Future of Consumerism - MITX FutureM Conference 2010 - AMP Agency Presentation

Upload

neil-clemmonsCategory

view

346download

0

Pondering The Agency of The Future

[Experience] Writing, Sales, Marketing, Customer Experience

[Client side] Startups, Apple, USRobotics, 3Com

[Agency] Critical Mass / Omnicom

[Advisory] Mobile, eCommerce, Analytics, SaaS

[Verticals] Technology, Financial Services, Retail, CPG, Automotive Luxury, Healthcare, Telecom, Professional Services

[Passions] Strategy / Technology / Consumer Behavior / Developing Talent

About Me

@neilclemmons

The Marketing Landscape

The Agency Landscape

The Opportunity Ahead

Implications for IMC Students

Agenda

The Marketing LandscapeThe Agency Landscape

The Opportunity Ahead

Implications for IMC Students

Agenda

• Marketing is increasingly about customer experience and engagement augmented by context.

• Context comes from data. Data feeds both the impression and the experience.

• Context is derived from many activities & sources - Transactions, Participation, Information, Conversation, Applications, Location, and others.

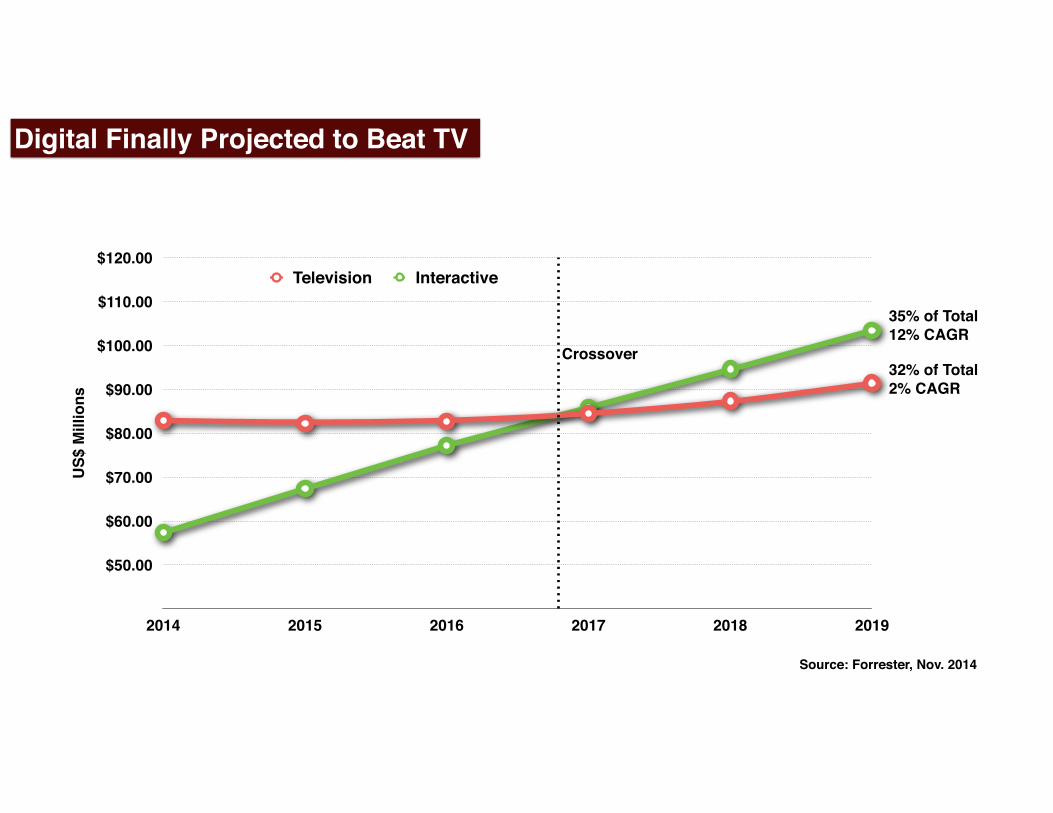

• Interactive media will reach 24% of spend in 2014. and surpass TV by 2017. Digital CPM’s have declined but are stabilizing with strongest growth in mobile and video over typical paid search and banner ads.

• Increasingly, brands and retailers are integrating services to deepen digital interactions and augment a product experience - compelling content, commerce, community, and connectivity tools.

• More and more, marketers are embracing pull efforts over the typical push efforts of the past. These include social media and hosted communities.

• Many marketers are wrestling with mobile as a key opportunity (and it’s the fastest area of investment right now). Yet most marketers have yet to establish a compelling mobile strategy.

• In time, we will see platforms and ecosystems of engagement and customer value that define marketing and value exchange to sustain relationships and encourage loyalty.

What’s Happening?

What’s Happening?

Accountability Increasing

Channel Choices Exploding

Speed Increasing

Budgets Shifting

Consumers Even More in Control

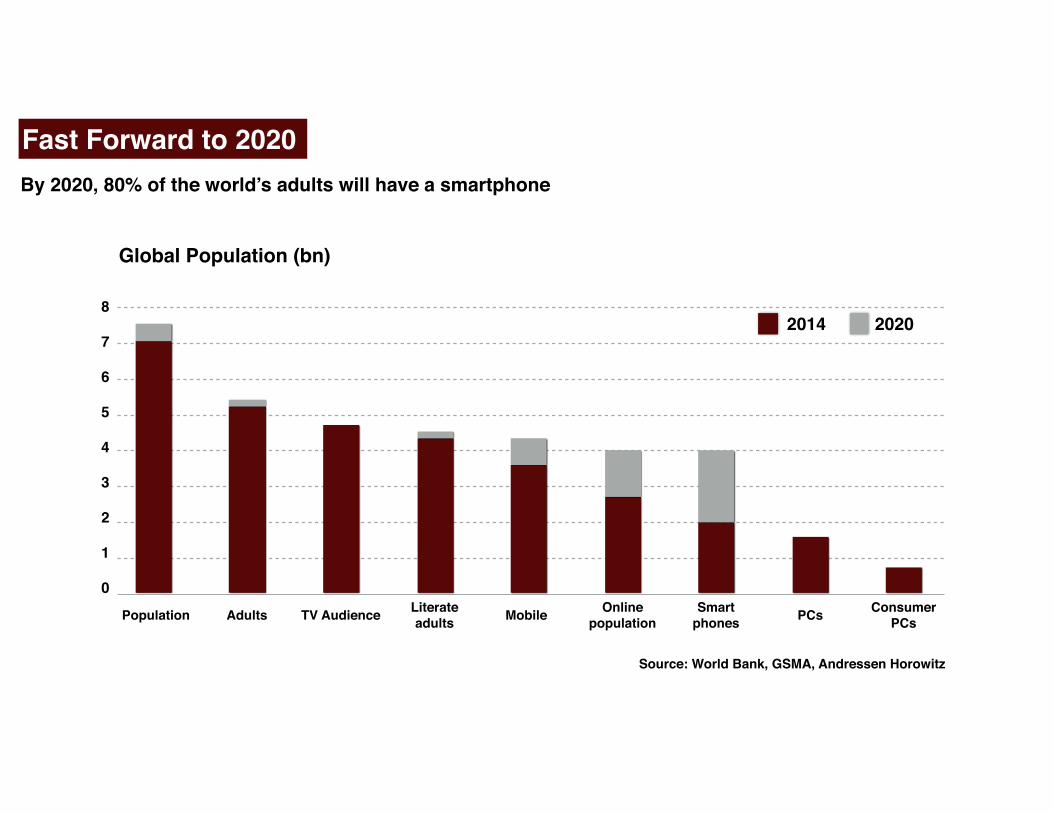

Fast Forward to 2020By 2020, 80% of the world’s adults will have a smartphone

Source: World Bank, GSMA, Andressen Horowitz

Population Adults TV Audience Literate adults Mobile Online

populationSmart

phones PCs ConsumerPCs

8

7

6

5

4

3

2

1

0

Global Population (bn)

2014 2020

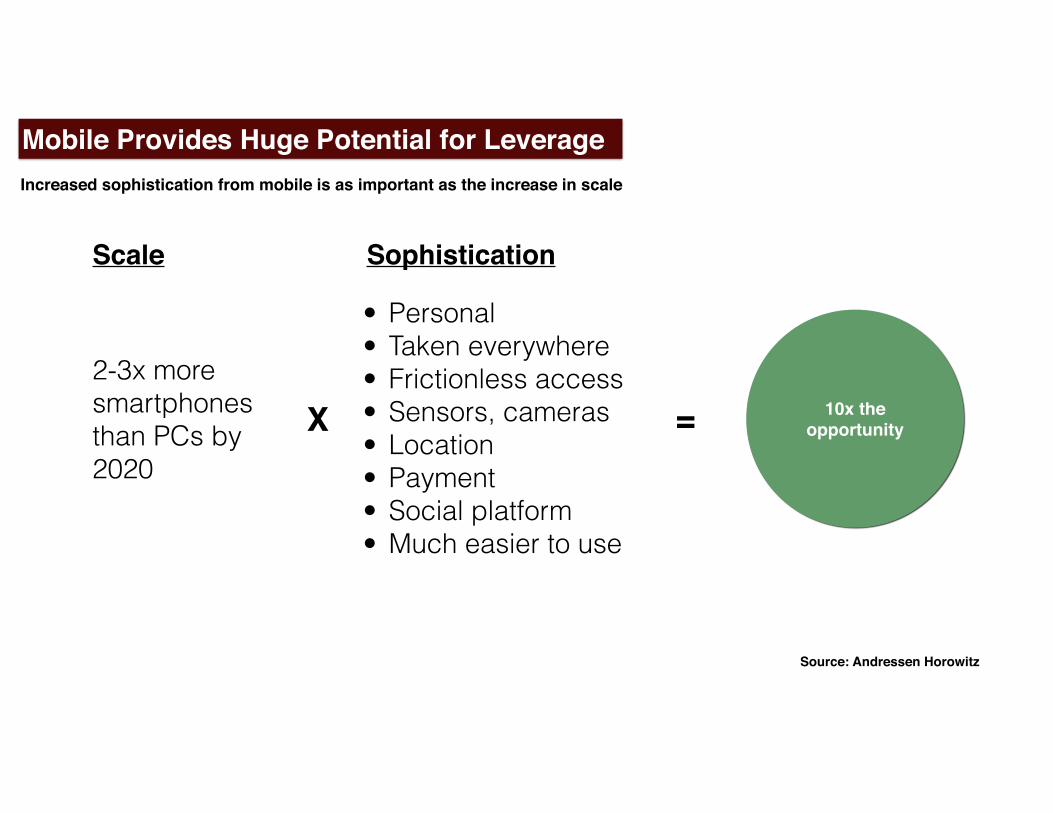

Mobile Provides Huge Potential for LeverageIncreased sophistication from mobile is as important as the increase in scale

2-3x more smartphones than PCs by 2020

• Personal • Taken everywhere • Frictionless access • Sensors, cameras • Location • Payment • Social platform • Much easier to use

10x the opportunityX =

Scale Sophistication

Source: Andressen Horowitz

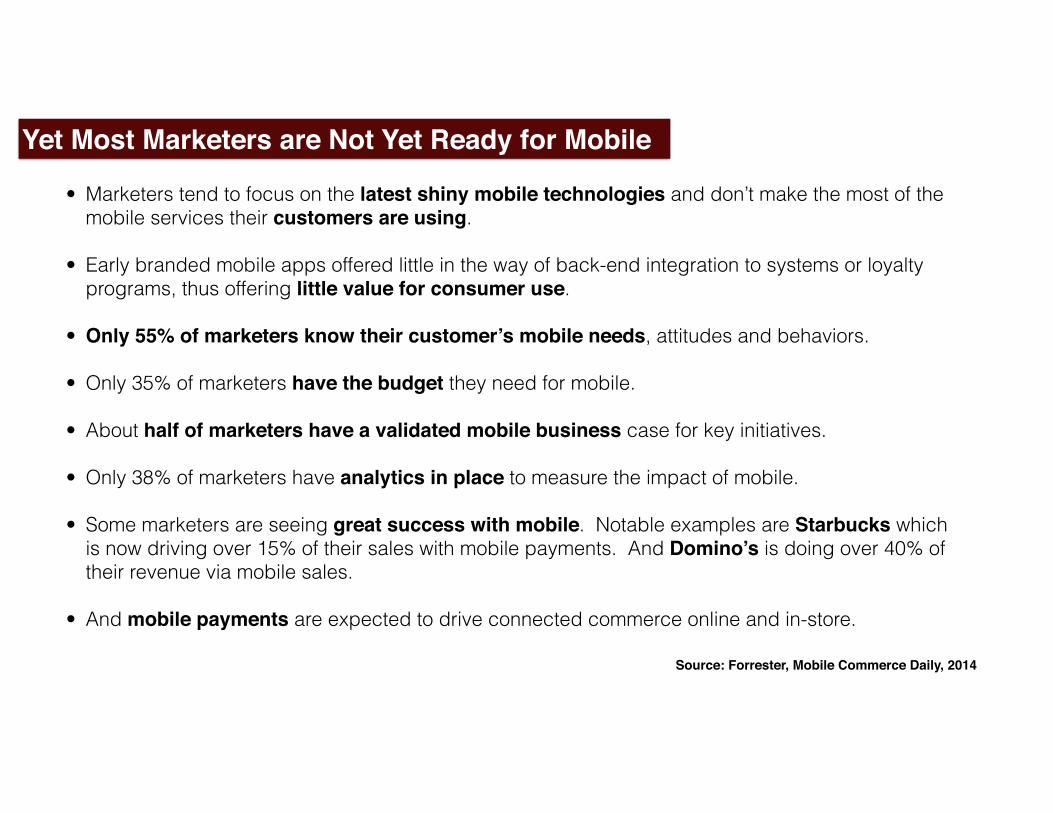

Yet Most Marketers are Not Yet Ready for Mobile

Source: Forrester, Mobile Commerce Daily, 2014

• Marketers tend to focus on the latest shiny mobile technologies and don’t make the most of the mobile services their customers are using.

• Early branded mobile apps offered little in the way of back-end integration to systems or loyalty programs, thus offering little value for consumer use.

• Only 55% of marketers know their customer’s mobile needs, attitudes and behaviors.

• Only 35% of marketers have the budget they need for mobile.

• About half of marketers have a validated mobile business case for key initiatives.

• Only 38% of marketers have analytics in place to measure the impact of mobile.

• Some marketers are seeing great success with mobile. Notable examples are Starbucks which is now driving over 15% of their sales with mobile payments. And Domino’s is doing over 40% of their revenue via mobile sales.

• And mobile payments are expected to drive connected commerce online and in-store.

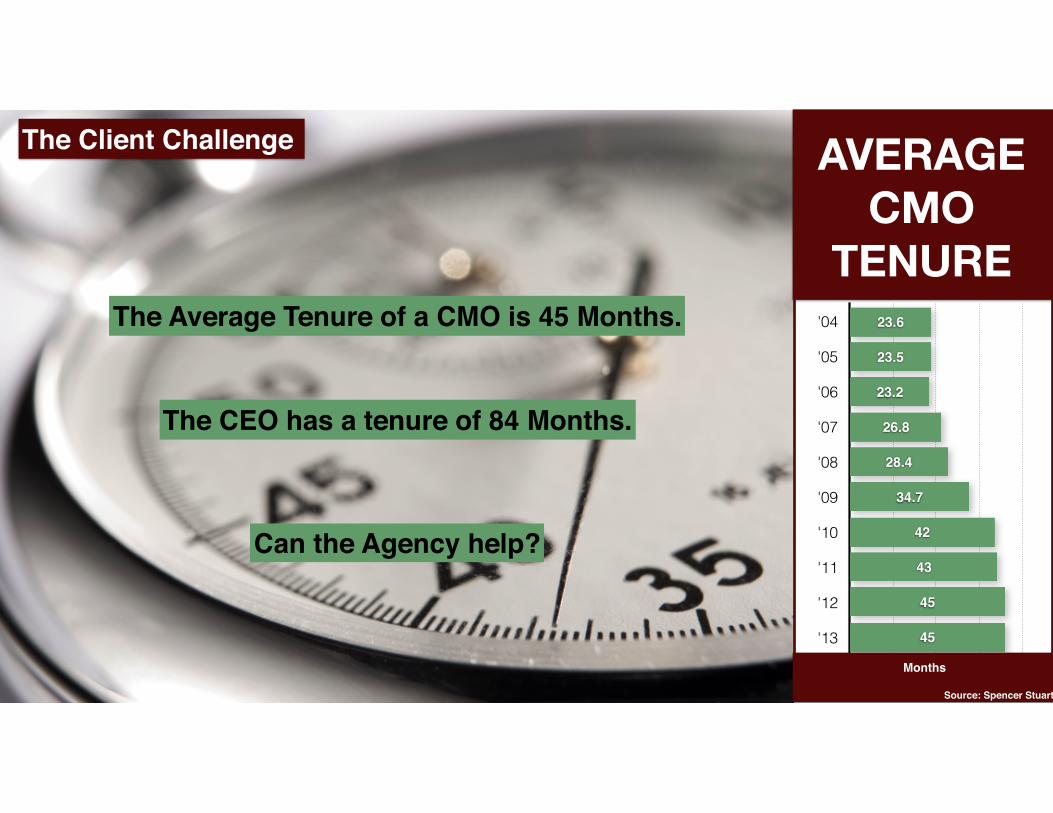

The Client Challenge

The Average Tenure of a CMO is 45 Months. '04

'05

'06

'07

'08

'09

'10

'11

'12

'13

$ 25 B $ 50 B

45

45

43

42

34.7

28.4

26.8

23.2

23.5

23.6

AVERAGECMO

TENURE

Months

Source: Spencer Stuart

The CEO has a tenure of 84 Months.

Can the Agency help?

This Isn’t the Future of Marketing

Customer

The Future is About Connected Experiences and Platforms

Journey Clarity

Realtime Feedback

Valuable Platforms

CustomerContext

Needs & Behaviors

Communications

Community

Content

Commerce

Competitive Landscape

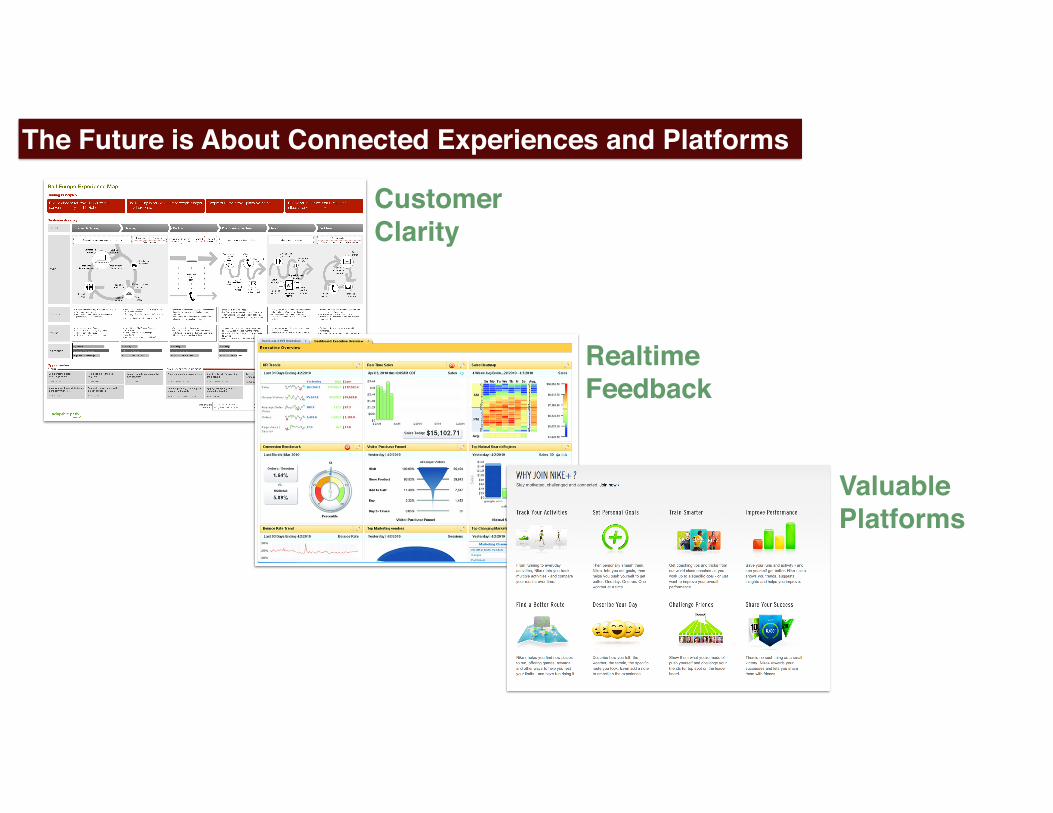

The Future is About Connected Experiences and Platforms

Customer Clarity

Realtime Feedback

Valuable Platforms

The New Reality for a Real Time Age

Strategic Plans Matter Less Than Strategic Thinkingand Opportunistic Decision Making

A Huge Strategic Shift

Idea Driven Advertising & Promotion Led

Planned Quarterly A Few Channels

Integrated in Look, Feel, Tone Reported Data

Brand-out Half-life Measured in Years

Insights Led Customer Experience Focused

Executed Real-timeHundreds of Channels

Integrated in Experience & Relevance Algorithmically Generated

Customer-in Half-life Measured in Weeks

What Was… What Must Be…

The Marketing Landscape

The Agency LandscapeThe Opportunity Ahead

Implications for IMC Students

Agenda

Agencies in the News…

Apple shifts away from TBWA/ Media Arts Lab to in-house team, April, 2014

Capital One acquires Adaptive Path as captive in-house agency. Oct, 2014

Publicis to acquire Sapient for $3.5B in cash, Nov. 2014

Smart Design SF shutting down. Cannot compete with startups for talent, Oct, 2014

The Rise of the In-house Agency, ANA, Sept. 2013

Razorfish & Peets Ink Deal for Profit Sharing on eCommerce, March, 2014

Agencies Paying Top Dollar for Data Analysts, Oct, 2014

Kraft Cuts More than Ten Agencies, Consolidates on Fewer AOR’s, Nov. 2014

What do Clients Look for Most in an Agency?

• Strategic Thinking• Creativity• Responsiveness• Low Cost• Process / Approach• Results

Source: Ignition, AAAA

What do Clients Look for Most in an Agency?

• Strategic Thinking• Creativity• Responsiveness• Low Cost• Process / Approach• Results

Source: Ignition, AAAA

But Clients Want More Than Just The Category Benefit!

No Brand can Survive Delivering Only the Category Benefit!!

• Strategic Thinking• Creativity• Responsiveness• Low Cost• Process / Approach• Results

Neither Can Agencies!

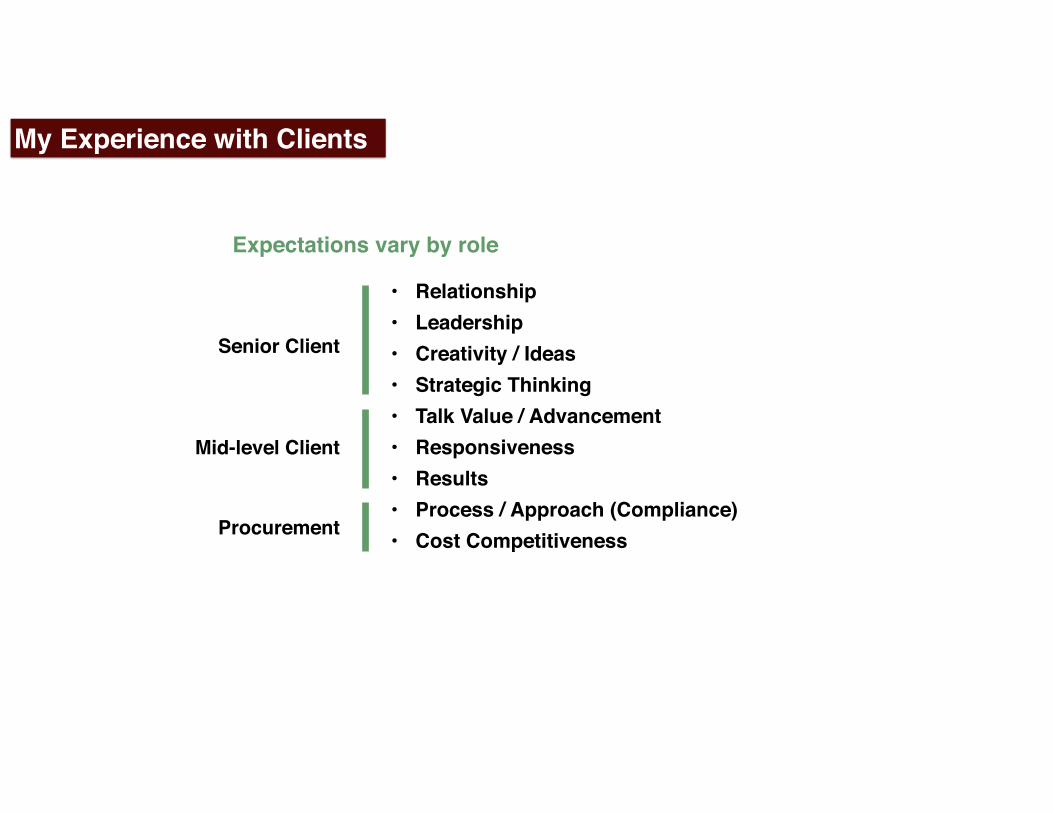

My Experience with Clients

• Relationship• Leadership• Creativity / Ideas• Strategic Thinking• Talk Value / Advancement• Responsiveness• Results• Process / Approach (Compliance)• Cost Competitiveness

Senior Client

Mid-level Client

Procurement

Expectations vary by role

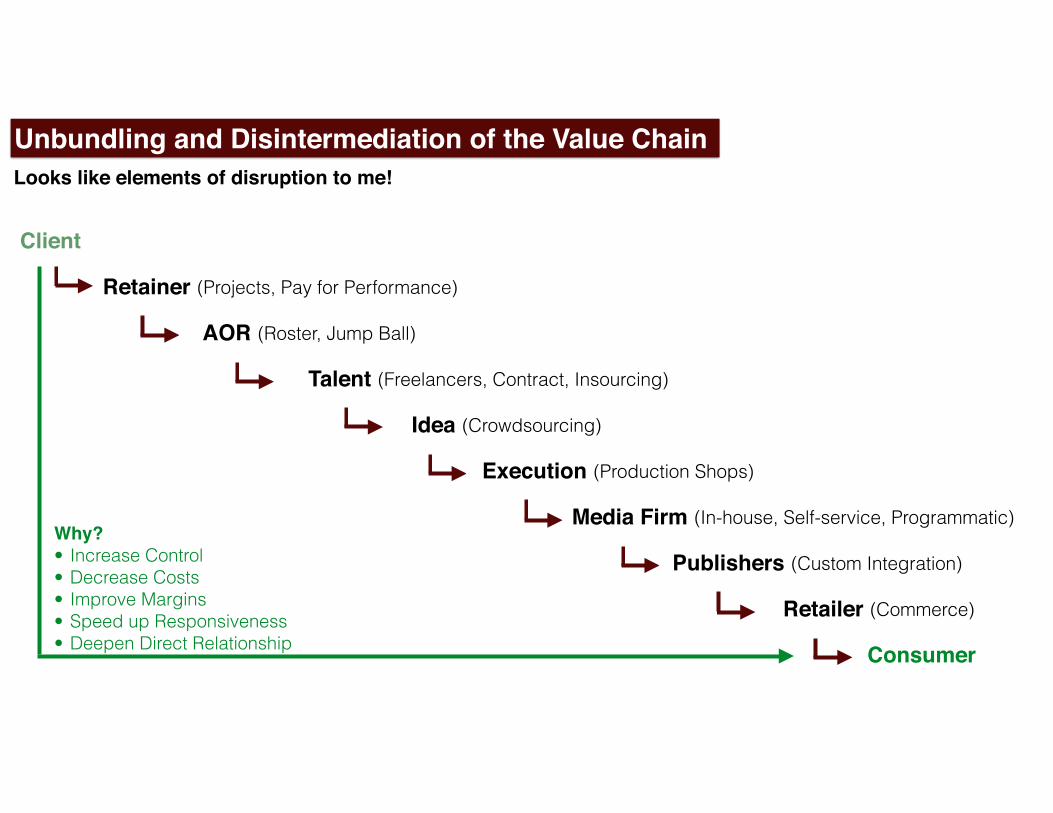

AOR (Roster, Jump Ball)

Talent (Freelancers, Contract, Insourcing)

Idea (Crowdsourcing)

Execution (Production Shops)

Media Firm (In-house, Self-service, Programmatic)

Publishers (Custom Integration)

Retailer (Commerce)

Retainer (Projects, Pay for Performance)

Unbundling and Disintermediation of the Value Chain

Client

Consumer

Why?• Increase Control • Decrease Costs • Improve Margins • Speed up Responsiveness • Deepen Direct Relationship

AOR

Talent

Idea

Execution

Media Firm

Publishers

Retailer

Retainer

Looks like elements of disruption to me!

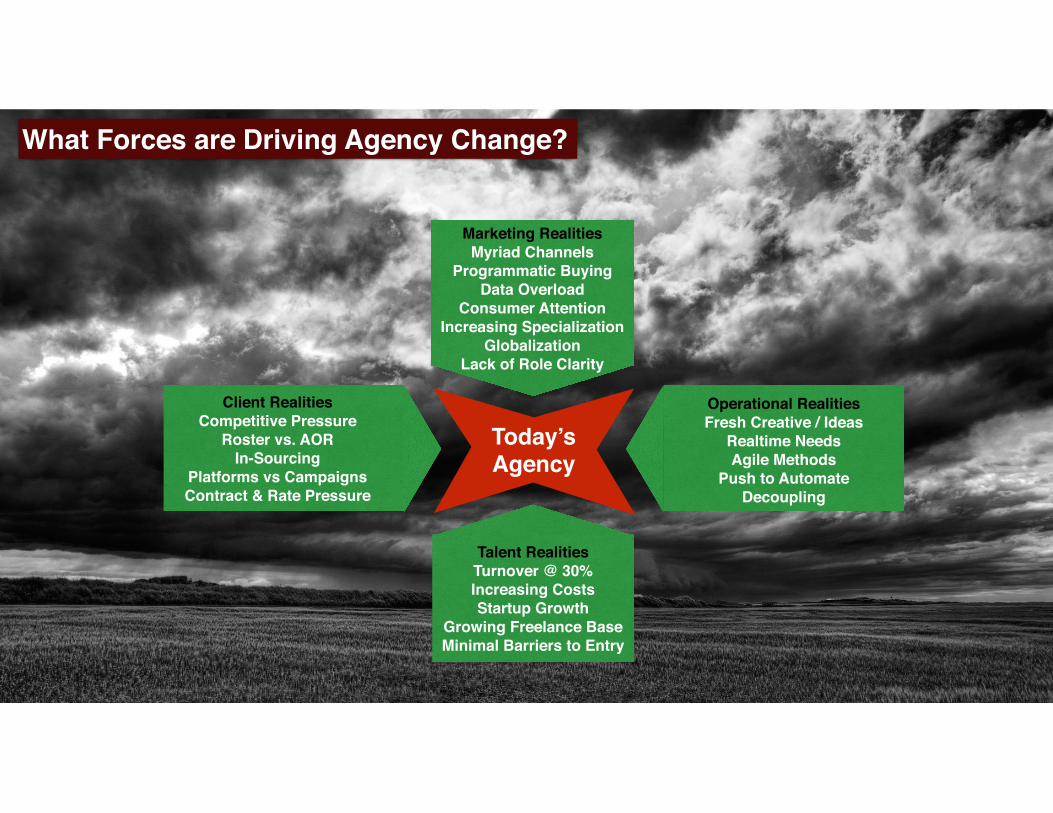

What Forces are Driving Agency Change?

Today’sAgency

Client RealitiesCompetitive Pressure

Roster vs. AORIn-Sourcing

Platforms vs CampaignsContract & Rate Pressure

Marketing RealitiesMyriad Channels

Programmatic BuyingData Overload

Consumer AttentionIncreasing Specialization

GlobalizationLack of Role Clarity

Operational RealitiesFresh Creative / Ideas

Realtime NeedsAgile Methods

Push to AutomateDecoupling

Talent RealitiesTurnover @ 30%Increasing CostsStartup Growth

Growing Freelance BaseMinimal Barriers to Entry

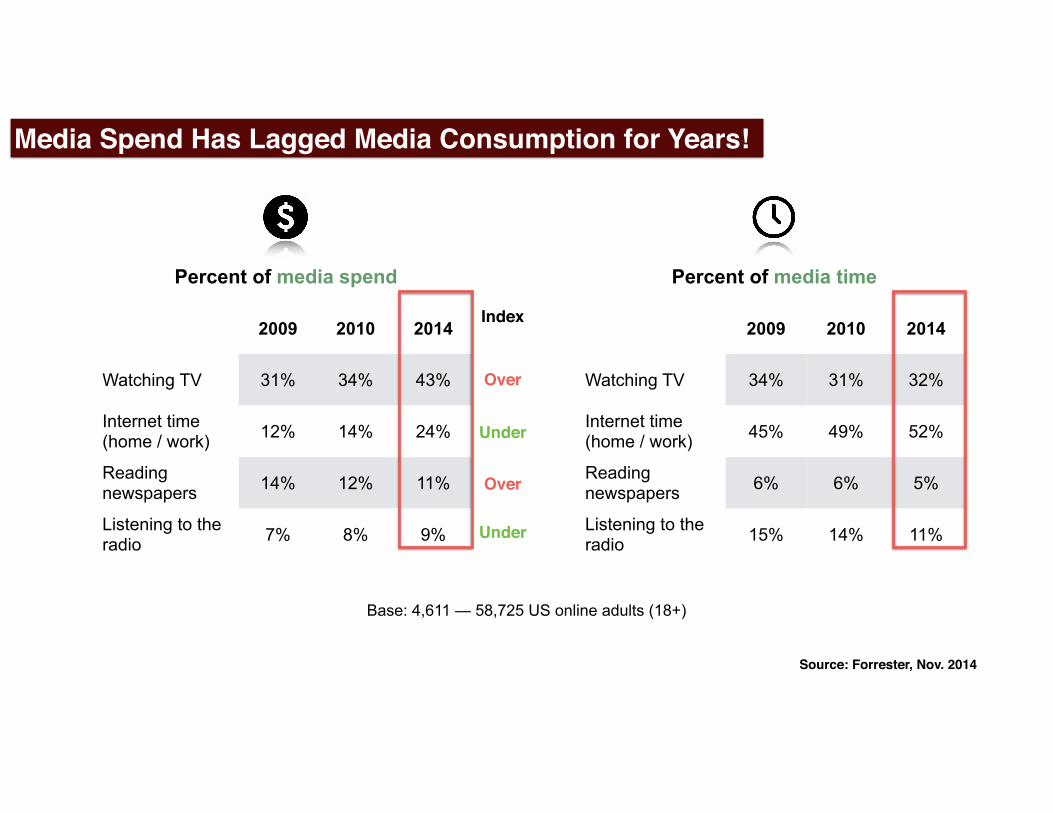

Media Spend Has Lagged Media Consumption for Years!

Percent of media time

2009 2010 2014

Watching TV 34% 31% 32%

Internet time (home / work) 45% 49% 52%

Reading newspapers 6% 6% 5%

Listening to the radio 15% 14% 11%

Source: Forrester, Nov. 2014

Percent of media spend

2009 2010 2014

Watching TV 31% 34% 43%

Internet time (home / work) 12% 14% 24%

Reading newspapers 14% 12% 11%

Listening to the radio 7% 8% 9%

Over

Over

Under

Index

Under

Base: 4,611 — 58,725 US online adults (18+)

Source: Forrester, Nov. 2014

US$

Mill

ions

$50.00

$60.00

$70.00

$80.00

$90.00

$100.00

$110.00

$120.00

2014 2015 2016 2017 2018 2019

Television Interactive

Digital Finally Projected to Beat TV

32% of Total2% CAGR

35% of Total12% CAGR

Crossover

The Marketing Landscape

The Agency Landscape

The Opportunity AheadImplications for IMC Students

Agenda

It’s a Crowded Services Field Surrounding Marketers Today

CMO, CDO & Teams

Customer Experience Agencies

Creative Agencies

Ad & Marketing

TechnologyFirms

Startups & Product

Development Shops

MediaAgencies

InnovationConsultancies

Brand Agencies

ManagementConsultancies

PR & SocialMedia Firms

Mobile Development& Marketing

Firms

EventMarketingAgencies

Shopper & Location-

Based Marketing

eCommerce Consultancies

Analytics & Data

ManagementConsultancies

Systems Integrators

DirectMarketingAgencies

SponsorshipAgencies

MarketResearch

Firms

Aggregators (FB, Google,

etc)

Publishers (Digital, TV,

Print)

Data ProvidersLoyalty

Program Consultancies

And They Are Focused On…

A Seat at the Table (Access to Budgets)

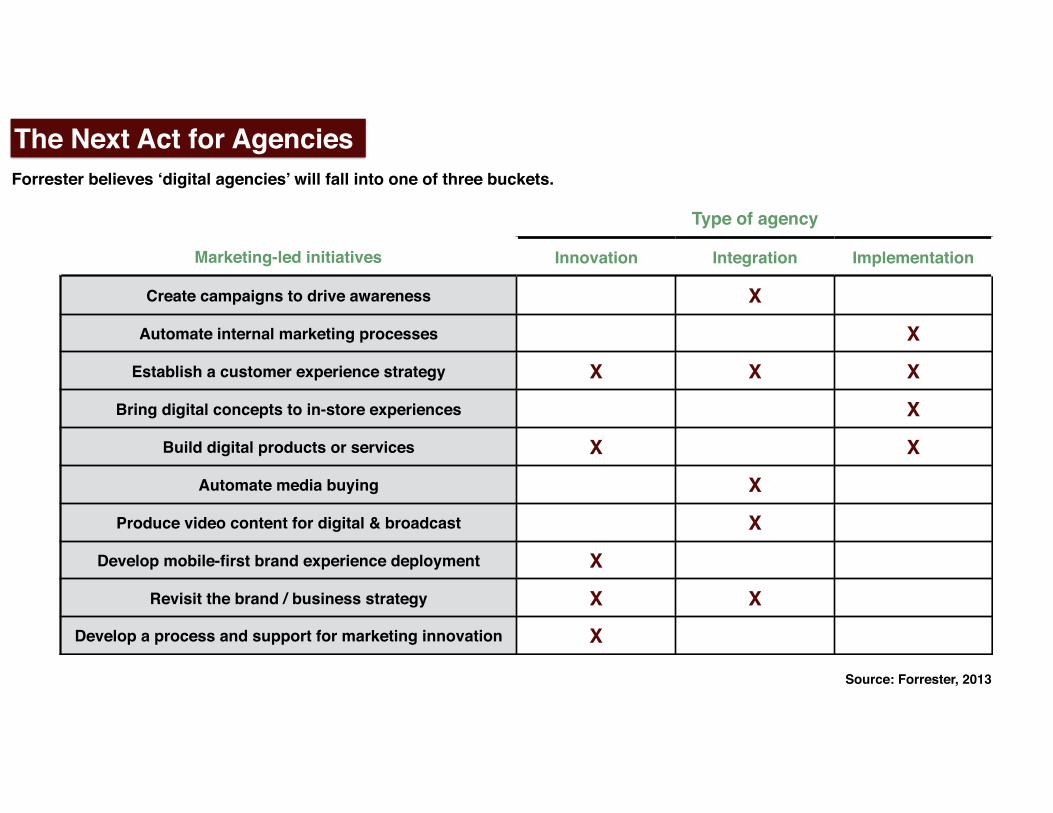

The Next Act for Agencies

Type of agency

Marketing-led initiatives Innovation Integration Implementation

Create campaigns to drive awareness X

Automate internal marketing processes X

Establish a customer experience strategy X X X

Bring digital concepts to in-store experiences X

Build digital products or services X X

Automate media buying X

Produce video content for digital & broadcast X

Develop mobile-first brand experience deployment X

Revisit the brand / business strategy X X

Develop a process and support for marketing innovation X

Source: Forrester, 2013

Forrester believes ‘digital agencies’ will fall into one of three buckets.

What’s Holding Progress Back?

CMOs are feeling pressure to tie marketing efforts to financial impact

• Leapfrog / Medill IMC Study • Reported October, 2014

CMO’s Struggling with Data, Digital, Mobile

Barriers to Success: • Limited Internal Expertise • Siloed Organizations • Resistance to Change

Where do Marketers Need Help?

• Develop breakthrough ideas - creative, yet strategic, based on market or customer insight. Execution may not happen by the same firm, however.

• Harness & optimize data - data cleansing, system setup, analytics, customer analysis, loyalty program optimization, customer experience optimization.

• Offer channel expertise & leadership - from social to mobile to shopper marketing or native advertising, clients are looking for channel-specific depth.

• Content development - original content, story telling, social content, online content; most marketer’s second highest spending area behind paid media.

• Real-time agility - Operations, tools and talent to respond to the real time demands of their target audience interacting across channels. Automate, simplify and empower them to drive smart engagement at scale.

• Get shit done - Ability to scale, execute and deliver under tight timelines. Operationally execute the campaigns, social efforts and myriad tactics. Get stuff off the clients plate and take care of it to drive impact.

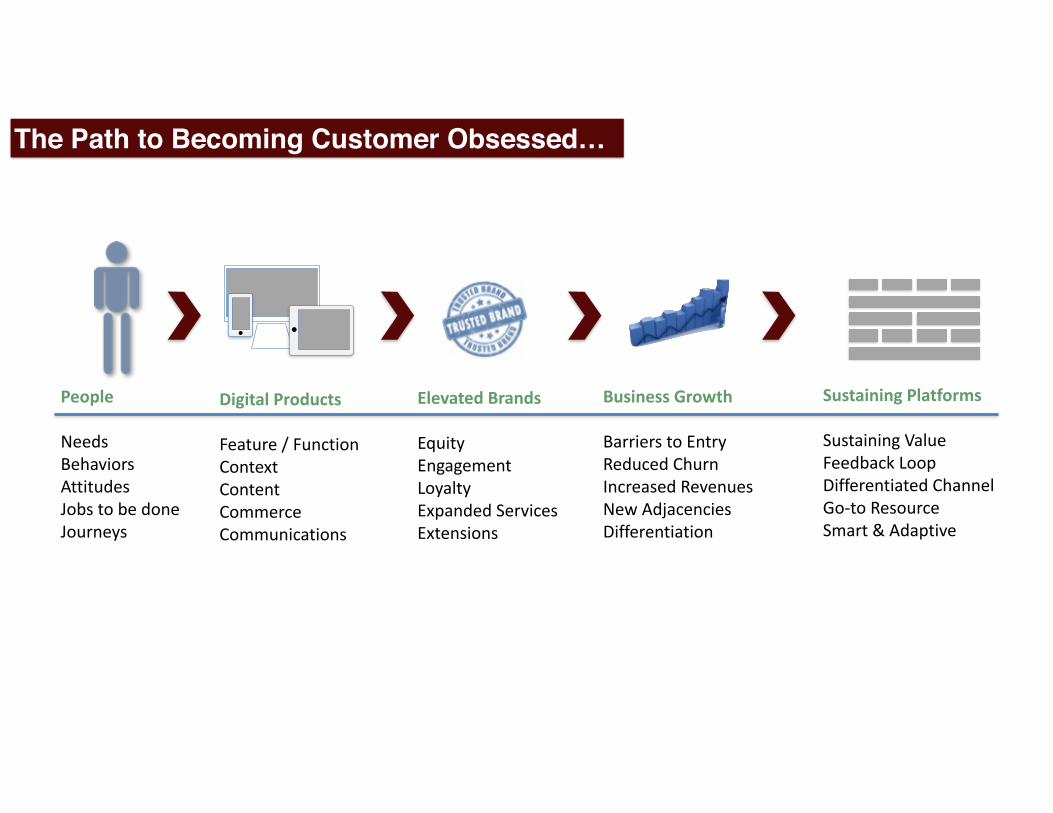

Connected Thinking for the Connected Age

• Customer behavior observed in context • Smart ideas derived from insights • Platforms differentiated with value to the customer • Initiatives supported by experience mapping • Relevance defined in real time • Results reinforced with data • Touch points integrated across the lifecycle • All designed for dissemination and adaptive access • With approaches and process based on agile methods • Continuous improvement to reinforce accountability • And smart collaboration across client and partners

People

Needs Behaviors Attitudes Jobs to be done Journeys

Digital Products

Feature / Function Context Content Commerce Communications

Elevated Brands

Equity Engagement Loyalty Expanded Services Extensions

Business Growth

Barriers to Entry Reduced Churn Increased Revenues New Adjacencies Differentiation

Sustaining Platforms

Sustaining Value Feedback Loop Differentiated Channel Go-‐to Resource Smart & Adaptive

The Path to Becoming Customer Obsessed…

The Marketing Landscape

The Agency Landscape

The Opportunity Ahead

Implications for IMC Students

Agenda

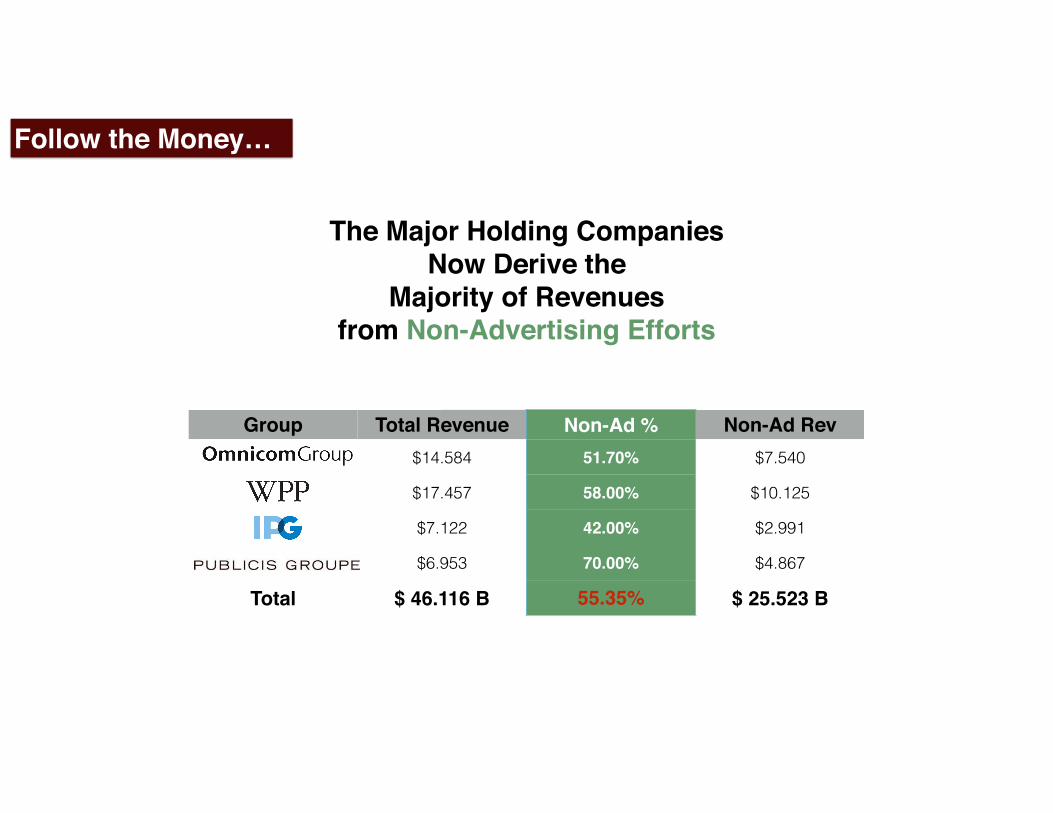

Group Total Revenue Non-Ad % Non-Ad Rev$14.584 51.70% $7.540

$17.457 58.00% $10.125

$7.122 42.00% $2.991

$6.953 70.00% $4.867

Total $ 46.116 B 55.35% $ 25.523 B

Follow the Money…

The Major Holding Companies Now Derive the

Majority of Revenuesfrom Non-Advertising Efforts

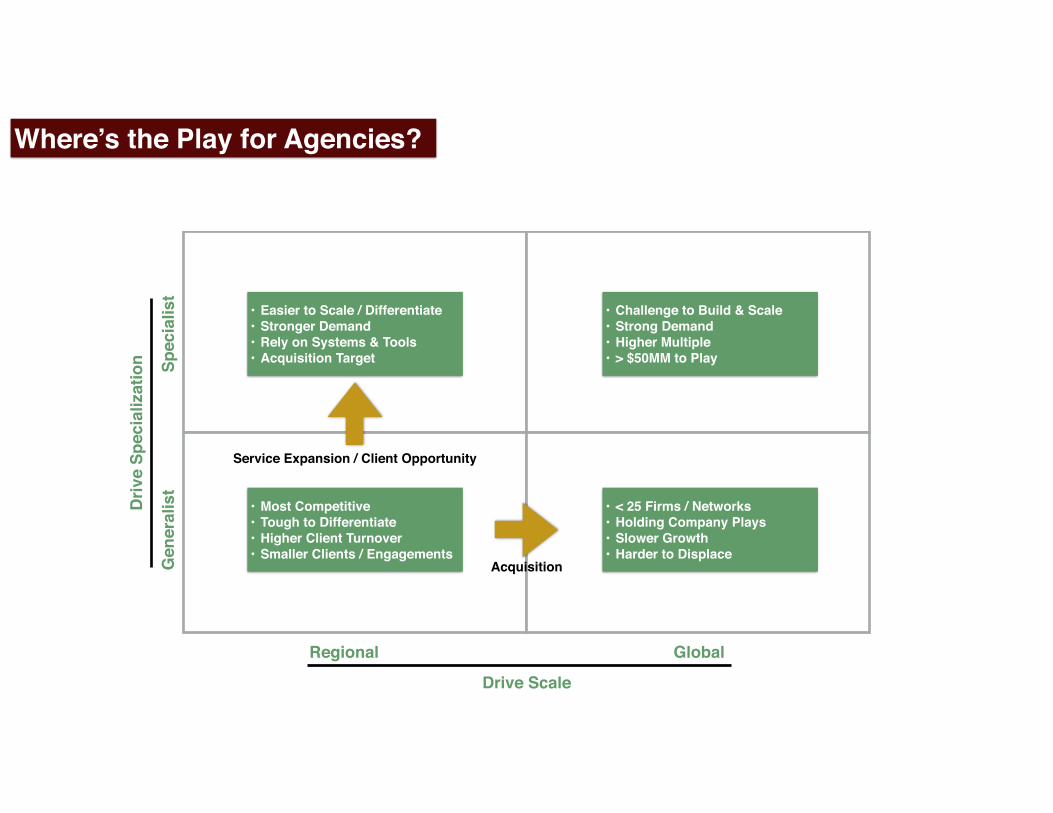

Where’s the Play for Agencies?

Drive Scale

Driv

e Sp

ecia

lizat

ion

Regional Global

Gen

eral

ist

Spec

ialis

t

• Challenge to Build & Scale• Strong Demand• Higher Multiple• > $50MM to Play

• Most Competitive• Tough to Differentiate• Higher Client Turnover• Smaller Clients / Engagements

• Easier to Scale / Differentiate• Stronger Demand• Rely on Systems & Tools• Acquisition Target

• < 25 Firms / Networks• Holding Company Plays• Slower Growth• Harder to Displace

Acquisition

Service Expansion / Client Opportunity

What Can We Learn from Startups?

Software is Eating The World - Embrace it.

Recurring Revenue Drives Growth / Value.

Extreme Focus. Minimum Viable / Desirable Product.

Full Stack - Talent with Multiple Dimensions.

Seven Skills Marketers Will Need

People First: Design for Use

Agility: Speed & Nimbleness

Perspective: Global + Local

GLOCAL

Viewpoint: Outside in, not Inside out

OUTSIDE IN

Problem Solver: Remove the Friction

Opportunity: Moments of Truth

Measure: Usage & Delight

Customer Obsession

Questions?