ANNUAL REPORT 2009 - bancatransilvania.ro · ANNUAL REPORT 2009 Banca Transilvania is the bank for...

103

ANNUAL REPORT 20 09

Transcript of ANNUAL REPORT 2009 - bancatransilvania.ro · ANNUAL REPORT 2009 Banca Transilvania is the bank for...

ANNUAL REPORT

2 0 0 9

ANNUAL REPORT

2 0 0 9

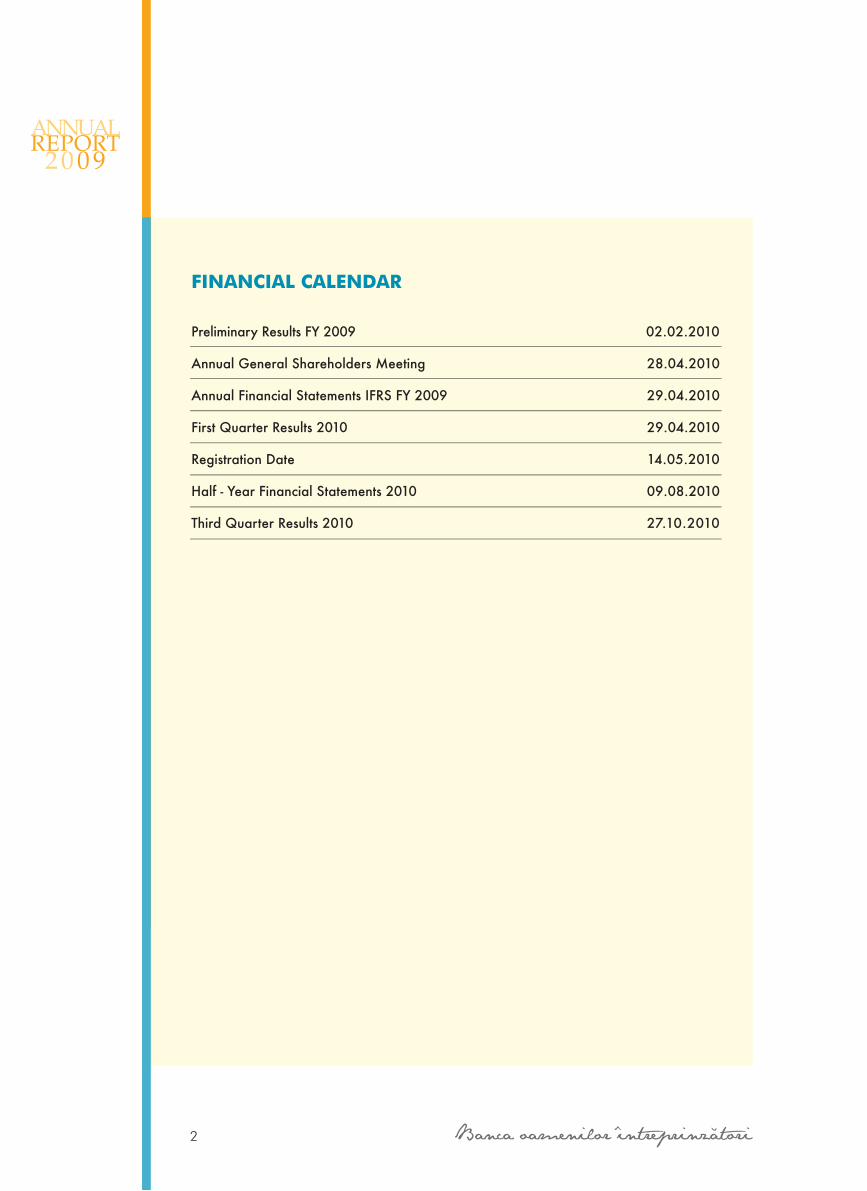

Preliminary Results FY 2009 02.02.2010

Annual General Shareholders Meeting 28.04.2010

Annual Financial Statements IFRS FY 2009 29.04.2010

First Quarter Results 2010 29.04.2010

Registration Date 14.05.2010

Half - Year Financial Statements 2010 09.08.2010

Third Quarter Results 2010 27.10.2010

FINANCIAL CALENDAR

2

ANNUAL REPORT

2 0 0 9

Banca Transilvania is the bank for entrepreneurial

people in Romania.

Our mission, as a privately owned Romanian bank,

is to support the business environment development

through innovative products and services offered

with professionalism. We believe in a mentality

aimed at finding solutions for our clients. There is

soul and energy in everything we do, motivated by

the respect for our clients and a responsibility for

the community.

MIssIoN stAtEMENt

3

ANNUAL REPORT

2 0 0 9Financial Calendar

Mission Statement

Highlights

Chairman and CEO Statement

Corporate & SME Banking

ClubulÎntreprinzãtoruluiRomân(TheRomanianEntrepreneursClub)

Retail Banking

Cards

InternetBanking

The Healthcare Division

Risk Management

Internal Audit System

Compliance

Sustainable Banking

EnvironmentalPerformance

CorporateSocialResponsibility

Human Resources

Marketing & Communication

Public Relations

Operations and IT

Main Subsidiaries

BTLeasingTransilvaniaIFNS.A.

BTSecuritiesS.A.

BTAssetManagementS.A.I.S.A.

MedicreditLeasingIFNS.A.

BTDirectIFNS.A.

Financial Section

Auditor’sReport

tABLE oF CoNtENts

4

2

3

5

6

8

10

12

13

14

16

17

22

23

25

25

26

29

31

33

34

35

35

35

36

37

37

38

39

ANNUAL REPORT

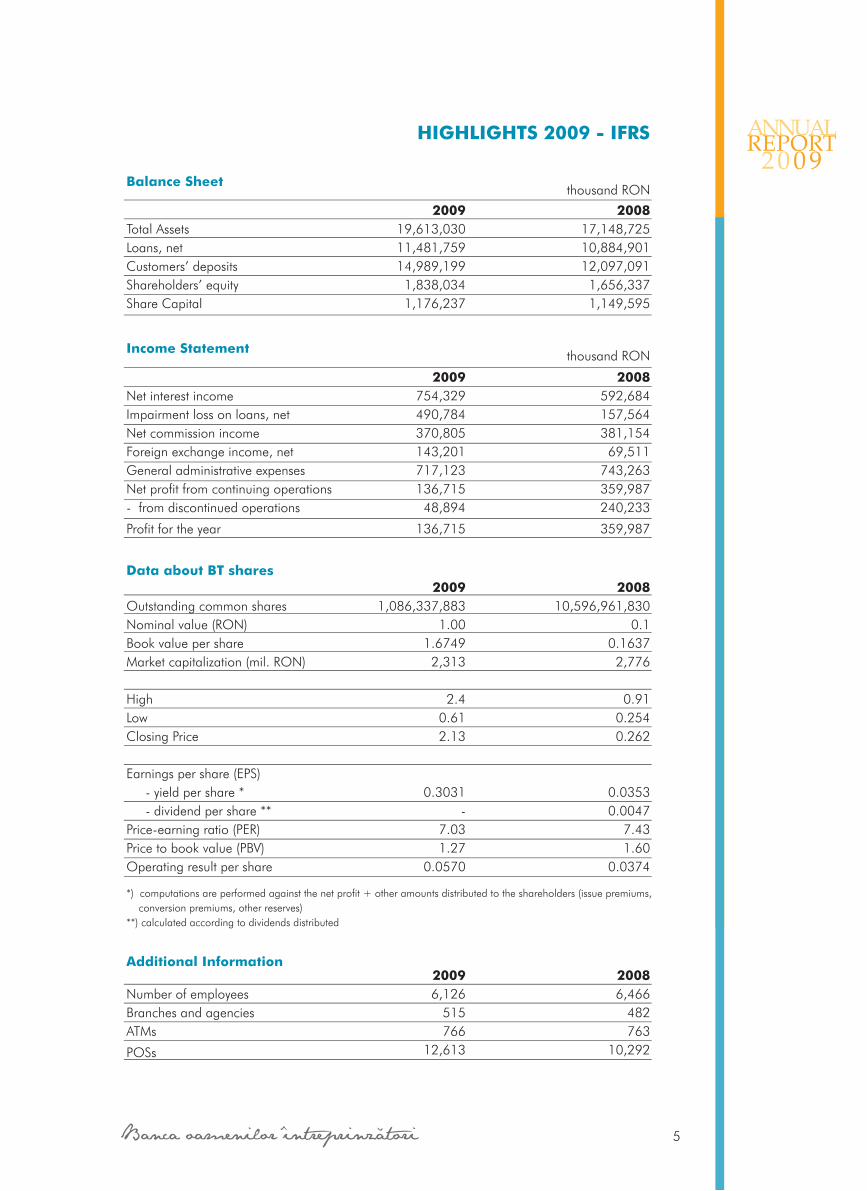

2 0 0 9HIGHLIGHts 2009 - IFRs

Income statement

TotalAssetsLoans,netCustomers’depositsShareholders’equityShareCapital

200919,613,03011,481,75914,989,1991,838,0341,176,237

200817,148,72510,884,90112,097,0911,656,3371,149,595

thousandRON

NetinterestincomeImpairmentlossonloans,netNetcommissionincomeForeignexchangeincome,netGeneraladministrativeexpensesNetprofitfromcontinuingoperations-fromdiscontinuedoperations

Profitfortheyear

2009754,329490,784370,805143,201717,123136,71548,894

136,715

2008592,684157,564381,15469,511

743,263359,987240,233

359,987

thousandRON

Data about Bt shares

OutstandingcommonsharesNominalvalue(RON)BookvaluepershareMarketcapitalization(mil.RON)

HighLowClosingPrice

Earningspershare(EPS)-yieldpershare*-dividendpershare**Price-earningratio(PER)Pricetobookvalue(PBV)Operatingresultpershare

20091,086,337,883

1.001.67492,313

2.40.612.13

0.3031-

7.031.27

0.0570

200810,596,961,830

0.10.16372,776

0.910.2540.262

0.03530.0047

7.431.60

0.0374

*)computationsareperformedagainstthenetprofit+otheramountsdistributedtotheshareholders(issuepremiums,conversionpremiums,otherreserves)**)calculatedaccordingtodividendsdistributed

NumberofemployeesBranchesandagenciesATMs

POSs

20096,126

515766

12,613

20086,466

482763

10,292

Additional Information

Balance sheet

5

ANNUAL REPORT

2 0 0 9

Chairman’s and Chief Executive officer’s statement

Everybodyknewthat2009wouldbeachallengingyear.Strategiesneededtobereconsidered,

businessmodelsreviewedandworkingtoolsrenderedmoreefficient.

2009hasbeena yearof consolidation forBancaTransilvania.Ouroperatingprofitwas96

percenthigherthanin2008andthecost-incomeratioimprovedto55percentversus70percent

theyearbefore.

Liquidityremainedatcomfortablelevel,withloantodepositratiobelowoneandastrongposition

intermsofraiseddepositsonthedomesticmarket.Wemaintainedcapitalrequirementsathigh

standards(14percent),significantlyabovethe8percentminimumlimitimposedbytheNational

RegulatoryAuthority.

Tocopewithbusinessenvironmentuncertainties,weimplementedacoherentandaggressive

provisioningpolicy,withenhancedprotectivemeasuresovertheloanportfolio.Additionalloan

lossprovisionsagainstfutureeconomicdeteriorationwerecreated,non-deductiblesaccounting

for17.6percentoftotalprovisions,whileEUR126millionwasthetotalamountallocatedfor

theincreaseinnetriskcost.

BancaTransilvaniarealizedthattimehascometoadapt,reinforcingtherangeofservicesand

making room for innovativebusinessproducts. In this context, flexibilityandcustomer facing

solutionswerekeywordsforBTtoreclaimmarketshare,meetrevenueandmargintargets.

The Anti-Crisis Platform was designed, setting the foundation for opportune services, much

neededinthemarketplacefloodedbyconcerns.Wefacilitatedaccesstofinancingresources,

improvedcash-flowandreducedoperationalcosts.

In this unsettled economic environment it is important to create strong partnerships with the

public sectors. The National Guarantee Fund for SMEs is our business associate in two

importantprojects.ApremiereontheRomanianbankingmarket,Creditul Gata Garantat-the

ReadySecuredLoan-isaco-brandedproductdesignedtosolvetheentrepreneurs’liquidityand

6

ANNUAL REPORT

2 0 0 9

All in all, we can say that 2008 was a year of strategy adjustment, BT consolidatingits market position. Efficient management of operational expenses, increased riskmanagement and constant communication with the market were just a few mitigationmeasures taken to tackle the effects generated by the economic upheaval.

As for 2009, discussions will revolve around the deployment of thecapital we hold, the duration and sources of our funding, the qualityof the assets. We will continue to monitor the soundness of loanportfolio and aspects pertaining to liquidity and risk management.We will pay great attention to cost reduction and try to constantlymould on market realities.

The bank and its clients are part of the real economy; therefore BT isnot immune to the crisis. However, being flexible, prudent andcapable to adjust our business model to the new market conditions,we feel that we will be able to safely pass these turbulent times.

Moreover, counting on the valuable support of our strategic partnersand shareholders, we remain committed to sustain the localeconomy, being the largest privately-owned bank with majorityRomanian capital.

Horia Ciorcila Robert C. RekkersChairman Chief Executive Officer

7

collateraldifficulties,providingfinancingbasedonstateguarantees.Thesecondproject-Prima

Casa- isaprogramcreatedbytheRomanianGovernment inordertoexpandthemortgage

lendingpace.BTenrolledintheprojectandplacedEUR30millionintotal.

Another aspect revealed by the crisis was the importance of financial support from the EU,

materializedintheformofstructuralfunds.Furthertothese,BThasdecidedtosetupanother

importantplatform- theEU Structural Funds Platform.Ourclientsareprovidedwithadvisory

servicesandco-financingforbusinessturnaroundornewinvestmentprojects.

All our 2009 endeavors benefited from the EBRD’s ongoing support as shareholder and

businesspartnerandwewelcomed thearrivalofnewkey shareholders, IFC -aWorld Bank

Division-andBankofCyprus.

Steeledbyachallenging2009,wecautiouslylookat2010.Weareawarethatthiswillnotbe

aneasyyear,butBT,astheBankforEntrepreneurialPeople,willcontinuetoactwithcourage,

intelligenceand responsibility, relyingonsoundstakeholdersandpartners,professional team

players,localapproachandloyalcustomers.

HoriaCiorcila RobertC.Rekkers

Chairman ChiefExecutiveOfficer

7

ANNUAL REPORT

2 0 0 9

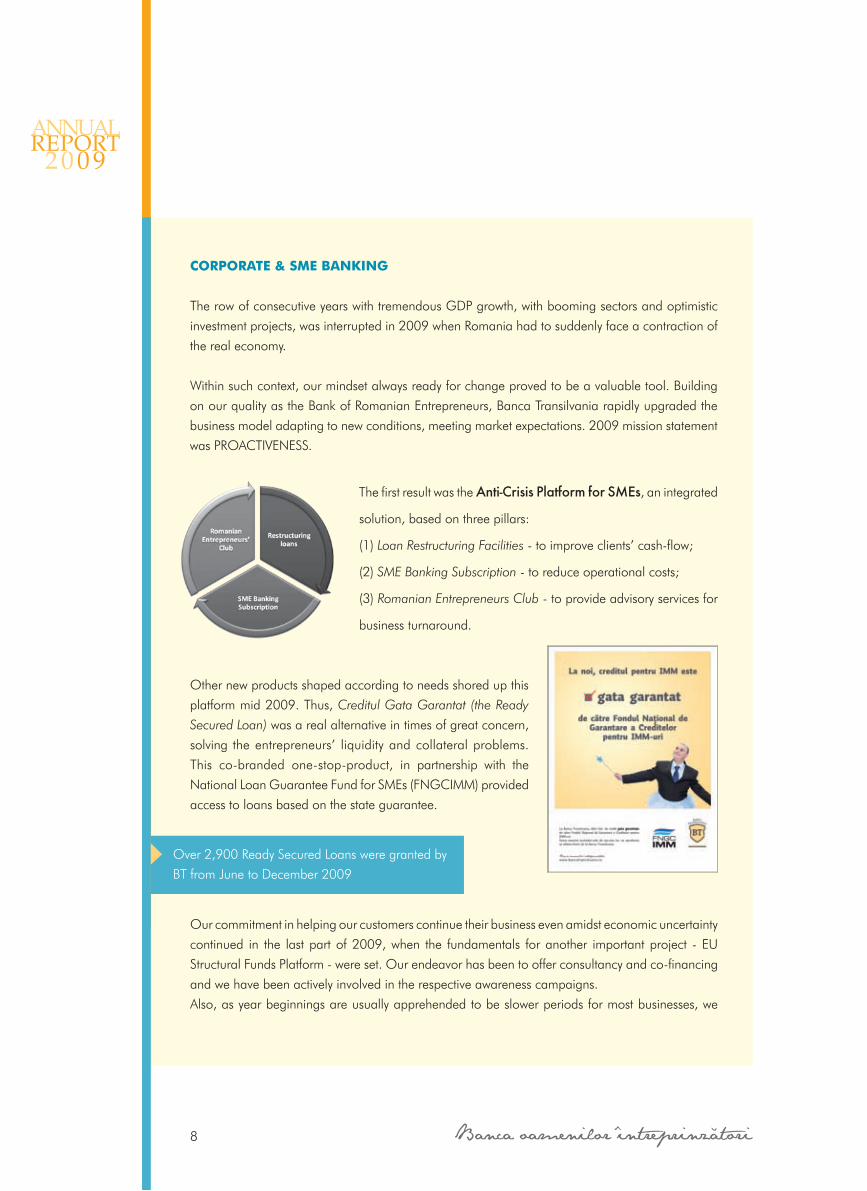

CoRpoRAtE & sME BANkING

TherowofconsecutiveyearswithtremendousGDPgrowth,withboomingsectorsandoptimistic

investmentprojects,wasinterruptedin2009whenRomaniahadtosuddenlyfaceacontractionof

therealeconomy.

Withinsuchcontext,ourmindsetalwaysreadyforchangeprovedtobeavaluabletool.Building

onourqualityastheBankofRomanianEntrepreneurs,BancaTransilvaniarapidlyupgradedthe

businessmodeladaptingtonewconditions,meetingmarketexpectations.2009missionstatement

wasPROACTIVENESS.

ThefirstresultwastheAnti-Crisis Platform for SMEs,anintegrated

solution,basedonthreepillars:

(1)Loan Restructuring Facilities-toimproveclients’cash-flow;

(2)SME Banking Subscription-toreduceoperationalcosts;

(3)Romanian Entrepreneurs Club-toprovideadvisoryservicesfor

businessturnaround.

Othernewproductsshapedaccordingtoneedsshoredupthis

platformmid2009.Thus,Creditul Gata Garantat (the Ready

Secured Loan)wasarealalternativeintimesofgreatconcern,

solving theentrepreneurs’ liquidityandcollateralproblems.

This co-branded one-stop-product, in partnership with the

NationalLoanGuaranteeFundforSMEs(FNGCIMM)provided

accesstoloansbasedonthestateguarantee.

Ourcommitmentinhelpingourcustomerscontinuetheirbusinessevenamidsteconomicuncertainty

continued in the lastpartof2009,when the fundamentals foranother importantproject -EU

StructuralFundsPlatform-wereset.Ourendeavorhasbeentoofferconsultancyandco-financing

andwehavebeenactivelyinvolvedintherespectiveawarenesscampaigns.

Also,asyearbeginningsareusuallyapprehendedtobeslowerperiodsformostbusinesses,we

Over2,900ReadySecuredLoansweregrantedby

BTfromJunetoDecember2009

8

ANNUAL REPORT

2 0 0 9

launchedIesirea din iarna (Getting through winter)asolutionofferedtoimproveclients’cash-flow,

anddealwithadversebusinessconditionsduringthefirstmonthoftheyear.

Besidesadaptingourbankingproductstohelpclientsweatherthecrisis,wealsostreamlinedthe

bank’sstrategyintermsofcustomerriskprofileinordertobuildamorerobustSMEclientbaseand

acquirecorporateclientswithseminalbusinessmodels.

Alltheseactionsprovedsuccessful,thenumberofcorporateandSMEclientsgrewlastyearby6%

to194,100,corporateplacementsbeing14%abovethe2008value,whileintermsofdeposits,

werecordedayear-on-year17%growth.

Furthermore,thepreviousyearmissionstatamenttocapitalizeourpositionasoperationalfriendly

bankwaskept.Thus,wemanagedtohaveoneofthebestcashcollectionservices(over-the-counter,

ATM,directdebit),but,mostimportantly,wehavebecomeavaluedpartnerforRomanianutility

suppliers. Invoicepayment cooperationagreementswithmajornationaland regional suppliers

weresigned,creatingtrafficinBT’sunitsandsubsequentbusinesswithourretailcustomers.

Inallouractionsweaimed to improveoperational efficiency in sales,by valuingour relevant

expertiseinSMElendingandbycultivatingtheentrepreneurialspiritofoursalespeoplespecifically

intheareaofowninitiativeandabilitytoidentifycross-sellingopportunities.

Corporate Loan Portfolio as at 31.12.2009

40.4%

35.3%

0.3%

24.0%

39.7%

41.1%

0.4%

18.8%

Corporate Loan Portfolio as at 31.12.2008

9

ANNUAL REPORT

2 0 0 9

Clubul Întreprinzãtorului Român - CIR (the Romanian Entrepreneurs Club)

Trainingsessionsontopicsofinteresttothebusinesscommunity,networkingprograms,assistance

inapplyingforEUstructuralfundsandfinancial&bankingconsultancyserviceswerefrontlinesin

our2009activity.

The Club counted almost 12,000 members at the end of 2009, with approximately 1,800

newcomersovertheprevious12months.

In2009,theClubappliedforEUstructuralfunds,eitherasmainapplicantorasco-participant.

Asmostoftheprojectswereapprovedwemanagedtoraisesignificantfunds,provingonceagain

thatweactuponourstatements.

The website www.btclub.ro was upgraded, with new tools and functions in order to increase

attractivenessandaccessibility.

InJune2009,theproduct“Site-ul meu pe BT Club” (My site on BT Club)waslaunchedfor

companiesthatdidnothavetheirownwebsite.Asaresult,213webpagesweredesignedandare

currentlyhostedontheCIRsite.

Furthermore, Google partnered with CIR to grant 100 RON vouchers for Google AdWords

campaigns,whichwereusedbyapproximately130companies.

training programs and Events

Morethan360trainingsessionswereorganized,sincetheClubwasestablishedthreeandahalf

yearsago.41eventswereheldin2009andprofessionalspeakers,eitherfromBancaTransilvania

orconsultingcompaniestookthefloor.6,000participantsattendedtheseseminarsin21towns,

gettingacquaintedwithboththetraditionalbusinesstopicsandthechallengesimposedbythe

21stcentury.

Feed-backprovidedbyparticipantsencouragedustostrengthenoureffortsinthisarea.Thus,the

Clubestablished“mobileconsultingoffices”insixtowns,offeringsupporttoSMEswhichwould

liketotakeadvantageoftheEUstructuralfunds.

10

ANNUAL REPORT

2 0 0 9

Furthermore,CIRenteredaspecialpartnershipwithGoogle,organizing“GooglecomestoCluj”

event,withlivebroadcastingontheClub’swebpageandover1,500Internetuserstunedin.

The Club also organized 4 events under the auspices of the “First European SME Week”

(May6-14,2009)andaspartofthe“GlobalEntrepreneurshipWeek”(November16-22,2009).

Alltopicswerereceivedwithgreatinterest,especiallytheEUstructuralfunds.

the Networking program

Theprogramwaslaunchedbackin2008,supportingnationwidenetworkingamongCIRmembers

andofferingexclusivebenefits.

Accreditedmembersbenefitedfromdiscountsthatrangedfrom1%to50%,grantedbyover130

partnersacrossthecountryandcoveringalargevarietyofproductsandservices.

partnerships

Newcollaborationswithconsultingfirmswereestablished,amongthemEurocenterManagement

Network,PNOGrantConsultants,Ecocare,CBCTraining,RomanianTrainingInstitute,Codecs,

DeKlausen,Rentrop&Straton,EcartorShoreBankInternationalandUPCBusiness.Thelatter

co-sponsoredthreeofthe2009events.

Consultancy and newsletter

TheClubprovidesbothfinancialandbankingconsultancy,aswellasotherservicestoitsmembers,

viathetollfreenumber0800800466,bye-mailandthroughitswebsitewww.btclub.ro.

Also,awiderangeoftopicsofinterestforentrepreneursaroundthecountryareapproachedand

debatedinnewsletterssenttotheClub’smembers.

11

ANNUAL REPORT

2 0 0 9

REtAIL

Loans and Deposits, simple products

Overthepast10years,BancaTransilvania’sfocusonRetailBankinghasbeenreinforcedyearafter

yearsothatendof2009,theretailcustomerbasecountedonemillioneighthundredthousand

clients.Theextensivegrowth in termsofclientnumberwascomplementedby intensivegrowth

strategies,theaveragenumberofproductsperclientdevelopingfrom2.12to2.37,thatisa12%

increase.

Weprovidedloananddepositpackageswithfeaturestriggeredbytheeconomicbackground.

Newmortgageloansandupdatedhomeequitylendingproductswerelaunched,aimedatraising

retailcustomers’appetiteforcredit,giventheabruptconsumptiondownslope.

Moreover,tosupplyourclientswiththe

necessary funds and simultaneously

sustain the real estate market, we

enrolled, in partnership with the

National Guarantee Fund, in the

Prima Casa Program. As part of this

project, we managed to grant 753

loans,equivalentofEUR30million.

In 2009, people’s behavior faced

amigration from consumerism to savings. Backed by our retail business focus, expertise and

reputation,wecontinuedtoembraceadispersedliquiditymodelandaheterogeneouscustomer

breakdown,preservingaloantodepositratioconstantlybelowone.Furthertothis,during2009,

our retail deposits grew by 24%, standing for 66% of total

deposits.

Combined services, lined up with market requirements

In 2009 we expanded the channels to insurance products.

The Savings and Protection Plan,launchedinpartnershipwith

AEGON Romania, met the requirements of a savings-prone

and risk-averse market. This co-branded financial solution

combinedtheadvantagesofasavingsaccountwiththoseofa

lifeinsurancefacilitywithinacustomizedinvestmentprogram.

12

2009 Retail Loan Portfolio

17.01%

6.71%

30.42%

20.93%

20.32%2.63%

1.98% housing

mortgage

home equity

consumer loans

card loans

car loans

other

ANNUAL REPORT

2 0 0 9

Card platform

BeingthefourthlargestissuerinRomania,wemaintainedourkeyplayerpositionwithstraightforward

andclient-friendlyproducts.14%marketsharereflectsthatcardshaveremainedastayingpower

forBT,withaportfolioof1,700,000.Morethanthat,wearemarketleadersforpremiumcards

undertheVisabrand(Platinum&Gold),withalmost10,000issuesendofDecember2009.

Due to an extensive purpose range, VISA ELECTRON gained the status of Daily Card. The

1,200,000portfolioandthe22.7%increaseinPOSpurchasesduringthesecondhalfof2009

wereamongthemainreasonstoreceivetwoimportantawardswithintheNOCASHGALA,9th

edition:The Best Sold Debit Card & The Shopping Card of the Year.Furthermore,Visaconfirmed

thecommercialvalueofourVisa – Your Daily Cardusagecampaign,byselectingBTforasuccess

storycasestudy.

13

2005 2006 2007 2008 2009

642,933893,677

1,706,8741,609,8731,181,318

Number of BT CARDS issued Number of Issued Cards

1,181,318

642,933

0200,000400,000600,000800,000

1,000,0001,200,0001,400,0001,600,0001,800,000

2005 2006 2007 2008 2009

1,706,8741,609,873

893,677

salary cards

premium cards

MasterCard Forte

EURO<26

Business cards

MasterCard vs Visa

BT Cards Portfolio 2009

0

200,000

400,000600,000

800,0001,000,000

1,200,000

1,400,0001,600,000

1,800,000

2006 2007 2008 2009

MasterCard

Visa

1%

8%

5%4% 2%

80%

Maestro Direct

Credit Cards vs. Debit Cards 2009

Number of ATMs and POSs

2,850

4,646

10,292

12,613

356 528 675 763 766

7,321

0

2000

4000

6000

8000

10000

12000

14000

2005 2006 2007 2008 2009

POSsATMs

91%

9 %

credit cards

debit cards

Credit Cards vs. Debit Cards 2009

Number of ATMs and POSs

2,850

4,646

10,292

12,613

356 528 675 763 766

7,321

0

2000

4000

6000

8000

10000

12000

14000

2005 2006 2007 2008 2009

POSsATMs

91%

9 %

credit cards

debit cards

ANNUAL REPORT

2 0 0 9

In its turn,MasterCard is theothermilestone

inourportfolio,withatotalof325,000cards

reflectedparticularlyinthe144,000issuesin

2009.

Besides the cards for retail customers, we

developed VISA BUSINESS SILVER CREDIT

CARD & VISA BUSINESS GOLD CREDIT

CARD. These cards provide easy access to

money for any type of payments, as well as

additional advantages such as travel assistance services, emergency cash, medical and legal

assistance.

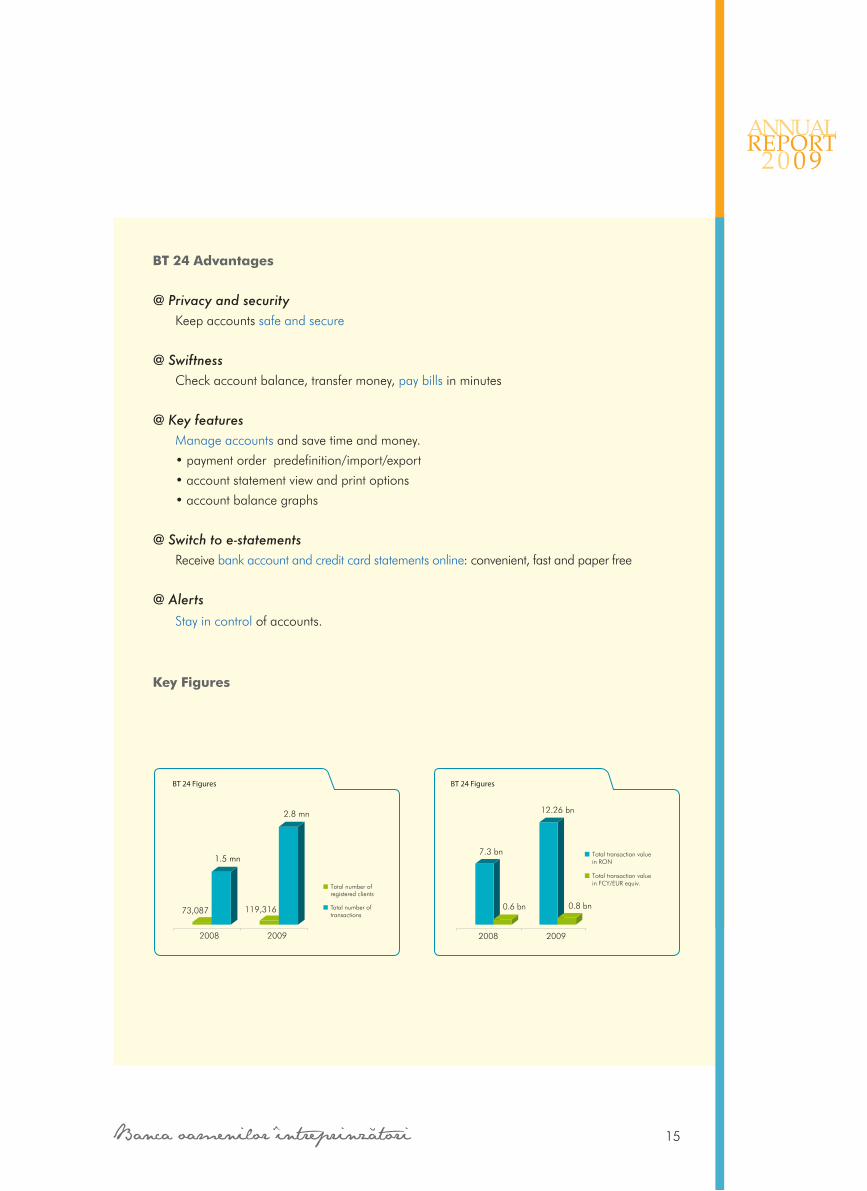

Internet Banking - Bt 24 OurInternetBankingprovideseasyaccesstobankingservicesandproductsandincludesmany

featurestohelpcustomersmanagetheiraccountsonline.

Basedon feedbackandsuggestionsprovidedbyourcustomers,wecontinued to improve the

relevanceparametersofdisplayedinformationintheapplicationreports,especiallywithrespectto

cardaccountsandpaymentstatus.Also,weextendedthenumberofpredefinedpaymentorders,

whichsimplifiesthepaymentprocessandbringscostreductionforclients.

ThenumberofInternetbankingsubscribersincreased1.6

times as compared to the previous year, reaching over

127,000associateusersforanumberofcloseto119,000

subscribers.

Ourclients’constant interest inInternet-Bankingusageis

confirmedbythenumberoftransactions,whichincreased

bymore than80%in2009against2008,aswellasby

thevalueoftransactionsprocessedviaBT24whichgrew

rapidlywithapproximately50%ascomparedto theyear

before.

14

salary cards

premium cards

MasterCard Forte

EURO<26

Business cards

MasterCard vs Visa

BT Cards Portfolio 2009

0

200,000

400,000600,000

800,0001,000,000

1,200,000

1,400,0001,600,000

1,800,000

2006 2007 2008 2009

MasterCard

Visa

1%

8%

5%4% 2%

80%

Maestro Direct

ANNUAL REPORT

2 0 0 9

Bt 24 Advantages

@ Privacy and securityKeepaccountssafeandsecure

@ SwiftnessCheckaccountbalance,transfermoney,paybillsinminutes

@ Key featuresManageaccountsandsavetimeandmoney.

paymentorderpredefinition/import/export

accountstatementviewandprintoptions

accountbalancegraphs

@ Switch to e-statementsReceivebankaccountandcreditcardstatementsonline:convenient,fastandpaperfree

@ AlertsStayincontrolofaccounts.

key Figures

•

•

•

BT 24 Figures BT 24 Figures

73,087

1.5 mn

119,316

2.8 mn

Total number of registered clients

Total number of transactions

2008 2009 2008 2009

7.3 bn

0.6 bn

12.26 bn

0.8 bn

Total transaction value in RON

Total transaction value in FCY/EUR equiv.

15

BT 24 Figures BT 24 Figures

73,087

1.5 mn

119,316

2.8 mn

Total number of registered clients

Total number of transactions

2008 2009 2008 2009

7.3 bn

0.6 bn

12.26 bn

0.8 bn

Total transaction value in RON

Total transaction value in FCY/EUR equiv.

ANNUAL REPORT

2 0 0 9

tHE HEALtHCARE DIvIsIoN

In2009BancaTransilvania’sHealthcareDivisioncontinued

tosupporttheRomanianhealthcareprofessionalsoffering

a customized range of products and services via a

specialized teamofphysiciansandfinancialconsultants.

The initial packages -Rezident, Specialist, Praxis –were

supplemented with other specialized products targeting

dentaltechnicians.

OurHealthcareDivisionendedtheyearwithacustomer

baseofmorethan18,000clients,managingaportfolio

ofover8,000loanstotalingaboutEUR100million.

ThebusinessmodelofourHealthcareDivisionrelieson:

•apackageoffourlendingproductsexclusivelydedicatedtotheHealthcaresector;

•specializedsalespeople-doctors&financialconsultants-andcreditanalysts;

•anetworkofconsultingcompanies,whichoffersupportforopeningamedicalpracticeor

receivingtheauthorizedindividualstatus;

•anetworkofaccountingfirms,offeringfiscalassistance.

In2009BTwastheofficialbankoftheRomanianSocietyofCardiologyandRomanianHeart

Foundation, for the support offered in fighting cardiovascular diseases. Moreover, during the

Medica GalaorganizedbytheRomanianCollegeofPhysicians,wewererewardedwithThe Best

Banking Initiativeprize.

AnotherimportantachievementfortheHealthcareDivision

wastheEUR50millionfacilityfromIFCtofinancetheprivate

healthcaresectorinRomania,availablealsotomediumsize

clinics,andindividualpractitioners.Thiscreditlineunderlines

thatBancaTransilvania’sendeavortoassisttheimprovement

of the Romanian healthcare system is recognized by top

internationalplayers.Furthermore, thecontributionsof the

HealthcareDivisiontotheoperational incomeofthebank

havebecomesignificant.

16

ANNUAL REPORT

2 0 0 9

RIsk MANAGEMENt

2009wasmarkedbytheglobaleconomiccrisis.Mostbankssufferedfromthevolatilemarket

surroundingsand thebulkof the corporate sector showedpoor financial results inall sectors

duetothesharpdownturnoftherealeconomy.WhiletheeconomiesofFranceandGermany

emergedfromrecessionfasterthanexpected,otherWesternandCEEcountriesendedtheyear

withsevereshrinkagesofGDPs.

The international banking system was under constant pressure, caused by substantial non-

performingloanswhichhadanadverseeffectonthelendingcapacity.Tacklingthischallenge

became themainconcernofbanksallover theworld.CentralBanks interfered,adjusting the

monetarypolicy,reducinginterestratesanddevelopingprogramstoensurethenecessaryliquidity.

Butastheyearendedconcernsaboutsovereignandcommercialdebtscontinuedtofuelanxiety,

triggeringacontinuedreluctanceofinvestors.

Within this macroeconomic context, the Romanian National Bank initiated several support

measurestoensuretheliquidityoftheRomanianbankingmarket,keepinginflationandexchange

ratevolatilityundercontrol.

Ifgovernmentsand financial supervisingauthoritiesplaced theirattentiononmeasuresmeant

tocombatandbalancesystemicmalfunctions,BancaTransilvaniaadapted itsbusinessmodel

enhancingtheriskmanagementframeworktobetterassisttheorganizationtoadequatelyprocess

andreportriskrelatedinformation.

Formally,BancaTransilvaniaclassifiesriskintothefollowingmaincategories:(1)creditrisk,(2)

liquidityrisk,(3)marketriskwithitsmaincomponents:(3.1)currencyriskand(3.2)interestrisk,(4)

operationalriskand(5)reputationalrisk,(6)compliancerisk.Infact,thebank’sendeavorsareto

assesandrecognizethepotentialriskrelatedtoanysingletransactionoroperation,quantifying

theirimpactintermsofcapitalrequirements.

Severalscenariosandtheirimpactoncapitaladequacywereregularlyscreenedandoverall2009

targetsweredefinedaccordingly.

Themainriskmanagementprinciplesfollowedbythebankwhendefiningitsyearlystrategy:

•Financialstabilityprotection:limitingtheimpactofpotentialadverseeventsoncapital

andincome;

•Independentperspective:riskmanagement,aswellasthelegalandcompliancefunctions

operatefullyindependently,ensuringtheintegrityofthebank’scontrolprocesses;

•Investmentsdiversificationtoavoidriskconcentration;

•Uniformapproachofriskmonitoringwithinthebankanditssubsidiaries;

•Constantreviewofriskscenariosadaptedtocurrentsituations.

17

ANNUAL REPORT

2 0 0 9

Risk Management system

Credit risk

Oneof themaindecisions promptedby the economic surroundings in the first part of 2009

waslinkedtoBT’slendingapprovalprocesswhichwasshiftedtoheadquarterlevel,thatiscredit

authorityatbranchnetworklevelwastemporarysuspended.Afterthenecessaryaccommodation

processtothenewmacroeconomicconditionswascompleted,i.e.adjustmentoflendingpolicies,

product termsandconditionsandeligibilitycriteria, thebranchnetwork regainedgradually its

lending approval limits. Today, additional monitoring and early warning systems have been

implemented,toavoidadverseeffectscausedbynegativedevelopmentsoftheexisting,aswellas

newlyacquiredportfolio.

Thebasiccreditriskmanagementcomponentssuchas:

•individualcounterpartyratingsystem;

•transactionriskassessmentsystem;

•regional/sectoralconcentrationlimits;

•pricingmethodologybasedonrisks;

wereenhancedby:

•anactivemanagementofloanportfolio;

•newpost-approvalmonitoringsystems(reports&on-sitevisits);

• stringent credit risk provisioningpolicy, includingnon-deductibleprovisions (from the

fiscalperspective),countingfor17.6%oftotalloanprovisions,accordingtoRAS.

Market risk

Inordertoreducemarketrisksinherenttofinancialoperations,theBankadoptedaprudentbut

proactiveapproachtoprotectexpectedtransactionprofitsfromanymarketvolatilityininterestand

exchangerates.

18

Risk Management Department

Corporate Credit Risk Analysis

Risk Inspection

Department

Risk and Monitoring

Department

Operational Risk

Department

Risk Analysis and

ReportingOffice

Operational Risk Monitoring and

InspectionOffice

ANNUAL REPORT

2 0 0 9

BancaTransilvaniafine-tuneditssecuritiesportfoliobyconcentratingonlessvolatile,liquidand

well-dispersed(intermsofmaturityandriskprofile)assets.

Although,BancaTransilvaniadoesnothaveaValue-at-Risksystem,simulations(stresstests)are

constantlyperformedtoprepareforunforeseeablemarketswingsandtoproperlymanagethis

risk.Theroleofstresstestingistoenhanceapro-activemanagement,especiallyastheprofileset

bythebankforthemarketriskis“low/conservative”.Asageneralstrategy,BToptsforplainvanilla

operations,strictlylimitinganyopenpositions.

During2009theNationalBankofRomaniaactivelyusedoneofitsmainmonetarylevers,reducing

theinterestreferenceratefrom10%to8%andpreparingafurtherdecreaseinJanuary2010to

7.5%.Thesedecisions,intendedtostimulatetheeconomiccome-back,wereimmediatlytranslated

by Banca Transilvania which acted as trend setter among the commercial banks, diminishing

lendingrates.

Liquidity risk

Theannualliquiditymanagementstrategysetsprudentialratiolimitsandguidelinesforthebalance

sheetstructure,soastoensurecompliancewiththebestpracticesandthespecificnorms,while

balancingthemaintenanceofsufficientliquiditywithprojectedoperationalprofit.

Liquiditymanagementrelieson3components:

•Strategic Component-balancesheetstructureandannualliquiditymanagementstrategy,

withoptimallevelsofratiosassumedbythebankduringtheyear;

•Management Component-monitoringandapprovingtheshortandmediumtermactions,

onamonthlyandquarterlybasis;

•Operational Component-dailyactionswithinpre-definedcompetencelimits;

IntermsofliquidityratiosobservedbyBT,especiallycashandcashequivalents,liquidassetsto

totalassetsandtheloan-to-depositratioareofutmostimportance.Theirlevelsarepermanently

monitoredand theAssetsandLiabilityCommitteemeetsanddiscussesonaweeklybasis the

actionstobetakentokeeptheseratioswithinthelimitssetbytheannualliquiditystrategy.

Fromaliquidityriskperspective,makinguseofitslargenetwork,thebankalwaysfocusedonraising

retaildepositsinsteadofwholesalefunding.BTtraditionallyreliedonthisbroadretaildepositors’

base,constantlymaintainingaloantodepositratiobelowone.

19

ANNUAL REPORT

2 0 0 9

Furthermore,2009wasmarkedbyashiftinconsumerbehavior,triggeredbythefastexpanding

crisis. In thisclimate,peoplespent lessandsavedmore.Thisnewsituationwasclearly toBT’s

benefit,causingretaildepositstorecordastaggeringincreaseof22%yoy.

Moreover, the National Regulatory Authority reduced the minimum reserve requirement on

deposits both in RON and foreign currency, making available more liquidity to the domestic

economicsystem.Preferringasoundriskprofile,BToptedforsafeandliquidinvestments,placing

availablefundsinTreasuryBillswithanadequatematuritymix,consequentlyboostingtheweight

ofliquidassetsintotalassets.

operational risk

BTdevelopedan internalmechanism toautomaticallygenerate reportsonanyevent thatcan

beclassifiedaccording tooperational riskdefinitionsbasedon itsownoperational riskevents

statistics,national regulations, international standards, recommendationsand systemstatistical

data.

Besidestheelectronicmonitoringtoolsverifyingthecompliancewithoperationalriskmanagement

procedures,aspecializedteam,partoftheOperationalRiskDepartment,performson-sitecontrols

ratingthequalityofoperationalriskmanagementateachunit/department.

Banca Transilvania is continuously building new features to its operational risk management

system:

•Ensuring that thebank-levelpoliciesandproceduresarewrittenaccordinglywith the

operationalriskmanagementprinciplesandcontrols;

• Performing operational risk assessment for the bank’s products and processes and

identifyingtheaggregatelevelofresidualriskfortheseelements;

•Modelingandmaintainingthebusinesscontinuityplan;theprimarysolutionsite(Data

Center)isfullybackedbythesecondaryone(DataRecoveryCenter);theDisasterRecovery

Site isabletosustainall theBank’smainactivities;specificbusinesscontinuityplansfor

eachsubsystemareinplacetestedonaregularbasis;

•Continuouslyenhancingoperationalriskmanagementforbettercapitalallocation;

•Limitingtheeffectsofoperationalrisk,viaspecificinsurancepolicies.

In termsof capital allocation to cover theoperational riskourbankused for2009 thebasic

indicatorapproach(BIA).

20

ANNUAL REPORT

2 0 0 9

Reputational risk

TheefficientmanagementofreputationalriskrepresentsakeymarkerofBT’sstrategy,impacting

thebank’sfinancialpositionatalessforeseeablelevel,onshort,mediumandlongterm.

Monitoringof this typeof risk isbasedonspecific ratiosand takes intoaccount the reporting

of reputational riskeventsaffecting themanagementandsupervision functionof thebank.By

adoptingsuchmeasures,BT takesaction towardsanefficientmanagementofpotentialevents

generatingreputationalriskandsetsupclearobjectivesinordertocounteractthisrisk,toprevent

brandawarenessdepreciationandlossofcustomerconfidence.

Compliance risk

Theyear2009wasimpactedbytheNBRprojecttargetingtheimplementationofcreditinstitutions’

activitymanagementframework,theinternalprocessofcapitaladequacyassessment,aswellas

outsourcingconditions.

TheelementofnoveltybroughtbythisregulationapprovedinSeptember2009isthedefinitionof

compliancefunctionandofcompliancerisk.

Compliance risk awareness has determined to rethink organizational and management

structuresbycreatingthecompliancecoordinationfunction,bydraftingandapplyingassessment

methodologies forcompliance risk,byusingactivityperformance ratiosandbyassigningnew

complianceriskresponsibilitiesrelatedtothemanagementandsupervisionfunction.

TheimplementationofthisprojectistobefinalizedbytheendofH12010.Thiswillrendermore

efficient thecompliance riskmanagementprocess,as it isdefinedby theNBRRegulationno.

18/2009.

21

ANNUAL REPORT

2 0 0 9

INtERNAL AUDItsYstEM

Banca Transilvania’s Internal Audit Department conducts the internal audit of the Group’s

operations,contributingtotheoptimalmanagementofallsystems.TheDepartment’sactivities

arebuiltontheAnnual Audit PlanapprovedbytheBoardofDirectors.

TheAuditDepartmentensurestheproperconductoftheGroup’soperations,beingresponsible

fortheoverallsupervisionofinternalsystems.

Theaudit unitwithin Banca Transilvaniaworks to apply best practices, performing risk based

auditsonpastdatainspections.Auditsarenotonlylimitedtoverifyingandcontrollingdeficiencies,

buttheyalsopointoutcomplianceandriskmanagementproblemsandmakerecommendations

forrequiredfutureactions.

Audit Reporting and subordination

TheAudit Committeewasestablishedtostreamlinetheauditprocess.Thecommitteemeetsevery

monthanddiscussesimportantmattersrelatingtointernalauditing,basedonreportsprepared

bytheauditunit.Functionally,theauditreportsarehandedoverbothtotheAuditCommitteeand

ExecutiveManagementtoassessthefindingsandprovidethebestlinesofreaction.

The internal audit procedures are designed and updated to ensure the communication flow

betweentheBoard,AuditCommittee,thebank’sExecutiveManagementandtheexternalfinancial

auditor.

22

GeneRAlShARehOldeR’SMeetInG

BOARD OF DIRECTORS

Executive Management Committee

Audit Committee

InternalAudit

Department

ExternalAuditor

Committeefor InternalAssessment

ANNUAL REPORT

2 0 0 9

Internal Audit principles within Banca transilvania

Permanence

• Independence

• Objectivity & Impartiality

• Integrity & Professional Competence

• Confidentiality

Internal Audit Ratings within Banca transilvania

•Excellent –risks&processesarecorrectlycontrolled

•Satisfactory–minorproblems,risks&processescontrolledadequately

•Marginally satisfactory-significantproblems,stillacontrollevelofrisks&processes

•Unsatisfactory –seriousproblems,risks&processescontrolledinadequately;

Unacceptable –majorproblems,risks&processesarenotcontrolled

CoMpLIANCE

Anti-Money Laundering, know-Your-Customer & Counter terrorism Financing Legislation

Thecrisishasmadecertainfinancialsystemsmorevulnerabletomoneylaunderingandterrorist

financingthreats.Inthisgloomycontext,theriseof“intelligent”criminalsandmoneylaunderers

renderedsuchactivitiesmoreandmoredifficulttodetectinspiteoftheirapparentlegitimacy.

Compliance with money laundering obligations is one of the greatest challenges nowadays.

Governmentsand supervisoryauthoritiesworldwideare introducingnew lawsand regulations

imposingnewrequirementsinordertoprovidearobustdefenseagainstmoneylaundering.

Amajorissuetobeaddressedbyfinancialinstitutionsistheneedtocomplywithenhancedanti-

money laundering and suspicious transaction reporting laws. Thus, the compliance agenda

formostbanksandfinancial institutionshasrapidlyshiftedfromanarbitrarycommitment toa

mandatoryone.

•

•

23

ANNUAL REPORT

2 0 0 9

Inlightofthenewlegislation,BTgrantsfurtherattentiontothe“compliancefunction”,underlining

its role in assisting the management bodies in the identification, assessment, monitoring and

reportingof compliance risk, ensuring the complianceorganizational structure, reviewingand

draftingtheinternalregulationstoproperlyimplementcompliancestandards.

In2009,wecontinuedsupervisingtheimplementationofthe3rdEuropeanDirective(Directive

2005/60/EC) on the prevention of the use of the financial system for the purpose of money

launderingandterroristfinancing,therequirementsofwhicharetransposedintoNBRRegulation

no. 9/2008 and Law no. 656/2002. Through the application of these regulations, the client

portfolio of Banca Transilvania is reviewed and updated in accordance with the new legal

requirementsconcerningbeneficialownersandpoliticallyexposedpersons.

kYC and AML systems

definingandprioritizingKYCdataqualityrequirements:workingcloselywithregulatory

expertsinanti-moneylaunderingcomplianceanddatamanagement;

focusing on key areas:criticalKYCdatafieldsnecessarytodetectunusualtransactions,

identifyand risk-ratecustomersandprevent financialcrime;gettingparticipation fromkey

personnelincompliance,operations,ITandfrontoffice;

sustaining data quality over time: once the data has been cleansed and integrated,

developsustainedmeasurestoensurethatdataqualitycontinuestomeetorexceedrequired

levelsovertime.Thesemeasuresshouldincludedatamonitoringprograms,developmentof

appropriatepoliciesandprocedures,andcontrolimplementationsforallkeysystems;

assigning individual responsibilitytotheinvolvedpersonnel.

In summary,dataqualityanddata integrationplaya crucial role in renderingKYCandAML

strategiesfunctional,engagingquicklyandcomprehensivelyproactiveresponses.

•

•

•

•

24

Problemnoticed

Actiontaken

Crisissolved

ANNUAL REPORT

2 0 0 9

sUstAINABLE BANkING

Environmental performance

BancaTransilvaniadecidedtobeasupporterofenvironmentalinitiatives,acorporatecitizenwho

believesinefficientlyimplementingacoordinatedenvironmentalriskmanagementframework.

BancaTransilvania’senvironmentalapproachfocusesontwodimensions:

1.Defining,controllingandreducingitsownenvironmentalimpactarisingfromoperationalactivity:

•Electricitymanagement;

•Water&paperconsumption;

•Useofnaturalventilationsystemsvs.airconditioning.

Proactive solutionsareacknowledgedbyBancaTransilvaniaemployees,whovoluntarilymake

efforts tominimize theenvironmental impactsof their dailyactivitiesatwork. Since2008,BT

started the renovation of the headquarters building to optimize the consumption in terms of

electricity,water,fuel,gas,paperandotherwaste.

2.Sustainablebankingviaproductsandservices:

•Financingrenewableenergy;

•Energyefficiencyplatform;

•Environmentinvestments.

In2008,BancaTransilvaniaproposedtoengageitscustomersandpartnersinadvancing

smarterenergyefficiencypractices.Inlinewiththiscommitment,BT’s2009aimwastoframethe

25

Environmental risk management policy

Environmental initiatives implementation

Reduce environmental impact

Promote environmental related business

Energy Efficiency

electricity management

water & paper level reduction

natural ventilation system

ANNUAL REPORT

2 0 0 9

environmentalimpactsregardingfinancedprojectsandsupportclientstominimizetheundesired

environmentaleffects.

Withinthiscontext,anewriskevaluationmodel,ascreeningprocess,wasdesignedtoidentify

thepotentialenvironmentalissuesassociatedwithaproject,soastorecognizeboththenegative

aspectsofcertainundertakings,aswellaspositiveoutcomes.

EnergyEfficiencyfacilitiesatcompetitiverates,withgrantsforsuccessfulfinalizationoftheinvestment

wereofferedtoourclients.Wealsoprovidedfreetechnicalassistancefortheseprojects,withon-

linesupport,thecustomers’soleconcernbeingtheircommitmenttowardsviableenergysaving

solutions.

Withitsspecializedbankingproductsandservices,BancaTransilvaniawillcontinuetosupport

innovativetechnologiesandenergysavingprojectstocontributetomaintaininganecologically

balancedenvironment.

Corporate social Responsibility

BancaTransilvaniapreservedinatransparentandethicalmannerits2009socialinvolvement,

regardlessoftheeconomicenvironment.

ThemostimportantprojectcontinuedtobeClujul areSuflet,whichhasgainedbynowitsown

identity.Withover twoyearsofexperience, theproject reaching thematurity stage,managed

to engage as many Cluj citizens as possible. This undertaking in partnership with Romanian

Foundation for Children, Community and Family - Cluj (FRCCF), helped and supported over

500teenagerstoreintegratesocially.InadditiontothedirectmaterialaidofferedbyBT,during

September –December2009 for eachpaymentwithaBT card,1RONwasdonated to the

Foundation.

BT’stotaldonationswereRON450,000,ofwhichRON250,000viaFundatiaTransilvaniaand

therestasaconsequenceofthecardpaymentcampaign.

26

Wemanagedtoassist:

115studentstoimprovetheirgrades

26studentstopasstheirfinals

41youthstoqualifyforajob

69teenagerstofindajob

ANNUAL REPORT

2 0 0 9

OureffortswereacknowledgedbyForbesmagazine,whichplacedBTthirdin2009amongstthe

mostgenerousRomaniancompanies.WealsoreceivedtheExcellencyawardgrantedbyTVRCluj

for“efficientmanagementofemotionalcapitalandcivicspirit”atMediaExcellencyawards.

Clujul areSufletwasaninspirationnotonlyforClujcitizensbutforourBucharestcolleagues

aswell.Theyhelpedthelessfortunate,withasmallscaleundertaking,butwithgreataffective

impact.NewfurniturewassuppliedtoFundeniHospital,PediatricOncologyDepartment,sothat

thechildrencouldenjoyanewcolorfulenvironment.

social welfare

Beforemajorholidays (suchasChristmas,Easter,March1st– thebeginningofspring,March

8th – International Women’s Day) the bank’s ground floor becomes a charity bazaar, where

theheadquartersemployeescanpurchasecardsandornaments,whichareskillfullycraftedby

childrenwithspecialneeds(eitherphysical,psychologicalorsocial).BT’smanagementstrongly

supportstheseactivitiesandtheemployeesenjoyacquiringbeautifulhandicrafts,whilemakinga

contributiontoprovidinglittleartistswithabetterfuture.

Community projects

Banca Transilvania also provides support for students via “Student Plus” program. Highly

attractiveplatform,allowingyouthswithOmnipassandVisaElectronEuro<26cardstobenefit

fromcertainpricediscounts(suchaspublictransportation)matchingtheirlifestyle.Wewerejoined

inthisundertakingbyprestigiouslocalinstitutions,suchastheTechnicalUniversity,Babeş-Bolyai

UniversityandtheLocalTown-HallandCouncil.

CsR in the medical field

BancaTransilvaniaofferedsupporttothemedicalsector,evenmoresosinceBThasadedicated

businesslinetoassisttheRomanianmedicalsystem.Weencouragedandhelpedaseriesofspecific

programs,thuscontributingtothesuccessofcertainphysician’sinitiativeswithentrepreneurialspirit.

27

Projects:

FirstprivategeriatricscenterinArad

StateoftheartmedicalimaginginGiurgiu,Galaøi,SatuMare,

Baia Mare and Piteşti Hospitals

FirstprivategastroenterologycenterinCluj-Napoca

FirstdentalchairinasmallvillageinTulcea

FinancingaprivatestemcellbankinBucharest

ANNUAL REPORT

2 0 0 9

CsR for entrepreneurs

Support the Romanian businesses!showedourcommitmentandinvolvementinthesociallifeof

Clujcitizens,supportingthejumpstartofmicro-businesses.Togetherwiththeonlinepublication

HotNews.ro,weorganizedacontestmeanttorewardthebestbusinessinitiative,andsowedid.

“Carry me, mommy”hadgreatimpact,asitproposedaneasyandinventivewaytohelpyoung

motherscarry theirbabies,byusingbabyslings.BTwilloffersupportviafinancialconsultancy

services,designofaprofessionalsiteandpromotiononGoogle AdWords.

CsR for employees

InOctober 2009, BTorganized the11th editionof the running contest –Crosul BT, by now

an official trademark of the bank, which had Gabriela Szabo, multiple international athletics

champion,asspecialguest.The4kmracewasheldforamateursportsmenandBTemployees.

Dear participants,

I was happy to learn that the tradition of this running

competition was revived. This is why I will be by your side

at the start line, to get to know you and cheer you on.

I look forward to giving the official start to this wonderful health

training program!

All the best,

Gabi Szabo

28

BT’ssocialresponsibility“comesfrom

theinside”,fromitsteamdrivenby

involvement,commitmentandproactive

attitudecombinedwithresponsibility.

ANNUAL REPORT

2 0 0 9

HUMAN REsoURCEs

Evenif2009broughtashiftinHRpriorities,BTcontinuedtofocusonefficienthumanresource

services, so that the bank’s near term objectives could be balanced with long term business

requirements.

Withcompaniesandbankinginstitutionsreducingtheirworkforce,wewerereadytoadaptquickly

tothechangingbusinesspriorities,retaininganddevelopingourexistingemployees’corebase.

To be among the winners, the executive management, together with our HR Department

consideredthebestpracticestoprovideamovingforwardbalancedapproach,byincludingboth

costreductionmeasures,andsmartinvestmentsintalentsaswell.

Staffprofile

Skill and competence were our assets in times

of crisis. 2009 human resources strategy was

centered on key personnel. Communication,

initiative and talent were rewarded and

encouraged,soastomaintainBT’scompetitive

edge.

hRinfigures:2008vs.2009

29

Gender Breakdown

male

female

23.7%

76.3%

Staff Average Age

2003

34.5

2004

32.2

2005

31.1

2006

30.6

2007

31.1

2008

31.2

2009

33.24

Headcount Evolution

2003 2004 2005 2006 2007 2008 2009

staff numbernewcomers

TotalHeadcount

ActiveEmployees

Dec 2008

6,507

6,036

Dec 2009

6,126

5,285

ANNUAL REPORT

2 0 0 9

Withinthiscontext,theactivityofBT Academycapitalizedontheexistingtalentpool,identifying,

retainingandrewardingviatrainingprograms,theemployeesthatmakeadifference.

Financialanalysisandcreditriskmanagementwerethetwomaintrainingdirectionsof2009.650 corporate and SME division employeeswereengagedinspecifictrainingprogramsmoderated

byoutsidespeakersandBTspecialists.Theseminarsweretargetedatraisingemployees’awareness

withrespecttoBaselIIrequirementsandcompliancewiththevastarrayofregulationsimposedby

thesupervisionauthority.

A solid operational risk management training platform was built up by the top management

togetherwithComplianceprofessionals,soastosupportthehighvelocitychangesimposedbythe

2009climate.Consequently,850colleaguesattendedtrainingsessionsonfraudidentification

andprevention,know-your-customerandoperationalriskmanagement.

Asproductsandservicessetusapartfromourcompetitors,wedevelopedmultiplecoursesmeant

toenhanceouremployees’customercareskills.Training on products and servicescomprises

alargerangeofsessionsprovidedtoourstafftobecomethoroughlyaccustomedwiththebest

possiblepracticestoensurecustomersatisfaction.

HRDepartmentwithinBancaTransilvaniaiscontinuallybeingchallengedtoprovidemanagement programsintendedtoraiseexpertise,efficiencyandcompetenceofkeypersonnelandenhance

communicationskillsandinterpersonalrapportsatdifferenthierarchicallevels.Asaresult,MBA

programs,leadershipandcommunicationcourseswereimplementedduring2009.

30

Reinforcing “BT Spirit”

Professionaland

risk aware

Teamwork

Human capital•retention•performance management•training

Staffreallocation/re-qualification

Reinforcing BT Spirit Teamwork

Professional & risk aware

Human capital

Staff reallocation &

re-qualification

ANNUAL REPORT

2 0 0 9

MARkEtING AND CoMMUNICAtIoN

TheBank for Entrepreneurial Peopleconceptcontinuedtobepromotedduring2009throughout

allmarketingprojectsrolledoutbyBancaTransilvania.Notonlydidweconveytothepublicthe

messagethatBTsupportsentrepreneurialpeople,butwealsoacted“entrepreneurial”throughlarge

scaleadvertisementcampaignsandspecific,punctualactivities,beingbothinnovativeandefficient.

TheacknowledgementofoureffortswasreflectedinaSynovate studywhereBancaTransilvaniawas

placedamongthefivemostwell-knownbrandsinRomania,intheBanking–Insurancecategory.

As the crisis determined several banking players to retreat our two

TV campaigns promoting the SME dedicated products: Banking Subscription and the Ready Secured LoanmonopolizedtheTV

communication(93%).

In times of great difficulty, BT offered

supporttosmallentrepreneurs,extending

productswithadvantageousfeestructures,

the Fairy Man cutting banking expenses

forSMEs.

The Banking Subscription Campaign

enjoyedtheattentionofthepublic.Over

12,600 new subscriptions were entered

fromFebruary toAugust 2009, accounting for 27%of total

subscriptionsgrantedsinceproductlaunch.

The campaign for the Ready Secured Loan,productdeveloped togetherwith theNational

GuaranteeFund for SMEs,oneof the first private-publicpartnerships inRomania launched to

defendSMEsagainst thehostilemacroeconomicenvironment,had theexpected impacton the

market.ThisCampaignwasrewardedwiththeprestigiousSilvereffieaward,BT’s4thEffieprize.

This is thehighesthonourfor thefinancialbankingsector in2009(as therewasnoGoldEffie

winner),basedonadcampaignefficiency.

Whilethemarketingactivityforcorporateclientsfocusedmainlyontheirneedstoovercomethe

crisis,retailcustomerstargetwasaimedmainlytoenhancetheuseofproductsandservicesalready

existingintheportfolio:cards,BT24.

31

ANNUAL REPORT

2 0 0 9

Cardswereagainstarproducts,asignificantpartofthemarketing

activitytargetedthissegment.VISA ELECTRON,Your Daily Card Campaignpositionedtheuseofcardsasaday-by-day

instrument,even forsmallpayments. In fact, increase inPOS

cardusagefulfilledourexpectationsfor2009andrecordeda

22.7% rise in December 2009 vs. June 2009.

Besidesthe“classical”promotiontools,over400ATMswere

redesignedtodisplayspecificcampaignlogos.

DuringtheWin in 3 Moves!campaign,theFairy Manoffered

prizes to customerswhoused threeoutof fiveBTproducts.

Thisprogramcontributed significantly to the intensiveuseof

productsbytheexistingcustomerbase.

Moreoverin2009,westrengthenedtheconceptof“The Bank for utilities”. Pay your bills at Banca Transilvaniawaslaunchedforourcustomerstomakebillpaymentaneasy,linefreeactivity.

Theco-brandedBT - Western Unioncampaignmadeproof

ofsimplicityandreliabilitytothebestofourcustomers.Thus,

themarketshareonthissegmentincreasedto20.35%.

Inonlinemarketing,wecontinuedto improveInternetbrand

awarenessandsales.

Anewtypeofonlinecommunicationwasinitiatedbycreatinga

BTprofileonFacebook,thelargestsocialnetworkingwebsite.

OurpresenceinthistypeofenvironmentenhancesBT’sonline

visibility,placingthebankinthespotlight.

WeweretheBank for Entrepreneurial peopleontheInternet

aswell.HundredsofRomanianentrepreneursbenefitedfrom

advertisingspaceinGoogleAdWords,followingthe Google Friend Campaign.

AnotheringeniousinitiativewasBT-Daily Planner,anonline

applicationhelpingourclientstoefficientlymanagetheirdaily

tasks.

32

ANNUAL REPORT

2 0 0 9

public relationscontinuedtosupporttheBank’sintegratedcommunication,focusingonthe

relationshipwiththemass-media.Foraconsistentandtransparentcommunication,severalpress

releases were sent per week, thus ensuring an outstanding information flow between Banca

Transilvaniaandthepress.Thetopicscoveredinformationonthebank’sfinancialresults,business

line results, financings received from strategicpartners (IFC,EBRD),

partnerships,Clubul Întreprinzătorului Românactivities.

Internal communication played an important role in Banca

Transilvaniatoo,greatemphasisbeingplacedonkeepingour

employeespermanentlyupdated.

PR strategy in2009 targetedawareness and reputation

preservation,aswellasthepromotionofBTastheBank

forEntrepreneurialPeople.

Integrated communication was the key to success in 2009, achieved by

efficient means, via marketing and PR initiatives, in environments meant to

createvisibilityandbrandawareness.

33

During2009,thesitehad1,644,742solevisitorswith

5,402,288logins

www.bancatransilvania.rowasviewed14milliontimes

Eachvisitlastedinaverage2minutes

ANNUAL REPORT

2 0 0 9

opERAtIoNs AND It

2009 main achievementsWehadagoodbusinessevolutionin2009,markedbytheincreaseandconsolidationofmarket

shareinseveralsegments(domesticpayments,cards,debitinstruments)reachingvaluescloseto

15%.

Duetotechnicalstaffwithhighlevelexpertise,wesucceededindevelopingadequateITsupport,

whilemaintaininglowoperationalcosts.

WorthmentioningisthechangeoftheCardSystemITplatformandtheacquisitionofExadataV2

equipmentprovidedbyOracle&Sun,inordertoincreaseperformancerelatedtoDataWarehouse

andMIS.

2010 priorities and objectivesFortheyeartocome,weintendtodevelopnewandmoresophisticatedbankingproductsoffered

viavariousdistributionchannels.Therefore,itisessentialtoincreaseefficiencyandperformancein

ourcorebankingsystemtosupportthebank’sintensivegrowthandthehightransactionvolumes,

butalsotocomplywiththesuperiorqualitystandardssetforourclients,theNationalBankand

theAuditors.

Ouroperationalinitiativesconsistin:

business reengineering,throughactivitycentralizationandcostcontrolusinge-channels;

quality managementintermsofproductsandservicesandproductlifecycles.

In terms of technologies, we analyze the opportunity of implementing a new, scalable Core-

BankingsystemandanenhancedInternetBankingsolution.

AmongourITstrategicgoals,wemention:

customerserviceenhancement,expressingoureffortstorespondtocustomerneedsina

timelyandeffectivemanner;

alignmentandagility,becausewesetprioritiesbasedonbusinessdriversandweadaptto

changingcustomerneeds;

financialcontribution, for thepurposeofaccuratecostestimationandefficient resource

allocation;

updatedtechnologyinordertoensureconfidentiality,securityanddataintegrity;

enterprisearchitecture,meaningourattemptstosimplifytheenvironmenttoensurestable

andefficientperformanceforcrucialapplications.

••

•

•

•

•

•

34

ANNUAL REPORT

2 0 0 9

MAIN sUBsIDIARIEs

Bt Leasing transilvania IFN s.A.

Withover14yearsofexperience,staffprofessionalismandclient-tailoredfinancialsolutions,BT

Leasingoffersaccessibleandadvantageous funding for theacquisitionofgoodsbymeansof

financelease.

In2009,BTLhad2,475clientsservicedvia25branchesthroughoutthecountry.Ourbusiness

modelisstrategicallyconnectedtoBancaTransilvania’s,creatinginter-groupsynergyandcross-

sellingopportunities.

TheleasingproductsaredesignedascomplementarytoBT’sbankingoffer:

•LeasingStandard–basicproduct;

•LeasingRapid-designedforcorporateclients;

•LeasingTakeandGo-bothforretailandcorporateclients;

•RefinanceLeasing-uniqueproductfullyadaptedtotheclient’sneeds;

•Lease-Back/Cash In -productwhichallowscompanies toenjoy thebenefitsofworking

capital,whilestillusingthe“Sale&Leaseback”goods;

Ourcontinuedsuccessinthemarketin2009washighlightedbytheincreaseinsharecapitalRON

3,643,321,reachingRON39,910,314,whiletheturnoverrosetoRON43,276,225,comparedto

RON38,368,887attheendof2008.

Bt securities s.A.

2009activity startedwith clear cut,well-definedobjectives, so as to reflect the consolidation

processontheprimarycapitalmarket.Increasingmarketshare,raisingefficiency,improvingrisk

managementactivity,anddevelopingtheITinfrastructure,inordertoaccommodatethesubstantial

workloadweretheguidingprinciplesthroughouttheyear.

IntermsofmarketshareandnetworkBTSecuritieswasamongtheleadinginstitutions.Inthearea

ofstocktradingandbrokeragehousesonBucharestStockExchange,BTSwasranked1stin2009,

withamarketshareof9.87%.Moreover,16RomanianCountiesarecoveredbyBTSecurities

network,themostextensiveplatformofanybrokeragecompanyinRomania.

In2009,BTSecuritiesmaintaineditsstatusastheonlyintermediaryinRomaniawhichofferedits

clientsmarginanddirecttransactionsontheViennaStockExchange(WienerBörse).

35

ANNUAL REPORT

2 0 0 9

36

Capital market development fully confirmed the accuracy of the company’s market research

reports,encouragingitsspecialiststocontinueonthesamepath.

BTScarriedonitsstrategybyactiveinvolvementontheprimarycapitalmarket,bymeansof:

issuing municipal bonds for Alba-Iulia Town Hall & County Council, Focşani, Orãştie and

NãvodariTownHalls;

winning the tender for financing Botoşani Town Hall;

finalizingfivepublictenderoffersinitiatedbydifferentlistedcompanies;

startingtheinitialpublicoffering,followedbylistingontheBSE,for3internationalairports:

“Henri Coandã” in Bucharest, “Mihail Kogãlniceanu” in Constanøa and “Traian Vuia” in

Timişoara.

Bt Asset Management s.A.I. s.A.

BTAssetManagement,thebiggestequityfundmanagerontheRomanianmarket,rankedfourthin

theassetmanagementbusinesswithamarketshareof5.5%.Itspecializesinfundandindividual

investmentaccountsmanagement.

Attheendof2009,theassetsunderthecompany’smanagementamountedtoRON171milion,

representinga136.52%risecomparedto2008.Thenumberofclientsalsoincreasedtoover

6,500in2009.

In2009,therewasasignificantboostinmanagedassets,onthebackgroundoftheincreased

attractivenessofourproductsgiventheirappealingyields.

•

•

•

•

YIELD, 2009

BTObligatiuni

BTClasic

BTIndex

BTMaxim

14.01%

25.84%

50.11%

62.78%

AssetsunderManagement

Numberofclients

2008

72,355,608

2,237

2009

171,135,214

6,521

%

136.52

191.51

ANNUAL REPORT

2 0 0 9

37

Medicredit Leasing IFN s.A.

Establishedin2003asanon-bankingfinancialinstitution,MedicreditLeasinghasmanagedto

gainthestatusofleaderontheprivatemedicalmarket,witha54%marketsharein2009interms

ofmedicalequipmentleasing.

Over theyears, thecompany succeeded inaddressingdifferentneeds,whetherclientswished

to expand existing medical businesses or required technical-financial solutions for a start-up

company.

Medicredit Leasing provides to its customers integrated technical-financial solutions through

packageoffers,consistingoftechnicaladviceonmedicalequipment,businessandmanagerial

consultancy,followedbyfinancialsupport.

BancaTransilvaniabecameashareholderin2006,increasingitsparticipationto57.39%in2008.

Startingwith2010MedicreditLeasingisfullyownedbyBT,thebankcompletingitsproductoffer

fortheHealthcareDivision,addingleasingfacilitiestothebankingproductsandservices.

Duetoitsexpertiseinthemedicalfieldandtrustgainedamongstphysicians,Medicreditextended

itsactivitycountrywidein2009servicing29largeclinics,5newscreeningcenters,aswellasa

newmultidisciplinarymedicalcenter.

Bt Direct IFN s.A.

Specializedinconsumerfinance,BTDirectportfoliodynamicsin2009showedatotalfinancing

valueofRON16.3millionfor7,767newcontracts,withthefollowingbreakdown:RON6million

financeleasingagreementsandRON10.3millionlendingcontracts.

BTDirectcollaborateswith460partnerstoresandfinancesover18,600clients.

FINANCIAL HIGHLIGHTS, 2009

Totalincomefromfinancingoperations

Totalincome

Grossprofit

Taxonprofit

Netprofit

2009

5,931,218

6,581,418

1,548,816

203,480

1,345,336

2008

4,805,492

5,403,547

432,885

252,588

180,297

RON

BANCA TRANSILVANIA S.A.

Consolidated Financial Statements31 December 2009

Prepared in accordance with the International Financial Reporting Standards

as endorsed by the European Union

TRANSLATOR’S EXPLANATORY NOTE:

The above is provided as a free translation from Romanian which is the official and binding version.

INDEPENDENT AUDITORS' REPORT(free translation1)

The ShareholdersBanca Transilvania S.A.

Report on the consolidated financial statements

1 We have audited the accompanying consolidated financial statements of Banca Transilvania S.A. and its subsidiaries (the“Group”), which comprise the consolidated statement of financial position as at 31 December 2009 and the consolidatedincome statement, the consolidated statement of comprehensive income, the consolidated statement of changes in equity andthe consolidated cash flow statement for the year then ended, as well as a summary of significant accounting policies andother explanatory notes.

Management's responsibility for the consolidated financial statements

2 Management is responsible for the preparation and fair presentation of these consolidated financial statements in accordancewith International Financial Reporting Standards as endorsed by the European Union. This responsibility includes: designing,implementing and maintaining internal control relevant to the preparation and fair presentation of consolidated financialstatements that are free from material misstatements, whether due to fraud or error; selecting and applying appropriateaccounting policies; and making accounting estimates that are resonable under the circumstances.

Auditors' responsibility

3 Our responsibility is to express an opinion on the consolidated financial statements of the Group based on our audit. Weconducted our audit in accordance with Standards on Auditing as adopted by the Romanian Chamber of Financial Auditors.Those standards require that we comply with relevant ethical requirements and plan and perform the audit to obtainreasonable assurance whether the consolidated financial statements are free from material misstatements.

4 An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the consolidatedfinancial statements. The procedures selected depend on our judgment, including the assessment of the risks of materialmisstatement of the consolidated financial statements, whether due to fraud or error. In making those risk assessments, weconsider internal control relevant to the entity’s preparation and fair presentation of the consolidated financial statements inorder to design audit procedures that are appropriate under the circumstances, but not for the purpose of expressing anopinion on the effectiveness of the entity’s internal control. An audit also includes evaluating the appropriateness ofaccounting principles used and the reasonableness of accounting estimates made by management, as well as evaluating theoverall presentation of the consolidated financial statements.

5 We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our opinion.

Opinion

6 In our opinion, the accompanying consolidated financial statements of Banca Transilvania S.A. and its subsidiaries presentfairly, in all material respects, the consolidated financial position of the Group as at 31 December 2009, and its consolidatedfinancial performance and its consolidated cash flows for the year then ended in accordance with International FinancialReporting Standards as endorsed by the European Union.

2

1 TRANSLATOR'S EXPLANATORY NOTE: The above translation of the auditors' report is provided as a free translation from Romanian whichis the official and binding version.

Emphasis of matters

7 Without qualifying our opinion, we draw attention to the following:

• As presented in Notes 3j, 19 and 20 to the consolidated financial statements, the Group has estimated the impairment lossprovision for loans and advances to customers and net lease investments at RON 826,912 thousand based on the internalmethodologies developed and applied as at 31 December 2009. We draw attention to the limitations mentioned in Note3j and to the uncertainties on the local financial markets regarding the operating environment and assets valuationmentioned in note 4f to the consolidated financial statements.

• As presented in Note 2c to the consolidated financial statements, the Group has presented in Euros for the convenience ofreaders the amounts reported in Lei in the consolidated balance sheet and in the consolidated income statement. Thispresentation does not form part of the audited financial statements.

Other Matters

8 This report is made solely to the Bank’s shareholders, as a body. Our audit work has been undertaken so that we might stateto the Bank’s shareholders those matters we are required to state to them in an auditor's report and for no other purpose. Tothe fullest extent permitted by law, we do not accept or assume responsibility to anyone other than the Bank and the Bank’sshareholders as a body, for our audit work, for this report, or for the opinions we have formed.

Report on conformity of the administrators’ report with the consolidated financial statements

In accordance with the Order of the National Bank of Romania no. 13/2009, article no. 223, point (e) we have read theaccompanying administrators’ report on the consolidated financial statements of Banca Transilvania S.A. and its subsidiaries (the“Group”) prepared in accordance with International Financial Reporting Standards as endorsed by the European Union as at andfor the year ended 31 December 2009. The administrators’ report as presented from page 1 to 22 is not a part of the Group'sconsolidated financial statements. In the administrators’ report we have not identified any financial information which is notconsistent, in all material respects, with the information presented in the Group's consolidated financial statements as at 31December 2009.

Please refer to the original signed Romanian version

For and on behalf of KPMG Audit SRL:

Cezar Gabriel Furtuna KPMG AUDIT SRL

registered with the Chamber of Financial registered with the Chamber of FinancialAuditors of Romania under no. 1626/2003 Auditors of Romania under no. 9/2001

Bucharest, 29 March 2010

3

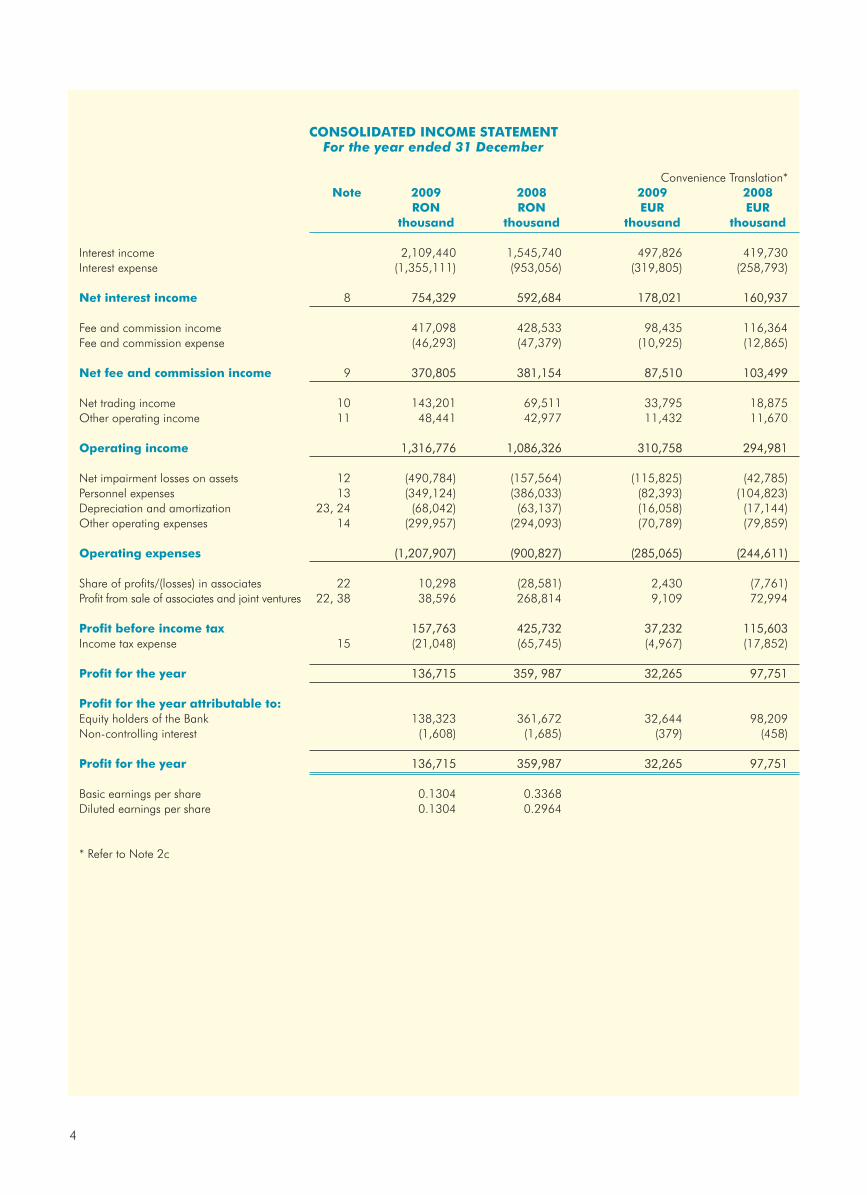

CONSOLIDATED INCOME STATEMENTFor the year ended 31 December

Convenience Translation*Note 2009 2008 2009 2008

RON RON EUR EURthousand thousand thousand thousand

Interest income 2,109,440 1,545,740 497,826 419,730 Interest expense (1,355,111) (953,056) (319,805) (258,793)

Net interest income 8 754,329 592,684 178,021 160,937

Fee and commission income 417,098 428,533 98,435 116,364 Fee and commission expense (46,293) (47,379) (10,925) (12,865)

Net fee and commission income 9 370,805 381,154 87,510 103,499

Net trading income 10 143,201 69,511 33,795 18,875 Other operating income 11 48,441 42,977 11,432 11,670

Operating income 1,316,776 1,086,326 310,758 294,981

Net impairment losses on assets 12 (490,784) (157,564) (115,825) (42,785)Personnel expenses 13 (349,124) (386,033) (82,393) (104,823)Depreciation and amortization 23, 24 (68,042) (63,137) (16,058) (17,144)Other operating expenses 14 (299,957) (294,093) (70,789) (79,859)

Operating expenses (1,207,907) (900,827) (285,065) (244,611)

Share of profits/(losses) in associates 22 10,298 (28,581) 2,430 (7,761)Profit from sale of associates and joint ventures 22, 38 38,596 268,814 9,109 72,994

Profit before income tax 157,763 425,732 37,232 115,603 Income tax expense 15 (21,048) (65,745) (4,967) (17,852)

Profit for the year 136,715 359, 987 32,265 97,751

Profit for the year attributable to:Equity holders of the Bank 138,323 361,672 32,644 98,209 Non-controlling interest (1,608) (1,685) (379) (458)

Profit for the year 136,715 359,987 32,265 97,751

Basic earnings per share 0.1304 0.3368Diluted earnings per share 0.1304 0.2964

* Refer to Note 2c

4

CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOMEAs at 31 December

Convenience Translation*Note 2009 2008 2009 2008

RON RON EUR EURthousand thousand thousand thousand

Profit for the year 136,715 359,987 32,265 97,751

Other comprehensive income, net of income tax

Fair values gains/(losses) from available for sale investments (net of deferred tax) 44,405 (65,890) 10,480 17,892Other changes 2,950 (17,853) 696 (4,848)

Total comprehensive income for the period 184,070 276,244 43,441 110,795

Total comprehensive income attributable to:Equity holders of the Bank 186,692 276,028 44,059 74,952Non-controlling interest (2,622) 216 (618) 59

Total comprehensive income for the period 184,070 276,244 43,441 75,011

* Refer to Note 2c

The consolidated financial statements were approved by the Board of Directors on 29 March 2010 and were signed on its behalf by:

Horia Ciorcila Maria MoldovanChairman Chief Financial Officer

5

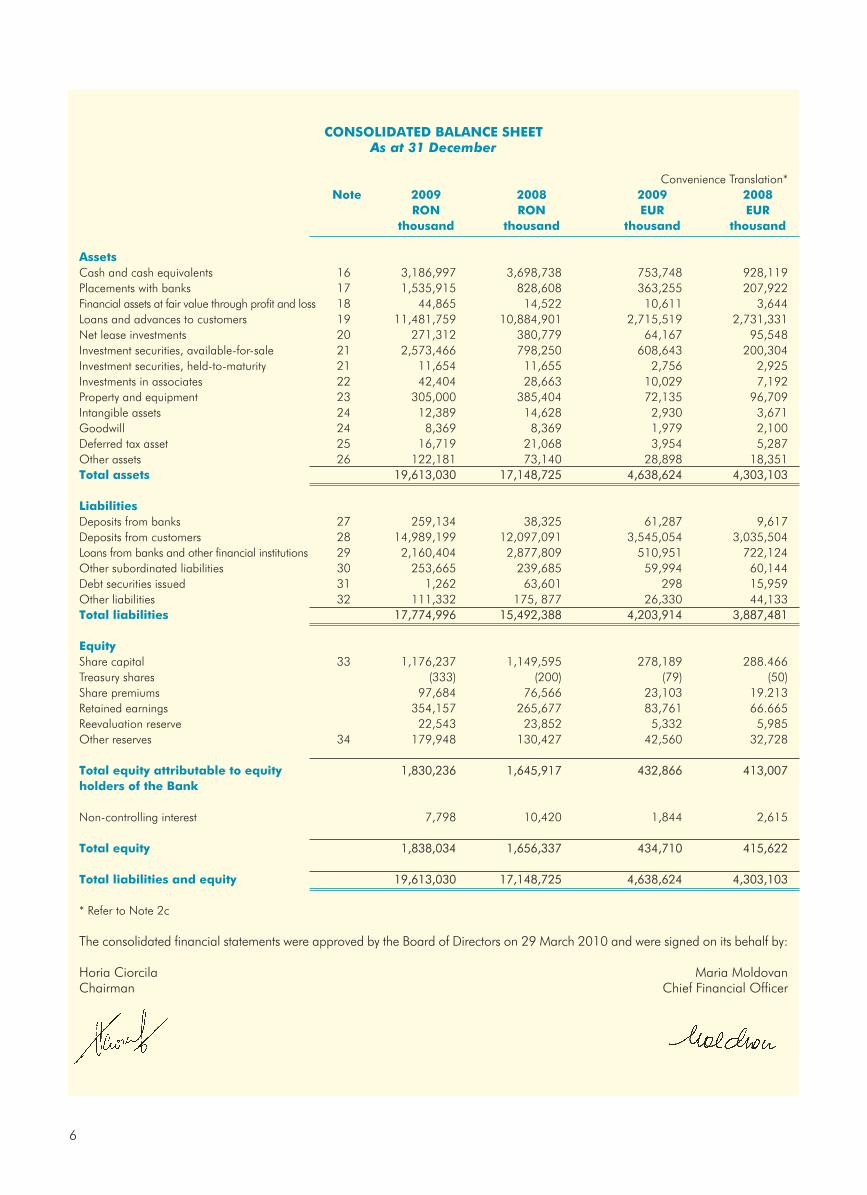

CONSOLIDATED BALANCE SHEETAs at 31 December

Convenience Translation*Note 2009 2008 2009 2008

RON RON EUR EURthousand thousand thousand thousand

AssetsCash and cash equivalents 16 3,186,997 3,698,738 753,748 928,119 Placements with banks 17 1,535,915 828,608 363,255 207,922 Financial assets at fair value through profit and loss 18 44,865 14,522 10,611 3,644 Loans and advances to customers 19 11,481,759 10,884,901 2,715,519 2,731,331Net lease investments 20 271,312 380,779 64,167 95,548 Investment securities, available-for-sale 21 2,573,466 798,250 608,643 200,304 Investment securities, held-to-maturity 21 11,654 11,655 2,756 2,925 Investments in associates 22 42,404 28,663 10,029 7,192 Property and equipment 23 305,000 385,404 72,135 96,709 Intangible assets 24 12,389 14,628 2,930 3,671 Goodwill 24 8,369 8,369 1,979 2,100 Deferred tax asset 25 16,719 21,068 3,954 5,287 Other assets 26 122,181 73,140 28,898 18,351Total assets 19,613,030 17,148,725 4,638,624 4,303,103

LiabilitiesDeposits from banks 27 259,134 38,325 61,287 9,617 Deposits from customers 28 14,989,199 12,097,091 3,545,054 3,035,504 Loans from banks and other financial institutions 29 2,160,404 2,877,809 510,951 722,124 Other subordinated liabilities 30 253,665 239,685 59,994 60,144 Debt securities issued 31 1,262 63,601 298 15,959 Other liabilities 32 111,332 175, 877 26,330 44,133Total liabilities 17,774,996 15,492,388 4,203,914 3,887,481

EquityShare capital 33 1,176,237 1,149,595 278,189 288.466Treasury shares (333) (200) (79) (50)Share premiums 97,684 76,566 23,103 19.213 Retained earnings 354,157 265,677 83,761 66.665Reevaluation reserve 22,543 23,852 5,332 5,985 Other reserves 34 179,948 130,427 42,560 32,728

Total equity attributable to equity 1,830,236 1,645,917 432,866 413,007holders of the Bank

Non-controlling interest 7,798 10,420 1,844 2,615

Total equity 1,838,034 1,656,337 434,710 415,622

Total liabilities and equity 19,613,030 17,148,725 4,638,624 4,303,103

* Refer to Note 2c

The consolidated financial statements were approved by the Board of Directors on 29 March 2010 and were signed on its behalf by:

Horia Ciorcila Maria MoldovanChairman Chief Financial Officer

6

7

CO

NSO

LID

ATE

D S

TATE

MEN

T O

F C

HA

NG

ES I

N E

QU

ITY

For

the y

ea

r en

ded

31

Dece

mb

er

20

09

Att

rib

uta

ble

to e

qu

ity

hold

ers

of

the B

an

k

In R

ON

thou

sand

Sha

re

Trea

sury

Sha

reRee

valu

ation

Oth

er

Ret

ain

edN

on

-con

trollin

gTo

tal

cap

ita

lsh

are

sp

rem

ium

sre

serv

esre

serv

esea

rnin

gs

inte

rest

Ba

lan

ce a

s a

t 31 D

ece

mb

er

2008

1,14

9,59

5(2

00)

76,5

6623

,852

130,

427

265,

677

10,4

201,

656,

337

Tota

l co

mp

reh

en

sive

in

com

e

for

the p

eri

od

Prof

it fo

r th

e ye

ar-

--

--

138,

323

(1,6

08)

136,

715

Oth

er

com

pre

hen

sive

in

com

e,

net

of

inco

me t

ax

Tran

sfer

from

ree

valu

atio

n su

rplu

s to

re

tain

ed e

arni

ngs

--

-(1

,309

)-

1,30

9-

-Fa

ir va

lue

gain

s fro

m a

vaila

ble

for

sale

inve

stm

ents

(net

of d

efer

red

tax)

--

--

44,4

05-

-44

,405

Oth

er c

hang

es-

--

-1,

376

2,58

8(1

,014

)2,

950

Tota

l co

mp

reh

en

sive

in

com

e

for

the p

eri

od

---

(1,3

09)

45,7

8114

2,22

0(2

,622

)18

4,07

0

Incr

ease

in s

hare

cap

ital t

hrou

gh

conv

ersi

on o

f bon

ds26

,642

--

--

--

26,6

42In

crea

se in

sha

re p

rem

ium

s th

roug

h in

corp

orat

ion

of d

iffer

ence

s fro

m th

e co

nver

sion

of b

onds

--

21,1

18-

--

-21

,118

Dis

tribu

tion

to s

tatu

tory

res

erve

s-

--

-3,

740

(3,7

40)

--

Acqu

isiti

on o

f tre

asur

y sh

ares

-(1

33)

--

--

-(1

33)

Dist

ribut

ion

of d

ivid

ends

for 2

008

finan

cial

yea

r-

--

--

(50,

000)

(50,

000)

Con

trib

uti

on

s b

y a

nd

d

istr

ibu

tion

s to

ow

ners

26,6

42(1

33)

21,1

18-

3,74

0(5

3,74

0)-

(2,3

73)

Ba

lan

ce a

s a

t 31 D

ece

mb

er

2009

1,17

6,23

7(3

33)

97,6

8422

,543

179,

948

354,

157

7,79

81,

838,

034

8

CO

NSO

LID

ATE

D S

TATE

MEN

T O

F C

HA

NG

ES I

N E

QU

ITY

For

the y

ea

r en

ded

31

Dece

mb

er

20

08

Att

rib

uta

ble

to e

qu

ity

hold

ers

of

the B

an

k

In R

ON

thou

sand

Sha

re

Trea

sury

Sha

reRee

valu

ation

Oth

er

Ret

ain

edN

on

-con

trollin

gTo

tal

cap

ita

lsh

are

sp

rem

ium

sre

serv

esre

serv

esea

rnin

gs

inte

rest

Ba

lan

ce a

s a

t 31 D

ece

mb

er

2007

700,

979

-98

,602

24,0

6117

2,95

726

6,37

110

,204

1,27

3,17

4

Tota

l co

mp

reh

en

sive

in

com

e

for

the p

eri

od

Prof

it fo

r th

e ye