Effects of Gas Deregulation in Europe

23

1 Effects of Gas Deregulation in Europe Chris Walters Gas Strategies Consulting Ltd. Monday 7 th June

Transcript of Effects of Gas Deregulation in Europe

1

Effects of GasDeregulation in Europe

Chris Walters Gas Strategies Consulting Ltd.Monday 7th June

2© Gas Strategies Consulting Ltd

Disclaimer

The information on which this presentation is based derives from our own experience,knowledge, data and research. The opinions expressed and interpretations offered are thoseof Gas Strategies and have been reached following careful consideration. However, the gas

business is characterised by much uncertainty and all of our comments and conclusionsshould be taken in that light. Accordingly, we do not accept any liability for any reliance

which our clients may place on them.

3© Gas Strategies Consulting Ltd

Author

n Chris Walters – Consulting Manager Gas Strategies

nIn addition to managing Gas Strategies Consulting practice Chris is responsible formonitoring changes in the European energy market with a particular focus on liberalisationand regulation. He is also a key member of the team which produces gas and energydemand forecasts for our European Supply and Demand Service and contributes tonumerous consulting projects. Recent assignments include a study examining the strategicresponse to liberalisation adopted by key European market players, a study on thedevelopment of the wider European gas market (25 countries) from 1990 to the present dayand a study looking at LNG supply into Southern Europe and the potential for oversupply inthe region out to 2010. Chris has a Ph.D. in economic history from King's College London.

4© Gas Strategies Consulting Ltd

Gas Market Liberalisation - Aims

Aims“…[to create] a fully operational internal gas market,

in which fair competition prevails…”EU Gas Directive2003/55/EC

n to provide efficiently priced energy to allconsumers thereby benefiting the EuropeanUnion economy as a whole

5© Gas Strategies Consulting Ltd

Gas Market Liberalisation - Mechanisms

1st EU Gas Directive 98/30/EC (June 1998)Key Provisionsn Non discriminatory access to gas infrastructuren Accounts unbundling of monopoly activityn Market opening timetablen Dispute settlement authority

Directive flawed – failed push forward process

6© Gas Strategies Consulting Ltd

Gas Market Liberalisation – Mechanisms II

2nd European Gas Directive – 2003/55/ECAddresses some key weaknesses in 1st Directiven Regulated Third party access now mandatory

except for storage (Major Omission)n Vertically integrated players now forced to

separate monopoly businesses legallyn Market opening timetable brought forwardn Commission to benchmark progress annuallyn Independent regulator to be set up in every

country

7© Gas Strategies Consulting Ltd

Ranking of Market Opening by Key Indicators

Low

High

D SW Fr Lux Irl Au NL Be Dk Sp It UK

8© Gas Strategies Consulting Ltd

Ranking by Market Share Indicators

Low

High

Lux Sw Au It Dk Be NL Fr D Sp Irl UK

9© Gas Strategies Consulting Ltd

D

SW

Fr

Au

NL

Sp

It

UK

Low

High

Low HighRanking by Key Indicators

Ran

kin

g b

y M

arke

t S

har

es

Liberalisation Matrix – April 2004

10© Gas Strategies Consulting Ltd

Effects of Liberalisation – So Far

n General view that despite progress, there remain too manybarriers to a genuine competitive market

n However some progress has been made:n Significant switching from incumbent suppliers in some

markets – esp. Spainn Indications that gas prices particularly for large customers

may be becoming more competitive – evidence inpublished statistics though is still unclear

n Some incumbents increasingly under pressure in homemarkets from competition and legislative limitations onactivity (market share restrictions)

n Companies increasingly looking outside home marketsand core activity to mitigate risks at home

11© Gas Strategies Consulting Ltd

Strategic Response to Liberalisation

n Expansion by companies away from home gasmarkets

n Horizontal integration into electricity generationand sales

n Vertical Integration up and down the gas chain tosecure supplies and market and mitigate risk

n Greater consolidation of companies operating inthe European gas market -

To date Merger and Acquisition Activity in theEuropean utilities sector estimated at $328 billion

12© Gas Strategies Consulting Ltd

GDF – Geographic Expansion and HorizontalIntegration

1993 2004

13© Gas Strategies Consulting Ltd

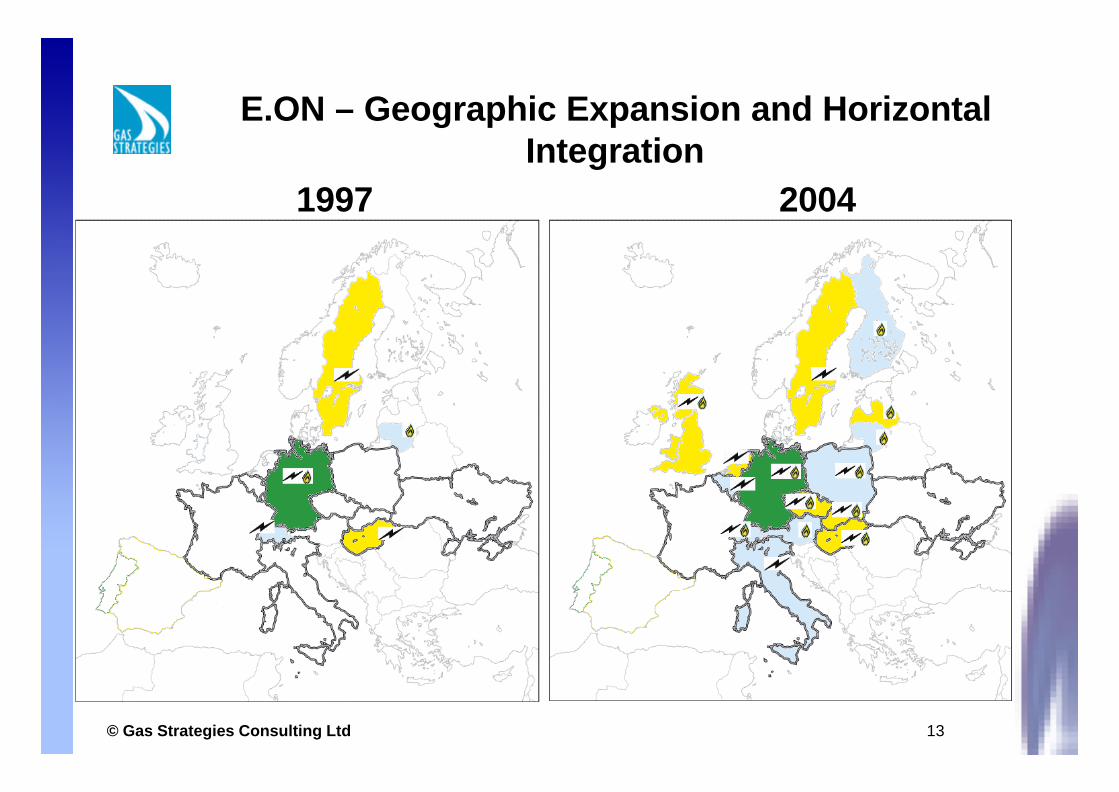

E.ON – Geographic Expansion and HorizontalIntegration

1997 2004

14© Gas Strategies Consulting Ltd

Matrix of Horizontal and Vertical Integrationversus Geographic Diversity

Wintershall

Gas Natural

Galp

OMV

GDF

ENI

EDFRWE

SuezE.ON

Centrica

Edison

Horizontal and Vertical Integration

Geo

grap

hic

Div

ersi

ty

HIGH

LOWHIGH

15© Gas Strategies Consulting Ltd

Creation of Pan-European Energy Companies

n Is the creation of Pan-European Energy companies goodor bad for the development of competition?

Only time will tell …n The benefits of harmonising gas regulation may appeal to

large companies operating across national boundariesButThe risk that national monopolies will be replaced by a pan

European oligopoly is a genuine possibility

Regulation and the use of EU Competition rules will be thedeciding factors

16© Gas Strategies Consulting Ltd

New Measures

n National regulatory authorities are not adequate toregulate a pan-European market

n The Madrid Forum provides a useful debate but carries noauthority

However two new initiatives could change the processn The Formation in November last year of the European

Regulatory Group for Electricity and Gasn The proposed directive dealing with Cross Border Trade

in GasAlso the Competition authorities have also been willing to

show their teeth – Ruhrgas and GdF Marathon settlement

17© Gas Strategies Consulting Ltd

Nirvana…?

n Effective harmonisation of regulation across memberstates

n Effective regulation of cross border infrastructuren Rigorous oversight and persecution of infringements of

monopoly or cartel behaviour by national and EUcompetition authorities could lead to

A fully functioning internal market for gas characterised by:n Liquid trading hubsn Gas on Gas pricingn Entry – Exit regimesn Fair and transparent cross border capacity allocationn UIOLI rules on all capacityn Fair and transparent balancing regimes

18© Gas Strategies Consulting Ltd

Conclusions

n The Internal Market is moving slowly towardliberalisation

n Timing and extent will depend heavily onconcerted regulatory pressure

n Competition authorities will play a key rolen Supply overhangs in key markets may boost

competition on a temporary basis

20© Gas Strategies Consulting Ltd

Supply Side Question

0%

100%

1990 1995 2000 2001

Norway Russia Algeria Other

EU 15 Imports by SourcenThe EU 15 countries aredependent on imports forover 47% of total supplynThe EU 25 close to 50%.n Import dependence isforecast to grow to 61% in2010, 75% in 2020 and over80% in 2030nRussia is currentlyresponsible for 50% ofimports to the EU 25

21© Gas Strategies Consulting Ltd

Supply Routes to Western EuropeCurrent and Possible

Russia & others

Iran, Turkmenistan, AzerbaijanAlgeria

Norway LNG

Pipe

Egypt & Middle EastLibya

22© Gas Strategies Consulting Ltd

Required New Supply v Potential New Projects

-100

0

100

200

300

400

500

600

2005 2010 2015 2020 2025 2030

Russia Yamal to Poland

Nigeria Trans-Sahara to Italy

Iran Iran 3-4

Russia Baltic to Germany

Turkmenistan To Slovakia

Iraq Turkey Corridor to Bulgaria

Venezuela New Plant

Iran New Plant

Qatar New Plant

Kazakhstan Kazakhstan to Slovak border

Norway Baltic Pipe to Poland

Libya New plant

Egypt To Egypt-Libya-Italy

Algeria GALSI to Italy/France

Algeria New train

Trinidad Atlantic 5&6

Iran Turkey Corridor to Bulgaria

Turkmenistan Turkmenistan to Slovak border

Norway Britpipe to UK

Angola Train 1

Norway Snøhvit 2

Egypt BG

Nigeria New plant

Venezuela Trains 1-2

Norway Snøhvit 1

Qatar New trains

Azerbaijan To Turkey/Greece/Italy

Libya Green Stream to Italy

Algeria Medgaz to Spain

New Supplies Required

23© Gas Strategies Consulting Ltd

0.00

1.00

2.00

3.00

0 100 200 300 400 500 600

BCM

$/M

MB

tu PipelineLNG

Estimated Supply Cost Curve NWE to 2020– Existing Technology