CMO Industry Update - PharmSource · 2016-04-29 · CMO Industry Update Interphex 2016 April 27,...

18

CMO Industry Update Interphex 2016 April 27, 2016 Jim Miller PharmSource www.pharmsource.com 1

Transcript of CMO Industry Update - PharmSource · 2016-04-29 · CMO Industry Update Interphex 2016 April 27,...

CMO Industry Update

Interphex 2016 April 27, 2016

Jim Miller

PharmSource

www.pharmsource.com 1

Agenda

• Market conditions overview

• Industry M&A activity and its

implications

www.pharmsource.com 2

Results reflect pipeline

and small molecule strength

8.7%

4.1%

0.7%

11.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

DEV CLIN DP DS

Bio/Pharma Services Revenue Growth

2014-2015 Company Segment Growth

Cambrex DS 24%

Dottikon DS 7%

Lonza DS 10%

AMRI DS 7%

Avid DS 20%

Sharp PKG 37%

Patheon DP 5%

Baxter DP -10%

Catalent DEV 7%

Metrics DEV 9%

SGS DEV 7%

Charles River DEV 8%

www.pharmsource.com 3

Dev = development services

CLIN = clinical research

DP = dose manufacturing

DS = API manufacturing

Source: Public company reports

Individual Company Performance

2015 vs. 2014

NDA approvals are way up

10 12 10 11 22

33 17 17 18 16

10 3 8 20

17

15

19 13 22 23

37

30 23

36 31

24

27 27

38 49

39

28 37

21 27 22

25 33

23

28

0

20

40

60

80

100

120

140

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Mid Size

Global

Smallcommercial

Generic

www.pharmsource.com 4

Global bio/pharma has returned as major driver

Source: PharmSource CMO Scorecard

Market environment

Propensity to outsource unchanged

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Generic SmallCommercial

Global Mid Size All

2015 2010-2014

www.pharmsource.com 5

Source: PharmSource CMO Scorecard

Market environment

Clinical activity indicators are positive

0

100

200

300

400

500

600

700

800

900

IND Filings at FDA 2009-2015

NDA/BLA Biosimilars

0

20

40

60

80

100

120

140

160

2013 2014 2015

NDA Submissions to FDA

NMEs Non-NMEs

www.pharmsource.com 6

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

Q1 New Registrations in clinicaltrials.gov

Phase 1 Phase 2

Phase 3

Source: FDA Source: FDA Source: clinicaltrials.gov

Market environment

Financing and R&D spend have been strong

$-

$5

$10

$15

$20

$25

$30

$35

$40

$45

2008 2009-12 2013/14 2015

$ B

illi

on

Funding to Early Stage Companies

Other Private equity

IPO Secondary offering

Venture capital Upfront license fees

www.pharmsource.com 7

Source: PharmSource Lead Sheet

$-

$20

$40

$60

$80

$100

2010 2011 2012 2013 2014 2015

US

$ B

illi

on

s

R&D Spending by Top 25 Bio/Pharma Companies

Top 25 companies spending

20% of revenue on R&D

Source: public financial reports

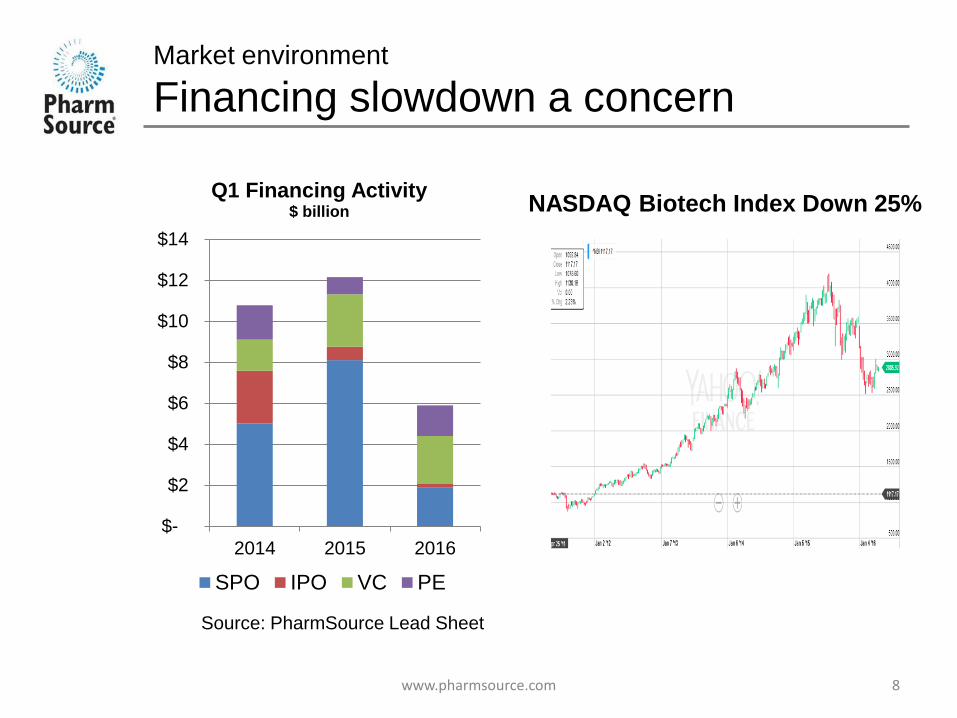

Market environment

Financing slowdown a concern

$-

$2

$4

$6

$8

$10

$12

$14

2014 2015 2016

Q1 Financing Activity $ billion

SPO IPO VC PE

www.pharmsource.com 8

Source: PharmSource Lead Sheet

NASDAQ Biotech Index Down 25%

Market conditions takeaways

• Financing picture bears watching

– Bio/pharma funding always cyclical

– Lower valuations means fewer deals and less $ per deal

– “What if we can’t replace what we spend?”

• CMO dependence on small bio/pharma at risk

when global bio/pharma dominates funding,

pipeline and approvals

www.pharmsource.com 9

M&A re-shaping CDMO industry

Target

API Dose Other

Bu

yer

AP

I

AMRI/Gadea

AMRI/Cedarburg

Siegfried/BASF CM

Novacap/Chemie Uetikon

Siegfried/Hameln

Piramal/Coldstream Labs

AMRI/Aptuit Glasgow

AMRI/Oso

AMRI/Whitehouse Labs

Johnson-

Matthey/Pharmorphix

AMRI/SSCI

Do

se Patheon/Irix

Patheon/Gallus

Catalent/Micron Tech

Capsugel/Xcelience

Synerlab/Alcala Farma

Patheon/Agere

Recipharm/Kemwell

Oth

er PCI/Penn Pharma BioDuro/Formex

Charles River/WIL-QS

Evans Analytical/ABC Labs

www.pharmsource.com 10

Lots more to come

• PE holding periods maturing

• IPO market is difficult

• Strategic buyers scramble for assets

Source: PharmSource STRATEGIC ADVANTAGE database

M&A

Deal values have been rich

Year Buyer Target Service

Value

US$ M

Revenue

Multiple

EBITDA

Multiple

2012

Patheon

Banner Dose $ 269 1.1 x 10 x

2014 Gallus Bio API $ 257 2.6 x

2015 Irix SM API $ 161 1.6 x

2012

Siegfried

Alliance Medical Dose $ 58 2.9 x

2014 Hameln Dose $ 62 0.7 x

2015 BASF assets SM API $ 300 1.0 x

2014

AMRI

Oso Bio Dose $ 110 1.9 x 11 x

2014 Cedarburg SM API $ 41 2.2 x 7.5 x

2015 Gadea SM API $ 174 2.1 x 9 x

2015 Shenxhen

Hepalink

Cytovance Bio API $ 206 5.0 x

2015 Piramal Coldstream Labs Dose $ 31 2.2 x

2014 Consort Aesica Dose $ 374 1.3 x 11.5 x

2016 Recipharm

Kemwell Biopharma Dose $ 205 2.2 x 15.0 x

2016 Nitin Lifesciences (74%) Dose $ 102 2.9 x 11.7 x

www.pharmsource.com 11

Source: PharmSource STRATEGIC ADVANTAGE database

M&A binge has big business risks

• Can management integrate rapidly-acquired businesses

operationally?

• Is there a comprehensive underlying strategy and can it be

executed?

– Chain only as strong as weakest link

• Will there be enough cash flow to fund capex and

innovation?

• Can they service the debt in a downturn or adverse event?

www.pharmsource.com 12

Financial restructurings not unprecedented

2007 – Patheon rescued by JLL after Mova acquisition

2016 – Aenova restructuring following roll-up binge

Ultimate endpoint: full service CMO

13 www.pharmsource.com

• Complete suite of

offerings • Component

• Scale

• Technology

• Principal examples

• Patheon

• Catalent

• Siegfried

• AMRI

• Corden Pharma

• Fareva

What is the full service model really about?

• Response to slow organic growth • Dose CMOs generally growing in single digits

• Achieving breadth and scale • Capture more client spend with broader service offering

• Cost savings in sales, marketing, G&A

• Private equity opportunity to employ capital • PE firms like roll-up model

• Response to customer desire to work with fewer suppliers • Pricing leverage, lower vendor management costs

www.pharmsource.com 14

Challenge:

Can CMOs create real value in full service model?

Two successful routes to full service CMO model

Acquired asset Redundant facility CMO business

Route • Acquire unneeded facility from

bio/pharma company

• Acquire functioning CMO

Advantages • Low capital cost

• Contracts for legacy products

• Immediate EBITDA

• Established client base and

reputation

• Appropriate cost structure

• Established service culture

• US opportunities

• Larger top line increments

Disadvantages • High cost base

• Legacy products in decline

• Underutilized capacity

• Must create service culture

• Technology may be old

• Mostly limited to Europe

• High initial investment

• High purchase multiple

• Integration costs and risks

Examples • Fareva

• Corden Pharma

• Patheon

• AMRI

• Siegfried

www.pharmsource.com 15

Growing number of very large CMOs

Size Company Route

Bio

API

SM

API Dose Develop

$1+

billion

Lonza Organic

Patheon CMO acquisition

Catalent CMO acquisition

$500+

million

Aenova CMO acquisition

Fareva Facility acquisition

Siegfried CMO acquisition

Evonik Organic

Vetter Organic

B-I Organic

Famar Facility acquisition

Recipharm CMO acquisition

www.pharmsource.com 16

Source: PharmSource analysis

Final thoughts

• CDMO scale increasingly important but will

it be enough?

– Strategy, integration, operational skills key

• Buyers should do careful due diligence for

operational and financial risks

• CMOs may have to learn how to sell again

www.pharmsource.com 17

18 www.pharmsource.com