Colombia Power Sector Report

58

- 1 - Any redistribution of this information is strictly prohibited. Copyright © 2014 EMIS, all rights reserved. Produced by: Any redistribution of this information is strictly prohibited. Copyright © 2014 EMIS, all rights reserved. Power Sector Colombia May 2014

description

contains the details of power sector structure of colombia and the regulations applicable in colombia.

Transcript of Colombia Power Sector Report

- 1 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Produced by:

Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Power Sector Colombia

May 2014

- 2 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Table of Contents

I. Sector Overview

1. Sector Highlights

2. Main Sector Indicators

3. Power Sector Forecast

4. Electricity Demand, Capacity Forecast

5. Natural Gas Demand Forecast

6. Energy System Balance

7. Power Sector Snapshot

8. Power Sector Snapshot (cont´d)

9. FDI

10.CPI and PPI

11.Government Policy

12.Government Policy (cont'd)

II. Power Generation Overview

1. Power Generation Highlights

2. Power Generation Demand

3. Electricity Input and Water Reserves

4. Electricity Generation

5. Electricity Demand and Consumption

6. Other Energy Indicators

III. Power Generation by Type of Fuel

1. Fuel Consumption

2. Coal Mining

3. Coal Mining (cont´d)

4. Gas Generation

5. Gas Generation (cont´d)

6. Hydropower Generation

7. Hydropower Reserves

8. Renewable Energy

9. Small Power Plants

10.Power Generation SWOT Analysis

11.Power Transmission and Distribution

IV. Power Exports

1. Energy Exports

2. Power Foreign Trade

3. Power Exchange and Trading

4. Power Exchange and Trading (cont´d)

V. Natural Gas Distribution

1. PNG in Colombia

2. Natural Gas Coverage

3. Car Fuel

- 3 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Table of Contents

VI. Main Players

1. Ecopetrol S.A.

2. Ecopetrol S.A. (cont´d)

3. Interconexión Eléctrica S.A.

4. Interconexión Eléctrica S.A. (cont´d)

5. Codensa S.A. E.S.P

6. Codensa S.A. E.S.P (cont´d)

7. Empresas Publicas de Medellin E.S.P

8. Empresas Publicas de Medellin E.S.P (cont´d)

9. Emgesa S.A. E.S.P.

10.Emgesa S.A. E.S.P. (cont´d)

- 4 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

I. Sector Overview

- 5 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Power Sector Highlights

Colombia's power supply chain is fed by generation plants with a combined net installed capacity of 14,555 MW, of which 63.7% comes from

hydropower plants, 31.5% - from thermal power plants, 4.4% - from small power plants and 0.4% - from cogeneration units. The domestic utilities

fully cover local demand, which reached 9,956.02 MW in 2013. The government projects a domestic demand of 13,070 MW in 2019, a growth trend

that has turned the construction of new infrastructure and the strengthening of the supply chain into a national priority.

System Capacity

Exports

Forecast

Diversification

According to the government's mining and planning unit UPME, Colombia is a net exporter of electricity, with a total of 57.8 GWh in exports during

2013, which 89% was exported to Venezuela and the remainder to Ecuador. During same period, Colombia used imports from neighbouring

Ecuador to cover 0.1% of its consumption.

The 2013-2027 electricity strategy of UPME is designed to boost the power sector capacity and encourage investments in the energy sector in order to satisfy the growing electricity demand. According to the government, Colombia's overall power generation during the period will increase by an annual average of 3.4% to 76.0 TWh with an average annual growth of 3.6% in hydroelectric power generation, while coal and gas-fired generation are forecast to increase by an annual average of 2.9% and 2.7%, respectively.

Hydroelectric power accounts for 75% of the total consumption in Colombia, despite the problems associated with this source of energy such as

protests at construction sites and a risk of guerrilla attacks. In a bid to diversify and attract foreign investments, the government has decided to sell

a 57.6% stake in the nation's third-biggest electricity generator Isagen. The government is seeking USD 2.5 billion for its stake and plans to invest

the proceeds from the sale into electricity infrastructure. Isagen owns and operates six electricity generators in the provinces of Antioquia,

Santander, Caldas and Tolima.

- 6 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

Comments

Main Sector Indicators

In 2013, the revenues from power generation in Colombia grew at a slightly faster pace in comparison to 2011 and 2012. The total growth rate for the sector

was 4.9% - electric power grew by 4.0%, utility gas by 14.4% and growth on the added value of water supply, sewerage and waste reached 3.8%. This

growth was fuelled by rising consumption from both private and household users. The strong growth of Colombia's economy also contributed to the positive

trend, especially with the rise in electricity consumption by public companies and civil works.

Main Sector Indicators

National Administrative Department of Statistics

2005 2006 2007 2008 2009 2010 2011 2012 2013

Electricity revenues, COP tn 8.5 8.8 9.2 9.3 9.4 9.8 10.1 10.3 10.7

Electricity growth y/y 4.7% 4.3% 3.8% 1.5% 0.8% 4.5% 3.3% 2.0% 4.0%

Utility gas revenues, COP tn 1.2 1.3 1.4 1.3 1.5 1.6 1.7 1.7 2.0

Utility gas growth y/y 4.7% 5% 10% -7,4% 11% 6.5% -1% 1.4% 14.4%

Water supply revenues, COP tn 4.0 4.2 4.3 4.4 4.4 4.5 4.6 4.7 4.8

Water supply growth y/y 2.8 5.7 2.7 1.4 0.3 1.5 2.6 2.1 3.8

Electricity revenues/GDP 2.5% 2.6% 2.7% 2.7% 2.8% 2.9% 3.0% 2.9% 2.1%

Utility Gas revenues/GDP 0.4% 0.4% 0.4% 0.4% 0.4% 0.5% 0.36% 0.36% 0.4%

Water supply revenues/GDP 0.8% 0.8% 0.8% 0.9% 0.9% 0.9% 0.9% 1% 1%

GDP growth y/y 4.7% 6.7% 6.9% 3.5% 1.7% 4.0% 6.6% 4.0% 4.3%

GDP real value, COP tn 340.2 362.9 388.0 401.7 408.4 424.6 452.8 470.9 490.9

Power sector growth y/y 3.8% 3.8% 2.5% 1.4% 2.9% 1.6% 2.4% 3.8% 4.9%

*Colombian currency in constant price 2005 = 100

- 7 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

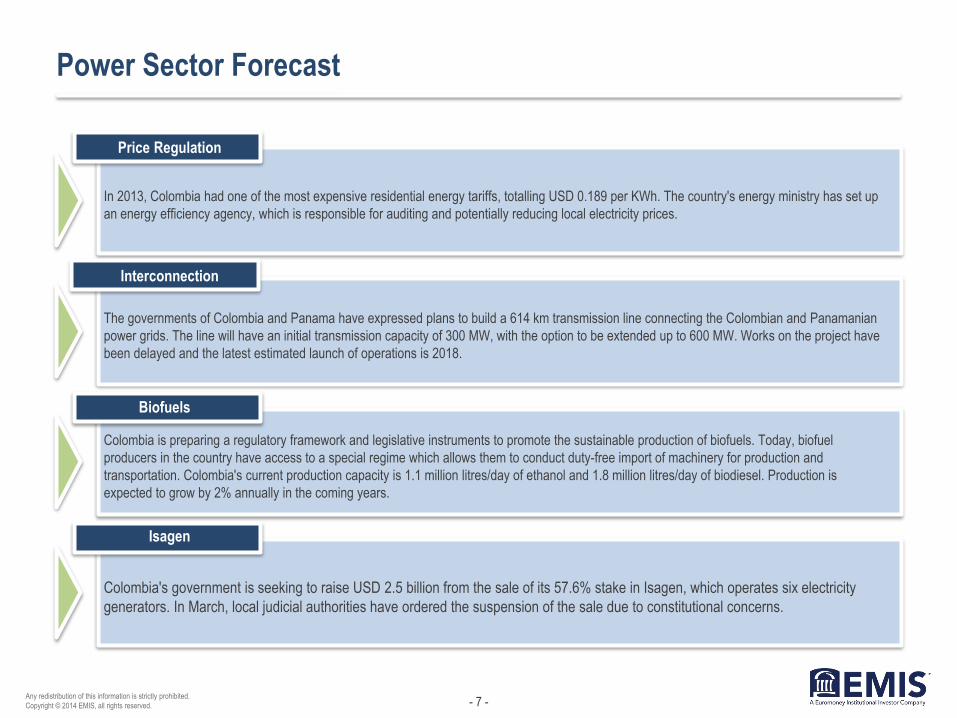

Power Sector Forecast

In 2013, Colombia had one of the most expensive residential energy tariffs, totalling USD 0.189 per KWh. The country's energy ministry has set up

an energy efficiency agency, which is responsible for auditing and potentially reducing local electricity prices.

Price Regulation

Biofuels

The governments of Colombia and Panama have expressed plans to build a 614 km transmission line connecting the Colombian and Panamanian

power grids. The line will have an initial transmission capacity of 300 MW, with the option to be extended up to 600 MW. Works on the project have

been delayed and the latest estimated launch of operations is 2018.

Colombia is preparing a regulatory framework and legislative instruments to promote the sustainable production of biofuels. Today, biofuel

producers in the country have access to a special regime which allows them to conduct duty-free import of machinery for production and

transportation. Colombia's current production capacity is 1.1 million litres/day of ethanol and 1.8 million litres/day of biodiesel. Production is

expected to grow by 2% annually in the coming years.

Colombia's government is seeking to raise USD 2.5 billion from the sale of its 57.6% stake in Isagen, which operates six electricity

generators. In March, local judicial authorities have ordered the suspension of the sale due to constitutional concerns.

Isagen

Interconnection

- 8 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

Electricity Demand, Capacity Forecast

Electricity National Demand (GWh) National Maximum Capacity (MW)

UPME

Year High Scenario Medium Scenario Low Scenario

2014f 65,000 63,481 61,963

2015f 67,070 65,526 63,983

2016f 69,704 68,134 66,563

2017f 71,773 70,172 68,572

2018f 74,668 73,034 71,401

2019f 77,613 75,944 74,276

2020f 79,708 78,002 76,296

2021f 81,531 79,786 78,040

2022f 83,297 81,510 79,723

2023f 84,654 82,825 82,995

2024f 86,524 84,650 82,776

2025f 88,448 86,529 84,610

2026f 90,308 88,342 86,375

2027f 92,279 90,265 88,250

Year High Scenario Medium Scenario Low Scenario

2014f 10,600 10,352 10,104

2015f 10,776 10,524 10,272

2016f 10,940 10,648 10,429

2017f 11,184 10,923 10,662

2018f 11,418 11,152 10,885

2019f 11,668 11,396 11,124

2020f 11,900 11,623 11,345

2021f 12,120 11,926 11,641

2022f 12,499 12,208 11,916

2023f 12,798 12,500 12,202

2024f 13,072 12,767 12,462

2025f 13,426 13,113 12,800

2026f 13,754 13,433 13,113

2027f 14,091 13,673 13,434

- 9 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

Natural Gas Demand Forecast

Natural Gas Demand by Sector Forecast, 2022

Natural Gas Demand by Industry (GBTUD)

Comments

Ministry of Mining and Energy, UPME

214 224 234 242 250 256 263

269 275 280 285 289

293

308 322 336

350 363 378 392 406 420 434 448

461 474

275 267

310

384

519

193 207 226 236 277

317 334 390

214

282 309

340 377

373

469 491 491 491 491 491 491

85 89 92 95 98 101 105 108 111 114 117 120 124

2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026

Domestic Industrial Electric Generation Oil Sector Automotive

Domestic 21.5%

Industrial 30.8%

Electric Generation

6.5%

Oil Sector 31.4%

Automotive 8.0%

Petrochemical 1.9%

Domestic natural gas demand is slowing due the fact that service

coverage has nearly reached its peak in 2013 with 6.8 million consumers,

of whom 98.14% are residential, 1.80% - commercial and 0.06% -

industrial consumers. A major increase in the electricity generation sector

is forecast for 2018 due to the expected launch of the transmission

network project between Colombia and Panama. Industry and the oil

sector will be the driving forces behind the forecast demand, as these

two sectors have the largest number of projects (especially in

infrastructure, construction and extraction).

- 10 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

Energy System Balance

National Power Transmission Network Indicators

XM Compañía de Expertos en Mercados S.A ESP

2012 2013 Growth

SUPPLY

Net Daily Volume (GWh) 11,180.61 10,495.05 -6.1%

Volume / Useful Capacity 73.4% 69.5% -4.0%

Hydropower Imput (GWh) 56,446.7 49,619.2 -12.1

Net Capacity 14,361 14,559 1.4%

GENERATION

Hydropower (GWh) 44,923.6 41,835.9 -6.9%

Thermal (GWh) 11,506.0 16,838.6 46.3%

Small Hydropower Plants (GWh) 3,212.6 3,170.0 -1.3%

Cogenerators (GWh) 346.6 352.0 1.5%

Total (GWh) 59,988.9 62,196.6 3.7%

INTERNATIONAL EXCHANGE

Exports to Ecuador (GWh) 236.0 662.3 180.6%

Imports from Ecuador (GWh) 6.5 28.5 337.8%

Exports to Venezulea (GWh) 478.4 715.0 49.4%

DEMAND

Commercial (GWh) 59,508.6 61,499.3 3.3%

National, handled by the national transmission company SIN

(GWh) 59,369.9 60,890.3 2.8%

Regulated (GWh) 39,174.7 40,282.0 3.1%

Unregulated (GWh) 19,799.9 20,237.4 2.5%

Unmet due to unavilability, natural disasters or terrorism

(GWh) 89.0 42.5 -52.2%

Maximum load per hour (MW) 9,504 9,383 -1.3%

- 11 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

Power Sector Snapshot

World energy consumption by region (quadrillion Btu)

World energy consumption by fuel type (mn tonnes )

World proved natural gas reserves 2013 (tn cub ft)

World Proved Natural Gas Reserves (tn cub ft)

U.S. Energy Information Administration, World Bank, Exxon-Mobil

120 121 126 130 133 137 144

129 132 138 146 152 158 162

199 235 273

306 335 363 383

28 33

37 39

43 46

49

19 20

22 24

27 31

35

29 31

33 35

39 42

47

0

100

200

300

400

500

600

700

800

900

2010 2015 2020 2025 2030 2035 2040

Central & South America

Africa

Middle East

Asia

Europe

Americas Coal 4,382.0

Oil 4,367.3

Natural Gas 3,685.9

Hydroelectricity 963.9

Nuclear Energy 704.3

Renewables 505.5

Biofuels 78.9

3,159 3,287 3,581

3,912 4,038 4,131 4,227 4,447

4,671 4,837 4,967

1,768 1,926 2,177

2,500 2,864 2,987

3,258 3,267

3,959 4,285

4,631

2,211 2,235 2,342

2,923

3,464 3,730 3,960

4,368 4,551

4,650 4,743

453 526 584 627 626 569 630

794 771 839 859 490 563 602 662 782 831 859 964 1,065 1,155 1,246

1990 1995 2000 2005 2010 2012 2015 2020 2025 2030 2035

Liquids Natural Gas

Coal Nuclear Energy

Hydroelectricity

2,824

2,178

515

504

358

269

146

Middle East

Eurasia

Africa

Asia

North America

Central & South America

Europe

- 12 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

Comments

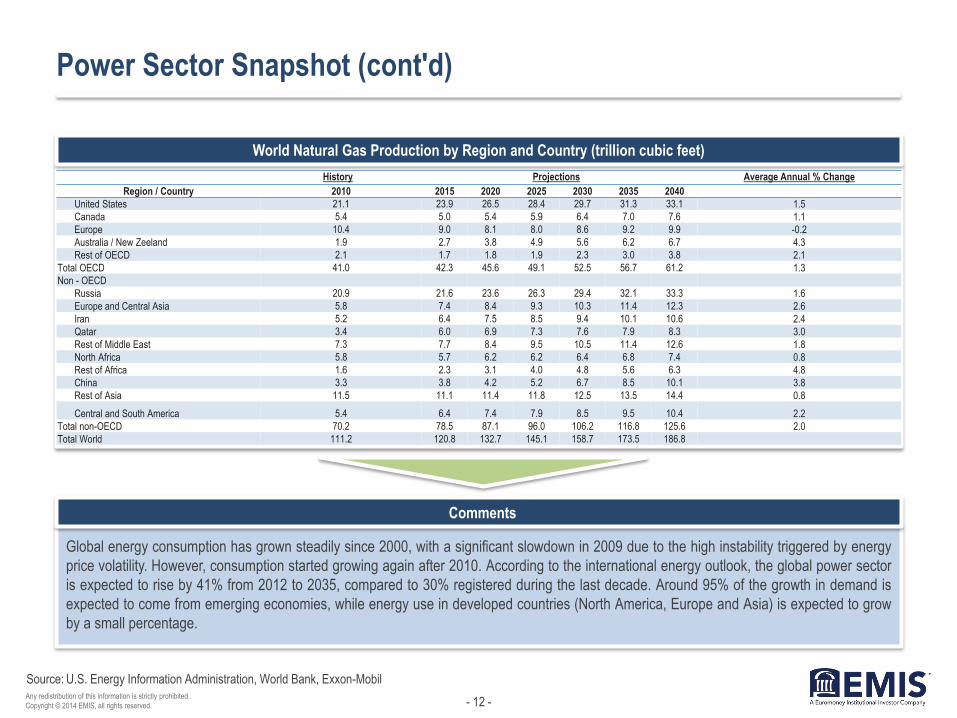

Power Sector Snapshot (cont'd)

Global energy consumption has grown steadily since 2000, with a significant slowdown in 2009 due to the high instability triggered by energy

price volatility. However, consumption started growing again after 2010. According to the international energy outlook, the global power sector

is expected to rise by 41% from 2012 to 2035, compared to 30% registered during the last decade. Around 95% of the growth in demand is

expected to come from emerging economies, while energy use in developed countries (North America, Europe and Asia) is expected to grow

by a small percentage.

World Natural Gas Production by Region and Country (trillion cubic feet)

U.S. Energy Information Administration, World Bank, Exxon-Mobil

History Projections Average Annual % Change

Region / Country 2010 2015 2020 2025 2030 2035 2040

United States 21.1 23.9 26.5 28.4 29.7 31.3 33.1 1.5

Canada 5.4 5.0 5.4 5.9 6.4 7.0 7.6 1.1

Europe 10.4 9.0 8.1 8.0 8.6 9.2 9.9 -0.2

Australia / New Zeeland 1.9 2.7 3.8 4.9 5.6 6.2 6.7 4.3

Rest of OECD 2.1 1.7 1.8 1.9 2.3 3.0 3.8 2.1

Total OECD 41.0 42.3 45.6 49.1 52.5 56.7 61.2 1.3

Non - OECD

Russia 20.9 21.6 23.6 26.3 29.4 32.1 33.3 1.6

Europe and Central Asia 5.8 7.4 8.4 9.3 10.3 11.4 12.3 2.6

Iran 5.2 6.4 7.5 8.5 9.4 10.1 10.6 2.4

Qatar 3.4 6.0 6.9 7.3 7.6 7.9 8.3 3.0

Rest of Middle East 7.3 7.7 8.4 9.5 10.5 11.4 12.6 1.8

North Africa 5.8 5.7 6.2 6.2 6.4 6.8 7.4 0.8

Rest of Africa 1.6 2.3 3.1 4.0 4.8 5.6 6.3 4.8

China 3.3 3.8 4.2 5.2 6.7 8.5 10.1 3.8

Rest of Asia 11.5 11.1 11.4 11.8 12.5 13.5 14.4 0.8

Central and South America 5.4 6.4 7.4 7.9 8.5 9.5 10.4 2.2

Total non-OECD 70.2 78.5 87.1 96.0 106.2 116.8 125.6 2.0

Total World 111.2 120.8 132.7 145.1 158.7 173.5 186.8

- 13 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Comments

Source:

FDI

Colombia attracted a record-high FDI of USD 16.7bn in 2013, which is equal to 4.5% of the country's GDP. In terms of sectors, 46.7% of the inflows went

into mining, 15.9% to manufacturing, 10.4% into transport and communications, 9.4% into financial institutions and 9.4% into commerce.

FDI in Electricity, Gas and Water (USDmn) FDI in Mining, Oil and Derivatives (USDmn)

Central bank

-71

135 68 88

-251 -141

-79

156

36 36

380

819

470

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

1,044 915 905

1,741

3,282 3,777

4,433

5,203 5,453

4,540

7,516 7,732 7,825

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

- 14 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

CPI and PPI

Consumer and Producer Price Index (COP)

Central bank

107.97 112.69

118.90

115.39 114.82

2%

3.17%

3.73%

2.44%

1.94%

2009 2010 2011 2012 2013

PPI CPI

- 15 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

Government Policy

Key Bodies

Ministry of Mining and Energy (MinMinas) – The ministry acts as a liaison between the central government and state utilities with both public and private ownership, as well acts as

leading regulator of the energy sector and implements sectorial policies.

Mining and Energy Panning Unit (UPME) - Its main function is to conduct the energy planning, advise and provide support for the implementation of the ministerial sector policies.

UPME is responsible for the development of the “Expansion Plan Reference Generation and Transmission” and is also responsible for the selection of the investors which will

undertake and contribute in the Expansion Plan project development .

Energy and Gas Regulatory Commission (CREG) – The commission is responsible for the regulatory aspects of the market; it also promotes competition and prevents abuse of

dominant position by companies.

Superintendence of Public Services (SSPD) – This body supervises and monitors the utilities, compliance with the law and the relevant regulations in terms of current contracts

between firms service provides and final consumers. JAIRO: It means this institution works based on the regulations, legislation, politics, etc.

The energy development plan for the period 2013-2027 aims to assure the adequate supply of electricity and also makes a projection for the sector development in the 15-year period.

Electricity

Market

Colombia has the Wholesale Energy Market (MEM), where power generation companies, as well as public, private and mixed

commercial traders, buy and sell energy in large blocks within a regulatory framework, established by CREG. There is a market for

short-term deals (Bolsa de Energía) where market players offer prices and availability of their energy stock through daily auctions.

Also, there is a market for long-term contracts under a financial scheme, where agents obtain coverage against the high volatility of

energy prices on the short-term market. The main operator and administrator of the energy market in Colombia is XM S.A. E.S.P., a

subsidiary of state-run energy company ISA.

Compensation

and Fee

Setting

In Colombia, there are two schemes for electric transmission assets remuneration. The first one applies for electric transmission

assets generated until 1999, this scheme pays to the carrier an annual fee as a compensation for the annual valuation of the electric

transmission assets; this fee is calculated under electric assets “Replacement Value to New” (VRN), where VRN is calculated using

the approved structural unit for each unit costs and a discount rate defined by the Energy and Gas Regulatory Commission (CREG).

The second one applies in the case of a Public Offer, where the remuneration consist in paid to the investor an annual fee due to his

investment in a transmission project. This fee corresponds to the investment in the power assets divided by the first 25 years of the

project operation. Remuneration offer is made in U.S. dollars as of December 31 prior to the project award and payments are updated

in an annual base under the Producer Price Index of the respective payment year.

Ministry of Mining and Energy, UPME, Energy and Gas Regulatory Commission

- 16 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Government Policy (cont'd)

Energy Market

Energy generation in Colombia is open to competition therefore prices are defined by the market. Generation agents carry out

their energy transactions on the stock energy market. Revenues from generation are derived from the sale of energy through

bilateral contracts to the regulated and unregulated markets, energy exchange, secondary frequency regulation service and

reliability charges. The Colombian generation system had a installed capacity of 14,559 MW at the end of 2013.

Energy

Transmission

The voltage of the national transmission network, operated by Empresa de Energia de Bogota (EEB), is equal to or greater

than 220kV. ISA and Transelca control 80% of the transmission network. This network consist of equipment of 220kv, 230kv

and 500kV. The planning of the transmission network and its new lines is developed by the UPME, most of the tender are

adjudicated for 25 years.

Energy

Distribution

The distribution of energy under 220kV is fully regulated. Colombia's energy regulator CREG defines and reviews the

distribution price component on a 5-year basis. The methodology differs depending on the voltage. In the case of level 4 it

corresponds to regulated revenue; for levels 3, 2, and 1, the methodology corresponds to a maximum price. The voltage levels

are as follows: Level 1 (1kV), Level 2 (1 to 30kV), Level 3 (30 to 57.5kV) and Level 4 (57.5 to 220kV).

Energy Trade

Trade can be carried out by the generators and distributors of electricity, or can be performed independently. The trader acts as

an intermediary between the final consumers and all the other agents along the chain (generation, transmission, distribution

companies and the market administrator). The international trade of energy is operated in two ways: the international

transactions system that is a spot market with Ecuador and the interconnections with Venezuela that are managed by ISA.

There are two interconnections of 230kV (Circuitos –Cuestecitas-Cuatricentenario and Corozo-San Mateo) The daily average

of exports has reached levels of 2.5GWh since 2008.

- 17 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

II. Power Generation Overview

- 18 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Power Generation Highlights

Power generation companies in Colombia had a difficult year in 2013 due to adverse weather conditions which resulted in volatile prices and

threatened the stability of the market. Hydropower was particularly affected by the bad weather. Meanwhile, electricity generator Celsia, a

subsidiary of holding firm Grupo Argos, posted better financial results through diversification of its sources (50% thermal and 50% hydropower) and

higher prices on the stock market.

Performance

Generation

Energy Supply

Fuel Consumption

The national transmission network transported 62,296.6 GWh of electricity in 2013. The effective capacity in 2013 was 14,559 MW up by 198 MW

compared to 2012 mainly due to the entry into operation of hydroelectric plants Amoya la Esperanza and Valencia Samper.

The generated power in 2013, together with the 28.5 GWh imported from Ecuador during the year, satisfied the 60,890.3 GWh in domestic

demand.

Fuel consumption by thermal power plants in Colombia rose by 42% in 2013. This growth was spurred by the 46% hike in thermal generation.

- 19 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Comments

Source:

Power Demand

Energy demand in 2013 increased by 2.8%, slightly lower than the 3.8 growth rate registered in 2012. This slowdown was largely due to lower

consumption by traditional consumers such as oil, coal and cement, as well as the fall in public orders. The unfavourable weather conditions,

which brought hydropower generation and reserves to their lowest levels since 2000, also resulted in highly volatile energy prices.

Demand (GWh) Installed Capacity by Technology Type (%)

National Administrative Department of Statistics, XM Compañía de Expertos en Mercados S.A ESP

47,

017

48,8

29

50,8

13

52,8

53

53,

870

54,

679

56,

148

57,

150

59,

370

60,

890

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Hydraulic 64.0%

Gas 13.5%

Coal 6.8%

Diesel 6.2% Small

Hydraulic 3.8%

Number 6 fuel oil 2.1%

Gas.Jett A1 1.8%

Small Thermal 0.5%

Cogenerators 0.5%

Jett1 0.3%

Wind 0.1%

- 20 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Comments

Source:

Electricity Imputs and Water Reserves

Due to adverse weather conditions, the cumulative energy contributions in 2013 fell by 9% from the previous year. The total hydropower reserves stored in

national reservoirs amounted to 10,495.1 GWh of electricity or 6.1% less than 2012.

Cumulative Energy Inputs vs Monthly Average Values Hydropower share in national power transmission network, December 2013

National Administrative Department of Statistics, XM Compañía de Expertos en Mercados S.A ESP

0

10,000

20,000

30,000

40,000

50,000

60,000

GWh Average Cumulative

GWh 2013 Cumulative

Antioquia Region 41.6%

Caribbean Region 1.5%

Central Region 25.6%

East Region 28.4%

Valle Region 2.8%

- 21 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Comments

Source:

Electricity Generation

Domestic power generation increased by 3.7% in 2013 to 62,196.6 GWh on the back of increased demand and exports to Venezuela and Ecuador.

Hydropower generation accounted for 67.3% of the total, compared to 74.9% in 2012. The most important power generators in 2013 were Empresas

Publicas de Medellin E.S.P., EMGESA, Isagen and GECELCA with a combined market share of 71.6%.

Power Generation by Source (GWh) 2013 Power Generation by Company (GWh)

XM Compañía de Expertos en Mercados S.A ESP

14,518

12,877

10,322

6,833

3,461 3,373 2,474 2,041

1,317 1,078 680 506 445 428

1,843

23%

21%

17%

11%

6% 5% 4% 3%

2% 2% 1% 1% 1% 1%

3%

Output (GWh) Share

Hydraulic 67.3%

Thermal 27.1%

.Small and Cogenerators

5.7%

- 22 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

Electricity Demand and Consumption

Energy Monthly Demand Performance (GWh)

Electricity production indicators

Energy consumption by economic activity in 2013(GWh)

National Administrative Department of Statistics, XM Compañía de Expertos en Mercados S.A ESP

5.03

4.61

5.03 5.11

5.16

4.96

5.21 5.20 5.09 5.25

5.09 5.18

4.81 4.63

5.03

4.73

5.03

4.89

5.03 5.10 5.03 5.07 4.98

5.03

2013 2012

8,304.2

4,201.2

2,605.8 1,856.3

1,443.9 701.6 547.0 531.4

46.1

2006 2007 2008 2009 2010 2011 2012 2013

Real Cost of Energy, COP/KWh 25,3 27,8 28,3 30,8 28,5 30,5 33,52 35,02

Maximum Load per Hour, MW 8,762 9,093 9,079 9,290 8,946 8,917 9,504 9,383

Net Installed Capacity, MW 13,279 13,410 13,479 13,543 14,423 14,420 14,361 14,559

- 23 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

Other Energy Indicators

Real Cost of Energy (COP/KWh)

National Administrative Department of Statistics, XM Compañía de Expertos en Mercados S.A ESP

Maximum Power Demand (MW)

Net Installed Capacity MW

25.3 27.8 28.3 30.8 28.5 30.5 33.5 35.0

2006 2007 2008 2009 2010 2011 2012 2013

13,279 13,410 13,479 13,543

14,423 14,420 14,361 14,559

2006 2007 2008 2009 2010 2011 2012 2013

8,762

9,093 9,079 9,290

8,946 8,917

9,504 9,383

2006 2007 2008 2009 2010 2011 2012 2013

- 24 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

III. Power Generation by Type of Fuel

- 25 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

Comments

Fuels Consumption

Fuel consumption in Colombia rose by 42.4% in 2013, with a total consumption of 151,638.8 GBTU due to a 46% rise in thermal power

generation in 2013.

Fuel Consumption of the Thermal Power Generation Plants GBTU

UPME, National Administrative Department of Statistics

2011 2012 2013 Total Share 2013

Gas 71,359.4 75,576.4 98,224.6 64.8%

Coal 16,748.9 26,894.9 50,017.3 33.0%

Diesel 38.3 1,635.8 1,547.9 1.0%

Fuel Oil No. 6 1,589.0 2,326.0 1,757.8 1.2%

Jet fuel A1 0.0 78.8 91.1 0.1%

Total consumption 89,735.6 106,511.9 151,638.8 100.0%

- 26 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

Coal Mining

Coal Production and Price

Colombian coal production decreased by 3.7mn tonnes or

4% to 85.5mn tonnes in 2013. Two events seriously

affected the output during the year – a 32-day walkout of

workers at Colombia's largest coal exporter Cerrejon and

the suspension of loading cranes and barges for 23 days

due to a contamination of the Drummond port.

Not all regions in the country registered a slowdown in

production. For example, the Boyaca region reported a

rise of 2.7 million tonnes, while the Cundinamarca region

produced 2.4 million tonnes more coal.

As much as 94.3% of the coal production was bound for

exports while the remaining 5.7% went to the domestic

market mainly to the thermoelectric, cement and

metallurgical industries.

Coal exports in value terms fell by 11.75% in 2013 mainly

as a result of the decline in international coal prices.

Exports and Imports of Coal

Ministry of Mining and Energy, UPME, Energy and Gas Regulatory Commision

66.2 69.9

73.5 72.8 74.3

85.8 89.2

85.5

55.0

37.0

47.4 43.1

52.5 50.4 55.8

73.2

2006 2007 2008 2009 2010 2011 2012 2013

Coal Production (mn tonnes) Coal Price (USD/tonne)

5,416,385 6,015,180

8,396,847 7,805,190

6,887,834

6,309 6,819

7,068

4,402

7,858

2009 2010 2011 2012 2013

Coal Exports (USD thou) Coal Imports (USD thou)

- 27 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

Coal Mining (cont’d)

Coal FDI (USD mn)

The share of mining sector (except oil), in total of FDI in

Colombia has averaged at 24.5% over the past decade,

reflecting the sector's economic importance and its

stability.

The sector was, however, inevitably affected by the global

crisis and in particular by the significant drop in prices that

since 2011 went from 80 USD/tonne in 2011 to 54

USD/tonne in November 2013, affecting the product

environment and consequently mining FDI in Colombia.

Royalties from the mining sector have been rising

considerably in the recent years, while in 2004, royalties

provided by this sector corresponded 9.9% of the total

royalties, in 2012 accounted 18.7%, almost twice. The

amount paid in royalties during same period increased

from 285 to 1,958 billion COP.

Coal and Hydrocarbons Royalty Payments

Colombian Mining Information System (SIMCO), National Administrative Department of Statistics, Central Bank.

507 524 466 627

1,246

2,157

1,783

1,100

1,798

3,025

1,755

2,546

2,250

2,926

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Royalties 2004 Royalties 2012

COP bn GDP % Total Royalty % COP bn GDP % Total Royalty %

Hydrocarbons 2,585 0.8% 90.1% 8,500 1.3% 81.3%

Coal 285 0.1% 9.9% 1,958 0.3% 18.7%

Total 2,870 0.9% 100.0% 10,458 1.6% 100%

- 28 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

Gas Production

National Gas Production

In 2013, natural gas production in Colombia increased by

4.5%, with over 47% of the output coming from the La

Guajira region.

In December 2013, national demand increased by 3.4% to

1,038 GBTUD, compared with same month in 2012.

According to Colombia's energy ministry, the proved gas

reserves in the Andean nation reached 5,727 GPC in

2012, a figure that should secure gas supply for the

country by 2026.

In 2012, a total of 131 exploratory draw-wells were drilled.

Under a bilateral agreement, Colombia is expected to

start importing gas from Venezuela from the second half

of 2014.

National Production and Reserves

Ministry of Mining and Energy, National Association of Hydrocarbons

1,040 1,064

1,134

1,188 1,179

2010 2011 2012 2013 March 2014

Gas Production (GBTUD)

7,277

8,460

7,058 6,630

7,008

4,384 4,737 5,405 5,463 5,727

319 371 398 387 423

2008 2009 2010 2011 2012

Resereves (GPC) Proved Reserves (GPC) Production (GPC)

- 29 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Comments

Source:

Gas Generation (cont’d)

Domestic gas demand in the 2009-2013 period increased by an annual average of 3.93% for the unregulated sector, which in the last year had a share of

79% in the total gas demand, and by 4.61% in the regulated market (21% market share).

Gas exports increased by 8.4% in 2013. Liquefied petroleum gas (LPG) has accounted for a significant part of Colombia's gas exports in recent years.

Annual Average Demand (GBTUD) Gas Annual Exports (million tonnes)

National Administrative Department of Statistics, XM Compañía de Expertos en Mercados S.A ESP

695 715 690 707 823

179 188 202 198

215

874 903 892 905 1,038

0

200

400

600

800

1,000

1,200

2009 2010 2011 2012 2013

Regulated(GBTUD)

Unregulated(GBTUD)

Total

195.2

223.6

185.4 201.1

2010 2011 2012 2013

- 30 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

Comments

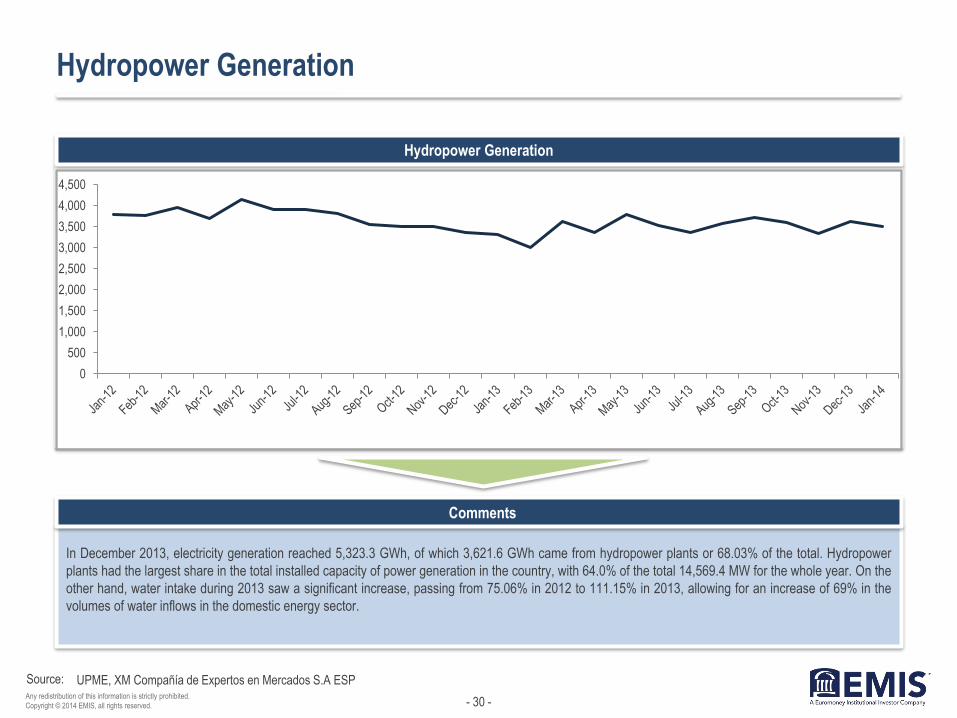

Hydropower Generation

In December 2013, electricity generation reached 5,323.3 GWh, of which 3,621.6 GWh came from hydropower plants or 68.03% of the total. Hydropower

plants had the largest share in the total installed capacity of power generation in the country, with 64.0% of the total 14,569.4 MW for the whole year. On the

other hand, water intake during 2013 saw a significant increase, passing from 75.06% in 2012 to 111.15% in 2013, allowing for an increase of 69% in the

volumes of water inflows in the domestic energy sector.

Hydropower Generation

UPME, XM Compañía de Expertos en Mercados S.A ESP

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

- 31 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

Comments

Hydropower Reserves

At the end of 2013, water reserves in the country were estimated at 10,495 GWh with a decrease of 6.1% y/y when the total reserves totalled 11,180 GWh,

a reduction that was the result of the low levels of hydropower intakes that during 2013 decreased by 9% due to adverse weather conditions. The lowest

reservoir level since 2004 was registered in April with 5,843 GWh, while in the second half of 2013 the levels recovered due to better weather conditions.

Reserves Level GWh

UPME, XM Compañía de Expertos en Mercados S.A ESP

9,132

7,921

6,756

5,843

7,568 7,843 8,420

9,556 9,516 9,531

10,436 10,495

Jan-13 Feb-13 Mar-13 Apr-13 May-13 Jun-13 Jul-13 Aug-13 Sep-13 Oct-13 Nov-13 Dec-13

- 32 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

Renewable Energy

Colombian Renewable Energy Basket, April 2014

As of April 2014, the net energy installed capacity in the

country stood at 14,665.05 MW, out of which renewable

energy accounted for 725.29 MW or 4.94%.

Small hydropower plants accounted for 77.3% of the

capacity, followed by small thermal plants (11.5%) and

bagasse cogenerators (2.1%).

The northern part of Colombia has the best potential to

generate wind energy where Empresas Publicas de

Medellin (EPM) has put the first wind farm into operation,

with 15 turbines, providing 19.5 MW.

According to the Colombian government, based on recent

biomass production studies, 1.5 million tonnes of

sugarcane, and 450,000 tonnes of rice a year can be

utilised for biofuel.

Net Energy Capacity including Renewable Sources (MW)

Ministry of Foreign Affairs, UPME, XM Compañía de Expertos en Mercados S.A ESP

Small Hydropower

77.3%

Small Thermal 11.5%

Bagasse Cogenerator

9.1%

Wind Power 2.1%

Type Effective Capacity

Hydropower 9,415

Thermal 4,521

Cogeneration Bagasse 66.30

Wind Power 18.42

Small Hydropower 560.98

Small Thermal 83.35

Total Net Effective Capacity 14,665.05

- 33 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

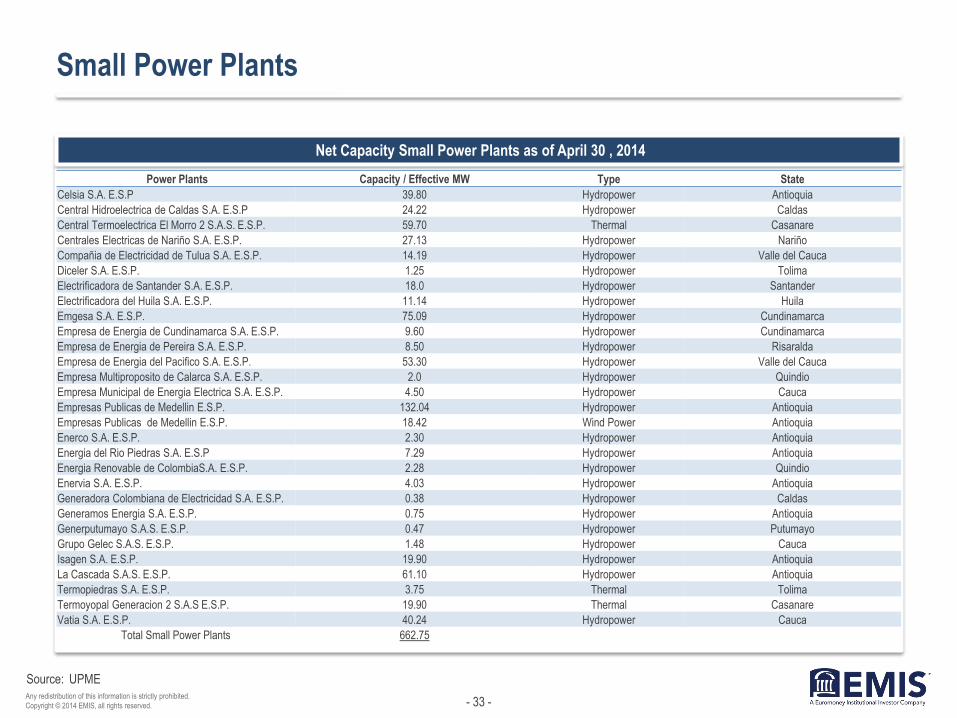

Small Power Plants

Net Capacity Small Power Plants as of April 30 , 2014

UPME

Power Plants Capacity / Effective MW Type State

Celsia S.A. E.S.P 39.80 Hydropower Antioquia

Central Hidroelectrica de Caldas S.A. E.S.P 24.22 Hydropower Caldas

Central Termoelectrica El Morro 2 S.A.S. E.S.P. 59.70 Thermal Casanare

Centrales Electricas de Nariño S.A. E.S.P. 27.13 Hydropower Nariño

Compañia de Electricidad de Tulua S.A. E.S.P. 14.19 Hydropower Valle del Cauca

Diceler S.A. E.S.P. 1.25 Hydropower Tolima

Electrificadora de Santander S.A. E.S.P. 18.0 Hydropower Santander

Electrificadora del Huila S.A. E.S.P. 11.14 Hydropower Huila

Emgesa S.A. E.S.P. 75.09 Hydropower Cundinamarca

Empresa de Energia de Cundinamarca S.A. E.S.P. 9.60 Hydropower Cundinamarca

Empresa de Energia de Pereira S.A. E.S.P. 8.50 Hydropower Risaralda

Empresa de Energia del Pacifico S.A. E.S.P. 53.30 Hydropower Valle del Cauca

Empresa Multiproposito de Calarca S.A. E.S.P. 2.0 Hydropower Quindio

Empresa Municipal de Energia Electrica S.A. E.S.P. 4.50 Hydropower Cauca

Empresas Publicas de Medellin E.S.P. 132.04 Hydropower Antioquia

Empresas Publicas de Medellin E.S.P. 18.42 Wind Power Antioquia

Enerco S.A. E.S.P. 2.30 Hydropower Antioquia

Energia del Rio Piedras S.A. E.S.P 7.29 Hydropower Antioquia

Energia Renovable de ColombiaS.A. E.S.P. 2.28 Hydropower Quindio

Enervia S.A. E.S.P. 4.03 Hydropower Antioquia

Generadora Colombiana de Electricidad S.A. E.S.P. 0.38 Hydropower Caldas

Generamos Energia S.A. E.S.P. 0.75 Hydropower Antioquia

Generputumayo S.A.S. E.S.P. 0.47 Hydropower Putumayo

Grupo Gelec S.A.S. E.S.P. 1.48 Hydropower Cauca

Isagen S.A. E.S.P. 19.90 Hydropower Antioquia

La Cascada S.A.S. E.S.P. 61.10 Hydropower Antioquia

Termopiedras S.A. E.S.P. 3.75 Thermal Tolima

Termoyopal Generacion 2 S.A.S E.S.P. 19.90 Thermal Casanare

Vatia S.A. E.S.P. 40.24 Hydropower Cauca

Total Small Power Plants 662.75

- 34 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

.

…

Source:

Power Generation SWOT Analysis

• Main players such us Ecopetrol EPM and ISA which have

achieved high levels of regional presence, diversifying the

export market and generating new business in the power

sector.

• Building of new energy networks, development of

infrastructure projects and high international presence via

national power transmission network.

• Low share of renewable energy.

• Attacks on the country's electricity infrastructure by guerrillas,

which both jeopardises energy supplies and drives away

potential foreign investors.

• Dissatisfied labour force, which leads to frequent stoppages

and security issues.

• Unfavourable weather conditions.

• Lack of security in regions far from urban centres.

Carrying out the expansion plan of power transmission networks

for the next 15 years, developed by the Ministry of Mines and

Energy and Mining Energy Planning Unit.

The plan features 16 projects worth USD 1.680mn, which would

result in building 3,000 km of power grids.

Power Sector

SWOT Analysis

Strengths Opportunities

Weaknesses Threats

- 35 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

Power Transmission and Distribution

Power Transmission Net Income (COPmm)

Power Transmission Losses

UPME

103

,628

102

,873

103

,931

102

,832

105

,253

104

,846

103

,892

103

,989

104

,644

105

,161

104

,979

103

,893

103

,325

102

,699

103

,744

104

,005

105

,330

105

,939

107

,259

107

,557

107

,273

107

,050

106

,378

106

,986

1.6% 1.8% 1.9% 2.0%

1.5% 1.7% 1.7% 1.8%

2005 2006 2007 2008 2009 2010 2011 2012

- 36 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

Power Transmission and Distribution (Cont´d)

Transmission Lines by Operator

XM Compañía de Expertos en Mercados S.A ESP

Operator Length (Km) Length (%)

Electrificadora del Caribe S.A. E.S.P. 1,441.72 5.94%

Empresas Publicas de Medellin E.S.P. 2,089.21 8,61%

International Colombia Resources Corporation 304.0 1.25%

Transelca S.A. E.S.P. 1,577.01 6.50%

Zona Franca Celsia S.A. E.S.P. 3.20 0.01%

Central Hidroelectrica de Caldas S.A. E.S.P. 501.47 2.07%

Centrales Electricas de Nariño S.A. E.S.P. 476.50 1.96%

Centrales Electricas del Norte de Santander S.A. E.S.P. 348.06 1.43%

Codensa S.A. E.S.P. 1,119.57 4.61%

Compañia Energetica de Occidente S.A. E.S.P. 338.70 1.40%

Compañia Energetica del Tolima S.A. E.S.P. 504.27 2.08%

Electrificadora de Santander S.A. E.S.P. 553.03 2.28%

Electrificadora de Caqueta S.A. E.S.P. 111.50 0.46%

Electrificadora del Huila S.A. E.S.P. 297.67 1.23%

Electrificadora de Meta S.A. E.S.P. 385.47 1.59%

Empresa de Energia de Arauca E.S.P. 60.0 0.25%

Empresa de Energia de Boyaca S.A. E.S.P. 543.59 2.24%

Empresa de Energia de Casanare S.A. E.S.P. 373.50 1.54%

Empresa de Energia de Cundinamarca S.A. E.S.P. 106.59 0.44%

Empresa de Energia de Pereira S.A. E.S.P. 7.80 0.03%

Empresa de Energia del Bajo Putumayo S.A. E.S.P. 102.0 0.42%

Empresa de Energia del Pacifico S.A. E.S.P. 1,258.16 5.18%

Empresa de Energia del Quindio S.A. E.S.P. 17.0 0.07%

Empresa de Energia Electrica del Departamento del Guaviare S.A. E.S.P. 187.0 0.77%

Empresa Distribuidora del Pacifico S.A.E.S.P. 281.75 1.16%

Empresas Municipales de Cali E.I.C.E. E.S.P. 3.40 0.01%

Inteercolombia S.A. E.S.P. 9,780.30 40.30%

Termoyopal Generacion 2 S.A.S.E.S. P. 27.31 0.11%

Distasa S.A.E.S.P. 18.75 0.08%

Empresa de Energia de Bogota S.A. E.S.P. 1,451.14 5.98%

TOTAL 24,269.67 100%

- 37 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

IV. Power Exports

- 38 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

Comments

Energy Exports

Electricity Exports to Ecuador and Venezuela (GWh)

UPME, XM Compañía de Expertos en Mercados S.A ESP

The total energy exports reached 149 GWh in December 2013. Exports to Ecuador in December 2013 grew by 1,317% compared to same month in 2012

due to adverse weather conditions in Ecuador that decreased its domestic power generation capacity.

43

5 5 - 1

53 59 52 72

111

203 193

180

126

257

103

70 59

46 67

119

155

223

137

34 32 40 54 52 56 63 61

124

63 81

53 68

168 155

133

225

108 124

66 49

58 73

149

jan-

10

Feb

-10

Mar

-10

apr-

10

May

-10

Jun-

10

Jul-1

0

aug-

10

Sep

-10

Oct

-10

Nov

-10

dec-

10

jan

-11

Feb

-11

Mar

-11

apr-

11

May

-11

Jun-

11

Jul-1

1

aug-

11

Sep

-11

Oct

-11

Nov

-11

dec-

11

jan

-12

Feb

-12

Mar

-12

apr-

12

May

-12

Jun-

12

Jul-1

0

aug-

12

Sep

-12

Oct

-12

Nov

-12

dec-

12

jan

-13

Feb

-13

Mar

-13

apr-

13

May

-13

Jun-

13

Jul-1

3

aug-

13

Sep

-13

Oct

-13

Nov

-13

dec-

13D

ec-1

3

- 39 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

Comments

Power Trade with Ecuador

Colombia and Ecuador Power Trade (MWh)

XM Compañía de Expertos en Mercados S.A ESP

Since 2002, Colombia has exported 11,645,891.5 MWh of electricity to Ecuador worth a total of USD 973mn. In 2013, Colombian exports to Ecuador

reached 662,343.7 MWh, up by 236,034.5 MWh compared to the previous year.

Energy Exports (MWh) Energy Imports (MWh) Exports (USD thou) Imports (USD thou)

2013 662,343.7 28,502.4 78,442.1 1,682.5

2012 236,034.5 6,510.2 24,148.3 243.2

2011 1,294,591.8 8,218.5 92,995.8 231,3

2010 797,690.0 9,745.0 73,825.1 565.3

2009 1,076,725.6 20,764.1 107,751.0 1,118.5

2008 509,782.2 37,533.3 35,908.4 2,309.4

2007 876,602.3 38,392.6 66,269.4 1,336.0

2006 1,608,628.9 1,070.4 127,104.5 50.0

2005 1,757,882.9 16,028.8 151,733.7 509.8

2004 1,681,088,1 34,974.3 135,109.1 738.0

2003 1,144,521.6 67,202.7 80,309.2 2,334.7

Total 11,645,891.5 268,942.2 973,596.7 11,118.7

- 40 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

Comments

Power Exchange and Trading

Wholesale Market Prices (COP/KWh)

UPME, XM Compañía de Expertos en Mercados S.A ESP

In February 2014, energy stock prices stood at an average of 189.38 COP/KWh, higher by 4.71 COP/KWh compared to February 2012.

0

100

200

300

400

500

600

National Exchange Price COP/KWh Average Contracts Price COPKWh Scarcity Price (COP)

- 41 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

Power Exchange and Trading (cont'd)

Market Sales by Type (COPmn)

Total Exchange Purchases (COPmn)

UPME

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

National Exchange Sales COP mn Contract Sales COP mn

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

- 42 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

V. Natural Gas Distribution

- 43 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

PNG in Colombia

Piped Natural Gas Status as of December 31, 2013

Superintendent of Public Utility Services

Company Name Domestic

consumers

Non-Domestic

consumers

Total Invoiced

Domestic consumers (COP)

Total Invoiced

Non-Domestic consumers (COP)

Alcanos de Colombia 533,959 5,512 120,896,934,553 28,519,726,551

Empresa Integral de Servicios OP&S 1,413 14 298,741,371 33,126,245

ORECUE 1,056 30 112,834,157 10,310,588

EPM 744,621 13,206 125,303,998,927 89,694,325,151

ESPIGAS 2,005 63 405,662,972 261,493,140

G8 Proyectos Energeticos 305 - 4.072.608 -

Gas Natural Cundiboyacense 254,829 8,218 39,041,864,349 27,309,280,326

Gas Natural del Cesar 57,494 385 12,386,396,602 1,338,740,700

Gas Natural del Oriente 238,872 7,464 43,523,443,039 23,986,200,666

Gas Natual S.A. 1,804,091 46,482 431,338,266,576 233,688,378,483

Gases de la Guajira 77,753 1,677 14,570,727,576 5,800,202,557

Gases de Occidente 852,472 12,234 131,318,433,455 76,418,834,393

Gases del Caribe 705,713 10,783 133,411,795,207 72,913,709,717

Gases del Cusiana 42,760 1,558 4,502,066,368 1,480,512,276

Gases del Llano 144,964 4,097 19,052,760,082 8,606,447,784

Gases del Oriente 88,035 115 25,209,355,205 2,495,570,667

Ingenieria y Servicios 4,028 47 981,370,483 157,103,754

Medigas 21,990 438 3,483,040,052 784,512,205

Metrogas de Colombia 92,075 505 22,459,780,446 4,343,976,241

Nacional de Servicios Publicos Domiciliarios 2,337 - 751,903,632 -

Promotora de Servicios Publicos Domicialiarios 13,076 43 3.848.843.706 88,286,384

Servicios Publicos Ingeniaria y Gas 1,798 17 415,705,910 34,068,878

Surcolombiana de Gas 23,060 54 7,215,088,897 255,859,512

Surtidora de Gas del Caribe 568,430 5,519 119,809,617,099 25,819,444,887

Yavegas 673 - 136,491,054 -

Total 6,277,809 118,461 1,260,479,194,326 604,040,111,105

- 44 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

Natural Gas Coverage

Natural Gas Consumption by Electric Generation Plant (GBTUD)

Number of Regions Covered by User Type

Concentra Information System

Year Termosierra Termocentro Termovalle Merilectrica Termoemcali Termodorada

2009 19.6 12.7 7.8 2.4 0.4 0.9

2010 21.8 12.7 8.2 0.7 0.1 0.5

2011 1.7 7.9 n/a 2.9 0.3 0.3

2012 14.0 9.4 2.9 3.5 0.6 0.5

2013 7.9 29.3 5.7 5.3 4.3 n/a

Year Domestic Commercial Industrial Total

2009 383 354 141 878

2010 401 365 142 908

2011 434 398 158 990

2012 481 435 163 1,079

2013 501 459 165 1,125

- 45 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

Car Fuel

Gas Stations by Region

Cars Converted to Compressed Natural Gas

Superintendent of Public Utility Services

Region 2009 2010 2011 2012

Bogota 145 148 154 156

Valle del Cauca 101 103 106 109

Antioquia 70 75 79 83

Atlantico 69 74 78 79

Cundinamarca 22 26 29 31

Santander 22 23 27 29

Bolivar 25 27 28 28

Meta 21 22 26 26

Tolima 23 25 26 26

Risaralda 20 22 22 22

City 2009 2010 2011 2012 2013

Bogota 6,694 4,772 11,239 13,305 5,830

Cali 2,674 3,246 5,292 4,738 2,396

Medellin 1,648 2,482 5,096 3,913 1,891

Barranquilla 1,853 3,121 4,672 1,863 1,573

Pereira 715 970 1,795 2,124 926

Manizales 520 503 1,555 1,729 677

Santa Marta 392 334 325 671 508

Armenia 443 452 664 850 486

Bucaramanga 1,093 607 560 716 445

Ibague 690 489 733 1,022 327

- 46 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

VI. Main Players

- 47 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

Ecopetrol S.A.

Financial Indicators (USD mn)

Ecopetrol S.A. is the largest petroleum company in

Colombia. The company is also among the 35

largest petroleum companies in the world and among

the top four petroleum companies in Latin America.

Ecopetrol extracts petroleum, hydrocarbons and

natural gas and accounts for over 60% of the

national oil production. The company was founded in

1948. Ecopetrol is publicly traded and controlled by

the Ministry of Mines and Energy.

In 2013, Ecopetrol S.A. made investments for USD

4.5 million primarily aimed at drilling activities,

especially in the Rubiales and Quifa fields, and

facilities construction, primarily in the Castilla and

Chichimene fields that comprised a total of 22 wells

explored in the year. The company’s investments

also included contributions to Reficar modernization

project, Barrancabermeja refinery and Bioenergy.

For 2014, Ecopetrol expects a Capex of USD 10.6bn

distributed as follows: USD 5.1bn for production,

USD 1.8bn for exploration, USD 2.1bn for refining

and USD 1.4bn for transportation.

Company data

18,785

27,904

32,990 31,734

4,361

7,952 8,468

6,930

2010Y 2011Y 2012Y 2013Y

Total Operating Revenue Net Profit (Loss)

- 48 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

Ecopetrol S.A. (cont’d)

Return on Assets and Equity (%)

Ecopetrol in Figures

Capex Breakdown (USD9.5 billion for 2013)

Company data

10.76

24.15

9.90 12.82

18.12 14.88

11.71

19.31

33.59

16.07 20.10

28.08

22.94

18.60

2007 2008 2009 2010 2011 2012 2013

ROA ROE

Production 44%

Exploration 18%

Refining 18%

Transport 19%

Other 1%

Type Indicator 2009 2010 2011 2012 2013

EXPORTS Volume (Kbdc) 302 370 493 521 540

Value (USDmn) 5,825 11,420 16,062 19,127 18,879

PRODUCTION Oil and Gas Ecopetrol Property (Kbpde) 520 616 724 754 788

Total Oil (Kbpd) 426 482 569 591 612

FUELS Gas Sales (Bpd) 68,990 72,940 74,500 76,974 80,401

Diesel Sales (Bpd) 99,730 100,580 109,000 110,746 114,406

TRANSPORT Volumes of Oil Transported (Kbdc) 576,2 770,9 916,2 917,5 950,3

Refined Volumes Transported (Kbdc) 223,3 264,9 289,0 234,0 237,0

RESERVES Oil and Gas (Mbpe) 1,538 1,714 1,857 1,877 1,972

Replacement Index (%) 351% 193% 164% 109% 139%

- 49 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

Interconexión Eléctrica S.A.

Financial Indicators (USD mn)

Interconexion Electrica S.A. (ISA) is a Latin American

business group, whose activities include electricity

transmission, telecommunications transmission,

operation of roads concessions, intelligent

management of real-time systems and infrastructure

construction projects.

Today, ISA has presence in eight countries through

33 companies and operates 40,630 km of high-

voltage power lines and 75,960 MVA of

transformation capacity.

In 2013, ISA added 1,900 MVA of transformation

capacity and about 270 km of power-lines to its

network with an investment of close to USD 300

million. The company plans to invest additional USD

3bn to expand its power grid by 5,000 km and

increase transformation capacity by 16,000 MVA.

In the third quarter of 2013, ISA won a new

concession to design, finance, build, operate and

maintain the transmission line Mantaro-Marcona-

Socabaya-Montalvo of 500 kV and 920km and its

associated substations. It is the largest concession

won by ISA in the recent years.

Company data

492 513

571

517

180 173 154

225

2010Y 2011Y 2012Y 2013Y

Total Operating Revenue Net Profit (Loss)

- 50 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

Interconexión Eléctrica S.A. (cont’d)

Return on Assets and Equity (%)

Colombian Shareholding

Electric Energy Business Unit Evolution (USD mn)

Electric Infrastructure

Company data

3.56 3.23

3.70 3.81 3.59 3.06

4.22

5.90

4.92 5.15 5.34 5.27

4.46

5.81

2007 2008 2009 2010 2011 2012 2013

ROA ROE

1,803 1,896

1,390 1,322

1,354

726

2011 2012 2013

Income EBITDA

The State 51.4%

Private Investors

31.4%

EPM 10.2%

Ecopetrol 5.3%

EEB 1.7%

Country Company

Operational

Circuit Km Transformation MVA

COLOMBIA ISA

10,144 13,040

TRANSELCA 1,585 3,848

PERU

REP 6,230 2,605

Transmantaro 2,465 4,325

ISA Peru 393 235

BOLIVIA ISA Bolivia

588 370

BRAZIL

CTEEP 18,893 45,587

IEMG 172 3,900

PINHEIROS 6 1,600

EVRECY 154 450

TOTAL

40,630 75,960

- 51 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

Codensa S.A. E.S.P

Financial Indicators (USD mn)

Codensa S.A. E.S.P. activities include distribution

and sales of electric energy and other utility-related

activities. The company was established in October

1997 as a joint venture of Empresa de Energia de

Bogota (EEB) and Grupo Endesa.

Codensa is the main electricity distributor in the city

of Bogota. The company is currently managed by

Grupo Endesa, as part of the agreement signed

between this international group and the EEB in the

late nineties.

Codensa has expressed interest in participating in

the privatization of electric companies across

Colombia and has created a unit, Inversora Codensa

S.A.S., for this purpose.

In 2013, Codensa approved an investment budget of

USD 110.5mn aimed at covering local power

demand. Based on this investment budget, Codensa

is working on two new projects Nueva Esperanza

Substation with a high-voltage circuit of 459 MVA and

North Substation of 300 MVA, both in Bogota.

Company data

374 407

1,777

1,667

69

289 278

2010Y 2011Y 2012Y 2013Y

Total Operating Revenue Net Profit (Loss)

- 52 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

Codensa S.A. E.S.P (cont’d)

Return on Assets and Equity (%)

Power Purchases

Ownership Structure (%)

Company data

7.6 9.2 9.0 9.0 9.5 9.7

14.1 16.1

17.0 17.0 16.4 17.0

2008 2009 2010 2011 2012 2013

ROA ROE

Empresa de Energia de Bogota S.A.

51.5%

Enersis S.A. 39.1%

Chilectra S.A. 9.4%

Others 0,03%

Type GWh COP mn

Regulated Market 8,769 1,244,044

Contracts 7,995 1,102,035

EMGESA 4,131 573,205

Other Suppliers 3,854 528,830

Stock Market Purchases 773 142,009

Non-Regulated Market 240 33,358

Contracts 221 29,433

EMGESA 105 14,193

Other Suppliers 116 15,241

Stock Market Purchases 19 3,924

Purchases 9,008.29 1,277,402

Stock Market Sales 22.62 3,668

Total Energy Purchases 8,985.67 1,273,734

- 53 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

Empresas Publicas de Medellin E.S.P

Financial Indicators (USD mn)

Empresas Publicas de Medellin E.S.P (EPM)

provides water and sewage services, power and gas

fuel distribution, fixed and mobile telephony and

other telecommunications services. EPM group is

comprised of 45 companies, including 20 in

Colombia and 25 in Central America and Caribbean,

South America, the USA and Spain.

In December 2013, EPM approved and investment

program of COP 10.1bn, COP 2.5bn were allocated

to improving infrastructure and COP 1bn would be

transferred to the Municipio de Medellin for public

works investments. The remaining investment

resources would be allocated to different business

projects, including capitalization, production, sales

and others.

In 2013, EPM expanded its international coverage by

creating a new unit in Chile, EPM Chile S.A., and the

acquisition of Tecnologia Intercontinental S.A. de

C.V. through EPM’s Mexican subsidiary EPM Capital

Mexico S.A. de C.V.

Company data

2,351

2,529

3,070

2,847

762 786

992 858

2010Y 2011Y 2012Y 2013Y

Total Operating Revenue Net Profit (Loss)

- 54 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

Empresas Publicas de Medellin E.S.P (cont’d)

Return on Assets and Equity (%)

EBITDA Breakdown (%)

EBITDA (USD mn)

EPM Ratios

Company data

7.16 7.22 7.19

5.55 5.33 5.87

5.19

9.01 8.96 9.59

7.90 7.64 8.25

7.43

2007 2008 2009 2010 2011 2012 2013

ROA ROE

677 888

1,262 1,463

1,976 2,119

2,029

2007 2008 2009 2010 2011 2012 2013

Energy 74%

Hodropower 9%

Telecom 17%

TYPE EPM Group 2012 EPM Group 2013

EBITDA Margin 30% 29%

Net Margin 13% 13%

Net Debt 37% 40%

Financial Debt 22% 24%

EBITDA / Financial Expenses 6.52 6.91

Financial Debt / EBITDA 2.02 2.43

- 55 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

Emgesa S.A. E.S.P.

Financial Indicators (USD mn)

Emgesa S.A. E.S.P activities include generation

include generation and sales of electric energy. The

company owns ten hydropower plants and two

thermal plants. Emgesa was established in October

1997 as a joint venture of Empresa de Energia de

Bogota (EEB) and Capital Energia, a unit of Endesa

International.

In 2013, Emgesa’s sales on the non-regulated

market marked an increase of 3.4% compared to

2012, mainly due to a contract with Ecopetrol S.A.

The contract with Ecopetrol will be valid for five years

from 2013 to 2018, with total energy consumption

estimated at 5,613 GWh during the contract period.

Emgesa is currently building the El Quimbo

hydroelectric power project, a plant with installed

capacity of 400MW that is expected to generate

2,216 GWh per year. The construction is scheduled

to be completed in 2014 with an estimated

investment budget of USD 837mn. The power plant

is located in the Huila department and will use water

from the Suaza and Magdalena rivers.

Company data

238

978

1,213 1,244

81

344

443 452

2010Y 2011Y 2012Y 2013Y

Total Operating Revenue Net Profit (Loss)

- 56 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

Emgesa S.A. E.S.P. (cont’d)

Return on Assets and Equity (%)

Power Purchases (GWh)

Ownership Structure (%)

Power Generation by Power Plant

Company data

5.29 5.64 6.58

2.00

8.08 8.57 8.89

7.18 7.87

9.06

3.03

12.27 13.69

14.99

2007 2008 2009 2010 2011 2012 2013

ROA ROE

Empresa de Energia de Bogota S.A.

51.5%

Endesa Chile 26.9%

Enersis 21.6%

379

574

204

135

2010 2011 2012 2013

Power Plant % GWh

GUAVIO 42,4% 5,403.9

PAGUA 33,1% 4,222.1

BETANIA 15,2% 1,932.4

SMALL Power Plants 1,8% 225.5

TERMOZIPA 6,8% 872.6

CARTAGENA 0,7% 91.1

Total 100.0% 12,747.6

- 57 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Contact:

Corporate Headquarters

Nestor House

Playhouse Yard

London EC4V 5EX

UK

Voice: +44 207 779 8471

Fax: +44 207 779 8224

Americas Headquarters

225 Park Avenue South

New York, New York 10003

US

Voice: +1 212 610 2900

Fax: +1 212 610 2950

Asia Headquarters

Eucharistic Congress Bldg. No.

III

4th Floor, 5 Convent Street

Mumbai 400 001

India

Voice: +91 22 22881123

Fax: +91 22 22881137

Disclaimer:

The material is based on sources which we believe are reliable, but no warranty, either expressed or implied, is provided in relation to the accuracy or completeness

of the information. The views expressed are our best judgment as of the date of issue and are subject to change without notice. EMIS and Euromoney Institutional

Investor PLC take no responsibility for decisions made on the basis of these opinions.

Any redistribution of this information is strictly prohibited. Copyright © 2014 EMIS, all rights reserved. A Euromoney Institutional Investor company.

About EMIS Insight

EMIS Insight is a unit of EMIS that produces proprietary strategic research and analysis. The service features market overviews, industry trend analysis, legislation

and profiles of the leading sector companies provided by locally-based analysts.

About EMIS

Founded in 1994, EMIS (formerly known as ISI Emerging Markets) was acquired by Euromoney Institutional Investor PLC in 1999. EMIS works from over 15 offices

around the world to deliver electronic information products, by subscription, to institutional customers globally. EMIS provides hard-to-get information covering more

than 100 emerging markets. Its flagship products are EMIS Intelligence and EMIS Professional.

EMIS clients include top investment banks, corporations, law firms, consultants, investment and insurance companies, universities and libraries, multilateral

organizations, and others.

- 58 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Contact:

Corporate Headquarters

Nestor House

Playhouse Yard

London EC4V 5EX

UK

Voice: +44 207 779 8471

Fax: +44 207 779 8224

Americas Headquarters

225 Park Avenue South

New York, New York 10003

US

Voice: +1 212 610 2900

Fax: +1 212 610 2950

Asia Headquarters

Eucharistic Congress Bldg. No.

III

4th Floor, 5 Convent Street

Mumbai 400 001

India

Voice: +91 22 22881123

Fax: +91 22 22881137

Disclaimer:

The material is based on sources which we believe are reliable, but no warranty, either expressed or implied, is provided in relation to the accuracy or completeness

of the information. The views expressed are our best judgment as of the date of issue and are subject to change without notice. EMIS and Euromoney Institutional

Investor PLC take no responsibility for decisions made on the basis of these opinions.

Any redistribution of this information is strictly prohibited. Copyright © 2014 EMIS, all rights reserved. A Euromoney Institutional Investor company.

About EMIS Insight

EMIS Insight is a unit of EMIS that produces proprietary strategic research and analysis. The service features market overviews, industry trend analysis, legislation

and profiles of the leading sector companies provided by locally-based analysts.

About EMIS

Founded in 1994, EMIS (formerly known as ISI Emerging Markets) was acquired by Euromoney Institutional Investor PLC in 1999. EMIS works from over 15 offices

around the world to deliver electronic information products, by subscription, to institutional customers globally. EMIS provides hard-to-get information covering more

than 100 emerging markets. Its flagship products are EMIS Intelligence and EMIS Professional.

EMIS clients include top investment banks, corporations, law firms, consultants, investment and insurance companies, universities and libraries, multilateral

organizations, and others.