Fixed Income Investor/Analyst Seminar June 8, 2004.

59

Fixed Income Investor/Analyst Seminar June 8, 2004

-

Upload

marvin-mckinney -

Category

Documents

-

view

217 -

download

1

Transcript of Fixed Income Investor/Analyst Seminar June 8, 2004.

Fixed Income Investor/Analyst Seminar

June 8, 2004

Payout Ratio Affords Substantial Flexibility

Net cash provided by operating activities Acquisition of Bridgelands

(included in land acquisition expenditures) Improvements to existing properties Dividends paid

Common 150Preferred 12

Cash from operations available for reinvestment

$ 376

22

(71)

(162)

$ 165

Millions

For the year endedDecember 31, 2003

Cash from Operations Supplemented byCapital Raising/Recycling

Cash from operations available for reinvestment

Proceeds from the disposition of properties to PREIT, Kravco and other properties

Proceeds from exercise of stock options

Net borrowings (note 1)

Other, net

Net proceeds from capital transactions

Total capital transactions and cash from operations

$ 165

396

110

95

(4)

$ 597

$ 762

Millions

Note 1 Net proceeds from the issuance and repayment of debt, excluding construction loan draws.

For the year ended December 31, 2003

How Did We Spend It ?

Acquisitions of interests in properties and other assets

Acquisitions of Christiana/Staten Island/ Mizner Park / Other

Acquisition of interest in Woodlands

9.25% QUIPS (preferred securities) retired

Repurchase of shares --- Hughes participation

Bridgelands acquisition

Equity in development (note 1)

Millions

Note 1 Includes expenditures for properties in development and investments in joint ventures in development, net of construction loan draws.

Net capital redeployed

$ 437

57

72

22

97

$ 685

253

184

For the year ended December 31, 2003

Net capital redeployments

Cash from operations available for reinvestment

Net proceeds from capital transactions

Net capital redeployments

$ 165

$ 597

$ 762

$ 685

MillionsFor the year ended December 31, 2003

$77

Reconciliation of cash from operations available for reinvestment, net proceeds from capital transactions and net capital redeployments to Statement of Cash Flows

Millions

Net cash provided by operating activities Expenditures for the acquisition of Bridgelands included in land acquisition expenditures Expenditures for improvements to existing properties Dividends paid

Cash from operations available for reinvestment

Proceeds from capital transactions Proceeds from the disposition of properties to PREIT, Kravco and other properties

Proceeds from the disposition of interests in properties Expenditures for acquisition of Christiana netted with proceeds from dispositions Proceeds from the exercise of stock options Net proceeds from the issuance and repayment of debt, excluding construction loan draws Net other investing and other financing activities

Net proceeds from capital transactions

Capital redeployments Total expenditures for acquisitions of interests in properties and other assets

Expenditures for acquisitions of interests in properties and other assets Expenditures for acquisition of Christiana netted with proceeds from dispositions

Purchase of Parent Company-obligated mandatorily redeemable preferred securities Repurchases of common stock Expenditures for the acquisition of Bridgelands included in land acquisition expenditures Equity in development

Expenditures for properties in development Expenditures for investments in unconsolidated real estate ventures in development Proceeds from borrowings on construction loans

Net capital redeployments

Net change in cash

Year ended 12/31/2003

$ 376 22

(71) (162)

165

396

110 95 (4)

597

(437)

(57) (72) (22)(97)

(685)

$ 77

35640

(397) (40)

(168) (27) 98

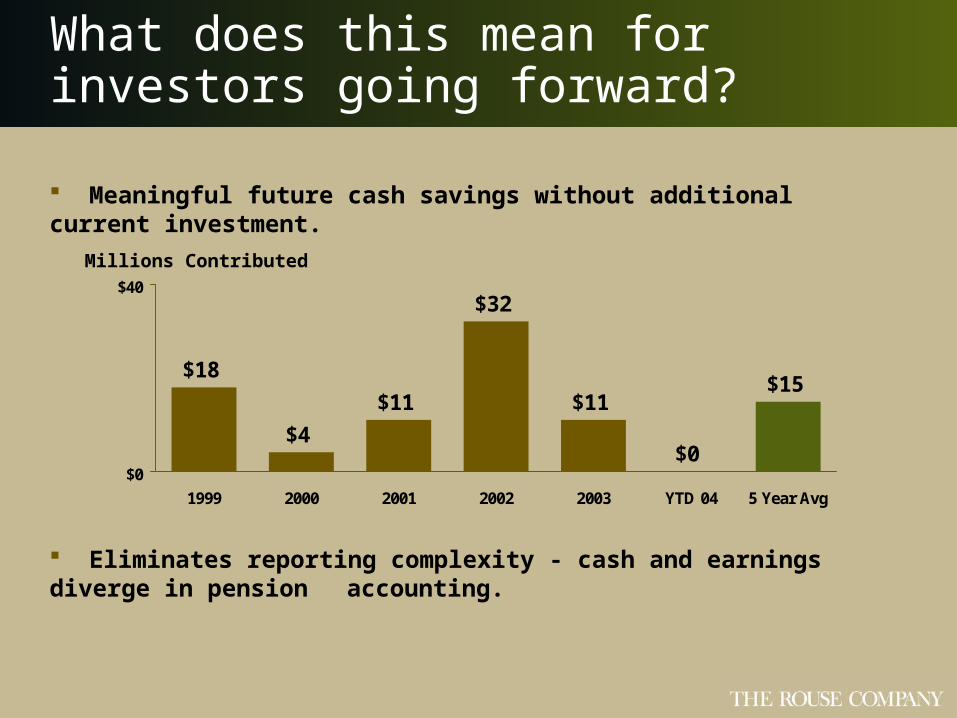

What does this mean for investors going forward?

Meaningful future cash savings without additional current investment.

$18

$4

$11

$32

$11

$0

$15

$0

$40

1999 2000 2001 2002 2003 YTD 04 5 Year Avg

Millions Contributed

Eliminates reporting complexity - cash and earnings diverge in pension accounting.

Organization Changes /Early Retirements

Provision for personnel changes

(Includes $11 M for retirementsof two Vice Chairmen & CFO)

$ 22

Millions

*Assumes 1/1/02 internal cost structure grows at CAGR of 4% and includes 2004 projected internal costs/savings.

$22*

January 1, 2002 –December 31, 2004

SAVINGS

January 1, 2002 - March 31, 2004

Fixed Income Investor/Analyst Seminar

June 8, 2004

Regional Centers

(1) Excludes urban centers, projects with less than two anchors, and centers open less than one year. (2) Includes current and recently opened development projects.

1993 Portfolio51 Centers

Current Portfolio31 Centers

Total RegionalCenters (1)

2007 Portfolio (2)

34 Centers

Mall RankingA+ or A B C

5 10% 13 25% 33

19 61% 10 32% 2 7%

Number Percent Number Percent Number Percent

22 65% 12 35% --

65%

Dispositions & Acquisitions

Dispositions in 2003

Cherry Hill Mall

Echelon Mall

Exton Square

Gallery at Market East

Moorestown Mall

Plymouth Meeting

Average Sales of $350 psf

Acquisitions in 2003 & 2004

Christiana Mall

Staten Island Mall

Mizner Park

2003

Providence Place

2004

Average Sales of $500 psf

$280.0

$327.2

$365.3 $368.3 $375.7

$469.8

$545-$555

$508.9

$100

$600

1997 1998 1999 2000 2001 2002 2003 2004Est.

Retail Centers Net Operating Income

Millions

Retail Centers

Occupancy

93%

Comp Tenant Sales

$439 psf

Comp Space Sales

+ 9%

1 Excludes urban centers, projects with less than two anchors, and centers open less than two years2 Comparable tenants, excluding spaces >10,000 s.f.

2004 Sales per Square Foot 2

Center Ranking

A+ or A

B

C

RegionalCenters 1

2004 AverageOccupancy

% 2004 NetOperating Income

$ 489

$ 357

$ 286

94 %

94 %

91 %

73 %

24 %

3 %

Rouse Regional CentersKey Performance Measures

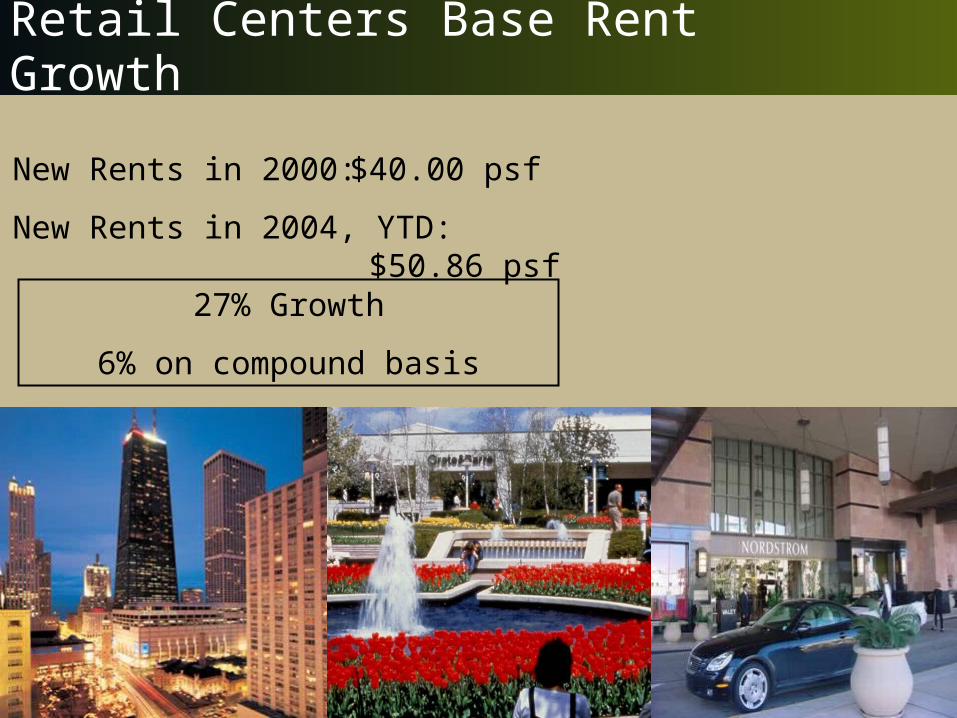

Retail Centers Base Rent Growth

New Rents in 2000:

New Rents in 2004, YTD:

$40.00 psf

$50.86 psf27% Growth

6% on compound basis

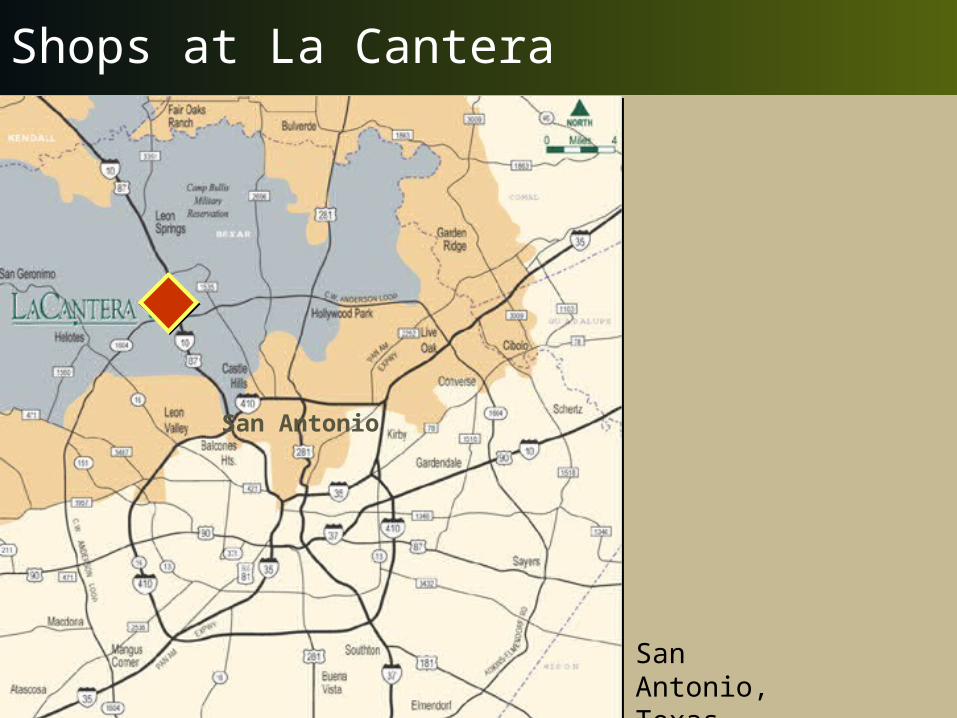

Shops at La Cantera

San Antonio

San Antonio, Texas

Shops at La Cantera

Nordstrom

Neiman Marcus

Dillard’sFoley’s

Future Expansion

Site

Shops at La Cantera

Shops at La Cantera

Kendall Town Center

Miami, Florida

Miami

Kendall Town Center

Dillard’s

Bridgewater Commons

New York

Trenton

Bridgewater, New Jersey

Bridgewater Commons

Bloomingdale’s

Lord & Taylor

Macy’s

Lifestyle Center

Retail Centers

Summerlin Town Centre

Summerlin, Nevada

Summerlin Town Centre

Dillard’s Robinsons - May

Anchor

AnchorAnchor

Fixed Income Investor/Analyst Seminar

June 8, 2004

Community Development

Quality of the AssetsColumbia, Maryland

Quality of the AssetsSummerlin, Nevada

Quality of the AssetsThe Woodlands, Texas

Size (acres)

Remaining Saleable acres

Current residents

Residents at completion

Current jobs

Jobs at completion

17,000

1,000

96,000

100,000

91,000

100,000

Columbia

22,500

6,600

67,000

170,000

20,000

50,000

Summerlin

1,160

475

500

4,500

--

500

Fairwood

76,660

19,575

233,500

454,500

141,000

240,500

Total

9,000

6,400

--

60,000

--

40,000

Bridgelands

27,000

5,100

70,000

120,000

30,000

50,000

Woodlands

Recent Acquisitions

Rouse Master Planned Communities

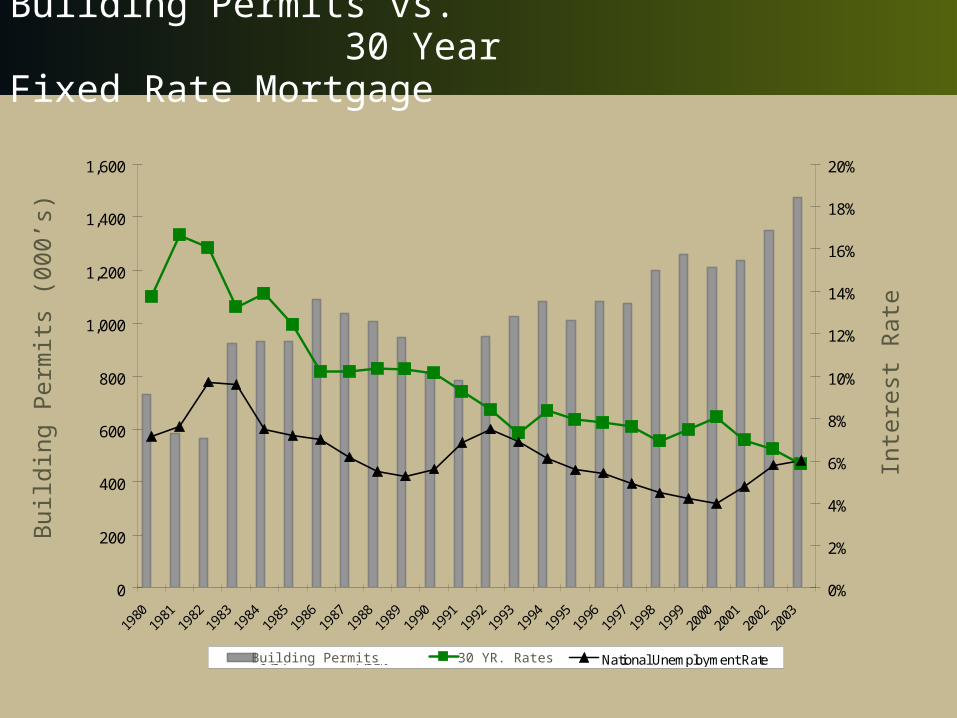

Building Permits vs. 30 Year Fixed Rate Mortgage

0

200

400

600

800

1,000

1,200

1,400

1,600

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

U.S. 7.31% 30 YR. FMR National Unemployment Rate

Bui

ldin

g P

erm

its (

000’

s)

Inte

rest

Rat

e

Building Permits 30 YR. Rates

Columbia Land Sales vs. 30 Year Fixed Rate Mortgage

$0

$50

$100

$150

0%

5%

10%

15%Columbia land sales30 yr. fixed rate mortgage

Col

umbi

a La

nd S

ales

(M

illio

ns)

30 Y

ear

Fix

ed R

ate

Mor

tgag

e

*Revenue figures include builder participation

Factors Affecting Mortgage Rates

National & local employment trends

Land supply & barriers to entry

Diversity of product offerings

Geographic diversity

Pricing power

“Knowledge” advantage

Diversity of Assets

The Woodlands

The Woodlands

Bridgelands

The Woodlands

Canyon Gate/Stone Gate

Sienna Plantation

Shadow Creek Ranch

Cinco Ranch

Kingsbridge

Teal Run

Waterside

Grand Lakes

Gleannloch Farms

The Woodlands

Rank Community Annual Starts Price Range

Source: American Metrostudy

1

2

3

4

5

6

7

8

9

10

1,311

687

514

476

472

365

332

329

327

322

$3,000,000

$291,000

$1,587,000

$559,000

$740,000

$208,000

$220,000

$426,000

$505,000

$671,000

$67,000

$110,000

$102,000

$144,000

$62,000

$93,000

$89,000

$127,000

$127,000

$125,000

Master Planned Community RankingsRanked by 2003 starts

Bridgelands

Bridgelands

The Woodlands

Bridgelands

Creating Long Term Value - Urbanization

Columbia Town Center

Columbia Town Center

Columbia Town Center

Retention of parking fields

Utilization of shared parking

Strategic utilization of ground leases

Ongoing ownership of operating properties

Community Development – Columbia Based

Fairwood

Stone LakeEmerson

Baltimore

Washington

Fairwood Emerson

Stone Lake

Community Development – Columbia Based

Community Development – Summerlin Based

The Woodlands

Community Development – Houston Based

Community Development

Fixed Income Investor/Analyst Seminar

June 8, 2004

Total Debt /Gross Asset Value

Total Debt & Preferred Stock /Gross Asset Value

Secured Debt /Gross Asset Value

61.0 %

66.3 %

52.5 %

March 31,2004

53.7 %

53.7 %

37.3 %

December 31,1999

Total Leverage and Secured Leverage

65.0 %

--

55.0 %

CurrentCovenant

Requirements

Combined Interest Coverage

Combined Fixed Charge Coverage Pro Forma

Combined Fixed Charge Coverage Without Principal Amortization

Pro Forma

2.05 x

1.55 x--

March 31,2004

2.80 x

2.07 x2.18 x

December 31,1999

(1) Adjusted to give effect to the redemption of the 9.25% QUIPS and the conversion of the Series B preferred stock as of the beginning of the period

Interest and Fixed Charge Coverage

Twelve Months Ended

1.70 x

1.30 x--

CurrentCovenant

Requirements

(1)

1.83 x--

2.58 x2.76 x

----

(1)

Before Hughes Heirs Expense

Adjusting for Hughes Heirs Expense

26.9%

32.9%

39.8%

43.4%

12 Months12/31/03

3 Months3/31/04

Unencumbered NOI

Retail

Office & Other

Community Development

Unencumbered NOI

Hughes Heirs Expense

Unencumbered NOI Adjusted for Hughes Heirs Expense

Total Net Operating Income

Hughes Heirs Expense

Total NOI Adjusted for Hughes Heirs Expense

$ 64,369

6,210

123,890

194,469

64,293

$ 258,762

$ 722,177

64,293

$ 786,470

$ 30,335

1,772

41,165

73,272

11,545

$ 84,817

$ 184,081

11,545

$ 195,626

12 Months12/31/03

3 Months3/31/04

Unencumbered NOI

In Thousands

NOI

Interest expense

NOI of discontinued operations

Depreciation and amortization

Other provisions and losses, net

Impairment losses on operating properties

Income taxes, primarily deferred

Our share of interest expense, ground rent expense,

depreciation and amortization, other provisions and

losses, net, income taxes and gains (losses) on operating

properties of unconsolidated real estate ventures, net

Other

Earnings before net gains (losses) on dispositions of interests in

operating properties and discontinued operations in condensed

consolidated financial statements

$ 184,081

(58,284)

(1,724)

(47,910)

(5,109)

---

(18,616)

(19,966)

(1,796)

$ 30,676

$ 722,177

(222,766)

(45,163)

(173,280)

(32,513)

(7,900)

(42,500)

(68,894)

(16,270)

$ 112,891

Reconciliation of NOITo Most Comparable GAAP Measure

3 monthsMarch 31,

2004

12 monthsDecember 31,

2003

In Thousands

Notes / Definition of NOI

Segment operating data are presented in accordance with Statement of Financial Accounting Standards No. 131, “Disclosures about Segments of an Enterprise and Related Information.” As required by the Statement, segment data are reported using the performance measure and accounting policies followed by the Company for internal reporting to management which differ, in certain respects, from those used for reporting under accounting principles generally accepted in the United States of America (“GAAP”). The performance measure used by the Company is Net Operating Income (“NOI”). The Company defines NOI as segment revenues less segment operating expenses (including provision for bad debts, losses (gains) on marketable securities classified as trading, net losses (gains) on sales of properties developed for sale and partner’s share of NOI of the venture developing The Woodlands, but excluding income taxes, fixed charges, as defined below, and real estate depreciation and amortization). Prior to July 1, 2003, the Company included certain current income taxes in its definition of NOI. Effective July 1, 2003, the Company revised its definition to exclude these amounts from NOI, affecting primarily the definition of the Company’s community development activities. The amounts from prior periods have been reclassified to conform to the current definition. The accounting policies used to calculate NOI and other operating results data are the same as those used by the Company in its condensed consolidated financial statements prepared in accordance with GAAP, except that the NOI of the venture developing the community of The Woodlands is consolidated and the other partner’s share is classified as operating expense rather than using the equity method. In addition, real estate ventures in which the Company has joint interest and control and certain other unconsolidated ventures are accounted for using the proportionate share method rather than the equity method and the Company’s share of FFO of other unconsolidated ventures is included in revenues. Also, discontinued operations and minority interests are included in NOI rather than separately presented. These segment accounting policies affect only the reported revenues and expenses of the segments and have no effect on our reported net earnings.

Notes / Leverage Ratios

The leverage calculations presented above are calculated in accordance

with certain covenants applicable to our public debt and not in accordance

with GAAP. They are not liquidity measures and should not be considered

alternatives to cash flows. The terms “Gross Asset Value,” “Total Debt”

and “Secured Debt” include our consolidated amounts and our pro rata

share of unconsolidated real estate ventures and exclude minority interests

in consolidated amounts. Gross Asset Value for (1) operating properties is

calculated using NOI (less ground rents) divided by stated percentages, or,

if owned less than one year, the acquisition cost, (2) master-planned

communities is the latest annual current value as set forth in appraisals and

(3) other assets is the GAAP carrying value. Gross Asset Value is not

necessarily indicative of the fair values of our assets.

Notes / Coverage Ratios

The coverage ratios presented above are calculated in accordance with certain covenants in our

credit facility agreement and not in accordance with GAAP. These ratios are presented to

illustrate our level of compliance with these covenants. They are not liquidity measures and

should not be considered alternatives to cash flows. The terms “Combined EBITDA,” “Combined

Interest Expense” and “Combined Fixed Charges” include our consolidated amounts and our pro

rata share of unconsolidated real estate ventures and exclude minority interests in consolidated

amounts. Combined interest coverage means Combined EBITDA divided by Combined Interest

Expense. Combined Fixed Charge Coverage means Combined EBITDA plus base ground rent

divided by Combined Fixed Charges.

Combined EBITDA means net earnings before extraordinary items and cumulative effects of

changes in accounting principle, excluding gains and losses on operating properties, impairment

losses, plus Combined Interest Expense, depreciation and amortization expense (including our

share of that of unconsolidated real estate ventures), income taxes, distributions on preferred

securities and expenses pursuant to the Contingent Stock Agreement.

Combined Fixed Charges includes Combined Interest Expense, scheduled principal payments

(including our share of principal payments of unconsolidated real estate ventures), base ground

rents and distributions on preferred securities.

Notes / Unencumbered NOI

Unencumbered NOI is the NOI of properties that were not encumbered

by mortgages as of the dates presented and, at March 31, 2004, also

included Fashion Show, which was encumbered at that date by a

mortgage with a face value of approximately $33 million that the

Company intends to repay without penalty before December 31, 2004. In

January 2004, the Company repaid a $240 million construction loan that

had previously encumbered Fashion Show.

Fixed Income Investor/Analyst Seminar

June 8, 2004