Sri Lanka: growing the SME sector and opportunities for trade

Trade obstacles to SME participation in tradeSection D investigates the major trade-related impediments to SMEs’ participation in trade. A key finding in this section is that all types of trade costs, whether they are fixed or variable, adversely affect the ability of SMEs to participate in trade, to a greater extent than large enterprises. Since SMEs are more sensitive to trade barriers than large firms, removing obstacles to trade benefits SMEs disproportionately. It is therefore important to understand what these major obstacles are.

D

Contents1. SME perceptions of barriers to access international markets 78

2. Trade policy and SMEs 83

3. Other major trade-related costs 91

4. ICT-enabled trade: benefits and challenges for SMEs 98

5. SME access to GVC-enabled trade 102

6. Conclusions 106

Some key facts and findings

•• Tariffs•and•non-tariff•restrictions•affect•the•ability•to•participate•in•trade•of•SMEs•more•adversely•than•that•of•large•enterprises.•

•• Trade•facilitation•promotes•the•entry•of•SMEs•into•export•markets.•Small•exporting•firms•profit•relatively•more•when•trade•facilitation•improvements•relate•to•information•availability,•advance•rulings•and•appeal•procedures.

•• Services•SMEs•are•relatively•more•impacted•by•barriers•on•“establishment”•than•by•barriers•on•“operations”,•notably•when•these•concern•mode•4•trade.

•• Logistics•tend•to•cost•more•for•SMEs•than•for•large•enterprises.•For•example,•in•Latin•America,•domestic•logistics•costs•can•add•up•to•more•than•42•per•cent•of•total•sales•for•SMEs,•as•compared•to•15-18•per•cent•for•large•firms.•

•• SMEs•face•more•credit•rationing,•higher•“screening”•costs•and•higher•interest•rates•than•larger•enterprises.•SMEs•are•also•the•most•credit•constrained.•It•is•estimated•that•half•of•their•requests•for•trade•finance•are•rejected,•compared•to•only•7•per•cent•for•multinational•corporations.

•• The•benefits•from•the•ICT•revolution•are•particularly•high•for•SMEs.•However,•there•are•some•unique•costs•of•online•trade,•such•as•the•costs•of•accessing•ICTs•and•the•need•for•certainty•and•predictability•in•regimes•governing•global•data•transfers.•Small•firms•in•LDCs•only•attain•22•per•cent•of•the•connectivity•score•of•large•firms•in•LDCs,•compared•to•64•per•cent•in•developed•countries.•

•• GVCs•help•SMEs•to•overcome•some•of•the•difficulties•they•face•in•accessing•international•markets.•However,•lack•of•skills•and•technology,•together•with•poor•access•to•finance,•logistics•and•infrastructure•costs•and•regulatory•uncertainty•make•it•difficult•for•SMEs•to•participate•in•GVCs.

WORLD TRADE REPORT 2016

78

Section D.1 identifies the obstacles to trade thatfirmsperceiveasmajorchallengesfor theiraccesstointernationalmarkets.1SectionsD.2andD.3provideasenseofthemagnitudeofthesebarrierstotradeandtheir effects on SMEs, looking at tariff and non-tariffbarriers and other trade-related barriers, respectively.SectionsD.4andD.5explainhowSMEscanovercomesome of these barriers through trade, particularlyonline trade and global value chains (GVCs). ThesesubsectionsalsoexploretheobstaclesfacedbySMEsastheyexploittheopportunitiesofferedbyonlinetradeandGVCstoaccessinternationalmarkets.

1. SMEperceptionsofbarrierstoaccessinternationalmarkets

Onewaytogetasenseofthemainobstaclestotradefor SMEs is through survey data. The United StatesInternationalTradeCommission(USITC),theEuropeanCommission, the World Bank, the International TradeCentre (ITC) and the Organisation for EconomicCo-operationandDevelopment(OECD),inconjunctionwiththeWTO,haveconductedanumberofsurveysthatallowfirmstobeclassifiedbytheirsize.TheresultsofthesesurveyshelptoidentifysomeoftheSME-specificobstaclesthatareexploredinthischapter.

Itisimportanttostressattheoutsetthattheresultsofsurveysareverysensitivetothedesignofthesurveyitself.Asurveydesignedtoidentifytradecostsshouldtypicallyaskthefirmsurveyedtoindicatewhatcosts,outofapredefinedsetofoptions, thefirmperceivesasamajorobstacletotrade. Ifacost isnot includedin the predefined multiple choice set of costs, it willnot appear as a major trade cost. For this reason,differentsurveysarenotreallycomparable.However,rankingthelistedtradecostsineachsurveymaystillhelptounderstandwhichtradecostsarethemostandthe least significant for firms, and, more importantlyfor the purpose of this report, which trade costs arerelatively more important for SMEs relative to largeenterprises.

Most of the information on obstacles to trade asperceived by SMEs in developing countries does notallow a comparison between the relative importanceof obstacles to trade between small and large firms,because studies tend to focus on SMEs only.2 Onenotableexceptionistheseriesofbusinesssurveysonnon-tariff measures (NTMs) undertaken by the ITC,3whichsuggeststhatSMEsaremoreaffectedbyNTMsthanlargefirms.

Allthesestudiespointustosomeofthemajorperceivedobstaclestotrade.TableD.1offersareviewofselectedempirical investigations conducted in developing

countries. The main obstacles to international tradeemergingfromthisrevieware:

(i) limitedinformationabouttheworkingoftheforeignmarkets, and in particular difficulties in accessingexport distribution channels and in contactingoverseascustomers;

(ii) costly product standards and certificationprocedures,and,inparticular,alackofinformationaboutrequirementsintheforeigncountry;

(iii)unfamiliar and burdensome customs andbureaucraticprocedures;and

(iv)poor access to finance and slow paymentmechanisms.

In order to get a sense of the relative importance ofthe obstacles to trade for small and large firms indeveloping countries, the database of the FourthGlobal Review of Aid for Trade (OECD and WTO,2013) isused.Thissurvey looksataslightlydifferentquestion:thatis,obstaclestoenterandmoveupvaluechains rather than the obstacles to trade. However,as discussed in Section B, internationalization ofSMEs mostly takes place through indirect channels,through the contribution that SMEs make to exportsasupstreamproducers invaluechains.Directexportsarealmostexclusivelydonebylargefirms.Indevelopedand developing countries alike, the top 5 per cent offirms account on average for 80 per cent of exports.Therefore, the perceived obstacles to participating ina supply chain provide important clues into the moregeneral question of what are the major obstacles totrade.

Table D.2 reports the ranking of the major obstaclesto enter and move up value chains as perceived byinterviewed firms by sectors. In the OECD and WTO(2013) publication, a survey of 122 questions wascompleted by 524 firms and business associations indevelopingcountries,presentingthebindingconstraintsthesefirmsfaceinentering,establishingormovingupvaluechains.4 Inaddition,173 leadfirms,mostly fromOECD countries, also completed the questionnaireto highlight the obstacles they face in integratingdevelopingcountryfirmsintotheirvaluechain.5

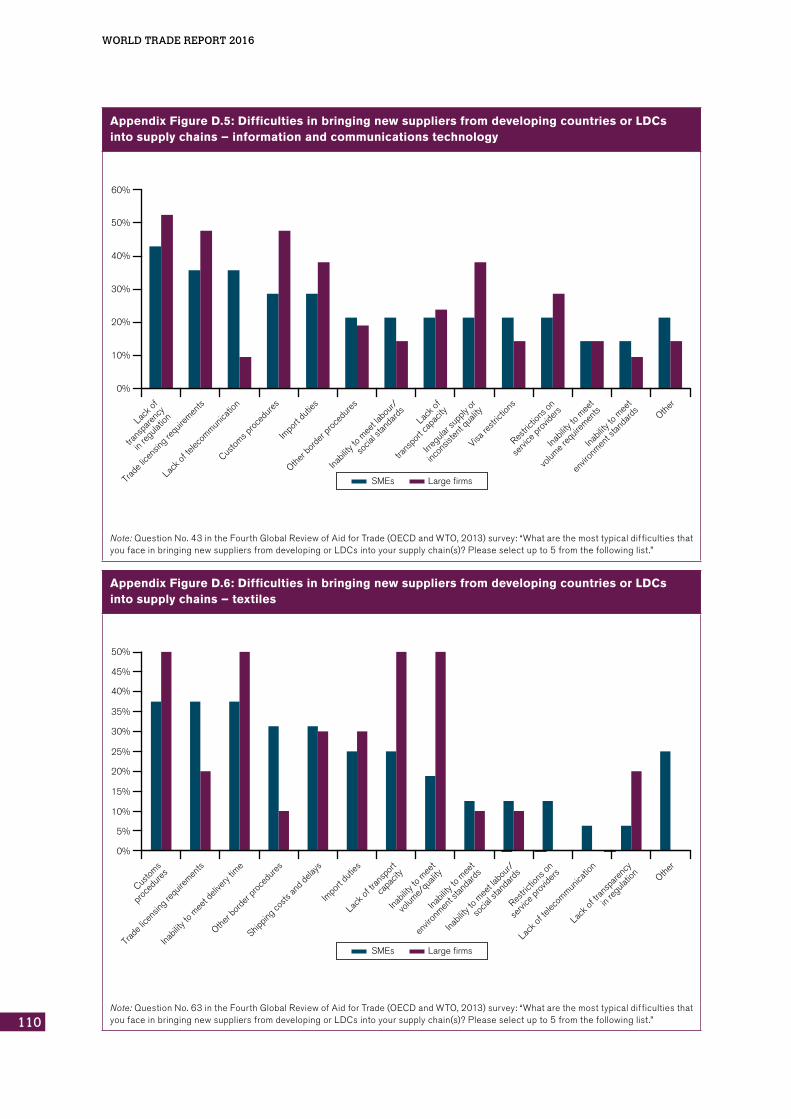

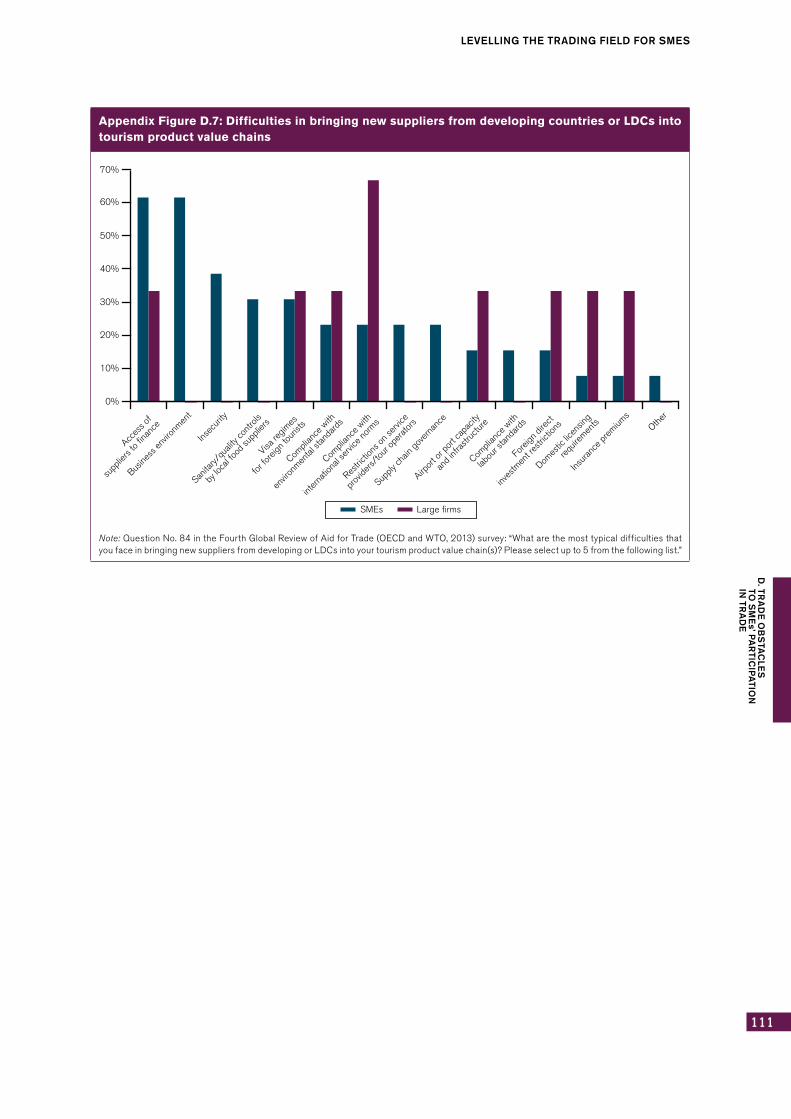

The questionnaire focused on businesses integratedinto value chains in five key sectors: agrifood,information and communication technology (ICT),textiles and apparel, tourism, and transport andlogistics.6Theoriginalquestionnairedividedresponsesinto five categories: micro firms with less than 10employees; small firms, with 10 to 49 employees;medium-sized firms, with 50 to 250 employees; large

79

D. TR

AD

E O

BS

TAC

LES

TO

SM

Es’ P

AR

TICIP

ATIO

N

IN TR

AD

ELEVELLING THE TRADING FIELD FOR SMES

Table D.1: A review of export barriers as emerging in selected studies on developing countries

Ethiopia Iran Jordan Mauritius Nigeria Sri Lanka

LakewandChiloane-Tsoka(2015)surveyednineSMEsbasedinAddisAbabaproducingleatherandleatherproducts.

KabiriandMokshapathy(2012)surveyed76SMEsproducingfruitandvegetablesinTehran.

Al-Hyarietal.(2012)surveyed135JordanianmanufacturingSMEs.

Dusoyeetal.(2013)surveyed41SMEsexportersinMauritius.

Okpara(2009)surveyed72manufacturingSMEsinNigeria

Gunaratne(2009)undertookapostalquestionnairesurveyofSMEsinSriLanka.

MAJOR TRADE BARRIERS

– Lackoffinance– Tariffandnon-

tariffbarriers– Unfamiliarwith

exportprocedures– Slowcollection

ofpaymentfromabroad

– Foreigndistribution

– Complexexportdocument

– Politicalinstabilityinforeignmarkets

– Foreignexchangerate

– Exportingprocedures/documentation

– Communicationwithforeigncustomers

– Collectionofpaymentsfromabroad

– Exportrestrictions– Politicalinstability

inforeignmarkets– Tariffand

non-tariffbarriers– Unfamiliarforeign

businesspractices– Sociocultural

differences– Language– Lackof

informationonforeignmarket

– Distributionchannels

– Logisticcost

– Transportationcosts

– Governmentregulationsandrules

– Foreignrulesandregulations

– Collectionofpaymentsfromabroad

– Costofcapitaltofinanceexport

– Foreigncurrenciesrisk

– Insufficientinformationaboutoverseasmarkets

– Currencyfluctuations

– Hightransportationcost

– Costofestablishinganofficeabroad

– Currencyfluctuations

– Lackoffinance– Government

bureaucracy– Obtaining

reliableforeignrepresentation

– Exchangeratepolicies

– Lackofexportmarketknowledge

– Lackofexportfinance

– Difficultyinhandlingexportdocumentationrequirement

– Transportationandinsurancecosts

– Languagedifferences

– Lackoffinance– Corrupt

bureaucraticpracticesinthehomecountry

– Tariffandnon-tariffbarriers

– Language– Lackofreliable

dataonforeignmarket

– Difficultyinmanagingadvertisingandpromotion

OECD and APEC countries ALADI countries CBI7 Export Coaching Programmes

OECD(2008)surveyed978SMEs’perceptionofthebarrierstotheirinternationalizationacross47countries.

AreportbytheOECD(2005)presentsthefindingsofastudyon30SMEsin12ALADI(AsociaciónLatinoamericanadeIntegración–LatinAmericanIntegrationAssociation)countriesonthebarrierstoaccessingforeignmarketsperceivedbyfirmsinALADIcountries.

Vonketal.(2015)evaluatedfiveofCBI’sExportCoachingProgrammes(ECPs).TheseprogrammesaimtoincreaseexportsfromdevelopingcountriesintoEurope.TheevaluationwasconductedthroughinterviewsandquestionnairessubmittedtoselectedSMEs.Thirty-threeresponseswerereceived(24wereIndianfirms)indicating“themostimportantreasonfornotexporting(more)totheEU”.

TRADE BARRIERS

– Identifyingforeignbusinessopportunities– Limitedinformationwithwhichtolocate/

analysemarkets– Inabilitytocontactpotentialoverseas

customers– Obtainingreliableforeignrepresentation– Lackofmanagerialtimetodealwith

internationalization– Inadequatequantityofpersonneland/or

untrainedpersonnelforinternationalization– Excessivetransportationcosts

– Lackofinformationandrequirements– Customsandbureaucraticprocedures– Financeandpaymentmechanisms– Non-tariffbarriers– Transportation:costs,frequency,and

insecurity;inadequatelogistics– Marketingregulationsandregional

agreements– SPSandheterogeneoustechnical

measures– Asymmetricphysicalandtechnological

infrastructureofcountries– Politicalandeconomicinstability– Subsidies

– Lackofbusinesscontact– Lackofmarketinformation

Notes:Thesestudieslookedatobstaclestotradebothinternalandexternaltothefirm,thetablehoweveronlyreportstradebarriers.Forexample,difficultyinobtaininginformationonrulesandregulationsinaforeignmarketisabarriertoexportbecauseitinvolvesextracoststhatthefirmshavetomeetinordertoexport.Lackofpersonneltolookintotherulesandregulationintheforeignmarketisaninternalproblemofthefirm.

WORLD TRADE REPORT 2016

80

firms,withmorethan250employees;andmultinationalfirms, with more than 250 employees and operatingin more than one country. In Appendix Figures D.1-3,the survey data from large and multinational firms iscombined and presented as “large firms” whereas“MSMEs” represents the combined data from micro,smallandmedium-sizedfirms.

Accesstofinanceandtradefinance,lackoftransparencyintheregulatoryenvironmentandcustomspaperwork,and delays are among the major obstacles to enterandmoveupthevaluechainsforSMEs indevelopingcountries. Certification costs for SMEs in agricultureand inadequate telecommunication networks in ICTalso prevent SMEs from entering supply chains andupgrading.

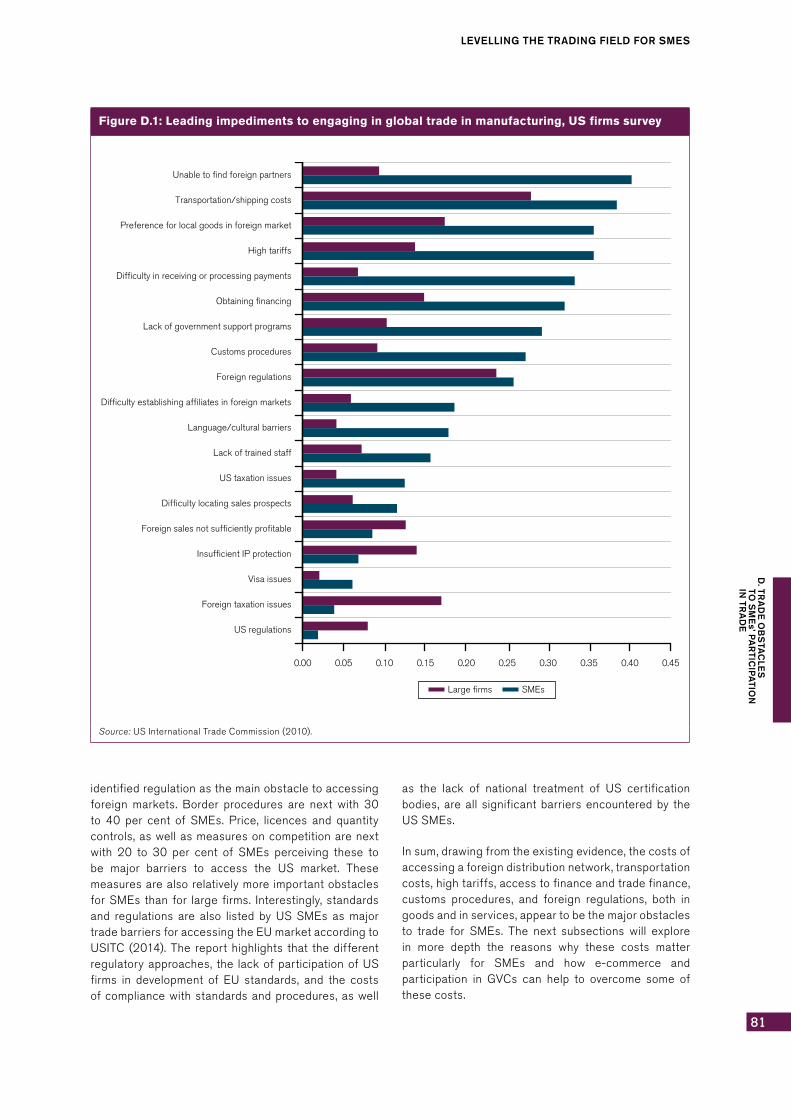

FiguresD.1andD.2showthemainperceivedobstaclesto trade in manufacturing and services based on asurvey of US firms (USITC, 2010). The questionnaireconcerning the leading impediments to engagingin global trade employs a stratified random sampleto survey more than 8,400 US firms. The results areweightedonthebasisoftheproportionoffirmsintheoverall population and the response rates of variouscategories of firms. Firms with between 0 and 499employees in the United States are categorized asSMEs whilst those with 500 or more employees arecategorizedaslargefirms.Respondingfirmsratedtheseverity of 19 impediments on a 1-to-5 scale, with 1indicatingnoburdenand5indicatingasevereburden.FiguresD.1andD.2showresponsesof4or5onthe1 to5scale, illustrating theshareofSMEsand largefirmsratingimpedimentsasburdensome.8

Interestingly,accesstoaforeigncountry’sdistributionnetwork is perceived as the major obstacle by USSMEs in the manufacturing sector. Conversely, this isperceivedasarelativelyminorobstaclebylargefirms.Similarly, high tariffs and difficulties in accessingfinance and processing payments appear to be

relatively more important obstacles for SMEs’ tradethanforlargefirms’trade.

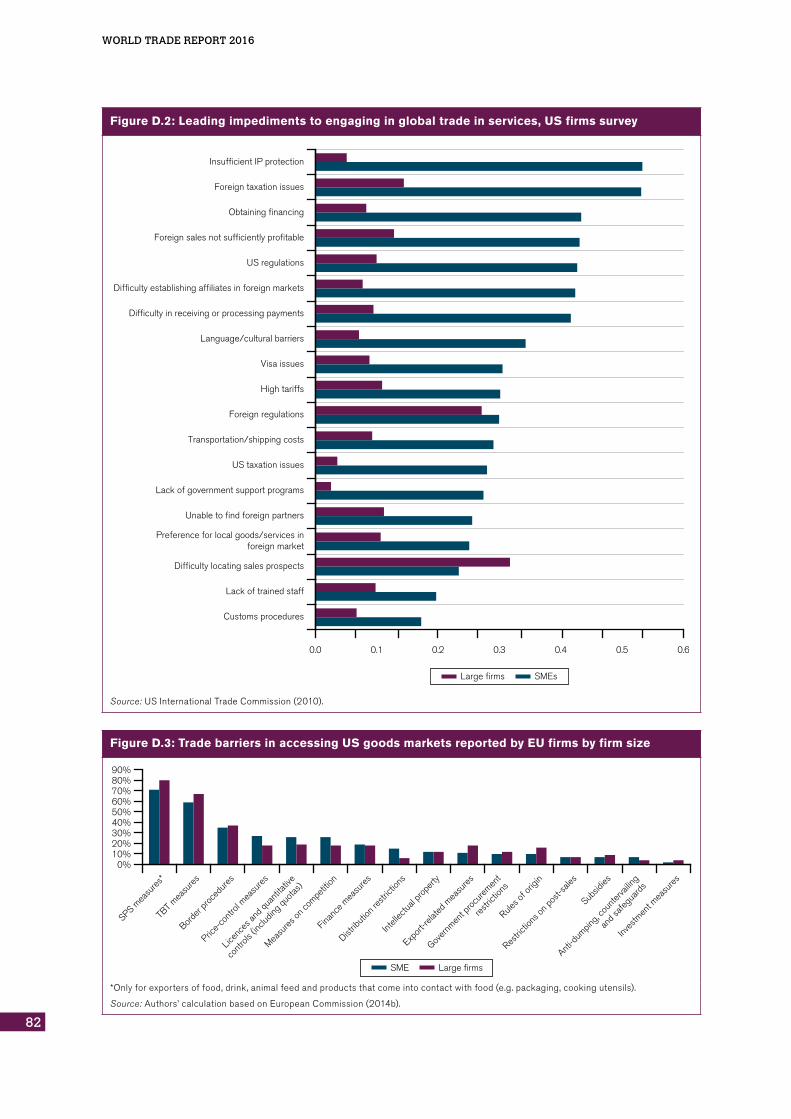

In the services sector,USSMEs reported insufficientIP protection as the major obstacle to export. Forexample,exportersoffilmandtelevisionprogrammingreportedthatseekingremediestoIPinfringementwasoften too expensive for SME producers (IndependentFilm&TelevisionAlliance,2010).

Figure D.3 from the European Commission’sReport Small and Medium Sized Enterprises and theTransatlanticTradeandInvestmentPartnership reportsthemainobstacles to trade forEU firmsexporting totheUnitedStates(EuropeanCommission,2014b).Thefigurepresentstheresultsofanonlinesurveyof869European companies carried out with the support ofthe Enterprise Europe Network from July 2014 untilJanuary2015.

The companies were asked whether they felt theyfaced barriers in the US market and to identify thenature of those barriers based on a standard list ofnon-tariff measures. The respondents included microfirms employing one to nine people, small firms with10 to 50 employees, medium-sized firms with 51 to250 employees, and big firms with more than 250employees. This survey provides a broad view of theissues that are most important for SMEs, such ascompliance with regulation and standards, customsprocedures, and restrictions on the movement ofpeople and of distribution channels. It also suggeststhatmanyoftheseissuesrepresentlargerbarriersforSMEsthanforlargerfirms,giventhatsmallcompanieshavetospreadfixedcostsofcomplianceoversmallerrevenuesthanthoseoflargerfirms.

Regulations, i.e. sanitary and phytosanitary (SPS)and technical barriers to trade (TBT) measures, areperceived to be the most important obstacle to tradefor all firm sizes. More than 50 per cent of firms

Table D.2: SMEs’ top five perceived constraints in entering, establishing or moving up value chains

Agriculture ICT Textile

Accesstobusinessfinance

Transportationcosts

Certificationcosts

Accesstotradefinance

Customspaperworkanddelays

Accesstotradefinance

Lackoftransparencyinregulatoryenvironment

Unreliableand/orlowbandinternetaccess

Inadequatenationaltelecommunicationsnetworks

Customspaperworkordelays

Accesstotradefinance

Customspaperworkordelays

Shippingcostsanddelays

Supplychaingovernanceissues(e.g.anti-competitivepractices)

Otherborderagencypaperworkordelays

Note:ThespecificquestionforAgriculture,ICTandTextilesectorsis:“Whatdifficultiesdoyoufaceinentering,establishingormovingupthevaluechains?Pleaseselectupto5fromthefollowinglist.”

Source:OECDandWTO(2013).

81

D. TR

AD

E O

BS

TAC

LES

TO

SM

Es’ P

AR

TICIP

ATIO

N

IN TR

AD

ELEVELLING THE TRADING FIELD FOR SMES

identifiedregulationasthemainobstacletoaccessingforeign markets. Border procedures are next with 30to 40 per cent of SMEs. Price, licences and quantitycontrols,aswellasmeasuresoncompetitionarenextwith 20 to 30 per cent of SMEs perceiving these tobe major barriers to access the US market. ThesemeasuresarealsorelativelymoreimportantobstaclesforSMEs than for large firms. Interestingly,standardsand regulations are also listed by US SMEs as majortradebarriersforaccessingtheEUmarketaccordingtoUSITC (2014).The reporthighlights that thedifferentregulatoryapproaches, the lackofparticipationofUSfirms in development of EU standards, and the costsofcompliancewithstandardsandprocedures,aswell

as the lack of national treatment of US certificationbodies, areall significantbarriersencounteredby theUSSMEs.

Insum,drawingfromtheexistingevidence,thecostsofaccessingaforeigndistributionnetwork,transportationcosts,hightariffs,accesstofinanceandtradefinance,customs procedures, and foreign regulations, both ingoodsandinservices,appeartobethemajorobstaclesto trade for SMEs. The next subsections will explorein more depth the reasons why these costs matterparticularly for SMEs and how e-commerce andparticipation in GVCs can help to overcome some ofthesecosts.

Figure D.1: Leading impediments to engaging in global trade in manufacturing, US firms survey

Unable to find foreign partners

Transportation/shipping costs

Preference for local goods in foreign market

High tariffs

Difficulty in receiving or processing payments

Obtaining financing

Lack of government support programs

Customs procedures

Foreign regulations

Difficulty establishing affiliates in foreign markets

Language/cultural barriers

Lack of trained staff

US taxation issues

Difficulty locating sales prospects

Foreign sales not sufficiently profitable

Insufficient IP protection

Visa issues

Foreign taxation issues

US regulations

Large firms SMEs

0.00 0.05 0.10 0.15 0.20 0.25 0.30 0.35 0.40 0.45

Source:USInternationalTradeCommission(2010).

WORLD TRADE REPORT 2016

82

Figure D.2: Leading impediments to engaging in global trade in services, US firms survey

Insufficient IP protection

Foreign taxation issues

Obtaining financing

Foreign sales not sufficiently profitable

US regulations

Difficulty establishing affiliates in foreign markets

Difficulty in receiving or processing payments

Language/cultural barriers

Visa issues

High tariffs

Foreign regulations

Transportation/shipping costs

US taxation issues

Lack of government support programs

Unable to find foreign partners

Preference for local goods/services inforeign market

Difficulty locating sales prospects

Lack of trained staff

Customs procedures

Large firms SMEs

0.0 0.1 0.2 0.3 0.4 0.5 0.6

Source:USInternationalTradeCommission(2010).

Figure D.3: Trade barriers in accessing US goods markets reported by EU firms by firm size

0%10%20%30%40%50%60%70%80%90%

SPS mea

sure

s*

TBT m

easu

res

Borde

r pro

cedu

res

Price-

contr

ol mea

sure

s

Licenc

es an

d qua

ntitat

ive

contr

ols (in

cludin

g quo

tas)

Measu

res o

n com

petiti

on

Financ

e mea

sure

s

Distrib

ution

restr

iction

s

Intell

ectua

l pro

perty

Expor

t-rela

ted m

easu

res

Gover

nmen

t pro

cure

ment

restr

iction

s

Rules o

f orig

in

Restric

tions

on po

st-sa

les

Subsid

ies

Anti-d

umpin

g, co

unter

vailin

g

and s

afegu

ards

Inves

tmen

t mea

sure

s

SME Large firms

*Onlyforexportersoffood,drink,animalfeedandproductsthatcomeintocontactwithfood(e.g.packaging,cookingutensils).

Source:Authors’calculationbasedonEuropeanCommission(2014b).

83

D. TR

AD

E O

BS

TAC

LES

TO

SM

Es’ P

AR

TICIP

ATIO

N

IN TR

AD

ELEVELLING THE TRADING FIELD FOR SMES

2. TradepolicyandSMEs

Thissubsectionlooksattariffandnon-tariffobstaclesto trade, their magnitude and their effects on SMEparticipation in trade in goods. It also discussesbarriersthatmaybeparticularlyburdensomeforSMEsoperatingintheservicesector.

(a) TariffbarriersmaymattermoreforSMEs

As shown in Figure D.1, SMEs in the manufacturingsector consider high tariffs to be a greater obstacleto exporting than large manufacturing firms do. Whatexplainsthisperception?

One explanation is the effect that higher tariffs haveon the participation of SMEs in trade. Higher tariffsindestinationmarketsmake itmoredifficult for firmsto profitably export. Only the more productive firmswillexport insuchanenvironment,whilst smallerandless productive firms will not. As tariffs are reduced,smaller firmsprogressivelyenter in themarket.Usingfirm-levelinformationforIreland,FitzgeraldandHaller(2014)estimatethatreducingtariffsfrom10percentto zero increases participation of medium-sized firms(firmswith100-249employees)from11.5percentto14.2percent.But theydonot findsignificanteffectsonfirmsofsmallersize.

A second explanation is provided by the effect thathighertariffshaveonthevolumeofexportsofafirm.A growing body of theoretical literature emphasizeshow the impact of trade policy depends on firm

characteristics such as size and productivity.9 Smallfirms are more sensitive to tariff changes becausethey produce goods whose demand is more sensitiveto price changes or they pay lower costs to reachadditionalconsumersthanlargefirms(seeBoxD.1foramoredetailedexplanation).

Heterogeneous effects of tariffs across firms ofdifferentsizescanalsobeexplainedby thepresenceof non-ad valorem tariffs. Specific tariffs (per unittariffs) and tariff rate quotas (through the impositionof a quota licence price) act as additive trade costs,that is a cost that is independent of the unit price ofthegood.Anadditivetradecostshassystematicallyadifferentimpactbetweenfirmsthatproducelow-pricedandhigh-pricedgood.Clearly,addingaUS$1tariffona good for which the price is US$ 1 is a much morerestrictivemeasurethanaddingUS$1tariffonagoodfor which the price in the market is US$ 100. If low-priced firmare small firms, theprevalenceof additivetradecostscanalsoexplaintheperceivedimportanceof high tariffs as barriers to trade for small firms(Irarrazabaletal.,2015).10

Athirdexplanationbehindsmallfirms’perceptionthattariffsaffectthemdisproportionatelycouldactuallybethatthereisananti-SMEs-biasinconditionsofmarketaccess.Thatis,SMEsfacehighertariffsonaverageintheir exportmarketdestinations than large firms, andthisiswhySMEsperceivetariffstobeamajorbarrierto trade. Political economy provides some argumentsthatexplainthispotentialoutcome.

Inaworldwheregovernmentsnegotiatingagreementsare influenced by strong lobbying powers, large firms

Box D.1: Firms’ responses to higher tariffs

Spearot(2013)explainsthedifferentialeffectsacrossfirmsofagiventariffincrease(reduction)withthefactthatfirmsfacedifferentdemandelasticities.Inparticular,lowrevenuegoodsexhibitahigherdemandelasticity.Forthisreason,thetraditionalnegativeeffectofhighertradecostsontradeflowsisamplifiedforlow-revenuevarieties (firmswitha lowvalueofexportsprior to thenew restrictivemeasure).11Theopposite is truewhentariffsarecut.Infact,Spearotfindsthatafter1994,followingtheUruguayRound,forthesametariffcut,USimportsoflowrevenuevarietiesincreaseddisproportionallymorethanimportsofhighrevenuevarieties.Insomecases,importsofhighrevenuevarietiesfallafterliberalization.

Anotherstudy(Arkolakis,2011)explainsthedifferentialimpactofhighertariffsbetweensmallandlargefirmsonthebasisofdifferencesinmarketpenetrationcosts.Payinghighercostsallowsfirmstoreachanincreasingnumberofconsumersinacountry.Butthecostofreachingmoreconsumersincreaseswhenafirmhasalreadyreachedahighvolumeofsales.Thatis,reachingmoreandmoreconsumersbecomesincreasinglymoredifficult.Inthisset-up,allfirmslosefromanincreaseintariffs,butfirmsdifferintheirsupplyresponsedependingonthecoststheyfaceinreachingmoreconsumers.Theseadditionalcostsarelargeforlargefirmsandsmallforsmallfirms.Exportsofsmallfirmsgrowmorefollowingtariffliberalizationthandothoseoflargefirms,becausesmallfirmsfacelowercoststhanlargefirmstoreachadditionalconsumers;andviceversa,largefirmsrespondlesstotariffincreases,becauseforeachunitofexportreductiontheysavemorethansmallfirmsintermsofthecoststoreachconsumers.

WORLD TRADE REPORT 2016

84

aremorelikelytoengageinlobbyingthansmallfirms.Large firms have more resources and are better ablethan SMEs to engage in lobbying. Moreover, sectorswith few large firms are likely to be more effectivethansectorswithmanysmallfirmsininfluencingtradepolicyoutcomes.Therefore, a country’s sectoral tariffprofile is likely to depend on the size of firms in thatsector. While in a unilateral set-up, this would leadto higher tariffs in sectors dominated by large firms(Olson,1965;Bombardini,2008),whentariffsaresetin a cooperative environment, export–oriented largefirmswilllobbyfortradeliberalizationandwillsucceedin lowering tariffs (Plouffe, 2012).12 Therefore, to theextentthatlargefirmsarepresentinthesamesectors,theyarelikelyalsotofacelowertariffs.

Available data does not allow for a systematicassessmentof tariffsfacedby individualfirms intheirdestination market. Ideally, in order to calculate theaveragetarifffacedbysmallfirms,onewouldneedtoknowwhatproduct small firmsexport ineachmarketandaveragethetarifffacedacrossmarkets.Thistypeofdataisnotpubliclyavailableforallcountries.

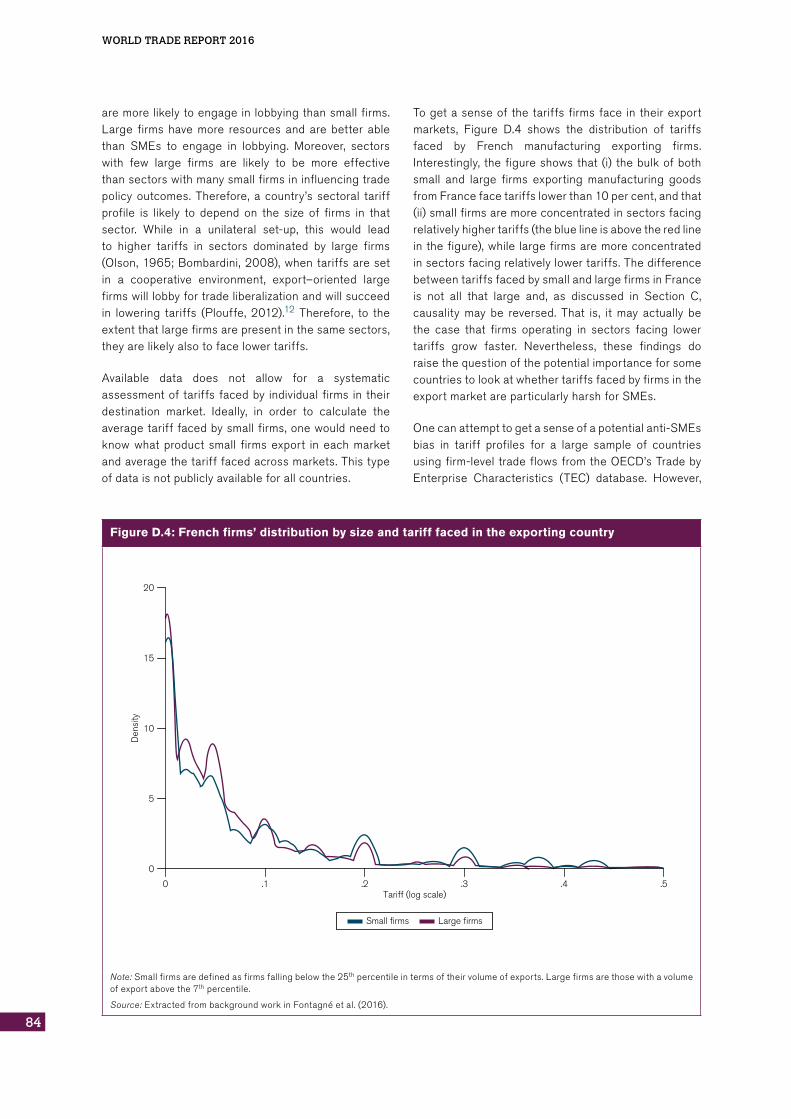

Togetasenseof thetariffs firmsface in theirexportmarkets, Figure D.4 shows the distribution of tariffsfaced by French manufacturing exporting firms.Interestingly, thefigureshowsthat(i) thebulkofbothsmall and large firms exporting manufacturing goodsfromFrancefacetariffslowerthan10percent,andthat(ii)smallfirmsaremoreconcentratedinsectorsfacingrelativelyhighertariffs(thebluelineisabovetheredlineinthefigure),whilelargefirmsaremoreconcentratedinsectorsfacingrelativelylowertariffs.ThedifferencebetweentariffsfacedbysmallandlargefirmsinFranceis not all that large and, as discussed in Section C,causality may be reversed. That is, it may actually bethe case that firms operating in sectors facing lowertariffs grow faster. Nevertheless, these findings doraisethequestionofthepotentialimportanceforsomecountriestolookatwhethertariffsfacedbyfirmsintheexportmarketareparticularlyharshforSMEs.

Onecanattempttogetasenseofapotentialanti-SMEsbias in tariff profiles for a large sample of countriesusingfirm-leveltradeflowsfromtheOECD’sTradebyEnterprise Characteristics (TEC) database. However,

Figure D.4: French firms’ distribution by size and tariff faced in the exporting country

Den

sity

Tariff (log scale)

20

15

10

5

0

0 .1 .2 .3 .4 .5

Small firms Large firms

Note:Smallfirmsaredefinedasfirmsfallingbelowthe25thpercentileintermsoftheirvolumeofexports.Largefirmsarethosewithavolumeofexportabovethe7thpercentile.

Source:ExtractedfrombackgroundworkinFontagnéetal.(2016).

85

D. TR

AD

E O

BS

TAC

LES

TO

SM

Es’ P

AR

TICIP

ATIO

N

IN TR

AD

ELEVELLING THE TRADING FIELD FOR SMES

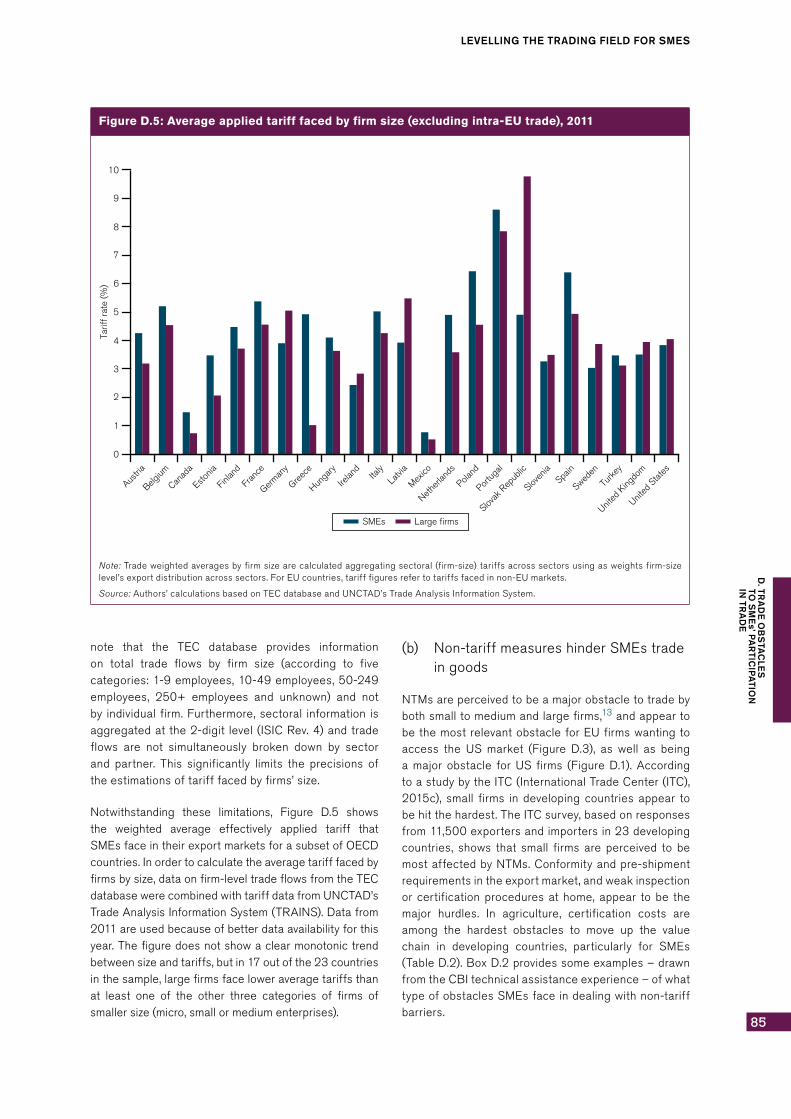

note that the TEC database provides informationon total trade flows by firm size (according to fivecategories:1-9employees,10-49employees,50-249employees, 250+ employees and unknown) and notby individual firm.Furthermore,sectoral information isaggregatedatthe2-digit level(ISICRev.4)andtradeflows are not simultaneously broken down by sectorand partner. This significantly limits the precisions oftheestimationsoftarifffacedbyfirms’size.

Notwithstanding these limitations, Figure D.5 showsthe weighted average effectively applied tariff thatSMEsfaceintheirexportmarketsforasubsetofOECDcountries.Inordertocalculatetheaveragetarifffacedbyfirmsbysize,dataonfirm-leveltradeflowsfromtheTECdatabasewerecombinedwithtariffdatafromUNCTAD’sTradeAnalysisInformationSystem(TRAINS).Datafrom2011areusedbecauseofbetterdataavailabilityforthisyear.Thefiguredoesnotshowaclearmonotonictrendbetweensizeandtariffs,butin17outofthe23countriesinthesample,largefirmsfaceloweraveragetariffsthanat least one of the other three categories of firms ofsmallersize(micro,smallormediumenterprises).

(b) Non-tariffmeasureshinderSMEstradeingoods

NTMsareperceivedtobeamajorobstacletotradebybothsmalltomediumandlargefirms,13andappeartobethemostrelevantobstacleforEUfirmswantingtoaccess the US market (Figure D.3), as well as beinga major obstacle for US firms (Figure D.1). AccordingtoastudybytheITC(InternationalTradeCenter(ITC),2015c), small firms in developing countries appear tobehitthehardest.TheITCsurvey,basedonresponsesfrom11,500exportersandimportersin23developingcountries, shows that small firms are perceived to bemostaffectedbyNTMs.Conformityandpre-shipmentrequirementsintheexportmarket,andweakinspectionor certificationproceduresathome, appear tobe themajor hurdles. In agriculture, certification costs areamong the hardest obstacles to move up the valuechain in developing countries, particularly for SMEs(TableD.2).BoxD.2providessomeexamples–drawnfromtheCBItechnicalassistanceexperience–ofwhattypeofobstaclesSMEsfaceindealingwithnon-tariffbarriers.

Figure D.5: Average applied tariff faced by firm size (excluding intra-EU trade), 2011

Tarif

f rat

e (%

)

0

1

2

3

4

5

6

7

8

9

10

Austria

Canad

a

Belgium

Finlan

d

Estonia

France

German

y

Greec

e

Hunga

ry

Irelan

dIta

ly

Mexico

Latvia

Nether

lands

Poland

Slovak

Rep

ublic

Sloven

ia

Portug

al

Spain

Sweden

Turke

y

United

Stat

es

United

King

dom

SMEs Large firms

Note:Tradeweightedaveragesbyfirmsizearecalculatedaggregatingsectoral(firm-size)tariffsacrosssectorsusingasweightsfirm-sizelevel’sexportdistributionacrosssectors.ForEUcountries,tarifffiguresrefertotariffsfacedinnon-EUmarkets.

Source:Authors’calculationsbasedonTECdatabaseandUNCTAD’sTradeAnalysisInformationSystem.

WORLD TRADE REPORT 2016

86

VeryfewstudiesprovideanindicationastohowNTMsaffectexportersofdifferentsizes.Yet,thetradeimpactofSPS/TBTmeasuresislikelytodependonthesizeoftheexporter.NTMsarecommonlyregardedashavinganimportantfixedcostcomponent,whichsignificantlydifferentiates them from tariffs. For example, a largeinitial investmentmayberequiredforafirmtocomplywith a certain foreign standard, but once the newtechnology is acquired there may be no additionalvariablecosts.14Similarly,aqualificationorcertificationrequirement for service-providing personnel mayinvolve an initial cost of obtaining the qualification orcertification, but no additional variable costs. Fixedcosts, independent of the volume/value of trade, arerelatively more burdensome for SMEs because theyrepresentahighershareoftheirvolumeofaffairs.

Evidence shows that tighter TBT/SPS measures areparticularly costly for smaller firms. Focusing on theelectronicssector,Reyes(2011)examinestheresponseof US manufacturing firms to the harmonization ofEuropeanproductstandardstointernationalnorms.Hefinds that harmonization increases the entry of non-exportingfirmstotheEUmarket,andthattheeffectisstrongerforUSfirmsthatalreadyexporttodevelopingcountriesbutnottotheEU.Thesefirmsareonaveragesmaller than firms exporting to the EU. Focusing on

Senegal, Maertens and Swinnen (2009) show thatvegetableexports to theEuropeanUnionhavegrownsharply between 1991 and 2005 despite increasingSPSrequirements,resultinginimportantincomegainsand poverty reduction. But tightening food regulationhas induced a shift from small farmers to large-scaleintegratedestateproduction.

When a new restrictive SPS measure is introducedina foreignmarket, smallerexporting firmsare thoseexiting the foreign market as well as those that losemore in terms of volumes of trade. The paper byFontagnéetal.(2016)istheonlyonetoprovidesomeevidenceonhowmarketsadjusttotheintroductionofmorerestrictiveSPSmeasures.UsingindividualexportdataonFrenchfirmsprovidedbytheFrenchCustoms,Fontagnéetal. findthatrestrictiveSPSmeasures(asmeasuredbyspecifictradeconcerns)negativelyaffectbothsmallfirms’participationintradeandtheirvolumeoftrade.Inparticular,theyestimatethatrestrictiveSPSmeasuresthathavetriggeredtheexportingcountrytoraise a concern at the WTO SPS Committee, reduceonaverageafirm’sprobabilitytoexportby4percent.Themeaneffectofa restrictiveSPSmeasureon thevalueofexports(theintensivemargin)isapproximately18percent.However,thisnegativeimpactofrestrictiveSPSisreducedforlargerplayers.

Box D.2: SMEs and non-tariff barriers: the importance of transparency and predictability

Each year, the CBI (Centre for the Promotion of Imports from developing countries, part of the NetherlandsEnterprise Agency and commissioned by the Ministry of Foreign Affairs of the Netherlands) provides trade-relatedtechnicalsupporttoover700SMEexportersindevelopingcountries.AnimportantlessonfromSMEsinCBIprogrammesconcernsthepredictabilityandtransparencyofstandardsandregulations.

InKenya’steasector,forexample,CBIhassupportedtheproductandmarketdiversificationintovalue-addedteaswithspecialflavoursandprocessedintoteabags.AsCBIExpertPhoebeOwuorsays:“Whereasmarketaccessbarriers in theEUmarkets areoftenhighandcostly to complywith for the tea-exportingSMEs, theexports to regionalandemergingmarketshaveprovedmoredifficultasa resultof lackof informationaboutactualconditions”.

CBI’s experience in company-level technical assistance has shown that exporting SMEs from developingcountriesincreasinglyinvestinstaffskillsandknowledgepertainingtomarketaccessrequirements.Increasingly,exportingSMEsalsoestablishclearinternalprocessesandguidelinestoensurecompliancewithdomesticaswellasinternationallyagreedregulations.

ConductingmarketresearchiskeyforSMEswishingtotargetnewmarkets,bylookingatworldwideandlocaldemand,competitors,andmarketaccessconditions(includingbothtariffandnon-tariffbarriers).Usefultoolsinclude paid services (often with a sector focus), as well as “global public goods” such as those offered byITCMarketAccesstools(includingTrademap,MacmapandStandardsmap),aswellasBI’sMarketIntelligenceplatformontheEuropeanmarkets,whichcontainscontentbasedonacombinationofquantitativeandqualitativeresearch, including inputs from 24 sectoral sounding boards consisting of experts and entrepreneurs fromEuropeanimportingindustries(www.cbi.eu/market-information).ButSMEexportscontinuetobehamperedbychangingregulations,lackofclarity,andunpredictability.

Source:SchaapandHekking(2016).

87

D. TR

AD

E O

BS

TAC

LES

TO

SM

Es’ P

AR

TICIP

ATIO

N

IN TR

AD

ELEVELLING THE TRADING FIELD FOR SMES

As shown in Fontagné et al. (2016), larger firmslose less than smaller firms from the introductionof restrictive SPS measures into the export marketbecause they are able to absorb part of the highercosts.15 Prices increase follow the introduction of arestrictive measure in the export market, but this islessthecaseforlargerfirms.Thisisbecauselargeandpotentiallymoreefficientfirmsarelikelytocomplywithmorestringent requirementsmoreeasilyandat lowercost. Large exporters with higher market shares andlower demand elasticities also pass less of the costincreaseontotheconsumer.

There is also some case-specific evidence that theimpact of NTMs on trade depends on the size of theexporters. The impactof certificationon thesourcingstrategyoffirmsinasparagusexportsfromPeruisanexampleofthepotentialnegativeimpactthatNTMscanhaveonsmallfirms.Peruisthelargestexporteroffreshasparagus worldwide and the sector has significantlyincreasedinthelastdecadeboth intermsofvolumesofexportsandnumberofexporters.Thishappenedatthe same time that the number of private standardsin the sector multiplied. This success story, however,goes togetherwith theevidence that theproliferation

ofprivatestandardshasaffectedthesourcingstrategyof firms, at the expense of small producers. Certifiedexport firms currently source less from smallholderproducers (1.5 per cent) than do non-certified firms(25 per cent). Before becoming certified (in 2001),instead, export firms sourced more from smallholderproducers(20percent)(MaertensandSwinnen,2015).

(c) Customsprocedures

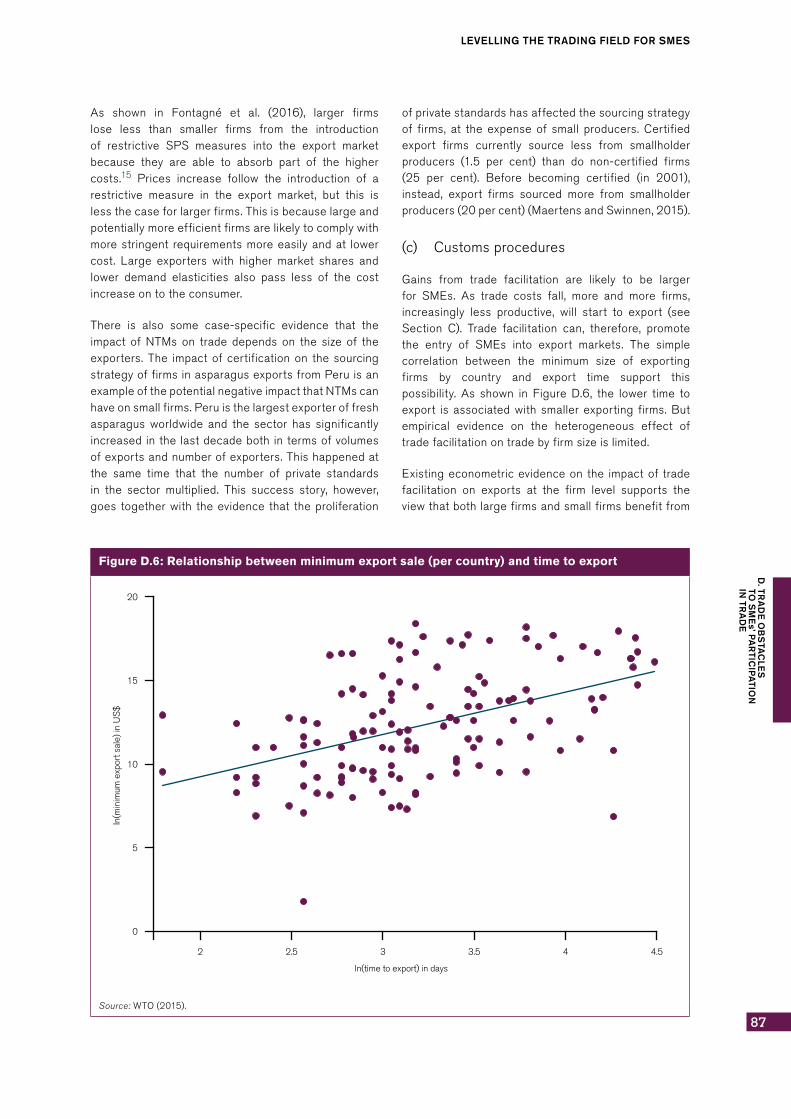

Gains from trade facilitation are likely to be largerfor SMEs. As trade costs fall, more and more firms,increasingly less productive, will start to export (seeSection C). Trade facilitation can, therefore, promotethe entry of SMEs into export markets. The simplecorrelation between the minimum size of exportingfirms by country and export time support thispossibility. As shown in Figure D.6, the lower time toexport is associatedwith smaller exporting firms.Butempirical evidence on the heterogeneous effect oftradefacilitationontradebyfirmsizeislimited.

Existingeconometricevidenceon the impactof tradefacilitation on exports at the firm level supports theviewthatbothlargefirmsandsmallfirmsbenefitfrom

Figure D.6: Relationship between minimum export sale (per country) and time to export

2

0

5

10

15

20

2.5 3

ln(time to export) in days

ln(m

inim

um e

xpor

t sal

e) in

US

$

3.5 4 4.5

Source:WTO(2015).

WORLD TRADE REPORT 2016

88

trade facilitation, and that, in particular, small firmsbenefit the most in term of exports, when the effectoftradefacilitationonfosteringtheentryofnewfirmsin theexportmarket isalsotaken intoaccount.Usingthe World Bank Enterprise Surveys database, Hanand Piermartini (2016) show that the effect of tradefacilitationontradedependsonafirm’ssize.Whenbothexportingandnon-exporting firmsare included in thesampleofanalysis,micro,SMEsprofitmorethanlargefirmsfromreducedtimetoexport.HanandPiermartiniestimate that tradefacilitationmeasures that reducedexporttimeforallfirmsatthemedianregionallevelmayboosttheshareofSMEexportsbynearly20percentandthatoflargefirmsby15percent.Thisisbecausesmallfirmsaremorelikelytostartexporting.Whenonlyexportingfirmsaretakenintoaccount,(HoekmanandShepherd, 2015) find, however, that reduced time toexportdoesboostfirms’exportshares,butitdoesthisequallyforsmallandlargefirms.

There isalsoevidence thatdifferentprovisionsof theTrade Facilitation Agreement affect small and largefirms differently. Using the firm-level customs data ofFrenchexports,and lookingat theeffectsona firm’sexport of improving trade facilitation in the importingcountry rather than in the exporting country itself,Fontagnéetal. (2016)show thatwhile, ingeneral, allexporting firms gain from improved trade facilitationin the importing country, the relative effects on smallandlargefirmsvaryaccordingtothetypeoffacilitationmeasure.

The study finds that small exporting firms profitrelatively more when trade facilitation improvementsrelate to information availability, advance rulings andappealprocedures.Forexample, ifallEastAsianandPacific countries adopted the region’s best practicesinmeasuresthatimproveinformationavailability,smallexporting firms would export 48 per cent more thantheycurrentlydoandmedium-sizedfirmswouldexport25percentmore(therewouldbenosignificanteffectfor big firms). Large exporting firms profit relativelymorewhentheimportingcountry’sfacilitationreformsrelatetothesimplificationofformalities.Onepossibleexplanation, provided by the authors, is that thesimplification of formalities reduces corruption at theborderandthatthis,inturn,hasapositiveeffectonthepropensity of large firms to trade. Large firms are, infact,empiricallyfoundtobemoresensitivethansmallfirmstocorruption.

(d) TradepolicyandservicesSMEs

Assessing which trade barriers are particularlyburdensome for SMEs’ services exports presentsa number of challenges. First, services trade asdefined in the GATS is multimodal: it encompasses

not only cross-border transactions (mode 1), but alsoconsumption of a service in a foreign territory (mode2) and the movement of the supplier abroad, eitherto establish a commercial presence (mode 3) or inperson (mode 4).16 Most services may be traded viamore than one mode of supply. As such, the impactof barriers to trade inoneparticularmode is likely todepend on whether or not the mode in question is aservice supplier’s preferred export avenue. Second,there are no theoretical analyses and few empiricalstudiesdirectlyaddressingthisquestion.Third,littleisknownabout thecharacteristicsofservicesexportingSMEs,andwhatinformationexistsislargelybasedonexperiencesindevelopedcountries.

Nevertheless, available empirical literature on theexport behaviour of services SMEs (Lejárraga andOberhofer,2013)providesausefulbackgroundagainstwhichtoassessthisquestion.ServiceSMEsthatexportemployrelativelymorehighlyskilledworkers,payhigherwagesandaremoreinnovative,butarenotnecessarilyalways larger. The positive relationship between firmsizeandexport likelihoodis infact inconclusiveinthecase of services, whereas it is firmly established formanufacturing.

Usingfirm-leveldataforFrance,LejárragaandOberhofer(2013)findthatfirmsizehasapositiveeffectontheexportprobabilityforsuppliersoffinancial,ICTandprofessionalservices, butno impact for travel serviceproviders, forinstance. Importantly, as already discussed in SectionB.1 and evidenced by the survey results presented inSection D.1, the one element that emerges stronglyfromavailableresearchisthesubstantialheterogeneityin traders’ characteristics across services industries(Lejárragaetal.,2015).Drawingfirmconclusionsabout“service-exportingSMEs”asonemonolithiccategoryis,therefore,ratherdifficult.

In terms of how to export, services SMEs’ choice ofmodeofsupplydependsonthecomparativecostandexpected revenue involved. They may choose onemode,ormaywish,orneed, to relyonseveralmodestoserveforeignmarkets.Mode1tradeinICTservices,for instance, will be facilitated by associated mode 4movements that enable the supplier to be physicallyclose to its customers. Moreover, not all modes areequally feasible ways of exporting services: hotelservices can be supplied essentially via mode 2 only,forinstance,whileexportsofconstructionservicesarehardlypossiblecross-border.

Persin (2011) argues that service SMEs tend to leantowards“soft”formsofinternationalization,becauseofsizeconstraints,andexportessentiallyviamode1andmode 4. Kelle et al. (2013) analyse firms’ choices ofexportingacrossbordersorthroughtheestablishment

89

D. TR

AD

E O

BS

TAC

LES

TO

SM

Es’ P

AR

TICIP

ATIO

N

IN TR

AD

ELEVELLING THE TRADING FIELD FOR SMES

ofacommercialpresence.Relyingonfirm-leveldataforGermany, they empirically confirm SMEs’ preferencesformode1.InastudybyHentenandVad(2001),DanishSMEsarealsofoundtoexportservicesbyrelyingmoreon cross-border trade than on the establishment of acommercial presence, except in the case of financialservices.

Inadditiontodirectexports,SMEshaverecoursealsoto indirect formsof internationalization.These includeindirect exports through intermediaries, which werediscussedaspartof theGVCanalysis inSectionB.2,technological cooperation with foreign enterprises ornon-equitycontractualmodessuchasfranchisingandlicensing.Nordås(2015)observesthatmanufacturersoften rely on franchises with services SMEs, such ascardealerships,petrolstations,pubsorhairdressers,todistributetheirgoods.

Barrierstoservicestradearevirtuallyallofaregulatorynature, but someare likely toaffectSMEsmore thanothers. A useful distinction in this sense is betweenmeasures thataffect firms’ability toenterorbecomeestablished in a foreign market (“establishment”measures), and those that have an impact on their

operations once they are present in that market(“operation” measures) (see WTO, 2012 for a fullerdiscussion). As the former usually designate fixedcosts, whereas the latter are more likely to implyvariable costs, it may be assumed that, for SMEs,“establishment” measures will be relatively moreburdensome(DeardorffandStern,2008).

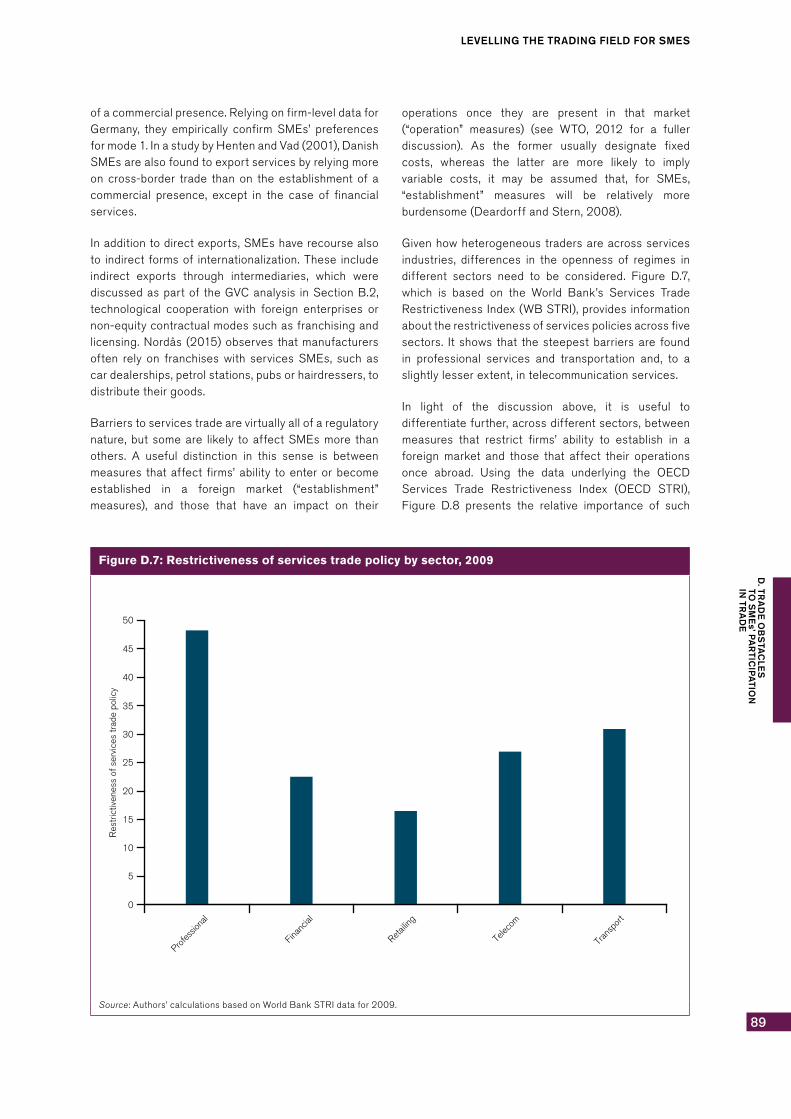

Givenhowheterogeneoustradersareacrossservicesindustries, differences in the openness of regimes indifferent sectors need to be considered. Figure D.7,which is based on the World Bank’s Services TradeRestrictivenessIndex(WBSTRI),providesinformationabouttherestrictivenessofservicespoliciesacrossfivesectors. It shows that thesteepestbarriersare foundin professional services and transportation and, to aslightlylesserextent,intelecommunicationservices.

In light of the discussion above, it is useful todifferentiatefurther,acrossdifferentsectors,betweenmeasures that restrict firms’ ability to establish in aforeign market and those that affect their operationsonce abroad. Using the data underlying the OECDServices Trade Restrictiveness Index (OECD STRI),Figure D.8 presents the relative importance of such

Figure D.7: Restrictiveness of services trade policy by sector, 2009

Res

tric

tiven

ess

of s

ervi

ces

trad

e po

licy

0

5

10

15

20

25

30

35

40

45

50

Profes

siona

l

Retailin

g

Financ

ial

Telec

om

Tran

spor

t

Source:Authors’calculationsbasedonWorldBankSTRIdatafor2009.

WORLD TRADE REPORT 2016

90

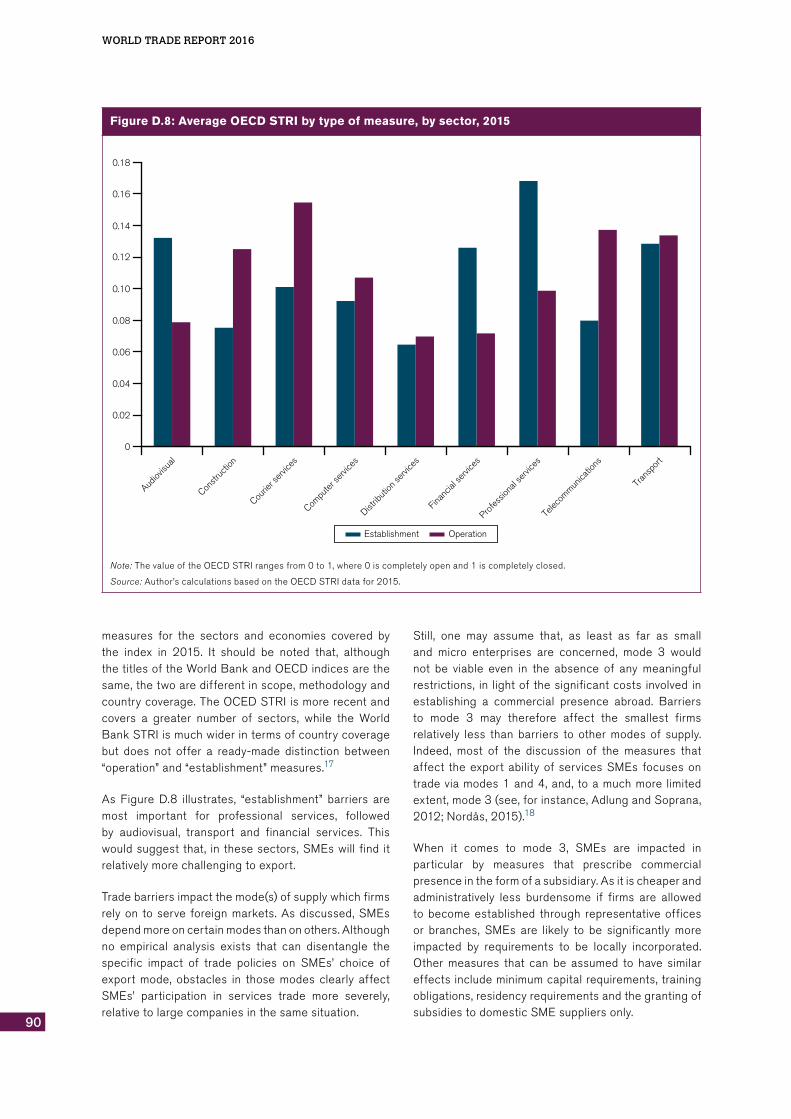

measures for the sectors and economies covered bythe index in 2015. It should be noted that, althoughthetitlesoftheWorldBankandOECDindicesarethesame,thetwoaredifferentinscope,methodologyandcountrycoverage.TheOCEDSTRIismorerecentandcovers a greater number of sectors, while the WorldBankSTRIismuchwiderintermsofcountrycoveragebut does not offer a ready-made distinction between“operation”and“establishment”measures.17

As Figure D.8 illustrates, “establishment” barriers aremost important for professional services, followedby audiovisual, transport and financial services. Thiswouldsuggestthat, inthesesectors,SMEswill find itrelativelymorechallengingtoexport.

Tradebarriersimpactthemode(s)ofsupplywhichfirmsrelyon toserve foreignmarkets.Asdiscussed,SMEsdependmoreoncertainmodesthanonothers.Althoughno empirical analysis exists that can disentangle thespecific impact of trade policies on SMEs’ choice ofexport mode, obstacles in those modes clearly affectSMEs’ participation in services trade more severely,relativetolargecompaniesinthesamesituation.

Still, one may assume that, as least as far as smalland micro enterprises are concerned, mode 3 wouldnot be viable even in the absence of any meaningfulrestrictions, in lightofthesignificantcosts involvedinestablishing a commercial presence abroad. Barriersto mode 3 may therefore affect the smallest firmsrelatively less than barriers to other modes of supply.Indeed, most of the discussion of the measures thataffect theexportabilityof servicesSMEs focusesontradeviamodes1and4,and, toamuchmore limitedextent,mode3(see,forinstance,AdlungandSoprana,2012;Nordås,2015).18

When it comes to mode 3, SMEs are impacted inparticular by measures that prescribe commercialpresenceintheformofasubsidiary.Asitischeaperandadministratively less burdensome if firms are allowedtobecomeestablished through representativeofficesor branches, SMEs are likely to be significantly moreimpacted by requirements to be locally incorporated.Other measures that can be assumed to have similareffectsincludeminimumcapitalrequirements,trainingobligations,residencyrequirementsandthegrantingofsubsidiestodomesticSMEsuppliersonly.

Figure D.8: Average OECD STRI by type of measure, by sector, 2015

0

0.02

0.04

0.06

0.08

0.10

0.12

0.14

0.16

0.18

Audiov

isual

Courie

r ser

vices

Constr

uctio

n

Distrib

ution

servi

ces

Compu

ter se

rvice

s

Financ

ial se

rvice

s

Profe

ssion

al se

rvice

s

Telec

ommun

icatio

ns

Tran

spor

t

Establishment Operation

Note:ThevalueoftheOECDSTRIrangesfrom0to1,where0iscompletelyopenand1iscompletelyclosed.

Source:Author’scalculationsbasedontheOECDSTRIdatafor2015.

91

D. TR

AD

E O

BS

TAC

LES

TO

SM

Es’ P

AR

TICIP

ATIO

N

IN TR

AD

ELEVELLING THE TRADING FIELD FOR SMES

The most relevant barriers, as far as mode 1 isconcerned, are measures requiring firms to establisha commercial presence in the host market in orderto supply cross-border services. Similarly, measuresimposing data localization requirements in foreignmarketsareboundtoimposeahigherburdenonSMEs.

Finally, barriers to mode 4 trade would appear to beof particular relevance for SMEs. For starters, themode 4 category of “independent professionals” (i.e.self-employed individuals supplying a service abroad)concerns SMEs by definition. As such, all barriers tothemovementof independentprofessionals imposeaburdenwholly, andsolely, onSMEs.This isespeciallycrucial when considering the relevance that mode 4is likely to have for exports from these “ultra-micro”enterprises, and in viewof thehigherprobability that,given their relatively more highly skilled workforce,smaller services firms may be contracted to supplyservicesinternationally.

Barriers applicable to the mode 4 category of“contractualservicesuppliers”canalsobeparticularlyburdensome for SMEs. Contractual service suppliersareemployeesofaservice firmwhoenter theexportmarketpursuanttoacontractconcludedbetweentheiremployerandalocalconsumer.Similarlytoindependentprofessionals,servicesexportedbycontractualservicesuppliers are not contingent on the establishment ofacommercialpresence,andare,therefore, lesscostlyto provide. Therefore, market access limitations suchas quotas or economic needs tests, as well as anyrelevant discriminatory measures such as residencyrequirements, non-eligibility under subsidy schemes,discriminatory tax treatment or obligations to traindomestic workers that are applicable to these twomode4categories,disproportionatelyaffectSMEs.

There are a number of other services measures that,althoughnottradebarriersperse(i.e.notfallingunderthe six measures that are defined as market accesslimitationsundertheGATSandnotviolatingtheGATSnationaltreatmentdisciplines),mayneverthelessrestricttrade opportunities for SMEs in particular. Amongstthesearelicensingandqualificationrequirementsandprocedures, and technical standards, to the extentthat these are particularly costly or administrativelycomplex to fulfil and, as such, significantly increasethefixedcostofenteringaforeignmarket.Itshouldbenoted,however,that,providedthatthesemeasuresarenon-discriminatory, theireffect isnotonly feltonlybyforeignSMEs,butalsobydomesticones.Byraisingthecost of serving the domestic market, such measuresdisproportionatelyaffectsmallfirmsofanyorigin.

Still,itistruethat,forthosefirmsthatexport,domesticregulatory measures are a cost to be borne in each

individual foreign market. SMEs are therefore lesslikely than larger firms to export to multiple markets,thuspotentiallyreducingtheextensivemarginoftrade.This seems tobe corroboratedbyempirical research.Lejárraga and Oberhofer (2013) and Lejárraga etal. (2014) find that SMEs’ export decisions are verypersistent, i.e. firms which enter a foreign market arelikelytocontinuetoexportservicestothatmarketovertheyears.Theirresearchalsoshowsthat,oncetheysellabroad, services SMEs tend to export a higher shareoftheirtotaloutputcomparedtolargerfirms.Assuch,theyaredisproportionallyaffectedbytrade-restrictingmeasures.

Lack of recognition of foreign work experience,education or qualifications is also likely to prove arelativelymoreburdensomehurdleforSMEswishingtoexportregulatedservices.Intheabsenceofrecognitionarrangements that “fast-track” the authorization tosupply a service in a foreign market, suppliers ofregulated services are required to embark in costlyand lengthy processes to demonstrate that they arequalified to supply the service in question. Again,supplierswillneedtosoforeverymarkettheywishtoenter. To the extent that firms have the resources tosetupacommercialpresenceabroad,theymayobviatethis obstacle by hiring locally qualified professionals,but this is likely to prove prohibitively expensive forSMEs.

Visaandworkpermitrequirementsandprocedurescanalsobeassumed to imposea relativelyhigherburdenonSMEs,inlightofthegreaterrelevancemode4hasfortheirexports.ThisislikelytobeespeciallytruefordevelopingcountrySMEs,astheiremployees(whoareusuallynationals)tendtobesubjectedtocomparativelymore stringent visa requirements, particularly sowhen they are seeking to access other developingcountrymarkets.19Theintroductionofprogrammestostreamlineentry formalities forbusinessesaccreditedas“premiumvisatraders”,i.e.usuallylargeconcerns,isalsolikelytoputSMEsatfurtherrelativedisadvantagecomparedtobiggerfirms.

3. Othermajortrade-relatedcosts

Thissectionfocusesonthosefirm-perceivedobstaclesto trade identified in Section D.1 that go beyond thestrict definition of trade policies (tariff, non-tariff andregulatory barriers discussed in Section D.2). Manyof the tradecostsdiscussed in thissectionare thosearising from the services needed to do trade, suchasdistributioncosts, transportationcostsandcost tofinance trading activity. In this respect, the analysishere differs from the discussion in Section D.2(d),whichdiscussedobstaclestotradeinservicesandnot

WORLD TRADE REPORT 2016

92

the costs related to the use of services necessary tothetradingactivity.

(a) Informationanddistributionchannels

Beyondmarketaccessandregulatorybarriersforgoodsand services, additional trade costs that are higherfor SMEs can be identified in relation to informationand distribution channels. There are intermediarycompanies,besidesproducersandconsumersofgoodsandservices,whichparticipateincreatingthestructureof a distribution network, with a specific function tofulfil.Distributionchannelscan,therefore,takevariousforms:(i)directsalesofproducerstoclients;(ii)salesthrough a retailer; (iii) sales through wholesaler(s)and retailer, or (iv) sales using an agent working ona commission basis (who can eventually bridge gapsbetween producers and wholesalers/retailers orclients).Therearealsosome important functions thatsupportanefficientdistributionnetworkwhichmayormaynotbefulfilledbytheseintermediaries,e.g.marketanalysis, advertising, transport/logisticsorafter-salesservices.

ForSMEs,havingaccesstodistributionnetworksmaybe a crucial component to develop their business, inparticular for diversifying their customers within aregionorworldwide.AsshowninSectionD.1,reachingclients in other economies may be challengingfor SMEs without access to relevant distributionchannels and related functions. This is reflected inthe high proportion of responses citing trade-relatedimpediments for SMEs in Figure D.1 (“Unable to findforeignpartners”and“Transportation/shippingcosts”)forthegoodstrade.Forservices,thiscantoacertainextentbeillustratedbythenumberofresponsesciting“Difficultyestablishingaffiliates inforeignmarkets” inFigureD.2,whichreflectstheneed inmanycasesforproximity with the client given the intangibility of theproducts being traded and, in some instances, adaptto the culture/language of the destination market.Access to information by potential SME exporters ondistribution channels and destination markets can,therefore,alsoberelatedtoallthatisdescribedabove.

ItemsinthedistributionchannelthatcanbeidentifiedashurdlesforSMEexportersare:havingandchoosinggoods or services fit for the export market, whethertargeting specific countries, regions or worldwide;making their products known to potential clients;deliveryofproductsandassociatedrisks(e.g.transportand physical delivery of goods and services; onlinedelivery of products, ensuring that eventual propertyrightsarenotatthreat).Inthatcontext,itisimportanttonotethatsomeintermediaries,suchasthoseengagedine-commerce,maythemselvesbeSMEs. Inaddition,SMEexportersalsoneedtofacethecostofgathering

market information, as well as access to regulatoryinformationinexportdestinations.

Afirmthatwantstoexportgoodsorservicesneedstoknow about the regulations in the economy to whichit intendstoexport(forexample,technicalregulationsabout the characteristics that a product needs tomeet, rules and regulations relating to trade). Thatfirmalsoneedsinformationaboutexportopportunitiesin the destination market. Lack of knowledge aboutregulations could result in the product not complyingwith the importing country regulations, which, in turn,couldcausethefirmtofacethecostsoftheproduct’srejection at the border of the target country. Lack ofknowledge about the demand in the export marketmay also induce profit losses. Gathering informationiscostly.AndersonandvanWincoop (2004)estimatethatapproximately6percentoftotaltradebarriersareinformationcosts.Thesearebroadlydefinedtoincludeinformation flows generated by migration networksRauchandTrindade(2002),volumeoftelephonetrafficand number of branches of the importing country’sbankslocatedintheexportingcountry.

Gatheringinformationisacrucialfactorindeterminingexport decisions, but it bears a cost. This cost is toa large extent independent of how much a firm willexport. Therefore, it is a cost that affects especiallysmall firms that are less capable than large firms ofspreading information costs across output. A recentsurvey by the Conférence permanente des chambresconsulaires africaines et francophones (CPCCAF),asking “When exporting, what are the main types ofinformation you need?”, shows that trade contactsand business opportunities are the most significantinformation barrier faced by small firms in Africa,followedbyinformationonrelevantregulations,andonexportsupportmeasures(seeTableD.3).

Delivery and logistical aspects are also an issue intrade, in particular for SMEs, whether as producersor intermediaries. SMEs often have to rely onexisting solutions to have their products deliveredto clients. These include services offered by postalsystems, express delivery services, cloud services, or

Table D.3: Main information barriers faced by SMEs in Africa

Information on Average %

Tradecontactsandbusinessopportunities 69

Relevantregulations 41

Exportsupportmeasures 41

Targetmarkets 34

Others 2

Source:AdaptedfromWTOandITC(2014),basedonCPCCAFsurveydata.

93

D. TR

AD

E O

BS

TAC

LES

TO

SM

Es’ P

AR

TICIP

ATIO

N

IN TR

AD

ELEVELLING THE TRADING FIELD FOR SMES

downloadingplatformsthroughlicensingarrangements.Forthisreason,itisimportanttoensurethataneffectivesolution is chosen. Alternatively, SMEs may decide tobecreative.Forexample, ine-commerce“while largerbusinessesliketheonlineretailerOzon.rumaychooseto build their own distribution networks, this option isoutof reach formicroandsmall businesses thatmayneed to explore other innovative solutions, e.g. themotorbike delivery system used in Viet Nam. Out-of-home delivery – involving collection points, deliveryat work, parcel lockers and in-store pickup – is oneoptiontoincreasetheattractivenessofe-commerceindevelopingcountries”(UNCTAD,2015).

Thesupportofintermediariesinadistributionchannelis most often used by companies that cannot sellproducts by themselves. Although direct contact withclientshelpstoestablishprices,theparticipationofanintermediaryensuresthattheproductwillbeprovidedmoreefficientlybymeansof theirnetworks,contacts,experience,specializationor lowercostsborneby theintermediary. For example, some intermediaries holddirectories of potential clients and/or (specialized)distributionfirms,conductin-countrymarketresearch,help to address language barriers (e.g. via translationservices),orofferassistancefortravelarrangementsorfollow-upsupport.ForSMEs,directcontactwithclientshastraditionallybeenseenasmoreeffectivethanuseof intermediaries in the distribution channel, and thisis particularly true for services, with which exclusivedistributionstrategies,asingleproduct,clearlydefinedclientsandepisodicsalesaretherule.Whenitcomesto exporting its products, this “direct” model may bemore difficult to implement for SMEs, in particular ifthey want to reach a wider set of clients. For SMEs,using go-between services reduces the portion oftasksthattheywoulddothemselvesiftheydecidednottousesuchintermediaries.20Italsoreducespartoftheassociated risksorclients’ fears,byprovidingadvice/interactivity, trust with payments, or the perceptionthat purchases are not so complex. In addition, usingintermediariesmaybealightersolutionforSMEsthanestablishingaffiliatesinservices(oreventuallygoods)export markets, unless the size of business is bigenoughtojustifysuchanestablishment.

In the context of distribution networks, marketingthrough the Internet (e.g. through the use of searchengines) or email, social networking platforms (e.g.Facebook) and e-commerce have had an importantrole inrecentyears.Whetherusingthedirectchannel(i.e. direct sales of producers to clients) or indirectmeans (i.e. intermediaries), these distribution networkinstruments have enabled a greater participation ofSMEs in international tradeby increasing thevisibilityof their products and allowing the establishment oflinks with clients in potential overseas markets (see

SectionD.4below).Theyhavealsohelpedenterprises,inparticularSMEs,toobtaininformationmoreeasilyonforeignmarkets(e.g.analyticalsolutionssuchasthoseofferedbysearchenginesore-commercecompanies),aswellastoaccessinformationonregulatorymattersorstandards.Finally, thesedistributionnetworkshaveassisted SMEs to obtain information on the networkitself,tounderstandhowbesttheycanapproachclients(i.e. via the ideal agent/dealer/distributor, paymentsystems, marketing resources, shipping and receivinglogistics,etc.).

(b) Transportandlogistics

Trade logistics goes beyond shipping goods acrossborders; it covers a wide range of services fromthe pick-up of goods, consolidation of shipment,procurement of transportation, customs clearance,warehousinganddistribution, to thedeliveryofgoodsto final consumers. SMEs often lack internationalfreight shipment experiences, and their cargos areusuallysmallerandofmoreirregularfrequency.SMEs’importsandexportsthereforerelyonservicesprovidedbylogisticsproviders.

Compared tobig firms,SMEs faceparticular logisticschallengesarising fromhigher logisticscostsand theinabilityofaccessingefficientlogisticsservices,whicharetwosidesofthesamecoin.This isevenmorethecase for SMEs in developing countries, due to poorlogistics infrastructure and underdeveloped logisticsmarkets. The World Bank Logistics PerformanceIndex consistently shows that logistics costs in low-performance countries (mainly developing countries)arehigherthaninhigh-performancecountries(mainlydeveloped countries). Logistics challenges constitutean important impediment to SMEs’ participation intrade.

SMEstradesmallerquantitiesthanbigenterprisesdo.This implies that fixed trade costs, including logisticscosts, oftenmakeupagreater shareof theunit costof their goods when compared to rivals exportinglarger volumes. In other words, logistics tend to costmoreforSMEsthanforlargeenterprises.Forexample,in Latin America, domestic logistics costs, includingstockmanagement,storage,transportanddistribution,canadduptomorethan42percentoftotalsalesforSMEs,ascompared to15-18percent for large firms.InNicaragua, logisticscostsforsmallbeefproducers,fromfarmtoabattoir,aremorethandoubleofwhattheyareforlargeproducers.Forasmallexportertomoveakilogramme of tomatoes from a Costa Rican farm tothefinalpointofsaleinManagua,Nicaragua,transportrepresentsthemaincost,atalmostaquarterofthetotalcost (23per cent), followedbycustoms (11per cent)andtaxes(6percent).Incontrast,forlargeexporters,

WORLD TRADE REPORT 2016

94

themaincostsarecustoms(10percent), followedbytransport (6 per cent) and taxes (5 per cent) (OECD,2014).Hence,reducinglogisticscostsiscrucialfortheimprovementofSMEs’tradeopportunities.

Geographical distance clearly affects SMEs’participationonexport.Evidenceshowsthat,comparedto large firms, SMEs are discouraged from enteringdistant markets. For instance, research conductedon French firms indicates that small firms export onaverage 3.7 per cent less to export destinations thatare 10 per cent further away from France. For thoseSMEs exporting to distant markets, the averageshipmentsperproductandperfirmaregreaterinordertoovercomethetransportationcosts.

AccordingtoastudyundertakenbytheUSITC(USITC,2014), the low reliability and high costs of shippingrepresent significant barriers for US-based SMEs’exporting to the European Union. Cost and reliabilityproblemsofEUpostalsystemshaveforcedcompaniestouseprivatecouriersforshipping,whichresultsinhighercosts that are harder for small businesses to absorb.ShippingcostsarealsoamajorobstacleforEUSMEs’exports to theUnitedStates, “becauseof thedistancetotheUSmarket,businessownersareconcernedthatthecostoftransportationwillincreasethepriceoftheirproducts toapointwheretheycanno longercompetewithproductsmanufacturedlocally”(UPS,2014).

In order to reduce logistics costs, firms (especiallybig manufacturers or big retailers) tend to outsourcelogistics functions (transport, warehousing, inventorymanagement, freight forwarding, etc.) to specializedproviders, i.e.providersof “third-party logistics” (3PL).“Outsourcing in logistics is a sign of strong logisticsperformance and of a mature logistics market, andis often a direct marker of logistics sophistication”(World Bank, 2014). Partnerships with 3PL providersnot only allow firms to focus on their core business;it also means access to advanced logistics servicesand supply chain management. Advanced logisticsservices are ICT-intensive and adapt quickly to newtechnologies, which often require the integration ofsupply chain management platforms with customers’internal systems. Due to resource constraints, SMEsoftenlagbehindinadaptingtotechnologicaladvancesandarereluctanttotapintothe3PLmarket.ThesmallsizeoftheirbusinessesisalsoadisadvantageforSMEswishingtonegotiateaffordablecontractswith3PL.21

SMEs face disproportionally high logistics costs(Straube et al., 2013). For manufacturing firms withless than 250 employees, on average their logisticscostsaccountfor14.7percentoftheiroverallrevenue.Conversely, firms with more than 1,000 employeesstate that the logisticscostsonlyaccount for6.7per

centoftheirtotalrevenue.Thisfigureissimilarforfirmswith250to1,000workers,whichreportthat logisticscosts account for 6.4 per cent of their total revenue.The research includes 113 industrial firms across theworld,andthebreak-upfiguresonregionalornationallevelsaffirmtheabovefindings.Forexample,inChina,SMEs reported spending 15 per cent of their overallrevenueon logisticscosts,whereas large firms (morethan 1,000 workers) reported spending only 5.2 percent.InSouthAmerica,SMEsreportedspending15.3per cent of overall revenue and large firms reportedspending9.4percent(OECDandWorldBank,2015).

(c) Financingdifficulties

Internationalactivitiesaremoredependentonexternalcapital than domestic activities. Moreover, creditconstraintsareparticularlyreflectedinaccesstotradefinance. This subsection discusses access to financeforfirmsthatareinvolvedintrade,withafocusontradefinanceinthesecondpart.

(i) Accesstofinance

Selling to foreign markets involves specific fixed andvariablecosts:developingmarketingchannels,adaptingproductsandpackagingtoforeigntastes,andlearningtodealwithnewbureaucraticprocedures.Thetimelagfromproductiontotherealizationofthecorrespondingrevenues is longer for international than for domesticsales.Moreover,internationalsalescontractsaremorecomplex, more risky and less enforceable, thus oftenrequiringsomeformsofexternalcredit insurance.Forall these reasons, exporters are more likely to needexternalcredit.

Lackof,orinsufficientaccessto,financecanstronglyinhibitformalSMEdevelopment,regardlessofthelevelof per capita income of countries. Lending to SMEs,especiallyforlongermaturitydates,isofteninhibitedbyinformationalproblemsandtransactioncosts,includingthe absence of records of firm’s past performance(requiredwhenrequestingaloan),lackofcollateral,andhigh fixedcostsof financial transactions, all ofwhichoften translate into higher lending costs and greaterrisksforfinancialinstitutions,andhencehigherinterestratesandfeesforSMEsthanfor largerfirms. Indeed,recent research found that market failures, notablyin financial markets (due to either financial crisesor “information asymmetries”), fall disproportionallyon SMEs, resulting in more credit rationing, higher“screening”costsandhigherinterestratesfrombanksthan for larger enterprises (Stiglitz and Weiss, 1981;BeckandDemirguc-Kunt,2006).

Financial exclusion, by forcing small firms to relyexclusively on their own resources to meet their

95

D. TR

AD

E O

BS

TAC

LES

TO

SM

Es’ P

AR

TICIP

ATIO

N

IN TR

AD

ELEVELLING THE TRADING FIELD FOR SMES

financial needs, reduces economic opportunity. Becket al. (2008) find that small firms use less externalfinance, especially bank finance. SMEs rely more ontrade credit and informal sources and less on equityandformaldebtthanlargefirms.Availabilityofexternalfinance is positively associated with the number ofstart-ups–animportantindicatorofentrepreneurship– as well as with firm dynamism and innovation; andallowsexistingfirms toexploitgrowthand investmentopportunities,andtoachievelargerequilibriumsize.

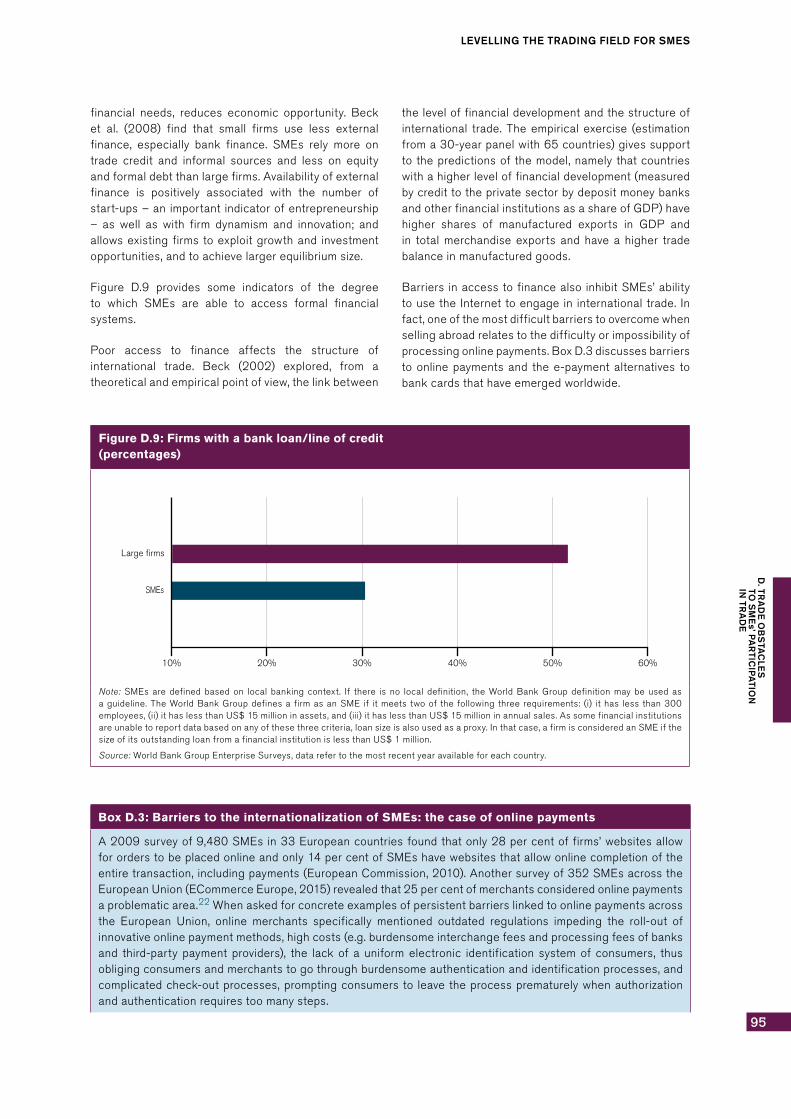

Figure D.9 provides some indicators of the degreeto which SMEs are able to access formal financialsystems.

Poor access to finance affects the structure ofinternational trade. Beck (2002) explored, from atheoreticalandempiricalpointofview,thelinkbetween

theleveloffinancialdevelopmentandthestructureofinternational trade. Theempirical exercise (estimationfroma30-yearpanelwith65countries)givessupportto thepredictionsof themodel,namely thatcountrieswithahigherleveloffinancialdevelopment(measuredbycredittotheprivatesectorbydepositmoneybanksandotherfinancialinstitutionsasashareofGDP)havehigher shares of manufactured exports in GDP andin total merchandise exports and have a higher tradebalanceinmanufacturedgoods.

Barriers inaccesstofinancealso inhibitSMEs’abilitytousetheInternettoengagein internationaltrade. Infact,oneofthemostdifficultbarrierstoovercomewhensellingabroadrelatestothedifficultyorimpossibilityofprocessingonlinepayments.BoxD.3discussesbarrierstoonlinepaymentsand thee-paymentalternatives tobankcardsthathaveemergedworldwide.

Figure D.9: Firms with a bank loan/line of credit (percentages)

Large firms

SMEs

10% 20% 30% 40% 50% 60%

Note: SMEs are defined based on local banking context. If there is no local definition, the World Bank Group definition may be used asaguideline.TheWorldBankGroupdefinesa firmasanSME if itmeets twoof the following three requirements: (i) ithas less than300employees,(ii)ithaslessthanUS$15millioninassets,and(iii)ithaslessthanUS$15millioninannualsales.Assomefinancialinstitutionsareunabletoreportdatabasedonanyofthesethreecriteria,loansizeisalsousedasaproxy.Inthatcase,afirmisconsideredanSMEifthesizeofitsoutstandingloanfromafinancialinstitutionislessthanUS$1million.

Source:WorldBankGroupEnterpriseSurveys,datarefertothemostrecentyearavailableforeachcountry.

Box D.3: Barriers to the internationalization of SMEs: the case of online payments

A2009surveyof9,480SMEsin33Europeancountriesfoundthatonly28percentoffirms’websitesallowfororderstobeplacedonlineandonly14percentofSMEshavewebsitesthatallowonlinecompletionoftheentiretransaction,includingpayments(EuropeanCommission,2010).Anothersurveyof352SMEsacrosstheEuropeanUnion(ECommerceEurope,2015)revealedthat25percentofmerchantsconsideredonlinepaymentsaproblematicarea.22Whenaskedforconcreteexamplesofpersistentbarrierslinkedtoonlinepaymentsacrossthe European Union, online merchants specifically mentioned outdated regulations impeding the roll-out ofinnovativeonlinepaymentmethods,highcosts(e.g.burdensomeinterchangefeesandprocessingfeesofbanksand third-party payment providers), the lack of a uniform electronic identification system of consumers, thusobligingconsumersandmerchantstogothroughburdensomeauthenticationandidentificationprocesses,andcomplicatedcheck-outprocesses,promptingconsumersto leavetheprocessprematurelywhenauthorizationandauthenticationrequirestoomanysteps.

WORLD TRADE REPORT 2016

96

(ii) Tradefinance

Difficulty inaccessingaffordable tradefinance isoneof the most cited constraints for SMEs engaging ininternational trade,affectingsmallbusinesses inbothdevelopedanddevelopingcountries.

Regardingdevelopedcountries,the2010USITCsurvey,covering2,350SMEsand850 largefirms,concludedthat32percentofSMEsinthemanufacturingsectorand46percentofSMEsinservicessectorsconsideredtheprocessofobtainingfinanceforconductingcross-border trade “burdensome”. Only 10per cent of largefirmsintheUSmanufacturingsectorand17percentintheservicessectorexperiencedthesamedifficulties.

TheUSITCstudyalsorevealedthat,forSMEslookingto start exporting or expanding into new markets,the lack of access to credit was the number oneconstraint for manufactured firms, and number threefor services firms, out of 19 constraints listed in thesurvey.Sectorswhichgenerallyshowsignificantlevelsof creditworthiness and collateral (such as transportequipment, information technology and professionalservices) considered that securing trade finance wasas“acute”aproblemforthemasforothersectors.

Finally, the survey highlights that while US banksconsidered the SME market segment as having alarge potential for profitability, SMEs were not theirpreferredborrowersinviewofthehighertransactionalandinformationalcostsofdealingwithsuchcompanies(relative to larger corporations). In turn, US-basedSMEs complained about bank’s “excessive” oversight,failuretomeettheirspecificborrowingneeds,andlackofflexibilityregardingtheuseofalternativesourcesoffinance,ratherthantheproposedones.

One may also mention the OECD-APEC study onRemoving Barriers to SME Access to InternationalMarkets,surveyingSMEs’perceptionofthebarrierstotheir internationalization (OECD, 2008). The shortageofworkingcapital tofinanceexports is rankedasthenumber one constraint to the internationalization ofSMEs. Surveys and studies found similar results inEuropeandJapan.Inastudycoveringdataon50,000Frenchexporters,itwasfoundthat,duringthefinancialcrisis of 2008-09, credit constraints on smallerexportersweremuchhigherthanonlargerfirms,tothepointofreducingtherangeofdestinationforbusinessor of leading the SME to stop exporting altogether(Bricongne et al., 2012). It was found that in Japan,SMEsarealsomorelikelytobeassociatedwithtroubledbanks,andhenceexportingSMEsareasaresultmorevulnerable in periods of financial crises (Amiti andWeinstein, 2011). In general, credit-constrained firms,mostly likely to be found among SMEs, are also lesslikelytoexport(Belloneetal.,2010;Manova,2013).

Accesstotradefinancetendstobethemostdifficultin developing countries. Part of the problem lies withthefactthat localbanksmaylackthecapacity,know-how,regulatoryenvironment,internationalnetworkandforeign currency to supply import and export-relatedfinance. Equally, traders may not know the productsavailabletothem,orhowtousethemefficiently.Banksinsomedevelopingcountriesmaybemorerisk-averse,inviewoftheirsmallercapitalbaseandabilitytohandleinternationaltrade-relatedcreditrisk.

AccordingtoarecentstudybytheAsianDevelopmentBank(ADB,2014),smallandmedium-sizedenterprises(SMEs)arethemostcredit-constrained;itisestimatedthat half of their requests for trade finance arerejected,comparedtoonly7percentformultinational

Box D.3: Barriers to the internationalization of SMEs: the case of online payments (continued)

The situation is not different in other regions. For example, the vast majority of payments for online retail inASEAN countries are still made offline, in methods such as cash-on-delivery. A survey conducted in 2013foundthatonly2to11percentofdigitalbuyersuseonlinepaymentsinASEANcountries,withtheexceptionofSingapore,where,accordingtotheCIMBASEANResearchInstitute(CARI,2015),therateofonlinepaymentusestandsat50percent.Financialexclusion(i.e.concerningthelarge“unbanked”population),concernsaboutdatasecurityandburdensomeknow-your-customerprocessesareusuallycitedastherootcausesofdeficientonlinepaymentpenetration.

Many e-payment alternatives to bank cards have emerged worldwide and are now widely, although not yetuniversally, accessible to Internet users, such as PayPal, Amazon Payments, and Alipay (CARI, 2015). Mobilebanking,i.e.theuseofmobilephonestosendandreceivepaymentsandconductotherbankingtransactions,hasbeensoaringthroughoutAfrica.KenyaisattheforefrontofAfrica’smobilemoneymarket,duetothesuccessofM-PESA,amobilebankingsystemlaunchedin2007bythecountry’sleadingmobileserviceprovider,Safaricom.Mobilebankingisevenacquiringacross-borderdimension.Lastyear,forexample,Vodafone(Safaricom’slargestshareholder)launchedM-PESAservicesbetweenKenyaandTanzania.Cross-bordermobilesolutionslikethisonemightcontributetofinancialinclusionandprovidealow-costoptionforSMEsengagingininternationaltrade.

97

D. TR

AD

E O

BS

TAC

LES

TO

SM

Es’ P

AR

TICIP

ATIO

N

IN TR

AD

ELEVELLING THE TRADING FIELD FOR SMES

corporations.With68percentofsurveyedcompaniesreporting that they did not seek alternatives forrejected transactions, trade finance gaps appear tobeexacerbatedbya lackofawarenessandfamiliarityamongcompanies–particularlysmallerones–aboutthemanytypesoftradefinanceproductsandinnovativeoptionswhichexistonthemarket(suchassupply-chainfinancing,bankpaymentobligationsand forfaiting).Alarge majority of firms stated that they would benefitfromgreaterfinancialeducation.