But … What About Tomorrow? Presentation to September 8 Leadership Summit Tom Stinson Tom Gillaspy...

30

But … What About Tomorrow? Presentation to September 8 Leadership Summit Tom Stinson Tom Gillaspy September, 2009

-

Upload

herbert-blake -

Category

Documents

-

view

216 -

download

0

Transcript of But … What About Tomorrow? Presentation to September 8 Leadership Summit Tom Stinson Tom Gillaspy...

But … What About Tomorrow?

Presentation toSeptember 8 Leadership Summit

Tom StinsonTom GillaspySeptember, 2009

Minnesota Has Been Very Successful

(Especially For A Cold Weather State at the End of the Road)

• Our economic growth rate has exceeded the national average

• Our population growth rate leads the frost belt

• We rank with the leaders on many social and economic indicators

• Education has been a key contributor to the state’s success

Past PerformanceDoes Not EnsureFuture Results

Minnesota Is Facing Significant Long-Term Budget Problems

This Recession Is Much More Severe Than Those of 1990-91 and 2001

Minnesota’s Recovery Will Be Slower than After Recent Downturns

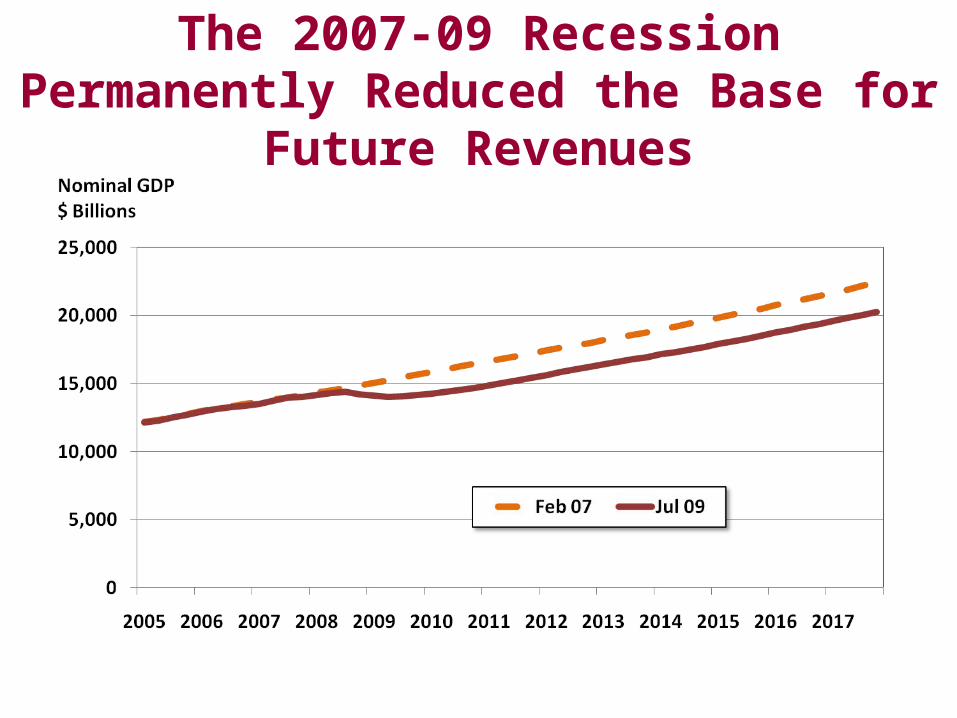

The 2007-09 Recession Permanently Reduced the Base for Future Revenues

The Economic/Demographic Environment Has Changed for as

Far as We Can Forecast

Short run economic cycle has merged with long run demographic cycle

We have entered the Age of Entitlement—economic growth in the next 25 years will be about half what it was in the past 25.

State revenue growth will slow while spending pressures will accelerate

This is a national/global issue

Minnesota Saw a 30 Percent Jump in Workers Turning Age 62 in 2008

0

10,000

20,000

30,000

40,000

50,000

60,000

7/05 to7/06

7/06 to7/07

7/07 to7/08

7/08 to7/09

7/09 to7/10

7/10 to7/11

7/11 to7/12

Year Turning Age 62

Wo

rke

d W

ith

in P

as

t 5

ye

ars

2005 ACS

Budget Pressures Will Change More 65+ Than School Age by 2020

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1950 1960 1970 1980 1990 2000 2010 2020 2030

18-24

65+

5-17

Census counts & State Demographer projection, revised 2007

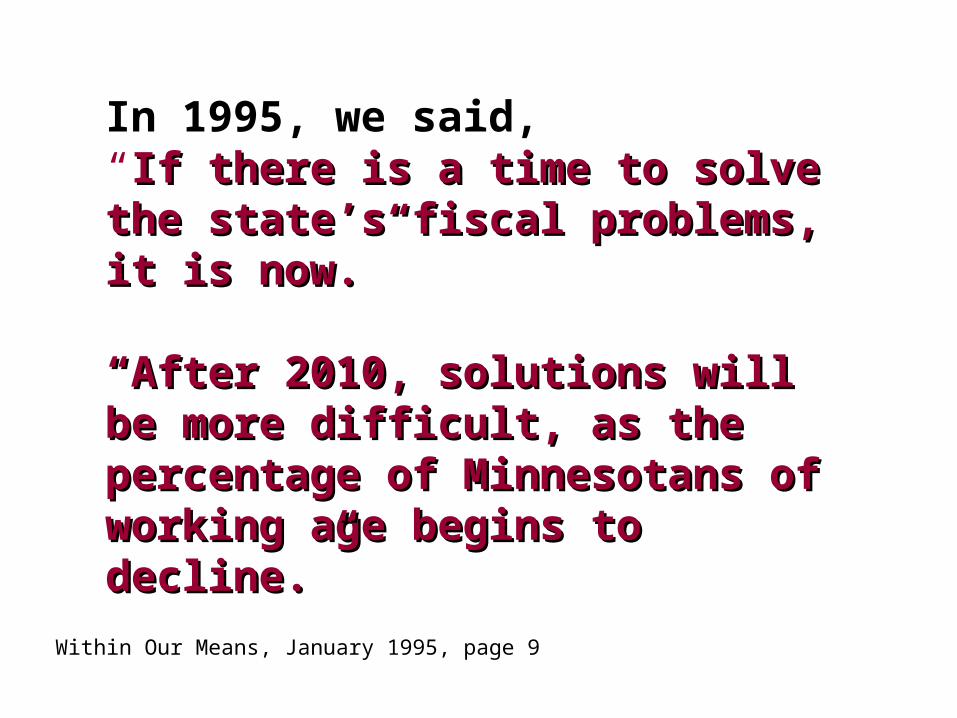

In 1995, we said,“If there is a time to solve the state’s If there is a time to solve the state’s fiscal problems, it is now.”fiscal problems, it is now.”

““After 2010, solutions will be more After 2010, solutions will be more difficult, as the percentage of difficult, as the percentage of Minnesotans of working age begins Minnesotans of working age begins to decline.”to decline.”

Within Our Means, January 1995, page 9

Labor Force Growth Is About To Slow Sharply

1.52%

1.12%

0.75%

0.43%

0.10% 0.13%

0.27%

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

1.2%

1.4%

1.6%

1990-2000

2005-10 2010-15 2015-20 2020-25 2025-30 2030-35

Ave

An

nu

al C

han

ge

Minnesota Faces a Fiscal Trap1. The issue is a long run, structural one—

short run solutions will not solve the problem

2. Trend growth alone will not be sufficient. Fundamental changes are necessary

3. Revenue growth will slow. Efforts to increase it will be met with resistance

4. Spending pressures will increase driven largely by issues of aging and health

5. State spending will shift its focus from education, infrastructure and higher education to care and support of the aging

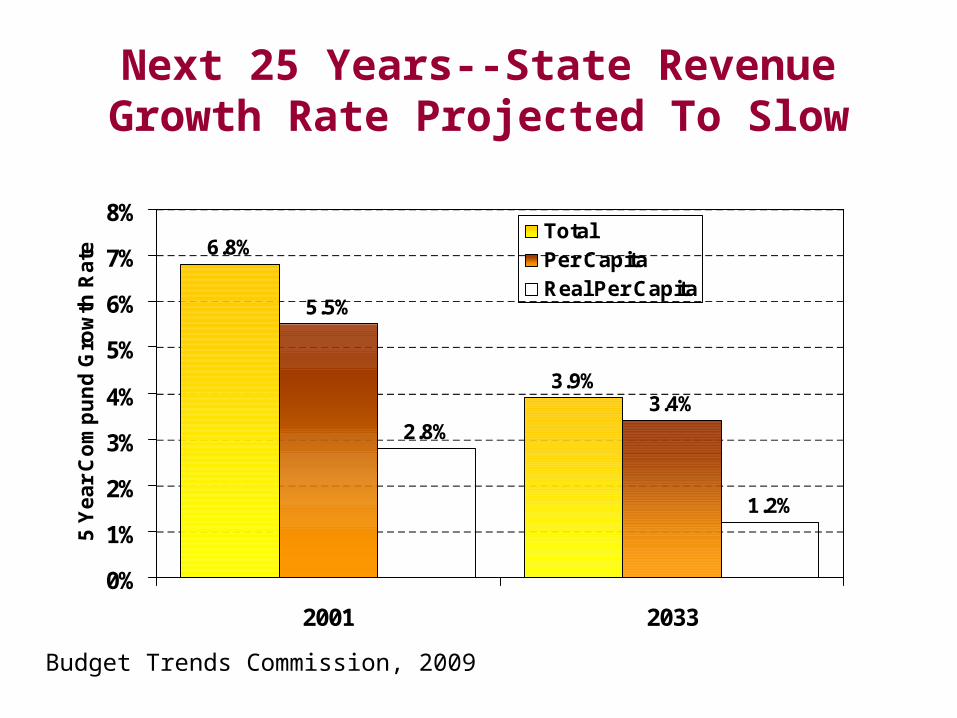

Revenue Growth Will Slow5 Year Compound Growth Rates

for Total State Revenues

Next 25 Years--State Revenue Growth Rate Projected To Slow

6.8%

3.9%

5.5%

3.4%2.8%

1.2%

0%

1%

2%

3%

4%

5%

6%

7%

8%

2001 2033

5 Y

ea

r C

om

pu

nd

Gro

wth

Ra

te

TotalPer CapitaReal Per Capita

Budget Trends Commission, 2009

From 2010 to 2020, Minnesota Will

See Large Increases Age 50s and 60s

20,15036,190

47,3305,050

-30,680-9,980

47,95061,920

-2,680-63,650

-42,31054,240

102,960112,540

91,37041,400

8,44016,500

0-45-9

10-1415-1920-2425-2930-3435-3940-4445-4950-5455-5960-6465-6970-7475-7980-84

85+

Source: Minnesota State Demographic Center, rev 2007Numbers are rounded

Health Care Spending Jumps After 55U.S. Health Care Spending By Age, 2004

$1,855$1,074 $1,445

$2,165$2,747

$3,496

$6,694

$9,017$9,914

$3,571

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

<55-

14

15-2

4

25-3

4

35-4

4

45-5

4

55-6

4

65-7

475

+

Avera

ge

Source: Agency for HealthCare Research and Quality, Medical Expenditure Panel Survey,data for per capita spending by age group in the Midwest. Excludes spending for long-term care institutions.

If State Health Care Costs Continue Their Current Trend, State Spending On Other Services Can’t

Grow

3.9%

8.5%

0.2%0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

Revenue Health Care Education & AllOther

An

nu

al

Av

e G

row

th 2

00

8-2

03

3

General Fund Spending Outlook, presentation to the Budget Trends Commission,August 2008, Dybdal, Reitan and Broat

The Political Economy Has Changed In Fundamental Ways

Minnesota had strong per capita economic growth since WWII

The global economic environment has changed.

The political economy is also changing

Aging means slower economic growth and rising government expenditures

Aging means more tax resistance

Phases in the Household Life Cycle

State/Local Government’s Share of Personal Income Has Declined

15.5%

16.5%15.9%

17.4%

15.4%

17.9%

10%

15%

20%

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008

Calendar Year

Price of Government

Mn Dept of Finance

How Do We Get Out Of This Fiscal Trap?

Revenue growth will depend increasingly on per capita economic growth

Future economic growth will depend increasingly on increasing productivity and less on labor force size

This plays to Minnesota’s historic strength

Productivity Remains The Key To Quality of Life In Minnesota

Economic Growth = Labor Force Growth + Productivity Growth

Productivity growth comes fromPrivate investment -- machines & processesSkills & abilities of workersPublic investment -- roads, bridges, etcTechnology from research, public & private

Productivity Is Not Just Producing at a Lower Cost

Increasing the Value of Products Produced Also Increases

Productivity

The Fiscal Catch-22

If we don’t make the necessary public investments in human capital, research and infrastructure, then we won’t have the productivity gains needed to provide the resources to make those investments.

We must avoid the California spiral

The Tale of Two EconomiesPer Capita Personal Income, 1960-2008

% of US Average

Education Is The Key To Productivity

Minnesota High School Graduation Ratio

57%

85%

60% 62%

89%85%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

AmericanIndian

Asian Hispanic Black White Total

2 Y

r A

ve R

ate

2004-05 through 2005-06 graduates. Based on 10th grade enrollment three years earlier.

Tough Decisions Must Be Made

• What is state government well positioned to do?

Some issues are national in scope

Some are local

Some are inherently private

• What activities are central to state government’s role?

Big Opportunities

• The challenge--building the foundation for future successEconomic prosperity

Environmental quality

Social justice

Quality of life

• The current situation is not sustainable

“If something can't go on forever, it will stop.”

Herbert Stein, chair President Nixon’sCouncil of Economic Advisors