Autumn Investor Seminar November 24, 2009 - AXA · The calm after the storm? 0% 20% 40% 60% 80% ......

24

Risk & Capital Management Denis Duverne CFO, member of the Management Board Autumn Investor Seminar November 24, 2009

Transcript of Autumn Investor Seminar November 24, 2009 - AXA · The calm after the storm? 0% 20% 40% 60% 80% ......

Risk & Capital Management

Denis DuverneCFO, member of the Management Board

Autumn Investor Seminar

November 24, 2009

2 – Autumn Investor Seminar – November 24, 2009 – Risk & Capital management

Certain comments contained herein are forward-looking statements including, but not limited to, statements that are predictions of or indicate future events, trends, plans or objectives. Undue reliance should not be placed on such statements because, by their nature, they are subject to known and unknown risks and uncertainties. Please refer to AXA's Annual Report on Form 20-F and AXA’s Document de Référence for the year ended December 31, 2008, for a description of certain important factors, risks and uncertainties that may affect AXA’s business.

In particular, please refer to the section "Special Note Regarding Forward-Looking Statements" in AXA's Annual Report on Form 20-F. AXA undertakes no obligation to publicly update or revise any of these forward-looking statements, whether to reflect new information, future events or circumstances or otherwise.

This document does not constitute an offer to sell or a solicitation of an offer to purchase or subscribe securities issued by AXA in any jurisdiction, including the United States.

Cautionary note

3 – Autumn Investor Seminar – November 24, 2009 – Risk & Capital management

The calm after the storm?

0%

20%

40%

60%

80%

100%

Jan-

97Ju

l-97

Jan-

98Ju

l-98

Jan-

99Ju

l-99

Jan-

00Ju

l-00

Jan-

01Ju

l-01

Jan-

02Ju

l-02

Jan-

03Ju

l-03

Jan-

04Ju

l-04

Jan-

05Ju

l-05

Jan-

06Ju

l-06

Jan-

07Ju

l-07

Jan-

08Ju

l-08

Jan-

09Ju

l-09

0

50

100

150

200

250

300

350

400

450

juin

05

déc

05

juin

06

déc

06

juin

07

déc

07

juin

08

déc

08

juin

09

Itraxx Europe Main EUR ML Single A (asset sw ap) EUR ML Double A (asset sw ap)

1%

2%

3%

4%

5%

6%

7%

8%

Jan-99 Jan-00 Jan-01 Jan-02 Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09

EUR - 10y USD - 10y

Equity volatility stabilizingStock markets have partially recovered

Low interest rates levelsSpreads stabilizing above historical average

Daily volatility over 20 days on the S&P 500

In bps In %

0%

20%

40%

60%

80%

100%

120%

01/0

1/20

00

01/0

5/20

00

01/0

9/20

00

01/0

1/20

01

01/0

5/20

01

01/0

9/20

01

01/0

1/20

02

01/0

5/20

02

01/0

9/20

02

01/0

1/20

03

01/0

5/20

03

01/0

9/20

03

01/0

1/20

04

01/0

5/20

04

01/0

9/20

04

01/0

1/20

05

01/0

5/20

05

01/0

9/20

05

01/0

1/20

06

01/0

5/20

06

01/0

9/20

06

01/0

1/20

07

01/0

5/20

07

01/0

9/20

07

01/0

1/20

08

01/0

5/20

08

01/0

9/20

08

01/0

1/20

09

01/0

5/20

09

01/0

9/20

09

EuroStoxx 50

4 – Autumn Investor Seminar – November 24, 2009 – Risk & Capital management

What went well? Page 5Diversification benefits were real Page 5Risk management actions worked Page 7

Lessons from the crisis Page 9

Keeping market risk under control Page 12

New key performance indicators Page 20

Table of content

5 – Autumn Investor Seminar – November 24, 2009 – Risk & Capital management

We experienced diversification benefits

Business

2008 Revenues Mix

P&C32%

L&S64%

Asset management5%

Financial crisis

Property &Casualty

Life & Savings AssetManagement

+31%

-43%

+6%

FY08 Underlying earnings growth

2008 Revenues Mix

Geography

Financial crisis

Mediterranean & LA region

* Excluding International Insurance, Asset Management, Banking & Holdings

18%

10%

13%

24%

10%

26%

NORCEE UK &Ireland

NorthAmerica

France

Asia-Pacific (incl. Japan)

+54%+35%

+6%

FY08 Underlying earnings growth

-5% -9%

N/A

6 – Autumn Investor Seminar – November 24, 2009 – Risk & Capital management

We experienced diversification benefits

Clients

57%

36%

7%

2008 Revenues

88%

12%

2008 APE

Life & Savings Property & Casualty

+1million clients

Net inflows

€ +7billion

39% 49%

61% 51%

2008 APE 2008 Revenues

Mix

Non proprietary

Proprietary

Life & Savings Property & Casualty

Partnerships & JV

Exclusive agents

Distribution

Financial crisis

Life & Savings Property & Casualty

Mix Financial crisis

L&S -13%P&C -1%

L&S -2%P&C +1%

Individual/ personal

Group/ commercial

7 – Autumn Investor Seminar – November 24, 2009 – Risk & Capital management

Risk management actions were effective

Assets

• Efficient equity hedge: €1.6 billion gain

• No credit default above €300 million

• Systematic collateralization of derivatives

Liabilities

• No liquidity issues

• No credit enhancement activity

Asset Liability Management (ALM)

• Limited duration gap: less than 1 year• Gain versus 2 years gap:

• 14 pts in Solvency II

• 10 pts in Rating Agency models

Solvency & ratings

• Rating remained in AA range • Average rating of the sector down 1 notch

• Solvency II ratio (QIS4) > 155%

• Solvency I ratio > 140%

8 – Autumn Investor Seminar – November 24, 2009 – Risk & Capital management

Table of contents

What went well? Page 5

Lessons from the crisis Page 9The unthinkable can happen Page 9Higher proportion of market risk Page 10

Keeping market risk under control Page 12

New key performance indicators Page 20

9 – Autumn Investor Seminar – November 24, 2009 – Risk & Capital management

• Equities -25%• Interest rates -100bps/+100bps• Credit spreads (corp) +75bps• Credit defaults (corp) 1%• Other: ABS, real estate, private equity, hedge funds, volatility…

The unthinkable can happen: more weight on stress test scenarios

VALUE CAPITAL

EARNINGS LIQUIDITY

Our internal framework based on stochastic calculations was in place and embedded in business decision…

Adverse events (1/20 years)

• Equities -40%• Interest rates -150bps/+250bps• Credit spreads (corp) +150bps• Credit defaults (corp) 2%• Other: ABS, real estate, private equity, hedge funds, volatility…

Extreme events (1/200 years)

Combined scenarios

…still, we have changed calculation frequency (quarterly basis) &

tail risk scenarios on corporate spreads and correlations

10 – Autumn Investor Seminar – November 24, 2009 – Risk & Capital management

Extreme financial scenarios in light of the crisis

Before diversification

Diversification

STEC

Market risk: 61% Life: 21% P&C: 24%

Counterparty9%

Operational 13%

100%

-29%

Market risk represents 61% of total Internal STEC before diversification: how to maintain it at a reasonable level?

Breakdown of STEC by risk categories

How does this measure of Internal STEC impact our key performance indicators?

A high proportion of financial risk

11 – Autumn Investor Seminar – November 24, 2009 – Risk & Capital management

Table of contents

What went well? Page 5

Lessons from the crisis Page 9

Keeping market risk under control Page 12

Refining our asset allocation Page 12Evolution of Variable Annuities Page 16

New key performance indicators Page 20

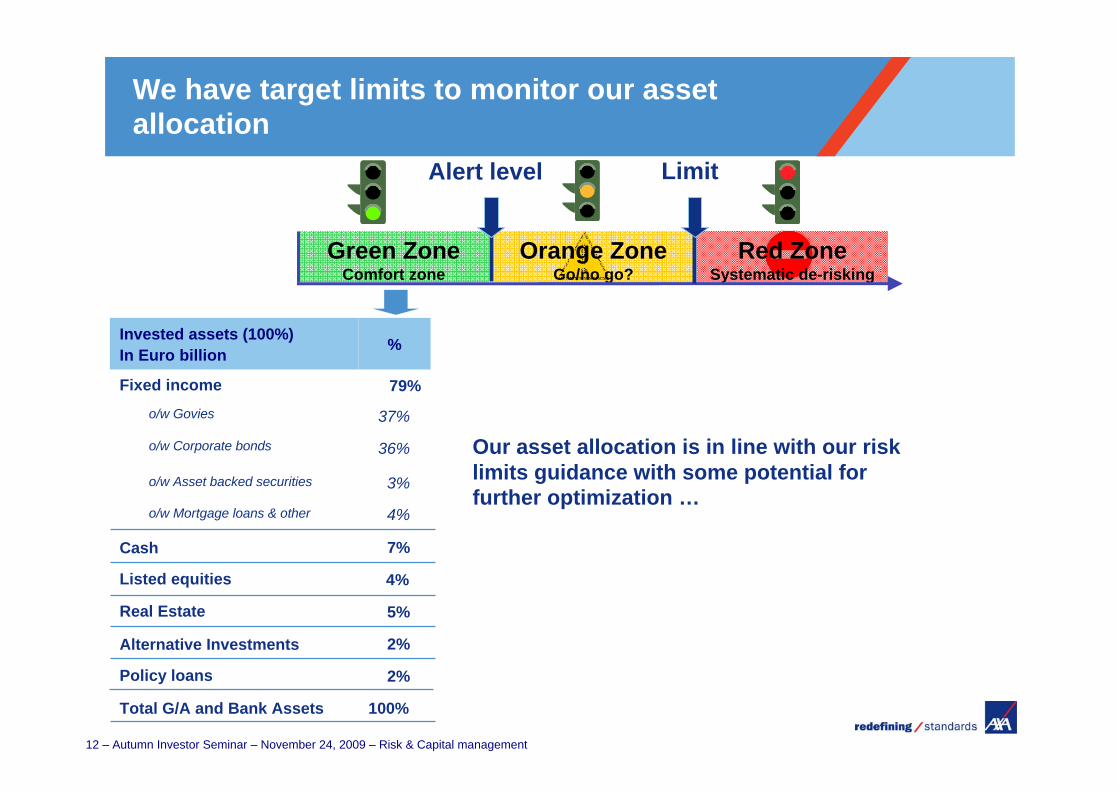

12 – Autumn Investor Seminar – November 24, 2009 – Risk & Capital management

Orange ZoneGo/no go?

Green ZoneComfort zone

Red ZoneSystematic de-risking

LimitAlert level

Invested assets (100%)In Euro billion %

Fixed income 79%o/w Govies 37%

o/w Corporate bonds 36%

o/w Asset backed securities 3%

o/w Mortgage loans & other 4%

Cash 7%

Listed equities 4%

Real Estate 5%

Alternative Investments 2%

Policy loans 2%

Total G/A and Bank Assets 100%

Our asset allocation is in line with our risk limits guidance with some potential for further optimization …

We have target limits to monitor our asset allocation

13 – Autumn Investor Seminar – November 24, 2009 – Risk & Capital management

0%

2%

4%

6%

8%

10%

Corporate BondsIG

Corporate BondsBIG

Equity Property Hedge Funds Private Equity

Expected return by asset class

Internal STEC requirements*

0%

25%

50%

75%

100%

Corporate BondsIG

Corporate BondsBIG

Equity Property Hedge Funds Private Equity

* STEC calibration is more conservative than QIS4 but less conservative than QIS5 (third consultation paper)

Risk free rate

Illustrative expected return by asset class & internal STEC requirements

14 – Autumn Investor Seminar – November 24, 2009 – Risk & Capital management

Under Solvency II, corporate bonds have a better risk / returntrade off than all other asset classes.

Expected risk premium on required Internal STEC capital*

* Shareholders’ share net of cost of capital and diversification benefits

0%

20%

40%

Corporate BondsIG

Corporate BondsBIG

Equity Property Hedge Funds Private Equity

Corporate bonds: relatively attractive assets

15 – Autumn Investor Seminar – November 24, 2009 – Risk & Capital management

Underwriting:

• Selection process based on a dual credit analysis (Asset Management analyst + Insurance company analyst)

• Second opinion from risk management

• Group Chief Investment Officer review/approval

Risk management:

• Diversification at Group level (country, issuer, sector…)

• Corporate bonds portfolio duration limited to 4/5 years

Managing corporate bond risk

16 – Autumn Investor Seminar – November 24, 2009 – Risk & Capital management

Allocation funds & guided architecture

Japan developments

Evolution of Variable Annuities

US developments

Very limited involvement in the under priced Variable Annuities market expansion until 2008

First mover in 2009 to reduce commissions and reprice GMIB products

Market share gains since 2009 with a double digit NBV margin

Reduced rollup rate (6.5% to 6%)Eliminated GWBL

Increased pricing

November 2008

Lowered annuitization rate

Reduced rollup rate (5%)Limit fund lineup

February 2009

New Accumulator 9.0February 2009

Retirement CornerstoneNovember 2009

Improved hedging efficiency across the board

Basis risk action planVolatility action plan

Germany developments

Stopped parts of “TwinstarInvest” new business

Optimized swaption strategy on Inforce books to reduce exposure to long term interest rates convexity

Early 2009

Redesigning “TwinstarInvest” with a launch expected early 2010

Going forward

17 – Autumn Investor Seminar – November 24, 2009 – Risk & Capital management

Allocation funds

New business systematically invested in:• Allocation funds• Guided architecture

Customer benefits• Simple for investors to adopt a strategy that matches their risk-tolerance profile and their

investment time horizon

• Capacity to invest in a thoughtfully constructed, professionally allocated portfolio of investment funds diversified across domestic and international as well as equity and fixed income asset classes

AXA’s benefits• Diversification of assets, and limits on equity allocation• Capacity to apply ATM process to mitigate equity volatility • Permanent flexibility on selection of asset managers

18 – Autumn Investor Seminar – November 24, 2009 – Risk & Capital management

Action plan on equity volatility

-38%

6%

-40%

5%

-30%

8%

-34%

5%

Total2008 2009YTD

+6%

2007

+2%

+0%

+8%

S&P 500 Index

Hypothetical ATM 500 Portfolio

Introducing AXA Tactical Manager (“ATM”) strategy…

Tactically Managed Portion of an ATM Portfolio

Low HighVolatility

100% Equity Exposure Exposure

0% Equity

Implementation of a new tactical strategy designed to reduce equity weightings during periods of high volatility (above ca. 30%) for all funds under guided allocation

…should allow to improve funds performance

Back testing

19 – Autumn Investor Seminar – November 24, 2009 – Risk & Capital management

Table of contents

What went well? Page 5

Lessons from the crisis Page 9

Keeping market risk under control Page 12

New key performance indicators Page 20New KPIs using Internal Short Term Economic Capital (STEC)Developments on the P&C front: New Combined Ratio & key findings

20 – Autumn Investor Seminar – November 24, 2009 – Risk & Capital management

Systematic measure of return on risk adjusted capital

• Definition:

• Granularity:

- Protection, investment & savings, mixed

- Individual, Group

- Motor, property, liability, health

- Personal, Commercial

Systematic measure of Value creation

• Definition:

New KPIs using Internal Short Term Economic Capital (STEC)

Net IncomeSTEC

Life & Savings

Property & Casualty

∆ AFR* STEC

* Available Financial Resources

21 – Autumn Investor Seminar – November 24, 2009 – Risk & Capital management

Economic Combined Ratio (ECR) has become one of our KPI’s, reflecting:

• Current year experience• Cost of risk• Business duration• Normalized Natural Catastrophe costs

Developments on the P&C frontA new Combined Ratio

Making Combined Ratios comparable across the various business lines and across the years

Calculation

AccountingCR

EconomicCR

Prior years reserve dev.

One-off expenses

Cat Nat events

Reserves discount

Cost of risk Tax

Objective: ECR ≤ 100%

• ECR = 100% return/STEC = 10% (RFR + Equity risk premium)• ECR < 100% return/STEC > 10%

22 – Autumn Investor Seminar – November 24, 2009 – Risk & Capital management

Impact on 2009/2010 action plan

• Repricing actions on Inforce business, taking into account price elasticity and market cycle• Moderating new business activity in soft countries

Most business lines are profitable but necessity to decrease ECR in some cases

Developments on the P&C frontKey findings 2008

PropertyMotor Liability Health

Group average ECR = 101.5%

Per Business Line

UK Germany Belgium

France Switzerland Med Region

Per Country

Group average ECR = 101.5%

< 101.5%

< 101.5%

> 101.5%

> 101.5%

23 – AXA Investor day – November 24, 2009 – Risk & Capital management

Conclusion

Life & Savings business has gone in 2008 through a crisis comparable to P&C in 2000/2002.

Risk management allowed us, as in 2000/2002, to navigate well through the storm.

The combination of:• normalized Solvency II rules across the sector, • upgraded risk management in Life & Savings, • key performance indicators to measure economic return of all business lines,

should lead to lower equity risk premium for the insurance sector and for AXA.