Cbm Report Sonu Kumar

56

FINANCE PROJECT REPORT ON “IMPLEMENTATION OF BASEL II WITH SPECIFIC FOCUS ON LIQUIDITY RISK MANAGEMENT” PRESENTED TO:- PRESENTED BY:- DR. VIDYA SHEKHRI, SAKSHI SINGH BM09183 (CHAIRPERSON, FINANCE) SHIKHAR SWAROOP BM09197 IMS GHAZIABAD SONU KUMAR BM09212 SUNEET KHANNA BM09217 VANDANA DUBEY BM09231 VARUN PRATAP SINGH BM09232 RISHABH AGARWAL BM09244

Transcript of Cbm Report Sonu Kumar

8/8/2019 Cbm Report Sonu Kumar

http://slidepdf.com/reader/full/cbm-report-sonu-kumar 1/56

FINANCE PROJECT REPORT

ON

“IMPLEMENTATION OF BASEL II

WITH SPECIFIC

FOCUS ON LIQUIDITY RISK MANAGEMENT”

PRESENTED TO:- PRESENTED BY:-

DR. VIDYA SHEKHRI, SAKSHI SINGH BM09183

(CHAIRPERSON, FINANCE) SHIKHAR SWAROOP BM09197

IMS GHAZIABAD SONU KUMAR BM09212

SUNEET KHANNA BM09217

VANDANA DUBEY BM09231

VARUN PRATAP SINGH BM09232

RISHABH AGARWAL BM09244

8/8/2019 Cbm Report Sonu Kumar

http://slidepdf.com/reader/full/cbm-report-sonu-kumar 2/56

CERTIFICATE

TO WHOM SO EVER MAY IT CONCERN

This is to certify that Sakshi Singh, Shikhar Swaroop, Sonu Kumar, Sunnet Khanna, Vandana

Dubey, Varun pratap singh and Rishabh Agarwal have completed the project report titled

“IMPLEMENTATION OF BASEL II WITH SPECIFIC FOCUS ON LIQUIDITYRISK MANAGEMENT” under my supervision. To the best of my knowledge and belief

this is their original work and this, wholly or partially, has not been submitted for any degree

of this or any other University.

8/8/2019 Cbm Report Sonu Kumar

http://slidepdf.com/reader/full/cbm-report-sonu-kumar 3/56

DECLARATION

We hereby declare that the project report on ““ IMPLEMENTATION OF BASEL II WITH SPECIFIC FOCUS ON LIQUIDITY RISK MANAGEMENT ”” in commercial bank

management is being submitted by the Group members to INSTITUTE OF MANAGEMENT

STUDIES, GHAZIABAD, is the result of our own work and efforts. It has not been

published in any magazine, book or newspaper yet. All other sources of information have

been duly acknowledged.

8/8/2019 Cbm Report Sonu Kumar

http://slidepdf.com/reader/full/cbm-report-sonu-kumar 4/56

ACKNOWLEDGMENT

It is an opportunity we take to acknowledge the efforts of many individuals who helped us in

making this project possible. First and foremost, we would like to express our heartfelt

appreciation and gratitude to our guide and facilitator of the course, Dr. Vidya Sekhri . Her

vision and execution aimed at creating a structure, definition, and realism around the course

of Commercial Bank Management fostered the ideal environment for us to learn and grow.

This project is a result of her teaching, encouragement and inputs in the numerous meetings

she had with us, despite her busy schedule. She has helped provide us the scope and direct

our research in a manner to make it most beneficial to us and to the topic.

We would also like to thank the Institute of Management Studies, Ghaziabad for providing

us the opportunity to do a project in Financial Management.

Last but not the least; we would like to thank the information technology without which this

project wouldn’t have been possible.

8/8/2019 Cbm Report Sonu Kumar

http://slidepdf.com/reader/full/cbm-report-sonu-kumar 5/56

TABLE OF CONTENT

CHAPTER NAME PAGE NUMBER

EXECUTIVE SUMMARY 7

BASEL COMMITTEE 8

BASEL II ACCORD 10

NEW ACCORD 12

FIRST PILLAR 13

SECOND PILLAR 14

THIRD PILLAR 14

INTRODUCTION TO BANKING REFORM 15

MAJOR RECOMMENDATIONS BY NARSIMHAM

COMMITTEE AND BANKING SECTOR REFORM 16

STRENGTHENING BANKING SYSTEM 16

ASSET QUALITY 17

PRUDENTIAL NORMS AND

DISCLOSURE REQUIREMENTS 18

SYSTEM AND METHIDS IN BANKS 18

STRUCTURAL ISSUES 19

RECENT CHRONONLOGICAL UPDATES 20

TYPES OF LIQUIDITY RISKS 22

CAUSES OF LIQUIDITY RISKS 22

MEASURES OF LIQUIDITY RISKS 24

MEASURES OF ASSET LIQUIDITY 24

MANAGING LIQUIDITY RISK 25

TRADE FINANCING AND NEW RULES FOR

8/8/2019 Cbm Report Sonu Kumar

http://slidepdf.com/reader/full/cbm-report-sonu-kumar 6/56

MANAGING LIQUIDITY RISKS 27

BASEL II LIQUIDITY RISKS 29

GOVERNANCE OF LIQUIDITY RISK MANAGEMENT 32

MEASUREMENT AND MANAGEMENT IN

LIQUIDITY RISK 33

CAMEL’S FRAMEWORK 36

RESEARCH METHODOLOGY 43

AREA OF SURVEY 44

DATA SOURCE 44

SAMPLING TECHNIQUE 44

PLAN OF ANALYSIS 44

ANALYSIS AND INTERPRETATION 45

CAPITAL ADEQUACY 45

ASSET QUALITY 47

MANAGEMENT SOUNDNESS 48

EARNING AND PROFITABILITY 49

LIQUIDITY 50

FINDINGS 52

RECOMMENDATIONS 53

SUGGESTIONS 54

LIMITATIONS 55

BIBILOGRAPHY 56

8/8/2019 Cbm Report Sonu Kumar

http://slidepdf.com/reader/full/cbm-report-sonu-kumar 7/56

EXECUTIVE SUMMARY

The banking sector has been undergoing a complex, but comprehensive phase of

restructuring since 1991, with a view to make it sound, efficient, and at the same time forging

its links firmly with the real sector for promotion of savings, investment and growth.

Although a complete turnaround in banking sector performance is not expected till the

completion of reforms, signs of improvement are visible in some indicators under the

CAMEL framework. Under this bank is required to enhance capital adequacy, strengthenasset quality, improve management, increase earnings and reduce sensitivity to various

financial risks. The almost simultaneous nature of these developments makes it difficult to

disentangle the positive impact of reform measures. Keeping this in mind, signs of

improvements and deteriorations are discussed for the three groups of scheduled banks in the

following sections.

8/8/2019 Cbm Report Sonu Kumar

http://slidepdf.com/reader/full/cbm-report-sonu-kumar 8/56

ABOUT THE BASEL COMMITEE

The Basel Committee on Banking Supervision provides a forum for regular cooperation on

banking supervisory matters. Its objective is to enhance understanding of key supervisoryissues and improve the quality of banking supervision worldwide. It seeks to do so by

exchanging information on national supervisory issues, approaches and techniques, with a

view to promoting common understanding. At times, the Committee uses this common

understanding to develop guidelines and supervisory standards in areas where they are

considered desirable. In this regard, the Committee is best known for its international

standards on capital adequacy; the Core Principles for Effective Banking Supervision; and the

Concordat on cross-border banking supervision.

The Committee's members come from Argentina, Australia, Belgium, Brazil, Canada, China,

France, Germany, Hong Kong SAR, India, Indonesia, Italy, Japan, Korea, Luxembourg,

Mexico, the Netherlands, Russia, Saudi Arabia, Singapore, South Africa, Spain, Sweden,

Switzerland, Turkey, the United Kingdom and the United States. The present Chairman of the

Committee is Mr Nout Wellink, President of the Netherlands Bank.

The Committee encourages contacts and cooperation among its members and other banking

supervisory authorities. It circulates to supervisors throughout the world both published and

unpublished papers providing guidance on banking supervisory matters. Contacts have been

further strengthened by an International Conference of Banking Supervisors (ICBS) which

takes place every two years.

The Committee's Secretariat is located at the Bank for International Settlements in Basel,

Switzerland, and is staffed mainly by professional supervisors on temporary secondment

from member institutions. In addition to undertaking the secretarial work for the Committee

and its many expert sub-committees, it stands ready to give advice to supervisory authorities

in all countries. Mr Stefan Walter is the Secretary General of the Basel Committee.

8/8/2019 Cbm Report Sonu Kumar

http://slidepdf.com/reader/full/cbm-report-sonu-kumar 9/56

Main Expert Sub-Committees

The Committee's work is organized under four main sub-committees (organisation chart):

• The Standards Implementation Group

• The Policy Development Group

• The Accounting Task Force.

• The Basel Consultative Group

1) The Standards Implementation Group (SIG) was originally established to share

information and promote consistency in implementation of the Basel II Framework. In

January 2009, its mandate was broadened to concentrate on implementation of Basel

Committee guidance and standards more generally. It is chaired by Mr José María Roldán,

Director General of Banking Regulation at the Bank of Spain.

Currently the SIG has two subgroups that share information and discuss specific issues

related to Basel II implementation.

2) The primary objective of the Policy Development Group (PDG) is to support the

Committee by identifying and reviewing emerging supervisory issues and, where appropriate,

proposing and developing policies that promote a sound banking system and high supervisory

standards. The group is chaired by Mr Stefan Walter, Secretary General of the Basel

Committee.

Working Group on Liquidity serves as a forum for information exchange on national

approaches to liquidity risk regulation and supervision. In September 2008, the Working

Group issued Principles for Sound Liquidity Risk Management and Supervision, the globalstandards for liquidity risk management and supervision. The Working Group is also

examining the scope for additional steps to promote more robust and internationally

consistent liquidity approaches for cross-border banks.

3) The Accounting Task Force (ATF) works to help ensure that international accounting

and auditing standards and practices promote sound risk management at financial institutions,

support market discipline through transparency, and reinforce the safety and soundness of the

banking system.

8/8/2019 Cbm Report Sonu Kumar

http://slidepdf.com/reader/full/cbm-report-sonu-kumar 10/56

BASEL II ACCORD

Bank capital framework sponsored by the world's central banks designed to promote

uniformity, make regulatory capital more risk sensitive, and promote enhanced risk

management among large, internationally active banking organizations.

The International Capital Accord, as it is called, will be fully effective by January 2008 for

banks active in international markets. Other banks can choose to "opt in," or they can

continue to follow the minimum capital guidelines in the original Basel Accord, finalized in

1988. The revised accord (Basel II) completely overhauls the 1988 Basel Accord and is based

on three mutually supporting concepts, or "pillars," of capital adequacy.

The first of these pillars is an explicitly defined regulatory capital requirement, a minimum

capital-to-asset ratio equal to at least 8% of risk-weighted assets. Second, bank supervisory

agencies, such as the Comptroller of the Currency, have authority to adjust capital levels for

individual banks above the 8% minimum when necessary. The third supporting pillar calls

upon market discipline to supplement reviews by banking agencies.

Basel II is the second of the Basel Accords, which are recommendations on banking laws and

regulations issued by the Basel Committee on Banking Supervision. The purpose of Basel II,

which was initially published in June 2004, is to create an international standard that banking

regulators can use when creating regulations about how much capital banks need to put aside

to guard against the types of financial and operational risks banks face.

Advocates of Basel II believe that such an international standard can help protect the

international financial system from the types of problems that might arise should a major

bank or a series of banks collapse. In practice, Basel II attempts to accomplish this by setting

up rigorous risk and capital management requirements designed to ensure that a bank holds

capital reserves appropriate to the risk the bank exposes itself to through its lending and

investment practices. Generally speaking, these rules mean that the greater risk to which the

bank is exposed, the greater the amount of capital the bank needs to hold to safeguard its

solvency and overall economic stability.

8/8/2019 Cbm Report Sonu Kumar

http://slidepdf.com/reader/full/cbm-report-sonu-kumar 11/56

The final version aims at:

1. Ensuring that capital allocation is more risk sensitive;

2. Separating operational risk from credit risk, and quantifying both;

3. Attempting to align economic and regulatory capital more closely to reduce the scope for

regulatory arbitrage.

While the final accord has largely addressed the regulatory arbitrage issue, there are still

areas where regulatory capital requirements will diverge from the economic.

Basel II has largely left unchanged the question of how to actually define bank capital, which

diverges from accounting equity in important respects. The Basel I definition, as modified up

to the present, remains in place.

The Accord in operation

Basel II uses a "three pillars" concept –

(1) Minimum capital requirements (addressing risk),

(2) Supervisory review and

(3) Market discipline – to promote greater stability in the financial system.

8/8/2019 Cbm Report Sonu Kumar

http://slidepdf.com/reader/full/cbm-report-sonu-kumar 12/56

The Three Pillars of Basel II

The Basel I accord dealt with only parts of each of these pillars. For example: with respect to

the first Basel II pillar, only one risk, credit risk, was dealt with in a simple manner while

market risk was an afterthought; operational risk was not dealt with at all.

The First Pillar

The first pillar deals with maintenance of regulatory capital calculated for three major

components of risk that a bank faces: credit risk, operational risk and market risk. Other risks

are not considered fully quantifiable at this stage.

The credit risk component can be calculated in three different ways of varying degree of

sophistication, namely standardized approach, Foundation IRB and Advanced IRB. IRB

stands for "Internal Rating-Based Approach".

8/8/2019 Cbm Report Sonu Kumar

http://slidepdf.com/reader/full/cbm-report-sonu-kumar 13/56

For operational risk, there are three different approaches - basic indicator approach or BIA,

standardized approach or TSA, and advanced measurement approach or AMA.

For market risk the preferred approach is VaR (value at risk).

As the Basel 2 recommendations are phased in by the banking industry it will move from

standardised requirements to more refined and specific requirements that have been

developed for each risk category by each individual bank. The upside for banks that do

develop their own bespoke risk measurement systems is that they will be rewarded with

potentially lower risk capital requirements. In future there will be closer links between the

concepts of economic profit and regulatory capital.

Credit Risk can be calculated by using one of three approaches

1. Standardized Approach

2. Foundation IRB (Internal Ratings Based) Approach

3. Advanced IRB Approach

The standardized approach sets out specific risk weights for certain types of credit risk. The

standard risk weight categories are used under Basel 1 and are 0% for short term government

bonds, 20% for exposures to OECD Banks, 50% for residential mortgages and 100%

weighting on commercial loans. A new 150% rating comes in for borrowers with poor credit

ratings. The minimum capital requirement( the percentage of risk weighted assets to be held

as capital) remains at 8%.

For those Banks that decide to adopt the standardized ratings approach they will be forced to

rely on the ratings generated by external agencies. Certain Banks are developing the IRB

approach as a result.

8/8/2019 Cbm Report Sonu Kumar

http://slidepdf.com/reader/full/cbm-report-sonu-kumar 14/56

8/8/2019 Cbm Report Sonu Kumar

http://slidepdf.com/reader/full/cbm-report-sonu-kumar 15/56

INTRODUCTION TO THE BANKING REFORMS

In 1991, the Indian economy went through a process of economic liberalization, which was

followed up by the initiation of fundamental reforms in the banking sector in 1992. The

banking reform package was based on the recommendations proposed by the Narsimhan

Committee Report (1991) that advocated a move to a more market oriented banking system,

which would operate in an environment of prudential regulation and transparent accounting.

One of the primary motives behind this drive was to introduce an element of market

discipline into the regulatory process that would reinforce the supervisory effort of the

Reserve Bank of India (RBI). Market discipline, especially in the financial liberalization

phase, reinforces regulatory and supervisory efforts and provides a strong incentive to banks

to conduct their business in a prudent and efficient manner and to maintain adequate capital

as a cushion against risk exposures. Recognizing that the success of economic reforms was

contingent on the success of financial sector reform as well, the government initiated a

fundamental banking sector reform package in 1992.

Banking sector, the world over, is known for the adoption of multidimensional strategies

from time to time with varying degrees of success. Banks are very important for the smooth

functioning of financial markets as they serve as repositories of vital financial information

and can potentially alleviate the problems created by information asymmetries. From a

central bank’s perspective, such high-quality disclosures help the early detection of problems

faced by banks in the market and reduce the severity of market disruptions. Consequently, the

RBI as part and parcel of the financial sector deregulation, attempted to enhance the

transparency of the annual reports of Indian banks by, among other things, introducing

stricter income recognition and asset classification rules, enhancing the capital adequacy

norms, and by requiring a number of additional disclosures sought by investors to make

better cash flow and risk assessments.

During the pre economic reforms period, commercial banks & development financial

institutions were functioning distinctly, the former specializing in short & medium term

financing, while the latter on long term lending & project financing.

8/8/2019 Cbm Report Sonu Kumar

http://slidepdf.com/reader/full/cbm-report-sonu-kumar 16/56

Commercial banks were accessing short term low cost funds thru savings investments like

current accounts, savings bank accounts & short duration fixed deposits, besides collection

float. Development Financial Institutions (DFIs) on the other hand, were essentially

depending on budget allocations for long term lending at a concessionary rate of interest.

The scenario has changed radically during the post reforms period, with the resolve of the

government not to fund the DFIs through budget allocations. DFIs like IDBI, IFCI & ICICI

had posted dismal financial results. Infact, their very viability has become a question mark.

Now they have taken the route of reverse merger with IDBI bank & ICICI bank thus

converting them into the universal banking system.

MAJOR RECOMMENDATIONS BY THE NARASIMHAM COMMITTEE ON

BANKING SECTOR REFORMS

Strengthening Banking System

Capital adequacy requirements should take into account market risks in addition to the credit

risks.

In the next three years the entire portfolio of government securities should be marked to

market and the schedule for the same announced at the earliest (since announced in the

monetary and credit policy for the first half of 1998-99); government and other approved

securities which are now subject to a zero risk weight, should have a 5 per cent weight for

market risk.

Risk weight on a government guaranteed advance should be the same as for other advances.

This should be made prospective from the time the new prescription is put in place.

Foreign exchange open credit limit risks should be integrated into the calculation of risk

weighted assets and should carry a 100 per cent risk weight.

8/8/2019 Cbm Report Sonu Kumar

http://slidepdf.com/reader/full/cbm-report-sonu-kumar 17/56

Minimum capital to risk assets ratio (CRAR) be increased from the existing 8 per cent to 10

per cent; an intermediate minimum target of 9 per cent be achieved by 2000 and the ratio of

10 per cent by 2002; RBI to be empowered to raise this further for individual banks if the risk

profile warrants such an increase. Individual banks' shortfalls in the CRAR are treated on the

same line as adopted for reserve requirements, viz. uniformity across weak and strong banks.

There should be penal provisions for banks that do not maintain CRAR.

Public Sector Banks in a position to access the capital market at home or abroad be

encouraged, as subscription to bank capital funds cannot be regarded as a priority claim on

budgetary resources.

Asset Quality

An asset is classified as doubtful if it is in the substandard category for 18 months in the first

instance and eventually for 12 months and loss if it has been identified but not written off.

These norms should be regarded as the minimum and brought into force in a phased manner.

For evaluating the quality of assets portfolio, advances covered by Government guarantees,

which have turned sticky, be treated as NPAs. Exclusion of such advances should be

separately shown to facilitate fuller disclosure and greater transparency of operations.

For banks with a high NPA portfolio, two alternative approaches could be adopted. One

approach can be that, all loan assets in the doubtful and loss categories should be identified

and their realisable value determined. These assets could be transferred to an Assets

Reconstruction Company (ARC) which would issue NPA Swap Bonds.

An alternative approach could be to enable the banks in difficulty to issue bonds which could

from part of Tier II capital, backed by government guarantee to make these instruments

eligible for SLR investment by banks and approved instruments by LIC, GIC and Provident

Funds.

8/8/2019 Cbm Report Sonu Kumar

http://slidepdf.com/reader/full/cbm-report-sonu-kumar 18/56

The interest subsidy element in credit for the priority sector should be totally eliminated and

interest rate on loans under Rs. 2 lakhs should be deregulated for scheduled commercial

banks as has been done in the case of Regional Rural Banks and cooperative credit

institutions.

Prudential Norms and Disclosure Requirements

In India, income stops accruing when interest or installment of principal is not paid within

180 days, which should be reduced to 90 days in a phased manner by 2002.

Introduction of a general provision of 1 per cent on standard assets in a phased manner be

considered by RBI.

As an incentive to make specific provisions, they may be made tax deductible.

Systems and Methods in Banks

There should be an independent loan review mechanism especially for large borrowal

accounts and systems to identify potential NPAs. Banks may evolve a filtering mechanism by

stipulating in-house prudential limits beyond which exposures on single/group borrowers are

taken keeping in view their risk profile as revealed through credit rating and other relevant

factors.

Banks and FIs should have a system of recruiting skilled manpower from the open market.

Public sector banks should be given flexibility to determined managerial remuneration levels

taking into account market trends.

There may be need to redefine the scope of external vigilance and investigation agencies with

regard to banking business.

8/8/2019 Cbm Report Sonu Kumar

http://slidepdf.com/reader/full/cbm-report-sonu-kumar 19/56

There is need to develop information and control system in several areas like better tracking

of spreads, costs and NPSs for higher profitability, , accurate and timely information for

strategic decision to Identify and promote profitable products and customers, risk and asset-

liability management; and efficient treasury management.

Structural Issues

With the conversion of activities between banks and DFIs, the DFIs should, over a period of

time convert them to bank. A DFI which converts to bank be given time to face in reserve

equipment in respect of its liability to bring it on par with requirement relating to commercial

bank.

Mergers of Public Sector Banks should emanate from the management of the banks with the

Government as the common shareholder playing a supportive role. Merger should not be seen

as a means of bailing out weak banks. Mergers between strong banks/FIs would make for

greater economic and commercial sense.

‘Weak Banks' may be nurtured into healthy units by slowing down on expansion, eschewing

high cost funds/borrowings etc.

The minimum share of holding by Government/Reserve Bank in the equity of the

nationalised banks and the State Bank should be brought down to 33%. The RBI regulator of

the monetary system should not be also the owner of a bank in view of the potential for

possible conflict of interest.

There is a need for a reform of the deposit insurance scheme based on CAMELs ratings

awarded by RBI to banks.

Inter-bank call and notice money market and inter-bank term money market should be strictly

restricted to banks; only exception to be made is primary dealers.

Non-bank parties are provided free access to bill rediscounts, CPs, CDs, Treasury Bills, and

MMMF.

RBI should totally withdraw from the primary market in 91 days Treasury Bills.

8/8/2019 Cbm Report Sonu Kumar

http://slidepdf.com/reader/full/cbm-report-sonu-kumar 20/56

RECENT CHRONOLOGICAL UPDATES

September 2005

On September 30, 2005, the four US Federal banking agencies (the Office of the Comptroller

of the currency, the Board of Governors of the Federal Reserve System, the Federal Deposit

Insurance Corporation, and the Office of Thrift Supervision) announced their revised plans for

the U.S. implementation of the Basel II accord. This delays implementation of the accord for

US banks by 12months

November 2005

On November 15, 2005, the committee released a revised version of the Accord, incorporating

changesto the calculations for market risk and the treatment of double default effects. These changes

had been flagged well in advance, as part of a paper released in July 2005

On July 4, 2006, the committee released a comprehensive version of the Accord, incorporating

the June 2004 Basel II Framework, the elements of the 1988 Accord that were not revised

during the Basel II

process, the 1996 Amendment to the Capital Accord to Incorporate Market Risks, and the

November 2005 paper on Basel II: International Convergence of Capital Measurement and

Capital Standards: A Revised Framework. No new elements have been introduced in this

compilation. This version is now the

currentversion.

November 2007

On November 1, 2007, the Office of the Comptroller of the Currency(U.S. Department

oftheTreasury) approved a final rule implementing the advanced approaches of the

BaselIICapitalAccord.Thisruleestablishes regulatory and supervisory expectations for credit

risk, through the Internal Ratings Based Approach (IRB), and operational risk, through the

Advanced Measurement Approach (AMA),andarticulates enhanced standards for the

supervisory review of capital adequacy and public disclosures forReserve System; the Federal

Deposit Insurance Corporation; the Office of the Comptroller of the

Currency, and; the Office of Thrift Supervision) issued a final guidance outlining the

supervisory review process for the banking institutions that are implementing the new advanced

8/8/2019 Cbm Report Sonu Kumar

http://slidepdf.com/reader/full/cbm-report-sonu-kumar 21/56

capital adequacy framework (known as Basel II). The final guidance, relating to the

supervisory review, is aimed at helping banking institutions meet certain qualification

requirements in the advanced approaches rule.

January 16, 2009

For public consultation, a series of proposals to enhance the Basel II framework was announced

by the Basel Committee. It releases a consultative package that includes: therevisions to the

BaselII marketrisk framework; the guidelines for computing capital for incremental risk in the

trading book;and the proposed enhancements to the Basel II framework.

July 8-9, 2009

A final package of measures to enhance the three pillars of the Basel II framework and to

strengthen the 1996 rules governing trading book capital was issued by the newly expanded

Basel Committee. These measures include the enhancements to the Basel II framework, the

revisions to the Basel II market-risk framework and the guidelines for computing capital for

incremental risk in the trading .

8/8/2019 Cbm Report Sonu Kumar

http://slidepdf.com/reader/full/cbm-report-sonu-kumar 22/56

TYPES OF LIQUIDITY RISK

Asset liquidity - An asset cannot be sold due to lack of liquidity in the market - essentially a

sub-set of market risk. This can be accounted for by:

• Widening bid/offer spread

• Making explicit liquidity reserves

• Lengthening holding period for VaR calculations

Funding liquidity - Risk that liabilities:

• Cannot be met when they fall due Can only be met at an uneconomic price

• Can be name-specific or systemic

Causes of liquidity risk

Liquidity risk arises from situations in which a party interested in trading an asset cannot do it

because nobody in the market wants to trade that asset. Liquidity risk becomes particularly

important to parties who are about to hold or currently hold an asset, since it affects their

ability to trade.

Manifestation of liquidity risk is very different from a drop of price to zero. In case of a drop

of an asset's price to zero, the market is saying that the asset is worthless. However, if one

party cannot find another party interested in trading the asset, this can potentially be only a

problem of the market participants with finding each other. This is why liquidity risk is

usually found higher in emerging markets or low-volume markets.

Liquidity risk is financial risk due to uncertain liquidity. An institution might lose liquidity if

its credit rating falls, it experiences sudden unexpected cash outflows, or some other event

causes counterparties to avoid trading with or lending to the institution. A firm is also

exposed to liquidity risk if markets on which it depends are subject to loss of liquidity.

Liquidity risk tends to compound other risks. If a trading organization has a position in an

illiquid asset, its limited ability to liquidate that position at short notice will compound its

market risk. Suppose a firm has offsetting cash flows with two different counterparties on a

given day.

8/8/2019 Cbm Report Sonu Kumar

http://slidepdf.com/reader/full/cbm-report-sonu-kumar 23/56

If the counterparty that owes it a payment defaults, the firm will have to raise cash from other

sources to make its payment. Should it be unable to do so, it too will default. Here, liquidity

risk is compounding credit risk.

A position can be hedged against market risk but still entail liquidity risk. This is true in the

above credit risk example—the two payments are offsetting, so they entail credit risk but not

market risk. Another example is the 1993 Metallgesellschaft debacle. Futures contracts were

used to hedge an Over-the-counter finance OTC obligation. It is debatable whether the hedge

was effective from a market risk standpoint, but it was the liquidity crisis caused by

staggering margin calls on the futures that forced Metallgesellschaft to unwind the positions.

Accordingly, liquidity risk has to be managed in addition to market, credit and other risks.Because of its tendency to compound other risks, it is difficult or impossible to isolate

liquidity risk. In all but the most simple of circumstances, comprehensive metrics of liquidity

risk do not exist. Certain techniques of asset-liability management can be applied to assessing

liquidity risk. A simple test for liquidity risk is to look at future net cash flows on a day-by-

day basis. Any day that has a sizeable negative net cash flow is of concern. Such an analysis

can be supplemented with stress testing. Look at net cash flows on a day-to-day basis

assuming that an important counterparty defaults.

Analyses such as these cannot easily take into account contingent cash flows, such as cash

flows from derivatives or mortgage-backed securities. If an organization's cash flows are

largely contingent, liquidity risk may be assessed using some form of scenario analysis. A

general approach using scenario analysis might entail the following high-level steps:

• Construct multiple scenarios for market movements and defaults over a given period

of time

• Assess day-to-day cash flows under each scenario.

Because balance sheets differ so significantly from one organization to the next, there is little

standardization in how such analyses are implemented.

Regulators are primarily concerned about systemic and implications of liquidity risk.

8/8/2019 Cbm Report Sonu Kumar

http://slidepdf.com/reader/full/cbm-report-sonu-kumar 24/56

Measures of liquidity risk:-

Liquidity gap

Culp defines the liquidity gap as the net liquid assets of a firm. The excess value of the firm's

liquid assets over its volatile liabilities. A company with a negative liquidity gap should focus

on their cash balances and possible unexpected changes in their values.

As a static measure of liquidity risk it gives no indication of how the gap would change with

an increase in the firm's marginal funding cost.

Liquidity risk elasticity

Culp denotes the change of net of assets over funded liabilities that occurs when the liquidity

premium on the bank's marginal funding cost rises by a small amount as the liquidity risk

elasticity. For banks this would be measured as a spread over libor, for nonfinancials the LRE

would be measured as a spread over commercial paper rates.

Problems with the use of liquidity risk elasticity are that it assumes parallel changes in

funding spread across all maturities and that it is only accurate for small changes in funding

spreads.

Measures of Asset Liquidity

Bid-offer spread

The bid-offer spread is used by market participants as an asset liquidity measure. To compare

different products the ratio of the spread to the product's mid price can be used. The smaller

the ratio the more liquid the asset is This spread is composed of operational, administrative,

and processing costs as well as the compensation required for the possibility of trading with a

more informed trader .

Hachmeister refers to market depth as the amount of an asset that can be bought and sold at

various bid-ask spreads. Slippage is related to the concept of market depth. Knight and

Satchell mention a flow trader needs to consider the effect of executing a large order on the

market and to adjust the bid-ask spread accordingly. They calculate the liquidity cost as thedifference of the execution price and the initial execution price.

8/8/2019 Cbm Report Sonu Kumar

http://slidepdf.com/reader/full/cbm-report-sonu-kumar 25/56

Immediacy

Immediacy refers to the time needed to successfully trade a certain amount of an asset at a

prescribed cost.

Resilience

Hachmeister identifies the fourth dimension of liquidity as the speed with which prices return

to former levels after a large transaction. Unlike the other measures resilience can only be

determined over a period of

Managing Liquidity Risk

Liquidity-adjusted value at risk

Liquidity-adjusted VAR incorporates exogenous liquidity risk into Value at Risk. It can be

defined at VAR + ELC (Exogenous Liquidity Cost). The ELC is the worst expected half-

spread at a particular confidence level.

Another adjustment is to consider VAR over the period of time needed to liquidate the

portfolio. VAR can be calculated over this time period. The BIS mentions "... a number of

institutions are exploring the use of liquidity adjusted-VAR, in which the holding periods in

the risk assessment are adjusted by the length of time required to unwind positions."

Liquidity at risk

Greenspan (1999) discusses management of foreign exchange reserves. The Liquidity at risk

measure is suggested. A country's liquidity position under a range of possible outcomes for

relevant financial variables (exchange rates, commodity prices, credit spreads, etc.) is

considered. It might be possible to express a standard in terms of the probabilities of different

outcomes. For example, an acceptable debt structure could have an average maturity—

averaged over estimated distributions for relevant financial variables—in excess of a certain

limit. In addition, countries could be expected to hold sufficient liquid reserves to ensure that

they could avoid new borrowing for one year with a certain ex ante probability, such as 95

percent of the time.

8/8/2019 Cbm Report Sonu Kumar

http://slidepdf.com/reader/full/cbm-report-sonu-kumar 26/56

Scenario analysis-based contingency plans

The FDIC discuss liquidity risk management and write "Contingency funding plans should

incorporate events that could rapidly affect an institution’s liquidity, including a sudden

inability to securitize assets, tightening of collateral requirements or other restrictive terms

associated with secured borrowings, or the loss of a large depositor or counterparty.".

Greenspan's liquidity at risk concept is an example of scenario based liquidity risk

management.

Diversification of liquidity providers

If several liquidity providers are on call then if any of those providers increases its costs of

supplying liquidity, the impact of this is reduced. The American Academy of Actuaries wrote

"While a company is in good financial shape, it may wish to establish durable, ever-green

(i.e., always available) liquidity lines of credit. The credit issuer should have an appropriately

high credit rating to increase the chances that the resources will be there when needed."

Derivatives

five derivatives created specifically for hedging liquidity risk.:-

• Withdrawal option: A put of the illiquid underlying at the market price.

• Bermudan-style return put option: Right to put the option at a specified strike.

• Return swap: Swap the underlings’ return for LIBOR paid periodically.

• Return swaption: Option to enter into the return swap.

• Liquidity option: "Knock-in" barrier option, where the barrier is a liquidity metric.

8/8/2019 Cbm Report Sonu Kumar

http://slidepdf.com/reader/full/cbm-report-sonu-kumar 27/56

TRADE FINANCING AND NEW RULES FOR MANAGING LIQUIDITY RISK

Since the outbreak of the credit crisis in mid-2007 many banks have faced serious difficulties

in obtaining liquidity adequate for the ongoing funding of their operations. These difficulties

have led to unprecedented levels of liquidity support from governments and central banks

together with other official intervention such as the arrangement of mergers for weakened or

failing institutions. Moreover the experience of the crisis highlighted the close connections

between banks’ liquidity risks and threats to their solvency (the target of Basel 2), and have

provided the impetus for new international initiatives on standards for banks’ management of

liquidity risk, i.e. the risk that a bank will not be able to meet its obligations as they fall due

(BCBS, 2008 and 2009).

The proposals of these initiatives make explicit reference to instruments of trade finance as a

subject which is to be taken into account as part of the management of liquidity risk.

Although management of liquidity risk is not formally part of Basel 2,acknowledgement of

the connections between liquidity risk and threats to solvency is likely to mean that the new

standards for liquidity risk will form an essential part of the package of revised regulatory

standards for banks being developed by the Basel Committee on Banking Supervision to

incorporate the lessons of the crisis. Since theproposals described in this section are still the

subject of a consultation process, their effects in practice cannot yet be the subject of

representations like those concerning the impact of Basel 2 on trade finance. However, like

the rest of the package, the new liquidity standards will eventually be assessed regarding their

impact on the financing of different kinds of economic activity including international trade.

The Basel Committee’s International Framework for Liquidity Risk Measurement,

Standards and Monitoring (BCBS, 2009) defines quantitative measures intended toaid

supervisors “to assess the resilience of banks’ liquidity cushions and constrain

any weakening in liquidity maturity profiles, diversity of funding sources, and stress

testing practices”. These measures are the Liquidity Coverage Ratio and the Net

Stable Funding Ratio.

The Liquidity Coverage Ratio is designed to identify the amount of unencumbered high-

quality liquid assets available to offset the net cash outflows which the bank would encounter

during short-term stress scenarios specified by its supervisors.

8/8/2019 Cbm Report Sonu Kumar

http://slidepdf.com/reader/full/cbm-report-sonu-kumar 28/56

Under the standard the ratio of high quality assets to net cash outflows over a 30- day period

should be at least 100 per cent. Cumulative cash outflows are calculated by multiplying

outstanding balances of different categories of liability by percentages reflecting the expected

run-off over a 30-day horizon, and by multiplying off balance-sheet commitments and other

contingent liabilities by factors reflecting expected rates of draw-down the contingent

liabilities include guarantees, letters of credit and other trade finance instruments. The draw-

down factors for such contingent liabilities are to be determined national supervisors.

The Net Stable Funding Ratio is designed to measure the amount of longer-term, stable

sources of funding in relation to the liquidity profiles of the assets funded and the potential

for liquidity calls due to contingent off-balance-sheet obligations over a one-year time

horizon under conditions of extended stress. Under the standard the ratio of available stable

funding to required stable funding should be at least 100 per cent.

A bank’s available stable funding includes its capital, preferred stock with a maturity of at

least one year, other liabilities with effective maturities of at least one year, and the portion of

other shorter-term deposits which would be expected to stay with the institution during

extended stress scenarios. Each category of stable funding is multiplied by a factor reflecting

its degree of stability, equity capital, for example, being multiplied by 100 per cent and

unsecured wholesale funding by 50 percent. Required stable funding (RSF) is measured on

the basis of supervisory assumptions, reflected in RSF factors, concerning the liquidity risk of

the bank’s assets, off balance-sheet exposures and certain other commitments including

guarantees, letters of credit and other trade finance instruments. The RSF factors assigned to

different categories of asset approximate the amount of the asset which could not be

monetised through sale or use as collateral in a secured borrowing during a period of liquidity

stress lasting a year. Off-balance-sheet exposures and other contingent liabilities generally

require little immediate funding but can lead to significant drains of liquidity during periods

of stress. The requirement of an RSF factor for such exposures would involve the

establishment of an allocated reserve. For the contingent liabilities due to trade finance the

RSF factors are to be left to national supervisory discretion.

8/8/2019 Cbm Report Sonu Kumar

http://slidepdf.com/reader/full/cbm-report-sonu-kumar 29/56

Management of banks’ balance sheets in accordance with the new standards for liquidity risk

will involve estimates of expected net cash outflows and of required amounts of stable

funding due to contingent liabilities linked to trade finance. The impact on trade finance will

depend on the changes from existing practices which follow from eventual introduction of the

Liquidity Coverage Ration and the Net Stable Funding Ratio. The details of the proposed

changes are currently left by the Basel Committee to national supervisory discretion. This has

the advantage of providing for flexibility which can take into account variations in national

circumstances and in policy objectives.

BASEL II LIQUIDITY RISK

Basel II Compliance - From The Bank for International Settlements (BIS)

The Working Group on Liquidity serves as a forum for information exchange on national

approaches to liquidity risk regulation and supervision. It is currently conducting a

fundamental review of the 2000 document Sound Practices for Managing Liquidity in

Banking Organisations, the global standards for liquidity risk management and supervision.

The Working Group is also examining the scope for additional steps to promote more robust

and internationally consistent liquidity approaches for cross-border banks. Liquidity is the

ability of a bank to fund increases in assets and meet obligations as they come due, without

incurring unacceptable losses. The fundamental role of banks in the maturity transformation

of short-term deposits into long-term loans makes banks inherently vulnerable to liquidity

risk, both of an institution-specific nature and that which affects markets as a whole.

Virtually every financial transaction or commitment has implications for a bank’s liquidity.

Effective liquidity risk management helps ensure a bank's ability to meet cash flow

obligations, which are uncertain as they are affected by external events and other agents'

behaviour.

Liquidit risk management is of paramount importance because a liquidity shortfall at a single

institution can have system-wide repercussions. Financial market developments in the past

decade have increased the complexity of liquidity risk and its management.

8/8/2019 Cbm Report Sonu Kumar

http://slidepdf.com/reader/full/cbm-report-sonu-kumar 30/56

The market turmoil that began in mid-2007 re-emphasised the importance of liquidity to the

functioning of financial markets and the banking sector. In advance of the turmoil, asset

markets were buoyant and funding was readily available at low cost. The reversal in market

conditions illustrated how quickly liquidity can evaporate and that illiquidity can last for an

extended period of time.

The banking system came under severe stress, which necessitated central bank action to

support both the functioning of money markets and, in a few cases, individual institutions.

In February 2008 the Basel Committee on Banking Supervision published Liquidity Risk

Management and Supervisory Challenges. The difficulties outlined in that paper highlighted

that many banks had failed to take account of a number of basic principles of liquidity risk

management when liquidity was plentiful.

Many of the most exposed banks did not have an adequate framework that satisfactorily

accounted for the liquidity risks posed by individual products and business lines, and

therefore incentives at the business level were misaligned with the overall risk tolerance of

the bank.

Many banks had not considered the amount of liquidity they might need to satisfy contingent

obligations, either contractual or non-contractual, as they viewed funding of these obligations

to be highly unlikely.

Many firms viewed severe and prolonged liquidity disruptions as implausible and did not

conduct stress tests that factored in the possibility of market wide strain or the severity or

duration of the disruptions. Contingency funding plans (CFPs) were not always appropriately

linked to stress test results and sometimes failed to take account of the potential closure of

some funding sources.

In order to account for financial market developments as well as lessons learned from the

turmoil, the Basel Committee has conducted a fundamental review of its 2000 Sound

Practices for Managing Liquidity in Banking Organisations.

8/8/2019 Cbm Report Sonu Kumar

http://slidepdf.com/reader/full/cbm-report-sonu-kumar 31/56

Guidance has been significantly expanded in a number of key areas. In particular, more

detailed guidance is provided on:-

• The importance of establishing a liquidity risk tolerance;

• The maintenance of an adequate level of liquidity, including through a

cushion of liquid assets;

• The necessity of allocating liquidity costs, benefits and risks to all significant

business activities;

• The identification and measurement of the full range of liquidity risks,

including contingent liquidity risks;

• The design and use of severe stress test scenarios;

• The need for a robust and operational contingency funding plan;

• The management of intraday liquidity risk and collateral; and

• Public disclosure in promoting market discipline.

Guidance for supervisors also has been augmented substantially. The guidance emphasises

the importance of supervisors assessing the adequacy of a bank’s liquidity risk management

framework and its level of liquidity, and suggests steps that supervisors should take if these

are deemed inadequate.

The principles also stress the importance of effective cooperation between supervisors and

other key stakeholders, such as central banks, especially in times of stress. This guidance

focuses on liquidity risk management at medium and large complex banks, but the sound

principles have broad applicability to all types of banks.

The implementation of the sound principles by both banks and supervisors should be tailored

to the size, nature of business and complexity of a bank’s activities. A bank and its

supervisors also should consider the bank’s role in the financial sectors of the jurisdictions in

which it operates and the bank’s systemic importance in those financial sectors.

8/8/2019 Cbm Report Sonu Kumar

http://slidepdf.com/reader/full/cbm-report-sonu-kumar 32/56

The Basel Committee fully expects banks and national supervisors to implement the revised

principles promptly and thoroughly. This guidance is arranged around seventeen principles

for managing and supervising liquidity risk. These principles are as follows: -

Principles for the management and supervision of liquidity risk

Fundamental principle for the management and supervision of liquidity risk

Principle 1: A bank is responsible for the sound management of liquidity risk. A bank should

establish a robust liquidity risk management framework that ensures it maintains sufficient

liquidity, including a cushion of unencumbered, high quality liquid assets, to withstand a

range of stress events, including those involving the loss or impairment of both unsecured

and secured funding sources.

Supervisors should assess the adequacy of both a bank's liquidity risk management

framework and its liquidity position and should take prompt action if a bank is deficient in

either area in order to protect depositors and to limit potential damage to the financial system.

GOVERNANCE OF LIQUIDITY RISK MANAGEMENT

Principle: A bank should clearly articulate a liquidity risk tolerance that is appropriate for its

business strategy and its role in the financial system.

Principle: Senior management should develop a strategy, policies and practices to manage

liquidity risk in accordance with the risk tolerance and to ensure that the bank maintains

sufficient liquidity. Senior management should continuously review information on the

bank’s liquidity developments and report to the board of directors on a regular basis.

A bank’s board of directors should review and approve the strategy, policies and practices

related to the management of liquidity at least annually and ensure that senior management

manages liquidity risk effectively.

8/8/2019 Cbm Report Sonu Kumar

http://slidepdf.com/reader/full/cbm-report-sonu-kumar 33/56

Principle: A bank should incorporate liquidity costs, benefits and risks in the product

pricing, performance measurement and new product approval process for all significant

business activities (both on- and off-balance sheet), thereby aligning the risk-taking

incentives of individual business lines with the liquidity risk exposures their activities create

for the bank as a whole.

Measurement and management of liquidity risk

Principle: A bank should have a sound process for identifying, measuring, monitoring and

controlling liquidity risk. This process should include a robust framework for

comprehensively projecting cash flows arising from assets, liabilities and off-balance sheet

items over an appropriate set of time horizons.

Principle: A bank should actively manage liquidity risk exposures and funding needs within

and across legal entities, business lines and currencies, taking into account legal, regulatory

and operational limitations to the transferability of liquidity.

Principle: A bank should establish a funding strategy that provides effective diversification

in the sources and tenor of funding. It should maintain an ongoing presence in its chosen

funding markets and strong relationships with funds providers to promote effective

diversification of funding sources.

A bank should regularly gauge its capacity to raise funds quickly from each source. It should

identify the main factors that affect its ability to raise funds and monitor those factors closely

to ensure that estimates of fund raising capacity remain valid.

Principle: A bank should actively manage its intraday liquidity positions and risks to meet

payment and settlement obligations on a timely basis under both normal and stressed

conditions and thus contribute to the smooth functioning of payment and settlement systems.

Principle: A bank should actively manage its collateral positions, differentiating between

encumbered and unencumbered assets. A bank should monitor the legal entity and physical

location where collateral is held and how it may be mobilised in a timely manner.

8/8/2019 Cbm Report Sonu Kumar

http://slidepdf.com/reader/full/cbm-report-sonu-kumar 34/56

Principle: A bank should conduct stress tests on a regular basis for a variety of institution-

specific and market-wide stress scenarios (individually and in combination) to identify

sources of potential liquidity strain and to ensure that current exposures remain in accordance

with a bank’s established liquidity risk tolerance. A bank should use stress test outcomes to

adjust its liquidity risk management strategies, policies, and positions and to develop

effective contingency plans.

Principle: A bank should have a formal contingency funding plan (CFP) that clearly sets out

the strategies for addressing liquidity shortfalls in emergency situations.

A CFP should outline policies to manage a range of stress environments, establish clear lines

of responsibility, include clear invocation and escalation procedures and be regularly testedand updated to ensure that it is operationally robust.

Principle: A bank should maintain a cushion of unencumbered, high quality liquid assets to

be held as insurance against a range of liquidity stress scenarios, including those that involve

the loss or impairment of unsecured and typically available secured funding sources.

There should be no legal, regulatory or operational impediment to using these assets to obtain

funding.

Public disclosure

Principle: A bank should publicly disclose information on a regular basis that enables market

participants to make an informed judgement about the soundness of its liquidity risk

management framework and liquidity position.

The role of supervisors

Principle: Supervisors should regularly perform a comprehensive assessment of a bank’s

overall liquidity risk management framework and liquidity position to determine whether

they deliver an adequate level of resilience to liquidity stress given the bank’s role in the

financial system.

8/8/2019 Cbm Report Sonu Kumar

http://slidepdf.com/reader/full/cbm-report-sonu-kumar 35/56

Principle: Supervisors should supplement their regular assessments of a bank’s liquidity risk

management framework and liquidity position by monitoring a combination of internal

reports, prudential reports and market information.

Principle: Supervisors should intervene to require effective and timely remedial action by a

bank to address deficiencies in its liquidity risk management processes or liquidity position.

Principle: Supervisors should communicate with other supervisors and public authorities,

such as central banks, both within and across national borders, to facilitate effective

cooperation regarding the supervision and oversight of liquidity risk management.

8/8/2019 Cbm Report Sonu Kumar

http://slidepdf.com/reader/full/cbm-report-sonu-kumar 36/56

The CAMELS FRAMEWORK

This rating system is used by the three federal banking supervisors (the Federal Reserve, the

FDIC, and the OCC) and other financial supervisory agencies to provide a convenient

summary of bank conditions at the time of an exam

The acronym "CAMEL" refers to the five components of a bank's condition that are assessed:

C apital adequacy, Asset quality, M anagement, E arnings, and Liquidity. A sixth component, a

bank's S ensitivity to market risk , was added in 1997; hence the acronym was changed to

CAMELS. (Note that the bulk of the academic literature is based on pre-1997 data and is thus

based on CAMEL ratings.) Ratings are assigned for each component in addition to the overall

rating of a bank's financial condition. The ratings are assigned on a scale from 1 to 5. Banks

with ratings of 1 or 2 are considered to present few, if any, supervisory concerns, while banks

with ratings of 3, 4, or 5 present moderate to extreme degrees of supervisory concern.

In 1994, the RBI established the Board of Financial Supervision (BFS), which operates as a

unit of the RBI. The entire supervisory mechanism was realigned to suit the changing needs

of a strong and stable financial system. The supervisory jurisdiction of the BFS was slowly

extended to the entire financial system barring the capital market institutions and the

insurance sector. Its mandate is to strengthen supervision of the financial system by

integrating oversight of the activities of financial services firms. The BFS has also established

a sub-committee to routinely examine auditing practices, quality, and coverage.

In addition to the normal on-site inspections, Reserve Bank of India also conducts off-site

surveillance which particularly focuses on the risk profile of the supervised entity. The Off-

site Monitoring and Surveillance System (OSMOS) was introduced in 1995 as an additional

tool for supervision of commercial banks. It was introduced with the aim to supplement the

on-site inspections. Under off-site system, 12 returns (called DSB returns) are called from the

financial institutions, wich focus on supervisory concerns such as capital adequacy, asset

quality, large credits and concentrations, connected lending, earnings and risk exposures (viz.

currency, liquidity and interest rate risks).

8/8/2019 Cbm Report Sonu Kumar

http://slidepdf.com/reader/full/cbm-report-sonu-kumar 37/56

In 1995, RBI had set up a working group under the chairmanship of Shri S. Padmanabhan to

review the banking supervision system. The Committee certain recommendations and based

on such suggetions a rating system for domestic and foreign banks based on the international

CAMELS model combining financial management and systems and control elements was

introduced for the inspection cycle commencing from July 1998. It recommended that the

banks should be rated on a five point scale (A to E) based on the lines of international

CAMELS rating model.

All exam materials are highly confidential, including the CAMELS. A bank's CAMELS

rating is directly known only by the bank's senior management and the appropriate

supervisory staff. CAMELS ratings are never released by supervisory agencies, even on a

lagged basis. While exam results are confidential, the public may infer such supervisory

information on bank conditions based on subsequent bank actions or specific disclosures.

Overall, the private supervisory information gathered during a bank exam is not disclosed to

the public by supervisors, although studies show that it does filter into the financial markets.

A Capital Adquecy Ratio is a measure of a bank's capital. It is expressed as a percentage

of a bank's risk weighted credit exposures.

(A) Also known as ""Capital to Risk Weighted Assets Ratio (CRAR).

Capital adequacy is measured by the ratio of capital to risk-weighted assets (CRAR). A

sound capital base strengthens confidence of depositors.

(B) This ratio is used to protect depositors and promote the stability and efficiency of

financial systems around the world.

(C) Capital adequacy ultimately determines how well financial institutions can cope with

shocks to their balance sheets. Thus, it is useful to track capital-adequacy ratios that take

into account the most important financial risks—foreign exchange, credit, and interest

rate risks—by assigning risk weightings to the institution’s assets.

Asset Quality Asset quality determines the robustness of financial institutions against loss of

value in the assets. The deteriorating value of assets, being prime source of banking

problems, directly pour into other areas, as losses are eventually written-off against capital,

which ultimately NPA: Non-Performing Assets

8/8/2019 Cbm Report Sonu Kumar

http://slidepdf.com/reader/full/cbm-report-sonu-kumar 38/56

Advances are classified into performing and non-performing advances (NPAs) as per RBI

guidelines. NPAs are further classified into sub-standard, doubtful and loss assets based on

the criteria stipulated by RBI. An asset, including a leased asset, becomes non-performing

when it ceases to generate income for the Bank.

An NPA is a loan or an advance where:

1. Interest and/or installment of principal remains overdue for a period of more than 90

days in respect of a term loan;

2. The account remains "out-of-order'' in respect of an Overdraft or Cash Credit (OD/CC);

3. The bill remains overdue for a period of more than 90 days in case of bills purchased

and discounted;

4. A loan granted for short duration crops will be treated as an NPA if the installments of

principal or interest thereon remain overdue for two crop seasons; and

5. A loan granted for long duration crops will be treated as an NPA if the installments of

principal or interest thereon remain overdue for one crop season.

Jeopardizes the earning capacity of the institution.

B) Management Soundness

Management of financial institution is generally evaluated in terms of capital adequacy, asset

quality, earnings and profitability, liquidity and risk sensitivity ratings. In addition,

performance evaluation includes compliance with set norms, ability to plan and react to

changing circumstances, technical competence, leadership and administrative ability. In

effect, management rating is just an amalgam of performance in the above-mentioned areas.

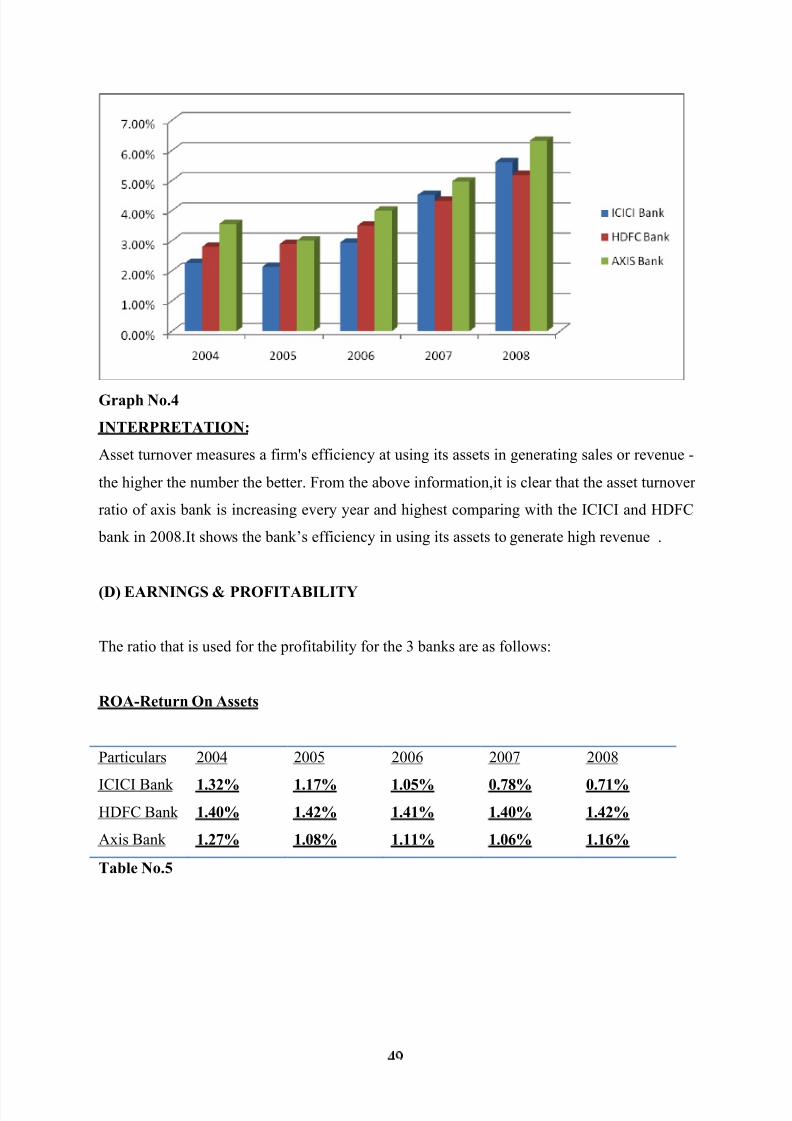

Efficiency Ratios demonstrate how efficiently the company uses its assets and how

efficiently the company manages its operations.

8/8/2019 Cbm Report Sonu Kumar

http://slidepdf.com/reader/full/cbm-report-sonu-kumar 39/56

C) Earnings & Profitability

Earnings and profitability, the prime source of increase in capital base, is examined with

regards to interest rate policies and adequacy of provisioning. In addition, it also helps to

support present and future operations of the institutions. The single best indicator used to

gauge earning is the Return on Assets (ROA), which is net income after taxes to total asset

ratio.

ROA tells what earnings were generated from invested capital (assets). ROA for public

companies can vary substantially and will be highly dependent on the industry. This is why

when using ROA as a comparative measure, it is best to compare it against a

company's previous ROA numbers or the ROA of a similar company.

D)Liquidity

An adequate liquidity position refers to a situation, where institution can obtain sufficient

funds, either by increasing liabilities or by converting its assets quickly at a reasonable cost.

It is, therefore, generally assessed in terms of overall assets and liability management, as

mismatching gives rise to liquidity risk. Efficient fund management refers to a situation

where a spread between rate sensitive assets (RSA) and rate sensitive liabilities (RSL) is

maintained. The most commonly used tool to evaluate interest rate exposure is the Gap

between RSA and RSL, while liquidity is gauged by liquid to total asset ratio.

Initially solvent financial institutions may be driven toward closure by poor management of

short-term liquidity. Indicators should cover funding sources and capture large maturity

mismatches.

The term liquidity is used in various ways, all relating to availability of, access to, or

convertibility into cash.

An institution is said to have liquidity if it can easily meet its needs for cash either because it

has cash on hand or can otherwise raise or borrow cash.

A market is said to be liquid if the instruments it trades can easily be bought or sold in

quantity with little impact on market prices.

An asset is said to be liquid if the market for that asset is liquid.

8/8/2019 Cbm Report Sonu Kumar

http://slidepdf.com/reader/full/cbm-report-sonu-kumar 40/56

The common theme in all three contexts is cash. A corporation is liquid if it has ready access

to cash. A market is liquid if participants can easily convert positions into cash—or

conversely. An asset is liquid if it can easily be converted to cash.

The liquidity of an institution depends on:

The institution's short-term need for cash;

Cash on hand;

Available lines of credit;

The liquidity of the institution's assets;

The institution's reputation in the marketplace—how willing will counterparty is to transact

trades with or lend to the institution?

The liquidity of a market is often measured as the size of its bid-ask spread, but this is an

imperfect metric at best. More generally, Kyle (1985) identifies three components of market

liquidity:

Tightness is the bid-ask spread;

Depth is the volume of transactions necessary to move prices;

Resiliency is the speed with which prices return to equilibrium following a large trade.

Examples of assets that tend to be liquid include foreign exchange; stocks traded in the Stock

Exchange or recently issued Treasury bonds. Assets that are often illiquid include limited

partnerships, thinly traded bonds or real estate.

Cash maintained by the banks and balances with central bank, to total asset ratio (LQD) is an

indicator of bank's liquidity. In general, banks with a larger volume of liquid assets are

perceived safe, since these assets would allow banks to meet unexpected withdrawals.

Liquidity risk is financial risk due to uncertain liquidity. An institution might lose liquidity if

its credit rating falls, it experiences sudden unexpected cash outflows, or some other event

causes counterparties to avoid trading with or lending to the institution. A firm is also

exposed to liquidity risk if markets on which it depends are subject to loss of

liquidity.

8/8/2019 Cbm Report Sonu Kumar

http://slidepdf.com/reader/full/cbm-report-sonu-kumar 41/56

Liquidity risk tends to compound other risks. If a trading organization has a position in an

illiquid asset, its limited ability to liquidate that position at short notice will compound its

market risk. Suppose a firm has offsetting cash flows with two different counterparties on a

given day. If the counterparty that owes it a payment defaults, the firm will have to raise cash

from other sources to make its payment. Should it be unable to do so, it too we default. Here,

liquidity risk is compounding credit risk.

Accordingly, liquidity risk has to be managed in addition to market, credit and other risks.

Because of its tendency to compound other risks, it is difficult or impossible to isolate

liquidity risk. In all but the most simple of circumstances, comprehensive metrics of liquidity

risk don't exist. Certain techniques of asset-liability management can be applied to assessing

liquidity risk. If an organization's cash flows are largely contingent, liquidity risk may be

assessed using some form of scenario analysis. Construct multiple scenarios for market

movements and defaults over a given period of time. Assess day-to-day cash flows under

each scenario. Because balance sheets differed so significantly from one organization to the

next, there is little standardization in how such analyses are implemented.

Regulators are primarily concerned about systemic implications of liquidity risk.

Business activities entail a variety of risks. For convenience, we distinguish between different

categories of risk: market risk, credit risk, liquidity risk, etc. Although such categorization is

convenient, it is only informal. Usage and definitions vary. Boundaries between categories

are blurred. A loss due to widening credit spreads may reasonably be called a market loss or a

credit loss, so market risk and credit risk overlap. Liquidity risk compounds other risks, such

as market risk and credit risk. It cannot be divorced from the risks it compounds.

An important but somewhat ambiguous distinguish is that between market risk and business

risk. Market risk is exposure to the uncertain market value of a portfolio. Business risk is

exposure to uncertainty in economic value that cannot be marked-to-market. The distinction

between market risk and business risk parallels the distinction between market-value

accounting and book-value accounting.

The distinction between market risk and business risk is ambiguous because there is a vast

"gray zone" between the two. There are many instruments for which markets exist, but the

markets are illiquid. Mark-to-market values are not usually available, but mark-to-model

8/8/2019 Cbm Report Sonu Kumar

http://slidepdf.com/reader/full/cbm-report-sonu-kumar 42/56

values provide a more-or-less accurate reflection of fair value. Do these instruments pose

business risk or market risk? The decision is important because firms employ fundamentally

different techniques for managing the two risks.

Business risk is managed with a long-term focus. Techniques include the careful

development of business plans and appropriate management oversight. book-value

accounting is generally used, so the issue of day-to-day performance is not material. The

focus is on achieving a good return on investment over an extended horizon.

Market risk is managed with a short-term focus. Long-term losses are avoided by avoiding

losses from one day to the next. On a tactical level, traders and portfolio managers employ a

variety of risk metrics —duration and convexity, the Greeks, beta, etc.—to assess their

exposures. These allow them to identify and reduce any exposures they might consider

excessive. On a more strategic level, organizations manage market risk by applying risk

limits to traders' or portfolio managers' activities. Increasingly, value-at-risk is being used to

define and monitor these limits. Some organizations also apply stress testing to their

portfolios.

8/8/2019 Cbm Report Sonu Kumar

http://slidepdf.com/reader/full/cbm-report-sonu-kumar 43/56

RESERCH METHODOLOGY

DESIGN OF THE STUDY

STATEMENT OF THE PROBLEM

In the recent years the financial system especially the banks have undergone numerous

changes in the form of reforms, regulations & norms. CAMELS framework for the

performance evaluation of banks is an addition to this. The study is conducted to analyze the

pros & cons of this model.

OBJECTIVES OF STUDY

To do an in-depth analysis of the model .

To analyze 3 banks to get the desired results by using CAMELS as a tool of measuring

performance.

RESEARCH PROPOSAL

The Bank after the implementation of the balanced scorecard in 2002 has under gone a

drastic change. Both its peoples and process perspectives have changed visibly and the

employees have full faith in the new strategy to produce quick results and keep them ahead in

the industry. The balanced scorecard approach has brought about more role clarity in the job

profile and has improved processes. In short it focuses not only on short term goals but is

very clear about its way to achieve the long term goal.

SCOPE OF THE RESEARCH

“To study the strength of using CAMELS framework as a tool of performance evaluation for

banking institutions.”

1. Type of research: Descriptive

8/8/2019 Cbm Report Sonu Kumar

http://slidepdf.com/reader/full/cbm-report-sonu-kumar 44/56

METHODOLOGY

i) AREA OF SURVEY:

The survey was done for banks. The study environment was the Banking industry.

ii) DATA SOURCE:

Primary Data: Primary data was collected from the company balance sheets and company

profit and loss statements.

Secondary Data: Secondary data on the subject was collected from ICFAI journals, company

prospectus, company annual reports and IMF websites.

iii) SAMPLING TECHNIQUE :

Convenience sampling: Convenience sampling was done for the selection of the banks.

iv) PLAN OF ANALYSIS:

The data analysis of the information got from the balance sheets was done and ratios were

used. Graph and charts were used to illustrate trends.

8/8/2019 Cbm Report Sonu Kumar

http://slidepdf.com/reader/full/cbm-report-sonu-kumar 45/56

ANALYSIS AND INTERPRETATION

Now each parameter will be taken separately & discussed in detail.

(A) CAPITAL ADEQUACY:

Capital adequacy ratio is defined as

where Risk can either be weighted assets ( ) or the respective national regulator's minimum

total capital requirement. If using risk weighted assets,

≥ 8%.

The percent threshold (8% in this case, a common requirement for regulators conforming to

the Basel Accords) is set by the national banking regulator.

Two types of capital are measured: tier one capital, which can absorb losses without a bank

being required to cease trading, and tier two capital, which can absorb losses in the event of a

winding-up and so provides a lesser degree of protection to depositors.

THE CAPITAL ADEQUACY RATIO FOR 3 MAJOR BANKS IN INDIA

Particulars 2004 2005 2006 2007 2008

ICICI Bank 10.36% 11.78% 13.35% 11.69% 13.97%HDFC Bank 11.66% 12.16% 11.40% 13.08% 13.73%

AXIS Bank 11.21% 12.66% 11.08% 11.57% 13.99%

Table No.1

8/8/2019 Cbm Report Sonu Kumar