Due Diligence - Balance Sheet Solutions

18

Due Diligence CenCorp has mailed a letter to members that invest through the SimpliCD program that summarizes the information needed to perform your due diligence. This letter was in response to guidance provided by the NCUA. To view the CenCorp or NCUA letters, please click on the appropriate link below. CenCorp Letter NCUA (Letter No.: 04-CU-04) Below are copies of letters from the NCUA and FDIC addressing deposit insurance coverage of certificates of deposit issued through the SimpliCD program. These letters were received by Primary Financial Company, LLC (Primary) when it was a wholly owned subsidiary of Corporate One Credit Union. Primary is the custodian for SimpliCD and is now owned by corporate credit unions, including CenCorp. The ownership change has not affected the deposit insurance coverage. To view the NCUA or FDIC letters, please click on the appropriate link below. NCUA – Insurance Coverage FDIC – Insurance Coverage To view Primary’s current Annual Report, please click on Annual Report . With the SimpliCD program, performance reviews of issuing institutions are provided by VERIBANC® Inc., a financial institution rating service. To learn more about VERIBANC®’s RATING SYSTEM, please click on VERIBANC® .

Transcript of Due Diligence - Balance Sheet Solutions

Due Diligence

CenCorp has mailed a letter to members that invest through the SimpliCD program that summarizes the information needed to perform your due diligence. This letter was in response to guidance provided by the NCUA. To view the CenCorp or NCUA letters, please click on the appropriate link below. CenCorp Letter NCUA (Letter No.: 04-CU-04) Below are copies of letters from the NCUA and FDIC addressing deposit insurance coverage of certificates of deposit issued through the SimpliCD program. These letters were received by Primary Financial Company, LLC (Primary) when it was a wholly owned subsidiary of Corporate One Credit Union. Primary is the custodian for SimpliCD and is now owned by corporate credit unions, including CenCorp. The ownership change has not affected the deposit insurance coverage. To view the NCUA or FDIC letters, please click on the appropriate link below. NCUA – Insurance Coverage FDIC – Insurance Coverage To view Primary’s current Annual Report, please click on Annual Report. With the SimpliCD program, performance reviews of issuing institutions are provided by VERIBANC® Inc., a financial institution rating service. To learn more about VERIBANC®’s RATING SYSTEM, please click on VERIBANC®.

June 2, 2004

Dear Member:

In April 2004, the NCUA sent a letter to credit unions that discussed due diligence related to the safekeeping of investments, particularly certificates of deposit (CDs). The NCUA letter (to view go to www.cencorpcu.com/simplicd.asp and click on Due Diligence Information) reviewed sound business practices that credit unions should use to insure CDs held in safekeeping are protected. CenCorp is sending this letter to assist you in performing your due diligence on the SimpliCD program that you participate in. It should be read in conjunction with the NCUA letter.

As background, Primary Financial Company LLC (Primary) is the safekeeper (or custodian) for the SimpliCD program. Along with other corporate credit unions, CenCorp owns Primary. Primary has brokered and serviced CDs and performed safekeeping services for credit unions nationally for more than seven years. Primary has been designated an Office of Supervisory Jurisdiction (OSJ) 1 of CU Investment Solutions, Inc. (ISI), a subsidiary of U.S. Central Credit Union. ISI is a registered broker/dealer that is supervised by the Securities and Exchange Commission (SEC) and a member of the National Association of Securities Dealers (NASD).

Primary requires the issuing financial institutions to title CDs to reflect Primary as the custodian, acting on behalf of the credit union owners. Each credit union is the beneficial owner of the underlying SimpliCD certificates purchased. Using this method, deposit insurance coverage from the FDIC and the NCUSIF is extended to the beneficial owners. Letters from the FDIC and the NCUA verifying the availability of deposit insurance for investors in the SimpliCD program are available at www.cencorpcu.com/simplicd.asp. In the event of the failure of the financial institution or Primary, the ownership interest of the credit union owners are identified and protected. Bentley Financial Services did not record certificates in this manner.

Other important information for you to consider in your due diligence is as follows:

• As a corporate-credit-union-owned CUSO, Primary regularly provides the NCUA access to its books and records.

1 An OSJ is a branch office of a NASD member that performs functions such as investment order execution and security safekeeping. Primary’s office is located at 3260 Middle Road, Columbus, IN 47203.

POST OFFICE BOX 5092 · SOUTHFIELD, MICHIGAN 48086-5092 · (888) 236-2677 · FAX (248) 351-2122 www.cencorpcu.com

• KPMG LLP performs an annual audit of the financial statements of Primary. KPMG’s report can be found in Primary’s most recent annual report. This report is available to you at www.cencorpcu.com/simplicd.asp.

• Condit and Associates, CPAs (Condit), annually examines compliance with the controls that Primary has in place over the safekeeping function of the SimpliCD program. Such tests are performed in accordance with Statement on Auditing Standards (SAS) No. 70, and include testing of Primary’s safekeeping records for completeness and accuracy. Condit issues a report on the results of its examination. A copy of the report is available upon request.

• A SimpliCD Coordinating-Custodial Agreement between Primary, CenCorp and your credit union was executed when you started on the SimpliCD program. This is an institutional agreement. It explains the various rights and duties of Primary as custodian. One of the requirements in this agreement is for Primary to exercise ordinary care in the safekeeping and administration of investments on your behalf and does not allow securities lending transactions.

• Primary provides a monthly statement detailing your credit union’s holdings, as well as statements detailing daily placements and maturities. These reports should be reconciled to your account records.

• The NASD Website provides information on a registered broker/dealer such as current registrations, pending civil actions, judicial orders, bankruptcies and judgments. To access information on ISI, visit www.NASDR.com, click on NASD BrokerCheck and follow the instructions. To research ISI you will need their Central Registration Depository (CRD) number, which is 43753. To review ISI’s latest annual report, go to www.epfc.com/pfcfinancials.html.

If you have any questions on the items above, please contact Linda Gassen at (888) 236-2677, extension 3022. We welcome your comments and look forward to continuing to provide you with investment options to successfully manage your credit union. Feel free to contact me at (888) 2362677, extension 3008.

Sincerely,

Ronald W. Boehnlein, CPA Chief Financial Officer

NCUA LETTER TO CREDIT UNIONS

NATIONAL CREDIT UNION ADMINISTRATION 1775 Duke Street, Alexandria, VA 22314

DATE: April 2004 LETTER NO.: 04-CU-04

TO: Federally Insured Credit Unions

SUBJ: Investment Safekeeping Due Diligence

Dear Board of Directors:

The purpose of this letter is to reiterate the need for credit unions to implement adequate due diligence methods and procedures for safekeeping investments, particularly certificates of deposit (CDs). Federally insured credit unions are encouraged to carefully review their safekeeping practices to ensure that they provide adequate protection against fraudulent investment schemes and potential losses.

Risk of Loss. Investment safekeeping problems can and have resulted in losses. Such a scenario was recently presented to those credit unions holding investments with Bentley Financial Services Inc. (Bentley) and Entrust Group (Entrust). The Securities and Exchange Commission (SEC) charged Bentley with securities fraud for selling securities misrepresented as insured CDs. Bentley created Entrust to safekeep CDs for investors. Entrust, however was not registered with the SEC and was not affiliated with a financial institution as is required for federal credit unions under Part 703 of NCUA Rules and Regulations. As a result, credit unions with Bentley-related investments incurred losses that may have been avoided had proper due diligence reviews been performed.

Safekeepers play an important role in securing the custody of the credit union’s investments. The accuracy and reliability of the safekeeper’s records are critical and serve to:

• Protect ownership interest in the event the safekeeper enters bankruptcy or liquidation; and

• Ensure the credit union can collect on deposit insurance in the event the CD issuer fails.

Due Diligence. A credit union should perform adequate and appropriate due diligence of its prospective safekeepers. This review should be periodically updated to protect the credit union against potential fraud or misconduct by the safekeeper

and any broker-dealer who may be acting in concert with the safekeeper. While minimum due diligence requirements are set forth in §703.9 of NCUA Rules and Regulations for federally-chartered credit unions, in our view, state-chartered credit unions could also benefit by following these or similar requirements. An appropriate and adequate due diligence review includes, among other things, the following:

• A determination that approved safekeepers are regulated by the SEC, or a federal or state depository institution regulatory agency such as the Federal Deposit Insurance Corporation, or a state trust company regulatory agency.

• An assessment of the reputation of the safekeepers. The credit union should track and review publicity regarding the safekeeper, both positive and negative.

• Documentation of the capital strength of the safekeeper. Generally, the safekeeper used by the credit union should have substantially more capital than the amount of investments it holds for that credit union. A safekeeper regulated by a depository institution or state trust regulatory agency must file financial reports that are publicly available. The SEC requires every registered broker-dealer to send to its customers its certified balance sheet on an annual basis. Credit unions can access public financial information for banks at www.fdic.gov, and for credit unions at www.ncua.gov. Information regarding broker-dealers can be accessed at www.sec.gov and www.nasdr.com.

• The execution of a written custodial agreement with the safekeeper before any transactions take place. A credit union should make certain that it enters into an “institutional” agreement and not a “retail” agreement. Retail agreements may allow the custodian to use the retail customer’s securities for activities such as securities lending transactions without notification of the retail customer and are not appropriate for credit unions . A simple way to differentiate a retail agreement from an institutional one is that a retail agreement generally will not include a signature block for signing on the behalf of a company or organization. A credit union should also ensure the agreement specifies the safekeeper will exercise at least “ordinary care.”

• A review of monthly safekeeping statements which are reconciled to the credit union’s records.

Credit unions that perform adequate and timely due diligence reviews for all safekeepers will greatly reduce the risk of loss from fraudulent investment schemes.

Should you have any questions, please do not hesitate to contact your district examiner, regional office, or state supervisory authority.

Sincerely,

/S/

Dennis Dollar Chairman

VERIBANC, Inc.1-800-442-2657

THE NATION’S FIRST BANK RATING SERVICE

VERIBANC®’s RATING SYSTEM

“It’s simple and it works!”

VERIBANC, Inc.’s two-part color code and star classification system rates financial institutions from two perspectives -- present standing and future outlook. It takes into account many financial ratios and measures, including all six factors Federal regulators utilize in determining the government’s “CAMELS” ratings. These factors include an institution’s Capital strength, Asset quality, Management ability, Earnings sufficiency, Liquidity, and Sensitivity to market risk.

Colors - The color code part of the VERIBANC rating system addresses the current financial condition of each institution. A green code means the institution meets high capital standards and is operating profitably. A yellow code means the institution’s equity capital protection is marginal and/or it has recently reported a net loss. Such a situation merits your attention. A red code signifies the institution has a serious shortage of equity capital and/or it has recently suffered a serious net loss. The reason(s) why an institution has been assigned a red code deserves your close attention.

Stars - The second part of the VERIBANC rating system uses three stars, two stars, one star, or no stars to assess an institution’s future prospects. The star classification examines (as appropriate for each kind of institution) threats offered by problem loans, overvalued securities, delinquent derivative contracts, failure to meet government capital requirements, significant asset growth/loss, insider lending, weakness of the holding company, recent regulatory sanctions and other criteria. Deficiencies in these areas could cause future concerns. A three stars rating is the most preferred. (See Exhibit A for a more detailed description of the rating criteria.)

A Warning Signal - If VERIBANC’s rating system produces a high rating in the color code but confers a low score in the star classification, a warning signal exists. In such a case, the color code indicates the institution’s reported basic financials appear strong but the star classification projects some possible deficiencies in other areas. Since the two parts of the rating system examine different criteria, the full color and star rating often hints about the specific nature of an institution’s problems.

An Investment Grade Rating or Better - In 1994, the VERIBANC Green, Three Stars rating was recognized by the Office of Management and Budget as an investment grade or better rating and as such was acceptable for a letter of credit in which the U.S. Government is the beneficiary.

BLUE RIBBON BANK COMMENDATION OF EXCELLENCE

The VERIBANC Blue Ribbon Bank Commendation of Excellence is the country’s oldest formal recognition of banks which have met exceptionally high standards. Based on Federal Reserve Board data and other criteria, this designation is accorded to those institutions that demonstrate exceptional attention to safety, soundness and financial strength. For a bank to qualify for the Blue Ribbon, it must receive VERIBANC’s highest Green, Three Stars rating in our eight level rating system, and it must satisfy additional safety related criteria. Our clients who have relied on Blue Ribbon Banks (only one has ever failed*) have had their risk of bank failure virtually eliminated. Nothing beats a Blue Ribbon.

* Fraud committed by the president whereby he was surreptitiously diverting deposits for his personal use.

MORE ABOUT CAMELS

Federal banking supervisors review six critical aspects of a bank’s operation and condition in their examination rating procedure (the Uniform Interagency Bank Rating System), commonly called the CAMELS ratings. The relationship between VERIBANC’s color and star risk ratings and the “estimated CAMELS” score is tabulated as follows:

Color & Star Ratings Estimated CAMELS Score†

Green, Three Stars with Blue Ribbon recognition CAMELS 1

Green, Three Stars BETWEEN 1 AND 2 without Blue Ribbon recognition (not directly comparable)

Green, Two Stars CAMELS 2

BETWEEN 2 AND 3Yellow, Two Stars (not directly comparable)

Green, One Star CAMELS 3Green, No Stars

Yellow, One Star CAMELS 4Yellow, No Stars

Red, No Stars CAMELS 5

PLEASE NOTE: Only the government and the institution itself, by law, have access to the “official CAMELS” ratings. Our studies have shown that our “estimated CAMELS” is close. Most other rating services and agencies consider only three, four or five of the six “CAMELS” factors. (Originally, there were only five CAMEL factors. The sixth one, “sensitivity to market risk,” was added by regulators several years ago.) VERIBANC takes all six into account.

VERIBANC’s TRACK RECORD

The accuracy of VERIBANC’s rating system is unmatched by any other company in the country. As an example of VERIBANC’s track record, the last thirteen years of bank failures and the associated ratings provided to clients are presented below. VERIBANC provides exact data on the accuracy of past ratings. (No other bank rating service or credit risk rating agency tells you exactly how accurate their ratings are. Some bank raters selectively tell you about their successes. VERIBANC believes that you should have enough information so that you can make up your own mind as to which bank to use -and which bank rating firm to use.) The ratings in the table that follows are the ones which were being furnished to VERIBANC’s customers before, and at the time, each bank failed. There are eight rating categories in VERIBANC’s system.

Average Number of Banks in Each Color and Star Classification With Failure Rates Between 1991 and 2003

Color Code and Star Rating

Average Number of Banks In Category

Average Percentage of Banks in Category

Annualized Failure Rate†

Green *** 8348 82.53 0.03

Green ** 924 9.13 0.08

Green * 53 0.52 2.20

Green, none 8 0.08 2.50††

Yellow ** 632 6.25 0.24

Yellow * 69 0.68 4.20

Yellow, none 27 0.26 13.74

Red, none 56 0.55 91.28

† 1991 through 2003 - chances per 1,000 banks per year. †† Statistical variance due to small sample of failures during this epoch. Note that the combinations Yellow ***, Red***, Red ** and Red* are not used.

HIGHLIGHTS OF VERIBANC’s TRACK RECORD

During the last thirteen years, most of the failures (332 bank failures) occurred among the Red, No Stars group which represented only 0.55% of the industry.

Only One Failure in Over Twenty Years For Blue Ribbon Banks - Additional support for VERIBANC’s exemplary track record derives from the almost zero failure rate for banks receiving the Blue Ribbon Bank designation. Since its introduction in 1982, only one Blue Ribbon Bank has ever failed.

For over twenty years, our clients who have relied on Blue Ribbon Banks have had their risk of bank failure virtually eliminated.

Timeliness - Another factor which heightens rating effectiveness is timeliness. Each quarter, when new data for all banks is released by the Federal Reserve Board, VERIBANC is the first organization (often by several weeks or more) to make this information and our associated analyses available to the public. Why do we place such urgency on rapid updating? Quite simply because we have found that the latest indicators of an institution’s performance are the best predictors of how it will do in the future. Our studies have shown that a lot can change in three months. Some organizations do not associate a date with their information. As you might imagine, they are often “behind” -- by six months or more.

Adjustments To Ratings - VERIBANC ratings and analysis have been subjected to exhaustive external critique for more than 20 years. We have invited review by observers ranging from industry experts to university researchers. Financial institutions are encouraged to contact us if they have more current data or unusual circumstances which they believe could or should affect their VERIBANC risk rating. We constantly monitor institutions and adjust, update and review ratings between quarters when appropriate. The purpose is to provide our clients with the best measure of banking risk that is possible.

It is because of our rating system’s unmatched track record that VERIBANC is considered to be the nation’s premier bank rating service.

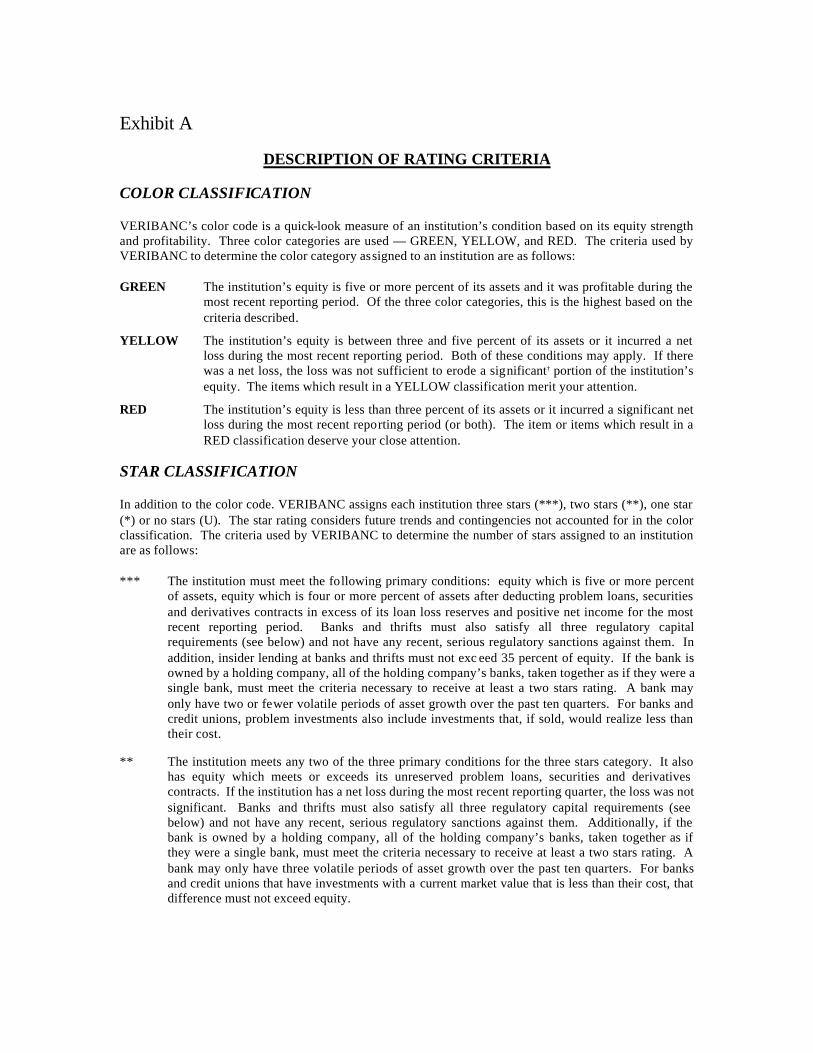

Exhibit A

DESCRIPTION OF RATING CRITERIA

COLOR CLASSIFICATION

VERIBANC’s color code is a quick-look measure of an institution’s condition based on its equity strength and profitability. Three color categories are used — GREEN, YELLOW, and RED. The criteria used by VERIBANC to determine the color category assigned to an institution are as follows:

GREEN The institution’s equity is five or more percent of its assets and it was profitable during the most recent reporting period. Of the three color categories, this is the highest based on the criteria described.

YELLOW The institution’s equity is between three and five percent of its assets or it incurred a net loss during the most recent reporting period. Both of these conditions may apply. If there was a net loss, the loss was not sufficient to erode a significant† portion of the institution’s equity. The items which result in a YELLOW classification merit your attention.

RED The institution’s equity is less than three percent of its assets or it incurred a significant net loss during the most recent reporting period (or both). The item or items which result in a RED classification deserve your close attention.

STAR CLASSIFICATION

In addition to the color code. VERIBANC assigns each institution three stars (***), two stars (**), one star (*) or no stars (U). The star rating considers future trends and contingencies not accounted for in the color classification. The criteria used by VERIBANC to determine the number of stars assigned to an institution are as follows:

*** The institution must meet the following primary conditions: equity which is five or more percent of assets, equity which is four or more percent of assets after deducting problem loans, securities and derivatives contracts in excess of its loan loss reserves and positive net income for the most recent reporting period. Banks and thrifts must also satisfy all three regulatory capital requirements (see below) and not have any recent, serious regulatory sanctions against them. In addition, insider lending at banks and thrifts must not exc eed 35 percent of equity. If the bank is owned by a holding company, all of the holding company’s banks, taken together as if they were a single bank, must meet the criteria necessary to receive at least a two stars rating. A bank may only have two or fewer volatile periods of asset growth over the past ten quarters. For banks and credit unions, problem investments also include investments that, if sold, would realize less than their cost.

** The institution meets any two of the three primary conditions for the three stars category. It also has equity which meets or exceeds its unreserved problem loans, securities and derivatives contracts. If the institution has a net loss during the most recent reporting quarter, the loss was not significant. Banks and thrifts must also satisfy all three regulatory capital requirements (see below) and not have any recent, serious regulatory sanctions against them. Additionally, if the bank is owned by a holding company, all of the holding company’s banks, taken together as if they were a single bank, must meet the criteria necessary to receive at least a two stars rating. A bank may only have three volatile periods of asset growth over the past ten quarters. For banks and credit unions that have investments with a current market value that is less than their cost, that difference must not exceed equity.

* The institution meets at least one of the primary conditions required for the three stars category. It reports equity which is both three or more percent of assets and also meets or exceeds unreserved problem loans, securities and derivatives contracts. If the institution has a net loss during the most recent reporting quarter, the loss was not significant. Moreover, if the institution is a bank or a thrift, it meets at least two of the three federal capital requirements for tier one (core) capital, total capital and capital as a percentage of risk weighted assets. A bank may receive no higher than a one star rating if it has been subject to a recent serious regulatory sanction, or if all of the banks in its holding company, taken together as if they were a single bank, receive a one star or a no stars rating, or has four or more volatile periods of asset growth over the past ten quarters.. Also, a bank or credit union may receive a one star rating if, absent other reasons for downrating as stated above, the difference between the cost and current market value of its investments exceeds the institution’s equity.

None The institution does not meet the criteria stated above.

† A quarterly loss is considered significant when it exceeds 18.75% of an institution’s equity. A semi-annual loss which exceeds 37.5% of a credit union’s equity may also be considered significant. If a bank, S&L or credit union’s loss continues to exceed 18.75% of its equity every quarter (or, 37.5% of its equity every six months), the institution could become insolvent within one year. VERIBANC has no way to know whether or not losses at an institution will continue.

Veribanc Inc. is a national, independent rating service of financial institutions. Veribanc is not affiliated with Primary Financial. Primary Financial makes no representations whatsoever about Veribanc or the information that it provides. Primary Financial furnishes the Veribanc rating system to its clients solely as a convenience and Primary Financial disclaims any warranty or representation regarding the effectiveness of the Veribanc rating system for financial institutions. The use of the Veribanc rating system, or any other rating system, in investment decisions regarding certificates of deposit is at the sole discretion of the client. Primary Financial's clients who are purchasers and sellers of certificates of deposit are responsible for all investment decisions; Primary Financial does not provide investment advice. Additionally, Primary Financial's providing of Veribanc ratings to its clients does not mean that Primary Financial endorses or accepts any responsibility for the content of the use of such ratings. IN NO EVENT WILL PRIMARY FINANCIAL BE LIABLE TO ANY PARTY FOR ANY DIRECT, INDIRECT, SPECIAL OR OTHER CONSEQUENTIAL DAMAGES FOR ANY USE OF INFORMATION PROVIDED BY VERIBANC.