Chunghwa Precision Test Tech. Co., Ltd. and Subsidiaries · Chunghwa Precision Test Tech. Co., Ltd....

38

Chunghwa Precision Test Tech. Co., Ltd. and Subsidiaries Consolidated Financial Statements for the Six Months Ended June 30, 2016 and 2015 and Independent Auditors’ Review Report

Transcript of Chunghwa Precision Test Tech. Co., Ltd. and Subsidiaries · Chunghwa Precision Test Tech. Co., Ltd....

Chunghwa Precision Test Tech. Co., Ltd. and Subsidiaries Consolidated Financial Statements for the Six Months Ended June 30, 2016 and 2015 and Independent Auditors’ Review Report

- 1 -

INDEPENDENT AUDITORS’ REVIEW REPORT

The Board of Directors and Stockholders

Chunghwa Precision Test Tech. Co., Ltd.

We have reviewed the accompanying consolidated balance sheets of Chunghwa Precision Test Tech. Co.,

Ltd. and its subsidiaries (the “Company”) as of June 30, 2016 and 2015, and the related consolidated

statements of comprehensive income for the three months ended June 30, 2016 and 2015, and for the six

months ended June 30, 2016 and 2015, as well as the consolidated statements of changes in equity and

cash flows for the six months ended June 30, 2016 and 2015. These consolidated financial statements

are the responsibility of the Company’s management. Our responsibility is to issue a report on these

consolidated financial statements based on our reviews.

We conducted our reviews in accordance with the Statement of Auditing Standards No. 36, “Review of

Financial Statements”, issued by the Auditing Committee of the Accounting Research and Development

Foundation of the Republic of China. A review consists principally of applying analytical procedures to

financial data and making inquiries of persons responsible for financial and accounting matters. It is

substantially less in scope than an audit conducted in accordance with auditing standards generally

accepted in the Republic of China, the objective of which is the expression of an opinion regarding the

financial statements taken as a whole. Accordingly, we do not express such an audit opinion.

Based on our reviews, we are not aware of any material modifications that should be made to the

consolidated financial statements referred to above for them to be in conformity with the Regulations

Governing the Preparation of Financial Reports by Securities Issuers and International Accounting

Standard 34, “Interim Financial Reporting” endorsed by the Financial Supervisory Commission of the

Republic of China.

August 2, 2016

Notice to Readers

The accompanying consolidated financial statements are intended only to present the financial position,

financial performance and cash flows in accordance with accounting principles and practices generally

accepted in the Republic of China and not those of any other jurisdictions. The standards, procedures

and practices to review such consolidated financial statements are those generally accepted and applied

in the Republic of China.

For the convenience of readers, the auditors’ review report and the accompanying consolidated financial

statements have been translated into English from the original Chinese version prepared and used in the

Republic of China. If there is any conflict between the English version and the original Chinese version

or any difference in the interpretation of the two versions, the Chinese-language auditors’ review report

and consolidated financial statements shall prevail.

- 2 -

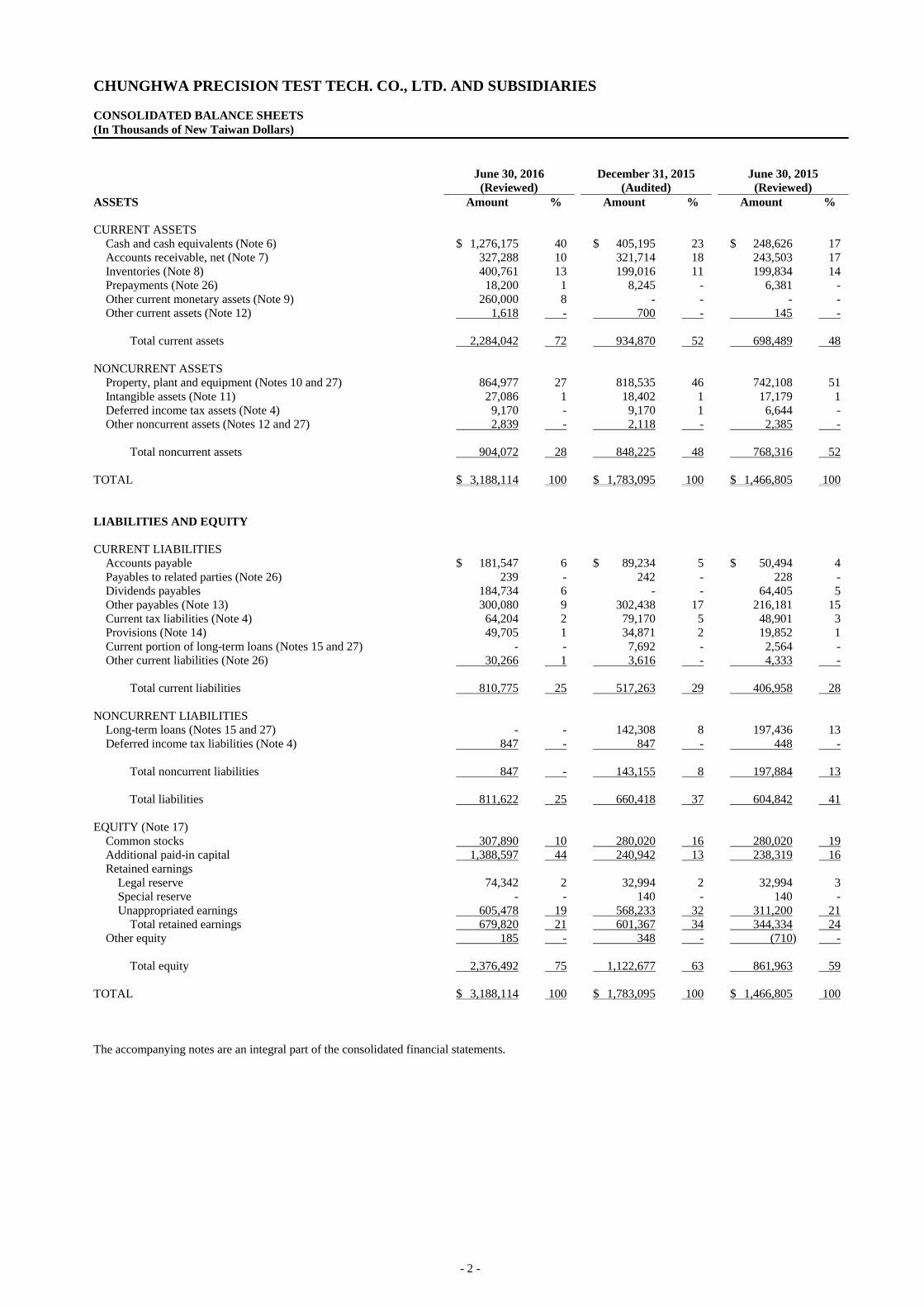

CHUNGHWA PRECISION TEST TECH. CO., LTD. AND SUBSIDIARIES

CONSOLIDATED BALANCE SHEETS

(In Thousands of New Taiwan Dollars)

June 30, 2016

(Reviewed)

December 31, 2015

(Audited)

June 30, 2015

(Reviewed)

ASSETS Amount % Amount % Amount %

CURRENT ASSETS

Cash and cash equivalents (Note 6) $ 1,276,175 40 $ 405,195 23 $ 248,626 17

Accounts receivable, net (Note 7) 327,288 10 321,714 18 243,503 17

Inventories (Note 8) 400,761 13 199,016 11 199,834 14

Prepayments (Note 26) 18,200 1 8,245 - 6,381 -

Other current monetary assets (Note 9) 260,000 8 - - - -

Other current assets (Note 12) 1,618 - 700 - 145 -

Total current assets 2,284,042 72 934,870 52 698,489 48

NONCURRENT ASSETS

Property, plant and equipment (Notes 10 and 27) 864,977 27 818,535 46 742,108 51

Intangible assets (Note 11) 27,086 1 18,402 1 17,179 1

Deferred income tax assets (Note 4) 9,170 - 9,170 1 6,644 -

Other noncurrent assets (Notes 12 and 27) 2,839 - 2,118 - 2,385 -

Total noncurrent assets 904,072 28 848,225 48 768,316 52

TOTAL $ 3,188,114 100 $ 1,783,095 100 $ 1,466,805 100

LIABILITIES AND EQUITY

CURRENT LIABILITIES

Accounts payable $ 181,547 6 $ 89,234 5 $ 50,494 4

Payables to related parties (Note 26) 239 - 242 - 228 -

Dividends payables 184,734 6 - - 64,405 5

Other payables (Note 13) 300,080 9 302,438 17 216,181 15

Current tax liabilities (Note 4) 64,204 2 79,170 5 48,901 3

Provisions (Note 14) 49,705 1 34,871 2 19,852 1

Current portion of long-term loans (Notes 15 and 27) - - 7,692 - 2,564 -

Other current liabilities (Note 26) 30,266 1 3,616 - 4,333 -

Total current liabilities 810,775 25 517,263 29 406,958 28

NONCURRENT LIABILITIES

Long-term loans (Notes 15 and 27) - - 142,308 8 197,436 13

Deferred income tax liabilities (Note 4) 847 - 847 - 448 -

Total noncurrent liabilities 847 - 143,155 8 197,884 13

Total liabilities 811,622 25 660,418 37 604,842 41

EQUITY (Note 17)

Common stocks 307,890 10 280,020 16 280,020 19

Additional paid-in capital 1,388,597 44 240,942 13 238,319 16

Retained earnings

Legal reserve 74,342 2 32,994 2 32,994 3

Special reserve - - 140 - 140 -

Unappropriated earnings 605,478 19 568,233 32 311,200 21

Total retained earnings 679,820 21 601,367 34 344,334 24

Other equity 185 - 348 - (710) -

Total equity 2,376,492 75 1,122,677 63 861,963 59

TOTAL $ 3,188,114 100 $ 1,783,095 100 $ 1,466,805 100

The accompanying notes are an integral part of the consolidated financial statements.

- 3 -

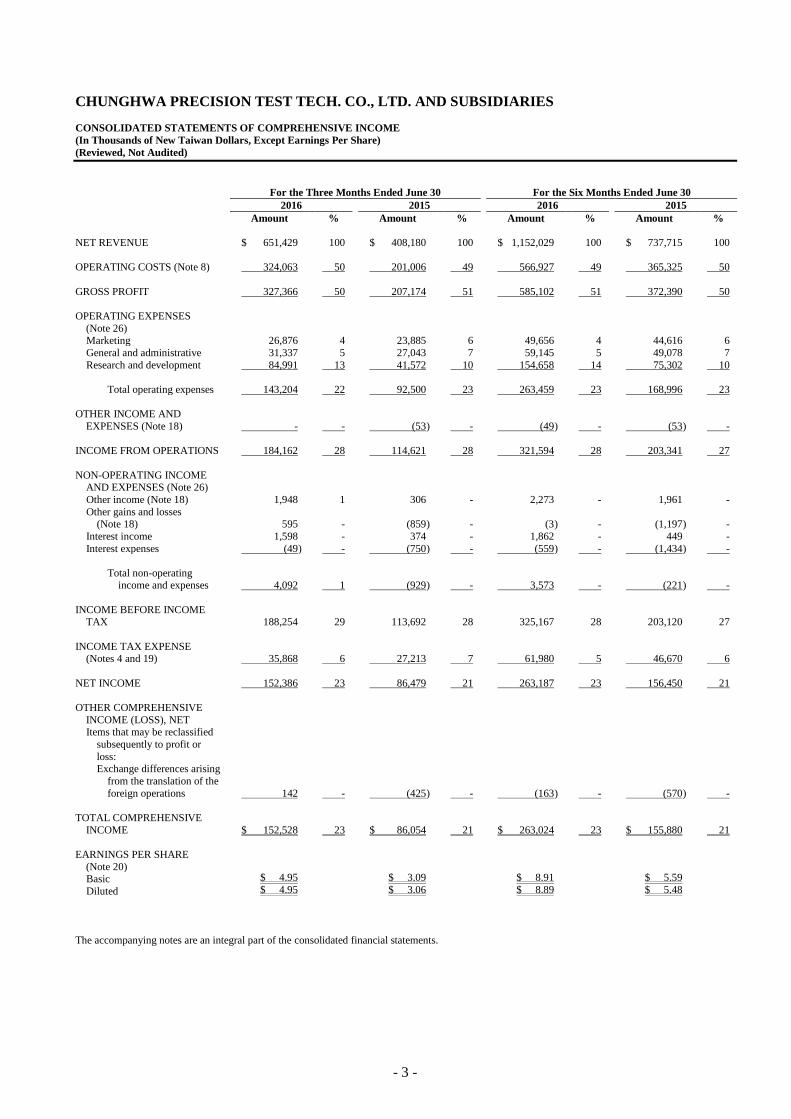

CHUNGHWA PRECISION TEST TECH. CO., LTD. AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME

(In Thousands of New Taiwan Dollars, Except Earnings Per Share)

(Reviewed, Not Audited)

For the Three Months Ended June 30 For the Six Months Ended June 30

2016 2015 2016 2015

Amount % Amount % Amount % Amount %

NET REVENUE $ 651,429 100 $ 408,180 100 $ 1,152,029 100 $ 737,715 100

OPERATING COSTS (Note 8) 324,063 50 201,006 49 566,927 49 365,325 50

GROSS PROFIT 327,366 50 207,174 51 585,102 51 372,390 50

OPERATING EXPENSES

(Note 26) Marketing 26,876 4 23,885 6 49,656 4 44,616 6

General and administrative 31,337 5 27,043 7 59,145 5 49,078 7

Research and development 84,991 13 41,572 10 154,658 14 75,302 10

Total operating expenses 143,204 22 92,500 23 263,459 23 168,996 23

OTHER INCOME AND

EXPENSES (Note 18) - - (53 ) - (49 ) - (53 ) -

INCOME FROM OPERATIONS 184,162 28 114,621 28 321,594 28 203,341 27

NON-OPERATING INCOME AND EXPENSES (Note 26)

Other income (Note 18) 1,948 1 306 - 2,273 - 1,961 -

Other gains and losses (Note 18) 595 - (859 ) - (3 ) - (1,197 ) -

Interest income 1,598 - 374 - 1,862 - 449 -

Interest expenses (49 ) - (750 ) - (559 ) - (1,434 ) -

Total non-operating income and expenses 4,092 1 (929 ) - 3,573 - (221 ) -

INCOME BEFORE INCOME TAX 188,254 29 113,692 28 325,167 28 203,120 27

INCOME TAX EXPENSE (Notes 4 and 19) 35,868 6 27,213 7 61,980 5 46,670 6

NET INCOME 152,386 23 86,479 21 263,187 23 156,450 21

OTHER COMPREHENSIVE

INCOME (LOSS), NET Items that may be reclassified

subsequently to profit or

loss: Exchange differences arising

from the translation of the

foreign operations 142 - (425 ) - (163 ) - (570 ) -

TOTAL COMPREHENSIVE

INCOME $ 152,528 23 $ 86,054 21 $ 263,024 23 $ 155,880 21

EARNINGS PER SHARE

(Note 20) Basic $ 4.95 $ 3.09 $ 8.91 $ 5.59

Diluted $ 4.95 $ 3.06 $ 8.89 $ 5.48

The accompanying notes are an integral part of the consolidated financial statements.

- 4 -

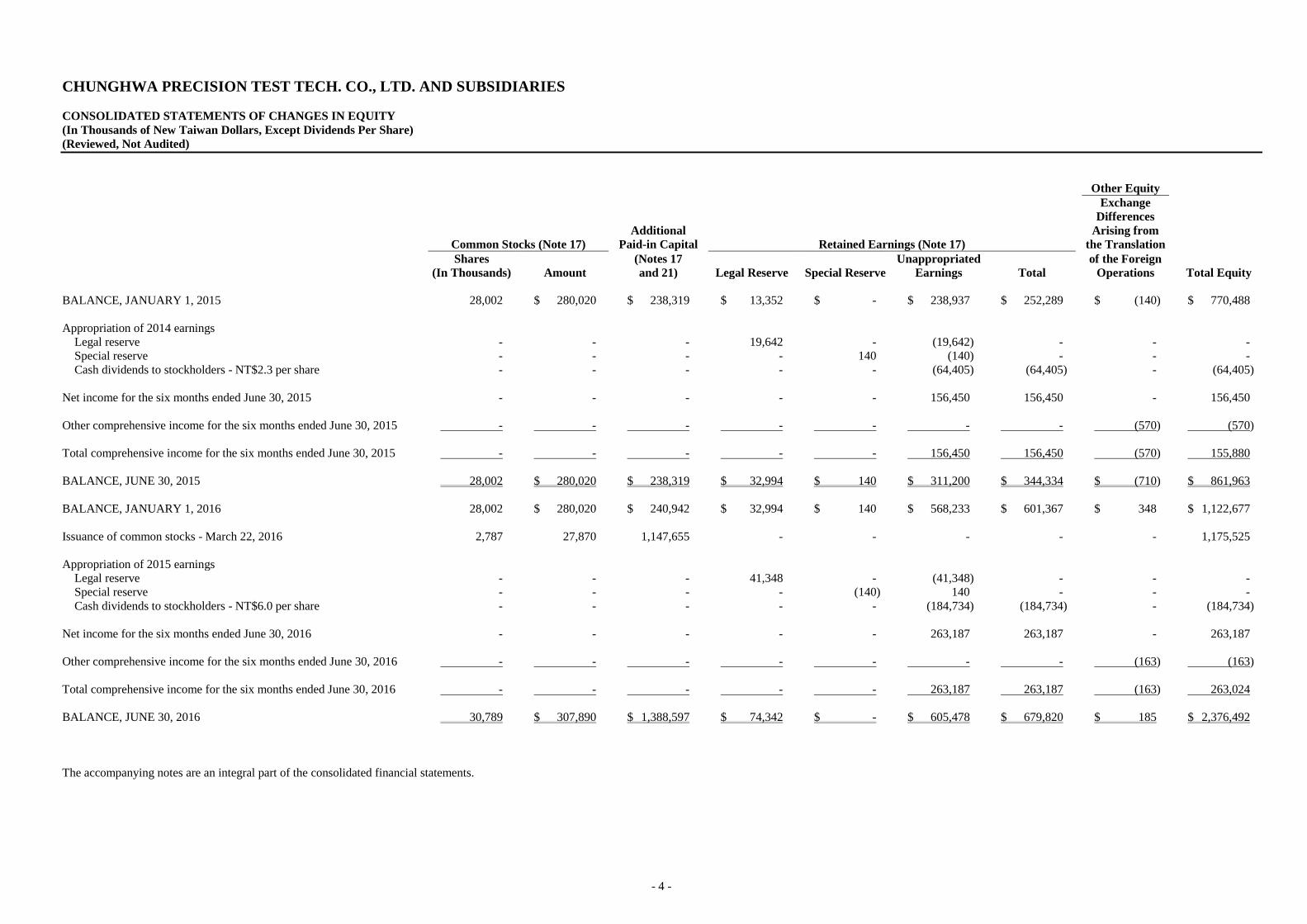

CHUNGHWA PRECISION TEST TECH. CO., LTD. AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF CHANGES IN EQUITY

(In Thousands of New Taiwan Dollars, Except Dividends Per Share)

(Reviewed, Not Audited)

Other Equity

Common Stocks (Note 17)

Additional

Paid-in Capital Retained Earnings (Note 17)

Exchange

Differences

Arising from

the Translation

Shares

(In Thousands) Amount

(Notes 17

and 21) Legal Reserve Special Reserve

Unappropriated

Earnings Total

of the Foreign

Operations Total Equity

BALANCE, JANUARY 1, 2015 28,002 $ 280,020 $ 238,319 $ 13,352 $ - $ 238,937 $ 252,289 $ (140) $ 770,488

Appropriation of 2014 earnings

Legal reserve - - - 19,642 - (19,642) - - -

Special reserve - - - - 140 (140) - - -

Cash dividends to stockholders - NT$2.3 per share - - - - - (64,405) (64,405) - (64,405)

Net income for the six months ended June 30, 2015 - - - - - 156,450 156,450 - 156,450

Other comprehensive income for the six months ended June 30, 2015 - - - - - - - (570) (570)

Total comprehensive income for the six months ended June 30, 2015 - - - - - 156,450 156,450 (570) 155,880

BALANCE, JUNE 30, 2015 28,002 $ 280,020 $ 238,319 $ 32,994 $ 140 $ 311,200 $ 344,334 $ (710) $ 861,963

BALANCE, JANUARY 1, 2016 28,002 $ 280,020 $ 240,942 $ 32,994 $ 140 $ 568,233 $ 601,367 $ 348 $ 1,122,677

Issuance of common stocks - March 22, 2016 2,787 27,870 1,147,655 - - - - - 1,175,525

Appropriation of 2015 earnings

Legal reserve - - - 41,348 - (41,348) - - -

Special reserve - - - - (140) 140 - - -

Cash dividends to stockholders - NT$6.0 per share - - - - - (184,734) (184,734) - (184,734)

Net income for the six months ended June 30, 2016 - - - - - 263,187 263,187 - 263,187

Other comprehensive income for the six months ended June 30, 2016 - - - - - - - (163) (163)

Total comprehensive income for the six months ended June 30, 2016 - - - - - 263,187 263,187 (163) 263,024

BALANCE, JUNE 30, 2016 30,789 $ 307,890 $ 1,388,597 $ 74,342 $ - $ 605,478 $ 679,820 $ 185 $ 2,376,492

The accompanying notes are an integral part of the consolidated financial statements.

- 5 -

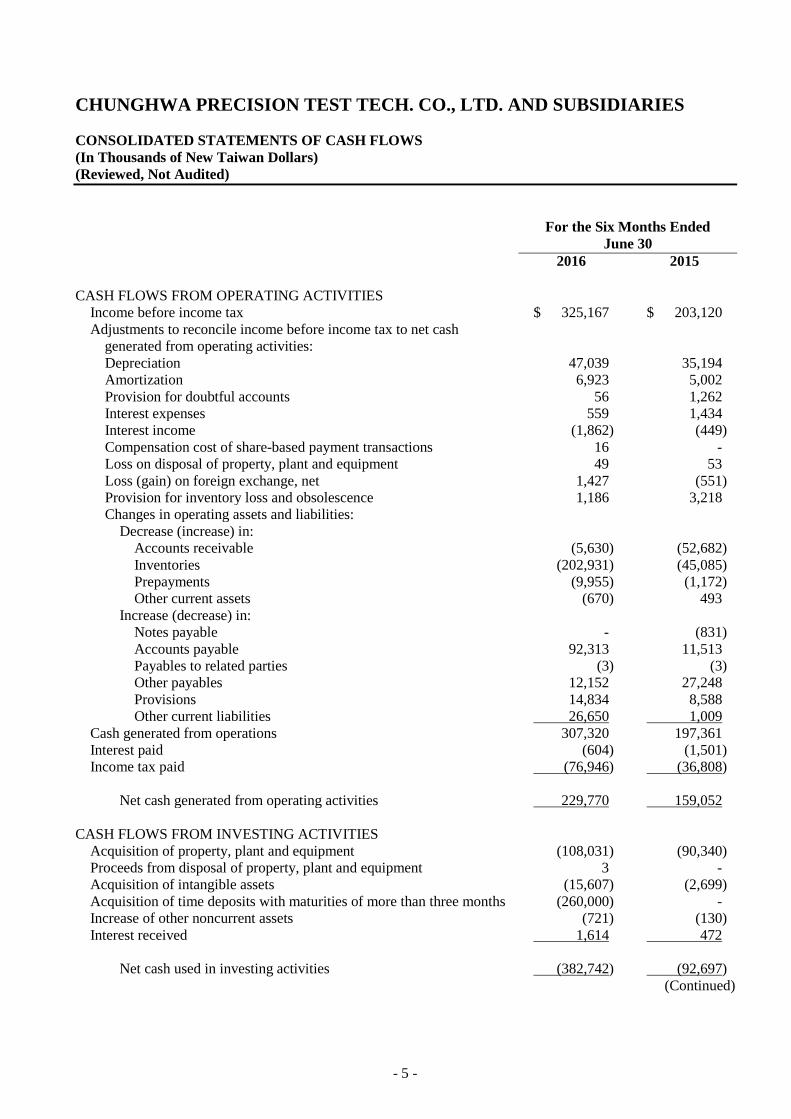

CHUNGHWA PRECISION TEST TECH. CO., LTD. AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF CASH FLOWS

(In Thousands of New Taiwan Dollars)

(Reviewed, Not Audited)

For the Six Months Ended

June 30

2016 2015

CASH FLOWS FROM OPERATING ACTIVITIES

Income before income tax $ 325,167 $ 203,120

Adjustments to reconcile income before income tax to net cash

generated from operating activities:

Depreciation 47,039 35,194

Amortization 6,923 5,002

Provision for doubtful accounts 56 1,262

Interest expenses 559 1,434

Interest income (1,862) (449)

Compensation cost of share-based payment transactions 16 -

Loss on disposal of property, plant and equipment 49 53

Loss (gain) on foreign exchange, net 1,427 (551)

Provision for inventory loss and obsolescence 1,186 3,218

Changes in operating assets and liabilities:

Decrease (increase) in:

Accounts receivable (5,630) (52,682)

Inventories (202,931) (45,085)

Prepayments (9,955) (1,172)

Other current assets (670) 493

Increase (decrease) in:

Notes payable - (831)

Accounts payable 92,313 11,513

Payables to related parties (3) (3)

Other payables 12,152 27,248

Provisions 14,834 8,588

Other current liabilities 26,650 1,009

Cash generated from operations 307,320 197,361

Interest paid (604) (1,501)

Income tax paid (76,946) (36,808)

Net cash generated from operating activities 229,770 159,052

CASH FLOWS FROM INVESTING ACTIVITIES

Acquisition of property, plant and equipment (108,031) (90,340)

Proceeds from disposal of property, plant and equipment 3 -

Acquisition of intangible assets (15,607) (2,699)

Acquisition of time deposits with maturities of more than three months (260,000) -

Increase of other noncurrent assets (721) (130)

Interest received 1,614 472

Net cash used in investing activities (382,742) (92,697)

(Continued)

- 6 -

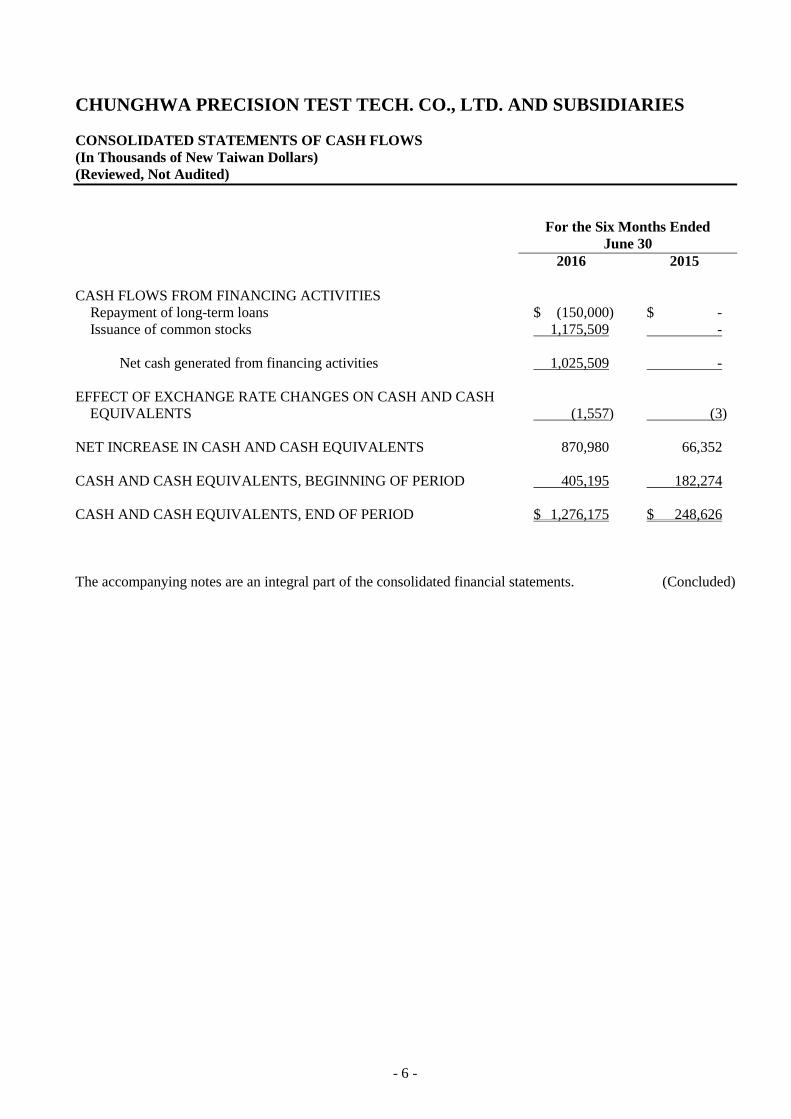

CHUNGHWA PRECISION TEST TECH. CO., LTD. AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF CASH FLOWS

(In Thousands of New Taiwan Dollars)

(Reviewed, Not Audited)

For the Six Months Ended

June 30

2016 2015

CASH FLOWS FROM FINANCING ACTIVITIES

Repayment of long-term loans $ (150,000) $ -

Issuance of common stocks 1,175,509 -

Net cash generated from financing activities 1,025,509 -

EFFECT OF EXCHANGE RATE CHANGES ON CASH AND CASH

EQUIVALENTS (1,557) (3)

NET INCREASE IN CASH AND CASH EQUIVALENTS 870,980 66,352

CASH AND CASH EQUIVALENTS, BEGINNING OF PERIOD 405,195 182,274

CASH AND CASH EQUIVALENTS, END OF PERIOD $ 1,276,175 $ 248,626

The accompanying notes are an integral part of the consolidated financial statements. (Concluded)

- 7 -

CHUNGHWA PRECISION TEST TECH. CO., LTD. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

FOR THE SIX MONTHS ENDED JUNE 30, 2016 AND 2015

(In Thousands of New Taiwan Dollars, Unless Stated Otherwise)

(Reviewed, Not Audited)

1. GENERAL

Chunghwa Precision Test Tech. Co., Ltd. (the “Company,” the Company and its subsidiaries are

collectively referred to as the “Group”) was incorporated on August 26, 2005. The Company engages

mainly in the testing of semiconductor components, production of printed circuit boards and marketing of

electronic products.

The Company’s shares have been listed on the Taipei Exchange (“TPEx”) since March 24, 2016.

Chunghwa Investment Co., Ltd. is the Company’s parent company, which owned 40.79%, 45.68% and

45.68% equity shares of the Company as of June 30, 2016, December 31, 2015 and June 30, 2015,

respectively. The Company’s ultimate parent company is Chunghwa Telecom Co., Ltd.

The consolidated financial statements are presented in the Company’s functional currency, New Taiwan

dollars.

2. APPROVAL OF FINANCIAL STATEMENTS

The consolidated financial statements were approved by the Board of Directors on August 2, 2016.

3. APPLICATION OF NEW AND REVISED STANDARDS AND INTERPRETATIONS

a. International Financial Reporting Standards (IFRS), International Accounting Standards (IAS),

International Financial Reporting Interpretation Committee Interpretations (IFRIC), and Standing

Interpretation Committee Interpretations (SIC) endorsed by the Financial Supervisory Commission

(FSC) will be adopted starting 2017 (collectively, “2017 Taiwan-IFRSs version”).

The FSC issued Rule No. 1050026834 to endorse the following 2017 Taiwan-IFRSs version.

New, Revised or Amended Standards and Interpretations

Effective Date Issued by

IASB (Note 1)

Annual Improvements to IFRSs 2010-2012 Cycle July 1, 2014 (Note 2)

Annual Improvements to IFRSs 2011-2013 Cycle July 1, 2014

Annual Improvements to IFRSs 2012-2014 Cycle January 1, 2016 (Note 3)

Amendments to IFRS 10, IFRS 12 and IAS 28 “Investment Entities:

Applying the Consolidation Exception”

January 1, 2016

Amendment to IFRS 11 “Acquisitions of Interests in Joint

Operations”

January 1, 2016

IFRS 14 “Regulatory Deferral Accounts” January 1, 2016

Amendment to IAS 1 “Disclosure Initiative” January 1, 2016

Amendments to IAS 16 and IAS 38 “Clarification of Acceptable

Methods of Depreciation and Amortization”

January 1, 2016

(Continued)

- 8 -

New, Revised or Amended Standards and Interpretations

Effective Date Issued by

IASB (Note 1)

Amendments to IAS 16 and IAS 41 “Agriculture: Bearer Plants” January 1, 2016

Amendment to IAS 19 “Defined Benefit Plans: Employee

Contributions”

July 1, 2014

Amendment to IAS 36 “Impairment of Assets: Recoverable Amount

Disclosures for Non-financial Assets”

January 1, 2014

Amendment to IAS 39 “Novation of Derivatives and Continuation of

Hedge Accounting”

January 1, 2014

IFRIC 21 “Levies” January 1, 2014

(Concluded)

Note 1: Unless stated otherwise, the above amendments and interpretations are effective for annual

periods beginning on or after their respective effective dates.

Note 2: The amendment to IFRS 2 applies to share-based payment transactions with grant date on or

after July 1, 2014; the amendment to IFRS 3 applies to business combinations with acquisition

date on or after July 1, 2014; the amendment to IFRS 13 is effective immediately; the

remaining amendments are effective for annual periods beginning on or after July 1, 2014.

Note 3: The amendment to IFRS 5 is applied prospectively to changes in a method of disposal that

occur in annual periods beginning on or after January 1, 2016; the remaining amendments are

effective for annual periods beginning on or after January 1, 2016.

The Group does not anticipate the adoption of the 2017 Taiwan-IFRSs version will have material

impacts on the Company’s consolidated financial statements.

b. IFRSs issued by the International Accounting Standards Board (IASB) but not yet endorsed by the FSC.

The Group has not applied the following IFRSs issued by the IASB but not yet endorsed by the FSC.

In addition, the FSC announced that the public companies in Taiwan should apply IFRS 15 starting

January 1, 2018. As of the date the consolidated financial statements were authorized for issue, the

FSC has not announced the effective dates of other new, amended and revised standards and

interpretations.

New, Revised or Amended Standards and Interpretations

Effective Date Issued by

IASB (Note 1)

Amendments to IFRS 2 “Classification and Measurement of

Share-based Payment Transactions”

January 1, 2018

IFRS 9 “Financial Instruments” January 1, 2018

Amendments to IFRS 9 and IFRS 7 “Mandatory Effective Date of

IFRS 9 and Transition Disclosures”

January 1, 2018

Amendments to IFRS 10 and IAS 28 “Sale or Contribution of Assets

between an Investor and its Associate or Joint Venture”

To be determined by IASB

IFRS 15 “Revenue from Contracts with Customers” January 1, 2018

Amendment to IFRS 15 “Clarifications to IFRS 15” January 1, 2018

IFRS 16 “Leases” January 1, 2019

Amendment to IAS 7 “Disclosure Initiative” January 1, 2017

Amendments to IAS 12 “Recognition of Deferred Tax Assets for

Unrealized Losses”

January 1, 2017

Note 1: Unless stated otherwise, the above amendments and interpretations are effective for annual

periods beginning on or after their respective effective dates.

- 9 -

Except for the following item, the application of the above new, revised or amended standards and

interpretations will not have material impact on the Group’s consolidated financial statements:

IFRS 16 “Leases”

IFRS 16 sets out the accounting standards for leases that will supersede IAS 17 and a number of related

interpretations.

Under IFRS 16, if the Group is a lessee, it shall recognize right-of-use assets and lease liabilities for all

leases on the consolidated balance sheets except for low-value and short-term leases. The Group may

elect to apply the accounting method similar to the accounting for operating lease under IAS 17 to the

low-value and short-term leases. On the consolidated statements of comprehensive income, the Group

should present the depreciation expense charged on the right-of-use asset separately from interest

expense accrued on the lease liability; interest is computed by using effective interest method. On the

consolidated statements of cash flows, cash payments for the principal portion of the lease liability are

classified within financing activities; cash payments for interest portion are classified within operating

activities.

The application of IFRS 16 is not expected to have a material impact on the accounting of the Group as

lessor.

When IFRS 16 becomes effective, the Company may elect to apply this Standard either retrospectively

to each prior reporting period presented or retrospectively with the cumulative effect of the initial

application of this Standard recognized at the date of initial application.

Except for the above impact, as of the date the consolidated financial statements were authorized for

issue, the Group is continuously assessing the possible impact that the application of other standards

and interpretations will have on the Group’s financial position and financial performance, and will

disclose the relevant impact when the assessment is completed.

4. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Statement of Compliance

The accompanying consolidated financial statements have been prepared in accordance with the

Regulations Governing the Preparation of Financial Reports by Securities Issuers and IAS 34 “Interim

Financial Reporting” as endorsed by the FSC. The consolidated financial statements do not present all the

disclosures required for a complete set of annual consolidated financial statements.

Basis of Consolidation

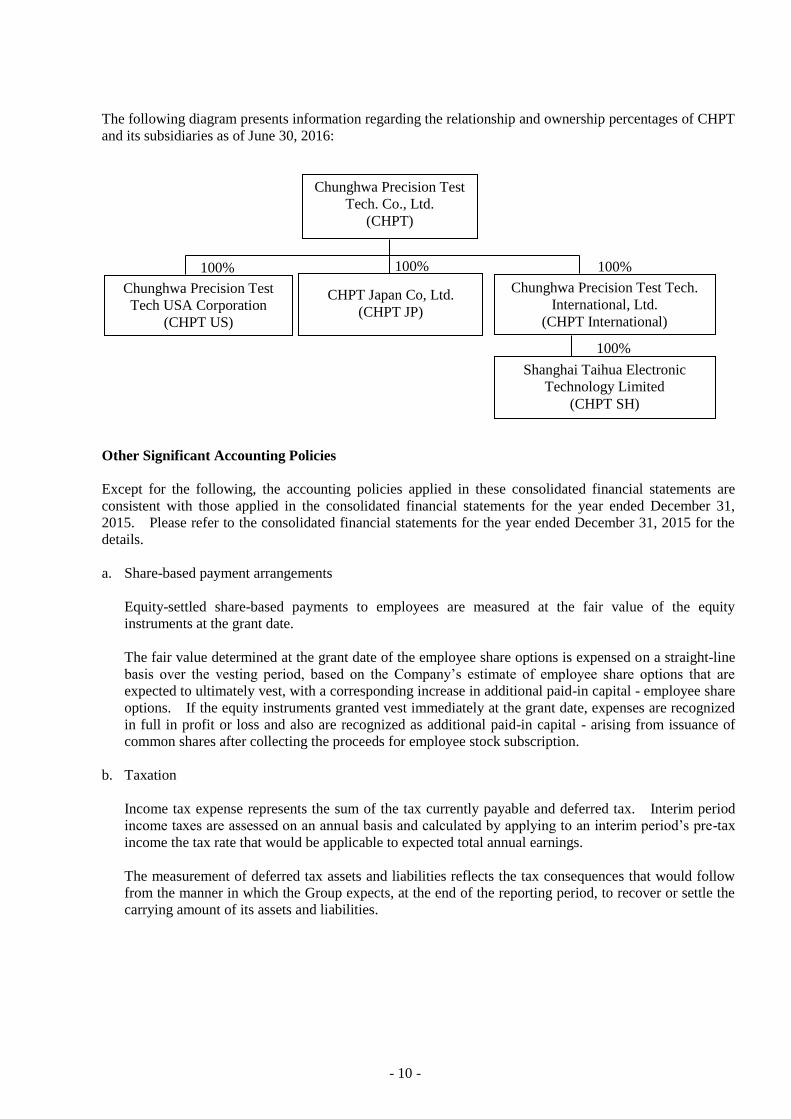

The detail information of the subsidiaries at the end of reporting period was as follows:

Percentage of Ownership

Name of Investor Name of Investee Main Businesses and Products June 30, 2016

December 31,

2015 June 30, 2015

Chunghwa Precision Test Tech.

Co., Ltd.

Chunghwa Precision Test Tech

USA Corporation (CHPT US)

Design of testing of semiconductor

components, production of

printed circuit boards, marketing

of electronic products and after

sales service

100 100 100

CHPT Japan Co., Ltd. (CHPT JP) Sale and maintenance of electronic

parts and machinery processed

products, and design of printed

circuit board

100 100 100

Chunghwa Precision Test Tech.

International, Ltd. (CHPT

International)

Electronic materials wholesale and

retail and investments

100 100 100

Chunghwa Precision Test Tech.

International, Ltd.

Shanghai Taihua Electronic

Technology Limited (CHPT SH)

Design of printed circuit board and

related consultation service

100 100 100

- 10 -

The following diagram presents information regarding the relationship and ownership percentages of CHPT

and its subsidiaries as of June 30, 2016:

Other Significant Accounting Policies

Except for the following, the accounting policies applied in these consolidated financial statements are

consistent with those applied in the consolidated financial statements for the year ended December 31,

2015. Please refer to the consolidated financial statements for the year ended December 31, 2015 for the

details.

a. Share-based payment arrangements

Equity-settled share-based payments to employees are measured at the fair value of the equity

instruments at the grant date.

The fair value determined at the grant date of the employee share options is expensed on a straight-line

basis over the vesting period, based on the Company’s estimate of employee share options that are

expected to ultimately vest, with a corresponding increase in additional paid-in capital - employee share

options. If the equity instruments granted vest immediately at the grant date, expenses are recognized

in full in profit or loss and also are recognized as additional paid-in capital - arising from issuance of

common shares after collecting the proceeds for employee stock subscription.

b. Taxation

Income tax expense represents the sum of the tax currently payable and deferred tax. Interim period

income taxes are assessed on an annual basis and calculated by applying to an interim period’s pre-tax

income the tax rate that would be applicable to expected total annual earnings.

The measurement of deferred tax assets and liabilities reflects the tax consequences that would follow

from the manner in which the Group expects, at the end of the reporting period, to recover or settle the

carrying amount of its assets and liabilities.

Chunghwa Precision Test

Tech. Co., Ltd.

(CHPT)

Shanghai Taihua Electronic

Technology Limited

(CHPT SH)

100%

100%

Chunghwa Precision Test

Tech USA Corporation

(CHPT US)

100%

CHPT Japan Co, Ltd.

(CHPT JP)

Chunghwa Precision Test Tech.

International, Ltd.

(CHPT International)

100%

- 11 -

5. CRITICAL ACCOUNTING JUDGMENTS AND KEY SOURCES OF ESTIMATION

UNCERTAINTY AND ASSUMPTION

In the application of the Group’s accounting policies, the management is required to make judgments,

estimates and assumptions which are based on historical experience and other factors that are not readily

apparent from other sources. Actual results may differ from these estimates.

The estimates and underlying assumptions are reviewed by the management on an ongoing basis.

Revisions to accounting estimates are recognized in the period in which the estimate is revised if the

revision affects only that period or in the period of the revision and future periods if the revision affects

both current and future periods.

For the critical accounting judgments and key sources of estimation uncertainty and assumption applied in

these consolidated financial statements, please refer to the consolidated financial statements for the year

ended December 31, 2015.

6. CASH AND CASH EQUIVALENTS

June 30, 2016

December 31,

2015 June 30, 2015

Cash

Cash on hand $ 150 $ 150 $ 150

Checking and current accounts 549,738 197,188 75,510

Foreign checking and current accounts 184,287 75,857 80,966

734,175 273,195 156,626

Cash equivalents

Time deposits with maturities of less than three

months 542,000 132,000 92,000

$ 1,276,175 $ 405,195 $ 248,626

The annual yield rates of bank deposits and time deposits with maturities of less than three months were as

follows:

June 30, 2016

December 31,

2015 June 30, 2015

Bank deposits 0.001%-0.45% 0.001%-0.43% 0.001%-0.45%

Time deposits with maturities of less than three

months 0.30%-0.73% 0.87% 0.88%-0.94%

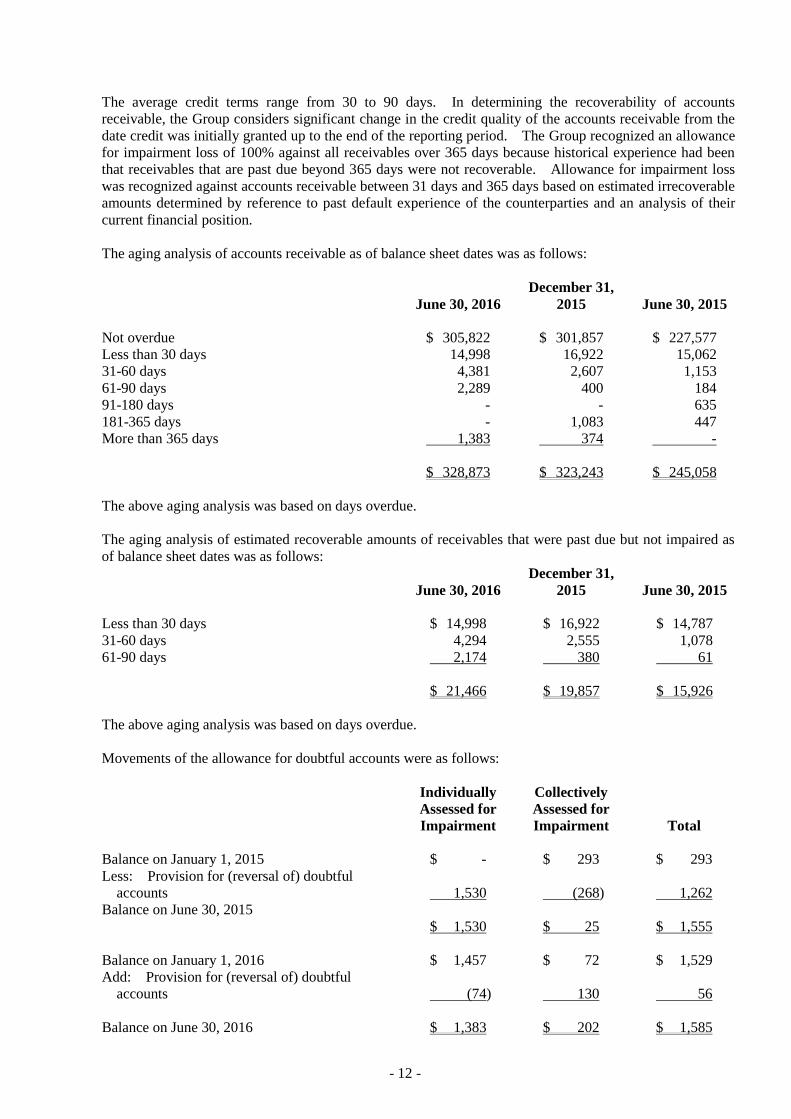

7. ACCOUNTS RECEIVABLE, NET

June 30, 2016

December 31,

2015 June 30, 2015

Accounts receivable $ 328,873 $ 323,243 $ 245,058

Less: Allowance for doubtful accounts (1,585) (1,529) (1,555)

$ 327,288 $ 321,714 $ 243,503

- 12 -

The average credit terms range from 30 to 90 days. In determining the recoverability of accounts

receivable, the Group considers significant change in the credit quality of the accounts receivable from the

date credit was initially granted up to the end of the reporting period. The Group recognized an allowance

for impairment loss of 100% against all receivables over 365 days because historical experience had been

that receivables that are past due beyond 365 days were not recoverable. Allowance for impairment loss

was recognized against accounts receivable between 31 days and 365 days based on estimated irrecoverable

amounts determined by reference to past default experience of the counterparties and an analysis of their

current financial position.

The aging analysis of accounts receivable as of balance sheet dates was as follows:

June 30, 2016

December 31,

2015 June 30, 2015

Not overdue $ 305,822 $ 301,857 $ 227,577

Less than 30 days 14,998 16,922 15,062

31-60 days 4,381 2,607 1,153

61-90 days 2,289 400 184

91-180 days - - 635

181-365 days - 1,083 447

More than 365 days 1,383 374 -

$ 328,873 $ 323,243 $ 245,058

The above aging analysis was based on days overdue.

The aging analysis of estimated recoverable amounts of receivables that were past due but not impaired as

of balance sheet dates was as follows:

June 30, 2016

December 31,

2015 June 30, 2015

Less than 30 days $ 14,998 $ 16,922 $ 14,787

31-60 days 4,294 2,555 1,078

61-90 days 2,174 380 61

$ 21,466 $ 19,857 $ 15,926

The above aging analysis was based on days overdue.

Movements of the allowance for doubtful accounts were as follows:

Individually

Assessed for

Impairment

Collectively

Assessed for

Impairment Total

Balance on January 1, 2015 $ - $ 293 $ 293

Less: Provision for (reversal of) doubtful

accounts 1,530 (268) 1,262

Balance on June 30, 2015

$ 1,530 $ 25 $ 1,555

Balance on January 1, 2016 $ 1,457 $ 72 $ 1,529

Add: Provision for (reversal of) doubtful

accounts (74) 130 56

Balance on June 30, 2016 $ 1,383 $ 202 $ 1,585

- 13 -

The Group recognized impairment loss on accounts receivable in the amounts of $1,383 thousand, $1,457

thousand and $1,530 thousand as of June 30, 2016, December 31, 2015 and June 30, 2015, respectively.

These amounts mainly related to customers that were in severe financial difficulties. The Group did not

hold any collateral over these balances.

8. INVENTORIES

June 30, 2016

December 31,

2015 June 30, 2015

Finished goods $ 210,039 $ 81,773 $ 131,207

Work in process 119,406 68,050 22,745

Raw materials 71,316 49,193 45,882

$ 400,761 $ 199,016 $ 199,834

The cost of goods sold included the valuation loss on inventories of $731 thousand and $0 thousand for the

three months ended June 30, 2016 and 2015, respectively, and the cost of goods sold included the valuation

loss on inventories of $1,186 thousand and $3,218 thousand for the six months ended June 30, 2016 and

2015, respectively.

9. OTHER CURRENT MONETARY ASSETS

June 30, 2016

December 31,

2015 June 30, 2015

Time deposits with maturities of more than three

months $ 260,000 $ - $ -

The annual yield rates of time deposits with maturities of more than three months were as follows:

June 30, 2016

December 31,

2015 June 30, 2015

Time deposits with maturities of more than three

months 0.82%-1.12% - -

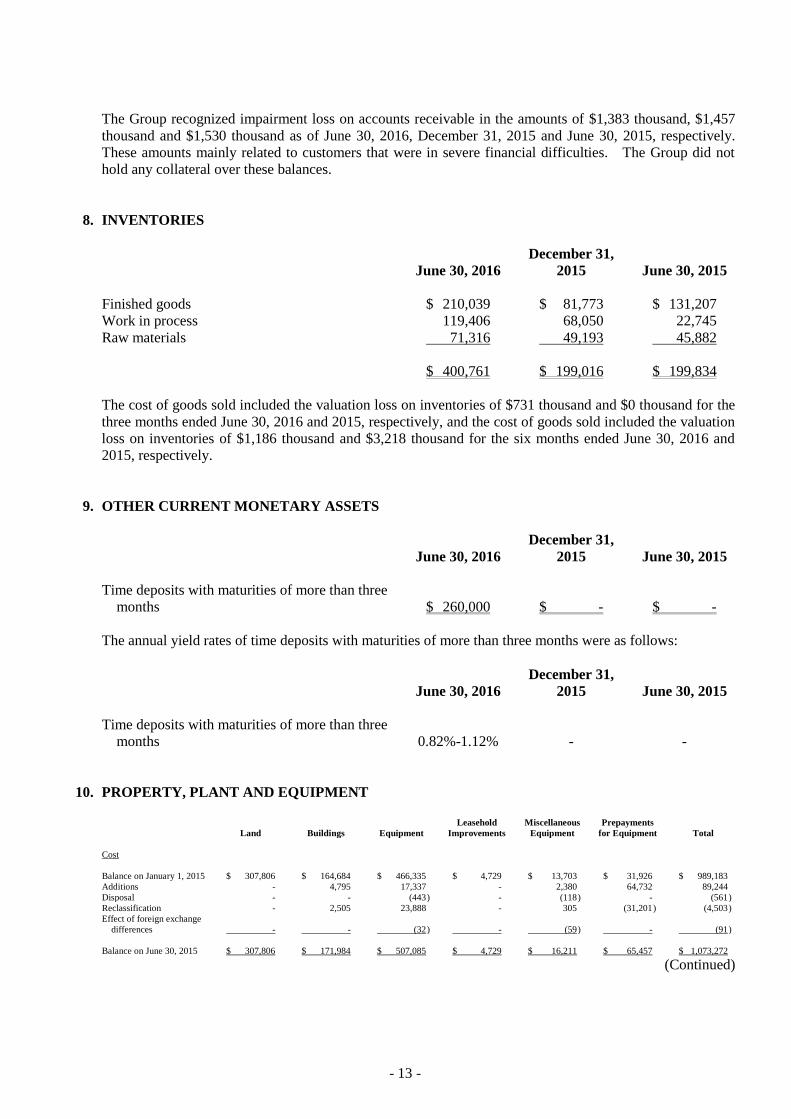

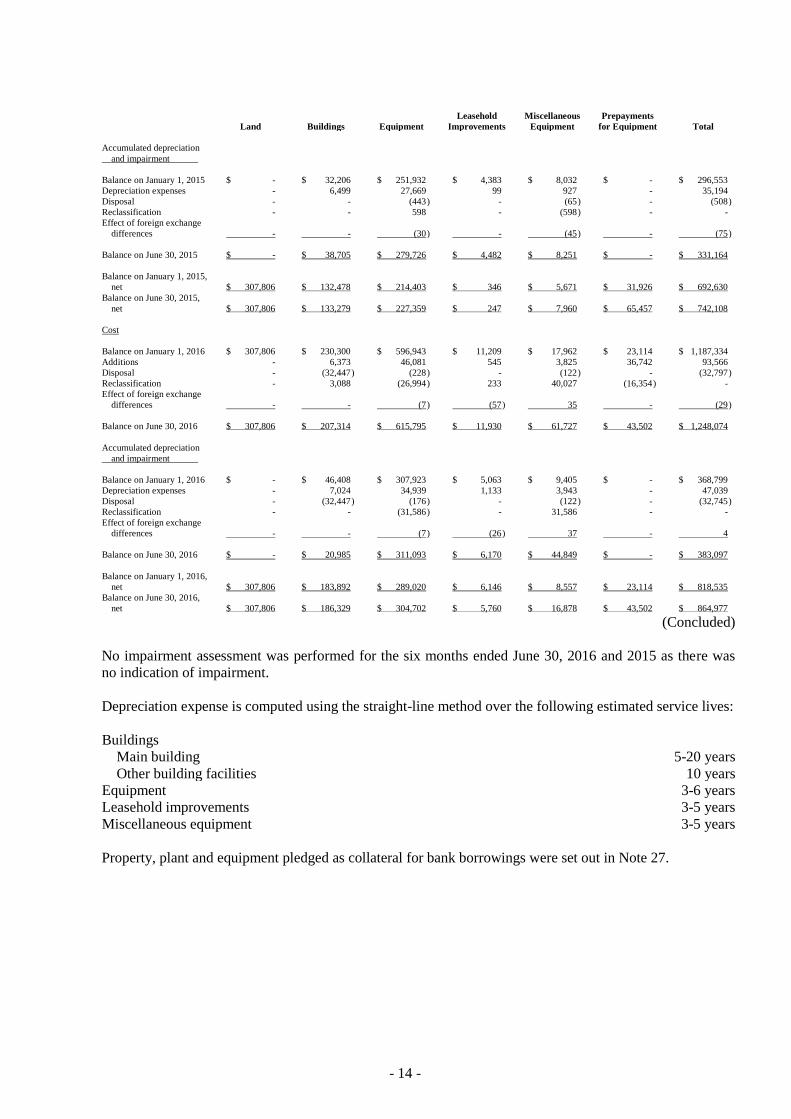

10. PROPERTY, PLANT AND EQUIPMENT

Land Buildings Equipment

Leasehold

Improvements

Miscellaneous

Equipment

Prepayments

for Equipment Total

Cost

Balance on January 1, 2015 $ 307,806 $ 164,684 $ 466,335 $ 4,729 $ 13,703 $ 31,926 $ 989,183

Additions - 4,795 17,337 - 2,380 64,732 89,244

Disposal - - (443 ) - (118 ) - (561 )

Reclassification - 2,505 23,888 - 305 (31,201 ) (4,503 )

Effect of foreign exchange

differences - - (32 ) - (59 ) - (91 )

Balance on June 30, 2015 $ 307,806 $ 171,984 $ 507,085 $ 4,729 $ 16,211 $ 65,457 $ 1,073,272

(Continued)

- 14 -

Land Buildings Equipment

Leasehold

Improvements

Miscellaneous

Equipment

Prepayments

for Equipment Total

Accumulated depreciation

and impairment

Balance on January 1, 2015 $ - $ 32,206 $ 251,932 $ 4,383 $ 8,032 $ - $ 296,553

Depreciation expenses - 6,499 27,669 99 927 - 35,194

Disposal - - (443 ) - (65 ) - (508 )

Reclassification - - 598 - (598 ) - -

Effect of foreign exchange

differences - - (30 ) - (45 ) - (75 )

Balance on June 30, 2015 $ - $ 38,705 $ 279,726 $ 4,482 $ 8,251 $ - $ 331,164

Balance on January 1, 2015,

net $ 307,806 $ 132,478 $ 214,403 $ 346 $ 5,671 $ 31,926 $ 692,630

Balance on June 30, 2015,

net $ 307,806 $ 133,279 $ 227,359 $ 247 $ 7,960 $ 65,457 $ 742,108

Cost

Balance on January 1, 2016 $ 307,806 $ 230,300 $ 596,943 $ 11,209 $ 17,962 $ 23,114 $ 1,187,334

Additions - 6,373 46,081 545 3,825 36,742 93,566

Disposal - (32,447 ) (228 ) - (122 ) - (32,797 )

Reclassification - 3,088 (26,994 ) 233 40,027 (16,354 ) -

Effect of foreign exchange

differences - - (7 ) (57 ) 35 - (29 )

Balance on June 30, 2016 $ 307,806 $ 207,314 $ 615,795 $ 11,930 $ 61,727 $ 43,502 $ 1,248,074

Accumulated depreciation

and impairment

Balance on January 1, 2016 $ - $ 46,408 $ 307,923 $ 5,063 $ 9,405 $ - $ 368,799

Depreciation expenses - 7,024 34,939 1,133 3,943 - 47,039

Disposal - (32,447 ) (176 ) - (122 ) - (32,745 )

Reclassification - - (31,586 ) - 31,586 - -

Effect of foreign exchange

differences - - (7 ) (26 ) 37 - 4

Balance on June 30, 2016 $ - $ 20,985 $ 311,093 $ 6,170 $ 44,849 $ - $ 383,097

Balance on January 1, 2016,

net $ 307,806 $ 183,892 $ 289,020 $ 6,146 $ 8,557 $ 23,114 $ 818,535

Balance on June 30, 2016,

net $ 307,806 $ 186,329 $ 304,702 $ 5,760 $ 16,878 $ 43,502 $ 864,977

(Concluded)

No impairment assessment was performed for the six months ended June 30, 2016 and 2015 as there was

no indication of impairment.

Depreciation expense is computed using the straight-line method over the following estimated service lives:

Buildings

Main building 5-20 years

Other building facilities 10 years

Equipment 3-6 years

Leasehold improvements 3-5 years

Miscellaneous equipment 3-5 years

Property, plant and equipment pledged as collateral for bank borrowings were set out in Note 27.

- 15 -

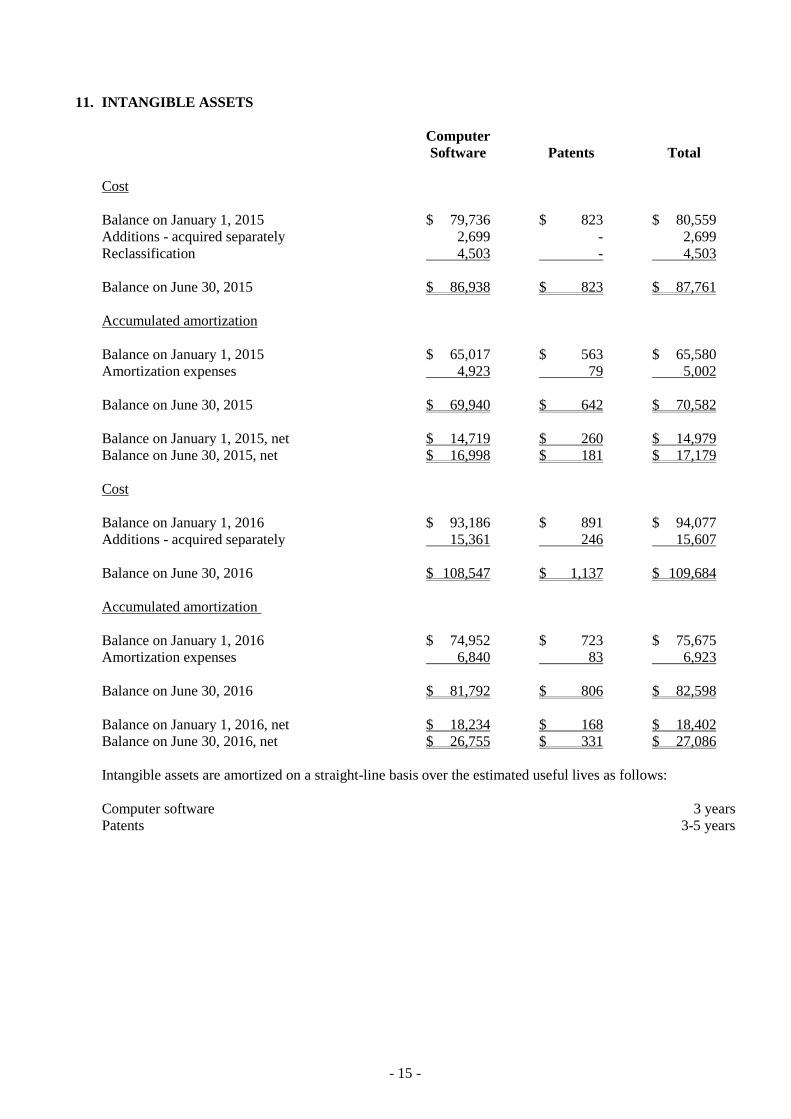

11. INTANGIBLE ASSETS

Computer

Software Patents Total

Cost

Balance on January 1, 2015 $ 79,736 $ 823 $ 80,559

Additions - acquired separately 2,699 - 2,699

Reclassification 4,503 - 4,503

Balance on June 30, 2015 $ 86,938 $ 823 $ 87,761

Accumulated amortization

Balance on January 1, 2015 $ 65,017 $ 563 $ 65,580

Amortization expenses 4,923 79 5,002

Balance on June 30, 2015 $ 69,940 $ 642 $ 70,582

Balance on January 1, 2015, net $ 14,719 $ 260 $ 14,979

Balance on June 30, 2015, net $ 16,998 $ 181 $ 17,179

Cost

Balance on January 1, 2016 $ 93,186 $ 891 $ 94,077

Additions - acquired separately 15,361 246 15,607

Balance on June 30, 2016 $ 108,547 $ 1,137 $ 109,684

Accumulated amortization

Balance on January 1, 2016 $ 74,952 $ 723 $ 75,675

Amortization expenses 6,840 83 6,923

Balance on June 30, 2016 $ 81,792 $ 806 $ 82,598

Balance on January 1, 2016, net $ 18,234 $ 168 $ 18,402

Balance on June 30, 2016, net $ 26,755 $ 331 $ 27,086

Intangible assets are amortized on a straight-line basis over the estimated useful lives as follows:

Computer software 3 years

Patents 3-5 years

- 16 -

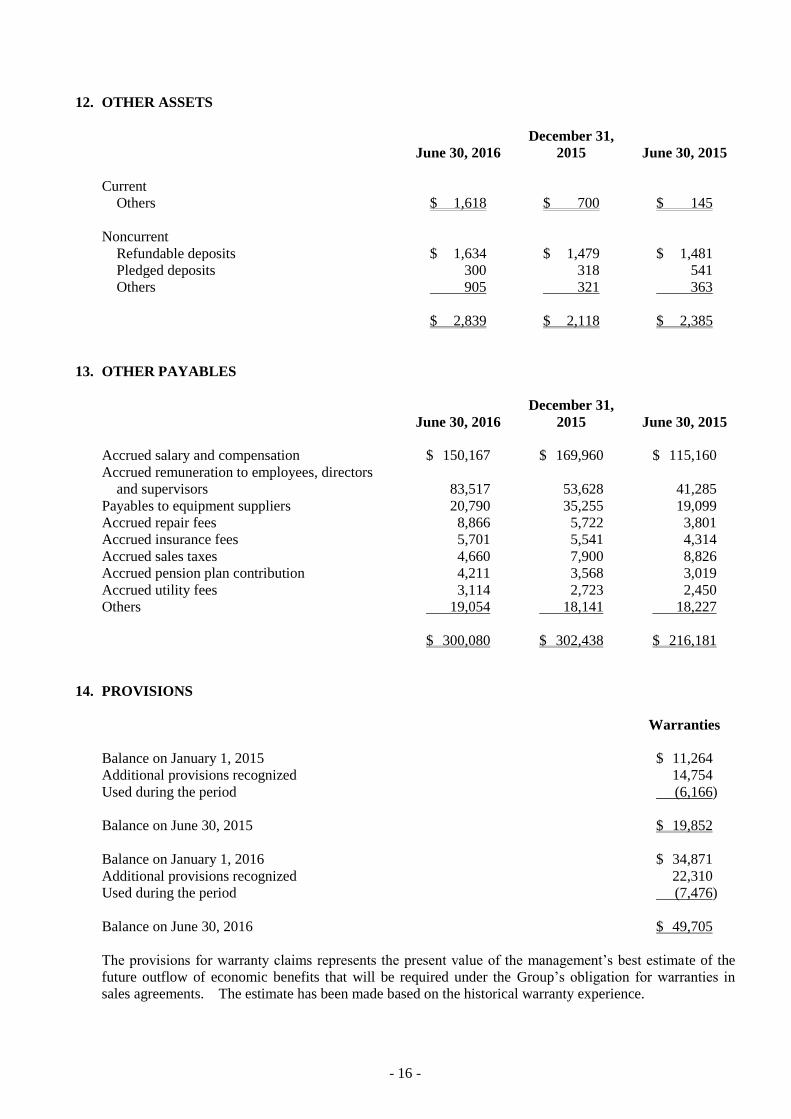

12. OTHER ASSETS

June 30, 2016

December 31,

2015 June 30, 2015

Current

Others $ 1,618 $ 700 $ 145

Noncurrent

Refundable deposits $ 1,634 $ 1,479 $ 1,481

Pledged deposits 300 318 541

Others 905 321 363

$ 2,839 $ 2,118 $ 2,385

13. OTHER PAYABLES

June 30, 2016

December 31,

2015 June 30, 2015

Accrued salary and compensation $ 150,167 $ 169,960 $ 115,160

Accrued remuneration to employees, directors

and supervisors 83,517 53,628 41,285

Payables to equipment suppliers 20,790 35,255 19,099

Accrued repair fees 8,866 5,722 3,801

Accrued insurance fees 5,701 5,541 4,314

Accrued sales taxes 4,660 7,900 8,826

Accrued pension plan contribution 4,211 3,568 3,019

Accrued utility fees 3,114 2,723 2,450

Others 19,054 18,141 18,227

$ 300,080 $ 302,438 $ 216,181

14. PROVISIONS

Warranties

Balance on January 1, 2015 $ 11,264

Additional provisions recognized 14,754

Used during the period (6,166)

Balance on June 30, 2015 $ 19,852

Balance on January 1, 2016 $ 34,871

Additional provisions recognized 22,310

Used during the period (7,476)

Balance on June 30, 2016 $ 49,705

The provisions for warranty claims represents the present value of the management’s best estimate of the

future outflow of economic benefits that will be required under the Group’s obligation for warranties in

sales agreements. The estimate has been made based on the historical warranty experience.

- 17 -

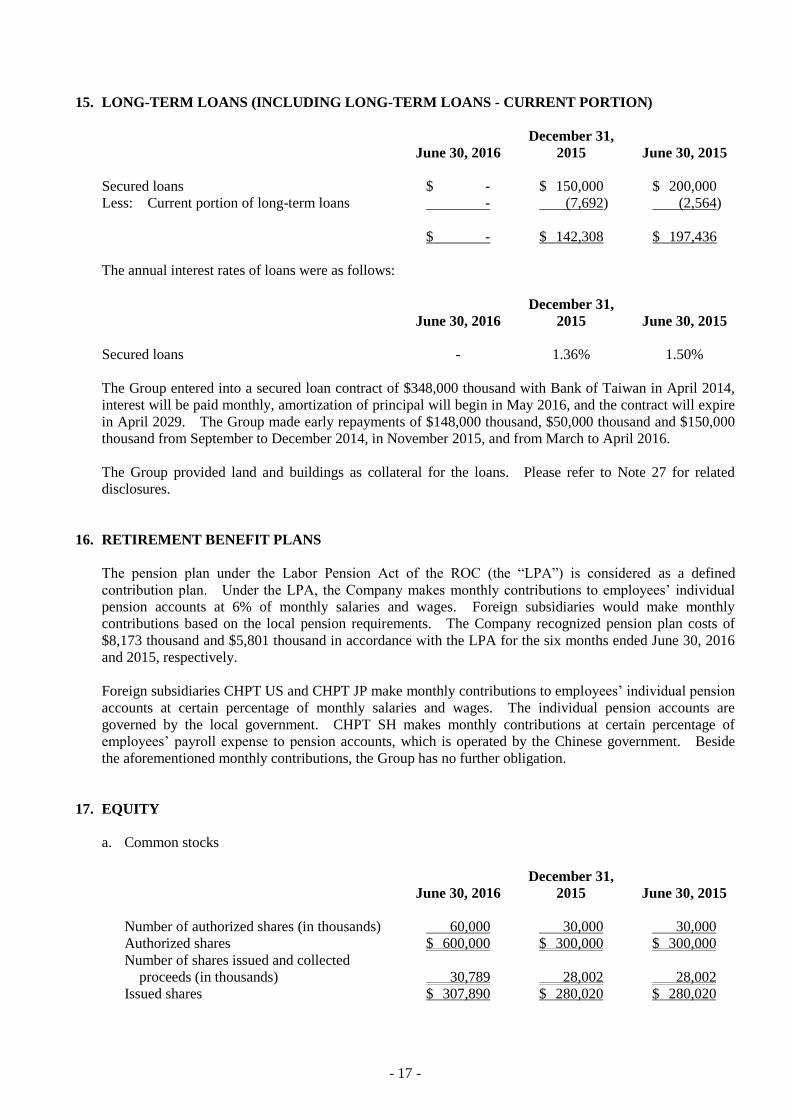

15. LONG-TERM LOANS (INCLUDING LONG-TERM LOANS - CURRENT PORTION)

June 30, 2016

December 31,

2015 June 30, 2015

Secured loans $ - $ 150,000 $ 200,000

Less: Current portion of long-term loans - (7,692) (2,564)

$ - $ 142,308 $ 197,436

The annual interest rates of loans were as follows:

June 30, 2016

December 31,

2015 June 30, 2015

Secured loans - 1.36% 1.50%

The Group entered into a secured loan contract of $348,000 thousand with Bank of Taiwan in April 2014,

interest will be paid monthly, amortization of principal will begin in May 2016, and the contract will expire

in April 2029. The Group made early repayments of $148,000 thousand, $50,000 thousand and $150,000

thousand from September to December 2014, in November 2015, and from March to April 2016.

The Group provided land and buildings as collateral for the loans. Please refer to Note 27 for related

disclosures.

16. RETIREMENT BENEFIT PLANS

The pension plan under the Labor Pension Act of the ROC (the “LPA”) is considered as a defined

contribution plan. Under the LPA, the Company makes monthly contributions to employees’ individual

pension accounts at 6% of monthly salaries and wages. Foreign subsidiaries would make monthly

contributions based on the local pension requirements. The Company recognized pension plan costs of

$8,173 thousand and $5,801 thousand in accordance with the LPA for the six months ended June 30, 2016

and 2015, respectively.

Foreign subsidiaries CHPT US and CHPT JP make monthly contributions to employees’ individual pension

accounts at certain percentage of monthly salaries and wages. The individual pension accounts are

governed by the local government. CHPT SH makes monthly contributions at certain percentage of

employees’ payroll expense to pension accounts, which is operated by the Chinese government. Beside

the aforementioned monthly contributions, the Group has no further obligation.

17. EQUITY

a. Common stocks

June 30, 2016

December 31,

2015 June 30, 2015

Number of authorized shares (in thousands) 60,000 30,000 30,000

Authorized shares $ 600,000 $ 300,000 $ 300,000

Number of shares issued and collected

proceeds (in thousands) 30,789 28,002 28,002

Issued shares $ 307,890 $ 280,020 $ 280,020

- 18 -

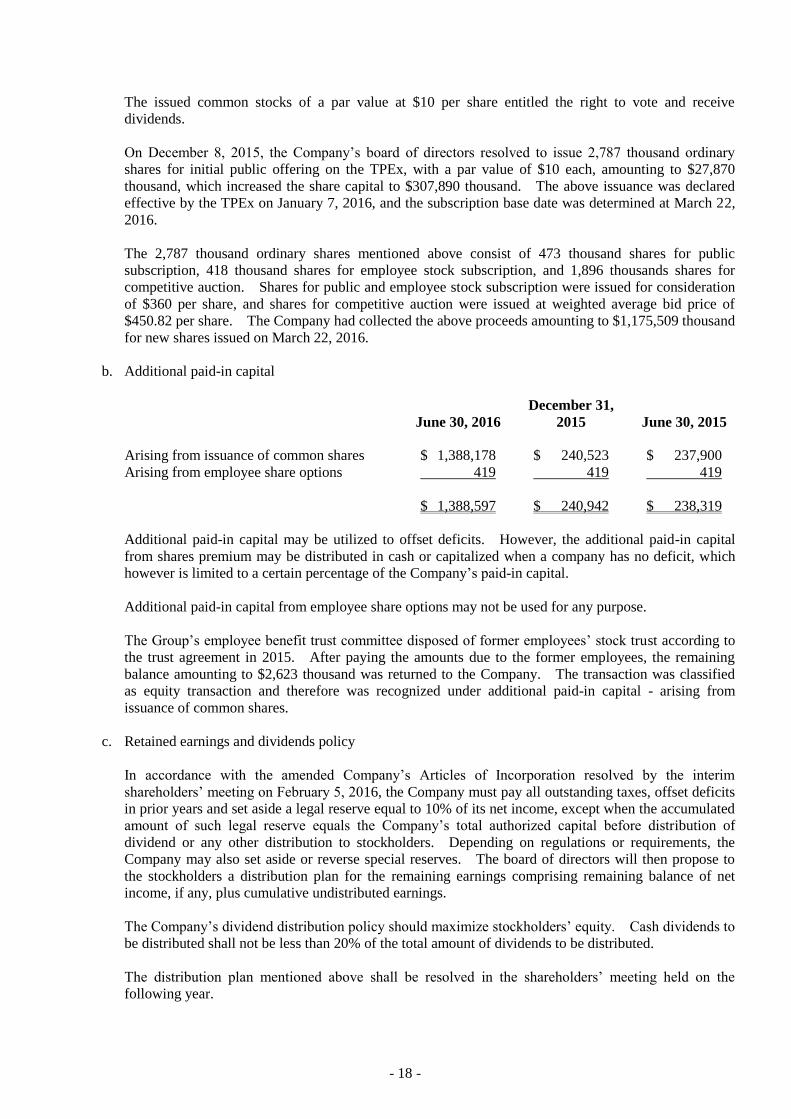

The issued common stocks of a par value at $10 per share entitled the right to vote and receive

dividends.

On December 8, 2015, the Company’s board of directors resolved to issue 2,787 thousand ordinary

shares for initial public offering on the TPEx, with a par value of $10 each, amounting to $27,870

thousand, which increased the share capital to $307,890 thousand. The above issuance was declared

effective by the TPEx on January 7, 2016, and the subscription base date was determined at March 22,

2016.

The 2,787 thousand ordinary shares mentioned above consist of 473 thousand shares for public

subscription, 418 thousand shares for employee stock subscription, and 1,896 thousands shares for

competitive auction. Shares for public and employee stock subscription were issued for consideration

of $360 per share, and shares for competitive auction were issued at weighted average bid price of

$450.82 per share. The Company had collected the above proceeds amounting to $1,175,509 thousand

for new shares issued on March 22, 2016.

b. Additional paid-in capital

June 30, 2016

December 31,

2015 June 30, 2015

Arising from issuance of common shares $ 1,388,178 $ 240,523 $ 237,900

Arising from employee share options 419 419 419

$ 1,388,597 $ 240,942 $ 238,319

Additional paid-in capital may be utilized to offset deficits. However, the additional paid-in capital

from shares premium may be distributed in cash or capitalized when a company has no deficit, which

however is limited to a certain percentage of the Company’s paid-in capital.

Additional paid-in capital from employee share options may not be used for any purpose.

The Group’s employee benefit trust committee disposed of former employees’ stock trust according to

the trust agreement in 2015. After paying the amounts due to the former employees, the remaining

balance amounting to $2,623 thousand was returned to the Company. The transaction was classified

as equity transaction and therefore was recognized under additional paid-in capital - arising from

issuance of common shares.

c. Retained earnings and dividends policy

In accordance with the amended Company’s Articles of Incorporation resolved by the interim

shareholders’ meeting on February 5, 2016, the Company must pay all outstanding taxes, offset deficits

in prior years and set aside a legal reserve equal to 10% of its net income, except when the accumulated

amount of such legal reserve equals the Company’s total authorized capital before distribution of

dividend or any other distribution to stockholders. Depending on regulations or requirements, the

Company may also set aside or reverse special reserves. The board of directors will then propose to

the stockholders a distribution plan for the remaining earnings comprising remaining balance of net

income, if any, plus cumulative undistributed earnings.

The Company’s dividend distribution policy should maximize stockholders’ equity. Cash dividends to

be distributed shall not be less than 20% of the total amount of dividends to be distributed.

The distribution plan mentioned above shall be resolved in the shareholders’ meeting held on the

following year.

- 19 -

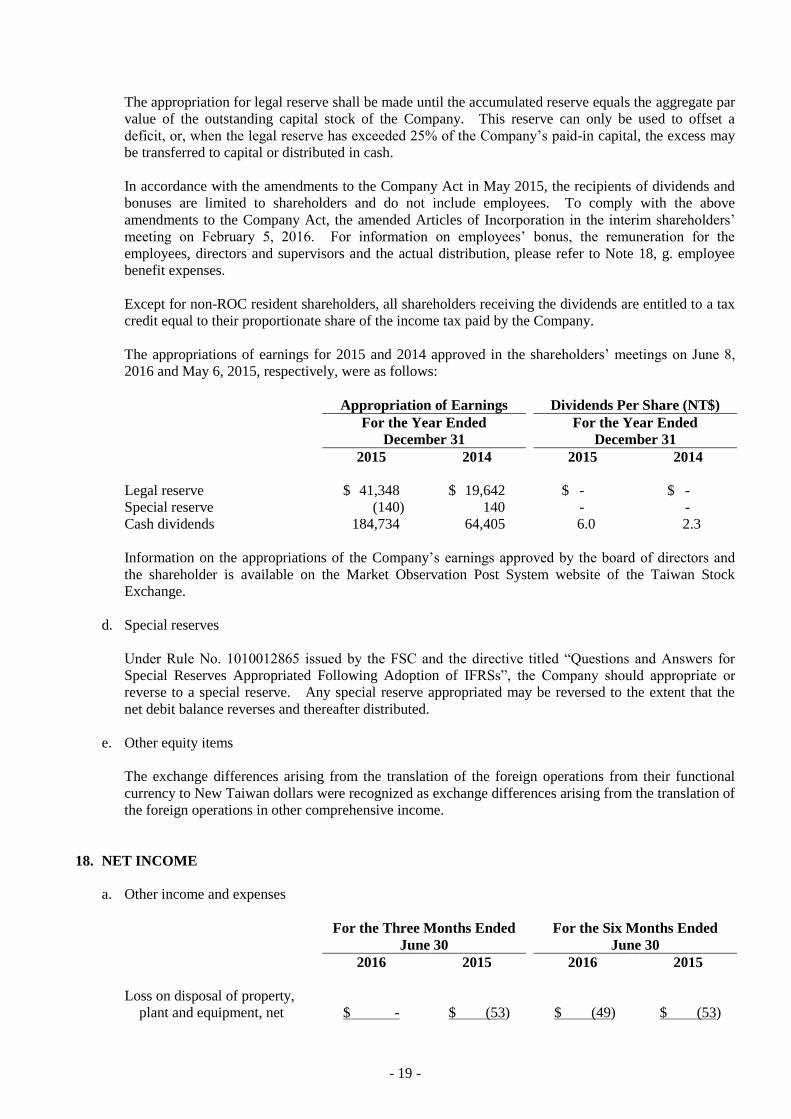

The appropriation for legal reserve shall be made until the accumulated reserve equals the aggregate par

value of the outstanding capital stock of the Company. This reserve can only be used to offset a

deficit, or, when the legal reserve has exceeded 25% of the Company’s paid-in capital, the excess may

be transferred to capital or distributed in cash.

In accordance with the amendments to the Company Act in May 2015, the recipients of dividends and

bonuses are limited to shareholders and do not include employees. To comply with the above

amendments to the Company Act, the amended Articles of Incorporation in the interim shareholders’

meeting on February 5, 2016. For information on employees’ bonus, the remuneration for the

employees, directors and supervisors and the actual distribution, please refer to Note 18, g. employee

benefit expenses.

Except for non-ROC resident shareholders, all shareholders receiving the dividends are entitled to a tax

credit equal to their proportionate share of the income tax paid by the Company.

The appropriations of earnings for 2015 and 2014 approved in the shareholders’ meetings on June 8,

2016 and May 6, 2015, respectively, were as follows:

Appropriation of Earnings Dividends Per Share (NT$)

For the Year Ended

December 31

For the Year Ended

December 31

2015 2014 2015 2014

Legal reserve $ 41,348 $ 19,642 $ - $ -

Special reserve (140) 140 - -

Cash dividends 184,734 64,405 6.0 2.3

Information on the appropriations of the Company’s earnings approved by the board of directors and

the shareholder is available on the Market Observation Post System website of the Taiwan Stock

Exchange.

d. Special reserves

Under Rule No. 1010012865 issued by the FSC and the directive titled “Questions and Answers for

Special Reserves Appropriated Following Adoption of IFRSs”, the Company should appropriate or

reverse to a special reserve. Any special reserve appropriated may be reversed to the extent that the

net debit balance reverses and thereafter distributed.

e. Other equity items

The exchange differences arising from the translation of the foreign operations from their functional

currency to New Taiwan dollars were recognized as exchange differences arising from the translation of

the foreign operations in other comprehensive income.

18. NET INCOME

a. Other income and expenses

For the Three Months Ended

June 30

For the Six Months Ended

June 30

2016 2015 2016 2015

Loss on disposal of property,

plant and equipment, net $ - $ (53) $ (49) $ (53)

- 20 -

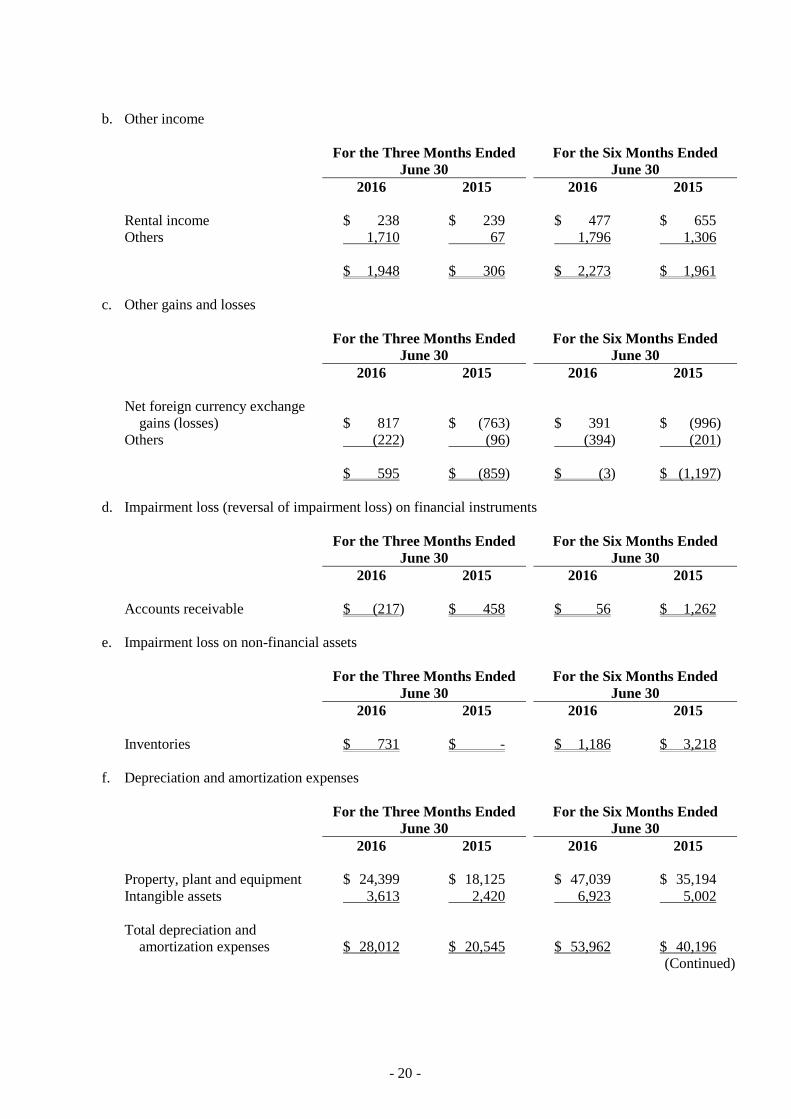

b. Other income

For the Three Months Ended

June 30

For the Six Months Ended

June 30

2016 2015 2016 2015

Rental income $ 238 $ 239 $ 477 $ 655

Others 1,710 67 1,796 1,306

$ 1,948 $ 306 $ 2,273 $ 1,961

c. Other gains and losses

For the Three Months Ended

June 30

For the Six Months Ended

June 30

2016 2015 2016 2015

Net foreign currency exchange

gains (losses) $ 817 $ (763) $ 391 $ (996)

Others (222) (96) (394) (201)

$ 595 $ (859) $ (3) $ (1,197)

d. Impairment loss (reversal of impairment loss) on financial instruments

For the Three Months Ended

June 30

For the Six Months Ended

June 30

2016 2015 2016 2015

Accounts receivable $ (217) $ 458 $ 56 $ 1,262

e. Impairment loss on non-financial assets

For the Three Months Ended

June 30

For the Six Months Ended

June 30

2016 2015 2016 2015

Inventories $ 731 $ - $ 1,186 $ 3,218

f. Depreciation and amortization expenses

For the Three Months Ended

June 30

For the Six Months Ended

June 30

2016 2015 2016 2015

Property, plant and equipment $ 24,399 $ 18,125 $ 47,039 $ 35,194

Intangible assets 3,613 2,420 6,923 5,002

Total depreciation and

amortization expenses $ 28,012 $ 20,545 $ 53,962 $ 40,196

(Continued)

- 21 -

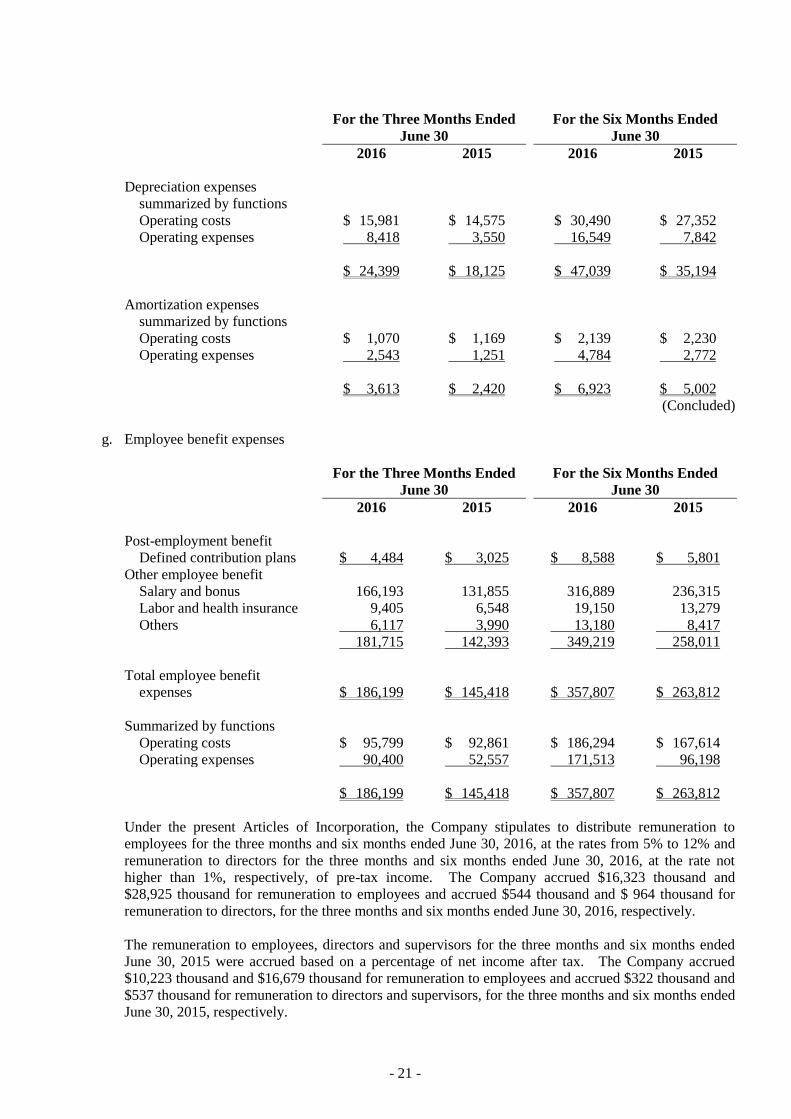

For the Three Months Ended

June 30

For the Six Months Ended

June 30

2016 2015 2016 2015

Depreciation expenses

summarized by functions

Operating costs $ 15,981 $ 14,575 $ 30,490 $ 27,352

Operating expenses 8,418 3,550 16,549 7,842

$ 24,399 $ 18,125 $ 47,039 $ 35,194

Amortization expenses

summarized by functions

Operating costs $ 1,070 $ 1,169 $ 2,139 $ 2,230

Operating expenses 2,543 1,251 4,784 2,772

$ 3,613 $ 2,420 $ 6,923 $ 5,002

(Concluded)

g. Employee benefit expenses

For the Three Months Ended

June 30

For the Six Months Ended

June 30

2016 2015 2016 2015

Post-employment benefit

Defined contribution plans $ 4,484 $ 3,025 $ 8,588 $ 5,801

Other employee benefit

Salary and bonus 166,193 131,855 316,889 236,315

Labor and health insurance 9,405 6,548 19,150 13,279

Others 6,117 3,990 13,180 8,417

181,715 142,393 349,219 258,011

Total employee benefit

expenses $ 186,199 $ 145,418 $ 357,807 $ 263,812

Summarized by functions

Operating costs $ 95,799 $ 92,861 $ 186,294 $ 167,614

Operating expenses 90,400 52,557 171,513 96,198

$ 186,199 $ 145,418 $ 357,807 $ 263,812

Under the present Articles of Incorporation, the Company stipulates to distribute remuneration to

employees for the three months and six months ended June 30, 2016, at the rates from 5% to 12% and

remuneration to directors for the three months and six months ended June 30, 2016, at the rate not

higher than 1%, respectively, of pre-tax income. The Company accrued $16,323 thousand and

$28,925 thousand for remuneration to employees and accrued $544 thousand and $ 964 thousand for

remuneration to directors, for the three months and six months ended June 30, 2016, respectively.

The remuneration to employees, directors and supervisors for the three months and six months ended

June 30, 2015 were accrued based on a percentage of net income after tax. The Company accrued

$10,223 thousand and $16,679 thousand for remuneration to employees and accrued $322 thousand and

$537 thousand for remuneration to directors and supervisors, for the three months and six months ended

June 30, 2015, respectively.

- 22 -

If there is a change in the proposed amounts after the annual consolidated financial statements were

authorized for issue, the differences are recorded as a change in accounting estimate, and adjusted in the

following year.

The remuneration to employees, directors and supervisors for 2015 has been approved in the Board of

Directors on April 28, 2016, and the bonus to employees and remuneration to directors and supervisors

have been approved in the shareholders’ meeting on May 6, 2015. The related information is as

follows. The remuneration to employees, directors and supervisors for 2015 were presented in

shareholders’ meeting on June 8, 2016.

For the Year Ended December 31

2015 2014

Cash Dividends Cash Dividends

Remuneration/bonus to employees $ 51,789 $ 23,267

Remuneration to directors and supervisors 1,839 802

There was no difference between the initial accrual amounts and the amounts approved in the Board of

Directors in 2016 and in shareholders’ meeting in 2015 of the aforementioned bonus to employees and

the remuneration to employees, directors and supervisors for 2015 and 2014, respectively.

Information of the appropriation of the Company’s bonus to employees and remuneration to employees,

directors and supervisors and those approved by the Board of Directors and stockholders’ meeting is

available on the Market Observation Post System website of the Taiwan Stock Exchange.

19. INCOME TAX

a. Income tax recognized in profit or loss

The major components of income tax expense were as follows:

For the Three Months Ended

June 30

For the Six Months Ended

June 30

2016 2015 2016 2015

Current tax

Current tax expenses

recognized for the current

period $ 36,811 $ 29,876 $ 62,061 $ 48,838

Income tax adjustments on

prior years (3,098) (999) (3,098) (999)

Others 2,155 85 3,017 580

35,868 28,962 61,980 48,419

Deferred tax

Deferred tax expenses

recognized for the current

period - (1,749) - (1,749)

Income tax recognized in profit

or loss $ 35,868 $ 27,213 $ 61,980 $ 46,670

- 23 -

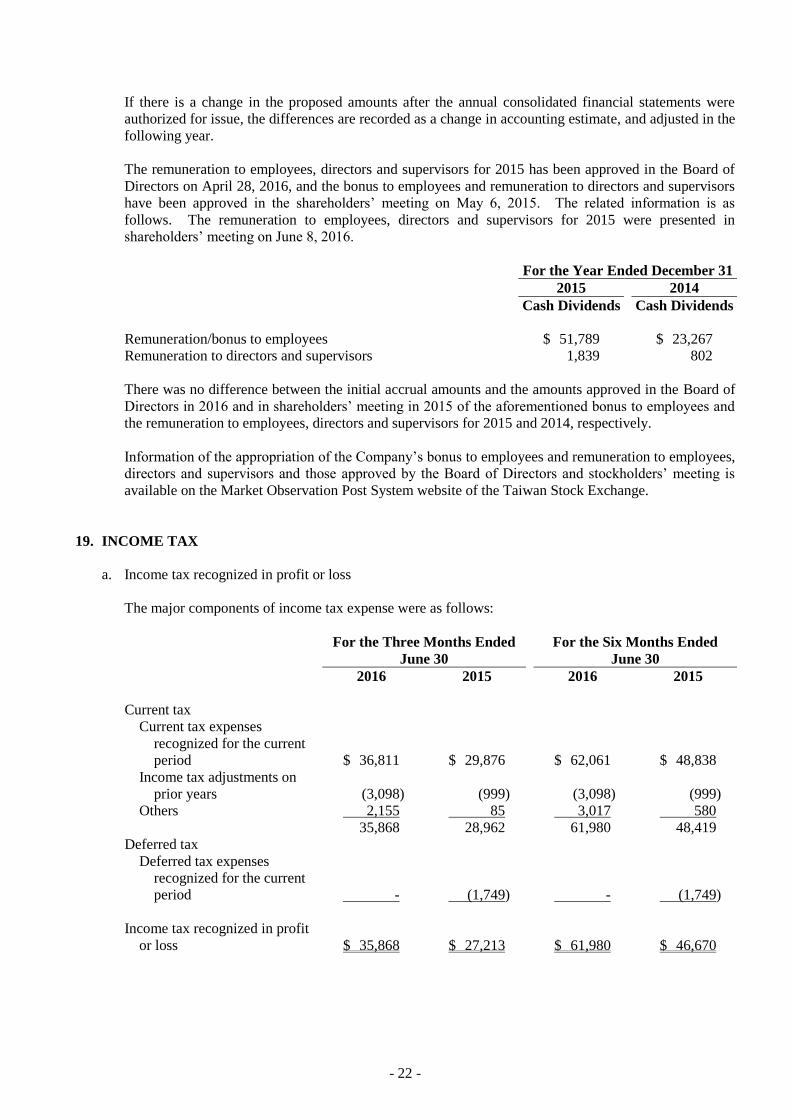

b. The related information under the Integrated Income Tax System is as follows:

Unappropriated earnings information

As of June 30, 2016, December 31, 2015 and June 30, 2015, the Company’s unappropriated earnings

were generated after the adoption of the Integrated Income Tax System.

Imputation credit account (“ICA”)

June 30, 2016

December 31,

2015 June 30, 2015

Balance of Imputation Credit Account $ 131,399 $ 55,362 $ 51,738

The creditable ratios for distribution of earnings of 2015 and 2014 were 23.12% and 21.65%,

respectively. However, according to the revised Article 66-6 of the Income Tax Law, effective from

January 1, 2015, the creditable ratio for individual shareholders residing in the ROC is half of the

original creditable ratio.

c. Income tax examinations

The Company’s income tax returns through 2013 have been examined by the tax authorities.

20. EARNINGS PER SHARE

Net income and weighted average number of common stock used in the calculation of earnings per share

were as follows:

Net Income

For the Three Months Ended

June 30

For the Six Months Ended

June 30

2016 2015 2016 2015

Net income used to compute basic

and diluted earnings per share $ 152,386 $ 86,479 $ 263,187 $ 156,450

Weighted Average Number of Common Stock

(Thousand Shares)

For the Three Months Ended

June 30

For the Six Months Ended

June 30

2016 2015 2016 2015

Weighted average number of

common stock used to compute

basic earnings per share 30,789 28,002 29,549 28,002

Assumed conversion of all dilutive

potential common stock:

Employee remuneration 18 247 47 563

Weighted average number of

common stock used to compute

the diluted earnings per share 30,807 28,249 29,596 28,565

- 24 -

If the Group may settle remuneration paid to employees in cash or shares, the Group assumed the entire

amount of the remuneration would be settled in shares and the resulting potential shares are included in the

weighted average number of shares outstanding used in the computation of diluted earnings per share, since

the effect is dilutive. Such dilutive effect of the potential shares is included in the computation of diluted

earnings per share until the number of shares to be distributed to employees is resolved in the following

year.

21. Share-based Payment Arrangement

On December 8, 2015, the Board of Directors of Company approved the cash injection to issue 2,787

thousand shares and simultaneously reserved 418 thousand shares for subscription by employees according

to the Company Act of the ROC. Furthermore, when the employees do not subscribe some or all of the

shares, the Board of Directors of Company authorizes the chairman of the Board of Directors to contact

specific people or group to subscribe.

The Company used the fair value method to evaluate the options granted to employees on March 10, 2016

using the Black-Scholes model and the related assumptions and the fair value of the options were as

follows:

Stock Options

Granted on

March 10, 2016

Grant-date share price (NT$) $302.46

Exercise price (NT$) $360.00

Expected volatility 37.43%

Expected life 12 days

Dividends yield -

Risk-free interest rate 0.37%

Weighted average fair value of grants (NT$) $0.04

Expected volatility was based on the average annualized historical share price volatility of the Company’s

comparable companies before the grant date.

The aforementioned options granted to employees are accounted for and measured at fair value in

accordance with IFRS 2. The recognized compensation cost was $16 thousand for the six months ended

June 30, 2016 and was recognized as additional paid-in capital - arising from issuance of common shares

after collecting the proceeds for employee stock subscription.

22. NON-CASH TRANSACTIONS

For the six months ended June 30, 2016 and 2015, the Group entered into the following non-cash investing

activities:

For the Six Months Ended

June 30

2016 2015

Increase in property, plant and equipment $ 93,566 $ 89,244

Movements on payables to equipment suppliers 14,465 1,096

$ 108,031 $ 90,340

- 25 -

23. OPERATING LEASE ARRANGEMENTS

a. The Group as lessee

The future aggregate minimum lease payments under non-cancellable operating leases are as follows:

June 30, 2016

December 31,

2015 June 30, 2015

Within one year $ 6,967 $ 10,513 $ 8,976

Longer than one year but within five years 2,063 3,656 7,192

$ 9,030 $ 14,169 $ 16,168

b. The Group as lessor

The future aggregate minimum lease collections under non-cancellable operating leases are as follows:

June 30, 2016

December 31,

2015 June 30, 2015

Within one year $ 740 $ 1,040 $ 1,137

Longer than one year but within five years 900 1,336 1,807

$ 1,640 $ 2,376 $ 2,944

24. CAPITAL MANAGEMENT

The Group manages its capital to ensure that entities in the Group will be able to continue as going

concerns and maintain good credit rating and capital ratio in order to lower the capital cost while

maximizing the return to stockholders.

The management reviews and adjusts the capital structure of the Group as needed. As part of this review,

the management considers the cost of capital and the risks associated with each class of capital. The

Group maintains a balanced capital structure through increasing its share capital, paying cash dividends,

purchasing treasury stock, and proceeds from new debt or repayment of debt.

25. FINANCIAL INSTRUMENTS

Fair Value Information

a. Fair value of financial instruments that are not measured at fair value

The Group believes the carrying amounts of financial assets and financial liabilities recognized in the

consolidated financial statements approximate their fair values.

b. Fair value of financial instruments that are measured at fair value

The Group does not hold financial instruments measured at fair value.

- 26 -

Categories of Financial Instruments

June 30, 2016

December 31,

2015 June 30, 2015

Financial assets

Loans and receivables (Note a) $ 1,865,397 $ 728,706 $ 494,151

Financial liabilities

Measured at amortized cost (Note b) 432,916 318,326 374,863

Note a: The balances included cash and cash equivalents, accounts receivable, other current monetary

assets, refundable deposits (classified as other assets) and pledged deposits (classified as other

assets) which were loans and receivables.

Note b: The balances included accounts payable, payables to related parties, dividends payable, partial

other payables and long-term loans which were financial liabilities carried at amortized cost.

Financial Risk Management Objectives and Policies

The main financial instruments of the Group include accounts receivable, accounts payable and loans.

The Group’s Finance Department provides services to its business units, monitors and manages the

financial risks relating to the operations of the Group through internal risk reports which analyze exposures

by degree and magnitude of risks. These risks include market risk (including foreign currency risk and

interest rate risk), credit risk, and liquidity risk.

a. Market risk

The Group is exposed to market risks of changes in foreign currency exchange rates and interest rates.

There were no changes in the Group’s exposure to market risks and the manner in which these risks are

managed and measured.

1) Foreign currency risk

The carrying amounts of the Group’s foreign currency denominated monetary assets and monetary

liabilities at the end of the reporting periods were as follows:

June 30, 2016

December 31,

2015 June 30, 2015

Assets

USD $ 257,981 $ 142,845 $ 117,543

JPY 3,145 2,904 7,932

RMB 31 94 167

Liabilities

USD 108,084 36,050 14,643

JPY 1,812 11,103 5,064

RMB 2,529 2,020 1,074

EUR 199 960 -

- 27 -

Foreign currency sensitivity analysis

The Group is mainly exposed to the fluctuations of the currencies listed above.

The following table details the Group’s sensitivity to a 5% increase and decrease in the functional

currency against the relevant foreign currencies. The rate of 5% is the sensitivity rate used when

reporting foreign currency risk internally to key management personnel and represents

management’s assessment of the reasonably possible change in foreign exchange rates. The

sensitivity analysis includes only outstanding foreign currency denominated monetary items. A

positive number below indicates an increase in pre-tax profit or equity where the functional

currency weakens 5% against the relevant currency.

For the Six Months Ended

June 30

2016 2015

Profit or loss

Monetary assets and liabilities*

USD $ 7,495 $ 5,145

JPY 67 143

RMB (125) (45)

EUR (10) -

* This is mainly attributable to the exposure to foreign currency denominated receivables and

payables of the Group outstanding at the end of the reporting period.

For a 5% strengthening of the functional currency against the relevant currencies, there would be a

comparable impact on the pre-tax profit or equity, and the balances above would be negative.

2) Interest rate risk

The carrying amounts of the Group’s exposures to interest rates on financial assets and financial

liabilities were as follows:

June 30, 2016

December 31,

2015 June 30, 2015

Fair value interest rate risk

Financial assets $ 790,000 $ 40,000 $ -

Cash flow interest rate risk

Financial assets 745,325 362,052 248,626

Financial liabilities - 150,000 200,000

Interest rate sensitivity analysis

The sensitivity analyses below have been determined based on the exposure to interest rates for

non-derivative instruments at the end of the reporting period. A 25 basis point increase or

decrease is used when reporting interest rate risk internally to key management personnel and

represents management’s assessment of the reasonably possible change in interest rates.

If interest rates had been 25 basis points higher/lower and all other variables were held constant, the

Group’s pre-tax profit would increase/decrease by $1,863 thousand and $122 thousand for the six

months ended June 30, 2016 and 2015, respectively. This is mainly attributable to the Group’s

exposure to floating rates on its financial instruments and long-term loan.

- 28 -

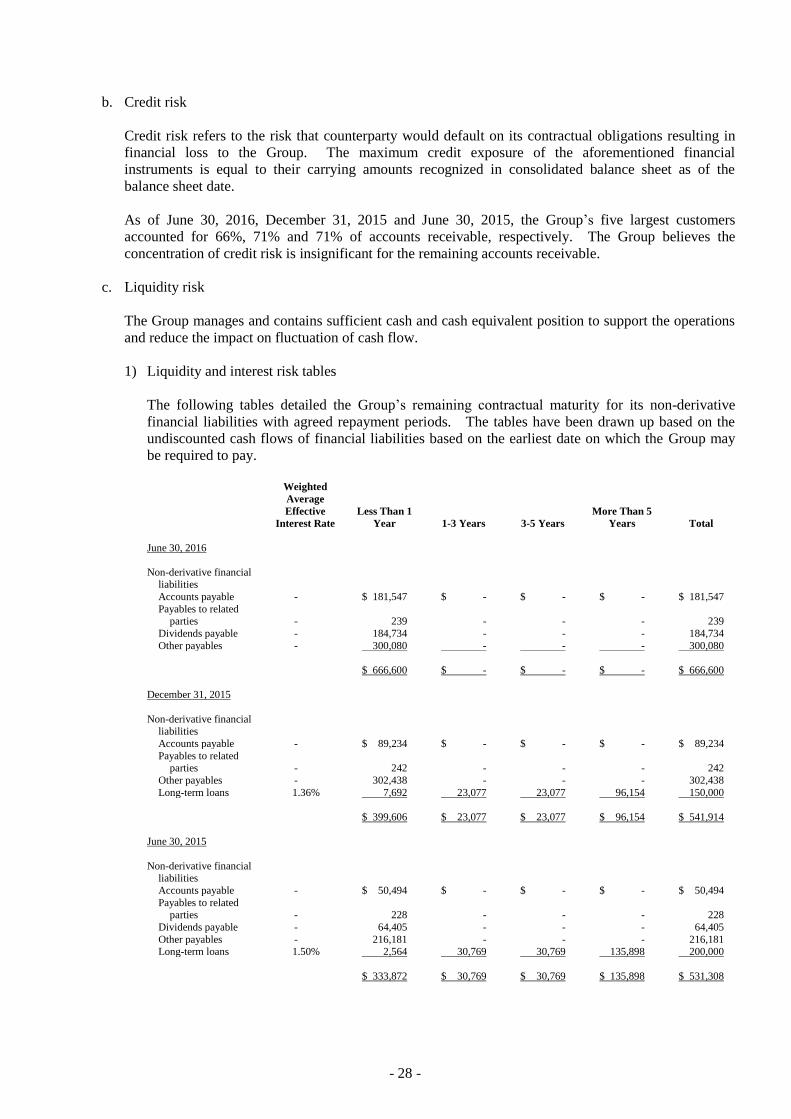

b. Credit risk

Credit risk refers to the risk that counterparty would default on its contractual obligations resulting in

financial loss to the Group. The maximum credit exposure of the aforementioned financial

instruments is equal to their carrying amounts recognized in consolidated balance sheet as of the

balance sheet date.

As of June 30, 2016, December 31, 2015 and June 30, 2015, the Group’s five largest customers

accounted for 66%, 71% and 71% of accounts receivable, respectively. The Group believes the

concentration of credit risk is insignificant for the remaining accounts receivable.

c. Liquidity risk

The Group manages and contains sufficient cash and cash equivalent position to support the operations

and reduce the impact on fluctuation of cash flow.

1) Liquidity and interest risk tables

The following tables detailed the Group’s remaining contractual maturity for its non-derivative

financial liabilities with agreed repayment periods. The tables have been drawn up based on the

undiscounted cash flows of financial liabilities based on the earliest date on which the Group may

be required to pay.

Weighted

Average

Effective

Interest Rate Less Than 1

Year 1-3 Years 3-5 Years More Than 5

Years Total

June 30, 2016

Non-derivative financial liabilities

Accounts payable - $ 181,547 $ - $ - $ - $ 181,547

Payables to related parties - 239 - - - 239

Dividends payable - 184,734 - - - 184,734

Other payables - 300,080 - - - 300,080

$ 666,600 $ - $ - $ - $ 666,600

December 31, 2015

Non-derivative financial liabilities

Accounts payable - $ 89,234 $ - $ - $ - $ 89,234

Payables to related parties - 242 - - - 242

Other payables - 302,438 - - - 302,438

Long-term loans 1.36% 7,692 23,077 23,077 96,154 150,000

$ 399,606 $ 23,077 $ 23,077 $ 96,154 $ 541,914

June 30, 2015

Non-derivative financial liabilities

Accounts payable - $ 50,494 $ - $ - $ - $ 50,494

Payables to related parties - 228 - - - 228

Dividends payable - 64,405 - - - 64,405

Other payables - 216,181 - - - 216,181 Long-term loans 1.50% 2,564 30,769 30,769 135,898 200,000

$ 333,872 $ 30,769 $ 30,769 $ 135,898 $ 531,308

- 29 -

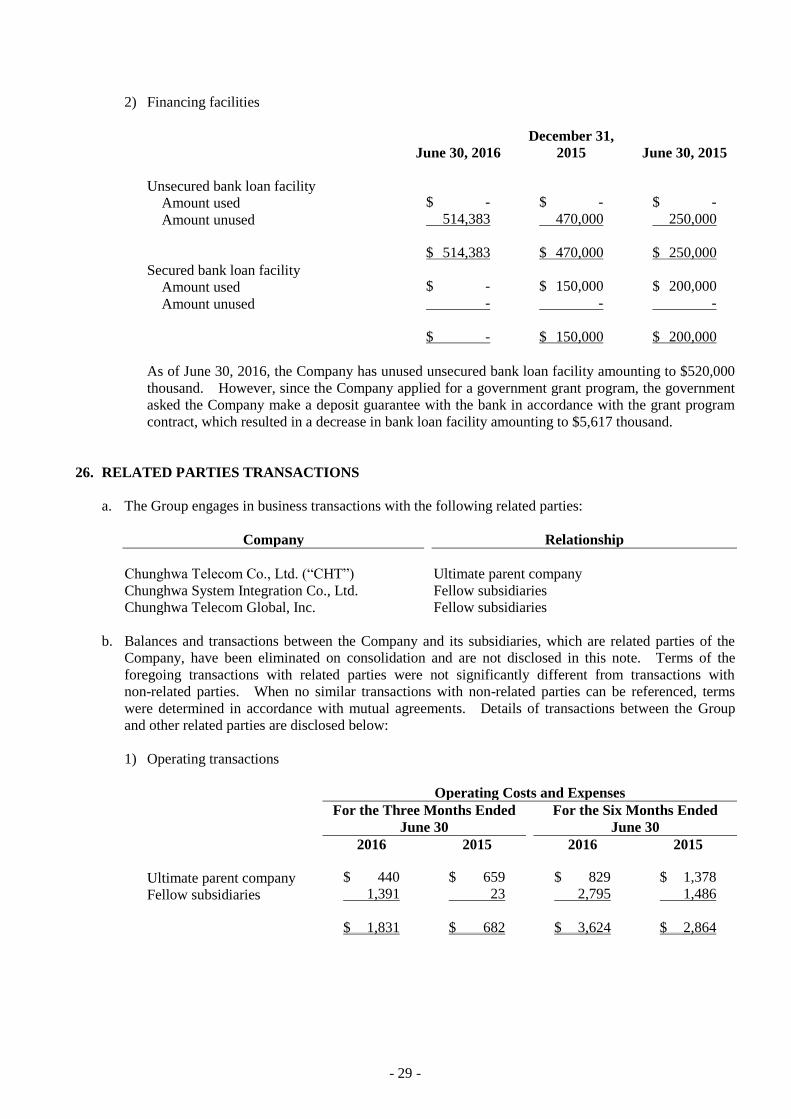

2) Financing facilities

June 30, 2016

December 31,

2015 June 30, 2015

Unsecured bank loan facility

Amount used $ - $ - $ -

Amount unused 514,383 470,000 250,000

$ 514,383 $ 470,000 $ 250,000

Secured bank loan facility

Amount used $ - $ 150,000 $ 200,000

Amount unused - - -

$ - $ 150,000 $ 200,000

As of June 30, 2016, the Company has unused unsecured bank loan facility amounting to $520,000

thousand. However, since the Company applied for a government grant program, the government

asked the Company make a deposit guarantee with the bank in accordance with the grant program

contract, which resulted in a decrease in bank loan facility amounting to $5,617 thousand.

26. RELATED PARTIES TRANSACTIONS

a. The Group engages in business transactions with the following related parties:

Company Relationship

Chunghwa Telecom Co., Ltd. (“CHT”) Ultimate parent company

Chunghwa System Integration Co., Ltd. Fellow subsidiaries

Chunghwa Telecom Global, Inc. Fellow subsidiaries

b. Balances and transactions between the Company and its subsidiaries, which are related parties of the

Company, have been eliminated on consolidation and are not disclosed in this note. Terms of the

foregoing transactions with related parties were not significantly different from transactions with

non-related parties. When no similar transactions with non-related parties can be referenced, terms

were determined in accordance with mutual agreements. Details of transactions between the Group

and other related parties are disclosed below:

1) Operating transactions

Operating Costs and Expenses

For the Three Months Ended

June 30

For the Six Months Ended

June 30

2016 2015 2016 2015

Ultimate parent company $ 440 $ 659 $ 829 $ 1,378

Fellow subsidiaries 1,391 23 2,795 1,486

$ 1,831 $ 682 $ 3,624 $ 2,864

- 30 -

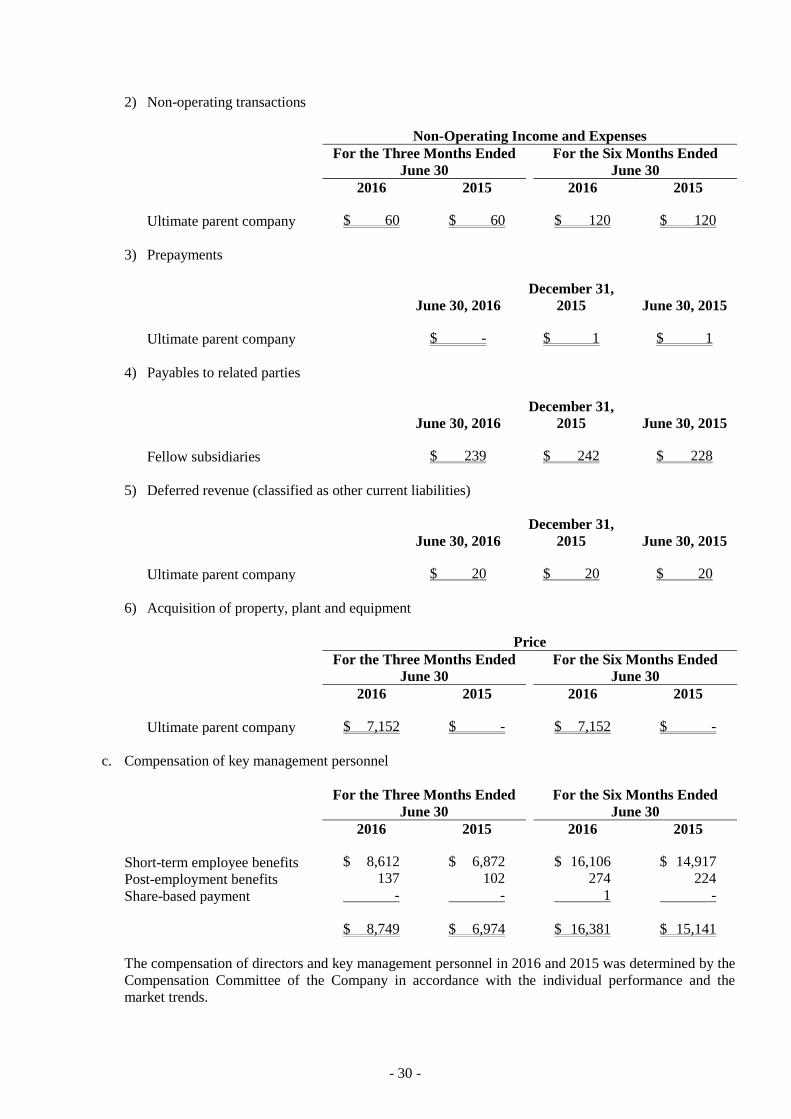

2) Non-operating transactions

Non-Operating Income and Expenses

For the Three Months Ended

June 30

For the Six Months Ended

June 30

2016 2015 2016 2015

Ultimate parent company $ 60 $ 60 $ 120 $ 120

3) Prepayments

June 30, 2016

December 31,

2015 June 30, 2015

Ultimate parent company $ - $ 1 $ 1

4) Payables to related parties

June 30, 2016

December 31,

2015 June 30, 2015

Fellow subsidiaries $ 239 $ 242 $ 228

5) Deferred revenue (classified as other current liabilities)

June 30, 2016

December 31,

2015 June 30, 2015

Ultimate parent company $ 20 $ 20 $ 20

6) Acquisition of property, plant and equipment

Price

For the Three Months Ended

June 30

For the Six Months Ended

June 30

2016 2015 2016 2015

Ultimate parent company $ 7,152 $ - $ 7,152 $ -

c. Compensation of key management personnel

For the Three Months Ended

June 30

For the Six Months Ended

June 30

2016 2015 2016 2015

Short-term employee benefits $ 8,612 $ 6,872 $ 16,106 $ 14,917

Post-employment benefits 137 102 274 224

Share-based payment - - 1 -

$ 8,749 $ 6,974 $ 16,381 $ 15,141

The compensation of directors and key management personnel in 2016 and 2015 was determined by the

Compensation Committee of the Company in accordance with the individual performance and the

market trends.

- 31 -

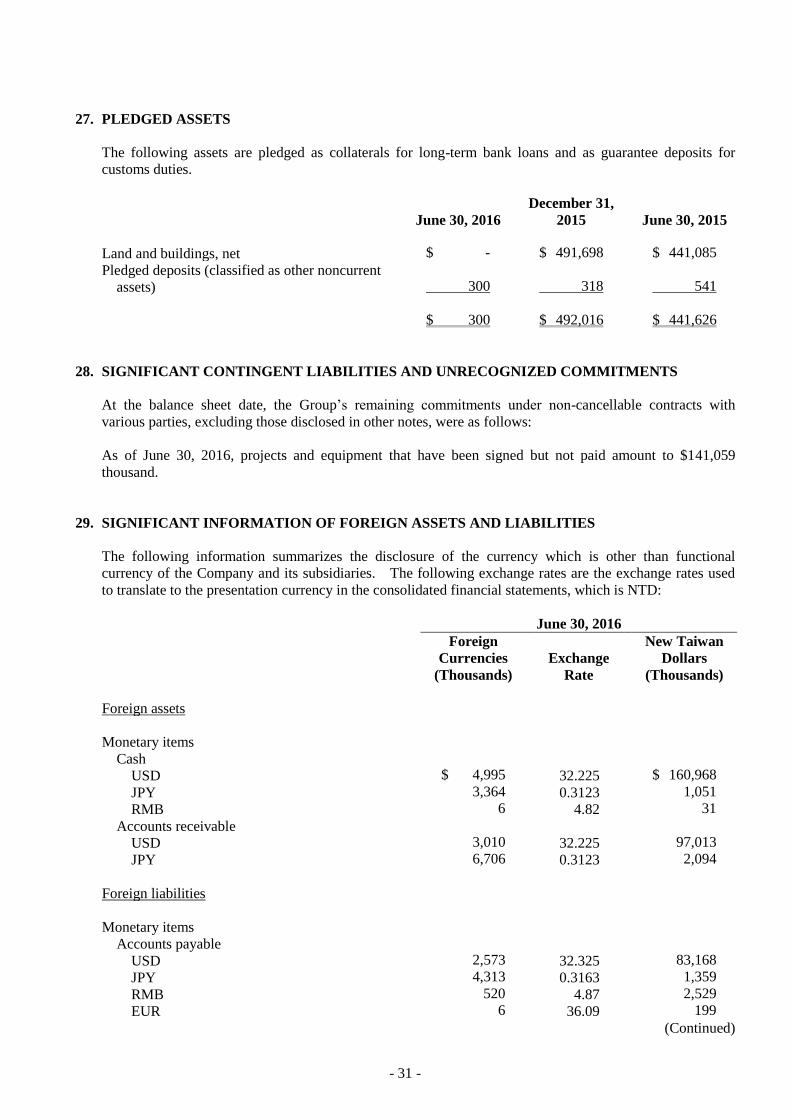

27. PLEDGED ASSETS

The following assets are pledged as collaterals for long-term bank loans and as guarantee deposits for

customs duties.

June 30, 2016

December 31,

2015 June 30, 2015

Land and buildings, net $ - $ 491,698 $ 441,085

Pledged deposits (classified as other noncurrent

assets) 300

318 541

$ 300 $ 492,016 $ 441,626

28. SIGNIFICANT CONTINGENT LIABILITIES AND UNRECOGNIZED COMMITMENTS

At the balance sheet date, the Group’s remaining commitments under non-cancellable contracts with

various parties, excluding those disclosed in other notes, were as follows:

As of June 30, 2016, projects and equipment that have been signed but not paid amount to $141,059

thousand.

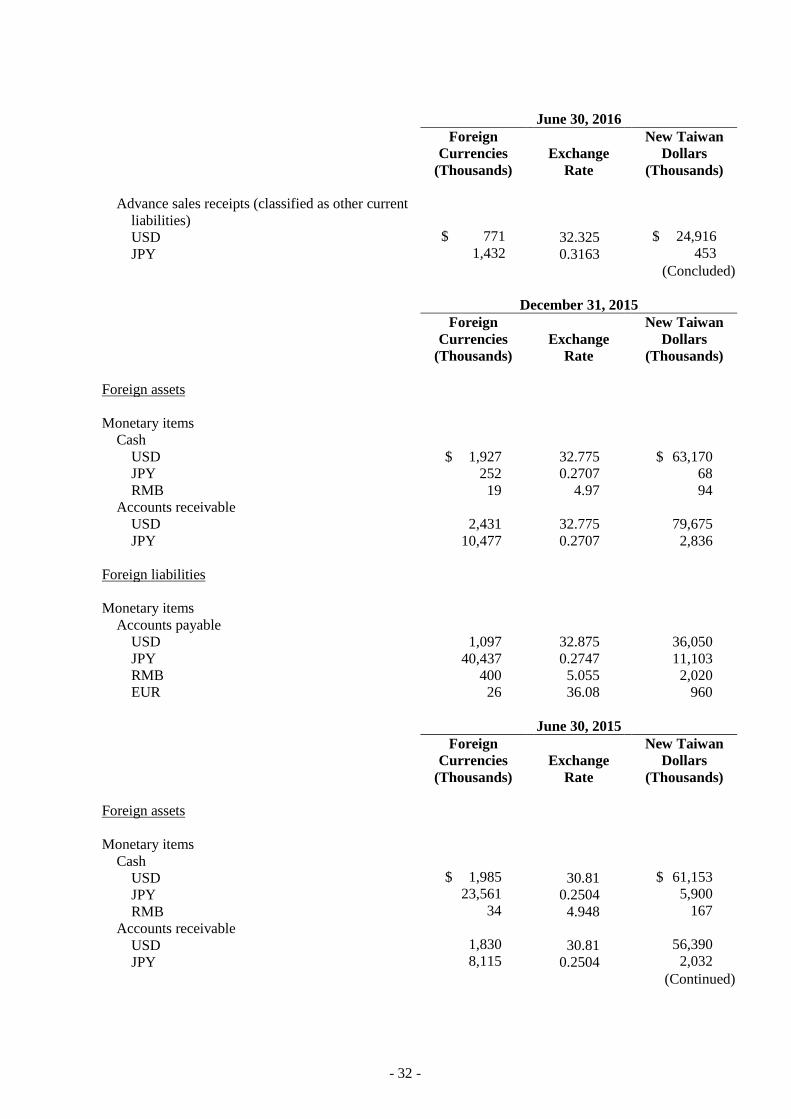

29. SIGNIFICANT INFORMATION OF FOREIGN ASSETS AND LIABILITIES

The following information summarizes the disclosure of the currency which is other than functional

currency of the Company and its subsidiaries. The following exchange rates are the exchange rates used

to translate to the presentation currency in the consolidated financial statements, which is NTD:

June 30, 2016

Foreign

Currencies

(Thousands)

Exchange

Rate

New Taiwan

Dollars

(Thousands)

Foreign assets

Monetary items

Cash

USD $ 4,995 32.225 $ 160,968

JPY 3,364 0.3123 1,051

RMB 6 4.82 31

Accounts receivable

USD 3,010 32.225 97,013

JPY 6,706 0.3123 2,094

Foreign liabilities

Monetary items

Accounts payable

USD 2,573 32.325 83,168

JPY 4,313 0.3163 1,359

RMB 520 4.87 2,529

EUR 6 36.09 199

(Continued)

- 32 -

June 30, 2016

Foreign

Currencies

(Thousands)

Exchange

Rate

New Taiwan

Dollars

(Thousands)

Advance sales receipts (classified as other current

liabilities)

USD $ 771 32.325 $ 24,916

JPY 1,432 0.3163 453

(Concluded)

December 31, 2015

Foreign

Currencies

(Thousands)

Exchange

Rate

New Taiwan

Dollars

(Thousands)

Foreign assets

Monetary items

Cash

USD $ 1,927 32.775 $ 63,170

JPY 252 0.2707 68

RMB 19 4.97 94

Accounts receivable

USD 2,431 32.775 79,675

JPY 10,477 0.2707 2,836

Foreign liabilities

Monetary items

Accounts payable

USD 1,097 32.875 36,050

JPY 40,437 0.2747 11,103

RMB 400 5.055 2,020

EUR 26 36.08 960

June 30, 2015

Foreign

Currencies

(Thousands)

Exchange

Rate

New Taiwan

Dollars

(Thousands)

Foreign assets

Monetary items

Cash

USD $ 1,985 30.81 $ 61,153

JPY 23,561 0.2504 5,900

RMB 34 4.948 167

Accounts receivable

USD 1,830 30.81 56,390

JPY 8,115 0.2504 2,032

(Continued)

- 33 -

June 30, 2015

Foreign

Currencies

(Thousands)

Exchange

Rate

New Taiwan

Dollars

(Thousands)

Foreign liabilities

Monetary items

Accounts payable

USD $ 474 30.91 $ 14,643

JPY 19,908 0.2544 5,064

RMB 215 4.998 1,074

(Concluded)

The unrealized foreign currency exchange losses were $4,492 thousand and $418 thousand for the six

months ended June 30, 2016 and 2015, respectively. Due to the various foreign currency transactions and

the functional currency of each individual entity of the Group, foreign exchange gains and losses cannot be

disclosed on the respective significant foreign currency.

30. ADDITIONAL DISCLOSURES

Following are the additional disclosures required by the SFC for the Group:

a. Financing provided: None.

b. Endorsement/guarantee provided: None.

c. Marketable securities held (excluding investments in subsidiaries, associates and joint ventures):

None.

d. Marketable securities acquired and disposed of at costs or prices at least $300 million or 20% of the

paid-in capital: None.

e. Acquisition of individual real estate at costs of at least $300 million or 20% of the paid-in capital:

None.

f. Disposal of individual real estate at prices of at least $300 million or 20% of the paid-in capital: None.

g. Total purchases from or sales to related parties amounting to at least $100 million or 20% of the paid-in

capital: None.

h. Receivables from related parties amounting to $100 million or 20% of the paid-in capital: None.

i. Names, locations, and other information of investees on which the Company exercises significant

influence (excluding investment in Mainland China): Please see Table 1.

j. Financial transactions: None.

k. Investment in Mainland China: Please see Table 2.

l. Intercompany relationships and significant intercompany transaction: Please see Table 3.

- 34 -

31. SEGMENT INFORMATION

Information reported to the chief operating decision maker for the purpose of resource allocation and

assessment of segment performance focuses on the types of goods or services delivered or provided.

Under the guideline of IFRS 8 “Operating Segments”, the Group’s measurement basis for operating

segment’s assets and liabilities are the same as the measurement basis for the financial statements.

- 35 -

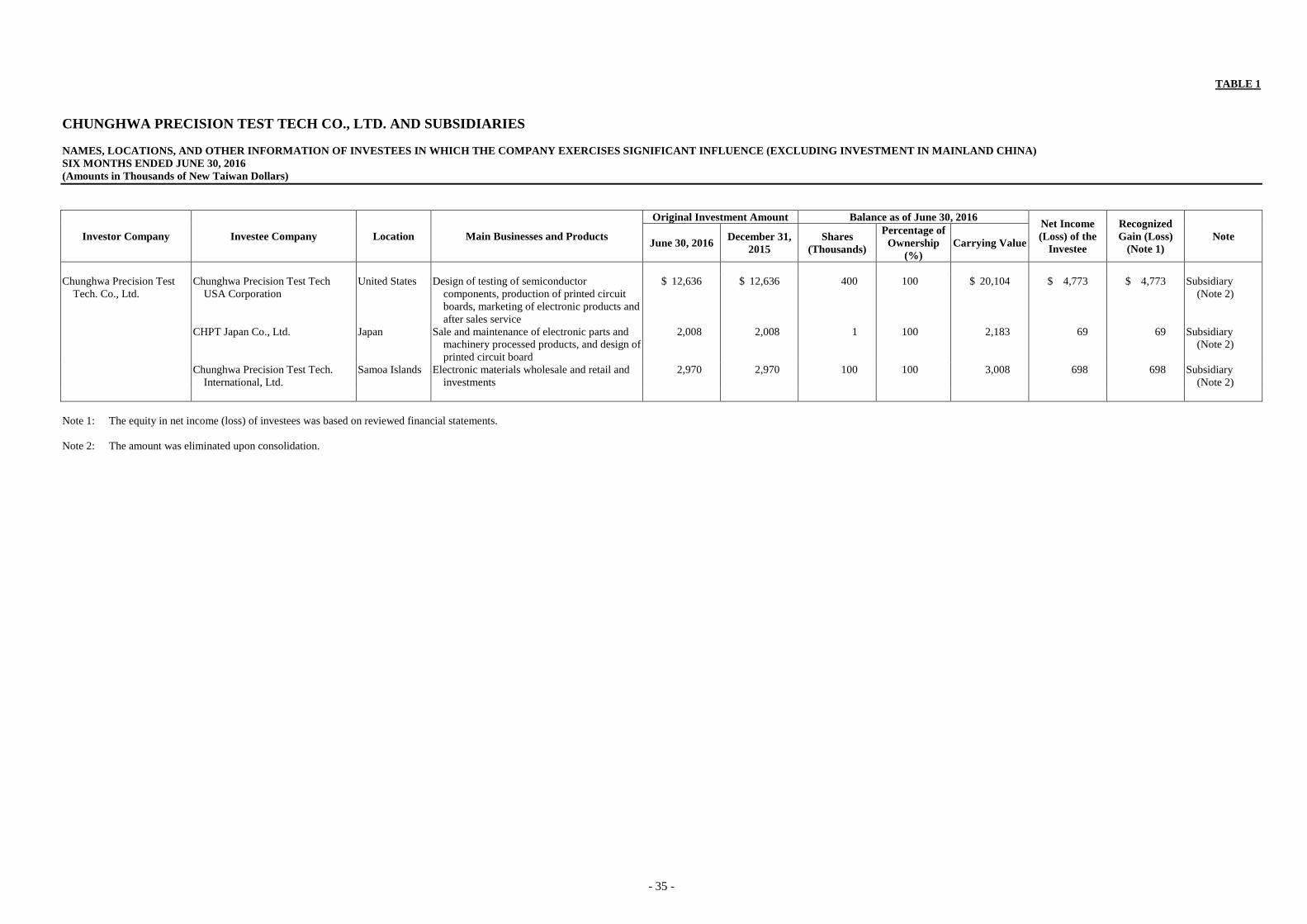

TABLE 1

CHUNGHWA PRECISION TEST TECH CO., LTD. AND SUBSIDIARIES

NAMES, LOCATIONS, AND OTHER INFORMATION OF INVESTEES IN WHICH THE COMPANY EXERCISES SIGNIFICANT INFLUENCE (EXCLUDING INVESTMENT IN MAINLAND CHINA)

SIX MONTHS ENDED JUNE 30, 2016

(Amounts in Thousands of New Taiwan Dollars)

Investor Company Investee Company Location Main Businesses and Products

Original Investment Amount Balance as of June 30, 2016 Net Income

(Loss) of the

Investee

Recognized

Gain (Loss)

(Note 1)

Note June 30, 2016

December 31,

2015

Shares

(Thousands)

Percentage of

Ownership

(%)

Carrying Value

Chunghwa Precision Test

Tech. Co., Ltd.

Chunghwa Precision Test Tech

USA Corporation

United States Design of testing of semiconductor

components, production of printed circuit

boards, marketing of electronic products and

after sales service

$ 12,636 $ 12,636 400 100 $ 20,104 $ 4,773 $ 4,773 Subsidiary

(Note 2)

CHPT Japan Co., Ltd. Japan Sale and maintenance of electronic parts and

machinery processed products, and design of

printed circuit board

2,008 2,008 1 100 2,183 69 69 Subsidiary

(Note 2)

Chunghwa Precision Test Tech.

International, Ltd.

Samoa Islands Electronic materials wholesale and retail and

investments

2,970 2,970 100 100 3,008 698 698 Subsidiary

(Note 2)

Note 1: The equity in net income (loss) of investees was based on reviewed financial statements.

Note 2: The amount was eliminated upon consolidation.

- 36 -

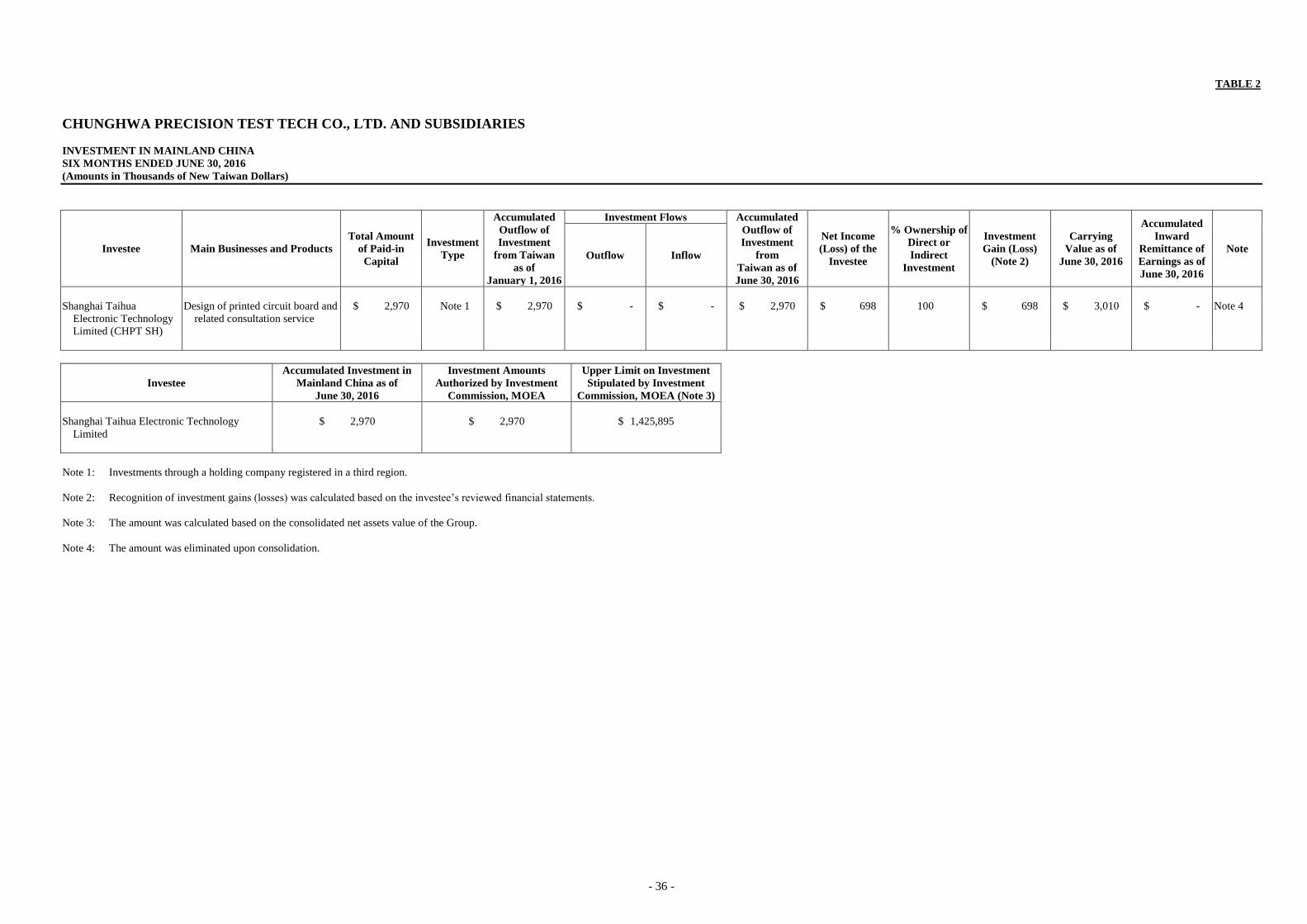

TABLE 2

CHUNGHWA PRECISION TEST TECH CO., LTD. AND SUBSIDIARIES

INVESTMENT IN MAINLAND CHINA

SIX MONTHS ENDED JUNE 30, 2016

(Amounts in Thousands of New Taiwan Dollars)

Investee Main Businesses and Products

Total Amount

of Paid-in

Capital

Investment

Type

Accumulated

Outflow of

Investment

from Taiwan

as of

January 1, 2016

Investment Flows Accumulated

Outflow of

Investment

from

Taiwan as of

June 30, 2016

Net Income

(Loss) of the

Investee

% Ownership of

Direct or

Indirect

Investment

Investment

Gain (Loss)

(Note 2)

Carrying

Value as of

June 30, 2016

Accumulated

Inward

Remittance of

Earnings as of

June 30, 2016

Note Outflow Inflow

Shanghai Taihua

Electronic Technology

Limited (CHPT SH)

Design of printed circuit board and

related consultation service

$ 2,970 Note 1 $ 2,970 $ - $ - $ 2,970 $ 698 100 $ 698 $ 3,010 $ - Note 4

Investee

Accumulated Investment in

Mainland China as of

June 30, 2016

Investment Amounts

Authorized by Investment

Commission, MOEA

Upper Limit on Investment

Stipulated by Investment

Commission, MOEA (Note 3)

Shanghai Taihua Electronic Technology

Limited

$ 2,970 $ 2,970 $ 1,425,895

Note 1: Investments through a holding company registered in a third region.

Note 2: Recognition of investment gains (losses) was calculated based on the investee’s reviewed financial statements.

Note 3: The amount was calculated based on the consolidated net assets value of the Group.

Note 4: The amount was eliminated upon consolidation.

- 37 -

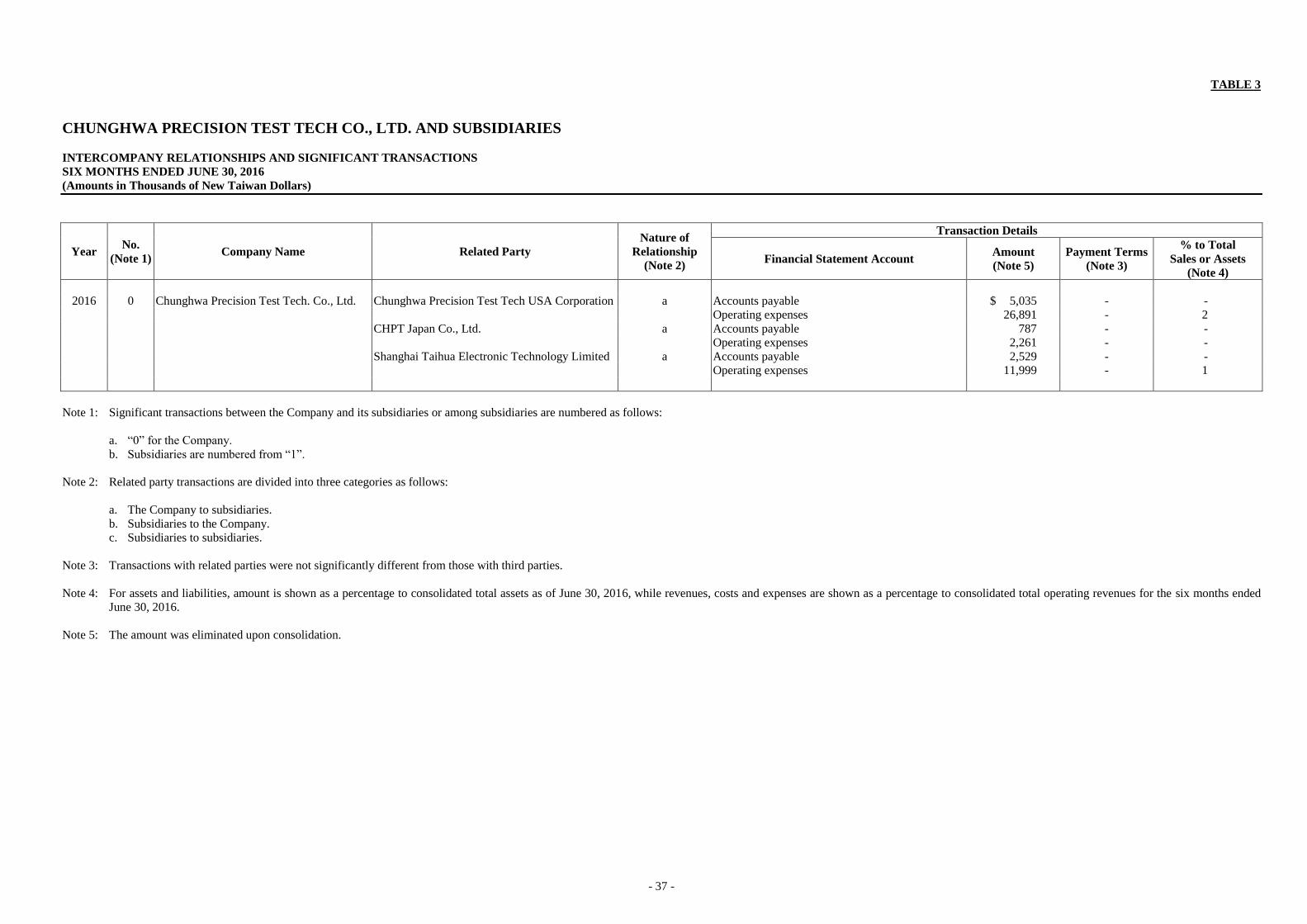

TABLE 3

CHUNGHWA PRECISION TEST TECH CO., LTD. AND SUBSIDIARIES

INTERCOMPANY RELATIONSHIPS AND SIGNIFICANT TRANSACTIONS

SIX MONTHS ENDED JUNE 30, 2016

(Amounts in Thousands of New Taiwan Dollars)

Year No.

(Note 1) Company Name Related Party

Nature of

Relationship

(Note 2)

Transaction Details

Financial Statement Account Amount

(Note 5)

Payment Terms

(Note 3)

% to Total

Sales or Assets

(Note 4)

2016 0 Chunghwa Precision Test Tech. Co., Ltd. Chunghwa Precision Test Tech USA Corporation a Accounts payable $ 5,035 - -

Operating expenses 26,891 - 2

CHPT Japan Co., Ltd. a Accounts payable 787 - -

Operating expenses 2,261 - -

Shanghai Taihua Electronic Technology Limited a Accounts payable 2,529 - -

Operating expenses 11,999 - 1

Note 1: Significant transactions between the Company and its subsidiaries or among subsidiaries are numbered as follows: