ACSDA Leadership Forum CDS Financial Risk Model Summary of Key Financial Risk Controls Nauman...

14

ACSDA Leadership Forum CDS Financial Risk Model Summary of Key Financial Risk Controls Nauman Mahmood, Managing Financial Risk Director October 9,2007

-

Upload

anderson-boarman -

Category

Documents

-

view

213 -

download

0

Transcript of ACSDA Leadership Forum CDS Financial Risk Model Summary of Key Financial Risk Controls Nauman...

ACSDA Leadership ForumACSDA Leadership ForumCDS Financial Risk ModelSummary of Key Financial Risk Controls

Nauman Mahmood, Managing Financial Risk Director October 9,2007

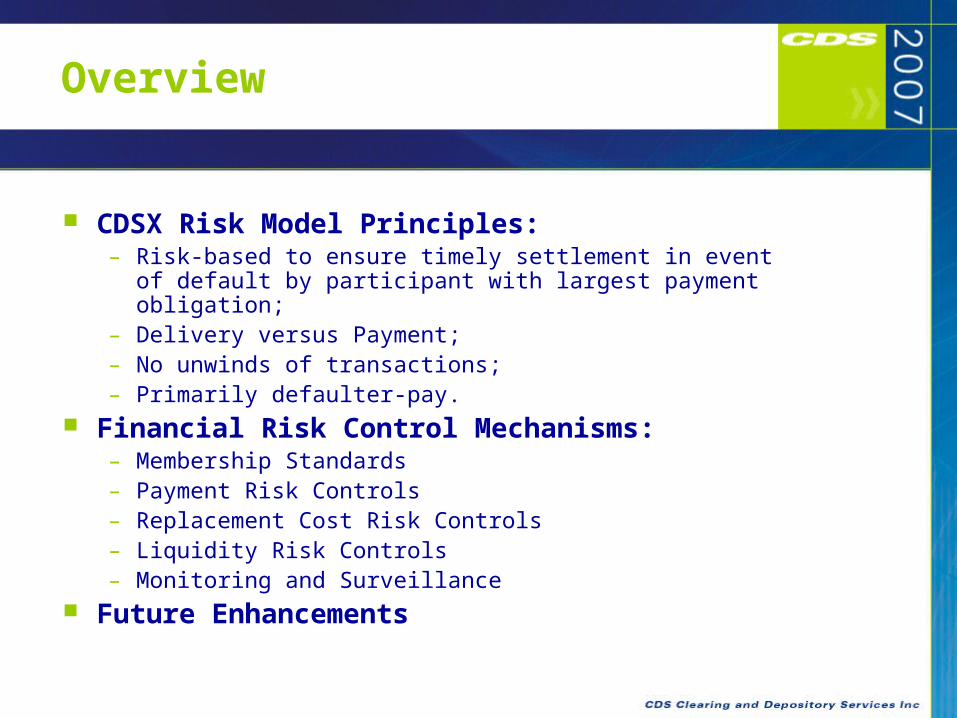

Overview

CDSX Risk Model Principles:– Risk-based to ensure timely settlement in event of default by

participant with largest payment obligation;– Delivery versus Payment;– No unwinds of transactions;– Primarily defaulter-pay.

Financial Risk Control Mechanisms:– Membership Standards– Payment Risk Controls– Replacement Cost Risk Controls– Liquidity Risk Controls– Monitoring and Surveillance

Future Enhancements

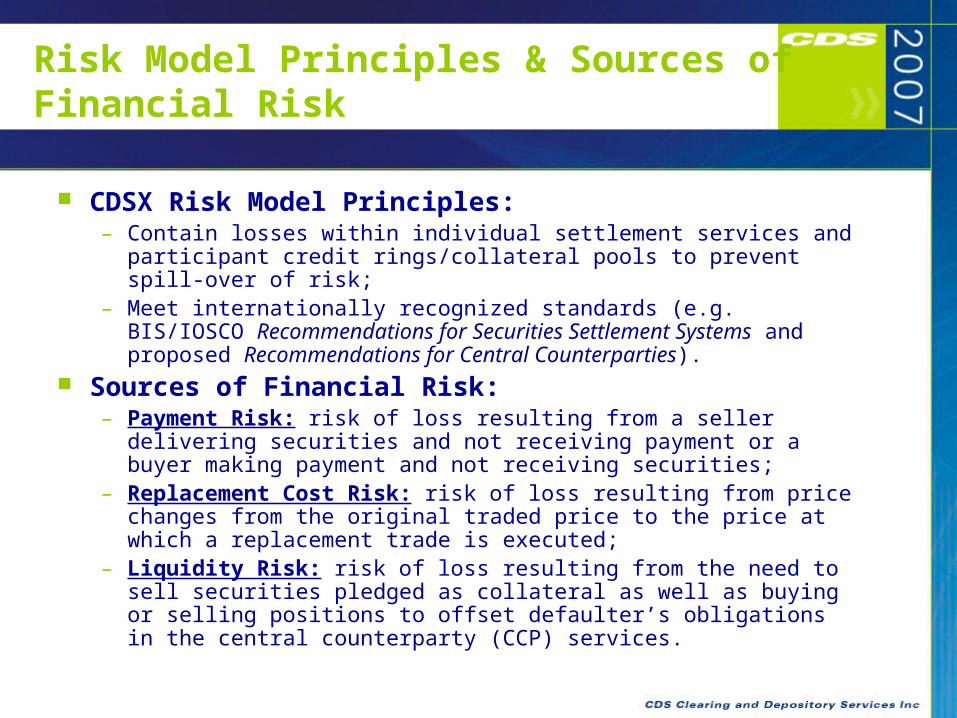

Risk Model Principles & Sources of Financial Risk

CDSX Risk Model Principles:– Contain losses within individual settlement services and participant

credit rings/collateral pools to prevent spill-over of risk;– Meet internationally recognized standards (e.g. BIS/IOSCO

Recommendations for Securities Settlement Systems and proposed Recommendations for Central Counterparties).

Sources of Financial Risk:– Payment Risk: risk of loss resulting from a seller delivering

securities and not receiving payment or a buyer making payment and not receiving securities;

– Replacement Cost Risk: risk of loss resulting from price changes from the original traded price to the price at which a replacement trade is executed;

– Liquidity Risk: risk of loss resulting from the need to sell securities pledged as collateral as well as buying or selling positions to offset defaulter’s obligations in the central counterparty (CCP) services.

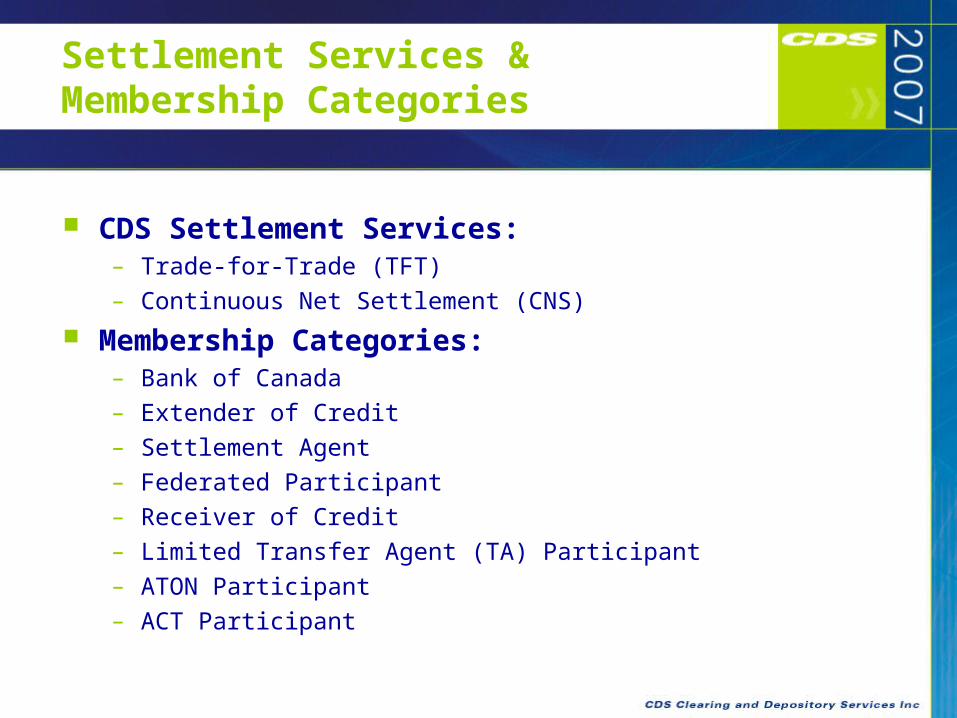

Settlement Services & Membership Categories

CDS Settlement Services:– Trade-for-Trade (TFT)

– Continuous Net Settlement (CNS)

Membership Categories:– Bank of Canada

– Extender of Credit

– Settlement Agent

– Federated Participant

– Receiver of Credit

– Limited Transfer Agent (TA) Participant

– ATON Participant

– ACT Participant

Payment Risk Controls

Funds Edit:– Each participant in CDSX has a limit on the size of payment

obligation (negative funds account balance) they can create;– Limit equals “cap” from collateralized credit ring plus lines of credit

granted by an Extender;– Does not apply to mark-to-market payments.

Aggregate Collateral Value (ACV) Edit:– Checks transactions prior to settlement to ensure that haircut value

of securities in “risk accounts” is sufficient to cover resulting negative funds account balance;

– Risk accounts are securities accounts which CDS has a legal right to use as collateral in event of participant default;

– The haircut applied to securities represents the potential for the collateral to decrease in value over the time required to liquidate the collateral;

– Sector limits control amount of ACV generated by certain security types (e.g. equities, private sector issuers, provincial governments).

Payment Risk Controls

Calculating Haircuts:– CDS uses Value-at-Risk (VaR) to calculate the haircut for each

equity security using a confidence interval of 99% over a 2, 3, 5 or 10-day holding period;

– Calculated weekly;– Debt haircuts are based on issuer type, credit rating and term to

maturity;– Holding period for equity haircuts determined by liquidity of each

security;– Illiquid securities (trading less than 10% of potential trading days)

are assigned 100% haircut;– Does not allow for diversification effects for ACV calculation.

Category Credit Rings:– Collateralized credit rings supporting payment obligations of each

participant category group.

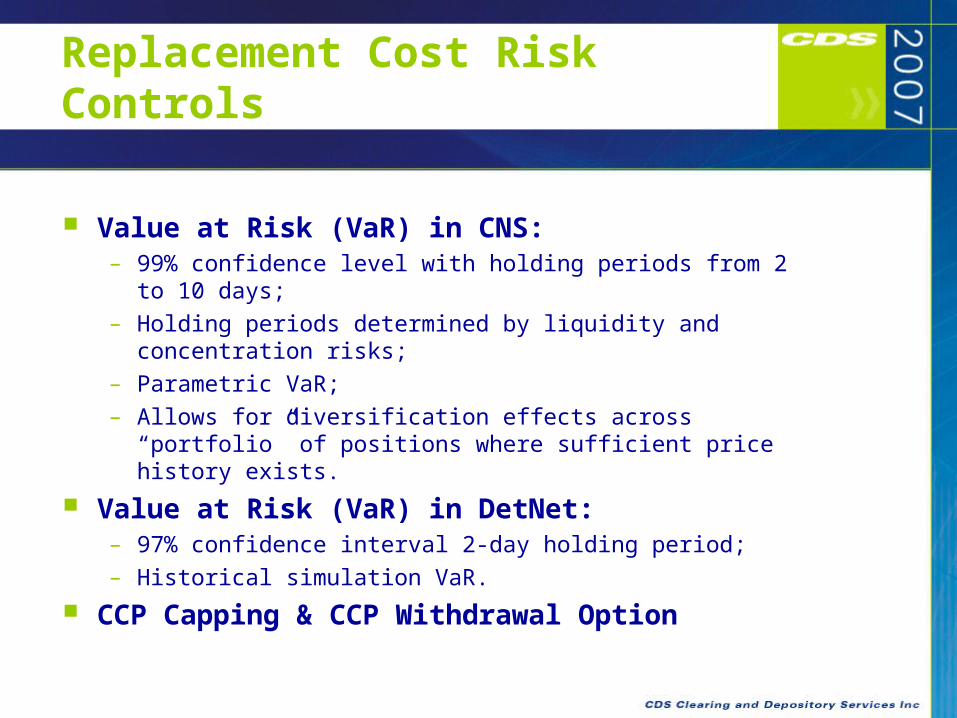

Replacement Cost Risk Controls

Apply to services where CDS assumes role of central counterparty (CCP):– CNS;

– DetNet.

Controls are:– Daily mark-to-market (MTM);

– Participant Funds.

Timing of Netting and Novation:– CNS: morning of T+3;

– DetNet: evening trades are confirmed;

– Results in a single “to-receive” or “to-deliver” position for each security in given service.

Replacement Cost Risk Controls

Daily Mark-to-Market:– All CCP trades/positions are subject to daily marking at most recent

closing price;– Debited or credited to participants’ funds accounts;– Not covered by caps or lines of credit.

CCP Participant Funds:– Established for each CCP service;– Designed to address two risks:

– failure of a defaulter to pay a mark owed to CDS;– cost to CDS of replacing defaulter’s security receipt and delivery

obligations.– Daily requirement consists of two components to address each of

the risks faced by the Fund:– MTM Component: Largest MTM paid or received in most recent

20 business days for DetNet; largest unpaid MTM paid in most recent 50 business days for CNS;

– Outstanding Component: VaR of current outstanding trades.

Replacement Cost Risk Controls

Value at Risk (VaR) in CNS:– 99% confidence level with holding periods from 2 to 10 days;

– Holding periods determined by liquidity and concentration risks;

– Parametric VaR;

– Allows for diversification effects across “portfolio” of positions where sufficient price history exists.

Value at Risk (VaR) in DetNet:– 97% confidence interval 2-day holding period;

– Historical simulation VaR.

CCP Capping & CCP Withdrawal Option

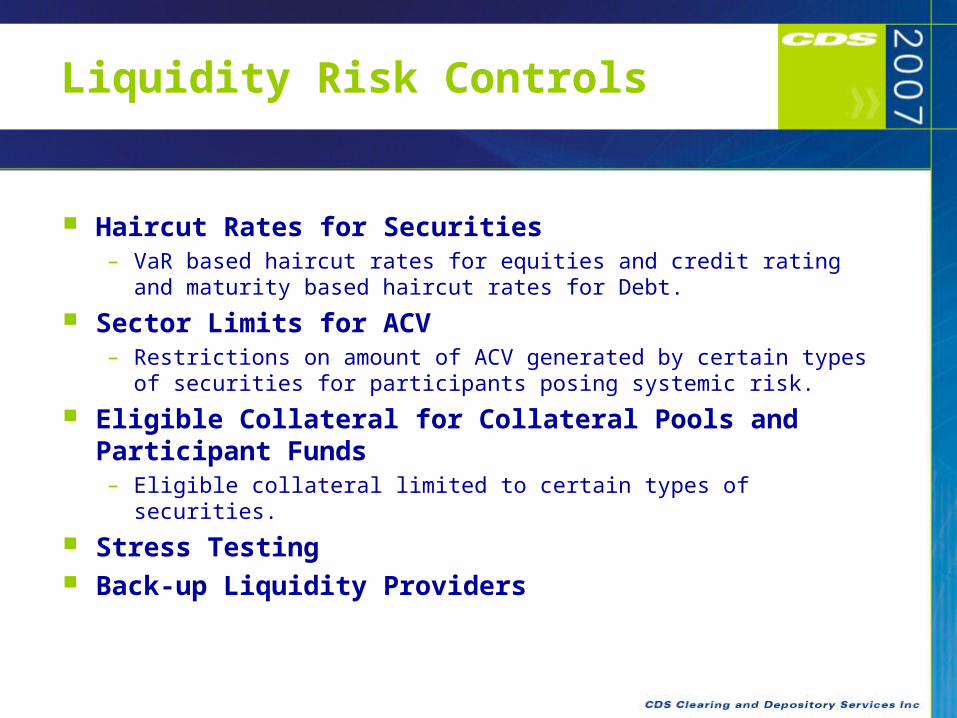

Liquidity Risk Controls

Haircut Rates for Securities– VaR based haircut rates for equities and credit rating and maturity

based haircut rates for Debt.

Sector Limits for ACV– Restrictions on amount of ACV generated by certain types of

securities for participants posing systemic risk.

Eligible Collateral for Collateral Pools and Participant Funds– Eligible collateral limited to certain types of securities.

Stress Testing Back-up Liquidity Providers

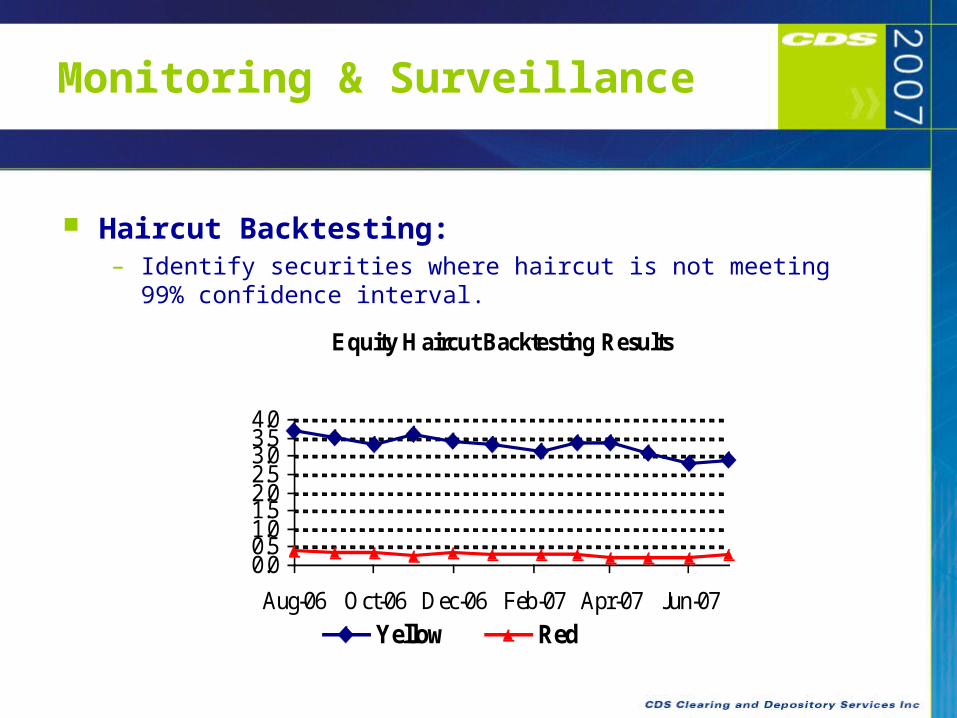

Monitoring & Surveillance

Haircut Backtesting:– Identify securities where haircut is not meeting 99% confidence

interval.

Equity Haircut Backtesting Results

0.00.51.01.52.02.53.03.54.0

Aug-06 Oct-06 Dec-06 Feb-07 Apr-07 Jun-07

% of Securities

Yellow Red

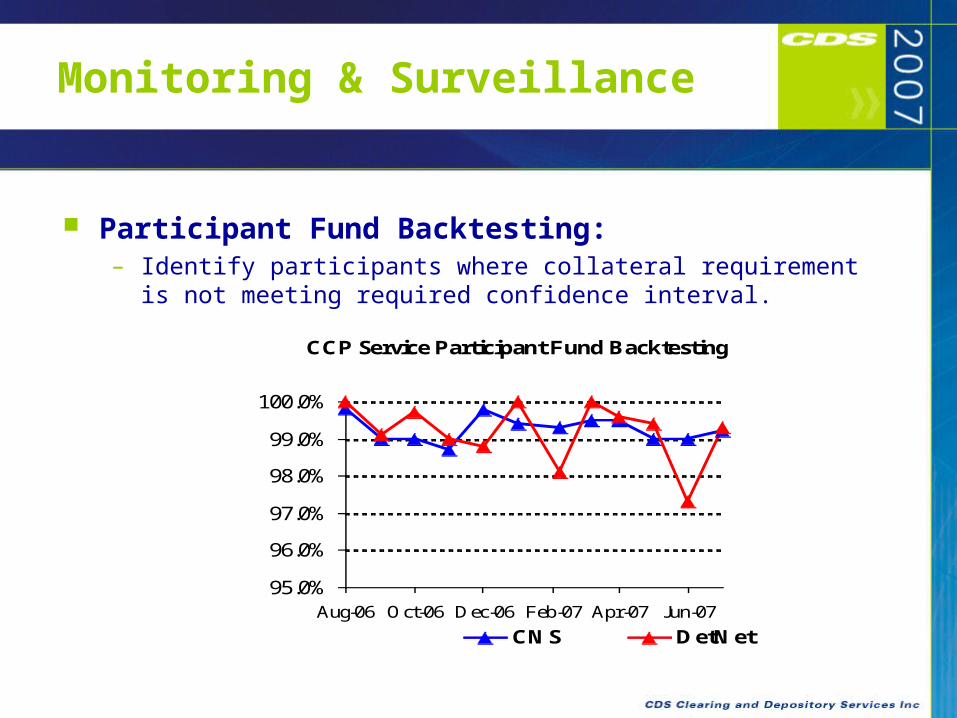

Monitoring & Surveillance

Participant Fund Backtesting:– Identify participants where collateral requirement is not meeting

required confidence interval.

CCP Service Participant Fund Backtesting

95.0%

96.0%

97.0%

98.0%

99.0%

100.0%

Aug-06 Oct-06 Dec-06 Feb-07 Apr-07 Jun-07% of Instances Where Collateral

Requirement Exceeded Loss

CNS DetNet

Monitoring & Surveillance

Aggregate Participant Funds:– Total collateral requirement of all participants in each CCP service.

Participant Compliance:– Ongoing monitoring of participants’ compliance to CDS Participant

Rules;

– MoU with participants’ Self Regulatory Organizations (SROs).

Future Enhancements

Improve Fixed Income Netting

Improve Debt Haircut Methodology

Earlier Novation and CCP Guarantee