Avianca Holdings Price (COP) 3,120 - investorideas.com · August 4th, 2015 Colombia, Equities...

16

August 4 th , 2015 Colombia, Equities Avianca Holdings Our BUY is unchanged on valuation but we expect a challenging environment for 2015 Company Update Rating: Buy Industry: Transport We are trimming our T.P to COP 4,100/share (USD 13.1/ADS) from COP 4,300/share (USD 16/ADS). However, our BUY rating remains unchanged; our initial BUY recommendation as of May 21 st – 2014 on Avianca has paid off as shares have declined 13.1% relative to 21.3% of the COLCAP. Valuation remains attractive and we believe that the drop in price has gone beyond what fundamentals suggest. That said, we believe that conditions will remain challenging for the remainder of 2015: an economic downturn across LatAm, currency depreciation, high leverage, and issues related to Venezuela are key risks to this name. Meanwhile, further delivery by management on deleveraging and profitability is yet to be seen. Despite the challenges, the company is our favorite choice in the sector. Our preference for Avianca relative to Latam is primarily related to its lower exposure to Brazil. Latam generates over 44% of total revenues in Brazil vs. our estimate of less than 15% for Avianca. In addition, the integration process after the merger with TAM continues to be a challenge for Latam. Avianca Holdings sold a 30% stake in LifeMiles for USD 343.7 mn. The transaction provides liquidity in the short term, while it could bring upside to the consolidated operation. Furthermore, we see an attractive investment opportunity as Avianca Holdings’ market cap reached USD 1.08 bn relative to the USD 1.145 bn valuation from LifeMiles. Currency depreciation across LatAm & reallocation of capacity from Venezuela will translate into a bumpy ride. The COP has suffered a 17.5% depreciation during 2015; other currencies in LatAm have also lost value relative to the USD. This has affected demand and yields. Meanwhile, the domestic market has not been able to fully absorb the reallocation of flights coming from Venezuela. *FV has been adjusted. The adjustment used in the industry is a multiple of 7x the annual rental expense. Stock data ADTV and Performance Source: Bloomberg, BVC, Credicorp Capital CREDICORP CAPITAL EQUITY RESEARCH Sebastián Gallego +(571) 339 4400 ext. 1594 [email protected] César Cuervo, CFA +(571) 339 4400 ext. 1012 [email protected] Credicorp Capital may do or seek to do business with companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. Refer to important disclosures on page 11 to 13. Analyst Certification on Page 11. Additional disclosures on page 13. 0 2 4 6 8 10 70 80 90 100 110 Jul-14 Nov-14 Mar-15 Jul-15 USD mn PfAvianca COLCAP Current Valuation Summary 2013 2014 2015E 2016E 2017E FV/EBITDA 9.4 12.7 11.1 9.6 7.0 FV/EBITDAR 6.3 7.9 6.8 6.1 4.9 P/E 7.2 13.9 7.2 7.1 3.7 P/BV 1.5 1.4 0.9 0.9 0.7 Div . Yield 2.0% 2.2% 6.4% 4.9% 5.0% Ticker pfav h cb / av h us Price (COP) 3,120 LTM Range (COP) 3,040 - 3,930 Target 4,100 (COP) / 13.1 (ADS) Total Return (C OP) 37.8% Market Cap (USD mn) 1,085 Shares Outstanding (mn) 997 Free Float 33.7% ADTV (USD mn) 1.2 (loc) / - 2.1 (NYSE)

Transcript of Avianca Holdings Price (COP) 3,120 - investorideas.com · August 4th, 2015 Colombia, Equities...

August 4th, 2015

Colombia, Equities

Avianca Holdings Our BUY is unchanged on valuation but we

expect a challenging environment for 2015

Company Update

Rating:

Buy

Industry:

Transport

We are trimming our T.P to COP 4,100/share (USD 13.1/ADS)

from COP 4,300/share (USD 16/ADS). However, our BUY rating

remains unchanged; our initial BUY recommendation as of May

21st – 2014 on Avianca has paid off as shares have declined

13.1% relative to 21.3% of the COLCAP. Valuation remains

attractive and we believe that the drop in price has gone

beyond what fundamentals suggest. That said, we believe that

conditions will remain challenging for the remainder of 2015:

an economic downturn across LatAm, currency depreciation,

high leverage, and issues related to Venezuela are key risks to

this name. Meanwhile, further delivery by management on

deleveraging and profitability is yet to be seen.

Despite the challenges, the company is our favorite choice

in the sector. Our preference for Avianca relative to Latam is

primarily related to its lower exposure to Brazil. Latam generates

over 44% of total revenues in Brazil vs. our estimate of less than

15% for Avianca. In addition, the integration process after the

merger with TAM continues to be a challenge for Latam.

Avianca Holdings sold a 30% stake in LifeMiles for USD

343.7 mn. The transaction provides liquidity in the short term,

while it could bring upside to the consolidated operation.

Furthermore, we see an attractive investment opportunity as

Avianca Holdings’ market cap reached USD 1.08 bn relative

to the USD 1.145 bn valuation from LifeMiles.

Currency depreciation across LatAm & reallocation of

capacity from Venezuela will translate into a bumpy ride.

The COP has suffered a 17.5% depreciation during 2015; other

currencies in LatAm have also lost value relative to the USD.

This has affected demand and yields. Meanwhile, the domestic

market has not been able to fully absorb the reallocation of

flights coming from Venezuela.

*FV has been adjusted. The adjustment used in the industry is a multiple of 7x the annual rental expense.

Stock data

ADTV and Performance

Source: Bloomberg, BVC, Credicorp Capital

CREDICORP CAPITAL EQUITY RESEARCH

Sebastián Gallego

+(571) 339 4400 ext. 1594

César Cuervo, CFA

+(571) 339 4400 ext. 1012

Credicorp Capital may do or seek to do business with companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. Refer to important disclosures on page 11 to 13. Analyst Certification on Page 11. Additional disclosures on page 13.

0

2

4

6

8

10

70

80

90

100

110

Jul-14 Nov-14 Mar-15 Jul-15U

SD

mn

PfAvianca COLCAP

Current Valuation Summary

2013 2014 2015E 2016E 2017E

FV/EBITDA 9.4 12.7 11.1 9.6 7.0

FV/EBITDAR 6.3 7.9 6.8 6.1 4.9

P/E 7.2 13.9 7.2 7.1 3.7

P/BV 1.5 1.4 0.9 0.9 0.7

Div . Yield 2.0% 2.2% 6.4% 4.9% 5.0%

Ticker pfavh cb / avh us

Price (COP) 3,120

LTM Range (COP) 3,040 - 3,930

Target 4,100 (COP) / 13.1 (ADS)

Total Return (COP) 37.8%

Market Cap (USD mn) 1,085

Shares Outstanding (mn) 997

Free Float 33.7%

ADTV (USD mn) 1.2 (loc) / - 2.1 (NYSE)

2

Avianca Holdings - Company Summary Company Description

Sector: Transport

Rating: BUY

Target Price: COP 4,100/share (13.1/ADS)

Stock Data

Ticker pfav h cb / av h us

Price (COP) 3,120

LTM Range (COP) 3,040 - 3,930

Market Cap (USD mn) 1,085

Shares Outstanding (mn) 997.0

Free Float 33.7%

ADTV (USD mn) 1.2 (loc) / - 2.1 (NYSE)

Revenue breakdown - 2014 Income statement

USD mn 2013 2014 2015E 2016E 2017E

Rev enues 4,610 4,702 4,613 4,995 5,749

EBIT 385 285 278 370 579

EBITDAR 828 784 848 945 1,178

Net Income 249 120 172 173 330

Basic EPS (USD/share) 0.27 0.12 0.17 0.17 0.33

EBIT Margin 8.4% 6.1% 6.0% 7.4% 10.1%

EBITDAR Margin 18.0% 16.7% 18.4% 18.9% 20.5%

Net Margin 5.4% 2.6% 3.7% 3.5% 5.7%

Balance Sheet

USD mn 2013 2014 2015E 2016E 2017E

Cash & Equiv alents 736 641 692 738 825

Total Current Assets 1,295 1,324 1,335 1,430 1,614

Costs breakdown - 2014 Total Assets 5,179 6,176 6,615 7,034 7,582

Current Liabilities 1,658 1,872 1,883 1,977 2,149

Financial Debt 2,265 3,171 3,162 3,172 3,182

Total liabilities 3,964 4,959 5,291 5,598 5,877

Minority interest 6.3 8.1 9.1 9.1 9.1

Shareholder's equity 1,208 1,209 1,314 1,427 1,696

Total liabilities + Equity + MI 5,179 6,176 6,615 7,034 7,582

EBITDAR / Fin. Ex penses 7.3x 5.8x 5.5x 6.2x 8.0x

Adjusted Financial Debt / EBITDAR 5.0x 6.7x 6.4x 5.9x 4.8x

Financial Debt / Equity 1.9x 2.6x 2.4x 2.2x 1.9x

ROE 20.6% 10.0% 13.1% 12.1% 19.4%

ROA 4.8% 2.0% 2.6% 2.5% 4.3%

Management ROIC 8.5% 4.3% 3.9% 4.9% 7.2%

Chairman: German Efromov ich

CEO: Fabio Villegas Cash Flow Statement

CFO: Gerardo Grajales USD mn 2013 2014 2015E 2016E 2017E

IR Manager: Andres Ruiz Initial Cash 403 736 641 692 738

w w w .av iancaholdings.com Cash from Operation 545 259 515 534 693

Cash from Inv esting -483 -244 -697 -534 -575

Changes in Financial Debt 411 905 -9 10 10

Div idends (Paid) Receiv ed -37 -39 -67 -60 -61

Other financing -286 -977 309 97 20

Changes in Equity 183 0 0 0 0

Final Cash 736 641 692 738 825

Change in Cash 333 -95 51 46 87

Sources: Company Reports, Bloomberg and Credicorp Capital; E Credicorp Capital Estimates

Source: Company reports - Credicorp Capital

Source: Company reports - Credicorp Capital

Sources: Company Reports, Bloomberg and Credicorp Capital; E

Credicorp Capital Estimates

Av ianca Holdings S.A. is a Panamanian company that represents the integrated operation of severalairlines that operate nationally and internationally, including Av ianca, Taca, among others. AviancaHoldings S.A. holds investments primarily in: passenger airlines, cargo airlines and related activ ities

including tourism, engineering, maintenance and specialized maintenanceservices.

The company generates around 80% of its operating rev enues from passengers, while the remainingoperating rev enues come from cargo, LifeMiles, and other segments.

- Market share leader

- Lifemiles: liquidity in ST and further

v alue discovery in the LT

- Rev enue diversification

- Valuation

ConcernsPositives

- Lev erage

- Economic growth in LatAm

- currency depreciation

- Redeploy ment from Venezuela

- Cash trapped

Passengers, 82.3%

Cargo & others, 17.7%

Aircraft fuel, 30.5%

Aircraft rental, 6.8%

Maintenance & repairs,

6.0%

Ground operations,

9.0%

Others, 47.7%

Avianca remains as

one of the top

airlines in LatAm.

The deal of LifeMiles

was a milestone for

Avianca.

Investment Thesis

We are trimming our T.P to COP 4,100/share (USD 13.1/ADS) from COP 4,300/share

(USD 16/ADS). However, our BUY rating is unchanged. Here, it is worth mentioning

that our initial BUY rating on Avianca was successful as shares have declined 13.1%

relative to 21.3% of the COLCAP. Valuation remains attractive and we believe that

the drop in price has gone beyond what fundamentals suggest. Furthermore, the

upcoming dividend, new synergies in terms of cost, and revenue diversification

mitigates current conditions across the industry. We warn investors that conditions

will remain challenging for the remainder of 2015: an economic downturn across

LatAm, currency depreciation, high leverage, and issues related to Venezuela are

key risks to this name. Meanwhile, further delivery by management on deleveraging

and profitability is yet to be seen. We have updated our T.P to better reflect these

conditions as we expect passenger yields to remain weak during the year, while

there are risks to the company meeting its guidance for operating margin in 2015.

Avianca’s leadership is not questioned. The company is the top airline in Colombia with

a domestic market share of roughly 60%. In addition, Avianca Holdings is a regional leader

through a multi-hub strategy based on Bogota, Lima, and San Salvador. Its market share

among intra home markets1 is currently placed at 65%, while this figure is placed at 28%

for flights between domestic markets to North America. On the other hand, Avianca is

currently flying to more than 100 destinations in 26 countries, while it is a member of the

Star Alliance group which flights to 194 countries and offers 21,900 daily flights.

Valuation2 remains attractive, while the dividend yield could support share price.

Avianca Holdings is currently trading below 8x earnings, which contrast to an average P/E

of 13.3x since April - 2013. In terms of P/B multiple, the company is trading below 1x, while

its average since April - 2013 is placed at 1.8x. Finally, Avianca is currently trading below

its average EV/EBITDAR since 2013 (6.8x vs. 7.5x). On the other hand, valuation also

remains attractive relative to peers in the region on a forward basis. In fact, Copa Holdings,

Latam, and Gol are currently trading at 8.52x, 7.6x and 7.83x on a EV/EBITDAR 2015E

basis. This contrasts with 6.83x from Avianca Holdings.

On the other hand, Avianca declared on April – 2015 a dividend payment of USD

0.06691/share, which is currently equivalent to a 6.4% dividend yield. The payment is

expected no later than the end of October 31st – 2015 while other major dividend payments

from other companies in the Colombian market have been already paid.

Cash is king - LifeMiles. The frequent flyer program of Avianca Holdings has become one

of the fastest growing segments of the company. As of today, it has nearly 6 million clients

and recorded revenues of USD 133 mn in 2014. Avianca Holdings recently announced that

it has sold a 30% stake of this segment to PE fund Advent International for USD 343.7 mn.

We consider that the transaction is positive for Avianca as it provides fresh resources that

could be used to deleverage and/or support its fleet renewal process. This is particularly

the case as adjusted debt/EBITDAR has increased over the last quarters (despite a small

decline in 1Q15) and ended 1Q15 at 6.6x. Meanwhile, the company continues to have

USD 280 mn in cash trapped in Venezuela. All in all, we estimate that new resources could

reduce adjusted debt/EBITDAR by 0.6x.

1 Colombia, Ecuador, Peru, El Salvador, Costa Rica, Nicaragua, Honduras, Guatemala, Belize, excluding Central American &

Caribbean (non-regional).

2*FV has been adjusted. The adjustment used in the industry is a multiple of 7x the annual rental expense.

3

The conversion of

common shares into

preferred shares

represents an

overhang to the

stock.

The company has lower exposure to Brazil relative to peers. The economic downturn

in Brazil has had a negative effect for airlines. For 2015, the consensus expects a

contraction of 1.6% in Brazil; the economic growth forecast for 2016 is below 1.0%. This is

particularly negative for passenger demand, especially in the corporate sector which has

been suffering in the recent quarters. Despite this ongoing situation, Avianca Holdings has

less exposure to Brazil relative to its LatAm peers. At the end of 2014, the local airline’s

passenger revenue towards South America was below 17% (Brazil by itself should be

less). This contrasts with Copa, LATAM, and Gol which at the end of last year had an

exposure to Brazil of 14.6%, 44.3%, and 88%, respectively.

Key risks to our T.P and rating on Avianca include: i) further economic downturn in

Colombia and LatAm; ii) further currency depreciation iii) higher than expected competition

iv) political instability in the region, particularly a further deterioration in Venezuela; v)

higher than expected oil prices vi) inability to successfully reallocate capacity from

Venezuela; vii) deterioration of debt metrics; viii) delay in fleet renewal delivery and ix)

significant changes in the regulatory front.

We would like to point out an additional risk which institutional investors have

expressed and it is worth mentioning: the conversion of common shares into

preferred shares by insiders. In connection with the ADS issuance, insiders converted

75.6 mn common shares into preferred shares. This represented 14.7 mn ADS, an amount

which was even higher than the 12.5 mn ADS issued by the company. Avianca Holdings

did not receive any proceeds from this conversion made by insiders, while the initial price

set for the ADS was lower than the equivalent of the company’s IPO price in Colombia

(COP 3,564.8/share vs. COP 5,000/share). Although insiders have not expressed any new

intention to convert more common shares, we believe that this has prevented investors

from being more constructive on Avianca Holdings; this overhang could continue to

interfere with the company’s fundamentals as investors remain uncertain when new

conversions could occur.

Finally, the company recently announced that Mr. Fabio Villegas, CEO of Avianca

Holdings, has resigned. Mr. Villegas will be in charge of the company until the year end,

but there is no news on the potential CEO. The news came in as a surprise for us as we

believe that Mr. Villegas has successfully led Avianca Holdings for the last 10 years. In our

view, the timing of his resignation is not the best as the company is currently engaged on a

major strategic plan to renovate the fleet and increase efficiencies. Meanwhile, the current

industry conditions remain challenging and therefore the transition for a new CEO could

delay key projects.

4

We expect the

company to use the

proceeds from

LifeMiles to

deleverage.

Compared to

Avianca, LifeMiles

has higher margins,

no debt, and

minimum CAPEX

needs.

LifeMiles provides liquidity, while it may contribute to

unlock further hidden value; delivery is yet to be seen

On July 13th – 2015, Avianca Holdings announced that it has entered into an agreement

with Advent International, where the latter will acquire 30% of LifeMiles, Avianca’s loyalty

program. Due to this transaction, the local airline expects to receive USD 343.7 mn while

retaining a 70% majority stake. (Please refer to: Advent International to acquire a 30%

stake in LifeMiles for USD 343.7 mn, released on July 14th – 2015 for further details on the

transaction). We believe that the operation was consistent with Avianca’s long term

strategy while it provides short-medium term financial flexibility given that leverage has

become an issue. We have also made a breakdown of what we consider key aspects for

Avianca and why this transaction could boost the airline’s valuation. At the same time, we

provide some pieces where we believe there is work to be done.

First, we consider that Avianca Holdings will benefit from the cash received in order to

improve liquidity and deleverage. We estimate that Adjusted debt/EBITDAR could be

reduced by 0.6x at the end of 2015 relative to 1Q15, should the company use these

proceeds to bring down debt. Here, we highlight that our estimate is consistent with the

company’s forecast. As a result, we anticipate that this indicator may be close to 6x at the

end of the year compared to 6.72x reported at the end of 2014.

Avianca’s leverage – before the LifeMiles transaction

Source: Credicorp Capital & company reports

Beyond the deleveraging process, we believe that this transaction should represent an

inflexion point regarding Avianca’s valuation. According to the transaction with Advent

International, LifeMiles is valued at USD 1.145 bn, which is equivalent to over 100% to the

whole company’s market cap. This seems particularly attractive even in the current

environment of the industry and the region. Here, we see an interesting investment

opportunity as investors are currently assigning no value to Avianca Holdings.

However, there is one case in LatAm related to the IPO of SMILES which suggest that

investors assign more value to the loyalty program relative to the airline itself. In fact, the

current market cap of SMILES is placed at USD 1.9 bn, 47.4% higher than when it began

trading; meanwhile, GOL has lost 61.2% during the same time frame. This could be the

case for LifeMiles, a business that does not demand significant CAPEX, it has no

debt, and generates operating margins close to 30% vs. single digit figure for the

airline. However, we reiterate that LifeMiles is more dependent upon the airline that the

other way around and therefore valuation on Avianca seems particularly attractive at the

moment.

5

5.53x 5.05x

6.72x 6.43x

5.91x

0.0x

1.0x

2.0x

3.0x

4.0x

5.0x

6.0x

7.0x

8.0x

2012 2013 2014 2015E 2016E

Adjusted debt/EBITDAR

Further value

creation on LifeMiles

is yet to be seen. We

estimate that the

deal was passed at

25x earnings.

Even though we believe that this transaction was positive from both a short and long term

perspective, we also reiterate that synergies and further value creation is yet to be

seen. We describe some aspects that may improve in order to boost Avianca’s value. At

the end of 2014, LifeMiles’ revenue per customer reached USD 22.5; this contrasts with

peers in the region such as Multiplus and Smiles who recorded USD 59.9/customer and

USD 32.5/customer, respectively. Higher revenue per customer could come from a faster

redemption period relative to the 10-month frame that the company currently has.

Meanwhile, Avianca needs to have a higher sustained earn-burn ratio as it is the case for

peers in LatAm. Here, we highlight that LifeMiles’ earn-burn ratio has been quite volatile

over the last quarters, ranging from 67% to 93% (average for Multiplus is above 80% on a

consistent basis).

In addition to higher revenue per customer and a more consistent earn-burn ratio, LifeMiles

will experience challenging macro conditions across the region at least for the next year.

Lower expected economic growth in Colombia and some other countries in LatAm may

harm demand. As a result, we consider that it is determinant for both Avianca and Advent

International to create key commercial partnerships as well as designing new marketing

strategies that could boost redemption of miles.

Adding value to shareholders will not be easy. However, we believe that Avianca’s new

partner, Advent International brings to the table both – key personnel and a well defined

strategic proposal. First, we believe that Advent’s operating partners and industry advisors

that have surrounded this operation are strong. This team not only includes Mr. Jorge

Londoño, former CEO of Bancolombia, but also two industry experts that have led key

projects similar to LifeMiles (JV between Aeromexico and AIMIA). Furthermore, under the

new strategic framework, both parties will look to enter new markets as well as strengthen

the commercial partnership network. Meanwhile, we believe that Advent’s ability and

expertise in non-airline retail relations could provide/lock new alliances for the loyalty

program.

Finally, we believe that further addition of value could come from new initiatives that have

been recently launched and will be tossed in the near future, so that customers could

increase redemption of mileage points. Avianca recently announced the mobile app for

LifeMiles, while the airline also enabled customers the use of the loyalty’s program card to

accumulate and redeem miles through a multichannel (Redeban) payment terminal in more

than 240 stores.

All in all, Avianca is expecting LifeMiles to continue to be the company’s crown jewel.

Although guidance has been limited, the new strategy designed for LifeMiles

includes an expected 16%-17% growth in revenues for the upcoming years, while

maintaining operating margins close to 30%. A successful delivery on both the

operating and financial figures should result in a fruitful IPO, the exit strategy (for Advent)

that we see as most likely given the cases of Smiles and Multiplus. Furthermore, a

successful exit strategy through an IPO could prove to be a new milestone towards

Avianca’s valuation as we estimate that the deal with Advent was closed at near 25x

earnings (based on 2014 figures). In any case, we expect Avianca to maintain the

control of Lifemiles in line with the company’s comments.

6

The macro

environment across

LatAm has

deteriorated.

What has changed?

The decision made in 1Q14 to redeploy the vast majority of flying capacity to/from

Venezuela brought a whole new picture for Avianca Holdings. Here, we expected a milder

effect given a different demand environment across the markets where Avianca Holdings

operates. That said, the economic downturn both in Colombia and LatAm along with higher

than expected currency depreciation across the continent presents a challenging

environment for the local airline for the remainder of 2015 and 2016.

Given the difficult economic situation and the political instability in Venezuela along with the

USD 280 mn trapped, Avianca Holdings decided to cut the frequency of flights to this

country from 7 to 2 daily roundtrips. Under the new strategy, the local airline reallocated

this capacity mostly to the domestic market in Colombia. However, the decline in oil prices

that started in mid 2014 has caused a major recoil of the local economy (we have adjusted

our GDP growth forecast for both 2015 and 2016 to 3.7% and 3% from 4.7%, respectively).

This has hurt demand in the domestic market, which has been unable to fully absorb the

capacity coming from Venezuela. The negative sentiment towards the local economy has

also caused a sharp depreciation of the COP relative to the USD (over 15% in 2015). In

addition to the internal shocks, the LatAm region has been suffering an economic

downturn. The consensus anticipates a negative growth of 0.2% for the region in 2015, led

by a negative economic growth of 1.4% in Brazil. Given this scenario, we expect a negative

effect on passenger demand, yields, and profitability for Avianca Holdings.

Due to the these effects, we anticipate for Avianca that growth in consolidated ASKs will be

in the higher range of the company’s guidance for 2015, at 6.8%. This will be driven by a

double digit growth in the domestic market. Meanwhile, the reallocation of flights from

Venezuela will harm the domestic load factors even below 75% as it has been the case for

1H15; however, we expect the consolidated figure to be slightly below 80% which is still

healthy given the challenging environment. On the other hand, the currency depreciation

across LatAm and lower economic growth will continue to harm consolidated passenger

yields as we expect negative growth in this indicator for the remainder of 2015. All in all,

we expect a 6% EBIT margin for 2015, which is below the company’s guidance of

8%-10%. At the same time, we estimate the company’s ROIC for 2015 to be the

lowest since 2012, and lower than the WACC (3.91% vs 8.04%). Going forward, we

expect a recovery; however, it is too early and we prefer to be conservative ahead of 2016.

Load factor and Avianca Holdings’ key profitability indicators

Source: Credicorp Capital & company reports

7

80.4%

79.4%

78.6%

78.0%

80.0%

76.5%

77.0%

77.5%

78.0%

78.5%

79.0%

79.5%

80.0%

80.5%

81.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

2013 2014 2015E 2016E 2017E

Lo

ad facto

r (on

ly)

Load factor EBIT Margin ROIC

Change in financial estimates

Source: Credicorp Capital & company reports

Valuation

Our valuation model is based on a 10 year - DCF model, which assumes a 6% and 7.6%

CAGR on revenues and EBITDAR (2015 – 2024 period), respectively. Despite our forecast

of 6% in terms of EBIT margin for 2015, we anticipate that the company will be able to

achieve an operating margin between 10%-11% in the long term. This is supported by

further synergies coming from the merger with TACA, the fleet renewal plan, and the new

initiatives to cut operating costs. Currently, the local airline is engaged in a fleet renewal

process that includes an optimization of aircraft families from 9 to 4. By doing so, Avianca

expects to increase fuel efficiency (A320 neos consume 15% less fuel), reduce training

cost, and decrease maintenance related expenses.

On the other hand, according to our DCF and the investment plan of the company, we

anticipate that the company will not generate FCF to the firm during 2015 and 2016, while

we expect a gradual recovery going forward. Finally, it is worth mentioning that the

proceeds from LifeMiles have been included in addition to the current cash position, while

we have included only 80% of the USD 280 mn trapped, to somehow incorporate this risk.

We reiterate our T.P of COP 4,100/share (USD 13.1/ADS). Here, it is worth mentioning that

our T.P derived in COP is based on an exchange rate of COPUSD 2,500 for 2015.

In terms of our WACC, we have followed our in-house methodology for key inputs such as

risk free rate, country risk, and market premium. Meanwhile, we have used a leveraged

beta of 1.89. Meanwhile, the cost of debt of Avianca remains low at nearly 4.3% before

taxes. All in all, our WACC for Avianca is placed at 8.04% in USD terms.

Avianca Holdings base case valuation

Source: Credicorp Capital & company reports

8

Avianca Holdings

USD mn Update Prior Diff Update Prior Diff

Income statement

Rev enues 4,613 5,175 -10.9% 4,995 5,608 -10.9%

EBITDAR 848 1,167 -27.3% 945 1,203 -21.5%

Net income 172 369 -53.3% 173 509 -66.0%

EPS (COP) 0.2 0.4 -53.3% 0.2 0.5 -66.0%

2015E 2016E

Risk free rate 2.22% Cash & equiv alents 788

Risk Premium 6.00% Inv estments 0

Lev ered Beta 1.89 Financial debt -3,210

Country Risk Premium 3.44% Others -206

Cost of Equity (USD) 20.04% Minority Interest -9

WACC 8.04% Equity value 1,637

EBITDAR ex it multiple 4x Shares outstanding (mn) 997

PV from DCF (USD mn) 903

PV from perpetuity (USD mn) 3,372

T.P 2015E (USD/share) 13.14

PV total (USD mn) 4,275 T.P 2015E (COP/share) 4,105

Relative valuation

Our target price set at COP 4,100 (USD 13.1/ADS) implies an EV/EBITDAR 2015E of 7.5x.

This multiple remains conservative relative to other peers in Latam. That said, we believe

that Avianca should still trade below a company such as Copa Holdings as this company

has higher operating margins and lower leverage.

Share price performance across the industry in LatAm has been weak on a YTD basis and

we do not anticipate a significant re-rating before the year end. That said, we highlight that

Avianca has outperform its LatAm’s peers, while it still remains negative on a USD

adjusted basis. Once again, we reiterate that in terms of our regional strategy we

prefer Avianca vs. Latam Group given a lower exposure to Brazil.

Finally, a re-rating for Avianca and across the industry could come from any improvements

on the macro front, which seems challenging at least for 2015. Meanwhile, any successful

strategy of Avianca to redeploy capacity from Venezuela and higher than expected growth

on passenger revenues should be positive for shares of Avianca Holdings.

Avianca Holdings – relative valuation across LatAm

Source: Credicorp Capital & Company Reports

** Consensus anticipates a net loss for GOL, but we have placed at 60x for illustration purposes

9

Market Cap EBIT Mg. EBITDAR Mg.

Company USD mn 2015E 2016E 2015E 2016E 2015E 2015E

LatAm

Av ianca Holdings 1,085 7.2x 7.1x 6.8x 6.1x 6.0% 18.4%

Latam Airlines 3,447 40.2x 17.9x 7.6x 7.2x 6.2% 19.1%

Gol 471 NM NM 7.8x 6.4x 3.0% 16.7%

Copa Holdings 3,322 10.2x 8.6x 8.5x 7.1x 12.7% 23.5%

Latam Average 2,081 19.2x 11.2x 7.7x 6.7x 7.0% 19.4%

North America

American Airlines 26,940 4.5x 6.8x 4.5x 4.2x 16.7% 24%

United Continental 21,302 5.5x 8.3x 4.5x 4.3x 12.8% 20%

Delta Airlines 35,268 9.9x 8.7x 5.0x 4.6x 15.7% 21%

North America average 27,837 6.6x 7.9x 4.7x 4.3x 15.1% 21.5%

Consolidated average 14,959 12.9x 9.6x 6.2x 5.5x 11.0% 20.5%

P/E FV/EBITDAR

Latam

GOL**

Copa Holdings

Avianca

-10.0x

0.0x

10.0x

20.0x

30.0x

40.0x

50.0x

60.0x

70.0x

5.0x 6.0x 7.0x 8.0x 9.0x 10.0x

P/E

201

5E

EV/EBITDAR 2015E

Financial Statements

10

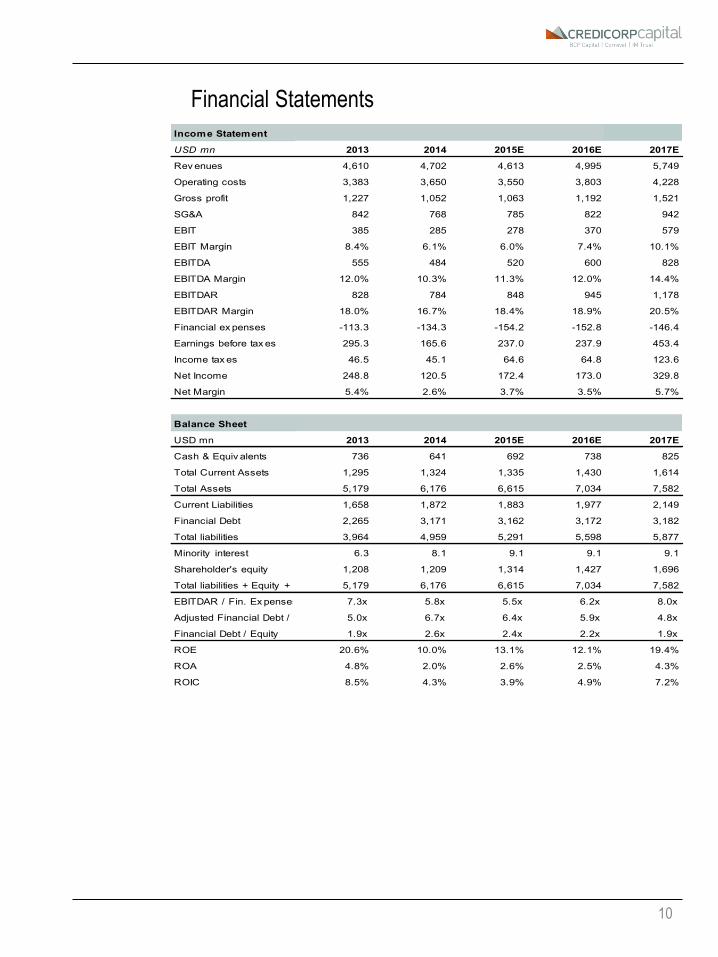

Income Statement

USD mn 2013 2014 2015E 2016E 2017E

Rev enues 4,610 4,702 4,613 4,995 5,749

Operating costs 3,383 3,650 3,550 3,803 4,228

Gross profit 1,227 1,052 1,063 1,192 1,521

SG&A 842 768 785 822 942

EBIT 385 285 278 370 579

EBIT Margin 8.4% 6.1% 6.0% 7.4% 10.1%

EBITDA 555 484 520 600 828

EBITDA Margin 12.0% 10.3% 11.3% 12.0% 14.4%

EBITDAR 828 784 848 945 1,178

EBITDAR Margin 18.0% 16.7% 18.4% 18.9% 20.5%

Financial ex penses -113.3 -134.3 -154.2 -152.8 -146.4

Earnings before tax es 295.3 165.6 237.0 237.9 453.4

Income tax es 46.5 45.1 64.6 64.8 123.6

Net Income 248.8 120.5 172.4 173.0 329.8

Net Margin 5.4% 2.6% 3.7% 3.5% 5.7%

Balance Sheet

USD mn 2013 2014 2015E 2016E 2017E

Cash & Equiv alents 736 641 692 738 825

Total Current Assets 1,295 1,324 1,335 1,430 1,614

Total Assets 5,179 6,176 6,615 7,034 7,582

Current Liabilities 1,658 1,872 1,883 1,977 2,149

Financial Debt 2,265 3,171 3,162 3,172 3,182

Total liabilities 3,964 4,959 5,291 5,598 5,877

Minority interest 6.3 8.1 9.1 9.1 9.1

Shareholder's equity 1,208 1,209 1,314 1,427 1,696

Total liabilities + Equity + Min int. 5,179 6,176 6,615 7,034 7,582

EBITDAR / Fin. Ex penses 7.3x 5.8x 5.5x 6.2x 8.0x

Adjusted Financial Debt / EBITDAR 5.0x 6.7x 6.4x 5.9x 4.8x

Financial Debt / Equity 1.9x 2.6x 2.4x 2.2x 1.9x

ROE 20.6% 10.0% 13.1% 12.1% 19.4%

ROA 4.8% 2.0% 2.6% 2.5% 4.3%

ROIC 8.5% 4.3% 3.9% 4.9% 7.2%

11

Important Disclosures This research report was prepared by CredicorpCapital Peru S.A and/or Credicorp Capital Colombia Sociedad Comisionista de

Bolsa and/or IM Trust S.A. Corredores de Bolsa, companies authorized to engage in securities activities in Peru, Colombia and

Chile, respectively and indirect subsidiaries of Credicorp Capital Ltd. (jointly referred to as “Credicorp Capital”). None of the

companies jointly referred to as Credicorp Capital are registered as broker-dealers in the United States and, therefore, they are not

subject to U.S. rules regarding the preparation of research reports and the independence of research analysts. This research report

is provided for distribution only to “major U.S. institutional investors” in reliance on the exemption from registration provided by Rule

15a-6 of the U.S. Securities Exchange Act of 1934, as amended (the “Exchange Act”).

Any U.S. recipient of this research report wishing to effect any transaction to buy or sell securities or related financial instruments

based on the information provided in this research report can do so only through Credicorp Securities Inc., a registered broker-

dealer in the United States. Under no circumstances may a U.S. recipient of this research report effect any transaction to buy or sell

securities or related financial instruments directly through Credicorp Capital.

Credicorp Securities Inc. accepts responsibility for the contents of this research report, subject to the terms set out below, to the

extent that it is delivered to a U.S. person other than a major U.S. institutional investor.

Any analyst whose name appears on this research report is not registered or qualified as a research analyst with the Financial

Industry Regulatory Authority (“FINRA”) and is not a registered representative of Credicorp Securities Inc. and, therefore, is not

subject to applicable restrictions under FINRA Rules on communications with a subject company, public appearances and trading

securities held by a research analyst account.

A.Analyst Disclosures

The functional job title of the person(s) responsible for the recommendations contained in this report is Equity Research Analyst

unless otherwise stated on the cover.

Regulation AC - Analyst Certification: Each Equity Research Analyst listed on the front-page of this report is principally

responsible for the preparation and content of all or any identified portion of this research report and hereby certifies thatwith

respect to each issuer or security or any identified portion of the report with respect to an issuer or security that the Equity Research

Analyst covers in this research report, all of the views expressed in this research report accurately reflect their personal views about

those issuer(s) or securities. Each Equity Research Analyst also certifies that no part of their compensation was, is, or will be,

directly or indirectly, related to the specific recommendation(s) or view(s) expressed by that Equity Research Analyst in this research

report.

Each Equity Research Analyst certifies that he or she is acting independently and impartially from the referenced

company/shareholders, directors and is not affected by any current or potential conflict of interest that may arise from any of the

companies’ activities.

Analyst Compensation: The research analyst(s) primarily responsible for the preparation of the content of this research report

attest(s) that no part of his or her compensation was, is or will be, directly or indirectly, related to the specific recommendations that

he or she expressed in the research report.

Registration of non-US Analysts: Unless otherwise noted, the non-US analysts listed on the front of this report are employees of

one of the companies jointly referred as Credicorp Capital, which are non-US affiliates of Credicorp Securities Inc., a SEC registered

and FINRA member broker-dealer. Equity Research Analysts employed by the companies jointly referred as Credicorp Capital, are

not registered/ qualified as research analysts under FINRA/NYSE rules, are not registered representatives of CredicorpSecurities

Inc. and may not be subject to NASD Rule 2711 and NYSE Rule 472 restrictions on communications with covered companies, public

appearances, and trading securities held by a research analyst account. Please refer to www.credicorpcapital.com for further

information relating to research and conflict of interest management.

12

B.Ownership and Material Conflicts of Interest

Neither Credicorp Securities Inc. or its affiliates ‘beneficially own’, as determined in accordance with Section 13(d) of the Exchange

Act, 1% or more of the equity securities of the company referenced in this report. Credicorp Securities Inc., its affiliates and/or their

respective officers, directors or employees may have interests, or long or short positions, and may at any time make purchases or

sales as a principal or agent of the securities referred to herein.

C.Compensation and Investment Banking Activities

Neither Credicorp Securities Inc. or any of its affiliates have managed or co-managed a public offering of securities for the subject

company in the past 12 months. Neither Credicorp Securities Inc. or its affiliates have received compensation for investment banking

services from the subject company in the past 12 months. Neither Credicorp Securities Inc. or its affiliates do expect to receive or

intend to seek compensation for investment banking services from the subject company in the next 3 months.

D. Rating System

Stock ratings are based on the analyst’s expectation of the stock’s total return during the twelve to eighteen months following

assignment of the rating. This view is based on the target price, set as described below, and on the analyst’s opinion, general market

conditions and economic developments.

Buy: Expected returns of 5 percentage points or more in excess over the expected return of the local index, over the next 12-18

months.

Hold: Expected returns of +/- 5% in excess/below the expected return of the local index over the next 12-18 months.

Underperform: Expected to underperform the local index by 5 percentage points or more over the next 12-18 months.

Under Review / Restricted: Company coverage is under review or restricted.

The IPSA, COLCAP and IGBVL indexes are the selective equity indexes calculated by the Bolsa de Comercio de Santiago, the

Bolsa de Valores de Colombia, and the Bolsa de Valores de Lima, respectively.

In making a recommendation, the analyst compares the target price with the actual share price, and compares the resulting

expected return for the IPSA, the COLCAP, and/or the IGBVL indexes, as estimated by IM Trust Corredores de Bolsa S.A.,

Credicorp Capital Colombia Sociedad Comisionista de Bolsa, and/or CredicorpCapital Peru S.A, and then makes a recommendation

derived from the difference in upside potential between the shares and the respective index.

E. Distribution of Ratings

Rating

N° of Companies covered with this

rating

Companies covered with this

rating (% )

Buy 29 35%

Hold 44 53%

Underperform 8 10%

Under Review 2 2%

Total 83 100%

13

F.Price Target

Unless otherwise stated in the text of this report, target prices in this report are based on either a discounted cash flow valuation or

comparison of valuation ratios with companies seen by the analyst as comparable or a combination of the two methods. The result of

this fundamental valuation is adjusted to reflect the analyst’s views on the likely course of investor sentiment. Whichever valuation

method is used there is a significant risk that the target price will not be achieved within the expected timeframe. Risk factors include

unforeseen changes in competitive pressures or in the level of demand for the company’s products. Such demand variations may

result from changes in technology, in the overall level of economic activity or, in some cases, in fashion. Valuations may also be

affected by changes in taxation, in exchange rates and, in certain industries, in regulations. Investment in overseas markets and

instruments such as ADRs can result in increased risk from factors such as exchange rates, exchange controls, taxation, and

political and social conditions. This discussion of valuation methods and risk factors is not comprehensive – further information is

available upon request.

II.ADDITIONAL DISCLOSURES

This product is not for retail clients or private individuals.

The information contained in this publication was obtained from various publicly available sources believed to be reliable, but has not

been independently verified by the companies jointly referred as Credicorp Capital, therefore they do not warrant the completeness

or accuracy of such information and does not accept any liability with respect to the accuracy or completeness of such information,

except to the extent required by applicable law.

This publication is a brief summary and does not purport to contain all available information on the subjects covered. Further

information may be available on request. This report may not be reproduced for further publication unless the source is quoted. This

publication is for information purposes only and shall not be construed as an offer or solicitation for the subscription or purchase or

sale of any securities, or as an invitation, inducement or intermediation for the sale, subscription or purchase of any securities, or for

engaging in any other transaction. This publication is not for private individuals.

Any opinions, projections, forecasts or estimates in this report are those of the author only, who has acted with a high degree of

expertise. They reflect only the current views of the author at the date of this report and are subject to change without notice. The

companies jointly referred to as Credicorp Capital have no obligation to update, modify or amend this publication or to otherwise

notify a reader or recipient of this publication in the event that any matter, opinion, projection, forecast or estimate contained herein,

changes or subsequently becomes inaccurate, or if research on the subject company is withdrawn. The analysis, opinions,

projections, forecasts and estimates expressed in this report were in no way affected or influenced by the issuer. The author of this

publication benefits financially from the overall success of Credicorp Capital.

The investments referred to in this publication may not be suitable for all recipients. Recipients are urged to base their investment

decisions upon their own appropriate investigations that they deem necessary. Any loss or other consequence arising from the use

of the material contained in this publication shall be the sole and exclusive responsibility of the investor and Credicorp Capital

accepts no liability for any such loss or consequence. In the event of any doubt about any investment, recipients should contact their

own investment, legal and/or tax advisers to seek advice regarding the appropriateness of investing. Some of the investments

mentioned in this publication may not be readily liquid investments. Consequently it may be difficult to sell or realize such

investments. The past is not necessarily a guide to future performance of an investment. The value of investments and the income

derived from them may fall as well as rise and investors may not get back the amount invested. Some investments discussed in this

publication may have a high level of volatility. High volatility investments may experience sudden and large falls in their value which

may cause losses. International investing includes risks related to political and economic uncertainties of foreign countries, as well

as currency risk.

14

To the extent permitted by applicable law, no liability whatsoever is accepted for any direct or consequential loss, damages, costs or

prejudices whatsoever arising from the use of this publication or its contents.

Credicorp Capital (and its affiliates) has implemented written procedures designed to identify and manage potential conflicts of

interest that arise in connection with its research business, which are available upon request. The Credicorp Capital research

analysts and other staff involved in issuing and disseminating research reports operate independently of Credicorp Capital’s

Investment Banking business. Information barriers and procedures are in place between the research analysts and staff involved in

securities trading for the account of Credicorp Capital or clients to ensure that price sensitive information is handled according to

applicable laws and regulations.

Country and region disclosures

United Kingdom: This document is for persons who are Eligible Counterparties or Professional Clients only and is exempt from the

general restriction in section 21 of the Financial Services and Markets Act 2000 on the communication of invitations or inducements

to engage in investment activity on the grounds that it is being distributed in the United Kingdom only to persons of a kind described

in Articles 19(5) (Investment professionals) and 49(2) (High net worth companies, unincorporated associations, etc.) of the Financial

Services and Markets Act 2000 (Financial Promotion) Order 2005 (as amended). It is not intended to be distributed or passed on,

directly or indirectly, to any other class of persons. Any investment to which this document relates is available only to such persons

and other classes of person should not rely on this document.

United States: This communication is only intended for, and will only be distributed to, persons residing in any jurisdictions where

such distribution or availability would not be contrary to local law or regulation. This communication must not be acted upon or relied

on by persons in any jurisdiction other than in accordance with local law or regulation and where such person is an investment

professional with the requisite sophistication to understand an investment in such securities of the type communicated and assume

the risks associated therewith.

This communication is confidential and is intended solely for the addressee. It is not to be forwarded to any other person or copied

without the permission of the sender. This communication is provided for information only. It is not a personal recommendation or an

offer to sell or a solicitation to buy the securities mentioned. Investors should obtain independent professional advice before making

an investment.

Notice to U.S. Investors: This material is not for distribution in the United States, except to “major US institutional investors” as

defined in SEC Rule 15a-6 ("Rule 15a-6") and related guidance. Credicorp Capital and its affiliates has entered into arrangements

with Credicorp Securities Inc., which enables this report to be furnished to certain U.S. recipients in reliance on Rule 15a-6 through

Credicorp Securities Inc., which is registered under the U.S. Securities Exchange Act of 1934, as amended.

Each U.S. recipient of this report represents and agrees, by virtue of its acceptance thereof, that it is a "major U.S. institutional

investor" (as such term is defined in Rule 15a-6) and that it understands the risks involved in executing transactions in such

securities. Any U.S. recipient of this report that wishes to discuss or receive additional information regarding any security or issuer

mentioned herein, or engages in any transaction to purchase or sell or solicit or offer the purchase or sale of such securities, should

contact a registered representative of the Credicorp Securities Inc. that provided the report.

Credicorp Securities Inc. is a broker-dealer registered with the SEC, a member of FINRA and SIPC. You can reach Credicorp

Securities Inc. At 121 Alhambra Plaza, suite 1200, Coral Gables, Miami 33134, phone (305) 4480971 Equity trading: 786 999 1633.

You may obtain information about SIPC, including the SIPC brochure, by contacting SIPC directly at 202-371-8300; website:

http://www.sipc.org

15

Credicorp Securities Inc., is a wholly owned subsidiary of Credicorp Capital Ltd.

Nothing herein excludes or restricts any duty or liability to a customer that Credicorp Securities Inc. have under applicable law.

Investment products provided by or through Credicorp Securities Inc. are not insured by the Federal Deposit Insurance Corporation

and are not deposits or other obligations of any insured depository institution, may lose value and are not guaranteed by the entity

that published the research as disclosed on the front page and are not guaranteed by Credicorp Securities Inc.

Investing in non-U.S. Securities may entail certain risks. The securities referred to in this report and non-U.S. issuers may not be

registered under the U.S. Securities Act of 1933, as amended, and the issuer of such securities may not be subject to U.S. reporting

and/or other requirements. Rule 144A securities may be offered or sold only to persons in the U.S. who are Qualified Institutional

Buyers within the meaning of Rule 144A under the Securities Act. The information available about non-U.S. companies may be

limited, and non-U.S. companies are generally not subject to the same uniform auditing and reporting standards as U.S. companies.

Securities of some non-U.S. companies may not be as liquid as securities of comparable U.S. companies. Securities discussed

herein may be rated below investment grade and should therefore only be considered for inclusion in accounts qualified for

speculative investment.

Analysts employed by one of the companies jointly referred to as Credicorp Capital, all of which are non-U.S. broker-dealers, are not

required to take the FINRA analyst exam. The information contained in this report is intended solely for certain "major U.S.

institutional investors" and may not be used or relied upon by any other person for any purpose. Such information is provided for

informational purposes only and does not constitute a solicitation to buy or an offer to sell any securities under the Securities Act of

1933, as amended, or under any other U.S. federal or state securities laws, rules or regulations. The investment opportunities

discussed in this report may be unsuitable for certain investors depending on their specific investment objectives, risk tolerance and

financial position.

In jurisdictions where Credicorp Securities Inc. is not registered or licensed to trade in securities, or other financial products,

transactions may be executed only in accordance with applicable law and legislation, which may vary from jurisdiction to jurisdiction

and which may require that a transaction be made in accordance with applicable exemptions from registration or licensing

requirements.

The information in this publication is based on sources believed to be reliable, but Credicorp Securities Inc. does not make any

representation with respect to its completeness or accuracy. All opinions expressed herein reflect the author's judgment at the

original time of publication, without regard to the date on which you may receive such information, and are subject to change without

notice.

Credicorp Securities Inc. or its affiliates may have issued other reports that are inconsistent with, and reach different conclusions

from, the information presented in this report. These publications reflect the different assumptions, views and analytical methods of

the analysts who prepared them. Past performance should not be taken as an indication or guarantee of future performance, and no

representation or warranty, express or implied, is provided in relation to future performance.

Credicorp Securities Inc. and any company affiliated with it may, with respect to any securities discussed herein: (a) take a long or

short position and buy or sell such securities; (b) act as investment and/or commercial bankers for issuers of such securities; (c) act

as market makers for such securities; (d) serve on the board of any issuer of such securities; and (e) act as paid consultant or

advisor to any issuer. The information contained herein may include forward-looking statements within the meaning of U.S. federal

securities laws that are subject to risks and uncertainties. Factors that could cause a company's actual results and financial condition

to differ from expectations include, without limitation: political uncertainty, changes in general economic conditions that adversely

affect the level of demand for the company's products or services, changes in foreign exchange markets, changes in international

and domestic financial markets and in the competitive environment, and other factors relating to the foregoing. All forward-looking

statements contained in this report are qualified in their entirety by this cautionary statement.

Other countries: Laws and regulations of other countries may also restrict the distribution of this report. Persons in possession of

this document should inform themselves about possible legal restrictions and observe them accordingly.

16

Hugo Horta

Director of Sales & Trading

CHILE COLOMBIA PERU Hernán Arellano

Head of Equities

Carolina Ratto Mallie César Cuervo Héctor Collantes [email protected]

Head of Equity Research - Retail Head of North Andean Equity Research Head of Equity Research

[email protected] [email protected] [email protected]

# (562) 2446 1768 # (571) 339 4400 Ext 1012 # (511) 416 3333 Ext 33052 Javier Günther Marilyn Macdonald Cristián Castillo

International Equity Sales International Equity Sales International Sales Trader

Arturo Prado Jaime Pedroza Iván Bogarín [email protected] [email protected] [email protected]

Senior Analyst: Natural Resources Senior Analyst: Utilities Senior Analyst: Utilities, Consumer & Others # (562) 2450 1695 # (4477) 7151 5855 # (786) 999 1633

[email protected] [email protected] [email protected]

# (562) 2450 1688 # (571) 339 4400 Ext 1025 # (511) 416 3333 Ext 33055 Christopher DiSalvatore

Institutional Sales

Andrés Ossa Juan C. Domínguez Jasmine Helme [email protected]

Analyst: Utilities, Telecom & I.T. Senior Analyst: Banks Senior Analyst: Mining & Infrastructure # (786) 999 1236

[email protected] [email protected] [email protected]

# (562) 2651 9332 # (571) 339 4400 Ext 1026 # (511) 416 3333 Ext 36065 CHILE PERU COLOMBIA

Tomás Sanhueza Sebastián Gallego Tamara Vasquez René Ossa Rodrigo Zavala Juan A. Jiménez

Analyst: Oil & Gas Research Assistant International Equity Sales Head of Equity - Peru Head of International Equity Sales

[email protected] [email protected] [email protected] [email protected] [email protected]

[email protected] # (571) 339 4400 Ext 1594 # (511) 416 3333 Ext 37946 # (562) 2651 9324 # (511) 313 2918 Ext 36044 # (571) 339 4400 Ext 1701

# (562) 2446 1751

Carlos E. Rodriguez Christian Munchmeyer Ursula Mitterhofer Santiago Castro

Andrés Cereceda Analyst: GEA & infrastructure International Sales & Trading Sales & Trading International Sales & Trading

Analyst [email protected] [email protected] [email protected] [email protected]

[email protected] # (571) 339 4400 Ext 1365 # (562) 2450 1613 # (511) 313 2918 Ext 32922 # (571) 339 4400 Ext 1344

# (562) 2446 1798

Lourdes Alamos

Research Coordinator & Holdings Analyst

[email protected] Felipe García

# (562) 2450 1609 Head of Fixed Income

Christian Jarrin

Fixed Income RM

CHILE COLOMBIA PERU # (786) 999 1616

Paulina Yazigi Daniel Velandia Irvin León CHILE COLOMBIA PERU

Head of Research & Chief Economist Head of Research & Chief Economist Senior Fixed Income Analyst

[email protected] [email protected] [email protected] Gonzalo Covarrubias Carlos Sanchez Alfredo Bejar

# (562) 2450 1637 # (571) 339 4400 Ext 1505 # (511) 416 3333 Ext 37854 Head of Capital Markets Head of Fixed Income Head of Fixed Income / FX

[email protected] [email protected] [email protected]

Felipe Lubiano Sergio Ferro Alberto Zapata # (562) 2450 1635 # (571) 323 9154 # (511) 205 9190 Ext 36148

Senior Fixed Income Analyst Fixed Income Analyst Fixed Income Analyst

[email protected] [email protected] [email protected] Guido Riquelme Camilo Moreno Evangeline Arapoglou

# (562) 2651 9308 # (571) 339 4400 Ext 1609 # (511) 416 3333 Ext 36018 Head of Sales Head of Sales Head of international FI Sales

[email protected] [email protected] [email protected]

Paulina Valdivieso Camilo A. Durán Catalina Luna # (562) 2446 1712 # (571) 323 9252 # (511) 313 2902 - # (511) 313 2908

Fixed Income Analyst Macro Analyst Research Assistant

[email protected] [email protected] [email protected] Belén Larraín Andrés Valderrama Tatiana Dasso

# (562) 2651 9337 # (5511) 339 4400 Ext. 1383 # (511) 416 3333 Ext 40332 Head of International FI Sales Fixed Income Trader Fixed Income Sales

[email protected] [email protected] [email protected]

Andrés Osorio # (562) 2446 1720 # (571) 323 9163 # (511) 313 2902

Economist

[email protected] Paz Stepke José Andrés Riveros Santiago de Aubeyzon

# (562) 2446 1760 International Fixed Income Sales Fixed Income Trader Fixed Income Sales

[email protected] [email protected] [email protected]

# (562) 2651 9336 # (571) 339 4400 Ext 1180 # (511) 313 2000 Ext. 36168

Benjamín Diaz

Local Fixed Income Sales

# (562) 2446 1738

FIXED INCOME SALES & TRADING

FIXED INCOME & ECONOMICS RESEARCH

ANDEAN RESEARCH TEAM SALES & TRADING

EQUITY RESEARCH EQUITY SALES & TRADING

Analyst: Food & Beverages, Healthcare,

Transport

![[Revista Avianca] Entrevista Luiza Possi](https://static.fdocuments.us/doc/165x107/568c0e621a28ab955a904383/revista-avianca-entrevista-luiza-possi.jpg)