Agriculture Economic ai- Diversification Trends in U.S. Food

50

¿«s, ynl,«istates. ^^ PrOClUCt |jL|ti|; Department of Agriculture Economic Research Service Agricultural Economic Report Number 521 ai- i' Diversification Trends in U.S. Food [\/lanufacturing James M. MacDonald xy '.M>>

Transcript of Agriculture Economic ai- Diversification Trends in U.S. Food

¿«s, ynl,«istates. ^^ PrOClUCt |jL|ti|; Department of Agriculture

Economic Research Service

Agricultural Economic Report Number 521

ai-

i'

Diversification Trends in U.S. Food [\/lanufacturing James M. MacDonald xy

'.M>>

Additional copies. • • of this report can be purchased from the Superintendent of Documents, U.S. Government Printing Office, Washington, DC 20402. Ask for Product Diver- sification Trends in U.S. Food Manufacturing (AER-521). Write to the above address for price and ordering instructions. For faster service, call the GPO order desk at (202) 783-3238 and charge your purchase to your VISA, Master- Card, or GPO deposit account, A 25-percent bulk discount is available on orders of 100 or more copies shipped to a single address. Add 25 percent for postage for foreign orders.

Microfiche copies ($4.50 each) can be purchased from the Identification Sec- tion, National Technical Information Service, 5285 Port Royal Road, Spring- field, VA 22161, Ask for Product Diversification Trends in U.S. Food Manufac- turing (AER-521). Enclose check or money order payable to NTIS. For faster service, call NTIS at (703) 487-4780 and charge your purchase to your VISA, MasterCard, American Express, or NTIS deposit account.

The Economic Research Service has no copies for free mailing.

Product Diversification Trends in U.S. Food Manufacturing. By James M. MacDonald. National Economics Division, Economic Research Service, U.S. Department of Agriculture. Agricultural Economic Report No. 521.

Abstract

Leading U.S. food manufacturers typically produce and sell a growing array of food products. Many have also expanded into related wholesale, transporta- tion, and food service industries, while avoiding large-scale involvement in agriculture and food retailing. Diversification by food manufacturers into unrelated product lines declined in the seventies. That decline, coupled with continued increases in diversification into food-related products, led to stabi- lization in average levels of diversification, after persistent increases since 1919. Successful diversification frequently depends on how readily employees' skills can be transferred to new products. Much recent diversification in the food industries has been based upon the transfer of marketing skills among consumer product industries and technical skills in commodity processing and transportation among producer goods industries.

Keywords: Diversification, food manufacturing, mergers, conglomerates.

Reference to commercial firms or brand names in this publication is for iden- tification only and does not imply endorsement by the U.S. Department of Agriculture.

Washington, DC 20250 March 1985

Contents

Page

Summary ....... ..............iil

Introduction 1

A Frameworlifor AnahrzingDivenMcation 2 Diversification^Importânt Theoretical Issues 2 Specific Sources of Diversification 3 The Incentive to Diversify 4

Data Sources and Measures of Dhrewification ... ^ 5 Sources of Diversification Data. 5 Measures of Diversification 6

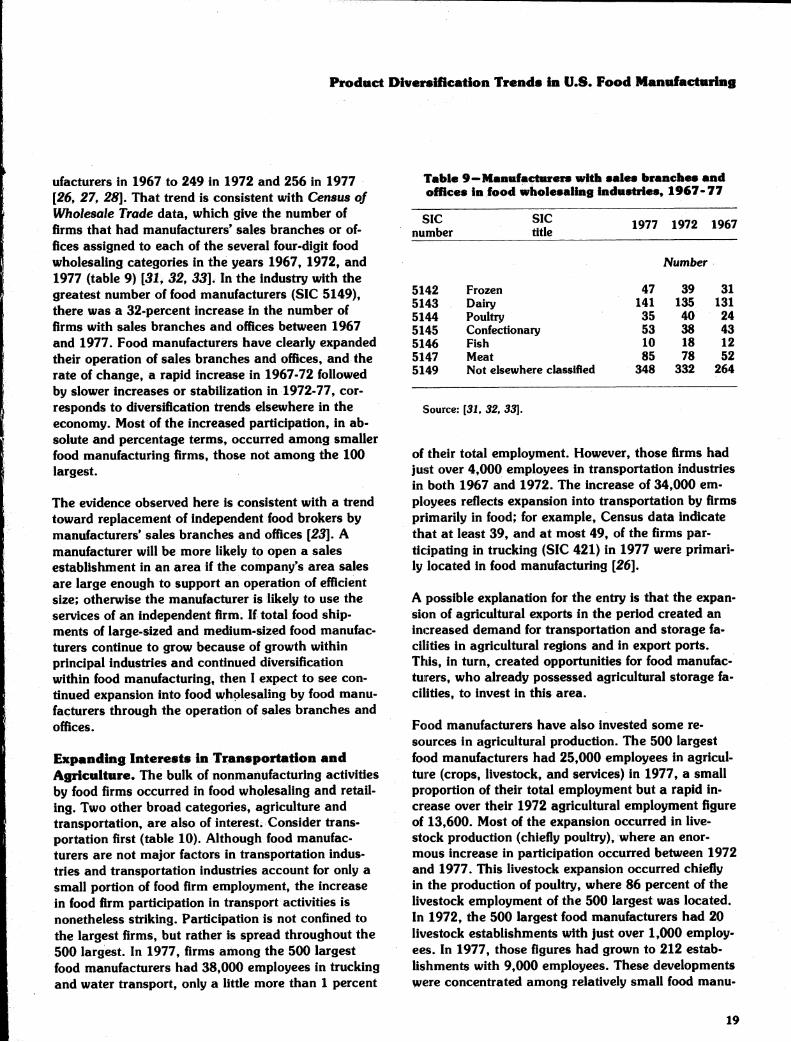

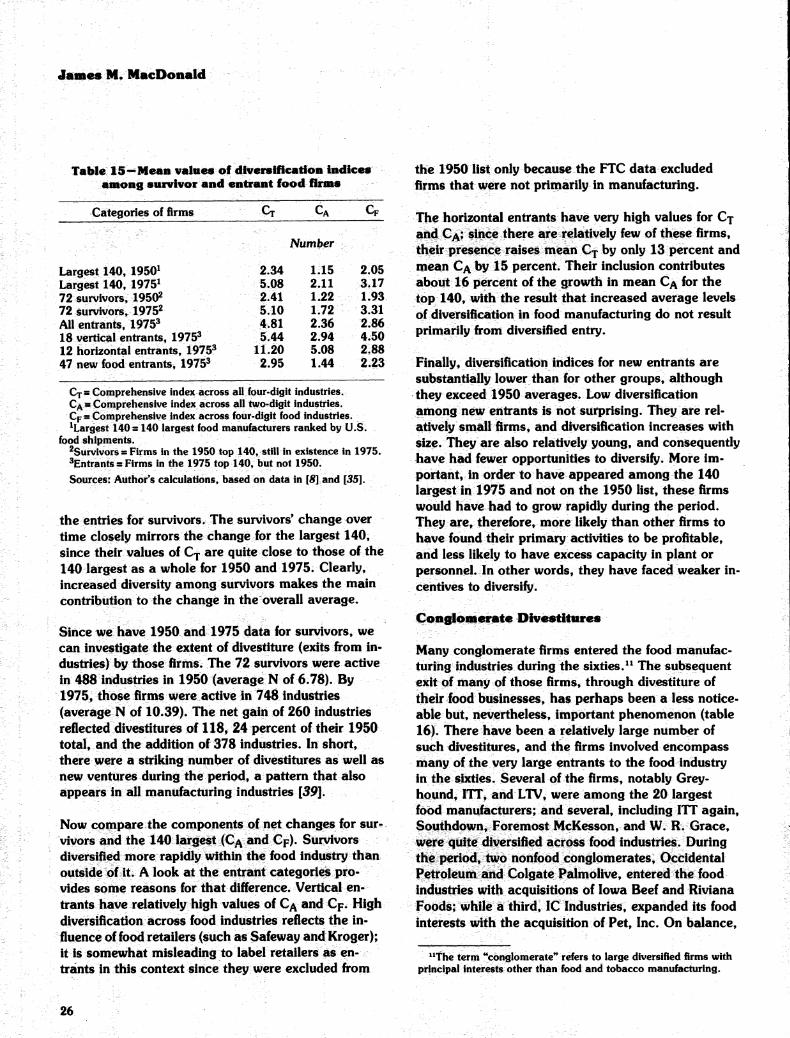

Current Directions of Diversification ................. 7 Levels of Diversification, 1975. ..... 8 Diversification Within Food Manufacturing 9 Diversification Into Other Manufacturing Industries 14 Diversification Outside of Manufacturing 16

Trends in Dfoersiflcatíon, 195^77..,....,.. 20 Levels of Diversification, 1950. 21 Marketing as a Basis for Diversification .... 22 Industrial Directions of 1950 Nonfood Dwersification ............. 22 Diversification Outside of Manufacturing 23 Changesin Diversification Since 1950 23 A Break in the Trend 24 Influence of Conglomerate Entry 25 Conglomerate Divestitures .........,.........*.................. 26 Small Firm Diversification 27

Early Diversification in Food Mannfaclitring, 1919-50 28 Characterístícs of Diversification in 1919 . ^.., 28 The Trend of Food Manufacturer Diversification, 1919-50 29

implications 30

Bibliograpliy 32

Appendix A: Organizational Changes Among Leading Food Manufacturers, 1975-84 34

Appendix B: Food Processing Industries 42

Summary

Leading U.S. food manufacturers typically sell an increasingly large number of different food products. Many have also expanded into related wholesale, transportation, and food service industries, while avoiding large-scale involve- ment in agriculture and food retailing. Unrelated diversification outside of food industries by food manufacturers declined in the seventies. After persistent in- creases since 1919, that decline, coupled with continued increases in diver- sification into food-related products, led to stabilization in average levels of diversification. Successful diversification frequently depends on how readily employees' skills can be transferred to new products. Much recent diversifica- tion in the food industries has been based upon the transfer of marketing skills among consumer product industries and technical skills in commodity proc- essing and transportation among producer goods industries.

Product diversification refers to the variety of products that a company sells; a firm diversifies its product mix whenever it begins to manufacture the products of an industry different from those in which it is already engaged. This report discusses product diversification among firms in the food manufacturing in- dustries. Some trends are highlighted below.

• Average levels of diversification among leading food manufacturers in- creased continually between 1919 and 1972. The firms diversified into other food industries, into related wholesale and food service in- dustries, and into a broad array of nonfood industries.

• Midsized regional food manufacturers, with between 400 and 2,000 employees, are typically diversified among a few food processing and wholesaling industries, and average levels of diversification among these firms also ro$e until 1972.

• Between 1972 and 1977, the extent of diversification stabilized, on average, among all size classes of food manufacturers. Since 1977, in- creased merger activity suggests some continued diversification among leading firms, but a corresponding increase in divestitures suggests a movement away from investment in industries unrelated to food.

• Conglomerate diversification into the food industries peaked in the late sixties and declined in the late seventies and early eighties.

• Successful diversification is often based on the transfer of the firm's existing skills in marketing, production, or management. Since 1950, diversification based on the transfer of marketing skills has become much more important.

ill

Product Diversification Trends in V.S. Food Manufacturing

James M. MacDonald'

Introduetion

A firm diversifies whenever it begins to manufacture the products of an industry different from those in which it is already engaged. Although diversification can have major consequences for diversifying firms, their competitors« and consumers, lack of data has restricted close study of the phenomenon.

This report presents an analysis of product diver- sification among firms in the food manufacturing in- dustries. I define industries at the four-digit level of the Standard Industrial Classification (SIC) System, as developed over a period of years by experts on classification in Government and private industry under the guidance of the U.S. Department of Com- merce [36y I describe the current extent of the phenomenon and its growth over time, and explore the impact of extensive diversification on firms, their competitors, and consumers.

For the firm, diversification can provide a means to grow or to increase profits through a shift of re- sources out of slow-growth, low-profit industries into industries with higher growth and profits. Diversifica- tion may also lead to more intensive use of existing resources; for example, the firm may diversify in order to further process the byproducts of a manufac- turing operation or to provide expanded opportunities for underutilized younger managers.

Firms that diversify reallocate capital, labor, and materials from one particular industry, and often from a particular region, to another. In doing so, the firms perform functions often carried out through markets for capital, labor, and materials; that is, diversification can substitute for market processes as a resource allocator. An immediate question arises;

*The author is a staff economist in the National Economics Divi- sion, Economic Research Service, U.S. Department of Agriculture.

'Italicized numbers in brackets refer to literature cited in the bibliography of this report.

that question, of how diversified firms perform as resource allocators relative to markets, is of great in- terest to economists, whose research often centers on the operation of markets. The issue also interests State and Federal policymakers because proposed legislation, such as that concerned with conglom- erate mergers, plant closings, and industrial policy, is often based on criticisms of the performance of diver- sified firms in the allocation of resources.

Finally, diversifiers can directly affect innovation in an industry, including the introduction of new prod- ucts and new production processes. Diversified firms finance a large share of organized private research and development, often acquire innovative and rapidly growing small firms, and introduce a major share of new food products each year. To the extent that di- versifying firms affect the flow of innovations to the economy, diversification will have further indirect in- fiiences on the growth of productivity and incomes.

The report's aim is to supply a broad, descriptive perspective, to provide the reader with the principal characteristics of diversification in the food indus- tries, including incidence, extent, trend over time, and industrial directions, with some inferences made to sources and effects.

Product diversification should be kept distinct from other ways in which a company may be diversified. For example, a firm may diversify geographically by expanding into a new region or a new country without altering the types of products it manufactures. The company may also diversify financially by holding a portfolio of securities that are combined in such a way as to minimize the risk attendant upon any ex- pected financial return, without controlling the com- panies whose securities it holds. Financial diversifica- tion is often offered as a goal of product diversifica- tion, but the connection is actually weak; product

James M. MacDonald

diversification is an unnecessary and relatively costiy means of achieving financial diversification. Finally, in the sense that decisionmaking is highly decentral- ized, a firm may diversify by having top management perform a few functions, such as capital allocation, while using a small staff. Again, managerial diver- sification may occur where a firm's product mix is diversified (all four types may be present in a large firm), but it is not necessary for product diversifica- tion, which refers specifically to the complexity in the mix of goods and services produced by the firm.

The Standard Industrial Classification (SIC), the basis for industry definitions in the report, is an elaborate hierarchical code for the classification of establishments according to the nature of their prod- ucts [36] J The first step in classification is to assign establishments to sectors, such as manufacturing, mining, or wholesale and retail trade. Sectors are further comprised of groups, of which there are 20 in manufacturing, including food manufacturing. For a manufacturing establishment, the first digit in its in- dustry code is a 2 or a 3; the second digit refers to the industry group, with the food group assigned to 20. Each manufacturing group consists of several in- dustry classes; there are nine such classes in food manufacturing, such as meat and dairy products, which are assigned the three-digit codes of 201 and 202, respectively. Each three-digit industry class con- tains one or more four-digit industries; for example, the meat products class, 201, has meatpacking plants, 2011, prepared meate, 2013, poultry dressing plants, 2016, and poultry and egg processing, 2017. As one moves down the hierarchy from sectors to in- dustries, one moves to finer separations in product characteristics.

Some four-digit industries are closely related in a pro- duction sense; that is, firms active in flour milling (2041) or in wet corn milling (2046) may decide to further process the byproducts and waste material from those mills in feed establishments (2048). Other industries may use similar raw materials as well as production methods; a firm producing condensed milk (2023) may open ice cream (2024) or cheese (2022) establishments. In other instances, the prod-

'An establishment refers to a single physical location at which production takes place, and should be distinguished from the term firm, or enterprise, which is a business organization consisting of one or more establishments under common ownership.

ucts of some industries may be distributed in similar fashion. That is, a firm may find that its distribution network for canned fruits and vegetables (2033) may be applied to candy (2065), canned fish (2091), or cooking oils (2079). In short, there are various ways in which the products of different industries may be related to one another, and that relation may be close or it may be rather distant. At the extreme, the company's products may have no identifiable relation to one another. We will follow popular prac- tice and refer to this type of firm and diversification as conglomerate.

A Framewerk for Analyzing Diveisification

This section outlines the simple theoretical frame- work used in this study. This framework cannot en- compass all of the causes and directions of diver- sification, but it does provide a useful means of categorizing the data and interpreting the observed trends. The following principal points are made:

• Diversification is fundamentally a process of reallocating resources [by a firm] from one use to another and is, therefore, a substitute for resource reallocation [between firms] via markets.

• Resource reallocation, whether accomplished through a firm or a market, is costly, and diversification in general will be preferred where the costs of reallocation via markets are relatively high.

• Certain intangible assets, such as in- vestments in research and development, mar- keting organizations, and byproduct develop- ment, have substantial amounts of firm- specific knowledge, whose exchange through markets is relatively costly. These assets should influence both the levels and direc- tions of food manufacturer diversification.

• Profit expectations influence diversification. Specifically, firms with opportunities to diver- sify will most likely leave low-profit industries and enter high-profit ones.

DJversificatioii—Important Theoretical Issues

What enables a firm with experience in one activity to compete successfully elsewhere? Rivals in a new ac-

Prodttct Diversificatioii Trends in U.S. Food Manuffaetaring

tivily have more experience than the diversifying en- trant and, to the extent that experience in an industry leads to declines in production costs, existing pro- ducers should have a cost advantage. If there are im- portant scale economies, existing producers also seem more likely to have attained them.

Some historical accounts advance excess capacity in certain inputs as a source of diversification. For ex- ample, Alfred Chandler interprets General Motors' ex- pansion into tractor and refrigerator production dur- ing and after World War I to be a response to excess capacity in its automobile plants and distribution net- work [6]. Given the excess capacity, m*arginal costs of production in those new areas may have been rela- tively low. Similarly, Edith Penrose asserts that cor- porate policies of diversification may result from ex- cess managerial capacity [29}.

The excess capacity notion focuses on assets that the firm can apply, at relatively low cost, to other ac- tivities. Such assets might be structures (factories or warehouses) that can be applied to several types of products, raw materials with a variety of industrial applications, or managers whose skills can be applied to the production or distribution of a variety of prod- ucts. Yet a fundamental problem still exists. The firm with excess capacity in some input can reallo- cate that input through diversification, but the firm also has the choice of selling the input to existing producers in the other activity. Consequently, there must be reasons for the firm's preference for an inter- nal reallocation (diversification) over a market reallo- cation via sale (divestiture) of the asset. Recent the- ories of vertical integration and diversification con- centrate on those reasons, identifying conditions under which the costs of using markets will be rel- atively high, with the result that diversification is preferred.

Specific Sources of Divei^ification

Four principal sources of diversification are based on an intangible asset, knowledge:

• Research and development of new products or manufacturing processes may generate new knowledge which can be applied to other activities of a firm.

• A firm's marketing organization may be adaptable to other product lines.

• Knowledge of manufacturing processes may be transferable to other product lines.

• Manufacturing processes may generate by- products which are potentially marketable on their own.

There are well-known obstacles to the exchange of knowledge within a market [2], First, it is difficult to agree upon the value of knowledge without revealing its content; revealing content makes it unnecessary to buy the knowledge. This is the "appropriability prob- lem," so named because of the difficulty of appro- priating the returns to knowledge in the market. Sec- ond, ''specific knowledge" is often used jointly with other inputs in production; it may be quite difficult to ascertain the contribution of knowledge to the value of output.^ This increases the uncertainty of invest- ment in knowledge. Third, many products require in- vestment in unique types of knowledge concerning the production characteristics at the plant or methods of distribution of the product. Those possessing the unique knowledge will have a degree of monopoly power in the sale of their services and will often face a single buyer. The resulting bilateral monopoly can cause production delays and increase costs as the parties bargain over division of profits [40]. By "inter- nalizing" the parties within a single firm, these costs of using markets can be reduced. Again, diversifica- tion is used where market solutions are relatively costly.

The costs of using markets are low where the prod- ucts exchanged are well-defined and have clearly defined property rights. For products such as infor- mation, where these characteristics do not necessari- ly hold, the cost of using markets may be relatively high.

The theoretical literature implies that diversification may arise where specific knowledge is an important component of sharable production and distribution in- puts. In other words, certain intangible assets may

'"Specific knowledge" is held by certain emplc^ees within the firm, but not, in general, by people outside the firm.

James M. MacDonald

strongly affect the level and directions of diversifica- tion. Research and developrnent (R & D) of new prod- ucts and processes often generate new knowledge ap- plicable to other activities technologically related to the firm's principal industry. This new knowledge may have to be applied internally, rather than ex- changed In markets, in order for the firm to appro- priate the returns to its investment. In their histori- cal accounts. Chandler and Penrose have emphasized the role of organized research and development (R & D) efforts in the growth and diversification of industrial firms [6, 19],

A firm's marketing organization contains a second sort of firm-specific knowledge, which is particularly important in the food industries. Firms with expertise in the marketing of their original products may apply those skills to other products which are marketed through similar channels. In the context of our theory, the resources of marketing organizations are less transferable through markets than others, since those resources consist substantially of the specific knowledge embodied in the organization's personnel and, therefore, must be reallocated through the firm. Marketing here refers to the pricing, warehousing, packaging, transportation, and retail distribution of the firm's products. Among food industries, there clearly are elements of similaril^ in the marketing channels of products. The most similar are the chan- nels for marketing products which use the same physical distribution facilities (warehouses, trucks); two such groups are refrigerated grocery products and alcoholic beverages. Moving along a continuum through less similar products, we encounter products sold through the same retail outlet (for example, grocei^ products) and then produce sold to similar classes of buyers (consumer nondurables). Using this notion of a continuum, marketing expertise should lead firms to diversify into those products which are relatively closer to their own, and industries with strong similarity in marketing links are more likely to be linked by diversification than industries with weaker or nonexistent similarity.

A third type of firm-specific knowledge arises in the firm's manufacturing organization; The technological problems of commodify processing may be quite sim- ilar to those of other products. Therefore, expertise in the preservation, separation, and acquisition of raw materials^ and in machinery design, inventory con-

trol, and jquality control may be transferred to tech- nologically related products. Within the food indus- tries, for example, skill in one of the canning in- dustries provides a basis for diversification into another; the same may be said for diversificaron among the industries In grain milling or vegetable oil refining.^ As in the marketing case, the resources of production organizations which generate diversifica- tion are personnel who possess the sharable, firm- specific knowledge of production techniques.

A last source of diversification also arises firom pro- duction. As output grows in the primary activity, the firm often generates large quantities of byproducts and may o^n require iarge quantities of a particular input. If there are high transportation costs and econ- omies of scale in production of the input or in further processing of the raw material, the least-cost organi- zation of production of the item may be a single plant. In such a case, our original firm faces the risk that its byproduct generation or input demands will face a simple buyer of byproducts or a monopolist seller of inputs. The efficient solution is for the firm to in- tegrate into^he upstream or downstream activity and manage input production and byproduct processing itself. ' This situation should occur only among large producers of a primary good with scale economies and high transport costs in inputs or byproducts. For example, leading canners often manufacture their own cans.

The Incentive to Divers^

The incentive for a firm to diversify is increased prof- its. Relatively high expected profits in a primary in- dustry should lead the firm to invest there. Girowth in the primary Industry, coupled with market character- istics which require vertical integration, lead to in-

^In the SIC system of plant classification» there are seven four- digit grain milling industries, anci the differences among products in the seven industries are subsUintial enough to generally require processing In separate es^blishments. Most firms that produce grain mill products specialize in one of these industries; those that eventually diversi^ production are likely to enter other grain mill- ing industries because of similarities in raw materials, techniques, and distribution jskills.

'The solution is efficient in two sensesv First, the integrating firm can reduce its costs. Second, monopsony will raise thé price of a producty relative to other inputs, and if input substitution exists, the buyer will shift to an Input combination that is inefficient under competitive prices. Integration will lead to lower total production costs in the two stages and gféatér output. A similar condition holds for monopoly.

Product Diversification Trends in U.S. Food Manufacturing

vestments in vertically related activities such as byproduct, input, and ñnal product processing/Rela- tively low expected profits in the primary industry should lead firms to diversify toward those higher profit secondary industries in which the firmes shar- able assets can be applied.

The factors mentioned thus far should influence the industrial directions of diversification and the level of diversification that a firm might attain. Another fac- tor, the size of the firm, should also constrain the level of diversification. Given competition and scale economies, in order to achieve least-cost production levels, the firm must be large enough to achieve min- imally efficient scale in all products. Therefore, the larger the firm, the greater will be the number of in- dependent products that can be manufactured. In this way, factors that influence firm size will also indirect- ly influence levels of diversification. Such factors in- clude communications technologies, which alter the relative cost of managing large organizations; those government tax, procurement, and antitrust policies whose effects vary with size of firms; and intersec- toral demand shifts (since average firm sizes vary greatly across sectors). During periods in which large firms grow rapidly and more firms become large, average levels of diversification in the economy should increase. Alternatively, during periods in which large firm growth stagnates and smaller firms begin to proliferate, average levels of diversification should decline.

In the process described so far, firm size places a constraint upon the amount of diversification that a firm may achieve. Relative profits and intangible assets should influence both the level and the direc- tions of diversification. Firms should diversify into in- dustries related to their own through marketing and production similarities. The degree of relatedness among industries will vary; firms should diversify first into those industries most closely related to their own, and then into industries with more tenuous links. Firms should be far less likely to diversify into unrelated industries.

The outline provided here is rather simple. Indeed, it is kept purposefully so in the belief that a simple framework can aid in identifying the principal under- lying sources of diversification without treating each instance as a special case.

Data Sources and Measures of Diversification

Several sources and measures of diversification data are used in this report. They differ in units of observa- tion (single firms or groups of firms), level of industry detail, and extent of information provided (table 1).

Sources of Diversification Data

For 1975, diversification data were obtained for the 200 largest food manufacturers from Economic Infor- mation Systems, Inc. (EIS). The original EIS set lists for each firm the location, principal industry, and number of employees of all establishments with more than 20 employees. In order to obtain estimates of the dollar value of plant shipments, the employment figures were multiplied by the average value of ship- ments per employee in the relevant industry (using Census Bureau ratios); estimated firm shipments in an industry are then the sum of establishment ship- ments [8], Note that secondary output of plants is assigned to the principal industry of the plant; that is, I follow the Census Bureau convention.

The EIS data provide information on the extent and directions of large firm diversification in 1975. Federal Trade Commission (FTC) data provide the same information for 1950, thereby allowing for in- vestigation of 1950-75 change [35]. The FTC source includes shipments, by five-digit product class (a nar- rower level of detail than industry), for the 100 largest food manufacturing firms. The data were ag- gregated to the four-digit industry level for analysis. FTC data detail the secondary output of establish- ments, while the EIS data do not; the consequences will be explored in the statistical sections.

Special tabulations by the Census Bureau provide a third source of data. The Census data are for group- ings of firms (for example, the largest 25, or all firms in flour milling), without company detail. Census di- versification data are of two sorts: one is the average number of industries participated in by a group of firms, while the second shows the number of firms in a group who were active in a particular industry. The Census Bureau provided special tabulations for the 500 largest food manufacturers (and various sub- groups) in 1967, 1972, and 1977 [26, 27, 28]. Similar special tabulations were obtained earlier for 1954,

James M. MacDoiiald

Tabks 1 -Data acia usad in n^rt

Data set Ycar(s) covered Universe Comments

EIS

FTC

1975 200 largest focHl manufacturers.

1950 140 largest food manufacturers.

Individual firm data; covers aU activities; ignores secondaQjr output of ^tabltehments.

Individual firm data; only manufacturing is covered.

Moody's Industrial Manual

Census Special Tabulations

1919 1929 19a9 1950

1954 1958 1963 1967 1972 1977

53 large food manufacturéis (37 for 1919).

100 and 500 largest food manufacturers.

Individual firm data; does not give shipments ^timates; all firms are in FTC set.

Observations are for ^oups of firms; data presented are counts of the number of firms in an activity or the number of activities of a group of firms.

Census Enterprise Statistics

1963 1967 1972 1977

Three-digit food industries. Observations are for all firms assigned to an industry; data are largely shares of empfoyment in primary and secondai^ industries.

Sources: [5, 17, 18, 26, 27, 28, 29, 30,35],

1958, and 1963 [IS]. The Census Bureau also pub- lishes diversification data, at the three-digit leveU for all firms in a specific industry. These Enterprise Statistics are avaltable for 1963 through 1977 [29, 30], Census data do not provide the company detail of the other sources, but they cover a wide size range of companies, and they allow for closer analysis of time trends.

Finalty, early^data for the 1919-50 period were ob- tained ñt>mJtfoody's Industrial Manuals [17] for a sample of large publicly held firms. Moöd%^sMarmals provide accurate listings of the industries that ifi- dividuaL firms participated in during a given year. The MoodyV information, collected for 1919, 1929, 1939, and 1950^âtUows for an o^^rview of ead^r trends in food manufacturer diversification. Other trade pub- lications provide diversification detail, thereby sup- plementing the large data sets for the period up to 1984.

Measure« of Dlvei^ifieation

I used three measures of diversification. Each yields similar results, and they are highly correlated. Subtle differences, however, may appear in analyses of par- ticular flrmsv

The industry count (N), a simple count of the number of industries in which a firm engages, is widely used because it is easily available. N Is the only measure that can be used priorio 1950, and it is also the most common measure in the Census special tabula- tions. Although readily comprehensible, N measures only one aspect of diversification, ignoring the distribution of a firm's shipments across industries.

The specialization ratio (P), the share of primary in- dustiv shipments in the firm's total (the primary in- dustiv has iBhe largest share of firm shipments), is a crude means of meeting the distribution criterion.

Product Diversification Trends in U.S. Food ManuflK^iiring

The measure ignores the number of activities of a firm and the distribution of sales among secondary activities, but it is easily obtained and is highly cor- related with N and with more comprehensive indices.

Comprehensive indices reflect both the number of in- dustries of a firm and the complete distribution of shipments across them. The comprehensive index (C) used here is defined as follows:

N 0 = 11 {1/pfi

isl

or

N

logC = EPilog(l/Pi)

(1)

(2)

where Pj is the share of firm shipments in the i**^ in- dustry. The C index, also known as the entropy and the Shannon index, has been used in several eco- nomic analyses of diversification [3, 4, 13, 16] and is widely used in ecology in the study of species diversi- ty in a particular habitat. Given the distribution of shipments across industries, the C index increases as the number of industries increases. Given the number of industries, the index increases as smaller activities grow relative to large ones.

The index has two particularly desirable characteris- tics. First, it is expressed as a numbers equivalent. The significance of this can be grasped with an ex- ample. Assume that a firm is active in 15 industries. Five are important, each accounting for 15 percent of firm sales; five are quite minor, each accounting for 1 percent of sales, and the others each account for 4 percent of sales. Now, clearly this firm is not as diversified as one with sales evenly divided among 15 industries, since its sales are concentrated in 5 of the 15. It is clearly more diversified than one with sales evenly spread across 5 industries because it has an even spread across 5 and also has 10 more. The weighting scheme embodied in the formula for C places this representative firm more precisely be- tween the two extremes. According to the formula, the value of C for this firm is 7.3, which says that the firm is more diversified than one with sales evenly spread across seven industries. The maximum value

of C for any firm is N, the number of industries of the firm, and the minimum is 1.

The second characteristic is decomposability. Spe- cifically, the comprehensive index across all of a firm's activities, Cj, may be decomposed as follows:

CT = CA + CW

1 s 1

(3)

(4)

where C/v is a comprehensive index defined across a firm's two-digit industry groups (the P| of the entropy definition then becomes the share of firm sales in the ith two-digit group). In the present analysis, C^ is a measure of diversification outside of food manufactur- ing, while Cw is the weighted average of comprehen- sive indices across four-digit industries within each two-digit group. The weights (Pj) are the share of firm shipments in each group. One component of C^y is of particular interest. That is Cp, a comprehensive index defined across all four-digit food industries. The several comprehensive indices can be used in com- bination to describe the industrial directions of food manufacturer diversification.

Current Directions of Diversification

Large firms in today's economy produce in an enor- mous number of industries. Here I detail the extent of diversification by food manufacturers, the principal industries to which they've directed their expansion, and the connections among their industries. The prin- cipal conclusions are as follows:

• Leading food manufacturers are highly diver- sified, within food manufacturing as well as outside of it. Very few large firms are not diversified.

• Within food manufacturing, there is a system- atic clustering of firms among particular groups of industries. Some firms confine their activities to branded food products sold in grocery stores, ignoring products with more disparate sales patterns and those sold to other producers. Other firms concentrate on producer goods industries, avoiding consumer products.

M. MaeDanald

Marketing organizations are Important bases of diversification, and their importance as a base tias greafly increased since 1950.

diversified across food industries (Np). The smaller firms among the top 200 are also generally active in

While there have been significant investments in the food industries by conglomerates from other manufacturing si^tors, their activity has usually been limited to a small number of industries, and they account for a small share of shipments in most food industrie.

By implication, much diversification within the food industries is at least potentially based on the transfer of marketing and production assets to new activities.

Diversification into other manufacturing ac- tivities, outside of food, is relatively small, restricted to the largest food companies and concentrated in consumer products and in- dustries that are vertically related to the food industries (such as packaging and food proc- essing machinery).

Diversification outside of manufacturing has been an important and rapidly growing com- ponent of the total. Smaller food manufac- turers, as weU as large, have diversified into wholesaling, retailing, transportation, and agriculture. Food manufacturers have exten- sive, expanding operations in food wholesal- ing and in eating and drinking places. They are not major factors in transportation or agriculture, but their Investmente in those areas have grown rapidly in recent years.

Levels of Diversification, 1975

Average 1975 levels of diversification among food manufacturing firms, using N and C indices, are presented in tables 2 and 3.

Indtts^ Counts. Measures of N are presented in table 2. Nj is the number of industries in all sectors; Njj^ is the number of industries in manufacturing, and Np is the number of Industries in food manufac- turing. Mean values generally exceed medians, but the difference is small, and average levels of diver- sification clearly increase with size. The largest firms average over 20 Industries each (Nj) and are widely

Table 2 --Nnnber of industries of leading firnis, 1975

Indices Size dass of firms, ranked by food shipments

1-25 26-50 51-100 101-200

Number

Median NT 20.00 12.00 7.00 4.00 MeanNr 23.12 13.08 8.40 6.97 Median NtM 15.00 11.00 4.00 4.00 Median Nn« 19.44 11.64 6.80 5.41 Median Np 9.00 8.00 4.00 3.00 Mean Np 11.36 8.00 4.76 3.50

NT S number of manufocluring industries participated in, across all sectors;

N-pM» number of manufeicturing industries; Np s number of food manufocturing industries.

Source: Author's calculations, based on data acquired by John Connor and Loys Mather from Economic Information Systems, Inc.

IMite 3-DiveñMcation levels, 1975

Indices Size class oí firms, ranked by food shipments

1-25 26-50 51-100 101-200

Number

Median Q 6.31 4.60 3.11 2.14 Mean C^ 9.12 6.38 3.85 3.59 Median C^ 6.15 4.49 2.66 1.98 MeanCxM 8.26 5.42 3.28 3.08 Median C^ 2.08 1.71 1.48 1.22 MeanCA 2.52 1.96 1.88 1.92 Median CAM 1.42 1.30 1.00 1.00 Mean CAM 1.95 1.41 1.32 1.46 Median Cp 3.76 3.67 1.92 1.96 MeanCf 4.56 4.10 2.71 2.14

CTS comprehensive diversification index across alt four-digit manufacturing industries; CTM - diversification across ail four-digit manufacturing industries; CA s dh;ersification across all two-digit indùistries; CAM ^ diversification across all two-digit manufacturing industries; Cp s diversiflcation across four-digit food manufacturing industries.

Source; Author^ calculations, based upon data acqjulred by John Connor and Lo|^ Mather from Economic Information Systems, inc.

8

Product Diversification Trends in U.S. Food Mannfactoring

several food industries. Only modest manufacturing activity occurs outside food; food industries account for roughly 70 percent of all manufacturing industries of food firms ranked 26-200, and 60 percent of the top 25 firms. The largest class has significant non- food interests, with an average of eight other manu- facturing industries and about four nonmanufacturing industries.

Comprehensive Indices. Comprehensive indices, presented in table 3, provide a more complete view of 1975 levels of diversification. Cj, C^, and Cp refer to diversification across all four-digit industries, all two- digit groups, and all four-digit food manufacturing in- dustries, respectively. For purposes of comparison to the 1950 data, Cj and C^ were recomputed for the manufacturing sector only. The adjusted indices were

Mean values of the C indices substantially exceed me- dian values, reflecting especially extensive diversifica- tion by a few firms.^ Because the correlation coeffi- cient between Cj and firm shipments was -i- 0.56, diversification is strongly associated with firm size. Because median C^j^ in the two smaller size groups is 1.00, most of those firms have no nonfood manu- facturing, and entry into other manufacturing groups is therefore clearly restricted, for the most part, to the largest companies.

Several additional conclusions seem obvious in table 3. Values of C are generally 40-50 percent as large as corresponding values of N, with larger percentages among smaller firms. If a firm's shipments in each of its industries were equal, N and C would be identical. The large differences indicate that firms in 1975 typically had a few major industries and a large num- ber of relatively minor activities. Considering the low values of C^, diversification across groups, the me- dian firm in size classes below the'top 25 was con- siderably less diversified than one with sales evenly divided across two manufacturing groups. Finally, food firms concentrated most of their manufacturing diversification within food. Elsewhere I have shown that food manufacturers are unique in this respect [14]. In manufacturing groups other than food, niost secondary manufacturing employment in 1977 was

outside of the primary two-digit group, a pattern also true of Japan, Canada, and Great Britain [5, 12, 37],

Diversification Witliin Food Mannfactaring

Leading food manufacturers are widely diversified within the food industries (see Np and Cp in tables 2 and 3), and certain patterns stand out. Consider here the typical directions of diversification within food manufacturing (table 4). (SIC numbers only are listed to conserve space. See appendix B for füll titles and descriptions.) Column 1 lists the average number of diversified entrants, from the list of the 200 largest food manufacturers, in each four-digit industry. An entrant to an industry is here defined as a diversified producer for whom the industry is not primary; for example, Kellogg would be defined as an entrant in all industries but breakfast cereals. Column 2 lists the estimated share of industry sales accounted for by those large diversified entrants. The estimates appear to be reasonably accurate when compared with data from the Bureau of the Census.^

On average, large diversified entrants account for 35 percent of shipments in food industries in 1975, but there was a great deal of variation across industries. Almost no diversified entry occurred in beet sugar or in cottonseed oil, for example, while entrants ac- counted for almost all shipments in pet food. When the sample is broken down into 11 producer goods and 34 consumer goods industries, levels of entry (by number of entrants or share of shipments) are substantially lower in producer goods."

Functional Relationships Between Primary and Secondary Industries. In columns 3 through 5 of tables 4 and 5, the market share of diversified en- trants is distributed among three categories accord* ing to the relationship between the secondary in-

^Because the N index did not show a large discrepancy between mean and median values, the source of the difference must lie in the distribution of shipments across industries, rather than in the number of industries of diversified firms.

'The Census Enterprise Statíatica listed the share of industry shipments accounted for by firms for whom the industry is primary [29, 30]. The Enterprise Statistics industries often include several four-digit SIC industries, so one must aggregate the EIS industries for comparison. Secondary production, in the Enterprise Statistics, includes all firms, not just the 200 largest. My EiS-based estimates, therefore, should be smaller than the Enterprise Statistics,

"Consumer goods industries are those for whom at least 50 per- cent of total commodity output was sold to final consumer demand or to eating and drinking places, according to 1972 detailed Input- Output Tables [34].

TaMe 4—DIverslllcatloii within food manufactariiig by the 200 largest food ataiiiifactiirers« 1975

Industry SIC

number^

(1)

Entrants

(2) Share of Industry

sales

(3) Production- related as

percent of (2)

(4) Marketing- related as

percent of (2)

(5) unrelated as percent of

(2)

Number

2011 18 2013 39 2016-7 29

2021 12 2022 23 2023 17 2024 26 2026 16

2032 25 2033 38 2034 22 2035 31 2037 34 2038 37

2041 12 2043 14 2044 2 2045 12 2046 8 2047 24 2048 37

2051 26 2052 19

2061 7 2062 4 2063 1 2065 35 2066 9 2067 6

2074 2 2075 13 2076 8 2077 7 2079 19

2083 6 2082 5 2084 18 2085 7 2086 26 2087 17

2091 15 2092 13 2095 10 2097 6 2098 7

18 36 29

26 22 35 69 19

32 34 60 60 50 55

22 43 11 45 28 90 28

22 23

39 19 2 44 43 52

3 35 44 16 71

48 13 46 27 22 18

71 25 31 31 19

28 69 86

85 88 88 84 97

6 14 3 17 15 6

100 66 0

80 69 44 84

48 32

54 59 0 14 30 0

59 94 100 100 31

100 0 0 0

27 0

71 0

11 0 13

Percent —

0 20 14

15 10 10 16 3

54 52 91 75 69 68

0 31 100 8 0 46 0

13 34

0 0 0

62 70 25

0 0 0 0

65

0 0 98 48 14 90

23 53 86 100 51

72 11 0

0 2 2 0 0

40 34 6 8 16 26

0 3 0 12 31 10 16

39 34

46 41 100 24 0

75

41 6 0 0 4

0 100 2 52 59 10

6 47 3 0

36

^See appendix B for titles and descriptions of SIC numbers.

Source: Author's calculations, based on data in [8].

10

Product Dhreratficatlon Trends in U.S. Food Mannfactaring

Table 5-A saniniary of divefsification within food manufactnring by the 200 largest food flms, 1975

Industry category

All food industries

11 producer goods industries

34 consumer goods industries

(1)

Average number

of entrants

(2)

Entrant share of

ship- ments

(3) (4)

Production- Marketing- related as related as

percent of (2) percent of (2)

(5)

Unrelated as percent of

(2)

Number

17

10

19

35

26

38

44

69

36

■ Percent •

33

0

44

22

31

20

Source: Author's catculations, based on data in [S].

dustry and the primary industry of the diversifying firm. There is an unavoidable amount of subjectivity in such an exercise, and so the conclusions should be viewed as tentative.

Column 3 lists the share of entrant shipments by di- versified entrants whose primary industry is related to the secondary (entered) industry through production similarities. Production-related activities fall into two categories. One covers vertically related industries, where one industry supplies another. In this category, I included the activities of meat packers in processed meats, for example, and also the activities of feed producers in broiler processing. I also included by- product activities, chiefly in feeds and animal oils. Finally, I included the activities of retail foodstores in grocery product manufacturing. The vertical category is fairly clearcut and should not be controversial. The second production category is horizontal production relatedness; here, I grouped activities with a common raw material or with production processes deemed to be quite similar. For example, activities of fluid milk processors in other dairy industries were grouped here because they use a common raw material. Pro- duction by soybean oil processors in other vegetable oU industries was also grouped here because oil prod- ucts use similar technological processes and face similar problems in raw material preservation, stor- age, and processing. Finally, processors of substitute products are included (for example, beet, cane, and corn sugar), even though production processes may differ, because the industries share a common tech-

nical knowledge of the properties of the final product, and firms with the skills to produce in one may there- by generate the technical skills to introduce products in the other industry.

Column 4 lists marketing-related activities, falling in two categories. One consists of products distributed through the same physical marketing channels as the primary product. For example, a firm with a wide- spread refrigerated distribution system may market a variety of meats, dairy products, and refrigerated preserved products through the system. A firm with an alcoholic beverage distribution network may mar- ket wines as well as liquor in that network. The sec- ond type of marketing similarity is broader; it con- sists of grocery store food products sold by firms with widespread grocery manufacturing activities. This cat- egory consists of firms with skills in pricing, pro- moting, transporting, and storing consumer food products through a broad distribution network.

Column 5 lists unrelated diversification, which in- cludes diversification into food industries by firms from other consumer product industries, diversifica- tion among food industries with no obvious similar- ities, and conglomerate entry into food. In short, there are also various graduations of unrelatedness. This category should, however, correspond to the FTC merger series category of "other conglomerate mergers," with "other" essentially meaning unrelated.

There is one last conceptual problem in assigning firms to categories. We can probably agree that the

11

James M. MacDonald

1975 meatpacking activities (SIC 2011) of LTV Cor- poration (pTimarily active in steel, aerospace, and electronics) fall into the unrelated category. What about production by LTV's meatpacking subsidiary in processed meats (SIC 2013)? This type of case, an in- direct relatedness, was resolved by classifying the meat processing activities as production related (since there is a strong technological relation to meatpacking) while classifying the mealpadting ac- tivities as unrelated.

On average, 44 percent of shipments by firms enter- ing food industries were production related. Percent- ages of production-related shipments vary greatly across industries. They are very high in the dairy industries; almost all diversification into dairy in- dustries was carried out by other dairy firms, a phenomenon that occurred as far back as 1919 [25]. The remarkable absence of diversification into dairy industries by nondairy firms stands out clearly in the data. Production relatedness is also high, generally, in the producer goods industries. Horizontal relation- ships account for much diversified entry in the vege- table and animal oil industries, and vertical relation- ships appear to account for diversification links in the grain industries, malting, and in broiler processing.' The expansion of the agricultural export trade in the seventies provided profitable opportunities for these firms to expand into a range of related activities.

On average, an estimated 33 percent of large diver- sified entrant shipments were marketing related. This surely is higher for consumer food industries and was especially high in firms producing beverages and pre- served fruit and vegetables. Later we shall see that very little diversification in 1950 was based on mar- keting. By implication« application of marketing skills accounted for a substantial portion of the 1950-75 in- crease in diversification. The average share« while not dominant, has certainly grown since 1950, and the estimate is rather conservative. It would be quite a bit higher if I were less inclined to ascribe diver- sification among grains, oilseeds, and dairy industries to production similarities.

Finally, the percentage of firms in the unrelated cate- gory also varies substantially across industries. The

^One may argue that marketing actually accounts for the grain and oilseed figures, since these firms maintain extensive transpor- tation, storage, and distribution facilities.

share of all entrant shipments in the unrelated cate- gory tends to be highest where the total share of en- trants was relatively low—in meatpacking, sugar, cot- tonseed oil, brewing, and bottling. (Chewing gum was an exception.) Total entrant food shipments in the un- related category were also quite concentrated; 35 per- cent of con^merate shif>ments were in meatpacking, 10 percent were in bottling, and 6 percent each in brewing and feuit and vege^ble canning. Conglo- merate activity in the food industries Is still small.

This evidence suggests that while there Is significant unrelated diversification, many food firms do follow systematic strategies In their diversification within food manufacturing.

The Patteñis of Individual Firms. Commodity food processors—firms who transport, store, and proc- ess bulk grains, oilseeds, and meat products, but do not distribute to retail—have faced a distinct set of diversification opportunities.

At the beginning of the seventies, Cargill, the large grain trading firm, had an extensive network for transporting and storing grains, as well as obvious in- stitutional expertise in trading grains. During the sev- enties, Cargill used those assets to become a leading processor of a variety of commodity food produce. Through internal construction and acquisitions, Cargill became one of the largest flour millers in the country, and one of the four leaders In wet corn mill- ing. The firm also constructed several soybean and sunflower oil plants. Finally, Cargill has diversified into meatpacking, feeds, poultry processingi^^ and salt processing. Note that Cargill has not expanded Into branded consumer products, but has confined Itself to products related to its distribution network or prod- ucts that require the transporting and purchasing of bulk food commodities.

Archer-Daniels^Mldland (ADM) has followed a similar strategy. The firm is among the largest flour and wet corn millers in the countiv and has also expanded into soybeans and hydroponics. In response to the growth of agricultural exports in the seventies, ADM acquired grain elevators and transport firms^ increas- ing the scale of its distribution network. In general, the firm also avoided branded consumer food prod- ucts, but expanded in domestic and foreign grain and oilseed processing. Both Cargill and ADM, then, have

12

Product Diversification Trends in U.S. Food Manufacturing

based their expansion upon existing expertise in grain and oilseed transport, processing, and distribution. They have avoided consumer food products and entered other commodity industries that were rapidly growing (soybeans, wet corn milling) or subject to jfiindamen- tal shifts in the location or technology of production. Such industries offer significant profit opportunities, and diversifying commodity firms are well positioned to enter.

Conagra, rooted in grain processing, has expanded in a slightly different direction. The company became a leading poultry processor, a field which today is highly integrated, from chick and feed production (Conagra's base of entry) through broiler raising to processing and retailing. Innovative poultry proces- sors introduced more effective quality control, new developments in products (through bigger birds and different cuts) and production processes, and rapid distribution to retail outlets. Following diversification into broilers, Conagra diversified into meat, catfish, and seafood processing, all bulk-food operations in which opportunities for innovation in distribution, production methods, and new products may exist. Finally, with the growth of the grain export trade and the deregulation of grain transportation, Conagra has expanded its flour milling operations and its grain distribution network.

Many food processors sell their output through grocery stores to consumers, rather than to other producers. The largest of these firms have diversified extensively over time, and much of their diversifica- tion has been based upon their marketing experience. One might begin with the Campbell Soup Company, where diversification began in the fifties with the ac- quisition of the Swanson frozen food line. When the company later acquired the Pepperidge Farms bakery company, it had a nationwide distribution network available through which it could Introduce a variety of specialty baked goods, through frozen as well as regular channels. Later the firm acquired Mrs* Pauls fi'ozen fish plants and the Vlasic line of pickles. Campbell has confined itself to branded consumer food products, sold largely through grocery outlets, and has avoided entry into bulk commodity process- ing or unrelated manufacturing activity.

Nabisco Brands has also emphasized branded con- sumer food products. Prior to their 1981 merger.

Nabisco and Standard Brands each produced a varie- ty of dry grocery products in a large number of coun- tries, with some unrelated activities, such as Nabisco's toiletries business and Standard Brands' interests in wet corn milling and alcoholic beverages. Since the merger, the combined firm has sold off the toiletries, dog food, and alcoholic beverage businesses, has begun to exit from flour and wet corn milling, and has acquired Lifesavers Candy from Squibb. Nabisco Brands is now involved in a large variety of domestic and foreign grocery product industries, while avoiding further expansion in nonfood or producer goods industries.

The major tobacco firms faced a different set of in- centives, and a somewhat different set of opportu- nities, than those faced by processed food firms. As per capita tobacco consumption began to lag in the late fifties, large cigarette firms diversified. The firms did not have a distribution network that could easily be adapted to other products, and they did not have experience in large-scale food production. They were, however, experienced in the promotion (pricing, ad- vertising, and introducing new products) of branded consumer nondurable products and, in general, they diversified into those types of products. R. J. Reynolds, for example, has displayed a general strategy of diversifying into branded food products. Early acquisitions were in canned products, with the purchase of Pacific Hawaiian Products (^'Hawaiian Punch"), the Chun King Corporation, and Patio Pro- ducts. With acquisitions of Del Monte (canned fish, fruits, vegetables, and specialties) in 1979, Morton Frozen Foods in 1980, Heublein (alcoholic beverages, specialty canned goods, Kentucky Fried Chicken) in 1982, and Canada Dry (beverages) in 1984, Reynolds became one of the largest processors of branded, na- tionally distributed, food products. Reynolds has also invested in an unrelated area, petroleum, with ac- quisitions of Signal Petroleum, Aminoil, and the U.S. subsidiary of Burmah Oil but then sold its petroleum operations to Phillips Petroleum in 1984.

Phillip Morris has concentrated in branded consumer products: razor blades (Persona), beer (Miller), and soft drinks (Seven-Up). American Tobacco (now American Brands) has pursued a wide-ranging diver- sification strategy within consumer products and is now active in canned juices, cookies and crackers, snacks, alcoholic beverages, toiletries, home hard-

13

Jfâof ë» M. MacDônalil

ware (staplers), and office products/Less than half ^^o^ American's sales now x»*igmate in tobacco. Before its 1980 acquisition by Graind Metropolitan» Liggett and Myers had also reduced the shar^ of firm sales of tobacco to less than one^half through diversification into alcoholic beverages, pet foods, toiletries, and jewelry.

With the exception of Reynolds' oil interests, all ma^ jor cigarette firm diversification was directed toward branded consumer products in industries in which ad- vertising and new product introductions were impor- tant. Many of these industries are in food, and these firms have become major food processors.

Other food firms, market leaders in specific indus- tries, have diversified into other consumer food in- dustries, and have become diversified food marketers in the process. Pillsbury, with acquisitions since 1975 of Haagen-Dazs, Green Giant, Pioneer Food Indus- tries, American Beauty Macaroni Co., and Totino's Frozen Pizza, has expanded into canned and frozen fruits, vegetables, and specialties, as well as ice cream, rice, and pasta products. Since 1975, General Foods has expanded into specialty baking (Enten- manns), processed meats (Oscar Mayer), and pasta products (Ronzoni) in addition to its existing wide line. Coca-Cola, Pepsico, and Anheuser Busch have diversified into snacks, specialty baked goods, and other beverages. In short, market leaders in various branded food product categories have expanded into a variety of other consumer product food industries, in addition to firms such as Beatrice, Borden, Pet, General Mills, and Consolidated Foods, who had diversified widely across consumer food industries in the fifties and sixties. That these firms have chosen such industries suggests that marketing factors play a major role in current diversification strategies.

Marketing's Shift In Impoirtànçe. Thorp, writing in 1923, surmised that marketing could serve as a base for diversification among the food industries [25]. Yet marketing did not really become a major source until well after 1950.

Several factors have combined to alter the techno- logy of marketing since 1950. For example, televisiofi has become a very important advertising medium. Data from the National Commission on Food Market- ing indicate that food manufacturers (exclusive of tobacco and alcoholic beverage producers) allocated

about 7 percent of their total advertising expenditures to television in 1950 [18]; by 1980, the proporiion was 80 percent [20], The development of television advertising, along with improvements in ^ansporta- tion, communications, and production, may have reduced the costs of introducing products into nation- wide distribution, thereby increasing the number of nationally distributed products. Widespread distribu- tion often requires mass production in multiple plants and the development of large marketing organiza- tions within firms, with personnel oriented toward problems of retail distribution, new product introduc- tion, and advertising rather than production. As a result, those firms which could initially develop a na- tionwide distribution network for a particular food product often found that network to be adaptable to the advertising, retail distribution, inventory control, and transportation of other food produce enterifig na- tionwide distribution.

Diversification into Otiier Manufaetaring industries

Diversification into other manufacturing industries is mostly restricted to the largest food manufacturers. Census data show that those food firms ranked 201-500 in food shipments were diversified to some extent, but at least 92 percent of those smaller firms had no nonfood manufacturing activity. That pattern also generally holds among the 81 firms in ranks 101-200 who were primarily active in food; at least 82 percent had no nonfood manufacturing activity in 1977. Therefore, this discussion is largely liniited to activities of the largest food manufacturers and some conglomerate entrants with interests in food.

Principal Directions of Diversification ^Tw<i- Digit Groups. Table 6 describes the 1975 activities of the 200 largest food manufacturers in manufactur- ing industries outside of food. Because a number of leading food manufacturers have diversified into food industries from other nonfood industries, totals are described both for firms whose primary activity is food manufacturing or processing and those whose pri- mary activity is the manufacture of nonfood items. Note that the 200 largest food manufacturers had ap- proximately $51 billion in estimated shipments in nonfood manufacturing activities, or 18 percent of their total shipments.

14

Product Dlvenificatioii Trends in U.S. Food Manafaetnring

Table 6«* Distribution off aianvffactaring sUpaMimts outside off ffood and tobacco, l>y the 200 kurgest food uianufacturers, 1975

SIC number

All firms' Primarily food Primarily nonfood Title value of firms' value firms' value of

s hipments of shipments shipments

Number Mttlion dollars Number Maiion

dollars Number Million dollars

22 Textiles 15 1,117 9 347 6 770 23 Apparel 18 1,686 13 996 5 690 24 Lumber and wood 8 314 8 314 0 0 25 Furniture 9 407 7 372 2 35 26 Paper 23 6,958 18 2.039 5 4,919 27 Printing and publishing 13 717 7 163 6 554 28 Chemicals 59 19,004 45 6,933 14 12,071 29 Petroleum 0 0 0 0 0 0 30 Plastics and rubber 30 1,707 20 1,362 10 345 31 Leather 9 545 7 455 2 90 32 Stone, clay^ and glass 14 683 7 189 7 494 33 Primary metals 13 3,674 6 412 7 3,262 34 Fabricated metals 31 3.469 17 636 14 2.833 35 Machinery, except electrical 29 1,676 19 557 10 1.119 36 Electrical machinery 17 6.283 10 511 7 5.772 37 Transportation equipment 12 1,310 5 234 7 1.076 38 Instruments 15 960 6 105 9 855 39 Miscellaneous 22 1,221 16 1,007 6 214

All nonfood, nontobacco 92 51,731 72 15,632 20 35,099

Source: Author's calculations, based on data developed for Connor and Mather {8\,

The major direction of investment by food firms clear- ly is toward chemical manufacturing, SIC 28. Of the 72 firms who diversified from food manufacturing into other manufacturing industries, 45 were active in the manufacture of chemicals; chemicals accounted for 44 percent of the value of nonfood manufacturing shipments of those firms (table 6). Other product groups which attract large numbers of food firms in* elude paper (18 firms), plastics (20)vfabricated metals (17), and machinery (19). Inspection of un- published data revealed that most of the companies in these four groups were in activities vertically related to food manufacturing^ specifically packaging and food-processing machinery.

Now, consider the two right-hand columns of table 6. These give a picture of the spread of activities of con- glomerate firms who have diversified into food, mingled with the activity of other less diversified firms who are engaged in, say, food and another in* dustry. Most of the latter produce chemicals. A num- ber of firms in the chemical group have long had substantial food interests. The chemical firms also had large sales in instruments (SIC 38) primarily in the manufacture of health care equipment. The en- tries into the metal, machinery, equipment, and pa- per groups represent the interests of conglomerate in- dustrial firms like Gulf & Western, ITT, IC Industries, and LTV.

Some food firms have entered the apparel and mis- cellaneous product groups, including games and sporting goods. These apparently represent decisions by consumer product food firms to expand into other consumer products for which, given demographic trends, demand should grow rapidly through the re- mainder of this century.

The Link Between Food and Chemicals. Among firms engaged primarily in the manufacture of food, 44 percent of their nonfood shipments are chemicals. Table 7 shows shipments in each three-digit industry class within the chemicals group for firms whose pri- mary interest is the manufacture of food, for those primarily engaged in producing chemicals, and for conglomerates.

15

James M. NacDoñaId

Table 7*Di8tribtttfon of shipniento In chetnleal nianaffaçtariag (SIC 28) by firms in the top 200 In U.S. food and ttiliMco^aleêf 1975

Types of firms All Food Conglomerate Chemicals

Number

Firms 59 45 7 7

Million doffars

Shipments 19.004 6.933 2.056 10.015

Distribution of shipments across three-digit industries within SIC 28: Percent

Inorganic chemicals 4.0 2.2 14.2 3.1 Plastics and resins 9.8 18.2 14.3 3.1 Pharmaceuticals 19.5 3.4 16.3 31.3 Toiletries 47.3 56.0 13.2 48.3 Paints 2.6 1,1 .2 4.1 Organic chemicals 4.2 4.4 14.9 1.9 Agricultural chemicals 9.3 9.8 21.4 6.5 Miscellaneous 3.3 4.8 6.0 1.6

Percentages may not add to 100 because of rounding. Food s primary activity is food manufacturing. Chemicals s primary activity is chemicals manufacturing. Conglomerates s primary manufacturing activity is neither food nor chemicals. Source: Author^s calculation, based on data developed for [8].

Among the 45 firms principally active in food manufacturing, toiletries account for more than half of their chemical shipments. Other prominent direc- tions are plastics and resins (282) and agricultural chemicals (287). Investment in the former class chief- ly reflects decisions made some years ago by major food manufacturers such as Borden and National Distillers to expand into industrial chemicals, while the latter class is often handled by major agribusiness cooperatives and corporations who have diversified widely across agricultural input and processing oper- ations. These firms typically have experience In mar- keting producer goods and skill in the processing, by chemical and biological means, of agricultural raw materials. Finally, the conglomerate firms have their shipments rather evenly spread across chemicals.

Among the firms which primarily produce chemicals, 80 percent of their chemical shipments are toiletries and pharmaceuticals; firms in these specific areas are clearly far more likely to enter food industries than are other chemical firms.

One clear conclusion emerges. Toiletries obviously

represent a major source and direction of diversifica- tion with regard to food manufacturing. Such prod- ucts are sold through grocery outlets, are nationally distributed, and often are heavily advertised. That is, they bear strong similarities in marketing characteris- tics to branded food products. Marketing similarities, combined with profit opportunities, are potentially key sources of the observed links between food and chemical industries.

Diversiflcatioii Outside of Manttfactaring

There are important links between food manufactur- ing and several industries outside of the manufactur- ing sector and two categories of diversification based on those links. First, several firms fi'om nonmanufac- turing industries, principally food retailers, have im- portant food manufacturing activities; that^s, firms engaged in retailing have diversified Into food manu- facturing. Second, many firms originally in food manu- facturing have directed a large amount of diversifica- tion into a limited number of nonmanufacturing in- dustries. When I speak of the largest food manufac- turers (for example, the 200 or the 500 largest) I

16

Product Diversification Trends in U.S. Food Manufacturing

commingle these two categories (since some retailers are also major manufacturers). In what follows, I distinguish diversification into food manufacturing from that flowing in the opposite direction.

In 1977, employment outside of manufacturing ac- counted for 28 percent of the total employment of all companies principally in food manufacturing, accord- ing to the Census Bureau's Enterprise Statistics [29]. These firms clearly did not distribute their invest- ments at random; 52 percent of their nonmanufactur- ing employment was in wholesale or retail trade and evenly divided (26 percent each) between those two. Employment was, in turn, concentrated in specific areas within those sectors, udth 60 percent of whole- sale employment gathered within food wholesaling and 40 percent of retail employment assigned to eat- ing and drinking places.

Retailing Investments. The industry comprised of eating and drinking establishments grew rapidly dur- ing the seventies because of rising incomes and mobility, increases in female labor force participa- tion, and the rapid increase in households. The first two factors caused the time spent in home food prep- aration to become more expensive. Rising time costs, combined with rising incomes and demographic trends, have led to growing demand for convenient eating and subsequent rapid industry growth. These market changes created opportunities for firms with experience in the development and introduction of new food products, in food transportation and stor- age, and in the development of financial controls for multi-establishment enterprises, areas in which food manufacturers possessed substantial existing organi- zations. Of the 500 largest food manufacturers, 58 had chains of eating places in 1977, up from 25 in 1967. During 1967-77, food manufacturer employ- ment in the industry expanded almost fivefold, and the number of establishments grew sixfold. After ex- panding in this industry, some food manufacturers have lately entered other specialty retailing areas. For example, Quaker Oats has acquired and expanded chains of retail eyeglass, hardware, and yarn stores, and General Host has acquired retail tree nurseries and the Hickory Farms chain of specialty foodstores.

Food retailing also has important links with food . manufacturing. Although some firms have diversified from food manufacturing into convenience stores and

specialty foodstores, none have so far diversified into supermarkets. However, a number of large grocery chains, such as Safeway and Kroger, operate signifi- cant food manufacturing facilities. Thirty-four retail grocery chains processed food in 1977 and operated over 300 food manufacturing establishments. Sixteen chains were among the 500 largest food manufac- turers. Food retailers manufacture only a limited number of products; 60 percent of their employees are engaged in the manufacture of baked goods and fluid milk [29], In addition to products that they manufacture, the chains also market products that carry their own label but are manufactured by other firms. There is no evidence that grocery chains have expanded their food manufacturing operations in re- cent years.

Food Wliolesaling. A food manufacturer may oper- ate two types of wholesaling establishments. The first sells only the manufacturer's own products and is called a manufacturer's sales branch or office. The other type is like any other merchant wholesaling establishment in that it purchases, for resale, the products of many manufacturers. Both types are in- cluded in the Census of Wholesale Trade [31,32,33],

Since manufacturer's sales offices and branches are exclusively concerned with the products of the man- ufacturer, expansion into wholesaling via sales offices and branches is a case of pure vertical integration and an extension of the manufacturer's marketing ef- fort for its own products. Most manufacturer activity in wholesaling is of this sort, since sales offices and branches account for 78 percent of food wholesaling employment of firms primarily in manufacturing. A manufacturer that operates merchant wholesale es- tablishments (22 percent of manufacturer employ- ment in food wholesaling) may distribute the products of several manufacturers, and is likely to view expan- sion into wholesaling as diversification into a new area not necessarily tied to the marketing of its own products.

Wholesalers may diversify into manufacturing, but only three wholesalers, with 205 wholesaling establishments (less than 5 percent of those owned by the 500 largest), appear among the 500 largest food manufacturers.

Retail food chains also own both wholesaling and manufacturing establishments. However, the whole-

17

Jflniuïs M« MftcDanádd

saling establishments of food retailers appear in the Census of Wholesale Trade only if more than 50 per- cent of their shipments are sales to other firms [31], The 16 food retailers among the 500 largest food manufacturers of 1977 operated only 63 food whole- saling establishments so defined, less than 2 percent of all food wholesaling establishments owned by the 500 largest food manufacturers. Consequently, whole- saling data for the 500 largest food manufacturers consist almost entirely of diversification by firms primarily active in manufacturing (table 8).

Firms that are major food manufacturers account for 19 percent of total employment in food wholesaling and 24 percent of sales. Their relative importance varies across four-digit food wholesaling categories, reaching a maximum (42 percent of sales) in the gro- ceries and related products category (SIC 5149), where half of the food wholesaling employment of the 500 largest is located. That category consists of prod- ucts such as coffee, tea, baked goods, canned prod- ucts, flour, pet foods, breakfast cereals, soft drinks, shortenings, and cooking oils. Roughly one-half of the 500 largest food manufacturers maintain some facilities in food wholesaling, and most of this whole-

saling activity reflects operations by firms that are primarily food manufacturers, since 90 percent of all the establishments listed in table 8 and 96 percent of those in SIC 5149 are owned by firms whose primary industry is in food manufacturing.

The likelihood of diversification into wholesaling in- creases with firm size. The 20 largest food manufac- turers, for example, have 25 percent of the total value of food shipments of the 500 largest manufac- turers, but 37 percent of the total value of food wholesaling sales, largely through the operation of sales branches and offices. Seventy-six of the largest 100 and 50 of the next largest 100 have food whole- saling activities. However, food wholesaling is not ex* clusively the interest of the largest firms; smaller firms in the largest 500 have a 40- to 45-percent like- lihood of operating a wholesaling establishment, and small firms that diversify are most likely to enter either wholesaling or closely related food processing industries.