Chapter 13 Principles of Corporate Finance Eighth Edition Corporate Financing and the Six Lessons of...

24

Chapter 13 Principles of Corporate Finance Eighth Edition Corporate Financing and the Six Lessons of Market Efficiency Slides by Matthew Will Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved McGraw-Hill/Irwin

-

date post

22-Dec-2015 -

Category

Documents

-

view

229 -

download

4

Transcript of Chapter 13 Principles of Corporate Finance Eighth Edition Corporate Financing and the Six Lessons of...

Chapter 13

Principles of

Corporate FinanceEighth Edition

Corporate Financing and the

Six Lessons of Market Efficiency Slides by

Matthew Will

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

McGraw-Hill/Irwin

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

13- 2

McGraw-Hill/Irwin

Topics Covered

We Always Come Back to NPVWhat is an Efficient Market?

– Random Walk– Efficient Market Theory– The Evidence on Market Efficiency

Puzzles and AnomaliesSix Lessons of Market Efficiency

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

13- 3

McGraw-Hill/Irwin

Return to NPV

NPV employs discount ratesThese discount rates are risk adjustedThe risk adjustment is a byproduct of

market established pricesAdjustable discount rates change asset

values

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

13- 4

McGraw-Hill/Irwin

Return to NPV

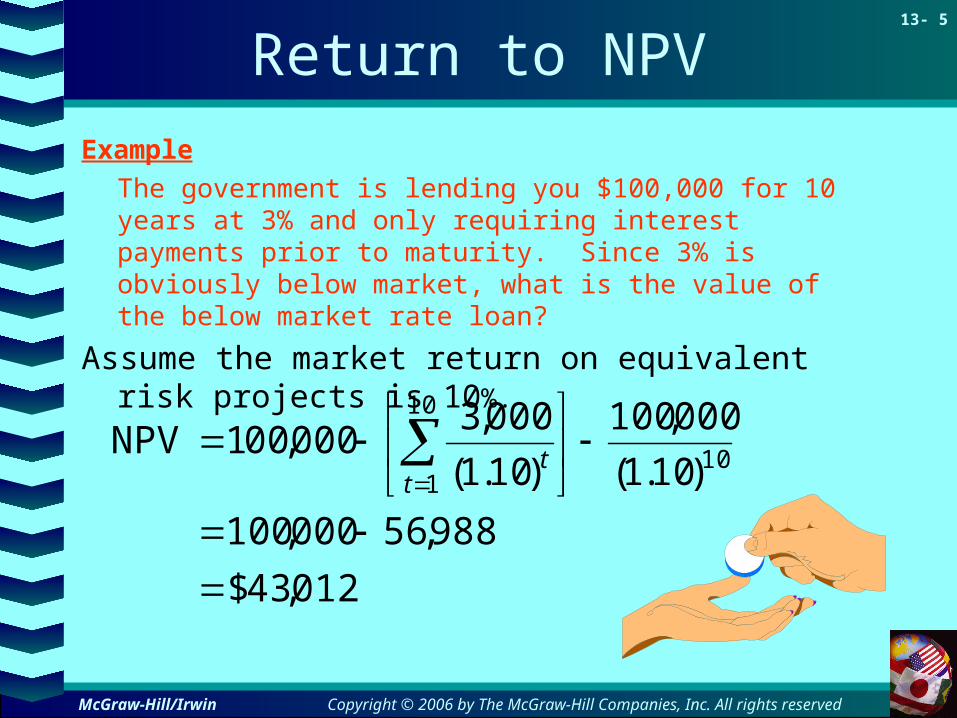

Example

The government is lending you $100,000 for 10 years at 3% and only requiring interest payments prior to maturity. Since 3% is obviously below market, what is the value of the below market rate loan?

repayment loan of PV-

pmtsinterest of PV- borrowedamount NPV

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

13- 5

McGraw-Hill/Irwin

Return to NPV

Example

The government is lending you $100,000 for 10 years at 3% and only requiring interest payments prior to maturity. Since 3% is obviously below market, what is the value of the below market rate loan?

Assume the market return on equivalent risk projects is 10%.

012,43$

988,56000,100

)10.1(

000,100

)10.1(

000,3000,001NPV

10

10

1

tt

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

13- 6

McGraw-Hill/Irwin

Random Walk Theory

The movement of stock prices from day to day DO NOT reflect any pattern.

Statistically speaking, the movement of stock prices is random (skewed positive over the long term).

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

13- 7

McGraw-Hill/Irwin

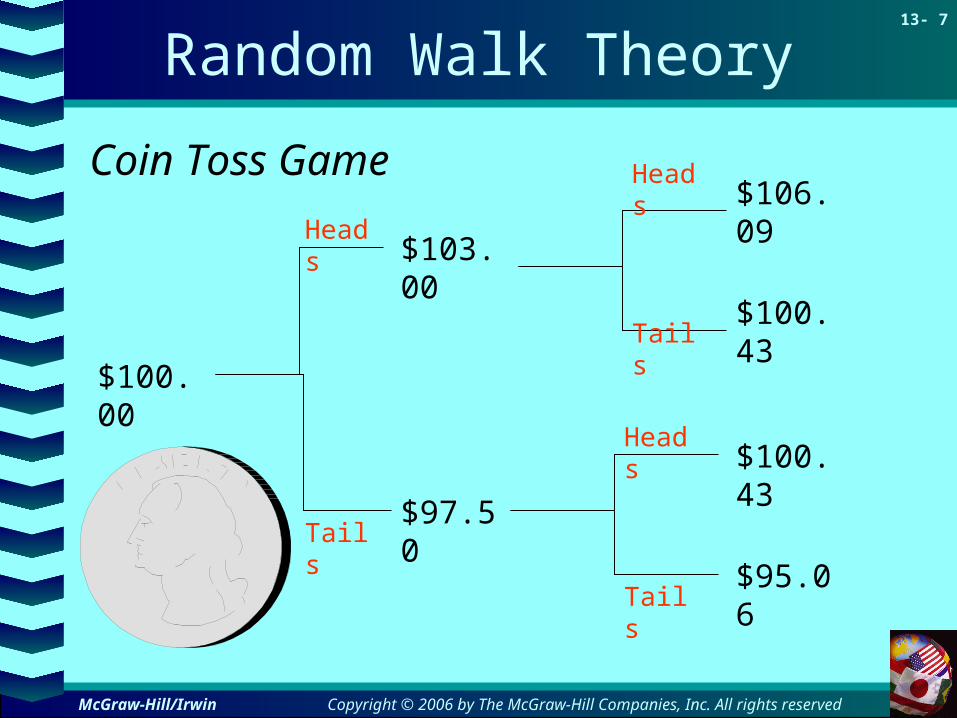

Random Walk Theory

$103.00

$100.00

$106.09

$100.43

$97.50

$100.43

$95.06

Coin Toss Game

Heads

Heads

Heads

Tails

Tails

Tails

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

13- 8

McGraw-Hill/Irwin

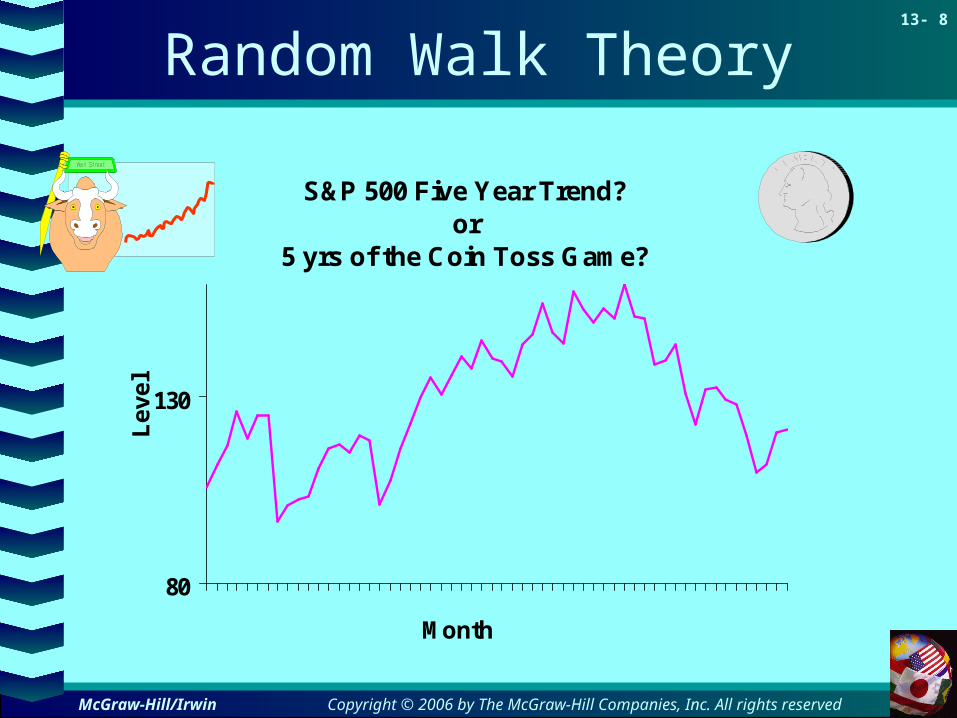

Random Walk Theory

S&P 500 Five Year Trend?or

5 yrs of the Coin Toss Game?

80

130

Month

Le

ve

l

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

13- 9

McGraw-Hill/Irwin

Random Walk Theory

S&P 500 Five Year Trend?or

5 yrs of the Coin Toss Game?

80

130

180

230

Month

Le

ve

l

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

13- 10

McGraw-Hill/Irwin

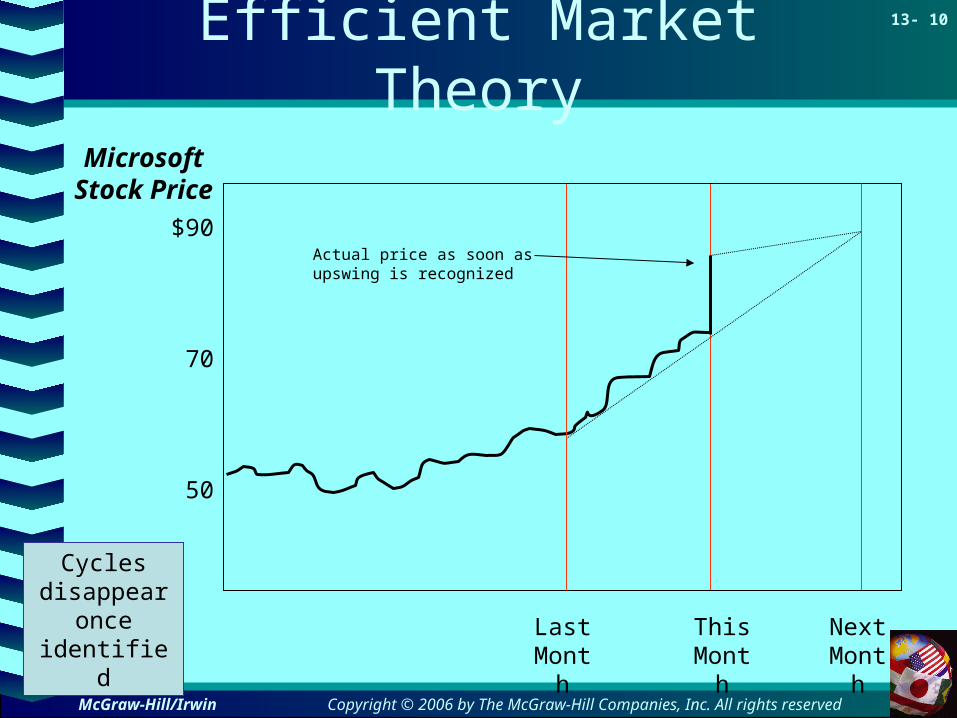

Efficient Market Theory

Last Month

This Month

Next Month

$90

70

50

Microsoft Stock Price

Cycles disappear

once identified

Actual price as soon as upswing is recognized

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

13- 11

McGraw-Hill/Irwin

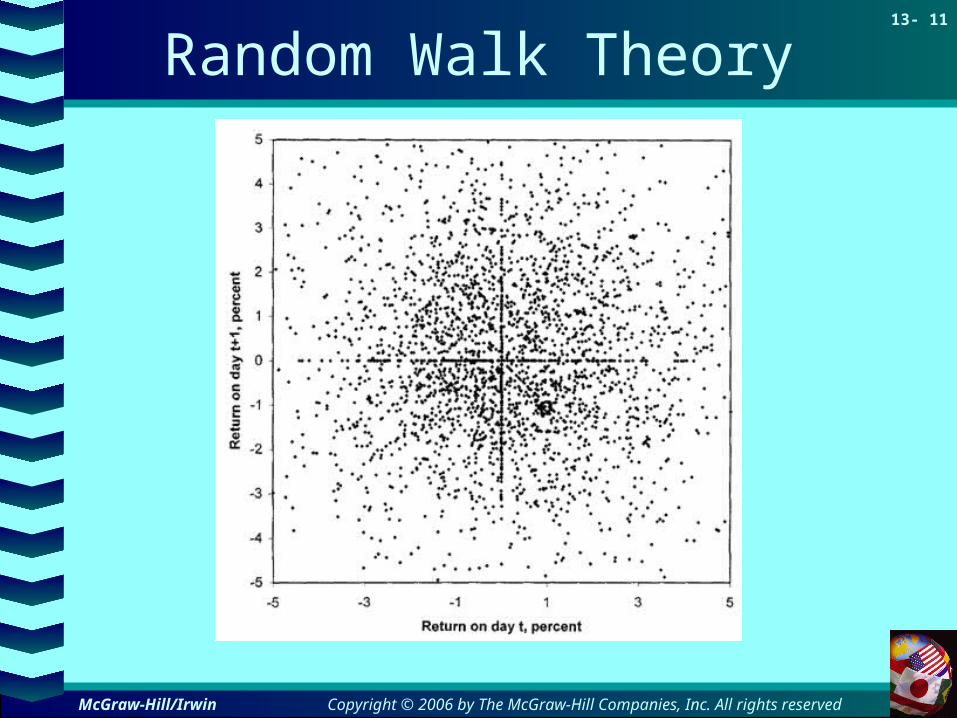

Random Walk Theory

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

13- 12

McGraw-Hill/Irwin

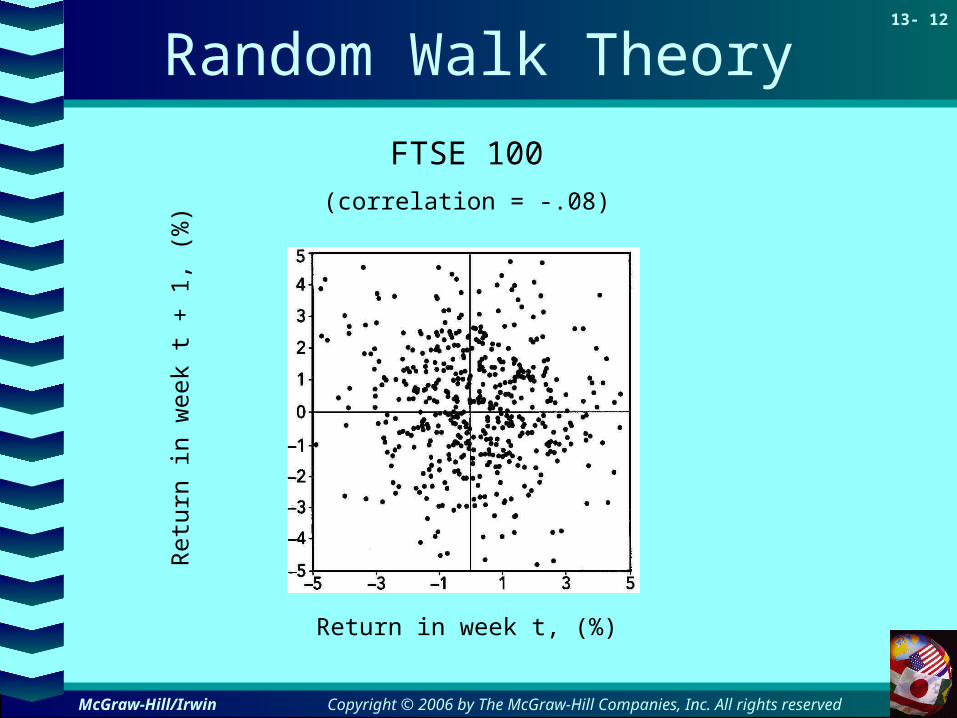

Random Walk Theory

Ret

urn

in w

eek

t + 1

, (%

)

Return in week t, (%)

FTSE 100

(correlation = -.08)

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

13- 13

McGraw-Hill/Irwin

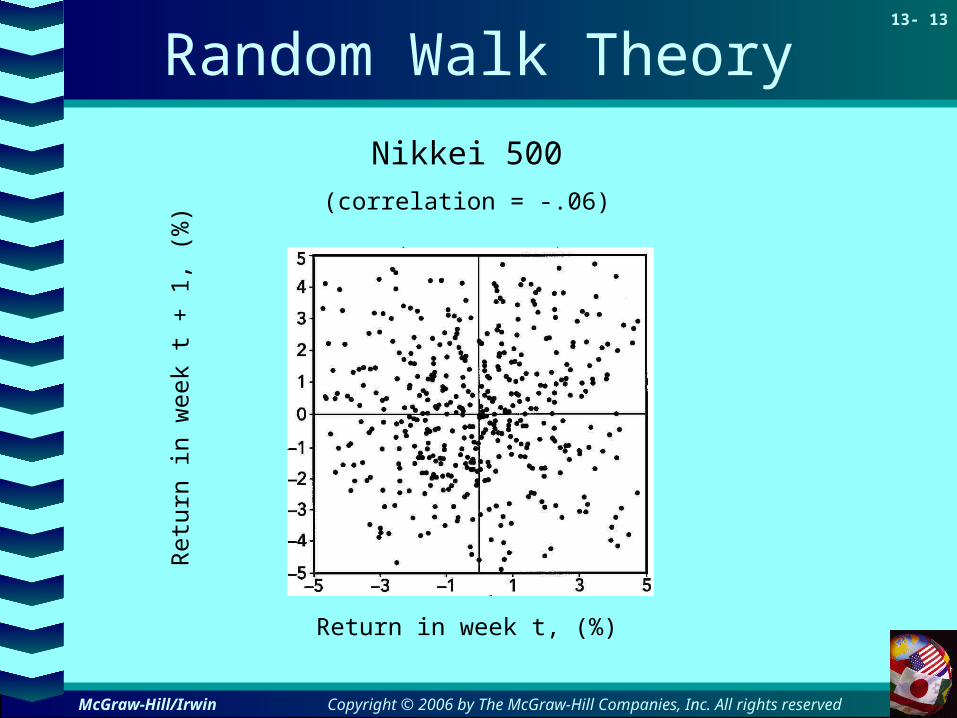

Random Walk Theory

Ret

urn

in w

eek

t + 1

, (%

)

Return in week t, (%)

Nikkei 500

(correlation = -.06)

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

13- 14

McGraw-Hill/Irwin

Random Walk Theory

Ret

urn

in w

eek

t + 1

, (%

)

Return in week t, (%)

DAX 30

(correlation = -.03)

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

13- 15

McGraw-Hill/Irwin

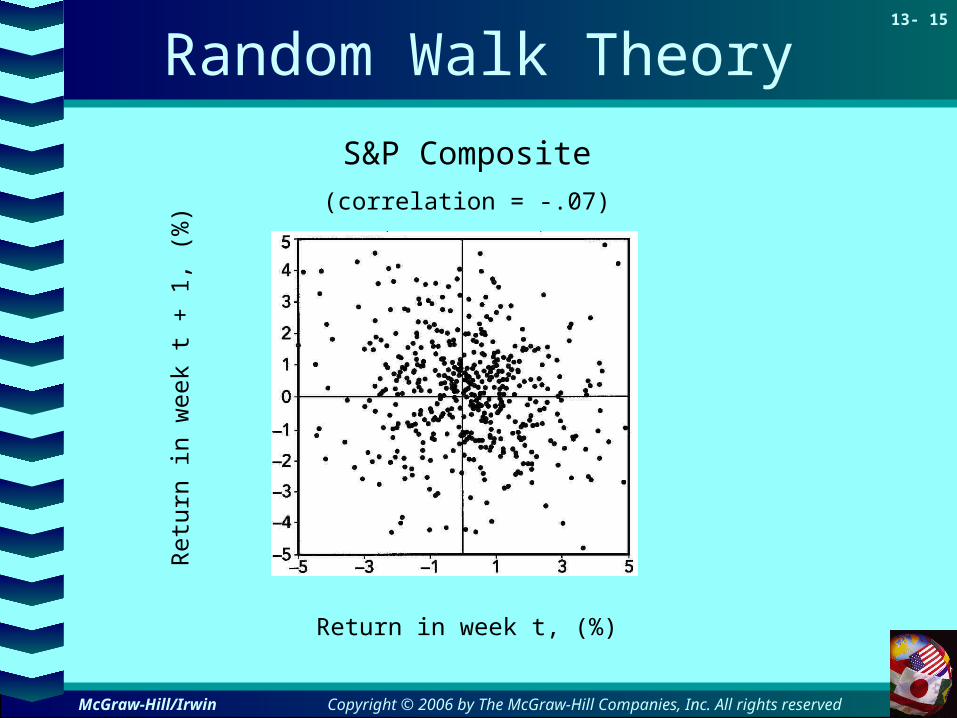

Random Walk Theory

Ret

urn

in w

eek

t + 1

, (%

)

Return in week t, (%)

S&P Composite

(correlation = -.07)

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

13- 16

McGraw-Hill/Irwin

Efficient Market Theory

Weak Form Efficiency– Market prices reflect all historical information

Semi-Strong Form Efficiency– Market prices reflect all publicly available

information

Strong Form Efficiency– Market prices reflect all information, both

public and private

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

13- 17

McGraw-Hill/Irwin

Efficient Market Theory

Fundamental Analysts– Research the value of stocks using NPV and other

measurements of cash flow

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

13- 18

McGraw-Hill/Irwin

Efficient Market Theory

Technical Analysts– Forecast stock prices based on the watching the

fluctuations in historical prices (thus “wiggle wiggle watcherswatchers”)

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

13- 19

McGraw-Hill/Irwin

Efficient Market Theory

-16

-11

-6

-1

4

9

14

19

24

29

34

39

Days Relative to annoncement date

Cu

mu

lati

ve

Ab

no

rma

l Re

turn

(%

)

Announcement Date

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

13- 20

McGraw-Hill/Irwin

Efficient Market Theory

-40

-30

-20

-10

0

10

20

30

40

1962

1977

1992

Re

turn

(%

)

Funds

Market

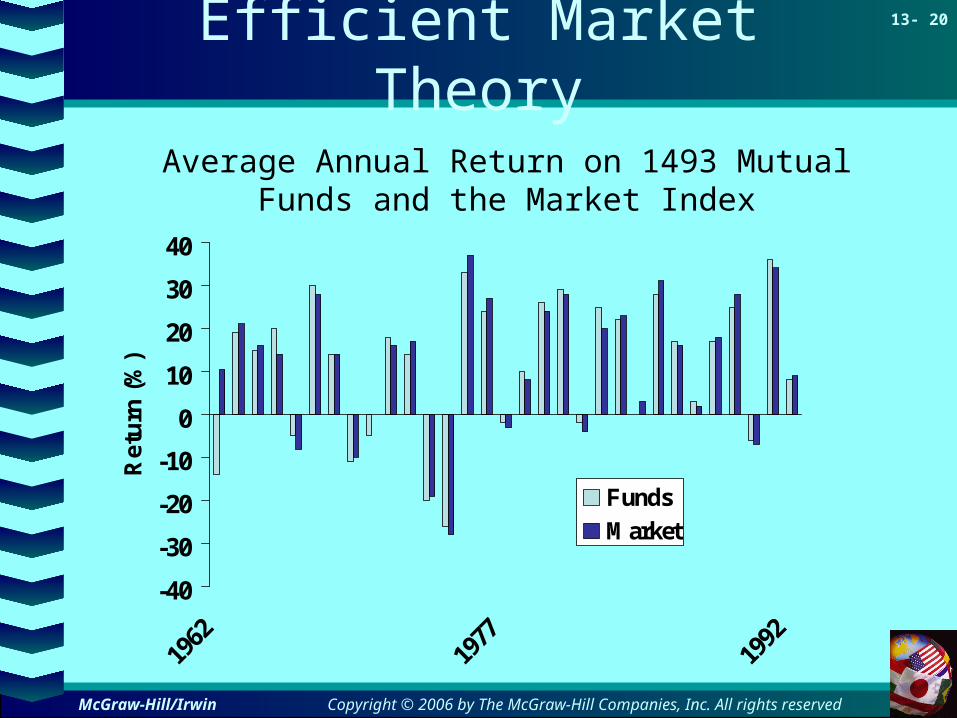

Average Annual Return on 1493 Mutual Funds and the Market Index

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

13- 21

McGraw-Hill/Irwin

Efficient Market Theory

0

5

10

15

20

First Second Third Fourth Fifth

Av

era

ge

Re

turn

(%

)

IPO

Matched Stocks

IPO Non-Excess Returns

Year After Offering

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

13- 22

McGraw-Hill/Irwin

Efficient Market Theory

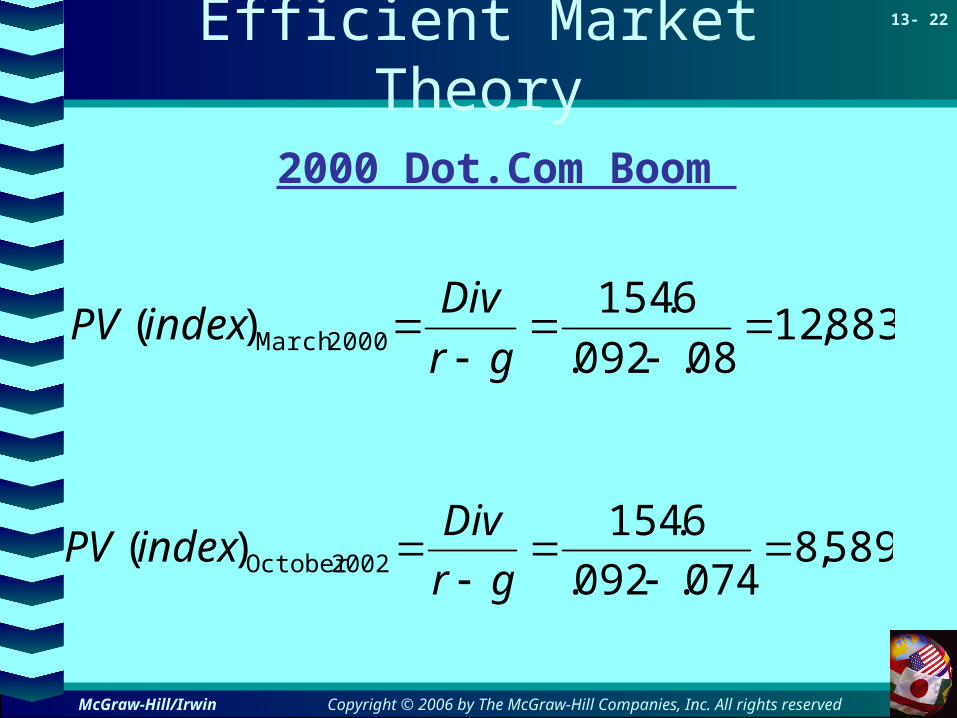

2000 Dot.Com Boom

883,1208.092.

6.154)( 2000 March

gr

DivindexPV

589,8074.092.

6.154)( 2002October

gr

DivindexPV

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

13- 23

McGraw-Hill/Irwin

Lessons of Market Efficiency

Markets have no memoryTrust market pricesRead the entrailsThere are no financial illusionsThe do it yourself alternativeSeen one stock, seen them all

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

13- 24

McGraw-Hill/Irwin

Example: How stock splits affect value

0

5

10

15

20

25

30

35

40

Month relative to split

Cumulative abnormal return %

-29 0 30

Source: Fama, Fisher, Jensen & Roll