EARNINGS RELEASE n - mz-prod-cvm.s3.amazonaws.com · Special note: figures for 1Q17 include the...

41

1 EARNINGS RELEASE 1Q18 ¹ Excludes investments in M&A and Special Projects. ² EBITDA excluding the capital gain from the divestment of NOVATEC in 4Q17. Special note: figures for 1Q17 include the operations of FAIR, FAC/FAMAT and NOVATEC while the figures for 4Q17 include only the results of NOVATEC. ¹ Excludes figures from FAIR, FAC/FAMAT and NOVATEC for 2017, as well as results relating to new On-Campus units (Greenfields). On April 10, Kroton announced the creation of Saber, its holding company dedicated exclusively to Primary & Secondary Education. On the same date, the Company concluded the acquisition of Centro Educacional Leonardo da Vinci (“CELV”), an institution with around 1,300 students and unique facilities located in Vitória, Espírito Santo. On April 23, Kroton, through its subsidiary Saber, signed an agreement to acquire the operations of Somos. The transaction was executed under typical precedent conditions, including approval by Brazil's antitrust authority CADE. If approved, the acquisition will perfectly complement Kroton’s operations in the Primary & Secondary Education segment with high-quality products, services and digital platforms with national coverage. In addition to representing an important strategic step, the acquisition of a leading player in this segment should further diversify the Company’s markets and revenue sources and offer synergies and operating efficiency gains. Values in R$ ('000) 1Q18 1Q17 Chg.% 4Q17 Chg.% Gross Revenue 1,757,827 1,740,781 1.0% 1,754,889 0.2% Net Revenue 1,363,325 1,365,122 -0.1% 1,349,690 1.0% Gross Income 1,050,550 1,061,151 -1.0% 956,622 9.8% Gross Margin 77.1% 77.7% -0.7 p.p. 70.9% 6.2 p.p. Operating Result 785,792 814,001 -3.5% 704,826 11.5% Operat ing Margin 57.6% 59.6% -2.0 p.p. 52.2% 5.4 p.p. Adjusted EBITDA 614,713 639,529 -3.9% 534,149 15.1% Adjust ed EBITDA Margin 45.1% 46.8% -1.8 p.p. 39.6% 5.5 p.p. Adjusted Net Income 538,991 577,063 -6.6% 488,638 10.3% Adjust ed Net Margin 39.5% 42.3% -2.7 p.p. 36.2% 3.3 p.p. Adjusted Net Income /share 0.33 0.35 -7.6% 0.30 10.0% Operating Cash Generation (OCG) after Capex ¹ (125,271) 51,155 n.a. 392,208 n.a. OCG aft er Capex 1 / EBITDA (unadjust ed)² - 8.6% n.a. 82.9% n.a. Consolidated - Values in R$ ('000) 1Q18 1Q17 Chg.% Net Revenue 1,357,949 1,357,256 0.1% Adjusted EBITDA 629,733 634,451 -0.7% Adjust ed EBITDA Margin 46.4% 46.7% -0.4 p.p. Adjusted Net Income 554,717 571,978 -3.0% Adjust ed Net Margin 40.8% 42.1% -1.3 p.p. HIGHLIGHTS – MANAGEMENT ANALYSIS HIGHLIGHTS – MANAGEMENT ANALYSIS (Ex-Sale of Assets and Greenfields) Belo Horizonte, May 11, 2018, Kroton Educacional S.A. (B3: KROT3; OTCQX: KROTY) – “Kroton” or “Company,” announces today its results for the first quarter of 2018 (1Q18). The Company’s financial information is presented on a consolidated basis and in Brazilian real, in accordance with Brazilian Corporate Law and Generally Accepted Accounting Principles in Brazil (BRGAAP), and already conforms to International Financial Reporting Standards (IFRS), except where stated otherwise. HIGHLIGHTS INVESTOR RELATIONS Carlos Lazar – IRO Pedro Gomes – IR Manager Ana Troster – IR Coordinator +55 11 3133-7309 / 7311 / 7314 [email protected] www.kroton.com.br/ir

Transcript of EARNINGS RELEASE n - mz-prod-cvm.s3.amazonaws.com · Special note: figures for 1Q17 include the...

1

EARNINGS RELEASE 1Q18

¹ Excludes investments in M&A and Special Projects.

² EBITDA excluding the capital gain from the divestment of NOVATEC in 4Q17.

Special note: figures for 1Q17 include the operations of FAIR, FAC/FAMAT and NOVATEC while the figures for 4Q17 include only the results of NOVATEC.

¹ Excludes figures from FAIR, FAC/FAMAT and NOVATEC for 2017, as well as results relating to new On-Campus units (Greenfields).

On April 10, Kroton announced the creation of Saber, its holding company dedicated exclusively to Primary &

Secondary Education. On the same date, the Company concluded the acquisition of Centro Educacional Leonardo

da Vinci (“CELV”), an institution with around 1,300 students and unique facilities located in Vitória, Espírito Santo.

On April 23, Kroton, through its subsidiary Saber, signed an agreement to acquire the operations of Somos. The

transaction was executed under typical precedent conditions, including approval by Brazil's antitrust authority

CADE. If approved, the acquisition will perfectly complement Kroton’s operations in the Primary & Secondary

Education segment with high-quality products, services and digital platforms with national coverage. In addition

to representing an important strategic step, the acquisition of a leading player in this segment should further

diversify the Company’s markets and revenue sources and offer synergies and operating efficiency gains.

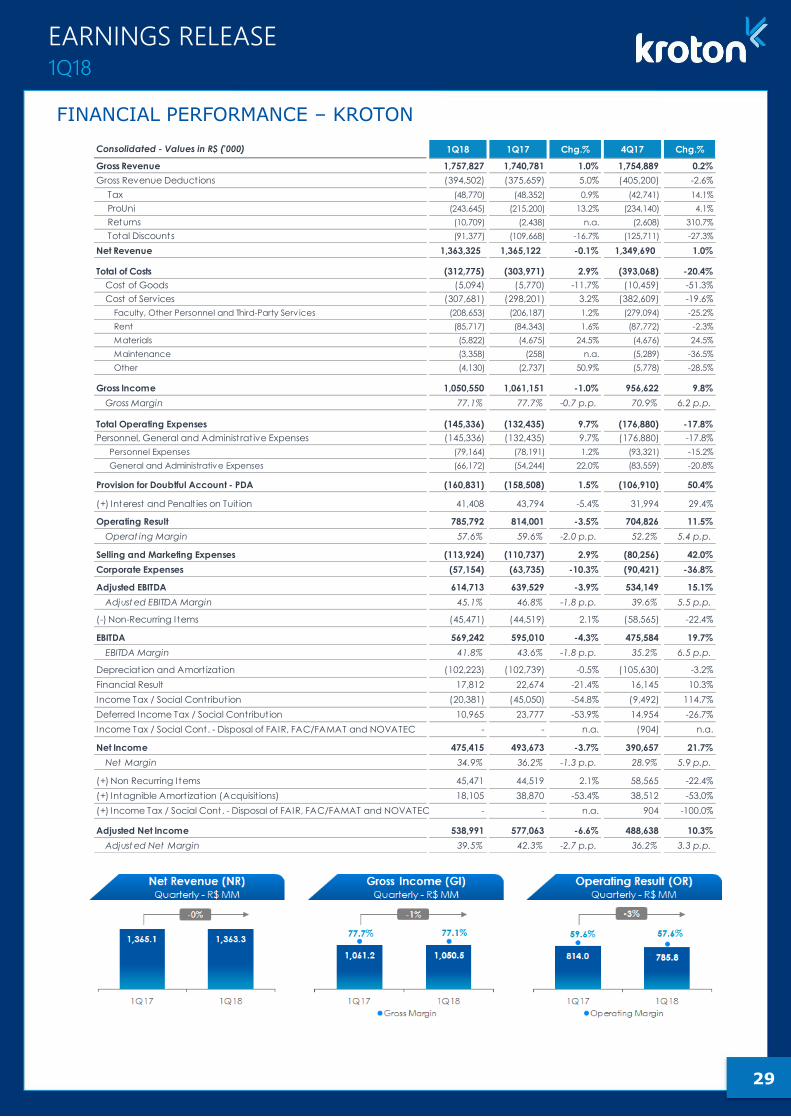

Values in R$ ('000) 1Q18 1Q17 Chg.% 4Q17 Chg.%

Gross Revenue 1,757,827 1,740,781 1.0% 1,754,889 0.2%

Net Revenue 1,363,325 1,365,122 -0.1% 1,349,690 1.0%

Gross Income 1,050,550 1,061,151 -1.0% 956,622 9.8%

Gross Margin 77.1% 77.7% -0.7 p.p. 70.9% 6.2 p.p.

Operating Result 785,792 814,001 -3.5% 704,826 11.5%

Operat ing Margin 57.6% 59.6% -2.0 p.p. 52.2% 5.4 p.p.

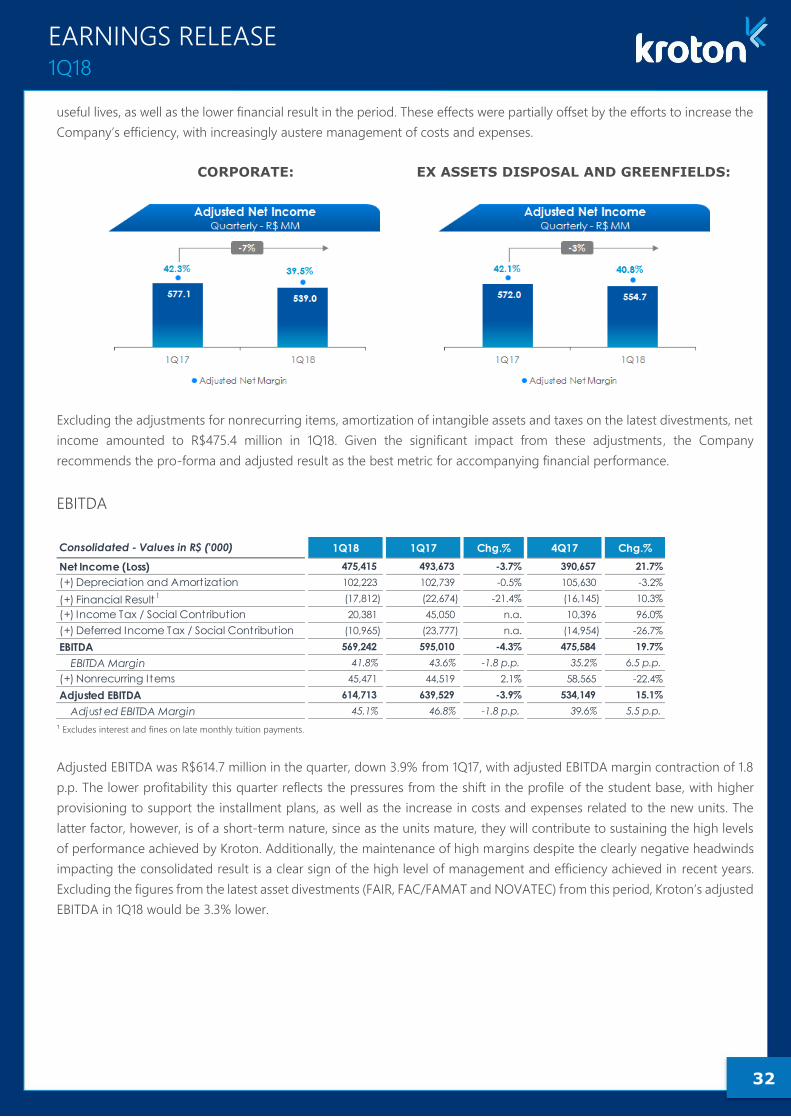

Adjusted EBITDA 614,713 639,529 -3.9% 534,149 15.1%

Adjust ed EBITDA Margin 45.1% 46.8% -1.8 p.p. 39.6% 5.5 p.p.

Adjusted Net Income 538,991 577,063 -6.6% 488,638 10.3%

Adjust ed Net Margin 39.5% 42.3% -2.7 p.p. 36.2% 3.3 p.p.

Adjusted Net Income /share 0.33 0.35 -7.6% 0.30 10.0%

Operating Cash Generation (OCG) after Capex ¹ (125,271) 51,155 n.a. 392,208 n.a.

OCG aft er Capex1

/ EBITDA (unadjust ed)² - 8.6% n.a. 82.9% n.a.

Consolidated - Values in R$ ('000) 1Q18 1Q17 Chg.%

Net Revenue 1,357,949 1,357,256 0.1%

Adjusted EBITDA 629,733 634,451 -0.7%

Adjust ed EBITDA Margin 46.4% 46.7% -0.4 p.p.

Adjusted Net Income 554,717 571,978 -3.0%

Adjust ed Net Margin 40.8% 42.1% -1.3 p.p.

HIGHLIGHTS – MANAGEMENT ANALYSIS

HIGHLIGHTS – MANAGEMENT ANALYSIS (Ex-Sale of Assets and Greenfields)

Belo Horizonte, May 11, 2018, Kroton Educacional S.A. (B3: KROT3; OTCQX: KROTY) –

“Kroton” or “Company,” announces today its results for the first quarter of 2018 (1Q18). The Company’s financial

information is presented on a consolidated basis and in Brazilian real, in accordance with Brazilian Corporate Law and

Generally Accepted Accounting Principles in Brazil (BRGAAP), and already conforms to International Financial

Reporting Standards (IFRS), except where stated otherwise.

HIGHLIGHTS

INVESTOR RELATIONS

Carlos Lazar – IRO

Pedro Gomes – IR Manager

Ana Troster – IR Coordinator

+55 11 3133-7309 / 7311 / 7314

[email protected] www.kroton.com.br/ir

2

EARNINGS RELEASE 1Q18

The pace of new unit openings remained robust and should accelerate over the coming months. Excluding the 10

units opened in the past few semesters and the 3 acquisitions of On-campus units in late 2017 and early 2018,

Kroton plans to open another 20 new campuses by the second semester of this year, as well as 100 new DL centers,

which should start operating in the coming months. As a result, the expectation is to end 2018 with 35 new units

in the On-campus segment and 400 new DL centers opened in the past year. Despite the natural maturation curve

and the short-term impact that these new units will have on the Company as a whole, this will serve as an important

future growth lever, expanding the addressable market and enabling increasingly broader offerings in all regions

in Brazil.

The first student-recruiting process of 2018 was concluded successfully and should enable the Company to deliver

solid performance over the year. In all, Kroton added 322,800 new Undergraduate On-Campus and Distance

Learning students, which represents growth of 3.4% compared to the same period last year, despite the more

challenging competitive landscape and still-high unemployment rates.

Kroton also was able to deliver strong results in controlling dropout indicators, which directly reflects the expansion

and consolidation of initiatives associated with the Retention Program, which now includes, among other actions,

retention teams at all units and predictive dropout models.

Accordingly, Kroton’s Postsecondary student base once again neared the one-million-student mark, growing 14%

on the prior quarter, reflecting the Company’s strong brand recognition, efficient sales team, balanced offering of

student installment products and an employability channel that has proven to be an important competitive

advantage. In relation to a year earlier, the student base contracted 1.3%, reflecting the greater number of

graduations in the period.

In terms of financial performance in 1Q18, net revenue was virtually stable compared to the same quarter last year.

The solid performance of the latest new enrollment and re-enrollment processes, coupled with the better mix of

academic programs and the higher average ticket, were offset by the asset divestments in late 2017 and the higher

number of graduates, which adversely affected the student base.

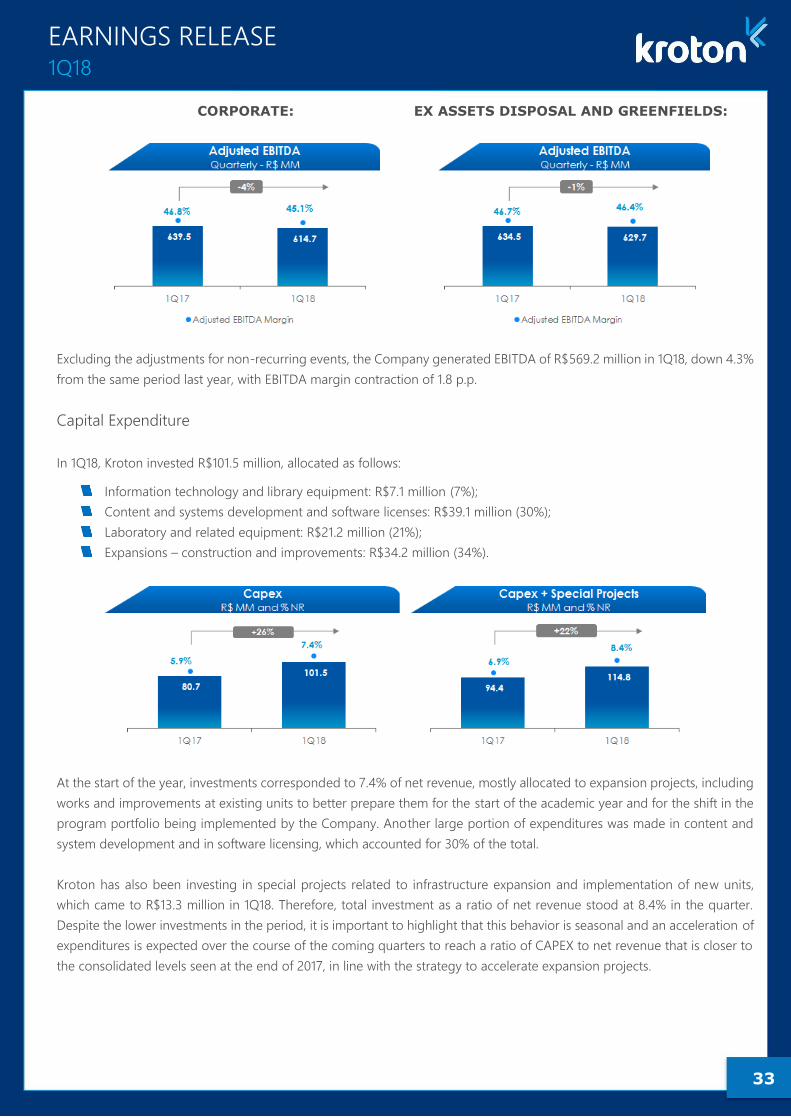

Adjusted EBITDA (managerial analysis) was R$614.7 million in the quarter, down 3.9% from 1Q17, with margin

contraction of 1.8 p.p., pressured by change in the student profile, with a higher level of provisioning to support

the student installment products, and by higher costs and expenses associated with the new units. The latter factor,

however, is of a short-term nature and should become less significant as the greenfield projects mature.

Adjusted net income (managerial analysis) came to R$539.0 million in 1Q18, down 6.6% from R$577.1 million in

the same quarter of 2017, with adjusted net margin contracting by 270 bps.

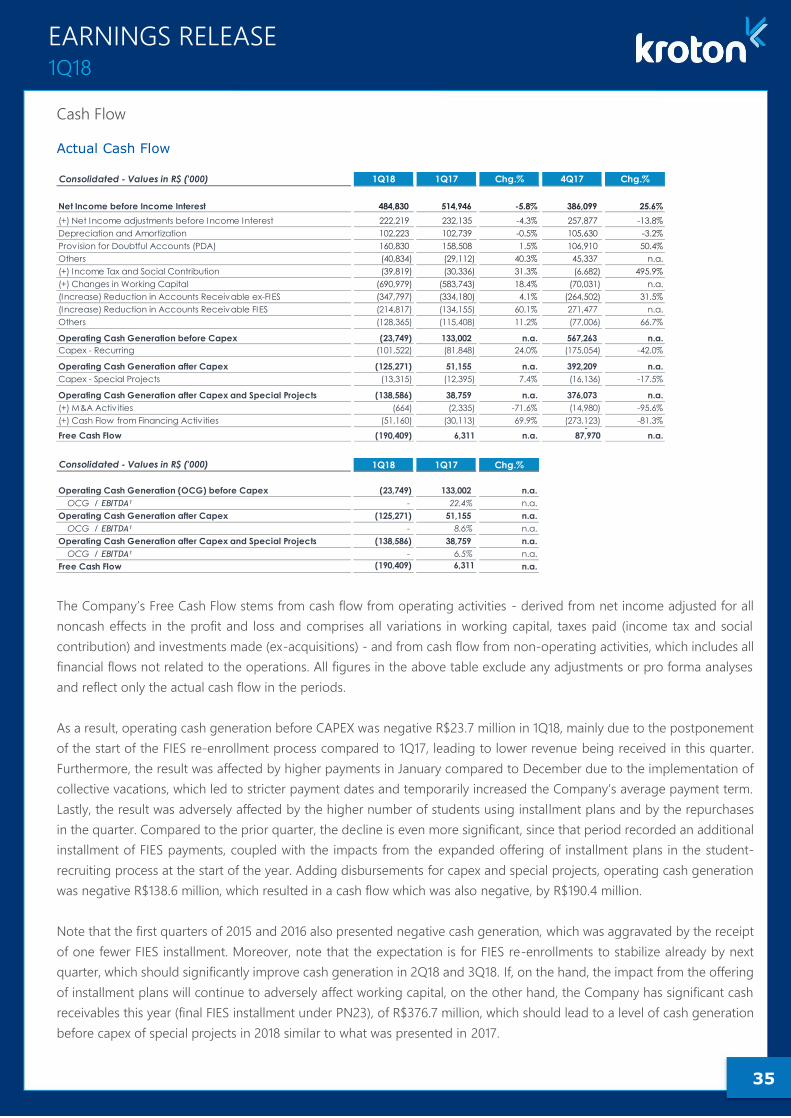

Operating cash generation after capex was negative R$125.3 million in 1Q18, with this reversal explained by the

postponement of the start of the re-enrollment process of FIES contracts compared to 1Q17, in addition to the

larger base of students with installment plans. On the other hand, the expectation is for this indicator to improve

as of the next quarter, with the normalization of FIES re-enrollments.

In April, the Company intensified its share repurchases as a way to optimize returns for shareholders, with

13,767,400 common shares repurchased since the start of the program at an average price of R$13.83 per share,

which represents 28.2% of the limit established in the program.

MESSAGE FROM MANAGEMENT

As we wrote in one of our Messages from Management a few years back, we believe that people figure at the center of the

educational process and that, at the end of the day, the most important agent in this process is the student.

Well, although not a new principle, the focus on our students has gained greater relevance as of the review of our strategic

planning process concluded in the first quarter of this year. More than that, “Student Success” has consolidated itself as the

structural pillar of all actions and decisions taken at the various levels of the organization as we strive to offer an exceptional

experience in our different learning platforms. To us, Student Success is a combination of i) academic quality, ii) employability

3

EARNINGS RELEASE 1Q18

and iii) the student experience in all its dimensions (physical and digital experience, in the academic and administrative areas).

That is what we seek relentlessly at Kroton, since our students’ success is an essential condition for our sustainable growth.

With that in mind, in April, we held our annual meeting with around 450 leaders of the Company to disseminate our strategic

guidelines and intensify all of the efforts to improve Kroton’s position from the perspective of our students and other

stakeholders. It was three intense days, filled with content and always highlighting that efficiency and a mindset guided by

Student Success go hand in hand, and will be embraced by all the digital transformation initiatives that we are currently

developing.

And, speaking of digital transformation, we have made extensive progress to date. We have approximately 150 professionals

with IT and Business profiles already working and organized into 3 “trains” of agile deliveries. Another 150 professionals are

being trained and reorganized into 3 new “trains,” to be launched in June. By the end of the year, 100% of Kroton’s system

development teams will be working under a Scalable Agile Framework (SAFe) model to ensure complete alignment between

the business and technology areas, which is an essential step on our digital transformation journey.

Meanwhile, we continue to advance in our strategy to promote structured organic growth. For the first student-recruiting

process of 2018, we were able to implement 13 new units, of which ten are greenfield projects (all of which enjoyed successful

student-recruiting and class-formation processes) and three are acquisitions of smaller institutions. Another 20 new units are

already in the process of recruiting students for the second semester of 2018 and another 38 greenfield projects are currently

being prepared to launch their recruiting processes for next year. So, we started with 115 units and will reach 186 on-campus

units by the end of 2019, representing expansion of 62% in three years. In Distance Learning, the situation is no different,

since we launched 300 new centers since August 2017 and will open another 100 for the recruitment process this second

semester, reaching a total of 1,310 centers, or 44% more than in July 2017 (before the new regulatory framework). But our

strategy is not just about opening a campus or center. We know there is a huge difference between obtaining authorization

to open a unit and successfully implementing it. Today, the competitive advantage no longer lies in obtaining accreditation,

but in the quality of the implementation process, which involves selecting the city, determining the best location in the city,

selecting a partner, training local teams and monitoring, managing and supporting the administration of these units. This is

the major competitive advantage for implementing new units, whether in the on-campus or distance learning segment, and

the positive results achieved by Kroton’s campuses and centers to date show that we are fully prepared to successfully deliver

this organic growth.

Having at Kroton people who truly understand education certainly continues to help us make the right strategic decisions.

That was the case of the acquisition of Unopar and the merger with Anhanguera, which were ideal partners for building the

Company we are today. Likewise, we are convinced that the acquisition of a controlling interest in Somos Educação (Somos)

by our holding company Saber, which was created exclusively to manage our Primary & Secondary Education assets, also has

the potential to become a new milestone in our history. More than that, the operation represents a return to our origins,

given that Kroton operated exclusively in the Primary & Secondary Education segment since its creation in 1966 up until 2001,

when it first began offering programs in Postsecondary Education. But our determination to strengthen our presence in th is

segment at this time was a very conscious decision. Some two years ago, we decided to conduct a more in-depth study of

this market and, after a comprehensive analysis, we began forming the management team and made the strategic decision

to grow in the segment. Somos is, without a doubt, the best partner for this new milestone in our history. The transaction is

subject to typical precedent conditions and must be submitted for analysis by Brazil's antitrust authority (CADE). If approved,

the acquisition will enable the creation of an educational platform with relevant operations in various segments. Moreover,

given the high degree of complementarity, we will be able to diversify our markets and revenue sources, opening up a new

growth avenue.

In a country that so desperately needs Education to sustain its development and reduce inequality, we will continue to work

tirelessly to do our part. To achieve that, we have over 26,000 employees who are fully engaged in transforming the lives of

our students.

4

EARNINGS RELEASE 1Q18

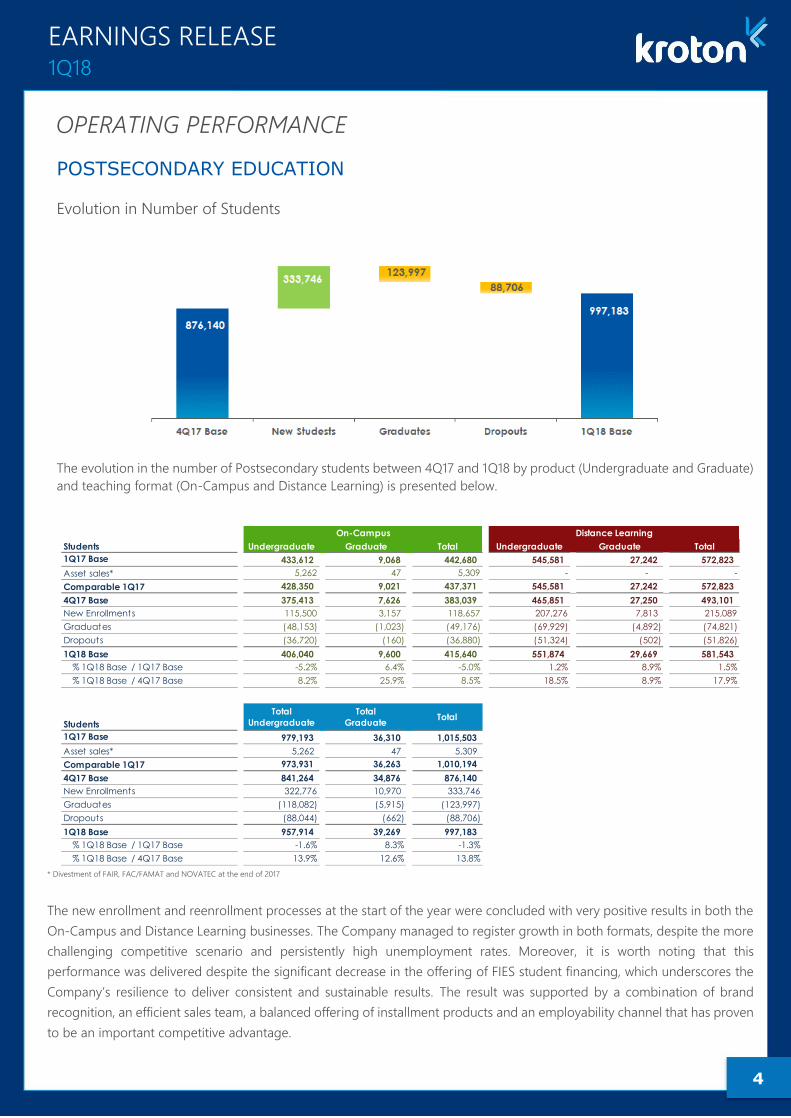

POSTSECONDARY EDUCATION

Evolution in Number of Students

The evolution in the number of Postsecondary students between 4Q17 and 1Q18 by product (Undergraduate and Graduate)

and teaching format (On-Campus and Distance Learning) is presented below.

* Divestment of FAIR, FAC/FAMAT and NOVATEC at the end of 2017

The new enrollment and reenrollment processes at the start of the year were concluded with very positive results in both the

On-Campus and Distance Learning businesses. The Company managed to register growth in both formats, despite the more

challenging competitive scenario and persistently high unemployment rates. Moreover, it is worth noting that this

performance was delivered despite the significant decrease in the offering of FIES student financing, which underscores the

Company’s resilience to deliver consistent and sustainable results. The result was supported by a combination of brand

recognition, an efficient sales team, a balanced offering of installment products and an employability channel that has proven

to be an important competitive advantage.

Students Undergraduate Graduate Total Undergraduate Graduate Total

1Q17 Base 433,612 9,068 442,680 545,581 27,242 572,823

Asset sales* 5,262 47 5,309 - - -

Comparable 1Q17 428,350 9,021 437,371 545,581 27,242 572,823

4Q17 Base 375,413 7,626 383,039 465,851 27,250 493,101

New Enrollments 115,500 3,157 118,657 207,276 7,813 215,089

Graduates (48,153) (1,023) (49,176) (69,929) (4,892) (74,821)

Dropouts (36,720) (160) (36,880) (51,324) (502) (51,826)

1Q18 Base 406,040 9,600 415,640 551,874 29,669 581,543

% 1Q18 Base / 1Q17 Base -5.2% 6.4% -5.0% 1.2% 8.9% 1.5%

% 1Q18 Base / 4Q17 Base 8.2% 25.9% 8.5% 18.5% 8.9% 17.9%

Students

1Q17 Base 979,193 36,310 1,015,503

Asset sales* 5,262 47 5,309

Comparable 1Q17 973,931 36,263 1,010,194

4Q17 Base 841,264 34,876 876,140

New Enrollments 322,776 10,970 333,746

Graduates (118,082) (5,915) (123,997)

Dropouts (88,044) (662) (88,706)

1Q18 Base 957,914 39,269 997,183

% 1Q18 Base / 1Q17 Base -1.6% 8.3% -1.3%

% 1Q18 Base / 4Q17 Base 13.9% 12.6% 13.8%

On-Campus Distance Learning

Total

Undergraduate

Total

GraduateTotal

OPERATING PERFORMANCE

5

EARNINGS RELEASE 1Q18

Overall, 322,800 new Undergraduate students were added, or 3.4% more than in the same period of 2017. This result reflects:

(i) the new programs being launched in both the On-Campus segment (especially in medical and engineering fields) and

Premium DL, which have helped to expand the product offering and addressable market; (ii) the offering of installment plans,

including the Private Special Installment Plan (PEP) and Late-Enrollment Installment Program (PMT), which can be considered

efficient student-recruiting tools; (iii) the good performance of new students paying out of pocket, which currently account

for the majority of freshmen; and (iv) the new campuses and centers opened in recent months, which, despite their low

significance in the first student-recruiting processes, will be important drivers of future growth.

The re-enrollment process (enrollments of students in the second to last academic semesters) also achieved very solid results

considering the market conditions faced in the period, registering a decline of 4% from the same period last year, a level

much lower than the increase in graduations which occurred before the start of this semester (+12% compared to 1Q17).

Considering only Graduate programs, the student base expanded 8.3% on the year-ago period, supported by the enrollment

of almost 11,000 new students coming mainly from Distance Learning programs, which more than offset the significant number

of graduations, of approximately 6,000 students in total. Bear in mind that the LFG brand also offers Graduate programs,

whose students are included in the above table.

Considering these results, the Company ended the quarter with nearly one million Postsecondary students (Undergraduate

and Graduate) in the On-Campus and Distance Learning segments combined, representing a slight reduction of 1.3% from

the same period last year and demonstrating the resilience of Kroton’s operations in a still-adverse scenario, with increased

competition, economic uncertainty and a higher number of graduations. Compared to 4Q17, the student base expanded

13.8%, supported by the solid student-recruiting process at the start of the year. Broken down by teaching format, the On-

Campus student base accounted for 42% of the total student base in the quarter, while the Distance Learning student base

accounted for 58%.

Note that the admissions and reenrollment processes for the second semester of 2018 already have begun and that Kroton

remains focused on maintaining its high academic standards, while strengthening its organic growth strategies, with the

opening of new On-Campus units and new Distance Learning centers, besides strengthening its brands and sales actions to

deliver growing results in student recruiting and retention.

Evolution of Undergraduate Dropouts

Dropout rates improved significantly in both segments. In On-Campus Education, the dropout rate stood at 11.2%, lower

even than in 1Q15. In the Distance Learning segment, the dropout rate was 13.0%, down by nearly 200 bps compared to last

year. These improvements directly reflect the expansion and consolidation of initiatives under the Retention Program, which

include, for instance, retention teams available at all units and predictive dropout models that seek to better understand the

6

EARNINGS RELEASE 1Q18

profile of Kroton’s students, aiming to identify and determine the dropout likelihood and treat the causes beforehand. Note

that this decrease in dropout rates occurred despite the change in the profile of the student base in both segments, which

makes the result in the period even more significant and reinforces the importance and success of the initiatives

implemented to improve this indicator.

FIES

Number of FIES Students

At the end of 1Q18, Kroton had 116,628 students enrolled with FIES financing, substantially fewer than in the same period of

2017, which confirms the lower share of FIES in recent student-recruiting cycles, as well as highlighting the higher number

of graduations of seniors with FIES financing. To illustrate this behavior, in the latest student-recruiting cycle, FIES accounted

for less than 3% of new enrollments in On-Campus Undergraduate programs and for only 1% of total Undergraduate new

enrollments. Moreover, the number of graduations of FIES students before the start of this semester was one of the highest

of recent years, which indicates that the program should account for a declining share of students over the coming years.

As a result, the penetration of students with FIES financing decreased 10.8 p.p. from the previous year, accounting for 28.7%

of the On-Campus Undergraduate student base, or 12.2% of the total Undergraduate student base.

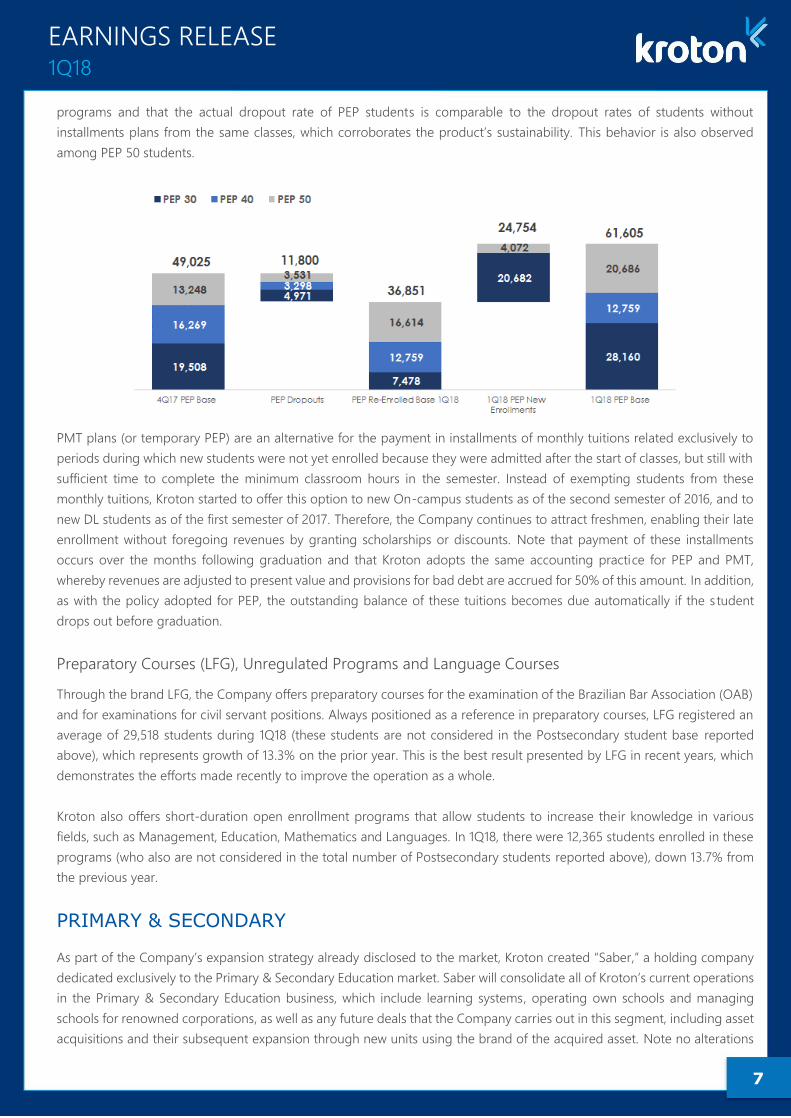

Private Special Installment Plan (PEP) and Late Enrollment Installment Plan (PMT)

At the end of 1Q18, Kroton had 61,605 students enrolled in PEP programs, of which 47,500 enrolled in PEP30 and 14,100 in

PEP50. In the most recent student-recruiting process, 24,754 new students were enrolled using PEP plans (PEP30 and PEP50),

representing approximately 21% of On-Campus new enrollments. This level was above that of the second semester of last

year and is in line with the commercial strategy adopted for the segment.

Remember that Kroton adopts a conservative approach for revenue recognition and provisioning for PEP students, which

includes Adjustment to Present Value (APV) of revenues and provisioning for bad debt equivalent to 50% of the amount

paid in installments by PEP students, as has been done since the launch of the program.

As already presented throughout 2017, the following analysis shows the evolution in the PEP30 student base, including the

number of students who migrated from PEP30 (who paid 30% of tuitions during the contract’s first year) to PEP40 and

PEP50 (who began paying 40% and 50% of tuitions during the contract’s second and third years, respectively), in accordance

with the plans’ rules. Likewise, students who re-enrolled and remained with PEP30 are those admitted in 3Q17 and who will

migrate to PEP40 in 3Q18. Furthermore, note that the dropout curve is naturally higher during the first semesters of academic

7

EARNINGS RELEASE 1Q18

programs and that the actual dropout rate of PEP students is comparable to the dropout rates of students without

installments plans from the same classes, which corroborates the product’s sustainability. This behavior is also observed

among PEP 50 students.

PMT plans (or temporary PEP) are an alternative for the payment in installments of monthly tuitions related exclusively to

periods during which new students were not yet enrolled because they were admitted after the start of classes, but still with

sufficient time to complete the minimum classroom hours in the semester. Instead of exempting students from these

monthly tuitions, Kroton started to offer this option to new On-campus students as of the second semester of 2016, and to

new DL students as of the first semester of 2017. Therefore, the Company continues to attract freshmen, enabling their late

enrollment without foregoing revenues by granting scholarships or discounts. Note that payment of these installments

occurs over the months following graduation and that Kroton adopts the same accounting practice for PEP and PMT,

whereby revenues are adjusted to present value and provisions for bad debt are accrued for 50% of this amount. In addition,

as with the policy adopted for PEP, the outstanding balance of these tuitions becomes due automatically if the s tudent

drops out before graduation.

Preparatory Courses (LFG), Unregulated Programs and Language Courses

Through the brand LFG, the Company offers preparatory courses for the examination of the Brazilian Bar Association (OAB)

and for examinations for civil servant positions. Always positioned as a reference in preparatory courses, LFG registered an

average of 29,518 students during 1Q18 (these students are not considered in the Postsecondary student base reported

above), which represents growth of 13.3% on the prior year. This is the best result presented by LFG in recent years, which

demonstrates the efforts made recently to improve the operation as a whole.

Kroton also offers short-duration open enrollment programs that allow students to increase their knowledge in various

fields, such as Management, Education, Mathematics and Languages. In 1Q18, there were 12,365 students enrolled in these

programs (who also are not considered in the total number of Postsecondary students reported above), down 13.7% from

the previous year.

PRIMARY & SECONDARY

As part of the Company’s expansion strategy already disclosed to the market, Kroton created “Saber,” a holding company

dedicated exclusively to the Primary & Secondary Education market. Saber will consolidate all of Kroton’s current operations

in the Primary & Secondary Education business, which include learning systems, operating own schools and managing

schools for renowned corporations, as well as any future deals that the Company carries out in this segment, including asset

acquisitions and their subsequent expansion through new units using the brand of the acquired asset. Note no alterations

8

EARNINGS RELEASE 1Q18

will be made to the educational projects of institutions under Saber, since they concentrate a large part of the value

attributed to the brand.

Through the Pitágoras Network, which offers Learning Systems, including textbook collections, teacher training, education;

assessments and other services to private schools in the Pre-School, Primary & Secondary Education, Saber serves a total

of 687 Associated Schools and approximately 227,000 students in the private sector, which represent increases of 2.2% and

3.1% compared to last year, respectively.

In April, Saber concluded its first acquisition, of Centro Educacional Leonardo Da Vinci (“CELV”). Founded in the 1990s and

located in Vitória, Espírito Santo, CELV has unique facilities and serves 1,311 students (December 2017 base), 71% of whom

are enrolled in full-time programs. With a strong focus on quality, CELV placed first in the state’s ENEM examination for six

times in recent years, and offers a bilingual program from pre school to secondary school, including the option of a high

school diploma that facilitates acceptance by U.S. universities.

More recently, on April 22, Saber announced the signing of an agreement to acquire a controlling interest in Somos

Educação S.A., which has complementary operations, offering a wide array of high-quality products and services in Primary

& Secondary Education, including high schools, learning systems, textbooks, publishing houses and language courses. With

the acquisition, Saber will serve 37,000 students in own schools, 25,000 students in language courses, 1.2 million students in

private schools served by learning systems, and reach 33 million students in public schools through the National Textbook

Program (PNLD). Saber will also become an important community of teachers who use its products and services in Brazil,

with approximately 85,000 professionals working in private schools and 1.7 million teachers in public schools.

Saber will be responsible for renowned teaching institutions, such as Pitágoras, PH, Anglo, Red Balloon, and publishing

houses, such as Ática, Scipione and Saraiva, among others, with a nationwide presence in all Brazilian states.

The consummation of the transaction is subject to evaluation and prior approval by Brazil's antitrust authority (CADE). Until

all due validations are obtained and the operation is approved by the regulatory agency, the companies wi ll continue to

operate independently.

9

EARNINGS RELEASE 1Q18

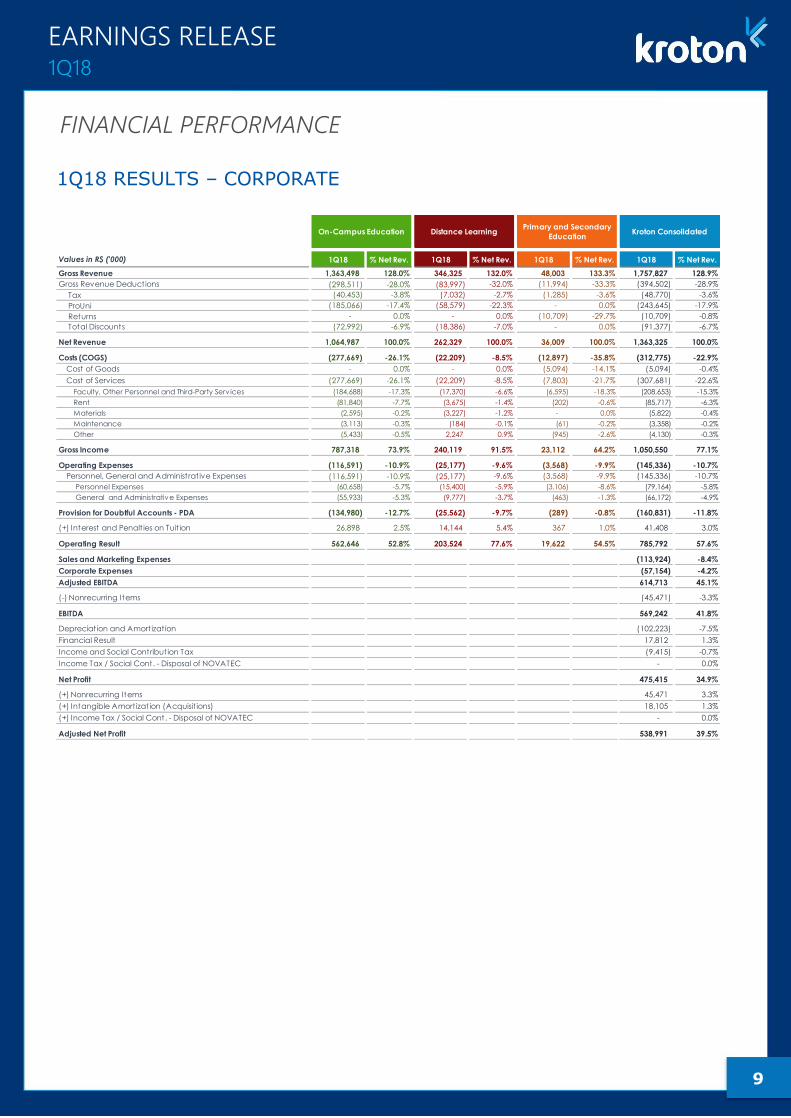

1Q18 RESULTS – CORPORATE

Values in R$ ('000) 1Q18 % Net Rev. 1Q18 % Net Rev. 1Q18 % Net Rev. 1Q18 % Net Rev.

Gross Revenue 1,363,498 128.0% 346,325 132.0% 48,003 133.3% 1,757,827 128.9%

Gross Revenue Deductions (298,511) -28.0% (83,997) -32.0% (11,994) -33.3% (394,502) -28.9%

Tax (40,453) -3.8% (7,032) -2.7% (1,285) -3.6% (48,770) -3.6%

ProUni (185,066) -17.4% (58,579) -22.3% - 0.0% (243,645) -17.9%

Returns - 0.0% - 0.0% (10,709) -29.7% (10,709) -0.8%

Total Discounts (72,992) -6.9% (18,386) -7.0% - 0.0% (91,377) -6.7%

Net Revenue 1,064,987 100.0% 262,329 100.0% 36,009 100.0% 1,363,325 100.0%

Costs (COGS) (277,669) -26.1% (22,209) -8.5% (12,897) -35.8% (312,775) -22.9%

Cost of Goods - 0.0% - 0.0% (5,094) -14.1% (5,094) -0.4%

Cost of Services (277,669) -26.1% (22,209) -8.5% (7,803) -21.7% (307,681) -22.6%

Faculty, Other Personnel and Third-Party Serv ices (184,688) -17.3% (17,370) -6.6% (6,595) -18.3% (208,653) -15.3%

Rent (81,840) -7.7% (3,675) -1.4% (202) -0.6% (85,717) -6.3%

Materials (2,595) -0.2% (3,227) -1.2% - 0.0% (5,822) -0.4%

Maintenance (3,113) -0.3% (184) -0.1% (61) -0.2% (3,358) -0.2%

Other (5,433) -0.5% 2,247 0.9% (945) -2.6% (4,130) -0.3%

Gross Income 787,318 73.9% 240,119 91.5% 23,112 64.2% 1,050,550 77.1%

Operating Expenses (116,591) -10.9% (25,177) -9.6% (3,568) -9.9% (145,336) -10.7%

Personnel, General and Administrat ive Expenses (116,591) -10.9% (25,177) -9.6% (3,568) -9.9% (145,336) -10.7%

Personnel Expenses (60,658) -5.7% (15,400) -5.9% (3,106) -8.6% (79,164) -5.8%

General and Administrative Expenses (55,933) -5.3% (9,777) -3.7% (463) -1.3% (66,172) -4.9%

Provision for Doubtful Accounts - PDA (134,980) -12.7% (25,562) -9.7% (289) -0.8% (160,831) -11.8%

(+) Interest and Penalt ies on Tuit ion 26,898 2.5% 14,144 5.4% 367 1.0% 41,408 3.0%

Operating Result 562,646 52.8% 203,524 77.6% 19,622 54.5% 785,792 57.6%

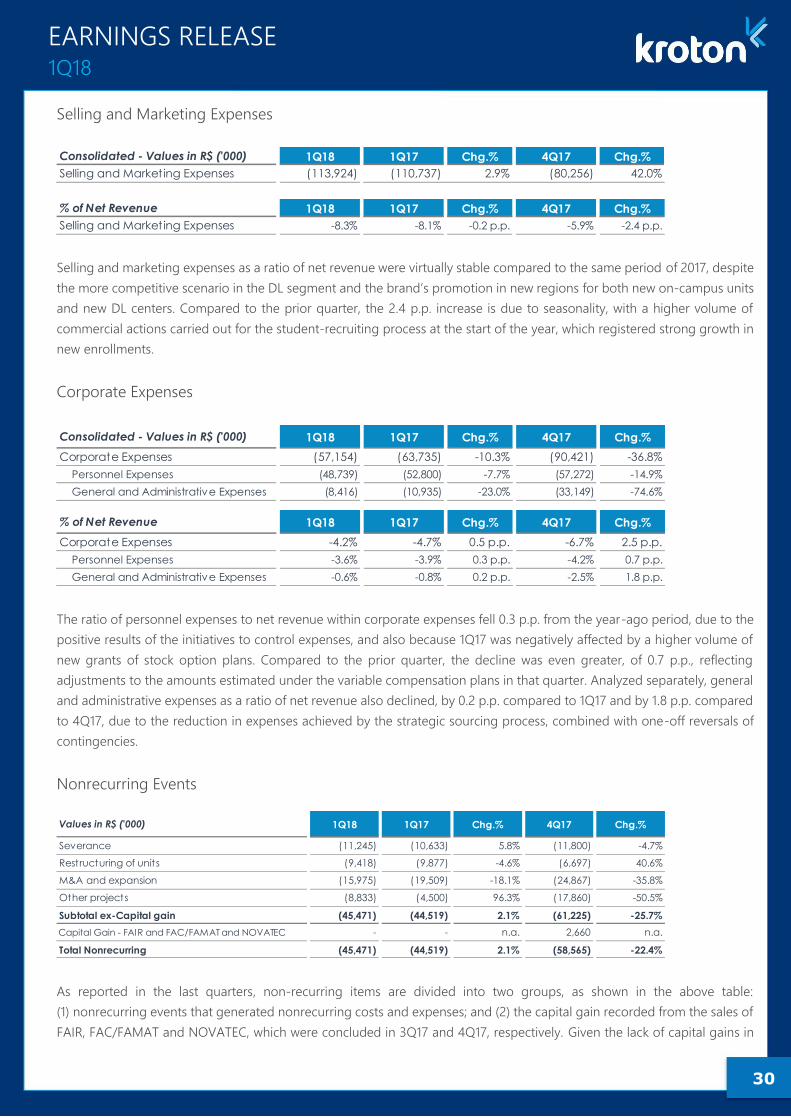

Sales and Marketing Expenses (113,924) -8.4%

Corporate ExpensesC

o(57,154) -4.2%

Adjusted EBITDA 614,713 45.1%

(-) Nonrecurring Items (45,471) -3.3%

EBITDA 569,242 41.8%

Depreciat ion and Amort izat ion (102,223) -7.5%

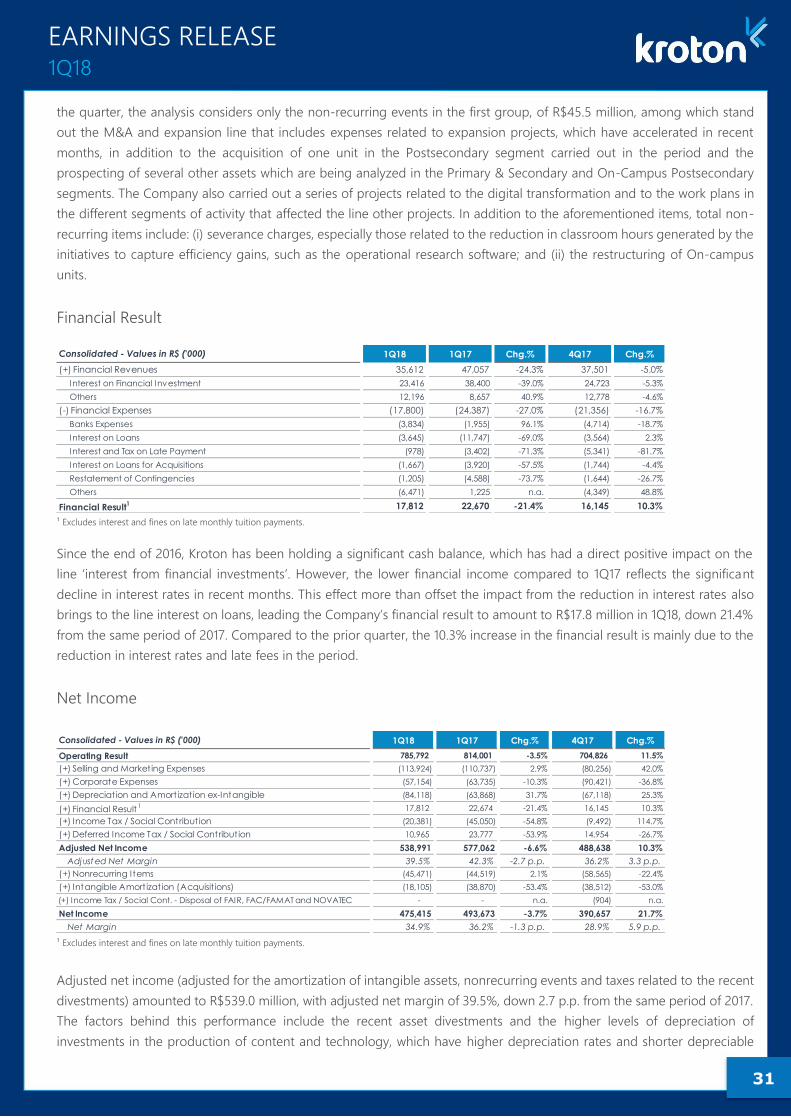

Financial Result 17,812 1.3%

Income and Social Contribut ion Tax (9,415) -0.7%

Income Tax / Social Cont. - Disposal of NOVATEC - 0.0%

Net Profit 475,415 34.9%

(+) Nonrecurring Items 45,471 3.3%

(+) Intangible Amort izat ion (Acquisit ions) 18,105 1.3%

(+) Income Tax / Social Cont. - Disposal of NOVATEC - 0.0%

Adjusted Net Profit 538,991 39.5%

On-Campus Education Distance LearningPrimary and Secondary

EducationKroton Consolidated

FINANCIAL PERFORMANCE

10

EARNINGS RELEASE 1Q18

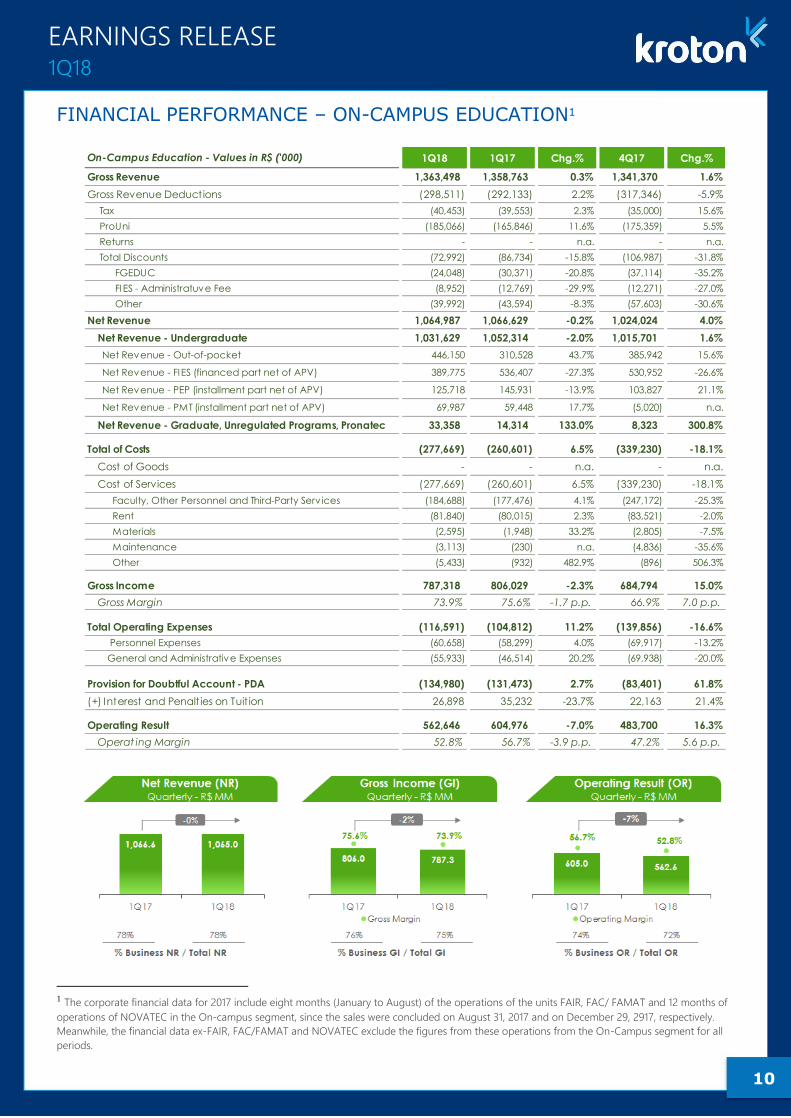

FINANCIAL PERFORMANCE – ON-CAMPUS EDUCATION1

1 The corporate financial data for 2017 include eight months (January to August) of the operations of the units FAIR, FAC/ FAMAT and 12 months of

operations of NOVATEC in the On-campus segment, since the sales were concluded on August 31, 2017 and on December 29, 2917, respectively.

Meanwhile, the financial data ex-FAIR, FAC/FAMAT and NOVATEC exclude the figures from these operations from the On-Campus segment for all

periods.

On-Campus Education - Values in R$ ('000) 1Q18 1Q17 Chg.% 4Q17 Chg.%

Gross Revenue 1,363,498 1,358,763 0.3% 1,341,370 1.6%

Gross Revenue Deductions (298,511) (292,133) 2.2% (317,346) -5.9%

Tax (40,453) (39,553) 2.3% (35,000) 15.6%

ProUni (185,066) (165,846) 11.6% (175,359) 5.5%

Returns - - n.a. - n.a.

Total Discounts (72,992) (86,734) -15.8% (106,987) -31.8%

FGEDUC (24,048) (30,371) -20.8% (37,114) -35.2%

FIES - Administratuve Fee (8,952) (12,769) -29.9% (12,271) -27.0%

Other (39,992) (43,594) -8.3% (57,603) -30.6%

Net Revenue 1,064,987 1,066,629 -0.2% 1,024,024 4.0%

Net Revenue - Undergraduate 1,031,629 1,052,314 -2.0% 1,015,701 1.6%

Net Revenue - Out-of-pocket 446,150 310,528 43.7% 385,942 15.6%

Net Revenue - FIES (financed part net of APV) 389,775 536,407 -27.3% 530,952 -26.6%

Net Revenue - PEP (installment part net of APV) 125,718 145,931 -13.9% 103,827 21.1%

Net Revenue - PMT (installment part net of APV) 69,987 59,448 17.7% (5,020) n.a.

Net Revenue - Graduate, Unregulated Programs, Pronatec 33,358 14,314 133.0% 8,323 300.8%

Total of Costs (277,669) (260,601) 6.5% (339,230) -18.1%

Cost of Goods - - n.a. - n.a.

Cost of Services (277,669) (260,601) 6.5% (339,230) -18.1%

Faculty, Other Personnel and Third-Party Serv ices (184,688) (177,476) 4.1% (247,172) -25.3%

Rent (81,840) (80,015) 2.3% (83,521) -2.0%

Materials (2,595) (1,948) 33.2% (2,805) -7.5%

Maintenance (3,113) (230) n.a. (4,836) -35.6%

Other (5,433) (932) 482.9% (896) 506.3%

Gross Income 787,318 806,029 -2.3% 684,794 15.0%

Gross Margin 73.9% 75.6% -1.7 p.p. 66.9% 7.0 p.p.

Total Operating Expenses (116,591) (104,812) 11.2% (139,856) -16.6%

Personnel Expenses (60,658) (58,299) 4.0% (69,917) -13.2%

General and Administrative Expenses (55,933) (46,514) 20.2% (69,938) -20.0%

Provision for Doubtful Account - PDA (134,980) (131,473) 2.7% (83,401) 61.8%

(+) Interest and Penalt ies on Tuit ion 26,898 35,232 -23.7% 22,163 21.4%

Operating Result 562,646 604,976 -7.0% 483,700 16.3%

Operat ing Margin 52.8% 56.7% -3.9 p.p. 47.2% 5.6 p.p.

11

EARNINGS RELEASE 1Q18

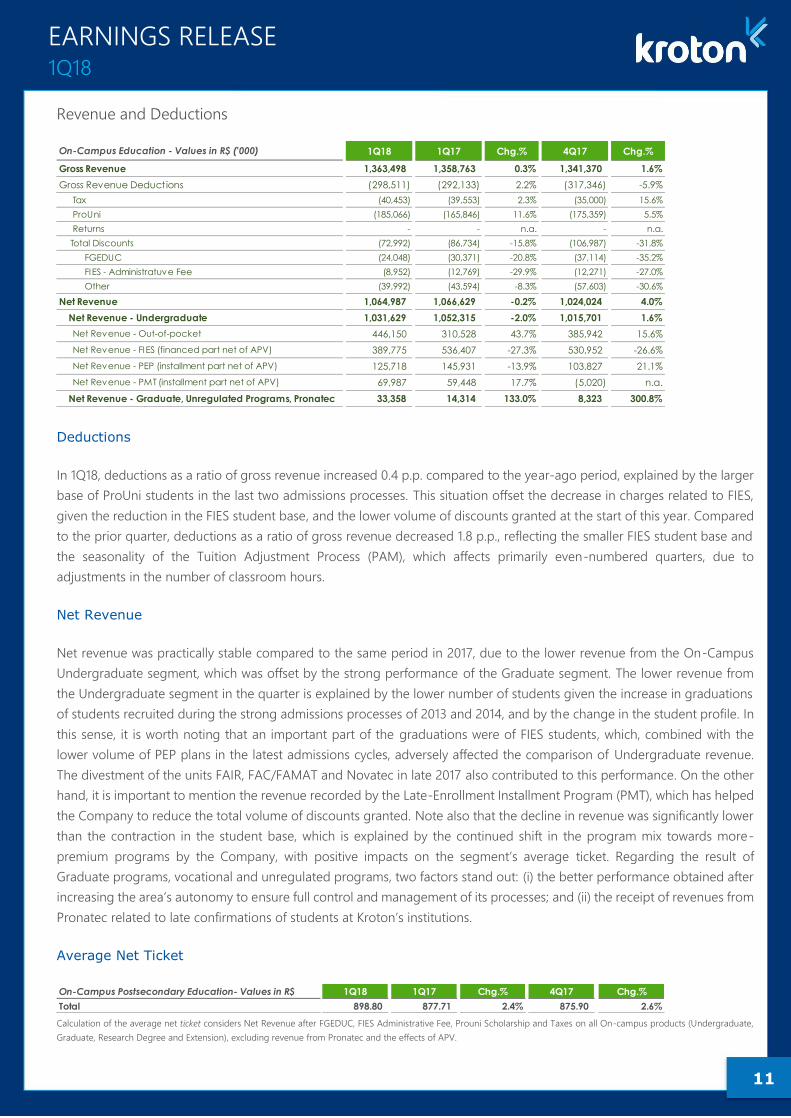

Revenue and Deductions

Deductions

In 1Q18, deductions as a ratio of gross revenue increased 0.4 p.p. compared to the year-ago period, explained by the larger

base of ProUni students in the last two admissions processes. This situation offset the decrease in charges related to FIES,

given the reduction in the FIES student base, and the lower volume of discounts granted at the start of this year. Compared

to the prior quarter, deductions as a ratio of gross revenue decreased 1.8 p.p., reflecting the smaller FIES student base and

the seasonality of the Tuition Adjustment Process (PAM), which affects primarily even-numbered quarters, due to

adjustments in the number of classroom hours.

Net Revenue

Net revenue was practically stable compared to the same period in 2017, due to the lower revenue from the On-Campus

Undergraduate segment, which was offset by the strong performance of the Graduate segment. The lower revenue from

the Undergraduate segment in the quarter is explained by the lower number of students given the increase in graduations

of students recruited during the strong admissions processes of 2013 and 2014, and by the change in the student profile. In

this sense, it is worth noting that an important part of the graduations were of FIES students, which, combined with the

lower volume of PEP plans in the latest admissions cycles, adversely affected the comparison of Undergraduate revenue.

The divestment of the units FAIR, FAC/FAMAT and Novatec in late 2017 also contributed to this performance. On the other

hand, it is important to mention the revenue recorded by the Late-Enrollment Installment Program (PMT), which has helped

the Company to reduce the total volume of discounts granted. Note also that the decline in revenue was significantly lower

than the contraction in the student base, which is explained by the continued shift in the program mix towards more-

premium programs by the Company, with positive impacts on the segment’s average ticket. Regarding the result of

Graduate programs, vocational and unregulated programs, two factors stand out: (i) the better performance obtained after

increasing the area’s autonomy to ensure full control and management of its processes; and (ii) the receipt of revenues from

Pronatec related to late confirmations of students at Kroton’s institutions.

Average Net Ticket

Calculation of the average net ticket considers Net Revenue after FGEDUC, FIES Administrative Fee, Prouni Scholarship and Taxes on all On-campus products (Undergraduate,

Graduate, Research Degree and Extension), excluding revenue from Pronatec and the effects of APV.

On-Campus Education - Values in R$ ('000) 1Q18 1Q17 Chg.% 4Q17 Chg.%

Gross Revenue 1,363,498 1,358,763 0.3% 1,341,370 1.6%

Gross Revenue Deductions (298,511) (292,133) 2.2% (317,346) -5.9%

Tax (40,453) (39,553) 2.3% (35,000) 15.6%

ProUni (185,066) (165,846) 11.6% (175,359) 5.5%

Returns - - n.a. - n.a.

Total Discounts (72,992) (86,734) -15.8% (106,987) -31.8%

FGEDUC (24,048) (30,371) -20.8% (37,114) -35.2%

FIES - Administratuve Fee (8,952) (12,769) -29.9% (12,271) -27.0%

Other (39,992) (43,594) -8.3% (57,603) -30.6%

Net Revenue 1,064,987 1,066,629 -0.2% 1,024,024 4.0%

Net Revenue - Undergraduate 1,031,629 1,052,315 -2.0% 1,015,701 1.6%

Net Revenue - Out-of-pocket 446,150 310,528 43.7% 385,942 15.6%

Net Revenue - FIES (financed part net of APV) 389,775 536,407 -27.3% 530,952 -26.6%

Net Revenue - PEP (installment part net of APV) 125,718 145,931 -13.9% 103,827 21.1%

Net Revenue - PMT (installment part net of APV) 69,987 59,448 17.7% (5,020) n.a.

Net Revenue - Graduate, Unregulated Programs, Pronatec 33,358 14,314 133.0% 8,323 300.8%

On-Campus Postsecondary Education- Values in R$ 1Q18 1Q17 Chg.% 4Q17 Chg.%

Total 898.80 877.71 2.4% 875.90 2.6%

12

EARNINGS RELEASE 1Q18

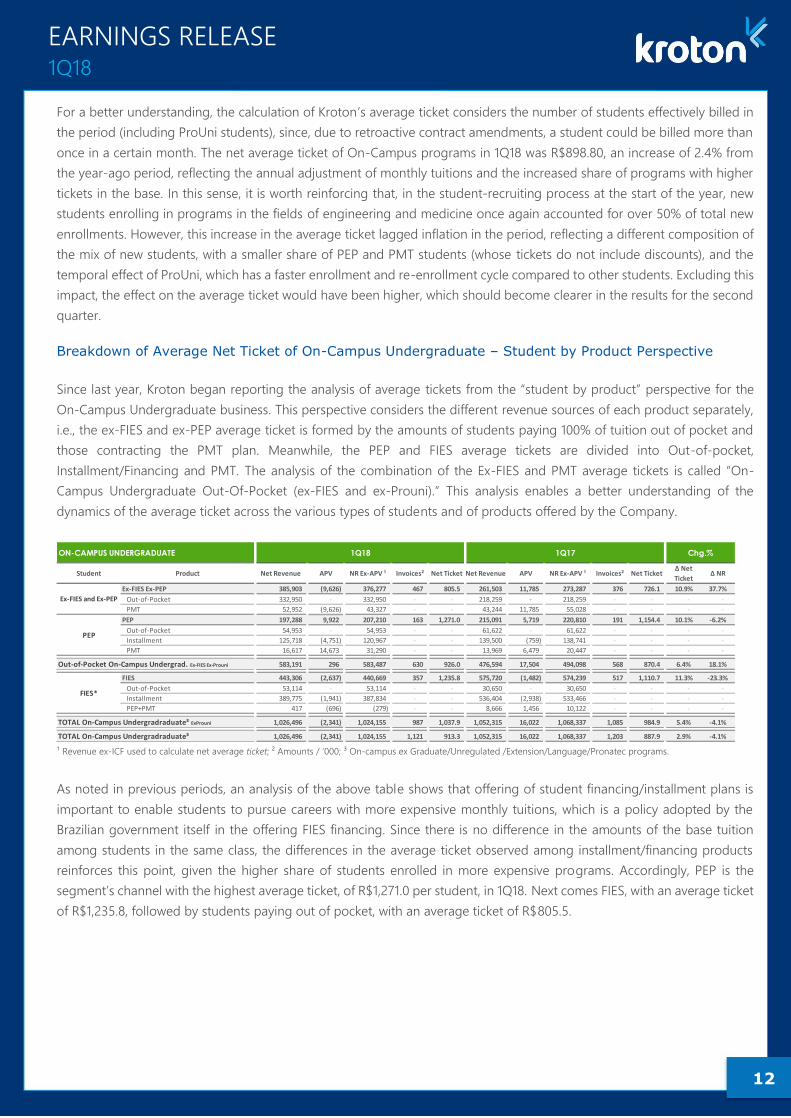

For a better understanding, the calculation of Kroton’s average ticket considers the number of students effectively billed in

the period (including ProUni students), since, due to retroactive contract amendments, a student could be billed more than

once in a certain month. The net average ticket of On-Campus programs in 1Q18 was R$898.80, an increase of 2.4% from

the year-ago period, reflecting the annual adjustment of monthly tuitions and the increased share of programs with higher

tickets in the base. In this sense, it is worth reinforcing that, in the student-recruiting process at the start of the year, new

students enrolling in programs in the fields of engineering and medicine once again accounted for over 50% of total new

enrollments. However, this increase in the average ticket lagged inflation in the period, reflecting a different composition of

the mix of new students, with a smaller share of PEP and PMT students (whose tickets do not include discounts), and the

temporal effect of ProUni, which has a faster enrollment and re-enrollment cycle compared to other students. Excluding this

impact, the effect on the average ticket would have been higher, which should become clearer in the results for the second

quarter.

Breakdown of Average Net Ticket of On-Campus Undergraduate – Student by Product Perspective

Since last year, Kroton began reporting the analysis of average tickets from the “student by product” perspective for the

On-Campus Undergraduate business. This perspective considers the different revenue sources of each product separately,

i.e., the ex-FIES and ex-PEP average ticket is formed by the amounts of students paying 100% of tuition out of pocket and

those contracting the PMT plan. Meanwhile, the PEP and FIES average tickets are divided into Out-of-pocket,

Installment/Financing and PMT. The analysis of the combination of the Ex-FIES and PMT average tickets is called “On-

Campus Undergraduate Out-Of-Pocket (ex-FIES and ex-Prouni).” This analysis enables a better understanding of the

dynamics of the average ticket across the various types of students and of products offered by the Company.

¹ Revenue ex-ICF used to calculate net average ticket; ² Amounts / ‘000; ³ On-campus ex Graduate/Unregulated /Extension/Language/Pronatec programs.

As noted in previous periods, an analysis of the above table shows that offering of student financing/installment plans is

important to enable students to pursue careers with more expensive monthly tuitions, which is a policy adopted by the

Brazilian government itself in the offering FIES financing. Since there is no difference in the amounts of the base tuition

among students in the same class, the differences in the average ticket observed among installment/financing products

reinforces this point, given the higher share of students enrolled in more expensive programs. Accordingly, PEP is the

segment’s channel with the highest average ticket, of R$1,271.0 per student, in 1Q18. Next comes FIES, with an average ticket

of R$1,235.8, followed by students paying out of pocket, with an average ticket of R$805.5.

Student Product Net Revenue APV NR Ex-APV ¹ Invoices² Net Ticket Net Revenue APV NR Ex-APV ¹ Invoices² Net TicketΔ Net

TicketΔ NR

Ex-FIES Ex-PEP 385,903 (9,626) 376,277 467 805.5 261,503 11,785 273,287 376 726.1 10.9% 37.7%

Out-of-Pocket 332,950 - 332,950 - - 218,259 - 218,259 - - - -

PMT 52,952 (9,626) 43,327 - - 43,244 11,785 55,028 - - - -

PEP 197,288 9,922 207,210 163 1,271.0 215,091 5,719 220,810 191 1,154.4 10.1% -6.2%

Out-of-Pocket 54,953 - 54,953 - - 61,622 - 61,622 - - - -

Installment 125,718 (4,751) 120,967 - - 139,500 (759) 138,741 - - - -

PMT 16,617 14,673 31,290 - - 13,969 6,479 20,447 - - - -

583,191 296 583,487 630 926.0 476,594 17,504 494,098 568 870.4 6.4% 18.1%

FIES 443,306 (2,637) 440,669 357 1,235.8 575,720 (1,482) 574,239 517 1,110.7 11.3% -23.3%

Out-of-Pocket 53,114 - 53,114 - - 30,650 - 30,650 - - - -

Installment 389,775 (1,941) 387,834 - - 536,404 (2,938) 533,466 - - - -

PEP+PMT 417 (696) (279) - - 8,666 1,456 10,122 - - - -

1,026,496 (2,341) 1,024,155 987 1,037.9 1,052,315 16,022 1,068,337 1,085 984.9 5.4% -4.1%

1,026,496 (2,341) 1,024,155 1,121 913.3 1,052,315 16,022 1,068,337 1,203 887.9 2.9% -4.1%

Ex-FIES and Ex-PEP

PEP

Out-of-Pocket On-Campus Undergrad. Ex-FIES Ex-Prouni

FIES*

TOTAL On-Campus Undergradraduate³ ExProuni

TOTAL On-Campus Undergradraduate³

ON-CAMPUS UNDERGRADUATE 1Q18 1Q17 Chg.%

13

EARNINGS RELEASE 1Q18

Costs

In 1Q18, cost of services as a ratio of net revenue increased by 1.6 p.p. compared to the same period of 2017. This result

shows the costs related to the expansion projects of the Company, which significantly increased the number of new units in

recent months. This ends up creating additional costs related to both faculty and rent, which are the segment’s main

expenses. Although all efficiency levers are functioning fully, it is only natural to assume that pressures from growth projects

will adversely affect results in the short term. However, initiatives related to implementing the operational research (OR)

software, combined with increased efficiency of faculty allocation and utilization of facilities, in addition to negotiations

related to strategic sourcing, remain the key factors for maintaining an optimized cost structure for the segment. Compared

to the prior quarter, total costs as a ratio of net revenue decreased 7.1 p.p., a result that exceeds the seasonality of the

business and attests to the robustness of the cost controls.

Gross Income

Gross income from On-Campus Education was R$787.3 million in 1Q18, decreasing 2.3% from the same period last year.

The combination of stable revenue and a larger cost structure to support growth projects led to gross margin contraction

of 1.7 p.p. in the period. Compared to the prior quarter, gross margin expanded 7.0 p.p., supported by revenue growth in

the period due to the solid student-recruiting results at the start of the year and by the seasonally lower operating costs.

On-Campus Education - Values in R$ ('000) 1Q18 1Q17 Chg.% 4Q17 Chg.%

Total of Costs (277,669) (260,601) 6.5% (339,230) -18.1%

Cost of Goods (CG) - - n.a. - n.a.

Cost of Services (CS) (277,669) (260,601) 6.5% (339,230) -18.1%

Faculty, Other Personnel and Third-Party Serv ices (184,688) (177,476) 4.1% (247,172) -25.3%

Rent (81,840) (80,015) 2.3% (83,521) -2.0%

Materials (2,595) (1,948) 33.2% (2,805) -7.5%

Maintenance (3,113) (230) n.a. (4,836) -35.6%

Other (5,433) (932) 482.9% (896) 506.3%

% of Net Revenues 1Q18 1Q17 Chg.% 4Q17 Chg.%

Total of Costs -26.1% -24.4% -1.6 p.p. -33.1% 7.1 p.p.

Cost of Goods (CG) 0.0% 0.0% n.a. 0.0% n.a.

Cost of Services (CS) -26.1% -24.4% -1.6 p.p. -33.1% 7.1 p.p.

Faculty, Other Personnel and Third-Party Serv ices -17.3% -16.6% -0.7 p.p. -24.1% 6.8 p.p.

Rent -7.7% -7.5% -0.2 p.p. -8.2% 0.5 p.p.

Materials -0.2% -0.2% -0.1 p.p. -0.3% 0.0 p.p.

Maintenance -0.3% 0.0% -0.3 p.p. -0.5% 0.2 p.p.

Other -0.5% -0.1% -0.4 p.p. -0.1% -0.4 p.p.

On-Campus Education - Values in R$ ('000) 1Q18 1Q17 Chg.% 4Q17 Chg.%

Gross Income 787,318 806,029 -2.3% 684,794 15.0%

Gross Margin 73.9% 75.6% -1.7 p.p. 66.9% 7.0 p.p.

14

EARNINGS RELEASE 1Q18

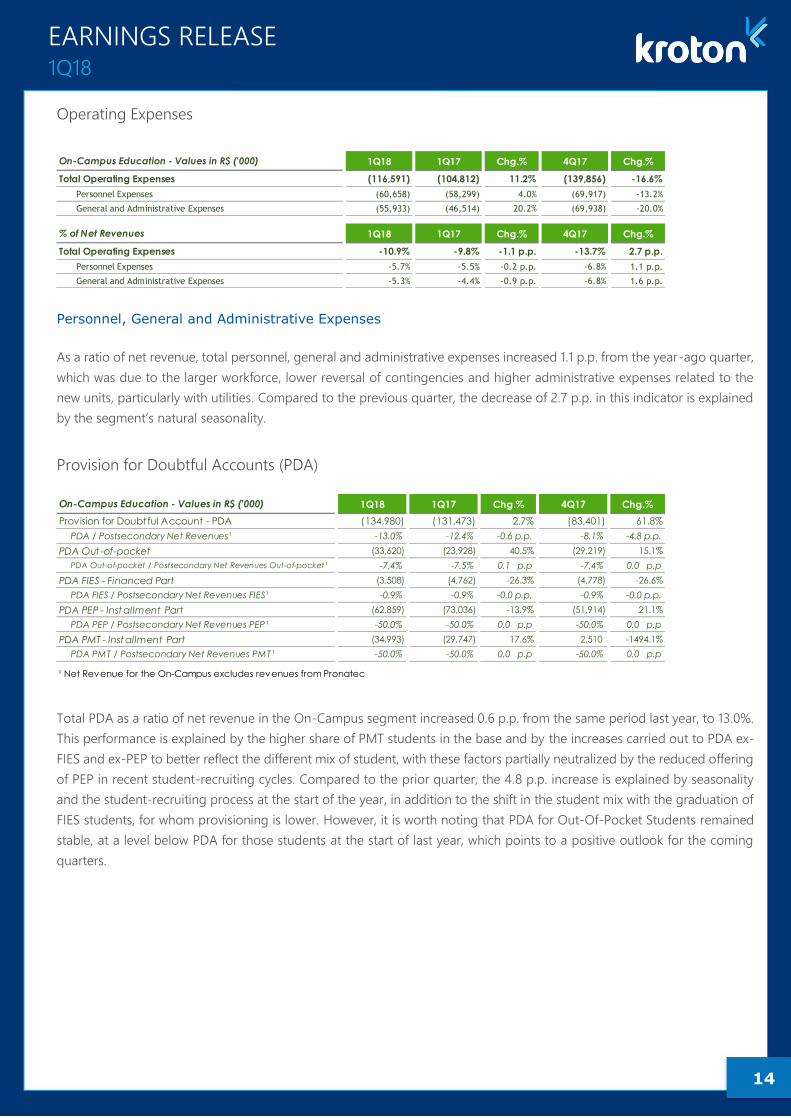

Operating Expenses

Personnel, General and Administrative Expenses

As a ratio of net revenue, total personnel, general and administrative expenses increased 1.1 p.p. from the year-ago quarter,

which was due to the larger workforce, lower reversal of contingencies and higher administrative expenses related to the

new units, particularly with utilities. Compared to the previous quarter, the decrease of 2.7 p.p. in this indicator is explained

by the segment’s natural seasonality.

Provision for Doubtful Accounts (PDA)

Total PDA as a ratio of net revenue in the On-Campus segment increased 0.6 p.p. from the same period last year, to 13.0%.

This performance is explained by the higher share of PMT students in the base and by the increases carried out to PDA ex-

FIES and ex-PEP to better reflect the different mix of student, with these factors partially neutralized by the reduced offering

of PEP in recent student-recruiting cycles. Compared to the prior quarter, the 4.8 p.p. increase is explained by seasonality

and the student-recruiting process at the start of the year, in addition to the shift in the student mix with the graduation of

FIES students, for whom provisioning is lower. However, it is worth noting that PDA for Out-Of-Pocket Students remained

stable, at a level below PDA for those students at the start of last year, which points to a positive outlook for the coming

quarters.

On-Campus Education - Values in R$ ('000) 1Q18 1Q17 Chg.% 4Q17 Chg.%

Total Operating Expenses (116,591) (104,812) 11.2% (139,856) -16.6%

Personnel Expenses (60,658) (58,299) 4.0% (69,917) -13.2%

General and Administrative Expenses (55,933) (46,514) 20.2% (69,938) -20.0%

% of Net Revenues 1Q18 1Q17 Chg.% 4Q17 Chg.%

Total Operating Expenses -10.9% -9.8% -1.1 p.p. -13.7% 2.7 p.p.

Personnel Expenses -5.7% -5.5% -0.2 p.p. -6.8% 1.1 p.p.

General and Administrative Expenses -5.3% -4.4% -0.9 p.p. -6.8% 1.6 p.p.

On-Campus Education - Values in R$ ('000) 1Q18 1Q17 Chg.% 4Q17 Chg.%

Provision for Doubtful Account - PDA (134,980) (131,473) 2.7% (83,401) 61.8%

PDA / Postsecondary Net Revenues¹ -13.0% -12.4% -0.6 p.p. -8.1% -4.8 p.p.

PDA Out -of-pocket (33,620) (23,928) 40.5% (29,219) 15.1%

PDA Out-of-pocket / Postsecondary Net Revenues Out-of-pocket¹ -7.4% -7.5% 0.1 p.p -7.4% 0.0 p.p

PDA FIES - Financed Part (3,508) (4,762) -26.3% (4,778) -26.6%

PDA FIES / Postsecondary Net Revenues FIES¹ -0.9% -0.9% -0.0 p.p. -0.9% -0.0 p.p.

PDA PEP - Inst allment Part (62,859) (73,036) -13.9% (51,914) 21.1%

PDA PEP / Postsecondary Net Revenues PEP¹ -50.0% -50.0% 0.0 p.p -50.0% 0.0 p.p

PDA PMT - Inst allment Part (34,993) (29,747) 17.6% 2,510 -1494.1%

PDA PMT / Postsecondary Net Revenues PMT¹ -50.0% -50.0% 0.0 p.p -50.0% 0.0 p.p

¹ Net Revenue for the On-Campus excludes revenues from Pronatec

15

EARNINGS RELEASE 1Q18

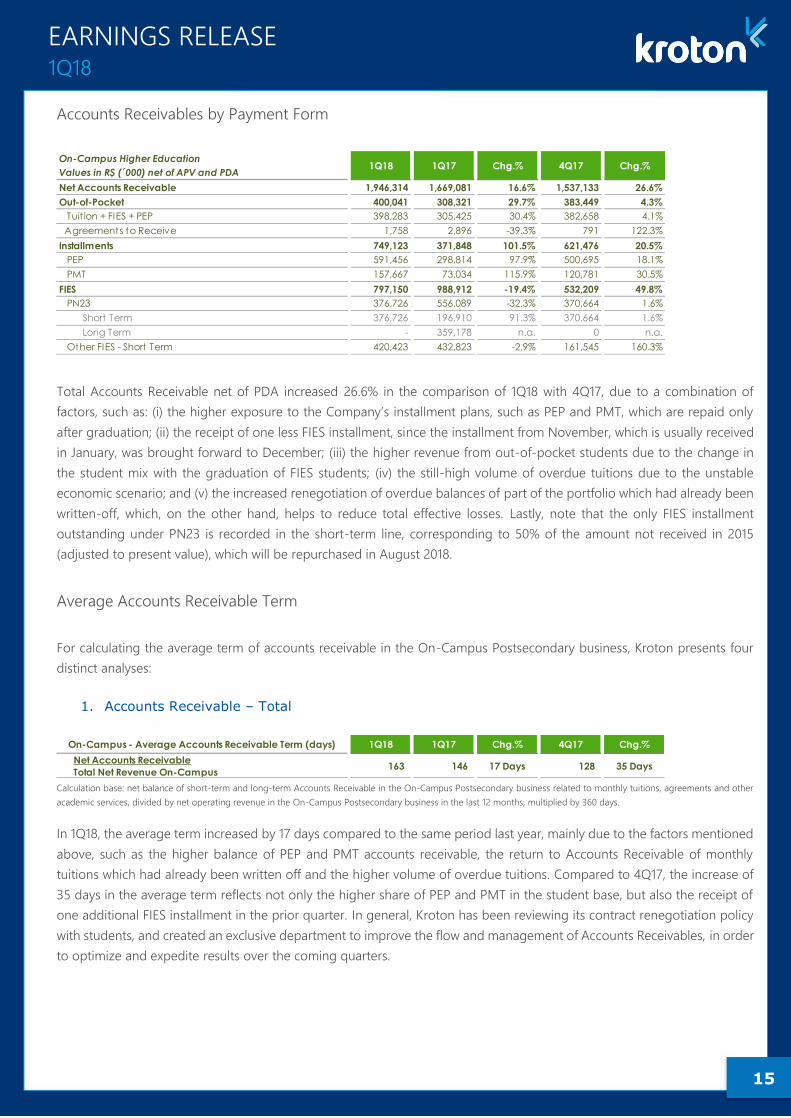

Accounts Receivables by Payment Form

Total Accounts Receivable net of PDA increased 26.6% in the comparison of 1Q18 with 4Q17, due to a combination of

factors, such as: (i) the higher exposure to the Company’s installment plans, such as PEP and PMT, which are repaid only

after graduation; (ii) the receipt of one less FIES installment, since the installment from November, which is usually received

in January, was brought forward to December; (iii) the higher revenue from out-of-pocket students due to the change in

the student mix with the graduation of FIES students; (iv) the still-high volume of overdue tuitions due to the unstable

economic scenario; and (v) the increased renegotiation of overdue balances of part of the portfolio which had already been

written-off, which, on the other hand, helps to reduce total effective losses. Lastly, note that the only FIES installment

outstanding under PN23 is recorded in the short-term line, corresponding to 50% of the amount not received in 2015

(adjusted to present value), which will be repurchased in August 2018.

Average Accounts Receivable Term

For calculating the average term of accounts receivable in the On-Campus Postsecondary business, Kroton presents four

distinct analyses:

1. Accounts Receivable – Total

Calculation base: net balance of short-term and long-term Accounts Receivable in the On-Campus Postsecondary business related to monthly tuitions, agreements and other

academic services, divided by net operating revenue in the On-Campus Postsecondary business in the last 12 months, multiplied by 360 days.

In 1Q18, the average term increased by 17 days compared to the same period last year, mainly due to the factors mentioned

above, such as the higher balance of PEP and PMT accounts receivable, the return to Accounts Receivable of monthly

tuitions which had already been written off and the higher volume of overdue tuitions. Compared to 4Q17, the increase of

35 days in the average term reflects not only the higher share of PEP and PMT in the student base, but also the receipt of

one additional FIES installment in the prior quarter. In general, Kroton has been reviewing its contract renegotiation policy

with students, and created an exclusive department to improve the flow and management of Accounts Receivables, in order

to optimize and expedite results over the coming quarters.

On-Campus Higher Education

Values in R$ (´000) net of APV and PDA1Q18 1Q17 Chg.% 4Q17 Chg.%

Net Accounts Receivable 1,946,314 1,669,081 16.6% 1,537,133 26.6%

Out-of-Pocket 400,041 308,321 29.7% 383,449 4.3%

Tuit ion + FIES + PEP 398,283 305,425 30.4% 382,658 4.1%

Agreements to Receive 1,758 2,896 -39.3% 791 122.3%

Installments 749,123 371,848 101.5% 621,476 20.5%

PEP 591,456 298,814 97.9% 500,695 18.1%

PMT 157,667 73,034 115.9% 120,781 30.5%

FIES 797,150 988,912 -19.4% 532,209 49.8%

PN23 376,726 556,089 -32.3% 370,664 1.6%

Short Term 376,726 196,910 91.3% 370,664 1.6%

Long Term - 359,178 n.a. 0 n.a.

Other FIES - Short Term 420,423 432,823 -2.9% 161,545 160.3%

On-Campus - Average Accounts Receivable Term (days) 1Q18 1Q17 Chg.% 4Q17 Chg.%

Net Accounts Receivable

Total Net Revenue On-Campus163 146 17 Days 128 35 Days

16

EARNINGS RELEASE 1Q18

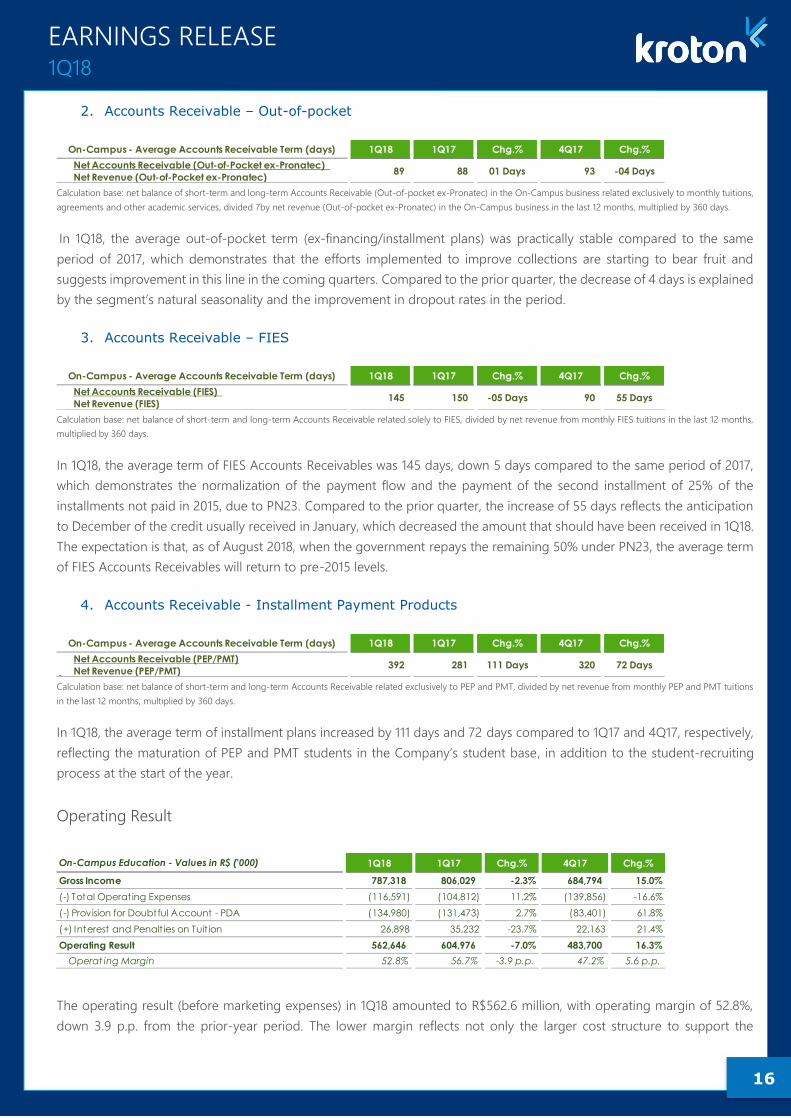

2. Accounts Receivable – Out-of-pocket

Calculation base: net balance of short-term and long-term Accounts Receivable (Out-of-pocket ex-Pronatec) in the On-Campus business related exclusively to monthly tuitions,

agreements and other academic services, divided 7by net revenue (Out-of-pocket ex-Pronatec) in the On-Campus business in the last 12 months, multiplied by 360 days.

In 1Q18, the average out-of-pocket term (ex-financing/installment plans) was practically stable compared to the same

period of 2017, which demonstrates that the efforts implemented to improve collections are starting to bear fruit and

suggests improvement in this line in the coming quarters. Compared to the prior quarter, the decrease of 4 days is explained

by the segment’s natural seasonality and the improvement in dropout rates in the period.

3. Accounts Receivable – FIES

Calculation base: net balance of short-term and long-term Accounts Receivable related solely to FIES, divided by net revenue from monthly FIES tuitions in the last 12 months,

multiplied by 360 days.

In 1Q18, the average term of FIES Accounts Receivables was 145 days, down 5 days compared to the same period of 2017,

which demonstrates the normalization of the payment flow and the payment of the second installment of 25% of the

installments not paid in 2015, due to PN23. Compared to the prior quarter, the increase of 55 days reflects the anticipation

to December of the credit usually received in January, which decreased the amount that should have been received in 1Q18.

The expectation is that, as of August 2018, when the government repays the remaining 50% under PN23, the average term

of FIES Accounts Receivables will return to pre-2015 levels.

4. Accounts Receivable - Installment Payment Products

Calculation base: net balance of short-term and long-term Accounts Receivable related exclusively to PEP and PMT, divided by net revenue from monthly PEP and PMT tuitions

in the last 12 months, multiplied by 360 days.

In 1Q18, the average term of installment plans increased by 111 days and 72 days compared to 1Q17 and 4Q17, respectively,

reflecting the maturation of PEP and PMT students in the Company’s student base, in addition to the student-recruiting

process at the start of the year.

Operating Result

The operating result (before marketing expenses) in 1Q18 amounted to R$562.6 million, with operating margin of 52.8%,

down 3.9 p.p. from the prior-year period. The lower margin reflects not only the larger cost structure to support the

On-Campus - Average Accounts Receivable Term (days) 1Q18 1Q17 Chg.% 4Q17 Chg.%

Net Accounts Receivable (Out-of-Pocket ex-Pronatec)

Net Revenue (Out-of-Pocket ex-Pronatec)89 88 01 Days 93 -04 Days

On-Campus - Average Accounts Receivable Term (days) 1Q18 1Q17 Chg.% 4Q17 Chg.%

Net Accounts Receivable (FIES)

Net Revenue (FIES)145 150 -05 Days 90 55 Days

On-Campus - Average Accounts Receivable Term (days) 1Q18 1Q17 Chg.% 4Q17 Chg.%

Net Accounts Receivable (PEP/PMT)

Net Revenue (PEP/PMT)392 281 111 Days 320 72 Days

On-Campus Education - Values in R$ ('000) 1Q18 1Q17 Chg.% 4Q17 Chg.%

Gross Income 787,318 806,029 -2.3% 684,794 15.0%

(-) Total Operating Expenses (116,591) (104,812) 11.2% (139,856) -16.6%

(-) Provision for Doubtful Account - PDA (134,980) (131,473) 2.7% (83,401) 61.8%

(+) Interest and Penalt ies on Tuit ion 26,898 35,232 -23.7% 22,163 21.4%

Operating Result 562,646 604,976 -7.0% 483,700 16.3%

Operat ing Margin 52.8% 56.7% -3.9 p.p. 47.2% 5.6 p.p.

17

EARNINGS RELEASE 1Q18

Company’s growth projects, but also all the associated pressures, which mainly refer to the shift in the profile of the On-

Campus student base and to the higher provisioning to support the Company’s installment plans in a conservative manner.

However, note that the maintenance of operating margins above 50%, despite the short-term challenges and accelerated

growth rate, demonstrates the consistency of the Company’s various levers to continuously deliver a high level of efficiency.

Compared to the prior quarter, operating margin expanded 5.6 p.p., reflecting the seasonality of the operation and the

strong results achieved in the new enrollment and re-enrollment processes at the start of the year.

OPERATING RESULT EX- FAIR, FAC/FAMAT and NOVATEC

Excluding the recent divestments of FAIR, FAC/FAMAT and NOVATEC from the results for 1Q17 leads to a slight difference

in indicators for the On-campus segment, with revenue growing 0.6%, reversing the decline registered in the corporate

result. Meanwhile, gross income in 1Q18 decreased by 1.5%, with margin contraction of 1.6 p.p. from the same period last

year. Operating margin, however, declined by 3.8 p.p. due to the higher provisioning and the larger cost structure to support

the growth projects.

On-Campus - Values in R$ ('000) 1Q18 1Q17 Chg.%

Net Revenue 1,064,987 1,058,764 0.6%

Gross Income 787,318 799,565 -1.5%

Gross Margin 73.9% 75.5% -1.6 p.p.

Operating Result 562,646 599,743 -6.2%

Operat ing Margin 52.8% 56.6% -3.8 p.p.

18

EARNINGS RELEASE 1Q18

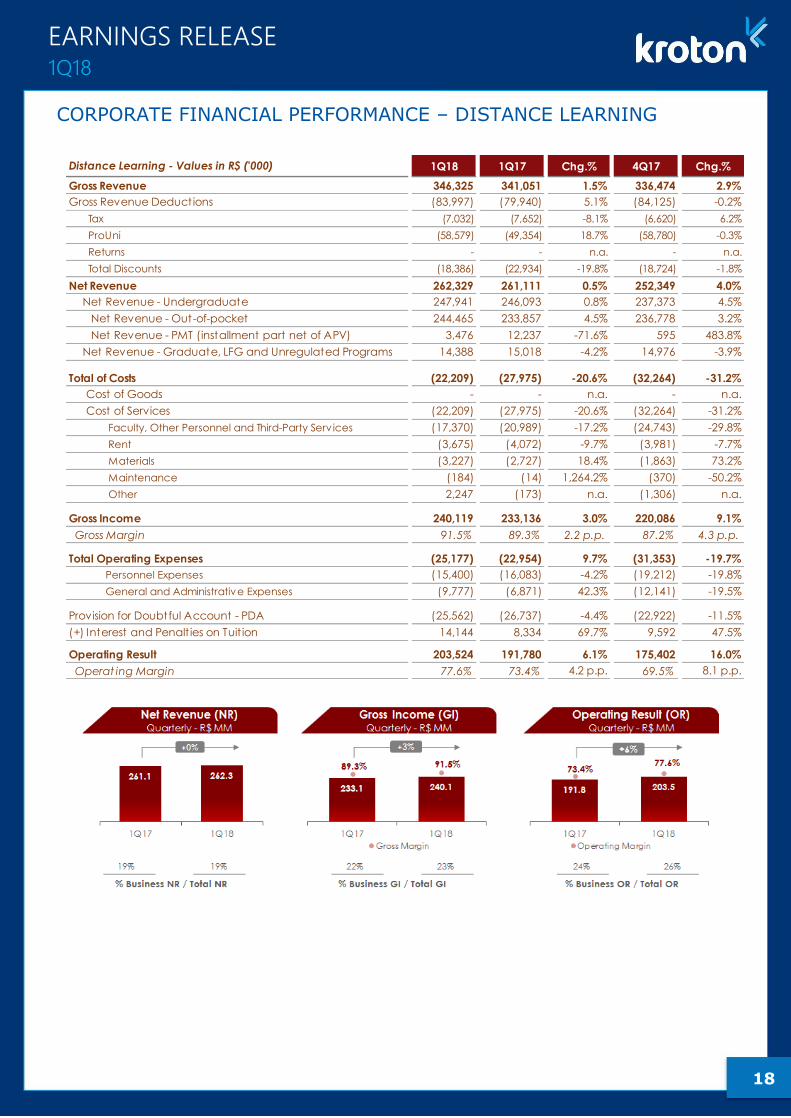

CORPORATE FINANCIAL PERFORMANCE – DISTANCE LEARNING

Distance Learning - Values in R$ ('000) 1Q18 1Q17 Chg.% 4Q17 Chg.%

Gross Revenue 346,325 341,051 1.5% 336,474 2.9%

Gross Revenue Deductions (83,997) (79,940) 5.1% (84,125) -0.2%

Tax (7,032) (7,652) -8.1% (6,620) 6.2%

ProUni (58,579) (49,354) 18.7% (58,780) -0.3%

Returns - - n.a. - n.a.

Total Discounts (18,386) (22,934) -19.8% (18,724) -1.8%

Net Revenue 262,329 261,111 0.5% 252,349 4.0%

Net Revenue - Undergraduate 247,941 246,093 0.8% 237,373 4.5%

Net Revenue - Out-of-pocket 244,465 233,857 4.5% 236,778 3.2%

Net Revenue - PMT (installment part net of APV) 3,476 12,237 -71.6% 595 483.8%

Net Revenue - Graduate, LFG and Unregulated Programs 14,388 15,018 -4.2% 14,976 -3.9%

Total of Costs (22,209) (27,975) -20.6% (32,264) -31.2%

Cost of Goods - - n.a. - n.a.

Cost of Services (22,209) (27,975) -20.6% (32,264) -31.2%

Faculty, Other Personnel and Third-Party Serv ices (17,370) (20,989) -17.2% (24,743) -29.8%

Rent (3,675) (4,072) -9.7% (3,981) -7.7%

Materials (3,227) (2,727) 18.4% (1,863) 73.2%

Maintenance (184) (14) 1,264.2% (370) -50.2%

Other 2,247 (173) n.a. (1,306) n.a.

Gross Income 240,119 233,136 3.0% 220,086 9.1%

Gross Margin 91.5% 89.3% 2.2 p.p. 87.2% 4.3 p.p.

Total Operating Expenses (25,177) (22,954) 9.7% (31,353) -19.7%

Personnel Expenses (15,400) (16,083) -4.2% (19,212) -19.8%

General and Administrative Expenses (9,777) (6,871) 42.3% (12,141) -19.5%

Provision for Doubtful Account - PDA (25,562) (26,737) -4.4% (22,922) -11.5%

(+) Interest and Penalt ies on Tuit ion 14,144 8,334 69.7% 9,592 47.5%

Operating Result 203,524 191,780 6.1% 175,402 16.0%

Operat ing Margin 77.6% 73.4% 4.2 p.p. 69.5% 8.1 p.p.

19

EARNINGS RELEASE 1Q18

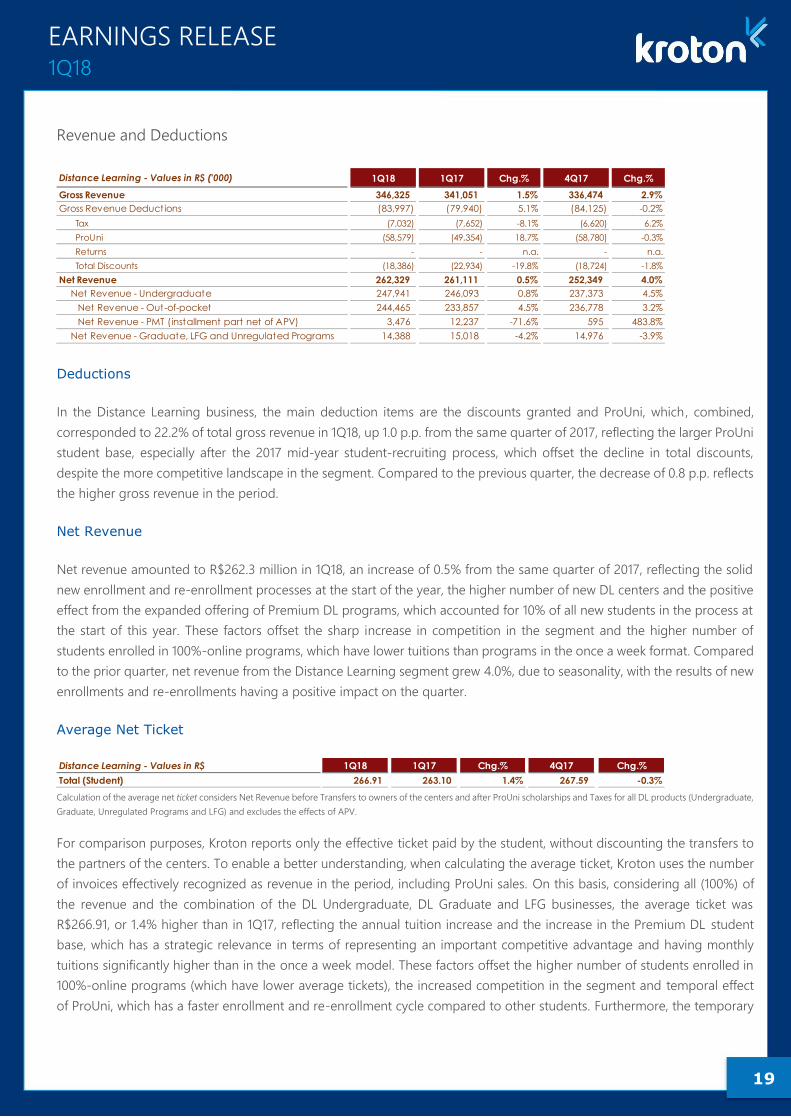

Revenue and Deductions

Deductions

In the Distance Learning business, the main deduction items are the discounts granted and ProUni, which, combined,

corresponded to 22.2% of total gross revenue in 1Q18, up 1.0 p.p. from the same quarter of 2017, reflecting the larger ProUni

student base, especially after the 2017 mid-year student-recruiting process, which offset the decline in total discounts,

despite the more competitive landscape in the segment. Compared to the previous quarter, the decrease of 0.8 p.p. reflects

the higher gross revenue in the period.

Net Revenue

Net revenue amounted to R$262.3 million in 1Q18, an increase of 0.5% from the same quarter of 2017, reflecting the solid

new enrollment and re-enrollment processes at the start of the year, the higher number of new DL centers and the positive

effect from the expanded offering of Premium DL programs, which accounted for 10% of all new students in the process at

the start of this year. These factors offset the sharp increase in competition in the segment and the higher number of

students enrolled in 100%-online programs, which have lower tuitions than programs in the once a week format. Compared

to the prior quarter, net revenue from the Distance Learning segment grew 4.0%, due to seasonality, with the results of new

enrollments and re-enrollments having a positive impact on the quarter.

Average Net Ticket

Calculation of the average net ticket considers Net Revenue before Transfers to owners of the centers and after ProUni scholarships and Taxes for all DL products (Undergraduate,

Graduate, Unregulated Programs and LFG) and excludes the effects of APV.

For comparison purposes, Kroton reports only the effective ticket paid by the student, without discounting the transfers to

the partners of the centers. To enable a better understanding, when calculating the average ticket, Kroton uses the number

of invoices effectively recognized as revenue in the period, including ProUni sales. On this basis, considering all (100%) of

the revenue and the combination of the DL Undergraduate, DL Graduate and LFG businesses, the average ticket was

R$266.91, or 1.4% higher than in 1Q17, reflecting the annual tuition increase and the increase in the Premium DL student

base, which has a strategic relevance in terms of representing an important competitive advantage and having monthly

tuitions significantly higher than in the once a week model. These factors offset the higher number of students enrolled in

100%-online programs (which have lower average tickets), the increased competition in the segment and temporal effect

of ProUni, which has a faster enrollment and re-enrollment cycle compared to other students. Furthermore, the temporary

Distance Learning - Values in R$ ('000) 1Q18 1Q17 Chg.% 4Q17 Chg.%

Gross Revenue 346,325 341,051 1.5% 336,474 2.9%

Gross Revenue Deductions (83,997) (79,940) 5.1% (84,125) -0.2%

Tax (7,032) (7,652) -8.1% (6,620) 6.2%

ProUni (58,579) (49,354) 18.7% (58,780) -0.3%

Returns - - n.a. - n.a.

Total Discounts (18,386) (22,934) -19.8% (18,724) -1.8%

Net Revenue 262,329 261,111 0.5% 252,349 4.0%

Net Revenue - Undergraduate 247,941 246,093 0.8% 237,373 4.5%

Net Revenue - Out-of-pocket 244,465 233,857 4.5% 236,778 3.2%

Net Revenue - PMT (installment part net of APV) 3,476 12,237 -71.6% 595 483.8%

Net Revenue - Graduate, LFG and Unregulated Programs 14,388 15,018 -4.2% 14,976 -3.9%

Distance Learning - Values in R$ 1Q18 1Q17 Chg.% 4Q17 Chg.%

Total (Student) 266.91 263.10 1.4% 267.59 -0.3%

20

EARNINGS RELEASE 1Q18

increase in discounts had a negative effect on average ticket for the period. The expectation is for recovery in the average

monthly tuition in the second quarter, bringing the result of the semester closer to the variation in inflation.

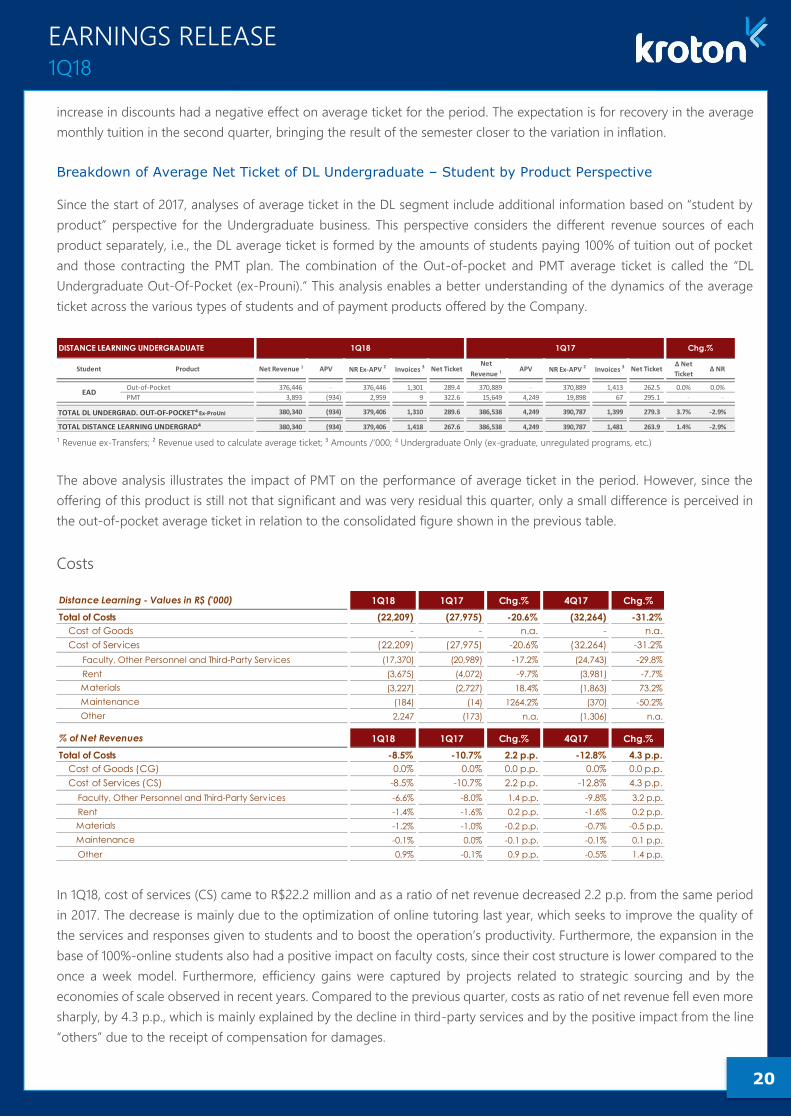

Breakdown of Average Net Ticket of DL Undergraduate – Student by Product Perspective

Since the start of 2017, analyses of average ticket in the DL segment include additional information based on “student by

product” perspective for the Undergraduate business. This perspective considers the different revenue sources of each

product separately, i.e., the DL average ticket is formed by the amounts of students paying 100% of tuition out of pocket

and those contracting the PMT plan. The combination of the Out-of-pocket and PMT average ticket is called the “DL

Undergraduate Out-Of-Pocket (ex-Prouni).” This analysis enables a better understanding of the dynamics of the average

ticket across the various types of students and of payment products offered by the Company.

¹ Revenue ex-Transfers; ² Revenue used to calculate average ticket; ³ Amounts /‘000; 4 Undergraduate Only (ex-graduate, unregulated programs, etc.)

The above analysis illustrates the impact of PMT on the performance of average ticket in the period. However, since the

offering of this product is still not that significant and was very residual this quarter, only a small difference is perceived in

the out-of-pocket average ticket in relation to the consolidated figure shown in the previous table.

Costs

In 1Q18, cost of services (CS) came to R$22.2 million and as a ratio of net revenue decreased 2.2 p.p. from the same period

in 2017. The decrease is mainly due to the optimization of online tutoring last year, which seeks to improve the quality of

the services and responses given to students and to boost the operation’s productivity. Furthermore, the expansion in the

base of 100%-online students also had a positive impact on faculty costs, since their cost structure is lower compared to the

once a week model. Furthermore, efficiency gains were captured by projects related to strategic sourcing and by the

economies of scale observed in recent years. Compared to the previous quarter, costs as ratio of net revenue fell even more

sharply, by 4.3 p.p., which is mainly explained by the decline in third-party services and by the positive impact from the line

“others” due to the receipt of compensation for damages.

Student Product Net Revenue 1 APV NR Ex-APV 2 Invoices 3 Net TicketNet

Revenue 1APV NR Ex-APV 2 Invoices 3 Net Ticket

Δ Net

TicketΔ NR

Out-of-Pocket 376,446 - 376,446 1,301 289.4 370,889 - 370,889 1,413 262.5 0.0% 0.0%

PMT 3,893 (934) 2,959 9 322.6 15,649 4,249 19,898 67 295.1 - -

380,340 (934) 379,406 1,310 289.6 386,538 4,249 390,787 1,399 279.3 3.7% -2.9%

380,340 (934) 379,406 1,418 267.6 386,538 4,249 390,787 1,481 263.9 1.4% -2.9%

Chg.%DISTANCE LEARNING UNDERGRADUATE 1Q18 1Q17

EAD

TOTAL DL UNDERGRAD. OUT-OF-POCKET⁴ Ex-ProUni

TOTAL DISTANCE LEARNING UNDERGRAD⁴

Distance Learning - Values in R$ ('000) 1Q18 1Q17 Chg.% 4Q17 Chg.%

Total of Costs (22,209) (27,975) -20.6% (32,264) -31.2%

Cost of Goods - - n.a. - n.a.

Cost of Services (22,209) (27,975) -20.6% (32,264) -31.2%

Faculty, Other Personnel and Third-Party Serv ices (17,370) (20,989) -17.2% (24,743) -29.8%

Rent (3,675) (4,072) -9.7% (3,981) -7.7%

Materials (3,227) (2,727) 18.4% (1,863) 73.2%

Maintenance (184) (14) 1264.2% (370) -50.2%

Other 2,247 (173) n.a. (1,306) n.a.

% of Net Revenues 1Q18 1Q17 Chg.% 4Q17 Chg.%

Total of Costs -8.5% -10.7% 2.2 p.p. -12.8% 4.3 p.p.

Cost of Goods (CG) 0.0% 0.0% 0.0 p.p. 0.0% 0.0 p.p.

Cost of Services (CS) -8.5% -10.7% 2.2 p.p. -12.8% 4.3 p.p.

Faculty, Other Personnel and Third-Party Serv ices -6.6% -8.0% 1.4 p.p. -9.8% 3.2 p.p.

Rent -1.4% -1.6% 0.2 p.p. -1.6% 0.2 p.p.

Materials -1.2% -1.0% -0.2 p.p. -0.7% -0.5 p.p.

Maintenance -0.1% 0.0% -0.1 p.p. -0.1% 0.1 p.p.

Other 0.9% -0.1% 0.9 p.p. -0.5% 1.4 p.p.

21

EARNINGS RELEASE 1Q18

Gross Income

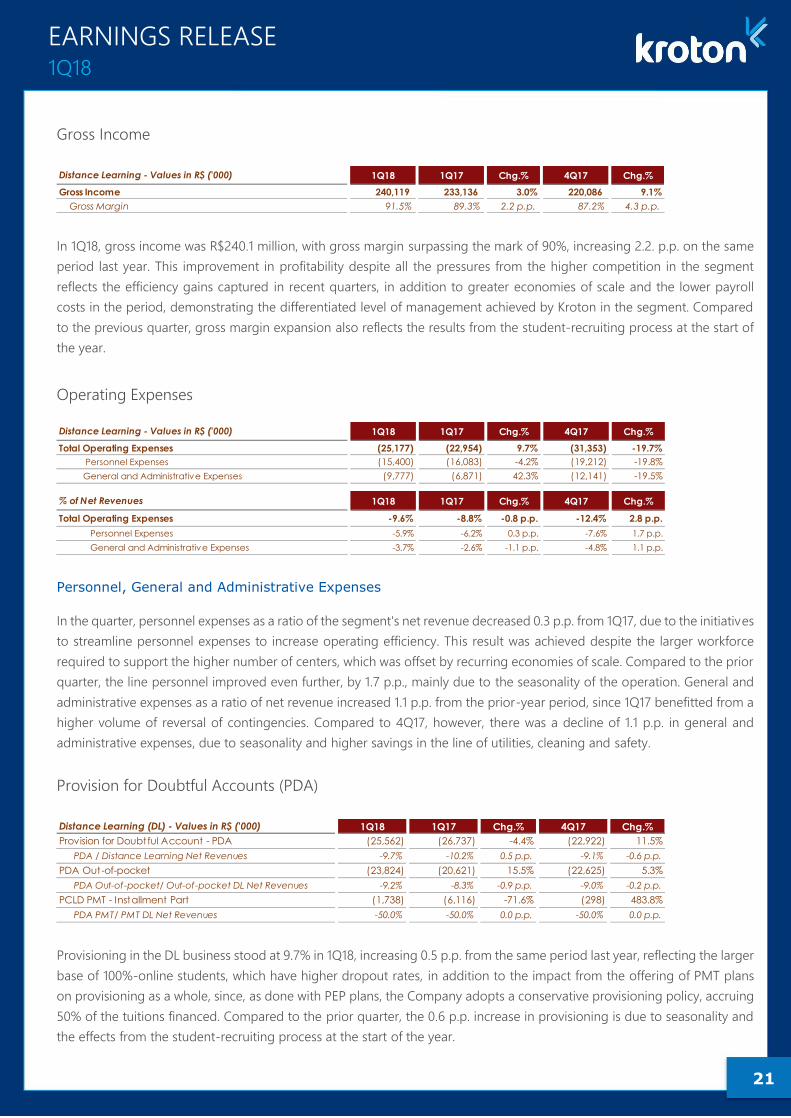

In 1Q18, gross income was R$240.1 million, with gross margin surpassing the mark of 90%, increasing 2.2. p.p. on the same

period last year. This improvement in profitability despite all the pressures from the higher competition in the segment

reflects the efficiency gains captured in recent quarters, in addition to greater economies of scale and the lower payroll

costs in the period, demonstrating the differentiated level of management achieved by Kroton in the segment. Compared

to the previous quarter, gross margin expansion also reflects the results from the student-recruiting process at the start of

the year.

Operating Expenses

Personnel, General and Administrative Expenses

In the quarter, personnel expenses as a ratio of the segment's net revenue decreased 0.3 p.p. from 1Q17, due to the initiatives

to streamline personnel expenses to increase operating efficiency. This result was achieved despite the larger workforce

required to support the higher number of centers, which was offset by recurring economies of scale. Compared to the prior

quarter, the line personnel improved even further, by 1.7 p.p., mainly due to the seasonality of the operation. General and

administrative expenses as a ratio of net revenue increased 1.1 p.p. from the prior-year period, since 1Q17 benefitted from a

higher volume of reversal of contingencies. Compared to 4Q17, however, there was a decline of 1.1 p.p. in general and

administrative expenses, due to seasonality and higher savings in the line of utilities, cleaning and safety.

Provision for Doubtful Accounts (PDA)

Provisioning in the DL business stood at 9.7% in 1Q18, increasing 0.5 p.p. from the same period last year, reflecting the larger

base of 100%-online students, which have higher dropout rates, in addition to the impact from the offering of PMT plans

on provisioning as a whole, since, as done with PEP plans, the Company adopts a conservative provisioning policy, accruing

50% of the tuitions financed. Compared to the prior quarter, the 0.6 p.p. increase in provisioning is due to seasonality and

the effects from the student-recruiting process at the start of the year.

Distance Learning - Values in R$ ('000) 1Q18 1Q17 Chg.% 4Q17 Chg.%

Gross Income 240,119 233,136 3.0% 220,086 9.1%

Gross Margin 91.5% 89.3% 2.2 p.p. 87.2% 4.3 p.p.

Distance Learning - Values in R$ ('000) 1Q18 1Q17 Chg.% 4Q17 Chg.%

Total Operating Expenses (25,177) (22,954) 9.7% (31,353) -19.7%

Personnel Expenses (15,400) (16,083) -4.2% (19,212) -19.8%

General and Administrative Expenses (9,777) (6,871) 42.3% (12,141) -19.5%

% of Net Revenues 1Q18 1Q17 Chg.% 4Q17 Chg.%

Total Operating Expenses -9.6% -8.8% -0.8 p.p. -12.4% 2.8 p.p.

Personnel Expenses -5.9% -6.2% 0.3 p.p. -7.6% 1.7 p.p.

General and Administrative Expenses -3.7% -2.6% -1.1 p.p. -4.8% 1.1 p.p.

Distance Learning (DL) - Values in R$ ('000) 1Q18 1Q17 Chg.% 4Q17 Chg.%

Provision for Doubtful Account - PDA (25,562) (26,737) -4.4% (22,922) 11.5%

PDA / Distance Learning Net Revenues -9.7% -10.2% 0.5 p.p. -9.1% -0.6 p.p.

PDA Out-of-pocket (23,824) (20,621) 15.5% (22,625) 5.3%

PDA Out-of-pocket/ Out-of-pocket DL Net Revenues -9.2% -8.3% -0.9 p.p. -9.0% -0.2 p.p.

PCLD PMT - Installment Part (1,738) (6,116) -71.6% (298) 483.8%

PDA PMT/ PMT DL Net Revenues -50.0% -50.0% 0.0 p.p. -50.0% 0.0 p.p.

22

EARNINGS RELEASE 1Q18

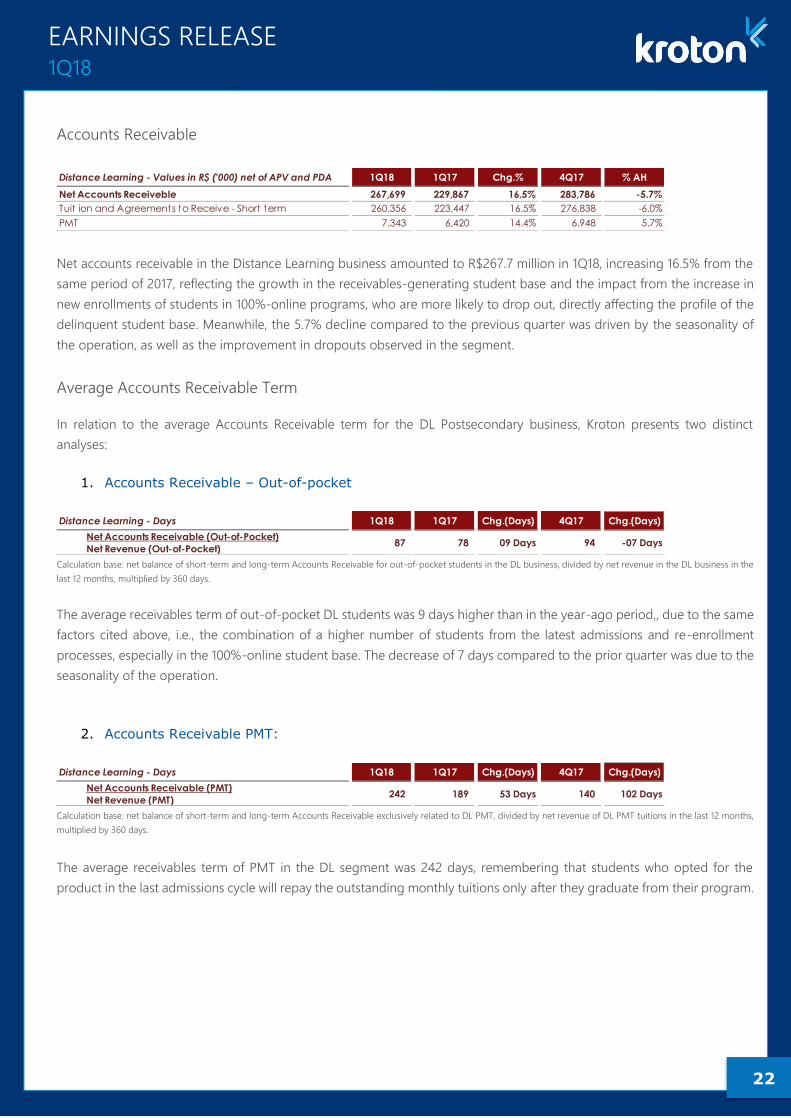

Accounts Receivable

Net accounts receivable in the Distance Learning business amounted to R$267.7 million in 1Q18, increasing 16.5% from the

same period of 2017, reflecting the growth in the receivables-generating student base and the impact from the increase in

new enrollments of students in 100%-online programs, who are more likely to drop out, directly affecting the profile of the

delinquent student base. Meanwhile, the 5.7% decline compared to the previous quarter was driven by the seasonality of

the operation, as well as the improvement in dropouts observed in the segment.

Average Accounts Receivable Term

In relation to the average Accounts Receivable term for the DL Postsecondary business, Kroton presents two distinct

analyses:

1. Accounts Receivable – Out-of-pocket

Calculation base: net balance of short-term and long-term Accounts Receivable for out-of-pocket students in the DL business, divided by net revenue in the DL business in the

last 12 months, multiplied by 360 days.

The average receivables term of out-of-pocket DL students was 9 days higher than in the year-ago period,, due to the same

factors cited above, i.e., the combination of a higher number of students from the latest admissions and re-enrollment

processes, especially in the 100%-online student base. The decrease of 7 days compared to the prior quarter was due to the

seasonality of the operation.

2. Accounts Receivable PMT:

Calculation base: net balance of short-term and long-term Accounts Receivable exclusively related to DL PMT, divided by net revenue of DL PMT tuitions in the last 12 months,

multiplied by 360 days.

The average receivables term of PMT in the DL segment was 242 days, remembering that students who opted for the

product in the last admissions cycle will repay the outstanding monthly tuitions only after they graduate from their program.

Distance Learning - Values in R$ ('000) net of APV and PDA 1Q18 1Q17 Chg.% 4Q17 % AH

Net Accounts Receiveble 267,699 229,867 16.5% 283,786 -5.7%

Tuit ion and Agreements to Receive - Short term 260,356 223,447 16.5% 276,838 -6.0%

PMT 7,343 6,420 14.4% 6,948 5.7%

Distance Learning - Days 1Q18 1Q17 Chg.(Days) 4Q17 Chg.(Days)

Net Accounts Receivable (Out-of-Pocket)

Net Revenue (Out-of-Pocket)87 78 09 Days 94 -07 Days

Distance Learning - Days 1Q18 1Q17 Chg.(Days) 4Q17 Chg.(Days)

Net Accounts Receivable (PMT)

Net Revenue (PMT)242 189 53 Days 140 102 Days

23

EARNINGS RELEASE 1Q18

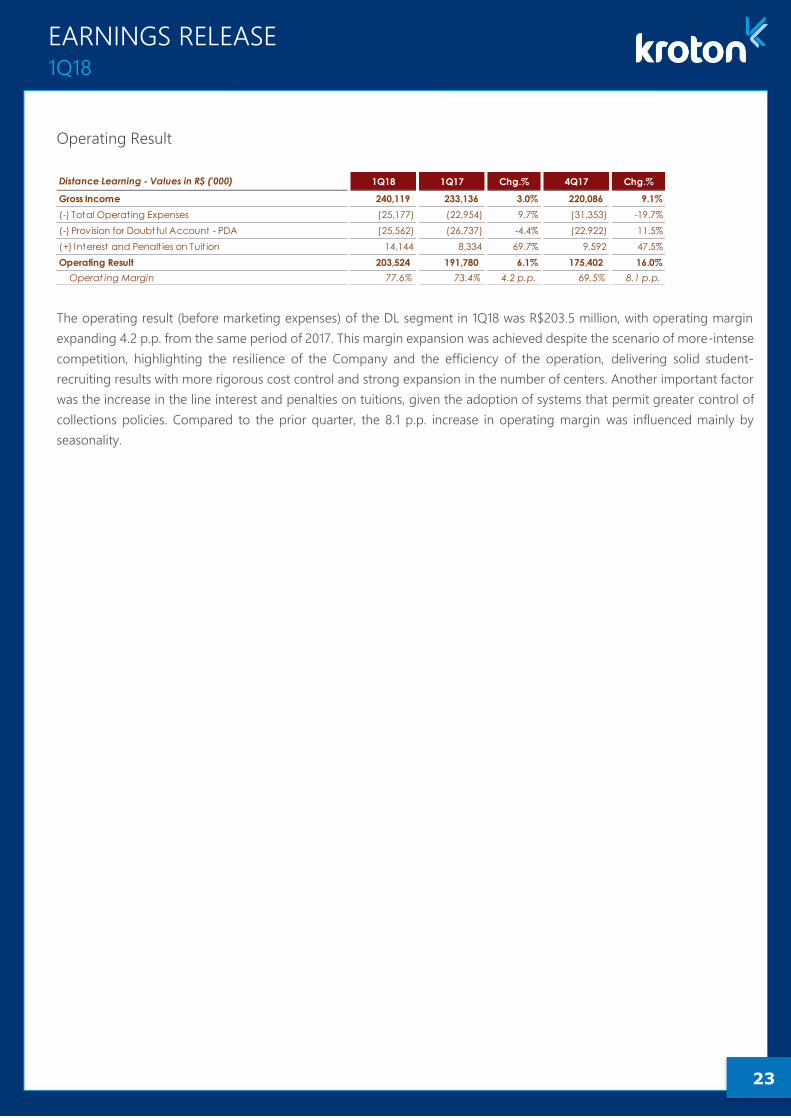

Operating Result

The operating result (before marketing expenses) of the DL segment in 1Q18 was R$203.5 million, with operating margin

expanding 4.2 p.p. from the same period of 2017. This margin expansion was achieved despite the scenario of more-intense

competition, highlighting the resilience of the Company and the efficiency of the operation, delivering solid student-

recruiting results with more rigorous cost control and strong expansion in the number of centers. Another important factor

was the increase in the line interest and penalties on tuitions, given the adoption of systems that permit greater control of

collections policies. Compared to the prior quarter, the 8.1 p.p. increase in operating margin was influenced mainly by

seasonality.

Distance Learning - Values in R$ ('000) 1Q18 1Q17 Chg.% 4Q17 Chg.%

Gross Income 240,119 233,136 3.0% 220,086 9.1%

(-) Total Operating Expenses (25,177) (22,954) 9.7% (31,353) -19.7%

(-) Provision for Doubtful Account - PDA (25,562) (26,737) -4.4% (22,922) 11.5%

(+) Interest and Penalt ies on Tuit ion 14,144 8,334 69.7% 9,592 47.5%

Operating Result 203,524 191,780 6.1% 175,402 16.0%

Operat ing Margin 77.6% 73.4% 4.2 p.p. 69.5% 8.1 p.p.

24

EARNINGS RELEASE 1Q18

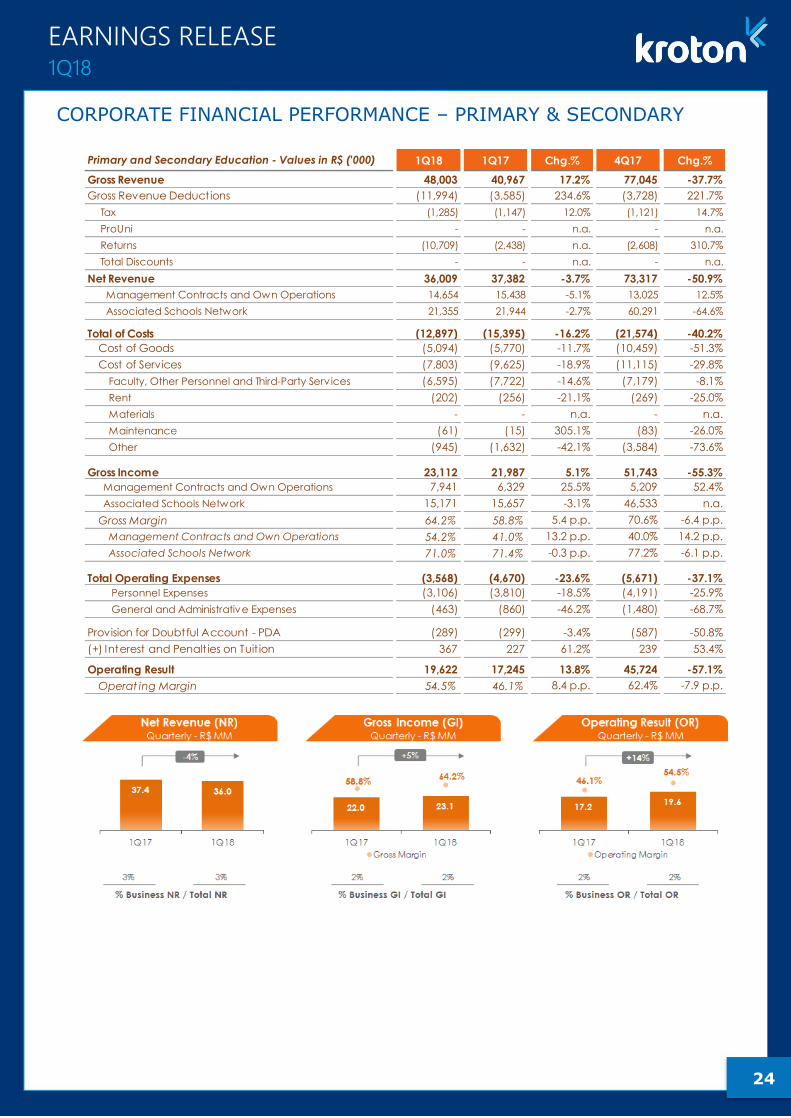

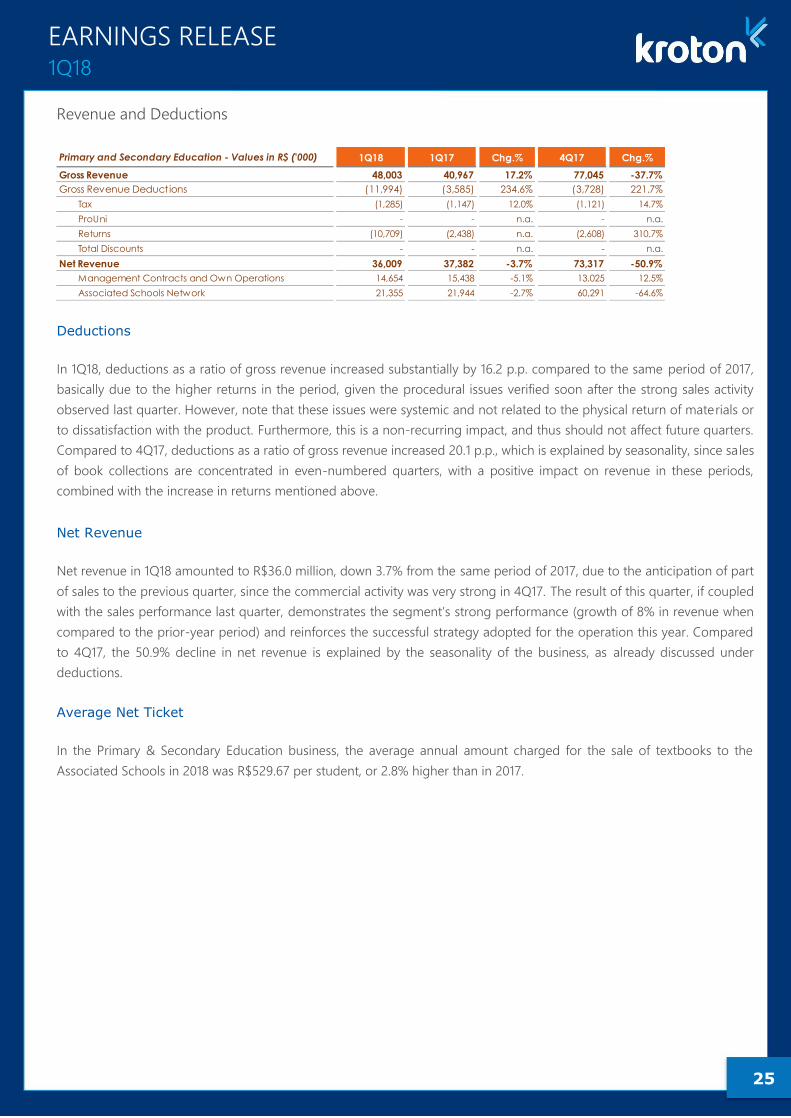

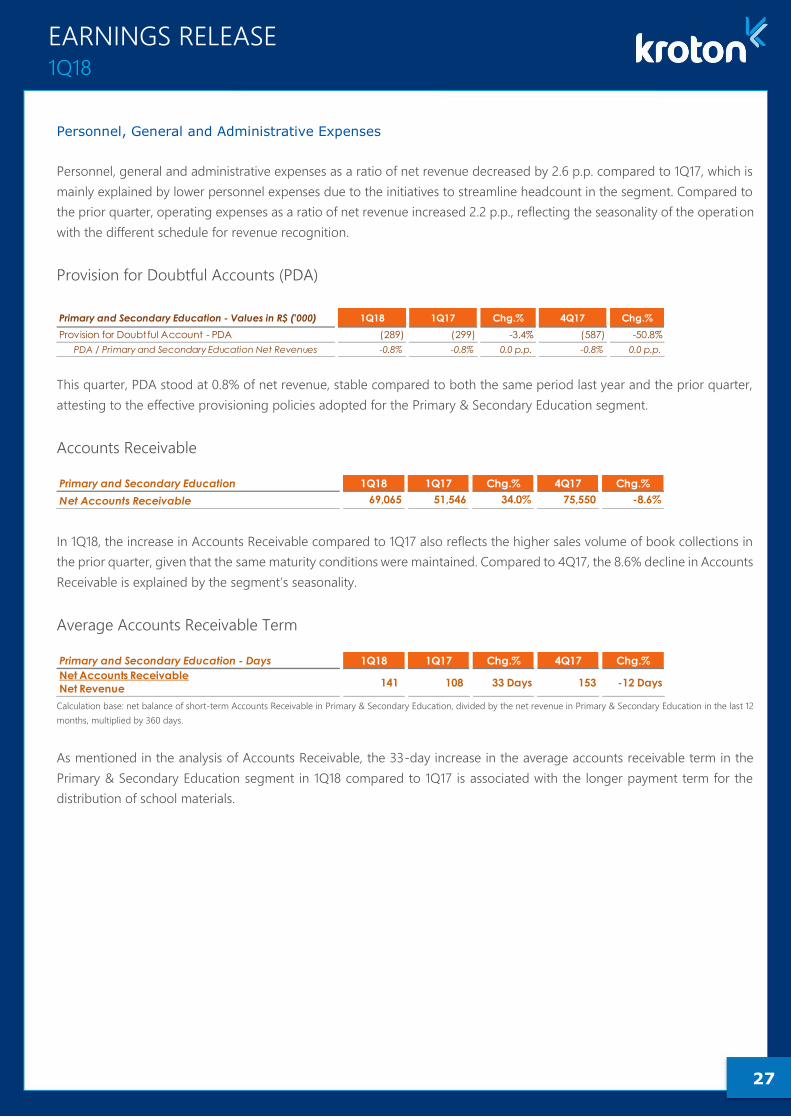

CORPORATE FINANCIAL PERFORMANCE – PRIMARY & SECONDARY

Primary and Secondary Education - Values in R$ ('000) 1Q18 1Q17 Chg.% 4Q17 Chg.%

Gross Revenue 48,003 40,967 17.2% 77,045 -37.7%

Gross Revenue Deductions (11,994) (3,585) 234.6% (3,728) 221.7%

Tax (1,285) (1,147) 12.0% (1,121) 14.7%

ProUni - - n.a. - n.a.

Returns (10,709) (2,438) n.a. (2,608) 310.7%

Total Discounts - - n.a. - n.a.

Net Revenue 36,009 37,382 -3.7% 73,317 -50.9%

Management Contracts and Own Operations 14,654 15,438 -5.1% 13,025 12.5%

Associated Schools Network 21,355 21,944 -2.7% 60,291 -64.6%

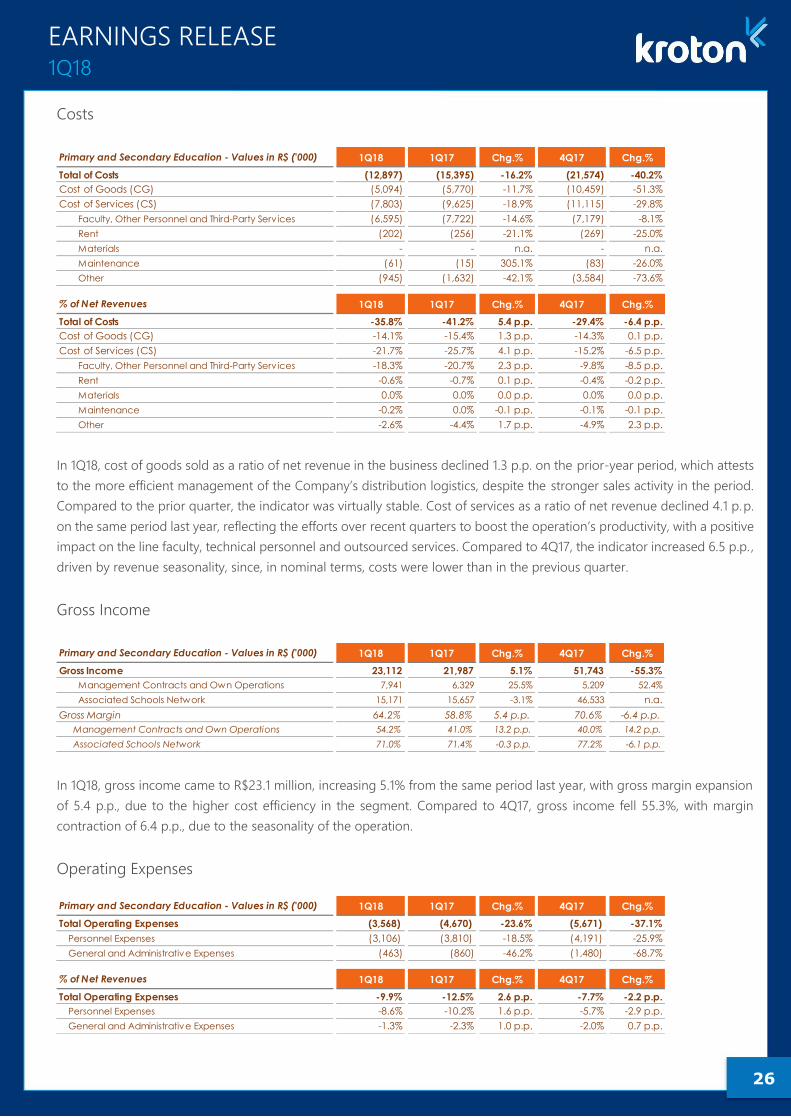

Total of Costs (12,897) (15,395) -16.2% (21,574) -40.2%

Cost of Goods (5,094) (5,770) -11.7% (10,459) -51.3%

Cost of Services (7,803) (9,625) -18.9% (11,115) -29.8%

Faculty, Other Personnel and Third-Party Serv ices (6,595) (7,722) -14.6% (7,179) -8.1%

Rent (202) (256) -21.1% (269) -25.0%

Materials - - n.a. - n.a.

Maintenance (61) (15) 305.1% (83) -26.0%

Other (945) (1,632) -42.1% (3,584) -73.6%

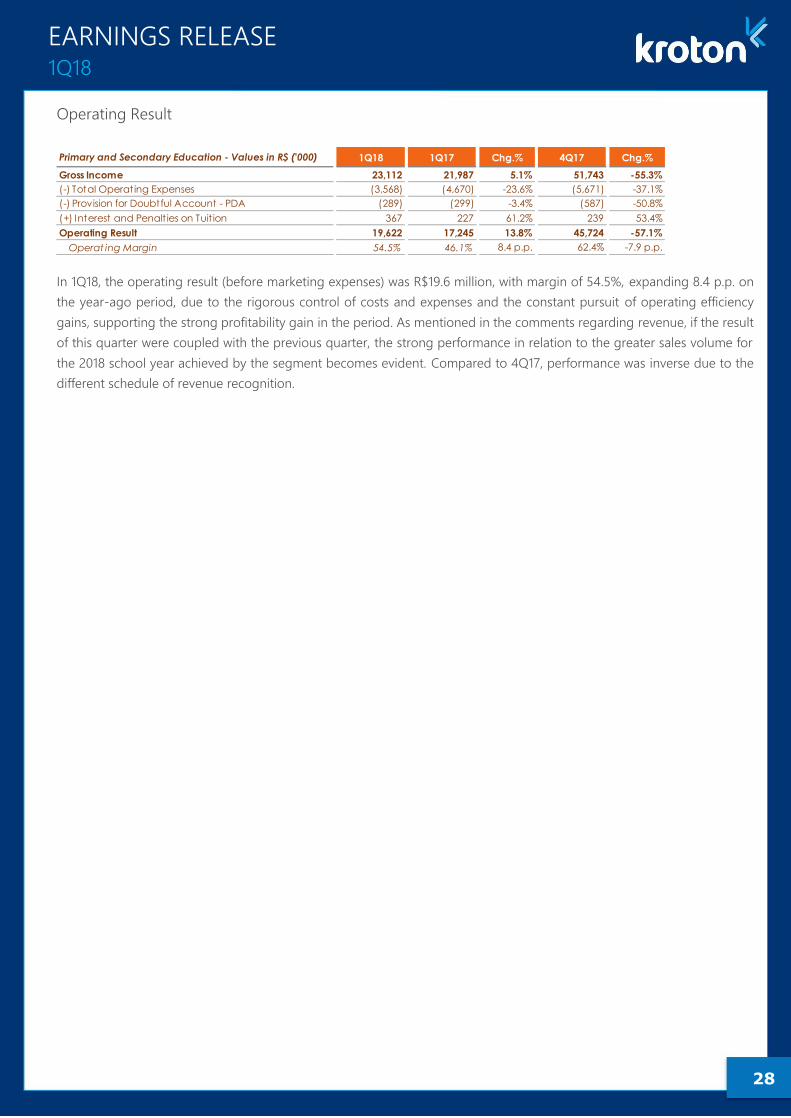

Gross Income 23,112 21,987 5.1% 51,743 -55.3%

Management Contracts and Own Operations 7,941 6,329 25.5% 5,209 52.4%

Associated Schools Network 15,171 15,657 -3.1% 46,533 n.a.

Gross Margin 64.2% 58.8% 5.4 p.p. 70.6% -6.4 p.p.