Economic - Banco de Portugal · challenges inherent to the ageing population must be overcome,...

122

Transcript of Economic - Banco de Portugal · challenges inherent to the ageing population must be overcome,...

Economic developments in Portuguese-speaking African countries and Timor-Leste2016|2017

Lisbon, 2017 • www.bportugal.pt

Economic developments in Portuguese-speaking African countries and Timor-Leste • Banco de Portugal Rua do Comércio,

148 | 1100-150 Lisboa • www.bportugal.pt • Edition International Relations Department • Design and printing

Communication Directorate | Image and Graphic Design Unit • ISSN 2182-3189 (online)

Contents

1. International environment | 7

1.1. Recent developments and outlook | 9

2. Economic developments in Portuguese-speaking African countries and Timor-Leste | 11

2.1. Angola | 14

2.2. Cabo Verde | 29

2.3. Guiné-Bissau | 45

2.4. Mozambique | 59

2.5. São Tomé e Príncipe | 75

2.6. Timor-Leste | 91

3. Portugal’s economic and financial relations with Portuguese-speaking African countries and Timor-Leste | 105

5

ForewordWith the goal of contributing to a better understanding of the current economic conditions in the Portuguese-speaking African countries and Timor-Leste, Banco de Portugal has released the publication Economic Developments In Portuguese-speaking African Countries and Timor-Leste since 1994, through which it presents key macroeconomic data for each economy and information on its economic and financial relations with Portugal.

Except for the 'International environment' chapter, the texts presented here were prepared on the basis of information received up to the end of July

2017, which in some cases may be subsequently revised, as it corresponds to estimates or preliminary data.

The cooperation of various entities contacted for the necessary data was key to the preparation of this report, as is always the case. These include the central banks of Angola, Cabo Verde, Mozambique, São Tomé and Príncipe and Timor-Leste and the national branch of the Central Bank of West African States in Guinea-Bissau.

October 2017

1.International environment

9

1.1. Recent developments and outlook World economic performance in the first half of 2017 justifies expectations of an upward revision of growth in 2017 and 2018.

Despite these signs of economic activity picking up again, many of the advanced economies continue to show low inflation, low productivity growth and an ageing population. The emerging and developing economies still face difficulties in returning to growth in per capita income and in adapting to the low-price environment for the commodities they export.

This adaptation is especially relevant given that international commodity prices continued their downward trend in the most recent months of 2017, most notably for oil, natural gas and some agricultural goods. These price reductions seem to be linked to higher than expected production or export levels by the United States and other global producers.

Along with the decreasing prices of important commodities, a set of factors contributed to a global low-inflation environment. For the advanced economies, these factors relate to falling unemployment being reflected weakly in increasing wages and to low productivity

growth. For the case of the emerging and developing economies, the general trend has been determined by the economic conjuncture in some of the major economies. This includes the price shock on foodstuffs in India and the economic slack accumulated during the recession in Brazil. South Africa and Russia are part of the falling inflation trend.

The resumption of capital flows towards the emerging economies showed signs of consolidation in the first half of 2017. The increase in capital flowing to the Chinese economy and the global recovery in portfolio investments are likely to have played a key role in that consolidation.

In the first half of 2017, growth in advanced economies has recovered more strongly than expected. For growth not to slow down as these economies approach their potential output, challenges inherent to the ageing population must be overcome, productivity growth must be revitalised and the working population's employability must be promoted. Expectations about a fiscal stimulus in the United States have not been confirmed, due to which moderate normalisation of US monetary policy is predicted.

Chart 1.1 • Real GDPAnnual percent change | Selected economies

Chart 1.2 • Inflation Year-on-year percent changes of the CPI | Selected economies

-5.0 0.0 5.0 10.0

World

Advanced economies

United States

Euro area

Japan

Emerging and developing economies

Emerging and developing Asia

Latin America and the Caribbean

Sub-saharan Africa

2015 2016 2017

0.0 5.0 10.0 15.0

World

Advanced economies

United States

Euro area

Japan

Emerging and developing economies

Emerging and developing Asia

Latin America and the Caribbean

Sub-saharan Africa

2015 2016 2017

Source: IMF, World Economic Outlook Database, July 2017.

International environment

BANCO DE PORTUGAL • Economic Developments in Portuguese-speaking African Countries and Timor-Leste • 2016 | 201710

In 2017, the emerging and developing economies as a whole have shown a slight increase in their growth rate.

This is the situation namely for emerging and developing Asia. The expansionary fiscal policy and the structural reforms under way in China resulted in a good performance in the first half of 2017. However, concern may intensify over the accumulation of debt. Symmetrically, the Indian economy should see its 2017 performance disrupted by tax and monetary reform with a potential positive impact over the medium term, but generating costs over the short term.

In Latin America and the Caribbean, the recovery should be particularly sharp in 2017. Similarly to the region as a whole, the outlook is favourable for Brazil and Argentina to transition from negative to positive growth rates, while growth in the Mexican economy is showing signs of slowing down.

After the slowdown in 2016 in Sub-Saharan Africa, growth is expected to accelerate in 2017, with a recovery in Nigeria – supported by rallying oil production and a solid performance from the agricultural sector – and strong growth prospects among fuel-importing countries.

After slowing down for years, international trade is showing signs of acceleration in 2017. Over the last few decades, trading has been an important driver of productivity growth. In a context where promoting economic growth faces structural challenges in advanced economies and where there is little room for fiscal stimulus in many emerging and developing economies, trade openness becomes one of the main instruments still available for creating a new structural and sustainable growth momentum.

Chart 1.3 • External current account Percentage of GDP | Selected economies

Chart 1.4 • Fiscal balance Percentage of GDP | Selected economies

-10.0 -5.0 0.0 5.0

Advanced economies

United States

Euro area

Japan

Emerging and developing economies

Emerging and developing Asia

Latin America and the Caribbean

Sub-saharan Africa

2015 2016 2017

-8.0 -6.0 -4.0 -2.0 0.0

Advanced economies

United States

Euro area

Japan

Emerging and developing economies

Emerging and developing Asia

Latin America and the Caribbean

Sub-Saharan Africa

2015 2016 2017

Source:IMF, World Economic Outlook Database, July 2017.

2.Economic developments in Portuguese- speaking African countries and Timor-Leste2.1. Angola

2.2. Cabo Verde

2.3. Guiné-Bissau

2.4. Mozambique

2.5. São Tomé e Príncipe

2.6. Timor-Leste

2.1. AngolaArea: 1,246,700 Km2

Capital city: Luanda

Population: 28.8 million (2016; source: UN)

Currency: Kwanza (AOA)

Unfavourable developments in the international oil price continued to stifle the Angolan economy during 2016. The economic slowdown continued, with no output growth in 2016. Inflationary pressures intensified over the last year, largely as a result of the depreciation of the kwanza. The economy showed deficits in the public and external accounts despite the contraction in imports of goods and services and in current expenditures.

BANCO DE PORTUGAL • Economic Developments in Portuguese-speaking African Countries and Timor-Leste • 2016 | 201714

The stabilisation of the international oil price at around USD 50 per barrel, significantly below the prices of 2011 to mid 2014, when they exceeded USD 100, continued to stifle the economy in Angola during 2016. The economy's high dependence on the oil sector, which accounted for around 40% of GDP in the years before the current shock, exposes economic performance strongly to that commodity's price, as was the case in 2008-2009.

The slowdown that began in 2014 has continued, with no output growth in 2016. The oil sector only grew by 0.8%, which compares to 6.4% in 2015. The non-oil economy performed negatively (-0.4%), with the industrial, construction and services sectors continuing to adjust to a context of lower private consumption and public investment. The difficulty in accessing foreign currencies led to declines in the supply of imported inputs used in the manufacturing process, considerably limiting the scope for import substitution. Projections for 2017 suggest economic growth of 1.3%, driven by the increase in public spending and an improvement in the terms of trade.

The ongoing deterioration of economic conditions placed the kwanza under strong downward pressure, with the currency falling 41% against the US dollar and 28% against the euro between July 2014 and April 2016, when the Angolan authorities repegged the exchange rate to the US dollar, after it had been abandoned in the second half of 2014. However, despite the gradual devaluation of the official exchange rate up to April 2016, it has continued to differ significantly from the parallel market exchange rate, with a spread estimated at 190% in November 2016 by the International Monetary Fund (IMF).

The combined effect of the kwanza's devaluation, the increase in fuel prices – following the removal of the energy subsidies – and the accommodative monetary conditions in the first half of 2016, have contributed to a sharp acceleration in the inflationary pace, with inflation reaching 41.9% in 2016, from 14.3% in 2015. The inflation rate has shown signs of slowing down in the first half of 2017, falling 10 percentage points versus the first half of 2016, driven in part by the stabilisation of the exchange rate against the US dollar (the kwanza's peg to the dollar had already been decisive in the economy's nominal stabilisation process from mid-2011).

The Angolan economy had twin deficits, for the third year in succession. The external current account improved in 2016, but stayed negative (-4.3% of GDP). Crude oil exports, which represent around 90% of total exports, fell again in 2016 (-17.9% on 2015), now accounting for less than half of the value exported in 2014. This decline in value of external sales led to a necessary adjustment in goods and services imports, which fell by 30% in 2016. In parallel, capital inflows into Angola during 2016 (worth 0.3% of GDP) proved insufficient to finance the current account deficit, leaving the remainder (4% of GDP) to be covered by official foreign exchange reserves. A new deterioration is expected in the external accounts in 2017, with a current account deficit projected of 6.1% of GDP.

Another of the main transmission mechanisms of the oil price shock to the Angolan economy came via the public finances, whose equilibrium depends heavily on the collection of taxes related to the oil industry (despite their share of total public revenue falling sharply, they nevertheless accounted for nearly half the total in 2016). For the third year in succession, the fiscal balance was negative in the year in review (-4.1% of GDP, deteriorating 0.8 percentage points from 2015). The 21.1% decline in oil revenue was the main factor explaining the fiscal position's deterioration in 2016, despite the containment of current expenditures. The State's General Budget for 2017 projects a new intensification in the deficit, expected to come to 5.7% of GDP.

The rising trend of public debt continued in 2016, reaching 71.9% of GDP at the end of the year (6.4 percentage points higher than in 2015), according to the IMF's most recent data. External debt has followed this trend, with a 7.2 percentage point estimated increase, bringing total external debt to 42.6% of GDP.

Repercussions of the economic slowdown have also spread to the financial system. The level of non-performing loans continues to increase, reaching 13.1% of total credit at the end of 2016, largely reflecting the corporate sector's greater difficulties in servicing its debt. Solvency levels among the financial institutions have also shown a gradual deterioration, with five banks having insufficient capital in September 2016. Developments in the solvency ratios may

15

however not yet fully reflect the deterioration in asset quality, given that certain loan restructuring operations have been extended to non-viable companies (source: IMF). Despite these less positive developments, the sector's profitability has recovered since 2014 and the dollarisation level in the banking system seems to have stabilised more recently at around 30% of assets and liabilities.

The external competitiveness gains achieved in 2015, in real terms, were reversed in 2016, as a result of the significant spreads between Angola's inflation and that of its main trading partners. Despite the 14.4% fall in the nominal effective exchange rate index (EERI), which was due to the depreciation of the kwanza against the currencies

of Angola's main trading partners, the real EERI appreciated 19.1% in 2016, particularly from April, when the price of the kwanza stabilised against the US dollar.

Broad money expanded in 2016 at a pace near that of the last few years (expansion of 14.1%). However, the main liquidity expansion/contraction factors changed compared to the year before, with credit to the economy falling and general government financing becoming one of the key drivers of broad money expansion. The increased value in kwanzas of the foreign exchange reserves, despite the reduction in their US dollar value, was the main liquidity expansion factor in 2016.

Table 2.1 • Main economic indicators2013 2014 2015 2016 2017

Est. Est. Est. Est. Proj.

Real GDP (annual % change) 6.8 4.8 3.0 0.0 1.3

7.7 7.5 14.3 41.9 15.8

13.2 16.2 11.8 14.1 –

6.7 -3.0 -10.0 -4.3 -6.1

0.3 -6.6 -3.3 -4.1 -5.7

22.6 28.4 35.3 42.6 –

Inflation (year-on-year % change)

Broad money (annual % change)

Current account (% of GDP)

Fiscal balance (% of GDP)

External public debt (% of GDP)

Sources (for the subsequent charts also): Banco Nacional de Angola, Ministry of Finance of Angola, European Central Bank, International Monetary Fund and Organisation for Economic Co-operation and Development.

Angola

BANCO DE PORTUGAL • Economic Developments in Portuguese-speaking African Countries and Timor-Leste • 2016 | 201716

Chart 2.1 • Real GDP Annual % change

Chart 2.2 • Inflation Annual % change in the CPI

2.43.4 3.9

5.2

6.8

4.8

3.0

0.01.3

0

2

4

6

8

10

2009 2010 2011 2012 2013 2014 2015(est.)

2016(est.)

2017(proj.)

0

10

20

30

40

50

2009 2010 2011 2012 2013 2014 2015 2016 2017Year-on-year % change Average % change

The stabilisation of the oil price at levels considerably below those of 2014 continues to stifle economic activity in Angola.

The upward trend of inflation intensified in 2016, reflecting the devaluation of the kwanza, increased fuel prices and accommodative monetary conditions in the first half of the year. By the end of 2016, inflation reached its highest level for a decade.

Chart 2.3 • External accounts % of GDP, average oil price per barrel in USD

Chart 2.4 • External public debt and foreign exchange reserves USD billions

-40

0

40

80

120

-20%

0%

20%

40%

60%

2009 2011 2013 2015(est.)

2017(proj.)

Trade balance Current accountOverall balance Avg. oil price per barrel (Brent)

0

10

20

30

40

50

2009 2010 2011 2012 2013 2014(est.)

2015(est.)

2016(est.)

Total external debt Gross foreign exchange reservesTotal external debt (% of GDP)

The external deficit fell by more than half in 2016, with imports falling in a context of increased difficulty in accessing foreign currencies. Although the impact of the oil price shock had been greater in 2015, the average price per barrel of Angolan oil fell 19% in 2016.

External debt has continued to increase, reaching 43% of GDP. The level of foreign exchange reserves stabilised, largely as a result of the decision by the authorities to allow the kwanza to devalue.

Chart 2.5 • Crude oil exportsDestinations as a percentage, total in USD billions

Chart 2.6 • Goods imports Origins as a percentage, total in USD millions

0

15

30

45

60

75

0%

20%

40%

60%

80%

100%

2009 2010 2011 2012 2013 2014 2015

China United States IndiaCanada Other Total

0

10

20

30

0%

20%

40%

60%

80%

100%

2009 2010 2011 2012 2013 2014 2015Portugal China United StatesBelgium Other Total

The geographical distribution of exports has remained relatively stable. External sales of crude oil, the main source of foreign currency, fell 17.9% in 2016, totalling USD 25.8 billion.

China replaced Portugal as the main supplier of goods in 2015. The value of imports of goods fell again in 2016, now representing half the value of the goods acquired from abroad in 2014.

17

Chart 2.7 • Public revenue % of GDP

Chart 2.8 • Public expenditure % of GDP

0

10

20

30

40

50

2009 2011 2013 2015(est.)

2017(budg.)

Oil revenue Other tax revenue Non-tax revenue

0

10

20

30

40

50

2009 2011 2013 2015(est.)

2017(budg.)

Compensation of employees Goods and services Interest Transfers Investment

Public revenue fell 8.7% in 2016, driven above all by the 21.1% fall in oil revenue. This component now accounts for less than half of total public revenue.

Public expenditure continued to fall in 2016, mainly due to the falling trend in goods and services spending. Offsetting this was the increase in interest charges on public debt, equating to 2.9% of GDP in 2016.

Chart 2.9 • Public accounts % of GDP

Chart 2.10 • Financial stability indicators

-10-505

101520

2009 2011 2013 2015(est.)

2017(budg.)

Current balance Overall balance

-5%5%

15%25%35%

Capital adequacy

Tier 1 ratio

Non-performingloans to total

credit

NLP net of provisions(% core capital)

Return on equity

Return on assets

2012 2014 2016

The public finances closed the 2016 financial year in negative territory for the third year in succession, with the deficit as a percentage of GDP increasing by 0.8 percentage points. The State's General Budget for 2017 projects a new intensification in the public deficit.

The challenging economic and financial context the country faces is reflected in the deterioration of the financial stability indicators, with certain financial institutions requiring recapitalisations.

Chart 2.11 • Liquidity expansion/contraction factors Changes in % of initial stock of broad money

Chart 2.12 • Effective exchange rateIndexes: 100 = 2000, monthly averages

-40-200

20406080

2009 2010 2011 2012 2013 2014 2015 2016(est.)

2017(May)

(Net) foreign assets (Net) claims on gen. gov.Credit to the economy Other (net) domestic assetsBroad money

225

250

275

300

325

350

5

7

9

11

13

2009 2010 2011 2012 2013 2014 2015 2016 2017Nominal index (left-hand scale) Real index (right-hand scale)

(appreciation: +; depreciation: -).

Broad money expanded in 2016 at a pace near that of the last few years. The increased value in the foreign exchange reserves (expressed in kwanzas) and increased credit to the Government were the main liquidity expansion factors in 2016.

Despite the devaluation of the kwanza in 2016, the spiking general price level resulted in the Angolan economy losing external competitiveness significantly, in real terms.

Angola

BANCO DE PORTUGAL • Economic Developments in Portuguese-speaking African Countries and Timor-Leste • 2016 | 201718

Table 2.2 • Economic indicators

2012 2013 2014 2015 2016 2017

Est. Est. Est. Est. Proj. Est. Proj. Est.

Output and pricesNominal GDP AOA billions 11,011 12,056 12,462 12,323 13,786 15,729 20,072 –

89.7 94.0 95.3 92.4 – 86.8 – –

115.4 124.9 126.7 102.7 81.5 96.1 121.0 –

5.2 6.8 4.8 3.0 1.3 0.0 1.3 –

4.5 -1.1 -2.6 6.4 – 0.8 1.5 –

5.5 10.9 8.2 1.6 – -0.4 1.3 –

9.0 7.7 7.5 14.3 [11.0-13.0] 41.9 15.8 31.9 June

10.3 8.8 7.3 10.3 – 32.4 – 37.8 June

45.9 40.2 35.3 27.3 25.5 19.5 18.3 –

37.3 30.1 23.8 15.4 12.3 9.5 8.4 –

39.3 39.9 41.9 30.6 31.2 23.6 24.0 –

28.9 28.5 29.4 24.6 25.2 19.1 19.0 –

10.4 11.4 12.5 6.0 5.9 4.5 5.0 –

6.6 0.3 -6.6 -3.3 -5.7 -4.1 -5.7 –

9.2 3.0 -2.4 -2.2 -5.7 -4.1 -5.7 –

8.2 -1.2 -1.1 15.8 – 11.3 – -14.8 May

23.9 10.5 0.7 17.7 – -0.9 – -1.9 May

5.7 13.2 16.2 11.8 – 14.1 – -3.4 May

15.3 15.1 17.4 15.4 – 15.8 – 15.7 May

3.8 3.9 4.4 5.2 – 5.2 – 6.2 May

2.4 2.3 2.1 2.5 – 2.1 – 2.2 May

18.3 19.5 19.8 19.8 – 19.2 – –

6.8 9.8 11.7 11.6 – 13.1 – –

12.5 10.9 4.9 12.9 – 15.6 – –

5.6 -3.2 -12.5 -43.4 -15.3 -16.9 14.3 –

4.4 7.3 8.8 -29.1 -5.5 -30.0 25.2 –

41.0 33.5 24.1 12.2 9.5 14.0 11.6 –

12.0 6.7 -3.0 -10.0 -14.9 -4.3 -6.1 –

32.2 32.2 27.9 24.4 – 24.4 – 21.6 May

17.6 21.2 27.0 32.7 – 37.0 – –

22.6 28.2 35.9 36.3 – 40.9 – –

19.6 22.6 28.4 35.3 – 42.6 – –

122.7 128.2 130.7 133.3 – – – –

95.4 96.5 98.3 120.0 – 163.7 – 165.9 June

-0.9 -2.4 -2.0 -21.0 – -14.4 – -2.3 June

4.6 2.1 3.7 -11.3 – 19.1 – 9.6 June

EUR billions

USD billions

Real GDP Annual % change

Oil sector Annual % change

Other sectors Annual % change

Inflation (CPI-Luanda) Year-on-year % changeAverage annual % change

Public finances

Total revenue % of GDP

Oil revenue % of GDP

Total expenditure % of GDP

Current expenditure % of GDP

Capital expenditure % of GDP

Overall balance (commitment basis) % of GDP

Overall balance (cash basis) % of GDP

Money and credit

Net foreign assets Annual % change

Credit to the economy Annual % change

Broad money (M3) Annual % change

Interest rates

Credit in national currency(a) (180 d) Annual rate

Deposits in national currency (180 d)

Annual rate

Deposits in foreign currency (180 d) Annual rate

Financial stability

Capital adequacy Percentage

Non-performing loans/total loans % of total loans

Return on equity Percentage

Balance of paymentsExports (current USD) Annual % change

Imports (current USD) Annual % change

Trade balance % of GDP

Current account % of GDP

Foreign reserves (gross) USD billions

External public debtTotal external public debt EUR billions

USD billions

% of GDP

Exchange rates

Bilateral rate EUR/AOA Average rate

Bilateral rate USD/AOA Average rate

Nominal EERI [appreciation: +](b) Annual % change

Real EERI [appreciation: +](b) Annual % change

Sources: Banco Nacional de Angola, Ministry of Finance of Angola, European Central Bank, International Monetary Fund, Organisation for Economic Co-operation and Development and Banco de Portugal calculations.Notes: (a) Credit granted to enterprises. (b) Effective exchange rate index (EERI), calculated on the basis of exchange rates applied to the currencies of the four major trading partners over the 2010/14 period.

19

Table 2.3 • Gross domestic productCurrent prices, AOA billions

2012 2013 20142015 2016 2017

Est. Proj. Est. Proj.

Agriculture 776 1,195 1,410 1,623 1,871 – –

27 30 38 47 48 – –

89 95 81 121 146 – –

5,160 5,018 4,414 2,958 3,283 – –

752 884 1,012 1,132 1,324 – –

947 1,109 1,267 1,499 1,673 – –

14 20 25 29 41 – –

2,428 2,813 3,215 3,755 4,147 – –

819 892 1,001 1,157 1,253 – –

11,011 12,056 12,462 12,323 13,786 15,729 20,072

89.7 94.0 95.3 92.4 – 86.8 –

115.4 124.9 126.7 102.7 81.5 96.1 121.0

12.6 9.5 3.4 -1.1 11.9 27.6 27.6

5.2 6.8 4.8 3.0 1.3 0.0 1.3

4.5 -1.1 -2.6 6.4 – 0.8 1.5

5.5 10.9 8.2 1.6 – -0.4 1.3

Fishing and related products

Diamonds and other

Oil

Manufacturing

Construction

Energy

Market services

Other

Gross domestic product (market prices)

Memo items:

Nominal GDPmp (EUR billions)

Nominal GDPmp (USD billions)

Nominal GDPmp (AOA, annual % change)

Real GDP (annual % change)

Oil sector

Other sectors

Sources: Banco Nacional de Angola, International Monetary Fund and Banco de Portugal calculations.

Angola

BANCO DE PORTUGAL • Economic Developments in Portuguese-speaking African Countries and Timor-Leste • 2016 | 201720

Table 2.4 • Consumer price indexPer cent

Monthly change Cumulative change Year-on-year change Average change

[1] [2] [3] [4]

2003 December2004 December2005 December

2006 December

2007 December

2008 December

2009 December

2010 December

2011 December

2012 December

2013 December

2014 December

2015 December

2016 December

2015 January

February

March

April

May

June

July

August

September

October

November

December

December (proj.)

2016 January

February

March

April

May

June

July

August

September

October

November

December

December (proj.)

2017 January

February

March

April

May

June

December (proj.)

Sources: Banco Nacional de Angola, International Monetary Fund and Banco de Portugal calculations.Notes: [1] month (n) / month (n-1); [2] month (n) / previous December; [3] month (n) / month (n) of the previous year; [4] last 12 months / previous 12 months.

– 76.6 76.6 98.2– 31.0 31.0 43.5

– 18.5 18.5 23.0

– 12.2 12.2 13.3

– 11.7 11.7 12.2

– 13.2 13.2 12.5

– 14.0 14.0 13.7

– 15.3 15.3 14.5

– 11.4 11.4 13.5

– 9.0 9.0 10.3

– 7.7 7.7 8.8

– 7.5 7.5 7.3

– 14.3 14.3 10.3

– 41.9 41.9 32.4

0.7 0.7 7.4 7.2

0.8 1.5 7.7 7.3

0.6 2.1 7.9 7.3

0.9 3.0 8.2 7.4

1.2 4.2 8.9 7.6

1.3 5.5 9.6 7.8

1.3 7.0 10.4 8.1

1.1 8.2 11.0 8.4

1.2 9.5 11.7 8.8

1.4 11.0 12.4 9.2

1.3 12.5 13.3 9.7

1.6 14.3 14.3 10.3

– – 9.0 –

3.4 3.4 17.3 11.1

3.3 6.8 20.3 12.2

3.4 10.5 23.6 13.5

3.1 13.9 26.4 15.0

3.5 17.9 29.2 16.8

3.3 21.7 31.8 18.7

4.0 26.7 35.3 20.8

3.3 30.8 38.2 23.1

2.1 33.6 39.4 25.4

1.8 36.0 40.0 27.8

2.1 38.9 41.1 30.1

2.2 41.9 41.9 32.4

– – [11.0-13.0] –

2.3 2.3 40.4 34.3

2.6 4.9 39.4 35.8

2.2 7.3 37.8 37.0

2.0 9.4 36.3 37.7

1.8 11.4 34.1 38.0

1.6 13.1 31.9 37.8

– – 15.8 –

21

Table 2.5 • Balance of paymentsUSD millions

2012 2013 2014 20152016 2017

Proj. Est. Proj.

Current account 13,853 8,348 -3,748 -10,273 -12,130 -4,101 -7,428

47,376 41,903 30,590 12,488 7,738 13,433 13,986

71,093 68,247 59,170 33,181 27,550 27,466 31,580

69,716 66,902 57,642 31,895 25,864 26,210 30,220

68,871 65,611 56,364 31,394 – 25,784 29,725

1,159 1,167 1,335 1,066 – 1,058 1,132

218 177 193 220 – 198 228

-23,717 -26,344 -28,580 -20,693 -19,811 -14,033 -17,594

-31,761 -31,430 -32,126 -21,928 -18,906 -16,763 -20,441

-21,339 -21,530 -23,276 -16,020 -14,430 -11,390 -14,550

780 1,316 1,681 1,256 1,621 1,156 1,139

-22,119 -22,846 -24,958 -17,276 -16,051 -12,546 -15,689

-4,595 -4,924 -5,628 -4,204 – – –

-6,230 -5,049 -6,673 -3,107 – – –

-8,908 -9,265 -10,050 -7,185 – – –

-10,422 -9,900 -8,850 -5,908 -4,476 -5,373 -5,891

-662 -1,090 -1,066 -1,287 -988 – –

-9,722 -9,331 -7,850 -4,292 -3,621 – –

-1,762 -2,124 -2,211 -834 -963 -771 -973

-8,885 -8,203 -486 6,908 6,511 252 4,4281 0 2 6 0 0 0

-9,639 -13,164 -2,331 8,235 7,121 -3,362 641

753 4,961 1,844 -1,334 -611 3,614 3,787

-462 199 336 354 0 0 0

4,506 344 -3,896 -3,010 -5,619 -3,850 -3,000

-4,506 -344 3,896 3,010 – 3,850 3,000

-4,505 -344 -3,896 3,010 – 3,850 3,000

-1 0 0 0 – 0 0

0 0 0 0 – 0 0

41.0 33.5 24.1 12.2 9.5 14.0 11.6

12.0 6.7 -3.0 -10.0 -14.9 -4.3 -6.1

Trade balance

Exports (f.o.b.)

Oil sector

of which: Crude oil

Diamonds

Other

Imports (f.o.b.)

Services and income

Services (net)

Credit

Debit

of which: Transportation and travel

Construction

Technical assistance

Income (net)

of which: Interest on public debt

Dividends and profits

Current transfers (net)

Capital and financial accountsCapital transfers (net)

Foreign direct investment (net)

Other net capital

Errors and omissions

Overall balance

FinancingChange in official reserves (increase: - )

Exceptional financing(a)

Financing gap

Memo items:

Trade balance (% of GDP)

Current account (% of GDP)

Sources: Banco Nacional de Angola, Ministry of Finance of Angola, International Monetary Fund and Banco de Portugal calculations.Notes: (a) Mainly, change in arrears and debt forgiveness or rescheduling .

Angola

BANCO DE PORTUGAL • Economic Developments in Portuguese-speaking African Countries and Timor-Leste • 2016 | 201722

Table 2.6 • Goods exportsProducts, USD millions | Destinations, % of total

2010 2011 2012 2013 20142015 2016 2010

a 2015

Est. Est. Est.

Total exports

Crude oilRefined oil products and gas

Diamonds

Other

Exports by destination(a)

Canada

China

France

India

Portugal

South Africa

Taiwan

United States

Other

Sources: Banco Nacional de Angola, International Monetary Fund and Banco de Portugal calculations.Note: (a) Crude oil exports only.

Table 2.7 • Goods importsProducts, USD millions | Origins, % of total

2010 2011 2012 2013 20142015 2016 2010

a 2015

Est. Est. Est.

Total imports 16,667 20,228 23,717 26,344 28,580 20,693 14,033 –

16,667 20,228 23,717 26,344 28,587 20,052 – –

7.3 6.0 6.7 5.5 6.0 6.6 – 6.3

5.1 4.2 4.4 4.3 4.4 4.0 – 4.4

8.5 7.6 9.2 10.1 12.2 14.3 – 10.4

14.5 15.4 16.4 16.4 15.3 13.1 – 15.3

4.0 3.8 3.8 3.7 3.6 3.8 – 3.8

5.1 2.9 2.4 3.4 4.0 3.2 – 3.5

7.4 8.2 5.5 4.7 6.8 6.5 – 6.4

48.1 52.0 51.7 51.8 47.7 48.6 – 50.0

of which: SNA(a)

Imports by originBelgium

Brazil

China

Portugal

South Africa

United Kingdom

United States

Other

Sources: Banco Nacional de Angola, International Monetary Fund and Banco de Portugal calculations.Note: (a) Data from the National Customs Service of Angola.

50,595 67,310 71,093 68,247 59,170 33,181 27,466 –

48,629 64,539 68,871 65,611 56,364 31,394 25,784 –

722 1,052 845 1,291 1,278 501 426 –

976 1,205 1,159 1,167 1,335 1,066 1,058 –

267 514 218 177 193 220 198 –

5.8 8.7 5.0 5.0 4.6 3.3 – 5.6

42.8 37.7 49.6 48.3 48.5 44.8 – 45.4

3.7 3.2 1.6 2.0 3.5 5.0 – 2.9

10.1 10.7 10.1 10.3 8.3 8.5 – 9.8

1.8 2.4 2.5 4.7 3.4 3.8 – 3.1

3.1 2.6 4.2 2.7 3.4 4.3 – 3.3

4.8 8.2 6.1 5.3 4.6 4.5 – 5.8

18.1 15.9 8.7 7.0 3.5 3.1 – 9.7

9.8 10.6 12.2 14.6 20.1 22.7 – 14.3

23

Table 2.8 • External public debt and foreign exchange reservesUSD millions

2012 2013 20142015 2016

Est. Est.

1. Net foreign assets 32,937 31,941 30,191 26,386 23,952

32,166 32,231 27,948 24,420 24,438

22,583 28,178 35,933 36,279 40,900

13,786 18,143 26,474 26,612 –

12,813 16,590 24,005 23,345 –

974 1,553 2,470 3,267 –

6978 8,433 7,788 7,906 –

1,813 1,598 1,666 1,756 –

6 4 4 4 –

28.5 25.6 23.8 25.7 24.9

27.9 25.8 22.1 23.8 25.4

19.6 22.6 28.4 35.3 42.6

of which: Foreign exchange reserves (gross)

2. External public debt (including arrears)

Commercial

Banking

Enterprises

Official bilateral

Official multilateral

Fees

Memo items:

Net foreign assets (% of GDP)

Gross foreign exchange reserves (% of GDP)

Total external debt (% of GDP)

Sources: Banco Nacional de Angola, International Monetary Fund and Banco de Portugal calculations.

Angola

BANCO DE PORTUGAL • Economic Developments in Portuguese-speaking African Countries and Timor-Leste • 2016 | 201724

Table 2.9 • Government operationsAOA billions

2012 2013 20142015 2016 2017

Est. Budg. Est. l.e.(a) Budg.

1. Total revenue 5,054 4,849 4,403 3,367 3,515 3,075 87.5 3,6684,826 4,602 4,098 3,042 3,235 2,762 85.4 3,404

4,103 3,630 2,970 1,898 1,690 1,498 88.7 1,695

723 972 1,128 1,144 1,545 1,264 81.8 1,709

226 245 303 324 279 312 111.7 264

2 2 2 1 0 1 – 0

4,329 4,816 5,222 3,774 4,296 3,718 86.6 4,8083,184 3,437 3,667 3,038 3,480 3,009 86.5 3,813

1,031 1,155 1,319 1,390 1,497 1,496 99.9 1,614

1,297 1,228 1,248 787 995 510 51.2 1,035

105 99 150 249 307 463 150.7 484

68 59 88 143 152 186 122.1 262

37 40 62 106 155 277 178.7 222

752 955 950 612 680 540 79.4 680

1,145 1,379 1,555 736 816 709 86.9 995

725 32 -819 -407 -781 -643–

-1,140

289 324 517 138 0 0 – 0289 324 – – 0 – – 0

0 0 – – 0 – – 0

1,014 356 -302 -269 -781 -644 – -1,140

-1,014 -356 302 269 781 644 – 1,140218 183 438 241 1,059 653 – 990

384 380 732 579 1,518 1,400 – 1,564

-166 -197 -294 -338 -459 -747 – -575

-1,231 -539 -136 29 -278 -9 – 150

-432 -597 – – – – – –

-800 58 – – – – – –

6.6 0.3 -6.6 -3.3 -5.7 -4.1 – -5.7

Tax revenue

Oil revenue

Non-oil revenue

Non-tax revenue

Grants

2. Total expenditureCurrent expenditure

Compensation of employees

Goods and services

Debt interest

Domestic

External

Transfers and subsidies

Capital expenditure

3. Overall balance (commitment basis) [ 1. - 2. ]

4. Change in arrears (net)Domestic(b)

External interest

5. Overall balance (cash basis) [ 3. + 4. ]

6. FinancingExternal financing (net)

Disbursements

Amortisation

Domestic financing (net)

Bank financing

Non-bank financing (incl. errors and omissions)

Memo item:

Overall balance, commitment basis (% of GDP)

Sources: Banco Nacional de Angola, Ministry of Finance of Angola, International Monetary Fund and Banco de Portugal calculations.Notes: (a) Level of budget execution (%). (b) Net of changes in arrears to suppliers (expenditure) and changes in Sonangol's arrears to the Treasury (revenue).

25

Table 2.10 • Monetary surveyAOA billions

2012 2013 2014 20152016 2016/2015 2017 May 2017/2016

Est. [1] [2] May [1] [2]

Net foreign assets

USD billions

Banco Nacional de Angola

Net international reserves

Gross reserves

USD billions

Short-term liabilities

Other foreign assets (net)

Commercial banks

Net domestic assetsDomestic credit (net)

Claims on general government (net)Credit to the economy

Other domestic assets (net)

Total assets

Broad money (M3)

Money and quasi-money (M2)

Money

Currency in circulation

Demand deposits

in national currency

in foreign currency

Quasi-money

Time deposits in national currencyTime deposits in foreign currency

Other financial instruments

Sources: Banco Nacional de Angola, International Monetary Fund and Banco de Portugal calculations.Notes: [1] Percentage changes from the end of the previous year. [2] Changes in % of initial stock of broad money (liquidity expansion/contraction factors)..

3,155 3,116 3,082 3,570 3,974 11.3 7.1 3,385 -14.8 -9.0

33 32 30 26 24 -9.2 – 20 -14.8 –

3,017 3,097 2,889 3,361 3,637 8.2 4.8 3,070 -15.6 -8.7

2,954 3,041 2,788 3,284 3,550 8.1 4.7 2,991 -15.8 -8.6

3,081 3,145 2,853 3,304 4,054 22.7 13.1 3,579 -11.7 -7.3

32 32 28 24 24 0.1 – 22 -11.7 –

-127 -103 -66 -21 -504 – -8.5 -589 16.7 -1.3

63 56 102 78 87 12.0 0.2 80 -8.3 -0.1

138 19 193 209 337 60.8 2.2 314 -6.6 -0.3

728 1,280 2,028 2,141 2,545 18.8 7.1 2,915 14.6 5.7

1,705 2,260 3,016 3,821 4,520 18.3 12.2 4,939 9.3 6.4

-943 -666 69 352 1,083 207.9 12.8 1,567 44.7 7.4

2,648 2,926 2,947 3,469 3,437 -0.9 -0.6 3,372 -1.9 -1.0

-977 -980 -988 -1,680 -1,975 17.6 -5.2 -2,024 2.5 -0.8

3,883 4,397 5,110 5,712 6,519 14.1 – 6,300 -3.4 –

3,883 4,397 5,110 5,712 6,519 14.1 – 6,300 -3.4 –

3,749 4,395 5,103 5,704 6,516 14.2 – 6,297 -3.4 –

2,272 2,585 3,097 3,420 3,845 12.4 – 3,608 -6.2 –

244 276 340 381 386 1.4 – 345 -10.8 –

2,028 2,309 2,757 3,039 3,459 13.8 – 3,264 -5.6 –

1,062 1,470 1,905 2,264 2,576 13.8 – 2,428 -5.7 –

966 839 852 775 883 13.9 – 835 -5.4 –

1,477 1,810 2,007 2,284 2,671 16.9 – 2,689 0.7 –

721 902 1,167 1,258 1,553 23.5 – 1,553 -0.0 –

756 908 840 1,026 1,118 9.0 – 1,136 1.6 –

134 2 7 8 4 -53.4 – 3 -12.7 –

Angola

BANCO DE PORTUGAL • Economic Developments in Portuguese-speaking African Countries and Timor-Leste • 2016 | 201726

Table 2.11 • Interest ratesAnnual rates, per cent

2012 2013 2014 2015 2016 2017

Dec. Dec. Dec. Dec. Mar. Jun. Sep. Dec. Mar. May

Deposits

(in national currency)

Demand deposits 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

3.1 3.5 3.5 5.0 5.1 5.4 5.6 6.8 6.0 6.4

3.8 3.9 4.4 5.2 5.0 4.8 5.0 5.2 5.2 6.1

4.8 5.8 4.5 3.9 3.8 4.1 4.0 3.9 3.9 3.9

6.7 4.9 5.2 4.6 5.0 5.0 5.1 4.8 4.9 5.0

0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

1.8 2.0 1.9 2.3 2.0 2.0 2.0 2.0 2.1 2.1

2.4 2.3 2.1 2.5 2.4 2.3 2.4 2.1 2.1 2.2

2.8 2.8 2.6 3.1 3.1 2.9 3.2 2.9 2.9 2.9

3.5 5.0 2.6 4.6 4.8 4.9 4.9 4.8 4.9 4.8

15.3 15.0 17.3 15.4 15.6 15.8 15.8 15.8 15.4 15.6

14.3 13.8 13.8 15.2 15.2 15.1 15.1 19.7 15.3 15.6

15.0 13.1 13.6 14.8 14.0 14.6 14.9 15.1 15.4 16.4

8.9 11.8 11.4 10.0 16.2 16.6 20.0 0.0 9.9 6.7

11.5 12.1 10.6 13.0 – – 11.6 8.4 6.7 6.7

11.3 9.8 10.0 9.8 8.4 7.9 8.5 8.7 9.0 8.8

20.0 10.3 9.8 15.0 15.0 16.0 20.0 20.0 20.0 20.0

10.2 9.2 9.0 11.0 14.0 16.0 16.0 16.0 16.0 16.0

11.5 10.3 9.8 12.5 16.0 20.0 20.0 20.0 20.0 20.0

1.5 0.8 1.8 0.0 2.3 2.3 7.3 0.0 0.0 0.0

6.2 4.7 6.1 11.3 11.0 13.9 14.5 23.4 23.7 22.4

9.0 7.7 7.5 14.3 23.6 31.8 39.4 41.9 37.8 34.1

Time deposits

Up to 90 days

91-180 days

181-365 days

Over 1 year

(in foreign currency)

Demand deposits

Time deposits

Up to 90 days

91-180 days

181-365 days

Over 1 year

Credit (to enterprises)

(in national currency)

Up to 180 days

181-365 days

Over 1 year

(in foreign currency)

Up to 180 days

181-365 days

Over 1 year

BNA intervention rates

Rediscount

Reference rate

Standing facilities

Liquidity provision facility

Overnight deposit facility

LUIBOR(a) overnight

Memo item:Inflation (y-o-y % change)

Source: Banco Nacional de Angola.Notes: (a) Luanda Interbank Offered Rate (weighted average rate of liquidity-providing operations without collateral, applied by banks in the interbank money market).

27

Table 2.12 • Financial stability indicatorsPer cent

2012 2013 2014 2015 2016

Dec. Dec. Dec. Dec. Dec.

SolvencyCapital adequacy

Tier 1 ratio

Credit risk

Non-performing loans to total loans

Non-performing loans net of provisions (% of core capital)

Credit in foreign currency (% of total credit)

Profitability

Return on equity

Return on assets

Liquidity risk

Loan-to-deposit ratio

Liquid assets/total assets

Foreign currency-denominated liabilities/total liabilities

Sources: Banco Nacional de Angola and International Monetary Fund.

18.3 19.5 19.8 19.8 19.2

13.6 14.3 13.9 13.8 14.3

6.8 9.8 11.7 11.6 13.1

11.6 22.3 32.8 19.6 27.4

42.7 37.8 27.4 30.8 29.5

12.5 10.9 4.9 12.9 15.6

1.6 1.4 0.6 1.7 2.2

65.5 63.3 59.9 59.0 51.6

26.3 30.1 33.9 39.7 46.3

50.7 43.0 33.1 33.5 34.4

Angola

BANCO DE PORTUGAL • Economic Developments in Portuguese-speaking African Countries and Timor-Leste • 2016 | 201728

Table 2.13 • Exchange ratesAverage rates

EERI(a) Index: 100 = 2000

EUR/AOA USD/AOA Nominal Real

2003200420052006200720082009201020112012201320142015

2016

2015 JanuaryFebruaryMarchAprilMayJuneJulyAugustSeptemberOctoberNovemberDecember

2016 JanuaryFebruaryMarchAprilMayJuneJulyAugustSeptemberOctoberNovemberDecember

2017 JanuaryFebruaryMarchAprilMayJune

Sources: Banco Nacional de Angola, European Central Bank, Organisation for Economic Co-operation and Development and Banco de Portugal calculations.Note: (a) Effective exchange rate index, calculated on the basis of official exchange rates applied to the currencies of the four main trading partners over the 2010/14 period. An increase/decrease in the EERI (nominal or real) corresponds to an appreciation/depreciation of the kwanza.

86.1 74.3 13.3 133.7104.3 83.4 11.9 165.4108.4 87.2 11.3 189.3101.2 80.4 12.1 222.7105.4 76.7 12.0 238.7110.8 75.0 11.6 245.3111.2 79.6 11.1 264.6121.3 92.0 9.6 252.2130.6 93.8 9.1 256.7122.7 95.4 9.0 272.3128.2 96.5 8.8 281.8130.7 98.3 8.7 292.0

133.3 120.0 7.4 270.1

– 163.7 5.7 267.3

121.4 103.6 8.4 292.8119.4 105.2 8.4 291.8116.2 107.1 8.3 289.5117.6 109.0 8.1 286.4122.5 109.7 8.0 287.0132.2 117.5 7.5 270.3137.3 124.7 7.1 258.6139.8 125.8 7.1 262.7148.5 131.8 6.8 253.1152.1 135.3 6.6 249.9145.6 135.3 6.7 255.2147.2 135.3 6.7 261.2169.2 155.6 5.9 237.2175.3 157.6 5.8 238.7178.1 159.4 5.7 241.7183.3 164.2 5.5 241.7

– 165.9 5.5 249.0– 165.9 5.6 258.8– 165.9 5.6 271.4– 165.9 5.6 279.0– 165.9 5.6 284.0– 165.9 5.6 291.0– 165.9 5.7 301.5– 165.9 5.8 311.0– 165.9 5.8 315.2– 165.9 5.7 322.1– 165.9 5.7 329.0– 165.9 5.7 333.9– 165.9 5.7 338.1– 165.9 5.6 340.8

2.2. Cabo Verde Área: 4,033 Km2

Capital city: Praia

Population: 531 thousand (2016; source: Cabo Verde National Institute of Statistics)

Currency: CV Escudo (CVE)

Domestic demand dynamics and the good performance of tourism and foreign direct investment led to an acceleration in economic growth in Cabo Verde in 2016. The ensuing sound tax collection and lower costs arising from the public investment programme resulted in a decline in the fiscal deficit, but failed to prevent the further increase in public debt. The current account deficit fell, due to the ongoing increase in both exports of services and private transfers. Foreign direct investment inflows, disbursements of foreign public loans and the unwinding of investments abroad funded the current deficit and facilitated an expansion in foreign exchange reserves. Due to the inflow of reserves and moderate inflation, the central bank was able to maintain an accommodative monetary policy in 2016, in order to foster credit to the economy.

BANCO DE PORTUGAL • Economic Developments in Portuguese-speaking African Countries and Timor-Leste • 2016 | 201730

In 2016 there was an acceleration in economic growth in Cabo Verde, to 3.8% (1.0% in 2015), furthered by buoyant domestic demand (mainly consumption but also investment) and the sound performance of tourism revenue and foreign direct investment.

The increase in private transfers, including emigrants’ remittances, together with the ongoing recovery in tourism demand (particularly from Italy, the United Kingdom and France), led to a reduction in the current account deficit, to 3.9% of GDP (4.6% in 2015). This improvement also benefited from a decrease in the income account deficit by virtue of the increase in inflows partly driven by remuneration of non-resident employees. The acceleration in economic activity boosted imports of both consumer and capital goods, which resulted in the worsening of the trade balance.

The current account deficit was funded by foreign direct investment inflows, disbursements of foreign public loans and the unwinding of investments abroad by the banking and non-banking sectors. Currency inflows also strengthened foreign exchange reserves, by EUR 88 million, rising to 6.9 months of goods and services imports, thus helping support the exchange rate peg with the euro in place since 1998.

The increase in foreign exchange reserves was accompanied by higher net domestic credit, combining increases chiefly in credit to the non-financial private sector, households and general government. As such, broad money accelerated in 2016, growing by 8.4% from 2015, as reflected mainly by the collection of CVE-denominated deposits (mostly, demand deposits but also time deposits) and emigrants’ deposits (albeit at a slower pace than before).

Price levels continued on a downward path in 2016, reflecting external price developments (mostly, oil products and products from euro area countries), greater domestic production of fresh produce and a reduction in the VAT rate (reversal of the 2015 tax increase in aid of Chã das Caldeiras). Inflation remained at negative levels throughout 2016, standing at -1.4% and

0.3% in December, in average and year-on-year terms respectively.

Against a background of well-performing reserves and controlled inflation, Banco de Cabo Verde (BCV) maintained its accommodative monetary policy over the year. The banking sector lowered some of its rates, which, given the persistent excess liquidity and low financial investment rates, has hampered the sector’s profitability, in a context of still high non-performing loans. Impaired loans accounted for 15.5% of total credit at the end of 2016, which, however, is down from 16.5% at the end of 2015.

Economic acceleration boosted tax collection, more specifically personal income tax (which also impacts on small and medium-sized enterprises), VAT and the tax on international transactions. Despite a continued increase in current expenditure, the sound performance of tax revenue helped to contain the fiscal deficit, at 3.6% of GDP (4.6% in 2015), which was also helped by the decrease in spending in the public investment programme. The results of the legislative elections in 2016 and the ensuing change of the ruling party caused significant delays in the implementation of a public investment programme that was already being phased down.

Albeit lower, the General government’s financing needs, which also include those resulting from financial asset operations (more specifically, loans used for on-lending), were mostly covered by domestic resources, with some contribution from external resources. Public debt proceeded on an upward path, with its share in GDP increasing to 129% at the end of 2016 (the external component dropped to 97% while the domestic component increased to 32%).

2017 should be characterised by economic growth similar to 2016, with projections pointing at a real GDP rise of 3.9%, largely on the back of investment and private consumption. Reflecting the expansion in imports, the current account deficit is expected to deteriorate, rising to 6.7% of GDP. However, the increase in foreign direct investment should be enough to continue to push reserves upwards, although reducing the coverage of goods and services imports.

31

In spite of the expected recovery in the public investment programme and the increase in current expenditure, the sound collection of taxes and projected inflows of grants should reduce the fiscal deficit to 3.4% of GDP.

The first months of 2017 have matched projections, as evidenced by an increase in the current account deficit and fiscal deficit improvements. Exceptions were mostly related to the non-resumption of the public investment programme, which contributed to a positive fiscal balance in the first quarter, and the decrease in foreign exchange reserves (by EUR 12 million, up to March).

Although back in positive territory, subdued inflation made it possible for BCV to introduce changes to monetary policy instruments in June, with a view to making them more effective: (i) marked reduction in rates on its main instruments (by 2 p.p. in its key, liquidity provision and rediscount rates – which moved down to 1.5%, 4.5% and 5.5% respectively; and by 0.15 p.p. in its liquidity absorption facility, to 0.1%); (ii) absorption of excess liquidity; (iii) removal of both the exemption on reserve requirements and the ceiling on its liquidity provision facility;

(iv) implementation of tender procedures for fixed-rate monetary regularisation securities (Portuguese acronym: TRM). With these measures, BCV has sought to stimulate financing for viable investment projects and, consequently, economic activity, which should be enhanced by the effective implementation of structural economic policy measures.

The sharper slowdown in the economies of its main trading partners, more specifically in the European Union, and the possible increase in global protectionism (and potential price increase in imports) are the more substantial external risks to Cabo Verde’s economy in 2017.

At domestic level, it is particularly important to monitor the costs and effects of recent changes to monetary policy instruments. Particular attention should also be paid to budgetary control, public debt management and financial stability. Under the latter, a resolution measure was applied to a small institution in March 2017, and part of its business was purchased by the second largest bank in Cabo Verde.

Table 2.14 • Main economic indicators

2014 2015 2016 2017

Est. Proj.

Real GDP (annual % change) 0.6 1.0 3.8 3.9

-0.4 -0.5 -0.3 1.2

7.3 5.9 8.4 5.5

-9.1 -4.6 -3.9 -6.7

5.4 6.4 6.9 7.0

-7.6 -4.6 -3.6 -3.4

115.9 126.0 129.0 –

Inflation (year-on-year % change)

Broad money (annual % change)

Current account (% of GDP)

Official reserves (months of imports)

Fiscal balance (% of GDP)

Public debt, excluding TCMF(a) (% of GDP)

Sources: (for the subsequent charts also): International Monetary Fund, Banco de Cabo Verde, Ministry of Finance (Cabo Verde) and Cabo Verde National Institute of Statistics.Note: (a) Títulos Consolidados de Mobilização Financeira (consolidated financial mobilisation securities), covered by the resources of an offshore Trust Fund.

Cabo Verde

BANCO DE PORTUGAL • Economic Developments in Portuguese-speaking African Countries and Timor-Leste • 2016 | 201732

Chart 2.13 • Real GDP Annual % change

Chart 2.14 • Inflation Annual % change in the CPI

-1.3

1.5

4.0

1.1 0.8 0.61.0

3.8 3.9

-2

-1

0

1

2

3

4

5

2009 2010 2011 2012 2013 2014 2015 2016(est.)

2017(proj.)

-4

-2

0

2

4

6

8

2009 2010 2011 2012 2013 2014 2015 2016 2017

Year-on-year % change Average % change

Following a number of years of weak growth, economic activity accelerated in 2016, owing to buoyancy mostly in consumption but also investment and to the performance of tourism revenue and foreign direct investment.

Throughout 2016 Cabo Verde posted negative inflation rates, chiefly reflecting the import component, particularly oil products, but also domestic factors such as the greater production of fresh produce.

Chart 2.15 • External accounts % of GDP

Chart 2.16 • Foreign exchange reserves Months of goods and services imports

-50

-40

-30

-20

-10

0

10

2009 2010 2011 2012 2013 2014 2015 2016(est.)

2017(proj.)

Trade balance Current account Overall balance

0

1

2

3

4

5

6

7

8

2009 2010 2011 2012 2013 2014 2015 2016 2017(proj.)

Total net foreign assets Net foreign assets - BCV

Despite an increase in imports due to economic acceleration, the current account improved in 2016, reflecting increasing private transfers, including emigrants’ remittances, and continued recovery in demand from tourism.

In 2016 foreign exchange reserves proceeded on an upward path, covering nearly 7 months of goods and services imports, driven by foreign direct investment inflows, disbursements of foreign public loans and unwinding of investments abroad by the banking and non-banking sectors.

Chart 2.17 • Goods exports Destinations as a %, total in USD millions

Chart 2.18 • Goods imports Origins as a %, total in USD millions

0

50

100

150

200

250

300

0%

20%

40%

60%

80%

100%

2009 2010 2011 2012 2013 2014 2015 2016

Other France El SalvadorSpain Portugal Total

0

200

400

600

800

1,000

1,200

0%

20%

40%

60%

80%

100%

2009 2010 2011 2012 2013 2014 2015 2016

Other Brazil NetherlandsSpain Portugal Total

In 2016 the Iberian Peninsula continued to be the main market for Cabo Verde’s exports, particularly Spain (mostly sea products). Portugal partly recovered its share in the total, thus interrupting the gradual fall that started in 2008.

Since 1998 Portuguese products have accounted for approximately half of Cabo Verde’s imports. The geographical structure of imports has remained relatively stable, with the Netherlands and Spain taking on around 25% of the total since 2002.

33

Chart 2.19 • Public accounts % of GDP

Chart 2.20 • Public debt % of GDP

-20

-16

-12

-8

-4

0

2009 2010 2011 2012 2013 2014 2015 2016(est.)

2017(budget)

Current balance Overall balance excl. grantsOverall balance

0

20

40

60

80

100

120

140

2009 2010 2011 2012 2013 2014 2015 2016(est.)

Mar-17(est.)

External - Multilateral External - BilateralDomestic (excl. TCMF) Domestic - TCMF

In 2016 the fiscal deficit continued to follow the downward trend that started in 2013, after the expanded public investment programme (launched as a response to the international crisis) had come to an end.

In addition to the need to fund fiscal deficits (although declining), it is also necessary to cover financial asset operations (more specifically, loans used for on-lending) and, consequently, public debt is still on the rise, although the external component is mostly concessional.

Chart 2.21 • Public revenue and expenditure % of GDP

Chart 2.22 • Financial stability indicators

-40-30-20-100

10203040

2009 2010 2011 2012 2013 2014 2015 2016(est.)

2017(budget)

Exp: Invest. Prog. Exp: Other current Exp: InterestExp: Subs.+Tr.+Soc. ben. Exp: Goods and serv. Exp: PersonnelRev: Grants Rev: Transf. f/ SOE Rev: Other currentRec: Social sec. Rev: Taxes

Expe

nditu

reRe

venu

e

0%

10%

20%

30%Capital adequacy

Liquid assets(% of total assets)

ROE

ROA

Non-performingloans

(% of total loans)

Provisions(% of total loans)

2012 2014 2016

The reduction of the public investment programme was accompanied by sound tax collection, which made it possible to cut the fiscal deficit in 2016. However, the pressure from current expenditure has kept total expenditure close to 30% of GDP.

Against a background of growing banking activity, the banking system’s liquidity and solvency increased in 2016. However, profitability is still restricted by the limited options for investing funds and the still high (although declining) non-performing loan levels.

Chart 2.23 • Liquidity expansion/contraction factors Changes in % of initial stock of broad money

Chart 2.24 • Effective exchange rateIndexes 100 = 2000, monthly averages

-10

-5

0

5

10

15

2009 2010 2011 2012 2013 2014 2015 2016(est.)

2017(proj.)

External position Net claims on gen. gov.Credit to the economy Other net assetsBroad money

96

97

98

99

100

101

102

103

104

105

2009 2010 2011 2012 2013 2014 2015 2016 2017

Nominal index Real index

(appreciation: +; depreciation: -)

Broad money growth accelerated in 2016, chiefly reflecting the improvement of the system’s net external position, as has been the case since 2013. Also, credit to the economy has grown, particularly loans to enterprises and to households for consumption.

In 2016 Cabo Verde’s escudo depreciated, in nominal effective terms, reflecting the Brazilian real’s appreciation against the euro. The escudo’s depreciation was exacerbated in real terms by the inflation differential vis-à-vis the other trading partners – Portugal, Spain and the Netherlands.

Cabo Verde

BANCO DE PORTUGAL • Economic Developments in Portuguese-speaking African Countries and Timor-Leste • 2016 | 201734

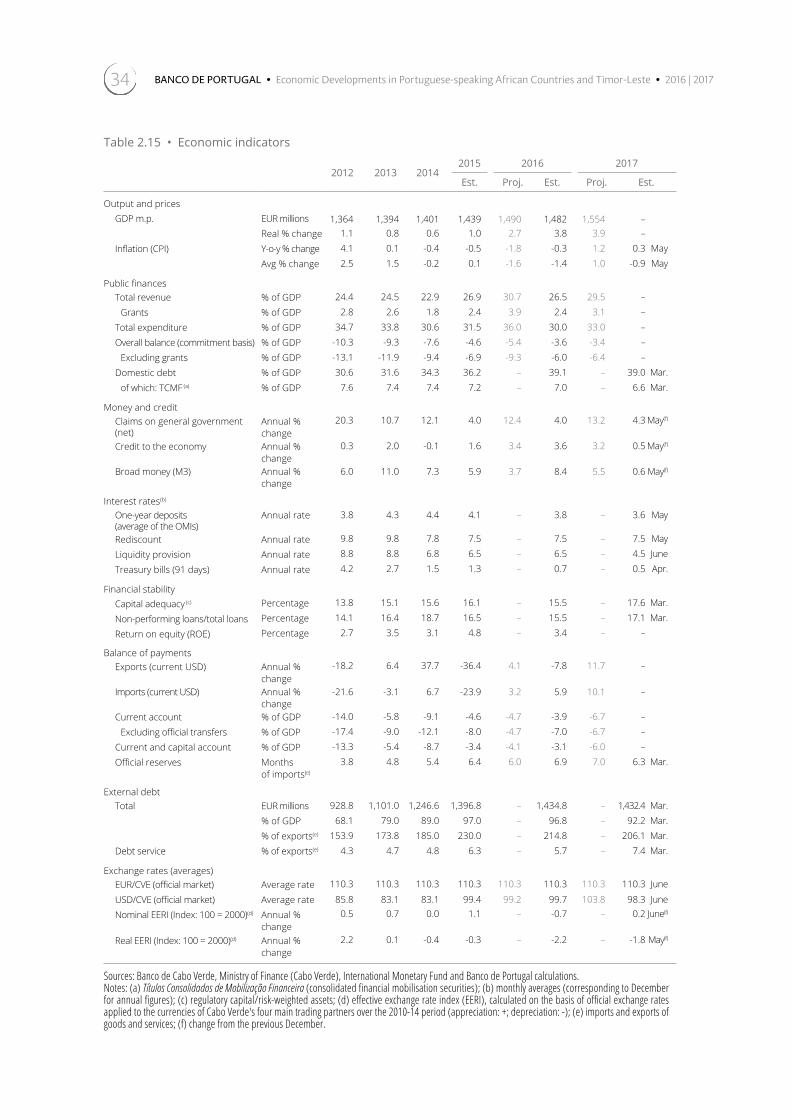

Table 2.15 • Economic indicators

2012 2013 2014 2015 2016 2017

Est. Proj. Est. Proj. Est.

Output and pricesGDP m.p. EUR millions

Real % changeInflation (CPI) Y-o-y % change

Avg % change

Public financesTotal revenue % of GDP

Grants % of GDPTotal expenditure % of GDPOverall balance (commitment basis) % of GDP

Excluding grants % of GDPDomestic debt % of GDP

of which: TCMF (a) % of GDP

Money and creditClaims on general government (net)

Annual % change

Credit to the economy Annual % change

Broad money (M3) Annual % change

Interest rates(b)

One-year deposits (average of the OMIs)

Annual rate

Rediscount Annual rateLiquidity provision Annual rateTreasury bills (91 days) Annual rate

Financial stabilityCapital adequacy (c) Percentage

Non-performing loans/total loans Percentage

Return on equity (ROE) Percentage

Balance of paymentsExports (current USD) Annual %

changeImports (current USD) Annual %

changeCurrent account % of GDP

Excluding official transfers % of GDPCurrent and capital account % of GDPOfficial reserves Months

of imports(e)

External debtTotal EUR millions

% of GDP% of exports(e)

Debt service % of exports(e)

Exchange rates (averages)EUR/CVE (official market) Average rateUSD/CVE (official market) Average rateNominal EERI (Index: 100 = 2000)(d) Annual %

changeReal EERI (Index: 100 = 2000)(d) Annual %

change

Sources: Banco de Cabo Verde, Ministry of Finance (Cabo Verde), International Monetary Fund and Banco de Portugal calculations.Notes: (a) Títulos Consolidados de Mobilização Financeira (consolidated financial mobilisation securities); (b) monthly averages (corresponding to December for annual figures); (c) regulatory capital/risk-weighted assets; (d) effective exchange rate index (EERI), calculated on the basis of official exchange rates applied to the currencies of Cabo Verde's four main trading partners over the 2010-14 period (appreciation: +; depreciation: -); (e) imports and exports of goods and services; (f) change from the previous December.

1,364 1,394 1,401 1,439 1,490 1,482 1,554 – 1.1 0.8 0.6 1.0 2.7 3.8 3.9 – 4.1 0.1 -0.4 -0.5 -1.8 -0.3 1.2 0.3 May2.5 1.5 -0.2 0.1 -1.6 -1.4 1.0 -0.9 May

24.4 24.5 22.9 26.9 30.7 26.5 29.5 – 2.8 2.6 1.8 2.4 3.9 2.4 3.1 –

34.7 33.8 30.6 31.5 36.0 30.0 33.0 – -10.3 -9.3 -7.6 -4.6 -5.4 -3.6 -3.4 – -13.1 -11.9 -9.4 -6.9 -9.3 -6.0 -6.4 – 30.6 31.6 34.3 36.2 – 39.1 – 39.0 Mar.

7.6 7.4 7.4 7.2 – 7.0 – 6.6 Mar.

20.3 10.7 12.1 4.0 12.4 4.0 13.2 4.3 May(f)

0.3 2.0 -0.1 1.6 3.4 3.6 3.2 0.5 May(f)

6.0 11.0 7.3 5.9 3.7 8.4 5.5 0.6 May(f)

3.8 4.3 4.4 4.1 – 3.8 – 3.6 May

9.8 9.8 7.8 7.5 – 7.5 – 7.5 May8.8 8.8 6.8 6.5 – 6.5 – 4.5 June4.2 2.7 1.5 1.3 – 0.7 – 0.5 Apr.

13.8 15.1 15.6 16.1 – 15.5 – 17.6 Mar.14.1 16.4 18.7 16.5 – 15.5 – 17.1 Mar.

2.7 3.5 3.1 4.8 – 3.4 – –

-18.2 6.4 37.7 -36.4 4.1 -7.8 11.7 –

-21.6 -3.1 6.7 -23.9 3.2 5.9 10.1 –

-14.0 -5.8 -9.1 -4.6 -4.7 -3.9 -6.7 – -17.4 -9.0 -12.1 -8.0 -4.7 -7.0 -6.7 – -13.3 -5.4 -8.7 -3.4 -4.1 -3.1 -6.0 –

3.8 4.8 5.4 6.4 6.0 6.9 7.0 6.3 Mar.

928.8 1,101.0 1,246.6 1,396.8 – 1,434.8 – 1,432.4 Mar.68.1 79.0 89.0 97.0 – 96.8 – 92.2 Mar.

153.9 173.8 185.0 230.0 – 214.8 – 206.1 Mar.4.3 4.7 4.8 6.3 – 5.7 – 7.4 Mar.

110.3 110.3 110.3 110.3 110.3 110.3 110.3 110.3 June

85.8 83.1 83.1 99.4 99.2 99.7 103.8 98.3 June0.5 0.7 0.0 1.1 – -0.7 – 0.2 June(f)

2.2 0.1 -0.4 -0.3 – -2.2 – -1.8 May(f)

35

Table 2.16 • Gross domestic productCurrent prices, CVE millions

2010 2011 2012 2013 2014 2015 2016 2017

Est. Est. Proj.

Primary sectorAgriculture, livestock and forestry

Fishing and aquaculture

Mining and quarrying

Secondary sector

Manufactured products

Electricity, gas, water

Construction

Tertiary sector

Whole. & retail trade; repair of motor vehicles

Accommodation and food service activities

Transportation and storage

Telecommunications and mail

Financial services

Real estate and other services

Corporate services

Public administration

Gross value added

Taxes and subsidies on products

Gross domestic product (m.p.)

Consumption

Public

Private

Investment

Gross fixed capital formation

Public

Private

Changes in inventories

Domestic demand

Exports of goods and services

Overall demand

Imports of goods and services

Memo items:

Gross domestic savings

Nominal GDPmp (EUR millions)

Nominal GDPmp (USD millions)

GDP deflator (annual % change)

Nominal GDP (annual % change)

Real GDP (annual % change)

Sources: Cabo Verde National Institute of Statistics, Banco de Cabo Verde, International Monetary Fund and Banco de Portugal calculations.

11,780 12,215 13,249 13,322 13,089 14,432 14,370 – 9,705 10,598 11,659 11,393 10,946 12,005 12,662 –

1,367 1,005 1,040 1,334 1,433 1,872 1,162 –

708 612 550 595 710 556 545 –

24,440 25,668 25,018 26,330 28,212 28,192 27,927 –

7,528 8,054 8,547 8,916 9,862 10,389 11,514 –

1,939 2,158 3,268 3,999 4,071 5,234 4,648 –

14,973 15,456 13,203 13,415 14,278 12,569 11,765 –

84,749 89,645 93,463 95,045 94,563 96,043 99,731 –

17,609 19,002 18,785 17,278 17,720 16,179 16,020 –

14,781 14,038 13,300 14,664 13,105 14,999 15,129 –

4,792 5,896 8,651 9,065 8,221 7,260 7,886 –

6,254 6,246 6,330 6,130 6,122 6,013 5,554 –

5,120 5,077 5,238 5,377 5,986 6,138 6,758 –

14,604 14,696 15,885 15,897 15,948 16,210 16,654 –

2,570 3,176 3,392 3,489 2,951 4,057 4,354 –

19,019 21,514 21,882 23,144 24,510 25,188 27,375 –

120,969 127,528 131,730 134,697 135,865 138,667 142,028 –

17,598 20,400 18,622 19,026 18,571 20,032 21,354 –

138,567 147,928 150,352 153,723 154,436 158,699 163,381 171,311

112,863 120,269 123,620 127,167 128,676 133,410 141,910 –

25,536 27,401 25,963 26,837 28,496 29,918 33,680 –

87,327 92,868 97,657 100,330 100,180 103,491 108,231 –

66,024 70,277 55,920 48,622 57,148 47,906 52,217 –

62,625 69,128 52,844 46,337 53,317 45,681 52,578 –

23,935 19,236 22,320 18,451 11,125 11,635 8,443 –

38,690 49,892 30,524 27,886 42,192 34,045 44,135 –

3,399 1,149 3,076 2,285 3,831 2,225 –361 –

178,887 190,546 179,540 175,789 185,824 181,316 194,127 –

45,271 52,541 60,790 62,246 62,332 71,268 73,660 –

224,158 243,087 240,330 238,035 248,156 252,583 267,787 –

85,591 95,159 89,978 84,312 93,720 93,884 104,406 –

25,704 27,659 26,732 26,556 25,760 25,289 21,471 –

1,257 1,342 1,364 1,394 1,401 1,439 1,482 1,554

1,664 1,866 1,752 1,850 1,859 1,597 1,639 1,650

0.5 2.7 0.6 1.4 –0.1 1.7 –0.8 0.9

2.0 6.8 1.6 2.2 0.5 2.8 3.0 4.9

1.5 4.0 1.1 0.8 0.6 1.0 3.8 3.9

Cabo Verde

BANCO DE PORTUGAL • Economic Developments in Portuguese-speaking African Countries and Timor-Leste • 2016 | 201736

Table 2.17 • Consumer price indexPercentages

Monthly change Year-on-year change Average change

[1] [2] [3]

2003 December

2004 December

2005 December

2006 December

2007 December

2008 December

2009 December

2010 December

2011 December

2012 December

2013 December

2014 December

2015 December

2016 December

2015 January

February

March

April

May

June

July

August

September

October

November

December

December (proj.)

2016 January

February

March

April

May

June

July

August

September

October

November

December

December (proj.)

2017 January

February

March

April

May

December (proj.)

Sources: Banco de Cabo Verde and Banco de Portugal calculations.Notes: [1] month (n) / month (n-1); [2] month (n) / month (n) of the previous year; [3] last 12 months / 12 previous months.

– -2.3 1.2 – 0.6 -1.9

– 1.8 0.4

– 5.8 4.8

– 4.0 4.4

– 6.7 6.8

– -0.4 1.0

– 3.4 2.1

– 3.6 4.5

– 4.1 2.5

– 0.1 1.5

– -0.4 -0.2

– -0.5 0.1

– -0.3 -1.4

0.2 0.1 -0.2

-0.4 -0.2 -0.3

-0.4 -0.2 -0.4

-0.3 0.3 -0.3

0.2 0.3 -0.3

0.0 0.3 -0.2

0.3 0.3 -0.2

0.1 0.3 -0.1

0.3 0.6 0.0

-0.1 0.4 0.1

-0.2 -0.2 0.1

-0.2 -0.5 0.1

– 2.0 1.5

-0.5 -1.2 0.0

-0.5 -1.3 -0.1

-0.3 -1.2 -0.1

0.0 -0.9 -0.2

0.1 -1.0 -0.4

-1.3 -2.3 -0.6

0.2 -2.3 -0.8

0.6 -1.8 -1.0

0.1 -2.1 -1.2

0.7 -1.3 -1.3

-0.1 -1.3 -1.4

0.8 -0.3 -1.4

– -1.8 -1.6

-0.7 -0.4 -1.3

0.3 0.3 -1.2

-0.2 0.5 -1.1

-0.3 0.3 -1.0

0.2 0.3 -0.9

– 1.2 1.0

37

Table 2.18 • Balance of paymentsCVE millions

2013 20142015 2016 2017

Est. Proj. Q I Est. Proj. Q I

1. Current accountTrade

Exports (f.o.b.)(a)

Imports (f.o.b.)

Services (net)

Exports

of which: Transport

Tourism

Imports

of which: Transport

Tourism

Income (net)

Exports

of which: Income f/ the TF(b) (prev. year)

Imports

of which: Interest on sched. public debt

Current transfers

Official transfers

Private transfers

of which: Emigrant remittances

2. Capital and financial accountCapital account

Capital transfers

Financial account

Direct investment

Portfolio investment

Other transactions

of which: Disburs. of loans to gen. gov.

Scheduled amortisation

3. Errors and omissions

4. Overall balance: (1)+(2)+(3)

5. FinancingChange in official reserves (increase: - ) Exceptional financing

of which: Drawings from ACC Facility(c)

Reimb. of ACC Facility(c)

Change in arrears (increase: +)

6. Financing GAP(d): (4)+(5)

Memo items:

Current account (% of GDP)

Current and capital account (% of GDP) Official reserves (in months of imports)(e)

Sources: Banco de Cabo Verde, International Monetary Fund and Banco de Portugal calculations.Notes: (a) Includes sales of fuel to ships and re-exports; (b) offshore fund (Trust Fund) to support the conversion of domestic debt; (c) Exchange Rate Cooperation Agreement (Acordo de Cooperação Cambial) between Portugal and Cabo Verde; (d) net borrowing (-)/net lending (+); (e) net foreign assets of BCV and imports of goods and services in the year.

-8,898 -14,025 -7,292 -7,683 124 -6,367 -11,495 -1,099-51,533 -50,277 -48,871 -50,297 -10,899 -54,113 -59,345 -17,579

15,283 21,044 16,024 16,681 4,008 14,813 16,548 3,844

-66,816 -71,322 -64,894 -66,977 -14,907 -68,926 -75,893 -21,422

25,207 21,904 22,086 22,813 6,172 23,367 26,405 10,283

54,551 53,241 50,940 52,447 15,017 58,847 60,083 19,271

11,235 9,526 9,478 – 2,563 10,397 – 3,456

33,325 32,121 33,182 35,372 9,748 34,877 36,759 12,288

-29,344 -31,337 -28,855 -29,634 -8,845 -35,480 -33,678 -8,988

-7,020 -7,842 -7,602 – -2,008 -8,726 – -2,234

-3,728 -2,692 -2,325 – -1,438 -5,812 – -1,328

-5,367 -7,692 -5,751 -6,365 -2,227 -5,634 -5,965 -1,496

1,151 1,165 1,254 – 421 2,361 – 588

373 373 414 267 0 267 – 0

-6,518 -8,857 -7,006 – -2,648 -7,995 – -2,084

-1,438 -1,518 -1,734 -1,771 -458 -1,662 -2,031 -495

22,795 22,039 25,244 26,165 7,079 30,013 27,410 7,692

4,948 4,664 5,395 – 989 4,998 – 1,939

17,847 17,375 19,850 – 6,089 25,015 – 5,753

14,441 16,158 19,679 19,144 4,916 20,503 – 4,727

14,619 19,390 13,251 9,857 -540 14,189 10,149 3,291

533 659 1,884 908 133 1,316 1,200 411

533 659 1,884 908 133 1,316 1,200 411

14,085 18,731 11,367 8,949 -673 12,873 8,949 2,880

4,627 10,557 9,359 10,506 2,900 10,862 10,506 3,712

-2,281 -2,001 -2,089 -416 -1,004 -4,024 -416 -1,023

11,739 10,175 4,098 -1,141 -2,569 6,035 -1,141 191

19,391 -18,911 13,074 – 665 5,819 – 588

-1,823 -2,036 -2,484 – -811 -2,553 – -1,071

-117 2,481 -2,436 0 332 1,328 4,581 -3,536

5,604 7,845 3,524 2,173 -83 9,150 3,235 -1,344-5,604 -7,845 -3,524 -2,173 83 -9,150 -3,235 1,344

-5,604 -7,845 -3,524 -2,173 83 -9,150 -3,235 1,344

0 0 0 – 0 0 – 0

0 0 0 – 0 0 – 0

0 0 0 – 0 0 – 0

0 0 0 – 0 0 – 0

0 0 0 0 0 0 0 0

-5.8 -9.1 -4.6 -4.7 – -3.9 -6.7 –

-5.4 -8.7 -3.4 -4.1 – -3.1 -6.0 –

4.8 5.4 6.4 6.0 6.1 6.9 7.0 6.3

Cabo Verde

BANCO DE PORTUGAL • Economic Developments in Portuguese-speaking African Countries and Timor-Leste • 2016 | 201738

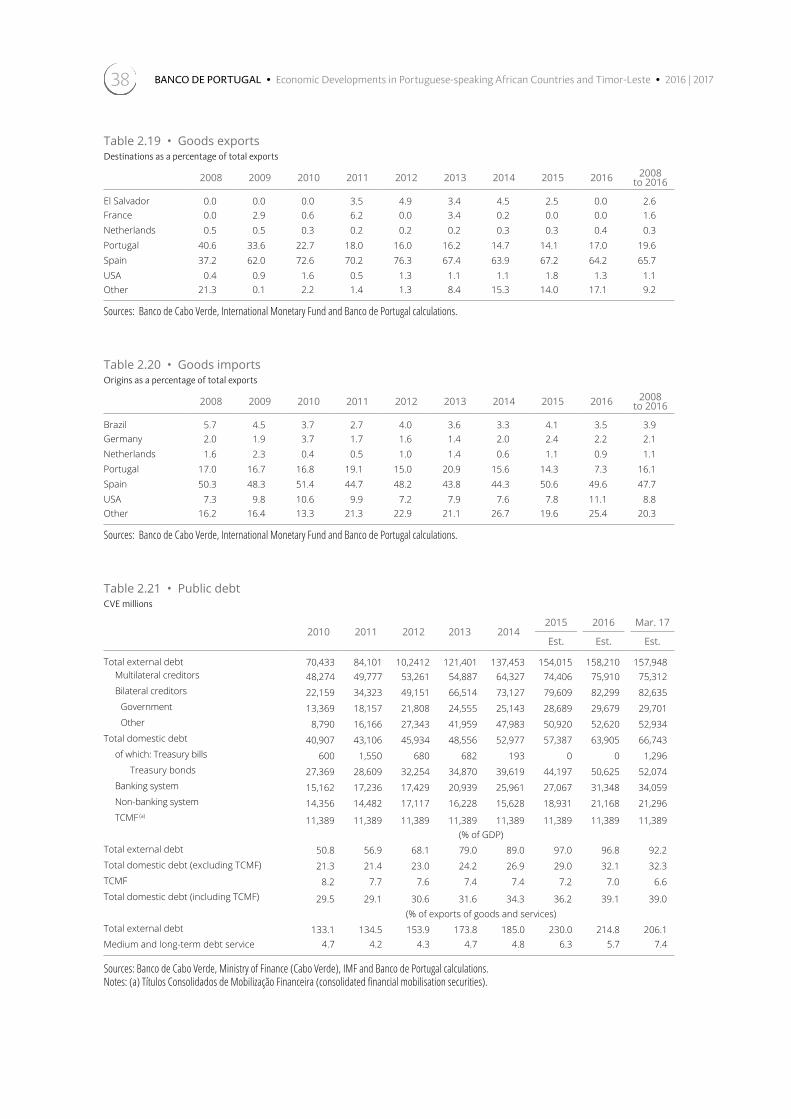

Table 2.19 • Goods exportsDestinations as a percentage of total exports

2008 2009 2010 2011 2012 2013 2014 2015 2016 2008 to 2016

El Salvador 0.0 0.0 0.0 3.5 4.9 3.4 4.5 2.5 0.0 2.6 0.0 2.9 0.6 6.2 0.0 3.4 0.2 0.0 0.0 1.6 0.5 0.5 0.3 0.2 0.2 0.2 0.3 0.3 0.4 0.3

40.6 33.6 22.7 18.0 16.0 16.2 14.7 14.1 17.0 19.6 37.2 62.0 72.6 70.2 76.3 67.4 63.9 67.2 64.2 65.7

0.4 0.9 1.6 0.5 1.3 1.1 1.1 1.8 1.3 1.1 21.3 0.1 2.2 1.4 1.3 8.4 15.3 14.0 17.1 9.2

FranceNetherlandsPortugalSpainUSAOther

Sources: Banco de Cabo Verde, International Monetary Fund and Banco de Portugal calculations.

Table 2.20 • Goods importsOrigins as a percentage of total exports

2008 2009 2010 2011 2012 2013 2014 2015 2016 2008 to 2016

Brazil 5.7 4.5 3.7 2.7 4.0 3.6 3.3 4.1 3.5 3.9 2.0 1.9 3.7 1.7 1.6 1.4 2.0 2.4 2.2 2.1 1.6 2.3 0.4 0.5 1.0 1.4 0.6 1.1 0.9 1.1

17.0 16.7 16.8 19.1 15.0 20.9 15.6 14.3 7.3 16.1 50.3 48.3 51.4 44.7 48.2 43.8 44.3 50.6 49.6 47.7

7.3 9.8 10.6 9.9 7.2 7.9 7.6 7.8 11.1 8.8 16.2 16.4 13.3 21.3 22.9 21.1 26.7 19.6 25.4 20.3

GermanyNetherlandsPortugalSpainUSAOther

Sources: Banco de Cabo Verde, International Monetary Fund and Banco de Portugal calculations.

Table 2.21 • Public debtCVE millions

2010 2011 2012 2013 2014 2015 2016 Mar. 17

Est. Est. Est.

Total external debtMultilateral creditors

Bilateral creditors

Government

Other

Total domestic debt

of which: Treasury bills

Treasury bonds

Banking system

Non-banking system

TCMF (a)

(% of GDP)Total external debt

Total domestic debt (excluding TCMF)

TCMF

Total domestic debt (including TCMF)

(% of exports of goods and services)Total external debt 133.1 134.5 153.9 173.8 185.0 230.0 214.8 206.1

4.7 4.2 4.3 4.7 4.8 6.3 5.7 7.4 Medium and long-term debt service

Sources: Banco de Cabo Verde, Ministry of Finance (Cabo Verde), IMF and Banco de Portugal calculations.Notes: (a) Títulos Consolidados de Mobilização Financeira (consolidated financial mobilisation securities).

70,433 84,101 10,2412 121,401 137,453 154,015 158,210 157,948 48,274 49,777 53,261 54,887 64,327 74,406 75,910 75,312

22,159 34,323 49,151 66,514 73,127 79,609 82,299 82,635

13,369 18,157 21,808 24,555 25,143 28,689 29,679 29,701

8,790 16,166 27,343 41,959 47,983 50,920 52,620 52,934

40,907 43,106 45,934 48,556 52,977 57,387 63,905 66,743

600 1,550 680 682 193 0 0 1,296

27,369 28,609 32,254 34,870 39,619 44,197 50,625 52,074

15,162 17,236 17,429 20,939 25,961 27,067 31,348 34,059

14,356 14,482 17,117 16,228 15,628 18,931 21,168 21,296

11,389 11,389 11,389 11,389 11,389 11,389 11,389 11,389

50.8 56.9 68.1 79.0 89.0 97.0 96.8 92.2

21.3 21.4 23.0 24.2 26.9 29.0 32.1 32.3

8.2 7.7 7.6 7.4 7.4 7.2 7.0 6.6

29.5 29.1 30.6 31.6 34.3 36.2 39.1 39.0

39

Table 2.22 • Government operationsCVE millions

2013 2014 2015 2016 2017

Budg. Q 1 Est. l.e.(a) Budg. Q 1 l.e.(a)

1. Total revenue1.1. Current revenue

TaxesIncome taxesTaxes on goods and services

of which: VATTaxes on international trans.Other taxes

Social contributionsTransfers (Public Administration)Other revenue

1.2. Grants1.3. Transf. f/ state owned entrep.(b)

2. Total expenditure2.1. Current expenditure(c)

of which: From invest. projectsCompensation of employeesGoods and services Interest and other charges

of which: Domestic debtExternal debt

SubsidiesTransfersSocial benefitsOther expenditure

of wich: Scholarships2.2. Investment programme

3. Non-financial assets: (3.1-3.2)3.1. Purchase of non-financial assets3.2. Sale of non-financial assets

4. Current balance: (1.1-2.1)

5. Overall balance excl. grants: (1-2-3-1.2)

6. Overall balance (commitment basis): (1-2-3)

7. Financing7.1. Financial assets

Loan repay. to state ow. enterp.Loans to state owned enterprisesShares and other equityOther financial assets

7.2. Financial liabilitiesExternal (net)

DisbursementsAmortisation

Domestic (net)Banking systemOther

8. Financing gap/discrepancy(e): (6+7)

Sources: Banco de Cabo Verde, Ministry of Finance (Cabo Verde), IMF and Banco de Portugal calculations.Notes: (a) Level of budget execution (%); (b) Share of capital expenditure of state-owned enterprises (usually to finance infrastructures related to the activities of these enterprises); (c) Includes values to settle in 2015; (d) Net borrowing (+)/net lending (-).

37,716 35,327 42,677 50,355 9,929 43,220 85.8 50,538 11,711 23.233,692 32,540 38,916 44,023 9,497 39,359 89.4 45,304 10,081 22.328099 27060 30,516 34,938 8,025 32,304 92.5 37,407 8,505 22.78,596 7,747 9,669 10,504 2,584 10,078 95.9 11,590 2,396 20.7

13,136 12,870 14,047 16,456 3,764 14,941 90.8 17,475 4,302 24.610,522 10,170 11,293 13,015 3,024 11,986 92.1 13,784 3,479 25.2

5,700 5,754 6,082 7,154 1,562 6,813 95.2 7,637 1,671 21.9668 688 719 824 115 472 57.3 705 136 19.3

43 56 46 208 13 56 27 59 15 24.90 0 197 0 4 94 – 273 1 0

5,550 5,424 8,157 8,877 1,454 6,906 77.8 7,564 1,560 20.64,024 2,787 3,761 6,332 432 3,861 61.0 5,234 1,630 31.1

0 0 0 0 0 0 – 0 0 –

51,982 47,240 50,024 59,139 10,602 49,060 83.0 56,535 10,974 19.435,436 37,549 41,068 49,614 9,946 44,147 89.0 48931 10,385 21.2

4,471 5,498 6,735 9,790 1,287 6,758 69.0 8,314 822 9.916,601 17,175 17,530 20,380 4,597 18,347 90.0 20,817 4,478 21.5

5,064 5,747 7,433 9,811 1,234 6,806 69.4 9,124 889 9.73,383 3,444 4,134 4,261 980 4,223 99.1 4,709 1,108 23.51,878 1,910 2,374 2,415 522 2,455 101.7 2,590 593 22.91,438 1,518 1,724 1,750 458 1,748 99.9 2,005 495 24.7

101 107 161 246 38 160 65.1 233 35 15.24,075 4,389 4,755 6,265 1,242 4,904 78.3 5,973 1,022 17.14,150 4,348 4,735 5,102 1,233 5,148 100.9 5,458 1,298 23.82,062 2,339 2,320 3,549 392 3,137 88.4 2,617 493 18.9

568 598 579 591 126 591 100.0 639 121 19.016,546 9,691 8,956 9,524 656 4,912 51.6 7,605 589 7.7

55 -150 -118 149 0 122 81.8 -205 -159 77.568 160 166 285 13 160 56.3 278 4 1.414 310 284 135 13 38 28.2 483 163 33.7

-1,744 -5,009 -2,152 -5,591 -449 -4,788 – -3,627 -304 –

-18,345 -14,550 -10,991 -15,265 -1,106 -9,823 – -11,027 -733 –

-14,321 -11,763 -7,229 -8,933 -674 -5,962 – -5,793 897 –

14,321 11,763 7,229 8,933 -1,499 5,962 – 5,793 495 – -6,311 -5,036 -5,092 -7,185 -417 -4,801 – -6,683 -339 –

128 129 273 267 135 313 – 303 8 – -5,629 -5,037 -3,929 -5,859 -178 -3,632 – -5,960 -382 –

-810 -101 -1,457 -2,000 -390 -1,510 – -1,108 0 – 0 -28 21 407 16 28 – 82 36 –