Business Analysis - Texas Tech University

64

1 Valuation Date: April 1 st , 2005 Chris Coffey [email protected] Keith Fraser [email protected] Heather Lee [email protected] Whitney Kelsay [email protected] Carrie Redgrave [email protected]

Transcript of Business Analysis - Texas Tech University

1

Valuation Date: April 1st, 2005

Chris Coffey [email protected]

Keith Fraser [email protected]

Heather Lee [email protected]

Whitney Kelsay [email protected]

Carrie Redgrave [email protected]

2

CVS Valuation

Table of Contents Executive Summary…………………… 3 Business & Industry Analysis………… 7 Five Forces Model………………………. …… 8 Competitive Advantage……………….. ……. 12 Key Success Factors………………………….. 15 Accounting Analysis…………………. 18 Quantitative Measures & Indicators……….. 18 Structure of the Formal Accounting Analysis…………………………… 19 Ratio Analysis & Forecast Financials. 27 Financial Ratio Analysis…………………….. 27 Cross-Sectional (Benchmark) Analysis…….. 29 Financial Statement Forecast

Methodology…………………………...... 39

Valuations Analysis………………….. 43 Discounted Dividends Method……………… 46 Discounted Free Cash Flows Method………. 46 Discounted Residual Income Method………. 47 Abnormal Earnings Growth Method….…… 49 Long-Run Average Residual Income

Perpetuity Method…………………….... 49 Appendix…………………………........ 52 Sources………………………………... 64

3

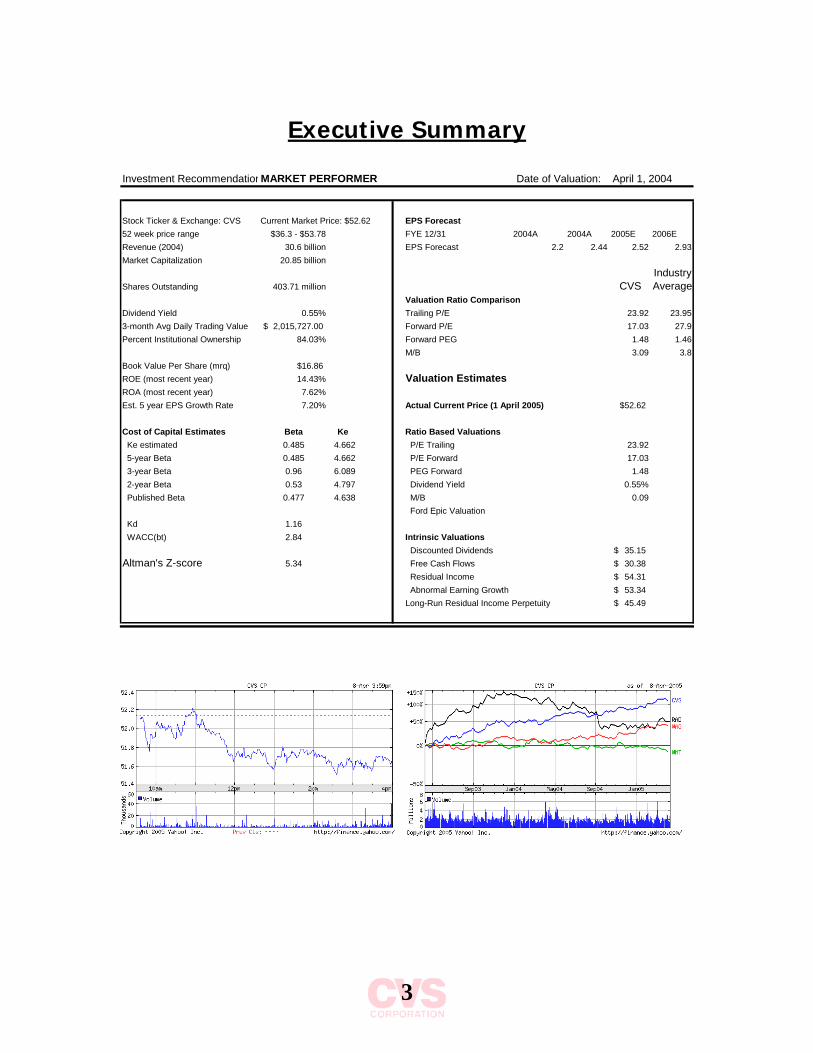

Executive Summary

Investment RecommendationMARKET PERFORMER Date of Valuation: April 1, 2004

Stock Ticker & Exchange: CVS Current Market Price: $52.62 EPS Forecast52 week price range $36.3 - $53.78 FYE 12/31 2004A 2004A 2005E 2006ERevenue (2004) 30.6 billion EPS Forecast 2.2 2.44 2.52 2.93Market Capitalization 20.85 billion

IndustryShares Outstanding 403.71 million CVS Average

Valuation Ratio ComparisonDividend Yield 0.55% Trailing P/E 23.92 23.953-month Avg Daily Trading Value 2,015,727.00$ Forward P/E 17.03 27.9Percent Institutional Ownership 84.03% Forward PEG 1.48 1.46

M/B 3.09 3.8Book Value Per Share (mrq) $16.86ROE (most recent year) 14.43% Valuation EstimatesROA (most recent year) 7.62%Est. 5 year EPS Growth Rate 7.20% Actual Current Price (1 April 2005) $52.62

Cost of Capital Estimates Beta Ke Ratio Based Valuations Ke estimated 0.485 4.662 P/E Trailing 23.92 5-year Beta 0.485 4.662 P/E Forward 17.03 3-year Beta 0.96 6.089 PEG Forward 1.48 2-year Beta 0.53 4.797 Dividend Yield 0.55% Published Beta 0.477 4.638 M/B 0.09

Ford Epic Valuation Kd 1.16 WACC(bt) 2.84 Intrinsic Valuations

Discounted Dividends 35.15$ Altman's Z-score 5.34 Free Cash Flows 30.38$

Residual Income 54.31$ Abnormal Earning Growth 53.34$ Long-Run Residual Income Perpetuity 45.49$

4

Recommendation- Fairly Valued Security

We have determined that CVS has a reasonable stock price, with a buy/hold

recommendation. The recent acquisition of Eckerd Drug Stores has made it a

growing firm. The company is expected to grow at a steady pace, hence our

recommendation to buy or hold. Investors should view this as a secure long term

investment. CVS is such a solid company that 85 percent of its stock is owned by

institutional investors.

CVS is a strong company that has realized a substantial gain in sales from

existing stores, and hopes to realize more gains in the future from new Eckerd

stores. The entire industry is expecting steady growth, with no major changes in

the distribution of market share. These observations support our forecasted

growth rates and financial statements.

Current Financial Position

CVS is in the business of providing prescription drugs in a convenient way. We

have discovered that the retail drug industry is a highly concentrated and

growing industry. CVS has the second highest market cap compared to

Walgreen’s.

CVS provides mediocre quality financial reports. They meet GAAP requirements,

but much of the information needed by investors is not provided clearly. The

5

other players in the industry take a conservative approach to reporting their

financial position, while CVS takes a slightly more aggressive approach.

Forecasts of Future Financial Performance

In determining the intrinsic value of CVS, we forecast their sales growth, and in

turn, we are able to forecast their future cash flows, dividend payouts, and net

earnings. Due to the recent acquisition of Eckerd, we designate a fairly high

growth rate for the next five years and a slightly less aggressive rate for the

remaining five years in our ten year forecast.

Estimation of Equity Value

After forecasting their financials out for ten years, we used that information to

value CVS. We then ran four valuation models that presented us with information

about the value of future dividends paid, future free cash flows, abnormal

earnings, and residual income. After evaluating the merit of each valuation

model, we realized some models gave a better estimation of the true value of

CVS stock and decided to let some models weight more heavily in the final value.

Although we did not completely ignore models such as discounted dividends, we

did feel it didn’t give use a good idea of the value of the total company, but we

were happy to find that a large percent of our stock price is from dividends paid.

We believe that this supports our recommendation to buy or hold. After

considering all factors and mainly focusing on the abnormal earnings and

6

residual income models we believe that the stock price if fairly value around a

price of $54.00.

Valuation Risks

We are confident that our valuation of CVS is accurate to the best of our

knowledge. However, the sensitivity analyses show that a slight error in the

prediction of the growth rate or the cost of equity could greatly sway the intrinsic

value determined. Upon acquiring Eckerd, CVS increased its amount of goodwill

by one billion dollars. If this purchase becomes unprofitable, CVS will have to

impair the goodwill, which would cause a fluctuation in their stock price.

7

Business Analysis

Consumer Value Store, or CVS, was established in 1963 in the small town of

Lowell, Massachusetts. It began by selling health and beauty products, but

expanded to selling pharmaceutical drugs and general merchandise in 1967.

CVS strives to make a simple and friendly environment for their customers;

helping them lead happier, healthier lives. Currently CVS is among the leaders in

the retail-drug industry. Their top competitors are Walgreen’s, Rite Aid, and

Wal-Mart. CVS filled 13% of prescriptions in 2004, while Walgreen’s filled 14%

(http://www.cvs.com, 2005).

As of January 2005, CVS’s two segments of operations were Retail Pharmacy and

Pharmacy Benefit Management (PBM). The Retail Pharmacy makes up 95% of

revenue and includes all of the following: prescription and over-the-counter

drugs, photography and film, greeting cards, convenience foods, seasonal

merchandise, and beauty products. With the recent acquisition of Eckerd’s, CVS

is now the number one retail chain with 5,375 stores in 36 states, including DC

and Hawaii (http://www.cvs.com, 2005).

The PBM offers full service prescription benefits to managed care and other

organizations including assisted living centers. CVS also calls this their Specialty

Pharmacy segment or “CVS ProCare,” and it consists of 47 pharmacies in 19

states. It focuses on assisting people with expensive drug costs in dealing with

8

conditions such as, AIDS/HIV, transplants, and genetic conditions

(http://www.cvs.com, 2005).

Five Forces Model

To asses the current situation of CVS in the marketplace, we use the five forces

model. There are two main parts of this model, the first being the degree of

actual and potential competition, including rivalry among existing firms, threat of

new entrants, and threat of substitute products. The second part is the

bargaining power in input and output markets, including the bargaining power of

buyers, and bargaining power of suppliers.

Competitive Force 1: Rivalry among Existing Firms

CVS and Walgreen’s are the main competitors in the retail drug industry. They

sold 13 and 14 percent, respectively, of the nation’s prescriptions last year. Wal-

Mart and Rite Aid are also considered competitors, but Wal-Mart is not

specifically in the pharmaceutical business, and Rite Aid does not have near the

market share to be a main rival. Rivalry in the pharmaceutical industry is high.

Since CVS and Walgreen’s each hold a generous share of the market, CVS’ share

is not conceding. In fact, this industry has seen remarkable growth in the last

three to five years, allowing CVS to maintain its market share while increasing its

revenues and profit percentages (http://www.finance.yahoo.com, 2005).

9

The retail pharmaceutical industry is highly concentrated by a few major firms.

CVS, Walgreen’s and Rite Aid have market caps of $20.66 billion, $43.03 billion,

and $2.08 billion, respectively; whereas Wal-Mart has a market cap of $200.43

billion. Because of this, CVS and those alike, have to follow Wal-Mart’s pricing

and standards to be competitive. Since CVS does not specialize in groceries, like

Wal-Mart does, they can not compete in that area. However, CVS does pride

itself on being a leader in pharmaceutical drugs. Over 70% of their revenue

comes from providing prescription drugs to its customers.

The retail industry provides a low switching cost for its customers. This is evident

because a large percentage of CVS’ retail drug sales come from its generic

brands; which means that customers are not dedicated to one brand if prices of

other brands are lower. By offering superior customer service and convenience,

CVS tries to set itself apart from its competitors. However, it has no choice but to

compete on price because of the relatively low switching costs for customers.

CVS is unable to achieve an economy of scale due to the fact that it has a

large number of small local stores and is unable to compete with competitors

such as Wal-Mart, that are able to spread their fixed costs across more products

per store. The large number of small stores dramatically increases CVS’ fixed

costs.

10

The retail drug industry is highly competitive because there is a high level of exit

barriers and it is at full capacity, so the stores must compete on price. This is

evident because of CVS’s recent acquisition of Eckerd. Because there was so

much competition in the industry, CVS bought Eckerd to expand and maintain its

market share.

This will allow CVS to grow at a faster pace and enter new areas of the market.

The acquisition provided them with 1,200 additional stores that competed in

markets unfamiliar to CVS. If CVS attempted to exit the industry altogether, it

would call for a complete change of its corporate structure and re-design of its

stores. For this reason, exit barriers are high in the retail drug industry.

Competitive Force 2: The Threat of New Entrants

Entering into the retail drug industry comes at a high cost. It would require a

large initial investment in real estate property, product inventory, and human

capital. Recently, the development of new internet-based mail-order prescription

drug companies has lowered the cost of entry into the market. This progress is

still relatively new, and has yet to create a large impact to the industry.

There is not much opportunity for a first mover advantage due the fact that

it is easy for competitors to quickly establish themselves in the market and adapt

to new trends. For example, CVS quickly answered Walgreens’ move to the

southern region of the United States with its own expansion in to the South

11

through the acquisition of Eckerd.

With the proper licenses, it is relatively easy for new competitors to gain access

to the merchandise in the retail drug industry. However, these new entrants may

not be able to demand low prices as easily as existing competitors. There might

also be difficulty in ordering large quantities of merchandise due to the fact that

they are smaller than established companies such as CVS and Walgreens.

For any new company, there are some legal barriers, such as obtaining a local

business license. It is also necessary to acquire state and federal government

licenses that allow the sale of prescription drugs. The pharmacists hired must

also be qualified and licensed. Specialized employees such as these, come at a

high cost to all employers in the industry.

Competitive Force 3: Threat of Substitute Products

In this industry, CVS, Walgreen’s, and Rite Aid are facilitators of the same

products and services. They receive the same prescriptions and general

merchandise as their competitors. The threat of customers going to the

competition is high and it leaves the company vulnerable to the customers

taste and preferences. What sets them apart is their level of service and

convenience to their customers.

12

Competitive Force 4: Bargaining Power of Buyers

The retail drug industry experiences a slim profit margin on prescriptions and a

larger margin on general merchandise. This makes customers more inclined to

shop around for cheaper prices on similar products. In this industry, buyers are

willing to compare prices at CVS and its competitors’ sores to find the best price

of a prescription. Since these stores carry many of the same brands, it is just a

matter of who has the lowest price.

Competitive Force 5: Bargaining Power of Suppliers

The suppliers of retail pharmacies are drug manufacturers like Eli Lilly.

Although the retail drug industry is very price sensitive, the suppliers

of CVS and Walgreens have some bargaining power due to the

fact that their customers incur a high cost of not doing business. This means that

the bargaining power of suppliers to this industry is relatively low.

Overall, the industry is profitable and would be a good market in which to invest.

Competition has always been high, so, as long as the main competitors continue

to perform as they currently are, they will remain profitable.

Competitive Advantage

Although CVS seems to be in the business of merchandising, their focus is on

selling customer service.

13

In the retail drug industry, the cost leadership is possessed by Wal-Mart.

CVS and Walgreens are unable to beat Wal-Mart’s prices. Competitors of Wal-

Mart do not have the resources or industry dominance to supply the same

products at or below the price Wal-Mart is able to offer its customers. Other

retailers are unable to compete with Wal-Mart’s economy of scale and scope.

Compared to competitors such as Walgreens, CVS boasts that it has the most

stores in the nation. This increases its fixed cost per store, hence, not giving

them an economy of scale. In the industry, all stores provide their products and

services to the consumers with about the same efficiency. CVS’s goal is to

provide a wide range and depth of products to its customers. By doing this they

differentiate themselves from other competitors, who attempt to cut costs by

providing their customers with a limited selection of choices. Because of its

power over its suppliers, Wal-Mart has the lowest input cost per unit of

merchandise, so other competitors must find other ways to compete. In addition,

Wal-Mart owns its own trucking line and distribution centers. Because of this,

competitors like CVS are unable to have the lowest distribution cost in the

industry. CVS does not do a lot of brand advertising as compared to competitors

like Wal-Mart and Walgreens, but many of the suppliers and manufacturers

advertise the products sold by CVS. This makes the costs of those specific

products higher, and CVS’s profit margin lower.

CVS finds its competitive advantage is differentiation. Its main advantage is

14

having the ability to carry and sell a wide variety of name brand and off-brand

drugs. It also has an advantage compared to its competitors in that it has a large

number of small local neighborhood stores, so customers have a sense of

security in purchasing medications from CVS. It also delivers a higher quality of

service and convince. CVS provides its customers with an alternative to high

priced name brand drugs with it generic brands which are much cheaper. It also

appeals to its customers by providing “Rapid Refill”, a service that refills

prescription drugs by phone 24 hours a day. In addition to retail drugs, CVS

provides a variety of other products and services, such as photo developing,

personal care products, and many other things that its customers use on a daily

basis. Customer service is where CVS sets itself apart from it competitors. It

provides a number of neighborhood stores with drive-through pick up service for

its prescription drugs. The company boasts its 5,375 stores, saying it has more

pharmacies than any other retailer in the industry. The acquisition of Eckerd has

really added to their advantage by giving them the chance to expand quickly.

CVS has strived to make itself a strong name among its customers. They want to

be thought of as a drug store where the customers can fill their prescriptions and

get sound medical advice.

CVS is constantly trying to come up with new ways to stay on top of its

competition, by providing better and more convenient services to its customers.

They are currently looking at how it is going to compete in the area of mail order

15

prescription drugs. They predict that in the future, many heath insurance

companies will want their customers to buy prescription drugs through the mail

in the belief it will save them money. CVS currently provides a mail order service

that is still in its developmental stages. Soon they hope to implement this service

nation-wide. They believe that due to the aging population of the baby boomers

they should see an increase in sales of prescription and over-the-counter drugs

in the years to come. CVS should also see a significant increase in profits due to

new legalization on Medicare and the introduction of new drugs. They can

sustain their advantages at least for the next few quarters, due to the unrealized

potential of the Eckerd acquisition and expansion into new geographic markets.

The retail drug industry is very competitive and the difference between the top

competitors in the industry is small, so CVS must find other new was to gain an

advantage. There are huge cost barriers to enter the industry or even to stay

alive in the industry. CVS and Walgreens are the two main competitors, but

when you take a broader look at who actually competes with CVS, companies

such as Wal-Mart, grocery stores, and even quick shops come into play.

Key Success Factors

Strengths

CVS is the leader in the retail pharmacy industry and has the second largest

pharmacy chain. CVS is able to offer their customers benefits on their

prescriptions through their own Pharmacy Benefit Management. They are in

16

control of their suppliers because the loss of one, to them, would not hurt their

business. They are in an industry that will always be needed by people. To gain a

strong customer base they offer incentives to their loyal customers. CVS is

currently expanding their stores into new and existing markets.

Weaknesses

Having such a huge competitor (Wal-Mart) in their industry can hinder their

profits and sales. The company has seen a decline in their sales percentage in

the health and beauty and general and seasonal merchandise over the last three

years. CVS relies on the main part of the profit from their front end store items

during end of the year sales. If the company’s profit in the pharmacy section

start to see a decline it will have a hard time producing profit in another section

and they would not easily be able to move into a different industry.

Opportunities

Currently, CVS has been growing to adapt to its environment and competitors.

Baby boomers have a large effect on the retail drug industry because they are a

very populous group that is seeking cheap prescriptions. Additionally, they are

expanding into the south and the west coast for comfortable living. CVS saw the

opportunity to take advantage of this growth by acquiring the Eckerd stores in

those areas. It is obvious that CVS values the acquisition of Eckerd very highly

because they paid over one billion dollars in goodwill to buy Eckerd.

Threats

A threat that CVS has been dealing with, is the growth of Wal-Mart into

17

neighborhood’s everywhere. With the growth of one-stop shopping and low

prices, CVS has to be innovative in the market. CVS’s main focus is competing

on convenience and customer service, while Wal-Mart is lacking in that aspect.

Also, CVS is under investigation for possible securities fraud, presently the case is

still under investigation.

18

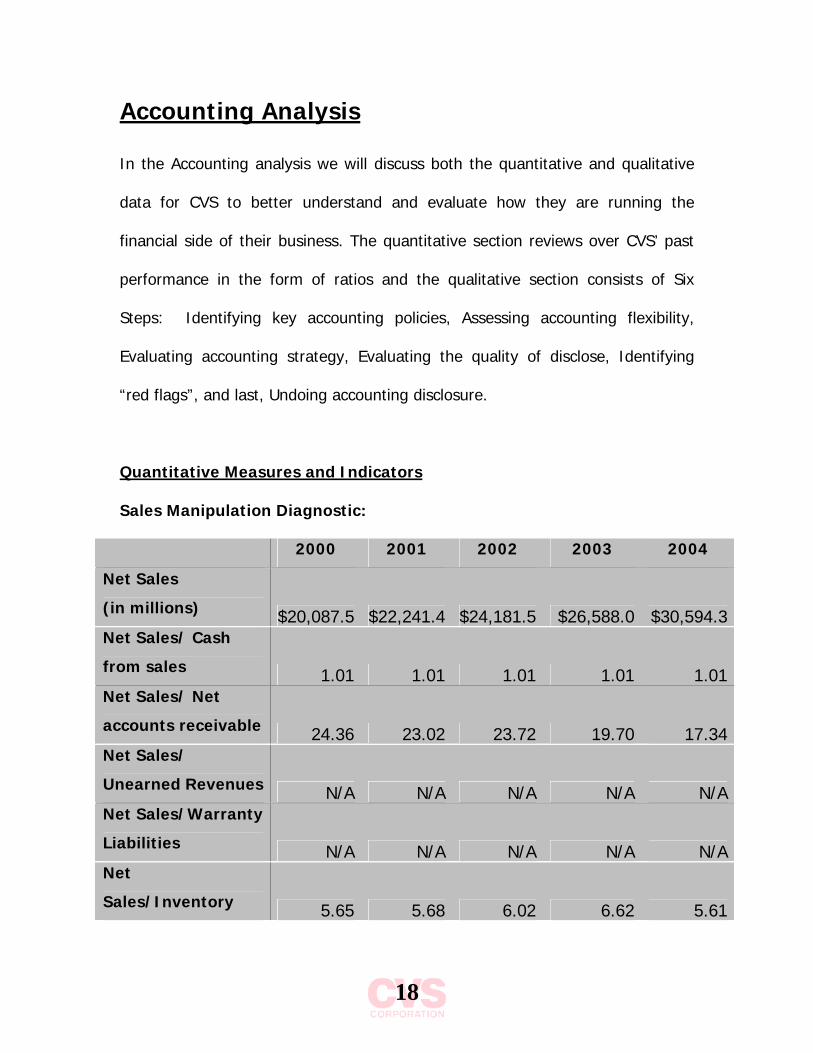

Accounting Analysis

In the Accounting analysis we will discuss both the quantitative and qualitative

data for CVS to better understand and evaluate how they are running the

financial side of their business. The quantitative section reviews over CVS’ past

performance in the form of ratios and the qualitative section consists of Six

Steps: Identifying key accounting policies, Assessing accounting flexibility,

Evaluating accounting strategy, Evaluating the quality of disclose, Identifying

“red flags”, and last, Undoing accounting disclosure.

Quantitative Measures and Indicators

Sales Manipulation Diagnostic:

2000 2001 2002 2003 2004

Net Sales

(in millions) $20,087.5 $22,241.4 $24,181.5 $26,588.0 $30,594.3 Net Sales/ Cash

from sales 1.01 1.01 1.01 1.01 1.01 Net Sales/ Net

accounts receivable 24.36 23.02 23.72 19.70 17.34 Net Sales/

Unearned Revenues N/A N/A N/A N/A N/ANet Sales/Warranty

Liabilities N/A N/A N/A N/A N/ANet

Sales/Inventory 5.65 5.68 6.02 6.62 5.61

19

These ratios illustrate:

CVS’ net sales to cash from sales remained steady, almost the same.

The Net sales to accounts receivables decreased by almost a fifth over the

five years which clearly shows that accounts receivables are increasing by a

significant rate since net sales are also increasing.

The net sales to inventory on the other hand is increasing which indicates

that either the company is reducing their inventory or their inventory is

remaining the same and the increase is just the result of net sales increasing.

Core Expense Manipulation Diagnostics:

2000 2001 2002 2003 2004

Asset Turnover 2.53 2.58 2.51 2.52 2.10

Changes in CFFO/OI 0.59 0.88 1.00 0.68 0.63

Changes in CFFO/

NOA N/A N/A N/A N/A N/A

Total Accruals/

Change in Sales N/A N/A N/A N/A N/A

Pension Expense/

SG&A 0.0714 0.0615 0.0709 0.0665 0.0580

Structure of the Formal Accounting Analysis

Qualitative Measures

STEP 1: Identification of Key Accounting Policies

CVS has identified many different critical and significant accounting policies for

their company. Higher management believes that some of their policies are held

20

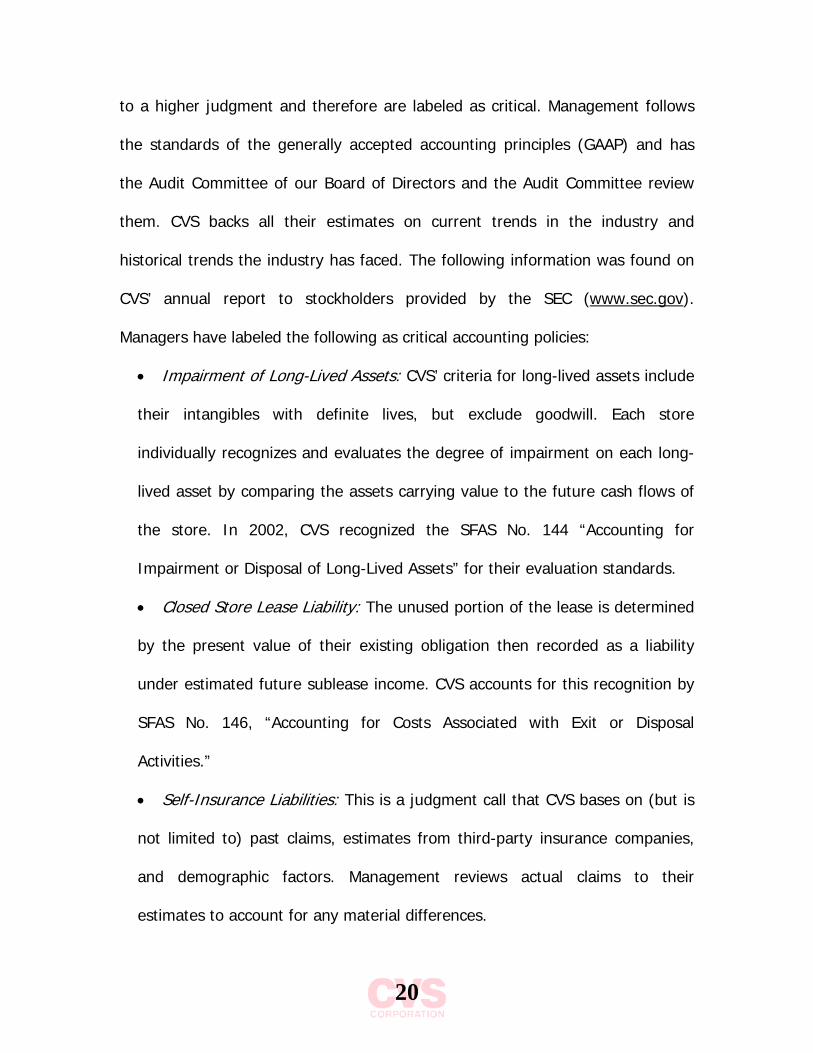

to a higher judgment and therefore are labeled as critical. Management follows

the standards of the generally accepted accounting principles (GAAP) and has

the Audit Committee of our Board of Directors and the Audit Committee review

them. CVS backs all their estimates on current trends in the industry and

historical trends the industry has faced. The following information was found on

CVS’ annual report to stockholders provided by the SEC (www.sec.gov).

Managers have labeled the following as critical accounting policies:

• Impairment of Long-Lived Assets: CVS’ criteria for long-lived assets include

their intangibles with definite lives, but exclude goodwill. Each store

individually recognizes and evaluates the degree of impairment on each long-

lived asset by comparing the assets carrying value to the future cash flows of

the store. In 2002, CVS recognized the SFAS No. 144 “Accounting for

Impairment or Disposal of Long-Lived Assets” for their evaluation standards.

• Closed Store Lease Liability: The unused portion of the lease is determined

by the present value of their existing obligation then recorded as a liability

under estimated future sublease income. CVS accounts for this recognition by

SFAS No. 146, “Accounting for Costs Associated with Exit or Disposal

Activities.”

• Self-Insurance Liabilities: This is a judgment call that CVS bases on (but is

not limited to) past claims, estimates from third-party insurance companies,

and demographic factors. Management reviews actual claims to their

estimates to account for any material differences.

21

• Inventory: Their inventory is stated at the lower of cost or market on a

first-in, first-out (FIFO) basis using the retail method of accounting to

determine cost of sales and inventory. It is adequately measured against

current market conditions and it is taken on a regular basis to ensure the

quality of their statements.

Managers have labeled these next set of accounting polices as significant to

their company, they are as follows:

• Fiscal Year: The Company’s fiscal year is a 52 or 53 week period ending on

the Saturday nearest to December 31 and unless stated all years refer to their

fiscal year.

• Cash and Cash Equivalents: These are all cash and those purchase

investments of three months or less.

• Accounts Receivables: This contains mainly those due from third party

providers (like insurance companies) and vendors. The amount is calculated

net of their uncollectible accounts.

• Property and Equipment: Property is generally depreciated over a 10-40

year period while fixtures and equipment are over a 5-10 year period.

Additional expenses such as maintenance and repair are recorded as incurred.

Anything that extends the useful life of an asset is capitalized and depreciated

accordingly.

• Intangible Assets: These are amortized on a straight-line basis either over

their useful life up to 10 years or for lease, their present lease time to end.

22

• Revenue Recognition: All revenue is recorded at the time the asset is sold

or at the time the service is provided. The company offers a discount to entice

them so to provide faster cash collections and is recorded at sale time. Any

returns are considered irrelevant.

• Vendor Allowances: They follow EITF No. 02-16, “Accounting by a Reseller

for Cash Consideration Received from a Vendor.” This allows them to have

lower inventory costs. The allowances are depreciated on a straight line bases

and are not amortized because the company feels it is not material.

• Store Openings and Closing Costs: New store openings are charged as

expense as is the book value of a closed store.

• Insurance: The Company is self-insured for the automotive, general and

worker’s compensation parts of their business. They have 3rd party insurance

to restrict exposure from the previous claims.

• Stock Based Compensation: These are recognized and recorded based on

the principles of Accounting Principles Board (“APB”) Opinion No. 25,

“Accounting for Stock Issued to Employees,” and related interpretations

• Advertising Costs: They are recorded as an expense when the advertising

takes place.

• Income Taxes: Taxes are recorded as payables because of the difference

in timing between the billing and actual period of accrual.

• Leases: Most of these are operating leases, as opposed to capital leases.

This makes their debt to equity ratio smaller than it would be if they used

23

more capital leases. Failure to recognize these as operating instead of capital

leases can lead to the understatement of lease assets.

STEP 2: Assessment of Accounting Flexibility

CVS has a significant amount of flexibility in the accounting policies chosen by

management. Some of the key policies that offer themselves to interpretation by

the managers include impairment of long-lived assets, self-insurance liabilities,

and inventory valuation. The methods of depreciating and amortizing long-lived

assets create flexibility for managers because they estimate the useful life of the

asset in the straight-line method. Self-insurance liabilities also allow for some

flexibility and interpretation. The level of expected risk determines the amount of

CVS’ insurance policies. Managers could choose to save money on insurance if

they are risk averse which would decrease their expenses, and in return

increasing their net income. On the other hand, managers might choose to

implement a larger insurance policy to increase expenses and decrease net

income to create a tax reduction. If they do this, they might also cut their

expenses in the long-run if other extraordinary expenses, like lawsuits and

environmental factors, are incurred. CVS uses FIFO to value their inventory and

cost of goods sold. Their other options are to use Last In, First Out (LIFO) or

weighted average. These methods each affect net income differently, so they

allow for some flexibility in management.

24

STEP 3: Evaluation of Accounting Strategy

CVS tries to be transparent in many areas to show their true financial standing,

although there are many areas that may be questionable in how they went about

estimating and reporting their financial numbers. CVS loosely follows the

guidelines set forth by the Securities Exchange Commission (SEC) when they are

given alternatives to choose from. They do conform to GAAP which allows

managers to make certain judgment calls. Their strategy appears to give just

what is required of them and no more detail than that. The company appears to

be taking a more aggressive approach to their accounting strategy.

The pharmaceutical section of the retail industry tends to lean to a more

conservative approach when choosing accounting standards. This industry is well

developed with a few main competitors which are Walgreen’s and Rite Aid. All

three firms tend to follow the same guidelines on many accounting policies such

as impairment of long-lived assets, not amortizing goodwill, depreciation on a

straight-line base, and their basis for insurance. Walgreen’s and Rite Aid both

use the LIFO method for inventory valuation while CVS choose to use the FIFO

method. All the firms conform to Accounting Standards No. 142 “Goodwill and

other Intangible Assets” when not amortizing their goodwill. CVS appears to have

no off-balance sheet accounting except for some operating leases but there is no

debt recorded. The company recognizes revenue at the time merchandise is sold

and when their service is provided. Their accounting strategy tends to follow

25

some trends of the industry while some of their other strategies lean towards

managements decisions and estimates.

STEP 4: Evaluation of the Quality of Disclosure

CVS has a low quality of disclosure in their footnotes. It appears that the

company follows GAAP’s requirement but fails to provide any information beyond

that on each of their policies. Their footnotes are broad and leave many

questions with unclear answers about where their numbers were derived from.

CVS provides very broad titles for their income and expense reporting and do not

allow users to see a detailed breakdown of what all is included in these

categories. CVS’s financial statements are not transparent from year to year

because they add and delete line items which cause inconsistency. Even though

CVS’s quality of disclosers leaves much to be desired by its users, we do not

believe that CVS is attempting to mislead users due to the fact that the quality of

disclosure is poor throughout the industry.

STEP 5: Identification of Potential “Red Flags”

CVS’ two competitors both have chosen to use LIFO for the valuation of

inventory while CVS uses FIFO. This might skew their net income level compared

to what their competitors are reporting. Due to the use of FIFO the assets value

will appear higher compared to their competitors leading others to believe that

they carry more inventory but this could be untrue since FIFO allows inventory

26

value to appear high. Their pension expenses and other employment expenses

as a percentage of total expenses have experienced a downward trend over the

past five years. This leads one to believe that the company’s expenses in other

areas have dramatically increased as a percentage of total expenses.

STEP 6: Undo Accounting Disclosure

After conducting our accounting analysis, we found out that CVS wasn’t quite as

transparent as they tried to appear to be. We couldn’t find anything of severe

relevance to initiate any further research. They followed the requirements of

GAAP, but chose not to disclose as much information. We don not believe as of

yet that they have used their flexibility in any inappropriate ways, but just that

their actions, if continued, may bring up questions from higher authority.

Because of this we don’t believe that we need to go back, revaluate, and correct

their financial statements. We would consider a more in-depth look into the

management’s decisions if this vague, unclear trend continues in upcoming

years.

27

Ratio Analysis & Forecast Financials

The purpose of this section is to predict the future performance of CVS. To do

this we forecast their financial statements for the next 10 years and compared

that to the forecasted industry average. The industry average is comprised of

Walgreen’s and Rite-Aid. Wal-Mart is not included in this because of the broad

scope of their business activities and the sheer size of their company. The

analysis of ratios, financial statements, and pro forma statements were used in

determining future values. A conservative approach was taken in predicting the

future figures and forecasting out the next 10 years.

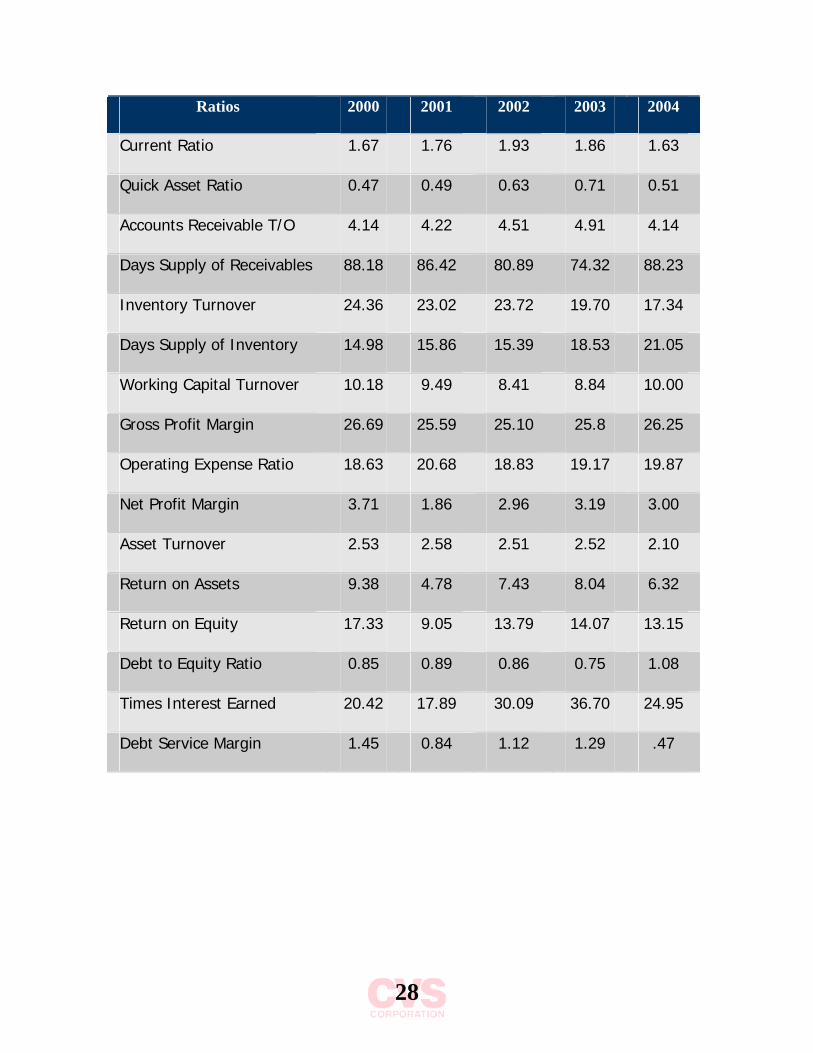

Financial Ratio Analysis

The following ratios were used in our trend (time series) analysis of CVS: Current

Ratio, Quick Asset Ratio, Accounts Receivable Turnover, Days Supply of

Receivables, Inventory Turnover, Days Supply of Inventory, Working Capital

Turnover, Gross Profit Margin, Operating Expense Ratio, Net Profit Margin, Asset

Turnover, Return on Assets, Return on Equity, Debt to Equity Ratio, Times

Interest Earned, and Debt Service Margin. A clear depiction of CVS’ standing was

determined by the basic fourteen ratios and no other ratios were deemed

necessary to use. This information can be found in the table below.

Table 1 - Financial Ratio Analysis

28

Ratios 2000 2001 2002 2003 2004

Current Ratio 1.67 1.76 1.93 1.86 1.63

Quick Asset Ratio 0.47 0.49 0.63 0.71 0.51

Accounts Receivable T/O 4.14 4.22 4.51 4.91 4.14

Days Supply of Receivables 88.18 86.42 80.89 74.32 88.23

Inventory Turnover 24.36 23.02 23.72 19.70 17.34

Days Supply of Inventory 14.98 15.86 15.39 18.53 21.05

Working Capital Turnover 10.18 9.49 8.41 8.84 10.00

Gross Profit Margin 26.69 25.59 25.10 25.8 26.25

Operating Expense Ratio 18.63 20.68 18.83 19.17 19.87

Net Profit Margin 3.71 1.86 2.96 3.19 3.00

Asset Turnover 2.53 2.58 2.51 2.52 2.10

Return on Assets 9.38 4.78 7.43 8.04 6.32

Return on Equity 17.33 9.05 13.79 14.07 13.15

Debt to Equity Ratio 0.85 0.89 0.86 0.75 1.08

Times Interest Earned 20.42 17.89 30.09 36.70 24.95

Debt Service Margin 1.45 0.84 1.12 1.29 .47

29

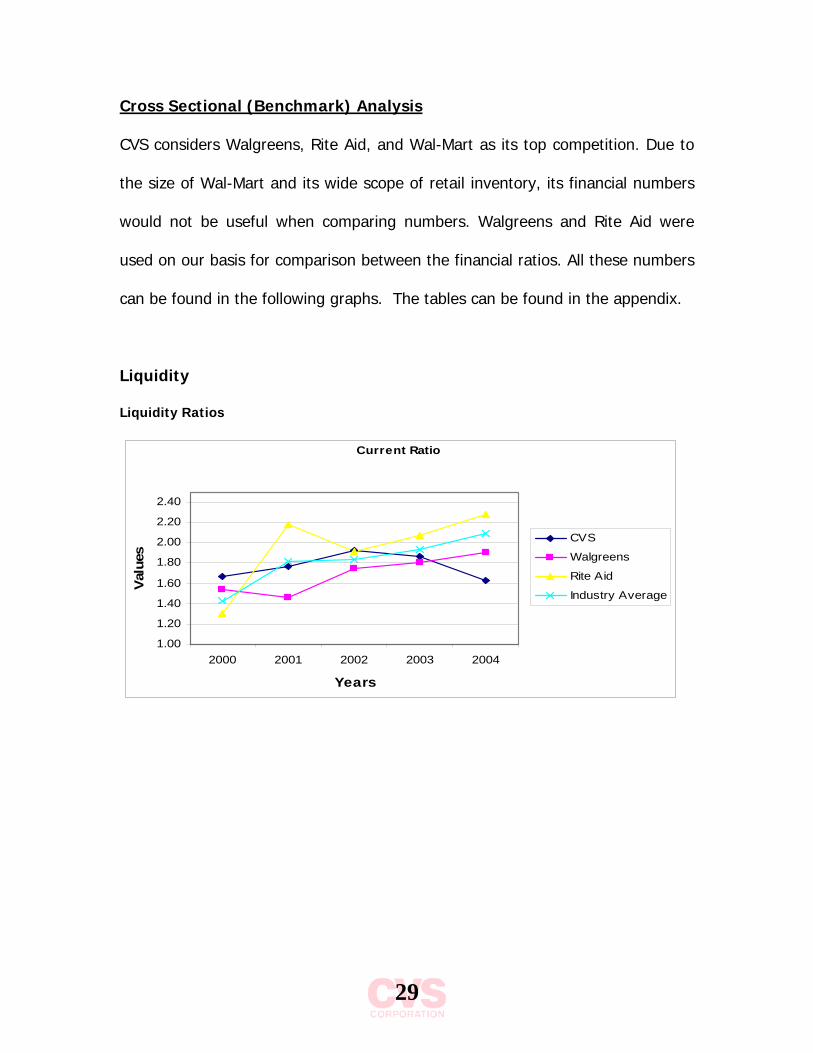

Cross Sectional (Benchmark) Analysis

CVS considers Walgreens, Rite Aid, and Wal-Mart as its top competition. Due to

the size of Wal-Mart and its wide scope of retail inventory, its financial numbers

would not be useful when comparing numbers. Walgreens and Rite Aid were

used on our basis for comparison between the financial ratios. All these numbers

can be found in the following graphs. The tables can be found in the appendix.

Liquidity

Liquidity Ratios

Current Ratio

1.00

1.20

1.40

1.60

1.80

2.00

2.20

2.40

2000 2001 2002 2003 2004

Years

Val

ues

CVS

Walgreens

Rite Aid

Industry Average

30

Quick Asset Ratio

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

2000 2001 2002 2003 2004

Years

Valu

es

CVS

Walgreens

Rite Aid

Industry Average

Inventory Turnover

3.00

3.50

4.00

4.50

5.00

5.50

6.00

2000 2001 2002 2003 2004

Years

Valu

es

CVS

Walgreens

Rite Aid

Industry Average

Days Supply of Inventory

0.0010.0020.0030.0040.0050.0060.0070.0080.0090.00

100.00

2000 2001 2002 2003 2004

Years

Valu

es

CVS

Walgreens

Rite Aid

Industry Average

31

Receivables

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

40.00

2000 2001 2002 2003 2004

Years

Valu

es CVS

Walgreens

Days Supply of Receivables

0.00

5.00

10.00

15.00

20.00

25.00

2000 2001 2002 2003 2004

Years

Valu

es CVS

Walgreens

32

Working Capital Turnover

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

18.00

20.00

2000 2001 2002 2003 2004

Years

Valu

es CVS

Walgreens

The current ratio is calculated by dividing current assets by current liabilities.

This shows if the company is able to pay off their current debt. The industry

average has steadily grown over the last five years from 1.42, in 2000, to 2.09,

in 2004. CVS, in comparison, appears to be following fairly closely with this

trend. Showing they are able to pay off the debt they have incurred. The quick

assets ratio is figured by dividing quick assets by current liabilities. By removing

inventories and prepaid it allows you to see what they can convert into cash this

instant to pay off its current debt. CVS has steadily been higher than the industry

average with the exception of the year 2001 where it was one point below. Being

able to quickly pay off debt is a strong point for this company. The current ratio

and the quick ratio are slowly improving. Both current assets and current

liabilities are increasing, but the assets are increasing at a higher rate than the

liabilities. A flag arises for the next four categories. Inventory turnover, how fast

you able to sale what you offer, and days supply of inventory how many days it

33

takes in a year to turnover you industry are to low and to long. CVS is gradually

below the industry on turning over their inventory, however they are slowly

moving at an increasing this rate since 2000. Therefore they are above the

industry on the days supply of inventory. In both case this is something to watch

out for. This could be a possible outcome of CVS using FIFO while its competitors

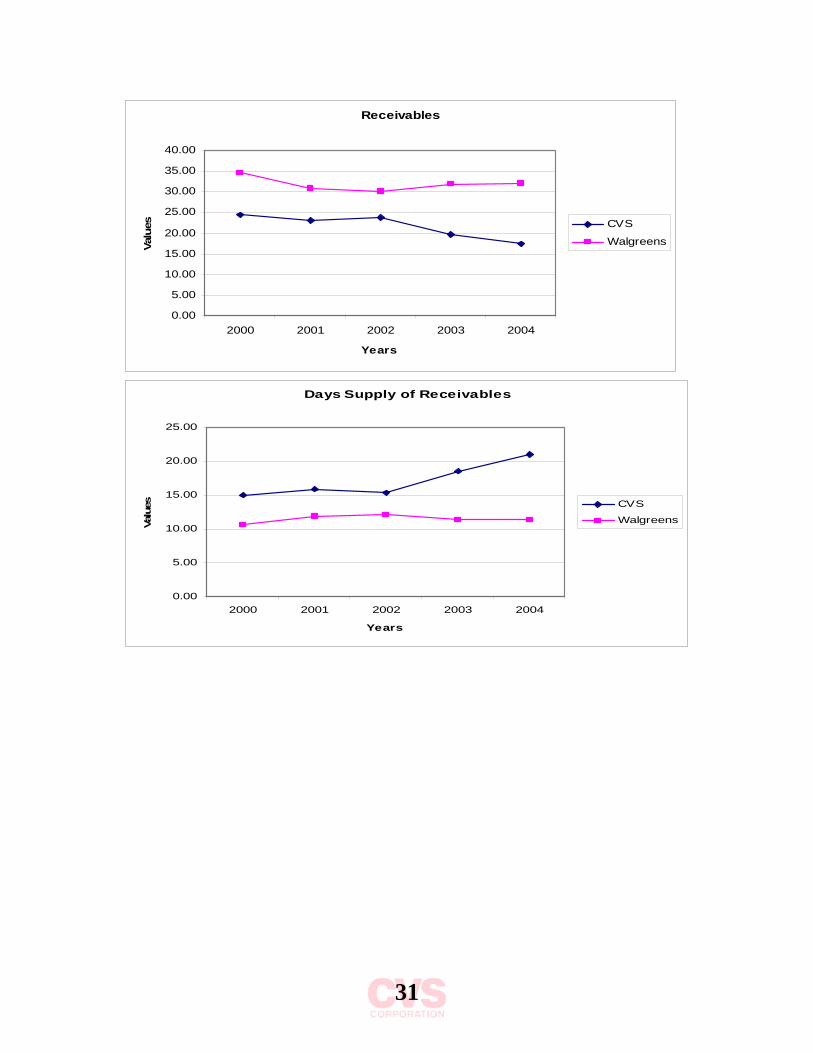

have both chosen to use LIFO. Receivables turnover, how quickly they are able

to collect cash for items on credit. The data for Rite Aid was not available so a

comparison between CVS and Walgreens was performed. CVS is below

Walgreens and is has steadily increased over the last five years. One wonders

why they are having problems collecting cash and should be closely watched for

improvement. Just the reverse holds true for days supply of receivable. They

were gradually increasing the last four years and took a jump this past year,

staying below the competition. This could effect there ability to remain liquid and

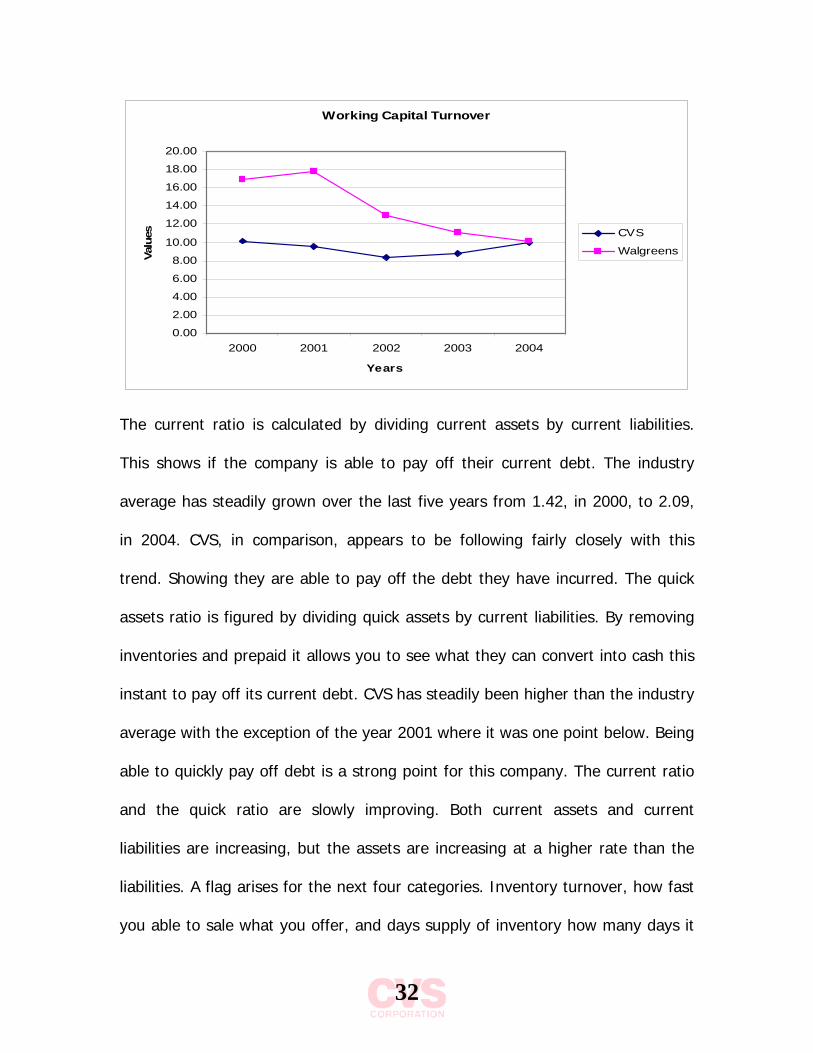

should be monitored for improvement. Working capital turnover is taken by

dividing sales by working capital. Working capital is just current assets minus

current liabilities. This shows how efficiently they are using there assets to

produce sales. A steady decrease is occurring between both firms here. CVS falls

short of Walgreens with numbers but this last year the gap between the two

significantly shorten. The industry trend should be watched for improvement.

Overall CVS is increasing is some aspects of their firm while others are falling

short of expectations.

34

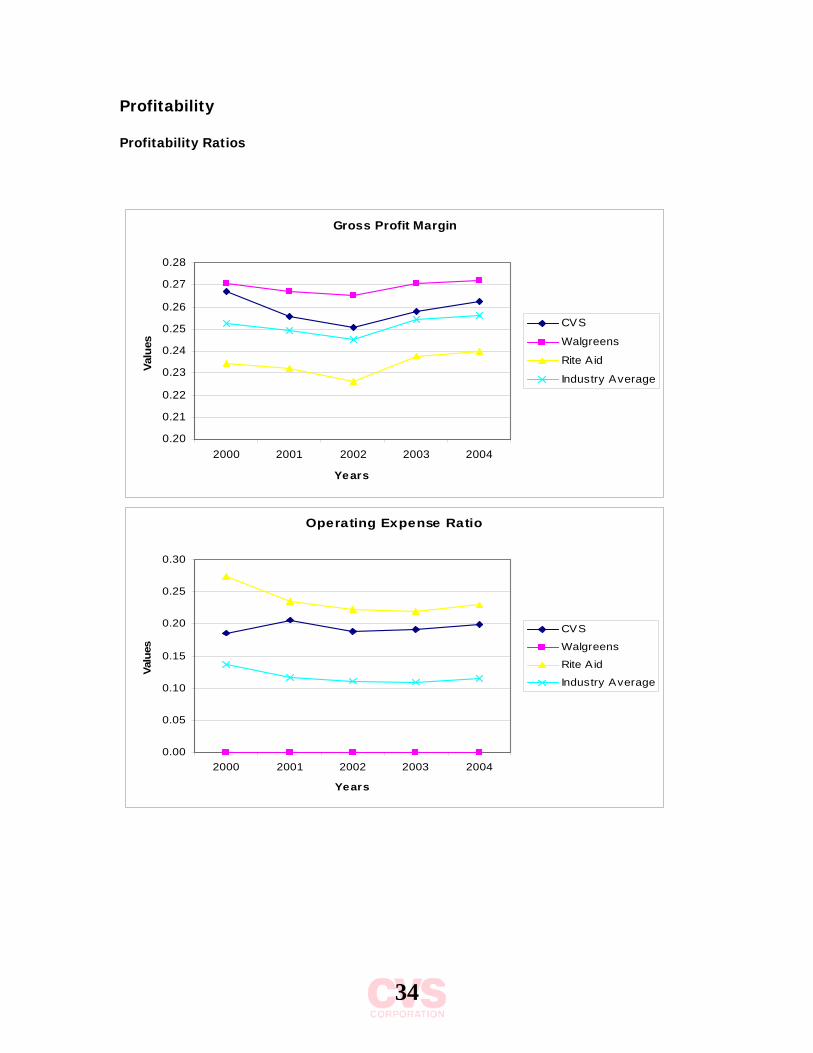

Profitability

Profitability Ratios

Gross Profit Margin

0.20

0.21

0.22

0.23

0.24

0.25

0.26

0.27

0.28

2000 2001 2002 2003 2004

Years

Valu

es

CVS

Walgreens

Rite Aid

Industry Average

Operating Expense Ratio

0.00

0.05

0.10

0.15

0.20

0.25

0.30

2000 2001 2002 2003 2004

Years

Valu

es

CVS

Walgreens

Rite A id

Industry Average

35

Net Profit Margin

-0.12

-0.10

-0.08

-0.06

-0.04

-0.02

0.00

0.02

0.04

0.06

2000 2001 2002 2003 2004

Years

Valu

es

CVS

Walgreens

Rite Aid

Industry Average

Asset Productivity

1.00

1.50

2.00

2.50

3.00

3.50

2000 2001 2002 2003 2004

Years

Valu

es

CVS

Walgreens

Rite Aid

Industry Average

Return on Assets

-0.25

-0.20

-0.15

-0.10

-0.05

0.00

0.05

0.10

0.15

2000 2001 2002 2003 2004

Years

Valu

es

CVS

Walgreens

Rite Aid

Industry Average

36

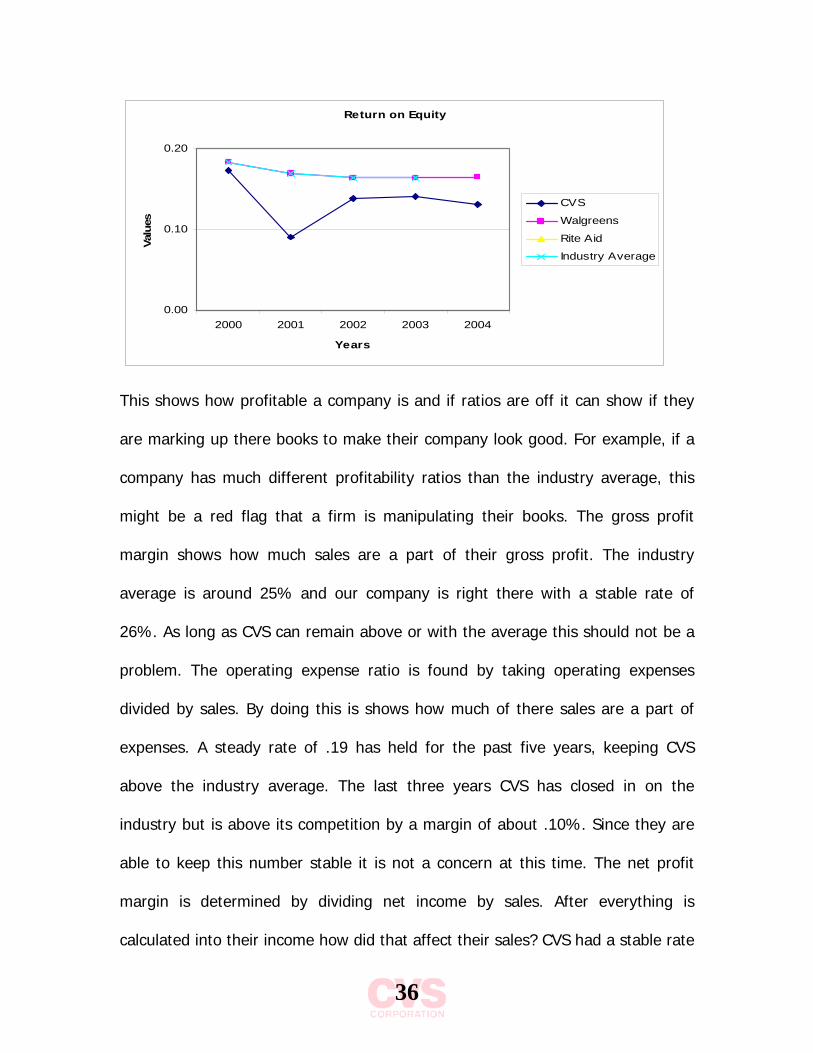

Return on Equity

0.00

0.10

0.20

2000 2001 2002 2003 2004

Years

Valu

es

CVS

Walgreens

Rite Aid

Industry Average

This shows how profitable a company is and if ratios are off it can show if they

are marking up there books to make their company look good. For example, if a

company has much different profitability ratios than the industry average, this

might be a red flag that a firm is manipulating their books. The gross profit

margin shows how much sales are a part of their gross profit. The industry

average is around 25% and our company is right there with a stable rate of

26%. As long as CVS can remain above or with the average this should not be a

problem. The operating expense ratio is found by taking operating expenses

divided by sales. By doing this is shows how much of there sales are a part of

expenses. A steady rate of .19 has held for the past five years, keeping CVS

above the industry average. The last three years CVS has closed in on the

industry but is above its competition by a margin of about .10%. Since they are

able to keep this number stable it is not a concern at this time. The net profit

margin is determined by dividing net income by sales. After everything is

calculated into their income how did that affect their sales? CVS had a stable rate

37

at .04 but in 2002 it dropped to .02, they were able to rise over the last two

years to .03. They are right with their competitor Walgreens and above the

industry average. CVS appears to have a constant Asset Productivity rate around

2.50 staying above the industry the except for the last two years. Asset turnover

is calculated by dividing sales by total assets. CVS appears to have a constant

rate around 2.50 staying above the industry the except for the last two years.

Return on equity figured by dividing net income by equity show that CVS had

slightly decreasing returns on equity. CVS had slightly decreasing returns on

equity. A high ROE is favorable because it means that net income is larger in

comparison to equity. This shows the profitability of CVS is going down. There

was a large drop in return on equity in 2001 for CVS, but the industry was not

affected.

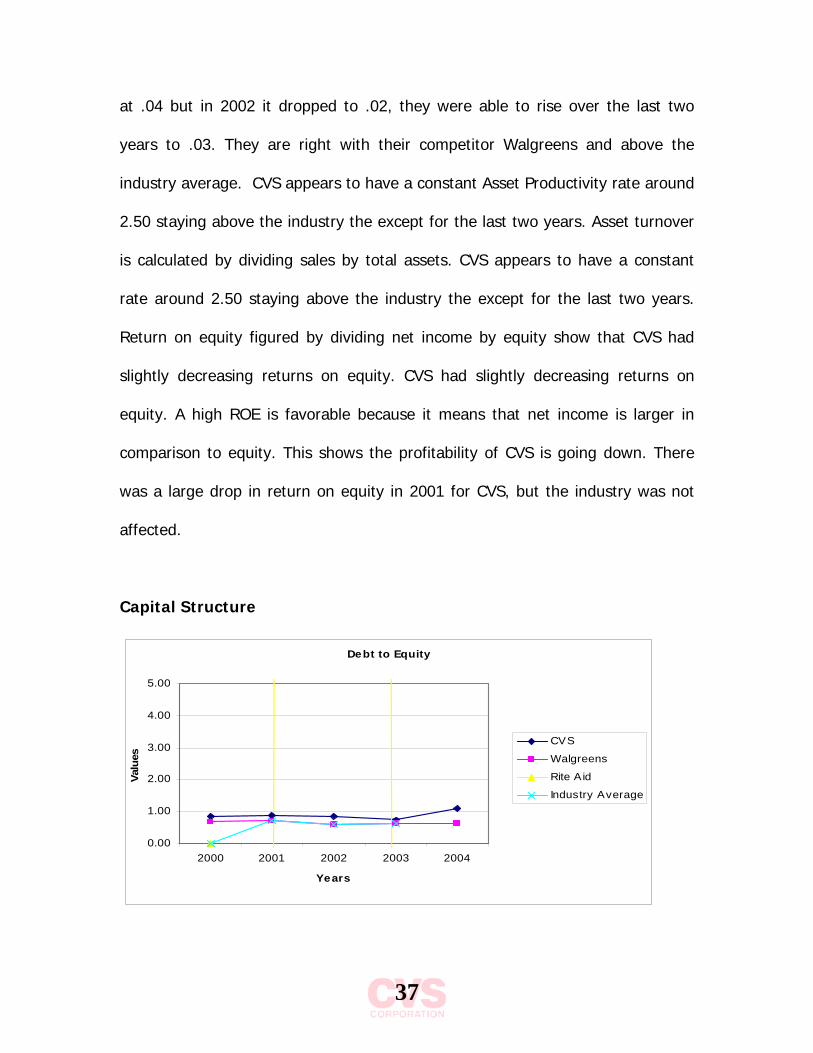

Capital Structure

Debt to Equity

0.00

1.00

2.00

3.00

4.00

5.00

2000 2001 2002 2003 2004

Years

Valu

es

CVS

Walgreens

Rite Aid

Industry Average

38

Times Interest Earned

-5.00

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

40.00

2000 2001 2002 2003 2004

Years

Valu

es

CVS

Walgreens

Rite Aid

Indus try Average

Debt Service Margin

-0.40

-0.20

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

2000 2001 2002 2003 2004

Years

Valu

es

CVS

Walgreens

Rite Aid

Industry Average

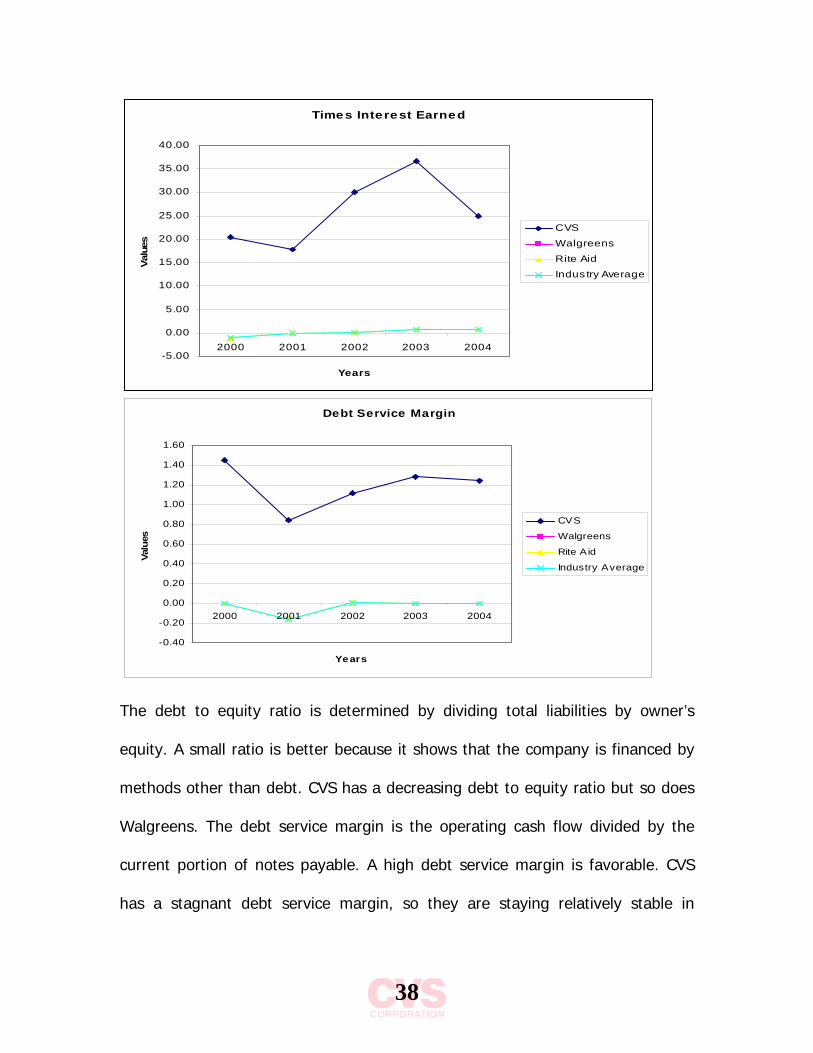

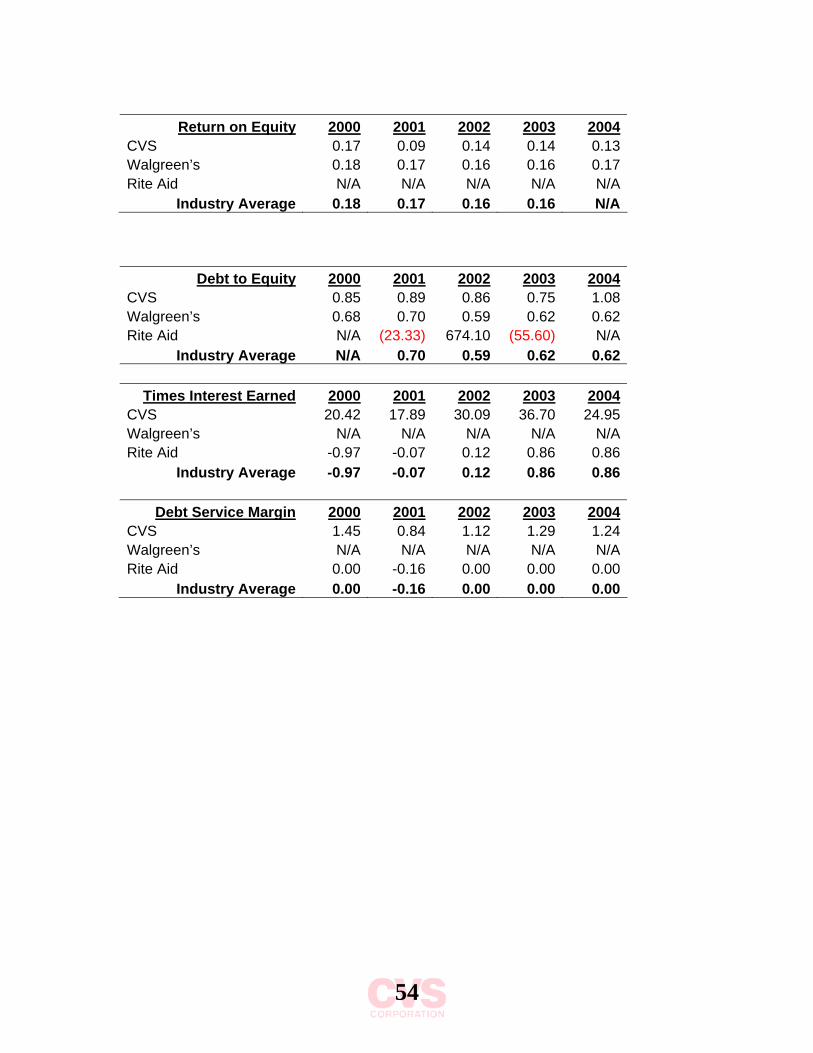

The debt to equity ratio is determined by dividing total liabilities by owner’s

equity. A small ratio is better because it shows that the company is financed by

methods other than debt. CVS has a decreasing debt to equity ratio but so does

Walgreens. The debt service margin is the operating cash flow divided by the

current portion of notes payable. A high debt service margin is favorable. CVS

has a stagnant debt service margin, so they are staying relatively stable in

39

respect to their operating cash flows and current notes payable. The industry’s

numbers were unavailable, so CVS cannot be compared to anyone else.

Times interest earned is net income before interest and taxes divided by interest

expense. It is favorable to have higher net income compared to interest

expenses, so a larger number is favorable. CVS has an improving times interest

earned because it is getting larger. Rite Aid’s is also increasing, but it is very

small compared to CVS.

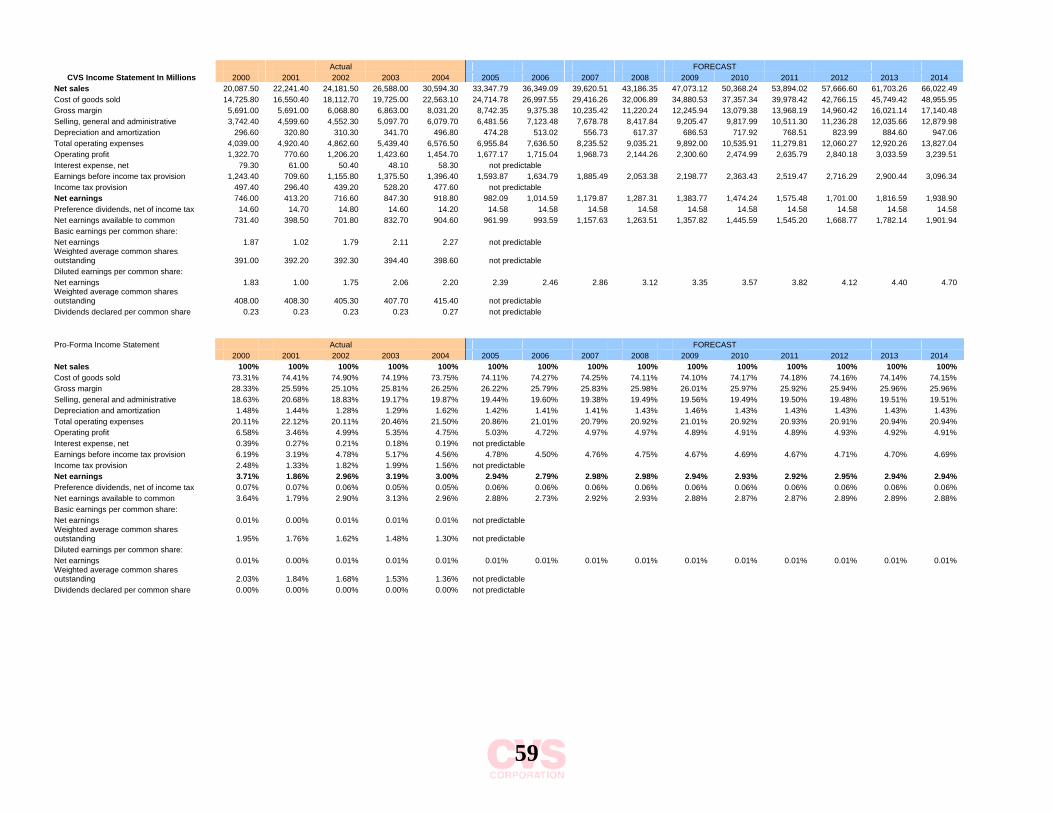

Financial Statement Forecasting Methodology:

Income Statement

The most important part of accurately forecasting a company’s future financials

is determining the sustainable growth rate. By analyzing the past 5 years’ net

income and dividend payout ratio we determined that the sustainable growth

rate (SGR) for our company will be around 9 percent. For the past five years CVS

had a growth rate around six percent and for 2003, it had a nine percent rate.

The Yahoo Finance website (www.finance.yahoo.com) predicted a growth rate

around 13 percent for the next five years. The acquisition of Eckerd was

completed in 2004, so we took into account the possible effects this will have on

CVS in the years to come. Because of this, CVS will most likely experience some

growth, so we figured that a rate of six percent was too low. We also felt that 13

was a very aggressive rate. Therefore we determined that a good growth rate for

40

2005 through 2009 would be 9 percent and for 2010 through 20014 would be 7

percent. It would be impossible for CVS to grow indefinitely, so it will most likely

level off in the distant future. In 2001 sales were negatively impacted by

pharmacy shortages. Many patents for brand name drugs began to expire in

2003, causing CVS to get a smaller profit margin on these items. This is because

generic drugs (with small profit margins) became available for sale, causing the

margin on the comparable brand name drugs to decrease in order to adequately

compete. Another incidence like this is not predictable, so it is safe to assume

the growth rates will be higher than in these years. We were unable to

determine a maximum sustainable growth rate because CVS does not pay

dividends.

For the most part, we used averages to forecast our pro forma income

statement. All of the data was taken 5 years back and will be forecasted 10 years

into the future. A conservative approach was taken when predicting the numbers

for future years.

For predicting the pro forma balance sheet a conservative approach was also

taken. The same method was applied over all the categories in this statement.

First a trend or pattern was established then an educated estimate was

determined.

41

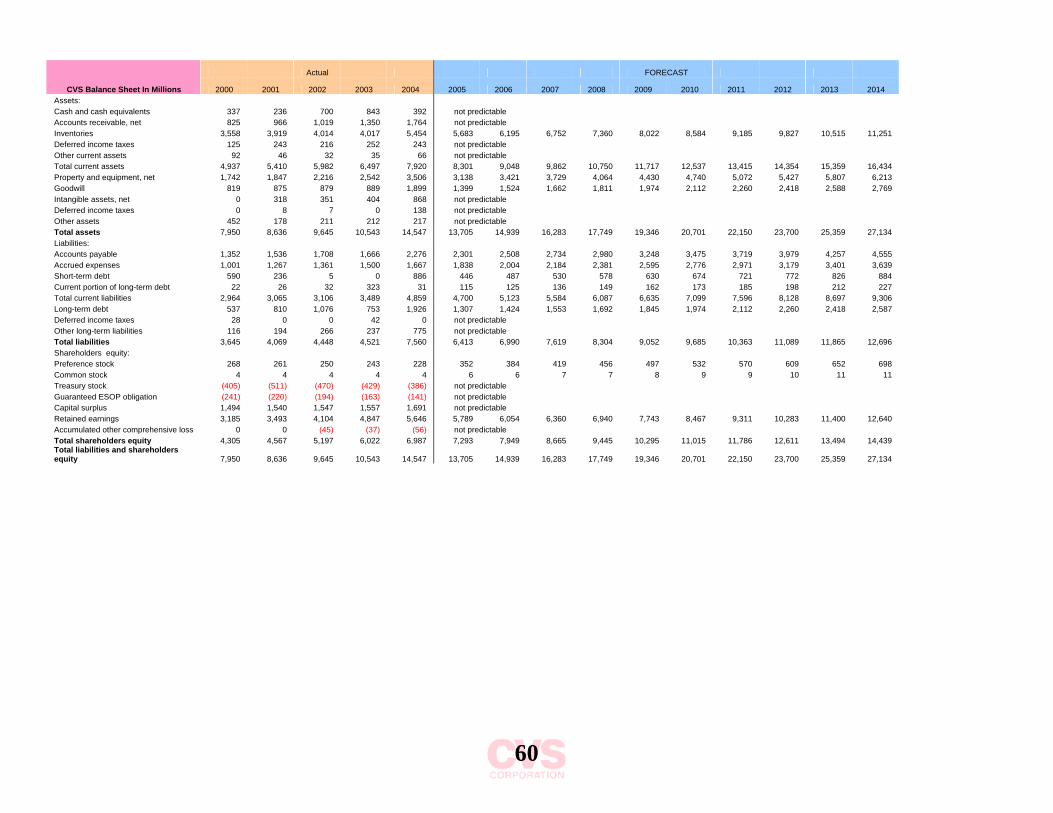

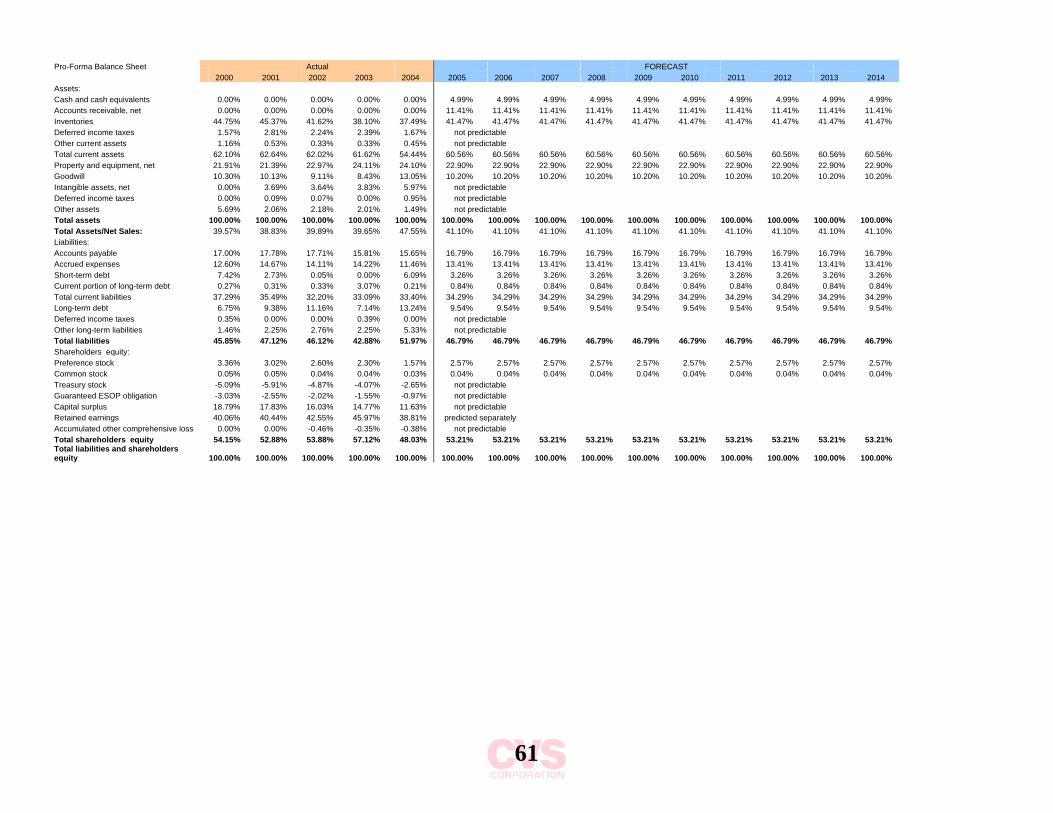

Balance Sheet

The Balance Sheet, like the Income Statement, was forecasted over the next ten

years. The methods for forecasting used were the average method, which is the

past five year’s data added together and divided by five, and the average-

difference method.

To predict future total assets, we computed assets as a percentage of sales

because sales have already been predicted. Then we averaged these

percentages to make assets 41.1 percent of sales for the next ten years. The

numbers we came up with for total assets will also be used as the forecasted

liabilities plus stockholder’s equity as these two numbers are always equal. To

come up with liabilities, we used the pro forma number (liabilities as a

percentage of assets). To get the equity section of the balance sheet, we used

the average of the pro forma numbers, with the exception of retained earnings

and other comprehensive loss. Retained earnings must equal the beginning

balance in retained earnings (last year’s RE) plus this year’s expected net

income, minus this year’s expected amount of dividend payment. The other

comprehensive loss was used as a plug to ensure that owner’s equity and

liabilities add up to total assets.

Even though these are good estimates taken from past years and applied

towards the future years, it’s impossible to predict major events that may occur.

42

While valuing a company, and especially forecasting, we have to keep this in

mind. We certainly hope that unfortunate events do not occur and throw off all

our predictions.

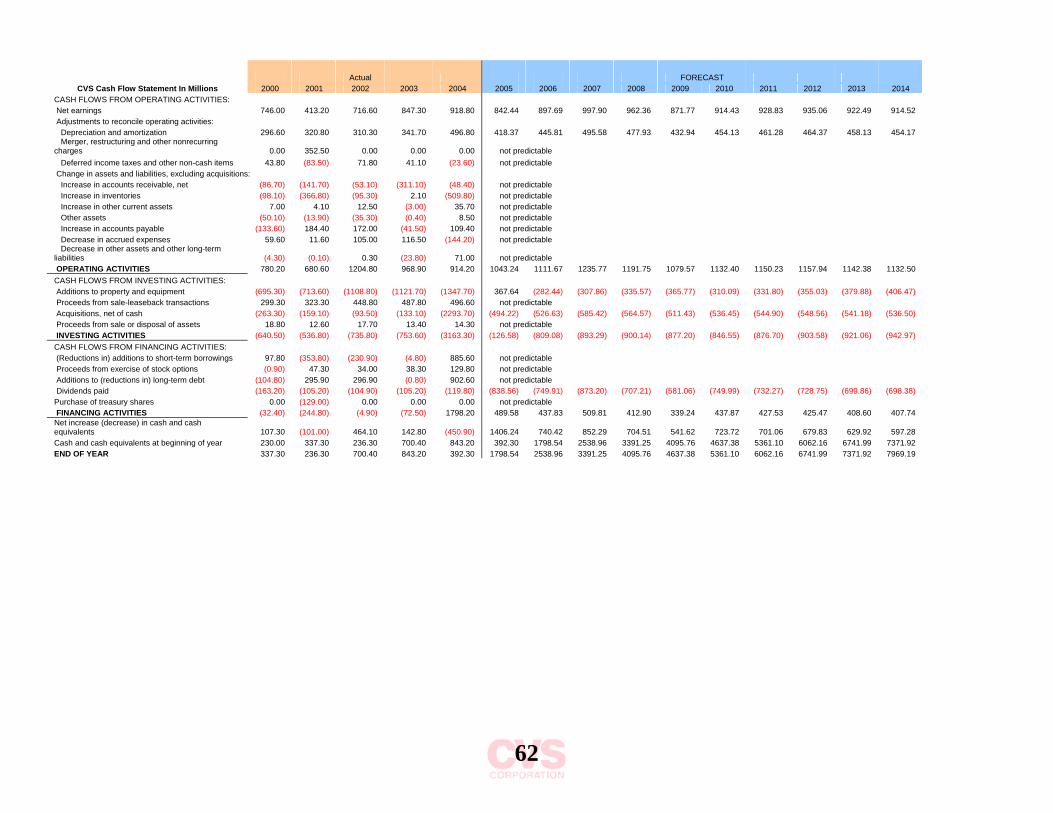

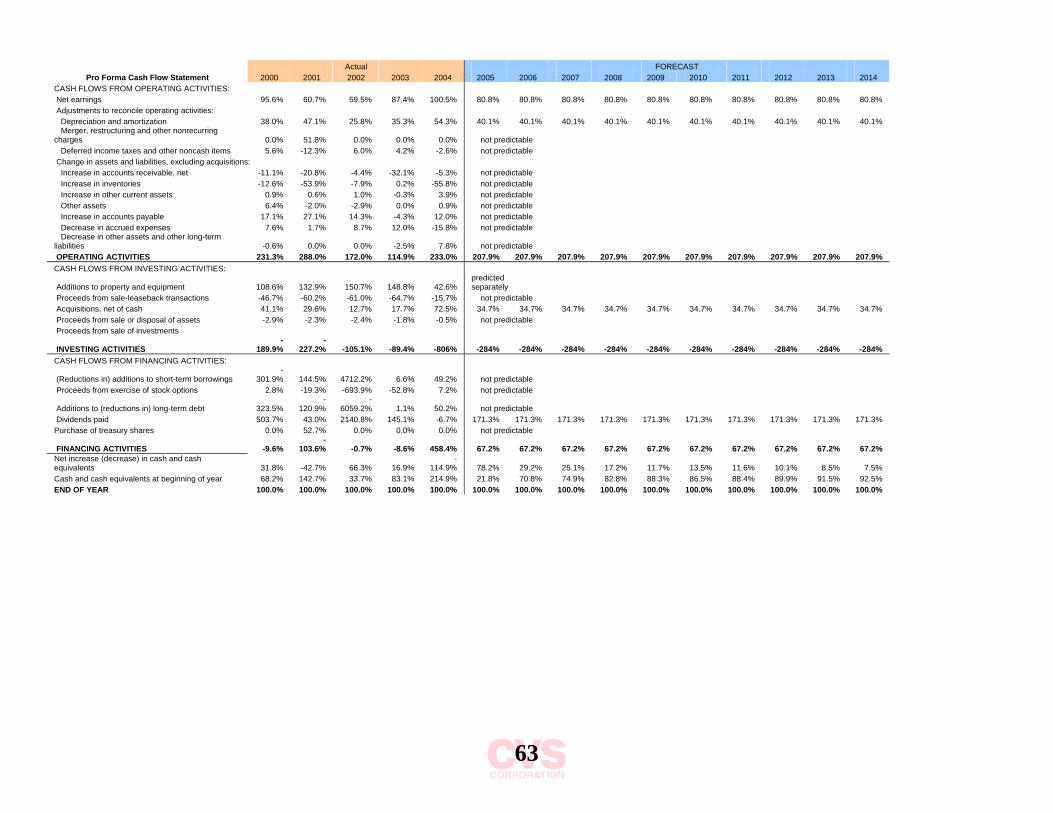

Statement of Cash Flows

To forecast the next 10 years of CVS’ cash flows we made a pro-forma CF sheet

for 2000 to 2004. Each line item in cash flows from operating activities was

divided by total CFFO, the line items in cash flows from investing activities were

divided by total CFFI, and the items in cash flows from financing activities were

divided by total CFFF. The total CFFO, CFFI, and CFFF were each divided by

cash and cash equivalents at the end of the year. An average of 2000 to 2004’s

pro forma percentages was used to forecast the CFFO, CFFI, and CFFF for years

2005 to 2014. This average was multiplied by the forecasted cash and cash

equivalents number to arrive at each of the line items of the cash flow

statement. Many of the items were not able to be forecasted because they are

influenced by unpredictable events. For the dividends paid we took the actual

five years data and used a moving average of a five year period to forecast the

next ten years. To get Additions to PP&E, we found the growth rate of PP&E

each year and determined those numbers to be the additions to PP&E. In order

to determine the cash flows from investing activities, we added Additions to

PP&E to Acquisitions Net of Cash, because these were the only predictable

numbers in this section.

43

Valuation Analysis

The purpose of this section is to determine the value of CVS. With the use of six

methods, we are able to determine if CVS is overvalued, undervalued, or

accurately valued. The six methods we have used to value CVS include the

following: method of comparables, discounted dividends, discounted free cash

flows, discounted residual income, abnormal earnings growth, long run average

residual income perpetuity based on the price to book ratio. The Ford Epic

valuation of CVS is $45.89. These methods allow us to view the firm with respect

to a variety of different aspects of the firm’s performance, and determine

whether it would be a good investment.

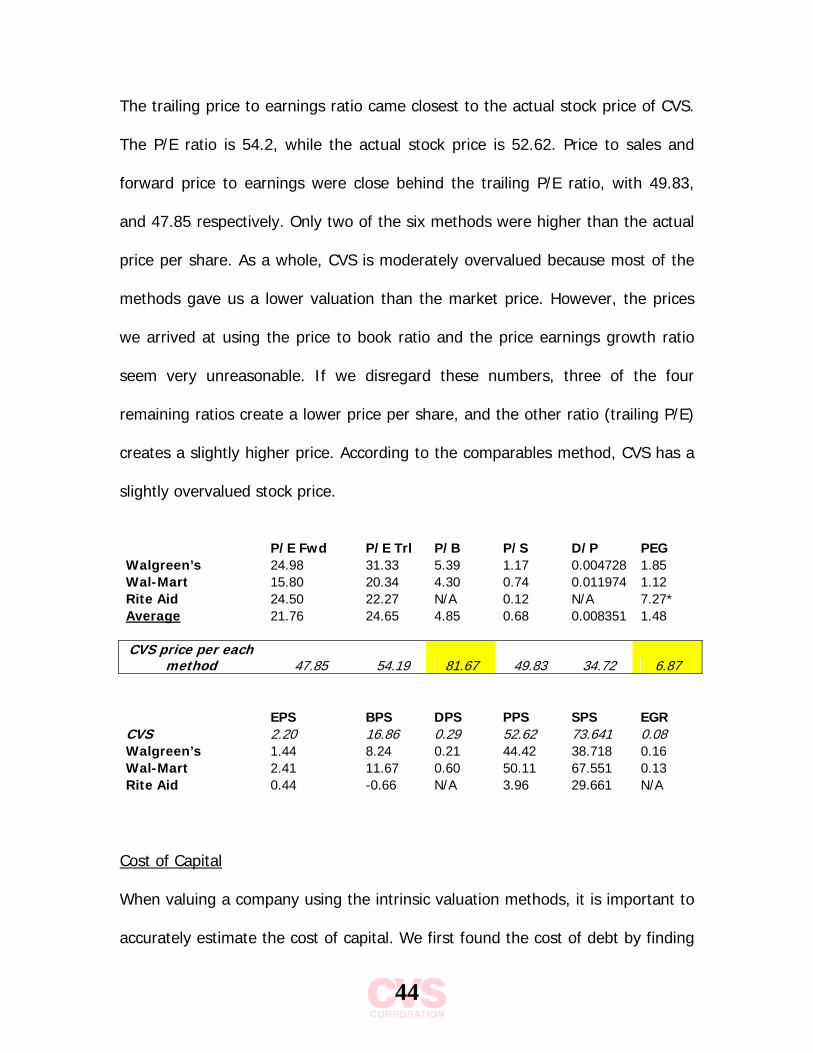

Comparables

The comparables method is the only non-intrinsic method of valuation we use;

this means that it does not only use information about the company to determine

its current value. It uses the industry average of certain ratios to determine the

company’s ideal stock price. The ratios used in comparing CVS to the industry

are the price to equity ratio (forward and trailing), price to book, dividend price

ratio, price to sales ratio, and the price earnings growth model. The closest

competitors to CVS in the retail pharmacy industry are Walgreen’s, Rite Aid, and

Wal-Mart.

44

The trailing price to earnings ratio came closest to the actual stock price of CVS.

The P/E ratio is 54.2, while the actual stock price is 52.62. Price to sales and

forward price to earnings were close behind the trailing P/E ratio, with 49.83,

and 47.85 respectively. Only two of the six methods were higher than the actual

price per share. As a whole, CVS is moderately overvalued because most of the

methods gave us a lower valuation than the market price. However, the prices

we arrived at using the price to book ratio and the price earnings growth ratio

seem very unreasonable. If we disregard these numbers, three of the four

remaining ratios create a lower price per share, and the other ratio (trailing P/E)

creates a slightly higher price. According to the comparables method, CVS has a

slightly overvalued stock price.

P/E Fwd P/E Trl P/B P/S D/P PEG Walgreen’s 24.98 31.33 5.39 1.17 0.004728 1.85 Wal-Mart 15.80 20.34 4.30 0.74 0.011974 1.12 Rite Aid 24.50 22.27 N/A 0.12 N/A 7.27* Average 21.76 24.65 4.85 0.68 0.008351 1.48 CVS price per each

method 47.85 54.19 81.67 49.83 34.72 6.87 EPS BPS DPS PPS SPS EGR CVS 2.20 16.86 0.29 52.62 73.641 0.08 Walgreen’s 1.44 8.24 0.21 44.42 38.718 0.16 Wal-Mart 2.41 11.67 0.60 50.11 67.551 0.13 Rite Aid 0.44 -0.66 N/A 3.96 29.661 N/A

Cost of Capital

When valuing a company using the intrinsic valuation methods, it is important to

accurately estimate the cost of capital. We first found the cost of debt by finding

45

a weighted value of each debt item. Then we found the interest rates charged on

each item and multiplied that by the weighted value. The product of these

numbers was added up to arrive at the weighted average cost of debt. This is

what we used in the valuation models as the cost of debt for CVS.

The cost of equity was found by using the Capital Asset Pricing Model (CAPM)

formula:

Rj= Rf + βj(Rm –Rf)

We found the risk free rate by averaging the past five year’s treasury bill monthly

yields, then multiplied it by 12 to get a yearly rate of 4.046 percent.

(http://research.stlouisfed.org)

The market premium was found by subtracting the risk-free rate from the

average market yield from the past five years. The firm’s beta was found by

getting the slope of the firm’s past five year’s returns. For each variable

estimated, we used a five year span because we are trying to value the company

on a long-term basis. Most individual stock investments are held over the span of

many years. We also believe that it is unreasonable to consider any amount of

time less than five years to be a trend. We determined CVS to have a cost of

equity of 5.501 percent. (http://finance.yahoo.com)

46

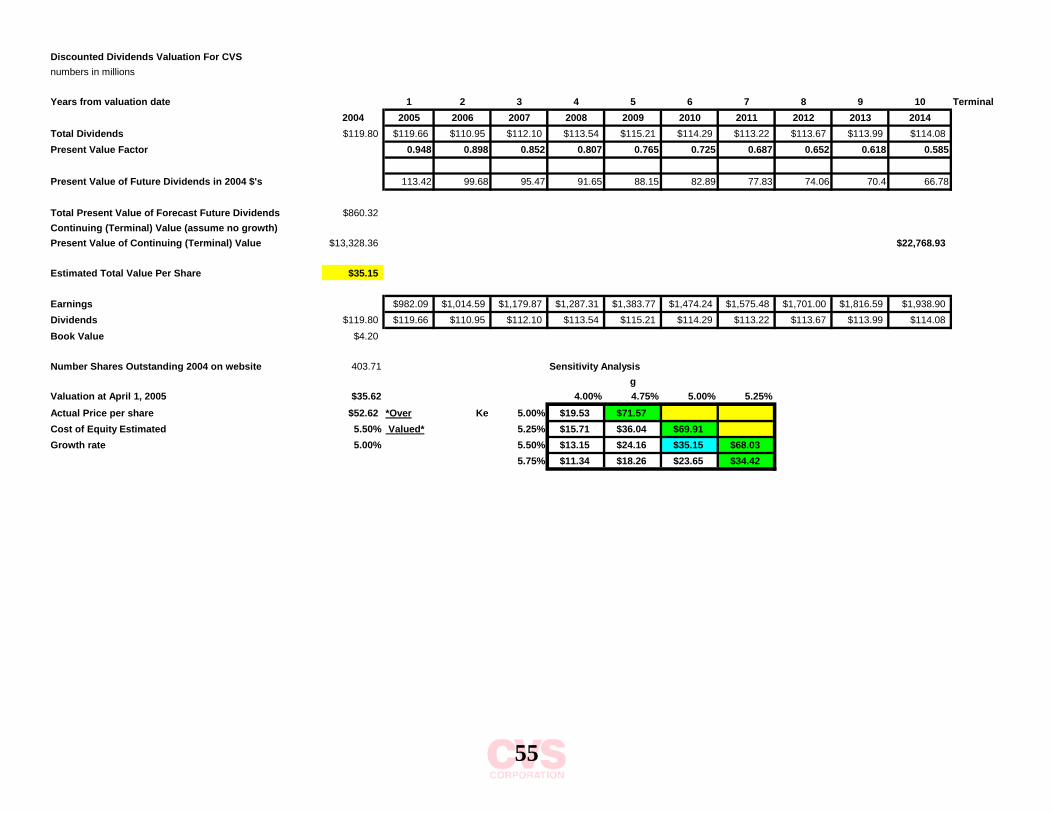

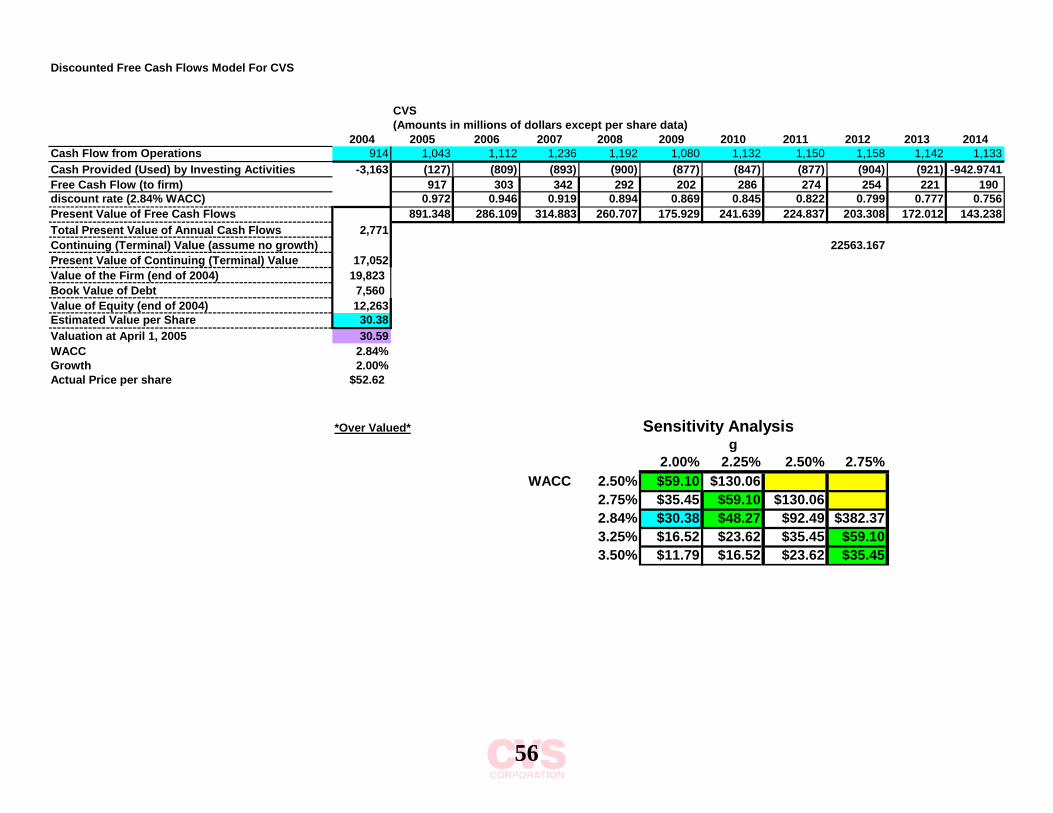

Discounted Dividends and Discounted Free Cash Flow Methods

The discounted dividend method and the discounted free cash flow method are

very similar. The only difference between the two methods of valuation is in the

item forecasted. For the discounted dividends method, we forecast the amount

of dividends to be paid over the next ten years; and for the free cash flow

method, we forecast the amount of free cash flows to be paid over the next ten

years. We arrive at the number used for free cash flow by subtracting cash flows

from operating activities by cash flows from investing activities in each year from

2005 to 20014. To discount these numbers back to the 2004 dollars, we multiply

by the present value multiplier. Next we get the sum of the present values of the

dividends for the DD method and the sum of the present values of the free cash

flows for the FCF method. If there is a perpetual growth rate for year 20015 and

beyond, the terminal value must be computed, discounted back to 2004, and

added to the sum of the present value of the dividends (or free cash flows). We

arrive at the terminal value in 2014 dollars by dividing the perpetual dividend

(free cash flow) amount by the cost of capital less the perpetual growth rate.

Once we determine the total present value of all the future dividends (free cash

flows) we divide by the firm’s number of shares outstanding. This gives us the

intrinsic value of CVS to date, which is $35.15 per share according to the

discounted dividends method. The free cash flow method gave us an intrinsic

value of $30.38. Both of these methods indicate that CVS is overvalued.

47

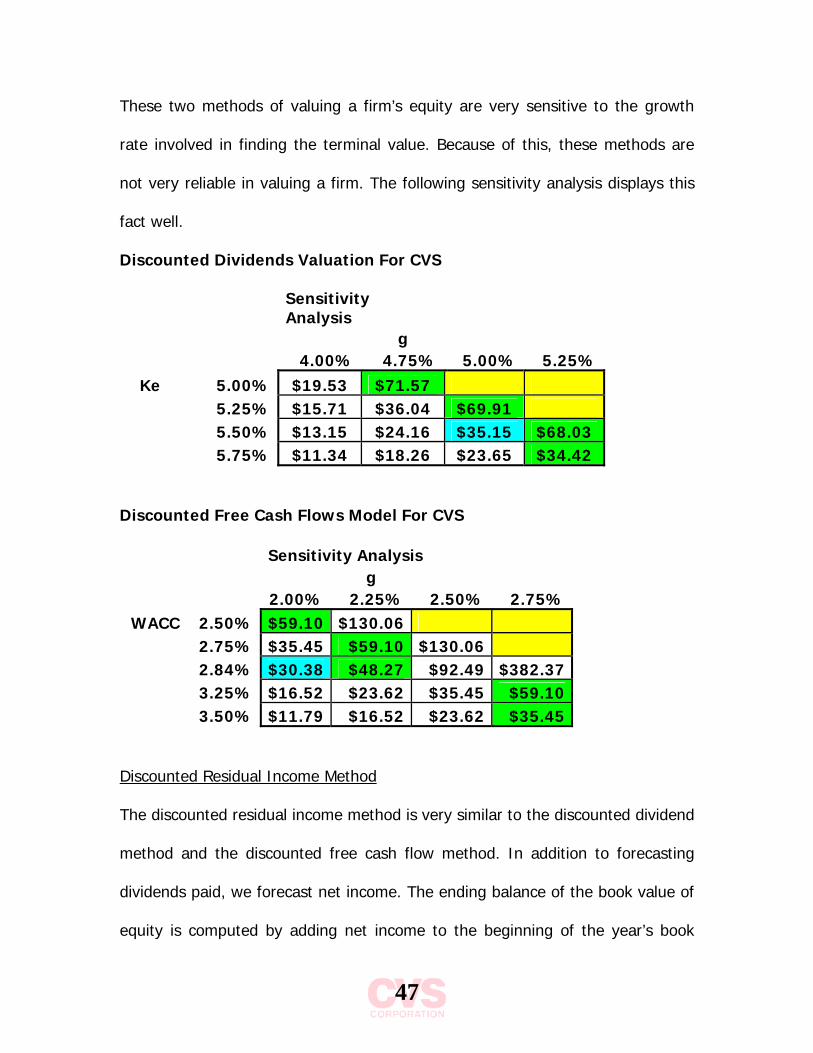

These two methods of valuing a firm’s equity are very sensitive to the growth

rate involved in finding the terminal value. Because of this, these methods are

not very reliable in valuing a firm. The following sensitivity analysis displays this

fact well.

Discounted Dividends Valuation For CVS

Sensitivity Analysis

g 4.00% 4.75% 5.00% 5.25%

Ke 5.00% $19.53 $71.57 5.25% $15.71 $36.04 $69.91 5.50% $13.15 $24.16 $35.15 $68.03 5.75% $11.34 $18.26 $23.65 $34.42

Discounted Free Cash Flows Model For CVS Sensitivity Analysis g 2.00% 2.25% 2.50% 2.75%WACC 2.50% $59.10 $130.06

2.75% $35.45 $59.10 $130.06 2.84% $30.38 $48.27 $92.49 $382.37 3.25% $16.52 $23.62 $35.45 $59.10 3.50% $11.79 $16.52 $23.62 $35.45

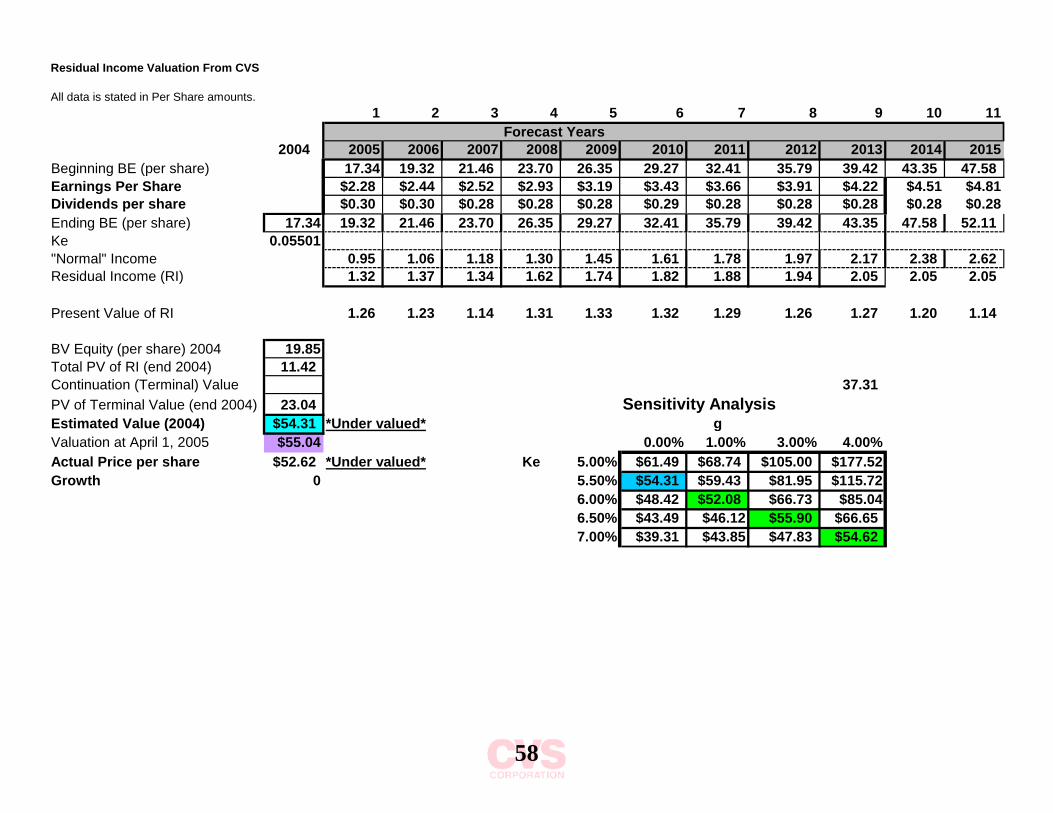

Discounted Residual Income Method

The discounted residual income method is very similar to the discounted dividend

method and the discounted free cash flow method. In addition to forecasting

dividends paid, we forecast net income. The ending balance of the book value of

equity is computed by adding net income to the beginning of the year’s book

48

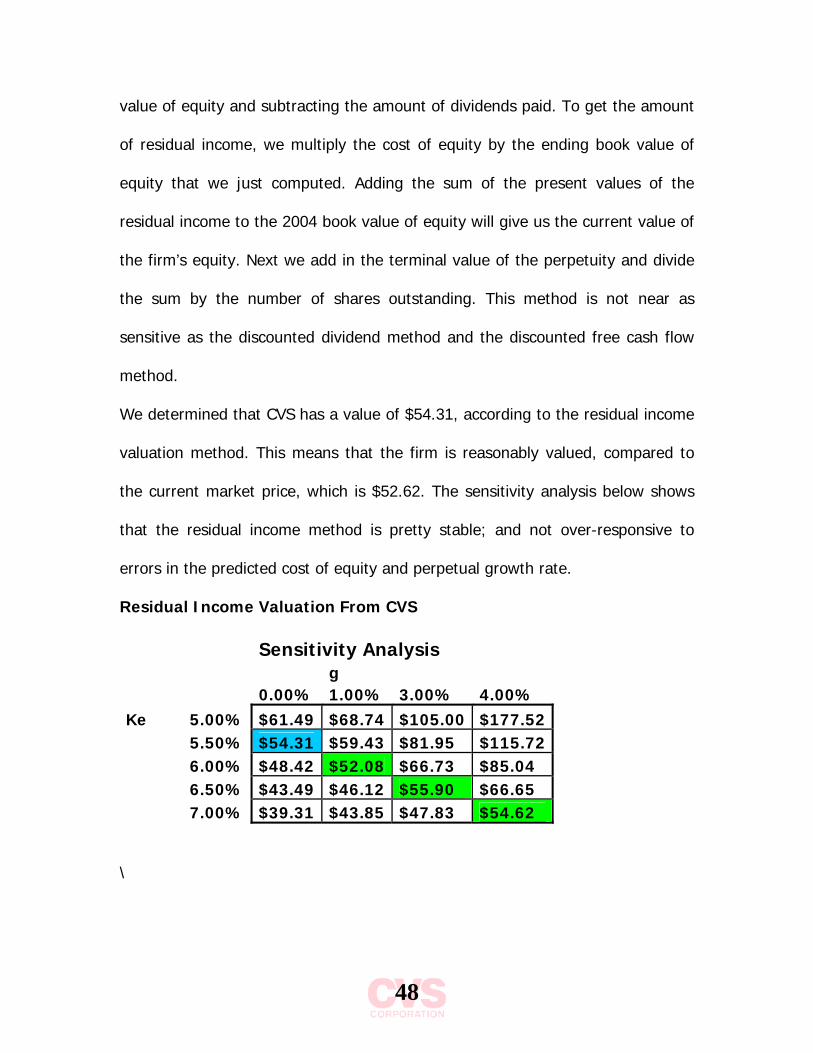

value of equity and subtracting the amount of dividends paid. To get the amount

of residual income, we multiply the cost of equity by the ending book value of

equity that we just computed. Adding the sum of the present values of the

residual income to the 2004 book value of equity will give us the current value of

the firm’s equity. Next we add in the terminal value of the perpetuity and divide

the sum by the number of shares outstanding. This method is not near as

sensitive as the discounted dividend method and the discounted free cash flow

method.

We determined that CVS has a value of $54.31, according to the residual income

valuation method. This means that the firm is reasonably valued, compared to

the current market price, which is $52.62. The sensitivity analysis below shows

that the residual income method is pretty stable; and not over-responsive to

errors in the predicted cost of equity and perpetual growth rate.

Residual Income Valuation From CVS

Sensitivity Analysis g 0.00% 1.00% 3.00% 4.00% Ke 5.00% $61.49 $68.74 $105.00 $177.52 5.50% $54.31 $59.43 $81.95 $115.72 6.00% $48.42 $52.08 $66.73 $85.04 6.50% $43.49 $46.12 $55.90 $66.65 7.00% $39.31 $43.85 $47.83 $54.62

\

49

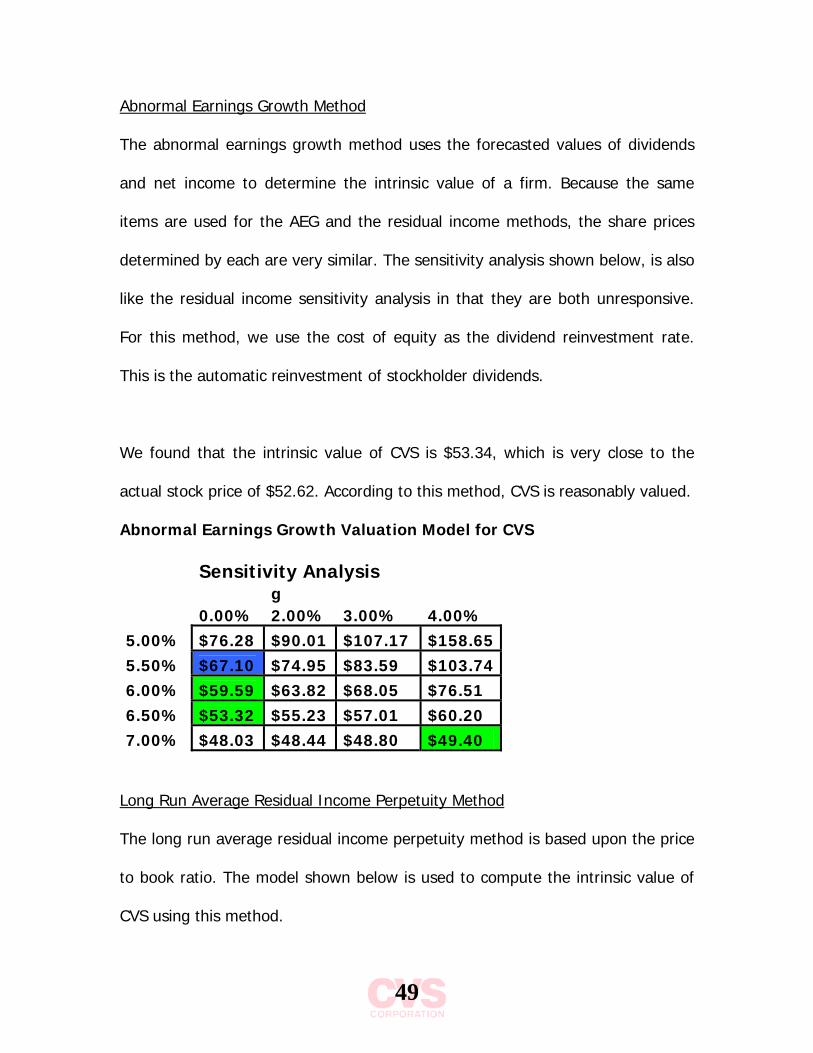

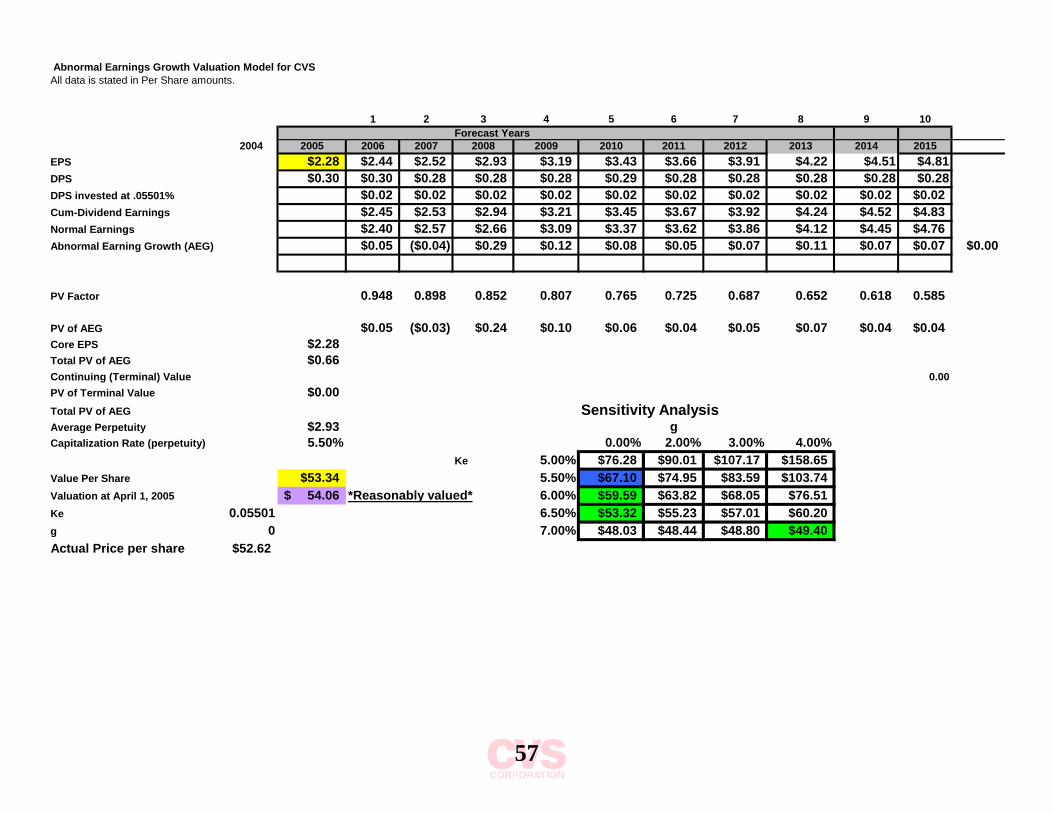

Abnormal Earnings Growth Method

The abnormal earnings growth method uses the forecasted values of dividends

and net income to determine the intrinsic value of a firm. Because the same

items are used for the AEG and the residual income methods, the share prices

determined by each are very similar. The sensitivity analysis shown below, is also

like the residual income sensitivity analysis in that they are both unresponsive.

For this method, we use the cost of equity as the dividend reinvestment rate.

This is the automatic reinvestment of stockholder dividends.

We found that the intrinsic value of CVS is $53.34, which is very close to the

actual stock price of $52.62. According to this method, CVS is reasonably valued.

Abnormal Earnings Growth Valuation Model for CVS Sensitivity Analysis g 0.00% 2.00% 3.00% 4.00% 5.00% $76.28 $90.01 $107.17 $158.65 5.50% $67.10 $74.95 $83.59 $103.74 6.00% $59.59 $63.82 $68.05 $76.51 6.50% $53.32 $55.23 $57.01 $60.20 7.00% $48.03 $48.44 $48.80 $49.40

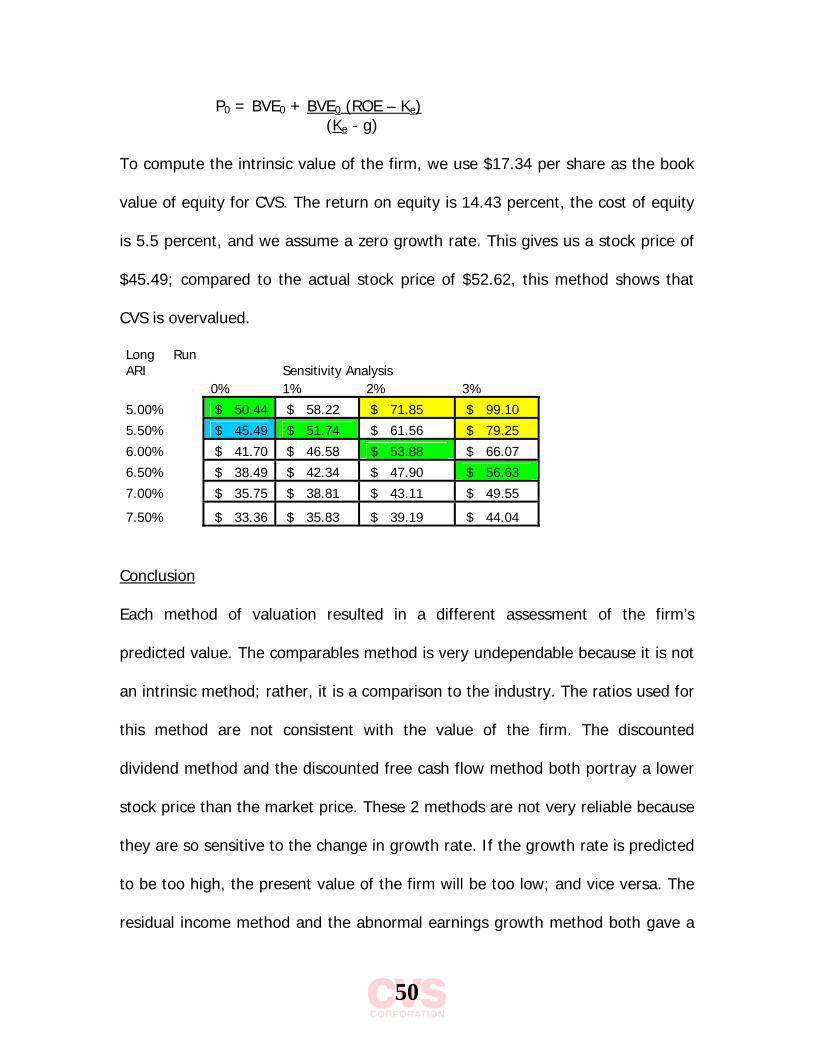

Long Run Average Residual Income Perpetuity Method

The long run average residual income perpetuity method is based upon the price

to book ratio. The model shown below is used to compute the intrinsic value of

CVS using this method.

50

P0 = BVE0 + BVE0 (ROE – Ke) (Ke - g)

To compute the intrinsic value of the firm, we use $17.34 per share as the book

value of equity for CVS. The return on equity is 14.43 percent, the cost of equity

is 5.5 percent, and we assume a zero growth rate. This gives us a stock price of

$45.49; compared to the actual stock price of $52.62, this method shows that

CVS is overvalued.

Long Run ARI Sensitivity Analysis 0% 1% 2% 3%

5.00% $ 50.44 $ 58.22 $ 71.85 $ 99.10

5.50% $ 45.49 $ 51.74 $ 61.56 $ 79.25

6.00% $ 41.70 $ 46.58 $ 53.88 $ 66.07

6.50% $ 38.49 $ 42.34 $ 47.90 $ 56.63

7.00% $ 35.75 $ 38.81 $ 43.11 $ 49.55

7.50% $ 33.36 $ 35.83 $ 39.19 $ 44.04

Conclusion

Each method of valuation resulted in a different assessment of the firm’s

predicted value. The comparables method is very undependable because it is not

an intrinsic method; rather, it is a comparison to the industry. The ratios used for

this method are not consistent with the value of the firm. The discounted

dividend method and the discounted free cash flow method both portray a lower

stock price than the market price. These 2 methods are not very reliable because

they are so sensitive to the change in growth rate. If the growth rate is predicted

to be too high, the present value of the firm will be too low; and vice versa. The

residual income method and the abnormal earnings growth method both gave a

51

very reasonable assessment of the intrinsic value of CVS. These two methods

prove to be the most reliable way to value a company because they use items

that are easy to accurately forecast. Also, the sensitivity analysis of these

methods is not very responsive to a change in the cost of capital and growth

rate. After analyzing each method of valuation, we can assume that CVS would

be a reasonable investment at its current market price.

52

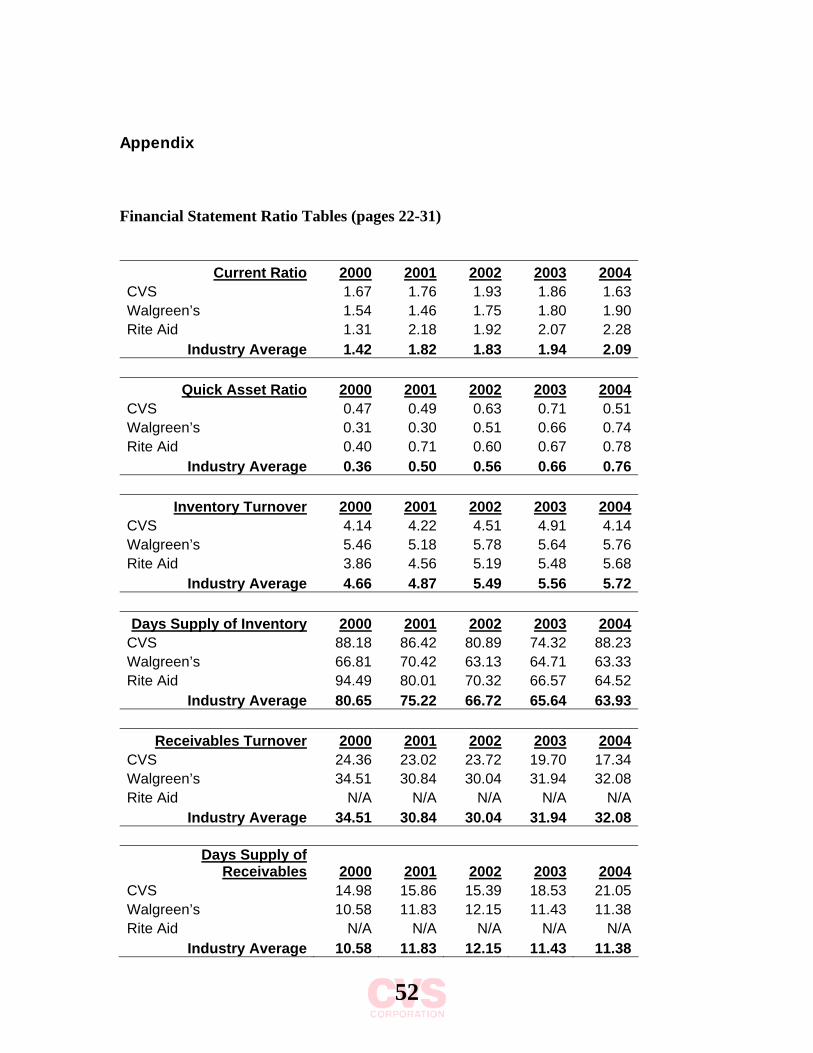

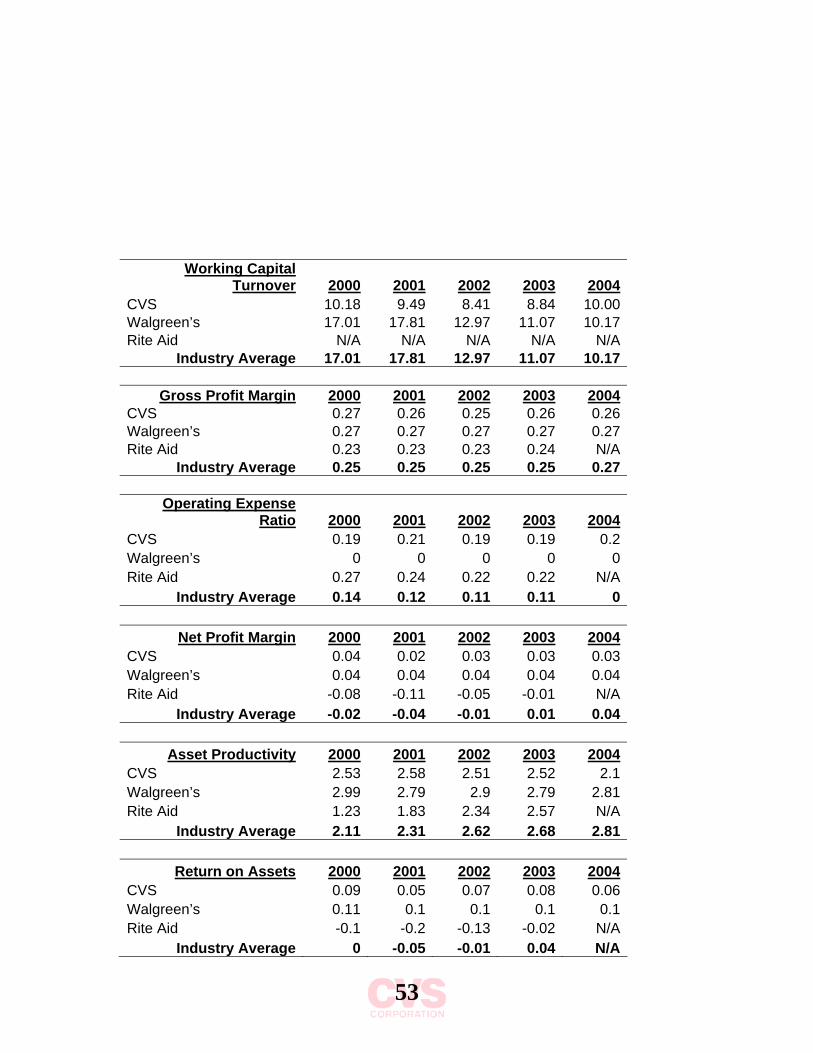

Appendix Financial Statement Ratio Tables (pages 22-31)

Current Ratio 2000 2001 2002 2003 2004 CVS 1.67 1.76 1.93 1.86 1.63 Walgreen’s 1.54 1.46 1.75 1.80 1.90 Rite Aid 1.31 2.18 1.92 2.07 2.28

Industry Average 1.42 1.82 1.83 1.94 2.09

Quick Asset Ratio 2000 2001 2002 2003 2004 CVS 0.47 0.49 0.63 0.71 0.51 Walgreen’s 0.31 0.30 0.51 0.66 0.74 Rite Aid 0.40 0.71 0.60 0.67 0.78

Industry Average 0.36 0.50 0.56 0.66 0.76

Inventory Turnover 2000 2001 2002 2003 2004 CVS 4.14 4.22 4.51 4.91 4.14 Walgreen’s 5.46 5.18 5.78 5.64 5.76 Rite Aid 3.86 4.56 5.19 5.48 5.68

Industry Average 4.66 4.87 5.49 5.56 5.72 Days Supply of Inventory 2000 2001 2002 2003 2004

CVS 88.18 86.42 80.89 74.32 88.23 Walgreen’s 66.81 70.42 63.13 64.71 63.33 Rite Aid 94.49 80.01 70.32 66.57 64.52

Industry Average 80.65 75.22 66.72 65.64 63.93

Receivables Turnover 2000 2001 2002 2003 2004 CVS 24.36 23.02 23.72 19.70 17.34 Walgreen’s 34.51 30.84 30.04 31.94 32.08 Rite Aid N/A N/A N/A N/A N/A

Industry Average 34.51 30.84 30.04 31.94 32.08

Days Supply of Receivables 2000 2001 2002 2003 2004

CVS 14.98 15.86 15.39 18.53 21.05 Walgreen’s 10.58 11.83 12.15 11.43 11.38 Rite Aid N/A N/A N/A N/A N/A

Industry Average 10.58 11.83 12.15 11.43 11.38

53

Working Capital

Turnover 2000 2001 2002 2003 2004 CVS 10.18 9.49 8.41 8.84 10.00 Walgreen’s 17.01 17.81 12.97 11.07 10.17 Rite Aid N/A N/A N/A N/A N/A

Industry Average 17.01 17.81 12.97 11.07 10.17

Gross Profit Margin 2000 2001 2002 2003 2004 CVS 0.27 0.26 0.25 0.26 0.26 Walgreen’s 0.27 0.27 0.27 0.27 0.27 Rite Aid 0.23 0.23 0.23 0.24 N/A

Industry Average 0.25 0.25 0.25 0.25 0.27

Operating Expense Ratio 2000 2001 2002 2003 2004

CVS 0.19 0.21 0.19 0.19 0.2 Walgreen’s 0 0 0 0 0 Rite Aid 0.27 0.24 0.22 0.22 N/A

Industry Average 0.14 0.12 0.11 0.11 0

Net Profit Margin 2000 2001 2002 2003 2004 CVS 0.04 0.02 0.03 0.03 0.03 Walgreen’s 0.04 0.04 0.04 0.04 0.04 Rite Aid -0.08 -0.11 -0.05 -0.01 N/A

Industry Average -0.02 -0.04 -0.01 0.01 0.04

Asset Productivity 2000 2001 2002 2003 2004 CVS 2.53 2.58 2.51 2.52 2.1 Walgreen’s 2.99 2.79 2.9 2.79 2.81 Rite Aid 1.23 1.83 2.34 2.57 N/A

Industry Average 2.11 2.31 2.62 2.68 2.81

Return on Assets 2000 2001 2002 2003 2004 CVS 0.09 0.05 0.07 0.08 0.06 Walgreen’s 0.11 0.1 0.1 0.1 0.1 Rite Aid -0.1 -0.2 -0.13 -0.02 N/A

Industry Average 0 -0.05 -0.01 0.04 N/A

54

Return on Equity 2000 2001 2002 2003 2004

CVS 0.17 0.09 0.14 0.14 0.13 Walgreen’s 0.18 0.17 0.16 0.16 0.17 Rite Aid N/A N/A N/A N/A N/A

Industry Average 0.18 0.17 0.16 0.16 N/A

Debt to Equity 2000 2001 2002 2003 2004

CVS 0.85 0.89 0.86 0.75 1.08 Walgreen’s 0.68 0.70 0.59 0.62 0.62 Rite Aid N/A (23.33) 674.10 (55.60) N/A

Industry Average N/A 0.70 0.59 0.62 0.62

Times Interest Earned 2000 2001 2002 2003 2004 CVS 20.42 17.89 30.09 36.70 24.95 Walgreen’s N/A N/A N/A N/A N/A Rite Aid -0.97 -0.07 0.12 0.86 0.86

Industry Average -0.97 -0.07 0.12 0.86 0.86

Debt Service Margin 2000 2001 2002 2003 2004 CVS 1.45 0.84 1.12 1.29 1.24 Walgreen’s N/A N/A N/A N/A N/A Rite Aid 0.00 -0.16 0.00 0.00 0.00

Industry Average 0.00 -0.16 0.00 0.00 0.00

55

Discounted Dividends Valuation For CVSnumbers in millions

Years from valuation date 1 2 3 4 5 6 7 8 9 10 Terminal2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Total Dividends $119.80 $119.66 $110.95 $112.10 $113.54 $115.21 $114.29 $113.22 $113.67 $113.99 $114.08Present Value Factor 0.948 0.898 0.852 0.807 0.765 0.725 0.687 0.652 0.618 0.585

113.42 99.68 95.47 91.65 88.15 82.89 77.83 74.06 70.4 66.78

Total Present Value of Forecast Future Dividends $860.32

Present Value of Continuing (Terminal) Value $13,328.36 $22,768.93

Estimated Total Value Per Share $35.15

Earnings $982.09 $1,014.59 $1,179.87 $1,287.31 $1,383.77 $1,474.24 $1,575.48 $1,701.00 $1,816.59 $1,938.90Dividends $119.80 $119.66 $110.95 $112.10 $113.54 $115.21 $114.29 $113.22 $113.67 $113.99 $114.08

Book Value $4.20

Number Shares Outstanding 2004 on website 403.71g

Valuation at April 1, 2005 $35.62 4.00% 4.75% 5.00% 5.25%Actual Price per share $52.62 *Over Ke 5.00% $19.53 $71.57Cost of Equity Estimated 5.50% Valued* 5.25% $15.71 $36.04 $69.91Growth rate 5.00% 5.50% $13.15 $24.16 $35.15 $68.03

5.75% $11.34 $18.26 $23.65 $34.42

Present Value of Future Dividends in 2004 $'s

Continuing (Terminal) Value (assume no growth)

Sensitivity Analysis

56

Discounted Free Cash Flows Model For CVS

CVS(Amounts in millions of dollars except per share data)

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014Cash Flow from Operations 914 1,043 1,112 1,236 1,192 1,080 1,132 1,150 1,158 1,142 1,133Cash Provided (Used) by Investing Activities -3,163 (127) (809) (893) (900) (877) (847) (877) (904) (921) -942.9741Free Cash Flow (to firm) 917 303 342 292 202 286 274 254 221 190discount rate (2.84% WACC) 0.972 0.946 0.919 0.894 0.869 0.845 0.822 0.799 0.777 0.756Present Value of Free Cash Flows 891.348 286.109 314.883 260.707 175.929 241.639 224.837 203.308 172.012 143.238Total Present Value of Annual Cash Flows 2,771Continuing (Terminal) Value (assume no growth) 22563.167Present Value of Continuing (Terminal) Value 17,052Value of the Firm (end of 2004) 19,823Book Value of Debt 7,560Value of Equity (end of 2004) 12,263Estimated Value per Share 30.38Valuation at April 1, 2005 30.59WACC 2.84%Growth 2.00%Actual Price per share $52.62

*Over Valued* Sensitivity Analysisg

2.00% 2.25% 2.50% 2.75%WACC 2.50% $59.10 $130.06

2.75% $35.45 $59.10 $130.062.84% $30.38 $48.27 $92.49 $382.373.25% $16.52 $23.62 $35.45 $59.103.50% $11.79 $16.52 $23.62 $35.45

57

Abnormal Earnings Growth Valuation Model for CVSAll data is stated in Per Share amounts.

1 2 3 4 5 6 7 8 9 10Forecast Years

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015EPS $2.28 $2.44 $2.52 $2.93 $3.19 $3.43 $3.66 $3.91 $4.22 $4.51 $4.81DPS $0.30 $0.30 $0.28 $0.28 $0.28 $0.29 $0.28 $0.28 $0.28 $0.28 $0.28DPS invested at .05501% $0.02 $0.02 $0.02 $0.02 $0.02 $0.02 $0.02 $0.02 $0.02 $0.02Cum-Dividend Earnings $2.45 $2.53 $2.94 $3.21 $3.45 $3.67 $3.92 $4.24 $4.52 $4.83Normal Earnings $2.40 $2.57 $2.66 $3.09 $3.37 $3.62 $3.86 $4.12 $4.45 $4.76Abnormal Earning Growth (AEG) $0.05 ($0.04) $0.29 $0.12 $0.08 $0.05 $0.07 $0.11 $0.07 $0.07 $0.00

PV Factor 0.948 0.898 0.852 0.807 0.765 0.725 0.687 0.652 0.618 0.585

PV of AEG $0.05 ($0.03) $0.24 $0.10 $0.06 $0.04 $0.05 $0.07 $0.04 $0.04Core EPS $2.28Total PV of AEG $0.66Continuing (Terminal) Value 0.00PV of Terminal Value $0.00Total PV of AEG Sensitivity AnalysisAverage Perpetuity $2.93 gCapitalization Rate (perpetuity) 5.50% 0.00% 2.00% 3.00% 4.00%

Ke 5.00% $76.28 $90.01 $107.17 $158.65Value Per Share $53.34 5.50% $67.10 $74.95 $83.59 $103.74Valuation at April 1, 2005 54.06$ *Reasonably valued* 6.00% $59.59 $63.82 $68.05 $76.51Ke 0.05501 6.50% $53.32 $55.23 $57.01 $60.20g 0 7.00% $48.03 $48.44 $48.80 $49.40Actual Price per share $52.62

58

Residual Income Valuation From CVS

All data is stated in Per Share amounts.1 2 3 4 5 6 7 8 9 10 11

Forecast Years2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Beginning BE (per share) 17.34 19.32 21.46 23.70 26.35 29.27 32.41 35.79 39.42 43.35 47.58Earnings Per Share $2.28 $2.44 $2.52 $2.93 $3.19 $3.43 $3.66 $3.91 $4.22 $4.51 $4.81Dividends per share $0.30 $0.30 $0.28 $0.28 $0.28 $0.29 $0.28 $0.28 $0.28 $0.28 $0.28Ending BE (per share) 17.34 19.32 21.46 23.70 26.35 29.27 32.41 35.79 39.42 43.35 47.58 52.11Ke 0.05501"Normal" Income 0.95 1.06 1.18 1.30 1.45 1.61 1.78 1.97 2.17 2.38 2.62Residual Income (RI) 1.32 1.37 1.34 1.62 1.74 1.82 1.88 1.94 2.05 2.05 2.05

Present Value of RI 1.26 1.23 1.14 1.31 1.33 1.32 1.29 1.26 1.27 1.20 1.14

BV Equity (per share) 2004 19.85Total PV of RI (end 2004) 11.42Continuation (Terminal) Value 37.31PV of Terminal Value (end 2004) 23.04 Sensitivity AnalysisEstimated Value (2004) $54.31 *Under valued* gValuation at April 1, 2005 $55.04 0.00% 1.00% 3.00% 4.00%Actual Price per share $52.62 *Under valued* Ke 5.00% $61.49 $68.74 $105.00 $177.52Growth 0 5.50% $54.31 $59.43 $81.95 $115.72

6.00% $48.42 $52.08 $66.73 $85.046.50% $43.49 $46.12 $55.90 $66.657.00% $39.31 $43.85 $47.83 $54.62

59

Actual FORECAST

CVS Income Statement In Millions 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 Net sales 20,087.50 22,241.40 24,181.50 26,588.00 30,594.30 33,347.79 36,349.09 39,620.51 43,186.35 47,073.12 50,368.24 53,894.02 57,666.60 61,703.26 66,022.49 Cost of goods sold 14,725.80 16,550.40 18,112.70 19,725.00 22,563.10 24,714.78 26,997.55 29,416.26 32,006.89 34,880.53 37,357.34 39,978.42 42,766.15 45,749.42 48,955.95 Gross margin 5,691.00 5,691.00 6,068.80 6,863.00 8,031.20 8,742.35 9,375.38 10,235.42 11,220.24 12,245.94 13,079.38 13,968.19 14,960.42 16,021.14 17,140.48 Selling, general and administrative 3,742.40 4,599.60 4,552.30 5,097.70 6,079.70 6,481.56 7,123.48 7,678.78 8,417.84 9,205.47 9,817.99 10,511.30 11,236.28 12,035.66 12,879.98 Depreciation and amortization 296.60 320.80 310.30 341.70 496.80 474.28 513.02 556.73 617.37 686.53 717.92 768.51 823.99 884.60 947.06 Total operating expenses 4,039.00 4,920.40 4,862.60 5,439.40 6,576.50 6,955.84 7,636.50 8,235.52 9,035.21 9,892.00 10,535.91 11,279.81 12,060.27 12,920.26 13,827.04 Operating profit 1,322.70 770.60 1,206.20 1,423.60 1,454.70 1,677.17 1,715.04 1,968.73 2,144.26 2,300.60 2,474.99 2,635.79 2,840.18 3,033.59 3,239.51 Interest expense, net 79.30 61.00 50.40 48.10 58.30 not predictable Earnings before income tax provision 1,243.40 709.60 1,155.80 1,375.50 1,396.40 1,593.87 1,634.79 1,885.49 2,053.38 2,198.77 2,363.43 2,519.47 2,716.29 2,900.44 3,096.34 Income tax provision 497.40 296.40 439.20 528.20 477.60 not predictable Net earnings 746.00 413.20 716.60 847.30 918.80 982.09 1,014.59 1,179.87 1,287.31 1,383.77 1,474.24 1,575.48 1,701.00 1,816.59 1,938.90 Preference dividends, net of income tax 14.60 14.70 14.80 14.60 14.20 14.58 14.58 14.58 14.58 14.58 14.58 14.58 14.58 14.58 14.58 Net earnings available to common 731.40 398.50 701.80 832.70 904.60 961.99 993.59 1,157.63 1,263.51 1,357.82 1,445.59 1,545.20 1,668.77 1,782.14 1,901.94 Basic earnings per common share: Net earnings 1.87 1.02 1.79 2.11 2.27 not predictable Weighted average common shares outstanding 391.00 392.20 392.30 394.40 398.60 not predictable Diluted earnings per common share: Net earnings 1.83 1.00 1.75 2.06 2.20 2.39 2.46 2.86 3.12 3.35 3.57 3.82 4.12 4.40 4.70 Weighted average common shares outstanding 408.00 408.30 405.30 407.70 415.40 not predictable Dividends declared per common share 0.23 0.23 0.23 0.23 0.27 not predictable Pro-Forma Income Statement Actual FORECAST 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 Net sales 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% Cost of goods sold 73.31% 74.41% 74.90% 74.19% 73.75% 74.11% 74.27% 74.25% 74.11% 74.10% 74.17% 74.18% 74.16% 74.14% 74.15% Gross margin 28.33% 25.59% 25.10% 25.81% 26.25% 26.22% 25.79% 25.83% 25.98% 26.01% 25.97% 25.92% 25.94% 25.96% 25.96% Selling, general and administrative 18.63% 20.68% 18.83% 19.17% 19.87% 19.44% 19.60% 19.38% 19.49% 19.56% 19.49% 19.50% 19.48% 19.51% 19.51% Depreciation and amortization 1.48% 1.44% 1.28% 1.29% 1.62% 1.42% 1.41% 1.41% 1.43% 1.46% 1.43% 1.43% 1.43% 1.43% 1.43% Total operating expenses 20.11% 22.12% 20.11% 20.46% 21.50% 20.86% 21.01% 20.79% 20.92% 21.01% 20.92% 20.93% 20.91% 20.94% 20.94% Operating profit 6.58% 3.46% 4.99% 5.35% 4.75% 5.03% 4.72% 4.97% 4.97% 4.89% 4.91% 4.89% 4.93% 4.92% 4.91% Interest expense, net 0.39% 0.27% 0.21% 0.18% 0.19% not predictable Earnings before income tax provision 6.19% 3.19% 4.78% 5.17% 4.56% 4.78% 4.50% 4.76% 4.75% 4.67% 4.69% 4.67% 4.71% 4.70% 4.69% Income tax provision 2.48% 1.33% 1.82% 1.99% 1.56% not predictable Net earnings 3.71% 1.86% 2.96% 3.19% 3.00% 2.94% 2.79% 2.98% 2.98% 2.94% 2.93% 2.92% 2.95% 2.94% 2.94% Preference dividends, net of income tax 0.07% 0.07% 0.06% 0.05% 0.05% 0.06% 0.06% 0.06% 0.06% 0.06% 0.06% 0.06% 0.06% 0.06% 0.06% Net earnings available to common 3.64% 1.79% 2.90% 3.13% 2.96% 2.88% 2.73% 2.92% 2.93% 2.88% 2.87% 2.87% 2.89% 2.89% 2.88% Basic earnings per common share: Net earnings 0.01% 0.00% 0.01% 0.01% 0.01% not predictable Weighted average common shares outstanding 1.95% 1.76% 1.62% 1.48% 1.30% not predictable Diluted earnings per common share: Net earnings 0.01% 0.00% 0.01% 0.01% 0.01% 0.01% 0.01% 0.01% 0.01% 0.01% 0.01% 0.01% 0.01% 0.01% 0.01% Weighted average common shares outstanding 2.03% 1.84% 1.68% 1.53% 1.36% not predictable Dividends declared per common share 0.00% 0.00% 0.00% 0.00% 0.00% not predictable

60

Actual FORECAST