Audit Core Team

52

Audit Core Team Responsibilities Procedures Deadlines Presented by Bob Muller, Steve Krovitz, Roger Wright, and Scott Elliott 2009/2010 CSP Contract Compliance Audit

-

Upload

halee-atkins -

Category

Documents

-

view

28 -

download

0

description

Audit Core Team. 2009/2010 CSP Contract Compliance Audit. Responsibilities Procedures Deadlines. Presented by Bob Muller, Steve Krovitz, Roger Wright, and Scott Elliott. Audit Core Team What is this??. - PowerPoint PPT Presentation

Transcript of Audit Core Team

Audit Core Team

ResponsibilitiesProceduresDeadlines

Presented by Bob Muller, Steve Krovitz, Roger Wright, and Scott Elliott

2009/2010 CSP Contract Compliance Audit

Audit Core TeamWhat is this??

The Audit Core Team is defined within Rule 806.3 –Administration of Compliance Audit Process of

Streamlined Sales Tax Rules and Procedures

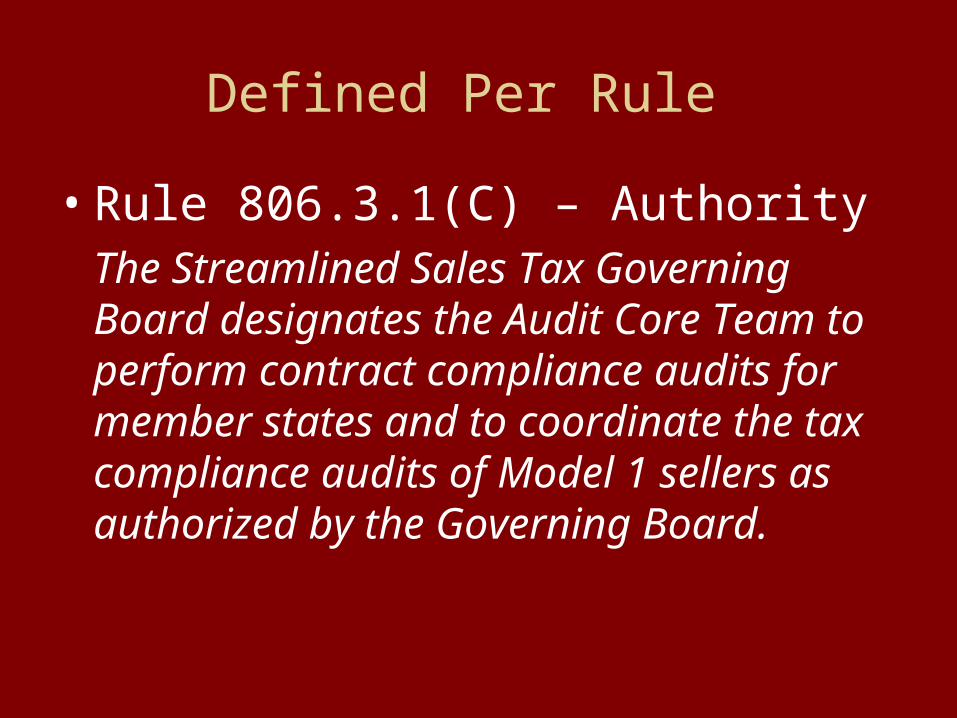

Defined Per Rule

• Rule 806.3.1(C) – AuthorityThe Streamlined Sales Tax Governing Board designates the Audit Core Team to perform contract compliance audits for member states and to coordinate the tax compliance audits of Model 1 sellers as authorized by the Governing Board.

Defined Per Rule

• Rule 806.3.2(D) – Audit Core Team The Audit Core Team is a group of

designated representatives from full member states who are responsible for coordinating compliance audits, performing contract compliance audits and compiling feedback reports for the Governing Board.

Defined Per Rule

• Rule 806.3.4(B) – Audit Core Team - Reporting Relationship

The Audit Core Team will report to the Streamlined Sales Tax Governing Board Executive Director or its designee for audit assignments, guidance and support.

Who is the Core Team

Steve KrovitzMinnesota Department

Of Revenue

Scott ElliottWashington

Department of Revenue

Who is the Core Team

Roger Wright West Virginia Dept.

Of Tax & Revenue

Bob MullerIndiana Department

Of Revenue

Let’s go over the Core Team concept?

Simply stated: The Core Team will

1. Complete the audit steps and procedures directly related to the CSP contract.

2. Review areas generic to all the SST Member and Associate Member States.

3. Coordinate a tax compliance audit of the CSP transactions with the State Auditors.

Simply stated: The State Auditors will

1. Complete tax compliance audit steps as part of the CSP contract audit that are specifically related to their state.

2. Complete a Sales Tax Audit for their state, using the policies and procedures set out in their own state.

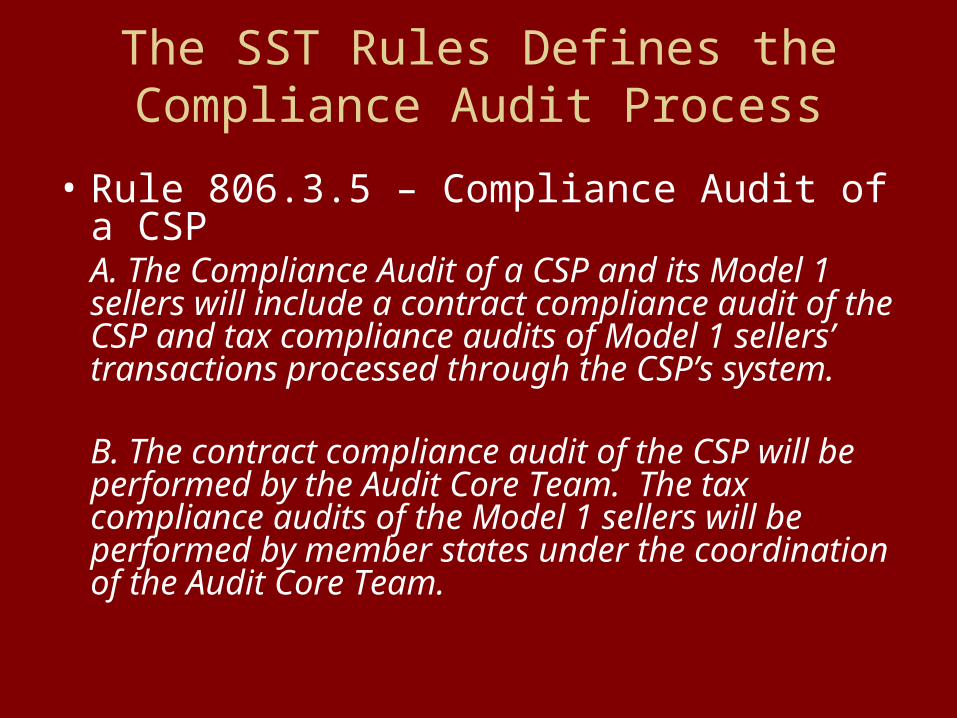

The SST Rules Defines the Compliance Audit Process

• Rule 806.3.5 – Compliance Audit of a CSPA. The Compliance Audit of a CSP and its Model 1 sellers will include a contract compliance audit of the CSP and tax compliance audits of Model 1 sellers’ transactions processed through the CSP’s system.

B. The contract compliance audit of the CSP will be performed by the Audit Core Team. The tax compliance audits of the Model 1 sellers will be performed by member states under the coordination of the Audit Core Team.

Clear as Day!(Right!!!!)

The Audit Core Team:• Will evaluate all pertinent elements of the

current contract between the CSPs and the Streamlined Sales Tax Governing Board and assess each CSP’s compliance with the terms of the contract.

• As part of this contract compliance audit, they will audit areas where they are in the unique position to review.

• Will advise the Member and Associate Member State Auditors if problems exist that would impact the tax compliance audits.

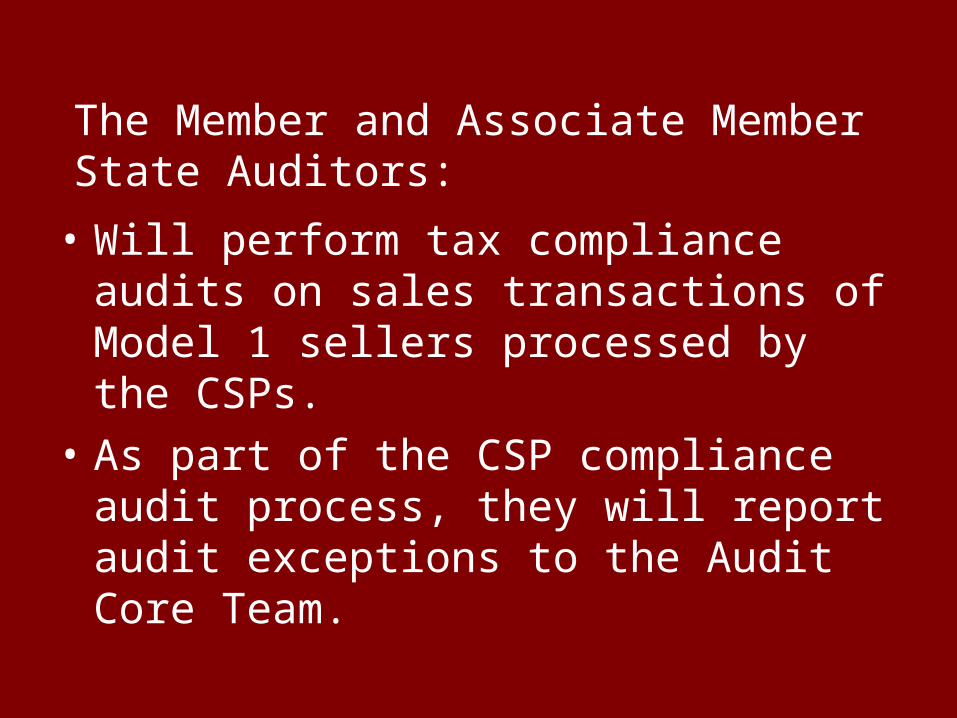

• Will perform tax compliance audits on sales transactions of Model 1 sellers processed by the CSPs.

• As part of the CSP compliance audit process, they will report audit exceptions to the Audit Core Team.

The Member and Associate Member State Auditors:

When the rubber hits the road, it could still be a little bumpy from time to time. Why….?

Because

• This is only the second time this type of audit has ever been done by the Audit Core Team.

• Theory does not always equal practice.

• Sometimes the road to knowledge can be full of potholes (large and small).

-Solution-

The Core Team will:• work hard• attempt to communicate effectively with everyone• be flexible in its approach• keep the goal in focus

The SST Audit Committee has:

• listened to the concerns of the Core Team, the CSPs, and the states

• diligently attempted to address area of concern from the first round of audits

Goal

To complete a timely, accurate, and professional audit that meets the needs and expectations of the Streamlined Sales Tax Governing Board.

The Core Team will provide the State Auditors with two reports.• A preliminary report of findings will be

issued to the state auditors in early November 2009. This report will include any audit results discovered by the Core Team that could be relevant to the tax compliance audits.

• The final contract compliance audit will be given to each Member and Associate Member State in March of 2010.

Audit Core TeamResponsibilities

Rule 806.3.4(D)(1)The Audit Core Team is responsible for performing contract compliance audits and coordinating tax compliance audits

with member states.

Rule 806.3.4(D)(2)Outlines ten (10) specific tasks the Audit Core Team is responsible for

completing.

Rule 806.3.4(D)(2)(i)

The Audit Core Team will:Create a uniform audit plan with a timeline to establish the projected dates that various audit steps should be completed

The audit timeline has been established and will be reviewed in the following slides.

Timeline07/15/09

through

08/24/09

• By July 15th the Audit Core Team will submit questionnaires to the CSPs, Member/Associate Member States, and the Office of Executive Director.

• All questionnaires must be returned to the Audit Core Team by the end of business on August 15 or the 1st business day thereafter.

• Member/Associate Member States must thoroughly report on their questionnaires any Model 1 Seller and/or CSP with return filing or delinquency problems.

Timeline• Between July 15th and August 15th the

Audit Core Team will request that the CSPs:– Supply a listing of Model 1 Sellers they have

preformed CSP services for during the audit period, along with the date they started performing services for each Model 1 seller. The CSPs will also be requested to supply a listing of the states in which each Model 1 Seller holds volunteer status.

– Prepare data downloads, obtain source documents, and prepare system descriptions, as specifically requested by the Audit Core Team for use in completing the audit responsibilities outlined in rule 806.3.4(D)(2). (This information should be available for the Core Team’s review at the CSPs during the on site visit.)

07/15/09

through

08/24/09 (Continued)

Timeline

07/15/09

through

08/24/09 (Continued)

• Confirm that the CSPs have distributed their various downloads of sales transaction information to the states and Testing Central as requested for quarters beginning with the 3rd quarter of 2007 and ending with the 1st quarter of 2009 and that the 2nd quarter of 2009 has been distributed in accordance with Appendix F.

• Follow-up with Member/Associate Member States to ensure that they have received all CSP download files and that they have thoroughly completed their questionnaires.

• Between August 1st and August 15th the Audit Core Team will conduct pre-audit conference calls with each of the CSPs.

Timeline

08/25/09

and

08/30/09

• The Audit Core Team will meet in St. Paul, Minnesota to review the completed questionnaires, go over data download issues, and finalize the CSP field work plans. A half day meeting is scheduled in the afternoon of Tuesday, August 25, 2007 and another half day meeting is planned for the morning of Friday, August 28, 2007.

• From Member/Associate Member States questionnaires the Core Team will prepare a preliminary informal report for the CSPs. This report should combine the reporting and delinquency errors noted by the states and will be provided to the CSPs during the field visits.

Timeline

08/31/09through 10/31/09

• The Audit Core Team will complete field work at the CSP locations. (It is important that during this time frame the Audit Core Team complete all field work in areas that could lead to an audit adjustment by any member/ associate member state.)

• The member and associate member states will start their review of the Model 1 sellers’ transactions. The states should immediately advise the Core Team if they discover any reporting problems not previously reported on the questionnaires.

• By November 1st or the 1st business day thereafter, The Audit Core Team will prepare preliminary reports that will be forwarded to the member states and associate member states detailing work completed in potential audit adjustment areas. These Reports will include the Core Team’s analysis of the descriptions within the transaction downloads.

Timeline

11/01/09

through

12/01/09

• During this period of time the Audit Core Team can continue to work on and finalize the contract compliance portion of the CSP audits.

• The member and associate member states will complete their transactions review for the contract compliance audits and prepare reports that notify the Audit Core Team of their findings.

• The member and associate member states’ Sales Tax Compliance Audit Reports must be forwarded to the Audit Core Team by the end of business on Friday, December 1st or the 1st business day thereafter.

Timeline

12/01/09through 01/08/10

• Conference calls and/or meetings to formally discuss a state’s preliminary findings can be conducted during this time period as needed or requested. The meetings could include both state representatives and/or representatives of a CSP.

• The Audit Core Team will coordinate and work with the CSPs and the states to resolve any issues between them that could be communication problems or misunderstandings, rather than true problems or errors.

• The Audit Core Team will prepare a preliminary report on the findings by January 8th. Each CSP compliance audit report on initial findings must be forwarded to the respective CSP by the end of business on January 8th or the 1st business day thereafter.

Timeline01/08/10through

02/08/10

• The CSP will review and comment on the preliminary findings of the contract compliance audit. Comments will be sent to the Audit Core Team and member/associate member states.

• Conference calls and/or meetings to formally discuss the preliminary report with the CSPs and/or the states can be conducted during the early days of this time period as needed or requested.

• Final comments to the Audit Core Team from the CSPs must be forwarded to the Audit Core Team by the end business on February 8th, or the 1st business day thereafter. The preferred method of delivery is electronic.

Timeline

02/09/10

through

02/28/10

• Conference calls or GoToMeeting conferences will be conducted, if necessary, with the CSPs on February 10th, 11th, or 12th to discuss the CSPs’ final comments.

• The Audit Core Team and member/associate member states will amend their findings, as needed.

• The Audit Core Team will prepare the final contract compliance audit reports to be sent to the Executive Director.

Timeline

03/01/10 • The final contract compliance audit reports on each CSP will be forwarded to the Executive Director by March 1st.

Rule 806.3.4(D)(2)(g)

The Audit Core Team will:Acquire a list of sellers represented by each CSP and provide this information to the Streamlined Sales Tax Governing Board member states

This information will be requested and forwarded to the various states.

Rule 806.3.4(D)(2)(h)

The Audit Core Team will:Coordinate with state auditors a download of all sales processed by the CSP for each seller, which will be available through access to a FTP site maintained by the SSTGB, Inc. to receive electronic records

The states should start receiving quarterly downloads according to Appendix F beginning with the 2nd Quarter of 2009. This download will be due on August 15, 2009. The Audit Core Team has been working with the CSPs to get the states the catch-up period’s data downloads (3rd Quarter 2007 through 1st Quarter 2009).

Rule 806.3.4(D)(2)(e)

The Audit Core Team will:

Verify that all tax collected was remitted timely to the appropriate tax

authority

1.) The Core Team will verify that all tax collected is remitted to a state.2.) The Core Team will rely on information received from the states that the tax was appropriately and timely remitted.

Rule 806.3.4(D)(2)(f)

The Audit Core Team will:

Verify that sales were accurately reported by the CSP/Seller on simplified electronic returns (SERs)

1.) The Core Team will verify that simplified electronic returns are being filed by the CSP for all sellers.2.)The Core Team will review the CSP’s procedures for extracting the SER data.3.)The Core Team will rely on information from the states that the SERs are accurate.

Rule 806.3.4(D)(2)(d)

The Audit Core Team will:

Verify that the appropriate entity use exemption data elements are captured by the CSP system

1.) The Core Team will evaluate the CSP’s system to be assured it has the ability capture exemption data elements. 2.) The Core Team will verify that exemption elements are being captured.(The Core Team can not be responsible for auditing whether a purchaser is claiming a proper exemption; it can only be responsible to document that the CSP is capturing the correct elements.)

ATTENTION !!!

• The next two areas to be discussed could result in audit findings relevant to the tax compliance audits.

Rule 806.3.4(D)(2)(b)

The Audit Core Team will:

Verify that compensation was calculated properly for all volunteer sellers

1.) The Core Team will evaluate the CSP’s system to be assured it is calculating compensation as dictated in the contract. 2.) Gross compensation figures will be reviewed and verified.3.) For the 2009 Contract Compliance Audits, the Core Team will review and verify that compensation is being properly allocated to the states.

Compensation:

• You may find the manner in which compensation is calculated interesting. Compensation is addressed in Section D of the current contract between the CSPs and SST Governing Board. The compensation formula can be reviewed in section “D.5”, the rate adjustment process is outlined in section “D.6”, and resetting rates annually is addressed in section “D.7”.

Rule 806.3.4(D)(2)(c)The Audit Core Team will:

Verify that appropriate procedures for mapping exist, are in conformance with the mapping requirements, and are followed in the initial mapping setup, as well as during updates and corrections to mapping

1.) The Core Team will evaluate the CSP’s procedures for implementing Mapping. 2.) The Core Team will complete audit steps to document whether product descriptions in the data downloads accurately depict the seller’s invoice level description.

Rule 806.3.4(D)(2)(a)The Audit Core Team will:

Determine the CSP’s level of compliance with the terms of the CSP contract. (Questionnaires and specific tests will be used to assess the CSP’s contract compliance.)

The Audit Core Team will issue questionnaires to the CSPs, each Member/Associate Member State, and the Office of Executive Director addressing various elements of the contract. The completed questionnaires will be analyzed and used as the starting point of the contract compliance audit.

(continued)

The SST Audit Committee has isolated areas of definite audit interest in the CSP contract. The Audit Core Team will specifically look at these areas and complete various compliance audit procedures to assess the CSP’s compliance with the contract.

Rule 806.3.4(D)(2)(a) - continued

Rule 806.3.4(D)(2)(j)The Audit Core Team will:

Compile the feedback reports from the member states, summarize the findings and report to the Executive Director of the Streamlined Sales Tax Governing Board. The summaries must comply with confidentiality restrictions that apply to the SST Governing Board regarding disclosure.

Continued – next slide

For each CSP, the Audit Core Team will incorporate its findings from the contract compliance audit with the feedback reports from the Member and Associate Member States into a final compliance audit package to be issued to the Executive Director of the Streamlined Sales Tax Governing Board.

The Executive Director and the Governing Board will use these audits to evaluate the CSPs for contract renewal.

Rule 806.3.4(D)(2)(j) - continued

Final Audit Report

• Per rule 806.3.5.3(C)

The feedback report on the audit findings that goes to the Executive Director will contain general information on errors found and will not contain specific taxpayer information to ensure the confidentiality of taxpayer information.

Important Dates for Member and Associate Member State Auditors

TodayAudit Core team will submit questionnaire to member/associate member states.

MondayAugust 17,

2009

All questionnaires must be returned to Audit Core Team by end of business today.

MondayAugust 17,

2009

The CSPs will have completed the delivery of the download files of the state specific sales transaction information, exemption information, and tax collection/remittance information for each model 1 seller they performed CSP services for.

Important Dates for Member and Associate Member State Auditors

August 31, 2009

thru December 1,

2009

Member/associate member states will review the sales transaction records provided by the CSP and prepare reports that notify the Audit Core Team of their findings.

The member/associate member state auditors should immediately advise the Core Team if they discover any reporting problems not previously

reported on their state questionnaires.

Important Dates for Member and Associate Member State Auditors

MondayNovember 2,

2009

The Audit Core team will forward to member/associate member states preliminary reports detailing work completed to date and outlining any potential audit adjustment areas that are discovered.

TuesdayDecember 1,

2009

By the end of the day all member/associate member states' Sales Tax Compliance Audit Reports must be forwarded to the Audit Core Team.

Important Dates for Member and Associate Member State Auditors

December 1, 2009

to January 8,

2010

The Audit Core Team will work with the CSPs and the states to resolve any issues that are a result of communication problems or misunderstandings.

January 8, 2010

toFebruary 8,

2010

The CSP will review and comment on the preliminary findings of the compliance audit. Comments will be sent to the Audit Core Team and member/associate member states.

Important Dates for Member and Associate Member State Auditors

February 8, 2010

to February 28,

2010

The Audit Core Team and member/associate member states can amend their findings, if necessary.

Monday March 1, 2010The final contract compliance audit report on each CSP will be forwarded to the Executive Director.

TIME WILL BE PROVIDED AT THE END OF THE WEBINAR

FOR QUESTIONS???

Thank You.&

Good Luck

Audit Core Team:

Steve Krovitz [email protected] 651-556-6017

Bob Muller [email protected] 765-289-8032 ext 236

Scott Elliott [email protected] 509-327-0270

Roger Wright [email protected] 304-558-8523