within the framework and in relation to the currently effective

legislation on publicly traded companies and securities and pursuant to the Rules and Regulations of the Ljubljana

Stock Exchange. These statements can be identified by the words such as "expected", "anticipated", "forecast",

"intended", "planned or budgeted", "probable or likely", "strive/invest effort to", "estimated", "will", "projected", or

similar expressions. These statements include, among others, financial goals and targets of the parent company

Gorenje, d.d., and the Gorenje Group for the upcoming periods, planned or budgeted operations, and financial plans.

These statements are based on current expectations and forecasts and are subject to risk and uncertainty which may

affect the actual results which may in turn differ from the information stated herein for various reasons. Various

factors, many of which are beyond reasonable control by Gorenje, affect the operations, performance, business

strategy, and results of Gorenje. As a result of these factors, actual results, performance, or achievements of Gorenje

may differ materially from the expected results, performance, or achievements as stated in these forward-looking

statements. These factors include, without prejudice to any not mentioned herein, the following: Consumer demand

and market conditions in geographical segments or regions and in the industries in which Gorenje Group is

conducting its operating activities; effects of changes in exchange rates; competitive downward pressure on

downstream prices; major loss of business with a major account/customer; the possibility of overdue or late payment

on the part of the customers; decrease in prices as a result of persistently harsh market conditions, in an extent much

higher than currently expected by the Gorenje Management Board; success of development of new products and

implementation in the market; development of manufacturer's liability for the product; progress of attainment of

operative and strategic goals regarding efficiency; successful identification of opportunities for growth and mergers

and acquisitions, and integration of such opportunities into the existing operations; further volatility and aggravation of

circumstances in capital markets; progress in attainment of goals regarding structural reorganization and

reorganization in purchasing. If one or more risks or uncertainties are in fact materialized or if the said assumptions

are proven wrong, actual results may deviate materially from those stated as expected, hoped for, forecast, projected,

planned, probable, estimated, or anticipated in this announcement. Gorenje does not intend to assume and will not

allow for any liability to update or revise these forecasts in light of development differing from the expected events.

37