clearin MS2003

12

Public sector banks have settled about 30% of their NPA (non-performing assets) cases for which they issued notices under the Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest (Sarfaesi) Act 2002. A total of 33,736 notices under the Sarfaesi Act were issued by 20 nationalised banks and the subsidiaries of SBI for recovery of Rs 12,147 crore after the enactment of the Act. These banks together have settled 9,946 cases, according to data compiled by CMIE. Though the percentage of dispute cases settled till June ‘03 amount to 29.5%, in terms of value it amounts to a paltry Rs 499 crore only, accounting for just 4.1% of the total outstanding amount for which notices were issued. State Bank of India and its subsidiaries together have recovered Rs 83 crore out of Rs 4,771 crore loan outstanding for which they had issued notices till June ‘03. Similarly, Punjab National Bank and Canara Bank, which had sent 3,015 and 1,011 notices respectively for recovery of loans amounting to Rs 711 crore and Rs 350 crore, have recovered Rs 39.3 crore and Rs 34.5 crore respectively till June ‘03. While banks succeeded in getting their smaller clients to pay up o n the strength of the new Act, a good number of companies with large amounts in outstanding against them continue to defy the banks’ notices. With the recent ruling by Supreme Court (upholding the Act), banks are now confident of a faster recovery of dues. Public Sector Banks (PSUs) have still facing tribulations shimmering from debt wavier of 2008 . Meanwhile the government has made another plan to provide overdraft facility or term loan up to Rs.10, 000/ - to agricultural land less labours. PUBLIC SECTOR units (PSUs) are still facing tribulations shimmering from debt wavier of 2008. Meanwhile the government has made another plan to provide overdraft facility or term loan up to Rs.10, 000/- to agricultural land less farmers. These credit facilities will be provided to them on the b asis of guarantee of another agricultural landless labour. The banks will not c ompel them to mortgage their properties against the said loan. The ministry of finance has already taken initiative in this direction. To meet the criteria for the loan, PSUs have been asked to make a list of eligible landless agricultural labourers. The Government’s intention behind this exercise is to increase consumption level of workers. The Congress-led government opines that landless agricultural labourers in villages are not capable to survive due to rising inflation. Even, they are incapable to fulfil their everyday requirements smoothly. To put together bread and butter on regular basis is beyond their capability.

-

Upload

vegesna-raju -

Category

Documents

-

view

220 -

download

0

Transcript of clearin MS2003

8/3/2019 clearin MS2003

http://slidepdf.com/reader/full/clearin-ms2003 1/12

Public sector banks have settled about 30% of their NPA (non-performing assets) cases

for which they issued notices under the Securitisation and Reconstruction of Financial

Assets and Enforcement of Security Interest (Sarfaesi) Act 2002.

A total of 33,736 notices under the Sarfaesi Act were issued by 20 nationalised banks and the

subsidiaries of SBI for recovery of Rs 12,147 crore after the enactment of the Act. These bankstogether have settled 9,946 cases, according to data compiled by CMIE.

Though the percentage of dispute cases settled till June ‘03 amount to 29.5%, in terms of value

it amounts to a paltry Rs 499 crore only, accounting for just 4.1% of the total outstanding

amount for which notices were issued.

State Bank of India and its subsidiaries together have recovered Rs 83 crore out of Rs 4,771

crore loan outstanding for which they had issued notices till June ‘03. Similarly, Punjab National

Bank and Canara Bank, which had sent 3,015 and 1,011 notices respectively for recovery of

loans amounting to Rs 711 crore and Rs 350 crore, have recovered Rs 39.3 crore and Rs 34.5crore respectively till June ‘03.

While banks succeeded in getting their smaller clients to pay up on the strength of the new Act,

a good number of companies with large amounts in outstanding against them continue to defy

the banks’ notices. With the recent ruling by Supreme Court (upholding the Act), banks are now

confident of a faster recovery of dues.

Public Sector Banks (PSUs) have still facing tribulations shimmering from debt wavier of 2008. Meanwhile the

government has made another plan to provide overdraft facility or term loan up to Rs.10, 000/- to

agricultural land less labours.

PUBLIC SECTOR units (PSUs) are still facing tribulations shimmering from debt wavier

of 2008. Meanwhile the government has made another plan to provide overdraft facility

or term loan up to Rs.10, 000/- to agricultural land less farmers. These credit facilities

will be provided to them on the basis of guarantee of another agricultural landless

labour. The banks will not compel them to mortgage their properties against the said

loan.

The ministry of finance has already taken initiative in this direction. To meet the criteria

for the loan, PSUs have been asked to make a list of eligible landless agriculturallabourers.

The Government’s intention behind this exercise is to increase consumption level of

workers. The Congress-led government opines that landless agricultural labourers in

villages are not capable to survive due to rising inflation. Even, they are incapable to

fulfil their everyday requirements smoothly. To put together bread and butter on

regular basis is beyond their capability.

8/3/2019 clearin MS2003

http://slidepdf.com/reader/full/clearin-ms2003 2/12

The government fears that if the stipulation does not improve, growth will be sluggish.

Since monetary and fiscal measures have failed to provide the pace of development

intensity. The Government feels that by adopting non-traditional methods, they may be

successful in its objectives.

In 1980, the PSUs had been selected by the government for escalation of welfare plansat grassroots level. In this way the loans were distributed by PSUs at that time were

drowned later on. To complete the cycle of Government’s welfare plans, PSU’s profit

has always remained in stagger. Levels of Non Performing Asset (NPA) have also

augmented significantly. Despite, the government is going to make the same blunder

again.

The recent statement of the Congress-led UPA government is going to create confusion

and controversy. The one side it is forcing the PSU’s to issue Kisan Credit Cards (KCC)

in more and more numbers to honest farmers, whereas it was disseminated debt waiver

in 2008 among tainted farmers. How will two contradictory aspects come together in

same platform?

Anyway, the government is saying that it will generate demand for diverse products

through this work out and it will result in the production of more food grains. Clear that

it will strengthen the economy and rural India can be saved from impending recession.

The debt waiver of 40, 000 million rupees was dispersed among defaulted farmers in

2008. Whole process was completed keeping in mind arriving general election of

parliament in 2009. It was just gimmick of appease the certain class of rural India, So

that, they could manage their win with comfortable margin in election.

Obviously the debt waiver has not yielded any affirmative domino effect. Most

beneficiaries of loan waiver are still deceitful. Yes, some farmers were truthful, but they

have also become fraudulent. Today, finding an honest farmers just like an exercise of

finding gold particles in sand.

Bankers and rich farmers were manipulated the fund of debt waiver profoundly. Their

modus operandi was simple. The Bankers were prepared forged list of eligible farmers

and in that list, they were included the name of influential farmers and after getting the

fund of debt waiver, they circulated their share among like minded Bank’s employees &

farmers.

Lately internal auditors of APEX Bank of Madhya Pradesh have disclosed fraud of million

& million rupees in delivery of debt waiver scheme of 2008. Several cases of incorrect

data of eligible farmers submitted by banks have come to light. Deliberately advantage

of debt waiver was prearranged to inept farmers. The entire process is glare example of

ignorance of Bankers concerning circulars of debt waiver or is also sheer violation of

RBI’sguidelines.

8/3/2019 clearin MS2003

http://slidepdf.com/reader/full/clearin-ms2003 3/12

It seems that the government has not learnt the lesson from Bankruptcy of Maharaja.

In 1980, profitability margin of PSU’s was under stress on account of such kind of

welfare schemes of the Government.

Nobody denies the importance of welfare schemes in democratic country like India, butits benefit must be reach up to beneficiaries also. In present circumstances, advantage

goes in the pocket of brokers, leaders or corrupt officials. Hence, the Government

should not turn away from its duty. Of course, the same is brought to the beneficiaries'

benefit.

Mumbai: In a move that will ease pressure on bank profits, Reserve Bank of India has said that

an earlier guideline requiring additional funds to be set aside for bad loans will not apply to loans

that turn bad after September 2010.

This move will benefit all lenders as RBI has now specified the end point for setting aside

additional provisions on bad loans. These guidelines on additional provisions were issued in

October 2009 after banks turned in large profits following a bounce back from the global

financial crisis.

At that time, the central bank had said that the idea was to build up a capital buffer during good

times so that it could be used if the outlook for the economy changes. suddenly

State Bank of India will gain directly from this measure as RBI has said that even for those banks

that have not achieved the prescribed provision coverage ratio, the target date continues to be

September 30, 2010. SBI has been struggling to meet the 70% PCR and was expected to meetthe target in the current fiscal. "Some of the banks that had been granted extension of time

beyond the stipulated date for achieving the PCR of 70% on their request should calculate the

required provisions for 70% PCR as on September 30, 2010 and compute the shortfall there

from," said RBI "What this means is that after making provisions for NPAs as on September 2010,

banks will only need to make the normal provisions for bad loans and the additional burden on

the balance sheet will cease. But going forward, provision requirement could get stiffer as

regulators move towards advanced accounting standards," said the chairman of a public sector

bank.

But banks that have already made a provision will need to keep it aside as an additional buffer."The surplus of the provision under PCR vis-Ã -vis as required according to prudential norms

should be segregated into an account styled as countercyclical provisioning buffer. This buffer

will be allowed to be used by banks for making specific provisions for NPAs during periods of

system-wide downturn with the prior approval of RBI," the central bank said.In a recent report

on the banking sector, Care ratings had said that banks had improved its provision coverage ratio

to 58.31% by end-December 2010 from 52.85% a year back.

8/3/2019 clearin MS2003

http://slidepdf.com/reader/full/clearin-ms2003 4/12

Private banks have already crossed RBI's prescriptions by achieving a PCR of 74% as against 70%

mandated by RBI but public sector banks continued to lag with a PCR of 54.41%. "On an overall

basis, provisioning expenses rose by 54.48% on y-o-y basis in 9MFY11 on back of higher NPA

provisioning by banks to achieve the RBI mandated 70% NPA provision coverage," Care said.

Since 1970s, the SCBs functioned as units cut off from international banking and unable toparticipate in the structural transformations and new types of lending products.

Audit and control functions were not independent and thus unable to correct the effect of

serious flaws in policies and directions

Banks were not sufficiently developed in terms of skills and expertise to regulate the

humongous growth in credit and manage the diverse risks that emerged in the proc and

directions

Banks were not sufficiently developed in terms of skills and expertise to regulate the

humongous growth in credit and manage the diverse risks that emerged in the process

Compromise Settlement Schemes

Restructuring / Reschedulement

Lok Adalat

Corporate Debt Restructuring Cell

Debt Recovery Tribunal (DRT)

Proceedings under the Code of Civil Procedure

Board for Industrial & Financial Reconstruction (BIFR)/ AAIFR

National Company Law Tribunal (NCLT)

Sale of NPA to other banks

Sale of NPA to ARC/ SC under Securitization and Reconstruction of Financial Assets and

Enforcement of Security Interest Act 2002 (SRFAESI)

Liquidation

Small NPAs up to Rs.20 Lacs

Speedy Recovery

Veil of Authority

8/3/2019 clearin MS2003

http://slidepdf.com/reader/full/clearin-ms2003 5/12

Soft Defaulters

Less expensive

Easier way to resolve

The banks and FIs can enforce their securities by initiating recovery proceeding under the

Recovery if Debts due to Banks and FI act, 1993 (DRT Act) by filing an application for

recovery of dues before the Debt Recovery Tribunal constituted under the Act.

On adjudication, a recovery certificate is issued and the sale is carried out by an

auctioneer or a receiver.

DRT has powers to grant injunctions against the disposal, transfer or creation of third

party interest by debtors in the properties charged to creditor and to pass attachment

orders in respect of charged properties

In case of non-realization of the decreed amount by way of sale of the charged properties,

the personal properties if the guarantors can also be attached and sold.

However, realization is usually time-consuming

Steps have been taken to create additional benches

The banks and FIs can enforce their securities by initiating recovery proceeding under the

Recovery if Debts due to Banks and FI act, 1993 (DRT Act) by filing an application for

recovery of dues before the Debt Recovery Tribunal constituted under the Act.

On adjudication, a recovery certificate is issued and the sale is carried out by an

auctioneer or a receiver.

DRT has powers to grant injunctions against the disposal, transfer or creation of third

party interest by debtors in the properties charged to creditor and to pass attachment

orders in respect of charged properties

In case of non-realization of the decreed amount by way of sale of the charged properties,

the personal properties if the guarantors can also be attached and sold.

However, realization is usually time-consuming

Steps have been taken to create additional benches

for claims below Rs.10 lacs, the banks and FIs can initiate proceedings under the Code of

Civil Procedure of 1908, as amended, in a Civil court.

The courts are empowered to pass injunction orders restraining the debtor through itself

8/3/2019 clearin MS2003

http://slidepdf.com/reader/full/clearin-ms2003 6/12

or through its directors, representatives, etc from disposing of, parting with or dealing in

any manner with the subject property.

Courts are also empowered to pass attachment and sales orders for subject property before

udgment, in case necessary.

The sale of subject property is normally carried out by way of open public auction subject

to confirmation of the court.

The foreclosure proceedings, where the DRT Act is not applicable, can be initiated under

the Transfer of Property Act of 1882 by filing a mortgage suit where the procedure is

same as laid down under the CPC.

A NPA is eligible for sale to other banks only if it has remained a NPA for at least two

years in the books of the selling bank

The NPA must be held by the purchasing bank at least for a period of 15 months before itis sold to other banks but not to bank, which originally sold the NPA.

The NPA may be classified as standard in the books of the purchasing bank for a period

of 90 days from date of purchase and thereafter it would depend on the record of recovery

with reference to cash flows estimated while purchasing

The bank may purchase/ sell NPA only on without recourse basis

If the sale is conducted below the net book value, the short fall should be debited to P&L

account and if it is higher, the excess provision will be utilized to meet the loss on

account of sale of other NPA.

Compromise Settlement Schemes

Restructuring / Reschedulement

Lok Adalat

Corporate Debt Restructuring Cell

Debt Recovery Tribunal (DRT)

Proceedings under the Code of Civil Procedure

Board for Industrial & Financial Reconstruction (BIFR)/ AAIFR

National Company Law Tribunal (NCLT)

8/3/2019 clearin MS2003

http://slidepdf.com/reader/full/clearin-ms2003 7/12

Sale of NPA to other banks

Sale of NPA to ARC/ SC under Securitization and Reconstruction of Financial Assets and Enforcement of

Security Interest Act 2002 (SRFAESI)

Liquidation

Chapter II of SARFESI provides for setting up of reconstruction and securitization companies for

acquisition of financial assets from its owner, whether by raising funds by such company from qualified

institutional buyers by issue of security receipts representing undivided interest in such assets or

otherwise.

The ARC can takeover the management of the business of the borrower, sale or lease of a part or whole

of the business of the borrower and rescheduling of payments, enforcement of security interest,

settlement of dues payable by the borrower or take possession of secured assets

Additionally, ARCs can act as agents for recovering dues, as manager and receiver.

Drawback – differentiation between first charge holders and the second charge holders

The second amendment and SARFESI are a leap forward but requirement exists to make the laws

predictable, transparent and affordable enforcement by efficient mechanisms outside of insolvency

No definite time frame has been provided for various stages during the liquidation proceedings

Need is felt for more creative and commercial approach to corporate entities in financial distress and

attempts to revive rather than applying conservative approach of liquidation

Does not introduce the required roadmap of the bankruptcy proceeding viz:

Application for initiating

Appointments & empowerment of trustee

Operational and functional independence

Accountability to court

Monitoring and time bound restructuring

Mechanism to sell off

Number of time bound attempts for restructuring

Decision to pursue insolvency and winding up

Strategies for realization and distribution

Need for new laws & procedures to handle bankruptcy proceedings in consultation with RBI

8/3/2019 clearin MS2003

http://slidepdf.com/reader/full/clearin-ms2003 8/12

NEGOTIATION PROCESS FOR SETTLEMENT OF

NON PERFORMING ASSETS

Factors AffectinBank’s Documentation.

Security value. Realizable sale value.

Bank’s ability to sell.

Ability & Source of the borrower.

Ability & Source of the guarantor.

Vulnerability of the borrower/guarantor.

Time frame.

Strength and Zeal of bank's field staff.

What message is bank sending out (No in a fraud case.)

Banks Policy.

Success rate.

g the Acceptance

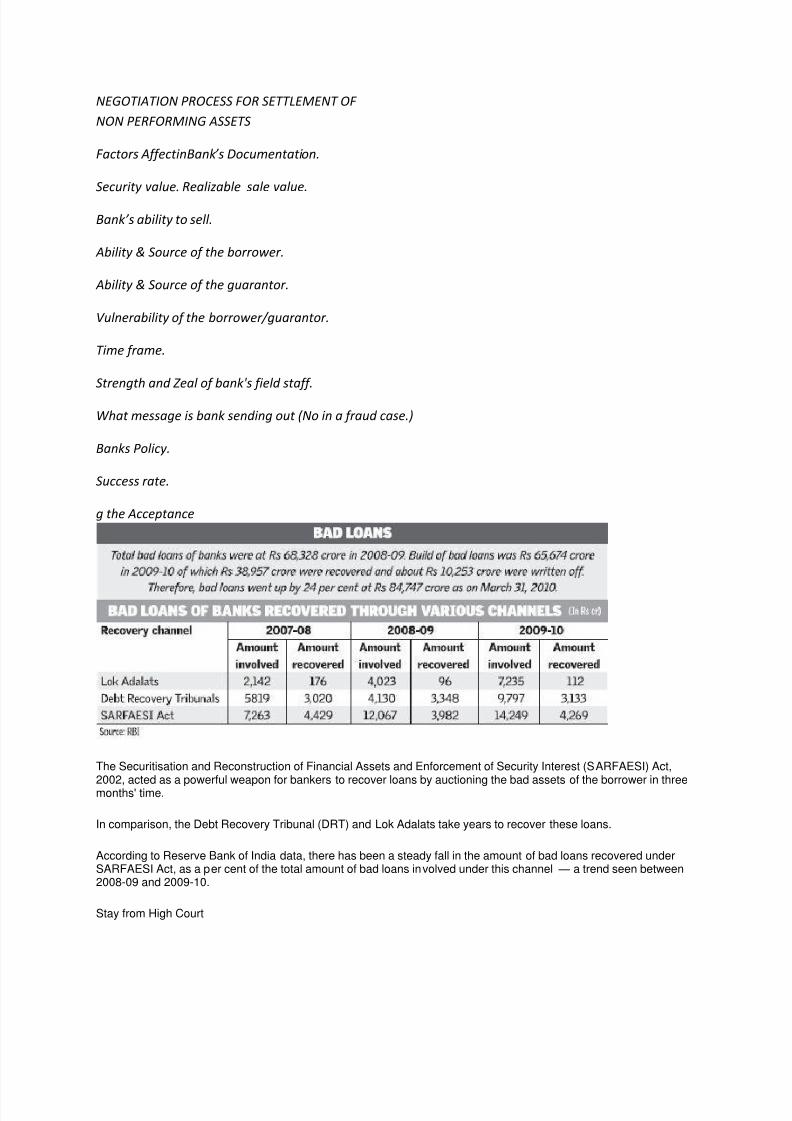

The Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest (SARFAESI) Act,

2002, acted as a powerful weapon for bankers to recover loans by auctioning the bad assets of the borrower in threemonths' time.

In comparison, the Debt Recovery Tribunal (DRT) and Lok Adalats take years to recover these loans.

According to Reserve Bank of India data, there has been a steady fall in the amount of bad loans recovered underSARFAESI Act, as a per cent of the total amount of bad loans involved under this channel — a trend seen between2008-09 and 2009-10.

Stay from High Court

8/3/2019 clearin MS2003

http://slidepdf.com/reader/full/clearin-ms2003 9/12

Mr A.K. Bansal, Executive Director, Indian Overseas Bank, said that big borrowers with outstandings of over Rs 10crore, stall the bank's efforts in taking possession of assets under SARFAESI Act, by getting a stay from the HighCourt or the Debt Recovery Tribunal.

A senior General Manager of a public sector bank said that nine out of 10 borrowers, who have been issued noticesunder SARFAESI, take banks to DRT to buy time.

No civil court (with the exception of the High Court) has judiciary powers when it comes to SARFAESI Act (Section34).

Under the Securitisation Act, banks should be able to recover their bad debt in three months' time (with a noticeperiod of 60 days). However, due to a large number of cases pending with the judiciary, it takes close to a year ormore before banks can take possession of the property for auction, said the General Manager.

Currently, Indian Bank has issued SARFAESI notices to about 10,000 bad loans amounting to Rs 1,000 crore.

Sluggish property market

Adding to the banks' woes is the sluggish nature of the property market in the last two years, due to which bankswere unable to recover the loan amount from such auctions.

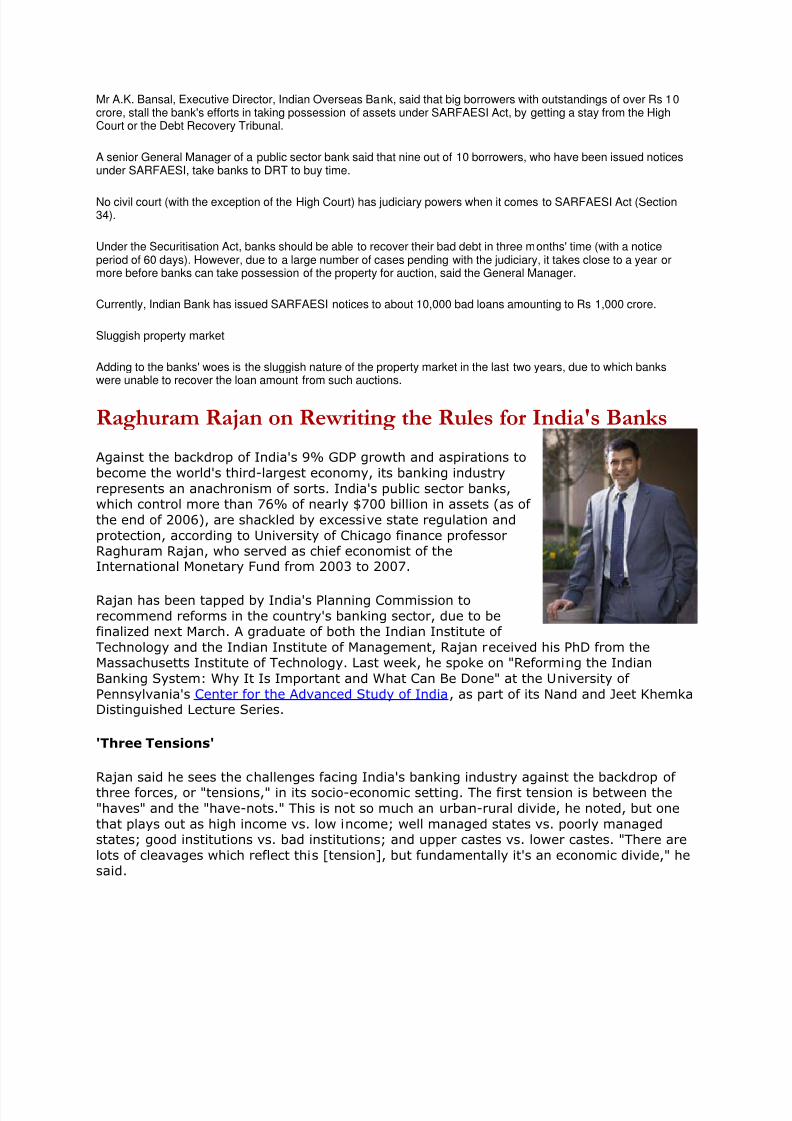

Raghuram Rajan on Rewriting the Rules for India's Banks

Against the backdrop of India's 9% GDP growth and aspirations to

become the world's third-largest economy, its banking industry

represents an anachronism of sorts. India's public sector banks,which control more than 76% of nearly $700 billion in assets (as of

the end of 2006), are shackled by excessive state regulation and

protection, according to University of Chicago finance professorRaghuram Rajan, who served as chief economist of theInternational Monetary Fund from 2003 to 2007.

Rajan has been tapped by India's Planning Commission to

recommend reforms in the country's banking sector, due to befinalized next March. A graduate of both the Indian Institute of

Technology and the Indian Institute of Management, Rajan received his PhD from theMassachusetts Institute of Technology. Last week, he spoke on "Reforming the Indian

Banking System: Why It Is Important and What Can Be Done" at the University of

Pennsylvania's Center for the Advanced Study of India, as part of its Nand and Jeet KhemkaDistinguished Lecture Series.

'Three Tensions'

Rajan said he sees the challenges facing India's banking industry against the backdrop of three forces, or "tensions," in its socio-economic setting. The first tension is between the

"haves" and the "have-nots." This is not so much an urban-rural divide, he noted, but one

that plays out as high income vs. low income; well managed states vs. poorly managedstates; good institutions vs. bad institutions; and upper castes vs. lower castes. "There are

lots of cleavages which reflect this [tension], but fundamentally it's an economic divide," hesaid.

8/3/2019 clearin MS2003

http://slidepdf.com/reader/full/clearin-ms2003 10/12

The second tension "is between the private sector and the public sector, or between themarkets and the state," Rajan continued. He pointed out that a common reading of this

"clash" is that it represents the rich-poor divide, where the markets are seen as favoring the

rich and the state as fighting on behalf of the poor. "This is where the wires get crossed inIndia," he said. "It is not necessarily [true] that currently or going forward, the state isdoing the right thing by the poor. In fact, what is happening is the state is treating the poor

miserably."

Rajan said the third clash is one "between the foreign and the domestic sectors," and that

this is compounded by the first two tensions. "These three tensions are all intertwined in theexample of the banking sector," he said.

To help India's public sector banks improve their financial health and promote growth andinvestment without having to constantly look over their shoulder at the government, the

rules need to be rewritten, Rajan said. "If we don't do the right things, it is quite possiblethat the state will be hijacked by the oligarchy and India will become a very differentcountry from the [one] we know now. That is a danger. I'm not saying it is about to happenor it's on the cards, but it is a possibility we have to keep track of."

A Dismal Record

Pointing to the track record of India's public sector banks (28 in all), Rajan argued that

state control has failed to meet the policy goals of providing credit access to the poor and

the underserved sections of society. Further, those goals have been thwarted by corruption,political meddling and largesse through loan waivers, he noted, adding that the prevailingenvironment has also impeded technological progress at India's public sector banks, and

proven a drag on their debt recovery and eventually their financial performance.

According to Rajan, the Indian central bank -- the Reserve Bank of India -- is also unhelpful,

with its directed lending policies and reserve requirements that favor banks' investments ingovernment bonds or state-approved securities. Currently, Indian banks are required to set

aside 40% of their net credit at below-market rates for the so-called "priority sectors,"including the agricultural sector, small-scale industries, retail trade and housing. Foreign

banks have a lower requirement of 32% of net credit. "We are now in a phase where we areprotecting the public sector and that is impeding reforms," he said.

Cash and statutory liquidity reserve requirements for Indian banks take away another

32.5% of their disposable credit, leaving limited elbow room for banks to improveprofitability. Banks have little incentive to stay financially healthy because of an unstated

understanding that the government will bail them out with capital infusions if ever they facethe threat of collapse, Rajan said. He added that compensation caps have hurt the ability of

banks to attract professional managerial talent, and the targeting of bank officers in casesof failed loans has instilled a deep-rooted culture of risk aversion.

"Everything started with bank nationalization in 1969," which included 14 large privatebanks, said Rajan. A second round followed in 1979-80. The 1969 nationalization programhad the stated rationale that India, then a planned economy, was obligated to direct credit

to the needy and underserved, and that private banks preferred to serve private sector

enterprises. Rajan pointed to another, unstated factor: Indira Gandhi, then the country'sprime minister, was "fighting the old guard in the Congress and trying to establish her own

unique brand, and this was her populist phase." Gandhi rode a campaign platform of "GaribiHatao (Banish Poverty)" to a landslide win in the 1971 national elections.

8/3/2019 clearin MS2003

http://slidepdf.com/reader/full/clearin-ms2003 11/12

The newly nationalized banks were compelled to expand their branch network in ruralareas; they were required to open four rural branches for every urban branch license. In the

first couple of years after nationalization, rural India witnessed a dramatic jump in newbranch openings and an explosion of credit availability.

But the policy seemed not to make commercial sense for the banks, Rajan said: They

sharply cut back their rural expansion after the statute which mandated it was repealed adecade later. "The charitable view of that was that there were enough rural branches; the

uncharitable view is that they were no longer forced by the government [to open ruralbranches]," he said.

While the rural binge did expand credit access, did it really achieve policy goals? Rajan saidthere exists "some evidence of poverty alleviation." But, he added, "if you throw money atanything, you are going to alleviate poverty a little bit." On the other hand, he said there is

"very little evidence" that all the additional rural credit helped agricultural investment orgrowth to any meaningful degree -- the most likely reasons being that much of the bankcredit was "misallocated" or not accompanied by sufficient public investment, leading to "alot of wastage."

Bank lending programs were also hijacked by politicians in the post-nationalization years,

said Rajan. "There was significant expansion of loans from banks around election times,

especially in the marginal constituencies where the ruling party had some chance of losingthe elections," he adds.

Price Tags on Loans

Rajan also faults the government for its successive rounds of the "uniquely Indianinvention" of loan melas (loan fairs). He said politicians summoned bank executives to these

"loan fairs," where they were told to whom they should lend. "This was without any credit

evaluation and purely on the politician's word," he said. "Obviously, [the politician's] friendsand relatives got the credit, and obviously they didn't bother to repay [the loans]."

"The problem is, rural India needs credit," said Rajan. "With the attraction of a highlysubsidized rate, do people with the best credit get the loan? The guy who has bribed the

most gets the loan." He cited household surveys where respondents reported paying bribes

of up to 43% of their loan amounts to secure their loans. He said the beneficiary has nointention of paying back the loan, "because that is the only way he can justify the bribe."

Rajan cited other studies that show the average time to get a loan from public sector banks

is 33 weeks, and that banks don't necessarily step forward with credit in times of ruraldistress. He said private sector banks have extended more agricultural credit than their

public sector counterparts in times of drought and in good times, whereas public sectorbanks tended to focus on "consumption credit," or non-emergency financing. "The theory of

nationalization would have it that in times of drought, the public sector banks would do farmore in making loans; that's not happening in terms of social insurance," he said.

Advent of Reforms

With the economic liberalization and reforms of the 1990s came "two extremely far-sightedreports," said Rajan, referring to bank sector reforms suggested by a committee headed by

M. Narasimham, a former governor of the Reserve Bank of India. "Essentially, they laid out

8/3/2019 clearin MS2003

http://slidepdf.com/reader/full/clearin-ms2003 12/12

steps the government could take: lift interest rate controls; reduce the amount thegovernment absorbs from the banking sector; de-politicize lending; professionalize bank

managements; don't force them to open branches in areas where they don't want to go; get

competition by allowing new private banks to be opened; allow foreign banks to come inand expand," he said.

According to Rajan, one of the key Narasimham committee recommendations thegovernment did not act upon was to reduce the level of state ownership in banks. He gave

an example of how state ownership typically interferes with prudent management at a

public sector bank: "If the market is having a really, really bad day, you may get a call fromthe government to put [in] some money and prop it up." Such interference, along with theloan melas and waivers end up saddling public sector banks with low asset quality

portfolios, he said.

In the 1990s, reforms and modernization worked well in another sector -- the stockmarkets, simply because "neither the government nor politicians had any stake in the[incumbent] Bombay Stock Exchange," which was eventually overtaken by the moremodern and technologically advanced National Stock Exchange of India.

Rajan explained why the success with stock market reforms did not occur with the banks:

"The upper middle class and the rich had migrated away from the nationalized banking

system towards foreign banks and the private banks, so the two important constituencies topush for reforms had been taken out of the equation. The nationalized banks are servingmore and more clientele that don't have as much of an economic voice."

However, the Narasimham committee reforms did yield gains on several fronts, said Rajan.

Banks brought down their non-performing assets, shortened debt recovery periods and used

that to expand credit availability for growth. Further, the industry saw increased competitionwith the entry of private banks and newer foreign banks, money market mutual funds and

insurance companies, alongside a booming stock market.

Among the priorities Rajan sees for India's public sector banks is a removal of the unspokengovernment guarantee of a bailout if any of them faces the threat of bankruptcy. "Bank

capital means that if you grow a hole in your balance sheet, you get cut off and you godown the tube or somebody takes you over," he said. "If the government is going to come

in and recapitalize you at that point, what does it mean?" He also would like directed

lending to be done "at the minimum level," and earmarked for "areas that have socialbenefits."

Finally, Rajan dismisses the often-repeated contention that Indian banks must be doingsomething right because the country has so far not faced a single major financial crisis.

"The RBI beat its drums and said we had no crises," he said. "I wouldn't focus too much on

the lack of crises. There is always a risk-return tradeoff." He recalls that Korea, at one time,

had the same per capita GDP as India's, but today it is 16 times as big. "I would settle for afew crises on the way to grow to that level of per capita GDP," he said.

![Compilation 2 Ms2003[1]](https://static.fdocuments.us/doc/165x107/558cf946d8b42a206f8b465d/compilation-2-ms20031.jpg)