Chapter 1 Introduction to Cost and Management Accounting in a Global Business Environment Cost...

34

Chapter 1 Introduction to Cost and Management Accounting in a Global Business Environment Cost Accounting Traditions and Innovations Barfield, Raiborn, Kinney

-

Upload

elinor-cameron -

Category

Documents

-

view

258 -

download

2

Transcript of Chapter 1 Introduction to Cost and Management Accounting in a Global Business Environment Cost...

Chapter 1

Introduction to Cost and Management Accounting in a Global Business

Environment

Cost AccountingTraditions and Innovations

Barfield, Raiborn, Kinney

Learning Objectives (1 of 3)

• Explain the relationship between financial and management accounting

• Describe the relationships among cost, financial, and management accounting

• Describe the role of ethics in guiding workforce behavior

• Identify the factors that influence the globalization of business

Learning Objectives (2 of 3)

• List the primary factors and constraints that influence an organization’s strategy

• Explain the impact of the competitive environment on an organization’s strategy

• Clarify the impact of the accounting function on achievement of strategic goals and objectives

Learning Objectives (3 of 3)

• Explain the effect of the product life cycle on the company segment’s mission

• Describe the importance of the value chain

Accounting

The Language

ofBusiness

Accounting• Provides information to external parties

– Stockholders, creditors, regulators

• Estimates the cost of products produced and services provided

• Provides information to internal decision makers– To plan, control, and evaluate performance

Two Types of Accounting

Financial• Meet external

information needs• Comply with GAAP

Management• Meet internal

information needs• Provide product

costing information

Financial Accounting Should

Provide information tostockholders, creditors, andvarious regulatory bodies

Comply with GAAP

Management Accounting Should

Provide informationuseful for

making decisionsand controlling

operations

Provide product costing informationfor external financial statements

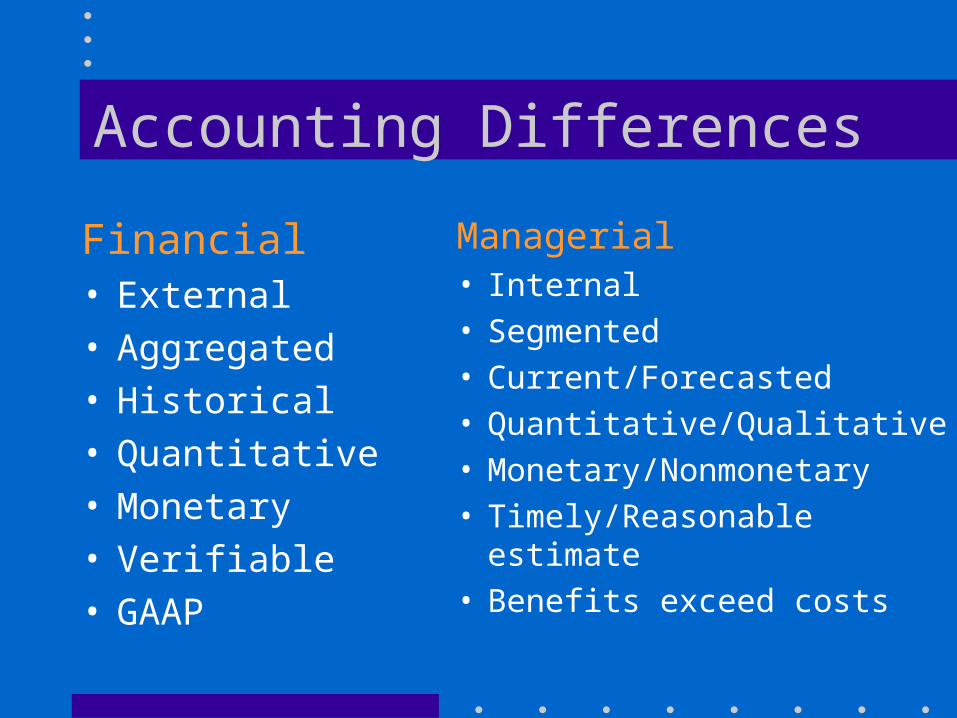

Accounting Differences

Financial• External• Aggregated• Historical• Quantitative• Monetary• Verifiable• GAAP

Managerial• Internal• Segmented• Current/Forecasted• Quantitative/Qualitative• Monetary/Nonmonetary• Timely/Reasonable estimate• Benefits exceed costs

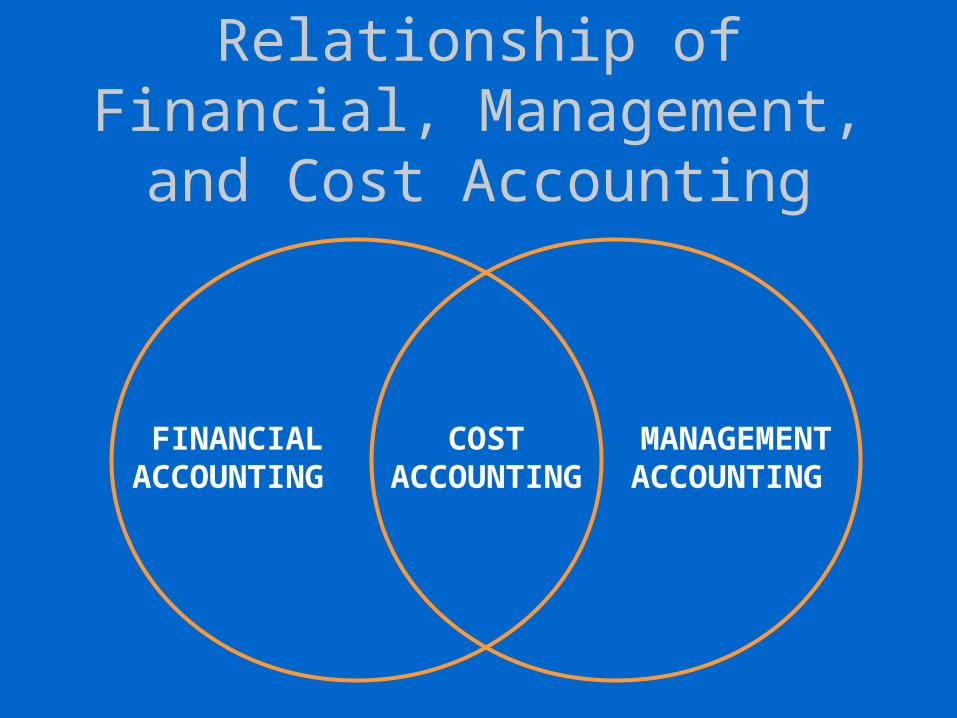

Relationship of Financial, Management, and Cost

Accounting

FINANCIALACCOUNTING

MANAGEMENTACCOUNTING

COSTACCOUNTING

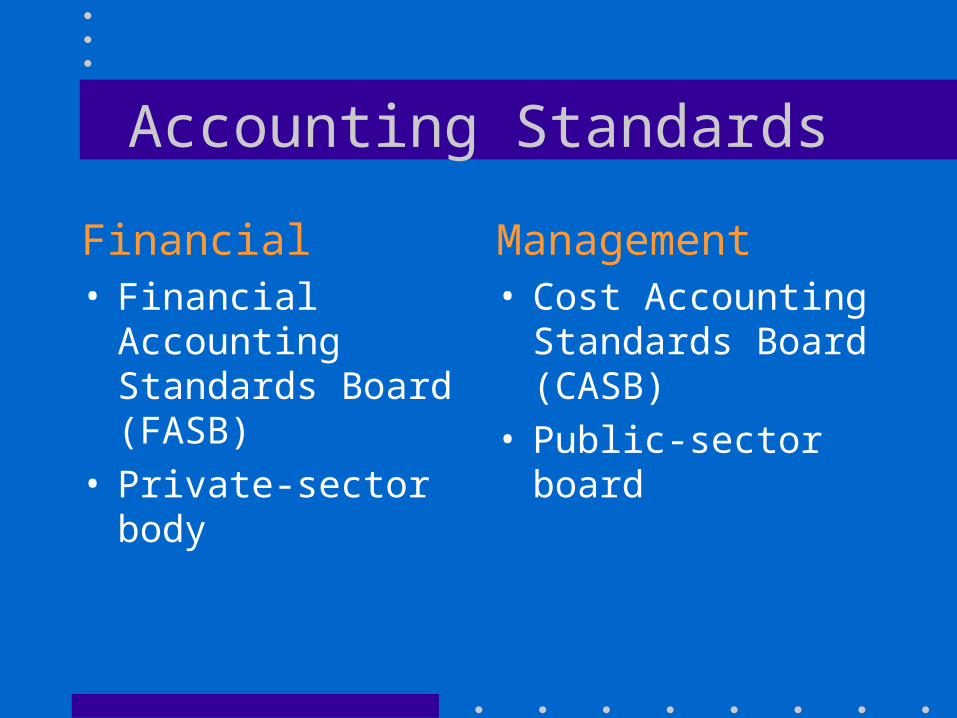

Accounting Standards

Financial• Financial Accounting

Standards Board (FASB)

• Private-sector body

Management• Cost Accounting

Standards Board (CASB)

• Public-sector board

Accounting OrganizationsInstitute of Management

Accountants (IMA)• Statements on Management

Accounting (not legally binding)

• Certified Management Accountant (CMA)

• Certified in Financial Management (CFM)

Society of Management Accountants of Canada

• Management Accounting Guidelines (not legally binding)

Ethics & Management Accountants

• Standards of Ethical Conduct for Management Accountants– Competence– Confidentiality– Integrity– Objectivity

CompetenceConfidentialityIntegrityObjectivity

International trade of goods and servicesInternational movement of laborInternational flows of capital and information

Global Business Environment

Global Business Challenges

• Understand the factors influencing international business markets

• Devise a long-term plan to achieve organizational goals

• Develop information systems that keep the company’s operations consistent with its plans and goals

Global Business Environment

• Electronic Commerce

• Trade Agreements– North American Free Trade Agreement

(NAFTA)– General Agreement on Tariffs and Trade

(GATT)

Members agreed to allow duty-free transfer of goods

under certain conditions

North American Free Trade Agreement (NAFTA)

General Agreement on Tariffs and Trade (GATT)

To provide a “level playing field” fortrade among the 100+ signatory nations

Global Business Environment

Risks

• Strategic– Environment and Organization

• Operating

• Financial

• Information

Ethical Considerations– Is it legal?– Does it comply with our values?– How will it look in the newspaper?– If you do it, will you feel bad?

– If it’s wrong, don’t do it.– If you’re not sure, ask.

Global Business Environment

Goals and Objectives

Strategic Planning

Tactical Planning

OrganizationalStrategy

Organizational Strategy

• Organizational Structure

• Core Competencies

• Organizational Constraints

• Organizational Culture

• Environmental Constraints

Organizational Strategy

• Organizational Structure

Centralization Decentralization

Organizational Strategy

• Organizational Structure

• Core Competencies– A higher proficiency than the competitors– Technological innovation– Engineering– Product development– After-sale service

Organizational Strategy

• Organizational Structure

• Core Competencies

• Organizational Constraints– Monetary Capital– Intellectual Capital

• Human Capital• Structural Capital• Relationship Capital

Organizational Strategy

• Organizational Structure

• Core Competencies

• Organizational Constraints

• Organizational Culture– An organization’s norms

• internal and external• formal and informal

Organizational Strategy• Organizational Structure

• Core Competencies

• Organizational Constraints

• Organizational Culture

• Environmental Constraints– Limitations on strategy caused by external

differences in culture, competitive market structures, fiscal policy, laws, or political situations

Business Intelligence System

• Information about internal processes

• Knowledge of markets, technologies, and competitors

Formal process for gathering and analyzing information and producing intelligence to

meet decision-making needs

Business Intelligence

Competitive Intelligence

CompetitorAnalysis

Levels of Intelligence Gathering

Business Segments

• Segment Mission relates to Product Life Cycle– Build– Hold– Harvest

Accounting Information• Strategic Resource Management

– Planning for deployment of resources to create value for customers and shareholders

• Value Chain—Foundation of SRM– Set of processes that convert inputs into products and

services

Use accounting information to evaluate the value chain to improve strategic resource management

The Accountant’s Role

• Accountants provide information that is used to– make strategic decisions– measure and evaluate management– provide appropriate incentives– provide information about the value chain

Questions

• What is the relationship among cost, financial, and management accounting?

• How do ethics guide workforce behavior?

• What is the impact of the accounting function on achievement of strategic goals and objectives?