FTE Holding GmbH

54

FTE Holding GmbH Financial results for the six months ended June 30, 2016 August 19, 2016

Transcript of FTE Holding GmbH

FTE Holding GmbH Financial results for the six months ended June 30, 2016 August 19, 2016

2

Contents

1. Presentation of financial and other information .............................................. 3

2. Consolidated Income Statement Consolidated Statement of EBITDA Consolidated Statement of Cash Flows ......................................................... 6

3. Consolidated Statement of Balance Sheet ................................................... 22

4. Capitalization, liquidity and other financial data ............................................ 25

5. Changes in material debt instruments .......................................................... 29

6. Subsequent events and material changes to risk factors ............................. 29

7. Summary of significant accounting policies .................................................. 30

8. Interim Consolidated Financial Statements as of June 30, 2016 of FTE Holding GmbH .................................................. 42

3

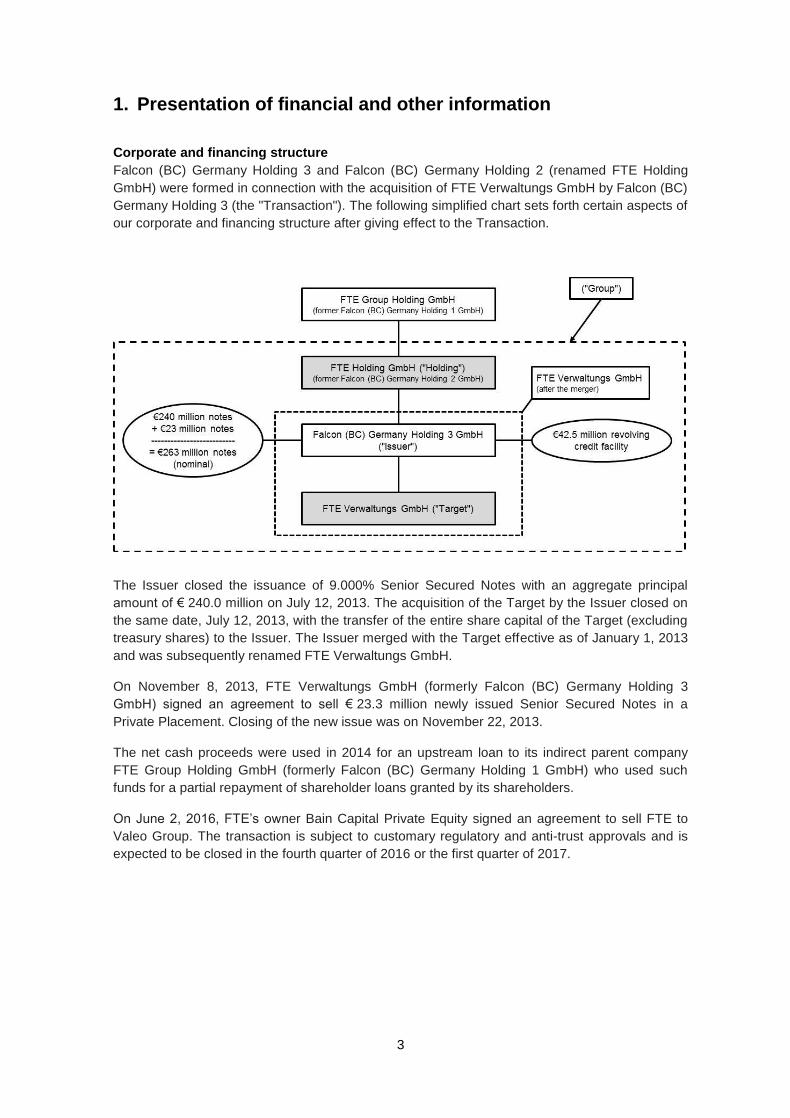

1. Presentation of financial and other information Corporate and financing structure

Falcon (BC) Germany Holding 3 and Falcon (BC) Germany Holding 2 (renamed FTE Holding

GmbH) were formed in connection with the acquisition of FTE Verwaltungs GmbH by Falcon (BC)

Germany Holding 3 (the "Transaction"). The following simplified chart sets forth certain aspects of

our corporate and financing structure after giving effect to the Transaction.

The Issuer closed the issuance of 9.000% Senior Secured Notes with an aggregate principal

amount of € 240.0 million on July 12, 2013. The acquisition of the Target by the Issuer closed on

the same date, July 12, 2013, with the transfer of the entire share capital of the Target (excluding

treasury shares) to the Issuer. The Issuer merged with the Target effective as of January 1, 2013

and was subsequently renamed FTE Verwaltungs GmbH.

On November 8, 2013, FTE Verwaltungs GmbH (formerly Falcon (BC) Germany Holding 3

GmbH) signed an agreement to sell € 23.3 million newly issued Senior Secured Notes in a

Private Placement. Closing of the new issue was on November 22, 2013.

The net cash proceeds were used in 2014 for an upstream loan to its indirect parent company

FTE Group Holding GmbH (formerly Falcon (BC) Germany Holding 1 GmbH) who used such

funds for a partial repayment of shareholder loans granted by its shareholders.

On June 2, 2016, FTE’s owner Bain Capital Private Equity signed an agreement to sell FTE to

Valeo Group. The transaction is subject to customary regulatory and anti-trust approvals and is

expected to be closed in the fourth quarter of 2016 or the first quarter of 2017.

4

Financial and operational data

The Holding and the Issuer were formed on February 21, 2013; opening balance sheets for these

entities were created on April 5, 2013 and they were registered on April 9, 2013. These

companies obtained control over the Target within the meaning of IFRS 3 on July 12, 2013.

The Holding prepared IFRS consolidated financial information as of June 30, 2016 and for the

period from January 1, 2016 to June 30, 2016 with comparative data as of December 31, 2015

and for the period from January 1, 2015 to June 30, 2015.

The financial results of the Holding and its subsidiaries are reported on a consolidated basis. This

report contains data that was neither prepared in accordance with IFRS nor any other generally

accepted accounting principles. It is for informational purposes only and does not purport to

represent or to be indicative of the consolidated results of operations or financial position that the

Group would have reported had the transaction and related financing as defined in the Offering

Memorandum been completed as of the dates presented, and should not be taken as

representative of the Group’s future consolidated results of operations or financial position, nor

does it purport to project the Group’s financial position as of any future date or results of

operations for any future period.

The following financial data, among other, is included herein:

the consolidated income statements for the six-month periods and three-month periods

ended June 30, 2016 and June 30, 2015;

the consolidated statements of cash flows for the six-month periods and three-month

periods ended June 30, 2016 and June 30, 2015;

the consolidated statement of balance sheet as of June 30, 2016 and

December 31, 2015.

The financial data as of December 31, 2015 is based on the audited IFRS consolidated financial

statements of the Holding as of December 31, 2015. The financial data for the six-month periods

and three-month periods ended June 30, 2016 and June 30, 2015 is based on the unaudited

financial statements of the Holding for the respective periods in accordance with International

Financial Reporting Standards (IFRS), which are included in section 8 of this report.

Some financial information in this report has been rounded and, as a result, the figures shown as

totals in this report may vary slightly from the exact arithmetic aggregation of the figures that

precede them. Percentage figures have not been calculated on the basis of rounded figures, but

have instead been calculated on the basis of such amounts prior to rounding.

Unless otherwise indicated, all financial information in this report has been prepared on the basis

of IFRS applicable at the relevant date and is presented in million Euro. IFRS differs in certain

material aspects from generally accepted accounting principles in the US.

Other financial measures

Certain financial measures and ratios related thereto in this report, including EBITDA and

Adjusted EBITDA (collectively, the “EBITDA Metrics”), are not specifically defined under IFRS or

any other generally accepted accounting principles. These measures are presented in this report

because we believe that they are among the measures used by management to evaluate the

cash available to us to fund ongoing, long-term obligations and they are frequently used by

securities analysts, high yield investors and other interested parties for valuation purposes or as a

common measure of the ability of issuers to incur and meet debt service obligations. These

measures may not be comparable to other similarly titled measures of other companies and are

not measurements under IFRS or other generally accepted accounting principles, and you should

not consider such items as alternatives to net income (loss), operating income or any other

performance measures derived in accordance with IFRS.

5

We believe that this information, along with comparable IFRS measures, may be useful to

investors because it provides a basis for measuring the operating performance of the periods

presented. These measures are used to manage our business, along with the most directly

comparable IFRS financial measures and to evaluate the operating performance.

The EBITDA Metrics have limitations as analytical tools, and you should not consider them in

isolation or as a substitute for analysis of our results or any performance measures under IFRS

as set forth in our financial statements. Some of these limitations are:

they do not reflect our cash expenditures or future requirements for capital expenditures;

they do not reflect changes in, or cash requirements for, our working capital needs;

they do not reflect the interest expense or cash requirements necessary to service

interest or principal payments on our debt;

they do not reflect any cash income taxes that we may be required to pay;

they are not adjusted for all non-cash income or expense items that are reflected in our

consolidated income statement;

they do not reflect the impact of earnings or charges resulting from certain matters that

we consider not to be indicative of our ongoing operations;

assets are depreciated or amortized over differing estimated useful lives and often have

to be replaced in the future, and these measures do not reflect any cash requirements for

such replacements; and

other companies in our industry may calculate these measures differently than we do,

limiting their usefulness as comparative measures.

Because of these limitations, the EBITDA Metrics should not be considered as measures of

discretionary cash available to us to invest in the growth of our business or as measures of cash

that will be available to us to meet our obligations. You should compensate for these limitations

by relying primarily on our IFRS results and using these non-IFRS measures only supplementary

to evaluate our performance. You are encouraged to evaluate each of the adjustments reflected

in our presentation of the EBITDA Metrics and whether you consider each to be appropriate.

Industry Data

In this report, we may rely on and refer to information regarding our business and the market in

which we operate and compete. We have obtained this information from various third party

sources, including providers of industry data, discussions with our customers and our own

internal estimates. We cannot assure you that any of this information is accurate or correctly

reflects our position in the industry, and none of our internal surveys or information has been

verified by any independent sources. We do not make any representation or warranty as to the

accuracy or completeness of any such information set forth in this report.

Forward looking statements and other qualifications

The following discussion and analysis is based on and should be read in conjunction with our

historical financial information included elsewhere in this annual report. Certain capitalized terms

used herein defined have the meaning set out in the Offering Memorandum relating to the

issuance of € 240.0 million senior secured notes dated July 9, 2013.

The discussion may include forward looking statements, which, although based on assumptions

that we consider reasonable, are subject to risks and uncertainties, which could cause actual

events or conditions to differ materially from those implied herein. You are cautioned not to place

undue reliance on these forward looking statements. These forward looking statements are made

as of the date of this report and are not intended to give any assurance as to future results.

6

2. Consolidated Income Statement

Consolidated Statement of EBITDA

Consolidated Statement of Cash Flows

2.1 Quarterly results from April 1 to June 30, 2016

Consolidated Income Statement

Holding

three months

ended June 30,

three months

ended June 30,

(€ million) 2015 2016 Change % Change

Revenues 134.4 147.9 13.5 10.0%

Cost of sales -107.1 -114.1 -7.0 -6.6%

Gross profit 27.3 33.7 6.4 23.6%

Distribution expenses -4.1 -3.6 0.5 13.0%

Administrative expenses -5.5 -5.5 0.1 1.3%

Research and development expenses -5.6 -7.5 -2.0 -35.4%

Restructuring expenses -0.5 0.0 0.6 >100.0%

Profit from operations 11.6 17.2 5.7 48.9%

Results from associated companies and joint ventures 0.4 0.3 -0.1 -35.5%

Finance income 0.6 1.2 0.6 >100.0%

Finance expenses -6.4 -6.8 -0.4 -5.6%

Finance result -5.4 -5.3 0.1 2.1%

Profit before income taxes 6.1 11.9 5.8 94.0%

Income taxes -2.8 -4.6 -1.8 -64.3%

Deferred taxes 0.9 0.8 -0.1 -10.4%

Net profit 4.3 8.2 3.9 90.5%

7

Revenues

Revenues increased by € 13.5 million, or 10.0%, to € 147.9 million in the three months ended

June 30, 2016 from € 134.4 million in the three months ended June 30, 2015. This increase was

primarily due to higher sales volume of Electric Shift Transmission (EST) and Electric Pump

Transmission (EPT) products in China and Germany.

The following table sets forth our revenues by customer location for the three months ended

June 30, 2015 and 2016:

Holding

three months

ended June 30,

three months

ended June 30,

(€ million) 2015 2016 Change % Change

Revenues (by customer location)

Germany(1) 33.4 44.2 10.7 32.1%

Europe (excluding Germany)(1) 60.6 60.8 0.2 0.3%

Americas 19.6 19.1 -0.5 -2.3%

Asia 19.9 23.1 3.2 16.3%

Rest of world 1.0 0.7 -0.2 -25.2%

Total 134.4 147.9 13.5 10.0%

(1) Figures 2015 have been adjusted for caliper sales-split Europe / Germany.

The following table sets forth our revenues by product categories (to the extent reported so far)

for the three months ended June 30, 2015 and 2016, reflecting our product portfolio changes:

Holding

three months

ended June 30,

three months

ended June 30,

(€ million) 2015 2016 Change % Change

Revenues (by product categories)

Clutch systems 81.6 93.0 11.4 14.0%

Brake systems 33.4 37.0 3.5 10.6%

Other(1) 19.4 17.9 -1.5 -7.7%

Total 134.4 147.9 13.5 10.0%

(1) Other revenues contain primarily spare parts and merchandise including CPx (controlled piston unit) .

8

The following table sets forth our revenues by new product categories for the three months ended

June 30, 2015 and 2016, reflecting our product portfolio changes:

Holding

three months

ended June 30,

three months

ended June 30,

(€ million) 2015 2016 Change % Change

Revenues (by product categories)

BAT(1) 33.4 37.0 3.5 10.6%

thereof brake calipers 13.4 12.9 -0.5 -3.5%

MST(2) 75.6 76.1 0.5 0.7%

EST(3) 16.0 22.3 6.3 39.2%

EPT(4) 0.5 1.9 1.4 >100.0%

Other(5) 8.8 10.5 1.7 19.5%

Total 134.4 147.9 13.5 10.0%

(1) BAT is an acronym for Brake Actuation Technology including brake caliper business. (2) MST is an acronym for Manual Shift Transmission. (3) EST is an acronym for Electric Shift Transmission including CPx (controlled piston unit). (4) EPT is an acronym for Electric Pump Transmission. (5) Other revenues contain primarily spare parts and merchandise.

Germany

Revenues in Germany increased by € 10.7 million, or 32.1%, to € 44.2 million in the three months

ended June 30, 2016 from € 33.4 million in the three months ended June 30, 2015 primarily due

to increased sales volume of EST and EPT products.

Europe (excluding Germany)

Revenues in Europe (excluding Germany) increased by € 0.2 million, or 0.3%, to € 60.8 million in

the three months ended June 30, 2016 from € 60.6 million in the three months ended

June 30, 2015, in line with market growth in manual shift transmission vehicles.

Americas

Revenues in Americas decreased by € 0.5 million, or 2.3%, to € 19.1 million in the three months

ended June 30, 2016 from € 19.6 million in the three months ended June 30, 2015, primarily due

to continuing difficult economical market conditions in Brazil and unfavorable currency effects.

Asia

Revenues in Asia increased by € 3.2 million, or 16.3%, to € 23.1 million in the three months

ended June 30, 2016 from € 19.9 million in the three months ended June 30, 2015 due to

increased sales volume of EST products.

9

Cost of Sales

Cost of sales increased by € 7.0 million, or 6.6%, to € 114.1 million (or 77.2% of revenues) in the

three months ended June 30, 2016 from € 107.1 million (or 79.7% of revenues) in the three

months ended June 30, 2015. The increase was mainly driven by higher sales volume.

Gross Profit

Gross profit increased by € 6.4 million, or 23.6%, to € 33.7 million in the three months ended

June 30, 2016 from € 27.3 million in the three months ended June 30, 2015. Gross profit was

mainly affected by higher sales volume.

Distribution Expenses

Distribution expenses decreased by € 0.5 million, or 13.0%, to € 3.6 million in the three months

ended June 30, 2016 from € 4.1 million in the three months ended June 30, 2015 due to lower

advertising expenses and one-time expenses in the previous year.

Administrative Expenses

Administrative expenses decreased by € 0.1 million, or 1.3%, to € 5.5 million in the three months

ended June 30, 2016 from € 5.5 million in the three months ended June 30, 2015.

Research and Development Expenses

Research and development expenses increased by € 2.0 million, or 35.4%, to € 7.5 million in the

three months ended June 30, 2016 from € 5.6 million in the three months ended

June 30, 2015. This increase was mainly the result of increased depreciation from capitalized

new R&D projects, higher R&D expenses and lower R&D capitalization in 2016.

Restructuring Expenses

Restructuring expenses decreased by 0.5 million in the six months ended June 30, 2016

compared to previous year, primarily comprising for severance expenses in connection with

production relocations in Europe and NAFTA in 2015.

Finance Result

Finance expenses decreased by € 0.1 million to € 5.3 million in the three months ended

June 30, 2016 from € 5.4 million in the three months ended June 30, 2015, primarily as a result of

revaluation of existing intercompany loans caused by currency changes.

Taxes

Tax expenses increased by € 1.9 million to € 3.7 million in the three months ended

June 30, 2016 from € 1.8 million in the three months ended June 30, 2015, mainly as a result of

increased profits.

Net Profit

Net profit increased by € 3.9 million to a profit of € 8.2 million in the three months ended

June 30, 2016 from a profit of € 4.3 million in the three months ended June 30, 2015.

This increase of net profit was mainly driven by higher sales volume and gross profit with lower

restructuring expenses.

10

The following table presents the reconciliation from net profit for the period to Adjusted EBITDA:

Consolidated Statement of EBITDA

Holding

three months

ended June 30,

three months

ended June 30,

(€ million) 2015 2016 Change % Change

Net profit 4.3 8.2 3.9 90.5%

Deferred taxes -0.9 -0.8 0.1 10.4%

Current income taxes 2.8 4.6 1.8 64.3%

Finance result 5.4 5.3 -0.1 -2.1%

Profit from operations 11.6 17.2 5.7 48.9%

Depreciation and amortization 8.7 8.9 0.2 2.0%

EBITDA(1) (14)

20.3 26.1 5.8 28.7%

EBITDA Margin(2) (14)

15.1% 17.7%

Personnel restructuring(3)

0.5 -0.0 -0.6 >-100.0%

Operational excellence projects(4)

0.7 0.4 -0.4 -50.2%

Management reorganization(5)

0.0 0.0 0.0 N/A

Pension interests(6)

0.4 0.4 -0.0 -0.3%

Bank charges(7)

0.1 0.1 0.0 37.5%

Allowances for doubtful accounts and customer insolvency

(8) 0.0 0.0 0.0 N/A

Consumption of revalued inventories(9)

0.1 0.1 -0.0 -1.4%

Integration projects(10)

0.0 0.1 0.1 N/A

Transaction costs(11)

0.6 0.2 -0.4 -63.6%

Non-recurring items(12)

0.3 0.0 -0.3 -100.0%

Adjusted EBITDA(13) (15)

23.0 27.4 4.3 18.9%

Adjusted EBITDA Margin(14) (15)

17.1% 18.5%

(1) EBITDA represents profit from operations (representing net profit for the period before deferred income taxes, current income taxes and finance result) before depreciation, amortization (including impairment losses). (2) EBITDA Margin represents EBITDA divided by revenues. (3) Represents costs relating to severance payments for employees in connection with restructuring our manufacturing capacity, mainly in Europe and NAFTA. (4) Includes consulting fees in connection with the optimization and improvement of several processes such as for supply chain, logistics, human resources and sales and distribution and consulting fees in connection with the Group strategy review. (5) Includes costs related to the reorganization of our management structure and strategy. (6) Represents non-cash accrued interest on defined benefit pension obligations. These items have been included in personnel costs, but are regarded by management as financial in nature. (7) Represents costs related to the collection and factoring of customer receivables, particularly in the aftermarket business. These items are included in administration costs, but are regarded by management as financial in nature. (8) Net sum of the recognition and release of allowances for doubtful accounts and customer insolvency, based on management’s determination of the likelihood of receipt of payment from certain customers. These items are recognized in costs of goods sold and administration costs, but are regarded as non-operational in nature. (9) Represents the part of the PPA 2013 based revaluation of inventories that were sold/consumed and therefore recognized in cost of sales. (10) Represents costs relating to integration of acquisitions. (11) Transaction costs include mainly costs for the acquisition of the Target and new acquisitions. (12) Includes non-recurring impacts in the reported period (e.g. accrual for risk of lawsuits, potential warranty claims) (13) Adjusted EBITDA represents EBITDA as adjusted for certain infrequent charges and nonoperational costs identified, showed in the table above. (14) Adjusted EBITDA Margin represents Adjusted EBITDA divided by revenues.

11

(15) EBITDA, EBITDA Margin, Adjusted EBITDA and Adjusted EBITDA Margin are not specifically defined under IFRS or any other generally accepted accounting principles and you should not consider them as an alternative to net income (loss) or any other performance measures derived in accordance with IFRS. Our management believes that EBITDA, EBITDA Margin, Adjusted EBITDA and Adjusted EBITDA Margin are meaningful for investors because they provide an analysis of our operating results, profitability and ability to service debt and because EBITDA, EBITDA Margin, Adjusted EBITDA and Adjusted EBITDA Margin are used by our management to track our business development, establish operational and strategic targets and make important business decisions. EBITDA, EBITDA Margin, Adjusted EBITDA and Adjusted EBITDA Margin are also measures commonly reported and widely used by analysts, investors and other interested parties in our industry. To facilitate the analysis of our operations, these indicators exclude amortization, impairment and depreciation expenses from operating profit in order to eliminate the impact of general long-term capital investment. Although we are presenting these measures to enhance the understanding of our historical operating performance, EBITDA, EBITDA Margin, Adjusted EBITDA and Adjusted EBITDA Margin should not be considered an alternative to operating profit as indicators of our operating performance, or as alternatives to cash flows from operating activities as measures of our liquidity.

EBITDA, EBITDA Margin

EBITDA increased by € 5.8 million, or 28.7%, to € 26.1 million (or 17.7% of revenues) in the three

months ended June 30, 2016 from € 20.3 million (or 15.1% of revenues) in the three months

ended June 30, 2015. EBITDA increased mainly due to growing sales volume and gross profit

with lower restructuring expenses.

The Adjusted EBITDA increased by € 4.3 million, or 18.9%, to € 27.4 million (or 18.5% of

revenues) in the three months ended June 30, 2016 from € 23.0 million (or 17.1% of revenues) in

the three months ended June 30, 2015 mainly due to higher sales volume and gross profit with

lower restructuring expenses.

12

Consolidated Statement of Cash Flows

Holding

three months

ended June 30,

three months

ended June 30,

(€ million) 2015 2016 Change % Change

Cash Flows from Operating Activities

Profit before income taxes 6.1 11.9 5.8 94.0%

Adjustments for

Depreciation and amortization 8.7 8.9 0.2 2.0%

Finance result 5.8 5.7 -0.1 -2.0%

Other non-cash expenses and income 0.1 -0.3 -0.4 >-100.0%

Total adjustments 14.6 14.3 -0.3 -2.1%

Changes in Working Capital and Other Assets and Liabilities

Trade receivables -9.2 -8.7 0.5 5.0%

Other assets 0.8 -0.3 -1.1 >-100.0%

Inventories 0.1 0.8 0.7 >100.0%

Trade payables 0.3 6.4 6.1 >100.0%

Total change in working capital -8.1 -1.8 6.3 77.5%

Changes in pension provisions -0.4 -0.5 -0.0

-8.3%

Changes in provisions -0.2 -0.2 -0.0 -0.6%

Changes in other liabilities 1.2 2.1 1.0 83.0%

Total change in working capital and other assets and liabilities -7.6 -0.4 7.2

95.3%

Interests paid / received -0.2 -0.2 0.0 15.1%

Income taxes paid / received -2.2 -2.5 -0.4 -17.2%

Net cash flows from operating activities 10.8 23.2 12.3

>100.0%

Cash Flows from Investing Activities

Investments in property, plant and equipment -4.7 -6.1 -1.3

-28.3%

Investments in intangible assets -0.0 -0.2 -0.2 >-100.0%

Proceeds from disposals of tangible and intangible assets 0.1 0.0 -0.0 -64.3%

Investments in development costs -2.6 -1.8 0.8 30.2%

Net cash flows from investing activities -7.3 -8.1 -0.8

-10.5%

13

Holding

three months

ended June 30,

three months

ended June 30,

(€ million) 2015 2016 Change % Change

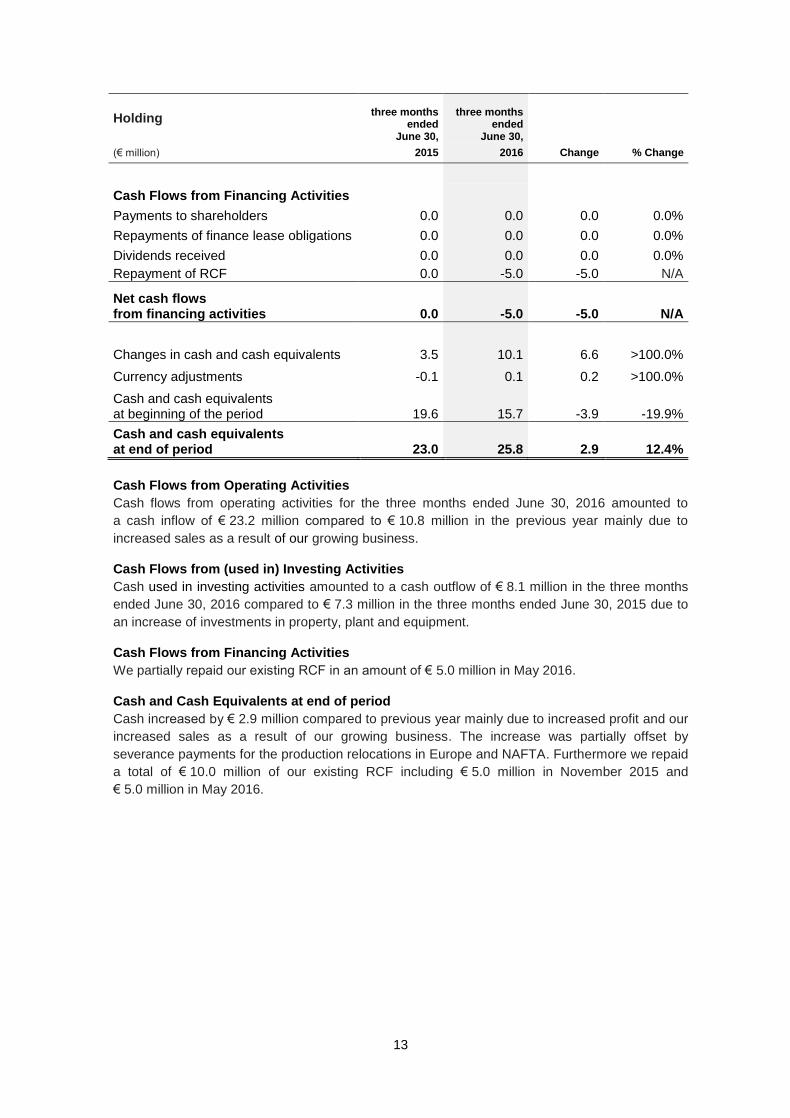

Cash Flows from Financing Activities

Payments to shareholders 0.0 0.0 0.0 0.0%

Repayments of finance lease obligations 0.0 0.0 0.0 0.0%

Dividends received 0.0 0.0 0.0 0.0%

Repayment of RCF 0.0 -5.0 -5.0 N/A

Net cash flows from financing activities 0.0 -5.0 -5.0 N/A

Changes in cash and cash equivalents 3.5 10.1 6.6 >100.0%

Currency adjustments -0.1 0.1 0.2 >100.0%

Cash and cash equivalents at beginning of the period 19.6 15.7 -3.9

-19.9%

Cash and cash equivalents at end of period 23.0 25.8 2.9

12.4%

Cash Flows from Operating Activities

Cash flows from operating activities for the three months ended June 30, 2016 amounted to

a cash inflow of € 23.2 million compared to € 10.8 million in the previous year mainly due to

increased sales as a result of our growing business.

Cash Flows from (used in) Investing Activities

Cash used in investing activities amounted to a cash outflow of € 8.1 million in the three months

ended June 30, 2016 compared to € 7.3 million in the three months ended June 30, 2015 due to

an increase of investments in property, plant and equipment.

Cash Flows from Financing Activities

We partially repaid our existing RCF in an amount of € 5.0 million in May 2016.

Cash and Cash Equivalents at end of period

Cash increased by € 2.9 million compared to previous year mainly due to increased profit and our

increased sales as a result of our growing business. The increase was partially offset by

severance payments for the production relocations in Europe and NAFTA. Furthermore we repaid

a total of € 10.0 million of our existing RCF including € 5.0 million in November 2015 and

€ 5.0 million in May 2016.

14

2.2 Year to date results ended June 30, 2016

Consolidated Income Statement

Holding

January 1

to June 30,

January 1

to June 30,

(€ million) 2015 2016 Change % Change

Revenues 260.2 286.7 26.5 10.2%

Cost of sales -207.9 -224.1 -16.3 -7.8%

Gross profit 52.4 62.6 10.2 19.5%

Distribution expenses -7.8 -7.1 0.8 9.8%

Administrative expenses -11.5 -11.0 0.5 4.0%

Research and development expenses -11.4 -14.5 -3.1 -27.3%

Restructuring expenses -2.9 -0.4 2.5 86.6%

Profit from operations 18.8 29.6 10.8 57.5%

Results from associated companies and joint ventures 0.6 0.4 -0.1 -23.1%

Finance income 1.7 2.1 0.4 24.2%

Finance expenses -15.0 -13.6 1.4 9.1%

Finance result -12.7 -11.0 1.6 13.0%

Profit before income taxes 6.1 18.6 12.5 >100.0%

Income taxes -3.8 -7.9 -4.1 >-100.0%

Deferred taxes 0.6 1.7 1.1 >100.0%

Net profit 2.9 12.4 9.5 >100.0%

15

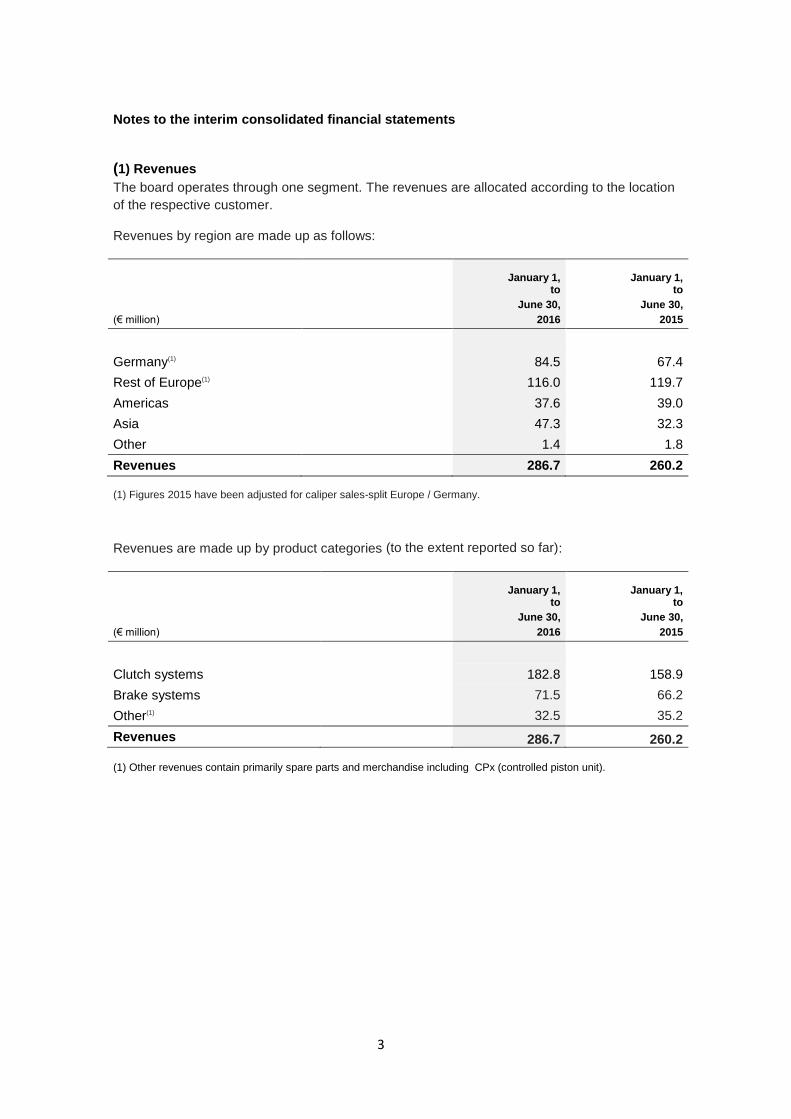

Revenues

Revenues increased by € 26.5 million, or 10.2%, to € 286.7 million in the six months ended

June 30, 2016 from € 260.2 million in the six months ended June 30, 2015. This increase was

primarily due to higher sales volume Electric Shift Transmission (EST) and Electric Pump

Transmission (EPT) products in China and Germany.

The following table sets forth our revenues by customer location for the six months ended June

30, 2015 and 2016:

Holding

January 1

to June 30,

January 1

to June 30,

(€ million) 2015 2016 Change % Change

Revenues (by customer location)

Germany(1) 67.4 84.5 17.1 25.4%

Europe (excluding Germany)(1) 119.7 116.0 -3.8 -3.1%

Americas 39.0 37.6 -1.4 -3.7%

Asia 32.3 47.3 14.9 46.2%

Rest of world 1.8 1.4 -0.3 -19.6%

Total 260.2 286.7 26.5 10.2%

(1) Figures 2015 have been adjusted for caliper sales-split Europe / Germany.

The following table sets forth our revenues by product categories (to the extent reported so far)

for the six months ended June 30, 2015 and 2016, reflecting our product portfolio changes:

Holding

January 1

to June 30,

January 1

to June 30,

(€ million) 2015 2016 Change % Change

Revenues (by product categories)

Clutch systems 158.9 182.8 23.9 15.1%

Brake systems 66.2 71.5 5.2 7.9%

Other(1) 35.2 32.5 -2.7 -7.6%

Total 260.2 286.7 26.5 10.2%

(1) Other revenues contain primarily spare parts and merchandise including CPx (controlled piston unit).

16

The following table sets forth our revenues by new product categories for the six months ended

June 30, 2015 and 2016, reflecting our product portfolio changes:

Holding

January 1

to June 30,

January 1

to June 30,

(€ million) 2015 2016 Change % Change

Revenues (by product categories)

BAT(1) 66.2 71.5 5.2 7.9%

thereof brake calipers 25.9 25.3 -0.6 -2.2%

MST(2) 149.4 149.9 0.5 0.3%

EST(3) 26.6 43.7 17.1 64.2%

EPT(4) 1.0 3.9 2.9 >100.0%

Other(5) 17.0 17.8 0.8 4.7%

Total 260.2 286.7 26.5 10.2%

(1) BAT is an acronym for Brake Actuation Technology including brake caliper business. (2) MST is an acronym for Manual Shift Transmission. (3) EST is an acronym for Electric Shift Transmission including CPx (controlled piston unit). (4) EPT is an acronym for Electric Pump Transmission. (5) Other revenues contain primarily spare parts and merchandise.

Germany

Revenues in Germany increased by € 17.1 million, or 25.4%, to € 84.5 million in the six months

ended June 30, 2016 from € 67.4 million in the six months ended June 30, 2015 primarily due to

increased sales volume of EST and EPT products.

Europe (excluding Germany)

Revenues in Europe (excluding Germany) decreased by € 3.8 million, or 3.1%, to € 116.0 million

in the six months ended June 30, 2016 from € 119.7 million in the six months ended

June 30, 2015 due to temporary higher demand of a series product in 2015.

Americas

Revenues in Americas decreased by € 1.4 million, or 3.7%, to € 37.6 million in the six months

ended June 30, 2016 from € 39.0 million in the six months ended June 30, 2015 primarily due to

continuing difficult economical market conditions in Brazil and unfavorable currency effects.

Asia

Revenues in Asia increased by € 14.9 million, or 46.2%, to € 47.3 million in the six months ended

June 30, 2016 from € 32.3 million in the six months ended June 30, 2015 due to increasing sales

of EST products.

17

Cost of Sales

Cost of sales increased by € 16.3 million, or 7.8%, to € 224.1 million (or 78.2% of revenues) in the

six months ended June 30, 2016 from € 207.9 million (or 79.9% of revenues) in the six months

ended June 30, 2015. The increase was mainly driven by higher sales volume.

Gross Profit

Gross profit increased by € 10.2 million, or 19.5%, to € 62.6 million in the six months ended

June 30, 2016 from € 52.4 million in the six months ended June 30, 2015. Gross profit was mainly

affected by higher sales volume, partially offset by unfavorable currency effects compared to

previous year.

Distribution Expenses

Distribution expenses decreased by € 0.8 million, or 9.8%, to € 7.1 million in the six months

ended June 30, 2016 from € 7.8 million in the six months ended June 30, 2015 due to lower

advertising expenses and one-time expenses in the previous year.

Administrative Expenses

Administrative expenses decreased by € 0.5 million, or 4.0%, to € 11.0 million in the six months

ended June 30, 2016 from € 11.5 million in the six months ended June 30, 2015 mainly due to

one-time expenses in the previous year.

Research and Development Expenses

Research and development expenses increased by € 3.1 million, or 27.3%, to € 14.5 million in the

six months ended June 30, 2016 from € 11.4 million in the six months ended

June 30, 2015. This increase was mainly the result of increased depreciation from capitalized

new R&D projects, higher R&D expenses and lower R&D capitalization in 2016.

Restructuring Expenses

Restructuring expenses decreased by 0.6 million in the six months ended June 30, 2016

compared to previous year, primarily comprising of severance expenses in connection with

production relocations in Europe and NAFTA in 2015.

Finance Result

Finance expenses decreased by € 1.6 million to € 11.0 million in the six months ended

June 30, 2016 from € 12.7 million in the six months ended June 30, 2015, primarily as a result of

the revaluation of existing intercompany loans caused by changes in currency exchange rates.

Taxes

Tax expenses increased by € 3.0 million to € 6.2 million in the six months ended

June 30, 2016 from € 3.2 million in the six months ended June 30, 2015, which was mainly a

result of increased profits.

Net Profit

Net profit increased by € 9.5 million to a profit of € 12.4 million in the six months ended

June 30, 2016 from a profit of € 2.9 million in the six months ended June 30, 2015.

This increase of net profit was mainly driven by higher sales volume and gross profit with lower

restructuring expenses.

18

The following table presents the reconciliation from net profit for the period to Adjusted EBITDA:

Consolidated Statement of EBITDA

Holding

January 1

to June 30,

January 1

to June 30,

(€ million) 2015 2016 Change % Change

Net profit 2.9 12.4 9.5 >100.0%

Deferred taxes -0.6 -1.7 -1.1 >-100.0%

Income taxes 3.8 7.9 4.1 >100.0%

Finance result 12.7 11.0 -1.6 -13.0%

Profit from operations 18.8 29.6 10.8 57.5%

Depreciation and amortization 17.0 17.8 0.8 4.4%

EBITDA(1) (14)

35.8 47.4 11.6 32.3%

EBITDA Margin(2) (14)

13.8% 16.5%

Personnel restructuring(3)

2.9 0.4 -2.5 -86.6%

Operational excellence projects(4)

1.2 0.6 -0.6 -47.8%

Management reorganization(5)

0.0 0.0 0.0 N/A

Pension interests(6)

0.8 0.8 -0.0 -0.5%

Bank charges(7)

0.1 0.2 0.0 32.7%

Allowances for doubtful accounts and customer insolvency

(8) 0.0 0.0 0.0 N/A

Consumption of revalued inventories(9)

0.1 0.1 -0.0 -1.4%

Integration projects(10)

0.0 0.1 0.1 N/A

Transaction costs(11)

0.8 0.5 -0.3 -40.2%

Non-recurring items(12)

2.9 0.0 -2.9 -100.0%

Adjusted EBITDA(13) (15)

44.6 50.1 5.5 12.2%

Adjusted EBITDA Margin(14) (15)

17.2% 17.5%

(1) EBITDA represents profit from operations (representing net profit for the period before deferred income taxes, current income taxes and finance result) before depreciation, amortization (including impairment losses). (2) EBITDA Margin represents EBITDA divided by revenues. (3) Represents costs relating to severance payments for employees in connection with restructuring our manufacturing capacity, mainly in Europe and NAFTA. (4) Includes consulting fees in connection with the optimization and improvement of several processes such as for supply chain, logistics, human resources and sales and distribution and consulting fees in connection with the Group strategy review. (5) Includes costs related to the reorganization of our management structure and strategy. (6) Represents non-cash accrued interest on defined benefit pension obligations. These items have been included in personnel costs, but are regarded by management as financial in nature. (7) Represents costs related to the collection and factoring of customer receivables, particularly in the aftermarket business. These items are included in administration costs, but are regarded by management as financial in nature. (8) Net sum of the recognition and release of allowances for doubtful accounts and customer insolvency, based on management’s determination of the likelihood of receipt of payment from certain customers. These items are recognized in costs of goods sold and administration costs, but are regarded as non-operational in nature. (9) Represents the part of the PPA 2013 based revaluation of inventories that were sold/consumed and therefore recognized in cost of sales. (10) Represents costs relating to integration of acquisitions. (11) Transaction costs include mainly costs for the acquisition of the Target and new acquisitions. (12) Includes non-recurring impacts in the reported period (e.g. accrual for risk of lawsuits, potential warranty claims) (13) Adjusted EBITDA represents EBITDA as adjusted for certain infrequent charges and nonoperational costs identified, showed in the table above. (14) Adjusted EBITDA Margin represents Adjusted EBITDA divided by revenues.

19

(15) EBITDA, EBITDA Margin, Adjusted EBITDA and Adjusted EBITDA Margin are not specifically defined under IFRS or any other generally accepted accounting principles and you should not consider them as an alternative to net income (loss) or any other performance measures derived in accordance with IFRS. Our management believes that EBITDA, EBITDA Margin, Adjusted EBITDA and Adjusted EBITDA Margin are meaningful for investors because they provide an analysis of our operating results, profitability and ability to service debt and because EBITDA, EBITDA Margin, Adjusted EBITDA and Adjusted EBITDA Margin are used by our management to track our business development, establish operational and strategic targets and make important business decisions. EBITDA, EBITDA Margin, Adjusted EBITDA and Adjusted EBITDA Margin are also measures commonly reported and widely used by analysts, investors and other interested parties in our industry. To facilitate the analysis of our operations, these indicators exclude amortization, impairment and depreciation expenses from operating profit in order to eliminate the impact of general long-term capital investment. Although we are presenting these measures to enhance the understanding of our historical operating performance, EBITDA, EBITDA Margin, Adjusted EBITDA and Adjusted EBITDA Margin should not be considered an alternative to operating profit as indicators of our operating performance, or as alternatives to cash flows from operating activities as measures of our liquidity.

EBITDA, EBITDA Margin

EBITDA increased by € 11.6 million, or 32.3%, to € 47.4 million (or 16.5% of revenues) in the six

months ended June 30, 2016 from € 35.8 million (or 13.8% of revenues) in the six months ended

June 30, 2015. EBITDA increased due to growing sales volume and gross profit with lower

restructuring expenses.

The Adjusted EBITDA increased by € 5.5 million, or 17.5%, to € 50.1 million (or 17.5% of

revenues) in the six months ended June 30, 2016 from € 44.6 million (or 17.2% of revenues) in

the six months ended June 30, 2015 due to higher sales volume and gross profit with lower

restructuring expenses.

20

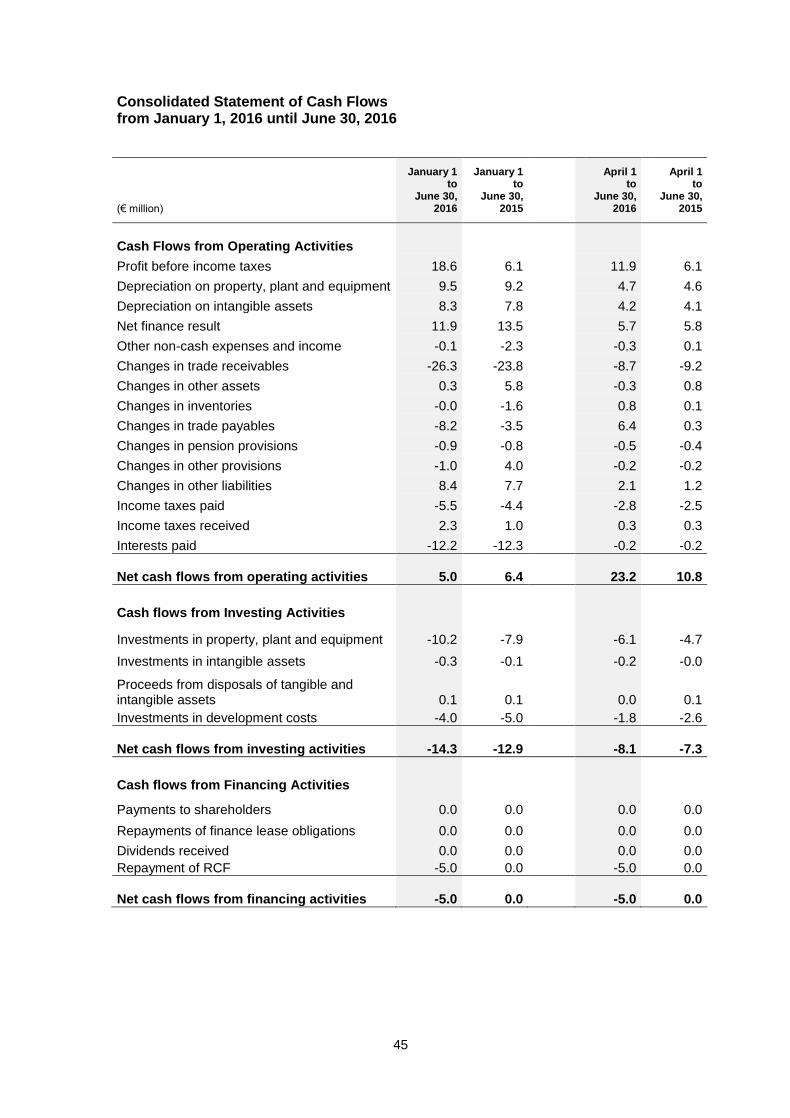

Consolidated Statement of Cash Flows

Holding

January 1

to June 30,

January 1

to June 30,

(€ million) 2015 2016 Change % Change

Cash Flows from Operating Activities

Profit before income taxes 6.1 18.6 12.5 >100.0%

Adjustments for

Depreciation and amortization 17.0 17.8 0.8 4.4%

Finance result 13.5 11.9 -1.6 -12.2%

Other non-cash expenses and income -2.3 -0.1 2.2 95.5%

Total adjustments 28.2 29.5 1.3 4.5%

Changes in Working Capital and Other Assets and Liabilities

Trade receivables -23.8 -26.3 -2.5 -10.4%

Other assets 5.8 0.3 -5.5 -95.1%

Inventories -1.6 -0.0 1.6 99.4%

Trade payables -3.5 -8.2 -4.7 >-100.0%

Total change in working capital -23.1 -34.2 -11.1 >-47.7%

Changes in pension provisions -0.8 -0.9 -0.2

-21.1%

Changes in provisions 4.0 -1.0 -4.9 >-100.0%

Changes in other liabilities 7.7 8.4 0.7 9.3%

Total change in working capital and other assets and liabilities -12.2 -27.7 -15.4

>-100.0%

Interests paid / received -12.3 -12.2 0.1 1.1%

Income taxes paid / received -3.4 -3.2 0.1 4.4%

Net cash flows from operating activities 6.4 5.0 -1.4

-22.1%

Cash Flows from Investing Activities

Investments in property, plant and equipment -7.9 -10.2 -2.3

-29.1%

Investments in intangible assets -0.1 -0.3 -0.2 >-100.0%

Proceeds from disposals of tangible and intangible assets 0.1 0.1 -0.0

-22.9%

Investments in development costs -5.0 -4.0 1.0 20.6%

Net cash flows from investing activities -12.9 -14.3 -1.5

-11.4%

21

Holding

January 1

to June 30,

January 1

to June 30,

(€ million) 2015 2016 Change % Change

Cash Flows from Financing Activities

Payments to shareholders 0.0 0.0 0.0 0.0%

Repayments of finance lease obligations 0.0 0.0 0.0 0.0%

Dividends received 0.0 0.0 0.0 0.0%

Repayment of RCF 0.0 -5.0 -5.0 N/A

Net cash flows from financing activities 0.0 -5.0 -5.0 N/A

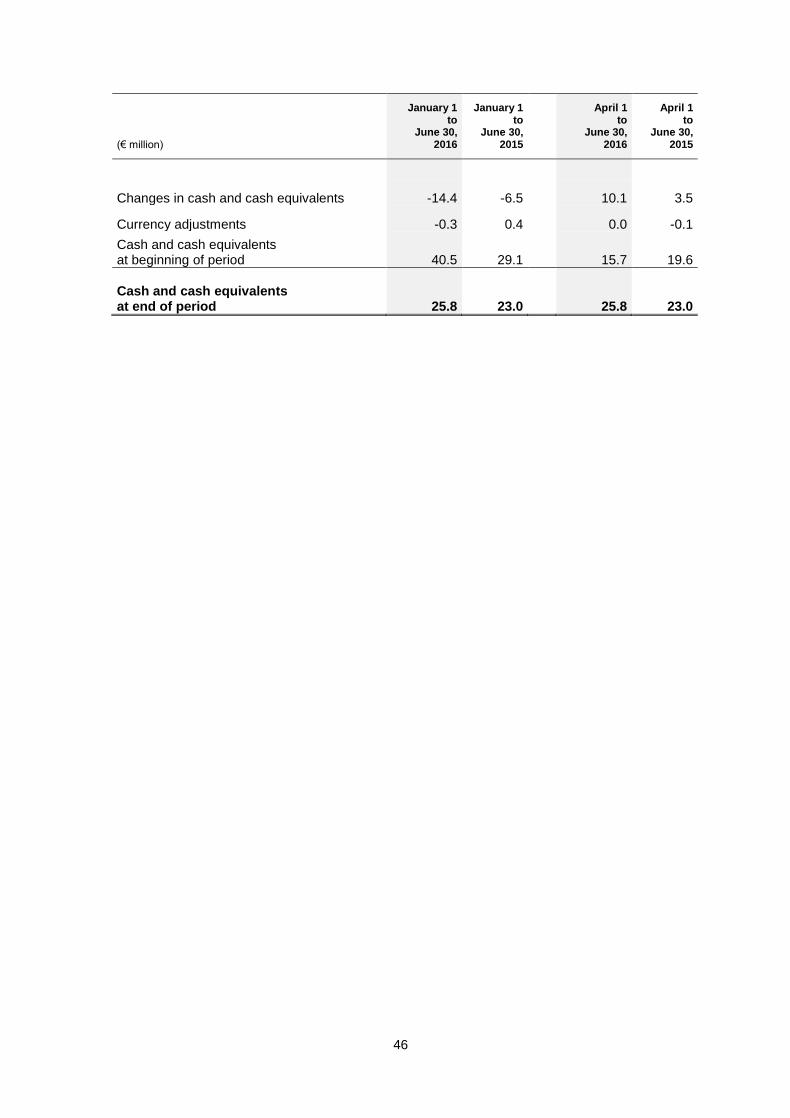

Changes in cash and cash equivalents -6.5 -14.4 -7.9 >-100.0%

Currency adjustments 0.4 -0.3 -0.7 >-100.0%

Cash and cash equivalents at beginning of the period 29.1 40.5 11.4

39.3%

Cash and cash equivalents at end of period 23.0 25.8 2.9

12.4%

Cash Flows from Operating Activities

Cash flows from operating activities for the six months ended June 30, 2016 amounted to

a cash inflow of € 5.0 million compared to € 6.4 million in the previous year mainly due to higher

working capital resulting from increased sales as a result of our growing business and severance

payments for the production relocations in Europe and NAFTA.

Cash Flows from (used in) Investing Activities

Cash used in investing activities amounted to a cash outflow of € 14.3 million in the six months

ended June 30, 2016 compared to € 12.9 million in the six months ended June 30, 2015 due to

an increase of investments in property, plant and equipment.

Cash Flows from Financing Activities

We partially repaid our existing RCF in an amount of € 5.0 million in May 2016.

Cash and Cash Equivalents at end of period

Cash increased by € 2.9 million compared to previous year mainly due to increased profit and

growing business. The increase was partially offset by severance payments for the production

relocations in Europe and NAFTA. Furthermore we repaid a total of € 10.0 million of our existing

RCF including € 5.0 million in November 2015 and € 5.0 million in May 2016.

22

3. Consolidated Statement of Balance Sheet

Holding

(€ million)

December 31, 2015

June 30, 2016

Change

% Change

Non-Current Assets

Property, plant and equipment 110.3 110.4 0.2 0.2%

Shares in associated companies and joint ventures 4.3 3.8 -0.5 -12.6%

Other assets 0.5 0.4 -0.1 -15.4%

Goodwill 97.5 97.5 0.0 0.0%

Other intangible assets 121.7 118.5 -3.2 -2.6%

Deferred tax assets 1.9 2.3 0.4 23.0%

Non-current assets 336.2 333.0 -3.2 -0.9%

Current Assets

Inventories 73.7 73.5 -0.2 -0.2%

Trade receivables 65.2 91.1 25.9 39.6%

Receivables shareholder 0.2 0.2 0.0 24.2%

Income tax receivables 3.9 1.7 -2.2 -56.6%

Other current assets 26.3 26.7 0.4 1.7%

Cash and cash equivalents 40.5 25.8 -14.7 -36.3%

Current assets 209.8 219.1 9.3 4.4%

Total assets 546.0 552.1 6.1 1.1%

Holding

(€ million)

December 31, 2015

June 30, 2016

Change

% Change

Equity

Share capital 0.0 0.0 0.0 0.0%

Capital reserve 90.6 90.6 0.0 0.0%

Currency translation reserve -1.4 -3.2 -1.8 >-100.0%

Retained earnings -19.1 -21.1 -2.0 -10.3%

Net result for the period 6.7 12.4 5.7 84.3%

Total equity 76.8 78.7 1.9 2.5%

Liabilities

Non-Current Liabilities

Notes 255.1 255.9 0.7 0.3%

Pension provisions 66.0 78.2 12.1 18.3%

Provisions 2.3 1.9 -0.5 -19.4%

Other liabilities 0.7 0.4 -0.3 -41.2%

Deferred tax liabilities 27.5 22.6 -4.9 -17.7%

Non-current liabilities 351.7 358.9 7.2 2.1%

23

Holding

(€ million)

December 31, 2015

June 30, 2016

Change

% Change

Current Liabilities

Other financial liabilities 8.1 3.4 -4.7 -58.4%

Trade payables 45.4 36.9 -8.5 -18.7%

Pension provisions 1.8 1.7 -0.1 -7.1%

Provisions 19.4 18.9 -0.5 -2.6%

Other current liabilities 41.0 49.3 8.3 20.3%

Current income tax liabilities 1.8 4.3 2.5 >100.0%

Current liabilities 117.5 114.5 -3.1 -2.6%

Total liabilities 469.2 473.4 4.2 0.9%

Total equity and liabilities 546.0 552.1 6.1 1.1%

Property, Plant and Equipment

Property, plant and equipment increased by € 0.2 million, or 0.2%, to € 110.4 million as of

June 30, 2016 from € 110.3 million as of December 31, 2015 due to investments exceeding

depreciation.

Intangible Assets

Intangible assets decreased by € 3.2 million, or 1.5%, to € 216.1 million as of June 30, 2016 from

€ 219.3 million as of December 31, 2015. This decrease was mainly due to the amortization of

the purchase price allocation for the acquisition of the Holding.

Inventories

Inventories decreased by € 0.2 million, or 0.2%, to € 73.5 million as of June 30, 2016 from

€ 73.7 million as of December 31, 2015. This decrease resulted from seasonal effects. See also

“Capitalization, liquidity and other financials – Trade Working Capital" (Note 4).

Trade Receivables

Trade receivables increased by € 25.9 million, or 39.6%, to € 91.1 million as of June 30, 2016

from € 65.2 million as of December 31, 2015 due to low levels of sales and trade receivables in

December 2015 as well as growing business in 2016. See also “Capitalization, liquidity and other

financials – Trade Working Capital" (Note 4).

Income Tax Receivables

Income tax receivables decreased by € 2.2 million, or 56.6%, to € 1.7 million as of June 30, 2016

from € 3.9 million as of December 31, 2015 due to tax reimbursement for 2014.

Equity

Equity increased by € 1.9 million, or 2.5%, to € 78.7 million as of June 30, 2016 from

€ 76.8 million as of December 31, 2015. The positive net result in first half year 2016 was partly

offset by negative foreign currency translation effects as well as actuarial losses on defined

benefit pension plans.

24

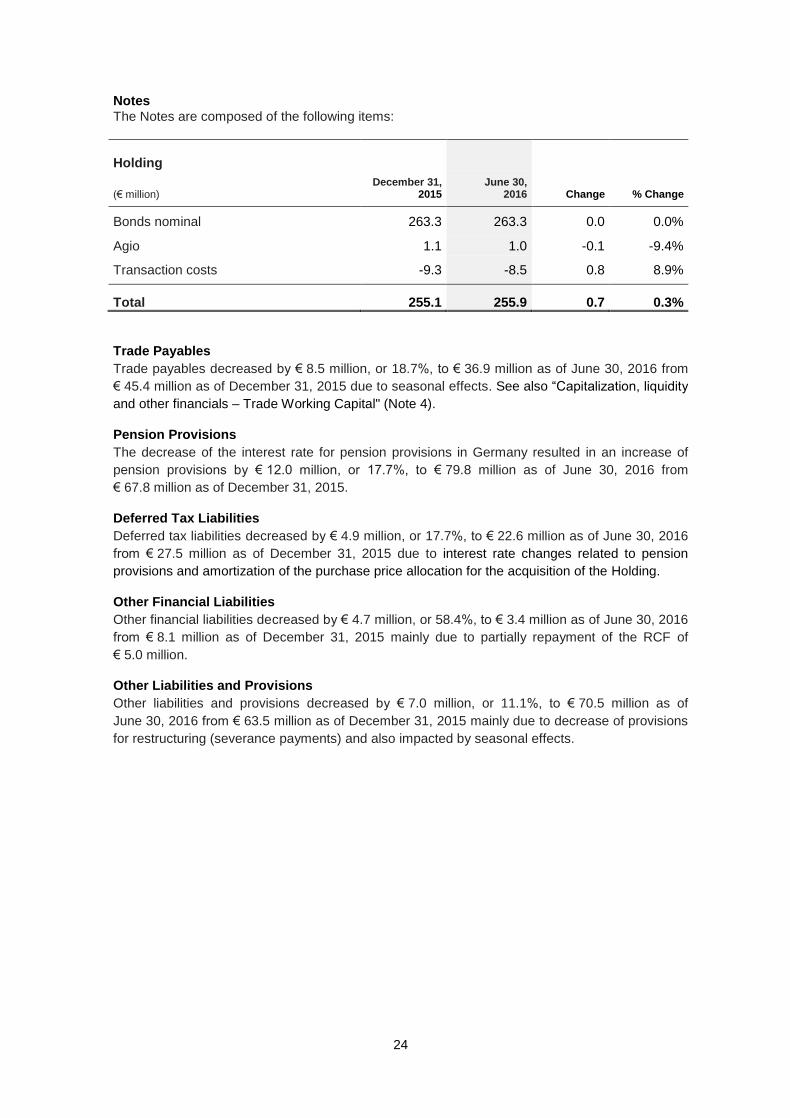

Notes

The Notes are composed of the following items:

Holding

(€ million)

December 31, 2015

June 30, 2016

Change

% Change

Bonds nominal 263.3 263.3 0.0 0.0%

Agio 1.1 1.0 -0.1 -9.4%

Transaction costs -9.3 -8.5 0.8 8.9%

Total 255.1 255.9 0.7 0.3%

Trade Payables

Trade payables decreased by € 8.5 million, or 18.7%, to € 36.9 million as of June 30, 2016 from

€ 45.4 million as of December 31, 2015 due to seasonal effects. See also “Capitalization, liquidity

and other financials – Trade Working Capital" (Note 4).

Pension Provisions

The decrease of the interest rate for pension provisions in Germany resulted in an increase of

pension provisions by € 12.0 million, or 17.7%, to € 79.8 million as of June 30, 2016 from

€ 67.8 million as of December 31, 2015.

Deferred Tax Liabilities

Deferred tax liabilities decreased by € 4.9 million, or 17.7%, to € 22.6 million as of June 30, 2016

from € 27.5 million as of December 31, 2015 due to interest rate changes related to pension

provisions and amortization of the purchase price allocation for the acquisition of the Holding.

Other Financial Liabilities

Other financial liabilities decreased by € 4.7 million, or 58.4%, to € 3.4 million as of June 30, 2016

from € 8.1 million as of December 31, 2015 mainly due to partially repayment of the RCF of

€ 5.0 million.

Other Liabilities and Provisions

Other liabilities and provisions decreased by € 7.0 million, or 11.1%, to € 70.5 million as of

June 30, 2016 from € 63.5 million as of December 31, 2015 mainly due to decrease of provisions

for restructuring (severance payments) and also impacted by seasonal effects.

25

4. Capitalization, liquidity and other financial data Liquidity

Our principal source of liquidity is, in general, our operating cash flow. The ability to generate

cash from our operations depends on our future operating performance, which is in turn

dependent, to some extent, on general economic, financial, competitive, market, regulatory and

other factors, many of which are beyond our control.

Our long-term indebtedness primarily consists of the Notes. The amounts available under the

Revolving Credit Facility are subject to our compliance with certain conditions, including certain

financial maintenance ratios.

Although we believe that our expected cash flows from operations, together with available

borrowings and cash on hand, will be adequate to meet our anticipated liquidity and debt service

needs, we cannot assure that our business will generate sufficient cash flows from operations or

that future debt and equity financing will be available to us in an amount sufficient to enable us to

pay our debts when due, including the Notes, or to fund our other liquidity needs.

We believe that the potential risks to our liquidity include:

a reduction in operating cash flows due to a decrease of operating profit from our

operations, which could be the result of a downturn in our performance or in the industry

as a whole;

the failure or delay of our customers to make payments due to us;

a failure to maintain working capital requirements; and

the need to fund expansion and other development capital expenditures.

If our future cash flows from operations and other capital resources (including borrowings under

our current or any future credit facility) are insufficient to pay our obligations as they mature or to

fund our liquidity needs, we may be forced to:

reduce or delay our business activities and capital expenditures;

sell our assets;

obtain additional debt or equity financing; or

restructure or refinance all or a portion of our debt, including the Notes, on or before

maturity.

We cannot assure you that we would be able to accomplish any of these alternatives on a timely

basis or on satisfactory terms, if at all. In addition, the terms of the Notes and any future debt may

limit our ability to pursue any of these alternatives.

Available Sources of Liquidity

Our principal sources of liquidity in the medium term are cash provided by operations and cash

from our short- and long-term borrowings.

26

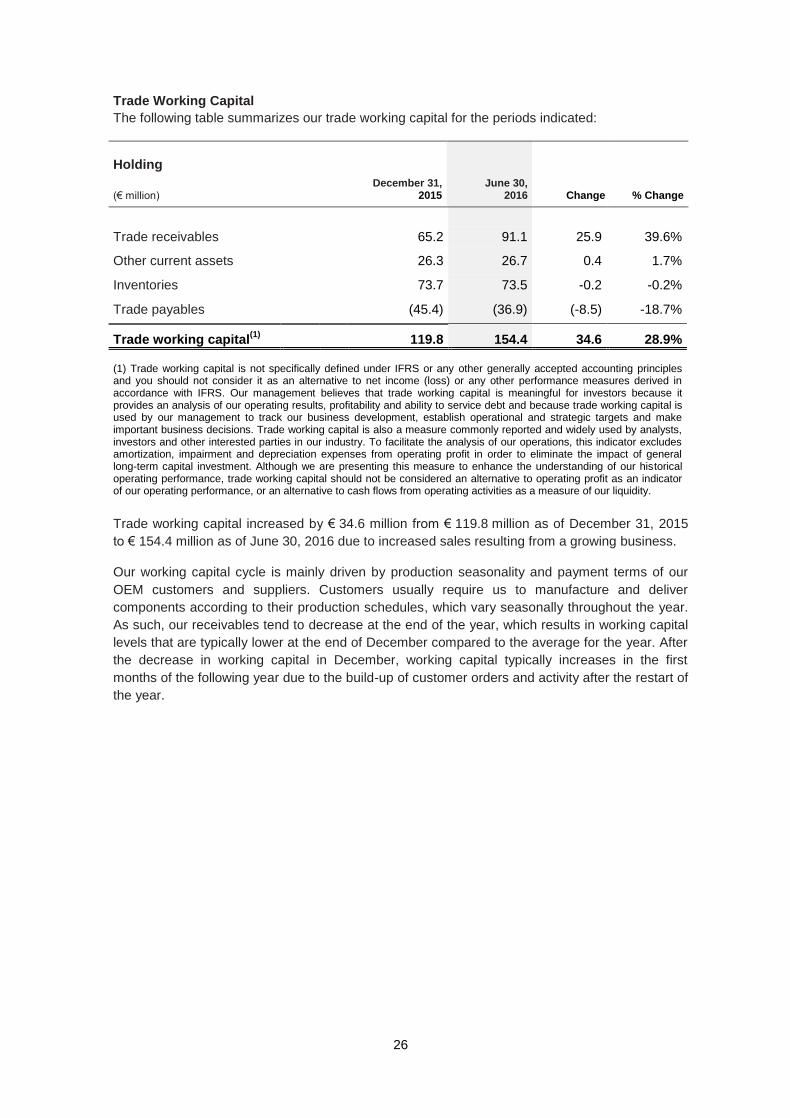

Trade Working Capital

The following table summarizes our trade working capital for the periods indicated:

Holding

(€ million)

December 31, 2015

June 30, 2016

Change

% Change

Trade receivables

65.2 91.1 25.9 39.6%

Other current assets

26.3 26.7 0.4 1.7%

Inventories

73.7 73.5 -0.2 -0.2%

Trade payables

(45.4) (36.9) (-8.5) -18.7%

Trade working capital(1)

119.8 154.4 34.6 28.9%

(1) Trade working capital is not specifically defined under IFRS or any other generally accepted accounting principles and you should not consider it as an alternative to net income (loss) or any other performance measures derived in accordance with IFRS. Our management believes that trade working capital is meaningful for investors because it provides an analysis of our operating results, profitability and ability to service debt and because trade working capital is used by our management to track our business development, establish operational and strategic targets and make important business decisions. Trade working capital is also a measure commonly reported and widely used by analysts, investors and other interested parties in our industry. To facilitate the analysis of our operations, this indicator excludes amortization, impairment and depreciation expenses from operating profit in order to eliminate the impact of general long-term capital investment. Although we are presenting this measure to enhance the understanding of our historical operating performance, trade working capital should not be considered an alternative to operating profit as an indicator of our operating performance, or an alternative to cash flows from operating activities as a measure of our liquidity.

Trade working capital increased by € 34.6 million from € 119.8 million as of December 31, 2015

to € 154.4 million as of June 30, 2016 due to increased sales resulting from a growing business.

Our working capital cycle is mainly driven by production seasonality and payment terms of our

OEM customers and suppliers. Customers usually require us to manufacture and deliver

components according to their production schedules, which vary seasonally throughout the year.

As such, our receivables tend to decrease at the end of the year, which results in working capital

levels that are typically lower at the end of December compared to the average for the year. After

the decrease in working capital in December, working capital typically increases in the first

months of the following year due to the build-up of customer orders and activity after the restart of

the year.

27

LTM Adjusted EBITDA

As of June 30, 2016, LTM Adjusted EBITDA amounted to € 92.3 million and net financial debt

amounted to € 242.5 million. This resulted in a ratio of net financial debt to LTM Adjusted EBITDA

of 2.63.

Holding

twelve

months ended

June 30,

twelve

months ended

September 30,

twelve

months ended

December 31,

twelve

months ended March

31,

twelve

months ended

June 30,

Change June

to March

(€ million) 2015 2015 2015 2016 2016 Change % Change

Net financial debt(1) (3)

255.3 255.5 232.8 257.6 242.5 -15.1 -5.9%

LTM Adjusted EBITDA

(2)(3) 79.7 83.1 86.8 87.9 92.3 4.3 4.9%

Ratio of net financial debt to LTM Adjusted EBITDA 3.20 3.07 2.68 2.93 2.63 -0.30 -10.3%

(1) Represents the amount of the Notes minus the amount of cash available. (2) Adjusted EBITDA represents EBITDA as adjusted for certain infrequent charges and nonoperational costs identified. (3) Net financial debt and LTM Adjusted EBITDA are not specifically defined under IFRS or any other generally accepted accounting principles and you should not consider them as an alternative to net income (loss) or any other performance measures derived in accordance with IFRS. Our management believes that net financial debt and LTM Adjusted EBITDA are meaningful for investors because they provide an analysis of our operating results, profitability and ability to service debt and because net financial debt and LTM Adjusted EBITDA are used by our management to track our business development, establish operational and strategic targets and make important business decisions. Net financial debt and LTM Adjusted EBITDA are also measures commonly reported and widely used by analysts, investors and other interested parties in our industry. To facilitate the analysis of our operations, these indicators exclude amortization, impairment and depreciation expenses from operating profit in order to eliminate the impact of general long-term capital investment. Although we are presenting these measures to enhance the understanding of our historical operating performance, net financial debt and LTM Adjusted EBITDA should not be considered an alternative to operating profit as indicators of our operating performance, or as alternatives to cash flows from operating activities as measures of our liquidity.

28

Gross Total Capital Expenditure

The following table sets forth our gross total capital expenditure for the periods indicated:

Holding

January 1 to

January 1

to

(€ million)

June 30, 2015

June 30, 2016

Change

% Change

Gross total capital expenditure (1)

12.9 14.3 1.5 11.4%

(1) Gross total capital expenditure is not specifically defined under IFRS or any other generally accepted accounting principles and you should not consider it as an alternative to net income (loss) or any other performance measures derived in accordance with IFRS. Our management believes that gross total capital expenditure is meaningful for investors because it provides an analysis of our operating results, profitability and ability to service debt and because gross total capital expenditure is used by our management to track our business development, establish operational and strategic targets and make important business decisions. Gross total capital expenditure is also a measure commonly reported and widely used by analysts, investors and other interested parties in our industry. To facilitate the analysis of our operations, this indicator excludes amortization, impairment and depreciation expenses from operating profit in order to eliminate the impact of general long-term capital investment. Although we are presenting this measure to enhance the understanding of our historical operating performance, gross total capital expenditure should not be considered an alternative to operating profit as an indicator of our operating performance, or an alternative to cash flows from operating activities as a measure of our liquidity.

Gross total capital expenditure increased by € 1.5 million, or 11.4%, to € 14.3 million in the six

months ended June 30, 2016 from € 12.9 million in the six months ended June 30, 2015 due to

increased investments, particularly in connection with our new Electric Shift Transmission (EST)

and Electric Pump Transmission (EPT) projects.

29

5. Changes in material debt instruments Changes in material debt instruments

Based on the agreement, dated June 2, 2016, between Bain Capital Private Equity and Valeo

Group it is our understanding that the Valeo Group intends to redeem the Notes on or about the

closing date of the acquisition. Any redemption will be within the buyer’s discretion (subject to the

terms of the identure).

6. Subsequent events and material changes to risk factors Subsequent events

No event with material impact on the unaudited financials occurred after the reporting date.

Material changes to risk factors

We are not aware of any material changes to the risk factors disclosed in the most recent

consolidated financial statements of the Holding for the period ended June 30, 2016.

30

7. Summary of significant accounting policies Financial information

A. Principles and methods

The consolidated interim financial statements of the Holding as of June 30, 2016 are prepared in

accordance with the International Financial Reporting Standards in effect and to be mandatorily

applied as of the balance sheet date; particularly the requirements of IAS 34 relating to interim

financial reporting were applied.

B. Consolidated companies and principles of consolidation

The consolidated interim financial statements as of June 30, 2016 include the interim financial

statements of the Parent and its subsidiaries.

The following table shows the list of consolidated entities and the interests held by the Group:

Subsidiary Location Country Share

FTE Verwaltungs GmbH

FTE automotive GmbH

Ebern

Ebern

Germany

Germany

100 %

100 %

FTE automotive systems GmbH Fischbach Germany 100 %

FTE automotive Möve GmbH Mühlhausen Germany 100 %

FTE Asia GmbH Ebern Germany 100 %

FTE automotive Slovakia s.r.o. Presov Slovakia 100 %

SFMC s.r.o. (until March 31, 2016) Presov Slovakia 100 %

FTE automotive France S.a.r.l. Nanterre Cedex France 100 %

FTE automotive Czechia s.r.o. Podborany Czech Republic 100 %

FTE automotive UK Limited Coventry Great Britain 100 %

FTE automotive Denmark ApS Stoevring Denmark 100 %

FTE Indústria e Comércio Ltda. Maua Brazil 100 %

FTE automotive USA Inc. Auburn Hills USA 100 %

FTE automotive North America Inc. Auburn Hills USA 100 %

FTE Mexicana S.A. de C.V. Puebla Mexico 100 %

FTE automotive (Taicang) Co. Ltd. Taicang China 100 %

On April 1, 2016 SFMC s.r.o. was merged into FTE automotive Slovakia s.r.o.

Companies over which FTE Holding GmbH can execute joint control are either included in the

consolidated financial statements with the proportionate assets, liabilities, earnings & expenses or

measured according to the equity method, depending on their type. In the absence of other

contractual agreements, a majority of the voting rights generally takes control. If the voting rights

are distributed equally, joint control generally results unless other (contractual) rights result in

control by the shareholder.

Associates on which FTE Holding GmbH can execute material influence within the meaning of

IAS are also measured according to the equity method. Significant influence is generally deemed

to exist if FTE is directly or indirectly entitled to a voting rights interest of at least 20%, but less

than 50%.

31

Associates are aggregated as equity-accounted investments.

Associated companies Headquarters Country Interest

APG-FTE automotive Co. Ltd Hangzhou China 49%

The financial year of FTE Holding GmbH ends on 31 December 2015. The reporting date for the

separate financial statements of the Group companies that are included in the scope of

consolidation is the same as the reporting date for the consolidated financial statements.

For consolidation purposes, the consolidated financial statements of FTE Holding GmbH were

prepared on the basis of uniform accounting principles pursuant to IFRS 10.

The consolidation of a portfolio company commences on the day on which the investor obtains

control over the company. It ends when the investor relinquishes control over the portfolio

company.

In case of a step merger, the previously-acquired equity share of the company is redetermined

using the fair value valid when the acquisition took place. The resulting profit or loss is to be

recorded in the income statement.

Interests in subsidiaries

Capital consolidation is performed by applying the purchase method pursuant to IFRS 3

(Business Combinations).

The purchase costs for the acquisition correspond to the fair value of the transferred assets, the

issued equity capital instruments, and the liabilities that arise or are transferred on the transaction

date. Incidental acquisition costs are expensed. Upon first consolidation, assets, liabilities and

contingent liabilities identified as part of a merger are generally valued at their fair value on the

date of acquisition, irrespective of the extent of the minority shares. The excess of the acquisition

costs over the Group's share in the net assets measured at fair value is recognized as goodwill. If

the acquisition costs are less than the fair value of the acquired identifiable assets and liabilities,

the difference is reported directly in the consolidated income statement. Acquisition costs are

expensed.

All receivables and liabilities, revenues, expenses and income, as well as intragroup profits and

losses between the companies included in the consolidated financial statements are eliminated

as part of consolidation.

These companies' financial statements are included by way of full consolidation.

Equity-accounted investments The shares in associated companies are balanced using the equity method and initially carried at

their acquisition cost. The Group’s share in associated companies includes the goodwill arising

upon acquisition. In subsequent periods, the acquisition costs are carried forward to include the

proportion of net assets attributable to the FTE Group.

This entails increasing or decreasing the carrying amounts annually by the proportional net profits

and losses, dividends distributed, and other equity changes. Impairment losses are applied to

equity accounted investments if their recoverable amounts are less than their carrying amounts.

Profits that require elimination arising from transactions with associates are offset against the

participating interest's carrying amount through profit or loss.

32

Currency translation

Functional currency

The items in the annual financial statements of each Group subsidiary are carried with the

currency that best reflects the economic content of the underlying business transactions and

circumstances relevant to the Company (functional currency). All transactions denominated in a

currency other than the functional currency are regarded as foreign currency transactions.

The consolidated financial statements are prepared in Euros, the functional currency of FTE

Holding GmbH. The annual financial statements of foreign subsidiaries with functional currencies

other than the Euro are translated in the consolidated financial statements into the Group

currency of the Euro according to the modified balance sheet date rate method on the basis of

the functional currency concept pursuant to IAS 21 (The Effects of Changes in Foreign Exchange

Rates).

Accounting for business transactions

Foreign currency transactions are translated into the functional currency by applying the rates

prevailing on the transaction date. Currency gains and losses arising from the settlement of such

business transactions and from the currency translation of monetary assets and liabilities are

reported in the consolidated income statement.

Group companies

Assets and liabilities of foreign Group companies with functional currencies other than the Euro

are translated at the exchange rate prevailing on the balance sheet date (reporting date rate),

while average exchange rates are applied to the translation of the consolidated income

statement.

The difference arising from the currency translation is recognized directly in equity under the

"foreign currency translation reserve" item.

Currency differences arising compared to the previous year's translation, or from the translation

as of the first-time consolidation date within the FTE Group, are also recognized directly in equity

under the "foreign currency translation reserve" item.

C. Accounting policies

(1) Revenue recognition The revenues are generated mainly from the sale of goods. Pursuant to IAS 18, these revenues

are reported excluding value added tax, and after deducting price reductions such as customer

rebates and price discounts. Revenue from the sale of goods is recognized if the significant risks

and opportunities connected with the asset's ownership have transferred to the buyer.

License income is recognized on an accrual basis in line with the underlying contract. Interest

income is reported pro rata temporis on the basis of outstanding amounts and effective interest

until the maturity date, if it is ascertained that such income is likely to be received. Dividend

income is reported when the legal entitlement to payment arises.

(2) Cost of sales Cost of sales comprises costs that have been incurred to produce and acquire merchandise to

the extent that such merchandise has been sold. It comprises all costs of sales reported for

revenue recognition.

33

(3) Balance sheet structure Pursuant to IAS 1.66, assets are classified as current if

the realization of the asset is expected within the normal business cycle, or the asset is held for

sale within this period,

the asset is primarily held for trading purposes,

the realization of the asset is expected within twelve months after the balance sheet date, or

it is in cash or cash equivalents, unless the exchange or utilization of the asset is restricted to

the purpose of fulfilling an obligation for a period of at least twelve months after the balance

sheet date.

All other assets are classified as non-current.

Pursuant to IAS 1.69, liabilities are classified as current if

the liabilities are expected to be settled within the normal business cycle,

the liabilities are primarily held for trading purposes,

the liabilities are expected to be settled within twelve months of the balance sheet date, or

the company does not have an unlimited right to postpone the settlement of the liability by at

least twelve months after the balance sheet date. If the liability is associated with terms and

conditions that allow it to be settled by issuing equity capital instruments thanks to a

counterparty option, this does not affect its classification.

All other liabilities are classified as non-current.

Claims and obligations arising from deferred taxes are generally reported as non-current assets

or liabilities. If assets and liabilities comprise both current and non-current components, they are

divided into their maturity components and reported as current and non-current assets or

liabilities according to the balance sheet structure.

(4) Property, plant, and equipment Property, plant and equipment are reported at cost less depreciation based on the estimated

normal useful operating lives of the assets. The revaluation method pursuant to IAS 16.31 - 42 is

not applied.

Along with costs directly attributable to the production process, costs for self-produced property,

plant, and equipment comprise an appropriate proportion of production-related overhead costs.

These include production-related depreciation and impairment losses, and an appropriate portion

of administrative and social costs. Borrowing costs are not reported, as no qualified assets exist.

Depreciation is applied straight-line in accordance with prospective useful economic lives:

Useful life

Years

Buildings 25-50 years

Improvements to buildings 3-10 years

Equipment and machinery 6-15 years

Furniture and office equipment and vehicle fleet 3-10 years

34

Land is not appreciated. Property, plant, and equipment with a cost of between € 150 and € 1,000

(low-cost assets) are written off fully in the year of purchase and reported correspondingly as

asset additions and as depreciation in the analysis of non-current assets.

Disposal gains and losses are calculated by comparing sales proceeds with the corresponding

carrying amounts, and reported through profit or loss.

Repair and maintenance expenses are expensed in the period in which they occur. Costs for

major repairs and maintenance are allocated to the asset's carrying amount if the recognition

criteria for property, plant and equipment are satisfied. Major repairs are depreciated over the

residual useful life of the related assets. Carrying amounts of previous repairs and maintenance

work are derecognized. The same accounting treatment is applied if assets need to be replaced

at regular intervals.

Carrying amounts, normal operating useful lives, and depreciation methods are reviewed

annually pursuant to IAS 16.51 and 16.61.

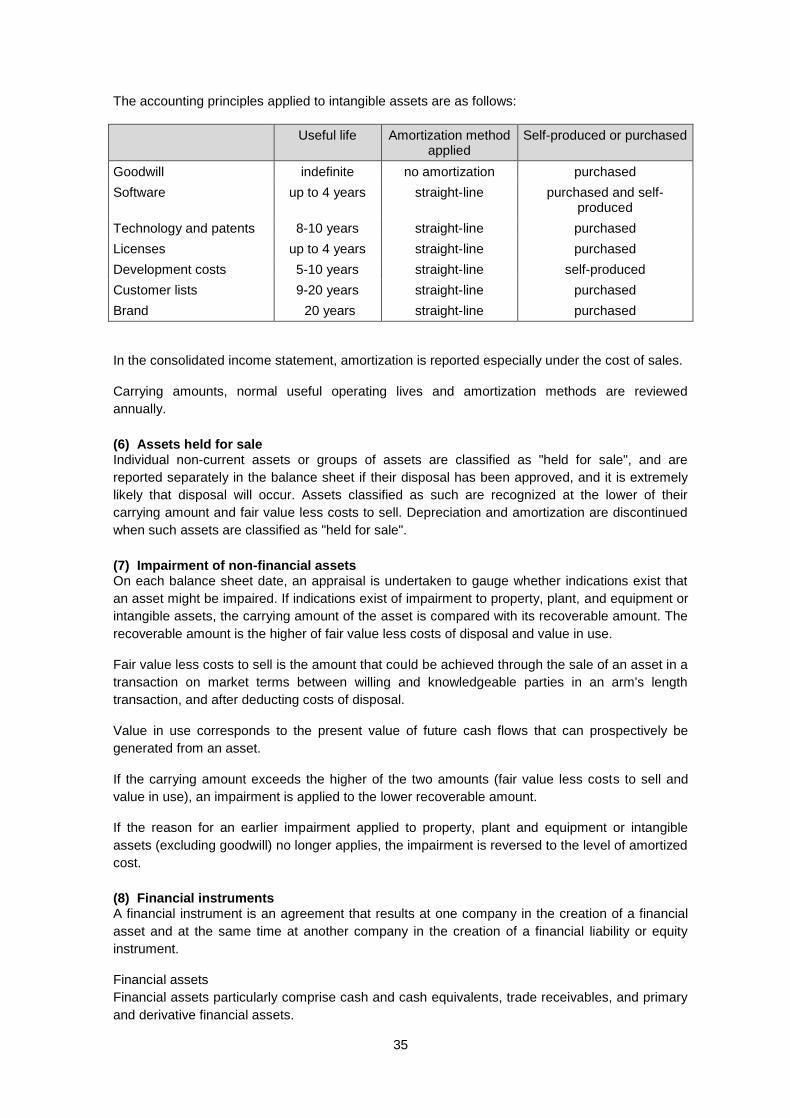

(5) Intangible assets Intangible assets comprise goodwill, customer lists, brands, technology, patents, software,

licenses and similar rights, as well as self-produced intangible assets deriving from development.

Goodwill

Purchased goodwill is capitalized and tested at least annually for impairment pursuant to IAS 36,

and whenever indications of impairment exist (so-called "triggering events"). Goodwill is tested for

impairment in a single-step process at the level of the cash-generating units, or groups of cash-

generating units to which it is allocated.

This entails comparing the carrying amount of the cash-generating unit to its recoverable amount.

If the carrying amount exceeds the recoverable amount, an impairment exists, and the goodwill is

written down to the recoverable amount.

The recoverable amount of the cash-generating unit corresponds to the higher of fair value less

costs to sell and value in use.

Subsequent reversals to goodwill impairment losses are not permitted if the reasons for previous

impairment no longer apply.

Development costs

Research costs are not capitalized but are instead expensed in the period in which they are

incurred pursuant to IAS 38.

Development costs are capitalized if the IAS 38 recognition criteria have been satisfied. After first-

time capitalization, the asset is carried at cost less cumulative amortization and cumulative

impairment losses. Capitalized development costs include all directly attributable specific costs,

proportional overhead costs, and borrowing costs pursuant to IAS 23, and are amortized over the

budgeted product life-cycle.

Other intangible assets Intangible assets with finite normal useful operating lives are capitalized according to the

purchase cost principle pursuant to IAS 38, and amortized straight-line over their normal

operating useful lives

By contrast, intangible assets with indeterminate useful lives cannot be amortized. Borrowing

costs for intangible assets whose production requires a considerable period of time (qualified

asset), and which can be directly attributable to the production of these assets, are capitalized

under the preconditions of IAS 23.

35

The accounting principles applied to intangible assets are as follows:

Useful life Amortization method applied

Self-produced or purchased

Goodwill indefinite no amortization purchased

Software up to 4 years straight-line purchased and self-produced

Technology and patents 8-10 years straight-line purchased

Licenses up to 4 years straight-line purchased

Development costs 5-10 years straight-line self-produced

Customer lists 9-20 years straight-line purchased

Brand 20 years straight-line purchased

In the consolidated income statement, amortization is reported especially under the cost of sales.

Carrying amounts, normal useful operating lives and amortization methods are reviewed

annually.

(6) Assets held for sale Individual non-current assets or groups of assets are classified as "held for sale", and are

reported separately in the balance sheet if their disposal has been approved, and it is extremely

likely that disposal will occur. Assets classified as such are recognized at the lower of their

carrying amount and fair value less costs to sell. Depreciation and amortization are discontinued

when such assets are classified as "held for sale".

(7) Impairment of non-financial assets On each balance sheet date, an appraisal is undertaken to gauge whether indications exist that

an asset might be impaired. If indications exist of impairment to property, plant, and equipment or

intangible assets, the carrying amount of the asset is compared with its recoverable amount. The

recoverable amount is the higher of fair value less costs of disposal and value in use.

Fair value less costs to sell is the amount that could be achieved through the sale of an asset in a

transaction on market terms between willing and knowledgeable parties in an arm's length

transaction, and after deducting costs of disposal.

Value in use corresponds to the present value of future cash flows that can prospectively be

generated from an asset.

If the carrying amount exceeds the higher of the two amounts (fair value less costs to sell and

value in use), an impairment is applied to the lower recoverable amount.

If the reason for an earlier impairment applied to property, plant and equipment or intangible

assets (excluding goodwill) no longer applies, the impairment is reversed to the level of amortized

cost.

(8) Financial instruments A financial instrument is an agreement that results at one company in the creation of a financial

asset and at the same time at another company in the creation of a financial liability or equity

instrument.

Financial assets

Financial assets particularly comprise cash and cash equivalents, trade receivables, and primary

and derivative financial assets.

36

Financial liabilities