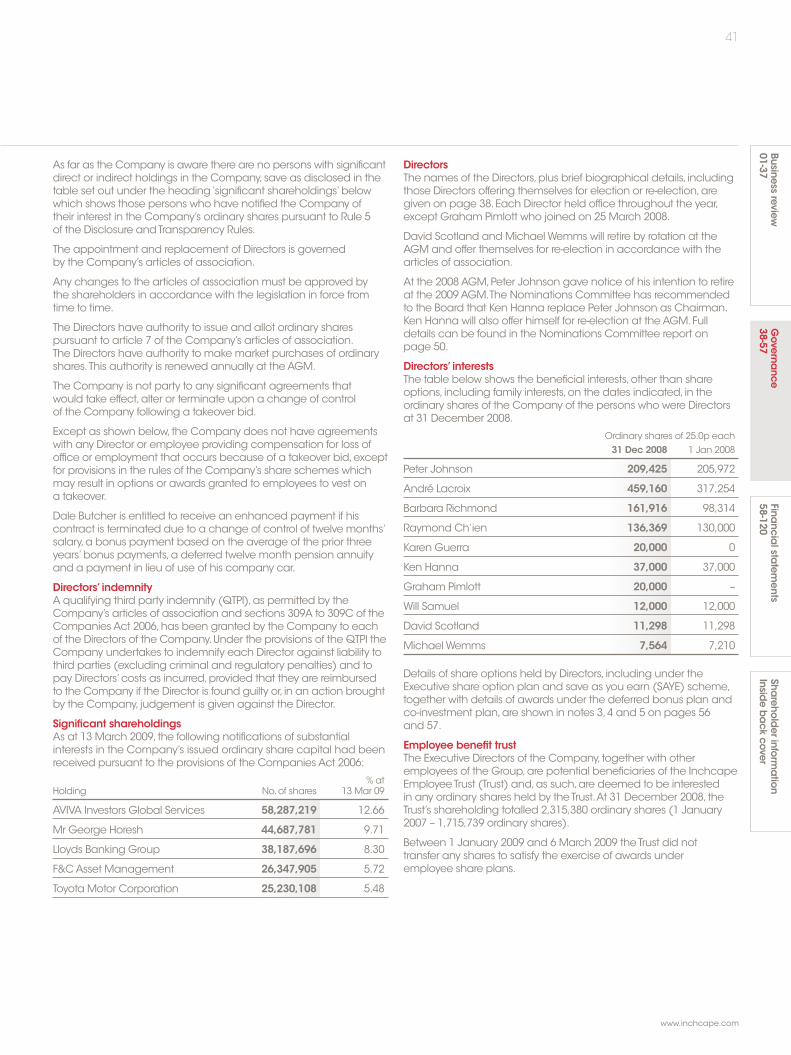

Financial highlights - inchcape.com · £2,340 .1m-13.8% Tradingprofit* £23 .1m-66.8% Sales £92...

124

Transcript of Financial highlights - inchcape.com · £2,340 .1m-13.8% Tradingprofit* £23 .1m-66.8% Sales £92...

Leading the way for over 160 yearsWe have chosen the Inchcape lighthouseas the symbol for this year’s annual reportbecause of the significance it holds –both for our Company’s founders andfor us today.

Our leading founder,James Lyle Mackay,was so inspired by the building of thelighthouse on the Inchcape Rock – a lethalsubmerged reef off the Scottish coast –that he took the title ‘Baron Inchcape ofStrathnaver’and so named the companythat he led.

From our Company’s earliest days as anintrepid trading pioneer to today’s statusas a leader in the highly competitiveautomotive industry, Inchcape has been abeacon of performance,even in the midstof the most disruptive economic storms.

Solid, responsive,confident, the qualities onwhich Inchcape was founded,are preciselythose that have seen the Company thriveand prosper throughmore than 160 oftenturbulent years.

As we face challenging times,we too areinspired by the Inchcape lighthouse.With itsrobust structure that stands strong againstthe North Sea and the pioneering spiritof those that built this lasting wonder of theindustrial age that even now continues tosave lives, its guiding light illuminates thejourney ahead.

ContentsBusiness review01-37

02 Our business at a glance04 Chairman’s statement06 Group Chief Executive’s review10 Focused on the fundamentals

– case studies16 Operating review16 Key performance indicators18 Group and regional reviews26 Financial review27 Principal business risk factors30 Corporate responsibility

Governance38-57

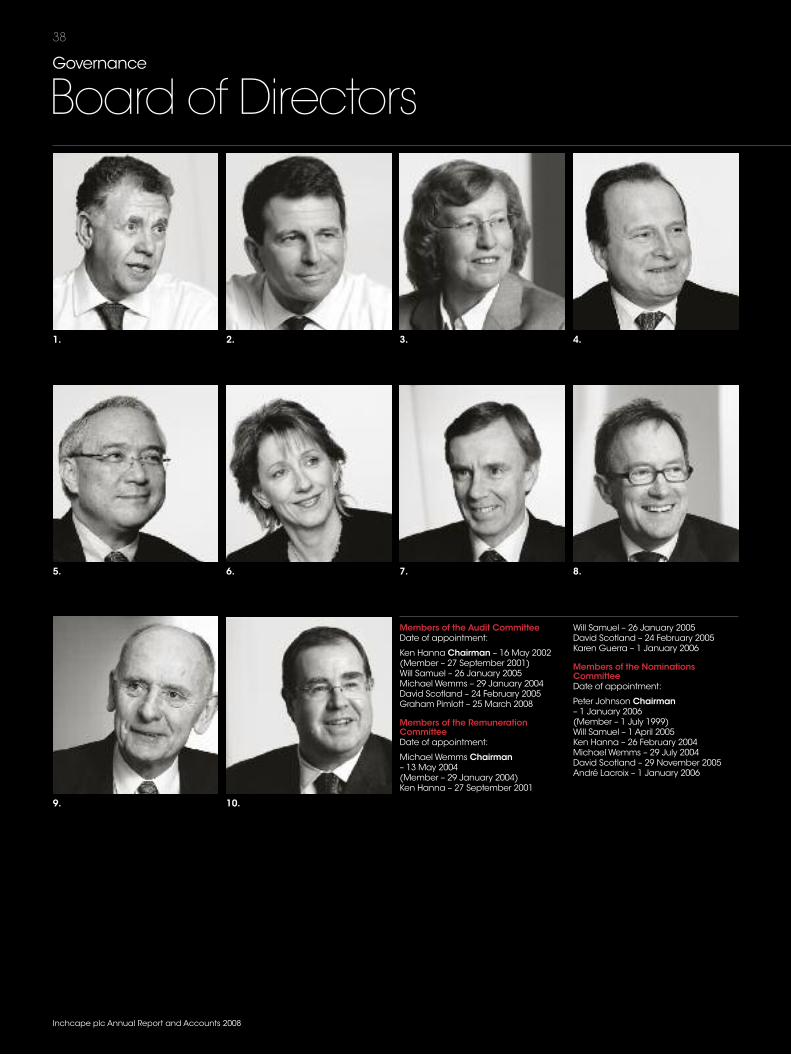

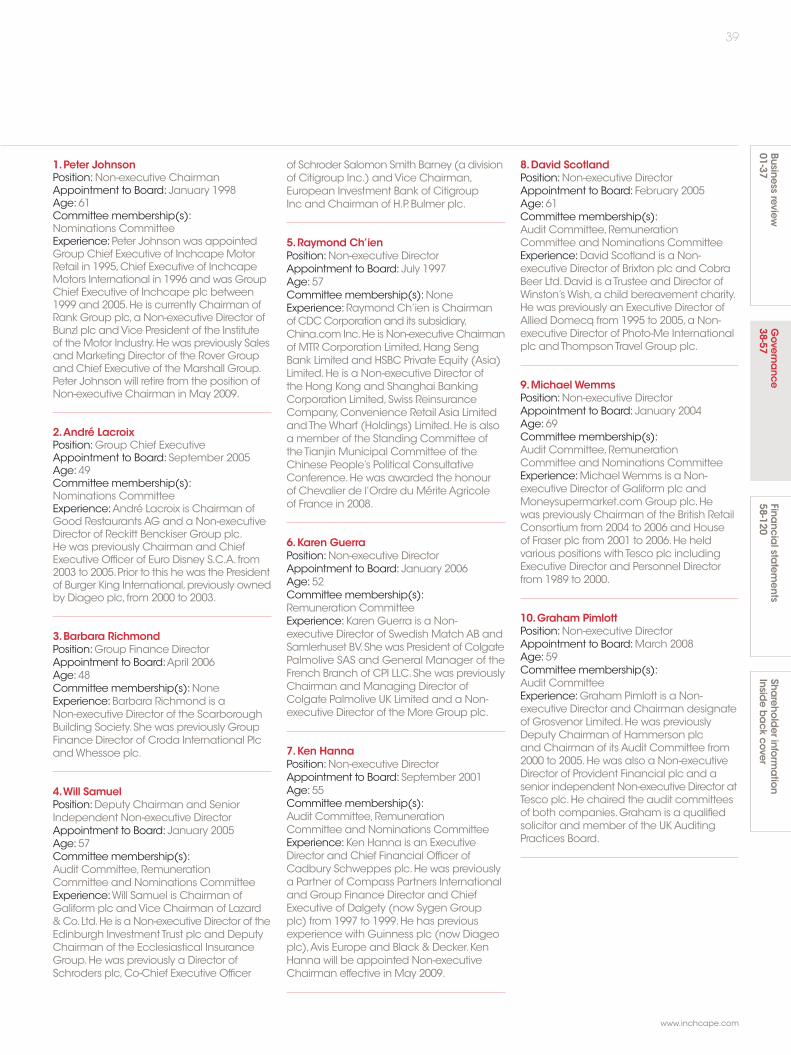

38 Board of Directors40 Directors’ report43 Executive Committee45 Corporate governance report51 Remuneration report

Financial statements58-120

Group financial statements58 Consolidated income statement59 Consolidated statement of

recognised income and expense60 Consolidated balance sheet61 Consolidated cash flow statement62 Accounting policies68 Notes to the accounts112 Five year record113 Report of theAuditors – Group

Company financial statements114 Company balance sheet115 Accounting policies116 Notes to the accounts120 Report of theAuditors – Company

Shareholder informationInside back cover

Company detailsFinancial calendar

Financial highlights

0807060504

Revenue

£6.3bn+3.4%

£4.1bn

£4.5bn

£4.8bn £6.1bn

£6.3bn

0807060504

Operating profitbefore exceptional items

£240.5m-9.2%

£172

.1m

£189

.4m

£213

.9m

£265

.0m

£240

.5m

0807060504

Profit before taxbefore exceptional items

£190.7m-18.9%

£168

.4m

£190

.3m

£213

.9m

£235

.1m

£190

.7m

0807060504

Adjusted earningsper sharebefore exceptional items

30.0p-18.9%

26.0

p

29.8

p 35.7

p

37.0

p

30.0

p

0807060504

Net assets

£1,019.6m+21.7%

£514

.7m

£591

.2m

£651

.0m

£837

.8m

£1,0

19.6

m

0807060504

Operating profit

£158.0m-41.5%

£161

.5m

£176

.4m

£213

.9m

£269

.9m

£158

.0m

0807060504

Profit before tax

£108.2m-54.9%

£163

.2m

£177

.3m

£213

.9m

£240

.0m

£108

.2m

0807060504

Earnings per share

11.2p-70.5%

24.8

p

27.0

p

37.5

p

38.0

p

11.2

p

Front cover image

1

www.inchcape.com

Businessreview

01-37Governa

nce38-57

Financia

lstatem

ents58-120

Shareho

lderinfo

rmation

Insidebackcover

Inchcape’s key strengths…Several factors combine to give Inchcape strength in theglobal automotive retail and distribution industry:

• An industry leader with a track record of growth andprudent governance.

• A proven and resilient business model with broad geographiccoverage across 26 mature and emerging markets,with scaleoperations and a leading position in 14 markets.

• Long-standing relationships with strong brand partners whohave a history of outperforming the market,providing accessto a pipeline of attractive new car models.

• A passionate and relentless focus on superior customer servicethat underpins a history of industry-leading performance.

• A proactive management team,with a blend of industryexpertise and blue-chip company experience,which hasresponded decisively to the rapid and unprecedenteddownturn in the automotive industry.

• Well positioned to benefit from opportunities when the marketrecovers – a leaner business with scale presence,broadgeographic spread,partnered with strong automotive brands.

As an industry leader,we see opportunity today as we buildthe platform to emerge even stronger tomorrow.

We are solid, responsive and confident.

André LacroixGroup Chief Executive

2

Inchcape plc Annual Report and Accounts 2008

Business review

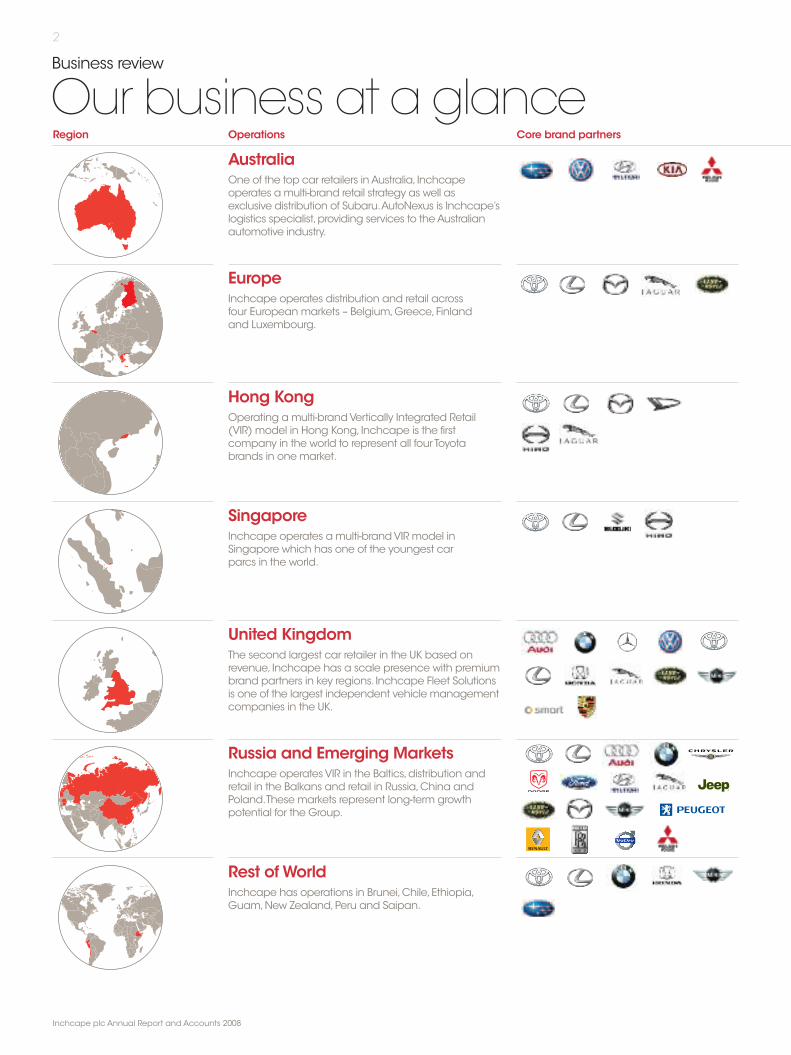

Our business at a glanceRegion Operations Core brand partners

One of the top car retailers inAustralia, Inchcapeoperates amulti-brand retail strategy as well asexclusive distribution of Subaru.AutoNexus is Inchcape’slogistics specialist,providing services to theAustralianautomotive industry.

Australia

Inchcape operates distribution and retail acrossfour Europeanmarkets – Belgium,Greece,Finlandand Luxembourg.

Europe

Operating amulti-brandVertically Integrated Retail(VIR) model in Hong Kong, Inchcape is the firstcompany in the world to represent all four Toyotabrands in one market.

Hong Kong

Inchcape operates a multi-brandVIR model inSingapore which has one of the youngest carparcs in the world.

Singapore

The second largest car retailer in the UK based onrevenue, Inchcape has a scale presence with premiumbrand partners in key regions. Inchcape Fleet Solutionsis one of the largest independent vehicle managementcompanies in the UK.

United Kingdom

Inchcape operatesVIR in the Baltics,distribution andretail in the Balkans and retail in Russia,China andPoland.These markets represent long-term growthpotential for the Group.

Russia and Emerging Markets

Inchcape has operations in Brunei,Chile,Ethiopia,Guam,New Zealand,Peru and Saipan.

Rest of World

3

www.inchcape.com

Businessreview

01-37Governa

nce38-57

Financia

lstatem

ents58-120

Shareho

lderinfo

rmation

Insidebackcover

Sales

£695.4m+5.8%

Financial highlights Contribution to Group profit

Trading profit*

£42.6m-2.7%

Sales

£1,229.2m+2.1%

Trading profit*

£40.6m-19.0%

Sales

£291.1m+20.5%

Trading profit*

£33.3m+17.7%

Sales

£484.4m+0.9%

Trading profit*

£57.0m+23.9%

Sales

£2,340.1m-13.8%

Trading profit*

£23.1m-66.8%

Sales

£929.0m+79.1%

Trading profit*

£22.5m-24.0%

Sales

£290.6m+20.3%

Trading profit*

£31.0m+23.5%

17.0%

16.2%

13.3%

22.8%

9.3%

9.0%

12.4%

*Trading profit is defined as operating profit before exceptional items and unallocated central costs.

Business review

Chairman’s statement4

Inchcape plc Annual Report and Accounts 2008Inchcape plc Annual Report and Accounts 2008

Despite the weakening trading conditionsin many markets around the world,weare pleased to report results for 2008 inline with our expectations, reflecting theprogress we have made against ourgrowth strategy and the benefits ofexcellent portfolio diversification.

PerformanceGroup sales have increased by 3.4% to£6.3bn for the full year to 31 December2008,benefiting from strategic and focusedacquisitions and from organic sales growthin most of our markets.On a like for like,constant currency basis, sales fell by 4.3%reflecting the impact of an unprecedentedand rapid downturn that started to affectour industry in the second half of 2008.

Profit before tax and exceptional items of£190.7m was 18.9% lower than 2007 andadjusted earnings per share fell 18.9% to30p.On a statutory basis,which includesexceptional items,profit before tax of£108.2m was 54.9% below 2007 andearnings per share fell 70.5% to 11.2p.

We responded swiftly to the market declineby reducing our cost base,closing 24 lessprofitable sites, reducing our workforce bymore than 2,000 people and implementingother restructuring measures which areexpected to generate an annualised savingof approximately £58m at 2009 exchangerates.These actions have resulted in anexceptional charge in 2008 of £28.3mtogether with a charge of £54.2m forgoodwill impairment largely due to thedownturn in Latvia.

When reviewing the performance ofour business units, trading profit is a keymeasure and is defined as operating profitexcluding the impact of exceptional itemsand unallocated central costs.

In our Distribution businesses we grewsales by 5.8% despite challenging tradingconditions.We primarily benefited fromstrong performances in Singapore,wherewe outperformed the market with newmodel launches and strong commercialvehicle sales resulting in a trading profitgrowth of 23.9%, in Hong Kong with atrading profit growth of 17.7% and in theRest ofWorld with trading profit growthof 23.2%.We retained market share as wellas market leadership in Greece and salesin Belgium grew 0.2% on 2007 under verydifficult conditions. In Australia,whilst newmodels helped to improve market shareby 10bp, the market decline resulted in atrading profit decrease of 3.7%.The UK fleetmanagement business, Inchcape FleetSolutions,suffered from a residual valueprovision increase of £8.5m.

4

Inchcape has a provenand resilient businessmodel.The industryfaces an unprecedenteddownturn but we willremain solid by focusingon our core activities.

Peter JohnsonChairman

5

www.inchcape.com

Businessreview

01-37Governa

nce38-57

Financia

lstatem

ents58-120

Shareho

lderinfo

rmation

Insidebackcover

Sales in our Retail businesses grew by 1.6%in 2008,benefiting from our acquisitions inRussia,9.3% growth in Australia and a newLexus retail centre in China.Across Europe,sales grew 3.0% as a result of strongperformance in Greece and Finland. In theUK we outperformed the market with like forlike sales falling 5.4% in a market which fell11.3%. In the Russia and Emerging Marketssegment, trading profits increased by 40.9%largely as a result of our acquisitions inRussia and growth in Poland.

Acquisition and disposal summaryWemade further progress in our UK disposalprogramme in accordance with our strategyto streamline the business following theacquisition of EuropeanMotor Holdings plc in2007.We sold ourVauxhall business and themajority of ourVolvo retail outlets for a totalconsideration of £17.0m.These transactionsfollowed the disposals of InchcapeAutomotive,Wilcomatic,and the Bentley,Ferrari and Maserati retail outlets in 2007.

We have reinvested the proceeds fromthese disposals into our Russia and EmergingMarkets segment,announcing in March theacquisition of the remaining 24.9% stake inour St Petersburg business for a total cashconsideration of £28.5m.This gave the Groupfull ownership of its operations in St Petersburgand was another step in the implementationof the Group’s multi-brand Retail footprint,providing broad segment coverage in whatis expected to be one of the fastest growingmarkets in the world.

In April,we announced further expansion inthis market with the acquisition of an initial75.1% shareholding in Musa Motors group,one of Russia’s largest car retailing groups,giving Inchcape a significant scale positionin Moscow through 16 sites with key globalbrand partners.The initial considerationwas £100.3m (see note 27 for details).Thisacquisition has positioned Inchcape withone of the largest networks of premiumbrands in Moscow.

In May we announced another landmarkin our expansion into the Chinese marketwith the official opening of our whollyowned Lexus retail centre in Shaoxing.

During the year we also sold our Frenchoperation to its management team for aconsideration of £7.6m.

DividendThe Board is not recommending thepayment of a final ordinary dividend for theyear in light of the current deterioration oftrading conditions (2007 – 10.5p).The Boardrecommended a half year dividend for 2008of 5.46p which reflected a 4.0% increase onthe half year 2007 dividend.

We currently do not expect to recommendany dividend for the financial year ending31 December 2009.

We intend to return to our stated aim ofmaintaining a progressive dividend policyas soon as trading conditions allow.

Share buy backThe Group purchased £16.0m of its sharesin 2008 through the acquisition of 4.5mshares,now held asTreasury shares atan average price of £3.59 per share.

Approach to governance andmanagementWe continue to focus on the importanceof good governance and observe theCombined Code and other relevantguidance for listed companies in our globaloperations. Integrating socially responsiblebehaviour into every aspect of how weoperate and define ourselves remains highon our agenda. In 2008 we have built onthe foundations of a global approach toCorporate Responsibility (CR) that is makingresponsible economic,environmental andsocial behaviour intrinsic to the way we work.

PeopleOur people strategy is to have engagedpeople in winning teams,creating theultimate customer experience for our brandpartners.On behalf of the Board, I wish toexpress thanks to our colleagues across theGroup for their commitment and spirit indelivering these results for 2008.

I would like tomake specialmention ofWilliamTsui,Chairman of InchcapeAsia-Pacific whosadly passed away in February 2009,after 18years with theGroup.Under his leadership,ourbusinesses in Hong Kong,Macau,Singapore,Brunei,Guam and Saipan consolidated theirmarket leading positions.LatterlyWilliamspearheaded our entry into China.Williamwill be remembered for his passion for themotor industry and our customers and forhis truly inspirational leadership.

Strengthening our capital structureThe Group has historically maintained whatwas considered to be an appropriate levelof borrowings given the prevailing economicenvironment.Given the prospect of a difficulttrading environment in 2009 and beyond,we intend to continue our actions to reducenet debt. In order to further strengthen theposition of the Group, the Board believes itis both appropriate and in the best interestsof its shareholders to raise net proceedsof approximately £232m in equity via aRights Issue which we announced on19 March 2009.

We intend to use the net proceedsof this Rights Issue to reduce the levelof indebtedness which in the short term

will increase headroom and delay therefinancing of existing facilities. In the longerterm,we expect that strengthening theGroup’s balance sheet through thisRights Issue together with the actionwe have taken to lower our cost base,our geographic spread and diversifiedrevenue streams,will better position usto take advantage of market recovery.

OutlookAlthough the Group expects tradingconditions to remain extremely challengingthroughout 2009 and the actual results forJanuary and February were well below lastyear, they have exceededmanagement’sexpectations in difficult markets,due to agood start to the year in Singapore anda stabilisation of UK used car margins.Currently,March order levels for the Group’sUK operations are in line with our revisedexpectations.The fundamentals of theGroup remain solid and our strategicdirection is clear.We have respondedquickly and decisively to global economicconditions.Our experiencedmanagementteams,our track record of operationalexcellence,our focus on superior customerservice and the strength of our relationshipswith our brand partners give us confidencethat we will successfully weather the currentstorm in our industry and emerge stronger.

Board changeAs previously announced, I will beretiring from the position of Non-executiveChairman in May 2009, following 14 yearswith the Company,six years as Group ChiefExecutive and three years as Chairman.I am delighted that Ken Hanna,who hasbeen a Non-executive Director of Inchcapefor six years, is to be appointed Non-executiveChairman of the Group with effect from14 May 2009.Ken has considerable skillsand expertise with a proven track recordboth at a financial and operational leveland as a Non-executive Director,as well asdirect experience of operating businessesin emerging and developedmarkets.

I have thoroughly enjoyed my years withInchcape,especially working with so manytalented colleagues both on the Board andin the business and I know that I am leavingthe Group in very good hands.

Peter JohnsonChairman

6

Inchcape plc Annual Report and Accounts 2008

Business review

Group Chief Executive’s review

André LacroixGroup Chief Executive Inchcape is a leading independent,

international automotive distributor andretailer,with scale operations in Australia,Belgium,Greece,Hong Kong,Russia,Singapore and the UK as well as operationsin 19 other markets.We represent some ofthe world’s leading automotive brands withwhomwe have long-standing relationships.

During 2008, the car industry facedunprecedented challenges as the economicdownturn spread rapidly across the world.

While Inchcape is not immune to thedownturn, I believe we are well placed toride it out successfully,based on the intrinsicstrengths of our business together with theprudent and decisive actions we are taking,so that we will be well positioned to capitaliseon market recovery.

We have more than 160 years of successfulinternational trade experience based ona pioneering spirit that has seen us at theforefront of every industry in which we haveparticipated.Our focus today is squarelyon the car market where we have beenan industry leading retailer and distributorfor many years.We continue to owe thispre-eminence to two fundamental factors:the resilience of our business model,andthe clarity of our vision and strategy.

In addition,we have an exceptional seniorteam with an in-depth knowledge of theautomotive industry and local markets andwho share a collective record of decisive,successful management in the face ofeconomic upheaval.

We are a provenindustry leader,solidly positionedfor market recovery.

7

www.inchcape.com

Businessreview

01-37Governa

nce38-57

Financia

lstatem

ents58-120

Shareho

lderinfo

rmation

Insideback

cover

Solid...Aproven track record A diversified and resilient business model

• 160 years of internationalbusiness experience

• Broad geographic spread

• Diversified multi-channelbusiness model

• Prudent governance

• Long-standing brand partnerrelationships

• Experienced managementteam

A diversified and resilient business modelWebelieve our businessmodel has a numberof key strengths including a diversity thatensures resilience and provides a balancedportfolio of income streams.

First,we have a broad geographic spreadwith scale positions and a presence acrossboth mature and emerging markets.Webenefit from a decentralised organisationalmodel which enables us to stay close tochanges in the marketplace and reactquickly to flex our operational focus.Weenjoy a leading market share in manymarkets thanks to our first-hand experienceand hard-won knowledge of different buyingpreferences and our relentless focus onsuperior customer service.

Second,we have long-standing relationshipswith strong brand partners who outperformthe market,giving us access to a pipelineof attractive newmodels.Our brand strategyis market specific,enabling us to fit the rightbrand with the right market to pursue ourcore purpose of creating the ultimatecustomer experience for our brand partners,whilst aiming to maximise market share.

Third,we have amulti-channel structure, inwhich our Distribution businesses – where werepresent every aspect of a brand partner’spresence in a specific national market –have historically delivered stable,strong cashgeneration and our Retail businesses provideaccess to diversified and resilient sources ofrevenue through, for example,aftersalesservice and parts.

Inchcape’s history of outperformance is dueto the key strengths of our business modeland the clarity of our vision and strategy.

These diversified income streams (our valuedrivers) give us both the growth opportunitiesthat drive our business forward (newandusedcar sales, third-party finance and insuranceproducts) and defensive income (aftersalesservice and parts) that becomes increasinglyimportant in times of economic difficulty.

Aftersales represents approximately 50% ofour gross margin.This is an area on whichwe are focusing greater resources thanever before as an integral component ofour Customer 1st strategy,emphasising thequality and value benefits for car-ownersin staying with their franchise retailer afterthe expiry of their warranty period.

It is a significant area of opportunity forus as even during times of declining newvehicle sales, the total population of carson the road (the car parc) continues togrow andmore motorists concentrate onmaintaining rather than replacing theirexisting vehicle.

Our focus on maximising the economiccontribution of all our value drivers byconstantly driving new efficiencies hasenabled us historically to deliver strongmargins.We seek to continue to improve ourperformance throughout 2009,when difficultmarket conditions mean that maximisingreturns will be particularly important.

A clear vision and strategyMeeting our vision of being the industry’smost customer-centric retailer anywhere inthe world is fundamental to the success ofour business model.

To be the world’smost customer-centric automotiveretail group

A clear vision and strategy

Our goal of creating and delivering theultimate customer experience is a keydifferentiator for Inchcape in our industryand provides the basis of our long-standingrelationships with many of the world’sleading motor manufacturers.Our passionfor superior customer service reflects directlyon the reputation of our brand partners,making this a compelling reason for them toselect Inchcape as their partner of choice.

This Customer 1st approach is central to ourbusiness and drives decisions taken at everylevel of the organisation.Understanding thecustomer’s view of our performance is vitaland we continue to invest strongly inmystery shopper and customer feedbackprogrammes and leading technologiesto support our activities.These combine togive us a constant view of our performancefrom the customer’s perspective and helpus identify opportunities the momentthey emerge.

The combination of our unique businessmodel and our differentiating customerfocus has underpinned Inchcape’s successfor many years.Today, it is enabling us tooutperform our competitors in the mostdifficult trading conditions to affect ourindustry for more than a generation.

Financean

dInsurance

Vehicle sales

Growth drivers

Serv

ice

Defensive drivers

Parts

Retail

Distribution

8

Inchcape plc Annual Report and Accounts 2008

Business review

Group Chief Executive’s review continued

Responsive... We have been responsive to therapid and unprecedented industrydownturn and are proactivelymanaging the business with ahigh-impact programme.

1GrowingmarketshareFocusing on brandmanagement,customer funnelconversion,outstanding serviceand new productlaunches

2Growingaftersales

Furtherstrengtheningcustomer service,increasingcustomer retentionand enhancingproductivity

3Reducingcosts

Prompt action byreducing employeeheadcount,closingnon-profitable sitesand reducing allnon-essentialprogrammes

4ManagingworkingcapitalFocusing onworking capitalcontrol to bringinventory levelsin-line with marketdemand

5ReducingcapitalexpenditureReducingdiscretionarycapital expenditurein agreement withbrand partners

Our five key priorities

Managing the downturnWe have responded swiftly to the economicdownturn with decisive management actionto make our business even sharper,moreeffective andmore efficient.We believethis will help us both minimise the negativeimpact from the current downturn andprepare us to emerge stronger whenthe market recovers.We have narrowedour management focus to the five basicsof our business,our ‘five key priorities’:growing market share whilst protectingmargins;growing aftersales; reducing costs;managing working capital; and reducinguncommitted capital expenditure.

Focusing on these priorities now,meansthat we will be well-placed to takeadvantage of the growth opportunitiesthat come with recovery.

Market share growthGrowing market share whilst protectingmargins in our Retail businesses springsdirectly from our Customer 1st strategy,with afocus on traffic conversion through rigorous,disciplined sales processes and outstandinglevels of customer service.Further, in today’smarket,our ability to help customers gainaccess to the finance credit they need tobuy a car is a clear advantage. In ourDistribution businesses we will grow ourmarket share through disciplined marketingeffectiveness, taking full advantage of ourbrand partners’new product launches andoffering strong value for money propositionsto our customers.

Aftersales growthGrowing our aftersales business will comefrom focused service and parts marketing,a strong emphasis on retaining customersand providing outstanding levels of customerservice through, for example,our ‘VehicleHealth Check’.The key for us today is torecognise and respond to every transactionas an opportunity to build a long-termcustomer relationship that delivers valueto both parties.This is central to ourCustomer 1st strategy.

Further, in our aftersales workshops,wecontinue to apply ourselves to drivingproductivity enhancement and thereforegross margin.

Cost reductionIn terms of cost saving,we already haveamajor restructuring programme underway that will deliver an annualised benefitof approximately £58m,based on 2009exchange rates.This includes a 12%reduction of our global workforce, tight newrestrictions on travel and a retail site andoffice rationalisation which by the first halfof 2009 will have resulted in the closure of24 less profitable sites,comprising 16 retailcentres,one used car centre and onePDI centre in the UK, two retail centres inGreece and four in the Baltics.The Grouphas implemented a general hiring freezeand a policy of no salary increases in 2009or management bonuses for 2008.

Additionally,we are negotiating harderthan ever before on everything we spendand successfully taking advantage ofreduced advertising media costs.

Working capital managementManaging our working capital as efficientlyas possible is a top priority right across thebusiness.Unsold stock on forecourts is amajor expense for any motor retailer andwe have set stock reduction targets acrossthe Group.We have the support of ourbrand partners to match our inventorylevels to the newmarket demand,whichis successfully helping us to contain ourworking capital levels.

Capital expenditure reductionOur forward capital expenditure programmeis largely driven by the agreements we havein place with our brand partners,some ofwhich commit us to building new retailcentres in an agreed expansion timetable.The excellent relationships we have withour brand partners however,mean wehave been able to defer some projects.In addition,we are slowing some aspectsof the implementation of our new SAPsystem across the Group,while streamliningits adoption in our Retail business to benefitas rapidly as possible from its maincommercial advantages.

p11 p12 p13 p14 p15

9

www.inchcape.com

Businessreview

01-37Governa

nce38-57

Financia

lstatem

ents58-120

Shareho

lderinfo

rmation

Insideback

cover

Confident We are planning for the future,so that whenthe recovery comes we will be uniquelypositioned to take advantage of the growthopportunities and emerge stronger.

Solidly positioned for market recoveryWe are confident that taking theseproactive steps now will prepare us for thebest possible performance once themarketrecovers when,we believe,opportunitieswill be significant.We see a number ofstructural and economic factors that willhelp shape the future of our industry.

It is likely that,when it comes, recovery willtake place faster in the emerging markets,where the current low levels of car ownershipmeans that there is greater potential forthe demand for new and used vehicles toincrease.We will be able to use our existingpresence in those emerging markets tofull advantage.

However,there will be significant opportunitiesin thematuremarkets too,stemming from theneed for vehicle replacement as the car parcages,combinedwith technological innovationwhichwill both stimulate demandand drivedown the cost of ownership.

Industry consolidation means that wewill face a reduced number of competitorsin some of our markets,so that when therecovery comes it is likely that we will begrowing from a position of higher marketshare,providing the opportunity for improvedthroughput and economic performance ofour retail centres.

Further,we believe vehiclemanufacturers willaddress the current oversupply of vehiclesby rationalising their production to createa better balance between supply and

demand,which should lead to enhancedmargins on both new and used cars.

For all these reasons,we are excited byour future prospects,while recognisingthe medium-term challenges that we face.And we have a number of Inchcape-specificfactors that give us great confidence.

We operate as market leader in manymarkets with a scale position and withbrand partners who continue to outperformthe industry and who have the resourcesto innovate and stimulate demand.We willbenefit from a pipeline of new productswhich are set to deliver better value,betterperformance and lower CO2 emissions.

Following a period of integration,our aimis to have established scale operations inemerging markets,enabling them to makea growing contribution to the Group.

Our decentralised organisational modelgives us a significant advantage as weare capable of responding rapidly to thechanges in our industry.

Superior levels of customer service basedon our differentiating Customer 1st strategyand leading retail operating systems willhelp us grow share in many of our markets.

As an organisation,we will be leaner andmore efficient which will provide us withleverage when the market returns.

Further, I am constantly impressed bythe quality of our employees across theGroup.Despite the economic downturn,

I see our people displaying a true‘Inchcape spirit’and a real passion fordelivering exceptional customer service.

In short,our proven business model andstrategy,allied with the firm and prudentactions being taken by our experiencedmanagement teams today,mean thatInchcape is set to emerge from thecurrent downturn leaner,stronger andmore successful than ever.

We are confident that we will emergea winner.

André LacroixGroup Chief Executive

Emerging a winner

Industry factors

• Structural growth inemerging markets

• Vehicle replacementin mature markets

• Industry consolidation

• Realignment of vehiclesupply and demand

Inchcape factors

• Scale operations in coremature and emerging markets

• A leader in 14 markets

• Strong brand partners

• Decentralised,customer-centric,able to respond swiftlyto market conditions

• Leaner and fitter

Solidly positioned formarket recovery

10

Our management teamacross the Group haveresponded decisively tothe challenging marketclimate and haveadapted quickly to focustheir attention on theimportant areas thatare fundamental to thefuture of our business

André LacroixGroup Chief Executive

Focused on the fundamentals

Responding quicklyActing decisively

11

Growingmarket shareFocusing on brandmanagement,customer funnel conversion,outstanding service and new product launches

1

In the prevailing challengingmarket conditions,we willseek to grow our market shareorganically without sacrificingmargins.The focus will be onusingmarketing and promotionalactivities to increase the numberof customers who visit our retailcentres and on increasingthe conversion rate of thosecustomers into sales.To buildcustomer loyalty,we willcontinue to emphasise highlevels of customer service andsatisfaction which wemeasurethrough our Net PromoterScore (NPS) system,usingfeedback from customers ontheir experience at our retailcentres.We will also seek tofacilitate access to credit forour customers and,of course,take full advantage of newopportunities arising from theintroduction of newmodelsfrom our brand partners.

Market illustrationInAustralia,we are both distributorand retailer of Subaru vehiclesand in 2008 we achieved aremarkable milestone of 11consecutive years of record salesin a market that dropped 4%.

Subaru’s core strength isunderlined by the success ofthe new generation Forester,which has regained the positionas the country’s best-sellingcompact SUV.

Our marketing messages aredemonstrating the value ofSubaru ownership to manythousands of customers in thesetough economic times,who arerecognising the benefit of greatretained value,engineering,safety and durability.

We will reinforce thesemessages in 2009 with someexciting developments thatwe expect will attract newcustomers to the brand whilestrengthening the advocacyof our existing customers.

We will continue to build uponour 2008 segment-leading sharefor the Forester.The launch ofthe Impreza sedan and the newWRX has broadened our productrange and will drive furthersegment share growth.In October2009 we launch the new Libertyand Outback range with the firstdiesel Subaru being launched atthe end of the year.Our productactivity will be supported with acombination of strong brandand tactical promotions.

12

2

Aftersales revenues havehistorically shown a greaterresilience tomarket downturnsthan new car sales,as theaftersales market is drivenmore by the size and age ofthe car parc and technologicaladvances than it is by newcar sales.Accordingly,we areimplementing a number ofactions to help maximise thebenefits of the aftersales revenuestream andmaintain long-termconsumer relationships.Keymeasures being undertakeninclude focusing marketingand sales efforts on the retentionof customers who are nearingthe end of the warranty periodon their new vehicle.There willalso be a focus on the use ofmanagement tools such ascapture rate,vehicle healthcheck and the NPS system tomonitor customer satisfactionand increase customer retention.

Market illustrationAtMazda Hong Kongwe haveapplied a strong focus onretaining customers of vehiclesover three years old.As a resultof effective local marketing

and adapting our serviceofferings to cars of different ageswe have increased service loyaltylevels significantly.

Flexible,pre-paidmaintenanceservice packages includeadditional benefits like prioritybooking and a free odourisingtreatment.We also offer a pre-inspection safety test packagewith special discounts onreplacement parts.

Packages for newer vehicleshave been developed too,like our 12-step exterior surfacetreatment, interior cleansing andengine compartment cleaning.

Growing aftersalesFurther strengthening customer service, increasingcustomer retention and enhancing productivity

13

Reducing costsPrompt action by reducing employee headcount,closingnon-profitable sites and reducing all non-essential programmes

3

As a result of prompt actionstaken to reduce the Group’s costbase to reflect the deterioration inmarket conditions,our workforcehas been reduced by more than2,000 people across the Group.

In addition,24 less profitablesites,comprising 16 retail centres,one used car centre and onePDI centre in the UK, two retailcentres in Greece and four inthe Baltics will be closed by thefirst half of 2009.The Group hasimplemented a general hiringfreeze and a policy of no salary

increases in 2009ormanagementbonuses for 2008.Further,wehave tight new restrictions ontravel.The cost of the restructuringwill be approximately £28.3m,with an expected annualsaving of approximately £58mat 2009 exchange rates from2009 onwards.

We will continue to monitorclosely and review our cost basein light of the prevailing tradingandmarket conditions to ensurethat it reflects appropriately ourongoing requirements.

Annualised benefit

£58m

Managingworking capitalFocusing on working capital control to bringinventory levels in line with market demand

4

14

As a result of the abrupt salesdeclines in many of our marketsand the long lead time on ordersfor new vehicles placed with ourbrand partners, inventory levelshave been higher than desirable.Vehicle orders were reducedduring the second half of 2008to reflect the prevailing marketconditions and we are seekingto reduce significantly the level ofinventory held across the Group’sDistribution and Retail businesses.

We are also targeting areduction in the length of timevehicles will remain in inventoryat current levels of trading.Specific sales incentives havebeen put in place with the aimof accelerating this reduction, inparticular in respect of vehicleswhich have been in inventory forover six months.

Market illustrationIn the UK,we have taken decisivemanagement action to addressour used car stock.In addition to adisciplined approach to reviewingdaily stock lists and applyingtight pricing management,wehave introduced an even firmerapproval process for all buyingof used cars.

Further, through our strongrelationships with our brandpartners,we have reduced thenumber of demonstrator vehiclesthat we hold in stock.Along withan incentive programme to drivedown inventory, this has led to asubstantial improvement in ourUK working capital and vehiclestock position.

15

Reducing capitalexpenditureReducing discretionary capital expenditurein agreement with brand partners

5

We are confident that our recentinvestments have placed us in astrong position to benefit whenthe markets rebound.Therewill be considerable pent-upconsumer demand in emergingmarkets,based on low levels ofcar ownership,and we believeour scale position in theseterritories will reap their reward.While we are putting on hold anyuncommitted new investments,we are completing projects thatare already under way andhonouring our commitments

to our brand partners,with whomwe have excellent relationships.This has meant that we havebeen able to defer some projectsand should we see furthermarket deterioration,we havescope for additional deferment.

Further,capital outlay on ournew SAP system has beenslowed whilst at the same timewe are accelerating its roll-outinto our Retail businesses,suchthat we can take advantage ofearlier gains from this investment.

16

Inchcape plc Annual Report and Accounts 2008

Business review

Operating review

Barbara RichmondGroup Finance Director

Key PerformanceIndicators (KPIs)The Inchcape plc Board of Directors andthe Executive Management teammonitorthe Group’s progress against its strategicobjectives and the financial performanceof the Group’s operations on a regularbasis.Performance is assessed againstthe strategy,budgets and forecasts.

To enhance comparability,we review theresults in a form that isolates the impact ofcurrency movements from period to periodby applying a constant currency rate.Unlessotherwise stated,all year on year changesin sales and trading profit figures quotedin the Operating review are provided inconstant currency.

We also measure the quality of revenuesthrough the mix of revenue streams,and theflow through of value from sales revenue totrading profit.

Financial KPIsVehicle market sizeDefined as total new vehicle registrations.

Vehicle market shareDerived from Inchcape’s registrations asa percentage of the overall market size.

SalesThe consideration receivable from the saleof goods and services. It is stated net ofrebates and any discounts and excludessales related taxes.

Trading profitDefined as operating profit excludingthe impact of exceptional items andunallocated central costs.

Trading margins (return on sales)Calculated by dividing trading profit by sales.

In a year of unprecedentedglobal economic slowdown,Inchcape has delivered aperformance in line with ourexpectations,demonstratingthe resilience of our provenbusiness model and ourprudent governance.

17

www.inchcape.com

Businessreview

01-37Governa

nce38-57

Financia

lstatem

ents58-120

Shareho

lderinfo

rmatio

nInsid

eback

cover

Like for like sales and like for like trading profitExcludes the impact of acquisitions from thedate of acquisition until the thirteenth monthof ownership and businesses that are sold orclosed. It further removes the impact of retailcentres that are relocated.This is from thedate of opening until the thirteenth monthof trading in the new location.

Group profit before taxThe profit made after operating and interestexpense but before tax is charged.

Group working capitalDefined as inventory, receivables,payablesand supplier-related credit.

Operating cash flowDefined as trading profit adjusted fordepreciation and amortisation plus thechange in working capital.

Non-financial KPIsWe continue to measure several non-financial KPIs,particularly regardingcustomer service, relating to both thepurchase of new and used vehicles andalso aftersales.For example,Net PromoterScore (NPS) is being used to measurecustomer satisfaction across the Group,in line with our vision to be the world’s mostcustomer-centric automotive retailer.

Further,wemeasure employee engagementGroup-wide through our annual Heartbeatsurvey conducted in partnership with Gallup.

Group overviewKey Performance Indicators*

Year Yearended ended

31.12.2008 31.12.2007£m £m

Sales 6,259.8 6,056.8

Like for like sales growth (%) 2.6 2.5

Trading profit 250.1 292.5

Like for like trading profit (decline)/growth (%) (16.1) 4.8

Trading margins (%) 4.0 4.8

Operating cash flow 210.7 306.9

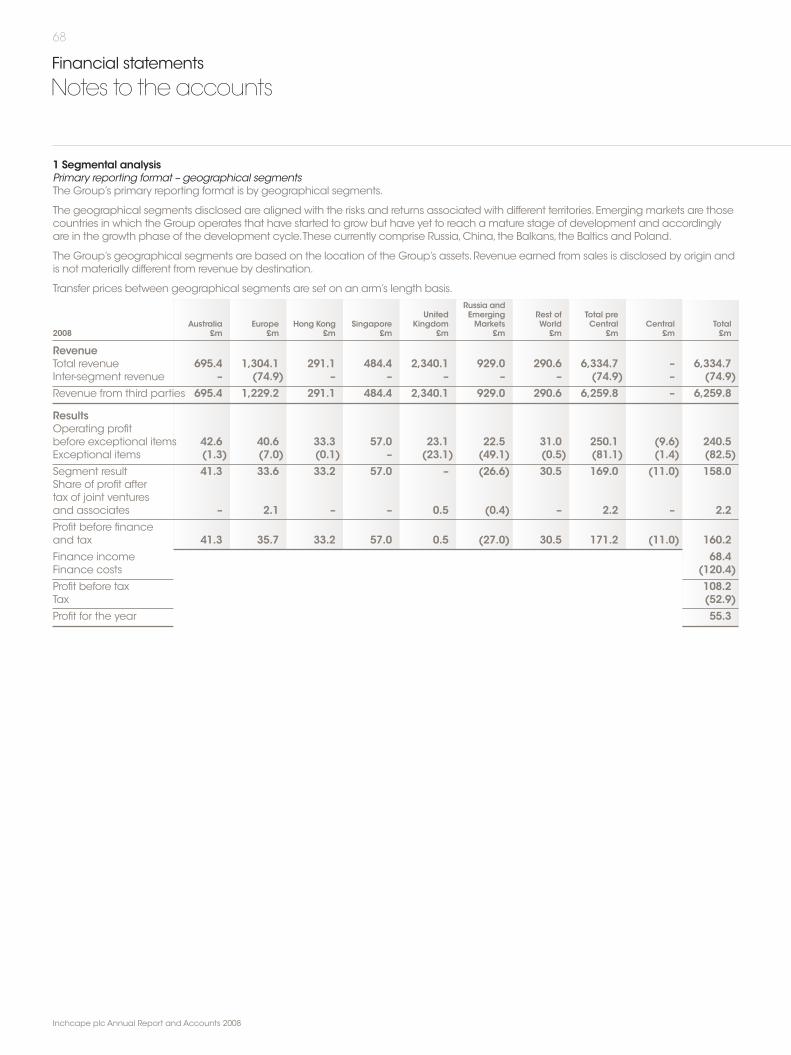

Regional analysis*2008 2008 2008 2007 2007 2007

Operating Exceptional Trading Operating Exceptional Tradingprofit items profit profit items profit£m £m £m £m £m £m

Australia 41.3 (1.3) 42.6 43.8 – 43.8

Europe 33.6 (7.0) 40.6 50.1 – 50.1

Hong Kong 33.2 (0.1) 33.3 40.3 12.0 28.3

Singapore 57.0 – 57.0 46.0 – 46.0

United Kingdom – (23.1) 23.1 62.5 (7.1) 69.6

Russia andEmerging Markets (26.6) (49.1) 22.5 29.6 – 29.6

Rest ofWorld 30.5 (0.5) 31.0 25.1 – 25.1

Total 169.0 (81.1) 250.1 297.4 4.9 292.5

Central costs (11.0) (1.4) (27.5) –

158.0 (82.5) 269.9 4.9

* At actual exchange rates

Foreign currency translationAverage rates Year end rates2008 2007 2008 2007

Euro 1.27 1.46 1.03 1.36

Hong Kong dollar 14.56 15.63 11.14 15.52

Singapore dollar 2.63 3.02 2.07 2.87

Australian dollar 2.19 2.39 2.06 2.27

US dollar 1.87 2.00 1.44 1.99

economic downturn resulting in a like forlike trading profit decline of 84.2% with theBaltics particularly affected.

Our Rest ofWorld segment delivered strongresults with like for like sales growth of 11.2%and like for like trading profit growth of 16.4%contributing a total trading profit for 2008of £30.8m.

Retail businessOur Retail businesses have been significantlyaffected by the global decline and overallwe saw a reduction in like for like sales of3.5%.Total trading profit decreased by 36.6%.

In the UK we continue to outperform. In amarket which declined by 11% our like forlike sales reduced by 5.4%.Trading marginsreduced from 2.4% to 1.2%.

Across Europe we continue to drive ourturnaround strategy. In 2008, like for likerevenues declined by 1.2%,delivering atotal trading profit of £0.7m.

In our Russia and EmergingMarkets segment,like for like sales increased by 3.8%, resultingin a total trading profit of £18.6m, largely dueto our recent acquisitions in Russia.

Distribution businessAlthough like for like sales were 5.2% downversus 2007, trading margins remainedbuoyant at 7.3%,delivering a total tradingprofit of £192.9m.

Across Europe,we delivered some solidresults in the face of significantly reducedmarkets.Our GreekToyota and Lexusbusiness retained its market leadershipposition to deliver trading profit growth of6.6%.The Belgian market grew 2%,partlyaided by the biennial motor show,howeverour share declined by 1.0ppt, resulting ina 12.8% decline in like for like sales.

The markets in Asia continued to be verycompetitive,with the market in Hong Konggrowing 7% for the full year,but declining by41% in Q4. In Singapore,market conditionswere challenging,as expected,and themarket declined by 13% (excluding parallelimports).However,with strong marketingcampaigns and newmodel launchestogether with the impact of the appreciationof theYen on our competitors,we achieveda 7.9% increase in trading profit.

Our Russia and Emerging Markets segmenthas been significantly affected by the

18

Inchcape plc Annual Report and Accounts 2008

Business review

Operating review continued

GroupThe prevailing conditions in the globalfinancial markets have significantly affectedthe demand for,and price levels of,newand used vehicles.

In Q4 2008 most of our markets experienceda significant downturn: the UK declined27%;Hong Kong 41%;Greece 21% andAustralia 15%.

These significant market declines havecontributed to a decline in our Groupoperating profit,before exceptional items,of 17.4% for the full year, from sales whichdeclined by 3.3%.This compares to the firstsix months where we reported operatingprofit growth of 13.4% before exceptionals,on sales which grew by 5.1%.

The sales decline was however partiallymitigated by a solid performance fromaftersales,on which our like for like revenuesgrew by 4.2% for the Group for the fullyear compared to 2007.This is an area ofsignificant opportunity which has receivedan increasing focus through 2008 and willcontinue to do so in 2009 and beyond.

We responded swiftly to the market declineby reducing our cost base,closing 24 lessprofitable sites, reducing our workforce bymore than 2,000 people and implementingother restructuring measures which areexpected to generate an annualised savingof approximately £58m at 2009 exchangerates.These actions have resulted in anexceptional charge in 2008 of £28.3mtogether with a charge of £54.2m forgoodwill impairment largely due to thedownturn in Latvia.

We continue to reflect our managementstructure in our reporting by separatelyproviding an analysis of the two segmentsof our business,Retail and Distribution,bygeographical region.We have continued ourexpansion into emergingmarkets,particularlyin the strategically important Russian market.We continue to include Russia,China, theBalkans, the Baltics and Poland within theRussia and Emerging Markets segment onthe basis that these markets have started togrow but have yet to reach amature stageof development and accordingly are in thegrowth phase of the development cycle.We have re-named the segment ‘Russiaand Emerging Markets’ in our reporting.

19

www.inchcape.com

Businessreview

01-37Governa

nce38-57

Financia

lstatem

ents58-120

Shareho

lderinfo

rmatio

nInsid

eback

cover

AustraliaYear ended Year ended % change31.12.2008 31.12.2007 in constant

Key financial highlights* £m £m % change currency

Sales 695.4 657.5 5.8 (3.1)

Retail 263.2 240.9 9.3 0.1

Distribution 432.2 416.6 3.7 (4.9)

Like for like sales 666.8 629.3 6.0 (2.9)

Retail 234.6 212.7 10.3 1.0

Distribution 432.2 416.6 3.7 (4.9)

Trading profit 42.6 43.8 (2.7) (11.0)

Retail 8.9 8.8 1.1 (7.7)

Distribution 33.7 35.0 (3.7) (11.8)

Like for like trading profit 42.1 43.8 (3.9) (11.8)

Retail 8.4 8.8 (4.5) (12.1)

Distribution 33.7 35.0 (3.7) (11.8)

Trading margin 6.1% 6.7% (0.6)ppt (0.5)ppt

Retail 3.4% 3.7% (0.3)ppt (0.3)ppt

Distribution 7.8% 8.4% (0.6)ppt (0.6)ppt

Operating cash flow 44.1 44.6

Retail 7.6 9.0

Distribution 36.5 35.6* At actual exchange rates

Core brand partners

StrategyWe have been the distributor for Subaruin Australia and New Zealand since 1992and a retailer since 2001.We currently own11 retail centres out of a total Subaru retailcentre network of 106 across Australia.Wealso operate nine retail centres for a furtherfour of the top 12 automotive brands byvolume inAustralia (Volkswagen,Hyundai,Mitsubishi and Kia). Inchcape retail centresare located in Melbourne (including aflagship retail centre for Subaru), the greaterSydney area and in the northern Brisbanedistrict of Queensland.

In Australia,we also ownAutoNexus whichprovides logistics services to the automotiveindustry. In 2008,AutoNexus was responsiblefor the storage and logistic managementof over 48,400 vehicles and 1.4m of partslines dispatched.

In our Subaru Distribution business we aim tobeAustralia’s premium Japanese automotivebrand and to leverage that position in ourRetail business to becomeAustralia’s mostcustomer-centric automotive retail group.

MarketTheAustralian vehicle market declined by4% in 2008,with the large engine passengercars segment particularly affected,whilediesel engine vehicles gained share.Themarket began to be affected by the globaldownturn in Q4 with a decline of 15%.Market conditions were very competitive,fuelled by high levels of sales support andmarketing expenditure with consumersparticularly sensitive to fuel consumption.

PerformanceOur Subaru Distribution business achievedamilestone of 11 consecutive years ofrecord sales in 2008.Sales of 38,492 vehiclesdistinguished the business in a difficultmarket where many competitors weakened.Subaru in Australia maintained the largestmarket share for the brand (3.8%) of anymajor region outside Japan.

Subaru’s core strength was underlined bythe success of the new generation Forester,which regained its position as the country’sbest-selling compact SUV,with best-eversales of 14,423 units in 2008,up 14.9%.TheSubaru Impreza became one of Australia’sfastest selling models of 2008.

Trading margins were below 2007,at 7.8%due to the investment required for thelaunch of two key newmodels.

Our Retail business achieved like for likerevenues of 1.0% above 2007,a performancewhich was further enhanced by grossmargins which grew by 0.6ppt versus lastyear.However total trading profits were 7.7%below 2007 (excluding a one off propertysale recorded in 2007).

Our AutoNexus business had anothersuccessful year,winning severalnew contracts.

OutlookThe new vehicle market is forecast to declinein 2009.We expect market conditions toremain highly competitive as the marketadjusts to lower sales volumes and excesslevels of inventory.The strength of the Subarubrand in Australia has enabled us to enterinto an agreement with Esanda to replaceGMAC for the provision of wholesale financeto support our dealer network.The Subaruproduct offering should enable us tocompete strongly in 2009.

Europe

Core brand partners

20

Inchcape plc Annual Report and Accounts 2008

Business review

Operating review continued

Year ended Year ended % change31.12.2008 31.12.2007 in constant

Key financial highlights* £m £m % change currency

Sales 1,229.2 1,203.9 2.1 (11.2)

Retail 391.3 379.8 3.0 (10.4)

Distribution 837.9 824.1 1.7 (11.5)

Like for like sales 1,149.0 1,076.2 6.8 (7.1)

Retail 311.1 273.8 13.6 (1.2)

Distribution 837.9 802.4 4.4 (9.2)

Trading profit 40.6 50.1 (19.0) (29.4)

Retail 0.7 0.8 (12.5) (14.6)

Distribution 39.9 49.3 (19.1) (29.7)

Like for like trading profit 40.1 48.8 (17.8) (28.7)

Retail 0.2 – n/a n/a

Distribution 39.9 48.8 (18.2) (29.1)

Trading margin 3.3% 4.2% (0.9)ppt (0.9)ppt

Retail 0.2% 0.2% – –

Distribution 4.8% 6.0% (1.2)ppt (1.2)ppt

Operating cash flow (18.7) 85.9

Retail 6.3 8.6

Distribution (25.0) 77.3* At actual exchange rates

StrategyIn Belgium,we are the distributor for Toyotaand Lexus.We own eight Toyota and Lexusretail centres in Belgium,with the remainingnetwork of 85 retail centres in Belgiumowned by independent third party retailers.

In Luxembourg,we are the distributor andretailer of Jaguar,Toyota and Lexus,withone retail centre for each brand.

In Greece,we are the distributor for Toyotaand Lexus.We own seven retail centres withthe remaining network of 35Toyota andLexus retail centres and 40 authorisedrepairers independently owned.

In Finland,we are the distributor for Jaguar,Land Rover andMazdawith four retail centresin Helsinki and three outside the city.

We aim to drive growth in market share inour Distribution business and to continueour turnaround plan for Retail. In Distribution,growth will be driven by newmodel launchesand a focus on operational excellence,supported by tight overhead cost control.In Retail,our plan continues to focus onoperational excellence and improvementsin footfall conversion.

MarketIn Belgium,the new car market was up by2% for the year,although Q4 was flat versus2007. In Greece, the market declined by 6%

in 2008.The Finnish car market grew by11% in part due to a car taxation change.

PerformanceIn a year that saw the run out of manyToyota models, trading profits in ourDistribution business declined by £16.8m(29.7%).The Retail business delivered a totaltrading profit of £0.7m which was in line withlast year following our disposal in July 2008of our French business.

In Belgium,with no new products,ourDistribution business sawmarket share reduceby 1.0ppt versus 2007 in amarket which grewby 2%.Like for like sales declined by 12.8%,andour grossmargin was lower than last year dueto intense competition and vehicles on runout campaigns.Together with flat overheads,trading profits were 80.3% down.The Retailbusiness experienced like for like sales downby 7.9%,and with overheads in line with 2007trading profits were 45.7% below last year.

In Greece,our Distribution businesscontinued to lead the market and hold a9.9% share of the passenger car market. Inthe Retail business,our Customer 1st focusand business restructuring continues todeliver results.Total sales declined by 0.2%,but with tight control on overheads, totaltrading profits were up by 8.3%.

In Finland,we gainedmarket share,but likefor like sales in our Distribution business fell

by 15.8% due to a significant decline of ourDistribution activities in the Baltics.Althoughthis was partly mitigated by a 1.3pptimprovement in gross margins, trading profitswere 48.2% lower than 2007.A large portionof the decrease year on year was as a resultof the market decline in the Baltics asFinland Distribution exports there.However,our Retail business performed better with a1.2% decline in like for like sales offset by a2ppt growth in trading margins and loweroverheads resulting in a like for like tradingloss which was 82.7% better than 2007.

OutlookOur markets in Europe are expected to bematerially down in 2009.

In Greece,we expect to minimise the impacton trading profit by closing two loss-makingretail centres, focusing on strict cost-controlsand by taking full advantage of the newmodel line up.

In Belgium,we are confident we will be ableto benefit from new product launches,acontinued focus on customer satisfaction,careful inventory management and theopening of a state of the art Toyota factoryat Anderlecht during the year.

In Finland,we aim to offset the decline withnewmodels exploiting trends towards dieseland the recent CO2 legislation.

Hong Kong

Core brand partners

21

www.inchcape.com

Businessreview

01-37Governa

nce38-57

Financia

lstatem

ents58-120

Shareho

lderinfo

rmatio

nInsid

eback

cover

Year ended Year ended % change31.12.2008 31.12.2007 in constant

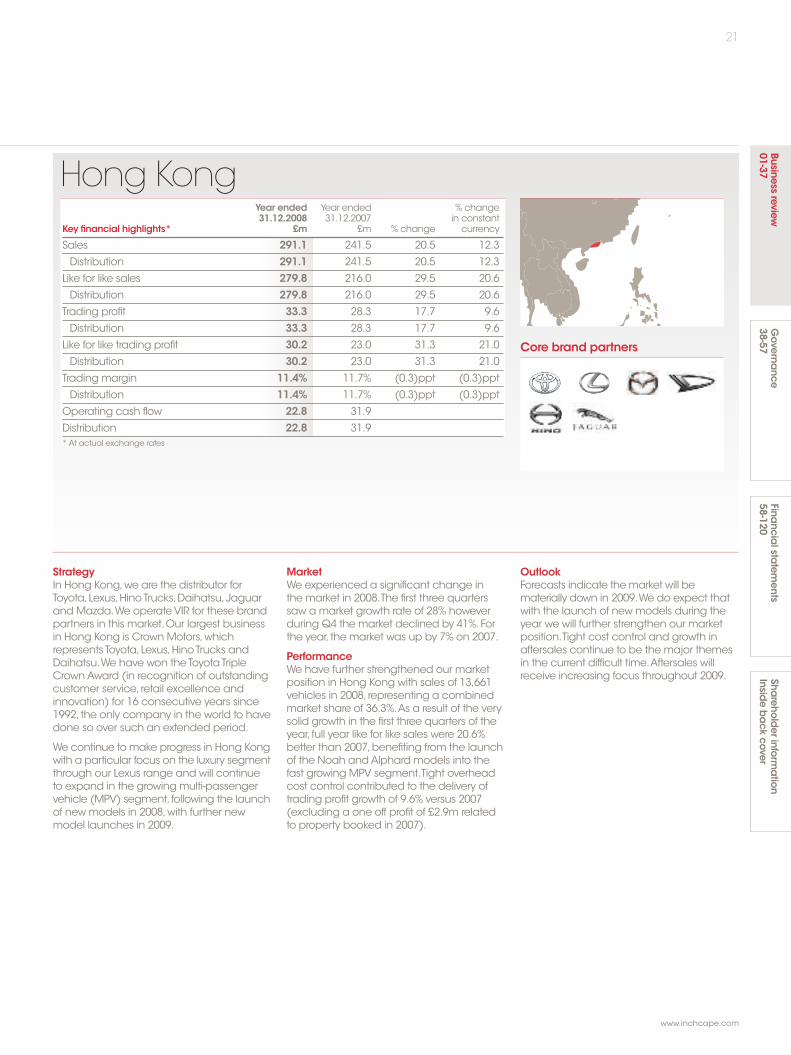

Key financial highlights* £m £m % change currency

Sales 291.1 241.5 20.5 12.3

Distribution 291.1 241.5 20.5 12.3

Like for like sales 279.8 216.0 29.5 20.6

Distribution 279.8 216.0 29.5 20.6

Trading profit 33.3 28.3 17.7 9.6

Distribution 33.3 28.3 17.7 9.6

Like for like trading profit 30.2 23.0 31.3 21.0

Distribution 30.2 23.0 31.3 21.0

Trading margin 11.4% 11.7% (0.3)ppt (0.3)ppt

Distribution 11.4% 11.7% (0.3)ppt (0.3)ppt

Operating cash flow 22.8 31.9

Distribution 22.8 31.9* At actual exchange rates

OutlookForecasts indicate themarket will bematerially down in 2009.We do expect thatwith the launch of newmodels during theyear we will further strengthen our marketposition.Tight cost control and growth inaftersales continue to be the major themesin the current difficult time.Aftersales willreceive increasing focus throughout 2009.

StrategyIn Hong Kong,we are the distributor forToyota,Lexus,HinoTrucks,Daihatsu,Jaguarand Mazda.We operateVIR for these brandpartners in this market.Our largest businessin Hong Kong is Crown Motors,whichrepresents Toyota,Lexus,HinoTrucks andDaihatsu.We have won theToyotaTripleCrownAward (in recognition of outstandingcustomer service, retail excellence andinnovation) for 16 consecutive years since1992, the only company in the world to havedone so over such an extended period.

We continue to make progress in Hong Kongwith a particular focus on the luxury segmentthrough our Lexus range and will continueto expand in the growing multi-passengervehicle (MPV) segment, following the launchof newmodels in 2008,with further newmodel launches in 2009.

MarketWe experienced a significant change inthe market in 2008.The first three quarterssaw amarket growth rate of 28% howeverduring Q4 the market declined by 41%.Forthe year, the market was up by 7% on 2007.

PerformanceWe have further strengthened our marketposition in Hong Kong with sales of 13,661vehicles in 2008, representing a combinedmarket share of 36.3%.As a result of the verysolid growth in the first three quarters of theyear, full year like for like sales were 20.6%better than 2007,benefiting from the launchof the Noah andAlphard models into thefast growing MPV segment.Tight overheadcost control contributed to the delivery oftrading profit growth of 9.6% versus 2007(excluding a one off profit of £2.9m relatedto property booked in 2007).

Singapore

Core brand partners

22

Inchcape plc Annual Report and Accounts 2008

Business review

Operating review continued

Year ended Year ended % change31.12.2008 31.12.2007 in constant

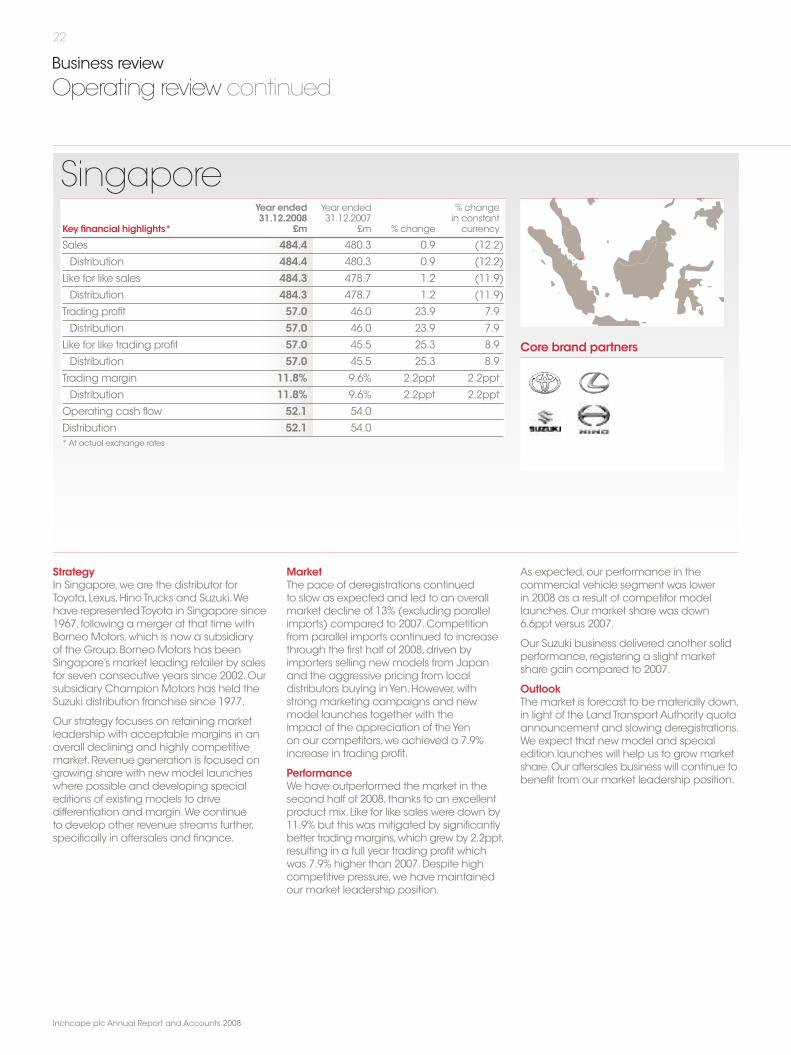

Key financial highlights* £m £m % change currency

Sales 484.4 480.3 0.9 (12.2)

Distribution 484.4 480.3 0.9 (12.2)

Like for like sales 484.3 478.7 1.2 (11.9)

Distribution 484.3 478.7 1.2 (11.9)

Trading profit 57.0 46.0 23.9 7.9

Distribution 57.0 46.0 23.9 7.9

Like for like trading profit 57.0 45.5 25.3 8.9

Distribution 57.0 45.5 25.3 8.9

Trading margin 11.8% 9.6% 2.2ppt 2.2ppt

Distribution 11.8% 9.6% 2.2ppt 2.2ppt

Operating cash flow 52.1 54.0

Distribution 52.1 54.0* At actual exchange rates

StrategyIn Singapore,we are the distributor forToyota,Lexus,HinoTrucks and Suzuki.Wehave representedToyota in Singapore since1967, following amerger at that time withBorneo Motors,which is now a subsidiaryof the Group.Borneo Motors has beenSingapore’s market leading retailer by salesfor seven consecutive years since 2002.Oursubsidiary Champion Motors has held theSuzuki distribution franchise since 1977.

Our strategy focuses on retaining marketleadership with acceptable margins in anoverall declining and highly competitivemarket.Revenue generation is focused ongrowing share with newmodel launcheswhere possible and developing specialeditions of existing models to drivedifferentiation andmargin.We continueto develop other revenue streams further,specifically in aftersales and finance.

MarketThe pace of deregistrations continuedto slow as expected and led to an overallmarket decline of 13% (excluding parallelimports) compared to 2007.Competitionfrom parallel imports continued to increasethrough the first half of 2008,driven byimporters selling newmodels from Japanand the aggressive pricing from localdistributors buying inYen.However,withstrong marketing campaigns and newmodel launches together with theimpact of the appreciation of theYenon our competitors,we achieved a 7.9%increase in trading profit.

PerformanceWe have outperformed the market in thesecond half of 2008, thanks to an excellentproduct mix.Like for like sales were down by11.9% but this was mitigated by significantlybetter tradingmargins,which grew by 2.2ppt,resulting in a full year trading profit whichwas 7.9% higher than 2007.Despite highcompetitive pressure,we have maintainedour market leadership position.

As expected,our performance in thecommercial vehicle segment was lowerin 2008 as a result of competitor modellaunches.Our market share was down6.6ppt versus 2007.

Our Suzuki business delivered another solidperformance, registering a slight marketshare gain compared to 2007.

OutlookThe market is forecast to be materially down,in light of the LandTransport Authority quotaannouncement and slowing deregistrations.We expect that newmodel and specialedition launches will help us to growmarketshare.Our aftersales business will continue tobenefit from our market leadership position.

UK

Core brand partners

23

www.inchcape.com

Businessreview

01-37Governa

nce38-57

Financia

lstatem

ents58-120

Shareho

lderinfo

rmatio

nInsid

eback

cover

Year ended Year ended % change31.12.2008 31.12.2007 in constant

Key financial highlights £m £m % change currency

Sales 2,340.1 2,713.5 (13.8) (13.8)

Retail 2,319.4 2,646.0 (12.3) (12.3)

Distribution 20.7 67.5 (69.3) (69.3)

Like for like sales 2,192.3 2,331.2 (6.0) (6.0)

Retail 2,171.6 2,294.8 (5.4) (5.4)

Distribution 20.7 36.4 (43.1) (43.1)

Trading profit 23.1 69.6 (66.8) (66.8)

Retail 28.8 64.7 (55.5) (55.5)

Distribution (5.7) 4.9 (216.3) (216.3)

Like for like trading profit 26.1 69.8 (62.6) (62.6)

Retail 31.8 64.8 (51.0) (51.0)

Distribution (5.7) 5.0 (214.0) (214.0)

Trading margin 1.0% 2.6% (1.6)ppt (1.6)ppt

Retail 1.2% 2.4% (1.2)ppt (1.2)ppt

Distribution (27.5)% 7.4% (34.9)ppt (34.9)ppt

Operating cash flow 154.1 60.0

Retail 154.8 53.3

Distribution (0.7) 6.7

IFS offers fleet management and leasingservices to corporate and governmentcustomers.With over 50 years’experience inthe automotive industry, IFS has a combinedfleet size of approximately 31,000 vehicles.

MarketThe economic downturn createdunprecedented challenges for the UKautomotive industry in 2008.We saw asignificant change in the market fromMay2008,with a rapid acceleration of the declinethrough the second and third quarters,resulting in a full year decline of 11% to 2.1munits.Diesel market share reached an all-timehigh of 43.6%.Market pricing was significantlyaffected, resulting in used car prices beingwell below 2007 levels.

PerformanceWe continue to outperform our competitorsand in the face of an 11%market decline,we achieved a like for like retail sales dropof 5.4% versus 2007.Pressure on new andusedmargins continued throughout 2008and as a result like for like trading marginsdeclined from 2.4% to 1.2% in 2008.

An £8.5m increase in residual valueprovision in IFS has resulted in a like for liketrading loss of £5.7m.This provision increaseis due to the fall in used car pricing, resultingin lower than expected realisable values onleased vehicles which will be returned overthe next two to three years.

OutlookThe new vehicle market is expected todecline materially in 2009.Notwithstandingthis decline,much greater stability isanticipated in the used vehicle marketwhile aftersales is expected to continueto make a significant contribution.

StrategyIn the UK, Inchcape has a significant retailbusiness with 130 franchised retail centresand a focus on core premium/premium-volume brand partners.We also operatea fleet leasing business, Inchcape FleetSolutions (IFS).

Since May 2006, the Group has acquiredand integrated LindAutomotive GroupHoldings Limited and European MotorHoldings plc.The enlarged portfolio hasextended the Group’s geographic reachand we now have scale operations in thecore regions of the South East,Midlands,North and North East of England.

We have streamlined our portfolio to focuson the following core brands:Audi,BMW,Honda,Jaguar,Land Rover,Lexus,Mercedes-Benz,MINI,Porsche,smart,Toyota andVolkswagen.

We aim to create significant differentiationby delivering an outstanding level ofcustomer service through our InchcapeAdvantage programme and drive growthin aftersales and car finance penetration.

Russia and Emerging Markets

Core brand partners

24

Inchcape plc Annual Report and Accounts 2008

Business review

Operating review continued

Year ended Year ended % change31.12.2008 31.12.2007 in constant

Key financial highlights* £m £m % change currency

Sales 929.0 518.6 79.1 57.1

Retail 623.9 276.6 125.6 98.5

Distribution 305.1 242.0 26.1 10.1

Like for like sales 573.6 518.6 10.6 (3.0)

Retail 326.3 276.6 18.0 3.8

Distribution 247.3 242.0 2.2 (10.7)

Trading profit 22.5 29.6 (24.0) (33.3)

Retail 18.6 13.2 40.9 24.2

Distribution 3.9 16.4 (76.2) (79.1)

Like for like trading profit 13.6 29.9 (54.5) (60.4)

Retail 10.6 13.5 (21.5) (31.4)

Distribution 3.0 16.4 (81.7) (84.2)

Trading margin 2.4% 5.7% (3.3)ppt (3.3)ppt

Retail 3.0% 4.8% (1.8)ppt (1.8)ppt

Distribution 1.3% 6.8% (5.5)ppt (5.5)ppt

Operating cash flow (67.3) 7.6

Retail (12.4) 5.5

Distribution (54.9) 2.1* At actual exchange rates

StrategyWe operate 20 retail businesses in Moscowand St Petersburg.Two further retail centresfor Toyota are under construction,one inMoscow and one in St Petersburg.

In St Petersburg,we own and operate one ofthe largest car retailing businesses in the city.In 2008,we acquired a 75.1% shareholdingin MusaMotors,one of the largest car retailgroups in Russia,providing the Group withscale presence in the Moscow region.

We are a distributor for Toyota and Lexusin Bulgaria and Romania. In Romania,we have increased our retail presence inBucharest with a new large-scale facility.In Bulgaria,we are increasing our retailpresence in Sofia and developing ourindependent network in the countryside.In addition,we are the distributor for Toyotaand Lexus in Macedonia andAlbania.

In Poland,we retail BMW andMINI inWarsaw andWroclaw.

In the Baltics,we are the distributor and weoperateVIR for Mazda,Jaguar and LandRover.We are also the retailer for BMW,Mitsubishi and Hyundai in these markets.We have market-leading positions in Latviawith a 12% share and in Lithuania with 15%.

In China,we haveToyota and Lexus retailcentres in Shaoxing.A third retail centre, forLexus in Shanghai, is due to open in 2009.

MarketThe second half of the year saw a significantshift in all emerging markets. In Russia, themarket for international brands fell by 6% inQ4, the first decline in many years. In China,although the passenger car market declinedby 6% in 2008, foreign brand sales grew by8%.The Balkansmarket dropped 11% in 2008(Q4 decline of 37%) and the Baltics marketdeclined 22% in 2008 (Q4 decline of 50%). InPoland, the market increased by 6% in 2008,largely reflecting good economic growth.

PerformanceOur Musa Motors acquisition performedin line with expectations in the six monthsto December.Our existing business inSt Petersburg delivered like for like tradingprofits that were 14.7% higher than 2007.Overall,Russia contributed £18.9m oftrading profit to the Group in 2008.

Our performance in the Baltics was affectedby a significant market decline with Latviathe worst affected.Overall trading profitsdeclined by £9.5m versus 2007.We continueto restructure our business in the region toreflect the current and projected futurebusiness environment.

In the Balkans,overall trading profit fell by£9.0m in 2008 primarily as a result of a 78.6%drop in trading profit in Romania.

In Poland, like for like trading profit increasedby 120.5% with a sales increase of 21%.

In China,we successfully opened our Lexussite in Shaoxing in January and we saw salesfrom our existingToyota site grow by 56.3%versus 2007. Including the new Lexus sitetotal revenues in China grew by 212.2%.

OutlookIn Russia,2009 is expected to be challenging,with the market forecast to be materiallydown.The Group should benefit fromexpected increase in the highly profitablearea of aftersales.

The markets in the Baltics and the Balkansare expected to be substantially down.

Although the Polish market is expectedto be down in 2009, the Group expectsimprovements in sales processes and theopening of a new BMW retail centre inWarsaw to offset this forecast lack of growth.

In China,growth is forecast to continue,althoughmore slowly than in recent years,and will be helped by our new Lexus siteopening in Shanghai in 2009.

Rest of World

Core brand partners

25

www.inchcape.com

Businessreview

01-37Governa

nce38-57

Financia

lstatem

ents58-120

Shareho

lderinfo

rmatio

nInsid

eback

cover

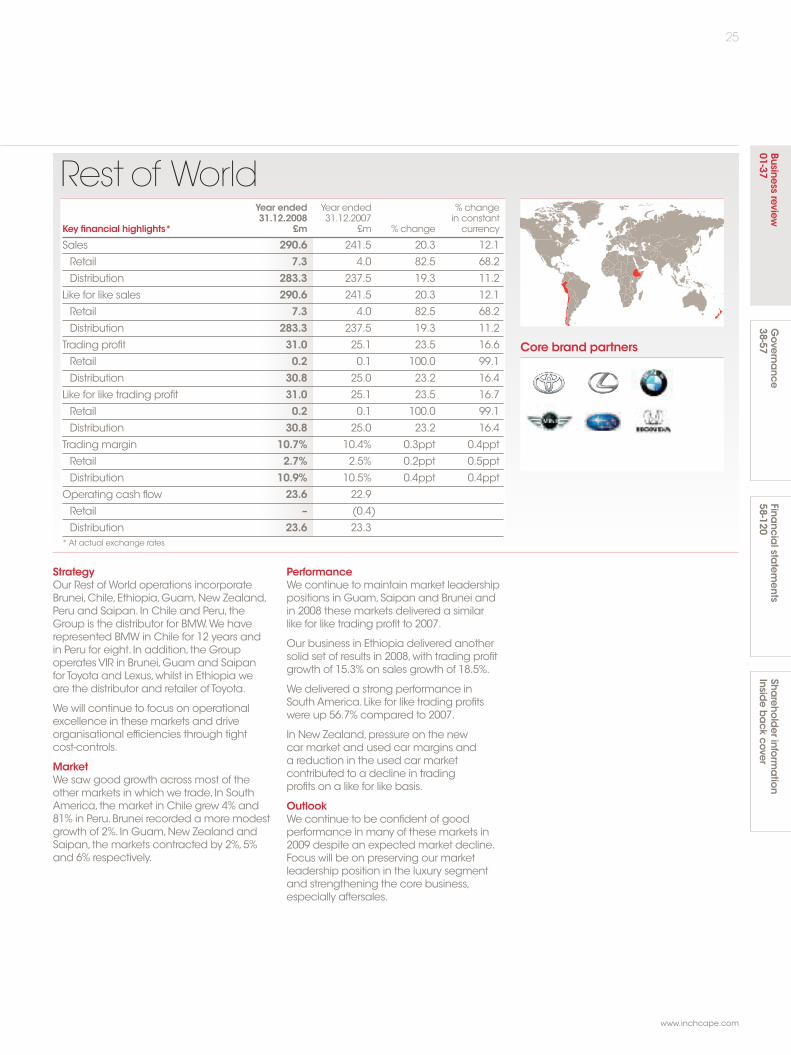

Year ended Year ended % change31.12.2008 31.12.2007 in constant

Key financial highlights* £m £m % change currency

Sales 290.6 241.5 20.3 12.1

Retail 7.3 4.0 82.5 68.2

Distribution 283.3 237.5 19.3 11.2

Like for like sales 290.6 241.5 20.3 12.1

Retail 7.3 4.0 82.5 68.2

Distribution 283.3 237.5 19.3 11.2

Trading profit 31.0 25.1 23.5 16.6

Retail 0.2 0.1 100.0 99.1

Distribution 30.8 25.0 23.2 16.4

Like for like trading profit 31.0 25.1 23.5 16.7

Retail 0.2 0.1 100.0 99.1

Distribution 30.8 25.0 23.2 16.4

Trading margin 10.7% 10.4% 0.3ppt 0.4ppt

Retail 2.7% 2.5% 0.2ppt 0.5ppt

Distribution 10.9% 10.5% 0.4ppt 0.4ppt

Operating cash flow 23.6 22.9

Retail – (0.4)

Distribution 23.6 23.3* At actual exchange rates

StrategyOur Rest ofWorld operations incorporateBrunei,Chile,Ethiopia,Guam,New Zealand,Peru and Saipan. In Chile and Peru, theGroup is the distributor for BMW.We haverepresented BMW in Chile for 12 years andin Peru for eight. In addition, the GroupoperatesVIR in Brunei,Guam and Saipanfor Toyota and Lexus,whilst in Ethiopia weare the distributor and retailer of Toyota.

We will continue to focus on operationalexcellence in these markets and driveorganisational efficiencies through tightcost-controls.

MarketWe saw good growth across most of theother markets in which we trade. In SouthAmerica, the market in Chile grew 4% and81% in Peru.Brunei recorded amore modestgrowth of 2%. In Guam,New Zealand andSaipan, the markets contracted by 2%,5%and 6% respectively.

PerformanceWe continue to maintain market leadershippositions in Guam,Saipan and Brunei andin 2008 these markets delivered a similarlike for like trading profit to 2007.

Our business in Ethiopia delivered anothersolid set of results in 2008,with trading profitgrowth of 15.3% on sales growth of 18.5%.

We delivered a strong performance inSouthAmerica.Like for like trading profitswere up 56.7% compared to 2007.

In New Zealand,pressure on the newcar market and used car margins anda reduction in the used car marketcontributed to a decline in tradingprofits on a like for like basis.

OutlookWe continue to be confident of goodperformance in many of these markets in2009 despite an expected market decline.Focus will be on preserving our marketleadership position in the luxury segmentand strengthening the core business,especially aftersales.

26

Inchcape plc Annual Report and Accounts 2008

Business review

Financial review

Acquisitions and disposalsThe Group continued its expansion inemerging markets in 2008 and invested atotal of £135.4m in acquisitions,offset bytotal proceeds from disposal of non-corebusinesses of £27.3m.

In March, the Group acquired theremaining 24.9% stake in the St Petersburgbusiness for a total cash consideration of£28.5m.As a result, the Group now owns100% of one of the largest automotive retailbusinesses in St Petersburg, the secondlargest city in Russia.

In July, the Group acquired a 75.1%interest in Musa Motors group for an initialconsideration of US$200m,with a furtherpayment due dependent on 2008 Earningsbefore Interest,Tax andAmortisation (EBITA)and subject to a cap of US$250m.Theremaining 24.9% is due to be acquired inearly 2011 for a payment dependent on2010 EBITA,again subject to a cap ofUS$250m.As a result, the Group hastherefore accounted for Musa Motorsgroup as if it was a wholly-owned subsidiary.This acquisition provides the Group with asignificant scale position in Moscow.

The Group disposed of its non-coreVauxhallbusiness and the majority of its Volvo retailcentres in the UK for £17.0m and also soldits French operation to its managementteam for a consideration of £7.6m.

Capital expenditureThe Groupmaintained its policy of investingto improve the operating standards of itsretail centres and to develop new greenfieldcentres at a cost of £117.8m.The Groupalso continued with its implementationplan for a global SAP system for its operatingbusinesses.The first retail centre went livewith the system in February 2009.

Capital expenditure relating to SAP in 2008was £18.7m.

Minority interestsProfits attributable to minority interestsreduced to £3.9m in 2008 from £5.7min 2007.This was largely the result of theacquisition in March 2008 of the remaining24.9% interest in our St Petersburg businessesfrom the joint venture partner, the OlimpGroup.The Group’s minority interests atthe year end principally comprise a 33%minority holding in UABVitvela,Lithuaniaand 10% in SubaruAustralia.

Foreign currencyDuring 2008,the Group benefited by £22.9mfrom translation of its overseas profits intoSterling at the 2008 average exchange rate.

Following the recent fall in Sterling againstmost of the Group’s major currencies,aBoard decision has been taken to protectthe 2009 earnings by purchasing Sterlingcall options on amatching basis withoverseas earnings for all major territories,excluding Russia.

Cash flow and net debtThe Group’s operations continued to becash generative in 2008,with cash flow fromoperating activities of £183.7m.The tightmanagement of working capital in the faceof the downturn in the automotive sector hasbeen a key factor in the delivery of this result.

During the year, the Group returned nearly£90m to shareholders with £73.1m throughdividend payments and £16.0m througha programme of buying shares in themarket. In addition, the Group invested£264.0m in acquisitions and capitalexpenditure, funded by additionalborrowing facilities,and realised £54.5mfrom the disposal of businesses and otherassets.Overall, the Group had net debt of£407.8m at 31 December 2008 comparedto £213.5m at 31 December 2007.

PensionsDuring the year,and in line with the fundingprogramme agreed with theTrustees in2006, the Groupmade cash contributions tothe UK defined benefit scheme amountingto £20.8m.However,a reduction in themarket value of scheme assets during 2007has resulted in a net pension surplus at31 December 2008 of £6.0m,compared toa net surplus at the end of 2007 of £28.5m.

The Group has produced results in line withour expectations.The following Financialreview details the financial implications ofour operational activity and the risks whichwemonitor and take steps to mitigate.

Central costsUnallocated central costs for the full yearare £9.6m before exceptional items,downfrom £27.5m in 2007.This decrease is largelya reflection of the Group’s performanceduring the year which has resulted in nomanagement bonuses being paid andan overall credit being recorded in respectof share-based awards.

Joint ventures and associatesThe share of profit after tax of joint ventureshas decreased by £1.3m to £2.2m in 2008.This is mainly as a result of the acquisitionof the remaining stake in our joint venturein Djibouti,thereby converting it to a 100%owned subsidiary.

Exceptional itemsThe exceptional items consist of goodwillimpairment charges of £54.2m,a one offcharge of £28.3m in connection with therestructuring of certain Group businesses,(which is expected to deliver approximately£58m of annualised cost savings at 2009exchange rates) and a £3.6m exceptionaltax charge.The exceptional profit recordedin 2007 related to the sale of Inchroy (£12.0mprofit), InchcapeAutomotive and non-coreretail centres in the UK (£7.1m loss).

Net financing costsThe net financing cost of £52.0mwas £18.6mhigher than in 2007 and is a reflection of theGroup’s higher level of net debt.The majorityof the additional interest relates to thefinancing of the Musa acquisition, togetherwith the annualised cost of the acquisition oftheAudi and Peugeot businesses in Russia,the acquisitions in the Baltics in 2007 andthe higher level of working capital reflectingthe downturn in the markets.

TaxThe subsidiaries headline tax rate for theyear is 26% compared to 25% in 2007.Thisincrease arises due to the mix of profitsacross the territories in which we operate.The rate is expected to increase in 2009due once again to the profit mix,and tothe restricted ability to obtain tax relief onUK financing costs.

Delivering solid results despitethe unprecedented globaldecline in the car industry.

27

www.inchcape.com

Businessreview

01-37Governa

nce38-57

Financia

lstatem

ents58-120

Shareho

lderinfo

rmation

Insideback

cover